operational impacts of proposed redemption restrictions on money

TRANSCRIPT

Operational Impacts of Proposed Redemption Restrictions on Money Market Funds

Copyright © 2012 by the Investment Company Institute. All rights reserved.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds i

Kathleen C. Joaquin, ICI Chief Industry Operations Officer; Martin Burns, ICI Senior Director, Operations and Distribution; Rochelle L. Antoniewicz, ICI Senior Economist; and Jane G. Heinrichs, ICI Senior Associate Counsel, prepared this report.

I. Overview: Redemption Restrictions Would Drive Investors and Intermediaries Away from Money Market Funds ......................................................................................................... 1

Box: Past Redemption Restrictions Have Been Rare and Carefully Crafted ....................................... 5

II. Investors Use Money Market Funds for Diverse Purposes ................................................................. 6

III. How the SEC’s Redemption Restriction Proposal Might Work ......................................................... 8

A. How the High-Water-Mark Method Might Work ....................................................................... 8

B. Tracking a High-Water-Mark Example ...................................................................................... 9

Box: Impact of Continuous Redemption Restrictions on a Typical Institutional Shareholder ............. 11

IV. Money Market Funds Operate in a Complex Environment .............................................................12

A. Intermediaries Play a Major Role ............................................................................................13

B. How Mutual Fund Transactions Are Processed ........................................................................15

C. Mutual Fund Transfer Agent, Intermediary, and Ancillary Systems ............................................19

V. Implementing Redemption Restrictions Would Create Significant Operational Difficulties and Costs ..................................................................................................................................20

A. Redemption Restrictions Require Major Operational Changes ...................................................26

B. Additional Operational Impacts Would Add Costs .....................................................................27

Box: Breaking the Dollar: What Happens to Shareholders’ Remaining Shares? ................................28

VI. Systems Complexities Present Significant Hurdles for Intermediaries .............................................30

VII. Applying Redemption Restrictions at the Intermediary Level Is Unworkable ..................................34

VIII. Conclusion .............................................................................................................................. 35

Operational Impacts of Proposed Redemption Restrictions on Money Market Funds

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 1

I. Overview: Redemption Restrictions Would Drive Investors and Intermediaries Away from Money Market Funds The Securities and Exchange Commission (SEC) is considering structural changes to money market funds that could fundamentally alter the nature of these funds. One such change would subject money market funds to “redemption restrictions” that would deny investors full use of their cash. It appears that regulators are looking at a variety of possible approaches that, in essence, would escrow a portion of a shareholder’s money market fund account on an ongoing basis. The money held back from an investor’s account due to redemption activity would be used to absorb first losses if a fund cannot maintain its $1.00 net asset value (NAV)—an event commonly referred to as “breaking the dollar.”

Proponents of redemption restrictions believe that such restrictions can prevent or mitigate redemption pressure similar to that experienced by prime money market funds in 2008 by removing investors’ incentives to be among the first to redeem (the so-called first mover advantage). They also believe that redemption restrictions will make explicit to investors that money market funds entail risk, which will be borne by investors in times of severe market stress.

The SEC’s contemplated redemption restrictions for money market funds would permanently alter the ability of fund investors to redeem all of their shares on a daily basis. They apparently would apply to all funds and all investors at all times, under all market conditions. As such, they would impair a core investor protection of mutual funds and reverse more than 70 years of SEC practice in fund regulation. (See box, “Past Redemption Restrictions Have Been Rare and Carefully Crafted” on page 5.)

The Investment Company Institute (ICI) opposes any sort of redemption restriction that would impair investor liquidity when liquidity is readily available within the money market fund. The SEC’s contemplated redemption holdback, if adopted, represents an experiment on the $2.6 trillion money market fund industry that could have harmful consequences for the broader financial markets, including financing for businesses and state and local governments.

These redemption restrictions also would create serious operational issues that would restrict or eliminate the usefulness of money market funds in many services that funds and financial providers extend to investors. This paper focuses on the operational implications of the SEC’s possible proposals for redemption restrictions.

Throughout the 40-year history of money market funds, investors have benefited from the convenience, liquidity, and stability of these funds. Individual or retail investors use money market funds as savings vehicles to amass money for future investments or purchases; as transaction accounts; and as stable-value investments in their retirement or other investment portfolios. Institutional investors—which include corporations of all sizes, state and local governments, securities lending operations, bank trust departments, sweep programs, securities brokers, and investment managers—use money market funds as a cost-effective way to manage and diversify credit risk, while providing same-day liquidity with market-based yields.

To meet these shareholder needs, funds, intermediaries, service providers, and investors have developed a wide array of arrangements for distributing and using money market funds efficiently. Investors can purchase and redeem money market fund shares directly from fund sponsors or through a wide array of platforms, portals, and financial intermediaries such as broker-dealers and retirement plans. Money market

2 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

funds are the primary investment for sweep accounts offered by broker-dealers and financial advisers. Investors also benefit from the convenience of check-writing or debit-card access to their money market funds. These offerings depend critically on an intricate and complex operational infrastructure created by the industry that allows investors to transact smoothly and efficiently, often with same-day settlement.

Implementing the SEC’s proposed freeze on shareholders’ assets would require changes to a myriad of systems that extend well beyond those under the control of the funds themselves. Fund complexes, intermediaries, and service providers have developed complex systems that allow them to communicate and process significant volumes of money market fund transactions on a daily basis through a variety of mechanisms on behalf of investors. To apply continuous redemption restrictions accurately and consistently across all investors in money market funds, each of these entities, including a host of intermediaries, would need to undertake intricate and expensive programming and other significant, costly system changes.

In many cases, daily redemption restrictions would simply render money market funds useless for offerings and services that investors and intermediaries value. Intermediaries and funds that can and choose to continue to provide money market funds would be required to make extensive and burdensome changes throughout their operational structure.1 The evidence of this paper indicates, however, that the costs of these changes could be prohibitive and that the industry would be unlikely to undertake them, particularly if the SEC’s changes result in shrinking the asset base of money market funds.

The SEC’s suggested redemption restrictions would remove money market funds as a viable option in many instances. Fiduciaries, such as retirement plans, trustees, and investment advisers, may be legally prohibited from using money market funds with redemption restrictions for their clients, because such restrictions would impair clients’ liquidity.2 Sweep programs, which rely upon the ability to move 100 percent of an investor’s available cash on a daily basis, would not be able to employ money market funds if they are subject to a holdback of investor assets.3 Retail investors’ ability to access their money market funds through checks and debit cards could also be impaired.

1 See Securities Industry Financial Markets Association (SIFMA) Money Market Reform Resource Center—Position at http://www.sifma.org/issues/regulatory-reform/money-market-reform/position. “The combination of capital requirements with redemption restrictions is an untenable alternative. … The redemption restrictions piece offers a host of other problems. Simply put, this proposal undermines one of the key features of MMMFs, which is ready liquidity. What’s more, there are significant operational challenges and costs in implementing this proposal.”

2 See Treasury Strategies, Inc., Proposed Holdback Requirement for Money Market Mutual Funds: Ineffective & Crippling Regulation (April 2012) (“TSI Holdback Report”), available at http://sec.gov/comments/4-619/4619-172.pdf. “Using an investment with a holdback would violate the fiduciary’s duty to minimize cost and ensure access to the investor’s money.” Id. at 8. See also Letter from Arnold and Porter submitted on behalf of Federated Investors, Inc. to Elizabeth M. Murphy, Secretary, Securities and Exchange Commission (February 24, 2012) (“Federated Letter”), available at http://sec.gov/comments/4-619/4619-122.pdf, at 19.

3 TSI Holdback Report, supra note 2, at 10 and 13. The TSI Holdback Report discusses the “operational infeasibility” of perpetually restricting cash and the elimination of bank sweep accounts that “would be rendered inoperable by the imposition of a holdback rule.” The report also notes that “if [money market fund] sweeps are operationally and financially destroyed by the holdback, banks would be left holding this cash on their balance sheets.”

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 3

In other uses, funds, intermediaries, and institutional investors conceivably could restructure and reprogram operational systems to incorporate daily redemption restrictions. This paper provides an overview of the systems and processes that would require modification by thousands of institutional investors, funds, intermediaries, and service providers. A thorough analysis of the costs of these changes is beyond the scope of this paper. Based on the Investment Company Institute’s cost-benefit analysis of a prior rule proposal requiring extensive systems and operational changes, however, it is reasonable to expect that requiring money market funds to adopt the SEC’s contemplated restricted share balance concept would cost the industry hundreds of millions of dollars.4 These costs are largely fixed and not scalable to the size of the asset base. It would be difficult for intermediaries, in particular, to justify such expenses even if money market fund assets were to remain at their current level.

Investor reaction to the SEC’s contemplated redemption restrictions, however, suggests that enactment of these proposals would reduce investor use of money market funds. In a major survey of corporate treasurers and other institutional investors, 90 percent of these investors indicated that they would reduce their usage or stop using money market funds altogether if the SEC’s contemplated redemption restrictions were put in place.5 Calculations based on these investors’ responses suggest that institutional assets in money market funds would shrink by two-thirds if the restrictions were imposed. Retail investors also

4 Two years ago, ICI conducted a cost-benefit analysis of proposed changes to Rule 12b-1 under the Investment Company Act that would have required extensive systems and operational changes. The estimated costs for these changes were $231 million for fund complexes only, not including additional costs that would have been incurred by intermediaries. See Investment Company Institute, Cost-Benefit Analysis of SEC Rule 12b-1 Reform Proposal (December 1, 2010), available at http://www.ici.org/pdf/10_12b1_sec_cba.pdf (“12b-1 Cost-Benefit Analysis”), at 11, Figure 4. We believe the changes that would be required to implement the SEC’s redemption restrictions easily could meet or exceed this prior estimate.

5 ICI commissioned a study by Treasury Strategies, Inc. to help understand the effects of the SEC concepts (floating NAV, redemption holdback, or capital requirements) on money market fund investors. The study, Money Market Fund Regulations: The Voice of the Treasurer (April 2012) (“TSI Voice of the Treasurer Study”), is available at http://www.ici.org/pdf/rpt_12_tsi_voice_treasurer.pdf. Corporate treasurers and other institutional investors are significant users of money market funds: institutional share classes account for $1.7 trillion, or 65 percent, of the $2.7 trillion in money market fund assets as of the end of February 2012. If money market funds were required to institute a 30-day holdback of 3 percent of all redemptions, 90 percent of those surveyed would either decrease their use or discontinue their use of money market funds altogether. Based on respondents’ estimates of their changed usage, Treasury Strategies calculated that 67 percent of institutional money market fund assets would move to other investments. BlackRock Inc., in separate interviews of its institutional money market fund shareholders, found “virtually without exception” that redemption restrictions “would cause them to abandon [money market funds].” See BlackRock ViewPoint, Money Market Funds: The Debate Continues—Exploring Redemption Restrictions, Revisiting Floating NAV (March 2012), available at http://sec.gov/comments/4-619/4619-127.pdf.

4 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

have indicated that they would limit their use of money market funds with redemption restrictions.6 Investors that hold accounts directly with funds may choose alternative products that better meet their liquidity needs.7

A sharp reduction in investors’ use of money market funds would have severe consequences. Money market funds hold more than one-third of corporate commercial paper and about three-quarters of state and local government short-term debt. Shrinkage of money market fund assets would significantly disrupt the f low of short-term financing within the American economy.

Adoption of redemption restrictions also likely would increase the size of pooled cash-like investment products that offer a stable NAV outside of Rule 2a-7, the Investment Company Act rule that governs money market funds. Such structural changes could thus move hundreds of billions of dollars of investor assets from highly regulated, clearly defined, and transparent money market funds to stable NAV products that are less regulated, widely varying, and more opaque. This movement would seem unlikely to reduce systemic risk and, indeed, would be more likely to increase risk.

The likely consequences of the SEC’s contemplated redemption restrictions are thus mutually reinforcing. Fund complexes, intermediaries, and service providers will be hard-pressed to justify undertaking the significant costs of compliance with the restrictions in the face of the rapid shrinkage of money market fund assets predicted by investors’ response to the proposals. We believe many intermediaries would make the business decision to migrate to unregulated or less-regulated money market investment vehicles or bank deposit products where possible, in lieu of implementing costly changes to their systems in order to continue to offer money market funds to a dwindling shareholder base. The total effect would be to drive users away from money market funds, disrupt short-term financing for the economy, and increase use of less-regulated, less-transparent alternatives.

6 In a survey of its retail clients, Fidelity Investments found that about half of its retail clients would invest less or stop investing in money market funds with redemption restrictions regardless of whether the restrictions were continual or applied only during periods of market stress. See Fidelity Investments Letter from Scott C. Goebel, Senior Vice President and General Counsel, to Elizabeth M. Murphy, Secretary, Securities and Exchange Commission (February 3, 2012) (“Fidelity Letter”), available at http://sec.gov/comments/4-619/4619-116.pdf.

See also Fidelity Investments Letter from Scott C. Goebel, Senior Vice President and General Counsel, to Elizabeth M. Murphy, Secretary, Securities and Exchange Commission (May 28, 2012) (“Fidelity IOSCO Letter”), available at http://sec.gov/comments/4-619/4619-185.pdf. “Fidelity opposes restrictions on redemptions that impair one of the primary features that attract investors to MMFs—the ability to redeem all shares on a daily basis. We have conducted research surveying both retail and institutional investors on their reactions to the possibility of a liquidity fee on MMFs. Fidelity retail and institutional investors overwhelmingly viewed protecting the principal of, and maintaining ready access to, their investments as the most important characteristics of MMFs. Accordingly, investors reported that they would invest less, or stop investing altogether, in MMFs if there was a possibility of being subjected to a redemption restriction. Given the importance investors place on the liquidity feature of MMFs, it is not surprising that investors reacted so negatively to a potential rule that would restrict access to principal. In addition, it is important to note that the operational challenges and costs of implementing redemption restrictions are extensive and extend beyond the control of MMFs and into the realm of service providers and intermediaries.” Id. at 16.

7 See Letter from Joseph L. Hooley, State Street Corporation (a major global provider of asset management and servicing to money market funds and similar collective investment vehicles), to Mary L. Schapiro, Chairman, Securities and Exchange Commission (February 24, 2012) (“State Street Letter”), available at http://sec.gov/comments/4-619/4619-124.pdf. State Street indicates that a redemption holdback proposal “will greatly reduce the usefulness of money market mutual funds to investors. By driving investors to less well-regulated products, these proposals could increase, rather than decrease, systemic risk.”

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 5

Past Redemption Restrictions Have Been Rare and Carefully Crafted

The SEC’s concept of redemption restrictions applied at all times to all money market funds would impair a core investor protection of mutual funds and reverse more than 70 years of SEC practice in fund regulation.

Under the Investment Company Act of 1940, one hallmark feature of mutual funds, including money market funds, is that they issue “redeemable securities,” meaning that the fund stands ready to buy back its shares at their current NAV. Section 22(e) of the Investment Company Act generally prohibits funds from suspending the right of redemption and from postponing the payment or satisfaction upon redemption of any redeemable security for more than seven days, except under extraordinary circumstances that are delineated in the statute or determined by SEC rule.8

The SEC has rarely exercised its authority to grant such suspensions.9 One exception came in the Commission’s major reform of regulation of money market funds in 2010. The SEC adopted Rule 22e-3, which exempts money market funds from Section 22(e) to permit them to suspend redemptions and postpone payment of redemption proceeds to facilitate an orderly liquidation of the fund.

Rule 22e-3 is carefully crafted and strictly limited to apply only in circumstances when such suspensions serve the best interests of fund shareholders. The rule permits a money market fund to suspend redemptions and payment of redemption proceeds only if the fund’s board, including a majority of disinterested directors, irrevocably has approved liquidation of the fund, based on its determination that the deviation between the fund’s amortized cost price per share and the market-based NAV per share may result in material dilution or other unfair results for shareholders.10 When it adopted the rule, the SEC noted that “Rule 22e-3 is intended to reduce the vulnerability of investors to the harmful effects of a run on the fund, and minimize the potential for disruption to the securities markets.”11

The SEC recognized, however, that suspension of this statutory protection should be limited to extraordinary circumstances. “Because the suspension of redemptions may impose hardships on investors who rely on their ability to redeem shares, the conditions of the rule limit the fund’s ability to suspend redemptions to circumstances that present a significant risk of a run on the fund and

8 Certain foreign regulatory regimes offer fund advisers mechanisms that, provided that the actions are in the interest of fund shareholders, give them significant discretion and flexibility to address extraordinary circumstances, such as an unexpected loss of liquidity in the markets, while also helping them stem an incipient run on a fund. For an overview of the various tools available to offshore funds, see Investment Company Institute, Report of the Money Market Working Group (March 17, 2009), available at http://www.ici.org/pdf/ppr_09_mmwg.pdf, at 85–86.

9 The SEC has not issued any exemptive orders permitting funds to suspend redemptions due to an emergency since 1972. Its staff has issued only three no-action letters permitting funds to suspend redemptions since 1986: during a municipal bond market crisis in 1986; following an earthquake in Hong Kong in 1987; and following the assassination of a Mexican presidential candidate in 1994. In each case, the relief was available for a very short period of time (one or two days) and extended only to those funds particularly affected by the event.

10 Rule 22e-3 also requires the fund, prior to suspending redemptions, to notify the SEC of its decision to liquidate and suspend redemptions.

11 See Money Market Fund Reform, SEC Release No. IC-29132 (February 23, 2010), 75 FR 10060 (March 4, 2010) at 10088.

6 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

potential harm to shareholders. The rule is designed only to facilitate the permanent termination of a fund in an orderly manner.”12 This extraordinary and far-reaching new rule has yet to be tested.

By contrast, the redemption restrictions that the SEC is now contemplating would permanently alter the ability of money market fund investors to redeem all of their shares on a daily basis. The SEC’s contemplated redemption restrictions apparently would apply to all funds and all investors at all times, under all market conditions.

These restrictions also would part from the SEC’s historic use of redemption suspensions only to provide equitable treatment for a fund’s investors. The contemplated redemption restrictions would be explicitly designed to treat shareholders who have redeemed money market fund shares—whether they did so out of concerns about a fund’s stability or in the normal course of their business—differently from non-redeeming shareholders, by imposing first losses in a fund on redeeming shareholders. This form of “asset freeze” thus would mark a significant and unprecedented departure from a hallmark principle of fund regulation.

II. Investors Use Money Market Funds for Diverse PurposesA wide variety of investors use money market funds, primarily because of the product’s liquidity and stable NAV. Funds, intermediaries, and service providers have developed a wide array of arrangements for distributing and using money market funds efficiently. Many of these arrangements would be drastically impaired by redemption restrictions applied continuously, even under normal market conditions, to money market funds.

Institutional investors—including corporations of all sizes, state and local governments, securities lending operations, bank trust departments, sweep programs, securities brokers, and investment managers—use money market funds as a cost-effective way to manage and diversify credit risk, while providing same-day liquidity with market-based yields. These investors often use money market funds as a temporary holding vehicle for cash to facilitate transactions for capital expenditures and day-to-day operations, including payroll.13 Similarly, trust account arrangements use money market funds on a short-term basis pending

12 Id.

13 For more detailed descriptions on how money market funds are used in corporate payroll processing; corporate and institutional operating cash balances; bank trust accounting systems; federal, state, and local government cash balances; municipal bond trustee cash-management systems; consumer receivable securitization; cash processing; escrow processing; 401(k) and 403(b) employee benefit plan processing; broker-dealer and futures dealer customer cash balances; investment of cash collateral for cleared and uncleared swap transactions; cash-management type accounts at banks and broker-dealers; portfolio management; and 529 plans, see Federated Letter, supra note 2.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 7

other activity, such as securities’ transaction settlements, beneficiary expenses, real estate transactions, and other beneficiary related distributions.14

Daily redemption restrictions, or even lack of clarity regarding account balances available for redemption, would severely hamper the f low of funds and the accessibility of cash for transactions that support these entities’ ongoing operations.

Sweep vehicles offered by brokerage firms, banks, and trading platforms use money market funds to invest cash held in customer accounts. Like institutional accounts, sweep vehicles hold investor cash on a temporary basis; customers intend to use this cash primarily to fund trading activity conducted in their accounts. Sweeps are initiated by intermediaries at the end of the day. Typically, after all other transactions for the day have been posted, the total remaining collected balances (or all available cash) in customer accounts are invested in (swept into) money market funds.

Daily redemption restrictions would impede the availability of funds to settle customers’ securities transactions and to remain in compliance with margin rule requirements applicable to brokerage accounts.

Retail investors often use money market funds to temporarily hold cash from redemption transactions on their long-term mutual funds. Cash in money market funds may also be used to fund future purchase transactions (through exchanges or other reinvestment transactions) or to pay ongoing expenses (using both check-writing15 and debit-card functionality) and future (planned) expenditures, including tuition and education related expenses.

As detailed below, continuous redemption restrictions would significantly impair money market funds’ and intermediaries’ ability to offer money market fund features and liquidity (e.g., check writing and debit cards) that retail investors expect and value.

Retirement account investors may choose to invest a portion of their tax-advantaged retirement assets in money market funds. These assets are often temporary in nature and used to fund other investment transactions. In other cases, retired investors use assets in money market funds to support ongoing expenses.

As fiduciaries, retirement plan sponsors may be barred from offering money market funds that are subject to redemption restrictions to plan participants.16 Such restrictions would also impair the features and liquidity of money market funds that retirees, along with other retail investors, rely upon and value.

14 See Letter from Robert K. Ward, SunGard Global Network, to Mary Schapiro, Chairman, Securities and Exchange Commission (March 16, 2012), available at http://sec.gov/comments/4-619/4619-151.pdf. SunGard and its affiliate (SunGard Institutional Brokerage Inc.) operate the SunGard Global Network Short-Term Cash Management Portal that enables customers to research, analyze, and trade hundreds of money market funds through a single connection. SunGard also offers cash-management tools for corporate treasuries and a trust accounting platform. SunGard helps its corporate treasury customers manage over $100 billion in money market fund assets. In a 2011 SunGard investment study of corporate treasurers and cash managers, 88 percent of those surveyed cited “immediate access to cash as a major requirement of their cash investment policies.” Thus the imposition of “any sort of a holdback requirement would eliminate the high degree of liquidity that is a sine qua non for the continued use of money market funds to hold corporate and trust liquidity balances.” Id.

15 See Letter from DST Systems, Inc. to Elizabeth M. Murphy, Secretary, Securities and Exchange Commission (March 12, 2012), available at http://sec.gov/comments/4-619/4619-128.pdf. DST Systems, Inc. provides information processing solutions and services to support the global asset management, insurance, retirement, brokerage, and health care industries. The letter cites that “over $1.9 million check writing drafts [on money market funds] cleared through their transfer agency systems in 2011.”

16 See TSI Holdback Report and Federated Letter, supra note 2.

8 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

III. How the SEC’s Redemption Restriction Proposal Might WorkShould the SEC choose to impose continuous redemption restrictions on money market funds and their investors, the possible restrictions could come in many forms.

Public statements indicate that regulators appear to be focusing on a restricted share balance approach. This approach would require funds and intermediaries to calculate and establish the number of shares that would be restricted or held back in each investor’s account every day. While various restriction terms and calculation methods are possible under this approach, our analysis will focus on a restricted share balance of 3 percent of an account’s shares based on a rolling 30-day time frame that would “look back” to the investor’s highest daily balance (the “high-water-mark method”).17

A. How the High-Water-Mark Method Might WorkEach business day, a high-water mark for each shareholder in the fund would be determined as the maximum of the shareholder’s daily account balance over the previous 30 days.

Based on the daily high-water mark, each shareholder would have a restricted share balance equal to 3 percent of that shareholder’s current high-water mark.

Shareholders could redeem nonrestricted shares at a stable $1.00 NAV. They would be prohibited, however, from redeeming shares in the restricted share balance. Thus, the maximum a shareholder could receive in immediate redemption proceeds on any given day would be the shareholder’s current account balance less the shareholder’s restricted share balance. If the shareholder wished to redeem the entire account balance, the restricted share balance would be held back for a period of 30 days and released to the shareholder if the fund did not break the dollar during that period.

Every shareholder’s restricted share balance would be available to absorb losses should the fund break the dollar. Shareholders who redeemed shares within the 30 days prior to the break-the-dollar event, however, would be subject to losses before other shareholders who had not redeemed.

The portion of each shareholder’s restricted share balance that would be first in line to absorb losses (the shareholder’s “subordinated restricted shares”) would be calculated each day and would depend primarily on the amount of net redemptions in the shareholder’s account over the past 30 days relative to the daily high-water mark.

If losses to the fund exceed the fund’s aggregate amount of subordinated restricted shares, the additional loss would be applied pro rata to the remainder of all investors’ restricted share balances, and, lastly, if necessary, to the unrestricted share balances of all remaining shareholders in the fund.

17 In addition to the high-water-mark method of calculation, other approaches to a daily restricted share balance approach could include applying a specific dollar amount or percentage or using a rolling 30-day average balance. These methods would impose smaller restrictions on shareholder redemption activity than the high-water-mark method, but would be less accurate or equitable from a “first-loss” perspective.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 9

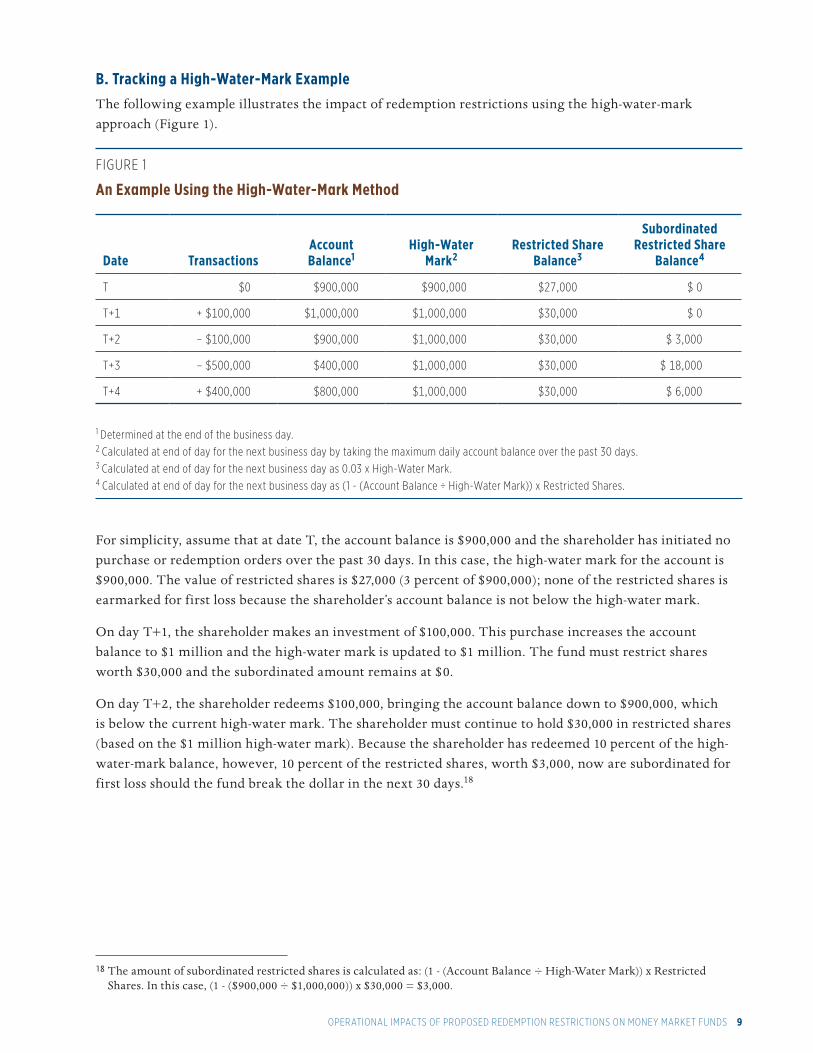

B. Tracking a High-Water-Mark ExampleThe following example illustrates the impact of redemption restrictions using the high-water-mark approach (Figure 1).

fiGure 1

An Example Using the High-Water-Mark Method

Date TransactionsAccount Balance1

High-Water Mark2

Restricted Share Balance3

Subordinated Restricted Share

Balance4

t $0 $900,000 $900,000 $27,000 $ 0

t+1 + $100,000 $1,000,000 $1,000,000 $30,000 $ 0

t+2 – $100,000 $900,000 $1,000,000 $30,000 $ 3,000

t+3 – $500,000 $400,000 $1,000,000 $30,000 $ 18,000

t+4 + $400,000 $800,000 $1,000,000 $30,000 $ 6,000

1 determined at the end of the business day.2 calculated at end of day for the next business day by taking the maximum daily account balance over the past 30 days.3 calculated at end of day for the next business day as 0.03 x High-Water mark.4 calculated at end of day for the next business day as (1 - (account Balance ÷ High-Water mark)) x restricted shares.

For simplicity, assume that at date T, the account balance is $900,000 and the shareholder has initiated no purchase or redemption orders over the past 30 days. In this case, the high-water mark for the account is $900,000. The value of restricted shares is $27,000 (3 percent of $900,000); none of the restricted shares is earmarked for first loss because the shareholder’s account balance is not below the high-water mark.

On day T+1, the shareholder makes an investment of $100,000. This purchase increases the account balance to $1 million and the high-water mark is updated to $1 million. The fund must restrict shares worth $30,000 and the subordinated amount remains at $0.

On day T+2, the shareholder redeems $100,000, bringing the account balance down to $900,000, which is below the current high-water mark. The shareholder must continue to hold $30,000 in restricted shares (based on the $1 million high-water mark). Because the shareholder has redeemed 10 percent of the high-water-mark balance, however, 10 percent of the restricted shares, worth $3,000, now are subordinated for first loss should the fund break the dollar in the next 30 days.18

18 The amount of subordinated restricted shares is calculated as: (1 - (Account Balance ÷ High-Water Mark)) x Restricted Shares. In this case, (1 - ($900,000 ÷ $1,000,000)) x $30,000 = $3,000.

10 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

On day T+3, the shareholder redeems an additional $500,000, further lowering the account balance to $400,000. The restricted share balance is unchanged at $30,000. The shareholder now has $18,000 worth of restricted shares subordinated for first loss.

On day T+4, the shareholder invests $400,000. The account balance of $800,000 is still lower than the high-water mark of $1 million, and the restricted balance is unchanged at $30,000. The shareholder is still subject to a first-loss position, but on a smaller amount of $6,000.

Those who favor a subordinated restricted share approach believe that it would stop shareholders from redeeming shares in times of stress. In addition, the intent of this approach is to penalize shareholders who redeemed shares within the previous 30 days should the fund experience a loss due to breaking the dollar. Requiring such restrictions every day and under all market conditions, however, imposes significant operational challenges, complexities, and costs on investors, funds, and their intermediaries. Further, these restrictions are unlikely to prevent shareholders from redeeming en masse during a time of crisis.19

19 See TSI Holdback Report, supra note 2, at 5 and 14.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 11

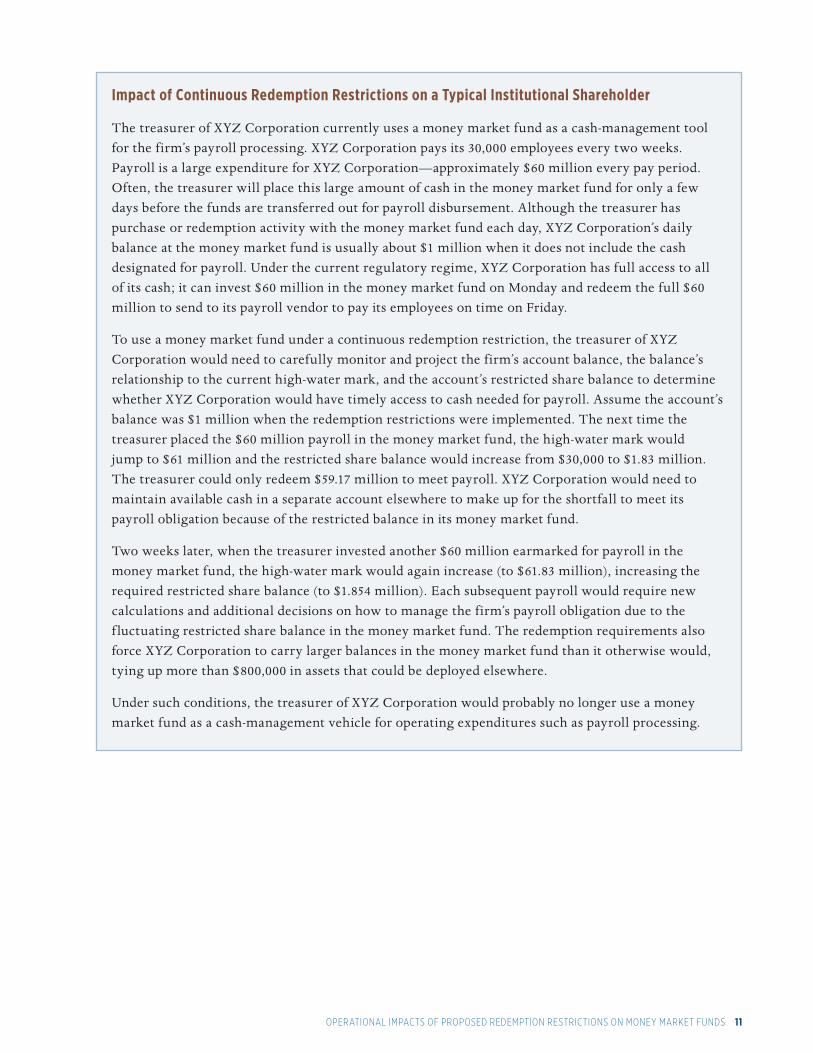

Impact of Continuous Redemption Restrictions on a Typical Institutional Shareholder

The treasurer of XYZ Corporation currently uses a money market fund as a cash-management tool for the firm’s payroll processing. XYZ Corporation pays its 30,000 employees every two weeks. Payroll is a large expenditure for XYZ Corporation—approximately $60 million every pay period. Often, the treasurer will place this large amount of cash in the money market fund for only a few days before the funds are transferred out for payroll disbursement. Although the treasurer has purchase or redemption activity with the money market fund each day, XYZ Corporation’s daily balance at the money market fund is usually about $1 million when it does not include the cash designated for payroll. Under the current regulatory regime, XYZ Corporation has full access to all of its cash; it can invest $60 million in the money market fund on Monday and redeem the full $60 million to send to its payroll vendor to pay its employees on time on Friday.

To use a money market fund under a continuous redemption restriction, the treasurer of XYZ Corporation would need to carefully monitor and project the firm’s account balance, the balance’s relationship to the current high-water mark, and the account’s restricted share balance to determine whether XYZ Corporation would have timely access to cash needed for payroll. Assume the account’s balance was $1 million when the redemption restrictions were implemented. The next time the treasurer placed the $60 million payroll in the money market fund, the high-water mark would jump to $61 million and the restricted share balance would increase from $30,000 to $1.83 million. The treasurer could only redeem $59.17 million to meet payroll. XYZ Corporation would need to maintain available cash in a separate account elsewhere to make up for the shortfall to meet its payroll obligation because of the restricted balance in its money market fund.

Two weeks later, when the treasurer invested another $60 million earmarked for payroll in the money market fund, the high-water mark would again increase (to $61.83 million), increasing the required restricted share balance (to $1.854 million). Each subsequent payroll would require new calculations and additional decisions on how to manage the firm’s payroll obligation due to the f luctuating restricted share balance in the money market fund. The redemption requirements also force XYZ Corporation to carry larger balances in the money market fund than it otherwise would, tying up more than $800,000 in assets that could be deployed elsewhere.

Under such conditions, the treasurer of XYZ Corporation would probably no longer use a money market fund as a cash-management vehicle for operating expenditures such as payroll processing.

12 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

IV. Money Market Funds Operate in a Complex EnvironmentBefore discussing in detail the difficulties associated with implementing daily redemption restrictions on money market fund shares, we summarize brief ly the role intermediaries play in servicing shareholders and provide an overview of mutual fund transaction processing. We believe this core knowledge is fundamental to understanding the operational complexities of applying a daily redemption restriction.

Today, 57 million retail investors20 and thousands of institutional investors use money market funds. These investors interact with their funds in a variety of ways. Investors can purchase shares and maintain their accounts directly with a fund company, through a broker-dealer, within a fund supermarket or platform, via a financial planner or registered investment adviser, within a retirement plan, or through a bank trust department.

Investors and their intermediaries use various technologies to interact with funds. An investor can obtain information and transact business by visiting a branch office, calling the toll-free number of a fund or intermediary, using automated telephone services, or accessing proprietary websites. The technologies and processes used to support each of these distribution channels require funds, intermediaries, and the various companies that provide services to them to synchronize efforts and share data on a near–real time basis so that investors receive accurate information on their transactions and balances, regardless of the channel or technology used. This complex network of entities includes:

» institutional and commercial investors (corporate entities, federal, state, and local governments, trusts, etc.) that use money market funds,

» mutual fund transfer agents, investment advisers, and distributors,

» intermediaries,

» third-party systems and service providers, and

» the Depository Trust & Clearing Corporation (DTCC) and its subsidiary, the National Securities Clearing Corporation (NSCC).21

Fund complexes and their vendors also have intricate and complex systems to accommodate the unique needs of money market fund investors.22 Because investors expect immediate access to their money market funds assets, liquidity and a stable NAV are essential product features in their lineup of investment options. Implementing redemption restrictions on money market fund assets would impair these key features and would create costly operational burdens for the wide range of entities and thousands of systems that support this infrastructure.

20 In 2011, ICI research found that 63 percent of mutual fund–owning households owned money market funds. Applying that to the number of mutual fund–owning households (52.3 million) and the average number of mutual fund owners in each mutual fund–owning household (1.728), we calculate that 56.9 million individuals owned money market funds in 2011. See “Ownership of Mutual Funds, Shareholder Sentiment, and Use of the Internet, 2011,” ICI Research Perspective (October 2011), available at www.ici.org/pdf/per17-05.pdf, Figures A1 and A2; and “Characteristics of Mutual Fund Investors, 2011,” ICI Research Perspective (October 2011), available at www.ici.org/pdf/per17-06.pdf, Figure 5.

21 For many mutual funds, transactions that occur through intermediaries are processed through the industry utility provided by the Depository Trust and Clearing Corporation (DTCC). The DTCC offers mutual fund services through its subsidiary, the National Securities Clearing Corporation (NSCC).

22 For a detailed description of money market fund operations and systems, see Letter from Karrie McMillan, General Counsel, Investment Company Institute, to Elizabeth M. Murphy, Secretary, Securities and Exchange Commission (September 8, 2009), available at http://sec.gov/comments/s7-11-09/s71109-117.pdf.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 13

A. Intermediaries Play a Major Role Today, rather than dealing directly with a money market fund, many shareholders purchase, sell, and hold their money market fund shares through intermediaries that provide recordkeeping and other services to their clients and transact money market fund shares on their behalf. Examples of intermediaries that offer money market funds to their customers are broker-dealers, portals, bank trust departments, insurance companies, and retirement plan administrators.

Intermediaries typically process customer transactions through omnibus or through intermediary-controlled accounts through the NSCC. An omnibus account includes the shares of multiple investors—sometimes numbering in the thousands—that are customers of the intermediary. Omnibus accounts are held on the books of a fund in the name of the financial intermediary, acting on behalf of its customers.23 When an intermediary submits its transactions for an omnibus account, it usually consolidates the transactions of all customers that are purchasing or redeeming shares of the same fund that day into one or a few “summary” transactions for processing by the money market fund. In some cases, the intermediary or a shareholder serviced by an intermediary may transact directly with the money market fund through its fund transfer agent.

As a result of investors’ extensive use of financial intermediaries to effect mutual fund transactions, a mutual fund recordkeeper may have limited information on the underlying shareholders in omnibus accounts.24 Although the fund’s lack of information does not affect the shareholder’s ownership rights, it does impair the fund’s ability to comply with any redemption restriction requirement predicated on the fund knowing the identity and detailed transaction activity of each underlying shareholder. Without a direct relationship with these underlying shareholders—which is often lacking when investors own funds through an intermediary—the fund does not have access to the account-level information necessary to apply a continuous redemption restriction accurately. (For more detailed information on the difficulties associated with funds applying daily redemption restrictions on omnibus accounts, see Section VII below.)

23 This includes omnibus account structures and intermediary-controlled individual accounts in which the fund has no relationship or contact with the customer, as well as other institutional customers for which the fund lacks direct knowledge of the beneficial owners of the shares.

24 If a customer opens an account directly with a fund, the fund recordkeeper is required by law to maintain certain ownership and account information on the investor. Fund recordkeepers, however, have little if any information about underlying customers that invest through an intermediary’s omnibus account. Instead, the shareholder reflected on the fund’s records is the financial intermediary. With omnibus accounts, the fund recordkeeper is not tracking which of the intermediary’s customers are buying or selling shares, how many of these customers are making transactions, or the number or details of individual transactions involved. Rather, the intermediary combines the transactions of underlying shareholders, and the fund’s recordkeeper is tracking only the aggregate activity and overall total balance for the intermediary. The intermediary maintains the records of each individual customer’s transactions and provides information, such as trade confirmations, statements, any tax documents, and shareholder communications to those customers.

14 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

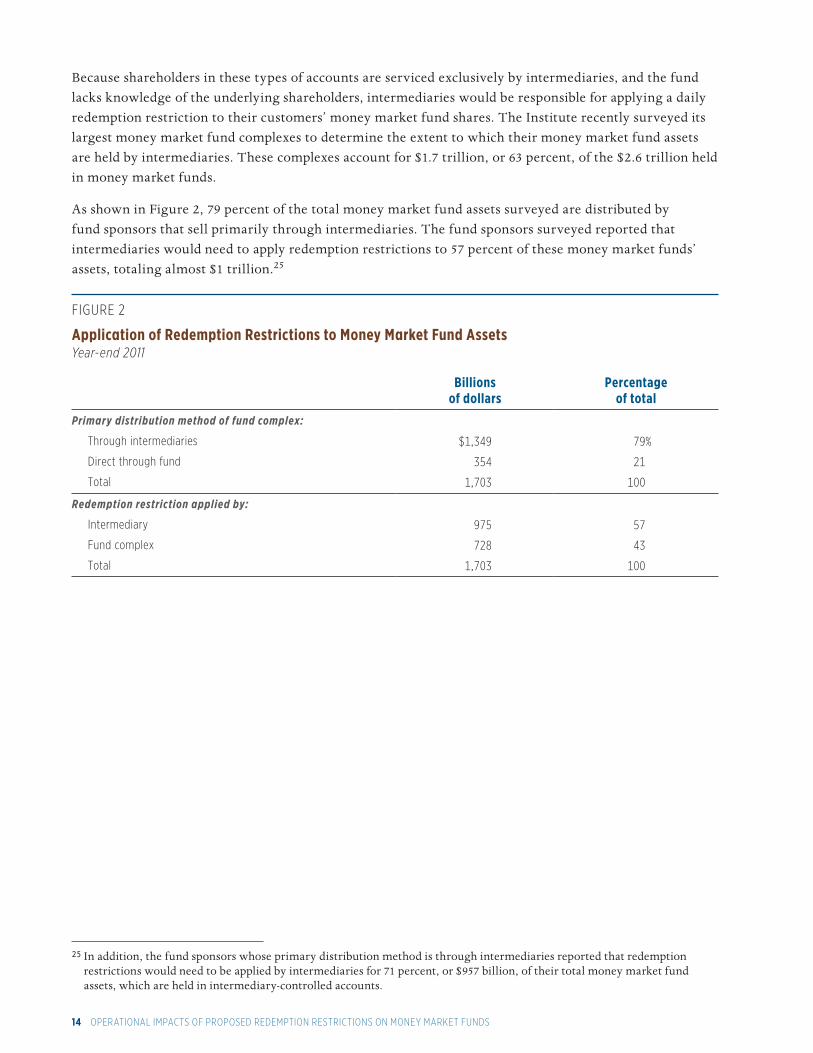

Because shareholders in these types of accounts are serviced exclusively by intermediaries, and the fund lacks knowledge of the underlying shareholders, intermediaries would be responsible for applying a daily redemption restriction to their customers’ money market fund shares. The Institute recently surveyed its largest money market fund complexes to determine the extent to which their money market fund assets are held by intermediaries. These complexes account for $1.7 trillion, or 63 percent, of the $2.6 trillion held in money market funds.

As shown in Figure 2, 79 percent of the total money market fund assets surveyed are distributed by fund sponsors that sell primarily through intermediaries. The fund sponsors surveyed reported that intermediaries would need to apply redemption restrictions to 57 percent of these money market funds’ assets, totaling almost $1 trillion.25

fiGure 2

Application of Redemption Restrictions to Money Market Fund AssetsYear-end 2011

Billions of dollars

Percentage of total

Primary distribution method of fund complex:

through intermediaries

direct through fund

total

$1,349

354

1,703

79%

21

100

Redemption restriction applied by:

intermediary

fund complex

total

975

728

1,703

57

43

100

25 In addition, the fund sponsors whose primary distribution method is through intermediaries reported that redemption restrictions would need to be applied by intermediaries for 71 percent, or $957 billion, of their total money market fund assets, which are held in intermediary-controlled accounts.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 15

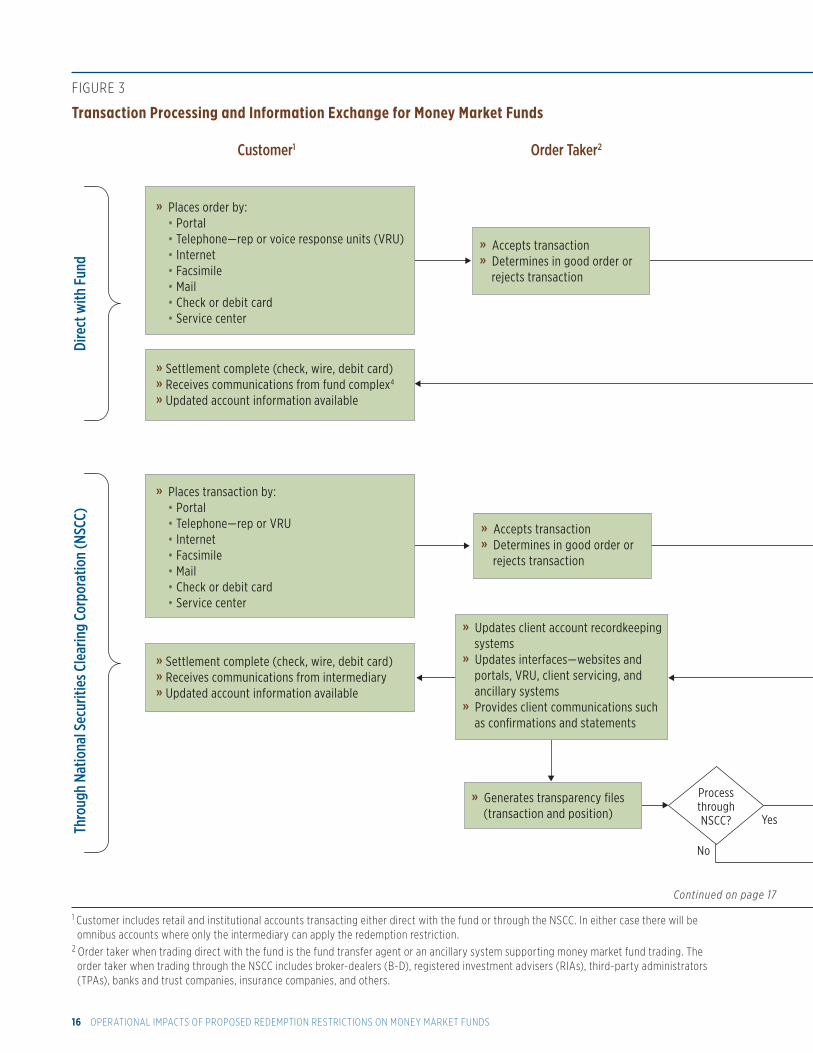

B. How Mutual Fund Transactions Are Processed Figure 3 on pages 16 and 17 illustrates how mutual fund customers and the various organizations in the industry interact when placing a purchase or redemption order. It also displays the role these entities play in processing the customer’s instructions and delivering critical information needed regarding the transactions. As illustrated in Figure 3, customer orders to purchase or redeem money market fund shares can be conveyed in a variety of ways, such as via a portal,26 telephone,27 Internet, mail, check, debit card, or a service center. The upper panel of Figure 3 depicts the transaction processing and information exchange that takes place for purchase or redemption orders that are submitted directly to a fund by investors.28 The lower panel depicts the transactions submitted to the fund for processing through the NSCC’s systems.29 Most of the shares transacted through the NSCC are held by intermediaries in omnibus accounts or intermediary-controlled networked accounts.

Although Figure 3 captures the various steps that occur in the transaction processing cycle for both scenarios, it does not highlight the thousands of intermediaries and vendors that would be affected or the wide range of systems involved that would require modifications to implement redemption restrictions. These difficulties are the focus of Sections V and VI and Figures 4, 5, and 6.

As illustrated in the top panel of Figure 3, after a customer submits a transaction request direct with the fund, the order is passed to the fund’s transfer agent, or recordkeeper, through both primary and ancillary systems. The fund transfer agent determines if the transaction is “in good order”30 and then executes the requested transaction (assuming it passes required systems edits). The transfer agent updates the fund’s primary recordkeeping and ancillary systems and then settles the transaction either the same day (trade date, or T) or the next day (one business day after trade date, or T+1). The fund’s transfer agent provides the necessary client communications, such as confirmations and statements, and then completes the settlement (e.g., for redemptions, the transfer agent forwards proceeds, such as checks or wires) for the customer. The fund then generates applicable internal reports for reconciliation, fund portfolio (cash management), accounting, and financial reporting purposes, among other things.

26 Portals are established by vendors as proprietary, automated, typically web-based services. Portals provide an order-routing conduit between institutional investors and an array of money market funds. Settlement of money market fund transactions placed through portals is typically done through the Fedwire system for same-day settlement. Same-day settlement transactions are those where the order (either to buy or to sell) is sent to the money market fund on day 1 and the money settlement for both purchases and redemptions also occurs on day 1. Approximately two-thirds of money market fund assets are in institutional share classes that primarily use same-day settlement for their money market fund transactions.

27 Shareholders can speak with a live representative or execute orders through automated telephone services (voice response unit or VRU).

28 Some intermediary omnibus accounts transact directly with a fund. The fund may or may not have knowledge of the underlying shareholders of such omnibus accounts.

29 The NSCC offers two services for mutual fund clearance and settlement, Fund/SERV and Networking. Fund/SERV provides a standardized and fully automated platform to process and settle purchase, exchange, and redemption orders. Networking supports the exchange and reconciliation of “networked” account information as held on the books of the transfer agent with the information held on the books of the intermediary. For NSCC participants, these automated services provide secure, efficient, and cost-effective trading, money settlement, and information exchange through dedicated system connections using standardized formats and procedures. Because these systems employ established requirements, time frames are set so a sender and a receiver know the parameters for exchanging trade and account-related information. Knowing the established requirements and time frames enables both sides to create control points for receipt of data and exception processing for missing data. Both omnibus and individual account transactions are processed through NSCC.

30 Transactions presented must meet processing guidelines as defined by the service provider or they will be rejected because they cannot be processed “in good order.”

16 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

fiGure 3

Transaction Processing and Information Exchange for Money Market Funds

Dire

ct w

ith F

und

Thro

ugh

Natio

nal S

ecur

ities

Cle

arin

g Co

rpor

atio

n (N

SCC)

Customer1 Order Taker2 NSCC Fund Transfer Agent Recordkeeper3Fund Portfolio Cash

Management/Fund Accounting and Financial Reporting

» Places order by: • Portal • Telephone—rep or voice response units (VRU) • Internet • Facsimile • Mail • Check or debit card • Service center

» Settlement complete (check, wire, debit card)» Receives communications from fund complex4

» Updated account information available

» Places transaction by: • Portal • Telephone—rep or VRU • Internet • Facsimile • Mail • Check or debit card • Service center

» Settlement complete (check, wire, debit card)» Receives communications from intermediary» Updated account information available

» Accepts transaction» Determines in good order or rejects transaction

» Accepts transaction» Determines in good order or rejects transaction

» Updates client account recordkeeping systems» Updates interfaces—websites and portals, VRU, client servicing, and ancillary systems» Provides client communications such as confirmations and statements

» Generates transparency files (transaction and position)

» NSCC passes transaction files

» NSCC passes confirmation and activity files» Provides T or T+1 net settlement

» NSCC passes transparency files

» Processes transactions for both individual and omnibus accounts» Updates fund recordkeeping systems including transfer agent and ancillary systems

» Updates client account recordkeeping systems» Updates interfaces—websites and portals, VRU, client servicing, and ancillary systems» Provides client communications such as confirmations and statements» Settles transaction on either the trade date (T) or on trade date+1 business day (T+1)

» Accepts/rejects and processes transactions for both networked (individual) and omnibus (aggregated) accounts» Updates fund transfer agent recordkeeping systems

» Settles transaction on either trade date (T) or on trade date+1 business day (T+1)» Generates intermediary communications such as NSCC confirmation and activity files

» Receives transparency files and updates corporate or ancillary repositories/systems

» Generates reports for cash management and settlement» Completes fund accounting and financial reporting

ProcessthroughNSCC? Yes

No

1 customer includes retail and institutional accounts transacting either direct with the fund or through the nscc. in either case there will be omnibus accounts where only the intermediary can apply the redemption restriction.

2 Order taker when trading direct with the fund is the fund transfer agent or an ancillary system supporting money market fund trading. the order taker when trading through the nscc includes broker-dealers (B-d), registered investment advisers (rias), third-party administrators (tpas), banks and trust companies, insurance companies, and others.

Continued on page 17

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 17

fiGure 3

Transaction Processing and Information Exchange for Money Market Funds

Dire

ct w

ith F

und

Thro

ugh

Natio

nal S

ecur

ities

Cle

arin

g Co

rpor

atio

n (N

SCC)

Customer1 Order Taker2 NSCC Fund Transfer Agent Recordkeeper3Fund Portfolio Cash

Management/Fund Accounting and Financial Reporting

» Places order by: • Portal • Telephone—rep or voice response units (VRU) • Internet • Facsimile • Mail • Check or debit card • Service center

» Settlement complete (check, wire, debit card)» Receives communications from fund complex4

» Updated account information available

» Places transaction by: • Portal • Telephone—rep or VRU • Internet • Facsimile • Mail • Check or debit card • Service center

» Settlement complete (check, wire, debit card)» Receives communications from intermediary» Updated account information available

» Accepts transaction» Determines in good order or rejects transaction

» Accepts transaction» Determines in good order or rejects transaction

» Updates client account recordkeeping systems» Updates interfaces—websites and portals, VRU, client servicing, and ancillary systems» Provides client communications such as confirmations and statements

» Generates transparency files (transaction and position)

» NSCC passes transaction files

» NSCC passes confirmation and activity files» Provides T or T+1 net settlement

» NSCC passes transparency files

» Processes transactions for both individual and omnibus accounts» Updates fund recordkeeping systems including transfer agent and ancillary systems

» Updates client account recordkeeping systems» Updates interfaces—websites and portals, VRU, client servicing, and ancillary systems» Provides client communications such as confirmations and statements» Settles transaction on either the trade date (T) or on trade date+1 business day (T+1)

» Accepts/rejects and processes transactions for both networked (individual) and omnibus (aggregated) accounts» Updates fund transfer agent recordkeeping systems

» Settles transaction on either trade date (T) or on trade date+1 business day (T+1)» Generates intermediary communications such as NSCC confirmation and activity files

» Receives transparency files and updates corporate or ancillary repositories/systems

» Generates reports for cash management and settlement» Completes fund accounting and financial reporting

ProcessthroughNSCC? Yes

No

3 systems supported by fund recordkeeper impacted by a redemption restriction may include: transfer agent, ancillary order management, corporate data repositories, tax, distributions, data communications, and settlement.

4 includes information to a broker-dealer who is recorded on the fund transfer agent’s records and whose customer initiates transactions directly with the fund. this information is provided through the nscc to meet broker-dealer books and records requirements.

Continued from page 16

18 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

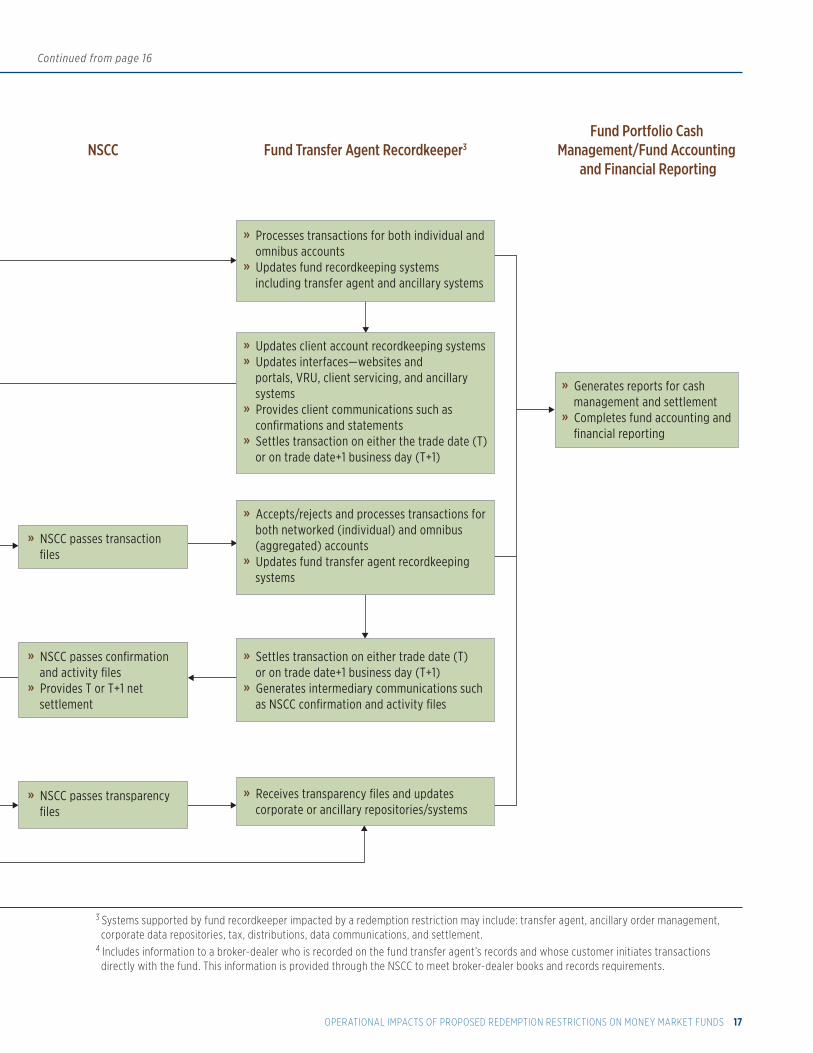

The lower panel of Figure 3 details the processing and information exchange for transactions that pass through the NSCC. For these transactions, a customer’s order is submitted to its intermediary, such as a broker-dealer or a retirement plan administrator or recordkeeper. The order taker determines whether the transaction is in good order and, if so, passes the order (usually aggregated with other orders from that order taker’s clients) to the NSCC. Through Fund/SERV, trade orders are electronically transmitted from the intermediary to the fund.31 Once processed, the NSCC forwards the acknowledgments (confirming transactions) to each of the intermediaries. This process supports account-opening trades, as well as subsequent purchases, redemptions, and exchanges for existing accounts. Fund/SERV also facilitates the settlement of trades so that funds and intermediaries are managing only a single net settlement each day.32 Once transaction processing through the NSCC is complete, the intermediary updates its client platforms, account recordkeeping systems, and ancillary systems; provides the necessary client communications, such as confirmations and statements; and then completes the settlement for its customers.

Figure 3 also demonstrates how intermediaries may provide transparency information for omnibus accounts through the NSCC’s Networking service. For example, a broker-dealer or retirement plan may transmit data files to a fund transfer agent or an affiliated entity that contains omnibus subaccounting details that the fund will utilize in separate databases or repositories for certain compliance or operations activities, such as monitoring for market timing to comply with SEC Rule 22c-2,33 fund blue-sky reporting,34 or to reconcile intermediary fee invoices. Fund transfer agents, however, cannot use the provided supplemental data to shadow recordkeep subaccounts held by intermediaries in omnibus positions; nor could they use it to apply redemption restrictions.35

31 The NSCC collects all the trades from intermediaries for a particular fund complex for the day and on a regular schedule transmits those collected orders to the fund’s transfer agent for processing. After the fund accountant provides that day’s NAV for the fund shares to the transfer agent, the transfer agent values the trades, creates acknowledgments, and transmits them to NSCC.

32 Under this arrangement, NSCC calculates the monetary impact of all trade activity for each day for any particular fund, as well as any particular intermediary, and provides a net settlement report to each. As part of service membership, fund complexes and intermediaries generally agree to allow NSCC to either credit or debit a designated bank account daily to complete the money movement for all amounts owed or expected that day.

33 SEC Rule 22c-2 under the Investment Company Act (adopted April 2006), is known as the “redemption fee rule.” It was enacted to combat frequent trading and market timing abuses. The rule requires, among other things, that funds enter into written agreements with intermediaries that hold shares on behalf of other investors, under which the intermediaries must agree to (a) provide funds with certain shareholder identity and transaction information if the fund requests it; and (b) implement any instruction from the fund to impose trading restrictions against shareholders the fund has identified as violating the fund’s market timing policies. For the bank and retirement channels, NSCC’s Standardized Data Reporting (SDR) system is used by certain intermediaries to supply subaccount details in response to a request for information from the fund complex to comply with Rule 22c-2.

34 Funds are subject to ongoing compliance with state blue-sky laws that require notice filings in each state where shares are expected to be sold. This includes initial registrations, annual filings, renewals, sales reports, and amendment filings.

35 Supplemental data that are provided by a subset of omnibus intermediaries are “point in time” data that do not replicate an underlying customer’s full account history and therefore are not useful in applying redemption restrictions such as the high-water-mark method.

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 19

Money market fund investor and intermediary transactions, whether processed direct with the fund through portals and customized interfaces or through the NSCC’s Fund/SERV system, are submitted for both same-day and T+1 settlement.36 Many money market fund investors (primarily intermediaries or institutions on behalf of beneficial owners) use same-day settlement to move money into and out of their accounts intraday for a variety of time-sensitive business and personal transactions.37 Since these transactions typically occur sporadically throughout the day or late in the day (especially for West Coast investors), most same-day settlement investors transact direct with the fund through vendor portals or through customized transmissions with the fund and settle via multiple Fedwires throughout the day.38 Many fund complexes, in servicing these institutional customers, have developed proprietary, customized “ancillary” systems that overlay or integrate with their fund transfer agent systems in order to use real-time processing. These systems were created to allow fund transfer agents to receive, process, and transmit updated settlement and share balance information intraday on transactions for intermediaries and customers using same-day settlement funds.39

For T+1 settlement, fund transfer agents and intermediaries process transactions received from investors in money market funds that settle the next business day. These systems also are complex because they collect all investor transactions received by various means throughout the trading day and then batch-process them as part of a nightly processing cycle.40

C. Mutual Fund Transfer Agent, Intermediary, and Ancillary SystemsA large percentage of mutual funds in the industry uses one of three large, external mutual fund transfer agent vendors in some capacity to process investor transactions. These arrangements vary. Some fund complexes rely on an external provider to perform all or some of the fund’s transfer agency function, while others operate their own transfer agency, but use a vendor’s transfer agent systems via remote access. A few large fund complexes have completely internalized the transfer agent function, using proprietary and highly customized transfer agent systems. Some smaller fund complexes also use proprietary systems, although many small fund complexes use systems and services from a number of smaller transfer agent vendors.

36 In limited situations, money market fund transactions may settle on T+3 to accommodate the need for advisers to synchronize settlement involving transactions with other securities (e.g., exchange-traded funds, equities, or fixed income products).

37 These include brokerage sweep, corporate, partnership, bank or trust, institutional, and individual investor accounts. Monies moved intraday are needed to fund other transactions (e.g., securities purchases, real estate settlements, or corporate treasury cash management).

38 The NSCC Fund/SERV order routing system (see NSCC workflow on Figure 3) handles only a small volume of same-day settlement transactions that occur early in the day. NSCC cutoff times for same-day settlement are midmorning on trade date (T).

39 Many same-day settlement transactions are received in a compressed time frame late in the day (prior to the fund’s and Fedwire’s closing).

40 Such transactions are received directly by the fund or intermediaries from investors via check and application, through the Internet, for automatic investment plans, systematic withdrawal plans, debit cards and check writing, for exchange transactions, by phone, etc. In “batch-processing,” all of these collected orders are processed at the same time on a predetermined schedule.

20 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

Even though a fund complex’s transfer agent system is the primary recordkeeping system for tracking share ownership in a fund, there are a substantial number of additional subsystems and ancillary systems that overlay, are integrated with, or feed to or from a fund’s primary transfer agent system. These systems have been created to accommodate the various features and services demanded by investors, and to comply with a fund’s regulatory and compliance obligations. A number of essential ancillary systems are used by funds in conjunction with the core transfer agent systems to complete the purchase or redemption processing cycle; provide shareholders updated account information through a variety of interfaces; generate related shareholder communications, including any required tax reporting;41 and report updated information both internally at the fund complex (e.g., for cash management, fund accounting, and compliance purposes) and externally to intermediaries for customer transactions processed directly at the fund. These ancillary systems typically incorporate custom development and may be proprietary or vendor dependent. For example, most transfer agents (whether proprietary or external) use print vendors to produce trade confirmations and shareholder statements.

There also are significant numbers of intermediary platforms, subaccounting, recordkeeping, and ancillary systems that support the processing of money market fund transactions for customers of intermediaries. These systems are tailored to support the business models of various intermediaries (e.g., broker-dealers, banks, insurance companies, trusts, and 401(k) administrators and recordkeepers), which vary in size and complexity (as they support other securities in addition to mutual funds), and may include proprietary or ancillary systems that are supported by a wide range of vendors.

V. Implementing Redemption Restrictions Would Create Significant Operational Difficulties and CostsImposing redemption restrictions on shareholders will require substantial and costly system changes, and place burdensome processes and procedures on thousands of entities that use and support money market funds. Implementing these restrictions would involve an extraordinary amount of coordinated effort to carry out changes to accommodate the new product features.42 Industry experts already have informed the SEC that such a requirement for money market fund investors would require “pervasive and expensive systems and operational changes for a wide variety of parties” that provide money market funds to investors.43 Those parties include:

» Funds: Modifying funds’ core transfer agent systems, integrated ancillary systems and the special same-day settlement processes and customized transmissions, and reporting mechanisms to handle redemption restriction requirements would be a significant undertaking that will require extensive analysis, programming, and testing to ensure the operational impacts are accurately addressed prior to implementation.

41 Ancillary systems also include year-end tax reporting for Internal Revenue Service Forms 1099-B and cost basis related systems that do not apply normally to money market funds but that may apply if a fund breaks the dollar or if a capital transaction is processed against restricted shares.

42 For further details on the operational challenges and impacts of redemption restrictions, see Federated Letter, supra note 2.

43 See e.g., Letter from DST Systems, Inc. to Elizabeth M. Murphy, Secretary, Securities and Exchange Commission (March 2, 2012), available at http://sec.gov/comments/4-619/4619-128.pdf. The letter focuses on U.S. money market funds and the “significant impacts potential redemption restrictions reform options will have on systems, operations, and shareholder behavior that could cripple if not destroy money market funds as a shareholder convenience.”

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 21

» Intermediaries: As noted above, a myriad of intermediary platforms, subaccounting, recordkeeping, and ancillary systems also would require extensive changes to implement redemption restrictions for money market fund shareholders. Thousands of intermediaries would need to make significant changes, similar to those made by funds, to systems that are tailored to their business models, which include both proprietary and ancillary systems that are supported by a wide range of vendors. As a result, the costs to intermediaries to implement money market fund redemption restrictions would be several times greater than the costs and efforts necessary to modify fund transfer agent and ancillary systems.

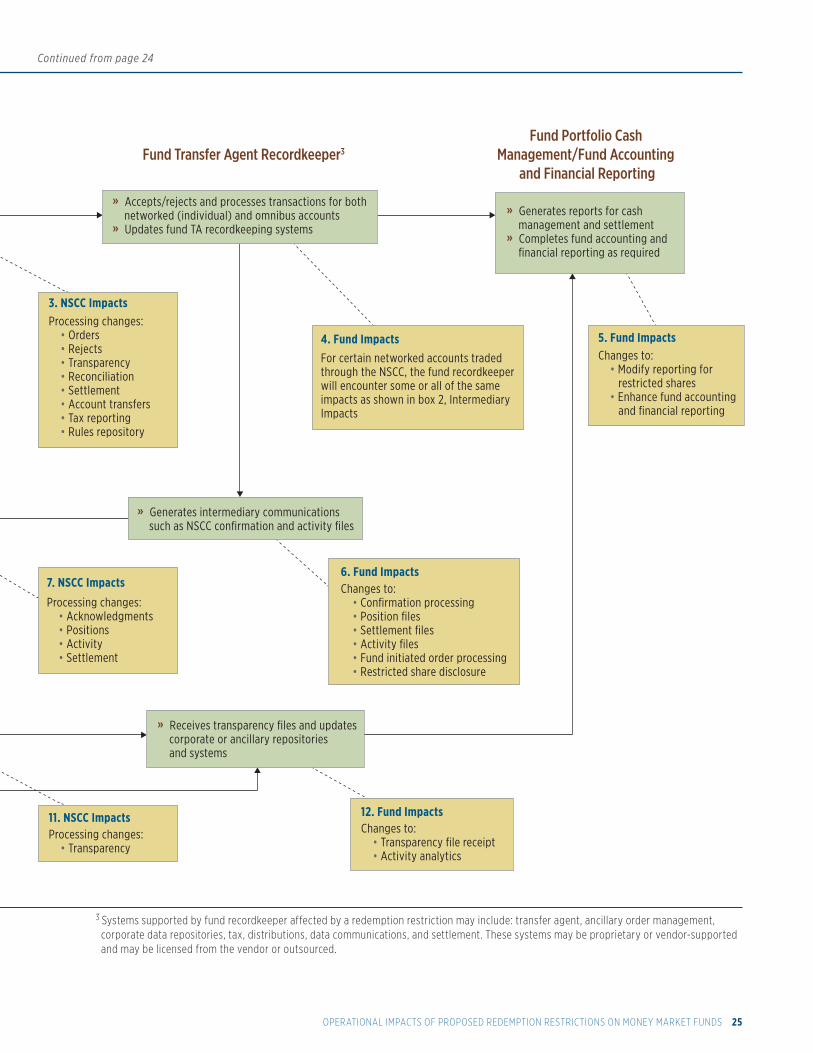

» NSCC: Redemption restriction changes would need to be implemented for transactions and activity processed through the NSCC. This will include programming and systems changes to NSCC standardized record layouts, as well as processes and procedures for both omnibus and networked accounts for transactions processed either same-day or next-day. In addition, new information regarding any restrictions applied will need to be shared with the fund. All of these changes will entail significant industry coordination, effort, and complexities for NSCC participants (funds, firms, and service providers), in addition to the conforming changes necessary for each of their own systems that interface with the NSCC.

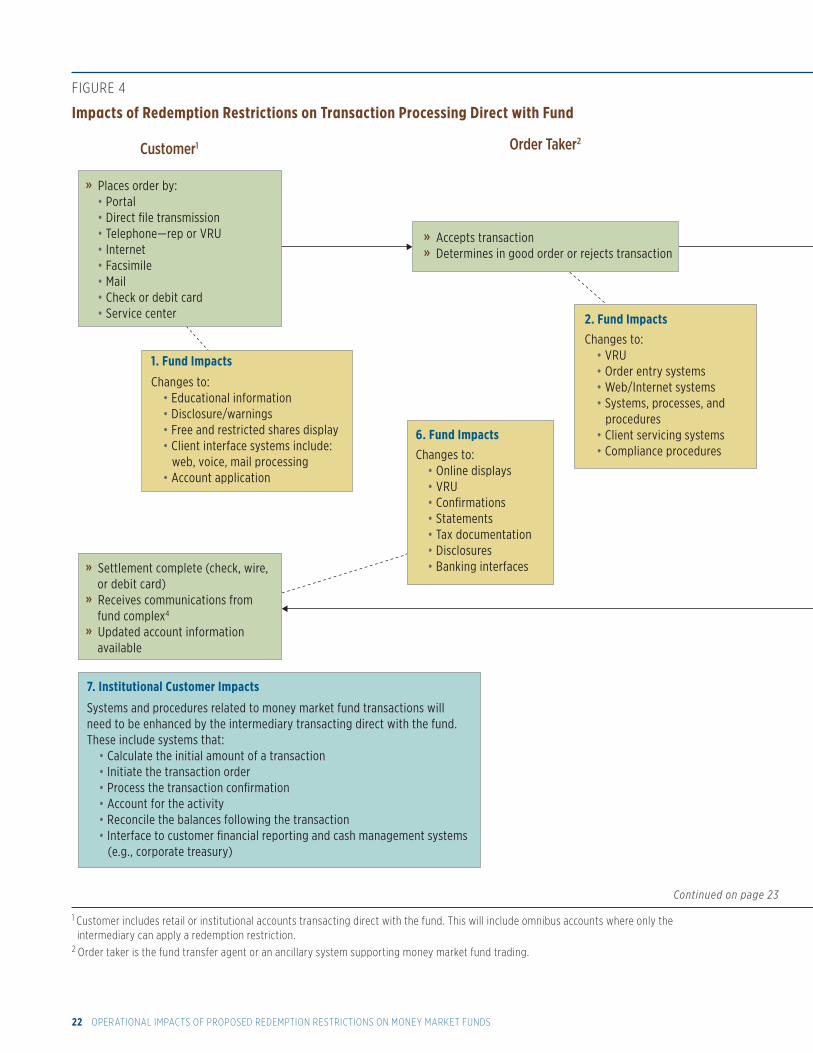

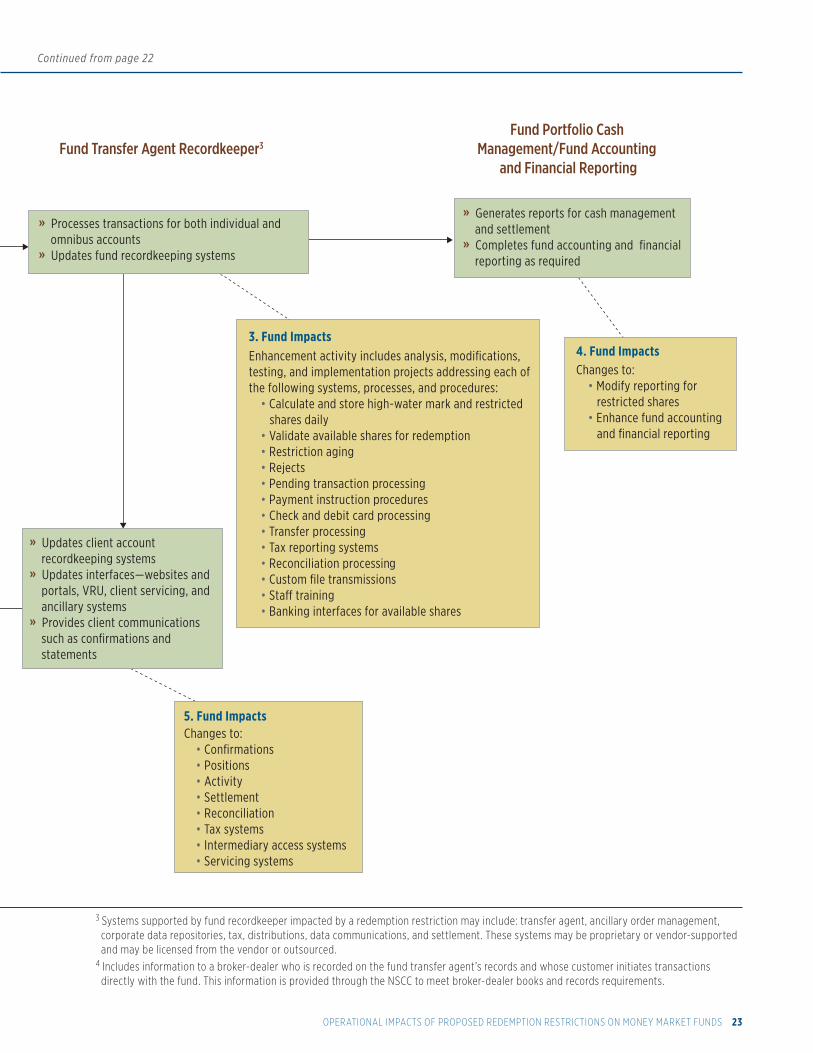

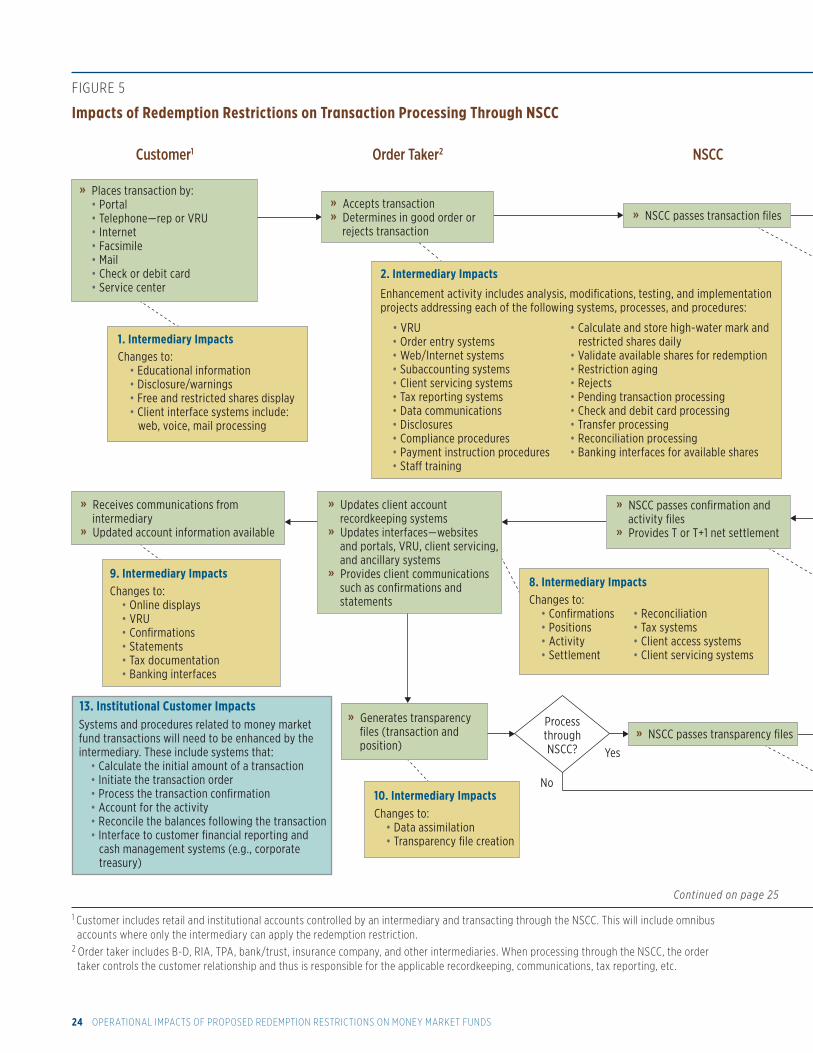

The operational impacts for funds and intermediaries to implement redemption restrictions are disaggregated and displayed in Figure 4 on pages 22 and 23 (for transaction processing direct with fund) and Figure 5 on pages 24 and 25 (for transaction processing through the NSCC). Both figures provide specific details on impacts identified throughout the transaction processing cycle for funds, intermediaries, and institutional customers. These changes will be extensive and costly to implement, and further changes may be required as dictated by final rules, if adopted.

22 OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds

fiGure 4

Impacts of Redemption Restrictions on Transaction Processing Direct with Fund

Customer1 Order Taker2Fund Transfer Agent Recordkeeper3

Fund Portfolio Cash Management/Fund Accounting

and Financial Reporting» Places order by: • Portal • Direct file transmission • Telephone—rep or VRU • Internet • Facsimile • Mail • Check or debit card • Service center

» Accepts transaction» Determines in good order or rejects transaction

Changes to: • Educational information • Disclosure/warnings • Free and restricted shares display • Client interface systems include: web, voice, mail processing • Account application

1. Fund Impacts

» Settlement complete (check, wire, or debit card)» Receives communications from fund complex4

» Updated account information available

7. Institutional Customer Impacts

Systems and procedures related to money market fund transactions will need to be enhanced by the intermediary transacting direct with the fund. These include systems that: • Calculate the initial amount of a transaction • Initiate the transaction order • Process the transaction confirmation • Account for the activity • Reconcile the balances following the transaction • Interface to customer financial reporting and cash management systems (e.g., corporate treasury)

Changes to: • Online displays • VRU • Confirmations • Statements • Tax documentation • Disclosures • Banking interfaces

Changes to: • VRU • Order entry systems • Web/Internet systems • Systems, processes, and procedures • Client servicing systems • Compliance procedures

2. Fund Impacts

» Processes transactions for both individual and omnibus accounts» Updates fund recordkeeping systems

» Updates client account recordkeeping systems» Updates interfaces—websites and portals, VRU, client servicing, and ancillary systems» Provides client communications such as confirmations and statements

3. Fund ImpactsEnhancement activity includes analysis, modifications,testing, and implementation projects addressing each of the following systems, processes, and procedures: • Calculate and store high-water mark and restricted shares daily • Validate available shares for redemption • Restriction aging • Rejects • Pending transaction processing • Payment instruction procedures • Check and debit card processing • Transfer processing • Tax reporting systems • Reconciliation processing • Custom file transmissions • Sta� training • Banking interfaces for available shares

Changes to: • Confirmations • Positions • Activity • Settlement • Reconciliation • Tax systems • Intermediary access systems • Servicing systems

5. Fund Impacts

» Generates reports for cash management and settlement» Completes fund accounting and financial reporting as required

Changes to: • Modify reporting for restricted shares • Enhance fund accounting and financial reporting

4. Fund Impacts

6. Fund Impacts

1 customer includes retail or institutional accounts transacting direct with the fund. this will include omnibus accounts where only the intermediary can apply a redemption restriction.

2 Order taker is the fund transfer agent or an ancillary system supporting money market fund trading.

Continued on page 23

OperatiOnal impacts Of prOpOsed redemptiOn restrictiOns On mOney market funds 23

Customer1 Order Taker2Fund Transfer Agent Recordkeeper3

Fund Portfolio Cash Management/Fund Accounting

and Financial Reporting» Places order by: • Portal • Direct file transmission • Telephone—rep or VRU • Internet • Facsimile • Mail • Check or debit card • Service center