operationalising the selection and application of macroprudential

TRANSCRIPT

Committee on the Global Financial System

CGFS Papers No 48

Operationalising the selection and application of macroprudential instruments Report submitted by a Working Group established by the Committee on the Global Financial System The Group was chaired by José Manuel González-Páramo, then European Central Bank

December 2012

JEL Classification numbers: E58, G01, G28

This publication is available on the BIS website (www.bis.org).

© Bank for International Settlements 2012. All rights reserved. Brief excerpts may be reproduced or translated provided the source is cited.

ISBN 92-9131-897-3 (print)

ISBN 92-9197-897-3 (online)

CGFS – Operationalising the selection and application of macroprudential instruments iii

Preface

Following the comprehensive stocktake of macroprudential policy developments conducted by the CGFS in 2010, in September 2011, the Committee established a Working Group, chaired by José-Manuel González-Páramo (then European Central Bank), to provide practical guidance for policymakers on how macroprudential instruments should be chosen, combined and applied.

To this end, the current report draws out three high-level criteria, which are key in determining instrument selection and application: (i) the ability to determine the appropriate timing for the activation or deactivation of the instrument; (ii) the effectiveness of the instrument in achieving the stated policy objective; and (iii) the efficiency of the instrument in terms of a cost-benefit assessment. In trying to operationalise these criteria, the report proposes a number of practical tools that can aid the choice and implementation of macroprudential instruments.

Following discussion and approval by the CGFS, the report was presented to central bank Governors at the Global Economy Meeting in November 2012, where it received endorsement for publication. We hope that the practical approaches described in this report will prove to be a relevant and timely input to the macroprudential policy frameworks that are currently being established in a large range of jurisdictions.

William C Dudley

Chairman, Committee on the Global Financial System President, Federal Reserve Bank of New York

CGFS – Operationalising the selection and application of macroprudential instruments v

Contents

Preface .................................................................................................................................... iii

Executive summary .................................................................................................................. 1

1. Introduction ...................................................................................................................... 3

2. Determining the appropriate timing for the activation or deactivation of MPIs ................ 5

2.1 Stylised scenarios for the activation and release of MPIs ...................................... 6

2.2 Indicators to guide MPIs: a three-step identification approach .............................. 8

2.3 Linking systemic risk assessment and MPI selection .......................................... 15

3. The transmission mechanism of MPIs .......................................................................... 17

3.1 Tightening capital-based MPIs ............................................................................. 18

3.2 Tightening liquidity-based tools ............................................................................ 24

3.3 Tightening asset-side MPIs .................................................................................. 27

3.4 Managing the release phase ................................................................................ 30

3.5 Interactions ........................................................................................................... 32

4. Macroprudential policy in practice: questions and answers .......................................... 35

Annex 1: Broad principles for the design and operation of macroprudential policy ............. 40

Annex 2: Instrument and signal threshold selection: a conceptual framework .................... 43

Annex 3: Indicators supporting the application of MPIs ....................................................... 45

Annex 4: The empirical strength of transmission channels ................................................. 51

Annex 5: How to operationalise sectoral capital requirements? .......................................... 58

Annex 6: The interaction of macroprudential instruments with other policies ...................... 60

References ............................................................................................................................. 63

Members of the Working Group .............................................................................................. 69

CGFS – Operationalising the selection and application of macroprudential instruments 1

Executive summary

As a response to the recent global crisis, new or strengthened mandates for macroprudential policies have been established in a range of jurisdictions. This report aims to help policymakers in operationalising macroprudential policies, building on earlier work by the Committee, particularly on the comprehensive stocktake of macroprudential instruments (MPIs) (CGFS (2010a)) and the seven broad principles for the design and operation of macroprudential policies formulated by the CGFS in 2011.

Specifically, this report provides guidance on how to assess three high-level criteria that are key in determining the selection and application of macroprudential instruments from a practical perspective: (i) the ability to determine the appropriate timing for the activation or deactivation of the instrument; (ii) the effectiveness of the instrument in achieving the stated policy objective; and (iii) the efficiency of the instrument in terms of a cost-benefit assessment.

In trying to operationalise these criteria, this report proposes a number of practical tools. First, to help policymakers determine the appropriate timing for the activation and deactivation of their policy tools, the report lays out stylised scenarios in which macroprudential instrument settings may be tightened or released. The identification of these states is facilitated by two alternative approaches that seek to link systemic risk analysis and instrument selection. Second, to support the evaluation of the effectiveness and efficiency of macroprudential tools for a range of macroprudential instruments, the report proposes “transmission maps” – stylised presentations of how changes in individual instruments are expected to contribute to the objectives of macroprudential policy.

Against this backdrop, this report concludes with a set of nine practical questions that can be helpful in guiding the selection and application of macroprudential instruments. These, and their respective answers, are set out and elaborated in detail in Section 4 of this report. In brief, they are as follows:

To what extent are vulnerabilities building up or crystallising?

How (un)certain is the risk assessment?

Is there a robust link between changes in the instrument and the stated policy objective?

How are expectations affected?

What is the scope for leakages and arbitrage?

How quickly and easily can an instrument be implemented?

What are the costs of applying a macroprudential instrument?

How uncertain are the effects of the policy instrument?

What is the optimal mix of tools to address a given vulnerability?

CGFS – Operationalising the selection and application of macroprudential instruments 3

1. Introduction

The recent financial crisis has accelerated efforts to develop macroprudential policy frameworks. As a result, new or strengthened mandates for macroprudential policies have been established in a growing range of jurisdictions. The broad goal of these policies is to limit the risk of financial system disruptions that can destabilise the macroeconomy (see Box 1). Such systemic risk arises from externalities (such as joint failures and procyclicality) that are not easily internalised by financial market participants themselves. Thus, by explicitly taking a system-wide perspective, macroprudential policies complement other policies, such as macroeconomic and prudential ones, which can also impact on financial stability conditions.

Despite progress over recent years, the development and implementation of macroprudential policies are still at an early stage. In the area of systemic risk monitoring, efforts have focused on closing data gaps and on developing better indicators and models to assess systemic risk. With respect to macroprudential tools, new instruments have been developed – for example, international agreement was reached on the introduction of countercyclical capital buffers and additional loss absorbency for global systemically important banks – and experience with the use of existing ones has been shared among policymakers. On the governance front, a number of jurisdictions have been adjusting institutional arrangements to support macroprudential policy, based on analyses identifying desirable characteristics of such governance frameworks. This includes work on the two appropriate objectives for macroprudential policies – increasing the resilience of the financial system and leaning against the financial cycle – and on principles for their design and operation (see CGFS (2010a) and FSB-BIS-IMF (2011); Annex 1 provides seven broad principles for the design and operation of macroprudential policy, as originally formulated by the CGFS in 2011). In contrast, practical issues of policy implementation have so far received less attention.

One such practical challenge is how to select and apply macroprudential policy instruments (MPIs). To help answer this question, this report provides guidance on how to assess three high-level criteria for determining MPI selection and application:1

(i) the ability to determine the appropriate timing for the activation or deactivation of the instrument;

(ii) the effectiveness of the MPI in achieving the macroprudential policy objective of limiting systemic risk; and

(iii) the efficiency of the instrument in terms of a cost-benefit assessment. 2

In trying to operationalise these criteria, the report proposes a number of practical tools that can aid the assessment of individual MPIs. Specifically:

(a) To help policymakers determine the appropriate timing for the activation and deactivation of MPIs, the report lays out stylised scenarios in which MPI settings may be tightened or released. The identification of these states is facilitated by two alternative approaches that seek to link systemic risk analysis and MPI selection.

1 The logic and interaction of these criteria are illustrated in a simple theoretical framework, as described in

Annex 2, that conceptualises MPI choice for a given policy objective. 2 For the purposes of this report, the effectiveness of MPIs refers to their capacity to fulfil the objective of limiting

systemic risk by enhancing resilience or leaning against the credit cycle. Efficiency, in turn, reflects their ability to achieve this objective at the lowest cost in terms of negative repercussions for other policy areas or the economy as a whole.

4 CGFS – Operationalising the selection and application of macroprudential instruments

(b) To support the evaluation of the effectiveness and efficiency of MPIs, “transmission maps” are being proposed as a practical tool for the evaluation of macroprudential instruments. These maps provide a stylised representation of how changes in individual MPIs are expected to contribute to the objectives of macroprudential policy as well as how they may interact with the objectives pursued in other policy areas.

In general, macroprudential instruments can be defined as primarily prudential tools that are calibrated and explicitly assigned to target one or more sources of systemic risk (see Box 1). While this gives rise to a large number of potential instruments, the focus of this report is on a small range of MPIs whose calibration can be varied over the cycle.3 Specifically, the

Box 1

Macroprudential policy frameworks: a short review

The basic features of macroprudential policy frameworks have been laid out in previous CGFS work, such as CGFS (2010a), as well as in reports published by other institutions, including FSB-BIS-IMF (2011). As discussed in more detail there, the main goal of macroprudential policies is to reduce systemic risk, defined as the risk of widespread disruptions to the provision of financial services that have serious negative consequences for the real economy. As such, macroprudential policy focuses on the interactions between financial institutions, markets, infrastructure and the wider economy. It complements the microprudential focus on risk positions of individual institutions, which largely takes the rest of the financial system and the economy as given.

In articulating the practical objectives of macroprudential policy, two aims can be distinguished (CGFS (2010a)). The first is to strengthen the resilience of the financial system to economic downturns and other adverse aggregate shocks. The second is to actively limit the build-up of financial risks. Such leaning against the financial cycle seeks to reduce the probability or magnitude of a financial bust. These aims are not mutually exclusive, and they both go beyond the purpose of microprudential policy with its focus on insuring that individual firms have sufficient capital and liquidity to absorb shocks. Macroprudential policy takes risk factors into account that extend further than the circumstances of individual firms. These include shock correlations and the interactions that arise when individual firms respond to shocks. Such factors determine the likelihood and consequences of the systemically important shocks that macroprudential policy seeks to mitigate.

To achieve these macroprudential aims, CGFS (2010a) and IMF (2011a) review a broad range of existing and proposed instruments. In general, macroprudential instruments can be defined as primarily prudential tools that are calibrated to target one or more sources of systemic risk, such as excessive leverage, excessive liquidity mismatches, too much reliance on short-term funding or interconnectedness.

_____________________ Between these two macroprudential aims, leaning against the financial cycle is the somewhat more

ambitious target. Accountability measures appear to be more straightforward to construct for an objective of strengthening the resilience of the financial system, given the long experience gained with (micro-)prudential interventions aimed at maintaining the resilience of individual institutions. By contrast, the concept of the financial cycle and its sensitivity to macroprudential interventions remain less well understood – a fact that supports a careful approach until more practical experience has been gained (CGFS (2010a)). In addition, some non-prudential tools, such as infrastructure policies, can also from part of the overall macroprudential toolkit. Yet, these tools would need to clearly target systemic risk to be considered macroprudential (FSB-BIS-IMF (2011)).

3 Based on an informal survey, the tools discussed in this report were identified by the majority of members as

promising or practical MPIs in their jurisdiction. Future work could provide guidance on how to operationalise other important macroprudential tools, in particular those addressing the cross-sectional dimension.

CGFS – Operationalising the selection and application of macroprudential instruments 5

analysis is limited to providing as much detailed guidance as possible on capital-based tools (eg countercyclical capital buffers, sectoral capital requirements and dynamic provisions), liquidity-based tools (eg countercyclical liquidity requirements) and asset-side tools (loan-to- value (LTV) and debt-to-income (DTI) ratio caps). However, many of the findings presented here also apply to other instruments.

The remainder of the report is organised as follows. Section 2 provides guidance on how to determine the appropriate timing for the application of MPIs. Section 3 explores the transmission mechanism of capital-based, liquidity-based and asset-side MPIs. Where possible, the analysis is supplemented with empirical evidence to provide some indications of the effectiveness and efficiency of different MPIs. The last section concludes with a set of nine practical questions and answers that can be helpful in guiding the selection and application of macroprudential tools.

2. Determining the appropriate timing for the activation or deactivation of MPIs

The ability to identify and measure systemic risks and vulnerabilities is a key factor for successfully implementing MPIs, because imprecise timing of MPI application can result in overshooting or undershooting of macroprudential objectives.4 Costs of a mistimed activation are asymmetric, as delayed action is generally more costly than a premature intervention. During the build-up phase of any vulnerability, delayed activation may imply that MPIs are less effective or even ineffective as there is insufficient time for them to gain traction. Alternatively, it may even initiate the disorderly unwinding of imbalances that have been built-up. In both cases, crises may materialise. Implementing MPIs too early, in contrast, is likely to incur unnecessary regulatory costs and may weaken the impact of the chosen instrument, as market participants will have more time to develop strategies to avoid and arbitrage them. During the release phase, on the other hand, deactivating MPIs too early may give market participants a wrong signal, whilst releasing them too late may amplify procyclical effects, as banks may have to deleverage more to satisfy additional macroprudential buffers.

In stylised terms, two approaches linking systemic risk assessments and MPI activation can be distinguished: (i) a top-down systemic risk approach; and (ii) a bottom-up tools-based approach. While the two approaches are generally mixed in practice, it is conceptually useful to look at them separately.

Top-down approach

Under the top-down approach, policy decisions are guided by a general, comprehensive, system-wide risk assessment. Decisions are taken in light of an accepted model which properly captures the links between systemic risk, market dynamics and macroprudential policy choices. Potential policy actions, by means of one or more instruments, are guided by the signals received from a combination of indicators and forecasting models. In an ideal world, such a top-down approach would allow for an assessment of the impact that particular macroprudential policy actions would have, including their effectiveness in reducing systemic

4 The experience of imposing quantitative limits on real estate lending by Japan in the early 1990s provides an

illuminating example of how important the appropriate timing is. In this case, a quantitative ceiling on banks’ real estate loans was introduced in March 1990, right before land prices peaked in early 1991. This measure came too late to achieve the goal of preventing excessive increases in land prices and ended up accelerating the decline in land prices. This example also shows how important it is to avoid regulatory arbitrage. The ceiling on the extension of real estate loans by banks encouraged the expansion of brokered loans placed through non-banks, parts of Japan’s shadow banking system. As a result, the original goal was not achieved in Japan.

6 CGFS – Operationalising the selection and application of macroprudential instruments

risk as well as their associated costs, possible side effects, and interactions with other policy objectives. This approach should, in principle, allow for the selection and use of the most effective instrument(s).

The main downside of the top-down approach is that a generally accepted theoretical and empirical framework for using macroprudential instruments is not yet available. And given the multifaceted nature of systemic risk, it is unclear whether this can be really achieved, even though progress has been made in developing key elements of such a framework.5

Bottom-up approach

The bottom up, instrument-based approach starts with a set of instruments and assesses the vulnerabilities they can address and the types of indicators that should be used to trigger their implementation and release. A key advantage of this approach is that it is more tractable than the systemic top-down approach in at least three respects. First, it allows for a direct and in-depth understanding of the basic features of each instrument without requiring the ex ante development of a general analytical framework. Second, it is less prone to model risk. Third, and depending on country characteristics, it is possible to build on the experience gained by other countries in using particular MPIs.

These advantages in implementing bottom-up approaches come with a number of potential downsides. Most importantly, potential spillovers, second-round effects and general-equilibrium effects of the respective policy measures are hardly, if at all, captured, even though they can dominate first-round effects. As such, particular vulnerabilities may be missed if they fall outside the range of instruments considered. The instrument-based approach may also neglect to take account of interactions with other policy objectives as well as interaction between MPIs, which are important to assess, as some vulnerabilities may be best addressed with a mix of instruments.

In the absence of a fully fledged top-down approach, it is useful as a first step to clarify in which high-level situations MPIs should be activated or released. In a second step, it is helpful to identify indicators that can provide real-time information about the scenario policymakers face. In the last step, policymakers have to bring this information together to determine the appropriate policy action. The contours of such an approach are outlined below.

2.1 Stylised scenarios for the activation and release of MPIs

As a starting point to judge the appropriate timing for the activation and release of MPIs, Table 2.1 sets out six scenarios which are deliberately stylised to focus on a limited number of key characteristics. In particular, they abstract from cross-border problems and the possibility that different vulnerabilities may emerge at different times. Both these questions are addressed below, once the scenarios have been covered in more detail.

Independently of whether the macroprudential objective is to increase resilience or to lean against the financial cycle (which is rather ambitious; see Box 1), macroprudential policies are designed to respond to or target developments in the financial cycle. Thus, the stage of the financial cycle is the main determinant in guiding the activation and release of MPIs. Yet, as financial cycles are considerably longer and more pronounced than standard business cycles,6 other macroeconomic conditions need not move in sync with the financial cycle, and it is important for macroprudential policymakers to take this cyclical backdrop into account.

5 For recent theoretical contributions see eg Adrian and Boyarchenko (2012), He and Krishnamurthy (2012) or

Goodhart et al (2012a). 6 See eg Aikman et al (2010), Claessens (2011) or Schularick and Taylor (2012).

CGFS – Operationalising the selection and application of macroprudential instruments 7

Table 2.1

High-level scenarios for the activation and release of MPIs1

Financial cycle

Boom Bust

With crisis Without crisis

Other macroeconomic

conditions

Strong Tighten

(Scenario 1)

Leave unchanged or release (Scenario 4)

Weak Leave unchanged

or tighten (Scenario 2)

Release2 (Scenario 3)

Release (Scenario 5)

1 Macroprudential policies are designed to respond to or target the financial cycle, taking other macroeconomic conditions as a cyclical backdrop. 2 To resolve some crises, it may be necessary to increase the overall level of capital and liquidity in the system to restore market confidence. As discussed in detail in Section 3.4, the effectiveness of releasing MPIs in such situations depends critically on several factors, such as the appropriate timing and the impact on market expectations.

The suggested policy action that is likely to be the least controversial applies when the financial cycle is booming and the real economy is strong (Scenario 1). In this case, provided that the build-up of a particular vulnerability can be reliably identified (see below), tightening MPIs seems self-evident to achieve both macroprudential objectives. The years in the run-up to the global crisis in many economies are the prime example in this regard.

The optimal course of policy may be less apparent when the financial cycle is booming, whilst the real economy is weak, potentially leading to higher loss rates on loans and similar instruments (Scenario 2). However, the release of MPIs may not be justified as long as a systemic risk event fails to materialise. Policymakers may thus want to leave MPI settings unchanged or even tighten them as long as the financial cycle continues to expand rapidly. An example of such a situation could be the shallow recession in some countries in the early 2000s, which coincided with rapid credit expansion and house price increases.

For the release phase, it is important to differentiate whether the downswing of the financial cycle coincides with a financial crisis or not. In a crisis context, MPIs may need to be released to avoid excessive deleveraging (Scenario 3). However, to resolve some crises, it may be necessary to increase the overall level of capital and liquidity in the system to restore market confidence – as was, for example, the case after the Supervisory Capital Assessment Program (SCAP) in the United States in 2009. As discussed in detail in Section 3.4, the effectiveness of releasing MPIs in such situations depends critically on several factors, such as the appropriate timing and the impact on market expectations.

At the same time, downswings in the financial cycle do not necessarily lead to crises. One example for this kind of scenario may be Germany in the early 2000s, which then experienced severe stress in parts of the banking sector. While output growth was very weak, no outright failures in the banking system occurred. In such a situation (Scenario 5), releasing previously tightened MPIs may be warranted to soften the impact of the downturn and avoid the asset disposals and bank deleveraging that might otherwise be necessary if MPI settings were to be held fixed.

Arguably, providing guidance for macroprudential policymakers is most difficult when the real economy is booming but the financial cycle has turned or is about to do so (Scenario 4). This happened, for example, in 2007, when money markets started to freeze, yet the real economy continued to expand for more than a year in a large number of economies and it was not yet obvious that a systemic crisis was about to crystallise. On the one hand, a release in this

8 CGFS – Operationalising the selection and application of macroprudential instruments

situation may have helped to absorb part of the impact of the turning financial cycle, thereby reducing the severity of the crisis. On the other hand, it may have also sent the wrong signal to markets, delaying the appropriate responses by banks and other market participants. The balance of these risks will be highly situation-dependent, so that no clear indication can be given ex ante whether it is optimal to release MPIs or keep them unchanged.

In a more benign situation, the economy could expand whilst the financial cycle is in a downswing, as systemic risk subsides smoothly. This would be the ideal outcome, if macroprudential policies are successful in leaning against the cycle. In this case, a gradual release seems appropriate.

A complicating factor in thinking through the scenarios laid out above is international interlinkages. Whereas Table 2.1 takes a domestic perspective, internationally active banks and other financial institutions are exposed to a range of financial and real cycles, which are not necessarily synchronised. The same applies to most asset markets, which are inherently global. This suggests that, in many cases, macroprudential requirements applied to a bank’s globally consolidated balance sheet cannot be determined by developments in one country alone. Rather, they would need to reflect changes in systemic risk and the macroprudential policy stance in the countries where the ultimate exposures reside. This may require international coordination – for example, through reciprocal arrangements applying to cross-border loans.7

Table 2.1 also abstracts from the possibility that different financial vulnerabilities may emerge at different times. While this does not affect the broad guidance for the build-up and release, different indicators are potentially useful for guiding different instruments, as discussed in more detail in the following.

2.2 Indicators to guide MPIs: a three-step identification approach

Judging the state of the economy to determine the appropriate policy action is not as clear-cut in practice as the discussion of Table 2.1 suggests. Given the lack of a fully fledged top-down approach, macroprudential indicators will play a crucial role in helping policymakers to identify the scenario they are faced with. This, in turn, raises the issue of how these indicators should be selected. As monitoring frameworks for the real economy are well established, the discussion here focuses entirely on the financial cycle. The link between risk assessment and MPI application is discussed in greater detail in Section 2.3.

The complexities of real-world policymaking suggest that, to be useful for policy implementation, macroprudential indicators would ideally be available in real time, while being robust, so that signals are noise-free and comparable across time. Robustness also requires that indicators are difficult to manipulate by individual institutions or market participants. Practical challenges in establishing robust indicators, which are compounded by data availability issues, are discussed in more detail in Annex 3.

Table 2.2 highlights a set of potential indicators that are useful in measuring the broad state of the financial cycle. Many of these indicators, such as credit developments or banking sector indicators, are slow-moving.8 As a result, they have been found to be more suitable in

7 This is, for instance, the case for the countercyclical capital buffer under Basel III, where banks’ total

countercyclical capital buffers are a weighted average of capital buffer requirements determined by policymakers in the various jurisdictions that the bank is exposed to (see Basel Committee (2010b)).

8 A downside of these types of indicators is that they are generally not available in real time and are only updated infrequently. This contrasts with market-based indicators or systemic risk measures based on market

CGFS – Operationalising the selection and application of macroprudential instruments 9

Table 2.2

Capturing the financial cycle: some useful indicators

Macroeconomic indicators Broad credit aggregates

Measures of debt sustainability (debt to income, debt service ratio)

Banking sector indicators Stress tests, bank risk metrics

Leverage ratios

Maturity and currency mismatch

Indicators of funding vulnerabilities

Profits and losses

Market-based indicators Asset valuations in equity and property markets

Corporate bond and CDS spreads and risk premia

Margins and haircuts

Lending spreads

Qualitative information Underwriting standards

Asset quality

Credit conditions

guiding the activation of MPIs (eg the build-up of buffers). For the same reason, they will be less useful in guiding the rapid release of policy instruments during crises, even though they may still be helpful in steering a more gradual release (ie, in cases when the financial cycle is in a downswing but no crisis emerges).

Indicator identification: three steps

A key challenge in the operationalisation of macroprudential policy is to narrow down the broad list of candidate indicators depicted in Table 2.2, and to assess how they relate to particular vulnerabilities, to then assign them to individual (classes of) MPIs. A three-step approach is being proposed for this purpose:

As a first step, Table 2.3 identifies potential indicators that could guide the build-up of the instruments discussed in this report. Indicator selection is being guided by three broad criteria: (i) relevance for the MPI, (ii) ease of data availability and (iii) simplicity (ie the ability to easily communicate and replicate).

Step 2 requires a more rigorous assessment of the empirical robustness of candidate indicators to guide the build-up or activation of specific MPIs. To provide a benchmark, it is useful for such an assessment to start with a cross-country analysis, which is then brought to the country level to account for potential country-specific factors. With the exception of countercyclical capital buffers and dynamic provisions, little empirical work has been done in this area. While a complete empirical assessment of the usefulness of each variable in Table 2.3 goes beyond the focus of this report, Section 2.2.1 below details the practical steps

data such as Acharya et al (2012), Adrian and Brunnermeier (2008) or Huang et al (2011). Yet, some of these indicators can be relatively noisy. Future work would therefore be useful to assess the robustness of market indicators as empirical guides for the calibration of macroprudential measures and the safeguards which need to be deployed while using them.

10 CGFS – Operationalising the selection and application of macroprudential instruments

Table 2.3

Policy instruments and potential indicators

Policy instrument Potential indicators

Capital-based instruments

Countercyclical capital buffers1 Measures of the aggregate credit cycle

Dynamic provisions1 Bank-specific credit growth and specific provisions (current and historical average)

Sectoral capital requirements Measures of the price and quantity of different credit aggregates (stock and new loans) on a sectoral basis: interbank credit, OFIs, non-financial corporate sector and households

Measures of sectoral concentrations

Distribution of borrowing within and across sectors

Real estate prices (commercial and residential, old and newly developed properties)

Price-to-rent ratios

Liquidity-based instruments

Countercyclical liquidity requirements

LCR and NSFR

Liquid assets to total assets or short-term liabilities

Loans and other long-term assets to long-term funding

Loan-to-deposit ratios

Libor-OIS spreads

Lending spreads

Margins and haircuts in markets Margins and haircuts

Bid-ask spreads

Liquidity premia

Shadow banking leverage and valuation

Market depth measures

Asset-side instruments

LTVs and DTIs Real estate prices (commercial and residential, old and newly developed properties)

Price-to-rent ratios

Mortgage credit growth

Underwriting standards

Indicators related to household vulnerabilities

Indicators of cash-out refinancing

1 To steer the application of countercyclical capital buffers and dynamic provisions, a range of indicators is useful. However, the table only shows the indicators which have been officially proposed or implemented (for countercyclical capital buffers, see Basel Committee (2010b); for dynamic provisions, see Saurina (2009)).

CGFS – Operationalising the selection and application of macroprudential instruments 11

necessary, based on a selection of indicator variables that can help gauge the potential build-up of vulnerabilities in the household sector.

Step 3 concerns the release phase. The scenarios discussed above highlight that, for the release of MPIs, policymakers have to assess whether there is a downswing in the financial cycle and whether there is a crisis or not. If not (Scenarios 4 and 5 in Table 2.1), a more gradual release may be warranted. In this case, indicators that are useful in steering MPI activation, such as the ones shown in Table 2.3, can be used to guide the release as well, because a return to more normal levels would signal that systemic risks have subsided.When crises emerge, they tend to erupt quickly (Scenario 3 in Table 2.1). In this case, many of the more slow-moving indicators highlighted above cannot be relied upon to inform the need to relax MPI settings. This suggests that market-based indicators, which are available at high frequencies, have an important role to play.9 In addition, a more detailed analysis of banks’ balance sheets, building on supervisory information, may be warranted to judge whether system-wide stress is about to materialise. Some indicators for this purpose are shown in Table 2.4. However, there is little empirical evidence capturing the performance of these indicators for crises except the most recent one. In this case, market-based indicators turned out to provide good signals of the onset of the crisis, even though they also issued warning signals for non-crisis countries like Canada, indicating that their reliability needs further evaluation.10

Table 2.4

Potential indicators to signal systemic crises

Market-based indicators Liquidity conditions in money markets

Credit and CDS spreads

Market risk premia and systemic risk measures

Margins and haircuts

Banking sector indicators Stress tests, risk metrics

Profitability

Losses

Lending standards

2.2.1 Evaluating macroprudential indicators: systemic risk in the household sector

This section illustrates the selection of robust indicators for the build-up phase of financial imbalances, based on the example of risks in the household sector. As such, the proposed process would form part of the implementation of MPIs that target this specific vulnerability, such as LTV or DTI caps, sectoral capital requirements and buffers related to household risk.

To provide a benchmark, the analysis starts with a cross-country analysis, which is then brought to the country level to illustrate how country-specific differences can potentially be accounted for.11

9 See also IMF (2011b). 10 For a statistical assessment of the performance of indicators for the release of MPIs, see Drehmann et al (2011). 11 While it is important to take account of country-specific characteristics, there is a risk of overemphasising such

factors, which could bias policymakers in the direction of “this country (or time) is different”. Across time and

12 CGFS – Operationalising the selection and application of macroprudential instruments

Cross-country analysis

Two broad categories of indicators are analysed, which together should provide useful and complementary information about the build-up of systemic risks in the household sector: variables related to credit developments and variables measuring developments in the residential housing market. Table 2.5 lists the specific indicators, which are a refinement of the class of indicators listed in Table 2.3 above.12

In general, a good indicator for the build-up or activation of MPIs is characterised by a systematic pattern prior to the onset of crisis episodes – such as high and increasing levels for instance – thus providing a persistent signal if imbalances are building up, and no false warnings during normal times. In addition, an ideal indicator would also provide the appropriate signals for the release, either rapidly in the case of crises or more gradually if imbalances unwind smoothly. It is unlikely in practice, though, that a single indicator can provide reliable signals with such different characteristics.

All indicators listed in Table 2.5 provide useful signals about the build-up of vulnerabilities ahead of crises. However, as expected, they are not well suited to guide releases once crises materialise. This can be seen from Graph 2.1, which presents average developments for each indicator variable around systemic crises.13 All indicators rise prior to a crisis, but some, such as the credit-to-GDP gap, continue to rise for some quarters even after the onset

Table 2.5

Potential indicators to measure risks in the household sector

Credit variables

Credit-to-GDP gap: deviation from a long-term trend (Basel III reference indicator)

Household credit-to-GDP: deviation from a long-term trend1

Annual growth rate in real household credit: deviation from a 15-year rolling average

Aggregate debt service ratio: deviation from a 15-year rolling average

Residential property market indicators

Annual growth rate in real residential property prices: deviation from a 15-year rolling average

Residential property prices over rents: deviation from a long-term trend1

1 Long-term trends are calculated as for the credit-to-GDP gap under Basel III (Basel Committee (2010b)).

countries and in different stages of development, certain indicators (eg excessive leverage and exuberant asset prices) have been shown to be a persistent feature ahead of financial crises (see eg Reinhart and Rogoff (2009) or Schularick and Taylor (2012)). A conservative approach for macroprudential policies could take these regularities into account by following the international benchmark unless country-specific factors suggest a more proactive policy stance.

12 Many of the indicators listed in Table 2.3 have trends, which have to be removed to achieve comparability across time and countries. For the purposes of this report, this is done by using either statistical filters or long- run averages (see also discussion on detrending in Annex 3).

13 Depending on data availability, at most 19 different crisis episodes in 11 countries are considered. Crisis dates are based on the IMF database (Laeven and Valencia (2012)) and conversations with central banks.

CGFS – Operationalising the selection and application of macroprudential instruments 13

Graph 2.1

Developments of indicators around crises

In percentage points

Credit-to-GDP gap HH credit-to-GDP gap HH credit growth

Debt service ratio Residential property price growth Price-to-rent gap

of the crisis, suggesting that they are not well suited to signal the appropriate release time. In contrast, valuation-based indicators, such as the price-to-rent gap or the residential property price gap, tend to peak four to eight quarters prior to the crisis. The debt service ratio is closest to being a contemporaneous indicator.14 The width of the 25–75 percentile bands indicates that some indicators provide very tight signals in the run-up to crises, while others are noisier.

On this basis and a statistical analysis (see Annex 3), the credit-to-GDP gap, the debt service ratio, the growth in residential property prices and their gap turn out to have been useful indicators in signalling past crises. Variables involving household credit, in turn, appear less reliable.

14 The construction of aggregate debt service ratios and their early warning properties for systemic crises are

analysed by Drehmann and Juselius (2012).

–10

0

10

20

30

–16 –12 –8 –4 0 4 8 12 16

Mean25th and 75th percentiles

–10

–5

0

5

10

–16 –12 –8 –4 0 4 8 12 16–10

–5

0

5

10

–16 –12 –8 –4 0 4 8 12 16

–3

0

3

6

9

–16 –12 –8 –4 0 4 8 12 16–16

–8

0

8

16

–16 –12 –8 –4 0 4 8 12 16–40

–20

0

20

40

–16 –12 –8 –4 0 4 8 12 16

The horizontal axis depicts plus/minus 16 quarters around a crisis, which is indicated by the vertical line. Zero on the vertical axiscorresponds roughly to the average in non-crisis periods. The historical dispersion of the relevant variable is taken at the specificquarter across crisis episodes. Depending on data availability, at most 19 different crisis episodes in 11 countries are considered. Fora definition of variables, see Table 2.5.

Sources: National data; BIS calculations.

14 CGFS – Operationalising the selection and application of macroprudential instruments

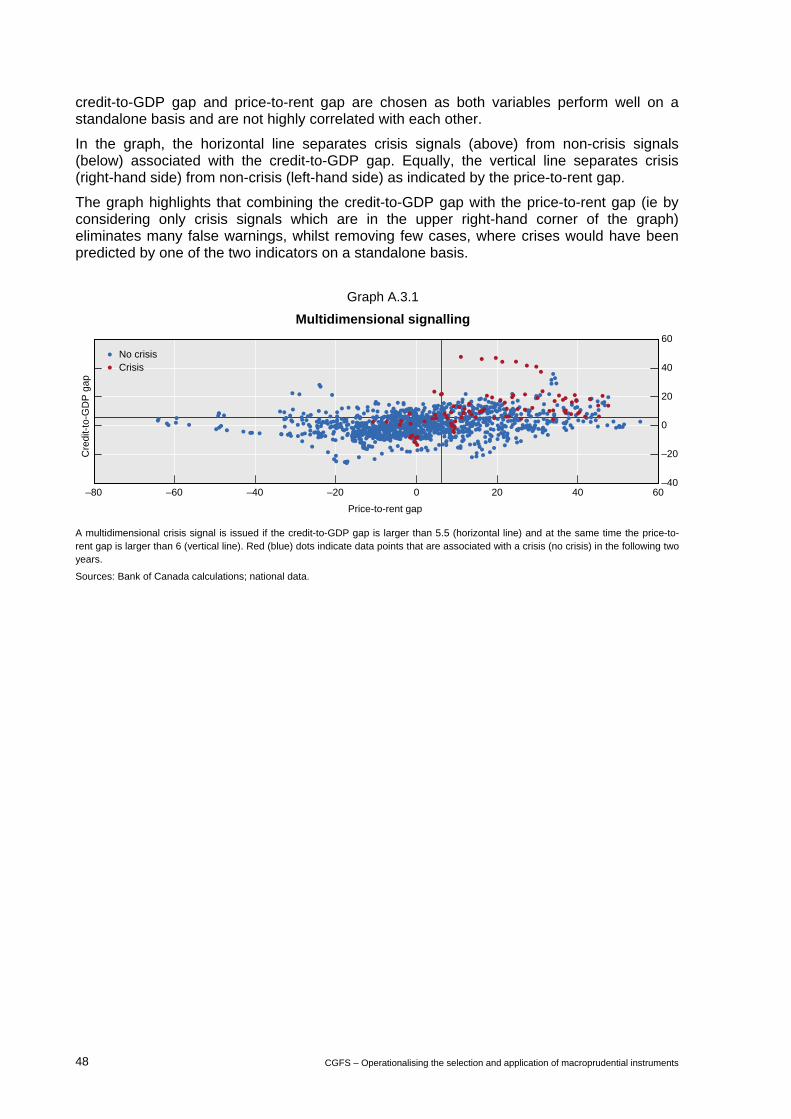

Country-level analysis

The next step in the selection of indicators is to break down cross-country evidence to the country-level. This step is illustrated below for the case of two candidate indicators: the credit-to-GDP gap and the price-to-rent gap. Both of these have been identified during the first stage of the analysis as providing useful signals in the build-up phase of the cycle. In addition, they are not highly correlated with each other. This suggests that their information could be considered complementary and should be combined using either judgment or statistical techniques (see Annex 3 for a description of how this could be done).

To highlight potential issues for country-level analysis, Graph 2.2 depicts the evolution of the two indicators around crisis periods for four countries (see Annex 3 for the remaining countries where both indicators were available). The vertical black lines denote financial crises and the vertical orange lines indicate other periods of interest, as discussed below. The red horizontal lines highlight the critical threshold, determined by statistical tests for the price-to-rent gap, while the green horizontal lines are the critical thresholds suggested under Basel III for the credit-to-GDP gap.

Graph 2.2

Price-to-rent and credit-to-GDP gaps for selected countries1

In percentage points

Price-rent gap2

Australia Switzerland Sweden United Kingdom

Credit-to-GDP gap3

Australia Switzerland Sweden United Kingdom

–40

–20

0

20

40

60

85 90 95 00 05 10–40

–20

0

20

40

60

85 90 95 00 05 10–40

–20

0

20

40

60

85 90 95 00 05 10–40

–20

0

20

40

60

85 90 95 00 05 10

–30

–20

–10

0

10

20

30

40

85 90 95 00 05 10–30

–20

–10

0

10

20

30

40

85 90 95 00 05 10–30

–20

–10

0

10

20

30

40

85 90 95 00 05 10–30

–20

–10

0

10

20

30

40

85 90 95 00 05 10

1 The black vertical lines indicate the beginning of systemic banking crises. The orange vertical lines indicate stress periods that did not result in crises. 2 The red horizontal line is the critical threshold (24 pps), determined by the statistical tests described inAnnex 3. 3 The credit-to-GDP gaps are based on bank credit to the private non-financial sector, using the same definitions as the countercyclical capital buffer guidance document (Basel Committee (2010b)). For Sweden, this includes lending from Swedish branches outside Sweden to non-resident entities. The green horizontal lines are critical thresholds as determined by Basel Committee(2010b). At 2 pps, the guidance given by the credit-to-GDP gap would suggest that buffers should start to accumulate. At 10 pps, thegap would suggest that buffers should have reached their maximum.

CGFS – Operationalising the selection and application of macroprudential instruments 15

Overall, the graph confirms that both indicators provide useful signals, as suggested above, albeit with different lead and lag structures around crises. Comparing statistical cross-country evidence with a country-specific perspective, several issues stand out.

First, the indicators under consideration are imperfect in that they issue wrong signals (ie they may signal a crisis without one materialising and vice versa, as highlighted by the orange lines in Graph 2.2). In Switzerland, for instance, one major bank required government support during the recent global crisis, but the indicators presented here correctly identified no domestic vulnerabilities. The reason for this dichotomy was losses stemming from oversees exposures, rather than domestic vulnerabilities, highlighting the importance of cross-border positions for macroprudential policy purposes (see Section 2.1).

Equally, the build-up of vulnerabilities as signalled by the indicators does not necessarily mean that crises will erupt. This was, for example, the case in Australia in the early 2000s, where imbalances decreased after Australian authorities implemented a series of measures targeting the exuberant residential property sector, which could be considered macroprudential.15 Rather than mechanically relying on specific indicators, though, the Australian authorities used a broad a range of information and supervisory judgment.

Second, structural features might render an indicator inappropriate as a reference point for MPIs in a particular country. One example is the price-to-rent gap in Sweden, which would have signalled vulnerabilities persistently since 1998. The housing market in Sweden is, however, characterised by a high degree of regulation, with rents in the public housing sector effectively capping those in the private sector. As a result, observed rents generally do not reflect the market value of the rented units, implying that the price-to-rent ratio cannot provide reliable information.

2.3 Linking systemic risk assessment and MPI selection

An overarching question that policymakers have to decide on is whether they want to link systemic risk assessments and MPI application in a rules-based or discretionary fashion. The principal trade-offs of both approaches are also discussed in detail in previous reports, such as CGFS (2010a).

Rules versus discretion

A rules-based application relies on indicators to provide correct signals for the build-up and release. Given the identification problems described above, this can raise serious calibration issues. In addition and depending on the policy implementation, the Lucas critique may also apply, ie the underlying dynamics may change once the policy is in place. However, a rules-based approach has the benefit of being very transparent, is easily communicated and may act as a commitment device to “take the punch bowl away once the party gets going”.

Alternatively, policymakers may want to act in a discretionary manner. In this case, policymakers would typically try to use as much information as possible and rely on judgment in drawing this information together. In this context, warning signals issued by indicators would tend to act as triggers for deeper analysis, which could involve the use of more formal methods, such as stress tests (see Box 2 in Section 3 below) or full-scale financial stability

15 In particular, APRA undertook a rigorous industry-wide stress test in 2003 designed around a scenario of a

severe housing bust. The results of this test spurred it to introduce a more risk-sensitive capital framework for high risk exposures to the household sector and significantly raise minimum regulatory capital requirements for the mortgage insurance sector as well as tighten other prudential standards.

16 CGFS – Operationalising the selection and application of macroprudential instruments

models.16 Practical experience has also shown that qualitative information can play an important role. For example, the implementation of macroprudential measures for the real estate sector in India was guided by supervisory judgment based on a softer type of information such as evidence of lax underwriting standards, a few fraud cases, anecdotal evidence of inventory build-up and emerging signs of underpricing of risks due to spiralling real estate prices (Table 2.6 suggests some questions that could be useful starting points to elicit this type of soft information during the build-up phase).

Table 2.6

Potential questions to provide qualitative information about the build-up of vulnerabilities

Are there signs of speculative behaviour?

Are particular asset classes heavily advertised or discussed in the media?

Are banks taking large positions where profits continuously exceed measured risks?

Are there relatively new products with large market shares, and have they been increasing rapidly?

Are lending standards falling?

Are profit margins decreasing?

Is competition increasing from the shadow banking sector?

Addressing measurement uncertainty

Measurement uncertainty is another issue that policymakers have to take into account. In part, this uncertainty is inherent to problems of measuring systemic risk, as fragilities emerge infrequently and often in new and unexpected ways. However, uncertainties also arise from problems common to other policy areas, such as delays in data reporting or conflicting messages arising from different sources of information.

The uncertainty of risk assessments has to be set against the cost of mistiming the application of MPIs. While the assessment of this trade-off is situation-dependent, policymakers can use different strategies to cope with it.

If the uncertainty is very large, but there is a clear sense of an underlying vulnerability, they may want to implement MPIs which are not time-varying.17 Similarly, if policymakers are confident that vulnerabilities are building up in a particular sector, sectoral capital requirements could be the appropriate tool. However, such an assessment would also need to take into account that spillovers from a small sector often tend to have broader, system-wide effects.18 In cases where uncertainties around the source of exuberance and potential spillovers are too large, a system-wide countercyclical buffer may be more appropriate. Alternatively, when the reliability of underlying risk weights is in doubt, a risk insensitive

16 For a survey of financial stability models for policy purposes, see Bisias et al (2012). For a more detailed

discussion of the advantages of two-stage frameworks for systemic risk monitoring, see Eichner et al (2010) and Cecchetti et al (2010).

17 See Annex 2 as to why this could be an optimal response in theory. 18 For example, a detailed analysis of spillovers from the household sector to the broader economy is provided

by Sveriges Riksbank (2011).

CGFS – Operationalising the selection and application of macroprudential instruments 17

instrument such as a leverage ratio may be a useful tool. Another strategy to manage uncertainty in risk assessments is based on gradualism, which Asian policymakers have tended to rely on in their application of macroprudential policies. That is, policymakers may adjust MPIs in small steps and sufficiently early, retaining the ability to observe the impact and change the setting, if necessary.

Taking account of instrument characteristics and the policy process

The appropriate timing for the application of MPIs also depends on inherent characteristics of the instruments and the policy process. For example, once the legal and operational infrastructure is in place, LTV and DTI caps can be implemented rather rapidly. On the other hand, banks may need possibly several months to adjust to higher capital or liquidity requirements without being forced into fire sales or deleveraging, unless these are applied just to the flow of new lending (see Annex 5 for a discussion). The policy process may also take some time, as for example data are reported with lags. In addition, in many cases the application of MPIs does not completely rest with one authority, but measures are often discussed and information is shared among a group of relevant agencies through inter-agency groups, which may prolong the process further. These considerations favour starting the process of adjusting MPIs early, and relying on instruments for which knowledge about any implementation lags already exists.

3. The transmission mechanism of MPIs

To select the appropriate MPIs, policymakers have to judge which instruments can effectively and efficiently address an identified vulnerability. This section studies the conceptual transmission mechanism for a range of MPIs to illustrate key aspects of how the efficiency and effectiveness of instruments could be judged in practice.

As a practical tool, “transmission maps” are proposed to draw attention to the main transmission channels through which MPIs can achieve the macroprudential objectives of increasing resilience and leaning against the credit cycle.19 Both objectives are highlighted, even though the latter (“leaning”) is the more ambitious one, which, if pursued, implies a careful approach until more practical experience has been gained with the impact of MPIs on the credit cycle (see CGFS (2010a) and Box 1).

Where possible, the analysis is supplemented with empirical evidence to provide some indications of the effectiveness and efficiency of different MPIs, as a full cost-benefit analysis of different tools is likely to be highly state-dependent in practice and fraught with uncertainties in the absence of a usable top-down approach. The main aim of the discussion is, therefore, to provide a clearer narrative on the transmission channels through which the tools can achieve the two macroprudential objectives.

The build-up and release phases are analysed separately, as the dynamics may differ, starting with the tightening phase of capital-based, liquidity-based and then asset-side tools. Subsequently, potential interactions between MPIs as well as with other policy areas are discussed.

19 The transmission maps are stylised representations of the transmission mechanism of MPIs, highlighting the

key channels through which MPIs can achieve both macroprudential objectives. As such, they abstract from potential second-round effects, like the feedback from the credit cycle to output, which in turn may impact on leverage, asset prices and risk-taking.

18 CGFS – Operationalising the selection and application of macroprudential instruments

3.1 Tightening capital-based MPIs

This section focuses on the tightening phase of countercyclical capital buffers as envisaged by Basel III, sectoral capital requirements, as well as dynamic provisions. These three MPIs are referred to as capital-based MPIs in the report.20 In addition, Box 2 discusses capital stress tests, which can be used to assess potential capital shortfalls.

A generic transmission map for capital-based MPIs is shown in Graph 3.1 (upper panel), reflecting the broad similarity of the transmission channels of the three different types of capital-based instruments. However, some differences remain. While aggregate, system-wide buffers are calibrated to ensure that the banking system as a whole is properly capitalised from a macroprudential perspective, sectoral capital requirements concentrate on the relative price of – and risks stemming from – lending to a particular sector in the economy (Graph 3.1, lower panel).21 Provisions, in turn, work through the profit and loss accounts of banks and are conceptually based on an assessment of impairments rather than unexpected losses. They may thus alter management’s incentives more directly than capital requirements.22

20 Macroprudential leverage ratios may be an alternative capital-based MPI. Their main benefit – but also main

drawback – is that they are not risk sensitive but based on capital relative to total assets. 21 Sectoral capital requirements can be operationalised in a number of different ways, as discussed in Annex 5. 22 An additional consideration is that capital requirements are fully within the realm of banking supervision. In

contrast, provisions are chiefly influenced by accounting practices.

Box 2

Stress testing

Stress tests have been used as a method to assess the resilience of banks and the banking sector for a while. Since the global crisis, stress testing has gained in prominence and in some countries, such as the United States, it has even been partly enacted in legislation. While stress testing is primarily a supervisory instrument, macro stress tests have the potential to reveal the build-up of financial system risks that might not be visible from standard supervisory information. As such, they can provide quantitative guidance on how capital levels should be adjusted. In addition, they can serve as the basis for coordinated, macroprudential disclosures aimed at reducing market uncertainty about risks related to the specified stress scenarios.

The transmission mechanics of stress tests are shown in Graph B1. The exercise begins with a stressed scenario. This is fed through a set of equations that forecast income and losses to determine net profits, which in turn determine bank capital. In the case of a shortfall, the transmission mechanism of tighter requirements is in line with the general case (Graph 3.1, upper panel). In normal conditions, stress tests imply that banks will be sufficiently well capitalised to be resilient against a severe but plausible downturn. When additional systemic risks are building up in a buoyant economy – because, for example, underwriting standards weaken – stress tests can result in higher pro forma levels of capital, as higher loss rates are likely to be revealed in the stress scenario. Thus resilience increases. If banks also internalise the (higher pro forma capital) cost of laxer lending standards, this may also slow their deterioration, any associated excessive credit growth, and thereby the build-up of systemic risk.

Conceptually, stress tests can assess various sources of systemic risk. Asset prices – such as residential or commercial real estate prices – can increase rapidly in buoyant times and present a common source of downside risk. Stress test scenarios can also be designed to address specific sources of systemic risk. For example, if systemic risk is building up on account of prices increasing

CGFS – Operationalising the selection and application of macroprudential instruments 19

Graph B.1

Transmission map of stress tests

Purple cells = possible bank reactions; blue cells = possible market reactions.

1 SEO: seasoned equity offer.

very rapidly for only one class of assets, such as residential real estate, the scenario can be tailored to this asset class, leading to higher pro forma capital ratios for loans to the targeted sector. Stress tests also have the potential to capture various channels of contagion, such as fire sales and liquidity dry-ups. However, modelling uncertainties remain large, requiring sound judgement during the application as well as for the interpretation of stress tests.

_____________________ Macro stress tests can also be an effective crisis management tool. In this case, the US and European experience suggests that this requires the existence of a credible mechanism for any necessary recapitalisations. The variables that would typically be included in this scenario are activity variables (such as real GDP growth and the unemployment rate), asset prices (such as equity prices and real estate prices) and interest rates (such as short- and long-term government bond rates, corporate bond rates and mortgage rates).

20 CGFS – Operationalising the selection and application of macroprudential instruments

Graph 3.1

Transmission map of raising capital or provisioning requirements

Transmission map of raising sectoral capital requirements

Purple cells = possible bank reactions; blue cells = possible market reactions. 1 SEO: seasoned equity offer. 2 The impact of tighter capital requirements for sector X on credit conditions in other sectors isambiguous. One the one hand, the quantity of credit in other sectors could decrease, if banks fulfill sector specific capital requirements by increasing spreads or curtailing credit across the board. On the other hand, the quantity of credit in other sectors may increase aslending to other sectors becomes relatively more attractive in comparison to lending to sector X.

CGFS – Operationalising the selection and application of macroprudential instruments 21

3.1.1 Transmission maps for capital-based MPIs

The transmission maps illustrate the key transmission channels through which tightening capital-based MPIs can impact on the resilience of the financial sector and the credit cycle. Expectations-based implications for bank behaviour and instrument leakages are also highlighted – effects that can impact on both objectives.

Impact on resilience. Raising capital or provisioning requirements enhances the resilience of the banking system in a direct fashion. The additional buffers mean that banks are able to weather losses of a greater magnitude before their solvency is called into question, thus reducing the likelihood of a costly disruption to the supply of credit and other financial intermediation services. In addition, resilience may also be increased indirectly via the impact on the credit cycle and by affecting expectations and, hence, market participants’ behaviours and banks’ risk management practices.

Impact on the credit cycle. Banks have four broad options to respond to a shortfall in capital or provisions: (i) increase lending spreads, (ii) decrease dividends and bonuses, (iii) issue new capital or (iv) reduce asset holdings.

The first three options may negatively affect credit demand, as lending spreads are likely to increase. Higher lending spreads are a common response to increased funding costs, as implied by both a reduction in dividends and the issuance of new equity. Lending spreads are likely to be increased disproportionately for new and repriceable loans, as interest rates on outstanding loans are often fixed in many countries.

The fourth option leads to a reduction in the supply of credit, as banks may respond to tighter MPI settings by rationing the overall quantity of credit. One possibility is to restrict the extension of new credit across the board. Another, more likely one, is to shift the composition of assets towards exposures that carry lower risk weights or lower provisioning requirements.

The impact on credit conditions of tightening sectoral capital requirements is broadly similar to that of the other two capital-based MPIs. However, there are differences. First, higher sectoral capital requirements increase the relative cost for banks of lending to the specified sector, providing sharper incentives to reduce activity there. Second, banks may find it hard to raise external equity to fund lending that has been singled out by the macroprudential authority as particularly risky, increasing the pressure on banks to build up capital through retained earnings or by reducing the supply of credit – most likely to the targeted sector.

Expectations-based effects. Expectations are central to banks’ capital planning, risk management and lending decisions as well as to those of other market participants. As in the case of the monetary policy transmission mechanism, expectations are therefore likely to be a key part of the transmission mechanism for MPIs.

One factor that is likely to influence the power of any expectations-based effect is the strength of the policy signal. As the activation of MPIs is costly in comparison with financial stability policies that predominantly rely on communication and moral suasion, credibility is enhanced. Such a signal should thus have broader effects on lending standards and risk management practices, which will in turn increase the resilience of the system.

Another factor determining the impact of MPI activation is whether market participants understand the policymaker’s reaction function and interpret it correctly. If policy is predictable in this way, banks may change their behaviour in anticipation of policy actions – for example, by reducing exposures to sectors showing signs of overheating. These expectational effects may become stronger once a history of macroprudential policymaking has been established. This suggests that it may be useful to employ a small set of

22 CGFS – Operationalising the selection and application of macroprudential instruments

instruments rather than a larger range of little-known tools that are similar, yet different and may be infrequently used. In addition, this underscores the importance of appropriate communication strategies as highlighted by Principle 7 in Annex 1.23

Leakages and potential unintended consequences. The possibilities for leakages and arbitrage are an important aspect of the transmission mechanism of MPIs. Part of the tightening of a capital-based MPI may become ineffective, if banks, for example, reduce any voluntary buffers one-for-one. But this effect has natural limits, suggesting that a gradual implementation may be useful to take account of these effects.

Some of the reduction in bank credit will also be taken up by non-bank intermediaries or internationally active banks that are not subject to the MPI.24 Large borrowers in developed markets, for example, may be able to substitute bank credit with the issuance of bonds and similar instruments. Cross-border sources of finance, in turn, can be tapped quite easily by all borrowers, including households.

Another example is outright regulatory arbitrage, which in practice often becomes apparent only once the MPIs are applied and market reactions are being observed (see Box 3). Banks may also try to dampen the impact of policy changes by gaming internal models to generate lower risk-weighted assets. This may happen already in normal times, but tightening capital requirements may increase these incentives.25 Gaming risk weights may occur in particular in response to increasing sectoral capital requirements, as only one part of a bank’s book is affected. Macroprudential supervisors, therefore, need to track regulatory arbitrage activity on an ongoing basis, which requires regular surveillance of key market participants and the ability to identify subtle trends or abnormal patterns in financial data reported by banks.

A useful approach to prevent regulatory arbitrage is to design simple rules that help improve regulatory compliance. As such leverage ratios could be useful complements to other capital-based tools which build on internal models to calculate risk weights. In addition, reciprocal arrangements are beneficial to containing cross-border arbitrage.26

An inappropriate application of MPIs to deal with the risks at hand could impair the resilience of the system as a whole. For instance, if the source of exuberance is general (eg due to abundant liquidity and aggregate mispricing of risk), raising capital requirements for some specific sectors may simply shift exuberance to other sectors – a “waterbed effect”. The correct identification of the underlying vulnerabilities is therefore critical for the use of these instruments (see Section 2.3).

23 To the extent that systemic risk can arise from coordination failures among different actors in the financial

system, signals from policymakers could also help to coordinate behaviour on better outcomes. Policy signals and expectations of future policy actions could, for example, alleviate pressure on individual banks to keep up with the behaviour of peers that are regarded as bellwethers or industry leaders, making it easier for them to step away from business activities in exuberant sectors.

24 As regulatory arbitrage via the shadow banking sector is a general problem beyond macroprudential regulation, steps are undertaken to strengthen the oversight of this sector (see eg FSB (2011)).

25 There is on-going work by the Basel Committee to assess the consistency in the measurement of risk-weighted assets in the banking and trading book.

26 In this context, in order not to affect banks’ choices of branching versus subsidiarisation, branches of foreign banks should be treated the same as subsidiaries.

CGFS – Operationalising the selection and application of macroprudential instruments 23

Box 3

Avoiding regulatory arbitrage in practice

Regulatory arbitrage is an important consideration when designing MPIs in practice. In some instances, though, the scope for regulatory arbitrage becomes apparent only once the MPI is in place. For example, Singapore implemented LTV caps on corporate borrowers to dampen demand from this sector. An additional consideration was to prevent individual buyers from circumventing existing LTV rules by forming companies to purchase residential property. To avoid arbitrage, Singapore’s authorities also tried to implement simple rules. For instance, Singapore’s LTV rule is applied to individuals with one or more housing loans outstanding at the time of application rather than to housing loans obtained for investment purposes. While the latter are self-declared and can thus be open to subjective interpretations, the former are identified on the basis of an objective criterion, which can be readily measured.

In contrast, regulatory arbitrage activity that seemed possible when designing the MPI may not actually occur. In Hong Kong SAR, for example, borrowers that cannot access domestic bank credit due to LTV rules could in theory seek cross-border or non-bank funding. So far, the Hong Kong Monetary Authority’s surveillance work – which includes regular and close dialogues with banks and the monitoring of banking statistics – suggests that no significant cross-border arbitrage has been taking place in response to the MPIs imposed in Hong Kong SAR.

3.1.2 Empirical evidence27

The transmission maps suggest that applying capital-based MPIs is likely to effectively impact on the resilience of the financial sector and the credit cycle. For efficiency assessments, potential costs have also to be taken into account. A sense of the empirical effects of tightening capital-based MPIs is provided by a range of studies:

Impact on resilience. While the impact of higher capital ratios and greater provisions on the resilience of individual banks is self-evident, the same applies from a system perspective. There is clear evidence that dynamic provisions increase the resilience of the financial system and several studies show that the same is true for higher levels of capital. For example, based on a range of models, the Long-term Economic Impact Assessment (LEI, Basel Committee (2010a)) estimates that a 1 percentage point rise in capital requirements leads to a 20–50% reduction in the likelihood of systemic crises. In absolute terms, however, marginal benefits of higher capital ratios decrease with higher initial capital levels.

Impact on the credit cycle. Empirical evidence also indicates that capital-based MPIs are effective in affecting (i) the price and (ii) the quantity of credit, even though the uncertainty about precise magnitudes is relatively large.

First, several studies suggest that lending spreads could increase between 2 and 20 basis points in response to a 1 percentage point increase in capital ratios, depending on whether funding costs change in response to greater equity cushions due to their effect on the likelihood of failure (ie depending on whether the Modigliani-Miller theorem is assumed to hold or not).

Second, tightening capital-based MPIs seems to decrease the volume of credit in the economy. There is evidence that, in the short run, banks seem to respond to an increase in target capital ratios by making about a half to three quarters of the required change through an increase in capital and the remainder through a reduction of risk-weighted asset (RWA),

27 References to the relevant literature can be found in Annex 4.1.

24 CGFS – Operationalising the selection and application of macroprudential instruments

of which in turn only half is in the form of reduced lending. This would imply that a bank with an initial capital ratio of 8% would decrease its lending by 1.5 to 3% for a 1 percentage point increase in capital requirements.28 Based on the increase in lending spreads and banks’ reduction in credit, the Macroeconomic Assessment Group (MAG (2010)) estimates that the median impact of increasing capital ratios by 1 percentage point is a reduction in lending by 1–2 percentage points. The evidence of the effects of higher provisions on the credit cycle is more mixed. While research indicates that they have been effective in this regard in Spain, this does not seem to be the case in Chile and Colombia.

The overall effectiveness of capital-based MPIs in affecting the credit cycle is, however, likely to be reduced by two factors. First, around 30–50% of the reduction in bank credit has historically been offset by an increase in lending by unaffected banks and other credit providers. Second, during booms it is not uncommon for real credit to grow by 15–25%, suggesting that capital-based MPIs would need to be tightened quite significantly to bring credit growth down to more normal levels.

Impact on output. The MAG finds that, in the short to medium run, the median impact of a 1 percentage point increase in capital requirements decreases annual GDP growth by 0.04 percentage points. In the long run, the LEI estimates that such an increases lowers long-run output by 0.09%, when the positive impact on the reduction of the frequency and severity of banking crisis is not taken into account.29 However, other studies find no long-run costs at all.

3.2 Tightening liquidity-based tools