opportunities for epichlorohydrin (ech) in...

TRANSCRIPT

www.klinegroup.com

Opportunities for Epichlorohydrin (ECH) in India

Presentation for:

March 07th, 2017

1

Presentation Outline

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

2

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

3

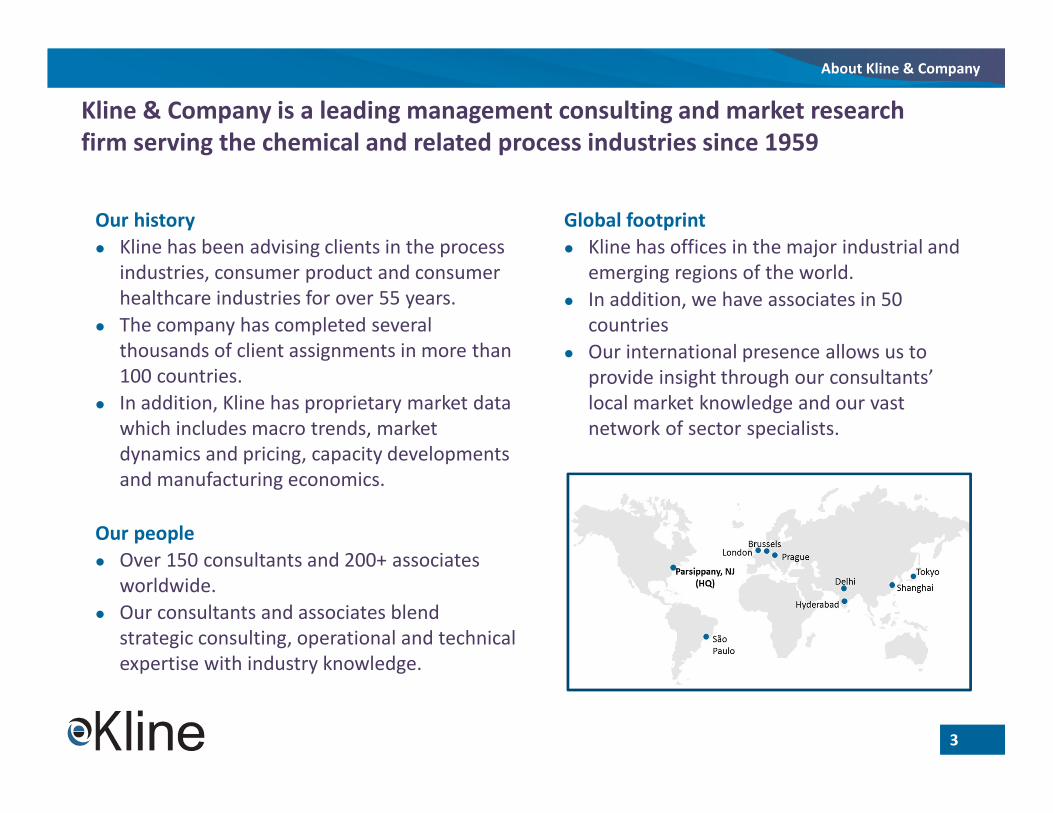

Kline & Company is a leading management consulting and market research

firm serving the chemical and related process industries since 1959

Our history

� Kline has been advising clients in the process

industries, consumer product and consumer

healthcare industries for over 55 years.

� The company has completed several

thousands of client assignments in more than

100 countries.

� In addition, Kline has proprietary market data

which includes macro trends, market

dynamics and pricing, capacity developments

and manufacturing economics.

Our people

� Over 150 consultants and 200+ associates

worldwide.

� Our consultants and associates blend

strategic consulting, operational and technical

expertise with industry knowledge.

Global footprint

� Kline has offices in the major industrial and

emerging regions of the world.

� In addition, we have associates in 50

countries

� Our international presence allows us to

provide insight through our consultants’

local market knowledge and our vast

network of sector specialists.

About Kline & Company

4

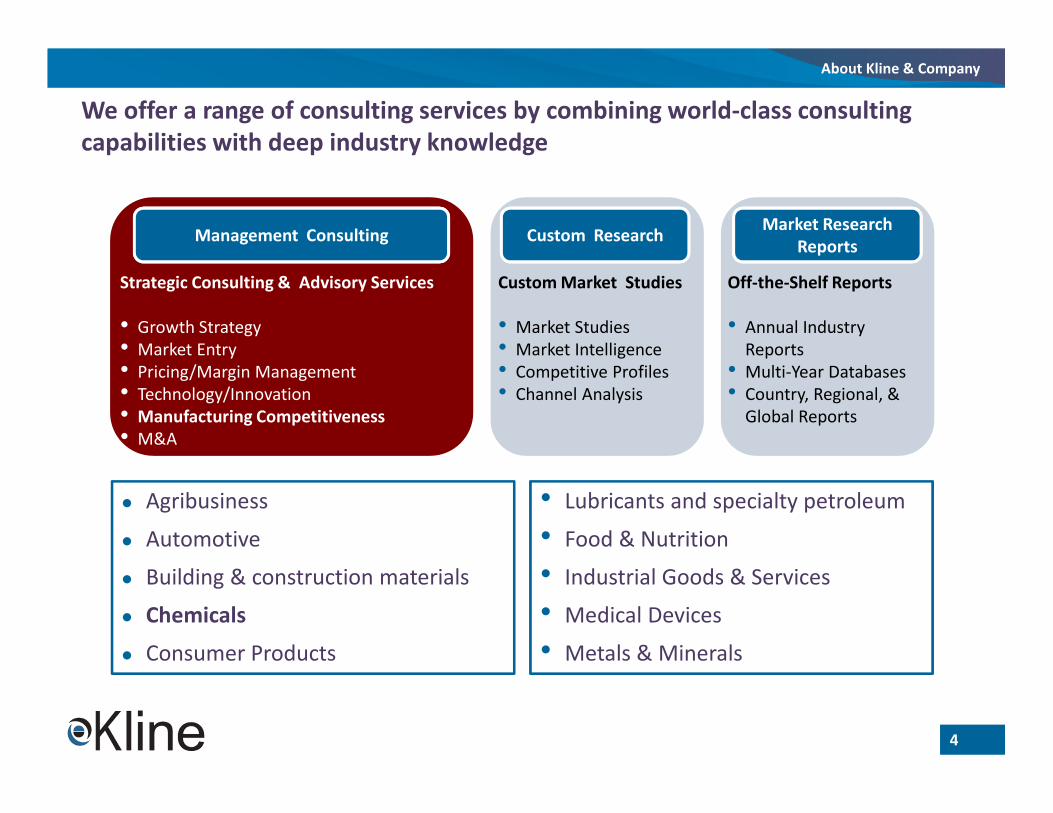

We offer a range of consulting services by combining world-class consulting

capabilities with deep industry knowledge

Management Consulting

Strategic Consulting & Advisory Services

• Growth Strategy

• Market Entry

• Pricing/Margin Management

• Technology/Innovation

• Manufacturing Competitiveness

• M&A

Custom ResearchMarket Research

Reports

Custom Market Studies

• Market Studies

• Market Intelligence

• Competitive Profiles

• Channel Analysis

Off-the-Shelf Reports

• Annual Industry

Reports

• Multi-Year Databases

• Country, Regional, &

Global Reports

� Agribusiness

� Automotive

� Building & construction materials

� Chemicals

� Consumer Products

• Lubricants and specialty petroleum

• Food & Nutrition

• Industrial Goods & Services

• Medical Devices

• Metals & Minerals

About Kline & Company

5

Our Management Consulting services are targeted to assist clients in meeting

their objectives for growth, cost reduction and enhancing profitability

Growth Considerations

Manufacturing CompetitivenessTechnology Management

Pricing & Margin Management Mergers & Acquisition

Management Consulting Services

6

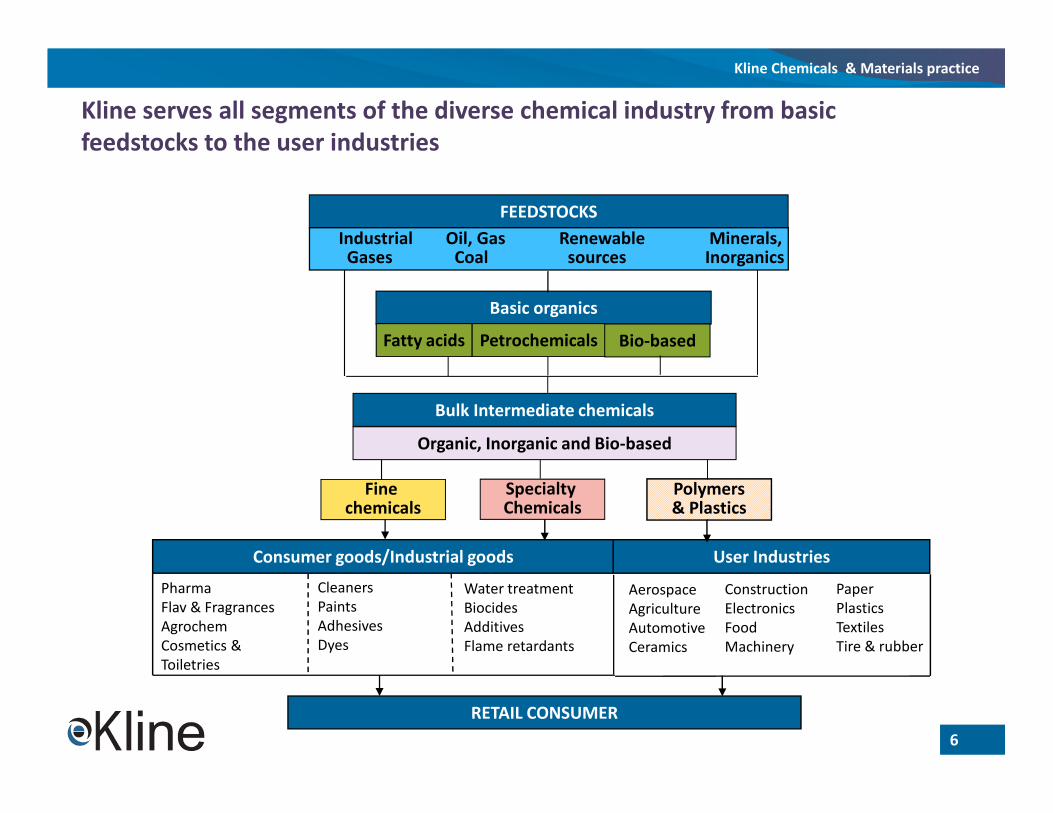

Kline serves all segments of the diverse chemical industry from basic

feedstocks to the user industries

Kline Chemicals & Materials practice

Consumer goods/Industrial goods

RETAIL CONSUMER

User Industries

Aerospace

Agriculture

Automotive

Ceramics

Construction

Electronics

Food

Machinery

Paper

Plastics

Textiles

Tire & rubber

Cleaners

Paints

Adhesives

Dyes

Water treatment

Biocides

Additives

Flame retardants

Basic organics

PetrochemicalsFatty acids

Bulk Intermediate chemicals

Pharma

Flav & Fragrances

Agrochem

Cosmetics &

Toiletries

FEEDSTOCKS

Industrial Oil, Gas Renewable Minerals,Gases Coal sources Inorganics

Organic, Inorganic and Bio-based

Fine chemicals

Polymers & Plastics

Specialty Chemicals

Bio-based

7

Kline covers all chemical product value chains, from feedstocks to individual

product families used in various applications

Kline Chemicals & Materials practice

8

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

9

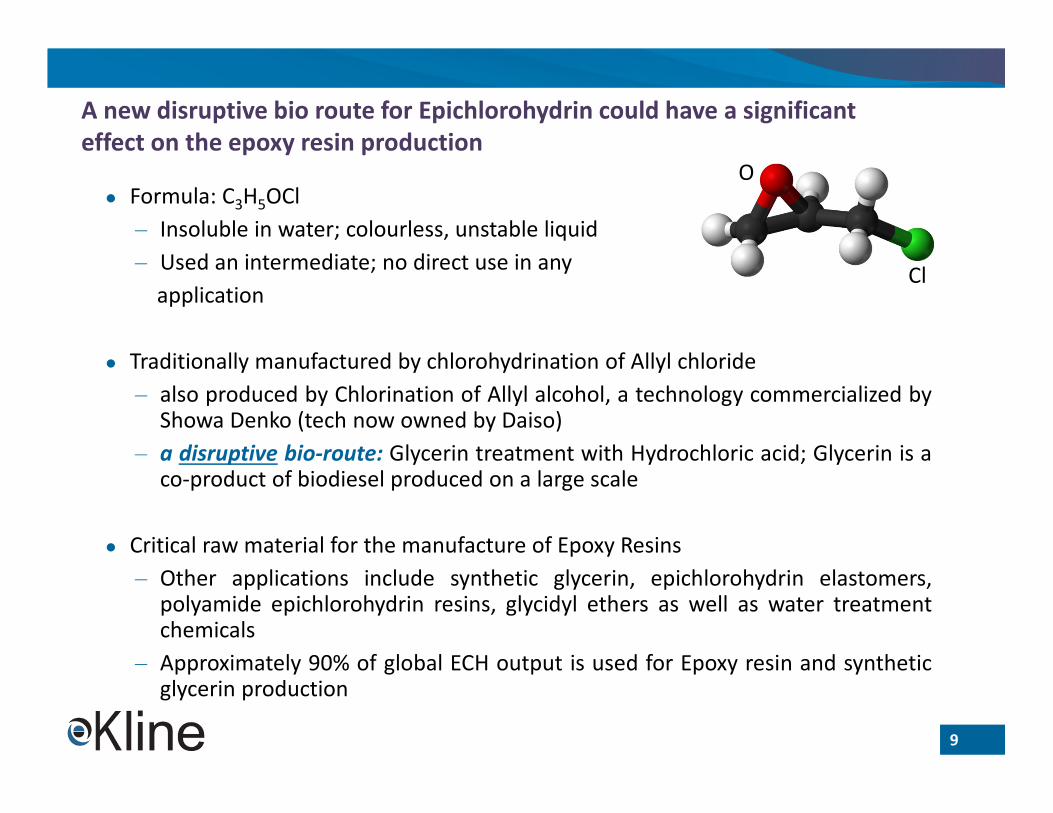

A new disruptive bio route for Epichlorohydrin could have a significant

effect on the epoxy resin production

� Formula: C3H5OCl

‒ Insoluble in water; colourless, unstable liquid

‒ Used an intermediate; no direct use in any

application

� Traditionally manufactured by chlorohydrination of Allyl chloride

‒ also produced by Chlorination of Allyl alcohol, a technology commercialized byShowa Denko (tech now owned by Daiso)

‒ a disruptive bio-route: Glycerin treatment with Hydrochloric acid; Glycerin is aco-product of biodiesel produced on a large scale

� Critical raw material for the manufacture of Epoxy Resins

‒ Other applications include synthetic glycerin, epichlorohydrin elastomers,polyamide epichlorohydrin resins, glycidyl ethers as well as water treatmentchemicals

‒ Approximately 90% of global ECH output is used for Epoxy resin and syntheticglycerin production

O

Cl

10

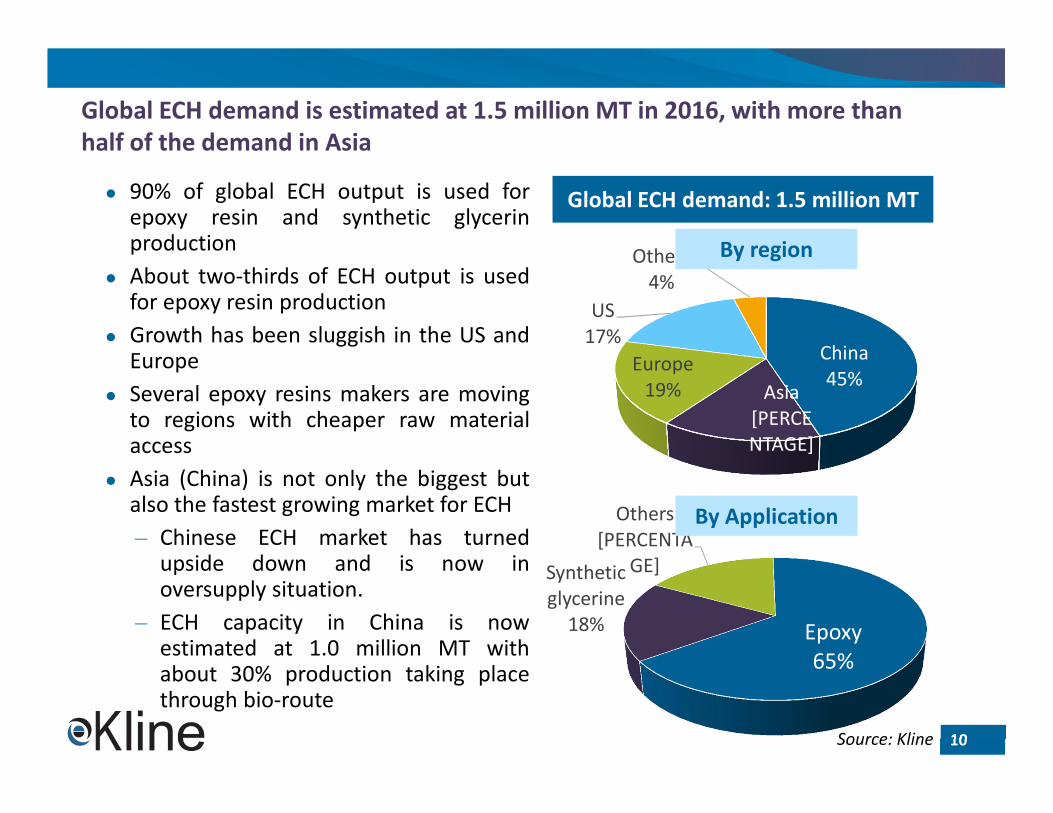

Global ECH demand is estimated at 1.5 million MT in 2016, with more than

half of the demand in Asia

China

45%Asia

[PERCE

NTAGE]

Europe

19%

US

17%

Others

4%

� 90% of global ECH output is used forepoxy resin and synthetic glycerinproduction

� About two-thirds of ECH output is usedfor epoxy resin production

� Growth has been sluggish in the US andEurope

� Several epoxy resins makers are movingto regions with cheaper raw materialaccess

� Asia (China) is not only the biggest butalso the fastest growing market for ECH

‒ Chinese ECH market has turnedupside down and is now inoversupply situation.

‒ ECH capacity in China is nowestimated at 1.0 million MT withabout 30% production taking placethrough bio-route

Global ECH demand: 1.5 million MT

Epoxy

65%

Synthetic

glycerine

18%

Others

[PERCENTA

GE]

By region

By Application

Source: Kline

11

ECH landscape has changed dramatically in the last decade, with new

technology footprint and capacity addition in Asia (China)

� Historically, the majority of ECH capacity had been focused in the US, Europe and

Japan (> 80% of global capacity)

� In the last decade, significant ECH capacity addition has taken place in Asia (mainly

China), mostly following new epoxy resin plant construction

� The traditional strong markets of the US and Europe for epoxy resins have grown

at a CAGR of about 2% over the last decade

� About 50% of the world ECH supply is controlled by the epoxy makers, this share

was about 70% a decade ago

� Dow and Solvay use in-house ECH technology (conventional as well as bio-based)

whereas others have licensed technology from such licensors as Conser SPA,

Solvay, Spolchemie

� Showa Denko, Hexion, Zachem, Tamilnadu Petro have ceased ECH production

� Almost all of the new ECH capacity in the last decade has been based on bio-

based routes

12

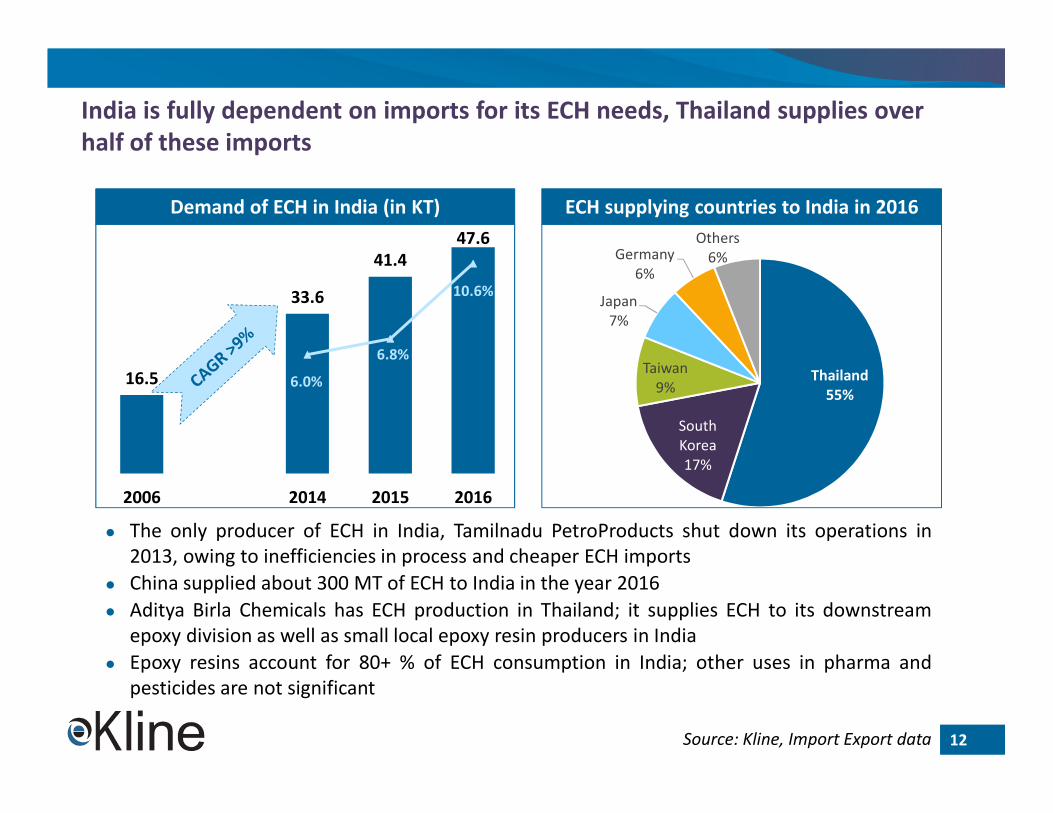

India is fully dependent on imports for its ECH needs, Thailand supplies over

half of these imports

Thailand

55%

South

Korea

17%

Taiwan

9%

Japan

7%

Germany

6%

Others

6%

16.5

33.6

41.4

47.6

6.0%

6.8%

10.6%

0

5

10

15

20

25

30

35

40

45

50

2006 2014 2015 2016

� The only producer of ECH in India, Tamilnadu PetroProducts shut down its operations in

2013, owing to inefficiencies in process and cheaper ECH imports

� China supplied about 300 MT of ECH to India in the year 2016

� Aditya Birla Chemicals has ECH production in Thailand; it supplies ECH to its downstream

epoxy division as well as small local epoxy resin producers in India

� Epoxy resins account for 80+ % of ECH consumption in India; other uses in pharma and

pesticides are not significant

ECH supplying countries to India in 2016Demand of ECH in India (in KT)

Source: Kline, Import Export data

13

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

14

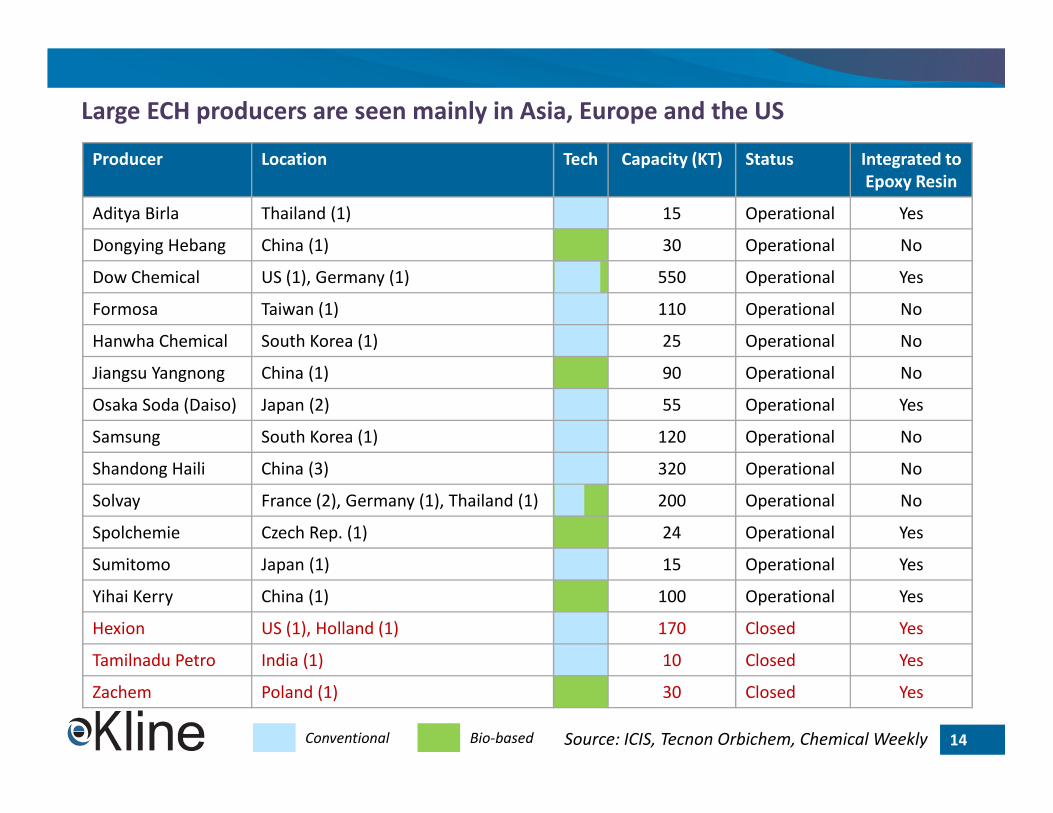

Large ECH producers are seen mainly in Asia, Europe and the US

Producer Location Tech Capacity (KT) Status Integrated to

Epoxy Resin

Aditya Birla Thailand (1) 15 Operational Yes

Dongying Hebang China (1) 30 Operational No

Dow Chemical US (1), Germany (1) 550 Operational Yes

Formosa Taiwan (1) 110 Operational No

Hanwha Chemical South Korea (1) 25 Operational No

Jiangsu Yangnong China (1) 90 Operational No

Osaka Soda (Daiso) Japan (2) 55 Operational Yes

Samsung South Korea (1) 120 Operational No

Shandong Haili China (3) 320 Operational No

Solvay France (2), Germany (1), Thailand (1) 200 Operational No

Spolchemie Czech Rep. (1) 24 Operational Yes

Sumitomo Japan (1) 15 Operational Yes

Yihai Kerry China (1) 100 Operational Yes

Hexion US (1), Holland (1) 170 Closed Yes

Tamilnadu Petro India (1) 10 Closed Yes

Zachem Poland (1) 30 Closed Yes

Conventional Bio-based Source: ICIS, Tecnon Orbichem, Chemical Weekly

15

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

16

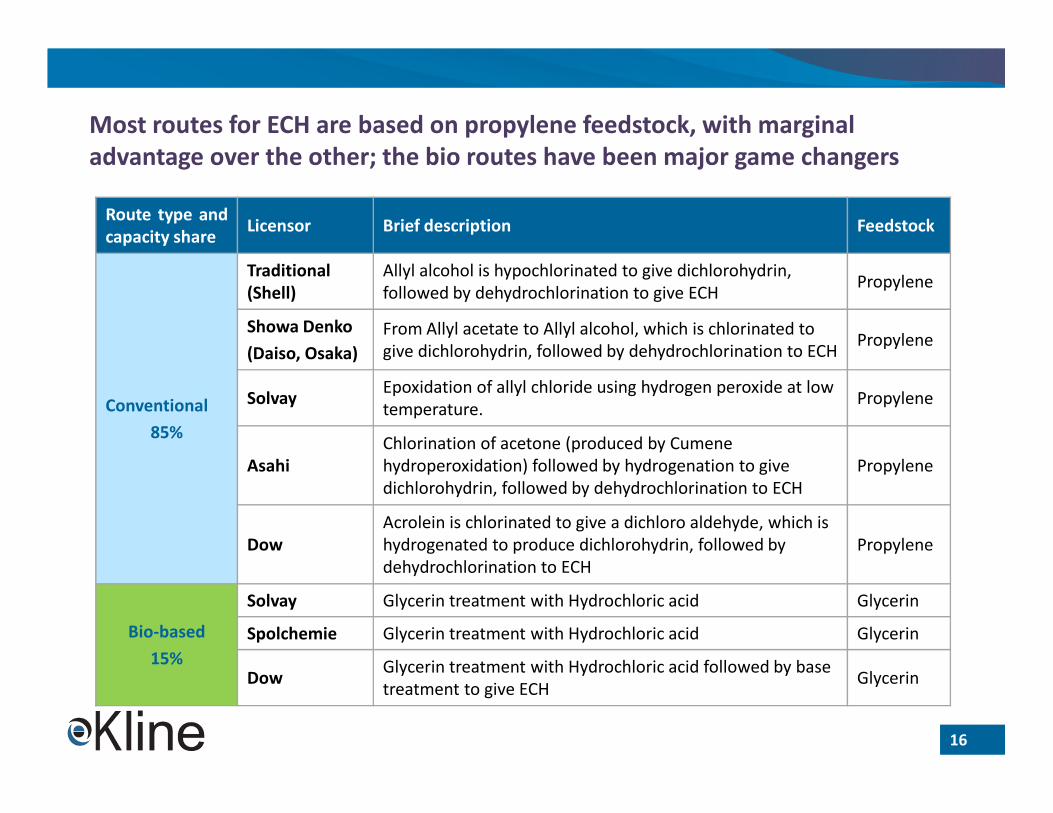

Most routes for ECH are based on propylene feedstock, with marginal

advantage over the other; the bio routes have been major game changers

Route type and

capacity shareLicensor Brief description Feedstock

Conventional

85%

Traditional

(Shell)

Allyl alcohol is hypochlorinated to give dichlorohydrin,

followed by dehydrochlorination to give ECHPropylene

Showa Denko

(Daiso, Osaka)

From Allyl acetate to Allyl alcohol, which is chlorinated to

give dichlorohydrin, followed by dehydrochlorination to ECHPropylene

Solvay Epoxidation of allyl chloride using hydrogen peroxide at low

temperature.Propylene

Asahi

Chlorination of acetone (produced by Cumene

hydroperoxidation) followed by hydrogenation to give

dichlorohydrin, followed by dehydrochlorination to ECH

Propylene

Dow

Acrolein is chlorinated to give a dichloro aldehyde, which is

hydrogenated to produce dichlorohydrin, followed by

dehydrochlorination to ECH

Propylene

Bio-based

15%

Solvay Glycerin treatment with Hydrochloric acid Glycerin

Spolchemie Glycerin treatment with Hydrochloric acid Glycerin

DowGlycerin treatment with Hydrochloric acid followed by base

treatment to give ECHGlycerin

17

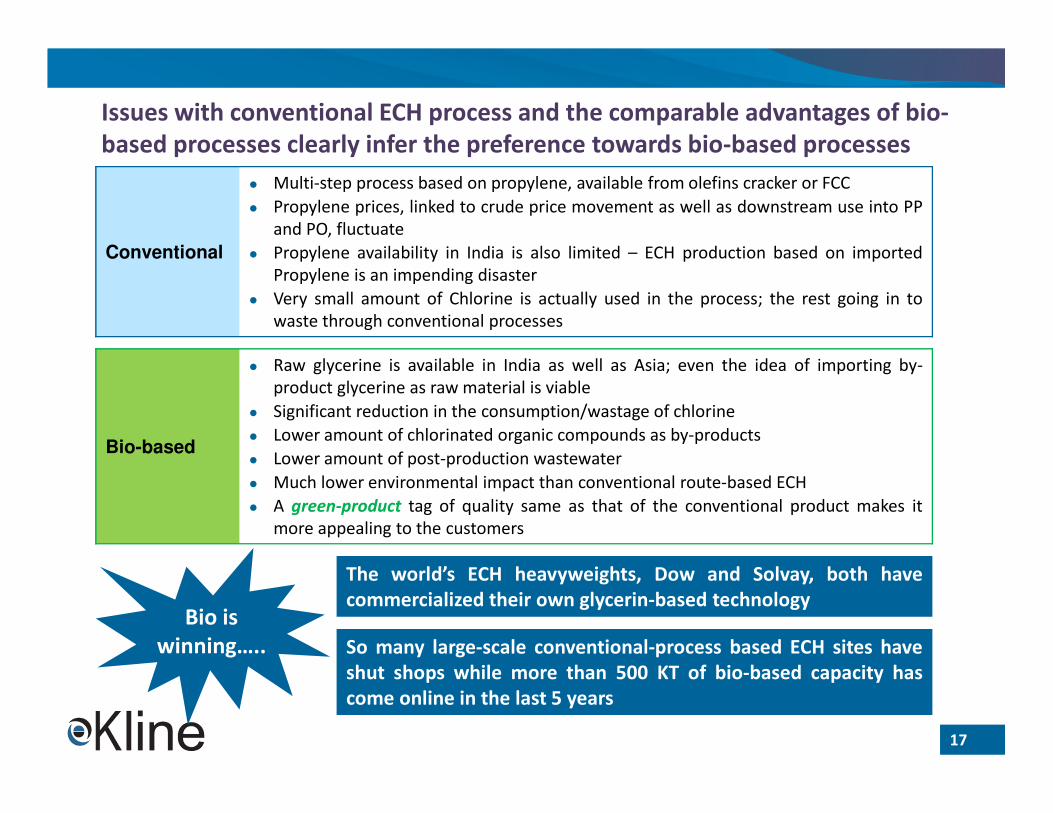

Issues with conventional ECH process and the comparable advantages of bio-

based processes clearly infer the preference towards bio-based processes

Conventional

� Multi-step process based on propylene, available from olefins cracker or FCC

� Propylene prices, linked to crude price movement as well as downstream use into PP

and PO, fluctuate

� Propylene availability in India is also limited – ECH production based on imported

Propylene is an impending disaster

� Very small amount of Chlorine is actually used in the process; the rest going in to

waste through conventional processes

Bio-based

� Raw glycerine is available in India as well as Asia; even the idea of importing by-

product glycerine as raw material is viable

� Significant reduction in the consumption/wastage of chlorine

� Lower amount of chlorinated organic compounds as by-products

� Lower amount of post-production wastewater

� Much lower environmental impact than conventional route-based ECH

� A green-product tag of quality same as that of the conventional product makes it

more appealing to the customers

The world’s ECH heavyweights, Dow and Solvay, both have

commercialized their own glycerin-based technology

So many large-scale conventional-process based ECH sites have

shut shops while more than 500 KT of bio-based capacity has

come online in the last 5 years

Bio is

winning…..

18

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

19

The demand of epoxy resins in India is estimated at 90 KT, with majority of

the demand in coatings and composites

Coatings

54%

Composite

s

30%

Electronics

8%

Adhesives

6%Others

2%

� Fragmented industry with key producers:

Atul, Huntsman, Resinova, Kemrock; many

small capacity epoxy makers making basic

BLER resins

� Imports quite prevalent (@ 35% of demand),

due to domestic demand, insufficient local

production and quality requirements

� Absence of global epoxy makers and raw

material suppliers

Epoxy resin market in India in 2016Indian Epoxy resins Industry overview

� Growth in Infrastructure (wind energy) and construction sector

� Emerging end use industries

� Increasing spending on consumer durable items

� Sustained reduction in import duties on epoxies

� Low-cost imports from South east Asia (Thailand)

� Exchange rate risk (since most of the raw material is imported)

� Import of advanced epoxy formulated grades

� New entrants making the market more competitive

� Usage of substitute products like UPR, acrylics

Constraints

Drivers

Source: Kline, Chemical Weekly

20

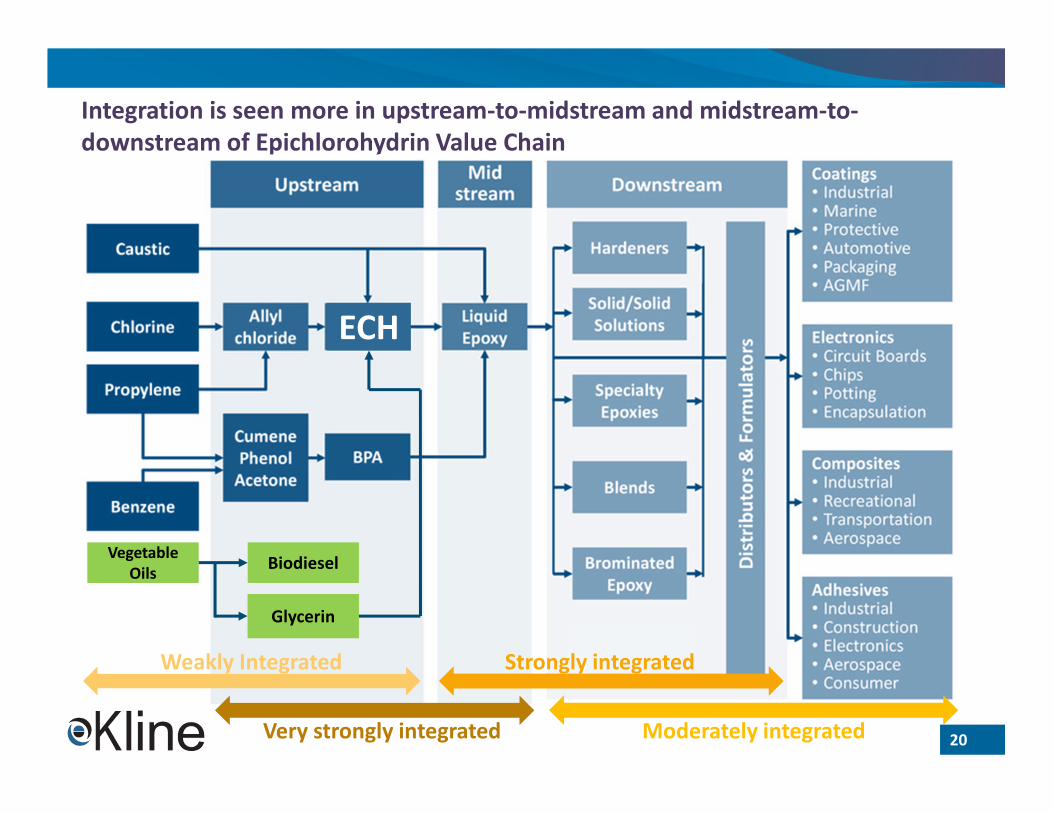

Integration is seen more in upstream-to-midstream and midstream-to-

downstream of Epichlorohydrin Value Chain

Glycerin

ECH

Weakly Integrated Strongly integrated

Very strongly integrated Moderately integrated

Vegetable

OilsBiodiesel

21

ECH - Global and Indian Market

Key ECH suppliers in the world

ECH - Alternate Technology Routes and feedstock assessment

Epoxy Resins Market Scenario in India and synergy with ECH

Issues and recommendations for ECH production in India

About Kline

22

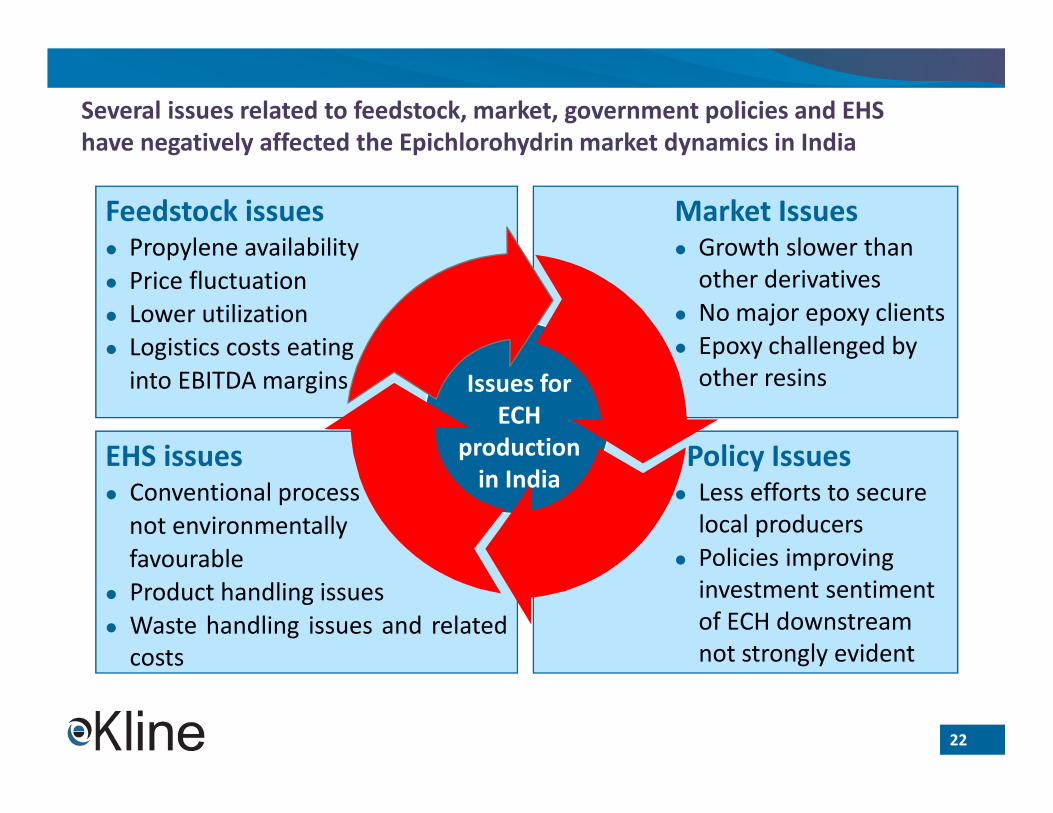

Several issues related to feedstock, market, government policies and EHS

have negatively affected the Epichlorohydrin market dynamics in India

Feedstock issues� Propylene availability

� Price fluctuation

� Lower utilization

� Logistics costs eating

into EBITDA margins

Market Issues� Growth slower than

other derivatives

� No major epoxy clients

� Epoxy challenged by

other resins

EHS issues� Conventional process

not environmentally

favourable

� Product handling issues

� Waste handling issues and related

costs

Policy Issues� Less efforts to secure

local producers

� Policies improving

investment sentiment

of ECH downstream

not strongly evident

Issues for

ECH

production

in India

23

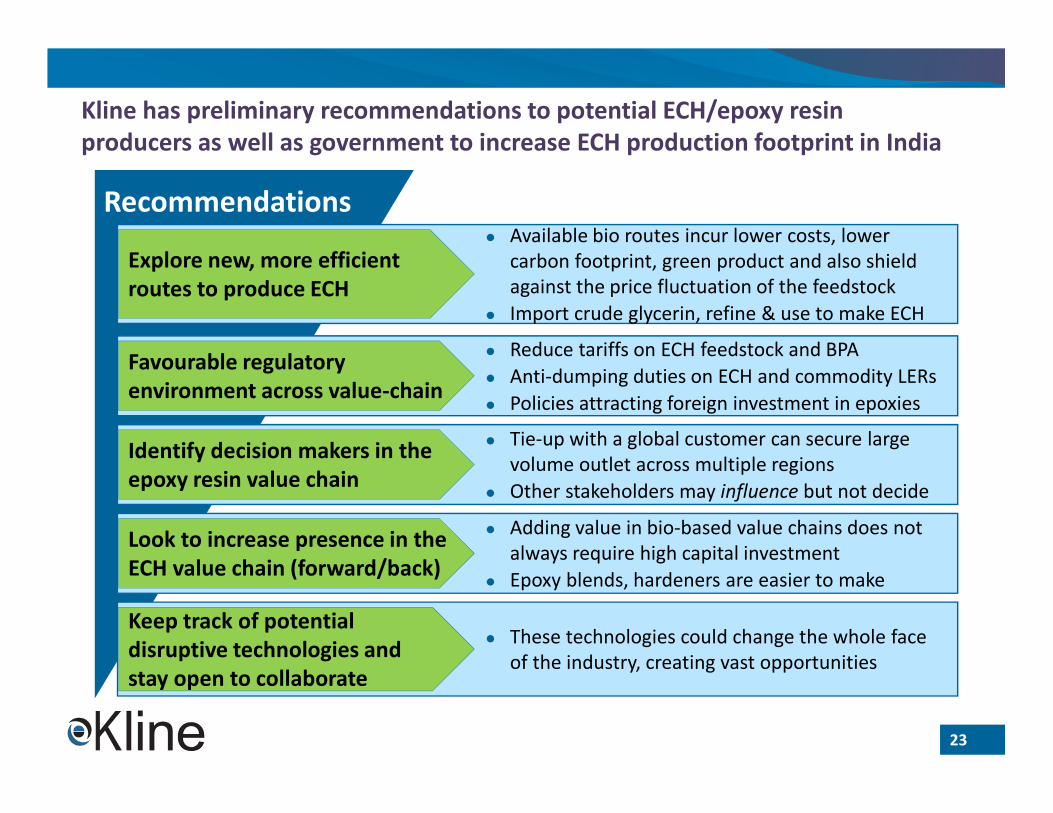

Kline has preliminary recommendations to potential ECH/epoxy resin

producers as well as government to increase ECH production footprint in India

� Available bio routes incur lower costs, lower

carbon footprint, green product and also shield

against the price fluctuation of the feedstock

� Import crude glycerin, refine & use to make ECH

Recommendations

� Reduce tariffs on ECH feedstock and BPA

� Anti-dumping duties on ECH and commodity LERs

� Policies attracting foreign investment in epoxies

� Tie-up with a global customer can secure large

volume outlet across multiple regions

� Other stakeholders may influence but not decide

� Adding value in bio-based value chains does not

always require high capital investment

� Epoxy blends, hardeners are easier to make

� These technologies could change the whole face

of the industry, creating vast opportunities

Explore new, more efficient

routes to produce ECH

Favourable regulatory

environment across value-chain

Identify decision makers in the

epoxy resin value chain

Look to increase presence in the

ECH value chain (forward/back)

Keep track of potential

disruptive technologies and

stay open to collaborate

GLOBAL HEADQUARTERS

Kline

35 Waterview Blvd.

Suite 305

Parsippany, NJ 07054

Phone: +1-973-435-6262

Fax: +1-973-435-6291

Kline is a worldwide consulting and research firm dedicated to providing the kind of insight and

knowledge that helps companies find a clear path to success. The firm has served the management

consulting and market research needs of organizations in the agrochemicals, chemicals, materials,

energy, life sciences, and consumer products industries for over 50 years.

For more information, visit www.KlineGroup.com.

www.klinegroup.com

DILIP CHANDWANI

Sr. Vice President

t. +1 201 887 6186

GAURAV NAGAR

Project Manager

t. +91 999 977 2372