options (1): concepts and uses - princeton...

TRANSCRIPT

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Chapter 8

Currency Options (1):Concepts and Uses

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Overview

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Overview

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Overview

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Overview

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Overview

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Overview

Overview

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Outline

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options

� Options: the holder has the right to{

buy (call option)sell (put option)

,{at (European-style option)up until (American style option)

an agreed-upon expiry

moment T, an agreed-upon quantity of a specied asset(“underlying”) at an agreed-upon price (strike or exerciseprice), from/to the writer of the option.

� Exercising (killing) the option: using the right, that is,buying (or selling) at the strike, at T or (for anAmerican-style:) possibly also early, i.e. before T

� Premium: the price paid (by the holder, to writer) for theoption, irrespective of exercising.Usually paid upfront, rarely at T (forward-style), sometimespartly via mark2market and partly final (futures-style).

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options (2)

� Intrinsic value or value dead: what the option wouldbe worth if the exercise decision would have to betaken now.

� In / at /out of the money (ITM, ATM, OTM): the strikerelative to the current price is such that immediateexercise would yield a positive / zero / negativecashflow.ITM means the intrinsic value is positive.

� Time value := premium - intrinsic value. Positive if themarket thinks that it’s better to postpone exercising.An ATM/OTM option’s premium is pure time value.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options (2)

� Intrinsic value or value dead: what the option wouldbe worth if the exercise decision would have to betaken now.

� In / at /out of the money (ITM, ATM, OTM): the strikerelative to the current price is such that immediateexercise would yield a positive / zero / negativecashflow.ITM means the intrinsic value is positive.

� Time value := premium - intrinsic value. Positive if themarket thinks that it’s better to postpone exercising.An ATM/OTM option’s premium is pure time value.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

A Young person’s Guide to FX Options (2)

� Intrinsic value or value dead: what the option wouldbe worth if the exercise decision would have to betaken now.

� In / at /out of the money (ITM, ATM, OTM): the strikerelative to the current price is such that immediateexercise would yield a positive / zero / negativecashflow.ITM means the intrinsic value is positive.

� Time value := premium - intrinsic value. Positive if themarket thinks that it’s better to postpone exercising.An ATM/OTM option’s premium is pure time value.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

IntroductionPuts and Calls

Some Jargon

Rational Exercising

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

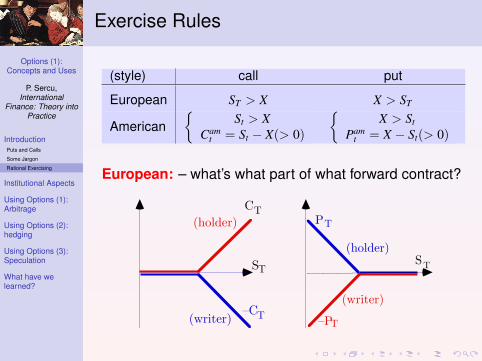

Exercise Rules

(style) call put

European ST > X X > ST

American{

St > XCam

t = St − X(> 0)

{X > St

Pamt = X − St(> 0)

European: – what’s what part of what forward contract?

P. Sercu and R. Uppal The International Finance Workbook page 8.5

• European Call: iff S T > X

! CT = Max(S T–X, 0) = (S T–X)+

C

–CT(writer)

T(holder)

ST

• American call: early exercise iff

Cat

m = (not !!) St – X > 0, i.e.

Value alive = Value dead > 0,

... otherwise it's better to sell the option(and not waste time value)

...• European Put: iff X > S T

! PT = Max(X–S T, 0) = (X–S T)+

–P

PT

(writer)

T

(holder)ST

• American put: early exercise iff

Pat

m = (not !!) X – St > 0, i.e.

Value alive = Value dead > 0

... otherwise it's better to sell the option(and not waste time value)

P. Sercu and R. Uppal The International Finance Workbook page 8.5

• European Call: iff S T > X

! CT = Max(S T–X, 0) = (S T–X)+

C

–CT(writer)

T(holder)

ST

• American call: early exercise iff

Cat

m = (not !!) St – X > 0, i.e.

Value alive = Value dead > 0,

... otherwise it's better to sell the option(and not waste time value)

...• European Put: iff X > S T

! PT = Max(X–S T, 0) = (X–S T)+

–P

PT

(writer)

T

(holder)ST

• American put: early exercise iff

Pat

m = (not !!) X – St > 0, i.e.

Value alive = Value dead > 0

... otherwise it's better to sell the option(and not waste time value)

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Outline

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Institutional stuff

� Traded v OTC

B Traded: Exchanges copied after futures: margin (for writer),clearing

B OTC: professionals

� Option on futures contract

B Call: if you exercise, you become long side of a contract withhistoric price X,never marked to market.

B Triggers MtM flow of ft,Tf − X.B Exercise rules: Eur:

Am:

� Futures-style options

B initial margin; daily MtM; final paymentB useful for speculatorsB price is [price of regular option]×(1 + rt,T)

B if on futures: convenient for put-call arbitrage

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Institutional stuff

� Traded v OTC

B Traded: Exchanges copied after futures: margin (for writer),clearing

B OTC: professionals

� Option on futures contract

B Call: if you exercise, you become long side of a contract withhistoric price X,never marked to market.

B Triggers MtM flow of ft,Tf − X.B Exercise rules: Eur:

Am:

� Futures-style options

B initial margin; daily MtM; final paymentB useful for speculatorsB price is [price of regular option]×(1 + rt,T)

B if on futures: convenient for put-call arbitrage

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Institutional stuff

� Traded v OTC

B Traded: Exchanges copied after futures: margin (for writer),clearing

B OTC: professionals

� Option on futures contract

B Call: if you exercise, you become long side of a contract withhistoric price X,never marked to market.

B Triggers MtM flow of ft,Tf − X.B Exercise rules: Eur:

Am:

� Futures-style options

B initial margin; daily MtM; final paymentB useful for speculatorsB price is [price of regular option]×(1 + rt,T)

B if on futures: convenient for put-call arbitrage

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Traded options: contract info (LIFFE)

8.2. INSTITUTIONAL ASPECTS OF OPTIONS MARKETS 279

Figure 8.3: Contract data for EUR/USD option (DEX) at LIFFE

Language EN FR NL PT Glossary Help Contact Sitemap

Search

Quotes Text

Currencies

News & Notices

Product information

Trading calendars

Wholesale trading

Publications

End of Day

Currencies > Currencies

News & Notices Product information

Contract specifications

US DOLLAR / EURO OPTIONS

Underlying :

Codes and classification

Mnemo DEX MEP AMS

Exercise type European Unit !

US Dollar / Euro Options

Unit of trading 100

Contract size USD 10.000

Expiry months 1) Initial lifetime: 1, 2, and 3 months Cycle: all months 2) Initial lifetime: 6, 9 and 12 months Cycle: March, June, September and December 3) Initial lifetime: 3 years Cycle: September

Quotation Euros per USD 100

Minimum price movement(tick size and value)

EUR 0.01 (= EUR 1 per contract)

Last trading day Trading in expiring currency derivatives have the EuroFX rate as their settlement basisand ends at 13.00 Amsterdam time on the third Friday of the expiry month, provided thisis a business day. If it is not, the previous business day will be the last day of trading.

Settlement EuroFX rate contracts: Cash settlement, based on the value of the Euro / US Dollar rateset by EuroFX at 13.00 Amsterdam time. For DEX, the inverse value of the EuroFX Euro/ US Dollar rate is used and rounded off to four decimal places.

Trading hours 9.00 – 17.25 Amsterdam time

Clearing LCH.Clearnet S.A.

Option style European style. Holders of long positions are not entitled to exercise their options before the exercisedate.

Exercise European

Last update 21/12/04

Trading Platform: LIFFE CONNECT®

Wholesale Service: Prof Trade Facility

Legal Notices:Prices are delayed at least by 15 minutes

Terms of Use, Privacy Policy and Trademarks

FTSEurofirst 80 5309.44 +0.06%

My Euronext Products & Prices Private investor News & Notices For our clients About us Tools & Services

Source http://www.euronext.com/trader/contractspecifications/derivative/wide/0,5786,1732 627733,00.html?euronextCode=DEX-AMS-OPT

someone else, his or her net obligation is zero. Another idea that option exchangeshave borrowed from futures markets is standardization:

• Expiration dates Originally, all options expired on the third Wednesday ofMarch, June, September, or December, and only the contracts with the threenearest expiration dates were traded. Nowadays this basic scheme, borrowedfrom futures markets, is often completed by extra short-lived options at the nearend (e.g. 1, 2, 3 months at LIFFE) and long-lived options at the far end (up to 3years, in LIFFE). Early exercise is possible until the last Saturday of the option’slife.

Formatted 09:31 on 26 May 2007 c!: P. Sercu, K.U.Leuven SB&E

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Traded options: price info (Neue Zurcher Zeitung)

DEVISENOPTIONEN

Strike Call Strike Put

Sep Dez Mar Jun Sep Dez Mar Jun$/Fr. Kassamittelkurs: 1.2235 100,000 $; Rp/$1.2000 2.60 3.06 3.41 3.65 1.2000 0.62 2.23 3.56 4.711.2250 1.07 1.90 2.34 2.66 1.2250 1.59 3.53 4.97 6.181.2500 0.41 1.12 1.57 1.91 1.2250 3.42 5.23 6.67 7.891.2750 0.25 0.67 1.05 1.37 1.2750 5.57 7.27 8.62 9.80C/Fr. Kassamittelkurs: 1.5781 100,000 C; Rp/C1.5750 2.60 3.06 3.41 3.65 1.5750 0.62 2.23 3.56 4.711.6000 0.23 0.37 0.47 0.53 1.6000 2.62 3.39 4.10 4.741.6250 0.22 0.25 0.30 0.34 1.6250 5.09 5.75 6.41 7.011.6500 0.21 0.23 0.26 0.27 1.6500 7.85 8.22 8.84 9.41C/$ Kassamittelkurs: 1.2917 100,000 $; Cent/$1.2750 2.74 4.01 5.12 6.02 1.2750 0.58 1.49 2.08 2.551.3000 1.02 2.61 3.73 4.66 1.3000 3.52 1.03 4.48 4.851.3250 0.42 1.63 2.66 6.54 1.3250 3.52 4.03 4.48 4.851.3500 0.26 1.01 1.87 2.66 1.3500 5.84 5.87 6.11 6.36

Quelle: UBS

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Outline

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

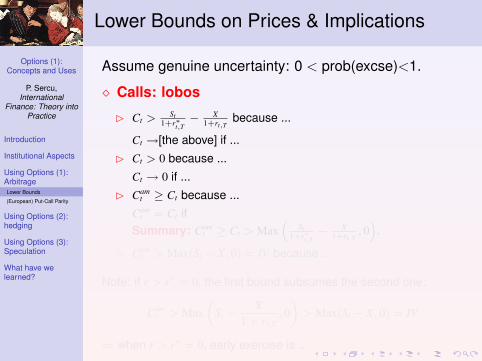

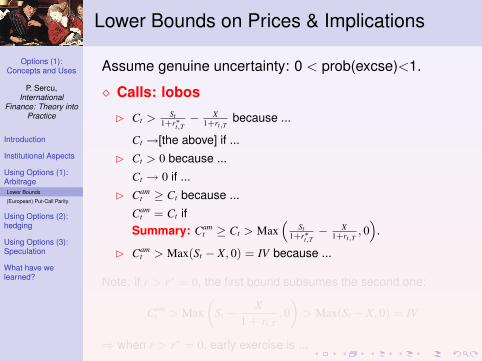

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(excse)<1.

� Calls: lobos

B Ct > St1+r∗t,T

− X1+rt,T

because ...

Ct →[the above] if ...B Ct > 0 because ...

Ct → 0 if ...B Cam

t ≥ Ct because ...Cam

t = Ct ifSummary: Cam

t ≥ Ct > Max“

St1+r∗t,T

− X1+rt,T

, 0”

.

B Camt > Max(St − X, 0) = IV because ...

Note: if r > r∗ = 0, the first bound subsumes the second one:

Camt > Max

„St −

X1 + rt,T

, 0«

> Max(St − X, 0) = IV

⇒ when r > r∗ = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Lower Bounds on Prices & Implications

Assume genuine uncertainty: 0 < prob(exrcise)<1.

� Puts: lobos

B Pt > X1+rt,T

− St1+r∗t,T

because ...

Pt →[the above] if ...B Pt > 0 because ...

Pt → 0 if ...B Pam

t ≥ Pt because ...Pam

t = Pt ifSummary: Pam

t ≥ Pt > Max“

X1+rt,T

− St1+r∗t,T

, 0”

.

B Pamt > Max(X − St, 0) = IV because ...

Note: if r∗ > r = 0, the first bound subsumes the second one:

Pamt > Max

„X − St

1 + r∗t,T, 0

«> Max(X − St, 0) = IV

⇒ when r∗ > r = 0, early exercise is ...

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

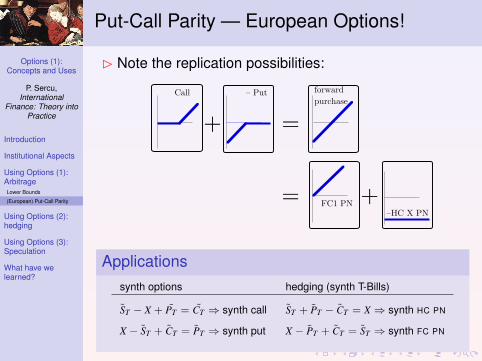

Put-Call Parity — European Options!

B Note the replication possibilities:

P. Sercu and R. Uppal The International Finance Workbook page 8.9

2.3. arbitrage2. Uses of options

• replication possibilities

+

+

=

=

Call – Put forward

purchase

FC1 PN–HC X PN

Synthetic options

S T – X + P T = C T ! synth call

X – S T + C T = P T ! synth put

Hedged positions

S T + P T – C T = X ! synth HCPN

X – P T + C T = S T ! synth FCPN

Applicationssynth options hedging (synth T-Bills)

ST − X + PT = CT ⇒ synth call ST + PT − CT = X ⇒ synth HC PN

X − ST + CT = PT ⇒ synth put X − PT + CT = ST ⇒ synth FC PN

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Put-Call Parity

� A no-arb relation: if at T: CT − PT = ST − X, by arb theremust be parity also at t:

Ct − Pt =Ft,T − X1 + rt,T

=St

1 + r∗t,T− X

1 + rt,T

(Put-Call Parity—Eur. options only!)

� Three implicationsB At-the-forward (ATF): if X = Ft,T then

Ct = Pt,

i.e. ATF puts and calls have equal pricesB At-the-money (ATM): if X = St then

Ct − Pt = Strt,T − r∗t, T

(1 + rt,T)(1 + r∗t,T)

>=<

0 if rt,T

>=<

r∗t, T.

i.e. ATM call (=upward potential) is more valuable than put(downward potential) if Ft,T > St (i.e. FC “strong”) & vv.

B As soon as we have a Call option price model, PCParityimplies the Put option pricing model.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Put-Call Parity

� A no-arb relation: if at T: CT − PT = ST − X, by arb theremust be parity also at t:

Ct − Pt =Ft,T − X1 + rt,T

=St

1 + r∗t,T− X

1 + rt,T

(Put-Call Parity—Eur. options only!)

� Three implicationsB At-the-forward (ATF): if X = Ft,T then

Ct = Pt,

i.e. ATF puts and calls have equal pricesB At-the-money (ATM): if X = St then

Ct − Pt = Strt,T − r∗t, T

(1 + rt,T)(1 + r∗t,T)

>=<

0 if rt,T

>=<

r∗t, T.

i.e. ATM call (=upward potential) is more valuable than put(downward potential) if Ft,T > St (i.e. FC “strong”) & vv.

B As soon as we have a Call option price model, PCParityimplies the Put option pricing model.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Put-Call Parity

� A no-arb relation: if at T: CT − PT = ST − X, by arb theremust be parity also at t:

Ct − Pt =Ft,T − X1 + rt,T

=St

1 + r∗t,T− X

1 + rt,T

(Put-Call Parity—Eur. options only!)

� Three implicationsB At-the-forward (ATF): if X = Ft,T then

Ct = Pt,

i.e. ATF puts and calls have equal pricesB At-the-money (ATM): if X = St then

Ct − Pt = Strt,T − r∗t, T

(1 + rt,T)(1 + r∗t,T)

>=<

0 if rt,T

>=<

r∗t, T.

i.e. ATM call (=upward potential) is more valuable than put(downward potential) if Ft,T > St (i.e. FC “strong”) & vv.

B As soon as we have a Call option price model, PCParityimplies the Put option pricing model.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):ArbitrageLower Bounds

(European) Put-Call Parity

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Put-Call Parity

� A no-arb relation: if at T: CT − PT = ST − X, by arb theremust be parity also at t:

Ct − Pt =Ft,T − X1 + rt,T

=St

1 + r∗t,T− X

1 + rt,T

(Put-Call Parity—Eur. options only!)

� Three implicationsB At-the-forward (ATF): if X = Ft,T then

Ct = Pt,

i.e. ATF puts and calls have equal pricesB At-the-money (ATM): if X = St then

Ct − Pt = Strt,T − r∗t, T

(1 + rt,T)(1 + r∗t,T)

>=<

0 if rt,T

>=<

r∗t, T.

i.e. ATM call (=upward potential) is more valuable than put(downward potential) if Ft,T > St (i.e. FC “strong”) & vv.

B As soon as we have a Call option price model, PCParityimplies the Put option pricing model.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

Outline

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

Using Options 2: hedging

� One-edged hedging of contractual exposure

P. Sercu and R. Uppal The International Finance Workbook page 8.5

1.3. Advantage as a hedge instrument1. Basics of options

• Forward hedge: eliminates all uncertainty—downward & upside

• Option: buy insurance against bad rates (: S below X in case of e.g. A/R; above X in caseof e.g. A/P)

C

hedged A/P

T

A/P

ST0

P

hedged A/R

T

A/R

TS0

� “Hedging exposures with big quantity risks”B Examples: Int tender, risky A/R etc, risky stock investments,

reinsurance,B “Advantage”: no risk of two bad tidings—losing on the exposed

position and on the hedge: OTM option not exercisedB Dubious argument: option’s added flexibility is still 100% tied to

Xrisk, not to quantity risk

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

Using Options 2: hedging

� One-edged hedging of contractual exposure

P. Sercu and R. Uppal The International Finance Workbook page 8.5

1.3. Advantage as a hedge instrument1. Basics of options

• Forward hedge: eliminates all uncertainty—downward & upside

• Option: buy insurance against bad rates (: S below X in case of e.g. A/R; above X in caseof e.g. A/P)

C

hedged A/P

T

A/P

ST0

P

hedged A/R

T

A/R

TS0

� “Hedging exposures with big quantity risks”B Examples: Int tender, risky A/R etc, risky stock investments,

reinsurance,B “Advantage”: no risk of two bad tidings—losing on the exposed

position and on the hedge: OTM option not exercisedB Dubious argument: option’s added flexibility is still 100% tied to

Xrisk, not to quantity risk

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

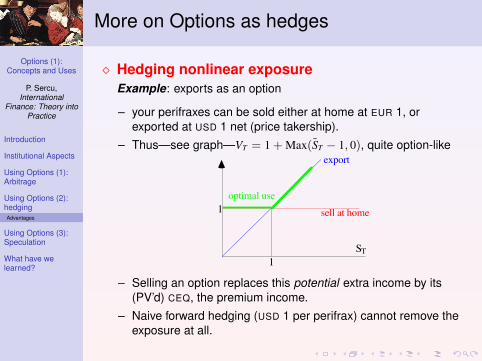

More on Options as hedges

� Hedging nonlinear exposureExample: exports as an option

– your perifraxes can be sold either at home at EUR 1, orexported at USD 1 net (price takership).

– Thus—see graph—VT = 1 + Max(ST − 1, 0), quite option-like

P. Sercu and R. Uppal The International Finance Workbook page 8.7

2. Uses of options 2.1 hedging

• To hedge away just the downside, keeping the upside risk.

But: bear in mind that one pays a price for this.

• "To hedge FC positions with risk (e.g. international tender, international reinsurance)"

But: the extra flexibility offered by options is still S-related, not Q-related.

• To hedge non-linear exposures (usually operating exposures)

Example: your prioblaphoxes can be soldat home at EUR 1, or exported at USD 1net (price takership). Thus, VT = 1 +Max(ST – 1, 0).

• Selling an option replaces this potentialextra income by its (PV-ed) CEQ, thepremium income.

• forward hedging cannot remove theexposure at all.

sell at home

export

optimal use

1

ST

1

– Selling an option replaces this potential extra income by its(PV’d) CEQ, the premium income.

– Naive forward hedging (USD 1 per perifrax) cannot remove theexposure at all.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

More on Options as hedges

� Hedging nonlinear exposureExample: exports as an option

– your perifraxes can be sold either at home at EUR 1, orexported at USD 1 net (price takership).

– Thus—see graph—VT = 1 + Max(ST − 1, 0), quite option-like

P. Sercu and R. Uppal The International Finance Workbook page 8.7

2. Uses of options 2.1 hedging

• To hedge away just the downside, keeping the upside risk.

But: bear in mind that one pays a price for this.

• "To hedge FC positions with risk (e.g. international tender, international reinsurance)"

But: the extra flexibility offered by options is still S-related, not Q-related.

• To hedge non-linear exposures (usually operating exposures)

Example: your prioblaphoxes can be soldat home at EUR 1, or exported at USD 1net (price takership). Thus, VT = 1 +Max(ST – 1, 0).

• Selling an option replaces this potentialextra income by its (PV-ed) CEQ, thepremium income.

• forward hedging cannot remove theexposure at all.

sell at home

export

optimal use

1

ST

1

– Selling an option replaces this potential extra income by its(PV’d) CEQ, the premium income.

– Naive forward hedging (USD 1 per perifrax) cannot remove theexposure at all.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

More on Options as hedges

� Hedging nonlinear exposureExample: exports as an option

– your perifraxes can be sold either at home at EUR 1, orexported at USD 1 net (price takership).

– Thus—see graph—VT = 1 + Max(ST − 1, 0), quite option-like

P. Sercu and R. Uppal The International Finance Workbook page 8.7

2. Uses of options 2.1 hedging

• To hedge away just the downside, keeping the upside risk.

But: bear in mind that one pays a price for this.

• "To hedge FC positions with risk (e.g. international tender, international reinsurance)"

But: the extra flexibility offered by options is still S-related, not Q-related.

• To hedge non-linear exposures (usually operating exposures)

Example: your prioblaphoxes can be soldat home at EUR 1, or exported at USD 1net (price takership). Thus, VT = 1 +Max(ST – 1, 0).

• Selling an option replaces this potentialextra income by its (PV-ed) CEQ, thepremium income.

• forward hedging cannot remove theexposure at all.

sell at home

export

optimal use

1

ST

1

– Selling an option replaces this potential extra income by its(PV’d) CEQ, the premium income.

– Naive forward hedging (USD 1 per perifrax) cannot remove theexposure at all.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedgingAdvantages

Using Options (3):Speculation

What have welearned?

Piecewise Linear Approximations & Options

S_T Cash Flow Approx1 Approx2

0.90 100.0 94.0 100.0

0.91 95.5 94.0 97.5

0.92 92.0 94.0 95.00.93 89.5 94.0 92.5

0.94 88.0 94.0 90.0

0.95 87.5 94.0 87.5

0.96 88.0 94.0 90.00.97 89.5 94.0 92.5

0.98 92.0 94.0 95.0

0.99 95.5 94.0 97.5

1.00 100.0 94.0 100.01.01 105.5 104.0 110.0

1.02 112.0 114.0 120.0

1.03 119.5 124.0 130.0

1.04 128.0 134.0 140.0

1.05 137.5 144.0 150.01.06 148.0 154.0 160.0

1.07 159.5 164.0 170.0

1.08 172.0 174.0 180.0

1.09 185.5 184.0 190.01.10 200.0 194.0 200.0

Non-constant exposure

0.0

50.0

100.0

150.0

200.0

250.0

0.90 0.95 1.00 1.05 1.10

S_T

Cash

Flo

w

Series1

Series2

Series3

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Outline

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Speculating on S or on σs

� Speculation on S

B Bulls buy calls or sell puts, Bears buy puts or sell callsB Buying options limits your risk to the premium

... but the chance of losing all is usually big (≈50%, ATM)B Selling options is risky

� Speculating on volatility

B Wait till T and cash in big-time—or so you hope

P. Sercu and R. Uppal The International Finance Workbook page 8.8

2.2. speculation2. Uses of options

• what is speculation?• means giving up diversification because of extra-ordinary expected return• reflects disagreement with market prices: over- or undervalued assets

• speculation with options• speculating à la hausse/baisse with limited

risk: max loss is …But bear in mind: still a large prob of losingthe entire initial investment!

• speculation on volatility by buying/sellingstraddles/strangles. See table below and graph.⇒ Buy both put and call because … strangle

straddle

prob(0.9) prob(1.0) prob(1.1) expectation for C, P (X=1)your opinion 0.25 0.50 0.25 Eyou(C or P) = 0.025mkt opinion 0.15 0.70 0.15 Emkt(C or P) = 0.015

B or cash in as soon as the market has seen the error of its waysand revalued the options—or so you hope

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Speculating on S or on σs

� Speculation on S

B Bulls buy calls or sell puts, Bears buy puts or sell callsB Buying options limits your risk to the premium

... but the chance of losing all is usually big (≈50%, ATM)B Selling options is risky

� Speculating on volatility

B Wait till T and cash in big-time—or so you hope

P. Sercu and R. Uppal The International Finance Workbook page 8.8

2.2. speculation2. Uses of options

• what is speculation?• means giving up diversification because of extra-ordinary expected return• reflects disagreement with market prices: over- or undervalued assets

• speculation with options• speculating à la hausse/baisse with limited

risk: max loss is …But bear in mind: still a large prob of losingthe entire initial investment!

• speculation on volatility by buying/sellingstraddles/strangles. See table below and graph.⇒ Buy both put and call because … strangle

straddle

prob(0.9) prob(1.0) prob(1.1) expectation for C, P (X=1)your opinion 0.25 0.50 0.25 Eyou(C or P) = 0.025mkt opinion 0.15 0.70 0.15 Emkt(C or P) = 0.015

B or cash in as soon as the market has seen the error of its waysand revalued the options—or so you hope

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Speculating on S or on σs

� Speculation on S

B Bulls buy calls or sell puts, Bears buy puts or sell callsB Buying options limits your risk to the premium

... but the chance of losing all is usually big (≈50%, ATM)B Selling options is risky

� Speculating on volatility

B Wait till T and cash in big-time—or so you hope

P. Sercu and R. Uppal The International Finance Workbook page 8.8

2.2. speculation2. Uses of options

• what is speculation?• means giving up diversification because of extra-ordinary expected return• reflects disagreement with market prices: over- or undervalued assets

• speculation with options• speculating à la hausse/baisse with limited

risk: max loss is …But bear in mind: still a large prob of losingthe entire initial investment!

• speculation on volatility by buying/sellingstraddles/strangles. See table below and graph.⇒ Buy both put and call because … strangle

straddle

prob(0.9) prob(1.0) prob(1.1) expectation for C, P (X=1)your opinion 0.25 0.50 0.25 Eyou(C or P) = 0.025mkt opinion 0.15 0.70 0.15 Emkt(C or P) = 0.015

B or cash in as soon as the market has seen the error of its waysand revalued the options—or so you hope

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?

Speculating on S or on σs

� Speculation on S

B Bulls buy calls or sell puts, Bears buy puts or sell callsB Buying options limits your risk to the premium

... but the chance of losing all is usually big (≈50%, ATM)B Selling options is risky

� Speculating on volatility

B Wait till T and cash in big-time—or so you hope

P. Sercu and R. Uppal The International Finance Workbook page 8.8

2.2. speculation2. Uses of options

• what is speculation?• means giving up diversification because of extra-ordinary expected return• reflects disagreement with market prices: over- or undervalued assets

• speculation with options• speculating à la hausse/baisse with limited

risk: max loss is …But bear in mind: still a large prob of losingthe entire initial investment!

• speculation on volatility by buying/sellingstraddles/strangles. See table below and graph.⇒ Buy both put and call because … strangle

straddle

prob(0.9) prob(1.0) prob(1.1) expectation for C, P (X=1)your opinion 0.25 0.50 0.25 Eyou(C or P) = 0.025mkt opinion 0.15 0.70 0.15 Emkt(C or P) = 0.015

B or cash in as soon as the market has seen the error of its waysand revalued the options—or so you hope

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

Outline

IntroductionPuts and CallsSome Jargon: IV, I-A-OTM, TVRational Exercising

Institutional Aspects

Using Options (1): ArbitrageLower Bounds(European) Put-Call Parity

Using Options (2): hedgingAdvantages

Using Options (3): Speculation

What have we learned?SummaryAre Options too Expensive?

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

What have we learned in this chapter?

� Chopped-up Forward Contracts

B European options provide the holder with the positive part ofthe payoff of the comparable forward contract—below X for theput, above X for the call. The writer gets the negative parts.

B Options being zero-sum games, the parties can agree only ifthe holder pays the writer a premium, which should be therisk-adjusted and discounted expected value.

� Lower Bounds on prices.

B As a European option provides the nice part of the comparableforwards, the value of the latter is a lower bound on the Eoption’s price.

B Zero is another lower bound.B American options are worth at least the E option, and also at

least the intrinsic value.For some interest-rate combinations the latter bound can neverbe reached, or is unlikely to ever be reached.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

What have we learned in this chapter?

� Chopped-up Forward Contracts

B European options provide the holder with the positive part ofthe payoff of the comparable forward contract—below X for theput, above X for the call. The writer gets the negative parts.

B Options being zero-sum games, the parties can agree only ifthe holder pays the writer a premium, which should be therisk-adjusted and discounted expected value.

� Lower Bounds on prices.

B As a European option provides the nice part of the comparableforwards, the value of the latter is a lower bound on the Eoption’s price.

B Zero is another lower bound.B American options are worth at least the E option, and also at

least the intrinsic value.For some interest-rate combinations the latter bound can neverbe reached, or is unlikely to ever be reached.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

What have we learned in this chapter? cont’d

� Put-Call Parity

B As (European!) puts & calls are bits & pieces of forwards, onecan replicate a forward from options, or one option fromforwards and the other option; or one can hedge.

B Traders do this to balance their books or fill holes in the market.B The resulting no-arb constraint is called Put-Call Parity.

� Using options

B Being broken-up forwards, options can be used for one-edgedhedging, or hedging of non-constant exposures

B Because of its convexity an option can also be used tospeculate on volatility, not just on the sign of ∆S.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

What have we learned in this chapter? cont’d

� Put-Call Parity

B As (European!) puts & calls are bits & pieces of forwards, onecan replicate a forward from options, or one option fromforwards and the other option; or one can hedge.

B Traders do this to balance their books or fill holes in the market.B The resulting no-arb constraint is called Put-Call Parity.

� Using options

B Being broken-up forwards, options can be used for one-edgedhedging, or hedging of non-constant exposures

B Because of its convexity an option can also be used tospeculate on volatility, not just on the sign of ∆S.

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

Are Options too Expensive?

� The most expensive option is cheap

B The most expensive option is a VeryDeep ITM one,B and it is priced as a forward,B which cannot be controversially expensive.

� Outrageous Bid-ask Spreads?B Bid-Ask for options is easily 5% or more. but ...B cannot be compared to spread on forwards, since the premium

is a levered net value while the forward is the price of one legExample: If Ft = 100 and Ft0 = 98 and r ≈ 0 then the market value is2; and a 0.10% spread on F would already be a 5% spread on 2.

B In addition, hedging the option is much more costly and risky,to the bank, than hedging a forward

� Lack of Understanding

B You need to read the next chapter

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

Are Options too Expensive?

� The most expensive option is cheap

B The most expensive option is a VeryDeep ITM one,B and it is priced as a forward,B which cannot be controversially expensive.

� Outrageous Bid-ask Spreads?B Bid-Ask for options is easily 5% or more. but ...B cannot be compared to spread on forwards, since the premium

is a levered net value while the forward is the price of one legExample: If Ft = 100 and Ft0 = 98 and r ≈ 0 then the market value is2; and a 0.10% spread on F would already be a 5% spread on 2.

B In addition, hedging the option is much more costly and risky,to the bank, than hedging a forward

� Lack of Understanding

B You need to read the next chapter

Options (1):Concepts and Uses

P. Sercu,International

Finance: Theory intoPractice

Introduction

Institutional Aspects

Using Options (1):Arbitrage

Using Options (2):hedging

Using Options (3):Speculation

What have welearned?Summary

Are Options too Expensive?

Are Options too Expensive?

� The most expensive option is cheap

B The most expensive option is a VeryDeep ITM one,B and it is priced as a forward,B which cannot be controversially expensive.

� Outrageous Bid-ask Spreads?B Bid-Ask for options is easily 5% or more. but ...B cannot be compared to spread on forwards, since the premium

is a levered net value while the forward is the price of one legExample: If Ft = 100 and Ft0 = 98 and r ≈ 0 then the market value is2; and a 0.10% spread on F would already be a 5% spread on 2.

B In addition, hedging the option is much more costly and risky,to the bank, than hedging a forward

� Lack of Understanding

B You need to read the next chapter