oracle’s dilemma: applications unlimited - rimini...

TRANSCRIPT

Forrester research, Inc., 60 acorn Park drive, Cambridge, ma 02140 Usa

Tel: +1 617.613.6000 | Fax: +1 617.613.5000 | www.forrester.com

Oracle’s Dilemma: Applications Unlimited Versus Oracle Fusion Applicationsby William Band, andrew Bartels, Paul d. Hamerman, and China martens, February 11, 2013

For: CIo Professionals

key TakeaWays

oracle’s application Revenues have hit pockets of Weakness in The past Two yearsIn recent quarters, Oracle’s application revenue growth has underperformed both the overall soft ware market and SAP, resulting from slowing growth in existing apps and too little revenue from its Oracle Fusion Applications. Recent acquisitions of SaaS companies (e.g., Taleo and RightNow Technologies) are not large enough to take up the slack.

oracle Clients show limited interest in or adoption of oracle Fusion applicationsIf Oracle Fusion Applications are the future for Oracle, most Oracle users haven’t gotten the memo. Of the Oracle clients we surveyed, 65% had no plans to implement Oracle Fusion Applications, and another 24% did not know if they would. Clients reported lack of clarity about Oracle’s app strategy and Fusion’s immaturity as the biggest barriers.

To Restore app Revenue growth, oracle Will need To kick-start Fusion demandOracle will need to increase client interest in Fusion or de-emphasize it as another app in Applications Unlimited. Th e current middle path of talking about Fusion while providing no disincentives against clients staying on existing apps will lead to mediocre growth. Our bet is that Oracle will push Oracle Fusion Applications.

© 2013, Forrester Research, Inc. All rights reserved. Unauthorized reproduction is strictly prohibited. Information is based on best available resources. Opinions reflect judgment at the time and are subject to change. Forrester®, Technographics®, Forrester Wave, RoleView, TechRadar, and Total Economic Impact are trademarks of Forrester Research, Inc. All other trademarks are the property of their respective companies. To purchase reprints of this document, please email [email protected]. For additional information, go to www.forrester.com.

For CIo ProFessIonals

Why Read This RepoRT

Oracle faces a strategic dilemma, and how it responds to this dilemma will present the CIOs at its clients with some tough choices. Oracle Fusion Applications — Oracle’s new generation of enterprise applications, as well as the focus of much Oracle innovation and development — have had low levels of adoption by existing Oracle customers, in part, because Oracle’s Applications Unlimited policy has provided them with little incentive to migrate. Oracle’s organic revenue growth has slowed over the past year or so as its existing products age, and it has needed acquisitions of leading software-as-a-service (SaaS) vendors like RightNow Technologies and Taleo to bolster its app revenues. Oracle has not wavered in its commitment to continue to support existing applications customers indefinitely; however, the company is clearly now more aggressive in promoting Oracle Fusion Applications and cloud deployment models (including private cloud and SaaS) to its customers. This report examines the Applications Unlimited versus Oracle Fusion Applications quandary Oracle faces, framed by the results of a Forrester survey of Oracle customers and Oracle’s recent financial results.

Table of Contents

something’s happening With oracle apps, What it is ain’t exactly Clear

applications Unlimited slows Customer Move To Fusion applications

reCommendaTIons

oracle Clients: Watch For More pressure To Move To Fusion applications

WHaT IT means

it’s Make-or-Break Time For oracle’s applications Business

supplemental Material

notes & resources

Forrester conducted an online survey of 139 clients who self-identified as users of oracle applications.

related research documents

selecting a services Provider For Your oracle Fusion applications ProjectJune 8, 2012

Understand oracle Better To marshal maximum software negotiation leverageapril 27, 2012

The state of erP In 2011: Customers Have more options In spite of market Consolidationmay 2, 2011

oracle’s dilemma: applications Unlimited Versus oracle Fusion applicationsoracle Customers Face a Choice: stay With apps They Have and miss out on Innovation or make The Painful switch To Fusionby William Band, andrew Bartels, Paul d. Hamerman, and China martenswith John r. rymer, Christopher mines, Jamie Warner, and Joanna Clark

2

18

7

18

17

FeBrUarY 11, 2013

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 2

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

soMeThing’s happening WiTh oRaCle apps, WhaT iT is ain’T exaCTly CleaR

Forrester is writing a series of reports that will take a temperature check of the enterprise application market during this period of rising interest in software-as-a-service through the lens of the leading business applications vendors. We are starting with Oracle, because of its size and scale in this market. Oracle has approximately 65,000 applications clients and offers a wide range of application suites, including the Oracle E-Business Suite, Oracle PeopleSoft, Oracle JD Edwards EnterpriseOne, and Oracle JD Edwards World. It also has specific application product suites like Oracle Agile in product life-cycle management, Oracle ATG in eCommerce, Oracle Hyperion in business intelligence, Oracle Primavera in project portfolio management, and Oracle Siebel in customer relationship management (CRM), plus recently acquired RightNow in CRM and Taleo in human capital management (HCM). Oracle also has a number of vertical applications in banking (formerly, i-flex solutions), retail management (formerly, Retek), and utilities (formerly, SPL WorldGroup). Oracle’s total application revenues (excluding software services) was $7.8 billion in calendar year 2011, and we estimated it was $8.4 billion in calendar year 2012, making it second in size in the applications market to SAP. Oracle’s app revenue also represents more than one-third of Oracle’s total software revenues and helps drive sales of Oracle’s middleware and hardware products.

We are also starting with Oracle because strange things have been happening over the past year and a half with Oracle’s applications revenues. Specifically, Oracle reported sharp declines in its application license revenues in Q4 2011 and Q1 2012, followed by a big but temporary bounce back in Q2 2012. Oracle’s two recent earnings release (Oracle’s fiscal Q1 2013, ending on August 31, 2012, and its Q2 2013 ending on November 30, 2012) no longer reported application revenues separately, so we don’t know for sure whether Oracle apps license revenue rose or fell in that quarter. However, according to its 10(Q) filings, Oracle’s software license revenues fell by 3% in calendar Q3, before rising by 10.8% in calendar Q4. Because Oracle’s app license revenues had grown less than its database and middleware license revenues through Q2, it is likely that this pattern continued in the rest of 2012. Oracle’s total application revenue (including maintenance and subscriptions as well as license revenues) has been in positive growth territory the entire time, but growth has been erratic and only twice gotten above 10% over the past five quarters (see Figure 1).

Some may argue that a vendor’s revenue performance is of little interest or importance to that vendor’s clients, as long as they have confidence that the vendor will keep supporting and enhancing the vendor’s products. But our view is that vendor revenue growth does matter to CIOs who use that vendor, because weak revenue performance should raise questions about the strength of those vendor commitments. If the vendor’s revenues from the products that a firm uses are flat or declining, there is a risk that the vendor will start treating those products as a cash cow, milking maintenance revenues and cutting back in its investment in enhancing and supporting them. That risk rises when the vendor has developed or acquired new products for which it can generate new revenues by pushing clients to migrate from old apps to the new ones.

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 3

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

For these reasons, we start our analysis with a question: Why have Oracle’s application revenues been so erratic and so often weak? Part of the answer is the broader software environment, where growth in revenues for many software vendors has slowed, especially growth measured in US dollars. But a large part of the answer is unique to Oracle. Was there a disruption in Oracle’s sales teams and activities in this period? Or is it the result of a more fundamental issue in its application product portfolio? Based on a survey of Oracle users, we think it’s the latter. Specifically, our survey strongly suggests that there’s a conflict between Oracle’s Applications Unlimited policy — which allows users of the many applications in Oracle’s product portfolio to continue to use them indefinitely — and its next-generation Fusion Application products.

oracle’s application Revenues are Riding a Roller Coaster

Oracle’s change in how it reports its revenues — from reporting application revenues and database and middleware revenues separately, with license and maintenance revenues for both through Q2 2012, to reporting that combines application and middleware license, maintenance, and subscriptions revenues since then — does complicate analysis of what is happening with Oracle’s application business. But sifting through its earnings statements and SEC filings and making some educated guesses, here are the trends that we see:1

■ Total Oracle application revenues have slowed, with maintenance softening the slowdown. When Oracle still reported application revenues separately, license revenue growth slowed from around 18% in the first half of 2011 to 7.5% in Q3 2011, then fell by 11% in Q4 2011 and by 5.5% in Q1 2012 before rising by 11% in Q2 2012. Since then, we estimate that its application license revenues fell by 5% in Q3, then rose by 11% in Q4 2012. Combined license and maintenance had a similar seesaw pattern. Because maintenance revenues are less volatile, the growth for total app revenues was not as high as for license revenues in the first three quarters of 2011; the slowdown was not as dramatic in Q4 2011, Q1 2012, and Q3 2012; and the bounce-backs in Q2 and Q4 2012 were milder.

■ Without Oracle’s recent acquisitions, its apps revenues would have even weaker growth. Among the many acquisitions that Oracle has made in the past year and a half, two were acquisitions of SaaS apps vendors with publicly reported revenues for the periods prior to the acquisition: RightNow, a provider of customer service automation software, in October 2011 and Taleo, a vendor of recruitment and talent management apps, in February 2012. To get a sense of how Oracle’s organic revenues performed without those acquisitions, we added these vendors’ revenues to those of Oracle’s in the base quarters of Q4 2010 to Q4 2011 from which year-over-year growth is measured.2 The resulting picture of how Oracle’s application revenues would have performed if it had owned those vendors throughout the period is a useful proxy for growth in Oracle’s core application portfolio and shows that the decline in Oracle’s application revenues in Q4 2011 to Q4 2012 was even weaker than growth in recorded revenues: 1.9% in Q1 2012 (versus reported growth of around 4%), 5.6% in Q2 2012 (instead of 11.2%), an estimated

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 4

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

-3.9%% in Q3 (instead of an unadjusted 3.9%), and 6.4% in Q4 2012 (instead of an unadjusted 11.2%) (see Figure 2).

What has caused Oracle’s application revenue growth to become so variable and often weak? Certainly, external forces are a factor, especially the stronger dollar, a recession in Europe, and slowing growth in other markets.

■ A shift from a weak dollar in 2011 to a strong dollar in 2012 has hurt Oracle’s app revenues. For a US-based vendor like Oracle, the shift from a relatively weak dollar in the first three quarters of 2011 to a much stronger dollar in 2012 means that currency-adjusted growth rates in 2011 were 4 to 7 percentage points lower in Q2 2012 and Q3 2012 than reported growth; the strong dollar since then has meant that Oracle’s constant-currency growth rates were higher than reported growth by about 1 percentage point in both Q4 2011 and Q1 2012, by 4 percentage points in Q2 2012, and by 5 percentage points in Q3 2012. Not until Q4 2012 did reported and constant currency growth rates become the same. So, adjusting for currency changes, Oracle’s app revenue growth in Q4 2011 and Q1 2012 was in the 1% to 3% range, compared with growth rates on a similar basis of 15% in Q2 2012 and, most likely, in the 8% to 9% range in the second half of 2012.

■ Weaker economic growth in Europe and elsewhere has also hurt Oracle’s app revenues. In Q1 2012, for example, Oracle’s application license revenues for Europe were down by almost 20%, while its application licenses revenues for the Americas were up by about as much. A similar gap occurred in Q2 2012, when Oracle’s app license revenues in Europe rose just 3% while app license revenues in the Americas rose by 36%. And in Q3 2012, Oracle’s total software license and subscriptions revenues in Europe fell by 8% while its global revenues rose by 5%. Only in Q4 2012 did Europe cease to be a drag on Oracle’s revenues, with its 10% growth in European license and subscriptions revenues matching its 10% global software revenue growth.

Still, only part of Oracle’s application slump can be attributed to external factors. SAP, Oracle’s biggest competitor in the application market, has been subject to the same factors, yet it has generally performed better over the past two years than Oracle in applications.3 Admittedly, SAP does not split its revenues between database and middleware versus applications as Oracle used to do, so it is hard to show an exact comparison between SAP’s app business and Oracle’s app business. Still, because 70% or more of SAP’s revenues come from applications rather than SAP’s app server (NetWeaver), database (Sybase), and business intelligence (BusinessObjects) products, a fair comparison with Oracle’s apps business can be made using SAP’s total software product growth rates (adjusted for its acquisition of SaaS talent management apps vendor SuccessFactors).4 And on that basis, except in Q2 2012, growth in Oracle’s app business has lagged behind growth in SAP’s revenues when both sets of revenues are in a common currency.5 We show this comparison using both euros in deference to SAP and in US dollars in deference to Oracle (see Figure 3).

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 5

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Figure 1 Oracle's License Revenues, Especially For Apps, Have Been On A Roller Coaster

Source: Forrester Research, Inc.82763

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

Oracle applicationsrevenue*

Oracle softwarelicense revenue

Source: Oracle earning releases Note: Because Oracle in its latest earnings releases stopped reporting revenues for its applications, Forrester has estimated these numbers for Q3 2012 and Q4 2012 based on its total software license and subscription revenues.

*Forrester estimates for application and application license revenues after Q2 2012

Percentage change from prior year in US dollars

Q12011

Q22011

Q32011

Q42011

Q42012*

Q32012*

Q12012

Q22012

Oracle applicationlicense revenue

Figure 2 Oracle’s App Revenue Growth Looks Worse When Acquisitions Are Counted In Base Period

Source: Forrester Research, Inc.82763

Oracle appsrevenue

Oracle’s apps revenuewith RightNow’s and Taleo’shistoric revenues included inthe base period

Source: Oracle, RightNow, and Taleo earnings releases*Forrester estimates for application revenues after Q2 2012

Percentage change from prior year in US dollars

Q12011

Q22011

Q32011

Q42011

Q42012*

Q32012*

Q12012

Q22012

-5%

0%

5%

10%

15%

20%

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 6

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Figure 3 Oracle’s App Revenue Growth Has Mostly Lagged Behind SAP’s

Source: Forrester Research, Inc.82763

SAP plusSuccessFactors

Oracle plusRightNow and Taleo

Percentage change from prior year in global application revenues ineuros adjusted for acquisitions

Q12011

Q22011

Q32011

Q42011

Q42012

Q32012

Q12012

Q22012

Comparing euro growth in Oracle application revenues versus SAP revenues3-1

SAP plusSuccessFactors

Oracle plusRightNow and Taleo

Source: Oracle, RightNow, Taleo, SAP, and SuccessFactors earnings releases

Percentage change from prior year in global application revenues inUS dollars adjusted for acquisitions

Q12011

Q22011

Q32011

Q42011

Q42012

Q32012

Q12012

Q22012

Comparing US dollar growth in Oracle application revenues versus SAP revenues3-2

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

5%

10%

15%

20%

25%

30%

35%

40%

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 7

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

appliCaTions UnliMiTed sloWs CUsToMeR MoVe To FUsion appliCaTions

Internal factors that drive financial results include sales incentives, motivation, and management; marketing resources; and the fit of product portfolio against customer needs. Based on our analysis of Oracle’s apps product portfolio, we believe that significant tensions exist between older and newer products.

Our theory: Too many Oracle applications clients are standing pat with older product lines and ignoring migrations to Oracle’s newer product lines — Fusion Applications and Oracle’s SaaS offerings. The result? While Oracle’s portfolio of applications continues to spin off a steady stream of maintenance revenues, customers’ comfort level with their current apps is hurting new license sales. The growth in Oracle Fusion Applications is coming mostly from sales to existing Oracle clients of one or several Oracle Fusion Applications modules rather than full-blown Oracle Fusion Applications replacement sales to either incumbent or new Oracle customers; as such, it is too small to add much to total application revenues. Moreover, as noted above, most of the reported growth in Oracle’s application revenues has come from its acquisitions of SaaS vendors like RightNow and Taleo.

To test our theory, we surveyed 139 Forrester clients who run all or part of their businesses on Oracle applications.6 More than half used Oracle PeopleSoft; two-fifths or more used Oracle Hyperion, Oracle E-Business Suite, or Oracle Siebel; about one-quarter used Oracle JD Edwards; and 3% to 12% used other apps like Agile, ATG, Primavera, and RightNow (see Figure 4).

We were particularly interested in how these Oracle customers viewed their next app investment — were they planning to stay with their on-premises apps and trade up to one of the latest releases; were they interested in Oracle Fusion Applications, which are available as on-premises, hosted, and SaaS deployment options; or were they going with a mix of one or more of those choices. Their responses represent mixed directions for Oracle’s future app revenue picture (see Figure 5). Survey respondents encouraged to provide multiple responses said they will do one or more of the following:

■ Upgrade what they have. The majority of respondents (64%) intend to upgrade to the next version of the Oracle apps they are currently using, translating to continued growth in Oracle maintenance revenue and perhaps an uptick in sales of newer Oracle Exadata servers and middleware.7 The flipside is once that app migration is done along with any accompanying hardware or middleware refresh, firms have likely exhausted their resources — money, time, and people — for any major app investments for the next five years or so.8

■ Opt for other Oracle apps. Compared with upgrading to the next release of their current Oracle app, the appetite among respondents for consuming other Oracle apps was comparatively low — 11% of respondents plan to move to an Oracle SaaS offering, and 8% intend to migrate to a packaged solution from Oracle different from what they’re currently using. That put Oracle a long way from realizing a return on investment on the seven years of development effort — the firm’s largest ever R&D project — that it has put into developing Oracle Fusion Applications.9

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 8

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

■ Stay put. One-quarter of respondents said they would maintain the Oracle app versions they have and limit further investment in them. In this case, either customers have recently upgraded their apps, or they’re sticking with an older app release. For the latter group of customers, continuing to pay Oracle maintenance may prove less and less appealing; 12% of our survey respondents said their firm planned to move to third-party support options.10

■ Move away. According to our survey respondents, Oracle is set to lose some of its business, as 17% of respondents plan to migrate to a SaaS offering from another vendor and 12% intend to move to a different packaged solution from a third-party vendor. There are three areas of particular customer discontent. According to our survey (which encouraged multiple responses), 43% of respondents believe that “high licensing costs” completely describes what they dislike most about their current Oracle apps, followed by “high maintenance costs” (38% of respondents), and “difficult to upgrade” (32% of respondents).

■ Not yet decided. Eight percent of respondents are still considering their options and reviewing their road map planning. Oracle clearly hopes that its recent SaaS acquisitions in CRM (RightNow) and in human capital management (Taleo) will help shore up customer defections, as will its purchases of smaller players in the emerging social software app arena, such as SelectMinds.

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 9

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Figure 4 Oracle Clients We Surveyed Mostly Use PeopleSoft, Hyperion, E-Business Suite, And Siebel

Source: Forrester Research, Inc.82763

Source: June 2012 Global Oracle Applications Online Survey

Oracle PeopleSoft

Oracle Hyperion

Oracle E-Business Suite

Oracle Siebel

Oracle JD Edwards

Oracle vertical packaged applications(e.g., Oracle Utilities, Oracle Financial Services)

Oracle ATG

Oracle Primavera

Oracle RightNow

My �rm does not use any packagedapplications from Oracle

Oracle Agile

Oracle Retail (formerly, Retek)

53%

45%

41%

39%

23%

12%

7%

6%

4%

4%

3%

3%

“Which of Oracle’s packaged applications does your organization use?”

Base: 114 respondents who use Oracle applications

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 10

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Figure 5 Oracle Clients Mostly Plan To Maintain Or Upgrade To The Next Version Of Current Apps

Source: Forrester Research, Inc.82763

Source: June 2012 Global Oracle Applications Online Survey

We will upgrade to the next version[of our current application] 64%

We will maintain the versions we have andlimit further investment in them 25%

We will migrate to a SaaS o�eringfrom another vendor 17%

We will move to third-party maintenanceproviders for the versions we have 12%

We will migrate to a di�erent packagedsolution from another vendor 12%

We will migrate to a SaaSo�ering from Oracle 11%

We will outsource hosting of one ormore of our Oracle applications 11%

We will migrate to a di�erentpackaged solution from Oracle 8%

Other 8%

Base: 77 respondents who use Oracle applications

“Which of the following statements best describes your organization’sfuture intentions for its most important Oracle application?”

has oracle’s applications Unlimited policy Become an anchor dragging down growth?

Back in mid-2006, Oracle’s Applications Unlimited policy looked like a very smart move designed to reassure thousands of worried acquired apps customers of Oracle’s commitment to invest in and support those apps.11 And, Applications Unlimited worked — there weren’t the predicted mass migrations away from JD Edwards, PeopleSoft, and Siebel to Oracle’s remaining apps competitors. Throughout this period, Oracle has maintained very high maintenance contract renewal rates, protecting a large and highly profitable revenue stream. Now, however, Oracle wants customers to move from the familiar to something new — Fusion Applications, which became generally available in November 2011.

The Applications Unlimited policy plays to what Oracle customers like best about their current Oracle apps — stability and scalability. According to our survey encouraging multiple responses, 62% of respondents liked that their current Oracle apps were “scalable and reliable,” while 67% said they liked that their apps were “stable” (see Figure 6).

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 11

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Ever since 2006, Applications Unlimited has represented a commitment by Oracle to: 1) continue enhancing enterprise resource planning (ERP) and CRM apps and not to enforce upgrades; 2) inform and involve customers in product road maps; 3) deploy dedicated development teams; and 4) tie acquired apps into Oracle Lifetime Support.12

Delivering on all four areas involves Oracle expending a good deal of resources and effort.13 Some of this work has undoubtedly helped in the development of Oracle Fusion Applications. But now that Oracle Fusion Applications are generally available, is Oracle deriving enough benefit from all its continued investment in both supporting and enhancing a wide range of other app suites? Even more important, has it put enough effort behind selling the benefits of a move to Oracle Fusion Applications?

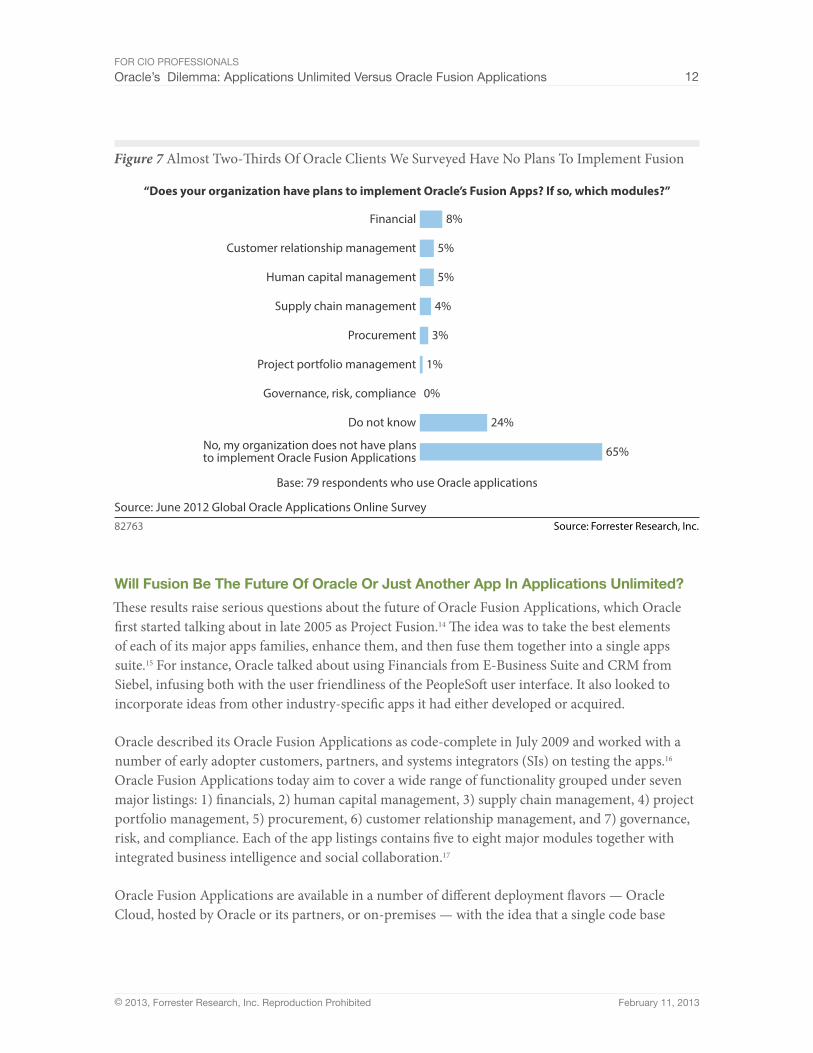

Our survey suggests that the answer to both questions is no — at least, with its installed client base. Among the firms that we surveyed, less than 10%, and in many cases less than 5%, had plans to migrate to at least one of the Oracle Fusion Applications. Sixty-five percent said they had no such plans, and 24% said they didn’t know (see Figure 7).

Figure 6 Oracle Clients Like Stability, Scalability, And Reliability Of Its Apps

Source: Forrester Research, Inc.82763

Source: June 2012 Global Oracle Applications Online Survey

Base: 80 respondents who use Oracle applications

Stable 67% 19% 14%

Scalable and reliable 62% 24% 14%

Easy to customize throughcon�guration of the solution 40% 31% 29%

Easy to customize using code 28% 32% 39%

Easy to integrate with otherapplications 27% 35% 38%

Cost e�ective solution 18% 32% 50%

Easy to upgrade so we canobtain new features 10% 29% 61%

Percentage of responses agreeingcompletely or mostly withthe statement

Percentage of responses neutral on the statement

Percentage of responsesdisagreeing completelyor mostly with the statement

“What do you like best about your �rm’s most important Oracle application?”

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 12

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Figure 7 Almost Two-Thirds Of Oracle Clients We Surveyed Have No Plans To Implement Fusion

Source: Forrester Research, Inc.82763

Source: June 2012 Global Oracle Applications Online Survey

“Does your organization have plans to implement Oracle’s Fusion Apps? If so, which modules?”

Base: 79 respondents who use Oracle applications

Customer relationship management

Human capital management

Project portfolio management

5%

Supply chain management

0%

Financial

65%No, my organization does not have plansto implement Oracle Fusion Applications

Governance, risk, compliance

24%

Procurement 3%

Do not know

5%

1%

4%

8%

Will Fusion Be The Future of oracle or Just another app in applications Unlimited?

These results raise serious questions about the future of Oracle Fusion Applications, which Oracle first started talking about in late 2005 as Project Fusion.14 The idea was to take the best elements of each of its major apps families, enhance them, and then fuse them together into a single apps suite.15 For instance, Oracle talked about using Financials from E-Business Suite and CRM from Siebel, infusing both with the user friendliness of the PeopleSoft user interface. It also looked to incorporate ideas from other industry-specific apps it had either developed or acquired.

Oracle described its Oracle Fusion Applications as code-complete in July 2009 and worked with a number of early adopter customers, partners, and systems integrators (SIs) on testing the apps.16 Oracle Fusion Applications today aim to cover a wide range of functionality grouped under seven major listings: 1) financials, 2) human capital management, 3) supply chain management, 4) project portfolio management, 5) procurement, 6) customer relationship management, and 7) governance, risk, and compliance. Each of the app listings contains five to eight major modules together with integrated business intelligence and social collaboration.17

Oracle Fusion Applications are available in a number of different deployment flavors — Oracle Cloud, hosted by Oracle or its partners, or on-premises — with the idea that a single code base

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 13

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

for Oracle Fusion Applications can enable customers to move back and forth between deployment options or mix and match those choices.18 With its recent SaaS apps purchases, RightNow and Taleo, Oracle has warmed to cloud computing. In addition, Oracle Fusion Applications are now being sold primarily as SaaS, whereas this was not a key part of the delivery strategy until recently.19 It’s also talking about the potential extensibility of Oracle Fusion Applications by customers, partners, and SIs due to its platform-as-a-service development component; it announced some integration-as-as-service capabilities at Oracle OpenWorld in October 2012.

Despite Oracle’s extensive marketing efforts, our survey results and our daily inquiries with Oracle customers suggest that Oracle’s strategy and road map for Oracle Fusion Applications isn’t getting through. Encouraged to provide multiple responses to why their firm doesn’t plan to use Oracle Fusion Applications, 60% of survey respondents said that Oracle’s app strategy was unclear, 54% said Oracle Fusion Applications weren’t mature enough, 36% cited high licensing costs, and 30% said Oracle lacks good customer references for Oracle Fusion Applications. When asked if Oracle had presented their firms with a credible plan to transition to Oracle Fusion Applications, 60% of our respondents said no, 4% said yes, 17% said they didn’t know, and 19% said they don’t plan to transition to Oracle Fusion Applications (see Figure 8).

Oracle has been cautious about introducing Oracle Fusion Applications to avoid the mistakes that plagued E-Business Suite’s buggy rollout a decade ago. To encourage migration at the customer’s own pace, it has advanced a number of different scenarios for Fusion adoption.20 In these scenarios, customers would:

■ Stay put, but prepare for Fusion. The focus here is about getting ready for Oracle Fusion Applications: In other words, moving to the same underlying infrastructure — Fusion Middleware — as Oracle Fusion Applications. As we’ve previously mentioned, Oracle has worked to ensure that the more recent releases of the existing ERP and CRM apps now run on Oracle Fusion middleware.21

■ Adopt some Oracle Fusion Applications modules to complement existing apps. The key here is co-existence, with companies remaining on their current apps from Oracle but opting to add in some Fusion functionality in strategic areas with lower transactional workloads. This is far and away the most popular approach to Fusion among the 400 customers who have licensed or signed up for the apps, about 100 of which have live implementations.22 For instance, within HCM, organizations are bringing in Fusion Performance Management, Fusion Workforce Compensation, and Fusion Talent Management. In favor of this approach, Oracle notes that anywhere between 45% and 67% of its apps users, depending on the specific app, are investing in new modules.23

■ Replace a key apps element or pillar with a Fusion alternative. In this scenario, a firm looking to upgrade its functionality, say its Financials or its HCM, chooses Oracle Fusion Applications

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 14

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

over the latest release of its existing apps.24 This may be a customer currently operating a single on-premises instance of say, E-Business Suite, which is keen to decouple HCM from that instance and move to SaaS HCM. Alternatively, another organization may look to consolidate multiple instances of E-Business Suite Financials apps through a migration to Fusion Financials.25

With its 65,000-strong apps customer base, the 400 Oracle Fusion Applications customer base is something of a drop in the ocean of Oracle apps. However, as more organizations look to have more choice in apps deployment, particularly in relation to SaaS apps, Oracle Fusion Applications may start to look more appealing. For the customers we talk to, the attractive features of Oracle Fusion Applications include the more friendly user interface, the embedded business intelligence, increased apps extensibility by both IT and business users, and the user experience across devices. These functionalities are all nice-to-haves, but one issue with slow Oracle Fusion Applications adoption is that none of those capabilities is a compelling driver for an app migration business case.26

Oracle is also building out more functionality within Oracle Fusion Applications, broadening international support, and talking about debuting industry-specific capabilities for Oracle Fusion Applications sooner rather than later.27 The vendor has also established a direct and telesales Oracle Fusion Applications sales force to go after new prospects as well as cross-sell and upsell opportunities among existing Oracle apps customers and project teams to provide rapid implementation of Oracle Fusion Applications.28

Figure 8 Lack Of Clarity About Oracle Strategy And Lack Of Maturity Hamper Fusion Adoption

Source: Forrester Research, Inc.82763

Source: June 2012 Global Oracle Applications Online Survey

“Why doesn’t your �rm plan to use Oracle Fusion Applications?”

Base: 51 respondents who use Oracle applications(multiple responses accepted)

Oracle’s applications strategy is unclear 60%

Not mature enough 54%

High licensing costs 36%

Oracle lacks good customer referencesfor the product 30%

High maintenance costs 28%

Other 26%

Satis�ed with present Oracle products 24%

Inadequate function 20%

Di�cult to integrate with other applications 12%

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 15

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

how oracle Can and should Resolve its applications dilemma

Many customers are re-evaluating or thinking about revisiting their current apps investments. In part, this is a result of the rise of SaaS applications, which often hold out the promise of more predictable IT costs; and, in part, some organizations have reached a point where their existing and often heavily customized on-premises apps are no longer sustainable. From our research, we find that a vendor pulling support from existing apps often acts as a catalyst for firms to reassess their next step with their apps. That’s one reason why we think Oracle will tread carefully when considering Applications Unlimited and how aggressively it positions Oracle Fusion Applications as the future destination for its customers. Our survey shows that Oracle does not have a high enough level of customer trust or satisfaction to support an aggressive transition to Oracle Fusion Applications. The Oracle clients we surveyed cited “difficult to upgrade” as the second most important factor that they disliked about Oracle apps, with 65% of respondents agreeing completely or mostly with that statement; 66% of respondents cited the perennial complaint about high maintenance costs (see Figure 9).

To allay customer concerns around Oracle Fusion Applications, like those expressed by our survey respondents, we think Oracle will take the following steps:

■ More clearly articulate the benefits of Oracle Fusion Applications. Oracle will try to demonstrate why firms need to embrace Oracle Fusion Applications; it will sell the speed and functionality of Fusion Apps as essential to businesses rather than a nice-to-have. However, Oracle will need to present more compelling migration paths to Oracle Fusion Applications for its customers, particularly those on older versions of its existing apps. There is a danger of Oracle ending up with something of a digital divide, with a group of early adopters pushing ahead with full-blown Oracle Fusion Applications deployments once the full functionality is available across all the modules, another set of customers preparing for the move to Fusion, while a third group doesn’t budge from the older Oracle apps releases. For Oracle, the laggard group is the one most under competitive threat and the ones most likely to move if Oracle were to set a firm cutoff point to Applications Unlimited.

■ Push ahead with Fusion Financials. As Oracle has only recently acknowledged, the future of business applications is in the cloud. It’s still a developing market, but one where Oracle, due to its late entry, is playing catch-up to pure-play SaaS vendors like salesforce.com in CRM and Workday in HCM. What’s lacking in today’s market is a set of strong enterprise SaaS financials, an area which Oracle could dominate if it moves fast enough as midmarket players like NetSuite continue to scale up their offerings and SAP looks to gain traction with its recently announced Financials OnDemand product, an outgrowth of its midmarket SaaS Business ByDesign apps suite.

■ Clarify long-term road maps for Applications Unlimited products. To protect billions of dollars of high-margin maintenance revenues, Oracle continues to support and enhance its older applications products. Indeed, many customers are likely to keep these applications

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 16

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

running for a decade or more despite usability, flexibility, and upgrade challenges. Oracle needs to be clearer about long-term product road maps to help customers understand the ramifications of staying on older products versus migrating to Oracle’s newer offerings or considering other alternatives.

We think Oracle has three primary options to resolve its Applications Unlimited versus Oracle Fusion Applications dilemma, each of which will have different implications for the revenue growth of its apps business. It can:

1. Push Oracle Fusion Applications more aggressively. In this scenario, it will reward Oracle Fusion Applications migrants with attractive module bundling price points and play a more active role in facilitating migrations, particularly when customers are moving from older app versions. Oracle is currently encouraging legacy apps clients to use certain Oracle Fusion Applications modules that complement their existing core legacy apps. Moving to a more aggressive posture involves providing incentives for customers (and Oracle sales) to adopt core Fusion transactional modules (e.g., finance, payroll, procurement), replacing the similar modules in EBS, PeopleSoft, and JD Edwards. It may also involve creating some disincentives to clients staying on existing apps, such as longer and more modest enhancement releases. This strategy is hampered by the fact that the older products support more industry nuances and localizations than the respective Fusion modules. It would tend to hurt Oracle’s revenues in the near term but improve them in the long term.

2. Retain Applications Unlimited and reduce the role of Oracle Fusion Applications. In this less likely scenario, Oracle pulls back on any major growth ambitions for Oracle Fusion Applications.29 Rather than expect Oracle Fusion Applications to replace legacy core transaction apps, Oracle would offer only the newer modules that complement the older products. As newer releases of existing apps and Oracle Fusion Applications gain more of a common look and feel, Oracle Fusion Applications will seamlessly blend into Oracle’s overall app portfolio. This will protect Oracle’s revenue growth in the near term but hurt its revenues in the longer term unless it pursues a more aggressive acquisition strategy.

3. Maintain current balance between Applications Unlimited and Oracle Fusion Applications. This approach, representing Oracle’s current position, allows Oracle to keep its (and its customers’) options open by not forcing a choice between Applications Unlimited and Oracle Fusion Applications. This scenario also allows for a longer period of time to see if Oracle Fusion Applications will catch fire among Oracle’s customer base on their own over several years. But as Fusion adoption evolves, Oracle’s commitment to enhancing the older products may fade, along with customers’ desire to continue to invest in upgrades and support. The result is likely to be weaker growth for Oracle’s apps than the other options both in the near and longer term.

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 17

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

Figure 9 Oracle Clients Dislike Upgrading As Much As They Dislike Maintenance Costs

Source: Forrester Research, Inc.82763

Source: June 2012 Global Oracle Applications Online Survey

Base: 78 respondents who use Oracle applications

Percentage of responses agreeing completely or mostly with the statement

Percentage of responses neutral on the statement

Percentage of responsesdisagreeing completelyor mostly with the statement

“What do you dislike most about your rm’s most important Oracle application?”

High maintenance costs 66% 26% 8%

Di�cult to upgrade 65% 19% 16%

High licensing costs 61% 29% 11%

Di�cult to customize and change 44% 27% 29%

Di�cult to integrate withother applications 39% 38% 23%

De�cient business function 26% 32% 42%

Di�cult to scale 19% 33% 48%

Unstable 7% 16% 77%

R e c o m m e n d at i o n s

oRaCle ClienTs: WaTCh FoR MoRe pRessURe To MoVe To FUsion appliCaTions

At this point, Oracle has sunk too much money and resources into Oracle Fusion Applications to abandon the effort. We anticipate that Oracle is likely to step up efforts to encourage its Applications Unlimited customers to move more rapidly to Oracle Fusion Applications and its cloud infrastructure offerings. Oracle applications customers should do the following to prepare:

■ Assess the sustainability of your applications portfolio. Take inventory of all business applications, including Oracle’s and those from other vendors, to determine current ownership costs and the technical debt resulting from deferred upgrades. Determine levels of investment needed to sustain the applications portfolio and risks of obsolescence.

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 18

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

■ Develop a long-term applications strategy. Determine which applications should be replaced, upgraded, or added. Customers running Oracle products (e.g., E-Business Suite, JD Edwards, PeopleSoft, and Siebel) should assess options to either upgrade within these product lines, adopt Fusion Applications, or migrate to competing products.

■ Strike the best deal possible for Fusion migrations. If you decide to migrate from older Oracle products to Fusion, hold Oracle to its trade-in promise for like-for-like exchanges. Beware of additional costs for middleware and cloud services in the Fusion stack, as well as integration costs. Don’t assume that integration between various Oracle applications products is plug-and-play.

■ Shift your applications updating model to the pace of the cloud. As you migrate existing applications to newer products like Oracle Fusion Applications, shift your updating model to the cadence of the cloud. Embrace the cloud’s managed services model to keep applications up-to-date, whether you opt for a pure-cloud model or a hybrid (e.g., hosted or private cloud) delivery model.

W H at i t m e a n s

iT’s Make-oR-BReak TiMe FoR oRaCle’s appliCaTions BUsiness

Oracle’s main challenge in applications is retaining profitable recurring revenues while increasing revenue growth from new licenses and subscriptions. For new customers, Oracle is in danger of appearing more of a me-too apps player than an innovator, given the time it’s taken to deliver complete versions of Fusion Applications and lay out its particular approach to cloud computing. Oracle Fusion Applications represents Oracle’s main strategy to grow its applications revenue and counter a variety of fast-growing SaaS competitors. Fusion Applications alone, however, may not provide the growth engine Oracle needs to protect its market position in applications. Look for Oracle to accelerate its growth strategy with more SaaS acquisitions, similar to Taleo and RightNow.

sUppleMenTal MaTeRial

Methodology

Forrester’s June 2012 Global Oracle Application Online Survey was fielded to 180 Forrester contacts that are IT decision-makers with knowledge of Oracle applications. For quality assurance, we screened respondents to ensure they met minimum standards in terms of content knowledge and job responsibilities.

Forrester fielded the survey from June to July 2012. Respondent incentives included a summary of the survey results. Exact sample sizes are provided in this report on a question-by-question basis.

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 19

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

This survey used a self-selected group of respondents and is therefore not random. This data is not guaranteed to be representative of the population, and, unless otherwise noted, statistical data is intended to be used for descriptive and not inferential purposes. While nonrandom, the survey is still a valuable tool for understanding where users are today and where the industry is headed.

endnoTes1 The quarters we discuss here are the calendar quarters that most closely coincide with Oracle’s fiscal

quarters. Because Oracle’s fiscal quarters end in February, May, August, and November of each year, Q4 2011 in our discussion would be Oracle’s fiscal Q2, which ended on November 2011; Q1 2012 would include Oracle’s fiscal Q3 2012 ending in February 2012; and Q2 2012 would include Oracle’s fiscal Q4 2012 ending in May 2012.

2 We want to note that this kind of analysis is not intended for investors in Oracle stock, who will not care whether Oracle’s revenue growth comes from new acquisitions or old products. Because Oracle does not provide information on product revenue growth, we cannot calculate the revenue it gets from its pre-acquisition products. While our approach of adding the acquired vendors’ pre-acquisition revenues to Oracle’s revenues in the base periods may overstate its organic growth if those vendors’ revenue growth was faster than that of Oracle’s pre-existing products, the discrepancy is likely to be small given how much larger the revenues from pre-existing products are compared with the revenues from the acquired vendors.

3 SAP is even more exposed to the weak economy of Europe than Oracle, as the Europe, the Middle East, and Africa region will represent 47% of SAP’s total revenues in 2012, compared with 28% of Oracle’s software revenues.

4 SAP announced its intention to acquire e-purchasing company Ariba for approximately $4.3 billion on May 22, 2012. SAP’s acquisition of Ariba closed on October 1, 2012. See the August 3, 2012, “The SAP/Ariba Merger Will Not Be Frictionless” report.

5 In this comparison, we converted Oracle’s US dollar revenues into euros using the average exchange rate for the week in which Oracle’s fiscal quarter ended, while using SAP’s reported revenues in euros.

6 Sixty percent of the respondents to our survey were located in the US and 40% in Europe. They included companies in manufacturing (28%); government, education, and healthcare (17%); transportation; professional, services and construction (11%); utilities and telecom (11%); media and entertainment (8%); and retail and wholesale (8%).

7 Oracle tends to cite a statistic regarding apps upgrades of around 80% of all users being on the latest version or on the two most recent releases of its apps. However, that figure tends to mask the very different user picture for different Oracle apps. For instance, while Oracle puts 93% of the E-Business Suite user base on the latest two releases, it has only 43% of JD Edwards customers in the same situation. Oracle notes that: “Percentage reflects a weighted average of customers on the latest releases of Oracle EBS, PeopleSoft Enterprise, JDE, Siebel, Agile PLM for Process, Agile Engineering Data Management, Oracle Transportation Manager, and Demantra. Source: “Charting Your Course with Oracle Applications,” Oracle, January 2011 (www.oracle.com/us/products/applications/charting-your-course-315028.pdf).

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 20

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

8 One comment we hear many times from Oracle customers is how weary they are of Oracle’s upsell and cross-sell approaches. This observation was borne out by our survey where 32 % of respondents encouraged to provide multiple responses said that the following statement completely described Oracle as a technology vendor for their firm: “Oracle is constantly trying to sell us more of its products.”

9 In some cases, customers have told us that they have already filled gaps in the Oracle apps suites they currently use with complementary Oracle on-premises apps and now feel too invested in those products and their current app suites to consider an apps migration.

10 A modest third-party support market is emerging, but Oracle has filed lawsuits against several of the key players. See the July 20, 2012, “Rimini Street Challenges Big Software Maintenance Fees” report and see the April 16, 2010, “Don’t Let Oracle’s Lawsuit Dissuade You From Considering 3SPs, But Recognize The Risks” report.

11 Charles Phillips, at that time Oracle president, gave a presentation on Applications Unlimited at Collaborate 2006, an annual gathering of Oracle user groups in April in Nashville, Tennessee. The presentation is available at SlideShare’s website. Source: Christian Hofer, “Oracle Applications Unlimited,” SlideShare, October 18, 2006 (http://www.slideshare.net/Fenomeno/oracle-applications-unlimited).

More information can be found at the Oracle website as well. Source: “An Executive Guide to Oracle Applications Unlimited,” Oracle, 2006 (http://www.oracle.com/us/products/applications/035821.pdf).

An open letter to Siebel customers sent in July 2006 from Oracle’s then senior vice president of CRM applications Ed Abbo introducing Applications Unlimited can be viewed at the Oracle Applications Users Group website (http://www.oaug.org/pls/portal/docs/page/oaug/usercommunities/siebelusercommunity/documents/2006-07siebelopenletter.pdf).

12 As part of Applications Unlimited, Oracle promised to provide three layers of paid support for its ERP and CRM apps: Premier Support (includes updates, bug fixes, security alerts, and certifications with Oracle and third-party products), which lasted for the first five years of an app release from the date it was first made available; Extended Support, for a further three years; and Sustaining Support, which effectively had no end date.

Oracle noted that some releases might not have an Extended Support phase, in which case customers would have the option to move to Sustaining Support once the five-year period of Premier Support expired. Source for Oracle Lifetime Support Policy as of June 2012: “Oracle Information-Driven Support,” Oracle, September 2012 (http://www.oracle.com/us/support/library/lifetime-support-applications-069216.pdf).

Oracle has also set new support timelines for some apps. For instance, Oracle recently announced changes in Oracle Lifetime Support policies for Oracle E-Business Suite releases 11i and 12.1. Source: Steven Chan,

“EBS 11i and 12.1 Support Timeline Changes,” Oracle E-Business Suite Technology blog, October 9, 2012 (https://blogs.oracle.com/stevenChan/entry/ebs_11i_and_12_1)

13 It’s worth noting that over time Oracle has expanded Applications Unlimited so it applies not only to its app suites — E-Business Suite, JD Edwards, PeopleSoft, and Siebel; it also applies across its other products lines such as Agile project life-cycle management and Primavera enterprise project portfolio management

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 21

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

software, both the result of acquisitions, and its industry-specific apps, many of which were the result of smaller “tuck in” purchases such as G-Log and Retek.

14 Source: “Oracle Fusion Human Capital Management Rethinking the Business of HR,” Oracle, April 2011 (http://www.oracle.com/us/products/applications/fusion-hcm-rethink-hr-wp-365545.pdf).

15 Other apps vendors were also looking to this kind of model. For instance, Microsoft had Project Green, an initiative to combine the best features of its four acquired Dynamics ERP families — Dynamics AX, GP, NAV, and SL — and of its Dynamics CRM apps into a next-generation single suite. Microsoft later abandoned that strategy and repositioned Project Green as a replacement of non-Microsoft infrastructure within Dynamics apps with support for Microsoft middleware and databases.

16 Oracle Fusion Applications early adopters, which Oracle has publicly highlighted, include Alcoa, Boeing, Elizabeth Arden, Green Mountain Coffee Roasters, McDonald’s, McKesson, Pacific Northwest National Lab, Principal Finance Group, Qualcomm, Siemens, and UBS. New additions to that list at OpenWorld 2012 included Ardent Leisure, Peach Aviation, Red Robin, Toshiba Medical Systems, and Zillow.

Oracle Fusion Applications partners include Acxiom, ADP, D&B Hoovers, Fujitsu, HireRight, InsideView, Nuance, SAVO Group, Silverpop, and Vertex.

Oracle Fusion Applications SIs include Accenture, Cognizant, Deloitte, Infosys, PricewaterhouseCoopers, and Wipro.

17 Oracle breaks down each module to more granular level still, which enables it to claim more than 100 Oracle Fusion Applications.

18 Oracle puts the current deployment profile for Oracle Fusion Applications at 65% software-as-a-service (Oracle Cloud), 26% on-premises, and 9% on-demand. The geographical split across 17 countries is North America 67%, Europe 23%, and Asia Pacific 10%. Source: Oracle OpenWorld 2012 presentations.

19 It’s interesting to listen to Oracle CEO Larry Ellison in full cloud computing dismissal in an address to financial analysts on September 25, 2008 (http://www.youtube.com/watch?v=0FacYAI6DYO). Ellison definitely has a point about the cloudiness or vagueness of the cloud computing term, but he goes on to say how Oracle doesn’t need to do anything differently to be a cloud computing player other than change the wording of some of its advertising. For a more famous and amusing cloud computing putdown, also listen to Ellison’s September 21, 2009, appearance at The Churchill Club (http:/www.youtube.com/watch?v=KmXJSeMaoTY).

20 Source: “Charting Your Course with Oracle Applications,” Oracle, January 2011 (http://www.oracle.com/us/products/applications/charting-your-course-315028.pdf).

21 It’s worth noting at this point that Oracle Fusion Applications don’t share the same code base as Oracle’s existing apps, whether homegrown or acquired. At present, upgrade scripts to Oracle Fusion Applications are limited to the latest releases of E-Business Suite, JD Edwards, PeopleSoft, and Siebel, making it less burdensome for customers on those versions to potentially move to Oracle Fusion Applications.

22 The number of Fusion customers is taken from presentations Oracle executives gave at OpenWorld 2012.

For CIo ProFessIonals

oracle’s Dilemma: applications Unlimited Versus oracle Fusion applications 22

© 2013, Forrester Research, Inc. Reproduction Prohibited February 11, 2013

23 For existing apps customers keen on adding in Oracle Fusion Applications or swapping out their current apps for Fusion alternatives. Oracle is providing software licenses credits as like-to-like functionality provided those customers are paying support fees. Customers need to pay extra for any net new Oracle Fusion Applications, in other words, modules that are not replacements for existing apps for which users are already paying maintenance. Oracle Fusion Applications are available via perpetual licensing or by subscription. Oracle Fusion Applications are priced by a variety of different metrics. Source: “Oracle Fusion Applications Global Price List,” Oracle, March 15, 2012 (http://www.oracle.com/us/corporate/pricing/fusion-applications-price-list-418746.pdf) and “Oracle Fusion Applications Cloud Service and Cloud Service Options Licensing Information,” Oracle, May 2012 (http://www.oracle.com/technetwork/fusion-apps/oraclefusionapplicensingcloudrel4-1612436.pdf).

24 At Oracle OpenWorld 2012 in October, Oracle executives positioned the split of Oracle Fusion Applications customers as 39% adopting HCM, 38% adopting CRM, and 23% adopting ERP modules.

25 One major systems integrator with an Oracle Fusion Applications practice shared with us that it has seven to eight active Oracle Fusion Applications client deployments and is in discussions with 30 or so more clients who are interested in adopting Oracle Fusion Applications. Typically, firms are looking to deploy Oracle Fusion Applications in specific divisions or business lines, with an eye on a future Oracle Fusion Applications global deployment. Organizations are tending to move to Oracle Fusion Applications from the most recent version of Oracle’s other apps. If they plan to migrate from earlier versions, firms are more looking at an apps re-implementation rather than a migration.

26 Forrester has published a report that includes drivers and user case studies around making major new apps investments. See the July 31, 2012, “Measure The Business Impact Of Improved App Strategy” report.

27 At Oracle’s OpenWorld user conference in October 2012 in San Francisco, Oracle executives said the firm will bring Fusion HCM on par with Oracle PeopleSoft in terms of international support over time. For instance, the plan is to expand the current number of supported payrolls from five countries to 15 by the end of 2013. On the industry support front, Oracle intends to verticalize Fusion Applications over the next few years and is also talking some specifics about particular areas. For instance, within Oracle Fusion HCM, a future goal is to cater to verticals including higher education by offering faculty management and manufacturing by providing scheduling and health and safety management. Oracle has yet to provide manufacturing apps as part of Oracle Fusion Applications.

28 One of the potential obstacles to on-premises Oracle Fusion Applications is the additional Oracle infrastructure software that customers might also have to purchase in relation to business intelligence, portal, and identity and access management apps.

29 A more extreme variant of this scenario would be to abandon Fusion Applications altogether, which Oracle may have considered at several points in the product suite’s rather long gestation period.

Forrester Research, Inc. (Nasdaq: FORR) is an independent research company that provides pragmatic and forward-thinking advice to global leaders in business and technology. Forrester works with professionals in 17 key roles at major companies providing proprietary research, customer insight, consulting, events, and peer-to-peer executive programs. For more than 29 years, Forrester has been making IT, marketing, and technology industry leaders successful every day. For more information, visit www.forrester.com. 82763

«

Forrester Focuses OnCIOs

as a leader, you are responsible for managing today’s competing

demands on IT while setting strategy with business peers and

transforming your organizations to drive business innovation.

Forrester’s subject-matter expertise and deep understanding of your

role will help you create forward-thinking strategies; weigh opportunity

against risk; justify decisions; and optimize your individual, team, and

corporate performance.

caRol ito, client persona representing CIOs

About Forrestera global research and advisory firm, Forrester inspires leaders,

informs better decisions, and helps the world’s top companies turn

the complexity of change into business advantage. our research-

based insight and objective advice enable IT professionals to

lead more successfully within IT and extend their impact beyond

the traditional IT organization. Tailored to your individual role, our

resources allow you to focus on important business issues —

margin, speed, growth — first, technology second.

foR moRe infoRmation

To find out how Forrester Research can help you be successful every day, please contact the office nearest you, or visit us at www.forrester.com. For a complete list of worldwide locations, visit www.forrester.com/about.

client suppoRt

For information on hard-copy or electronic reprints, please contact Client Support at +1 866.367.7378, +1 617.613.5730, or [email protected]. We offer quantity discounts and special pricing for academic and nonprofit institutions.