oregon – personal lines homeowners manual – personal lines homeowners manual indicates revision...

TRANSCRIPT

Oregon – Personal Lines Homeowners Manual

Indicates Revision Unigard Insurance Company February 2011

Homeowners Policy Program General Rules, Optional Coverages and Basic Premiums Index General Rules Rule No. Cancellation or Reduction .......................................................................... 13 Deductibles ................................................................................................ 5 (Deductible Options - See Basic Premium Section) Description of Coverages (Section I and Section II) ....................................... 2 Section I - Coverages Section II - Coverages Eligibility ..................................................................................................... 3 Additional Insureds - Co-owner or joint owner Condominiums Cooperatives Co-owner occupants - 2 Family Dwelling Farm Dwellings Joint Owners - non-occupant Life Estate Arrangement Manufactured Homes Owner-occupant(s) - 1-2 families Owner - occupant(s) - over 2 families Permitted Incidental Occupancies Purchaser - occupant(s) Seasonal Dwellings Tenant Limits of Liability and Coverage Relationship ............................................. 1 Coverage A - Limit of Liability Coverage B - See Other Structures Coverage C - See Personal Property Coverage D - See Loss of Use Coverage G - See Blanket Personal Articles Coverage Mandatory Coverages ................................................................................ 4 Additional Insured Locations Permitted Incidental Occupancies Residence Employees Manual Premium Revision ......................................................................... 14 Multiple Company Insurance ...................................................................... 8 Optional Coverages ................................................................................... 6 Other Insurance ......................................................................................... 12 Credit for Existing Insurance

Oregon – Personal Lines Homeowners Manual

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule No. Policy Period .............................................................................................. 10 Renewal Plan ............................................................................................. 11 Secondary Residence Premises ................................................................ 7 Waiver of Premium .................................................................................... 18 Whole Dollar Premium Rule ........................................................................... 19 Optional Coverages Property Blanket Personal Articles Coverage ............................................................... 50 Business Property - Increased Limits ............................................................. 27 Credit Card, Electronic Fund Transfer Card or Access Device, Forgery and Counterfeit Money Increased Limits ........................................................ 28 Dwellings - In Course of Construction (COC) ............................................... 52 Course of Construction Coverage Extension Transportation and Theft of Building Materials (COC) Earthquake ..................................................................................................... 29 Extended Replacement Cost - Coverage A ................................................. 48 Form HO-6 Coverage A Dwelling ................................................................... 31 Basic Limit Increased Limit Special Coverage Home Day Care Coverage ............................................................................ 33 All Forms Home Electronic Equipment Endorsement .................................................... 55 Identity Fraud Expense ................................................................................... 57 Limited Fungi, Wet or Dry Rot, or Bacteria Coverage ................................ 56 Section I Loss Assessment Coverage ........................................................................... 35 Residence Premises Loss of Use - Increased Limits ....................................................................... 36

Oregon – Personal Lines Homeowners Manual

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule No. Ordinance or Law Coverage........................................................................... 30 Other Structures - Section I ............................................................................ 38 Actual Cash Value Increased Limits Rented to Others Off-Premises Structures Permitted Incidental Occupancies .............................................................. 34 Other Structures Residence Premises Personal Property ...................................................................................... 39 Firearms Furs Increased Limit of Liability Increased Limits - Other Residences Increased Special Limits of Liability Jewelry and Watches Money and Securities Reduction in Limit of Liability Silverware and Goldware Personal Property - Scheduled ....................................................................... 42 Rental to Others - Theft Coverage ................................................................. 43 Replacement Cost Coverage ......................................................................... 40 Roof Loss Settlement - Actual Cash Value ................................................ 46 Special Computer Coverage .......................................................................... 45 Special Personal Property Coverage ............................................................. 41 Units Regularly Rented to Others ................................................................... 32 Water Back-Up and Sump Discharge or Overflow ......................................... 44 Optional Coverages Liability Additional Residence Rented to Others ......................................................... 64 Business Pursuits ........................................................................................... 69 Home Day Care Coverage ............................................................................. 67

Oregon – Personal Lines Homeowners Manual

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule No. Incidental Farming Personal Liability Residence Premises ............................ 75 Away From Residence Premises Incidental Motorized Land Conveyances........................................................ 71 Liability Coverage - Increased Limits .............................................................. 60 Limited Fungi, Wet or Dry Rot, or Bacteria Coverage .................................... 78 Other Insured Location Occupied by Insured ................................................. 62 Other Structures ............................................................................................. 65 Outboard Motors, Watercraft and Personal Watercraft Personal Watercraft . 72 Watercraft Liability Watercraft Medical Payments Coverage for Insureds Watercraft Physical Damage Permitted Incidental Occupancies – Residence Premises and Other Residences 68 Personal Injury ................................................................................................ 70 Residence Held in Trust ................................................................................. 66 Residence Premises - Increased Liability Limits ............................................ 61 Secondary Residence Premises Credit - Section II ........................................ 77 Snowmobile .................................................................................................... 73

Oregon – Personal Lines Homeowners Manual 1

Indicates Revision Unigard Insurance Company February 2011

General Rules The Homeowners Policy Program provides property and liability coverages, using the forms and endorsements specified in this manual. This manual contains the rules and classifications governing the writing of the Homeowners Policy. The rules, rates, forms and endorsements of Unigard for each coverage will govern in all cases not specifically provided for in this manual. Effective with this revision, all new and renewing policies will be written by Unigard Insurance Company, regardless of program. Rule 1. Limits of Liability and Coverage Relationships A. The Limits of Liability required under the Homeowners Policy are as follows: Section I - Property Damage Coverages

HO-3OR (1) HO-4OR HO-6OR (2) HO-3+ (1) HO-5+ (1) Bronze Bronze Bronze Silver Gold (147820OR) (147825OR) A-Dwelling Minimum Limit

$50,000 N/A $5,000 $50,000 $80,000

B-Other Structures 10% of A N/A N/A 10% of A 20% of A C-Personal Property Without Replacement Cost Contents

50% of A

$20,000

$25,000

N/A

N/A

With Replacement Cost Contents

50% of A

$30,000

$35,000

75% of A

75% of A

D-Loss of Use 50% of A 50% of C 50% of C 50% of A 50% of A (1) Secondary Residence - $50,000 - Entire State (2) Minimum limit: Secondary Residence - $20,000 without Replacement Cost Contents

$30,000 with Replacement Cost Contents

Section II - Liability Coverages

All Forms E- Personal Liability Including Personal Injury $100,000 Each Occurrence F- Medical Payments to Others $ 1,000 Each Person

The basic premiums displayed in the Relativities Section include $100,000 Personal Liability and $1,000 Medical Payments.

Oregon – Personal Lines Homeowners Manual 2

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 1. Limits Of Liability And Coverage Relationships (Continued) B. All Forms The limit of liability for Section I Coverages C or D and Section II Coverages E or F may be increased. C. Bronze Program For HO-3OR, under Coverage B of Section I, an additional amount of insurance may be written on a specific structure using HO448OR. Under Coverage C of Section I, the limit of liability may be reduced to a minimum of 40% of the limit on the dwelling. D. Condo For HO-6OR, the limit of liability for Coverage A of Section I may be increased. E. Silver and Gold Programs Under Coverage B of Section I, an additional amount of insurance may be written on a specific structure using HO448OR. Under Coverage C of Section I, the limit of liability may not be reduced. Rule 2. Description of Coverages A. Section I Coverages - Property Damage

Coverage A - Dwelling

Coverage B - Other Structures Coverage C - Personal Property Coverage D - Loss of Use The following is a general description of the coverages provided by the individual Homeowners Policy forms. The policy must be consulted for exact contract conditions.

Oregon – Personal Lines Homeowners Manual 3

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 2. Description of Coverages (Continued) 1. Form HO-3OR - Special Form - Coverage available in the Bronze Program only.

Covers dwelling, other structures and loss of use against most risks of physical loss, subject to certain exclusions. Personal property is covered for loss caused by:

• Fire or lightning • Windstorm or hail • Explosion except volcanic eruption • Riot or civil commotion • Aircraft • Vehicles • Smoke • Theft including theft from unattended auto and watercraft • Vandalism or malicious mischief • Breakage of glass or safety glazing material • Falling objects • Weight of ice, snow or sleet • Accidental discharge of water or steam • Sudden and accidental tearing apart of a heating system or appliance • Freezing • Sudden and accidental damage from electrical current • Volcanic eruption

2. Form HO-4OR - Contents Broad Form - Coverage available in the Bronze Program

only. Covers personal property, including the insured's interest in building additions and alterations, and loss of use against loss by the same perils as outlined under HO-3OR.

3. Form HO-6OR - Condominium Unit-Owners Form - Coverage available in the Bronze

Program only. Covers building additions and alterations of the unit, personal property, and loss of use against loss by the same perils as outlined under HO-3OR.

4. Form HO-3+ - Coverage available in the Silver Program only. Covers dwelling, other

structures, and loss of use against most risks of physical loss, subject to certain exclusions. Personal property is covered for loss by the same perils as outlined under HO-3OR. Loss to Personal Property is automatically covered at 75% of Coverage A on a replacement cost basis, if the contents are replaced. Certain types of personal property are not eligible for replacement cost settlement. These types of property are specified in the policy.

Extended Replacement Cost - Coverage A is automatically included. This coverage provides additional cost of repair or replacement of the building insured under Coverage A. It can be increased up to an additional 50% of the Coverage A limit shown in the Declarations. This extension does not apply to Ordinance or Law Coverage or to Land Stabilization Coverage.

Oregon – Personal Lines Homeowners Manual 4

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 2. Description of Coverages (Continued) 5. Form HO-5+ - Coverage available in the Gold Program only. Covers dwelling, other

structures, personal property, and loss of use against most risks of physical loss, subject to certain exclusions. Earthquake is not included for personal property coverage but is available by endorsement.

Loss to Personal Property is automatically covered at 75% of Coverage A on a replacement cost basis, if the contents are replaced. Certain types of personal property are not eligible for replacement cost settlement. These types of property are specified in the policy. Extended Replacement Cost - Coverage A is automatically included. This coverage provides additional cost of repair or replacement of the building insured under Coverage A. It can be increased up to an additional 50% of the Coverage A limit shown in the Declarations. This extension does not apply to Ordinance or Law Coverage or to Land Stabilization Coverage.

B. Section II Coverages Liability - All Forms Coverage E - Personal Liability including Personal Injury Coverage F - Medical Payments to Others 1. Personal Liability - Covers payment on behalf of any insured of all sums which the insured

will become legally obligated to pay as damages because of bodily injury or property damage arising out of an insured's premises or personal activities. It includes protection for Personal Injury to others, such as false arrest, libel or invasion of privacy. Personal Liability also includes the cost associated with providing a defense by council of our choice. This is an additional coverage, and is limited to the amount of Personal Liability shown in the Declaration.

2. Medical Payments to Others - Covers medical expenses incurred by persons, other than the

insured, who sustain bodily injury caused by an accident arising out of an insured's premises or personal activities.

Oregon – Personal Lines Homeowners Manual 5

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 3. Eligibility A. Bronze, Silver and Gold Programs For forms HO-3OR, HO-3+ and HO-5+, a Homeowners Policy may be issued: 1. To the owner-occupant(s) of a dwelling which is used exclusively for private residential

purposes (except as provided in General Rule 3.F.) and contains not more than 2 families and with not more than 2 boarders or roomers per family; or

2. To the purchaser-occupant(s) who has entered into a long term installment contract for the purchase of the dwelling and who occupies the dwelling but to whom title does not pass from the seller until all the terms of the installment contract have been satisfied. The seller retains title until completion of the payments and in no way acts as a mortgagee. The seller's interest in the building and premises liability may be covered using Endorsement HO-441OR - Additional Insured; or

3. To the occupant of a dwelling under a life estate arrangement. The owner's interest in the building and premises liability may be covered using Endorsement HO-441OR - Additional Insured; or

4. To the owner-occupant (Bronze Program) of a manufactured home which meets all of the following requirements: (a) It is the permanent residence of the insured and issued only for residential purposes; or

it is a seasonal residence of the insured who has other homeowner supporting coverage with Unigard.

(b) It was constructed in 1990 or a more recent year. (c) It must be located in Protection Class 1-8B. (d) It must be sitting on a fully enclosed masonry foundation with appropriate tie-downs.

Note: Residence Held in Trust - We may add the name of a trust to the Homeowners Policy

when: • The residence is a one family dwelling used exclusively for residential purposes; • Legal title to the dwelling unit is held by the trust; • The personal property held in trust is used by a tenant and insured under an HO 00 04; • The resident of the residence held in trust includes at least one of the following:

o The trustee; o The grantor of the trust; or o The beneficiary of the trust.

Refer to the Optional Coverages – Liability section or the Optional Coverages – Property section for more information. Attach Endorsement HO9443UN - Residence Held in Trust

Oregon – Personal Lines Homeowners Manual 6

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 3. Eligibility (Continued) B. Tenant - For HO-4OR, a Homeowners Policy may be issued only to: 1. The tenant(s) (non-owner) of a dwelling, mobile or manufactured home or an apartment

situated in any building; or 2. The owner-occupant(s) of a dwelling, cooperative unit or of a building containing an

apartment not otherwise eligible for a Homeowners Policy under General Rule 3.A. above; provided the residence premises occupied by the insured is used exclusively for residential purposes (except as provided in General Rule 3.F.) and is not occupied by more than one additional family or more than two boarders or roomers. Note: If multiple individuals are listed as named insureds, they must be related by blood,

marriage, or adoption. C. When a 2 family dwelling is occupied by co-owners, each occupying distinct living quarters

with separate entrances, a Homeowners Policy providing building coverage may be issued to only one of the co-owner occupants of the dwelling. The policy may be endorsed to cover the interest of the other co-owner(s) in the building and for premises liability. A separate Homeowners Policy Form HO-4OR may be issued to co-owner(s) occupying the other apartment dwelling. It is permissible to extend the Homeowners Policy, without additional premium charge, to cover the interest of a non-occupant joint owner in the building and for premises liability.

Attach Endorsement HO-441OR - Additional Insured D. Condo - For form HO-6OR, a Homeowners Policy will be issued to the owner of a

condominium or cooperative unit which is used exclusively for residential purposes, except as provided in General Rule 3.F, and is not occupied by more than one additional family or more than two boarders or roomers.

E. Subject to all other sections of this rule, a Homeowners Policy may be issued to cover a

seasonal dwelling. Unigard must also provide coverage for the insured’s primary residence. F. Certain occupancies incidental to the dwelling are permitted provided:

1. The premises is occupied principally for dwelling purposes; and 2. There is no other business conducted on the premises.

Refer to Rule 68. Permitted Incidental Occupancies for policy writing instructions.

Oregon – Personal Lines Homeowners Manual 7

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 3. Eligibility (Continued) G. A policy will not be issued covering any property to which farm forms or rates apply under

the rules of Unigard. In no event will a policy be issued to cover any property situated on premises used for farming purposes except as noted below. Optional Section II liability coverage is available for certain farm liability exposures as specified in Rule 75. Incidental Farming Personal Liability.

Rule 4. Mandatory Coverages A. It is mandatory that insurance be written for all coverages provided under both Sections I

and II of the policy, except as provided in General Rule 7. B. Section II of the policy requires coverage for the following exposures. When such

exposures exist, refer to the Optional Coverages-Section II Coverages of this manual. 1. All additional insured locations where the named insured, spouse, or registered domestic

partner legally recognized under Oregon law, maintain a residence other than business or farm properties.

2. Permitted incidental occupancies by the insured on residential premises of the named insured.

Rule 5. Deductibles Deductible options are shown in the Basic Premium Section of this manual. Rule 6. Optional Coverages Optional Section I and II Coverages are described in this section, General Rules and Optional Coverages Section, starting with Rule 27. Rule 7. Secondary Residence Premises Coverage on a secondary residence premises will be provided under a separate policy. The rules of this manual apply except that Section II Coverage is not mandatory for the secondary residence policy when: 1. Unigard insures the initial and secondary residence; and 2. The policy number of the initial residence is indicated on the policy covering the secondary

residence.

Oregon – Personal Lines Homeowners Manual 8

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 8. Multiple Company Insurance Unigard does not divide risks with other companies as our Section I and Section II Coverages are unique. Unigard has complete reinsurance facilities to write large Homeowners policies so the use of the Multiple Company Insurance rule is generally not necessary. If you have a large Homeowners policy, contact Unigard well in advance of the effective date. If the account meets our underwriting criteria, we will write the entire account. There is no need to split the coverage with one of your other carriers. Rule 9. Reserved for Future Use Rule 10. Policy Period The Policy may be written for a period of one year and may be renewed for successive policy periods by a Renewal Declaration based upon the premiums, forms and endorsements then in effect for Unigard. For maintaining common anniversary dates, a Homeowners Policy may be written for a period of less than one year on a pro rata basis. Rule 11. Renewal Plan A. A policy may be continued for another policy period upon payment of the required premium

to Unigard on or before the inception date of the next policy period. B. The Renewal premium will be based upon the premiums in effect on renewal date. Form or

endorsements will be issued only in cases where they have been revised. Additional premiums for policy changes occurring during the current policy term will be computed pro rata of the annual premium.

Rule 12. Other Insurance Credit for existing insurance is not permitted.

Oregon – Personal Lines Homeowners Manual 9

Indicates Revision Unigard Insurance Company February 2011

General Rules Rule 13. Cancellation or Reductions in Limits of Liability or Coverages It is not permissible to cancel any of the mandatory coverages in the policy unless the entire policy is cancelled. If insurance is cancelled or reduced at the request of either the insured or Unigard, the earned premium will be computed on a pro rata basis. Rule 14. Manual Premium Revision A manual premium revision, meaning any revision of premium applicable to the Program, will be made in accordance with the following procedures: A. The effective date of such revision will be as announced. B. The revision will apply to any policy or endorsement in the manner outlined in the

announcement of the revision. C. When an existing policy is endorsed to take advantage of a reduction in premium, the

adjustment will be made on a pro rata basis. D. Unless otherwise provided at the time the premium revision becomes effective, the premium

revision does not affect in-force policy forms and endorsements until the policy is renewed. Rule 15-17. Reserved for Future Use Rule 18. Waiver of Premium When a policy is endorsed subsequent to the inception date, any additional or return premium of $3 or less may be waived. Rule 19. Whole Dollar Premium Rule All premiums shown on the policy and endorsements shall be rounded to the nearest whole dollar. A premium of $.50 or more shall be rounded to the next higher whole dollar.

In the event of cancellation by Unigard, the return premium may be carried to the next higher whole dollar. Rule 20-24. Reserved for Future Use

Oregon – Personal Lines Homeowners Manual 10

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Section I - Coverages-Property Rules 25-26. Reserved for Future Use Rule 27. Business Property - Increased Limits - All Forms A. The limit of liability for business property on the residence premises may be increased to

$10,000. The basic limit is $2,500 for the Bronze Program and Silver Program. The basic limit is $7,500 for the Gold Program. The premium for each $2,500 increase is $25. The limit of liability in excess of $2,500 does not apply to: 1. Business property in storage or held as a sample or for sale or delivery after sale;

2. Business property pertaining to a business actually conducted on the residence premises. This exposure is addressed in the endorsements for Permitted Incidental Occupancies:

150230 - Bronze & Silver Programs 150235 - Gold Program

B. When the on-premises limit is increased, the off-premises limit of $250 in the Bronze and Silver Programs and the limit of $1,000 in the Gold Program are automatically increased at no additional premium charge, to an amount that is 10% of the total on-premises limit of liability.

Attach Endorsement 146860OR Increased Limits on Business Property

Oregon – Personal Lines Homeowners Manual 11

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 28. Credit Card, Electronic Fund Transfer Card or Access Device, Forgery and Counterfeit Money

A. Bronze Program When the $2,500 limit of liability afforded under the policy is increased, the additional premium will be developed as follows:

Limit of Liability Premium $ 5,000 $ 5

7,500 6 10,000 7

Attach Endorsement HO-453OR Credit Card, Electronic Fund Transfer Card or Access Device, Forgery and Counterfeit Money Coverage Increased Limits

B. Silver Program

When the $5,000 limit of liability afforded under the policy is increased, the additional premium will be developed as follows:

Limit of Liability Premium $ 7,500 $ 5

10,000 6

Attach Endorsement HO-453OR Credit Card, Electronic Fund Transfer Card or Access Device, Forgery and Counterfeit Money Coverage Increased Limits

C. Gold Program

The $10,000 basic limit included in the Gold Program may not be increased.

Oregon – Personal Lines Homeowners Manual 12

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 29. Limited Earthquake Coverage Coverages The policy may be endorsed to provide coverage against a loss resulting from the peril of earthquake. This peril will apply to all Section I Coverages for the same limits provided in the policy. 1. Dwelling

The dwelling coverage limit will always be the same as the Coverage A limit for the dwelling. Dwelling coverage does not include:

• outbuildings • appurtenant structures • swimming pools • masonry fences and walls not necessary for the structural • integrity of the dwelling • walkways and patios not necessary for regular ingress or egress from the dwelling • awnings or other patio covers • decorative or artistic features including plaster if other covering would be more

cost-effective • landscaping • masonry chimneys.

The policy does cover replacement of a damaged masonry chimney with a nonmasonry, earthquake resistant chimney.

2. Contents

Forms HO-3OR, HO-3+, HO-5+, HO-4OR and HO-6OR: The contents limit will always be the same as the Coverage C limit for Personal Property. Contents coverage does not include coverage for glassware, china, porcelain, or ceramic items, artwork or other decorative items.

3. Additional Living Expense The limit is $5,000 to cover expenses while the dwelling remains uninhabitable because of physical loss or damage by earthquake.

4. Earthquake coverage is available on Forms HO-3OR, HO-3+, HO-5+, HO-6OR and HO-

4OR, for frame and masonry veneer dwellings. Masonry veneer is excluded from coverage. Solid brick, stone or concrete dwellings are not eligible for earthquake coverage. For forms HO-3OR (Bronze), HO-3+ (Silver) and HO-5+ (Gold), the earthquake coverage premium is calculated based on the Coverage A limit and any Coverage C limit over 50% of Coverage A. For forms HO-4OR or HO-6OR (Bronze), the earthquake coverage premium is calculated based on the entire Coverage C limit and any increased Coverage A. The premium for each $1,000 of insurance will be developed as follows:

Oregon – Personal Lines Homeowners Manual 13

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 29. Limited Earthquake Coverage (Continued) Coverages (Continued)

A HO-3 , HO-3+, HO-5+

Coverage A

Zone 1 2 3 4

Per $1000 $0.44

.52

.86

.99 5 1.15 6 1.46

B HO-4, HO-6 Coverage A All forms Coverage C

1 2 3 4

$0.29

.35

.57

.66 5 .76 6 .97

A fully completed Earthquake Questionnaire, Form 148030, must accompany any request for Earthquake Coverage. Zone Definitions by County Zone 1 Zone 2 Zone 3 Zone 4 Zone 5 Zone 6 Rest of State Deschutes Clackamas Harney Benton Clatsop Hood River Marion Jackson Douglas Columbia Jefferson Lake Josephine Coos Linn Multnoma Lane Curry Wasco Washington Polk Klamath Yamhill Lincoln Tillamook Deductibles - All Programs The base deductible is 10% of the limit for each coverage and is subject to a $500 minimum. This deductible may be increased for a premium credit. The premium for higher deductibles is developed by applying the applicable credit to the Base Deductible premium.

Deductible Credit Percentage Frame

15% 11% 20% 22% 25% 33%

Oregon – Personal Lines Homeowners Manual 14

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 29. Limited Earthquake Coverage (Continued) Deductibles – All Programs (Continued) The deductible applies separately to loss under Coverage A – Dwelling and Coverage C - Personal Property. No deductible applies to Additional Living Expense. If the limit of liability on certain property is increased by endorsement, the total limit of liability is used to determine the deductible. Attach Endorsement 154440 Earthquake Rule 30. Ordinance or Law Coverage A. Bronze and Silver Programs For the HO-3OR (Bronze), HO-3+(Silver) programs excluding manufactured homes and HO-6OR: 1. Basic Limit

The policy automatically provides up to 10% of the Coverage A limit of liability to pay for the increased costs necessary to comply with the enforcement of an ordinance or law.

2. Increased Amount of Coverage a. The policy may be endorsed to increase the basic Ordinance or Law Coverage amount,

as noted below, to accommodate the increased costs known or estimated by the insured for materials and labor to repair or replace the damaged property and to demolish the undamaged portion of damaged property and clear the site of resulting debris according to the ordinance or law.

b. Premium Addition

The additional premium for increased amounts of Ordinance or Law coverage is developed by applying the appropriate factor to the adjusted basic premium.

Percentage of Coverage A

Factors

Increase in Amount

Total Amount

HO-3OR, HO-3+

HO-6OR

15% 25% 0.05 N/A 40% 50% 0.14 0.1 65% 75% 0.20 0.2 90% 100% 0.27 0.3

Attach Endorsement 150990OR Ordinance or Law - Increased Amount of Coverage

Oregon – Personal Lines Homeowners Manual 15

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 30. Ordinance or Law Coverage (Continued) B. Gold Program For the HO-5+ (Gold): 1. Basic Limit

The policy automatically provides up to 20% of the Coverage A limit of liability to pay for the increased costs necessary to comply with the enforcement of an ordinance or law.

2. Increased Amount of Coverage

a. The policy may be endorsed to increase the basic Ordinance or Law Coverage amount, as noted below, to accommodate the increased costs known or estimated by the insured for materials and labor to repair or replace the damaged property and to demolish the undamaged portion of damaged property and clear the site of resulting debris according to the ordinance or law.

b. Premium Addition

The additional premium for increased amounts of Ordinance or Law coverage is developed by applying the appropriate factor to the adjusted basic premium.

Percentage of Coverage A

Factors

Increase in Amount

Total Amount

HO-5+ Factor

5% 25% 0.02 30% 50% 0.10 55% 75% 0.16 80% 100% 0.23

Attach Endorsement 150992OR Ordinance or Law – Increased Amount of Coverage-Gold

Oregon – Personal Lines Homeowners Manual 16

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 31. HO-6OR - Coverage A - Dwelling Form - Bronze Program Only Basic and Increased Limits and Special Coverage A. Basic

The basic policy automatically provides $5,000 Coverage A on a named peril basis at no additional charge. If increased limits are not desired, enter "$5,000" under Coverage A - Dwelling on the application.

B. Increased Limits

The Coverage A limit may be increased in increments of $1,000 only. The premium is developed based on the additional limit of insurance. The premium for each additional $1,000 of insurance is $2.00. Enter the total Coverage A limit on the application.

C. Special Coverage The named perils may be broadened for Coverage A to cover additional risks of loss. The additional premium is developed as follows:

1. $5,000 basic policy limit . . . $2; plus 2. $1 is added to the applicable premium under HO-6OR "Each Additional $1,000 of

Coverage C" per $1,000 increased limits. Attach Endorsement 151610OR Unit Owners Coverage A - Special Coverage Rule 32. Form HO-6OR - Units Regularly Rented to Others - Bronze Program Only Form HO-6OR excludes Coverage C Personal Property and Section II Liability coverage when the residence premises is regularly rented or held for rental to others. The policy may be endorsed, however, to provide such coverage, including theft. The additional premium is 25% of the Coverage C adjusted basic premium. Attach Endorsement 151600OR Unit-Owners Rental to Others

Oregon – Personal Lines Homeowners Manual 17

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 33. Home Day Care Coverage - All Forms Coverage for a home day care business is limited under Section I and excluded under Section II. The policy may be endorsed to provide expanded Section I coverage and Section II coverage for a home day care business in the dwelling or in another structure on the residence premises. We provide optional coverage only for home day care operations caring for 3 or fewer children, not including the insured’s own children. If the home day care business is located in another structure, Coverage B does not apply to that structure. Optional Section I coverage for other structures used for a day care business is available. The rate is $3 per $1,000 of coverage for the Bronze program and $5 per $1,000 for the Silver and Gold programs. The Home Day Care Endorsement also covers personal property pertaining to this business within the Coverage C limits stated in the Declarations. See Rule 39 if increased Coverage C limits are desired. See Rule 67 to develop the premium for the increased Section II exposure. For Bronze and Silver Programs - Attach Endorsement 150200 Home Day Care Coverage - Oregon For Gold Program - Attach Endorsement 150210 Home Day Care Coverage - Oregon Rule 34. Permitted Incidental Occupancies - Residence Premises - All Forms Coverage for a permitted incidental occupancy is limited under Section I and excluded under Section II. The policy may be endorsed to cover expanded Section I coverage and Section II coverage on a permitted incidental occupancy in the dwelling or in another structure on the residence premises. If the business is located in another structure, Coverage B does not apply to that structure. Examples of eligible occupancies are offices, schools or studios meaning offices for business or professional purposes, and private schools or studios for music, dance, photography or other instructional purposes. The Permitted Incidental Occupancies Endorsement also covers personal property pertaining to the permitted incidental occupancy up to the Coverage C limits stated in the Declarations.

Oregon – Personal Lines Homeowners Manual 18

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 34. Permitted Incidental Occupancies - Residence Premises - All Forms (Continued) The additional Section I premium will be as follows: 1. If the permitted incidental occupancy is located in the dwelling, no additional charge is made. 2. If the permitted incidental occupancy is located in another structure, the charge is $3 per

$1,000 of specific insurance on the structure. The additional Section II premium is developed from Rule 68.

Attach Endorsement 150230 - Permitted Incidental Occupancies - Residence Premises, for Section I and Section II Coverage - Bronze and Silver Programs - Oregon Attach Endorsement 150235 - Permitted Incidental Occupancies - Residence Premises, for Section I and Section II Coverage - Gold Program - Oregon

Rule 35. Loss Assessment Coverage - All Forms The form automatically provides, at no additional charge, loss assessment coverage limits of $2,500 in the Bronze and Silver programs and $5,000 in the Gold program, excluding Earthquake, for assessments pertaining to the residence premises. These limits may be increased for an additional premium, as developed below: A. Residence Premises (Sections I and II)

* $5,000 limit is automatically included in the Gold Program.

Attach Endorsement 146910OR Loss Assessment Coverage - Bronze and Silver Programs Attach Endorsement 147870OR Loss Assessment Coverage - Gold Program

B. Earthquake (Section I only)

Coverage for loss assessment resulting from loss by earthquake is not available.

Total amount of Coverage HO-4OR, HO-6OR (Bronze Program)

HO-3OR (Bronze), HO-3+ (Silver), HO-5+ (Gold)

$ 5,000 $2 $3* 10,000 4 6

Each Add’l $5,000 (Up to $50,000)

1 2

Oregon – Personal Lines Homeowners Manual 19

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 36. Loss of Use - Increased Limit - All Forms The basic limit of liability is 50% of the Coverage A for Bronze, Silver and Gold policies. For Forms HO-4OR and HO-6OR, the basic limit of liability is 50% of Coverage C. When the basic limit is increased, the premium will be $2 per $1,000 of insurance for the Bronze program and $5 per $1,000 of insurance for the Silver and Gold programs. Rule 37. Reserved For Future Use

Oregon – Personal Lines Homeowners Manual 20

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 38. Other Structures When insurance is written on a specific structure on the residence premises for increased limits, or rented to others for dwelling purposes, the rates per $1,000 of insurance noted below will apply separately to each structure. A. Increased Limits - $2 per $1,000 of insurance

Attach Endorsement HO448OR Other Structures B. Rented to Others - Residence Premises

Use the sum of: 1. $3 per $1,000 of insurance, and 2. the premium for the increased Coverages E and F exposure, as developed from

Section II Coverages of this manual. Attach Endorsement HO440OR Structures Rented to Others-Residence Premises

C. Off-Premises Structures - The policy automatically provides Coverage B - Other Structures

at 10% of Coverage A in the Bronze and Silver programs and 20% of Coverage A in the Gold program on a blanket basis to structures located on the residence premises.

To endorse this blanket coverage to include structures located away from the residence premises, if used in connection with the residence premises charge an additional $15 per policy. Attach Endorsement 146895OR Coverage B - Off-Premises

D. Specific Structures Off Premises - When insurance is written on a specific structure located

away from the residence premises but used in connection with the residence premises, the additional premium is $3 per $1,000 of insurance for the Bronze program and $4 per $1,000 of insurance for the Silver and Gold programs. Attach Endorsement 146900 Specific Structures Away From Residence Premises

E. Other Structures – Actual Cash Value - Losses to other structures are generally settled on a

replacement cost basis if the structure is repaired or replaced. Some other structures, such as older Barns and other out buildings, may be more appropriately insured on an actual cash value basis. Attach Endorsement 145250 Other Structures - Actual Cash Value Settlement

Oregon – Personal Lines Homeowners Manual 21

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 39. Personal Property A. Increased Limit

When the limit of liability for Coverage C is increased, the additional premium per $1,000 of additional insurance is:

HO-3OR (Bronze Program)

HO-3+ (Silver Program) HO-5+ (Gold Program)

$1.75 $2.35

B. Increased Limits – Other Residences

Coverage for personal property at other residences is limited in the policy form to 10% of Coverage C or $1,000, whichever is greater. This limit may be increased. The additional premium is $7 per $1,000 of additional insurance. Attach Endorsement HO450OR Increased Limits on Personal Property in Other Residences

C. Reduction in Limit

Bronze Program - Form HO-3OR - The limit of liability for Coverage C may be reduced to an amount not less than 40% of the limit for Coverage A at a credit of $1 per $1,000 of insurance.

Silver and Gold Programs - The basic policy provides Coverage C at 75% of the limit for Coverage A. Coverage C may not be reduced below the basic limit provided.

D. Increased Special Limits of Liability

1. Money and Securities

a. Bronze and Silver Programs -

(1). The special limit of $200 on money may be increased to $1,000. The additional premium is $6 for each $100 increase.

(2). The $1,500 limit on securities may be increased to $2,000. The additional premium is $4 for each $100 increase.

b. Gold Program - The special limits of $1,000 on money and $5,000 on securities may

not be increased.

Oregon – Personal Lines Homeowners Manual 22

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 39. Personal Property (Continued) 2. Furs

a. Bronze Program - The special limit of $1,500 for loss by theft of furs may be increased to

a maximum of $7,500 in increments of $500, but not exceeding $1,500 per item. The additional premium is $7.50 for each $500 increase.

b. Silver Program - The special limit of $2,500 for loss by theft of furs may be increased to a

maximum of $7,500 in increments of $500, but not exceeding $1,500 per item. The additional premium is $7.50 for each $500 increase.

c. Gold Program - The special limit of $5,000 for loss by theft or mysterious disappearance

of furs may be increased by using Unigard's Blanket Personal Articles Coverage (see Rule 50), but not exceeding $2,500 per item.

3. Jewelry and Watches

a. Bronze Program - The special limit of liability of $1,500 for loss by theft of jewelry or

watches may be increased in increments of $500 to a maximum of $7,500 but not exceeding $1,500 per item. The additional premium is $7.50 for each $500 increase. Note: We do not increase coverage for unset gemstones.

b. Silver Program - The special limit of liability of $2,500 for loss by theft of jewelry or

watches may be increased in increments of $500 to a maximum of $7,500 but not exceeding $1,500 per item. The additional premium is $7.50 for each $500 increase. Note: We do not increase coverage for unset gemstones.

c. Gold Program - The special limit of $5,000 for loss by theft of or mysterious

disappearance of jewelry or watches may be increased by using Unigard's Blanket Personal Articles Coverage (see Rule 50), but not exceeding $2,500 per item. Note: We do not increase coverage for unset gemstones.

4. Silverware and Goldware

a. Bronze and Silver Programs - The special limit of liability of $2,500 for loss by theft of

silverware may be increased to a maximum of $10,000 in increments of $500. The additional premium is $1 for each $500 increase.

b. Gold Program - The special limit of $5,000 for loss by theft or mysterious disappearance

of silverware and goldware may be increased by using Unigard's Blanket Personal Articles Coverage (see Rule 50).

Oregon – Personal Lines Homeowners Manual 23

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 39. Personal Property (Continued) 5. Firearms

a. Bronze and Silver Program - The special limit of liability of $2,500 for loss by theft of

firearms may be increased to a maximum of $6,000 in increments of $100. The additional premium is $3 for each $100 increase.

b. Gold Program - The special limit of $2,500 for loss by theft or mysterious disappearance

of firearms may be increased by using Unigard's Valuable Personal Articles Coverage (see Rule 50). Attach Endorsement 146880 Coverage C Increased Special Limits of Liability - Bronze and Silver Programs

For HO-3OR or HO-6OR or Silver Program with Special Personal Property Coverage Attach Endorsement 147950 - Coverage C Increased Special Limits of Liability For HO-3OR or HO-6OR or Silver Program with Special Personal Property Coverage Attach Endorsement 147950S - Coverage C Increased Special Limits of Liability for Silverware For the Gold Program use Unigard’s Blanket Personal Articles Coverage.

Oregon – Personal Lines Homeowners Manual 24

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 40. Replacement Cost Contents Coverage - Personal Property – All Forms Under the policy, losses under Coverage C are settled on an actual cash value. Replacement Cost Contents Coverage extends coverage to include the full cost of repair or replacement without deduction for depreciation. Replacement Cost Contents Coverage is applicable only to Personal Property damaged or destroyed by the perils insured against. The coverage is available for both primary and secondary locations. Replacement Cost Contents Coverage also applies to articles or classes of property separately described and specifically insured in this policy, as listed in the Scheduled Personal Property endorsement. Certain types of personal property are not eligible for replacement cost settlement. These types of property are specified in the Personal Property Replacement Cost endorsement and include such items as antiques, fine arts, memorabilia, and articles not maintained in good or workable condition. A. Bronze Program The premium for this coverage is $0.23 per $1,000 of the Coverage C limit on the policy. If limits above 50% of Coverage A are desired, see Rule 39.A. Attach Endorsement 146915OR Personal Property Replacement Cost B. Silver and Gold Programs Replacement Cost Contents Coverage — Personal Property is automatically included. If limits above 75% of Coverage A are desired, see Rule 39.A.

Oregon – Personal Lines Homeowners Manual 25

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 41. Special Personal Property Coverage Excluding Earthquake – Forms HO-3OR & HO-6OR - Bronze Program, Silver Program and Gold Program A. Bronze Program HO-3OR

Coverages A and B are insured against additional risks of physical loss subject to certain exclusions. Coverage C is insured against perils named in the form. The policy may be endorsed to insure Coverage C Personal Property against additional risks of physical loss subject to certain exclusions. Earthquake coverage for personal property is not provided by this endorsement. The premium for this coverage is computed by increasing the adjusted basic dwelling premium by 12%.

For HO-3OR - Attach Endorsement 146850OR Special Personal Property Coverage B. Bronze Program Condo

Coverage is insured against perils named in the form. The policy may be endorsed to insure Coverage C against additional risks of physical loss subject to certain exclusions. Earthquake coverage for personal property is not included in this form. This option may only be used when the condominium or cooperative unit is owner occupied. The premium for this coverage is computed by increasing the adjusted basic dwelling premium by 25%. In addition, when this coverage is written, the following Coverage C – Personal Property – Special Limits of Liability are increased: • For loss by theft, misplacing or losing of furs from $1,500 to $5,000. • For loss by theft, misplacing or losing of jewelry, watches, precious and semi-precious

stones from $1,500 to $5,000. • For loss by theft, misplacing or losing of silverware, silver-plated ware, goldware, gold-

plated ware and pewterware. This includes flatware, hollowware, tea sets, trays and trophies made of or including silver, gold or pewter from $2,500 to $5,000.

• On “business” property, not otherwise excluded, while located on the ‘residence premises’ from $2,500 to $5,000.

• On “business” property, not otherwise excluded, while located away from the ‘residence premises’ from $250 to $500.

For HO-6OR - Attach Endorsement 149415OR Unit Owners - Coverage C Special Coverage

Note: If Replacement Cost Contents is afforded, refer to Rule 40. Replacement Cost

Contents Coverage - Personal Property.

Oregon – Personal Lines Homeowners Manual 26

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 41. Special Personal Property Coverage Excluding Earthquake – Forms HO-3OR & HO-6OR - Bronze Program, Silver Program and Gold Program (Continued) C. Silver Program

Coverages A and B are insured against additional risks of physical loss subject to certain exclusions. Coverage C is insured against perils named in the form.

The policy may be endorsed to insure Coverage C Personal Property against additional risks of physical loss subject to certain exclusions. Earthquake coverage for personal property is not included in this form. The premium for this coverage is computed by increasing the adjusted basic dwelling premium by 12%.

For Silver Program - Attach Endorsement 146855OR Special Personal Property Coverage

D. Gold Program

Coverages A, B, C and D are insured, at no additional charge, against additional risks of physical loss subject to certain exclusions. Earthquake coverage for personal property is not included in this form.

Earthquake coverage is available as an optional coverage by endorsement. See Rule 29. Earthquake Coverage.

Rule 42. Personal Property - Scheduled — All Forms Coverage may be provided on scheduled personal property subject to the rules and rates outlined in the Rate and Relativity Section. Unigard amends certain loss settlement provisions by paying for total losses of other than fine arts and postage stamps, based on the amount shown in the schedule including scheduled pairs and sets. This loss settlement enhancement is included for no additional premium. Attach Endorsement HO-461OR Scheduled Personal Property Rule 43. Reserved for Future Use

Oregon – Personal Lines Homeowners Manual 27

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 44. Water Back-Up and Sump Discharge or Overflow — Bronze and Silver Programs The policy may be endorsed to provide coverage to property covered under Section I for direct loss resulting from: 1. water, or water-borne material which backs up through sewers or drains originating off the

residence premises, or 2. water that overflows from a sump pump system. The limit of liability under this option applies to all losses under Coverages A, B and C arising from one occurrence. The premium charge for this coverage is determined by multiplying the base premium of $30 by factors for the limit and deductible chosen for this option and the Water Back-Up territory in which the property is located, and rounding to the nearest dollar. Available limits and deductibles for this option and their factors are as follows:

Limit Factor Deductible Factor

$1,000 0.31 $250 1.12 $2,500 0.63 $500 1.00 $5,000 0.90 $1,000 0.89 $10,000 1.15 $1,500 0.84 $15,000 1.38 $2,000 0.78 $20,000 1.91 $2,500 0.71 $25,000 2.27 $3,000 0.66 $30,000 2.60 $4,000 0.63 $35,000 2.90 $5,000 0.60 $40,000 3.17 $45,000 3.42 Territory Factor $50,000 3.67 Entire State 1.00 $55,000 3.90 $60,000 4.14 $65,000 4.37 $70,000 4.62 $75,000 4.93 $80,000 5.10 $85,000 5.33 $90,000 5.58 $95,000 5.81

Attach Endorsement 147875OR Water Back-Up and Sump Discharge or Overflow Note: Water back-up and sump discharge or overflow coverage is automatically included in

HO-5+ (Gold Program).

Oregon – Personal Lines Homeowners Manual 28

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 45. Special Computer Coverage — Bronze and Silver Programs The policy may be endorsed to broaden coverage for computers and related equipment against additional risks of physical loss subject to certain exclusions. This endorsement does not provide increased property limit for the computer. Additional coverage for computers is available under the Blanket Personal Articles Coverage - Coverage G, see Rule 50. Computer equipment means computer hardware, software, operating systems or networks. It also includes other electronic parts, equipment or systems designed for use with the equipment above. The additional premium is $15. Attach Endorsement 147955OR Special Computer Coverage Note: Special Computer Coverage is automatically included in the Special Personal Property

Coverage endorsement and in the HO-5+ (Gold Program). Rule 46. Roof Loss Settlement—Actual Cash Value Roof losses are generally settled on a replacement cost basis if the structure is repaired or replaced. Certain roofs may be more appropriately insured on an actual cash value basis. Attach Endorsement 151780OR Actual Cash Value Loss Settlement Losses to Roof Surfacing – Bronze Attach Endorsement 151785OR Actual Cash Value Loss Settlement Losses to Roof Surfacing – HO-6 Attach Endorsement 151790OR Actual Cash Value Loss Settlement Losses to Roof Surfacing – Silver & Gold Rule 47. Reserved for Future Use

Oregon – Personal Lines Homeowners Manual 29

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 48. Extended Replacement Cost - Coverage A - Building A. Bronze Program

For HO-3OR, the policy may be extended to provide additional cost of repair or replacement of the building insured under Coverage A. It can be increased up to an additional 50% of the Coverage A limit shown in the Declarations. This coverage is available for homes built in 1900 or later, and may be added to primary and secondary locations. This extension does not apply to Ordinance or Law Coverage or to Land Stabilization Coverage. When this coverage is written, please complete the replacement cost calculation using RCT ExpressTM, a residential replacement cost estimator from Marshall & Swift/Boeckh (MSB). Please refer to www.unigard.com for more information. The additional premium is $8. Attach Endorsement 138360OR Extended Replacement Cost - Coverage A - Building

B. Silver and Gold Program

Extended Replacement Cost - Coverage A - Building is automatically included and provides for the additional cost of repair or replacement of the building insured under Coverage A, up to a maximum of an additional 50% of the limit shown in the Declarations. This extension does not apply to Ordinance or Law Coverage or to Land Stabilization Coverage.

Rule 49. Reserved for Future Use

Oregon – Personal Lines Homeowners Manual 30

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 50. Blanket Personal Articles Coverage - Coverage G Optional Blanket Personal Articles coverage for the classes of property shown below may be provided by endorsement. This coverage is primary and any coverage provided by the basic policy is excess. When this endorsement is attached, it is not necessary to schedule items, nor are appraisals required. Losses are not settled on a valued basis as they are under our regular Inland Marine program. Losses are settled under the same provisions that apply to personal property under the homeowner policy. No deductible applies to Coverage G. However, a deductible will be subtracted from any payments made under Coverage C, Personal Property. A $2,500 per item limit applies to jewelry, furs, silverware and fine arts. A $1,000 per item limit applies to cameras, musical instruments, golfer's equipment and guns. A $500 per item limit applies to china/crystal and to data storage media used with a home computer. A $5,000 per item limit applies to personal computers. For jewelry, furs, silverware and fine arts, coverage is available at the following limits subject to the maximum limit per class: $1,000, $2,500, $5,000, $7,500, $10,000, $15,000 and $20,000. For all other classes, coverage is available in $1,000 increments subject to the maximum limit per class. The rates are determined as follows: Class of Property Rate per $1,000 Maximum Liability Jewelry $ 13.00 $ 20,000 Furs 5.00 20,000 Cameras 18.50 5,000 Musical Instruments 5.00 5,000 Silverware 2.90 20,000 Golfer's Equipment 7.50 5,000 Fine Arts 2.90 20,000 Guns 20.00 5,000 Personal & Home Computers 20.00 10,000 Attach Endorsement 146785OR Coverage G - Blanket Personal Articles Coverage – Bronze Attach Endorsement 146790OR Coverage G - Blanket Personal Articles Coverage - Silver Attach Endorsement 146795OR Coverage G - Blanket Personal Articles Coverage - Gold

Oregon – Personal Lines Homeowners Manual 31

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 51. Reserved for Future Use Rule 52. Dwelling - In the Course of Construction (COC) A. A homeowner policy may be issued to cover a dwelling in the course of construction (COC).

The policy may be issued only in the name of the intended owner-occupant(s) of the dwelling. The Coverage A - dwelling limit must be equal the completed value of the dwelling.

B. The premium in addition to the amount calculated for the completed value of the dwelling is

$100. C. While the dwelling is under construction, coverage is automatically extended for the full

Coverage C limit to the insured’s personal property at another location. Glass breakage caused by workers is excluded. This coverage ceases when any insured occupies the dwelling. This coverage is included for no additional charge. Attach Endorsement 147925OR - Dwelling Under Construction Coverage Extension.

D. Transportation and Theft of Building Materials - Coverage is available for dwellings under

the course of construction (COC) which provides protection for:

• Loss of building materials, plumbing, heating, lighting fixtures and other similar items, while in transit to the job site, and

• Theft of materials that have not been attached to and made a part of the dwelling at the dwelling location.

A separate $100 deductible applies to a covered loss. The premium is $50 for $10,000 of coverage. Attach Endorsement 1433, Transportation and Theft of Building Materials.

Rule 53-54. Reserved for Future Use

Oregon – Personal Lines Homeowners Manual 32

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 55. Home Electronic Equipment Endorsement – All Forms A. Bronze Program

This endorsement may be added to eligible policies which have Replacement Cost Contents Coverage.

B. Bronze, Silver and Gold Programs

This endorsement extends coverage for electronic equipment to include replacement with new electronic equipment of greater quality and usefulness, subject to a limit of 125% of replacement cost. The premium is $25. Attach Endorsement 144090OR Home Electronic Equipment Endorsement

Rule 56. Limited Fungi, Wet or Dry Rot, or Bacteria Coverage Limited Fungi, Wet or Dry Rot, or Bacteria Coverage automatically provides a Special Limit of Liability as follows: A. $10,000 to pay for loss to covered real or personal property, owned by an insured, that is

damaged by fungi, or wet or dry rot, or bacteria on the “residence premises” as defined in the coverage endorsements. This coverage applies only for the policy period in which the loss or costs occur.

B. For Property Coverage, the $10,000 is the most coverage that will be provided during the

policy period regardless of the number of locations insured for Limited Fungi, or Wet or Dry Rot, or Bacteria Coverage or the number of claims made during the policy period. This limit may not be increased. Refer to Rule 78. For a description of the Section II Liability. Limited Fungi, Wet or Dry Rot, or Bacteria Coverage. Read the endorsements for complete details on coverages, limitations, definitions and additional policy conditions applicable to this coverage. Attach Limited Fungi, Wet or Dry Rot, or Bacteria Coverage Endorsement: 153419OR – Limited Fungi, Wet or Dry Rot, or Bacteria Coverage – Silver 153422OR – Limited Fungi, Wet or Dry Rot, or Bacteria Coverage – Gold 153410OR – Limited Fungi, Wet or Dry Rot, or Bacteria Coverage – Bronze 153416OR – Limited Fungi, Wet or Dry Rot, or Bacteria Coverage – HO-6 153413OR – Limited Fungi, Wet or Dry Rot, or Bacteria Coverage – HO-4

Oregon – Personal Lines Homeowners Manual 33

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 57. Identity Fraud Expense Coverage A. Coverage Description

When the optional Identity Fraud Expense Coverage endorsement is attached to the policy, coverage is available to pay for expenses incurred by an insured as a direct result of any one identity fraud first discovered or learned of during the policy period. Such expenses include the costs of notarizing fraud affidavits or similar documents; certified mail sent to law enforcement, financial institutions and credit agencies; lost income resulting from time taken off work to meet with or talk to law enforcement or credit agencies; loan application fees for re-applying for a loan when the application is rejected solely because the lender received incorrect credit information; and reasonable attorney’s fees incurred to defend lawsuits brought against the insured and to remove criminal or civil judgments. Identity Fraud Expense Coverage will be offered as an optional endorsement. This endorsement will be available to all Bronze, Silver and Gold homeowner insureds, including HO-4 and HO-6 policyholders. An additional benefit provided by this coverage is the availability of the ID Theft Help Line. The Help Line will refer the insured to a Case Management designee who will provide counseling on how to manage identity theft, account take over or inquiries arising from the loss or theft of non public personal information such as the loss of a credit card, ATM card, checkbook, driver’s license or passport. Note: Coverage is not provided for lost funds incurred as a result of identity theft. Those

costs should be borne by creditors. Most individuals can’t be held liable for more than $50 in fraudulent credit card purchases or ATM transactions. Coverage is provided for expenses an insured incurs to remedy the stolen identity situation.

B. Limits of Liability

1. Bronze and Silver Programs – A $15,000 coverage limit will be provided for the identity

fraud of an insured discovered or first learned of during the policy period. 2. Gold Program – A $20,000 coverage limit will be provided for the identity fraud of an

insured discovered or first learned of during the policy period.

C. Deductible There is a separate $250 deductible for Identity Fraud Expense Coverage. No other deductible applies.

Oregon – Personal Lines Homeowners Manual 34

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Property Rule 57. Identity Fraud Expense Coverage (Continued) D. Premium

The premium charge for this coverage is $25 for the Bronze, Silver, and Gold Programs. Attach Identity Fraud Expense Coverage Endorsement HO455UN – Bronze & Silver Attach Identity Fraud Expense Coverage Endorsement HO455GD – Gold

Rule 58-59. Reserved for Future Use

Oregon – Personal Lines Homeowners Manual 35

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Section II - Coverages - Liability Rule 60. General Instructions When the limit of liability for Coverage E, Personal Liability, or F, Medical Payments to Others is increased or coverage for additional exposures is provided, the additional premium is developed from the following tables. The same limits must apply to all exposures. Coverage F limits indicated below are "each person" limits. See the Personal Umbrella Section of the Personal Lines Manual for limits in excess of those shown. The rate table below displays the liability rates for commonly rated liability options. Additional information on specific coverage options is presented under the individual coverage rules. Limits Of Liability

Cov. E $100,000 $300,000 $500,000 Exposure Cov. F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000 1. Residence

Premises Inc. 4 13 15 20 30 28 31 41

2. Other Insured Locations Occupied By Insured

1 Family .......... 6 7 10 8 9 12 9 10 13 2 Family .......... 12 13 16 16 17 20 18 19 22 3 Family .......... 24 25 28 32 33 36 36 37 40 4 Family .......... 26 27 30 35 36 39 39 40 43 3. Additional

Residence Rented to Others (a)

1 Family .......... 10 11 14 13 14 17 15 16 19 2 Family .......... 16 17 20 21 22 25 24 25 28 3 Family .......... 28 29 32 37 38 41 42 43 46 4 Family .......... 30 31 34 40 41 44 45 46 49 4. Residence Held in

Trust (b) Inc 1 4 8 9 12 12 13 16

Note: (a) See Rules 64 and 65 to determine the applicable endorsement.

(b) See Rule 66 for the applicable endorsement.

Oregon – Personal Lines Homeowners Manual 36

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule 61. Residence Premises Increased limits for Coverage E and Coverage F are available. Rates are displayed in the liability rate table in Rule 60. Rule 62. Other Insured Locations Occupied By An Insured Section II coverage may be provided on locations, other than the residence premises, where an insured resides, but which are insured for Section I coverage under another insurance program or by another company. Rates are displayed in the liability rate table in Rule 60. Rule 63. Reserved for Future Use Rule 64. Additional Residence Rented To Others The policy may be endorsed to provide coverage when an additional residence is rented to others. Rates are displayed in the liability rate table in Rule 60. Attach Endorsement 2470OR Additional Residence Rented to Others Rule 65. Other Structures Rented To Others - Residence Premises The policy may be endorsed to provide coverage when a structure on the residence premises is rented to others for dwelling purposes. Section I coverage and rate information can be found in Rule 38. Limits Of Liability

Cov. E $100,000 $300,000 $500,000 Expo-sure

Cov. F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000

Each Structure 12 13 16 16 17 20 18 19 22 Attach Endorsement HO440OR Structures Rented To Others - Residence Premises

Oregon – Personal Lines Homeowners Manual 37

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule 66. Residence Held in Trust When real and personal property is held in trust, coverage for the trust and trust members is afforded by this endorsement. The endorsement provides coverage for the grantor, beneficiary or trustee for:

• Coverage E - Personal Liability; and • Coverage F - Medical Payments to Others

Coverage under this endorsement applies only with respect to bodily injury or property damage arising out of the ownership, maintenance or use of the insured location owned by the trust. Rates for this option are displayed in the liability rate table in Rule 60. Attach Endorsement HO9443UN - Residence Held in Trust Rule 67. Home Day Care Liability Coverage The policy may be endorsed to provide liability coverage for the increased exposure arising from a home day care business on the residence premises. The endorsement provides for an annual aggregate limit of liability for Coverages E and F combined. Coverage F is subject to a sub-limit of liability which applies per person/per accident and does not increase the aggregate limit of liability. The aggregate limit of liability, Coverages E and F combined, for this endorsement is the same as the dollar amount of Coverage E shown in the Declarations. The Coverage F sub-limit for this endorsement is the same as the dollar amount of Coverage F shown in the Declarations. This premium is for 1, 2 or 3 persons, other than insureds, receiving day care services. If the day care business involves the care of more than 3 persons, the risk is not eligible for coverage under Unigard's Homeowner program. If the business is located in another structure on the residence premises, also refer to Rule 33. Home Day Care for rating the property exposure.

Limits Of Liability

Cov. E $100,000 $300,000 $500,000

Exposure Cov. F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000

1-3 Persons 100 105 119 133 138 152 149 154 168 Attach Endorsement 150200 Home Day Care Coverage - Bronze and Silver Programs - Oregon Attach Endorsement 150210 Home Day Care Coverage - Gold Program - Oregon

Oregon – Personal Lines Homeowners Manual 38

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule 68. Permitted Incidental Occupancies - Residence Premises and Other Residences The policy may be endorsed to provide coverage for the increased exposure arising from a permitted incidental occupancy on the residence premises or in another residence occupied by the insured. Limits Of Liability

Coverage E $100,000 $300,000 $500,000 Coverage F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000

Residence Premises (a)

19 24 38 25 30 44 28 33 47

Other Residence Occupied by Insured (b)

18 21 29 24 27 35 27 30 38

(a) Attach Endorsement 150230 Permitted Incidental Occupancies - Residence

Premises - Bronze and Silver Programs - Oregon (a) Attach Endorsement 150235 Permitted Incidental Occupancies - Residence

Premises - Gold Program - Oregon (b) Attach Endorsement HO2443OR Permitted Incidental Occupancies - Other Residence Rule 69. Business Pursuits Coverage may be provided for the personal liability of the Insured arising out of business activities. Coverage is excluded if Insured owns the business, is a partner, or maintains financial control in the business. Classifications A. Clerical Office Employees - Salesmen, Collectors or Messengers - No installation,

demonstration or servicing operations. B. Salesmen, Collectors or Messengers - Including installation, demonstration or servicing

operations. C. Teachers - Athletic, laboratory, manual training, physical training and swimming instruction,

excluding liability for corporal punishment of pupils. D. Teachers – Not otherwise classified - Excluding liability for corporal punishment of pupils.

Oregon – Personal Lines Homeowners Manual 39

Indicates Revision Unigard Insurance Company February 2011

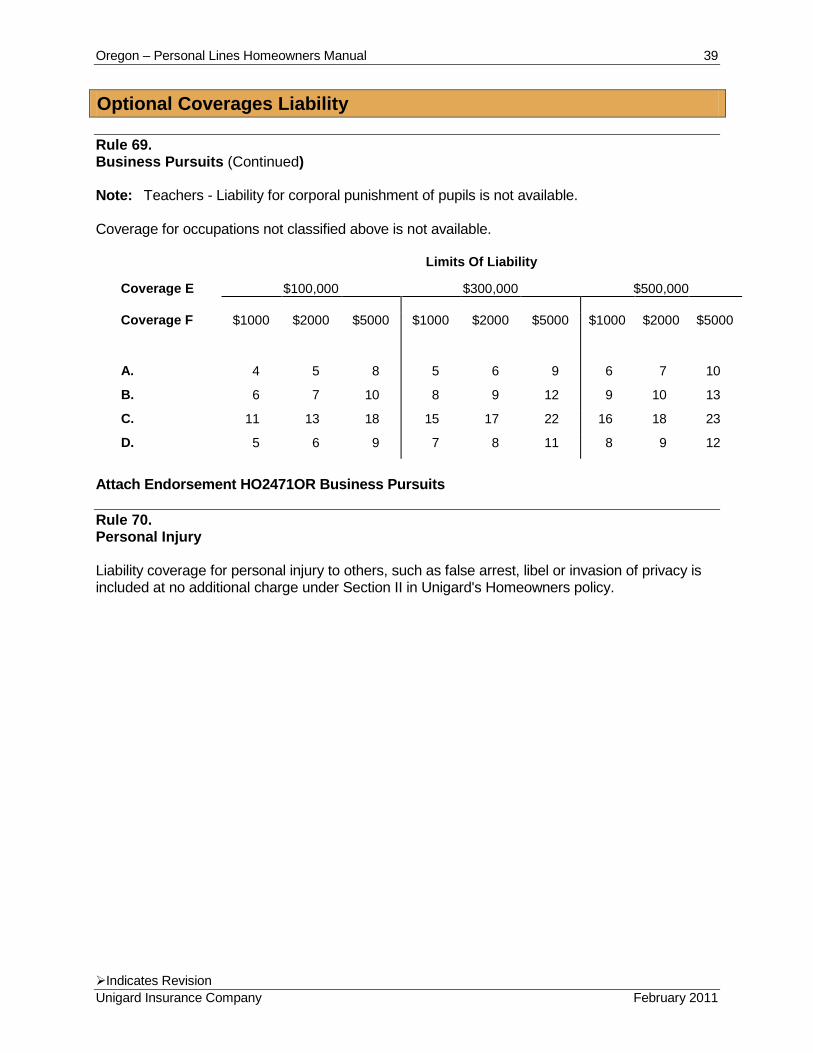

Optional Coverages Liability Rule 69. Business Pursuits (Continued) Note: Teachers - Liability for corporal punishment of pupils is not available. Coverage for occupations not classified above is not available. Limits Of Liability

Coverage E $100,000 $300,000 $500,000 Coverage F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000

A. 4 5 8 5 6 9 6 7 10

B. 6 7 10 8 9 12 9 10 13

C. 11 13 18 15 17 22 16 18 23

D. 5 6 9 7 8 11 8 9 12

Attach Endorsement HO2471OR Business Pursuits Rule 70. Personal Injury Liability coverage for personal injury to others, such as false arrest, libel or invasion of privacy is included at no additional charge under Section II in Unigard's Homeowners policy.

Oregon – Personal Lines Homeowners Manual 40

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule 71. Incidental Motorized Land Conveyances The policy may be endorsed to provide insurance under Coverages E and F for certain motorized land conveyances, with a 15 m.p.h. maximum attainable speed, which are not subject to motor vehicle registration. The following may not be covered: motorized bicycles, golf carts or mopeds, and all terrain vehicles (ATVs). Read the endorsement for conditions of coverage applying to eligible conveyances. Limits Of Liability

Coverage E $100,000 $300,000 $500,000 Coverage F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000

Each Conveyance 15 16 19 20 21 24 23 24 27

Attach Endorsement HO2413OR Incidental Motorized Land Conveyance Rule 72. Outboard Motors and Watercraft (Includes Inboards and Inboard-Outdrives) and Personal Watercraft A. Watercraft Liability Coverage

Coverage is included in the policy form, at no additional charge, for watercraft powered by an outboard engine or motor or a combination of outboard engines or motors of up to 50 horsepower, and sailboats less than 26 feet in overall length with or without auxiliary power. Coverage is available for an additional premium for watercraft less than 26 feet in length powered by outboard engines or motors, inboard engines or motors or inboard-outdrive engines or motors. Personal watercraft are small watercraft powered by an inboard engine and jet pump mechanism. They can have the capacity of either one, two or three persons. Coverage must be written to expiration of the policy, but it is permissible to stipulate for inboard-outdrive motorboats, the navigational period of each year. Premium shall be adjusted on a pro rata basis.

Oregon – Personal Lines Homeowners Manual 41

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule 72. Outboard Motors and Watercraft (Includes Inboards and Inboard-Outdrives) and Personal Watercraft (Continued)

Note 1: Accumulate total horsepower if two or more engines or motors of the same

horsepower are regularly used together with any single watercraft owned by the insured.

Note 2: If two or more engines or motors of different horsepower are regularly used together with any single watercraft, charge the liability rate for the motor or engine with the highest horsepower.

Coverage is not permitted under the Homeowners Policy for boats not described below. The premium in the state where the Insured's residence premises is located shall apply. However, if the Insured owns another residence premises in a different state and principally operates the boat from that residence, apply the premium for that state. Limits Of Liability

Coverage E $100,000 $300,000 $500,000 Coverage F $1000 $2000 $5000 $1000 $2000 $5000 $1000 $2000 $5000

1. Up to 15 feet Horsepower

51 to 100 15 16 21 20 21 26 23 24 29 101 to 150 27 29 37 36 38 46 41 43 51 151 to 200 34 36 44 43 45 53 48 50 58 201 to 250 42 44 52 53 55 63 59 61 69

2. 15 to 26 feet Horsepower

51 to 100 15 17 21 20 21 26 23 24 29 101 to 150 27 29 37 36 38 46 41 43 51 151 to 200 39 43 55 52 56 68 59 63 75 201 to 250 52 58 70 67 73 85 75 81 93 251 to 300 65 71 83 82 88 100 91 97 109

301 or more 78 84 96 97 103 115 107 113 125 Attach Endorsement 2475OR - Watercraft Liability

Oregon – Personal Lines Homeowners Manual 42

Indicates Revision Unigard Insurance Company February 2011

Optional Coverages Liability Rule 72. Outboard Motors and Watercraft (Includes Inboards and Inboard-Outdrives) and Personal Watercraft (Continued) B. Watercraft Medical Payments Coverage for Insureds

The policy may be extended to include Medical Payments for Watercraft Injury Coverage. This coverage provides protection for members of the insured’s family in the event an injury occurs out of the operation of or water-skiing from the insured watercraft. The additional premium is developed as follows:

Limit Of Liability Premium

$1,000 $14 $2,000 $19 $5,000 $34

Note: This coverage is available in all types of watercraft. Attach Endorsement 146610OR Watercraft Medical Payments Coverage for Insureds

C. Watercraft Physical Damage (Hull) Rates

Coverage for watercraft physical damage is available the following: boat and motor; trailer; and accessories. Please refer to Unigard’s separate boatowners Section for acceptability. The premium per $100 of coverage provided is developed as follows:

Deductible Premium $100 $1.30 $250 $1.20 $500 $1.00

Attach Endorsement 106980 Boatowners Endorsement

Oregon – Personal Lines Homeowners Manual 43

Indicates Revision Unigard Insurance Company February 2011