outlook for russia’s downstream industry, infrastructure ... · 1 context 1. russian oil products...

TRANSCRIPT

Outlook for Russia’s downstream industry, infrastructure

development and evolving export strategy

Maxim Nesmelov

Deputy Director of crude and oil products

trading Department, Head of products trading

E-mail: [email protected]

Antwerp, January 2014

1

Context

1. Russian oil products market overview

Refining throughput

Key events

2. Downstream modernization plan

Key goals

Schedule

Oil product balances

3. Rosneft refining position

Projects of new construction

Tuapse refinery portfolio

2

Introduction

“Russia’s crude refining throughput increased over recent

years… at the moment refinery industry is covering domestic demand in

full… In the period up to 2020 we expect huge flow of investments and a

number of new units are to be built along with modernization of existing

capacities.

Increase of technological effectiveness will allow reducing

refinery throughput up to 235mn t/year by 2030, but in the same time

ensuring stable growth of product output.”

Alexander Novak

Russia’s Energy Minister

Refining, mln. tn

Increase of conversion is the

key focus of Russian refining

industry upgrades not

throughput increase

150 156 168

-6%

2020

254

86

2017

260

104

2013

272

122

Light Heavy

10%

3

Refining throughput increases, effectiveness still low

0,0

5,0

10,0

15,0

20,0

25,0

Jan-1

1

Feb

-11

Ma

r-1

1

Apr-

11

Ma

y-1

1

Jun-1

1

Jul-1

1

Aug-1

1

Sep-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan-1

2

Feb

-12

Ma

r-1

2

Apr-

12

Ma

y-1

2

Jun-1

2

Jul-1

2

Aug-1

2

Sep-1

2

Oct-

12

No

v-1

2

De

c-1

2

Jan-1

3

Feb

-13

Ma

r-1

3

Apr-

13

Ma

y-1

3

Jun-1

3

Jul-1

3

Aug-1

3

Sep-1

3

Oct-

13

No

v-1

3

De

c-1

3

Motor gasoline

Jet

Diesel

Fuel oil

+6.4%

36,6

38,2

38,7

35,5

36,0

36,5

37,0

37,5

38,0

38,5

39,0

2011 2012 2013

Mogas

70,6

69,6

72,0

68,0

68,5

69,0

69,5

70,0

70,5

71,0

71,5

72,0

72,5

2011 2012 2013

Diesel

73,1

74,2

76,5

71,0

72,0

73,0

74,0

75,0

76,0

77,0

2011 2012 2013

Fuel oil

+5.7% +2.0% +4.6%

o Refining margins are high,

stimulating crude runs

o Pace of modernization was low

o Lack of sufficient investments

o Government’s taxation policy

bears fruits, but not enough time

4

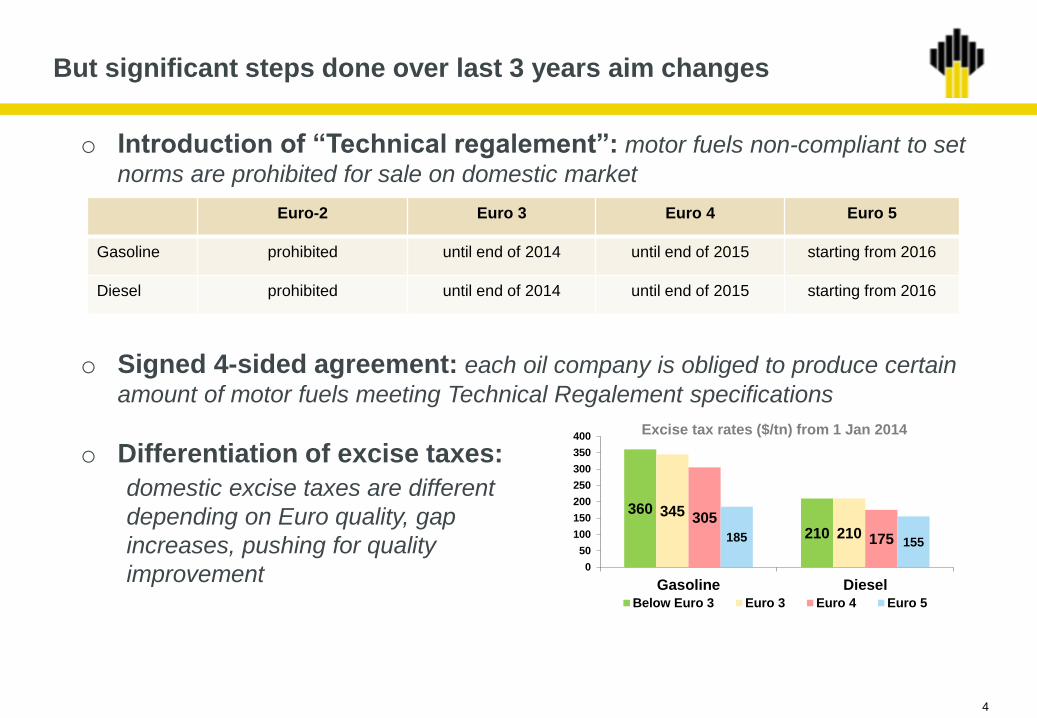

But significant steps done over last 3 years aim changes

o Introduction of “Technical regalement”: motor fuels non-compliant to set

norms are prohibited for sale on domestic market

o Signed 4-sided agreement: each oil company is obliged to produce certain

amount of motor fuels meeting Technical Regalement specifications

o Differentiation of excise taxes:

Euro-2 Euro 3 Euro 4 Euro 5

Gasoline prohibited until end of 2014 until end of 2015 starting from 2016

Diesel prohibited until end of 2014 until end of 2015 starting from 2016

360

210

345

210 305

175 185 155

0

50

100

150

200

250

300

350

400

Gasoline Diesel

Excise tax rates ($/tn) from 1 Jan 2014

Below Euro 3 Euro 3 Euro 4 Euro 5

domestic excise taxes are different

depending on Euro quality, gap

increases, pushing for quality

improvement

5

Government has proclaimed 3 key goals for Russian

refining industry upgrade campaign by 2020

• Increased motor fuel production

and Euro-5 compliance will remain

in focus in nearest years

Euro <5

Euro 5

2020

0%

100%

2012

70%

30%

• Minimal increase in crude units

capacities balanced by a closure

of simple refineries

• Key focus is on meeting demand

for gasoline and jet fuel

2020

66%

2012

55%

Source: Minenergo, Skolkovo business school

• Some experts estimate that 70% of Russian refining units have already exceed

their expected lifetime

• Key replacement goals:

−High health, security and environment standards

−Operations continuity

−Maximization of refinery utilization

−Decrease in labor due to automation & technology

Lights yield

(conversion)

Fuel

Standards

Replacement

of old units

1

2

3

126

89

Lights yield, %

Diesel fuel and gasoline production,

Mt

6

Key focus of refining upgrades is to meet motor fuels and jet fuel

demand

Source: Rosneft forecast, Petromarket

Gasoline

Diesel

Jet fuel

Fuel oil

Demand, mln. tn Supply, mln. tn

404033

+2%

2017 2012 2020

504536

+4%

2020 2012 2017

13129

+5%

2017 2012 2020

141416

2020 2012 2017

-1%

454535

2017 2012 2020

+3%

817354

+5%

2017 2020 2012

161510

2020

+6%

2017 2012

4054

76-8%

2020 2017 2012

• Mostly balanced with some

regional deficits

• Demand will be met through

secondary processes upgrades

• Always surplus export product

in Russia

• Overall demand growth will be

slightly above gasoline due to

increasing share of diesel

trucks

• The highest growing product

• Sufficient supply growth, since

most conversion upgrades are

middle distillates oriented

• New significant cracking

capacities

• Large export drop

• Growth in number of

passenger cars

• Growth in passenger

traffic

• Increase in fuel

efficiency of new

aircrafts

• Growth in number of

trucks

• Increase in fuel

efficiency

• Increase in fuel

efficiency

• Power generation

switching to natural gas

• Growth in bunker fuel

Demand level

7

2013 2014 2015 2016 2017

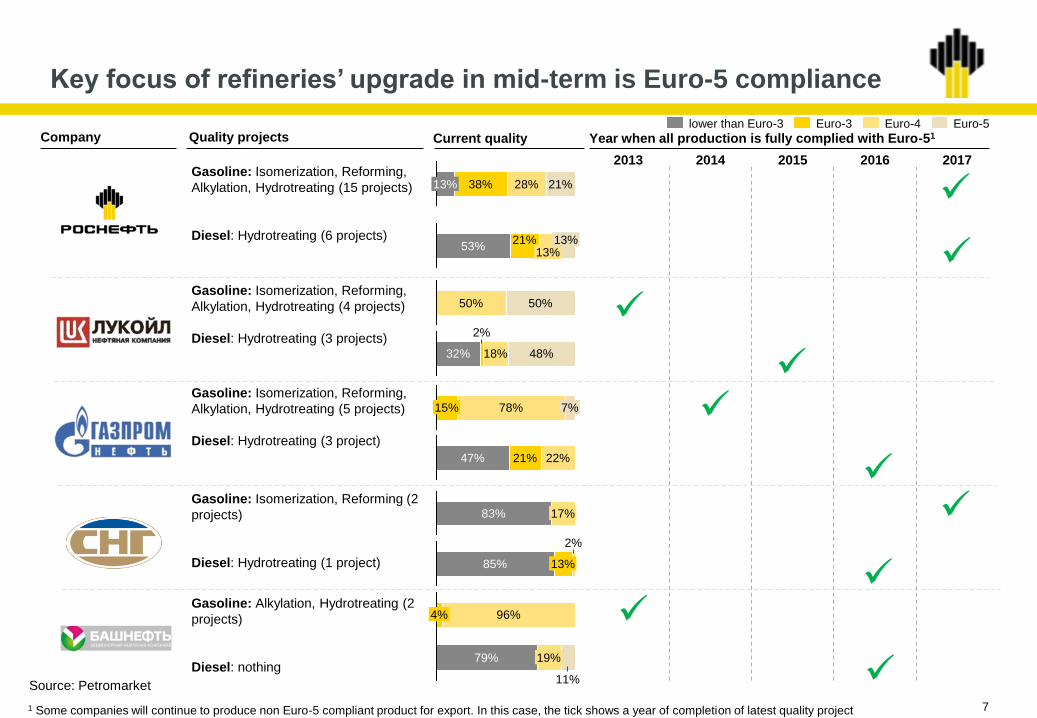

Key focus of refineries’ upgrade in mid-term is Euro-5 compliance

Company Quality projects

Gasoline: Isomerization, Reforming,

Alkylation, Hydrotreating (15 projects)

Diesel: Hydrotreating (6 projects)

Year when all production is fully complied with Euro-51 Current quality

Gasoline: Isomerization, Reforming,

Alkylation, Hydrotreating (4 projects)

Diesel: Hydrotreating (3 projects)

Gasoline: Isomerization, Reforming,

Alkylation, Hydrotreating (5 projects)

Diesel: Hydrotreating (3 project)

Gasoline: Isomerization, Reforming (2

projects)

Diesel: Hydrotreating (1 project)

Gasoline: Alkylation, Hydrotreating (2

projects)

Diesel: nothing

1 Some companies will continue to produce non Euro-5 compliant product for export. In this case, the tick shows a year of completion of latest quality project

13% 38% 28% 21%

Euro-3 Euro-4 Euro-5 lower than Euro-3

53% 21%

13% 13%

50% 50%

32%

2%

18% 48%

15% 78% 7%

47% 21% 22%

83% 17%

85% 13%

2%

4% 96%

79% 19%

11% Source: Petromarket

8

Implementation of modernization projects will lead to significant growth of

gasoil and gasoline supply (12 mln t gasoline and 20 mln t gasoil)

Company 2014 2015 2016 2017 2018 2019 2020

Rosneft Tuapse: AVT +1,6

Kuibyshev:

Isomerization +0,1;

Novokuibishevsk:

Isomerization +0,2;

Achinsk: CU +0,1;

Komsomolsk: HC VGO +0,7;

Syzran: FCC and MTBE +0,5;

Kuibyshev: FCC, alkylation, MTBE +0,9;

Angarsk: FCC, alkylation, MTBE +0,2; +0,2;

Ryazan: Isomerization -0,8; +0,4

Syzran: alkylation +0,1;

Novokuibishevsk: HC

VGO, рек. УЗК +0,1; +0,4;

Achinsk: HC VGO +1,6

Tuapse: HC VGO,

Isomerization,

Reformer +2,5; +2,6;

Ryazan: HT

gasoline FCC +1,0

Ryazan: HC

VGO, FCC:

+0,3;+0,9

BashneftUfa: FCC, AVT

+0,3; +0,6

Gasprom Neft

Moscow:

Isomerization, HT

gasoline: +0,3

Slavneft Yaroslavl: TAME +0,2

Surgutneftegas Kirishi: HC VGO +0,6

Kirishi:

Isomerization,

Riforming +0,9

Taif-NKVeba combi

cracking +0,3; +2,0

TatneftNizhnekamsk: HC

VGO +1,1

Nizhnekamsk:

Riforming,

Isomerization +1,0

GaspromSalavat: AVT +0,3;

+0,6

Salavat:

Isomerization. +0,4

Salavat: FCC +0,3 +0,1; Surgut: Isomerization

+0,5

Alliance Oil

Company

Khabarovsk: HC

VGO и HT diesel +1,4

Total +0,6; +5,3 +1,2; +0,9 +3,2; +2,9 +0,2; +3,8 +6,0; +2,6 +0,8; +3,7

Volgograd: FCC;

alkylate and MTBE

+0,6

LukoilVolgograd: AVT

+0,3; +0,1

Volgograd: AVT +0,2; +0,2; Perm: coking

+0,1; +1,2;

Nizhny Novgorod: Isomerization, FCC,

alkylation +1,1; +0,1

Volgograd: HC +1,8

Nizhny

Novgorod: HC

+0,5; +1,7

9

Due to ongoing conversion capacity increase projects Russia will remain

excessive in gasoline in next 10 years

Even if gasoline consumption continues to increase at CAGR 1,9% per year and key players implement announced

conversion capacity increase projects, Russia will remain excessive in gasoline up to 2022-2023.

Possible seasonal deficit in 2013-15 is covered with purchases from Belorussia

Gasoline balance in Russian Federation, mln tonnes

(scenario: only currently ongoing projects included in 4-side agreement)

-

10

20

30

40

50

60

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

* Announced but low probability projects are not taken into account

Rosneft

TNK-BP

Lukoil

Bashneft

Gazpromneft

Slavneft Surgutneftegaz Gazprom Other companies

Consumption

10

Diesel will remain export oriented commodity

Diesel production grows faster than its consumption

Diesel consumption growth is faster than gasoline - CAGR 3,5% versus 1,9%

Despite this, implementation of new conversion capacities for more diesel output will keep exported volumes

at 50% in next 10 years

-

20

40

60

80

100

120

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Diesel balance in Russian Federation, mln tonnes

(scenario: only currently ongoing projects included in 4-side agreement)

Rosneft

TNK-BP

Lukoil

Bashneft

Gazpromneft

Slavneft Surgutneftegaz Gazprom Other companies

Consumption

* Announced but low probability projects are not taken into account

11

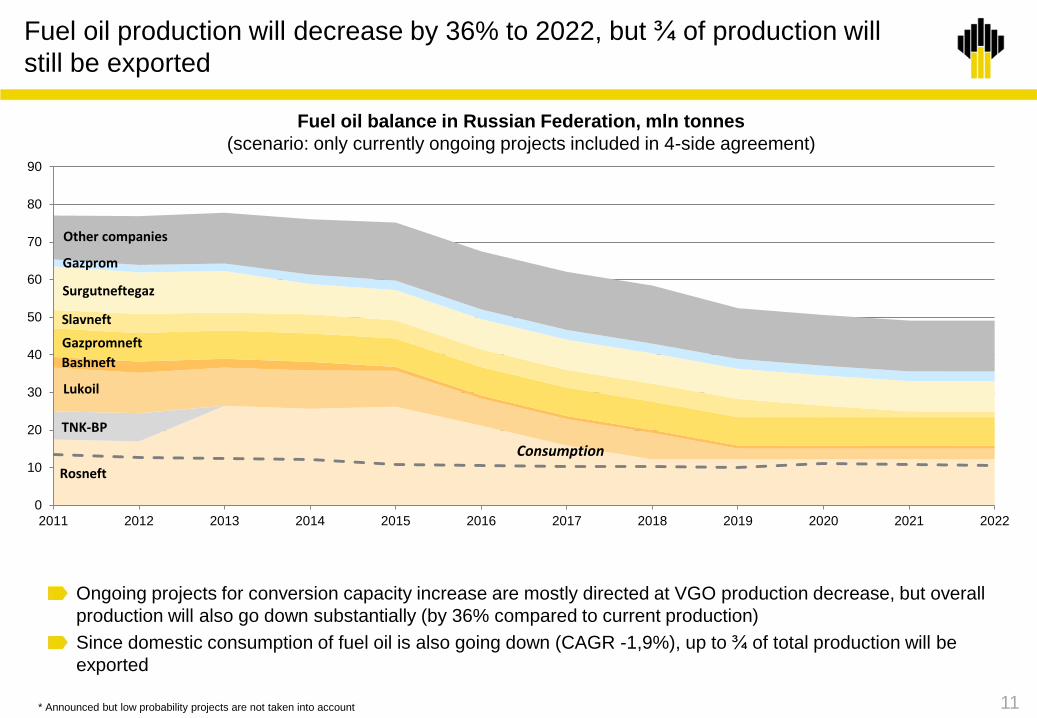

Fuel oil production will decrease by 36% to 2022, but ¾ of production will

still be exported

0

10

20

30

40

50

60

70

80

90

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Fuel oil balance in Russian Federation, mln tonnes

(scenario: only currently ongoing projects included in 4-side agreement)

* Announced but low probability projects are not taken into account

Ongoing projects for conversion capacity increase are mostly directed at VGO production decrease, but overall

production will also go down substantially (by 36% compared to current production)

Since domestic consumption of fuel oil is also going down (CAGR -1,9%), up to ¾ of total production will be

exported

Rosneft

TNK-BP

Lukoil

Bashneft

Gazpromneft

Slavneft

Surgutneftegaz

Gazprom

Other companies

Consumption

12

Jet fuel market will remain in surplus until 2022

0

2

4

6

8

10

12

14

16

18

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Jet fuel balance in Russian Federation, mln tonnes

(scenario: only currently ongoing projects included in 4-side agreement)

* Announced but low probability projects are not taken into account

Despite fast growth of jet fuel consumption (CAGR 4,9%), implementation of new conversion capacities for more

diesel output also leads to increased jet fuel production. This will keep surplus of jet fuel in Russia in next 10 years

Rosneft

TNK-BP

Lukoil

Bashneft

Gazpromneft

Slavneft Surgutneftegaz Gazprom Other companies

Consumption

13

Rosneft in the years 2008-2013 successfully implemented more than

20 projects for new construction and revamping of units and facilities

2008 2009 2010 2011 2012 2013 Refinery

Achinsk

Angarsk

Komsomolsk

Novokuibishevsk

Syzran

TNK-BP Refineries

Kuibyshev

Tuapse

• Isomerization

• Sulfur

production

• Hydrogen

production

• Hydrogen

production

• Isomerization

• Isomerization

(revamping)

• Reforming

• Isomerization

• Reforming

(revamping)

• Visbreaker

(revamping)

• Reforming

(revamping)

• Reforming

(revamping)

• Gasoline

blending

• Delayed coking

• «Wet

catalysis»

(revamping)

• Reforming

(revamping)

• LPG gantry

• Gasoline blending

• Visbreaking

(revamping)

• Revamping of

furnaces to gas

• Water supply

system

• Saratov isomerization

• Saratov crude unit

(revamping)

Integration of TNK-BP

• Crude unit

Total • New: 2 • New: 2 • New: 2

• Revamped: 3

• New: 2

• Revamped: 3

• New: 4

• Revamped: 2

• New 2

• Reforming

• Saratov diesel

HT

• Ryazan diesel

HT (revamping)

14

Rosneft refineries’ actual status and development

Process Samara Tuapse Komsomolsk Angarsk Achinsk Ryazan Saratov

Additional for

the second

processing, mln

t/y

Crude unit 12,0

Hydrocracking 12,0

Catalytic cracking 2,9

Coking/Flexicoking 1,0

Modernization Development Launch in 2012 Launch in 2013

Indexes/ Countries Russia Ukraine Belorussia Germany Italy Total

Number of refineries 10* 1 1 4 1 17

Capacity, mln. t/y 81,5* 6,4 2,6 11,6 15,0 127,3

Yield of light products 51,4% — 56,6% 72,9% 83,4% —

Modernization program of the Russian refineries

*Except for mini refineries, where the share of 50% in Yaroslavl and Tuapse aren’t working at full capacity

Data do not include Rosneft’s FEPCo project (first 12mn t/year stage scheduled for 2020)

15

Tuapse refinery – from topping to a new leader in Russia

Key success factors for Tuapse refinery:

• Strategic location:

Immediate proximity to large Southern Russian markets with growing demand

Close to Tuapse oil products terminal

which enables to flexibly distribute sales between export and internal trade channels

• Complete re-equipment of refinery, including:

Increase throughput from 5 to 12 mln. t./year

Achieve 90% lights yield

Achieve Nelson index of 8

3rd construction

stage 2018

11,4

0,7 0,0

6,5

4,4

0,1 2,0

1,4

0,9

0,4

2,2

0,8

4,3

3,7

0,5

11,9

2nd construction

stage 2017

0,7

2,4

1,0

Current

production 2012

Tuapse refinery production structure, mln.t

Tuapse

Saratov

Export to MED: Naphta,

Jet, Diesel, Fuel oil, etc.

Grozny

Filling stations

South Russia

LINIK

BATO TZK

Tuapse refinery in Rosneft portfolio

Bunker

Gasoline

Naphtha

Other

Fuel oil

Diesel

Jet

16

Conclusion

Russia’s refinery industry to develop in the coming years with goal

to meet Euro-5 standards and to increase conversion. Peak of

modernization is scheduled for 2016-2018

Government's taxation policy provokes for faster upgrades,

refining margins to decrease in 2015, but still attract a lot of

investments

Projected increase of diesel and gasoline supply unlikely to

change balances for motor fuels:

- Gasoline to remain domestic-oriented product with insignificant

surplus being exported during winter period

- Diesel exports are forecasted to stay on the same level with

euro-quality grades replacing high-sulfur flow

- major hit on exports is projected for fuel oil and naphtha

Rosneft to lead the industry: share both on domestic market and

exports – about 30pc