overview of differences between international financial ...file/ey - … · overview of differences...

TRANSCRIPT

Overview of Differencesbetween InternationalFinancial ReportingStandards and CzechAccounting Legislation2013

2

ContentsAuthors’ Comments 4

Financial Statements 5

Property, Plant and Equipment 10

Leases 13

Borrowing Costs 15

Investment Property 16

Intangible Assets 17

Inventories 19

Share-based Payment 21

Employee Benefits 22

Provisions, Contingent Liabilities and Contingent Assets 24

Financial Instruments 26

Non-current Assets Held for Sale and Discontinued Operations 30

Revenue 31

Construction Contracts 34

Impairment of Assets 35

Fair Value Measurement 37

Income Taxes 39

Consolidation and Business Combinations 40

3

IntroductionInternational Financial Reporting Standards (IFRS),i.e. a set of financial reporting standards issued by theInternational Accounting Standards Board (IASB) andrelated interpretations, rank among the most importantfinancial reporting standards in the world. These standardsdo not substitute generally applicable legislation, but forma principle-based accounting system designed primarily forlisted companies and large-scale businesses. Theapplication of the standards requires considerableprofessional skills of the assigned staff.

While not designated as generally applicable laws, IFRSmay be, to a greater or lesser extent, adopted in nationaland international legislation, depending on the type oflegal environment. In the Czech Republic, entities that arebusiness companies and issuers of securities listed in theregulated securities markets in the European UnionMember States currently use International FinancialReporting Standards as adopted by the European Union foraccounting purposes and for the preparation of financialstatements. Pursuant to an amendment to the AccountingAct, which came into effect on 1 January 2011, IFRS maybe applied in the preparation of separate financialstatements also by entities that are part of a consolidatedgroup that prepares consolidated financial statements inaccordance with IFRS.

Contrary to IFRS, Czech Accounting Standards (CAS) area national accounting system, based primarily on rules,which is subject to the EU regulatory requirements and theensuing obligations for the Czech Republic. As thecornerstone of Czech accounting legislation in its broadersense, the Accounting Act is the fundamental, generallyapplicable regulation nationwide, setting out accountingpolicies and financial reporting for all entities in thecountry’s territory, from the smallest to the largest(as well as multinational), whose scope and purpose ofbusiness may significantly differ. The form and content ofthe Act are governed not just by the requirements ofEuropean legislation, but also by Czech legislative rulesrequiring full compliance – material and terminological –with other regulations of the Czech legal system. Since theAct needs to be complied with – as mentioned above – evenby very small entities (sole traders, not-for-profitorganisations) that are unlikely to possess broadtheoretical knowledge of accounting and related fields, it is

instrumental that the text of the Act be as comprehensibleand unambiguous as possible.

Another factor affecting the Czech accounting rules andtheir application is that the income tax base is stillcomputed from results obtained in accordance with CAS.Consequently, in practice a great number of assumptionsmade by management in the preparation of financialstatements take into account potential tax implications ofthe selected accounting treatment. That might result inadopting accounting opinions based on tax impacts ratherthan on considerations of how to present a true and fairview of a transaction in its substance.

Given that each of the systems is based on differentpriorities and principles, there are many differences inboth conceptual and specific attributes. Any comparisonbetween the two systems is relatively difficult and hard toimplement in a simplified approach. Nonetheless, thisguide attempts to outline some of the differences.

The Overview of Differences between InternationalFinancial Reporting Standards (IFRS) and CzechAccounting Standards (CAS) follows a similar guidepublished in 2009. Due to a number of changesimplemented in the meantime, we decided to publisha new, updated version for 2013. The guide is written fromthe IFRS perspective and the sections are organisedaccording to specific standards.

We hope you find this guide useful.

Please do not hesitate to contact us with any questions.

Martin SkácelíkPartnerE-mail: [email protected].: +420 225 335 375

Alice MachováSenior managerE-mail: [email protected].: +420 225 335 169

4

Authors’ CommentsThis guide outlines the differences between IFRS and CASat the general level. For the purpose of this guide, IFRSmean a set of standards issued by the InternationalAccounting Standards Board, not International FinancialReporting Standards as adopted by the European Union.The guide is intended to provide general information onlyand is not for sale.

Obviously, no summary publication can fully encompass somany, often minor, differences between IFRS and CAS.Although some degree of harmonisation of thefundamental principles of IFRS and CAS has beenachieved, there are still significant differences in theirapplication that may have a material impact on financialstatements. The key focus is on the differences mostcommonly found in practice. When applying individualaccounting frameworks, readers must take into account allrelevant accounting regulations, standards and, whereapplicable, national legislation in their respectivecountries. In addition, listed companies must comply with

relevant regulations related to securities legislation, suchas decrees of the Czech National Bank.

The International Accounting Standards Board is currentlydeveloping a number of projects that will mostly havea significant impact on the existing standards. This guiderefers to IFRS standards effective at 1 January 2013 andcompares them with CAS that were in effect at 1 January2013. Where IFRS or IFRIC interpretations are mentionedthat came into force after this date, this fact is pointed outin the text. Czech Accounting Standards referred to in thisguide are those prescribed for entrepreneurs (except forspecific cases). The guide does not address any majordifferences pertaining to banks and other financialinstitutions, nor differences regarding IFRS orinterpretations that are perceived as less relevant in theCzech environment. Similarly, numerous differencesbetween IFRS and CAS in disclosure requirements are notaddressed either.

5

Financial Statements

Related IFRSs and IFRICs:

IAS 1 Presentation of Financial Statements

IAS 7 Statement of Cash Flows

IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors

IAS 21 The Effects of Changes in Foreign Exchange Rates

IFRS CAS

Financial statements Under IFRS, a complete set of financialstatements comprises: a balance sheet (nowknown as a statement of financial position),a statement of comprehensive income, ora separate income statement and a statement ofother comprehensive income (if preparedseparately from the statement of comprehensiveincome), a statement of changes in equity,a statement of cash flows, and notes (comprisinga summary of significant accounting policies andother explanatory information).

Financial statements are prepared for the currentperiod and the prior period. If an entity restatescomparable information retrospectively, it shallalso prepare a statement of financial position asat the beginning of the comparative period.

Under CAS, financial statements are an integralunit comprising: a balance sheet, an incomestatement and notes, including accountingpolicies and comments.

Financial statements are prepared for thecurrent period and the prior period. Entities tendto prepare a statement of changes in equity asthe primary statement, but they are allowed toinclude it in the notes to financial statements.The statement of cash flows is not required, butmost entities choose to prepare it.

Presentationcurrency

Under IFRS, profit or loss is reported in thepresentation currency. However, the statementsmay be adjusted and presented in anothercurrency.

CAS only allow the statements to be presented inCzech currency.

Balancesheet/statement offinancial position –format

IFRS do not prescribe any binding format fora balance sheet, but they set out the minimumscope. Entities classify assets and liabilities ascurrent and non-current, except whena presentation based on liquidity provides moredetailed information.

CAS prescribe a binding minimum scope, formatand description of items in an unconsolidatedbalance sheet. Entities may choose to classifyitems in more detail or, in specified cases, groupthem together.The format of the consolidated balance sheet isless structured.

6

IFRS CAS

Classification of non-current items

IFRS require that an entity distinguish betweencurrent and non-current items (unless thepresentation is based on liquidity).

An entity shall classify an asset as current whenit expects to sell or consume the asset in itsnormal operating cycle; it holds it primarily forthe purpose of trading; it expects to realise itwithin twelve months after the balance sheetdate; or the asset is cash or a cash equivalent.

An entity shall classify all other assets as non-current.

An entity shall classify a liability as current whenit expects to settle the liability in its normaloperating cycle or within twelve months after thebalance sheet date; it holds it primarily for thepurpose of trading; or it does not havean unconditional right to defer settlement of theliability for at least twelve months after thebalance sheet date.

An entity shall classify its financial liabilities ascurrent when they are due to be settled withintwelve months after the balance sheet date evenif the original term was for a period longer thantwelve months and an agreement to refinance, orto reschedule payments, on a long-term basis iscompleted after the balance sheet date andbefore the financial statements are authorisedfor issue.

An entity shall classify all other liabilities as non-current.

CAS require that an entity distinguish betweencurrent and non-current items, except foraccruals.

The classification of tangible and intangibleassets depends on their expected useful life(one year or longer) and the acquisition cost limitset by the entity with regard to presenting a trueand fair view of the items. Securities held for thepurpose of trading are classified as non-currentfinancial assets. The classification of receivablesand liabilities (including loans) depends on whenthey are due to be recovered/settled after thebalance sheet date (within one year or a periodlonger than one year).

7

IFRS CAS

Statement ofcomprehensiveincome – format

Under IFRS, the statement of comprehensiveincome shall include: profit or loss; othercomprehensive income; total comprehensiveincome (the sum of profit or loss and othercomprehensive income). The statement lists allchanges in comprehensive income that are nottransactions with owners.

An entity may prepare a single statement (thelong form of the statement) or two statements.The long-form statement includes an incomestatement and a statement of othercomprehensive income. If an entity presents twostatements, it prepares a separate incomestatement and a separate short-form statementof comprehensive income. The short-formstatement only comprises total profit or loss(without displaying its components) andcomponents of other comprehensive income. Thestandard does not prescribe any binding formatfor a profit or loss statement, but it sets out theminimum scope. Expenses must be disclosed byfunction or by nature.

The updated IAS 1 requires grouping of items ofcomprehensive income depending on whetherthey can be subsequently reclassified to profit orloss; i.e. the items that can be reclassified andthe items that cannot be reclassified.

CAS do not define a statement of comprehensiveincome.

CAS prescribe a binding format for anunconsolidated income statement. Expensesmust be disclosed by function or by nature.Entities may choose to classify items in moredetail or, in specified cases, group themtogether.

The format of the consolidated incomestatement is less structured.

Items of other comprehensive income areincluded in the summary of changes in equity(see below).

Exceptional andextraordinary items

IFRS do not specify the “exceptional items”category, but an entity presents separately itemsthat are material for the explanation of theentity’s financial performance (due to theiramount, nature or effect on profit or loss). Theseitems are presented either in the incomestatement/statement of comprehensive incomeor in the notes.

IFRS do not allow certain items to be presentedas “extraordinary”.

CAS do not specify the “exceptional items”category. The standard requires the explanationof material items of the financial statements, butdoes not allow the prescribed format to beamended.

In practice, exceptional items are reported withinextraordinary items or described in the notes.

Extraordinary items include transactions ofextraordinary nature in respect of the entity’sordinary course of business and randomlyoccurring events.

8

IFRS CAS

Statement ofchanges in equity

Under IFRS, the statement of changes in equitydiscloses for each component of equity changesresulting from: profit or loss; othercomprehensive income; transactions with ownersin their capacity as owners.

The statement includes information about totalcomprehensive income, showing separately thetotal amounts attributable to owners of theparent and to non-controlling interest; theeffects of retrospective application orretrospective restatement.

An entity is required to present a statement ofchanges in equity.

A statement of changes in equity is not requiredexcept for some selected entities. Changes inequity may be included in the notes to financialstatements instead of preparing a separatestatement of changes in equity.

Statement of cashflows

Under IFRS, the statement of cash flows shallreport cash flows classified by operating,investing and financing activities.

To prepare the statement, IFRS allow either thedirect method or the indirect method to be used.

An entity is required to present a statement ofcash flows.

CAS set out basic classification of cash flows andthe format of the statement for using theindirect method: cash flows from operating,investing and financing activities. Cash flowsrelated to extraordinary items, dividendcollection and payment (profit share) and incometax payment are reported separately.

To prepare the statement, CAS allow either thedirect method or the indirect method to be used.

An entity is not required to present a statementof cash flows, but most entities choose toprepare it (see above). A summary of cash flowsmay be included in the notes to financialstatements instead of preparing a separate cashflow statement.

Cash and cashequivalents -definition

Under IFRS, bank overdrafts (repayable ondemand) may be included in cash and cashequivalents. Conversely, short-term borrowingsare classified as cash flows from financingactivities and are not a component of cash andcash equivalents.

Cash equivalents are short-term investments thatare readily convertible to known amounts of cashand which are subject to an insignificant risk ofchanges in value.

Under CAS, stamps and vouchers (e.g. postalstamps, meal vouchers) are also included in cashequivalents, unlike IFRS which exclude theseitems.

Changes inaccounting policies

Under IFRS, voluntary changes in accountingpolicy are applied retrospectively in comparativeperiods. The resulting adjustment of comparativeinformation is made to the opening balance ofretained earnings for prior periods presented inthe financial statements.

Comparative information for prior periods is notadjusted if a new standard includes a specificexemption as a transitional provision.

The effects of changes in accounting policies arerecognised in equity as “other profit or loss forprior periods”.

9

IFRS CAS

Corrections ofmaterial errors

Under IFRS, corrections of material errors areapplied retrospectively in comparative periods. Ifan error occurred prior to the comparative periodpresented, an entity shall retrospectively restateand present the opening balance sheet of thecomparative period.

A prior period error is corrected in the period inwhich it is discovered. Financial statements,including comparative information for priorperiods, are restated as far back as ispracticable.

Corrections of material errors arising fromerroneous accounting or not accounting forexpenses and revenues in prior periods arerecognised in equity as “other profit or loss forprior periods”.

Changes inaccounting estimates

An entity may need to revise an estimate ifchanges occur in the circumstances on which theestimate was based or as a result of newinformation or more experience. By its nature,the revision of an estimate does not relate toprior periods and is not the correction of anerror. Changes in accounting estimates arerecognised in profit or loss in the current period.

Changes in accounting estimates are recognisedin profit or loss in the current period.

Notes IFRS require that a large scope of information isdisclosed in the notes to financial statements.Each standard specifies the required disclosures.

CAS only specify mandatory information relatedto the entity and the time of preparation offinancial statements, and generally requirean explanation of material items in the notes tofinancial statements.

10

Property, Plant and Equipment

Related IFRSs and IFRICs:

IAS 16 Property, Plant and Equipment

IFRS 13 Fair Value Measurement

IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

IFRIC 4 Determining whether an Arrangement Contains a Lease

IFRIC 12 Service Concession Arrangements

IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine

SIC 21 Income Taxes – Recovery of Revalued Non-depreciable Assets

IFRS CAS

Definition ofproperty, plant andequipment

Under IFRS, property, plant and equipment alsoinclude spare parts that are so-called strategicspare parts not intended for daily/regularconsumption.

Under CAS, spare parts are classified asinventories.

Assets available foruse

Depreciation of an asset begins when the asset isavailable for use.

CAS place a greater emphasis on meeting thelegal requirements for putting assets in use(e.g. issuance of an occupancy permit, legaltransfer of ownership, etc.). As a result, the dateof putting an asset in use may be later underCAS (it may affect the total amount ofcapitalised costs).

Initial recognition At cost. At cost. The definition of costs associated withthe acquisition of property, plant and equipmentis broader under CAS in comparison with IFRS(for instance, the disposal of existing buildingsfor the purpose of new development iscapitalised as part of the acquisition cost of thenewly developed asset).

Measurement ofinternally generatedassets

At cost. At accumulated cost – the costs may include partof the general overheads.

Restoration liabilities The initial estimate of the costs of dismantlingand removing the item and restoring the site onwhich it is located are part of the acquisition costof an item of property, plant and equipment andare offset by a provision. Any effects of changesin estimates on the level of provisions fordecommissioning and disposal are recognised asa change in the acquisition cost of an asset.

Not addressed.

11

IFRS CAS

Production strippingcosts

Stripping costs in the production phase ofa surface mine are accounted for as an additionto (an enhancement or a technical improvementof) an existing asset – a mineral ore deposit forwhich access has been improved by strippingactivity.

Production stripping costs are recognised if (i) itis probable that the future economic benefitassociated with the stripping activity will flow tothe entity; (ii) the entity can identify thecomponent of the ore body for which access hasbeen improved; and (iii) the costs relating to thestripping activity associated with that componentcan be measured reliably.

The stripping costs include the direct acquisitioncost plus an allocation of the directly attributableoverhead costs. They are classified in relation tothe existing asset with which they are associatedand are depreciated or amortised on a systematicbasis over the expected useful life of theassociated asset (which usually differs from theuseful life of the mine).

Not addressed. The definition of costs associatedwith the acquisition of property, plant andequipment is broader under CAS in comparisonwith IFRS.

Component approach A component is a specific part of an asset or ofa set of assets or a major inspection of faultswhose cost is significant in relation to the totalcost of the whole asset or set of assets andwhose useful life differs significantly from thatof an asset or of a set of assets.

Under the IFRS component approach, individualcomponents of an item of property, plant andequipment are recognised separately and,subsequently, depreciated separately.Depreciation methods are reviewed periodically.Residual values and useful lives are reviewed ateach balance sheet date.

Czech companies have been allowed to applydepreciation on a component basis. Unlike IFRS,the application of the component approach isoptional under CAS.

Companies using the component approach donot account for provisions for repairs ofproperty, plant and equipment.

Subsequentmeasurement andremeasurement ofassets

IFRS allow the traditional cost model where anitem of property, plant and equipment shall becarried at its cost less any accumulateddepreciation and any accumulated impairmentlosses. IFRS also allow the revaluation modelwhere after initial recognition an item ofproperty, plant and equipment shall be carried ata revalued amount, being its fair value at thedate of the revaluation less any subsequentaccumulated depreciation and subsequentaccumulated impairment losses.

CAS only allow the traditional cost model wherethe asset is carried at its cost less anyaccumulated depreciation and any accumulatedimpairment losses. Revaluation is only permittedin the case of company transformations andtransactions (contribution, divestment).

Residual valueconcept

IFRS apply the residual value concept for thedepreciation of property, plant and equipment(the carrying amount of an asset at the end of itsuseful life does not have to be zero).

CAS allow entities to apply the residual valueconcept for depreciation.

12

IFRS CAS

Impairment of assets IFRS require more detailed reviews of assets forimpairment performed according to therequirements specified in IAS 36 Impairment ofAssets (see a more detailed comparison in theImpairment of Assets section).

CAS allow a simplified approach to anassessment of assets for impairment.

Review of useful lifeand residual value ofan asset

IFRS expressly require that the useful life and theresidual value of an asset be reviewed at least ateach financial year-end. Changes in estimates, ifany, must be treated prospectively.

CAS require the reassessment of the useful lifeof an asset taking into account the manner inwhich the asset has been used and changes inthe pattern of its use.

Repairs andmaintenance

Generally, repairs and maintenance of property,plant and equipment are recognised in profit orloss as incurred. If asset overhauls qualify asa component of property, plant and equipment,they are recognised in the carrying amountof the asset.

Repairs and maintenance of property, plant andequipment are recognised in profit or loss. Theissue of overhauls is addressed by permittingrecognition of provisions.

Advances forproperty, plant andequipmentdenominated inforeign currencies

If non-refundable, advances for property, plantand equipment are treated as an integral part ofasset acquisition and, accordingly, the asset ismeasured at the original exchange rateprevailing at the time when the advance wasmade.

CAS classify advances for property, plant andequipment denominated in foreign currencies asfinancial assets that are measured at the currentexchange rate. The final acquisition cost of suchassets is therefore derived from the finalexchange rate.

Subsequent costs ofacquisition of anasset

Under IFRS, subsequent costs of acquisition aretreated consistently with the original acquisitioncost.

CAS adopt the technical improvement conceptset out in the Income Taxes Act.

Service concessionarrangements

Property, plant and equipment used undera service concession arrangement (provided theconditions defined in IFRIC 12 are met) arerecognised in the grantor’s balance sheet.The operator accounts for an intangible asset,a financial asset or their combination inaccordance with a specific contractualarrangement.

CAS do not expressly address service concessionarrangements. In practice, the business leaseconcept is often applied where property, plantand equipment are recognised in the operator’sbalance sheet.

13

Leases

Related IFRSs and IFRICs:

IAS 17 Leases

IFRIC 4 Determining whether an Arrangement Contains a Lease

IFRIC 12 Service Concession Arrangements

SIC 15 Operating Leases – Incentives

SIC 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease

SIC 32 Intangible Assets – Website Costs

The International Accounting Standards Board (IASB) is soon expected to issue a revised exposure draft on leases. The date ofthe final standard has not been announced yet.

The exposure draft no longer distinguishes between operating and finance leases; the new model would require lessees torecognise most leased assets and related liabilities on their balance sheets. New lease classification would be used principallyfor determining the method and timing for recognising lease revenue and expense. The classification would be based on theeconomic benefits of the underlying asset expected to be consumed by the lessee over the lease term. To apply that principle,the IASB provides criteria to consider based on whether the leased asset is property (i.e., land, building, part of a building) oran asset other than property (e.g., automobiles, machinery). For lessees, the recognition of lease-related assets could havesignificant implications in terms of financial performance indicators, debt ratios and borrowing capacity.

IFRS CAS

Definition of a lease An agreement whereby the lessor conveys to thelessee in return for a payment or series ofpayments the right to use an asset for an agreedperiod of time. Under IFRS, IAS 17 applies toa number of agreements that do not have thelegal form of a lease agreement. (e.g. some take-or-pay contracts, etc.).

CAS do not provide a specific definition ofa lease, the legal form of the transaction is ofprimary importance.

Classification ofleases

Under IFRS, a lease is classified either asa finance lease or as an operating lease.A finance lease transfers substantially all therisks and rewards incidental to ownership toa lessee. An operating lease is a lease that doesnot qualify as a finance lease. The standardprovides guidance on how to identify a financelease (e.g. the lease term, amount of leasepayments, option to purchase the asset at theend of the lease term, etc.)

CAS also differentiate between a finance leaseand an operating lease. A finance leasecustomarily comprises a prerequisite for thelessee’s purchase of the asset on expiry of thelease term. The Income Taxes Act stipulates theminimum lease term required for a lease to beclassified as a finance lease. CAS thereforeclassify leases according to the legal form ofthe transaction in contrast to IFRS wherethe economic substance is more material thanthe legal form.

Accounting for leases Under IFRS, recognition of a finance lease and anoperating lease differs.

CAS prescribe identical recognition of bothfinance and operating leases.

14

IFRS CAS

Accounting for anoperating lease

The lessor presents an asset subject to anoperating lease in the balance sheets. Leaseincome from operating leases is recognised inincome on a straight-line basis over the leaseterm (unless there is another systematic basiswhich is more suitable for lease incomeallocation).

The lessee recognises operating lease expenseson a straight-line basis over the lease term(unless there is another systematic basis whichis more suitable for lease expense allocation).

An asset under an operating lease is alsorecognised in the lessor’s balance sheet. Thelessor recognises lease income in accordancewith the terms of the operating lease contract(usually on a straight-line basis over the leaseterm).

The lessee recognises operating lease expensesin accordance with the terms of the operatinglease contract (usually on a straight-line basisover the lease term).

Accounting fora finance lease

An asset subject to a finance lease is, togetherwith the related liability, recognised in thelessee’s balance sheet. The lessor accounts forthe sale of an asset and the related receivable.The asset is depreciated by the lessee over thelease term; if there is no reasonable certaintythat the lessee will obtain ownership by the endof the lease term, the asset is depreciated overthe shorter of its useful life and the lease term.

An asset under a finance lease is accounted forusing the same method as an asset under anoperating lease.

Sale and leasebacktransactions

The accounting treatment of gains and lossesrealised by the lessee in a sale and leasebacktransaction depends on the nature of the leasecontract.

Sale and finance leaseback

If under IAS 17 a sale and leaseback transactionresults in a finance lease, any excess of salesproceeds over the carrying amount should not berecognised immediately as income bya seller/lessee. Instead, the excess is deferredand amortised over the lease term.

Sale and operating leaseback

If under IAS 17 a sale and leaseback transactionresults in an operating lease, any profit or lossshould be recognised immediately, unless theloss is compensated by future lease payments atbelow market price, in which case it should bedeferred and amortised in proportion to the leasepayments over the period for which the asset isexpected to be used. If the sale price is above fairvalue, the excess over fair value should bedeferred and amortised over the period for whichthe asset is expected to be used.

CAS treat sale and leaseback transactions asa separate sale transaction and a subsequentleaseback transaction regardless of the nature ofthe leaseback.

Disclosure IFRS require specified disclosures about financeand operating leases by both the lessee and thelessor.

CAS do not specify any requirements fordisclosure regarding leases; it merely requiresdisclosure about leased assets.

15

Borrowing Costs

Related IFRSs and IFRICs:

IAS 23 Borrowing Costs

IFRIC 12 Service Concession Arrangements

IFRS CAS

Accounting forborrowing costs

IAS 23 requires capitalisation of borrowing costsincurred in connection with the acquisition ofqualifying assets.

CAS currently allow borrowing costs to berecognised in profit or loss or for them to becapitalised.

Qualifying asset A qualifying asset is an asset that necessarilytakes a substantial period of time to get ready forits intended use or sale, such as property, plantand equipment and some inventories, etc.

An entity may decide whether it will capitaliseborrowing costs incurred in the acquisition ofproperty, plant and equipment and intangibleassets.

Capitalisation ofborrowing costs

Only those borrowing costs that are directlyattributable to the acquisition, construction orproduction of a qualifying asset and that wouldhave been avoided if the expenditure onthe qualifying asset had not been made may becapitalised. Borrowing costs are capitalised overthe period of construction, production andcompletion of the asset until it is ready for itsintended use or sale (the time of capitalisationmay differ under CAS and IFRS, see thedifferences in accounting for property, plant andequipment).

Interest on general/operating financing is alsocapitalised under IFRS if funds are borrowedgenerally and used for the purpose of obtaininga qualifying asset. The amount of borrowingcosts incurred in operating financing eligible forcapitalisation should be determined by applyinga capitalisation rate to the expenditures on thatasset.

All interest accrued on loans used specifically forthe construction of a qualifying asset arecapitalised less any investment income onthe temporary investment of an unused part ofthese specific borrowings.

Borrowing costs incurred in the acquisition ofproperty, plant and equipment or intangibleassets may be capitalised. CAS do not provideany other guidance.

16

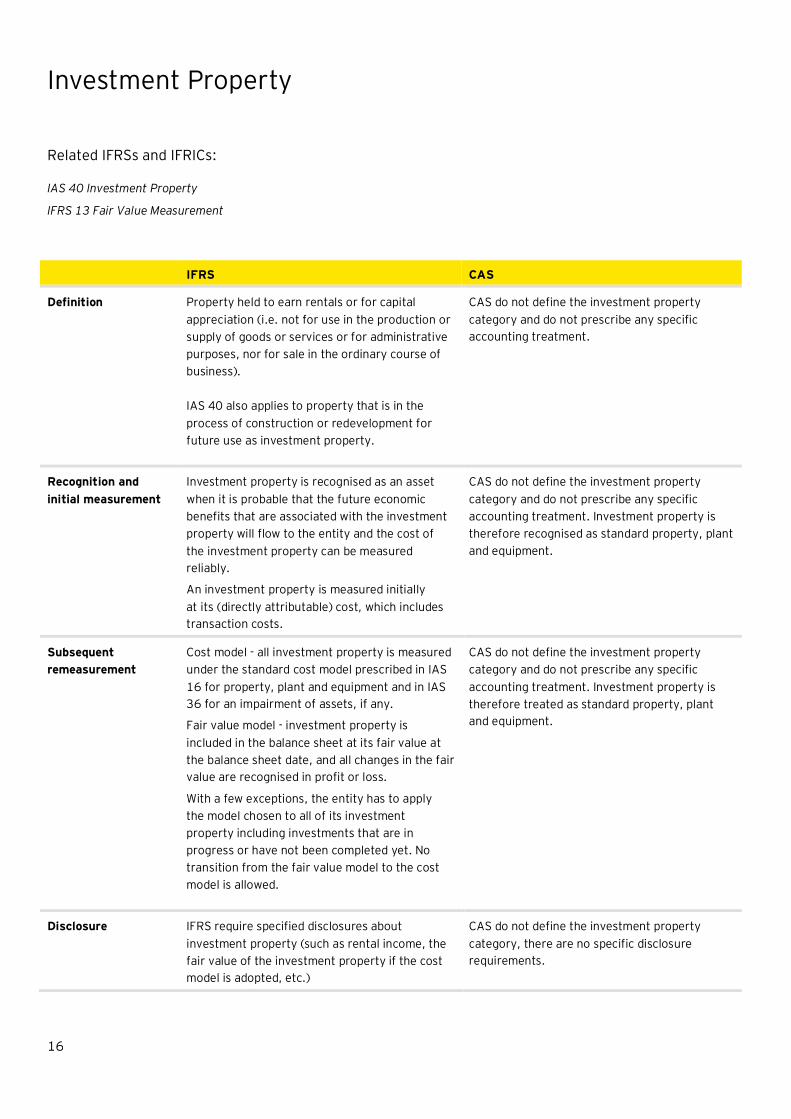

Investment Property

Related IFRSs and IFRICs:

IAS 40 Investment Property

IFRS 13 Fair Value Measurement

IFRS CAS

Definition Property held to earn rentals or for capitalappreciation (i.e. not for use in the production orsupply of goods or services or for administrativepurposes, nor for sale in the ordinary course ofbusiness).

IAS 40 also applies to property that is in theprocess of construction or redevelopment forfuture use as investment property.

CAS do not define the investment propertycategory and do not prescribe any specificaccounting treatment.

Recognition andinitial measurement

Investment property is recognised as an assetwhen it is probable that the future economicbenefits that are associated with the investmentproperty will flow to the entity and the cost ofthe investment property can be measuredreliably.

An investment property is measured initiallyat its (directly attributable) cost, which includestransaction costs.

CAS do not define the investment propertycategory and do not prescribe any specificaccounting treatment. Investment property istherefore recognised as standard property, plantand equipment.

Subsequentremeasurement

Cost model - all investment property is measuredunder the standard cost model prescribed in IAS16 for property, plant and equipment and in IAS36 for an impairment of assets, if any.

Fair value model - investment property isincluded in the balance sheet at its fair value atthe balance sheet date, and all changes in the fairvalue are recognised in profit or loss.

With a few exceptions, the entity has to applythe model chosen to all of its investmentproperty including investments that are inprogress or have not been completed yet. Notransition from the fair value model to the costmodel is allowed.

CAS do not define the investment propertycategory and do not prescribe any specificaccounting treatment. Investment property istherefore treated as standard property, plantand equipment.

Disclosure IFRS require specified disclosures aboutinvestment property (such as rental income, thefair value of the investment property if the costmodel is adopted, etc.)

CAS do not define the investment propertycategory, there are no specific disclosurerequirements.

17

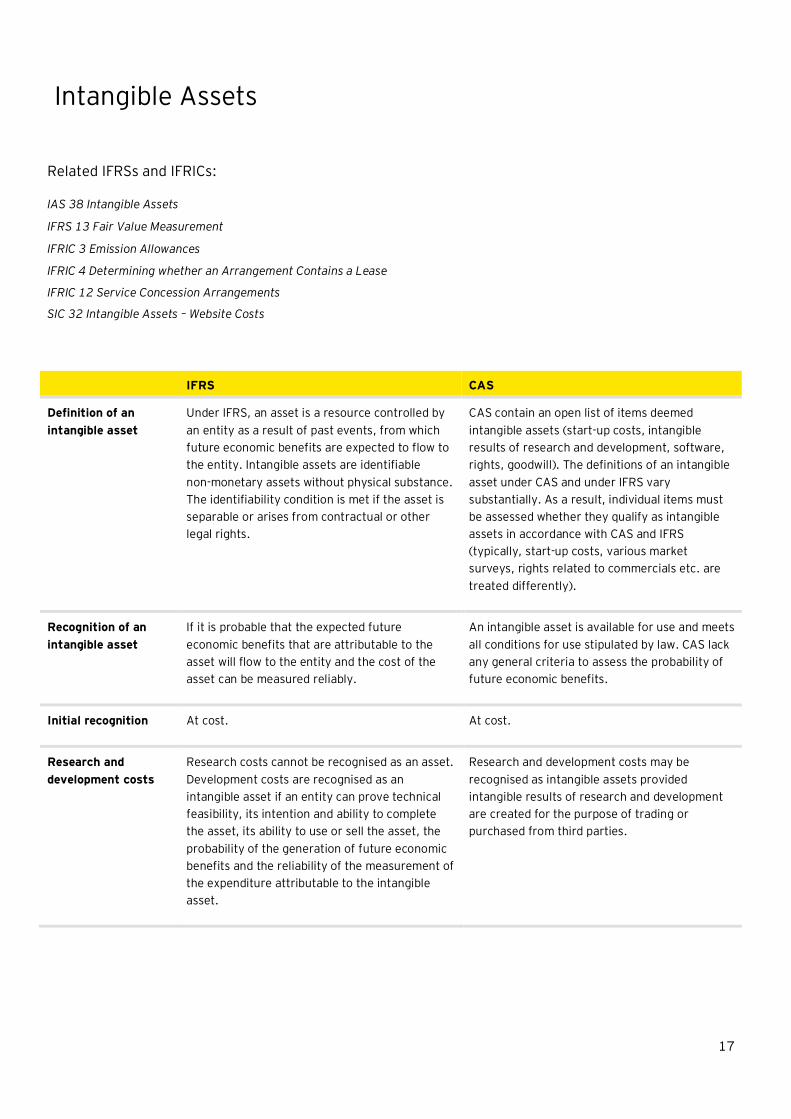

Intangible Assets

Related IFRSs and IFRICs:

IAS 38 Intangible Assets

IFRS 13 Fair Value Measurement

IFRIC 3 Emission Allowances

IFRIC 4 Determining whether an Arrangement Contains a Lease

IFRIC 12 Service Concession Arrangements

SIC 32 Intangible Assets – Website Costs

IFRS CAS

Definition of anintangible asset

Under IFRS, an asset is a resource controlled byan entity as a result of past events, from whichfuture economic benefits are expected to flow tothe entity. Intangible assets are identifiablenon-monetary assets without physical substance.The identifiability condition is met if the asset isseparable or arises from contractual or otherlegal rights.

CAS contain an open list of items deemedintangible assets (start-up costs, intangibleresults of research and development, software,rights, goodwill). The definitions of an intangibleasset under CAS and under IFRS varysubstantially. As a result, individual items mustbe assessed whether they qualify as intangibleassets in accordance with CAS and IFRS(typically, start-up costs, various marketsurveys, rights related to commercials etc. aretreated differently).

Recognition of anintangible asset

If it is probable that the expected futureeconomic benefits that are attributable to theasset will flow to the entity and the cost of theasset can be measured reliably.

An intangible asset is available for use and meetsall conditions for use stipulated by law. CAS lackany general criteria to assess the probability offuture economic benefits.

Initial recognition At cost. At cost.

Research anddevelopment costs

Research costs cannot be recognised as an asset.Development costs are recognised as anintangible asset if an entity can prove technicalfeasibility, its intention and ability to completethe asset, its ability to use or sell the asset, theprobability of the generation of future economicbenefits and the reliability of the measurement ofthe expenditure attributable to the intangibleasset.

Research and development costs may berecognised as intangible assets providedintangible results of research and developmentare created for the purpose of trading orpurchased from third parties.

18

IFRS CAS

Subsequentremeasurement

IFRS allow the traditional cost model wherea intangible asset shall be carried at its cost lessany accumulated amortisation and anyaccumulated impairment losses. IFRS also allowthe revaluation model where after initialrecognition a intangible asset shall be carried ata revalued amount, being its fair value at thedate of the revaluation less any subsequentaccumulated amortisation and subsequentaccumulated impairment losses.

CAS only allow the traditional cost model wherethe asset is carried at its cost less anyaccumulated amortisation and any accumulatedimpairment losses.

Amortisation period Both CAS and IFRS define useful life in a similarmanner. IFRS specify a category of intangibleassets that have an indefinite useful life. Goodwillis not amortised under IFRS.

CAS do not include a category of intangibleassets with an indefinite useful life. Goodwill,gain or loss on acquired assets and consolidationgain or loss are amortised over a defined periodunder CAS.

Residual valueconcept

IFRS apply the residual value concept foramortisation of intangible assets (the carryingamount of an asset at the end of its useful lifedoes not have to be zero).

CAS allow the residual value concept to beapplied for amortisation of intangible assets.

Impairment of anasset

IFRS require more detailed reviews of assets forimpairment performed according to therequirements specified in IAS 36 Impairment ofAssets (see a more detailed comparison in theImpairment of Assets section).

CAS allow a simplified approach to anassessment of assets for impairment.

Reassessment of theuseful life andresidual value of anintangible asset

IFRS expressly require that the useful lives andresidual values of assets be reviewed at least ateach financial year-end. Changes in estimates,if any, are recognised prospectively.

CAS require the reassessment of the useful lifeof an asset taking into account the manner inwhich the asset has been used and changes inthe pattern of its use.

Emission allowances IFRS currently do not provide specific guidanceon accounting for emission allowances. The netliability method is the most widely used inpractice (emission allowances allocated aremeasured at zero value and a provision isrecognised to cover their shortage, if any) or analternative approach according to the repelledIFRIC 3 interpretation (emission allowances areinitially recognised at fair value, witha corresponding government grant presented onthe balance sheet, and a provision for actualemissions is recognised at the fair value of theallowances at the balance sheet date).

Upon allocation, allowances are measured atreplacement cost, with a corresponding entryreflecting the grant received. Subsequently,allowances are used up in relation to the volumeof emissions and the received grant is amortisedto profit or loss.

CAS do not allow the net liability method.

Classification ofintangible assets

Intangible assets that are an integral part of therelated property, plant and equipment(e.g. operating systems) are accounted for aspart of the property, plant and equipment.

CAS do not classify software for technologymanagement or for equipment that cannot workwithout the relevant software as intangibleassets.

19

Inventories

Related IFRSs and IFRICs:

IAS 2 Inventories

IFRS CAS

Definition Inventories are assets held for sale in theordinary course of business; assets in theprocess of production for such a sale; or assets inthe form of materials or supplies to be consumedin the production process or in the rendering ofservices.

Under IFRS, some spare parts (so-called“strategic”) are treated as items of property,plant and equipment.

No general definitions are provided in CAS,specific inventory items are described within thescope of definitions of balance sheet items.

CAS classify spare parts as inventories.

Measurement Inventories are measured at the lower of costand net realisable value.

The cost of inventories comprises all costs ofpurchase, work in progress and other costsincurred in bringing the inventories to theirpresent location and condition. Overheads areincluded in the cost of inventories, but they donot include administrative overheads, and theallocation of fixed production overheads is basedon the normal capacity of the productionfacilities.

Inventories are measured at cost or ataccumulated costs, if produced internally.Temporary impairment of inventories should berecognised through allowances.

The costs of inventory produced internally neednot comprise production overheads inshort-cycle production. Administrativeoverheads may be included in the measurementof inventories with a long production cycle. CASdo not address allocation of overheads in detail.

Inventory impairment Allowances are recognised in the case ofa temporary diminution in value. Inventories arewritten down to their net realisable value; thepractice of writing inventories down below costto net realisable value is consistent with the viewthat assets should not be carried in excess ofamounts expected to be realised from their sale.No general allowances are allowed under IFRS.

The amount of the write-down may be reversed;the reversal is limited to the amount of theoriginal write-down.

CAS do not address the accounting treatmentof allowances in detail. For example, CAS do notspecify a) the IFRS requirement not to writedown the carrying amount of materials belowcost, even if the current market price is lower,in cases where the finished product in which thematerial will be incorporated is expected to besold at or above cost, or conversely, CAS doaddress b) general allowances, e.g. allowancesrecognised against slow-turnover inventory.

Similarly to IFRS, CAS allow the write-down to bereversed.

20

IFRS CAS

Capitalisation ofborrowing costs

IFRS require capitalisation of borrowing costsincurred in connection with the acquisition ofqualifying assets (see the Borrowing Costssection). Inventories that necessarily takea substantial period of time to get ready fortheir sale may be qualifying assets.

Under CAS, interest expense incurred inconnection with loans obtained for theacquisition of inventories cannot be capitalised.

Measurement ofinventories held fortrading

Under IFRS, an entity may choose to measureinventories held for trading either at fair valueless costs to sell or at the lower of cost and netrealisable value.

Not addressed.

21

Share-based Payment

Related IFRSs and IFRICs:

IFRS 2 Share-based Payment

IFRS 13 Fair Value Measurement

IFRIC 8 Scope of IFRS 2

IFRIC 11 IFRS 2 – Group and Treasury Share Transactions

SIC 12 Consolidation – Special Purpose Entities

IFRS CAS

Share-based payment IFRS specify three types of share-based paymenttransactions: equity-settled share-based paymenttransactions, cash-settled share-based paymenttransactions and share-based paymenttransactions with alternatives.

CAS do not expressly address share-basedpayment.

In practice, some entities recognise provisionsfor related costs.

Equity-settled share-based paymenttransaction

The transaction results in recognition of an assetor an expense with a corresponding increase inequity.

The transaction is measured at the fair value ofthe goods or services received and, in the case oftransactions with employees providing services,at the fair value of the equity instrumentsgranted.

CAS do not expressly address share-basedpayment.

Cash-settled share-based paymenttransaction

The transaction results in the recognition ofan asset or an expense against a liability (not inan increase in equity).

The transaction is measured at the fair value ofthe liability that is remeasured to fair value ateach reporting date, with any changes in fairvalue recognised in profit or loss.

CAS do not expressly address share-basedpayment.

Share-based paymenttransaction with cashalternatives

Transactions with alternatives are recognised asa cash-settled share-based payment transactionif the entity has incurred a liability to settle incash or other assets, or as an equity-settledshare-based payment transaction if no suchliability has been incurred.

CAS do not expressly address share-basedpayment.

22

Employee Benefits

Related IFRSs and IFRICs:

IAS 19 Employee Benefits

IFRIC 14 IAS 19 – The Limit on a Defined Benefit Asset, Minimum Funding Requirements and their Interaction

IFRS CAS

Definition ofemployee benefits

IAS 19 Employee Benefits establishes fourcategories of employee benefits as follows:

• Short-term employee benefits

• Post-employment benefits

• Other long-term employee benefits

• Termination benefits.

Post-employment benefits comprise definedcontribution plans and defined benefit plans.

CAS do not contain specific classification ofemployee benefits.

Short-term employeebenefits

Benefits payable within 12 months of the end ofthe period. The related liability and expense areaccrued and measured on an undiscounted basis.A liability arising from accrued vacation not usedby an employee is also recognised under IFRS.

CAS do not expressly address short-termemployee benefits. Expenses are recognised inthe period to which they relate. In practice,entities recognise provisions or estimates foraccrued vacation.

Defined contributionplans

Benefit plans under which an entity pays fixedcontributions into another entity and has noobligation to pay further contributions. Expensesand liabilities are recognised in the period inwhich an employee renders the related service.

CAS do not provide specific guidance regardingthe issue; an accounting treatment similar tothat under IFRS is applied in practice.

Defined benefitplans - definition

Any post-employment benefit plans that do notqualify as defined contribution plans are treatedas defined benefit plans.

CAS do not provide specific guidance on definedbenefit plans.

Defined benefitplans – amountpresented in balancesheet

A defined benefit plan obligation is measuredusing the Projected Unit Credit Method (actuarialmethod), which sees each period of service asgiving rise to an additional unit of benefitentitlement and measures each unit separately tobuild up the final obligation.

The amount recognised as a liability (asset) shallbe the net total of the following:

• The present value of the defined benefitobligation at the balance sheet date minus

• The fair value of plan assets at the balancesheet date.

In the case of a defined benefit plan surplus, theresulting net asset is measured at the lower ofthe defined benefit plan surplus and the assetmaximum amount (“asset ceiling”).

CAS do not provide specific guidance on definedbenefit plans.

In practice, liabilities are recognised throughprovisions.

23

IFRS CAS

Defined benefitplans – actuarialgains and losses

Actuarial gains and losses are changes in thepresent value of a liability or in the fair value ofplan assets arising from changes in actuarialassumptions (e.g. changes in discount rates).

Actuarial gains and losses are recognised inother comprehensive income.

CAS do not provide specific guidance on definedbenefit plans.

Defined benefitplans – past servicecost

Past service cost results from changes in benefitsthat are payable for past service underan existing defined benefit plan. Past service costis recognised as an expense on a straight-linebasis over the average period until the benefitsbecome vested.

CAS do not provide specific guidance on definedbenefit plans.

Other long-termbenefits

Long-term benefits not classified in othercategories (such as jubilee benefits). Other long-term benefits are measured using the ProjectedUnit Credit Method (actuarial method), with anyactuarial gains and losses and past service costrecognised immediately in profit or loss.

CAS do not provide specific guidance on otherlong-term benefits.

In practice, liabilities are recognised throughprovisions.

Termination benefits The principles governing the recognition ofa termination benefit liability are similar to thosefor a restructuring provision (i.e. it is recognisedwhen there is a detailed formal plan forrestructuring which was made public or whoseimplementation has started).

CAS do not provide specific guidance regardingthe issue; an accounting treatment similar tothat under IFRS is applied in practice.

Social fund Under IFRS, equity accounts are not used torecognise employee benefit transactions. Equityaccounts are restricted for transactions withshareholders or for other transactions specifiedby IFRS.

Under CAS, a social fund is recognised in equityaccounts in some cases.

24

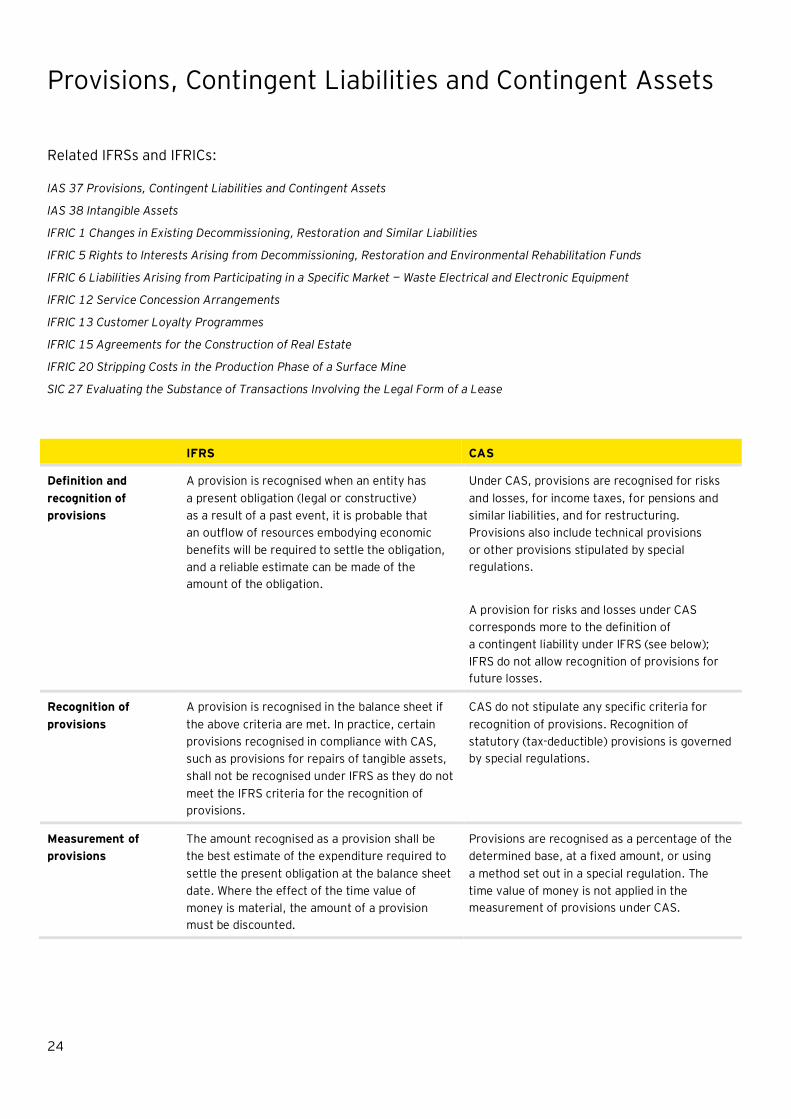

Provisions, Contingent Liabilities and Contingent Assets

Related IFRSs and IFRICs:

IAS 37 Provisions, Contingent Liabilities and Contingent Assets

IAS 38 Intangible Assets

IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

IFRIC 5 Rights to Interests Arising from Decommissioning, Restoration and Environmental Rehabilitation Funds

IFRIC 6 Liabilities Arising from Participating in a Specific Market — Waste Electrical and Electronic Equipment

IFRIC 12 Service Concession Arrangements

IFRIC 13 Customer Loyalty Programmes

IFRIC 15 Agreements for the Construction of Real Estate

IFRIC 20 Stripping Costs in the Production Phase of a Surface Mine

SIC 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease

IFRS CAS

Definition andrecognition ofprovisions

A provision is recognised when an entity hasa present obligation (legal or constructive)as a result of a past event, it is probable thatan outflow of resources embodying economicbenefits will be required to settle the obligation,and a reliable estimate can be made of theamount of the obligation.

Under CAS, provisions are recognised for risksand losses, for income taxes, for pensions andsimilar liabilities, and for restructuring.Provisions also include technical provisionsor other provisions stipulated by specialregulations.

A provision for risks and losses under CAScorresponds more to the definition ofa contingent liability under IFRS (see below);IFRS do not allow recognition of provisions forfuture losses.

Recognition ofprovisions

A provision is recognised in the balance sheet ifthe above criteria are met. In practice, certainprovisions recognised in compliance with CAS,such as provisions for repairs of tangible assets,shall not be recognised under IFRS as they do notmeet the IFRS criteria for the recognition ofprovisions.

CAS do not stipulate any specific criteria forrecognition of provisions. Recognition ofstatutory (tax-deductible) provisions is governedby special regulations.

Measurement ofprovisions

The amount recognised as a provision shall bethe best estimate of the expenditure required tosettle the present obligation at the balance sheetdate. Where the effect of the time value ofmoney is material, the amount of a provisionmust be discounted.

Provisions are recognised as a percentage of thedetermined base, at a fixed amount, or usinga method set out in a special regulation. Thetime value of money is not applied in themeasurement of provisions under CAS.

25

IFRS CAS

Provisions for assetdisposal

An initial amount of provision is capitalised aspart of the cost of the related asset. Anysubsequent changes in estimates for the level ofprovisions are recognised as a change in the costof an asset.

CAS do not set out any specific requirements forthe recognition of provisions for the disposal ofassets, i.e. such provisions are accounted for asany other provisions.

Provision for onerouscontracts

Generally, provisions shall not be recognised forfuture operating losses. However, if an entity isa party to an onerous contract (in which theunavoidable costs of meeting the obligationsunder the contract exceed the economic benefitsexpected to be received under it), the presentobligation under the contract shall be recognisedas a provision.

CAS do not expressly address the issue ofonerous contracts; general requirements applyfor recognition of provisions for anticipated risksand losses.

Contingent liabilities Contingent liabilities are possible obligations as ithas yet to be confirmed whether an entity hasan obligation that could lead to an outflow ofresources embodying economic benefits, orpresent obligations that do not meet the criteriafor the recognition of provisions (see above).Contingent liabilities are not recognised, onlydisclosed.

CAS do not provide any definition ofa contingent liability.

26

Financial InstrumentsRelated IFRSs and IFRICs:

IAS 32 Financial Instruments: Presentation

IAS 39 Financial Instruments: Recognition and Measurement

IFRS 7 Financial Instruments: Disclosures

IFRIC 2 Members’ Shares in Co-operative Entities and Similar Instruments

IFRIC 5 Rights to Interests Arising from Decommissioning, Restoration and Environmental Rehabilitation Funds

IFRIC 9 Reassessment of Embedded Derivatives

IFRIC 10 Interim Financial Reporting and Impairment

IFRIC 12 Service Concession Arrangements

IFRIC 16 Hedges of a Net Investment in a Foreign Operation

IFRS 19 Extinguishing Financial Liabilities with Equity Instruments

SIC 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease

IFRS 9 Financial Instruments1

As mentioned in the Introduction, the following section summarises the differences between IFRS and CAS applicable toentrepreneurs other than financial institutions. CAS for financial institutions may differ in some areas from how it is describedbelow:

1 The standard has not yet been finalised; so far, only the “Classification and Measurement” phase has been published.Moreover, the standard has yet to pass through the EU endorsement process.

27

IFRS CAS

Classification offinancial instruments

IFRS establish four categories of financial assetsand two categories of financial liabilities asfollows:

• Financial assets at fair value through profit orloss (“FVTPL”);

• Held-to-maturity investments (“HTM”);

• Loans and receivables (“LAR”);

• Available-for-sale financial assets (“AFS”);

• Other financial liabilities.

Under CAS, balance sheet items are primarilyclassified as current and non-current.

Financial assets are (directly or indirectly)classified into the following categories:

• Securities (and receivables) held for trading(non-current);

• Securities held to maturity (current and non-current);

• Other securities2 (current and non-current);

• Loans, bank deposits, receivables andadvances granted (current and non-current).

The classification of financial liabilities is similar:

• Issued bonds (current and non-current);

• Loans, payables and advances received(current and non-current).

“Other securities” virtually correspond to theavailable-for-sale category of financial assetsunder IFRS. Similarly, securities held to maturitycorrespond to held-to-maturity investmentsunder IFRS. In contract, CAS do not containan explicit specification of the held-for-tradingcategory for assets (generally) and liabilities;e.g. under CAS fair values of derivatives arereported within receivables/payables while underIFRS these are classified as FVTPL. For thedifferences between the other categories, referbelow.

Financial assets andliabilities at fair valuethrough profit or loss

The category includes the following:

• Assets and liabilities held for trading, includingderivatives;

• Assets and liabilities initially classified as at fairvalue through profit or loss. Generally, any assetcan be classified in this category if it results inmore relevant information for the financialstatements’ users, i.e. if the use of fair valueeliminates or significantly reduces inconsistency,and the portfolio of financial assets and liabilitiesis managed on a fair value basis. In addition,a contract containing one or more embeddedderivatives that otherwise would have to beseparated may be initially designated as FVTPL.

CAS only contain the category of securities andreceivables held for trading, which are financialassets held for trading for the purpose ofgenerating a profit from short-term fluctuationsin price (12 months at a maximum).

Unlike under IFRS, no asset may be initiallyclassified in this category to eliminatemeasurement inconsistencies.

Derivatives are also classified in this category(although this is not specifically stated andalthough they are presented within Otherreceivables/payables in the balance sheet). Thisis due to the fact that under CAS derivativesmust be measured at fair value and reported infinance income or cost.

2 Available-for-sale securities

28

IFRS CAS

Loans andreceivables

This category includes financial assets with fixedor determinable payments that are not quoted inan active market, that do not qualify for theFVTPL or AFS categories and that do not meetthe condition of the holder not recoveringsubstantially all of its initial investment, otherthan because of credit deterioration.

Under CAS, loans and receivable are not definedas a specific category of financial instruments.However, financial assets of this type arepresented in a way similar to IFRS, unlessdesignated by an entity as held for trading.Loans and receivables that have been acquiredand designated by the entity as held for tradingare remeasured at fair value with changesreported in finance income or cost. Thiscorresponds to the procedure applied underIFRS; however, under IFRS such loans would beclassified as FVTPL.

What is different is the treatment of receivablesoriginated by the entity (i.e. when the entity hassold goods or provided services) that will not beheld to maturity as the entity intends to sellthem before they become due. Under IFRS,these receivables are classified as FVTPL; underCAS originated loans may neither be classified inthis category nor remeasured at fair value.As mentioned above, only acquired receivablesmay be remeasured.

Initial measurement A financial asset or a financial liability is initiallyrecognised at fair value; for financial assets andliabilities other than those classified as FVTPL,the fair value is adjusted for directly attributabletransaction costs (or specific income, see below).

Loans and receivables (unless acquired forconsideration or by contribution) and payablesare initially measured at nominal value.

Other financial assets and liabilities are initiallyrecognised at cost plus acquisition-related costs.

Recognition ofinterestincome/expense

The effective interest method is required to beused for the subsequent remeasurement offinancial instruments measured at amortised cost(i.e. of financial instruments classified as LAR orHTM and of other financial liabilities) and for therecognition of interest income/expense. Over theperiod to expected maturity, the methodallocates to interest income/expense not onlycontractual interest, but also other items, suchas the above mentioned transaction costs andcertain specific income (e.g. a fee for theprovision of loan). The income statementprovides information about effective interestincome/expense.

For financial assets classified as AFS, the methodis required to be applied to report interestincome.

The effective interest method is not definedunder CAS; accordingly, it may not be applied onitems initially measured at nominal value toaccrue the related (transaction) costs.

Interest income/expense corresponds tocontractual interest (for financial instrumentsother than discounted securities where interestincome/expense corresponds to the differencebetween the nominal value and cost).

For securities held to maturity, the differencebetween cost and nominal value is reported inprofit or loss (as either finance income or cost,as appropriate), taking into account the accrualprinciple. As CAS do not provide specificguidance on accounting for interest income andinterest expense, practical approaches maydiffer, particular with the issue of long-term debt(direct expense vs. some form of accruals).

29

IFRS CAS

Derecognition offinancial assets

IFRS provisions governing the derecognition offinancial assets are fairly complex. The transferof risks and rewards and of control is decisive forthe derecognition of a financial asset.

CAS for entrepreneurs do not provide detailedguidance on derecognition. Additional guidancecan be found in Accounting Standards forFinancial Institutions. The derecognitionprinciple is also based on the transfer of control;however, no examples specifying the meaning ofthe transfer of control are provided. Moreover,the risk and reward concept is not applied.

Impairment offinancial assets

IFRS provide guidance concerning objectiveevidence that a financial asset or group offinancial assets is impaired.

An entity shall assess whether objective evidenceof impairment exists individually for financialassets that are individually significant, andcollectively for insignificant financial assets andfor significant financial assets that have beenindividually assessed, but for which there is noobjective evidence of impairment.

For financial assets classified as LAR or HTM, theamount of the loss is measured as the differencebetween the asset’s carrying amount and thepresent value of estimated future cash flows.Future cash flows from financial assets that aredebt instruments are discounted at the financialasset’s original effective interest rate,i.e. the effective interest rate computed at initialrecognition.

For financial assets classified as AFS, the amountof the loss is measured as the difference betweenthe asset’s fair value and amortised cost.

CAS do not specify objective evidence indicatingthat a financial asset is impaired and thatallowances should be recognised. Allowancesonly cover a temporary diminution in value ofassets (or, in the case of available-for-salesecurities, a diminution in value that is probablypermanent).

CAS provide no guidance on individual andsubsequent collective assessment of financialassets for impairment.

In addition, there is no detailed specification ofhow to compute impairment losses.

Embeddedderivatives

IFRS require that an embedded derivative beseparated if the economic characteristics andrisks of the embedded derivative differ fromthose of the host contract.

IFRS provide examples illustrating when theeconomic characteristics and risks of theembedded derivative differ and when theydo not.

Under CAS, accounting for embeddedderivatives is not obligatory, i.e. entrepreneurshave an option to do so. The conditions underwhich an embedded derivative is separated fromthe host contract are the same as under IFRS.What is different is the list of examples wherethe economic characteristics and risks of theembedded derivative are not closely related tothe host contract or, conversely, where thisrelationship is deemed close.

30

Non-current Assets Held for Sale and DiscontinuedOperations

Related IFRSs and IFRICs:

IFRS 5 Non-current Assets Held for Sale and Discontinued Operations

IFRS 13 Fair Value Measurement

IFRS CAS

Assets classified asheld for sale –definition

Under IFRS, a non-current asset is classified asheld for sale if its carrying amount shall berecovered principally through a sale transactionrather than through continuing use over itsuseful life.

A non-current asset is classified as held for saleif it is available for immediate sale and its saleis highly probable.

CAS do not establish the category of held-for-sale non-current asset and discontinuedoperations; no specific guidance provided.

Assets classified asheld for sale –measurement

At the lower of carrying amount (at the time ofreclassification to assets held for sale) and fairvalue less costs to sell.

CAS provide no guidance on this asset group –treated as a standard non-current asset.

Assets classified asheld for sale –depreciation

Assets are not depreciated. CAS provide no guidance on this asset group –treated as a standard non-current asset.

Assets classified asheld for sale –presentation

Presented separately on the face of the balancesheet within current assets or liabilities.

CAS provide no guidance on this asset group –treated as a standard non-current asset.

Discontinuedoperations –presentation

A discontinued operation is a separate line ofbusiness or geographical area of operations(taking into account its materiality) that eitherhas been disposed of, or is classified as held forsale. Under IFRS, an entity must providespecific disclosures about discontinuedoperations, including the separate profit or lossof the discontinued operation.

CAS do not address discontinued operations and,accordingly, no specific disclosures are required.

31

Revenue

Related IFRSs and IFRICs:

IAS 18 Revenue

IFRIC 12 Service Concession Arrangements

IFRIC 13 Customer Loyalty Programmes

IFRIC 15 Agreements for the Construction of Real Estate

IFRIC 18 Transfers of Assets from Customers

SIC 13 Jointly Controlled Entities — Non-monetary Contributions by Venturers

SIC 27 Evaluating the Substance of Transactions Involving the Legal Form of a Lease

SIC 31 Revenue — Barter Transactions Involving Advertising Services

The International Accounting Standards Board (IASB) is soon expected to issue the final version of a new standard dealing withrevenue recognition. An exposure draft Revenue from Contracts with Customers establishes fundamental principles to beapplied by entities for the preparation of financial statements to enable their users to understand the amount, timing anduncertainty of revenue and cash flows arising from contracts with customers, on the basis of which, an entity supplies finishedproducts or services to customers. The core principle of the standard is to recognise revenue so as to depict the transfer ofgoods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled inexchange for those goods or services. In addition, the exposure draft provides guidance on how to determine whethercustomer contract costs will be recognised as an asset or in profit or loss.

IFRS CAS

Definition of revenue IAS 18 defines revenue as the gross inflow ofcash, receivables or other consideration arisingin the course of the ordinary activities ofan entity from the sale of goods, from renderingof services, and from the use by others of entityresources yielding interest royalties anddividends.

CAS do not provide any definition of revenue.

Recognition ofrevenue from the saleof finished productsand goods

IFRS establish the following criteria for therecognition of revenue from the sale of finishedproducts and goods:

• transfer of the significant risks and rewards ofownership to the buyer;

• not retaining continuing managerialinvolvement to a degree usually associated withownership;

• the amount of revenue must be measuredreliably;

• the flow of economic benefits associated withthe transaction is probable;

• the costs incurred in respect of the transactioncan be measured reliably.

Under CAS, the approach to revenue recognitionis based on the transfer of a legal title ratherthan on the “transfer of risks and rewards”.

32

IFRS CAS

Recognition ofrevenue from therendering of services

IFRS establish the following criteria for therecognition of revenue from the rendering ofservices:

• the amount of revenue must be measuredreliably;

• the flow of economic benefits associated withthe transaction is probable;

• the stage of completion of the transaction atthe end of the reporting period can be measuredreliably; and

• the costs incurred for the transaction and thecosts to complete the transaction can bemeasured reliably.

Revenue from the rendering of services isrecognised upon agreed billing milestones orafter the transaction is completed. Thepercentage of completion method is notpermitted under CAS.

Measurement ofrevenue

Revenue is measured at the fair value of theconsideration received or receivable, taking intoaccount the amount of any trade discounts andvolume rebates and eliminating the effects ofa financing transaction (i.e. discounting futurereceipts).

CAS do not provide detailed guidance on themeasurement of revenue; no separation offinancing element from the revenue is required.

Complex transaction Under IFRS, individual components of a complextransaction are required to be identified inaccordance with its substance; the recognitioncriteria are then applied to separately identifiablecomponents. Revenue is allocated to eachtransaction component by reference to the fairvalue of the entire transaction and of eachcomponent.

IFRS provide guidance on the recognition ofdifferent types of sales transactions, such as salewith the right of withdrawal, etc.

CAS do not specifically address the issue.

33

IFRS CAS

Transfers of assetsfrom customers

An entity is required to assess agreements toreceive items of property, plant and equipment(or, alternatively, cash to acquire such items)which the entity must then use either to connectthe customer to a network or to provide thecustomer with ongoing access to a supply ofgoods or services (e.g. supplies of water, gas,electricity, and IT services). If the transferreditem of property, plant and equipment meets thedefinition of an asset (the transfer of the right ofownership is not essential), the item is measuredat fair value in accordance with IAS 16.

Revenue from an agreement on transfers ofassets from customers is recognised inaccordance with IAS 18 Revenue. If theconnection is a separately identifiable service,revenue is recognised over the life of theagreement. In the case of an ongoing service, theperiod over which revenue is recognised isdetermined by the terms of the agreement andshall not exceed the useful life of the asset usedto provide an ongoing service.

CAS do not specifically address the issue.

34

Construction ContractsRelated IFRSs and IFRICs:

IAS 11 Construction Contracts

IFRIC 12 Service Concession Arrangements

IFRIC 15 Agreements for the Construction of Real Estate

The International Accounting Standards Board (IASB) is soon expected to finalise a new standard dealing with revenuerecognition; for details refer to the Revenue section. Construction contracts shall be incorporated into the new standard andIAS 11 shall be withdrawn.

IFRS CAS

Definition ofconstructioncontracts

IFRS identify two specific types of constructioncontracts: a fixed price contract in which thecontractor agrees to a fixed contract price or toa fixed rate per unit of output; and a cost pluscontract.

There is no specific definition of constructioncontracts in CAS.

General principles apply to accounting forconstruction contracts, see below.

Contract costs Contract costs comprise costs that relate directlyto the specific contract; costs that areattributable to contract activity in general andcan be allocated to the contract; and costs thatare specifically chargeable to the customer underthe terms of the contract.

IFRS also specify the costs that cannot beattributed to contract activity or cannot beallocated to a contract. Such costs includegeneral administration costs for whichreimbursement is not specified in the contract;selling costs; research and development costs forwhich reimbursement is not specified in thecontract; and depreciation of idle plant andequipment that is not used on a particularcontract.

There is no specific definition of constructioncontracts in CAS. Costs related to constructioncontracts are recognised similarly to any otherproduction costs, i.e. as the contract progressesthe amount of completed work increases and isusually measured based on direct productioncosts and production overhead costs;administrative overhead costs are also permittedfor consideration.

Recognition ofcontract revenue andcosts

When the outcome of a construction contract canbe estimated reliably, contract revenue andcontract costs associated with the constructioncontract shall be recognised as revenue andexpenses, respectively, by reference to the stageof completion of the contract activity at thebalance sheet date. An expected loss on theconstruction contract shall be recognised asan expense immediately.

The stage of completion of a contract shall bedetermined using a method that measuresreliably the work performed, e.g. the proportionof contract costs incurred for work performed todate to the total contract costs.

CAS only state that revenues and costs arerecorded on an accrual, not cash, basis.

Under CAS, the percentage of completionmethod is neither required nor prohibited.Revenue is generally recognised upon agreedbilling milestones or after completion.

Expected loss on the contract can be treated asa general provision or a specific provision forwork in progress.

Disclosures IFRS require specific disclosures concerningconstruction contracts.

CAS do not specifically address constructioncontracts.

35

Impairment of AssetsRelated IFRSs and IFRICs:

IAS 36 Impairment of Assets

IFRS 13 Fair Value Measurement

IFRIC 1 Changes in Existing Decommissioning, Restoration and Similar Liabilities

IFRIC 3 Emission Allowances

IFRIC 10 Interim Financial Reporting and Impairment

IFRIC 12 Service Concession Arrangements

SIC 32 Intangible Assets — Website Costs

IFRS CAS

Impairment of assets IFRS provide detailed requirements forimpairment reviews of assets and specify whenand how impairment reviews shall be performed.In addition, IFRS specify accounting forimpairment losses and the conditions for theirreversal.

CAS stipulate only a general requirement forentities to account for impairment of assets.No detailed guidance on the determination ofimpairment losses is provided.

Timing of impairmenttest

Under IFRS, all intangible assets with anindefinite life, intangible assets not yet availablefor use and goodwill are required to be testedannually for impairment; an impairment test maybe performed at any time during the period, butit must be performed at the same time everyyear.

For all other assets, i.e. for property, plant andequipment and for intangible assets with finiteuseful lives, an entity is required to assess ateach balance sheet date whether there is anyindication of impairment. An impairment test isonly performed if any such indication exists.

Under CAS, all assets have to be reviewed forimpairment at the balance sheet date.

Impairment test An impairment test is performed at the level ofa separate cash-generation unit, i.e. either fora single asset or for a group of assets thatgenerate independent cash inflows.

An entity is required to compare the carryingamount of an asset with the recoverable amount.The recoverable amount of an asset is the higherof its value in use and fair value (determined inaccordance with IFRS 13) less costs to sell. Thevalue in use of an asset is the estimate ofdiscounted future cash flows that will be derivedfrom the use of the asset and from its ultimatedisposal.

Entities are required to assess and document theappropriateness and adequacy of amountsrecognised as allowances that reduce thecarrying amounts of the assets. CAS do notprovide any detailed guidance on the recognitionof the allowances or the method for theircalculation.

36

IFRS CAS

Reversal of animpairment loss

Generally, an impairment loss may be reversedunder IFRS provided that the impairment lossrecognised previously no longer exists or hasdecreased. The reversal of impairment losses ongoodwill is not permitted.

Under IFRS, the new (increased) carrying amountof an asset attributable to a reversal of animpairment loss may not exceed the carryingamount that would have been determined had noimpairment loss been recognised for the asset inprior years.