overview of economy 2020

TRANSCRIPT

OVERVIEW OF ECONOMY 2020

Tallinn 2021

2 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Contents

The macroeconomic situation ................................................................................................................................. 3

Foreign trade ........................................................................................................................................................... 9

The manufacturing industry .................................................................................................................................. 16

Food and beverage production ............................................................................................................................. 21

Textile production .................................................................................................................................................. 26

Clothing production ............................................................................................................................................... 29

Wood processing ................................................................................................................................................... 32

Manufacture of paper pulp, paper and paper products ........................................................................................ 36

The chemical industry ............................................................................................................................................ 39

Manufacture of rubber and plastic products ........................................................................................................ 44

Manufacture of metal and metal products ........................................................................................................... 48

Manufacture of electronic and electrical equipment ............................................................................................ 51

Manufacture of machinery and equipment .......................................................................................................... 56

Manufacture of means of transport ...................................................................................................................... 59

Manufacture of furniture ...................................................................................................................................... 63

The construction sector ......................................................................................................................................... 66

Domestic trade ...................................................................................................................................................... 72

Tourism .................................................................................................................................................................. 76

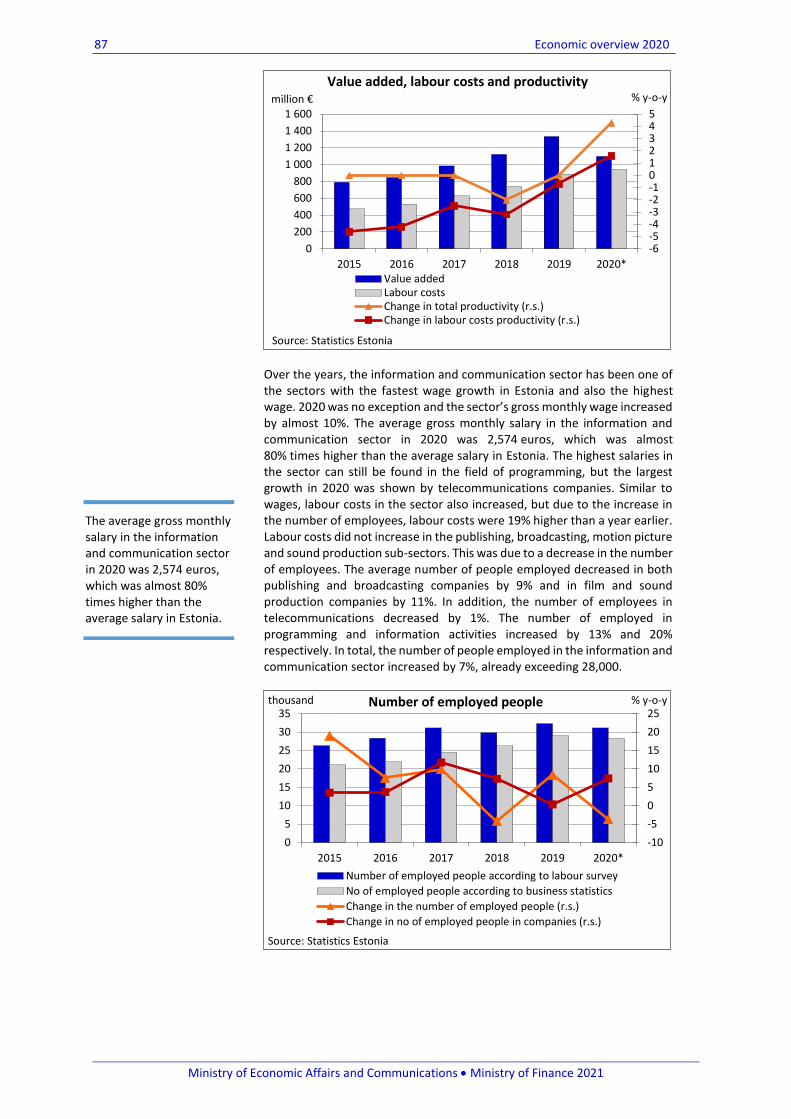

Information and communications ......................................................................................................................... 85

Transport ............................................................................................................................................................... 91

Annexes ................................................................................................................................................................. 97

Abbreviations in text:

*- preliminary, short term statistics

y-o-y – year-over-year

no – number

l.s. – left scale

r.s – right scale

3 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

The macroeconomic situation

Estonia’s economic downturn in 2020 (-2.9%) was twice smaller than the EU average and, like many other countries, smaller than initially forecast. The Estonian economy was supported by the resilience of its closest trade partners – in Finland, Sweden and Lithuania, GDP decreased less than in Estonia. Also, as a 2020 average, domestic restrictions on economic activity and to the free movement of people in Estonia were the mildest in comparison with the rest of the EU. In the first months of the crisis, the wage compensation measure was a great help to companies. Due to cross-border movement restrictions, the Estonian economy lost 1.3 billion euros in tourism revenue in 2020 and the recovery will take time. Hospitality and commerce sectors each accounted for 0.6 percentage points of the decline in 2020. However, the largest contribution to Estonia’s economic downturn last year was made by the manufacturing industry with its large number of employees (0.9 percentage points), but at the end of the year, this sector was already showing signs of recovery in relation to improving global demand. The financial sector and computer services survived the first year of the crisis well, with exports doubling in the last four years.

Domestic demand increased slightly in 2020, but statistics were distorted by a start-up whose investment in computer software in the second half of the year led to a ninefold increase in software investments in the entire business sector. Without it, domestic demand would have fallen sharply. The decline in private consumption was mainly caused by restrictions on the movement and assembly of people and on the business activities of services

-20

-15

-10

-5

0

5

10

15

2006 2008 2010 2012 2014 2016 2018 2020

% y-o-y

Source: Statistics Estonia

Economic growth

European Union Estonia

-40

-20

0

20

40

60

2006 2008 2010 2012 2014 2016 2018 2020

% y-o-y

Source: Statistics Estonia

Domestic demand

Private demand Investments

Estonia’s economic downturn was twice smaller than the EU average and, like many other countries, smaller than initially forecast.

Hospitality and commerce sectors each accounted for 0.6 percentage points of the decline in 2020.

Statistics were distorted by a start-up whose investment in computer software in the second half of the year led to a ninefold increase in software investments in the entire business sector.

4 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

companies and commercial establishments. However, the decline in private consumption (-2.5%) remained somewhat smaller than in the economy as a whole. Services made the largest contribution to the decline in consumption, since various restrictions hindered their provision the most. Consumption of transport and hospitality and leisure services decreased sharply, which was made even worse for the local undertakings by the lack of foreign tourists. However, the consumption of non-durable goods, which forms the lion’s share of the people’s consumption basket, increased in the first year of the crisis and the growth rate slowed down only slightly compared to the earlier times. The growth of consumption of basic non-durable goods, such as food and alcohol and tobacco, clearly accelerated compared to 2019, due to consumption restrictions in cafes and restaurants. Consumption of semi-durable goods decreased significantly in 2020, mainly due to decreased purchasing of clothing and footwear. This was due to restrictions on the opening hours of stores during the emergency situation in spring, as well as a reduced need to renew wardrobe goods due to working from home more and the lack of public events. Consumption of durable goods remained at pre-crisis levels, with lower purchases of personal means of transport offset by higher expenditure on household maintenance and repair goods. Investments are particularly sensitive to changes in economic conditions, and in the spring of 2020 it responded rapidly to growing uncertainty across the EU, with a deep decline in almost all countries in the first half of the year. Investment activity was actually slowing down already in 2019 due to global trade tensions, which is why the unexpected crisis intensified this trend. In the second half of 2020, the decline slowed down, but overall, investment remained lower than in the previous year almost everywhere in the EU. In Estonia, however, investments were increased by the government, households and companies in 2020, and investments as a whole grew by 18% at constant prices. Government investment was supported by a political decision to continue with the previously planned expenditures, and the spring supplementary budget encouraged local government investments. Residents’ real estate investments in new housing slowed down for only a few months in the spring and accelerated significantly at the end of the year. Businesses generally responded to the crisis as expected and investment activity declined in almost all areas. The rapid statistical growth of corporate investment is due to the software purchases of one company, which increased capital investment in computer software tenfold and led to a 23% increase in corporate investment as a whole. Time will tell whether such transactions that significantly affect statistics will take place in the future, but their impact on the supply potential of the Estonian economy is marginal. However, it can be expected that sooner or later this investment will also yield a return, but mostly as return on capital owned by a foreign owner. Against the background of the almost double-digit decline in euro area exports, export developments in the Baltic and Nordic countries were less affected by the virus. In 2020, Estonian exports of goods and services decreased by 5.5% and export prices dropped by 2.1%. Considering the 7.4% decline in external demand, we were able to increase our market share in foreign markets also during the corona crisis. Due to the rapid recovery of merchandise exports that started in autumn 2020, exports of goods also exceeded the last year’s result by 2%. Of the goods of Estonian origin, the largest contribution to growth was made by a one third increase in exports of communication equipment, mainly reflecting the transport of 5G equipment to the US market. Exports of optical equipment, chemical products and oil products, which gained momentum from the recovery in oil prices, also reached double-digit growth. The field

Against the background of the almost double-digit decline in euro area exports, export developments in the Baltic and Nordic countries were less affected by the virus.

The decline in private consumption was mainly caused by restrictions on the movement and assembly of people and on the business activities of services companies and commercial establishments.

5 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

of mechanical machinery and equipment did not perform so well and wooden house manufacturers also had difficulties with exports. Exports of services fell by almost a fifth in 2020, the decline being higher than in the euro area as a whole. The decline was driven by tourism services which account for a larger share of the economy than the euro area average. ICT and business services which create higher added value, have been playing an increasing role in the export of services in recent years. Even during the crisis, these industries were able to continue their growth. The import statistics of 2020 were distorted by launching of an automotive sector software development unit in Estonia. This was reflected in imports of intellectual property in the ICT sector and led to a 0.7% increase in imports. Due to the aforementioned large-scale acquisition, the current account turned into a deficit of 1% of GDP. Without this transaction, the current account surplus would have increased, as is typical to a crisis period. As a result of increasing household savings and declining corporate fixed investment, the trade deficit was the smallest in a decade. In 2020, consumer prices reacted strongly to the corona crisis and the resulting sharp fall in oil prices. Over the year, consumer prices fell by 0.4%, being one of the largest in the euro area. The last time there was a similar fall in prices was during the previous crisis 12 years ago. The bottom of the decline in consumer prices was in May (-1.7%) when the decline in prices was increased by temporary measures imposed by local governments during the emergency situation and the reduction of excise duties on fuel, gas and electricity. This tax measure lowered the consumer price index by an additional 0.5 percentage points. As a result of the pandemic, service prices began to decrease in the second half of the year. Prices of services were put under pressure by tourism-related fields that were in a more difficult situation during the crisis. At the end of the year, accommodation, plane and boat tickets became cheaper by 10% to 15%. At that, the decrease in accommodation prices was the largest in the euro area. Oil was almost one third cheaper in 2020 and accounted for most of the 7% drop in energy prices. Due to the decrease in consumption because of the restrictions and favourable weather conditions in the first half of the year, lower electricity prices also contributed significantly to the decrease in energy prices. The corona crisis did not affect food price developments much. The slowdown in increase of prices could not be seen until the autumn months, and food prices rose by 2% year-on-year.

-4-202468

101214

2005 2007 2009 2011 2013 2015 2017 2019 2021

% y-o-y

Source: Statistics Estonia, Eurostat

Consumer price index

Consumer price index: Estonia

Consumer price index: Euro zone (MUICP)

In 2020, consumer prices reacted strongly to the corona crisis and the resulting sharp fall in oil prices.

6 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

According to the labour survey, the number of employed decreased by 2.2% on a year-on-year basis and unemployment rose to 6.8%. The labour market situation deteriorated sharply with the outbreak of the corona crisis in spring 2020, but the negative effects were somewhat alleviated by the wage compensation measure paid from March to June. In total, around 17,500 companies benefited from this state aid and 137,500 people received compensation totalling 256 million euros. According to Praxis, it helped to save at least 65,000 jobs and reduce the increase in poverty. Despite the wage compensation, the growth of unemployment in Estonia was one of the largest in the European Union, rising to 8% by June, i.e. by 3 percentage points compared to the pre-crisis level. At the same time, unemployment in the European Union increased by only 0.4 percentage points. The crisis mainly affected the fields that are directly related to tourism and entertainment in which economic activities were physically restricted, and have lower-than-average wages. At the same time, the situation was also used to increase efficiency in other areas of activity. By the end of the emergency situation, one in five workers in the hospitality sector had lost their job. In terms of numbers, this number was the same as in the secondary industry sector, although the share of industry in total employment was 18% against the 4% of the hospitality sector. The number of jobs in industry were already declining before the crisis, and the first half of 2020 was still relatively successful in construction by virtue of orders made earlier. With the reduction of employees and using the wage compensation measure, companies in industry, construction and trade were mostly able to maintain profitability. According to Statistics Estonia, the average gross monthly wage increased by 2.9% in 2020. Wage growth slowed significantly during the emergency situation, but moderate wage growth has continued in many sectors since the summer. Wage growth remained surprisingly strong in all the economy, despite the rapid rise in unemployment. This reflects the nature of the current crisis – the situation is extremely poor in a limited number of areas of activity. Average wages fell only in the sectors that were hit very hard by the crisis, such as hospitality service activities, commerce, culture and entertainment. In the field of information and communication, rapid wage growth continued throughout the year. The financial sector has escaped this crisis relatively painlessly because it has not been accompanied by a widespread wave of bankruptcies and an increase in bad loans. In 2020, public sector wage growth was strong, but when taking into account the state aid to the private sector, the aggregate income of people working in the private sector did not decrease. Public sector workers were less affected by the crisis and wage growth there remained relatively strong throughout the year, but this was largely due to the increased workload due to the crisis, especially in the areas of health, education and internal security.

0

5

10

15

20

25

-80

-60

-40

-20

0

20

40

60

2006 2008 2010 2012 2014 2016 2018 2020

%thousand

Source: Statistics Estonia

Employment and unemployment

Change of number of employed

Unemployment rate (r.s)

The labour market situation deteriorated sharply with the outbreak of the corona crisis in spring 2020, but the negative effects were somewhat alleviated by the wage compensation measure paid from March to June.

Wage growth slowed significantly during the emergency situation, but moderate wage growth has continued in many sectors since the summer.

7 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

1 According to the ESA2010 methodology, the following is deemed to be included among labour taxes: social security contributions, personal income tax on wage income, personal income tax on social transfers and pensions, personal income tax on business activities. 2 According to the ESA2010 methodology, the following is deemed to be included among taxes on consumption: value added tax, customs duty, excise duties, motor vehicle registration fee, sales tax, pollution charges, fee for the right of fishery, boat tax, AAU sales revenue, liquid fuel reserve charge and Guarantee Fund contributions. 3 According to the ESA2010 methodology, the following is deemed to be included among capital taxes: corporate income tax, personal income tax on capital income, gambling tax, advertisement tax, land tax, heavy goods vehicles tax, state fees on activity licences and professional licences, fee for the special use of water, road and street closure tax, other taxes and fees.

In 2020, the general government budget position fell into a deep deficit due to the outbreak of the COVID-19 pandemic, which according to the preliminary data of Statistics Estonia amounted to 1.3 billion euros or 4.8% of GDP. The central government and social security funds were in deficit (3.6% and 1.2% of GDP, respectively), which was partly balanced by a surplus from local governments (0.02% of GDP). The central government deficit was due to the state budget, which was affected on the one hand by the decline in tax revenues and on the other hand by the increase in expenditures related to the crisis relief measures of the supplementary budget. The budget deficit of social security funds was also due to a sharp increase in expenditure levels due to the crisis. The financial situation of local governments also suffered as a result of the crisis due to reduced income tax revenues, but with the help of state support measures and more prudent spending, the year ended with a budget surplus of 6 million euros. The structural budget balance of the government sector was in a deficit of 3.6% of the GDP in 2020. The budget deficit in 2021 will reach 6% of GDP, taking into account the decisions of the budget strategy, which, despite the additional costs of the supplementary budget, will be 0.7% better than the original state budget due to the II pension pillar changes and improved economic environment. In 2022, the deficit will decrease by about 560 million euros and reach 3.8% of GDP. As the economic environment recovers, the deficit will decrease to 585 million euros or 1.7% of GDP by the end of the forecast period at 2025. The tax burden in 2020 amounted to 34.2% of GDP, which was 1.1% higher than the year before (2019). The pandemic affected taxes significantly less (-0.2%) than it did the GDP (-3.4%). Compared to 2019, the volume of labour taxes1 increased by 7.2%. This was partly due to the suspension of 4% payments from the state to the second pension pillar from 1 July 2020, which technically increased the tax burden by 143 million euros. At the same time, the state budget’s personal income tax receipts also increased by 23.3% due to various factors – the income tax receipts from pensions increased, as well as the ones from unemployment insurance and other benefits and dividends (at the rate of 7%). The receipt of labour taxes was also supported by the Unemployment Insurance Fund’s wage compensation. In 2020, consumption taxes2 decreased by 7.8% and capital taxes3 by 7.6%. According to the state budget strategy 2022–2025, the tax burden in 2021 will be 35.0% of GDP due to changes in the second pillar of the pension system. In 2022, these effects will decrease significantly and the tax burden will fall to 33.3% of GDP. In the period 2023–2025, labour taxes will increase due to an increase in the average wage, but this will be balanced by an increase in tax-free income from pensions from 2023 onwards. Capital taxes are growing somewhat faster than GDP due to rising dividends from state-owned enterprises. The tax burden will decrease during this period due to consumption taxes, as the growth of both VAT and excise duties will slow down significantly at the end of the forecast period. The tax burden will fall to 32.6% of GDP by 2025.

In 2020, the general government budget position fell into a deep deficit due to the outbreak of the COVID-19 pandemic, which according to the preliminary data of Statistics Estonia amounted to 4.8% of GDP.

As a result of the pandemic, the general government debt increased at a record rate in 2020, increasing by 9.8 percentage points or to 18.2% of GDP over the year

8 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

*The economic forecast for the spring of the Ministry of Finance is based on the assessment of the situation as of 31 March 2021.

As a result of the pandemic, the general government debt increased at a record rate in 2020, increasing by 9.8 percentage points or to 18.2% of GDP over the year. In 2021, the government sector’s debt burden is projected to increase to 21.4% of GDP. The debt is increasing both at central and local government’s level. The debt burden is projected to continue to increase due to negative cash flow and will make up 24.6% of GDP at the end of the year 2022.

% 2019 2020 2021* 2022*

Growth of real GDP 5,0 -2,9 2,5 4,8

Growth of nominal GDP 8,4 -3,4 4,9 7,0

GDP in current prices (bln €) 28,1 27,2 28,5 30,5

Change of consumer price index 2,3 -0,4 2,0 2,1

Employment (15–74-year-old, thousands) 671,3 656,6 650,6 655,9

Growth of employment 1,0 -2,2 -0,9 0,8

Unemployment rate 4,4 6,8 8,0 7,3

Average monthly wage (€) 1 407 1 448 1 504 1 588

Real growth of average monthly wage 5,1 3,4 1,8 3,4

Nominal growth of average monthly wage 7,5 2,9 3,9 5,6

Current account (% of GDP) 2,0 -1,0 3,4 3,3

Change in private consumption expenditure 3,1 -2,5 1,3 4,0

Change in gross fixed capital formation 11,0 18,4 -15,4 8,8

Change of domestic demand 4,5 2,4 -2,2 4,6

Change of exports of goods and services 6,2 -5,5 6,0 6,3

Change of imports of goods and services 3,7 0,7 -0,6 6,2

9 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Foreign trade

The year 2020 brought major changes in trade. Due to the global spread of COVID-19, overall economic activity in international commodity markets and external demand were extremely low. In addition, many companies were forced to reduce production volumes due to virus-related restrictions, and cross-border trade was also hindered. Therefore, in the first half of the year, Estonia’s trade decreased but already in the fourth quarter the economy gained momentum and Estonian companies were able to remain relatively competitive internationally and Estonia’s foreign trade turnover increased. In 2020, total Estonian exports of goods decreased by one percent and imports by six percent compared to the previous year. The foreign trade balance was still negative, but the deficit decreased twofold compared to the previous year. The decrease in the deficit was impacted the most by a decrease in imports of means of transport and an increase in exports of electrical equipment. The decrease in trade turnover was also influenced by export and import prices, dropping respectively by 5.1% and 5.0% over the year.

Estonia’s economic growth is largely influenced by foreign trade, the development of which is strongly related to the economic situation of its trading partners. A slight decline in foreign trade began already in 2019, but the COVID-19 virus that has devastated the world from the beginning of 2020 and the measures put in place to combat it led to an even greater decline in trade. The total trade turnover in Estonia decreased by 3.4% in 2020, remaining slightly below 30 billion euros. The volume of exports was 14.3 billion euros and the volume of imports was 15.2 billion euros. In 2020, the trade deficit was 0.8 billion euros. Estonia’s main trading partners performed better than the European Union countries on average, and as a result, the decline in Estonia’s foreign trade was more modest than in many other European Union countries. In addition, merchandise exports were supported by the manufacturing industry, which was able to withstand the crisis relatively well.

-10

0

10

20

30

40% y-o-y

Source: Statistics Estonia

Export and import growth

Nominal export growth Nominal import growth

-20-15-10

-505

101520

billion €

Source: Statistics Estonia

Trade dynamics

Exports Imports Balance

In the first half of the year, Estonia’s trade decreased but already in the fourth quarter the economy gained momentum.

The total trade turnover in Estonia decreased by 3.4% in 2020, remaining slightly below 30 billion euros.

10 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

In 2020, Estonia exported goods to 184 countries and imported from 143 countries. The foreign trade balance was positive with 140 countries. However, Estonia’s foreign trade is relatively concentrated, as trade with 10–12 main partner countries accounts for more than 70% of foreign trade. The largest trade surplus was in trade with the USA, Norway, and Sweden. The biggest trade deficit outcome was with Germany, Poland, and Lithuania. The shares of exports and imports in trade were 49% and 51%, respectively. Compared to the previous year, the share of exports increased by 2%. The share of goods of Estonian origin in total export of goods was 71%. Compared to the previous year, both exports of domestic goods and their re-exports decreased by one per cent. Big negative balances appeared in the trade of chemical products (-0.7 billion euros), means of transport (-0.56 billion euros), mechanical machinery (-0.34 billion euros), and rubber and plastic products (-0.39 billion euros). Greater surplus was in the trade of wood and timber products (0.9 billion euros), various industrial products such as furniture, pillows, blankets and wooden houses (0.7 billion euros), and electrical equipment (0.5 billion euros). Changes in trade are closely linked to the dynamics of price indices. Similar to trade, both the export and import price indices decreased by 5.1% and 5%, respectively. Price indices showed a positive development only in January, but were in decline in the remaining months. The export price index was mostly affected by changes in the prices of oil products and electricity. The fall in the price level was caused by both the low price of oil and the changes in the world economy caused by the corona crisis. Estonia is still in the grip of the coronavirus, but the ongoing vaccination gives cause for cautious optimism. In the event of a gradual reduction of restrictions, the Estonian economy is expected to start to recover from the crisis in 2021. The rapid rebound of the economy in the third quarter of 2020 showed that the Estonian economy will be able to recover quickly once the restrictions are lifted. The recovery of trade in Estonia is supported by the recovery of global demand. The number of export orders from local undertakings also remains strong, since the coronavirus has not had a significant impact on the euro area manufacturing sector in recent months. The expectations of the panel of experts of the Estonian Institute of Economic Research concerning the development of the general economic situation in the second half of 2021 were also positive. 71% of the experts predicted that the situation would improve, 22% that the situation would remain the same and only 7% that it would deteriorate.

Export In 2020, the export of Estonian goods reduced by 1% compared to the previous year. At the same time, the changes in the volume of exports in the first and second half of the year were very different. The COVID-19 pandemic sharply reduced external demand in the first half of the year, reducing exports of goods by 12%. However, after the virus withdrew in the summer, a rapid recovery in exports began, and the decline in trade in the first half of the year was somewhat balanced by growth in the last months of the year – in the fourth quarter, the export of goods increased by 13% compare to the previous year and in December, the export grew as much as 25%. Although the recovery of exports was not broad-based, the areas significant in the sense of added value did better. Electronic equipment and mineral oils and fuels, as well as the production of timber and timber products and metal products contributed the most to the growth in exports.

The foreign trade balance was positive with 140 countries.

The rapid rebound of the economy in the third quarter of 2020 showed that the Estonian economy will be able to recover quickly once the restrictions are lifted.

Although the recovery of exports was not broad-based, the areas significant in the sense of added value did better.

11 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

In 2020, as before, electrical equipment, mineral products, timber and timber products and agricultural products and foodstuffs were exported the most from Estonia. Exports were most affected by a 12% increase in exports of electrical equipment. About half of electrical equipment exports went to the United States in the form of communications equipment. In addition to electrical equipment, exports of optical, measuring and precision instruments, chemical products and plastic and plastic products also increased in 2020. Although the growth of exports of optical, measuring and precision instruments was the largest, i.e. 13%, their share in total exports was only 4%. The largest impact in this product group was made by the increase in exports of thermometers and X-ray-based equipment. The export growth of chemical products was more modest, remaining at only 3%. Fertilisers, one of the largest product groups, had a decline of more than 40%. However, the growth of chemical products was driven by cosmetics and disinfectants. The growth of plastic products was mostly influenced by the increase in exports of plastic pipes and hoses and plastic products for packaging.

The largest decline in export turnover in 2020 was in the group of goods for transport equipment. The 12% decrease in means of transport significantly affected the decrease in total export turnover since it accounts for 7% of Estonia’s total exports. The main reason for the decline was the decrease in exports of passenger cars, which is mostly transit trade. Mineral products which account for a larger share of means of transport (11%), fell by 8% in 2020. From the commodity group of mineral products, exports of goods based on local raw materials, such as peat, increased, but the decline in the volume of exports was influenced by a larger share of re-exported products, i.e. fuels. The change in export turnover was also significantly influenced by the decline in mechanical machinery, various industrial products and metals and metal products, which accounted for 9%, 8%, and 8%, respectively. Exports of mechanical machinery decreased by 8% in a year, mainly due to lower exports of construction machinery, such as shovel excavators, excavators and shovel loaders, and vending machines. Exports of various industrial products decreased by 5% and the decrease in this group of goods was mainly due to prefabricated wooden buildings. The export of wooden houses was very successful in 2019, elevating the comparison base. In addition, the manufacturers of wooden houses were affected by the pandemic, leading to the postponement of projects in Sweden and Norway. Norway and Sweden are the main target markets for housing developments, public buildings and apartment buildings. The volume of work there is usually quite large, and the postponement, suspension or cancellation of individual large transactions has a significant impact on the sector’s export turnover. The decrease in metals and metal products remained at 5% and was not caused by a decrease in exports of any specific product group, but of all product groups. One of the most important commodity groups for Estonia, timber and timber products, significantly positively affecting the foreign trade balance of Estonia, decreased by 2% in 2020. This was mainly

0 5 10 15 20 25 30

Means of transportation

Metals and metal products

Furniture, log houses

Wood and wood products

Mineral products

Machinery and equipment

Source: Statistics Estonia

%

Exports by commodity groups

2020 2019

About half of electrical equipment exports went to the United States in the form of communications equipment.

The largest decline in export turnover in 2020 was in the group of goods for transport equipment.

12 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

due to a decrease in exports of unprocessed timber which creates less added value. However, several commodity groups that create higher added value domestically were growing.

Out of goods of Estonian origin, the export of animal products grew the most, increasing by 25% over the year. The total export of goods of Estonian origin decreased by 1% in 2020, but their share in total export remained on the level of 2019, i.e. at 71%. Of goods of Estonian origin, optical, measuring and precision instruments showed a 15%, electrical equipment a 14%, plant products and chemical products both an 11% growth. Exports of Estonian shale oil, processed fuel oil, vending machines, equipment parts and prefabricated wooden buildings decreased significantly. The main destination countries for goods of Estonian origin were Finland, Sweden, and the USA.

In total, Estonia’s merchandise exports remained at a very good level in 2020, considering the difficulties that the COVID-19 pandemic caused to the undertakings. In addition, exports of higher value-added goods have shown growth in recent years, with contributions from the timber, metal and agricultural sectors.

In 2020, the share of the European Union in the total Estonian exports fell to 66% which is 4 percentage points less than a year earlier. The decline in exports was also affected by the departure of Great Britain from the EU. The export volume of Estonian businesses to the European Union internal market was 9.5 billion euros. Of the major single market partners, exports increased only to the Netherlands (20%), while volumes to other EU countries dropped. In trade with non-EU countries, Estonian exports increased by 7%, mainly due to increased exports of communication equipment to the United States.

Exports to the CIS countries have been in decline since 2018. In 2020, the export turnover was 4.5% lower than a year earlier. Exports to Russia had the greatest impact, making up almost 85% of all exports to the CIS countries. Export volume to Russia fell by 7%. Moreover, exports to Armenia, Georgia, and Moldova were in decline, but they have a marginal share in the total exports of the CIS countries. The larger decline in export sales was slightly offset by an increase in exports to Belarus. Belarusian exports accounted for 8% of the total CIS exports and increased by 20.5% in 2020.

In the markets of the NAFTA countries, however, exports increased by almost 10% in 2020 due to the growth of the US export turnover. Exports to the United States account for more than 90% of all NAFTA exports, so its 16% growth outweighed the 26% decrease to Canada and the 35% decrease to Mexico. Exports of electrical equipment (mainly 5G equipment) continue to lead the US and NAFTA exports.

0 3 6 9 12 15 18

Lithuania

Germany

USA

Latvia

Sweden

Finland

Source: Statistics Estonia

%

Exports target countries

2020 2019

The total export of goods of Estonian origin decreased by 1% in 2020, but their share in total export remained on the level of 2019

Exports of higher value-added goods have shown growth in recent years, with contributions from the timber, metal and agricultural sectors.

13 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

The trade volume of Finland, Estonia’s largest export partner, fell by 4% year-on-year, which also reduced Finland’s share by one percentage point compared to a year earlier. Yet, this export turnover was almost 750 million higher than with the second largest export partner, Sweden. The largest share of the Finnish export was made up by electrical machinery and equipment, the exports of which increased by 2%. Important export commodity groups included also miscellaneous industrial products and timber and timber products which decreased by 6% and 14%, respectively. Exports to Sweden fell by 1%, which was the smallest decline in recent years. The decline in Swedish exports has so far been due to a decline in exports of communications equipment due to changes in their supply chain. In 2020, however, it was the export of electrical equipment that increased by 18%. The decline in exports was mostly influenced by a 12% decline in timber and timber products and a 9% decline in various industrial products, including, in particular, prefabricated wooden houses. In 2020, Latvia remained in the third place with a similar level as in 2019, i.e. 9%. However, exports dropped by 2% in a year. Among the target markets of Estonian exports, the share of the USA has grown strongly, being the fourth largest export partner for several years already. This is mainly due to the increase in exports of a single commodity group – communication equipment, but given the increasing use of 5G, there is a cause for optimism about further export volumes as well. In 2020, a year of decline for many markets, exports to the United States increased by 16%, increasing its share of total exports to 8%. Germany remained in the fifth place in the ranking of destination countries, with its share and export turnover remaining at the same level as in 2019. At the beginning of 2021, trade in international commodity markets picked up and the export growth expectations of the Estonian manufacturing industry, as the largest industry exporting goods, were also promising. World trade volumes started to grow already at the end of 2020, mainly with the support of Asia, but the purchasing managers index of the euro area turned to growth again at the end of the first quarter of 2021 after a six-month break. This was driven by a record high level of export orders, supporting the revival of trade in Estonia as well. The assessments of the experts of the Estonian Institute of Economic Research concerning the development of foreign trade in March 2021 were quite optimistic. Experts’ expectations were divided as follows: 64% were expecting an increase in the export volume, 22% projected the export volumes to remain at the same level, and 14% of the exports expected export volumes to decrease.

Import

In 2020, imports fell more than exports, reducing the trade deficit twofold compared to 2019. Imports fell by 6% year-on-year to 15.1 billion euros. Like exports, imports also declined at the beginning of the year and only increased in the last two months of the year. The imports increased by 7% in November and by 10% already in December.

0 5 10 15 20 25 30

Prepared foodstuffs and…

Metal and metal products

Chemical products

Means of transport

Mineral products

Machinery and equipment

Source: Statistics Estonia%

Imports by commodity groups

2020 2019

Exports of electrical equipment (mainly 5G equipment) continue to lead the US and NAFTA exports.

Export growth expectations of the Estonian manufacturing industry, as the largest industry exporting goods, were also promising.

14 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

The decrease in imports was mostly influenced by the decrease in imports of transport equipment, mineral products and machinery and equipment (incl. electrical equipment). Imports of transport equipment fell by 19% year-on-year, mainly due to reactions to the coronavirus pandemic which led to a decline in the sales of passenger cars. In total, almost 30% less new cars were sold in Estonia than a year earlier. Imports of mineral products fell by 16% in a year, the main reason being the fall in oil prices on the world market. The import turnover of the machinery and equipment commodity group decreased by 6% and the import of mechanical machinery (-6%) and electrical equipment (-7%) were also in decline. Electrical equipment was the largest outsourced group of goods with a share of 12%, as it includes many inputs od goods. Imports of electronic integrated circuits decreased the most during the year, by almost 40%. In addition, among the main goods, imports of printed circuits, radar equipment, electric capacitors and transformers decreased as well. The main goods that affected the decline of mechanical machinery were self-propelled bulldozers (-54%), elevators, conveyors and similar handling equipment (-32%) and air conditioners (-22%). Import turnover grew in only three commodity groups – timber and timber products by 8%, optical, measuring and precision instruments by 6% and chemical products by 3%. Of these, chemical products accounted for the largest share of total imports, accounting for 10%. The shares of timber and timber products and optical, measuring and precision instruments were 4% and 2%, respectively. The growth of chemical products was influenced by the growth of imports of goods and pharmaceutical products with the largest share. Compared to the previous year, in 2020, Estonia imported more unprocessed wood and sawn timber and the growth of optical, measuring and precision instruments was mostly impacted by the increase in the import of medical equipment.

Estonia’s main import partners are EU countries. The EU’s share of total imports was almost 76% in 2020, four percentage points less than in 2019. The turnover of imports from EU countries decreased by 7% within the year. Imports from non-EU countries fell by 3%.

The volume of imports from the CIS countries decreased by 8% in 2020. Imports from Russia, which accounted for 83% of total imports from the CIS countries, also fell by 8% over the year, having the largest impact on the indicator. This was mainly due to a decrease in imports of mineral fuels and fertilizers. Another important supplying country among the CIS countries is Belarus, the import volume of which decreased by almost 10% in a year. The

0 4 8 12 16

Sweden

Russia

Lithuania

Latvia

Germany

Finland

Source: Statistics Estonia

%

Imports by country of consigner

2020 2019

Imports of transport equipment fell by 19% year-on-year, mainly due to reactions to the coronavirus pandemic which led to a decline in the sales of passenger cars.

Electrical equipment was the largest outsourced group of goods with a share of 12%, as it includes many inputs od goods.

15 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

volume of imports from Belarus was also mostly affected by mineral products. However, import from NAFTA countries increased by 5%. This was supported by imports from the USA which increased by 8% and accounted for almost 90% of all NAFTA imports. The most important commodity group in imports from the USA was arms and ammunition, the import of which increased almost five times during the year. The volume of imports from Canada decreased by 5% and imports from Mexico by 40% in 2020. In 2020, Finland remained Estonia’s biggest import partner, although its share fell by one percentage point to 13.5%. Imports of goods from Finland remained on the same approximate level as in 2019. The second largest import market was Germany whose imports increased by 3%. The main group of goods was means of transport with a share of 17%, but their purchase decreased by 15% during the year because the sale of new passenger cars was declining in Estonia. Another important group of goods was mechanical machinery and equipment, their imports decreased by 8%. Electrical machinery and equipment was also more important with its imports increasing by 9%. Latvia rose to the third place among the supplying countries with 9.5%. Although the import turnover from Latvia was 1% lower than a year earlier, the volume of purchases from Lithuania which was fourth among the supplying countries decreased by as much as 15%, which raised Latvia to the third place among Estonia’s import partners. The main reason for the decline in Lithuanian imports was the 54% decline in the import of mineral products. Russia ranked fifth in the ranking of importing countries with an 8% share. Estonian production depends very much on imported production inputs, which is why exports and imports generally move in the same direction. General trade activity is expected to recover or even increase in 2021, increasing both Estonian exports and imports. Imports are increasing due to the increase in imports of inputs needed for production, acceleration of investment activities and also the growth of domestic demand. The assessment of the experts who participated in the March 2021 forecast of the Estonian Institute of Economic Research had not significantly improved compared to December 2020, but was still positive. Experts’ expectations were divided as follows: 72% were expecting an increase in the volume of imports, 14% left their expectations at the same level and 14% of the experts predicted a drop in the volume of import.

General trade activity is expected to recover or even increase in 2021, increasing both Estonian exports and imports.

Latvia rose to the third place among the supplying countries with 9.5%.

16 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

The manufacturing industry There are about 7,500 companies operating in the manufacturing industry in Estonia, most of them small and medium-sized. There are more than 200 companies with at least 100 employees, but they employ almost half of the employees in the industrial sector. Larger enterprises include manufacturers of cellular equipment, Ericsson Eesti AS, manufacturer of electrical equipment ABB AS, shipbuilding and metal processing group BLRT Grupp AS, woodworking company Stora Enso Eesti AS, manufacturer of industrial electronics Enics Eesti AS, manufacturer of automobile safety systems (seat belts) AS Norma, and producer of meat products AS HKScan Estonia.

In Estonia, the share of the industrial sector in the economy on the basis of value added is slightly smaller than the EU average (approximately 15%). However, the share of people employed in manufacturing in Estonia is one of the highest among the EU countries (almost one fifth), which shows that in the other EU countries it is possible to create more value added with the same number of employees.

The manufacturing industry as a whole is the largest employer in Estonia – almost every fifth employed person works in this field. The share of people employed in industry in the total economic circle has gradually decreased, while the number of people employed has not changed significantly in recent years (with the exception of 2020 which was heavily impacted by the coronavirus). A higher number of jobs have been created within ten years in the timber sector, the repair and installation of machinery and equipment, metal industry and the manufacturing of electrical equipment; timber sector is the one that has grown the most in terms of production volume. The largest industries in terms of number of employees are the wood industry, food production and the metal industry.

The sector is heavily dependent on foreign markets, where more than 60% of production is sold. The main export markets are Finland and Sweden, which also account for the largest share (more than half) of foreign direct investment in Estonian manufacturing.

The number of employees in the manufacturing industry is not expected to change remarkably in the coming years (excluding fluctuations due to the economic situation), but employment in the more labour-intensive sectors is expected to continue declining. Jobs are expected to be created in higher value-added sectors (electronics), but the wood industry based on local raw materials also sees growth potential. However, competitiveness remains based on increasing productivity, which requires continued investment in machinery and equipment, digital technologies and people, as well as product development and improved work organisation.

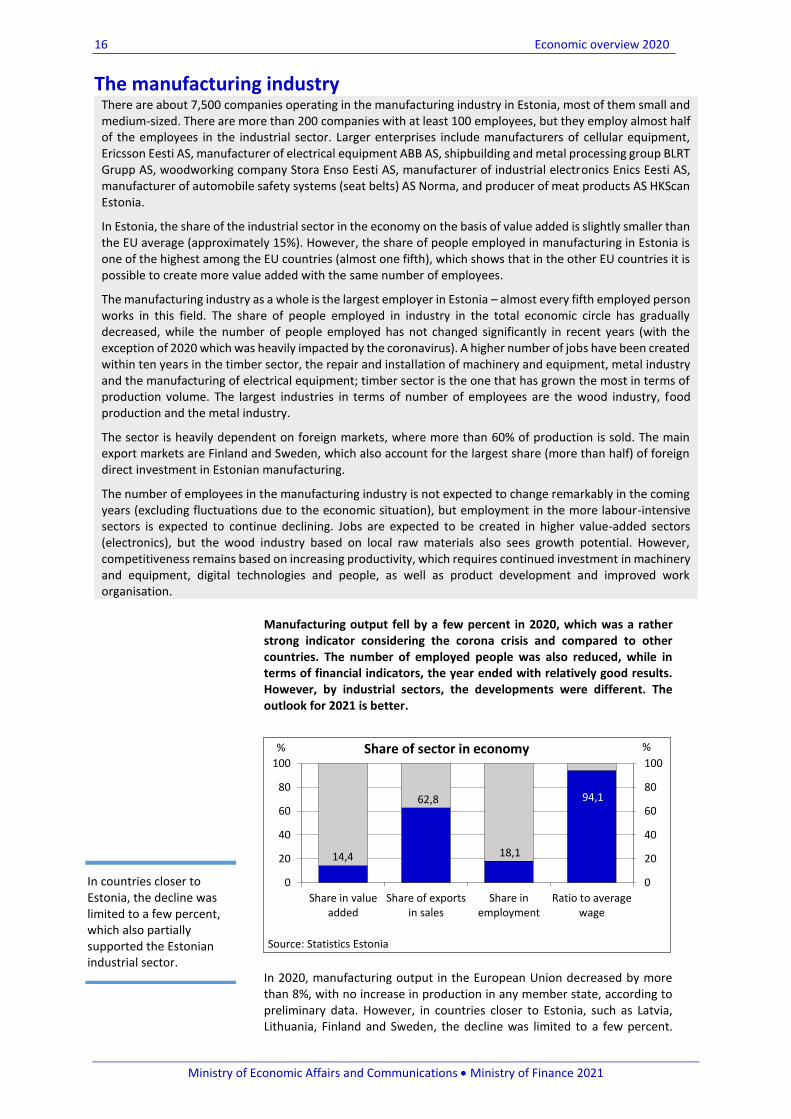

Manufacturing output fell by a few percent in 2020, which was a rather strong indicator considering the corona crisis and compared to other countries. The number of employed people was also reduced, while in terms of financial indicators, the year ended with relatively good results. However, by industrial sectors, the developments were different. The outlook for 2021 is better.

In 2020, manufacturing output in the European Union decreased by more than 8%, with no increase in production in any member state, according to preliminary data. However, in countries closer to Estonia, such as Latvia, Lithuania, Finland and Sweden, the decline was limited to a few percent.

14,4

62,8

18,1

94,1

0

20

40

60

80

100

0

20

40

60

80

100

Share in valueadded

Share of exportsin sales

Share inemployment

Ratio to averagewage

%%

Source: Statistics Estonia

Share of sector in economy

In countries closer to Estonia, the decline was limited to a few percent, which also partially supported the Estonian industrial sector.

17 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Since they are our most important trade partners and customers for industrial products, it also partially supported the Estonian industrial sector.

The spread of the coronavirus and the associated restrictions also hampered the work of the manufacturing industry. In April and May, the volume of industrial production fell by 15–20% compared to the same period in the previous year. In May, however, the production volume almost returned to the level of the previous year and in the fourth quarter it already increased slightly. This was partly due to a lower benchmark because production declined in the second half of 2019.

In the year as a whole, production in manufacturing decreased by more than 4%. The situation was quite different across branches. The volume of industrial production decreased by more than a tenth in the leather industry, the building materials industry, the machinery industry, the manufacture of motor vehicles and trailers, and printing. At the same time, together with the spread of the virus, the demand for many pharmaceutical and chemical products increased dramatically, leading to a 10-15% increase in production in these industries. Apart from these fields, only the timber industry was able to increase production in 2020.

Producer prices in the manufacturing industry decreased by 1.6% over the year – the decline was the same in the European Union as a whole. The fall in oil prices on the world market dropped producer prices in the oil industry by almost a fifth. A larger decline in producer prices also characterised paper and chemical industries. Similar developments were reflected in export and import prices. The increase in demand and also the increase in the price of inputs raised producer prices in the pharmaceutical industry.

Sales of industrial products decreased by almost 4% over the year, exports by somewhat less. While in the second quarter exports suffered a slightly larger setback than sales to the domestic market, the exports managed to increase already in the second half of the year. By industry, the developments of sales and exports were quite similar to the changes in production.

-6

-4

-2

0

2

4

6

8

0

2 000

4 000

6 000

8 000

10 000

12 000

14 000

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Sales and exports

Sales Exports Change in sales Change in exports

The exports managed to increase already in the second half of the year.

18 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

When the corona crisis broke out, efforts were made to save costs and also the wage growth slowed down. In the second quarter, the average wage in manufacturing was slightly lower than a year ago; in the second half of the year and in the year as a whole, the wage growth remained to a few percent. According to a labour force survey, the number of people employed in manufacturing (including employees abroad) also decreased by about 2%. However, according to short-term business statistics, the number of the employed fell by more than 4%, and the number of working hours even more. According to preliminary data, the largest reductions in the number of persons employed and hours worked were in the manufacture of clothing and leather, in the manufacture of furniture, in the manufacture of construction materials and in the manufacture of computers and electronic equipment. All in all, costs were reduced more than the sales revenue decreased and according to preliminary data, the total profit of industrial enterprises increased in 2020. Productivity indicators improved as well. However, the situation varied from industry to industry.

0 5 10 15 20 25

Rubber and plastic industry

Transport industry

Building materials industry

Furniture industry

Textile and clothing industry

Chemical industry

Metal industry

Other sub-sectors

Food industry

Equipment industry

Wood industry

Source: Statistics Estonia

%

Share of sub-sectors in sales of manufacturing industry

-5-4-3-2-101234

0

20

40

60

80

100

120

140

2016 2017 2018 2019 2020*

% y-o-ythousand

Source: Statistics Estonia

Number of employed people

Number of employed people (labour survey data)Number of employed people (business statistics)Change in number of employed people (r.s.)Change in number of employed people in companies (r.s.)

According to preliminary data, the largest reductions in the number of persons employed and hours worked were in the manufacture of clothing and leather, in the manufacture of furniture, in the manufacture of construction materials and in the manufacture of computers and electronic equipment.

Costs were reduced more than the sales revenue decreased and according to preliminary data, the total profit of industrial enterprises increased

19 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Investments in tangible fixed assets of manufacturing enterprises decreased by one fifth in 2020 (preliminary data). This cannot be directly related to the corona crisis – investments were lower already from the beginning of the year and increased every quarter. In contrast to general developments, the timber industry continued to invest actively. Traditionally, more than 60% of capital investments were aimed at machinery and equipment. According to short-term statistics, only investments in computers and computer systems increased, other types of assets were in decline.

In 2020, the assessments of entrepreneurs polled by the Estonian Institute of Economic Research fluctuated quite heavily when it came to business environment. The crunch of 2019 carried over to 2020, and the spread of the coronavirus, as well as the associated uncertainty, further undermined the estimations. In the second quarter, six out of ten industrial companies said

0

2

4

6

8

0

500

1 000

1 500

2015 2016 2017 2018 2019 2020

% y-o-y

Source: Statistics Estonia

Average gross wages

Average wages (in euros) Change (r.s.)

-6

-4

-2

0

2

4

6

8

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Value added, labour costs and productivity

Value addedLabour costChange in total productivity (r.s.)Change in labour costs productivity (r.s.)

-20

-15

-10

-5

0

5

10

15

0

100

200

300

400

500

600

700

800

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Investments of companies

Investments in fixed assets

Change in investments (r.s.)

In contrast to general developments, the timber industry continued to invest actively.

20 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

that there were fewer orders than usual, prices were forecast to fall and the number of employees were expected to decrease. At the end of the year, however, the situation changed and at the beginning of 2021, the estimates had returned to normal. The confidence indicator reached the level last seen 3 to 4 years ago. In the first months of 2021, expectations for the growth of production volume were quite high and an increase in sales prices and in the number of employees were expected. In April, the problem of labour shortage became topical again, with one in five respondents highlighting it. At the same time, the lack of materials and equipment was starting to become an obstacle.

However, the estimates of entrepreneurs were not similar across industries, and the industrial output of the first quarter of 2021 still remained lower than in the previous year in more than half of the industries. However, based on the decline caused by the coronavirus, rather strong growth numbers can be expected in 2021.

In the first months of 2021, expectations for the growth of production volume were quite high and an increase in sales prices and in the number of employees were expected.

21 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Food and beverage production The food industry is one of the largest ones in Estonia in terms of production volume and it is the main activity of more than 700 companies. Although most of the sales revenue comes from the domestic market, the volume of exports has also been growing steadily. In total, nearly 15,000 people find employment in the production of foodstuffs and beverages. Food and beverage companies may be found all over Estonia, and the food industry is an important employer in several rural areas. The largest company in this industry among the meat industries is AS HKScan Estonia in Lääne-Viru County. Another large meat industry is the Atria Group, located in Southern Estonia. The largest bakery companies are AS Eesti Pagar in Paide and OÜ Cristella VT in Võru. The largest companies in the food industry also include the beverage producers Saku Õlletehase AS in Harju County and AS A. Le Coq in Tartu County, the dairy industries Valio Eesti AS and the Maag Group which includes AS Farmi Piimatööstus and Tere AS. The largest fish processors are AS MVWool located in Harju County and AS Paljassaare kalatööstus belonging to the Vičiūnai group, AS Japs M.V.M. located in Pärnu County and OÜ Vettel operating in Saare County. The largest confectionery producer is the Kalev production unit belonging to the Orkla Eesti AS group. The largest producers of ready meals are Lunden Food OÜ and Kulinaaria OÜ, which belongs to the Tallinna Kaubamaja group. Oil is produced by AS Scanola Baltic and yeast is produced by AS Salutaguse pärmitehas. There is intense competition and a fast product cycle in the production of food and beverages. Success is possible only for companies that are able to offer consumers products that they have grown to love over time, that have the same taste and quality, but at the same time also add new products to their assortment.

2020 was a diverse year for the sector. On the one hand, the demand for food increased significantly in the spring just before the emergency situation, but on the other hand, the sector was hit by supply chain disruptions and the spread of coronavirus within the workplaces.

The food industry consists of two major sectors: food and beverage production. 2020 was a bit more successful for food producers; sales in beverage production fell by 8 percent over the year. In 2020, raw material prices were on a downward trend. The purchase price of milk decreased by 5% during the year, to 293 euros per ton. This was hard for the producers because the profitability limit at Estonian farms is around 300 euros per ton. The prices of goat meat, sheep meat, pork and beef fell by a few percent during the year. At the same time, beef and pork production increased over the year, but decreased slightly for sheep meat and goat meat. In the production of beverages, producer prices fell by 1.2% over the year. Labour continued to rise in price, competition was intense and export sales declined. In 2020, the grain harvest in Estonia was again the highest in history but grain prices were slightly lower than a year earlier and industry’s raw materials therefore slightly cheaper. Export growth accelerated in 2020. In total, 1% more products were sold to foreign markets than in the previous year. While previously, the largest

1,9

7,934,7

12,4

92,5

0

20

40

60

80

100

Share in valueadded

Share in man.industryexports

Share ofexports in

sales

Share inemploy-ment

of man.industry

Ratio toaverage wage

%

Source: Statistics Estonia

Share of sector in economy

Problems in supply chains and soaring demand made the year difficult for the sector.

Raw materials became cheaper during the year.

22 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

destination country was Finland, Latvia took this place in 2020 - 10% more goods were sold there than a year before. In total, the share of Latvia increased to 22%. Growth was driven by fish and dairy products. At the same time, alcohol sales decreased by almost a fifth due to the stopping of the vodka race. In addition to Latvia and Finland, exports to Lithuania also exceeded 100 million euros, growing by 4% in a year. The general trend was a decline in exports in the Nordic countries and growth in poorer countries. Exports to Ukraine increased by a fifth over the year and to China by almost a third. Exports of all kinds of residues and dairy products increased mainly to Ukraine. Chinese exports were also driven by dairy products. In addition, sales to Israel almost doubled because of an increase in rapeseed oil sales by 4.5 million euros. Of the larger product groups, rapeseed oil exports increased by a quarter, and exports of fish products decreased by the same amount. Shutdown in the HORECA sector also took away the market of Estonian fish product exporters.

2020 was quite successful for the dairy industry as the largest branch of the food industry. The purchase price of milk decreased significantly because milk production set a record of the last 17 years and the demand was not entirely consistent. At the same time, the export volume of dairy products increased. The decrease in the price of milk led to a decrease in the number of dairy cows, but the increase in productivity per cow improved and the total milk yield increased. At the beginning of 2021, the purchase price of milk went up and this will probably help to stop the decline in the number of cows. In the spring of 2021, the financing scheme for the new planned dairy industry of E-Piim was completed and the construction itself should start in the summer of the same year, production 2 years later. This will ensure additional demand for Estonian milk and help to add value to raw milk on the spot. In terms of tons, the production of drinking milk and cheese increased by 1% and the production of curd by 4%.

-10

-5

0

5

10

0

500

1 000

1 500

2 000

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Sales and exports

Sales Exports Change in sales (r.s.) Change in exports (r.s.)

Meat processing

industry20%

Fish processing

industry7%

Dairy industry22%

Production of bakery and pasta products

10%

Production of beverages

10%

Other27%

Processing and preserving of fruit

and vegetables4%

Share of sub-sectors in sales

Source: Statistics Estonia

Coronavirus reduced fish products exports, but increased oil exports.

Although the year was difficult, exports continued to increase.

23 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

In 2020, the productivity indicators of the dairy industry improved after several years of decline. Volumes increased, the number of employees decreased and profits increased by as much as a third. The growth of net value added reached 10% and investments increased by 15% during the year. 2020 turned out to be more successful for the meat industry than 2019. Total sales increased by 2%, which was lower than in the rest of the food industry, but at the same time losses were avoided and productivity indicators were improved. This was achieved thanks to cheaper raw materials and decreases in the number of employees. HKScan Estonia is at the top of the sector with a quarter of a billion euros in annual turnover and 1,100 employees. The next company is already 5 times smaller - Atria. The largest companies in the sector are all owned by Finnish capital and are part of larger multinational groups. For the beverage industry, 2020 was difficult. As a result of the change in excise policy, exports decreased, bars were closed to prevent the coronavirus from spreading and additional restrictions on alcohol sales were imposed. This led to an almost 8% decrease in beverage production. The drastic decline in the number of tourists also played a role in the reduced demand. As a result, the sector’s profits decreased by almost a quarter. Net value added decreased by 8% and labour productivity by 12% due to increase in labour costs and the number of people employed. A total of 62 million euros was exported in the beverage industry. The largest target market continued to be Latvia, sales to where decreased by 20% last year. The second target market was Finland, sales to where decreased by 18%. At the same time, exports to Lithuania increased by 43% over the year. Growth was driven by beer but Lithuanians were also happy to buy Estonian cider and vodka. For producers of bakery and pasta products, 2020 turned out to be rather poor. Quarantine significantly reduced orders in the HORECA sector and the exports also decreased slightly. Since the raw material prices did not change significantly over the year, producer prices also remained at the same level as a year before. The sector’s profit decreased by 5% and value added by 1% over the year. The frozen bakery segment, which has been growing rapidly so far, decreased by almost a tenth over the year. Fish industry sales decreased by 3% in 2020. Both the domestic market and exports were in decline. Although the listeria scandal that took place a year earlier had already been forgotten, the sector was plagued by a change in consumption patterns. Orders in the HORECA sector decreased and household demand was not able to fully cover the difference. At the same time, the companies managed to reduce losses and increase the net value added by 4%. Sales of Crustacea made the largest decline in exports, but frozen fish and fish fillets were also on decline.

The decline in the number of tourists and sales restrictions reduced alcohol sales.

24 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Employment in food and beverage production decreased by 3% in 2020. The growth of the average wage in the food industry was slightly quicker than the Estonian average growth, but still remained lower than the Estonian average. The average wage is lowered by food producers, where the average wage is about 80% of that of the Estonian average. In the production of beverages, wages were 1.2 times higher than these of the Estonian average.

0 5 10 15 20 25 30

Latvia

Finland

Lithuania

Sweden

Denmark

Ukraine

Source: Statistics Estonia

%

Exports by main target countries

2020 2019

Meat products10%

Fish products11%

Dairy products20%

Bakery and pasta products…

Beverages9%

Other43%

Main export product groups

Source: Statistics Estonia

-4

-2

0

2

4

6

8

10

02 0004 0006 0008 000

10 00012 00014 00016 00018 000

2015 2016 2017 2018 2019 2020*

% y-o-y

Source: Statistics Estonia

Number of employed people and wages

Number of employed peopleAverage wages (in Euros)Change in the number of employed people (r.s.)Change in wages (r.s.)

The growth of the average wage in the food industry was slightly quicker than the Estonian average growth, but still remained lower than the Estonian average.

25 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Investments in the food and beverage industry in 2020 decreased by 18% compared to the previous year. Two thirds of investments were made in machinery and equipment, where 27% less funds were invested than a year earlier. Besides fixed assets, it is important to invest in development activities to ensure competition in the sector. In 2019, there were only 4 full-time scientists or engineers in the production of food and beverages, which was three more than a year earlier. A total of 1.3 million euros was spent on research and development, which was 0.5 million euros less than a year earlier.

A survey of industrial enterprises conducted by the Estonian Institute of Economic Research in the spring of 2021 revealed that the confidence indicator, which summarises the production forecast, general demand and stocks of finished products of the enterprises, was more positive in both food and beverage production than a year earlier. Half of the beverage companies had increased their production volumes in recent months, but none had more orders than usually. The demand was not above the regular levels also in food production, but no redundancies were planned.

-10-8-6-4-20246810

050

100150200250300350400450500

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Value added, labour costs and productivity

Value addedLabour costsChange in total productivity (r.s.)Change in labour costs productivity (r.s.)

-20

-10

0

10

20

30

0

20

40

60

80

100

120

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Investments of companies

Investments in fixed assets

Change in investments (r.s.)

Investments decreased over the year as fewer machines and equipment were purchased.

In the spring of 2021, none of the beverage companies had more orders than usually.

26 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

Textile production The Estonian textile industry is mainly an export-oriented industry, which includes 300 companies, including 7 companies with more than 100 employees. The number of both companies and employees has been declining in recent years. Companies in the sector produce a wide range of textile products, from carpets and pillows to cords and life jackets. There are large textile industry companies in many parts of Estonia. The largest producer of finished textile products is AS Wendre in Pärnu County. The largest home textile producers are AS Mivar-Viva and Paragon Sleep AS in Viljandi County and Hilding Anders Baltic AS in Harju County. Carpets and rugs are produced by AS Mistra-Autex in Harju County. The largest textile finisher is AS Qualitex in Pärnu County and the largest producer of twine, rope and net linen is Saare Frydendahl OÜ in Saare County. The largest textile fibre producer is OÜ SKS Estonia Textile in Narva. There is intense competition in the textile industry and success is often determined by the ability to produce cheaper. Together with the increase in labour costs, also the textile industry in Estonia has reduced its activities in recent years.

The production volume of the textile industry decreased by 5% in 2020. Sales showed a slight increase due to higher prices. The growth of sales was driven by the domestic market, exports did not change during the year.

The share of exports in the sector’s sales has been historically high, but the growth has faltered in recent years. Since 2015, exports have grown by only 8%. At the same time, sales of the sector’s largest company, Wendre, have decreased for the past three years in a row. Hopefully, changes made in the management at the beginning of 2021 will be beneficial and the company will return to the growth path. In 2020, textile companies exported for a total of 261 million euros, which was 0.3% more than a year earlier. By major partners, exports to each country decreased. The biggest decline was in Germany, declining by 13% year-on-year. The largest increase came from Serbia to where there were no exports in the past, and in 2020 it rose to 2.9 million euros. Of the commodity groups, the sales of blankets and pillows decreased by 9% over the year, making a significant contribution to the decline in total exports, as this commodity group accounts for almost two thirds of the sector’s total exports. Furthermore, sales of wool yarn continued to decrease, with exports falling by 24%. At the same time, non-woven exports showed rapid growth, increasing by 72% in a year to 25 million euros. A somewhat worrying trend continued with the volume of goods in tons growing faster than their value. Thus, it can be concluded that the unit price of goods will decrease, i.e. more cheaper products will be exported.

0,4

3,4

73,8

3,0

71,2

0

20

40

60

80

100

Share in valueadded

Share in man.industryexports

Share ofexports in

sales

Share inemploy-ment

of man.industry

Relation toaverage wages

%

Source: Statistics Estonia

Share of sector in economy

Sales showed a slight increase due to higher prices.

27 Economic overview 2020

Ministry of Economic Affairs and Communications • Ministry of Finance 2021

The number of employees in the textile industry also continued to decrease in 2020. The rapid wage growth of the previous year did not continue and during the year, wages in the sector increased by 3%, which is significantly less than the Estonian average. According to preliminary data, the decrease in costs more than doubled the profit and increased the productivity indicators.

-10

-5

0

5

10

15

20

25

050

100150200250300350400

2015 2016 2017 2018 2019 2020*

% y-o-ymillion €

Source: Statistics Estonia

Sales and exports

Sales Exports Change in sales (r.s.) Change in exports (r.s.)

0 5 10 15 20 25 30

Poland

UK

Denmark

Germany

Finland

Sweden

Source: Statistics Estonia

%

Exports by main target countries

2020 2019

Other ready-made textile

products15%

Wool5% Carpets and

other textile floor covering

4%

Wadding, felt and nonwovens, cordage, ropes

17%

Blankets and pillows

53%

Other textile products6%

Main export commodity groups

Source: Statistics Estonia

By major partners, exports to each country decreased.

28 Economic overview 2020