overview of enterprise zones - miami-dade portal

TRANSCRIPT

MIAMI-DADE COUNTY

ENTERPRISE ZONE PROGRAM

Department of Regulatory and Economic Resources Business Affairs Division

111 NW 1st Street 22nd Floor

Miami, FL 33128

LORI WELDON, ENTERPRISE ZONE ADMINISTRATOR (305) 375-3623 (phone) (305) 375-5262 (fax)

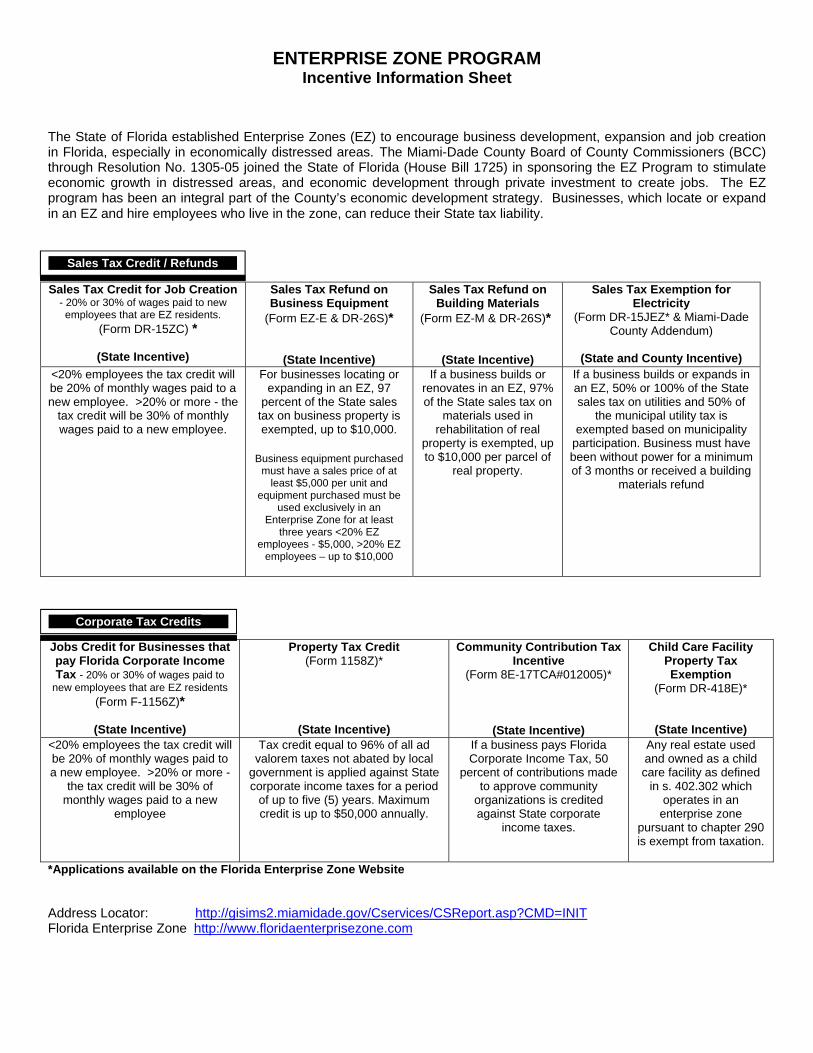

ENTERPRISE ZONE PROGRAM Incentive Information Sheet

The State of Florida established Enterprise Zones (EZ) to encourage business development, expansion and job creation in Florida, especially in economically distressed areas. The Miami-Dade County Board of County Commissioners (BCC) through Resolution No. 1305-05 joined the State of Florida (House Bill 1725) in sponsoring the EZ Program to stimulate economic growth in distressed areas, and economic development through private investment to create jobs. The EZ program has been an integral part of the County’s economic development strategy. Businesses, which locate or expand in an EZ and hire employees who live in the zone, can reduce their State tax liability.

*Applications available on the Florida Enterprise Zone Website Address Locator: http://gisims2.miamidade.gov/Cservices/CSReport.asp?CMD=INIT Florida Enterprise Zone http://www.floridaenterprisezone.com

Sales Tax Credit for Job Creation - 20% or 30% of wages paid to new employees that are EZ residents.

(Form DR-15ZC) *

(State Incentive)

Sales Tax Refund on Business Equipment

(Form EZ-E & DR-26S)*

(State Incentive)

Sales Tax Refund on Building Materials

(Form EZ-M & DR-26S)*

(State Incentive)

Sales Tax Exemption for Electricity

(Form DR-15JEZ* & Miami-Dade County Addendum)

(State and County Incentive)

<20% employees the tax credit will be 20% of monthly wages paid to a new employee. >20% or more - the

tax credit will be 30% of monthly wages paid to a new employee.

For businesses locating or expanding in an EZ, 97

percent of the State sales tax on business property is exempted, up to $10,000.

Business equipment purchased

must have a sales price of at least $5,000 per unit and

equipment purchased must be used exclusively in an

Enterprise Zone for at least three years <20% EZ

employees - $5,000, >20% EZ employees – up to $10,000

If a business builds or renovates in an EZ, 97% of the State sales tax on

materials used in rehabilitation of real

property is exempted, up to $10,000 per parcel of

real property.

If a business builds or expands in an EZ, 50% or 100% of the State sales tax on utilities and 50% of

the municipal utility tax is exempted based on municipality

participation. Business must have been without power for a minimum of 3 months or received a building

materials refund

Jobs Credit for Businesses that pay Florida Corporate Income Tax - 20% or 30% of wages paid to

new employees that are EZ residents (Form F-1156Z)*

(State Incentive)

Property Tax Credit(Form 1158Z)*

(State Incentive)

Community Contribution Tax Incentive

(Form 8E-17TCA#012005)*

(State Incentive)

Child Care Facility Property Tax Exemption

(Form DR-418E)*

(State Incentive) <20% employees the tax credit will be 20% of monthly wages paid to a new employee. >20% or more -

the tax credit will be 30% of monthly wages paid to a new

employee

Tax credit equal to 96% of all ad valorem taxes not abated by local

government is applied against State corporate income taxes for a period

of up to five (5) years. Maximum credit is up to $50,000 annually.

If a business pays Florida Corporate Income Tax, 50

percent of contributions made to approve community

organizations is credited against State corporate

income taxes.

Any real estate used and owned as a child care facility as defined

in s. 402.302 which operates in an enterprise zone

pursuant to chapter 290 is exempt from taxation.

Sales Tax Credit / Refunds

Corporate Tax Credits

NW 27TH AVE

SW 8T H ST

BISC

AYNE

BLV

D

SR 8

26 E

XT

NW 36TH S T I 195

COLL

INS

AVE

W FLA GLE R ST

NW 7TH S T

NW 22ND AVE

I 95 EXPY

I 75 EXT

NW 17TH AVE

SW 40T H ST

NW 32ND AVE

NW 167TH ST

NW 183RD ST

N MIAM

I AVE

NW 135TH ST

W 4

TH A

VE

PALM AVE

NW 199TH ST

E 4TH AVE

E 8TH AVE

SR 9

NW 37TH AVE

NE 6TH AVE

ALT ON RD

SW 24T H ST

NW 12TH S T

W 1

2TH

AVE

NW 46TH S T

NW 54TH S T

NW 79TH S T

NW 62ND ST

S DIX IE HW Y

NW 57TH AVE

NW 67TH AVE

W 16TH AVE

W OKEECHO BEE RD

W 68TH S T

NE 135TH S T

NW 47TH AVE

NW 119TH S T

SR 112

SW 7T H ST

GRATIG NY P KW Y

SR 934

NW 7

2ND

AVE

NW 186TH ST

W 49TH S T

PINE

TRE

E DR

NW 191ST S T

NW 95TH S T

NW 154TH ST

SW 27TH AVE

NW 175TH ST

SW 57TH AVE

SW 67T H AVE

E 10TH AVE

SW 1S T S T

W 60TH S T

NW 2

ND A

VE

NW 28TH S T

W DIX IE HW Y

SW 87TH AVE

NE 159TH S T

SW 97T H AVE

SW 92ND AVE

NW 25TH S T

NW 215TH ST

NW 97TH AVE

NW 58TH S T

SW 22ND S T

NE 151ST S T

SW 42ND AVE

W 29TH S T

SW 22ND AVE

NW 14TH S T

W 44TH P L

PO RT B LV D

NE 163RD ST

SW 82

ND A

VE

NW 11TH S T

NE 79TH S T

SW 16T H ST

FLORIDA TPKE EXPY

W 28TH AVE

W 37TH S T

NW 77TH CT

OPA LOCK A B LV D

GRANADA BLVD

LUDL

AM D

R

MA CA RT HUR CSW Y

S M IAM I AVE

SR 836 EX T

HARDING AVE

SW 32ND AVE

AL I BA B A AVE

NW 29TH S T

E 49TH S T

PRAI

RIE

AVE

NE 125TH S TW 8TH AVE

NW 8

2ND

AVE

NW 14TH AVE

W 53RD ST

SW 32ND S T

NW 143RD ST

SW 3RD AVE

NW 207TH ST

96TH S T

MERI

DIAN

AVE

SW 5T H TER

NE 15TH AVE

NW 4

2ND

AVE

E 65TH S T

RICKENBACKER CSWY

NE 215TH S T

SW 62

ND A

VE

NW 52ND AVE

NW 127TH ST

GRA ND AV E

NW 21ST S T

NE 185TH S T

BIRD AVE

GRIFFING BLVD

NE 19TH AVE

H IA LE AH DR

SW 37TH AVE S BAYSHO RE DR

I 95 EXT

E 57TH S T

SR 836 EX P Y

N BA

Y RD

E 40TH S T

LENA

PE D

R

NW N RIVER DR

NE 22ND AVE

JA NN AV E

NE 12TH AVE

E 33RD ST

NW S RIVER DR

OCEA

N BL

VD

NE 87TH S T

W 76TH S T

E 25TH S T

WASHINGTON AVE

I 395 E XP Y

NE 96TH S T

NE 203RD ST

NW 17TH S T

SW 33RD S T

PERI

MET

ER R

D

KE NNEDY CS WY

DEER RUN

NW 103RD STSE 8TH AVE

NW 169TH ST

NW 151ST S T

NW 36TH AVE

SW 2N

D AVE

LIT TLE RIV ER DR

NW 7

4TH

AVE

NW 87TH AVE

NW 202ND ST

NW 92ND AVE

NW 6TH S T

NE 171ST S T

NE 2

ND C

T

NW 178TH ST

NORM ANDY DR

NW 20TH S T

NE 71ST S T

NW 81ST S T

BYRO

N AV

E

BOBO

LINK DR

NE 199TH S T

SE 9TH CT

W 84TH S T

NE 183RD ST

NW 74TH S T

NE 103RD ST

NW 125TH ST

MINOLA DR

HAM

MON

D DR

NW 203RD ST

N A UGUS TA DR

INDIAN CREEK DR

NE 207TH S T

NW 196TH ST

SW 4TH AVE

W 9TH S T

I 95 RA MP

BAY VISTA BLVD

W OAKMO

NT DR

NE 54TH S T

W 16TH S T

NE 14TH AVE

W 21ST S T

NE 192ND ST

NW 145TH ST

W 65TH S T

NE 61ST S T

SW 7TH AVE

SW 74

TH AV

E

NE 2

ND A

VE

NE 213TH S T

NE 1

3TH

AVENE 177TH S T

NW 161ST S T

NW 156TH ST

NW 7

9TH

AVE

NW 195TH DR

VE NET IAN WA Y

77TH S T

FLORIDA TPKE RAMP

1S T S T

SW 15T H ST

NE 167TH S TNW

45T

H AV

E

NW 203RD T ER AVE NTURA B LV D

E FLA GLE R ST

NW 7TH AVE

VE NET IAN CS WY

NW 87TH S T

NW 12TH AVE

NW 159TH ST

NE 10TH AVE

NW 71ST S T

NW 37TH AVE

NW 87TH AVE

NW 3

2ND

AVE

NE 2ND AVE

NW 2ND AVE

NE 14TH AVE

W D

IXIE

HW

Y

NW 1

2TH

AVE

NE 10TH AVE

COLL

INS

AVE

NE 199TH S TNW 207TH ST

NE 2ND AVE

NW 7

9TH

AVE

NW N RIV ER DR

NW 17TH AVE

I 95 EXPYNW

2ND AVE

NW 7

TH A

VE

NW 71ST S T

NW 1

7TH

AVE

NE 14TH AVE

NW 14TH AVE

NW 42ND AVE

I 95

EXPY

NW 2ND AVE

NW 12TH AVE

I 195

NW 4

2ND

AVE

SR 826 EX T

NW 22ND AVE

NW 103RD ST

NE 163RD ST

NW 8

7TH

AVE

NE 2ND AVE

NW 32ND AVE

NW 215TH ST

Miami-Dade CountyEnterprise ZoneCentral

µLegend

Central Enterprise ZoneEmpowerment Zone

HighwayMajor Road

1 0 10.5 Mi le s

This map was prepared by the Miami Dade CountyEnte rprise Techno logy Services Department

Geographic Information Sys tems (GIS) Divi sionMarch, 2009

S DIX IE HW Y

SW 184TH S T

SW 152ND S T

SW 216TH S T

SW 117TH AVE

SW 87

TH AV

E

FLORIDA TPKE EXT

SW 168TH S T

SW 12

7TH

AVE

OLD CUTLER RD

CARIB BE A N BLVD

MARLIN RD

SW 160TH S T

SW 12

2ND

AVE

SW 200TH S T

SW 11

2TH

AVE

FRANJO RD

SW 144TH S T

SW 186TH S T

QUA IL ROO ST DR

SW 220TH S T

SW 174TH S T

BA ILES RD

SW 211TH S TSW 212TH S T

SW 92ND AVE

LINCO LN BLVD

SW 107TH AVE

FLOR

IDA

TPKE

RAM

P

SW 146TH S T

SW 97

TH AV

ESW

97TH

CT

SW 102ND AVE

SW 92ND AVE

SW 200TH S T

SW 92

ND A

VE

SW 12

2ND

AVE

SW 112TH AVE

SW 107TH AVE

SW 97

TH AV

E

Miami-Dade CountyEnterprise ZoneCutler Ridge/ Perrine

µLegend

South E nterprise Zone HighwayMajor Road

0.3 0 0.30.1 5 Mi le s

This map was prepared by the Miami Dade CountyEnte rprise Techno logy Services Department

Geographic Information Sys tems (GIS) Divi sionMarch, 2009

SouthOverview

S DIX IE HW YSW 248TH S T

SW 216TH S T

SW 16

7TH

AVE

SW 15

7TH

AVE

SW 16

2ND

AVE

SW 232ND S T

SW 288TH S T

FLORIDA TPKE EXT

SW 264TH S T

SW 14

7TH

AVE

SW 268TH S T

OLD DIXIE HWY

SW 296TH S T

SW 15

2ND

AVE

SW 272ND S T

SW 256TH S T

SW 320TH S T

SW 280TH S T

SW 13

7TH

AVESW

172N

D AV

E

SW 12

7TH

AVE

SW 14

2ND

AVE

SW 13

4TH

AVE

BA ILES RD

SW 13

2ND

AVE

NE 8TH S T

SW 240TH S T

E M OW RY DR

N F LAG LER AVE

SW 220TH S T

SW 12

2ND

AVE

NE 1

2TH

AVE

SW 145TH AV E

NE 6

TH A

VE

SW F

LORI

DA A

VE

SW 14

0TH

AVE

SW 117TH AVE

SW 312TH S T

NE 1

8TH

AVE

BO UGA NVILLE B LV D

NE 15TH S T SW 304TH S T

SW 272ND S T

SW 14

7TH

AVE

SW 256TH S T

SW 312TH S T

SW 12

7TH

AVE

SW 312TH S T

NE 6

TH A

VE

SW 15

2ND

AVE

SW 16

2ND

AVE

NE 15TH S T

SW 240TH S T

SW 13

7TH

AVE

SW 13

2ND

AVE

SW 12

2ND

AVE

SW 15

2ND

AVE

SW 312TH S T

SW 240TH S T

SW 320TH S T

SW 280TH S T

SW 12

2ND

AVE

SW 13

7TH

AVE

SW 13

7TH

AVE

SW 12

7TH

AVE

SW 232ND S T

Miami-Dade CountyEnterprise ZoneGoulds - Princeton/ Naranja

µLegend

South E nterprise Zone HighwayMajor Road

0.5 0 0.50.2 5 Mi le s

This map was prepared by the Miami Dade CountyEnte rprise Techno logy Services Department

Geographic Information Sys tems (GIS) Divi sionMarch, 2009

SouthOverview

NW 6

TH A

VE

NE 8TH S TNW 8TH S T

E PA LM DRW PA LM DR

N F LAG LER AVE

OLD DIXIE HWY

N KR

OME

AVE

NW 15TH S T

FLORIDA TPKE EXT

SW 18

7TH

AVE

W M OW RY DR

NE 1

2TH

AVE

E M OW RY DR

SW 328TH S T

N HO MESTEAD BLVD

SE 6

TH AV

E

NW 1ST AVE

NE 6

TH A

VE

NE 1

ST AV

E

SE 1

2TH

AVE

SW 6T

H AV

E

S DIX IE HW Y

NW 3RD AVE

S FLAGLER AVE

SW 17

2ND

AVE

SW 344TH S T

SW 14

TH AV

E

S HOMESTE

AD BLVD

SE 1

ST A

VE

SW 336TH S T

SW 5T

H AV

E

NE 1S

T RD

S KR

OME

AVE

SW 16

7TH

AVE

FLORIDA TPKE RAMP

SW 312TH S T

LUCY ST

S RE

DLAN

D RD

NW 1

4TH

AVE

SE 24T H ST

NE 15TH S TSW 304TH S T

ARTHUR V INING

SW 320TH S T

SE 8TH STE LUCY S TSW 8T H ST LUCY ST

SW 312TH S TNW 8TH ST

NW 1

4TH

AVE

NE 15TH S T

NE 6

TH A

VE

S DI

XIE

HWY

LUCY ST

NE 1

ST AV

ES

DIXI

E HW

Y

S KR

OME

AVE

SE 1

2TH

AVE

SW 187TH AVE

NE 1

2TH

AVE

SW 18

7TH

AVE

NE 15TH S T

NE 6TH AVE

SW 8T H ST

NW 1

4TH

AVE

NW 14TH AVE

SW 304TH S T

SW 187TH AVE

NW 6

TH A

VE

N KR

OME

AVE

SW 17

2ND

AVE

S DIX

IE HW

Y

Miami-Dade CountyEnterprise ZoneHomestead/ Florida City

µLegend

South E nterprise ZoneEmpowerment Zone

HighwayMajor Road

0.2 5 0 0.2 50.1 25 Mi le s

This map was prepared by the Miami Dade CountyEnte rprise Techno logy Services Department

Geographic Information Sys tems (GIS) Divi sionMarch, 2009

SouthOverview

COLL

INS

AVE

ALT ON RD

PINE TREE DR

NORMANDY DR

KE NNEDY CS WY

71S T S T

W 47TH S T

INDIAN CREEK DR

HARD

ING

AVE

63RD S T

PRAI

RIE

AVE

DICK

ENS

AVE

SHER

IDAN

AVE

77TH S T

ARTHUR G ODFRE Y RD

ABBOTT AVE

LA GORCE CIR

LA GORCE DR

W 41ST S T

W 44TH S T

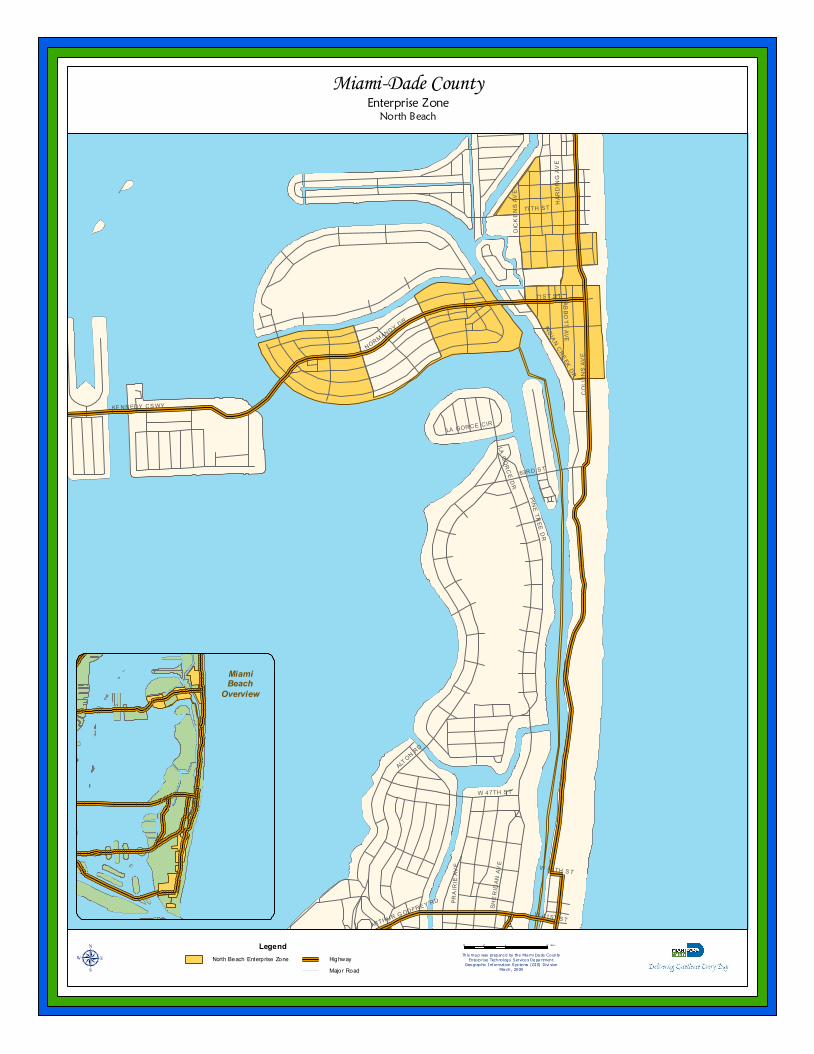

Miami-Dade CountyEnterprise ZoneNorth Beach

µLegend

North Beach Enterprise Zone HighwayMajor Road

0.2 0 0.20.1 Mi le s

This map was prepared by the Miami Dade CountyEnte rprise Techno logy Services Department

Geographic Information Sys tems (GIS) Divi sionMarch, 2009

MiamiBeach

Overview

I 195

ALTO

N RD

COLL

INS

AVE

MERI

DIAN

AVE

N BAY RD

DADE BLVD

PRAI

RIE

AVE

WASHINGT ON AVE

16TH S T

PINE

TRE

E DR

5T H ST

11TH S T

MA CA RT HUR CSW Y

SHER

IDAN

AVE

INDI

AN C

REEK

DR

CHAS

E AVE

1S T S T

VE NET IAN CS WY

W 27TH S T

W 25TH S T

W 24TH S TW 23RD ST

W 29TH S T

PO RT B LV D

N V IE W DR

SUNS

ET D

R

VE NET IAN WA Y

BAY

AVE

LAKE

AVE

SUNSET D R

BAY AVE

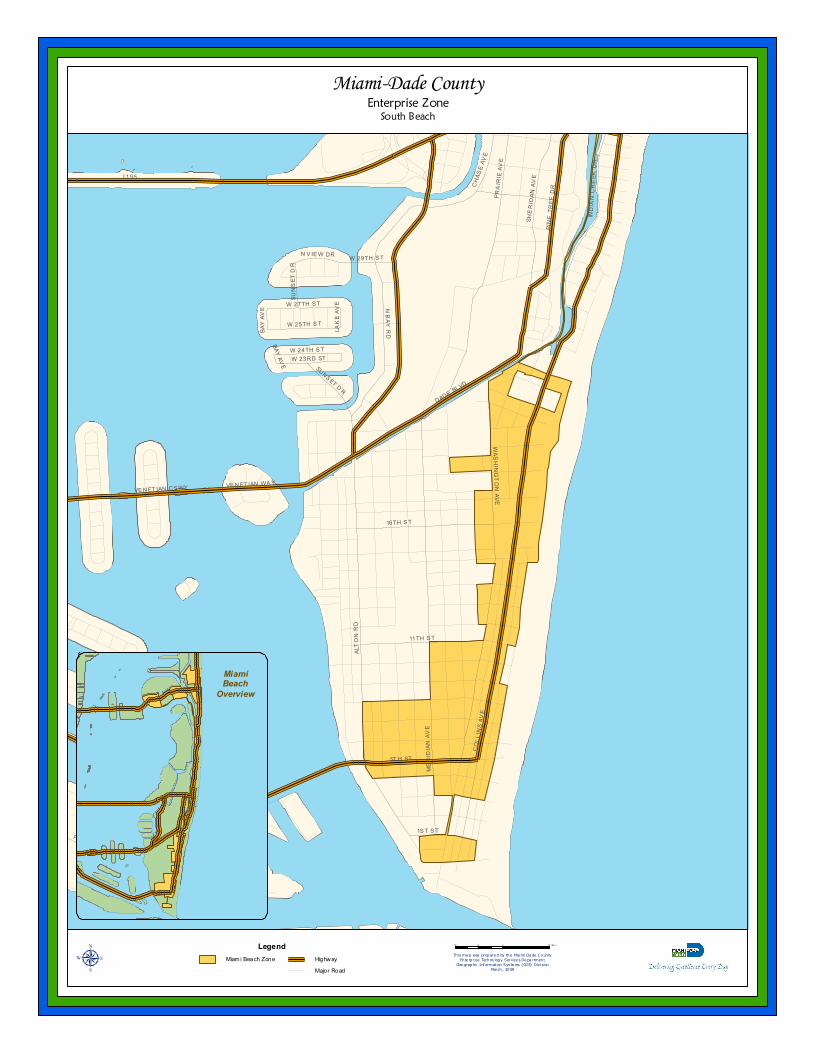

Miami-Dade CountyEnterprise ZoneSouth Beach

µLegend

Miam i Beach Zone HighwayMajor Road

0.2 0 0.20.1 Mi le s

This map was prepared by the Miami Dade CountyEnte rprise Techno logy Services Department

Geographic Information Sys tems (GIS) Divi sionMarch, 2009

MiamiBeach

Overview

JOBS TAX CREDIT (SALES TAX) FORM DR-15ZC (R. 01/03)

(Florida Enterprise Zone Jobs Credit Certificate of Eligibility for Sales Tax) (s. 212.096, F.S.)

Business Eligibility: Must be located within an Enterprise Zone Must collect and pay sales and use tax Must not be taking E.Z. Jobs Tax Credit against corporate income tax.

Employee Eligibility: Must reside and work in a Florida Enterprise Zone. A new job must be created before the business earns a tax credit. Welfare Transition Program participants may reside anywhere, but must work within a zone Must work an average of 36 hours per week (no part-time employees). Must be employed for a minimum of three consecutive months. New employee cannot be an Owner, Partner, or Stockholder. Employees leased from an employee leasing company (Chapter 468) must continuously be

leased to an employer for more than 6 months. Previous employees must not have been employed by the hiring business in the preceding 12

months. Tax credits shall be allowed for up to 24 months per new employee.

Tax credit amount cannot be more than amount of sales tax owed for the month. Calculations: Number of permanent, full-time employees (Zone residents)

DIVIDED BY Total number of permanent, full-time employees

If this percentage is less than 20% the tax credit will be 20% of monthly wages paid to new employee.

If this percentage is 20% or more the tax credit will be 30% of monthly wages paid to new employee.

Processing Time:

Form must be filed with the Department of Revenue within six months of the hire date (within 7 months after the employee is leased for leased employees)

Failure to file on time will result in credit being disallowed EDZA has 10 business days to process and certify the form Form DR-15CS (Sales and Use Tax Return) must be submitted by the business by the 20th of

the next month (or will be considered late). The Department of Revenue will notify the business that the tax credit application has been

approved (within 10 working days) Form DR-15ZC (when approved by EZDA Coordinator) is given to business who will submit

original with Form DR-15CS (Sales and Use Tax Return) to the Department of Revenue (see address below)

Copies:

EDZA mails a copy to the Department of Revenue (see address below) One copy for EDZA files.

Mailing Instructions:

EDZA mails a copy of Form DR-15ZC to: Florida Department of Revenue Return Reconciliation 5050 West Tennessee Street Tallahassee, FL 32399-0100

5

Advantages: Allows business located in a Florida Enterprise Zone a monthly credit against their tax due on wages paid to new employees.

Provides a credit of 20% of wages paid to new eligible employees who are residents of Florida Enterprise Zone.

If more than 20% of the employees are residents of a Florida Enterprise Zone, the credit is 30%

Limitations: The credit is limited to the amount of tax due on each return. There is no refund or carry-forward for credit in excess of the tax due. This credit is not available if the Enterprise Zone Jobs Tax Credit against corporate tax is

taken. The credit is limited to 24 months if the employee remains employed for 24 months.

Eligibility Requirements: Form DR-15ZC must be submitted to an EZ Coordinator and DOR within six months after the new employee is hired.

Questions? Tax Information Services: (850) 488-6800

6

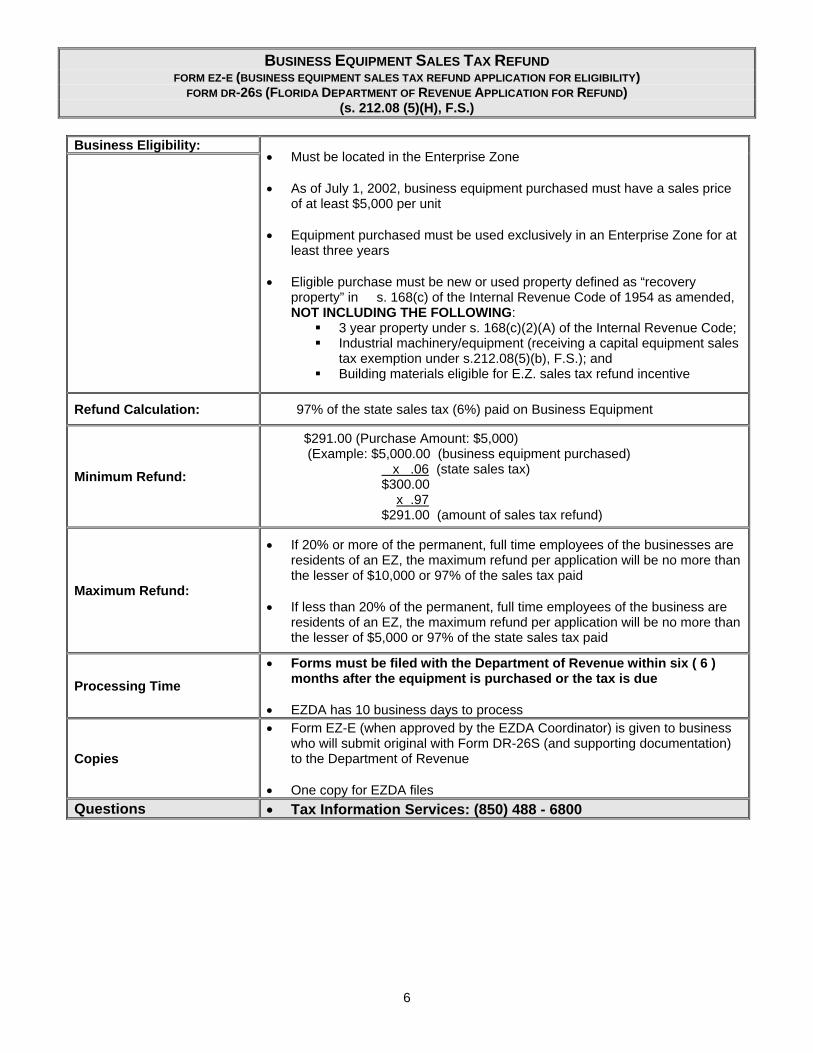

BUSINESS EQUIPMENT SALES TAX REFUND FORM EZ-E (BUSINESS EQUIPMENT SALES TAX REFUND APPLICATION FOR ELIGIBILITY)

FORM DR-26S (FLORIDA DEPARTMENT OF REVENUE APPLICATION FOR REFUND) (s. 212.08 (5)(H), F.S.)

Business Eligibility:

Must be located in the Enterprise Zone As of July 1, 2002, business equipment purchased must have a sales price

of at least $5,000 per unit Equipment purchased must be used exclusively in an Enterprise Zone for at

least three years Eligible purchase must be new or used property defined as “recovery

property” in s. 168(c) of the Internal Revenue Code of 1954 as amended, NOT INCLUDING THE FOLLOWING:

3 year property under s. 168(c)(2)(A) of the Internal Revenue Code; Industrial machinery/equipment (receiving a capital equipment sales

tax exemption under s.212.08(5)(b), F.S.); and Building materials eligible for E.Z. sales tax refund incentive

Refund Calculation: 97% of the state sales tax (6%) paid on Business Equipment

Minimum Refund:

$291.00 (Purchase Amount: $5,000) (Example: $5,000.00 (business equipment purchased) x .06 (state sales tax) $300.00 x .97 $291.00 (amount of sales tax refund)

Maximum Refund:

If 20% or more of the permanent, full time employees of the businesses are residents of an EZ, the maximum refund per application will be no more than the lesser of $10,000 or 97% of the sales tax paid

If less than 20% of the permanent, full time employees of the business are

residents of an EZ, the maximum refund per application will be no more than the lesser of $5,000 or 97% of the state sales tax paid

Processing Time

Forms must be filed with the Department of Revenue within six ( 6 ) months after the equipment is purchased or the tax is due

EZDA has 10 business days to process

Copies

Form EZ-E (when approved by the EZDA Coordinator) is given to business who will submit original with Form DR-26S (and supporting documentation) to the Department of Revenue

One copy for EZDA files

Questions Tax Information Services: (850) 488 - 6800

7

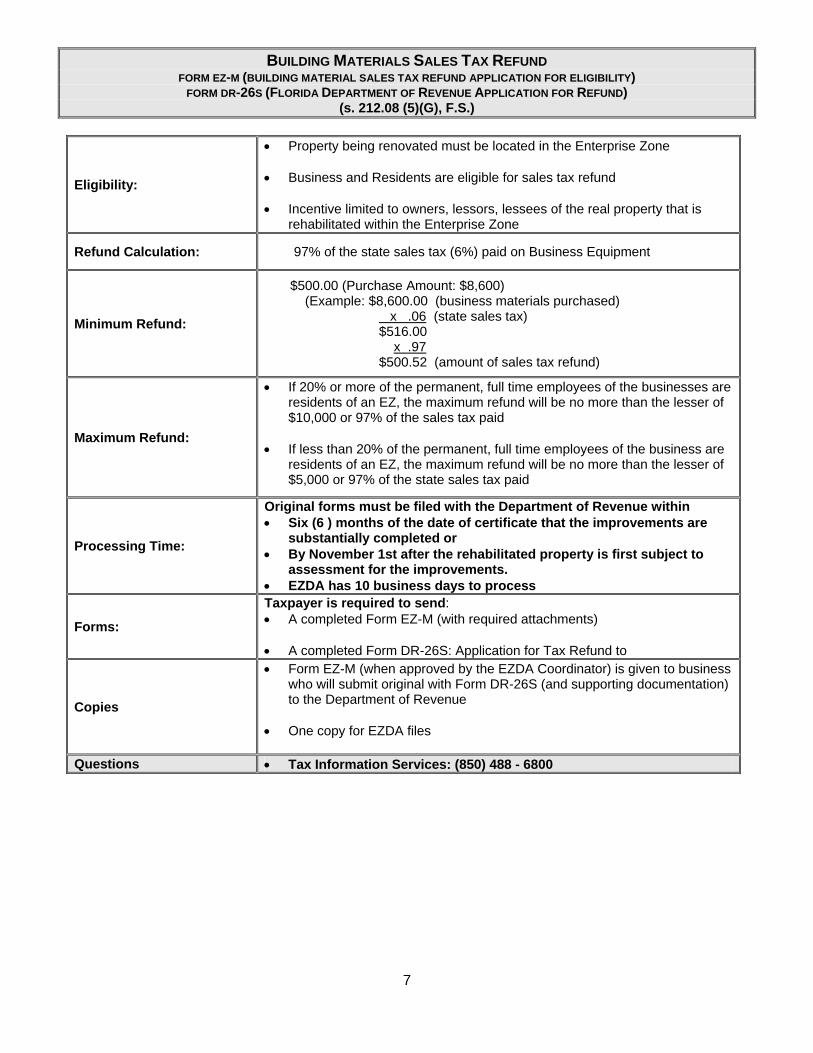

BUILDING MATERIALS SALES TAX REFUND FORM EZ-M (BUILDING MATERIAL SALES TAX REFUND APPLICATION FOR ELIGIBILITY)

FORM DR-26S (FLORIDA DEPARTMENT OF REVENUE APPLICATION FOR REFUND) (s. 212.08 (5)(G), F.S.)

Eligibility:

Property being renovated must be located in the Enterprise Zone Business and Residents are eligible for sales tax refund Incentive limited to owners, lessors, lessees of the real property that is

rehabilitated within the Enterprise Zone

Refund Calculation: 97% of the state sales tax (6%) paid on Business Equipment

Minimum Refund:

$500.00 (Purchase Amount: $8,600) (Example: $8,600.00 (business materials purchased) x .06 (state sales tax) $516.00 x .97 $500.52 (amount of sales tax refund)

Maximum Refund:

If 20% or more of the permanent, full time employees of the businesses are residents of an EZ, the maximum refund will be no more than the lesser of $10,000 or 97% of the sales tax paid

If less than 20% of the permanent, full time employees of the business are

residents of an EZ, the maximum refund will be no more than the lesser of $5,000 or 97% of the state sales tax paid

Processing Time:

Original forms must be filed with the Department of Revenue within Six (6 ) months of the date of certificate that the improvements are

substantially completed or By November 1st after the rehabilitated property is first subject to

assessment for the improvements. EZDA has 10 business days to process

Forms:

Taxpayer is required to send: A completed Form EZ-M (with required attachments) A completed Form DR-26S: Application for Tax Refund to

Copies

Form EZ-M (when approved by the EZDA Coordinator) is given to business who will submit original with Form DR-26S (and supporting documentation) to the Department of Revenue

One copy for EZDA files

Questions Tax Information Services: (850) 488 - 6800

8

SALES TAX EXEMPTION FOR ELECTRICAL ENERGY FORM DR-15JEZ (R. 08/09)

(s. 212.08 (15), F.S.)

(Application for the Exemption of Electrical Energy used in an Enterprise Zone) Business Eligibility: Must be located within an Enterprise Zone (EZ) in a:

Newly occupied structure (no previous electrical service); OR Renovated structure (no electrical service for 3 months); OR Has received a building materials sales tax refund

Tax exemption is limited to municipalities that have passed an ordinance to reduce the municipal utility tax (by at least 50%) for eligible EZ businesses

Sales exemption is available for 5 years Tax Credit Calculation: 50% or 100% exemption from state sales tax on utilities and the

abatement of municipality utility tax (based on local ordinance)

If 20% or more of the businesses’ employees are residents of an EZ, the business will receive a 100% exemption from sales tax

If less than 20% of the businesses’ employees are residents of

the EZ, the business will receive a 50% tax exemption

Forms: Form DR-15JEZ

Copies: Form DR-15JEZ (after approved by EZDA Coordinator) is returned to the business to submit the original to the Department of Revenue

EDZA mails a copy to the Department of Revenue (see address below) One copy for EDZA files.

Mailing Instructions:

EDZA mails a copy of Form DR-15JEZ to: Florida Department of Revenue Return Reconciliation 5050 West Tennessee Street Tallahassee, FL 32399-0100

Questions? Tax Information Services: (850) 488-6800

9

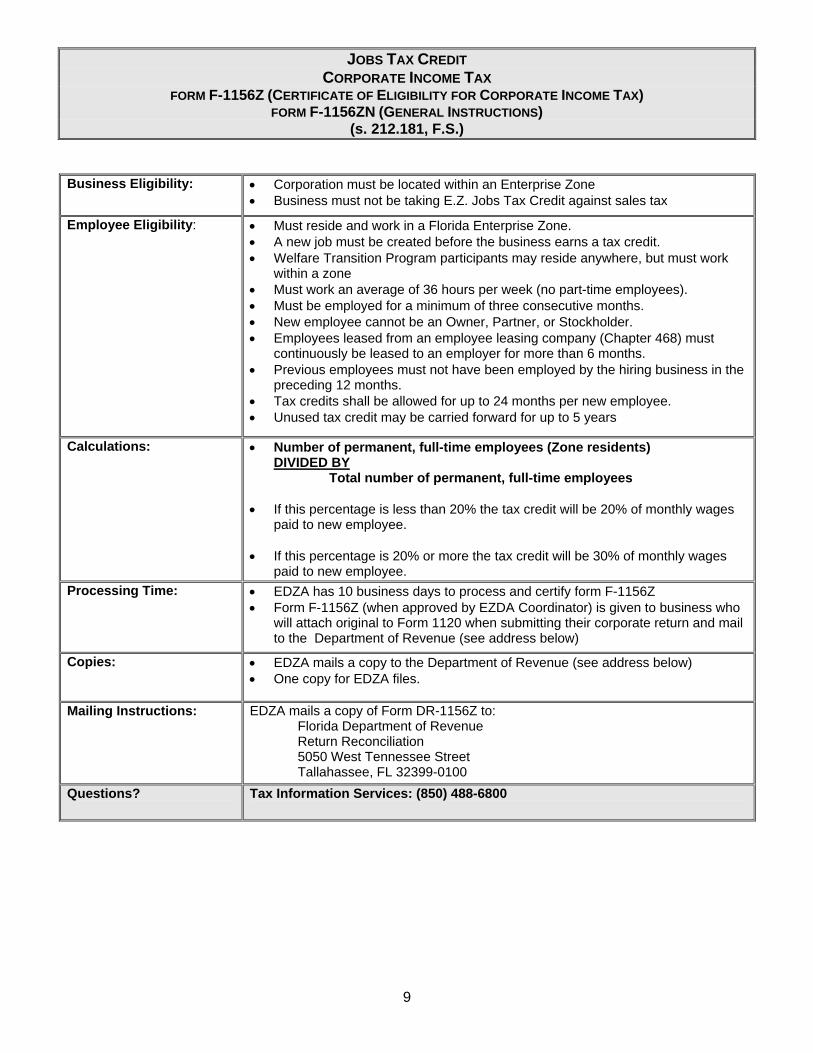

JOBS TAX CREDIT CORPORATE INCOME TAX

FORM F-1156Z (CERTIFICATE OF ELIGIBILITY FOR CORPORATE INCOME TAX) FORM F-1156ZN (GENERAL INSTRUCTIONS)

(s. 212.181, F.S.) Business Eligibility: Corporation must be located within an Enterprise Zone

Business must not be taking E.Z. Jobs Tax Credit against sales tax

Employee Eligibility: Must reside and work in a Florida Enterprise Zone. A new job must be created before the business earns a tax credit. Welfare Transition Program participants may reside anywhere, but must work

within a zone Must work an average of 36 hours per week (no part-time employees). Must be employed for a minimum of three consecutive months. New employee cannot be an Owner, Partner, or Stockholder. Employees leased from an employee leasing company (Chapter 468) must

continuously be leased to an employer for more than 6 months. Previous employees must not have been employed by the hiring business in the

preceding 12 months. Tax credits shall be allowed for up to 24 months per new employee. Unused tax credit may be carried forward for up to 5 years

Calculations: Number of permanent, full-time employees (Zone residents) DIVIDED BY Total number of permanent, full-time employees

If this percentage is less than 20% the tax credit will be 20% of monthly wages paid to new employee.

If this percentage is 20% or more the tax credit will be 30% of monthly wages

paid to new employee.

Processing Time:

EDZA has 10 business days to process and certify form F-1156Z Form F-1156Z (when approved by EZDA Coordinator) is given to business who

will attach original to Form 1120 when submitting their corporate return and mail to the Department of Revenue (see address below)

Copies:

EDZA mails a copy to the Department of Revenue (see address below) One copy for EDZA files.

Mailing Instructions:

EDZA mails a copy of Form DR-1156Z to: Florida Department of Revenue Return Reconciliation 5050 West Tennessee Street Tallahassee, FL 32399-0100

Questions? Tax Information Services: (850) 488-6800

10

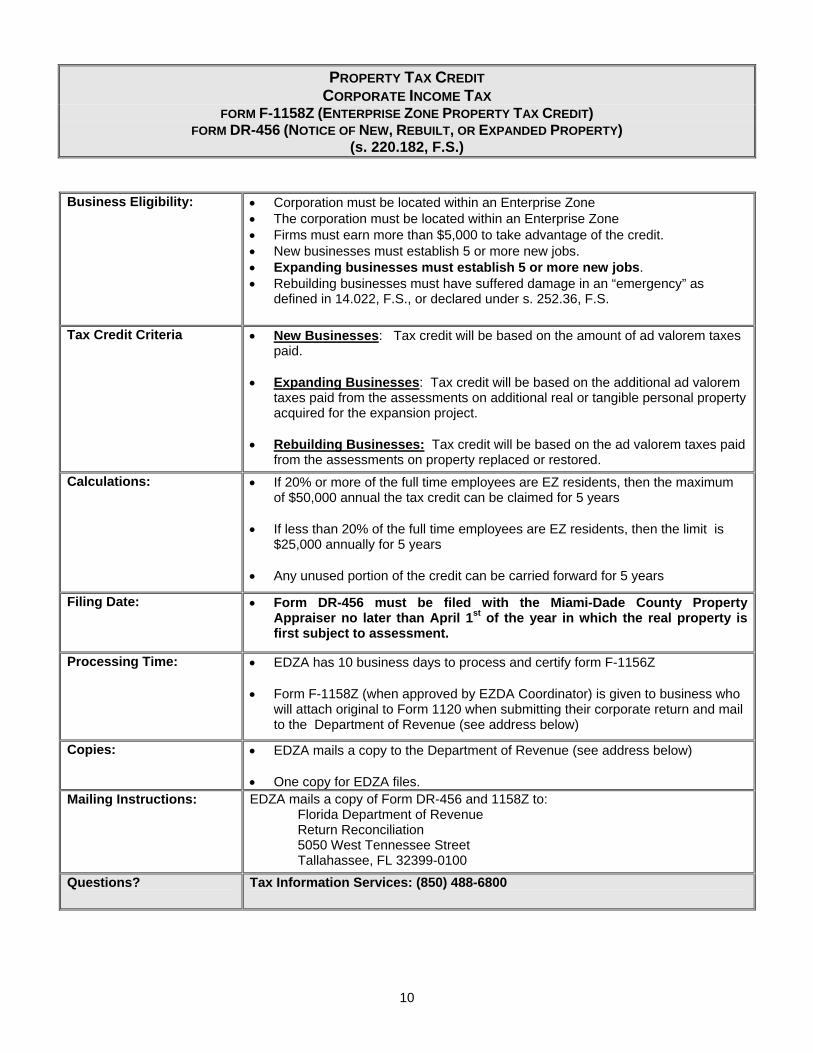

PROPERTY TAX CREDIT CORPORATE INCOME TAX

FORM F-1158Z (ENTERPRISE ZONE PROPERTY TAX CREDIT) FORM DR-456 (NOTICE OF NEW, REBUILT, OR EXPANDED PROPERTY)

(s. 220.182, F.S.) Business Eligibility: Corporation must be located within an Enterprise Zone

The corporation must be located within an Enterprise Zone Firms must earn more than $5,000 to take advantage of the credit. New businesses must establish 5 or more new jobs. Expanding businesses must establish 5 or more new jobs. Rebuilding businesses must have suffered damage in an “emergency” as

defined in 14.022, F.S., or declared under s. 252.36, F.S.

Tax Credit Criteria New Businesses: Tax credit will be based on the amount of ad valorem taxes paid.

Expanding Businesses: Tax credit will be based on the additional ad valorem

taxes paid from the assessments on additional real or tangible personal property acquired for the expansion project.

Rebuilding Businesses: Tax credit will be based on the ad valorem taxes paid

from the assessments on property replaced or restored.

Calculations: If 20% or more of the full time employees are EZ residents, then the maximum of $50,000 annual the tax credit can be claimed for 5 years

If less than 20% of the full time employees are EZ residents, then the limit is

$25,000 annually for 5 years Any unused portion of the credit can be carried forward for 5 years

Filing Date: Form DR-456 must be filed with the Miami-Dade County Property Appraiser no later than April 1st of the year in which the real property is first subject to assessment.

Processing Time:

EDZA has 10 business days to process and certify form F-1156Z Form F-1158Z (when approved by EZDA Coordinator) is given to business who

will attach original to Form 1120 when submitting their corporate return and mail to the Department of Revenue (see address below)

Copies:

EDZA mails a copy to the Department of Revenue (see address below) One copy for EDZA files.

Mailing Instructions:

EDZA mails a copy of Form DR-456 and 1158Z to: Florida Department of Revenue Return Reconciliation 5050 West Tennessee Street Tallahassee, FL 32399-0100

Questions? Tax Information Services: (850) 488-6800

11

THE COMMUNITY CONTRIBUTION TAX CREDIT PROGRAM

The Community Contribution Tax Credit Program (CCTCP) provides for financial incentives (50% tax credit or sales tax refund) to encourage Florida businesses to make donations toward community development and housing projects for low-income persons. The tax credit is easy for a business to retrieve. Business located anywhere in Florida that make donations to approved community development projects may receive a tax credit equal to 50% of the value of the donation. Businesses may take the credit on Florida corporate income tax, insurance premium tax, or as a refund against sales tax (for businesses registered to collect and remit sales tax with the Department of Revenue). Before making the donation, please be sure it will qualify. A list of eligible organizations is available from the Florida Department of Economic Opportunity (DEO). To receive approval, a business donating to an eligible sponsor need only submit a tax credit application with DEO. In order to claim the tax credit, simply attach proof of the approved donation when you file your state tax return. In order to claim a sales tax refund, submit an Application for a Sales Tax Refund. Non-profit organizations and units of state and local governments may apply to become eligible sponsors and solicit donations under the program. Eligibility requirements for an Approved Sponsor are on the following page. This summary is based on Florida Statutes (sections 212.08 (5)(q), 220.183 and 624.5105). Readers are advised to consult these references for additional details.

For Further Information, Please Contact

Burt C. Von Hoff

Executive Office of the Governor Florida Department of Economic Opportunity

107 East Madison Street; MSC 160 Tallahassee, Florida 32399

(Phone) 850-717-8518

Email: [email protected] Website: www.floridaenterprisezone.com

12

HOW TO BECOME AN APPROVED SPONSOR

To quality as a Sponsor, your organization is required to meet the following criteria ■ Be one of the Following: Community Action Program

Non-profit community-based development organization providing community development projects, housing for low-income households, or increasing entrepreneurial and job development opportunities for low-income persons Neighborhood Housing Services Corporation Local Housing Authority Community Redevelopment Agency Historic Preservation District Agency or Organization

Regional Workforce Board (formerly Private Industry Council) Direct-Support Organization (DSO) Enterprise Zone Development Agency Unit of Local Government Unit of State Government ■ Sponsor a project to provide, construct, improve, or substantially rehabilitate housing,

commercial, industrial, or public facilities, or to promote entrepreneurial or job development opportunities for low-income persons in an area designated as a Florida Enterprise Zone or Front Porch Community (Following page)

Or

■ Sponsor a project to increase access to high-speed broadband capability in rural

communities with Enterprise Zones. (Including projects that result in improvements to communication assets that are owned by a business).

Housing Projects for Low-Income Persons ■ A project designed to provide, construct or rehabilitate housing for low-income persons

does not have to be located within an Enterprise Zone or a Front Porch Community

ENTERPRISE ZONE AD VALOREM PROPERTY TAX EXEMPTION CHILD CARE FACILITY FORM DR-418E

(s. 196.095, F.S.)

13

PART I - TO BE COMPLETED BY APPLICANT

Complete Part I of this form and submit to the Enterprise Zone Development Agency for the enterprise zone in which the child care facility is located. To be eligible for the exemption, the facility must have been owned and used as a CHILD CARE facility, as defined in section 402.302, Florida Statutes, on January 1 of the year for which exemption is claimed. This application must be submitted to the Enterprise Zone Development Agency on or before February 1 (suggested date - see Part II for instructions to provide this application to the property appraiser by March 1), of the year for which exemption is claimed. A copy of the CHILD CARE facility’s license from the Florida Department of Children and Family Services must be attached to this application. A copy of this application certified by the Enterprise Zone Development Agency and a copy of your license from the Department of Children and Family Services must be submitted by March 1, to the Property Appraiser’s office in the county in which the CHILD CARE facility is located in order to receive the ad valorem property tax exemption. PART II - TO BE COMPLETED BY ENTERPRISE ZONE DEVELOPMENT AGENCY Section 196.095(2), F.S., requires a review of this application within 10 working days from receipt of the application. Upon your review, please complete Part II of this form and forward the certification to the applicant. It is the applicant’s duty to provide the property appraiser with this form and required attachments for property tax exemption purposes.

STATUTORY AUTHORITY 196.095 Exemption for a licensed child care facility operating in an enterprise zone.

(1) Any real estate used and owned as a child care facility as defined in s. 402.302 which operates in an enterprise zone pursuant to chapter 290 is exempt from taxation. (2) To claim an enterprise zone child care property tax exemption authorized by this section, a child care facility must file an application under oath with the governing body or enterprise zone development agency having jurisdiction over the enterprise zone where the child care center is located. Within 10 working days after receipt of an application, the governing body or enterprise zone development agency shall review the application to determine if it contains all the information required pursuant to this section and meets the criteria set out in this section. The governing body or agency shall certify all applications that contain the information required pursuant to this section and meet the criteria set out in this section as eligible to receive an ad valorem tax exemption. The child care center shall be responsible for forwarding all application materials to the governing body or enterprise zone development agency. (3) The production by the child care facility operator of a current license by the Department of Children and Family Services or local licensing authority and certification by the governing body or enterprise zone where the child care center is located is prima facie evidence that the child care facility owner is entitled to such exemptions.