overview & outlook for p/c insurance focus on michigan markets insurance institute of michigan...

TRANSCRIPT

Overview & Outlook for P/C Insurance

Focus on Michigan MarketsInsurance Institute of Michigan

Boyne Falls, MIJune 19, 2007

Robert P. Hartwig, Ph.D., CPCU, President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: (212) 346-5520 Fax: (212) 732-1916 [email protected] www.iii.org

Presentation Outline• P/C Profit Overview—2006, A Cyclical Peak

Michigan Markets Overview

• Underwriting Trends: Unsustainable?• Premium Growth: Approaching a Standstill• Pricing: Competitive Pressures Mounting• Capital & Capacity: UnderleveragedROE Pressure• Catastrophe Loss Management

What is the Appropriate Role for Government?

• Reinsurance Summary• Financial Strength & Ratings• Investments: Less Bang for the Buck• Tort System: Great News for a Change (Mostly)• Legislative & Regulatory Update• Q&A

P/C PROFIT:An Historical Perspective

Profits in 2006 ReachedTheir Cyclical Peak

P/C Net Income After Taxes1991-2006 ($ Millions)*

$14,178

$5,840

$19,316

$10,870

$20,598$24,404

$36,819

$30,773

$21,865

-$6,970

$3,046

$30,029

$63,695

$44,155

$20,559

$38,501

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

*ROE figures are GAAP; 1Return on avg. Surplus.Sources: A.M. Best, ISO, Insurance Information Inst.

2001 ROE = -1.2%2002 ROE = 2.2%2003 ROE = 8.9%2004 ROE = 9.4%2005 ROE= 10.5%2006 ROAS1 = 14.0%

Though up in 2006, insurer profits are highly volatile (2001 was the industry’s worst year ever). ROEs

generally fall below that of most other industries.

-5%

0%

5%

10%

15%

20%

US P/C Insurers All US Industries

ROE: P/C vs. All Industries 1987–2008E

*2007-08 P/C insurer ROEs are I.I.I. estimates.Source: Insurance Information Institute; Fortune

Andrew Northridge

Hugo Lowest CAT losses in 15 years

Sept. 11

4 Hurricanes

Katrina, Rita, Wilma

P/C profitability is cyclical, volatile and vulnerable

-5%

0%

5%

10%

15%

20%

25%

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 0607

F08

F

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2008F

*2007-08 P/C insurer ROEs are I.I.I. estimates.Source: Insurance Information Institute; ISO, A.M. Best.

1975: 2.4%

1977:19.0% 1987:17.3%

1997:11.6%

2006:14.0%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years

10 Years 9 Years

Insurance & Reinsurance Stocks: Slow Start in 2007 in P/C, Reins.

10.11%

7.03%

5.77%

1.68%

2.58%

12.86%

6.70%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0%

S&P 500

Life/Health

Reinsurers

P/C

All Insurers

Multiline

Brokers

Source: SNL Securities, Standard & Poor’s, Insurance Information Institute

Total YTD Returns Through June 15, 2007

P/C insurance, reinsurance stocks lagging on soft market

concerns and worries over 2007 hurricane season

Top Industries by ROE: P/C Insurers Still Underperformed in 2006*

30.7%30.3%

26.4%24.6%

24.2%22.6%

21.8%21.5%

20.9%20.9%

20.5%19.6%19.4%19.1%

14.9%15.4%

31.8%

0% 5% 10% 15% 20% 25% 30% 35%

Oil & Gas Equip., ServicesPetroleum Refining

MetalsFood Services

Household & Pers. ProductsPharmaceuticals

Industrial & Farm EquipmentMining & Crude Oil Prod.

Aerospace & DefenseChemicalsSecurities

Food Consumer Prod.Medical Prod. & Equip.

Specialty RetailersHomebuilders

P/C Insurers (Stock)All Industries: 500 Median

*Excludes #1 ranked Airline category at 65.1% due to special one-time bankruptcy-related factors.Source: Fortune, April 30, 2007 edition; Insurance Information Institute

P/C insurer profitability in 2006 ranked 30th out of 50

industry groups despite renewed

profitabilityP/C insurers

underperformed the All Industry median for the 19th consecutive

year

Advertising Expenditures by P/C Insurance Industry, 1999-2005

$ Billions

$1.736 $1.737 $1.803$1.708

$2.975

$2.111

$1.882

$1.5

$1.7

$1.9

$2.1

$2.3

$2.5

$2.7

$2.9

$3.1

99 00 01 02 03 04 05Source: Insurance Information Institute from consolidated P/C Annual Statement data.

Ad spending by P/C insurers is at a record high, signaling

increased competition

MICHIGAN MARKETS

Growth & Profitability Overview

-5%

0%

5%

10%

15%

20%

25%

93 94 95 96 97 98 99 0 01 02 03 04 05

Michigan US

Growth in Direct Written Premiums: Michigan and US

Source: Insurance Information Institute; NAIC.

Decline in premiums in MI was marginal (-0.50%) in 2004-5 while US was down 2.5%

-5%

0%

5%

10%

15%

20%

25%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05

US P/C Insurers All US Industries Michigan

ROE: P/C (US & MI) vs. All Industries, 1991–2005*

Source: Insurance Information Institute; NAIC, Fortune. *Latest available.

MI has recently under-performed US P/C insurers.

ROE for Major Commercial Lines in Michigan, 1994 - 2005

5.9%

9.8%

-1.0

%

-0.7

%

2.6%

-8.5

%

1.1%

16.6

%

18.8

%

11.5

%

1.3%

6.3%

10.9

%

26.6

%

-1.7

%

13.8

%

12.2

%

14.2

%

6.6%9.

1%

7.2%

-0.1

%

6.1%

5.2%

-15%

-5%

5%

15%

25%

35%

45%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Commercial Multi-Peril

Commercial Auto

Source: NAIC

Commercial Auto and CMP rebounded in

Michigan in recent years

ROE for Personal Linesin Michigan, 1994 - 2005

12.1% 13.8%

4.7%2.7%

-3.5%

6.1%

-2.2%-4.9%

-29.1%

13.5%

21.4%24.7%

7.2%10.7%

9.0%

-4.1%-5.8%-8.6%

3.3%

-9.3%-14.5%

-6.2%

0.8%

-4.9%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Personal Auto

Homeowners

Source: NAIC

12-Year Average:

Auto: 4.2% Home: -1.2%

Rates of Return on Net Worth for Homeowners Ins: US vs. MI

Source: NAIC, Insurance Information Institute

-1.7%3.6%

12.4%

5.4% 3.8%

0.8%

-8.6%

-14.5%-9.3%

-29.1%

3.3%

13.5%

21.4%

3.7%

-4.2%-2.8%

1.4%

9.7%

-7.2%

5.4%

-4.9%-4.9%

24.7%

-6.2%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

US

Michigan

Averages: 1994 to 2005

US HO Insurance = 2.46%

Michigan HO Insurance = -1.2%

Will coastal insurers reallocate resources to Midwest/Plains?

Rates of Return on Net Worth for Pvt. Passenger Auto: US vs. MI

Source: NAIC, Insurance Information Institute

11.4% 11.6% 12.1%10.1%

13.3%

11.0%

12.1%10.7%

4.7%

-5.8%-4.1% -3.5%

6.1%

-2.2%2.2%

12.4%

4.1%

9.4%

2.0%

7.7%7.2%

13.8%

2.7%

9.0%

-12%

-7%

-2%

3%

8%

13%

18%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

USMichigan

Averages: 1994 to 2005

US PPA Insurance = +8.94%

Michigan PPA Insurance = +4.2%

Rates of Return on Net Worth for Workers Comp: US vs. MI

Source: NAIC, Insurance Information Institute

14.4% 14.3%12.4%

8.8%10.1% 9.6%

17.2%18.6%

11.2%

7.8%9.2%

14.1%

17.6%

11.4%

6.0%

12.8%

2.4%

6.9%

0.2%

4.5%

12.2%

22.7%

13.0%15.8%

-5%

0%

5%

10%

15%

20%

25%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

USMichigan

Averages: 1994 to 2005

US WC Insurance = +8.5%

Michigan WC Insurance = +14.2%

Rates of Return on Net Worth for Comm. M-P: US vs. MI

Source: NAIC, Insurance Information Institute

3.7%

7.5% 8.8%5.7%

5.9%

-8.5%

-1.7%

13.8%16.6%

18.8%

26.6%

5.2%3.5% 6.7%

8.9%7.4%

11.2%

-5.5%

1.6%-1.0%

2.6%

9.8%

1.1%-0.7%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

USMichigan

Averages: 1994 to 2005

US Comm. M-P Insurance = +5.4%

Michigan Comm. M-P Insurance = +6.9%

Rates of Return on Net Worth for Comm. Auto: US vs. MI

Source: NAIC, Insurance Information Institute

10.1% 9.7%

13.7%11.5%

6.3%5.2%

14.2%14.0%

7.0% 3.9%

1.5%

7.6%

3.5%

10.1%

1.0%

0.1%

10.9%12.2%

-0.1%

6.6%

1.3%

9.1%

6.1%

7.2%

-5%

0%

5%

10%

15%

20%

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

USMichigan

Averages: 1994 to 2005

US Comm. Auto Insurance = +6.9%

Michigan Comm. Auto Insurance = +7.5%

PP AUTO: 10yr Avg Return on Equity, MI & Nearby States

4.5%

9.0%

10.0%

2.5%

8.4%

9.3%

10.7%

8.8%

0% 2% 4% 6% 8% 10% 12%

Ohio

Indiana

US

Michigan

Wisconsin

Illinois

Iowa

Kentucky

Source: NAIC, Insurance Information Institute

1996-2005

HOME: 10yr Avg Return on Equity, MI & Nearby States

-7.1%

-14.0%

-3.9%

0.5%

-1.2%

-5.2%

2.8%

-0.6%

-15% -10% -5% 0% 5%

Ohio

US

Indiana

Michigan

Wisconsin

Illinois

Iowa

Kentucky

Source: NAIC, Insurance Information Institute

1996-2005

WC: 10yr Avg Return on Equity, MI & Nearby States

5.9%

6.6%

7.2%

13.1%

7.4%

12.6%

6.5%

0% 5% 10% 15%

Indiana

US

Michigan

Wisconsin

Illinois

Iowa

Kentucky

Source: NAIC, Insurance Information Institute

1996-2005

UNDERWRITING

Extremely Strong 2006, Momentum for 2007/08

90

95

100

105

110

115

120

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

F0

8F

Combined Ratios

1970s: 100.3

1980s: 109.2

1990s: 107.8

2000s: 102.4*

Sources: A.M. Best; ISO, III *Through 2008E; 103.6 through 2006 actual.

P/C Insurance Combined Ratio, 1970-2008F

115.8

107.4

100.198.3

100.7

92.4

98.696.6

90

100

110

120

01 02 03 04 05 06 07F 08F

P/C Insurance Combined Ratio, 2001-2008F

Sources: A.M. Best; ISO, III. *Estimates/forecasts based on III’s 2007 Early Bird survey.

2005 figure benefited from heavy use of reinsurance which lowered net losses

2006 produced the best underwriting result

since the 91.2 combined ratio in 1949

As recently as 2001, insurers were paying out nearly $1.16 for

every dollar they earned in premiums

2007/8 deterioration due primarily to falling rates, but results still strong assuming

normal CAT activity

87.6

91.2

92.1 92.3 92.4 92.493.1 93.1 93.3

93.0

85

86

87

88

89

90

91

92

93

94

1949 1948 1943 1937 1935 2006 1950 1939 1953 1936

Ten Lowest P/C Insurance Combined Ratios Since 1920

Sources: Insurance Information Institute research from A.M. Best data.

The 2006 combined ratio of 92.4 was the best since the 87.6 combined in 1949

The industry’s best underwriting years are associated with

periods of low interest rates

-55-50-45-40-35-30-25-20-15-10-505

101520253035

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

Underwriting Gain (Loss)1975-2006

Source: A.M. Best, Insurance Information Institute

$ B

illi

ons

Insurers earned an underwriting profit of $31.2 billion in 2006, the largest ever but only

the second since 1978. Despite the 2006 underwriting profit, the cumulative

underwriting deficit since 1975 is $419 billion.

110.

3

110.

2

107.

6

103.

9

109.

7

112.

3

111.

1

122.

3

110.

2

102.

5

105.

1

94

102.

0

112.

5

85

90

95

100

105

110

115

120

125

93 94 95 96 97 98 99 00 01 02 03 04 05 06F

Commercial Lines Combined Ratio, 1993-2006E*

Source: A.M. Best; Insurance Information Institute .

Outside CAT-affected lines, commercial

insurance is doing fairly well. Caution is

required in underwriting long-

tail commercial lines.

2006 results will benefited from relatively disciplined underwriting

and low CAT losses

Commercial coverages have exhibited extreme variability. Are current

results anomalous?

103.

9

104.

5

103.

5

104.

9

99.8 10

2.7

104.

5

109.

9

110.

9

105.

3

98.4

94.3 96

.4

91.0

85

90

95

100

105

110

115

93 94 95 96 97 98 99 00 01 02 03 04 05 06F

Personal LinesCombined Ratio, 1993-2006E

Source: A.M. Best; Insurance Information Institute.

A very strong 2006 resulted from favorable frequency & severity

trends and low CAT activity

$1

0.8

$2

2.7

$1

3.9

$9

.9

$8

.0

$5

.0

$2.0$0.4

2.41.9

1.1

0.4

6.5

3.63.5

0.1

$0

$5

$10

$15

$20

$25

2000 2001 2002 2003 2004 2005E 2006E 2007E

Re

se

rve

De

ve

lop

me

nt

($B

)

0

1

2

3

4

5

6

7

Co

mb

ine

d R

ati

o P

oin

ts

PY Reserve Development Combined Ratio Points

Impact of Reserve Changes on Combined Ratio

Source: A.M. Best, Lehman Brothers for years 2005E-2007F

Reserve adequacy has improved substantially

PREMIUM GROWTH

Deceleration in 2006, Even Slower in 2007

-10%

-5%

0%

5%

10%

15%

20%

25%

19

70

19

71

19

72

19

73

19

74

19

75

19

76

19

77

19

78

19

79

19

80

19

81

19

82

19

83

19

84

19

85

19

86

19

87

19

88

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

F2

00

8F

20

09

F2

01

0F

Note: Shaded areas denote hard market periods.Source: A.M. Best, Insurance Information Institute

Strength of Recent Hard Markets by NWP Growth*

1975-78 1984-87 2001-04

*2007-10 figures are III forecasts/estimates. 2005 growth of 0.4% equates to 1.8% after adjustment for a special one-time transaction between one company and its foreign parent. 2006-2008 figures from III Groundhog Survey.

2006-2010 (post-Katrina) period could resemble 1993-97

(post-Andrew)

2005: biggest real drop in premium since early 1980s

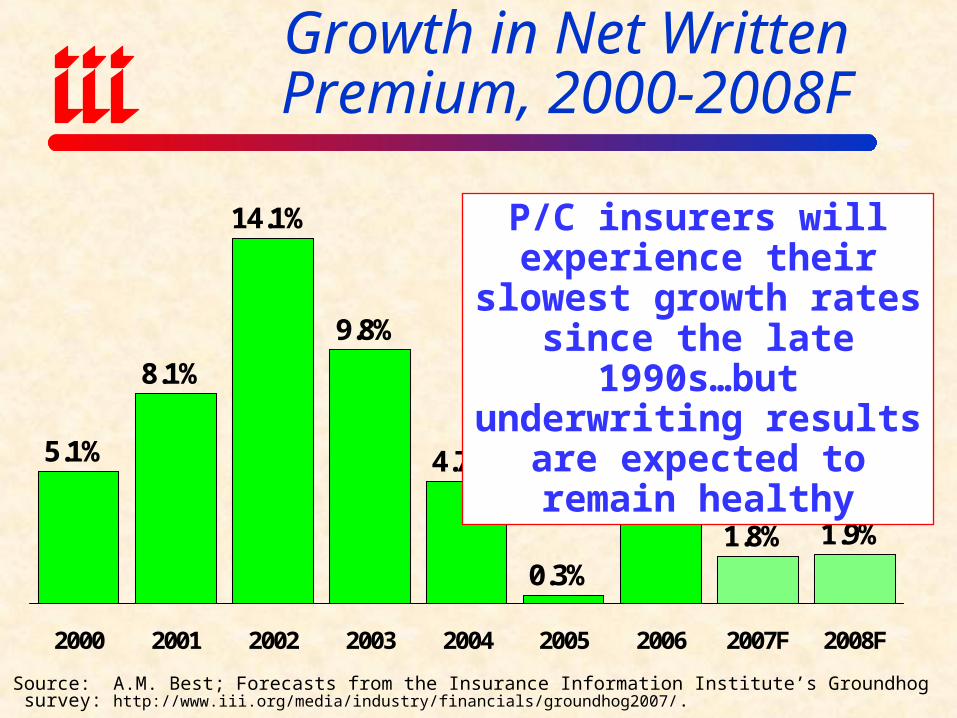

Growth in Net Written Premium, 2000-2008F

Source: A.M. Best; Forecasts from the Insurance Information Institute’s Groundhog survey: http://www.iii.org/media/industry/financials/groundhog2007/.

5.1%

8.1%

14.1%

9.8%

4.7%

0.3%

4.3%

1.8% 1.9%

2000 2001 2002 2003 2004 2005 2006 2007F 2008F

P/C insurers will experience their slowest growth rates since the late 1990s…but underwriting results are

expected to remain healthy

PRICING

Under Pressure in 2007

$651 $6

68 $691 $7

05

$703

$685

$690 $7

24

$780 $8

23 $851

$847

$838

$847

$600

$650

$700

$750

$800

$850

$900

$950

94 95 96 97 98 99 00 01 02 03 04 05* 06* 07*

Average Expenditures on Auto Insurance

*Insurance Information Institute Estimates/ForecastsSource: NAIC, Insurance Information Institute

Countrywide auto insurance expenditures

are expected to fall 0.5% in 2007, the first drop

since 1999

Lower underlying frequency and modest

severity are keeping auto insurance costs in check

Average Homeowners Insurance Expenditure, Selected States, 2004*

Source: NAIC; Insurance Information Institute. *Latest available.

$1,3

62

$1,0

74

$991

$929

$907

$767

$729

$726

$659

$636

$615

$575

$523

$483

$448

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

TX LA OK FL MS MN US MI IL IN KY IA OH WI ID

5 most expensive states are mostly coastal

Most Midwest states have below average home insurance costs.

OH ranks 45th and WI 49th

ID, UT are the least expensive

$418$440 $455

$481 $488 $508$536

$593

$668

$729

$868

$787$835

$400$450$500$550$600$650$700$750$800$850$900

95 96 97 98 99 00 01 02 03 04 05* 06* 07*

Average Expenditures on Homeowners Insurance**

*Insurance Information Institute Estimates/Forecasts**Excludes cost of flood and earthquake coverage.Source: NAIC, Insurance Information Institute

Countrywide home insurance expenditures rose an estimated 6% in 2006, 4% in 2007

Homeowners in non-CAT zones will see

smaller increases, but larger in CAT zones

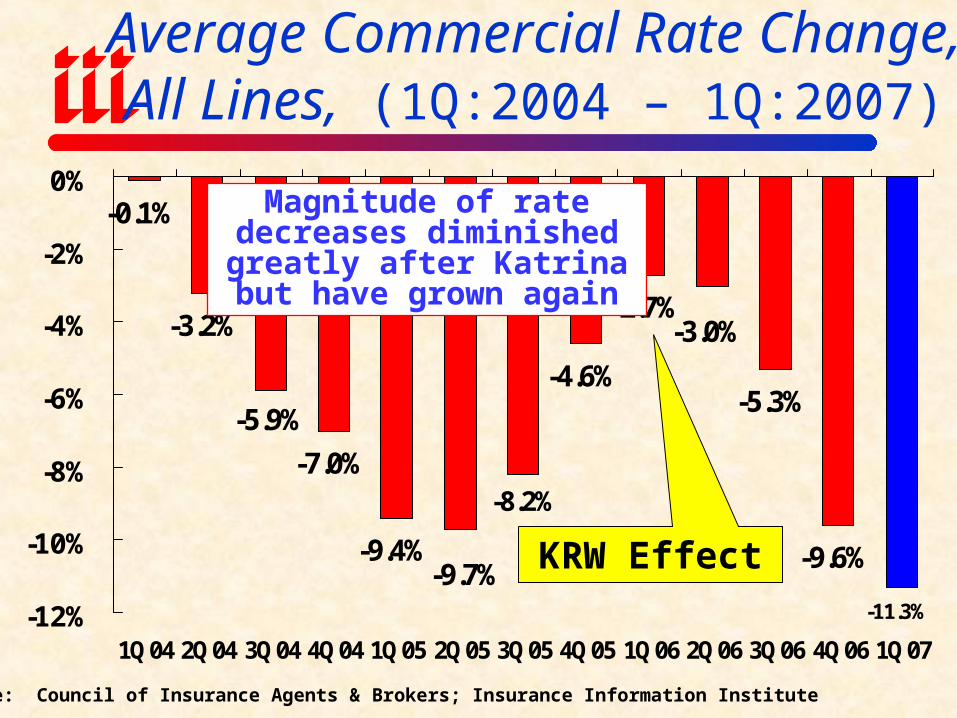

Average Commercial Rate Change,All Lines, (1Q:2004 – 1Q:2007)

-0.1%

-3.2%

-7.0%

-9.4%

-4.6%

-2.7%

-5.3%

-9.6%

-3.0%

-9.7%-11.3%

-5.9%

-8.2%

-12%

-10%

-8%

-6%

-4%

-2%

0%

1Q04 2Q04 3Q04 4Q04 1Q05 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07

Source: Council of Insurance Agents & Brokers; Insurance Information Institute

Magnitude of rate decreases diminished greatly after

Katrina but have grown again

KRW Effect

Average Commercial Rate Change by Line: 4Q99 – 1Q07

Source: Council of Insurance Agents & Brokers

Commercial accounts trended downward from early 2004 to mid-2005

though that trend moderated post-Katrina

Percent of Commercial Accounts Renewing w/Positive Rate Changes, 2nd Qtr. 2006

71%

48%

28%21%

63%

32%

21%

12% 10%

35%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Southeast Southwest Pacific NW Northeast Midwest

Commercial Property Business Interruption

Source: Council of Insurance Agents and Brokers

Largest increases for Commercial Property & Business Interruption are in the Southeast, smallest in Midwest

Percent of Commercial Accounts Renewing w/Positive Rate Changes, 1st Qtr. 2007

11% 9%

0% 0%

8% 5%9%

0% 0%

9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Southeast Southwest Pacific NW Northeast Midwest

Commercial Property Business Interruption

Source: Council of Insurance Agents and Brokers

Commercial Property & Business Interruption

increases are disappearing in the

Southeast; Completely gone in the Midwest &

Northeast

“Soft” market seemed to hit Midwest about 1 year before the rest of the US

CAPACITY/SURPLUS

The Industry in Underleveraged

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

$550

7576777879808182838485868788899091929394959697989900010203040506

U.S. Policyholder Surplus: 1975-2006

Source: A.M. Best, ISO, Insurance Information Institute.

$ B

illi

ons

“Surplus” is a measure of underwriting capacity. It is analogous to “Owners Equity” or “Net Worth” in non-insurance organizations

Capacity as of 12/31/06 was $487.1B (est.), 14.4% above year-

end 2005, 71% above its 2002 trough and 46% above its 1999

peak.Foreign reinsurance and residual market

mechanisms absorbed 45% of 2005 CAT

losses of $62.1B

Annual Catastrophe Bond Transactions Volume, 1997-2006

$966.9

$1,729.8

$4,693.4

$1,991.1

$1,142.8$1,219.5$846.1$984.8

$1,139.0

$633.0

$0$500

$1,000$1,500

$2,000$2,500$3,000

$3,500$4,000

$4,500$5,000

97 98 99 00 01 02 03 04 05 06

Ris

k C

apita

l Iss

ues

($ M

ill)

02

46

81012

1416

1820

Nu

mb

er o

f Iss

uan

ces

Risk Capital Issued Number of Issuances

Source: MMC Securities and Guy Carpenter; Insurance Information Institute.

Catastrophe bond issuance has soared in the wake of Hurricanes

Katrina and the hurricane seasons of 2004/2005

MERGER & ACQUISITION

Few Catalysts for Major P/C Consolidation

P/C Insurance-Related M&A Activity, 1988-2006

$2,4

35

$5,1

00

$19,

118

$40,

032

$1,2

49

$486

$20,

353

$425

$9,2

64

$35,

221

$55,825

$30,

873

$8,0

59

$11,

534

$1,8

82

$3,4

50

$2,7

80

$5,1

37

$5,6

38

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Tran

sact

ion

Val

ue ($

Mill

)

0

20

40

60

80

100

120

140

Num

ber o

f Tra

nsac

tions

Transaction Values Number of Transactions

*Announced May 7 and June 11, respectively.

Source: Conning Research & Consulting.

IN 2007, Liberty Mutual acquired Ohio Casualty

for $2.7B, D.E. Shaw acquired James River for

$575 million*

No model for successful

consolidation has emerged

INVESTMENT IRONY

Markets & Interest Rates Up, Returns Flat

Property/Casualty Insurance Industry Investment Gain*

$ Billions

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7$56.9

$51.9

$57.9

$0

$10

$20

$30

$40

$50

$60

94 95 96 97 98 99 00 01 02 03 04 05** 06*Investment gains consist primarily of interest, stock dividends and realized capital gains and losses. 2006 figure consists of $52.3B net investment income and $3.4B realized investment gain. **2005 figure includes special one-time dividend of $3.2B. Source: ISO; Insurance Information Institute.

Investment gains fell in 2006 and are now only

comparable to gains seen in the late 1990s

CATASTROPHICLOSS

Insurers Accused of Crying Wolf Over Cats

U.S. Insured Catastrophe Losses*$7

.5

$2.7

$4.7

$22.

9

$5.5 $1

6.9

$8.3

$7.4

$2.6 $1

0.1

$8.3

$4.6

$26.

5

$5.9 $1

2.9 $2

7.5

$1.2

$100

.0

$61.

9

$9.2

$0

$20

$40

$60

$80

$100

$120

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

07Q

1

20??

*Excludes $4B-$6b offshore energy losses from Hurricanes Katrina & Rita. Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B.Source: Property Claims Service/ISO; Insurance Information Institute

$ Billions

2006 was a welcome respite. 2005 was by far the worst

year ever for insured catastrophe losses in the US, but the worst has yet to come.

$100 Billion CAT year is coming soon

U.S. Catastrophe Losses 2006: States With Largest Losses ($ Millions)

*ISO defines a catastrophe event as an event causing $25 million or more in insured property losses.

Source: ISO; Insurance Information Institute

$601$688

$873$878

$1,500

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

Indiana Missouri Tennessee Texas Kansas

SURPRISE!! Indiana led the US with $1.5 billion in

insured CAT losses in 2006

Some 33 catastrophe events* in 34 states cost insurers an estimated $8.8bn in 2006, compared with $61.9bn in 2005. Cat losses in the following five states -- totaling $4.5bn -- represent half the

total catastrophe losses for the year.

Number of Tornadoes,1985 – 2006p

1071 12

16

941

1376

1819

1254 13

33

1132

1133

856

702

65676

5

684

1297

1173

1082 12

34

1173

1148

1424

1345

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06p

Source: US Dept. of Commerce, Storm Prediction Center, National Weather Service; Ins. Info. Inst.

There are usually more than 1,000 confirmed tornadoes each year in the US. They accounted for about 25% of

catastrophe losses since 1985

Inflation-Adjusted U.S. Insured Catastrophe Losses By Cause of Loss,

1986-2005¹

Utility Disruption0.1%

Terrorism7.7%

All Tropical

Cyclones3

47.5%

Tornadoes2

24.5%

Water Damage0.1%

Civil Disorders0.4%

Fire6

2.3%

Wind/Hail/Flood5

2.8%

Earthquakes4

6.7%

Winter Storms7.8%

Source: Insurance Services Office (ISO)..

1 Catastrophes are all events causing direct insured losses to property of $25 million or more in 2005 dollars. Catastrophe threshold changed from $5 million to $25 million beginning in 1997. Adjusted for inflation by the III.2 Excludes snow. 3 Includes hurricanes and tropical storms. 4 Includes other geologic events such as volcanic eruptions and other earth movement. 5 Does not include flood damage covered by the federally administered National Flood Insurance Program. 6 Includes wildland fires.

Insured disaster losses totaled $289.1 billion from

1984-2005 (in 2005 dollars). Tropical systems accounted for nearly half of all CAT losses from 1986-2005, up

from 27.1% from 1984-2003.

Hurricane Katrina Claim Status on Storm’s 1st Anniversary*

In Process, 3%

Mediation/ Litigation, 2%

Settled, 95%

95% of the 1.2 million homeowners insurance claims in

Louisiana & Mississippi were

settled by Katrina’s 1st anniversary of Katrina, with just

2% in dispute

*Hurricane Katrina made its north Gulf coast landfall August 29, 2005.Source: Insurance Information Institute survey, August 2006.

Total Value of Insured Coastal Exposure (2004, $ Billions)

$1,901.6$740.0

$662.4$505.8

$404.9$209.3

$148.8$129.7$117.2$105.3

$75.9$73.0

$46.4$45.6$44.7$43.8

$12.1

$1,937.3

$0 $500 $1,000 $1,500 $2,000 $2,500

FloridaNew York

TexasMassachusetts

New JerseyConnecticut

LouisianaS. Carolina

VirginiaMaine

North CarolinaAlabamaGeorgia

DelawareNew Hampshire

MississippiRhode Island

Maryland

Source: AIR Worldwide

Florida & New York lead the way for insured coastal

property at more than $1.9 trillion each.

CAT losses will drive or influence much of industry’s

legislative agenda

REINSURANCE MARKETS

Big Risk, Big Reward orBig Government?

Share of Losses Paid by Reinsurers, by Disaster*

30%25%

60%

20%

45%

0%

10%

20%

30%

40%

50%

60%

70%

Hurricane Hugo(1989)

Hurricane Andrew(1992)

Sept. 11 TerrorAttack (2001)

2004 HurricaneLosses

2005 HurricaneLosses

*Excludes losses paid by the Florida Hurricane Catastrophe Fund, a FL-only windstorm reinsurer, which was established in 1994 after Hurricane Andrew. FHCF payments to insurers are estimated at $3.85 billion for 2004 and $4.5 billion for 2005.Sources: Wharton Risk Center, Disaster Insurance Project; Insurance Information Institute.

Reinsurance is playing an increasingly

important role in the financing of mega-CATs; Reins. Costs

are skyrocketing

Ratio of Reinsurer Loss & Underwriting Expense to Premiums Written, 1985-2006

1.1

0

1.0

8

1.1

0

1.0

3

1.0

2

1.0

6 1.1

4

1.1

3

1.1

7

1.0

1 1.0

6

1.2

6

0.9

5

1.3

9

1.2

1

1.0

6

1.0

7

1.0

7

1.0

9 1.1

8

1.0

7 1.0

8

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

Lo

ss

& L

AE

Ra

tio

Source: Reinsurance Association of America.

Despite the respite in 2006, reinsurers paid an average of $1.11 in loss and expense

for every $1 in written premium since 1985

FINANCIAL STRENGTH &

RATINGS Industry Has Weathered

the Storms Well

Reasons for US P/C Insurer Impairments, 1969-2005

*Includes overstatement of assets.

Source: A.M. Best: P/C Impairments Hit Near-Term Lows Despite Surging Hurricane Activity, Special Report, Nov. 2005;

Catastrophe Losses8.6%

Alleged Fraud11.4%

Deficient Loss

Reserves/In-adequate Pricing62.8%

Affiliate Problems

8.6%

Rapid Growth

8.6%

2003-2005 1969-2005

Deficient reserves,

CAT losses are more important factors in

recent years

Reinsurance Failure3.5%

Rapid Growth16.5%

Misc.9.2%

Affiliate Problems

5.6%

Sig. Change in Business

4.6%

Deficient Loss

Reserves/In-adequate Pricing38.2%

Investment Problems*

7.3%

Alleged Fraud8.6%

Catastrophe Losses6.5%

P/C Insurer Impairments,1969-2006

815

127

11 934

913 12

199

16 14 1336

4931

3449 49

5460

5841

2915

1231

18 1949 50

4735

1813 15

0

10

20

30

40

50

60

70

69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

The number of impairments varies significantly over the p/c insurance cycle,

with peaks occurring well into hard markets

Source: A.M. Best; Insurance Information Institute

STATE RESIDUAL MARKETS

How Big is Too Big?

Florida Citizens Exposure to Loss (Billions of Dollars)

Source: PIPSO; Insurance Information Institute

408.8

$210.6$206.7$195.5

$154.6

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2002 2003 2004 2005 2006

Exposure to loss in Florida Citizens nearly doubled in 2006

Major Residual Market Plan Estimated Deficits 2004/2005 (Millions of Dollars)

* MWUA est. deficit for 2005 comprises $545m in assessments plus $50m in Federal Aid.Source: Insurance Information Institute

-$516

-$1,425

-$1,770

-$954

-$595 *

-$2,000-$1,800-$1,600-$1,400-$1,200-$1,000

-$800-$600-$400-$200

$0

Florida HurricaneCatastrophe Fund

(FHCF) Florida Citizens Louisiana Citizens

Mississippi WindstormUnderwriting

Association (MWUA)

2004 2005

Hurricane Katrina pushed all of the residual market property plans in

affected states into deficits for 2005, following an already record hurricane loss year in 2004

What Role Should the Federal Government

Play in Insuring Against Natural Disaster Risks?

Comprehensive National Catastrophe Plan Schematic

Personal Disaster Account

Private Insurance

State Regional Catastrophe Fund

National Catastrophe Contract Program

Source: NAIC, Natural Catastrophe Risk: Creating a Comprehensive National Plan, Dec. 1, 2005; Insurance Information. Inst.

State Attachment

1:50 Event

1:500 Event

Legislation has been introduced and ideas

espoused by ProtectingAmerica.org will likely get a more

thorough airing in 2007/8

FLORIDA’S APPROACH TO

MANAGING HURRICANE RISK

Does it Add Up?

Pre- vs. Post-Event in FL for 2007 Hurricane Season

$12.

4

$15.

0

$17.

6

$25.

8

$9.9

$14.

6

$24.

1

$31.

4

$34.

5

$37.

4

$54.

2

$10.9$10.4$10.1$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

1-in-20 1-in-30 1-in-50 1-in-70 1-in-85 1-in-100 1-in-250

Pre-Event Funding Post-Event Funding (Assessments & Bonds)

Bil

lion

s

Total = $20.0 Billion

Notes: Pre-event funding includes funds available to Citizens, FHCF and private carriers plus contingent funding available through private reinsurance to pay claims in 2007. Post-event funding is on a present value basis and does not includefinancing costs. Probabilities are expressed as “odds of a single storm of this magnitude or greater happening in 2007.”Source: Tillinghast Towers Perrin, Study of Recent Legislative Changes to Florida’s Property Insurance Mechanisms, 3/07.

$35.0B

$25.0B

$43.8B $49.5B

$55.0B

$80.0BThere is a very significant likelihood of major, multi-year assessments in 2007

Average Annual Assessment per Household, 1-in-100 Year Event in 2007

Source: Tillinghast Towers Perrin, Study of Recent Legislative Changes to Florida’s Property Insurance Mechanisms, 3/07.

The average Florida household will pay $8,699 over 30 years in assessments if a 1-in-100 year

event strikes in 2007. Assessments could rise if additional storms hit

in 2007 or beyond.

Savings vs. Costs by Region: Neither Equitable nor Proportionate

TALLAHASSEEAverage Savings: $20

Cost of 1-in-30 Storm: $2,000Cost is 100 times avg. savings

TAMPAAverage Savings: $100

Cost of 1-in-30 Storm: $2,300Cost is 23 times avg. savings

ORLANDO

Average Savings: $30

Cost of 1-in-30 Storm: $2,075

Cost is 69 times avg. savings

MIAMI

Average Savings: $1,120

Cost of 1-in-30 Storm: $3,375

Cost is 3 times avg. savings

STATEWIDE AVERAGEAverage Savings: $265

Cost of 1-in-30 Storm: $2,550Cost is 10 times avg. savings

Source: Tillinghast Towers Perrin, Study of Recent Legislative Changes to Florida’s Property Insurance Mechanisms, 3/07.

29% 25% 30%

22% 34% 31%

0%

10%

20%

30%

40%

50%

60%

70%

Coastal Counties Interior Counties Noncoastal States

Very unfair

Somewhat Unfair

Source: Insurance Research Council

Public Attitude Monitor 2006: Unfairness of Taxpayer Subsidies

Most non-coastal dwellers believe taxpayer subsidies for coastal property owners are unfair

Coastal States

KEY LINES

Discipline Will Remain (Mostly) Intact in 2007

Private Passenger Auto

101.7101.3101.3101.0

99.5

101.1

103.5

109.5

107.9

104.2

98.4

94.395.1

93.0

90

95

100

105

110

93 94 95 96 97 98 99 00 01 02 03 04 05 06F

Private Passenger Auto Combined Ratio

Average Combined 1993 to 2005= 101.4

Most auto insurers have shown sig-nificant improvements in underwriting

performance since mid-2002

Sources: A.M. Best; III

PPA is the profit juggernaut of the p/c

insurance industry today

Homeowners Insurance

117.7

158.4

113.6118.4

112.7

121.7

101.0

108.2111.4

121.7

109.3

98.294.4

100.3

93

113.0109.4

90

100

110

120

130

140

150

160

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06F

Homeowners Insurance Combined Ratio

Average 1990 to 2005= 113.1

Insurers have paid out an average of $1.13 in losses for every dollar earned

in premiums over the past 16 years

Sources: A.M. Best; III

COMMERCIAL MULTI-PERIL & COMMERCIAL

AUTO

119.0

119.8

108.5

125.0

113.1

115.0

121.0

116.2

116.1

104.9

101.9

100.7

116.8

113.6

115.3

122.4

115.0

117.0

97.3

89.0

97.7

93.8

80

85

90

95

100

105

110

115

120

125

130

95 96 97 98 99 00 01 02 03 04 05

CMP-Liability

CMP-Non-Liability

Commercial Multi-Peril Combined (Liability vs. Non-Liability Portion)

Liab. Combined 1995 to 2004 = 114.6

Non-Liab. Combined = 107.1

Sources: A.M. Best; III

CMP- has improved recently

112.

1

112

113 11

5.9 12

0.5

120.

1

106.

6

99.4

96.6

93.396

.7

102.

2

99.0

99.7

99.0

103.

6

102.

3

95.9

92.1

87.1 90

.7

122.5

80

85

90

95

100

105

110

115

120

125

95 96 97 98 99 00 01 02 03 04 05

Comm Auto Liab Comm Auto PD

Commercial Auto Liability& PD Combined Ratios

Average Combined: Liability = 110.2

PD = 97.1

Sources: A.M. Best; III

Commercial Auto has improved dramatically

WORKERS COMPENSATION

OPERATING ENVIRONMENT

Workers Comp Calendar Year vs. Ultimate Accident Year – Private Carriers

101

97

111

110

107

103

97

101 10

6

119

131

140

135

123

88 87 87

100

101 10

7 115 11

8 122

97

104

96

80

90

100

110

120

130

140

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006p

Calendar Year Accident Year

Percent

p Preliminary AY figure. Accident Year data is evaluated as of 12/31/2006 and developed to ultimateSource: Calendar Years 1994-2005, A.M. Best Aggregates & Averages; Calendar Year 2006p and Accident Years 1994-2006pbased on NCCI Annual Statement Analysis.Includes dividends to policyholders

Workers Comp Combined Ratios, 1994-2006P

Lost-Time Claims

-4.2 -4.4

-6.9

-4.5 -4.1 -3.9

-6.8

-9.2

0.3

-6.5

-4.5

0.5

-3.9

-2.3

-4.5

-6.6

-10

-8

-6

-4

-2

0

2

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06p

Cumulative Change of –52.1%since 1991 means that lost work

time claims have been cut by more than half

Accident Year

Percent Change

Workers Comp Lost-TimeClaim Frequency (% Change)

2003p: Preliminary based on data valued as of 12/31/20061991-2005: Based on data through 12/31/2005, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policiesSource: NCCI

IndemnityClaim Cost (000s)

Lost-Time Claims

$9.9 $9.6 $9.4 $9.8 $10.0$10.6

$11.4$12.4

$13.6

$15.1$16.5$16.9

$17.7$18.0$18.6

$19.6

$5

$7

$9

$11

$13

$15

$17

$19

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06p

Annual Change 1991–1996: +1.2%Annual Change 1997–2005: +6.6%

2005p: Preliminary based on data valued as of 12/31/20061991-2005: Based on data through 12/31/2005, developed to ultimateBased on the states where NCCI provides ratemaking servicesExcludes the effects of deductible policiesSource: NCCI

Accident Year

Workers Comp Indemnity Claims Costs Have Accelerated, 1993-2006p

Cumulative Change = +108.5%(1993-2006p)

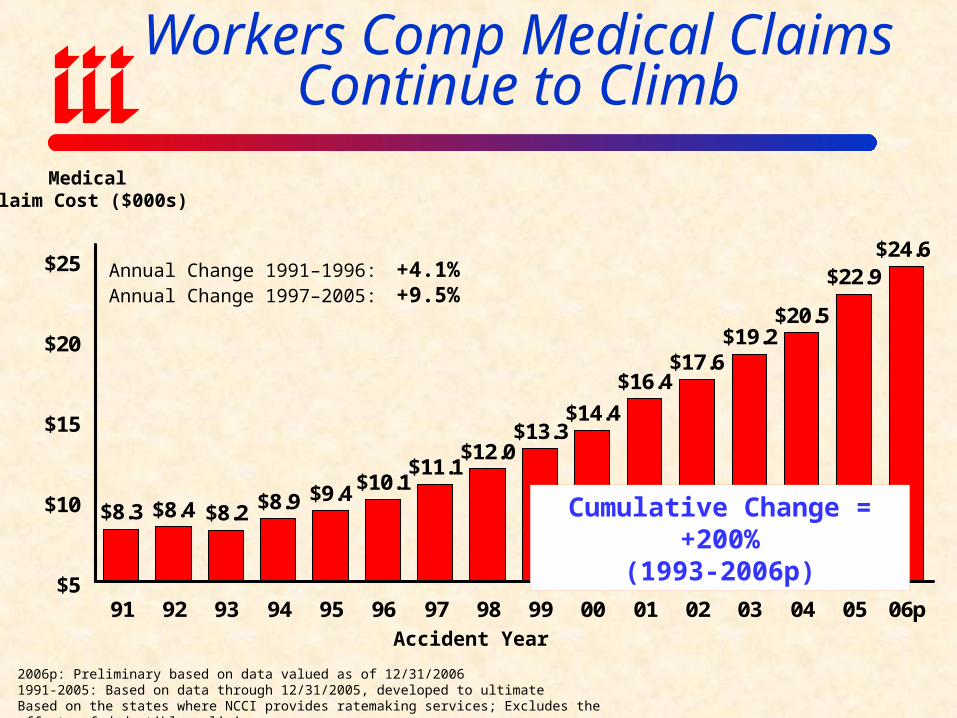

$8.3 $8.4 $8.2 $8.9 $9.4 $10.1$11.1

$12.0$13.3

$14.4

$16.4$17.6

$19.2$20.5

$22.9$24.6

$5

$10

$15

$20

$25

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06p

Annual Change 1991–1996: +4.1%Annual Change 1997–2005: +9.5%

Accident Year

MedicalClaim Cost ($000s)

2006p: Preliminary based on data valued as of 12/31/20061991-2005: Based on data through 12/31/2005, developed to ultimateBased on the states where NCCI provides ratemaking services; Excludes the effects of deductible policies

Workers Comp Medical Claims Continue to Climb

Cumulative Change = +200%(1993-2006p)

Med Costs Share of Total Costs is Increasing Steadily

Indemnity55%

Medical45%

Source: NCCI (based on states where NCCI provides ratemaking services).

Indemnity52%

Medical48%

Indemnity41%

Medical59%1986

1996

2006p

Legal Liability & Tort Environment

Definitely Improving ButNot Out of the Woods

Personal, Commercial & Self (Un) Insured Tort Costs*

$17.0$49.6 $58.7

$95.2

$17.1

$51.0$70.9

$86.7

$5.2

$20.4

$30.0

$49.4

$0

$50

$100

$150

$200

$250

1980 1990 2000 2005

Commercial Lines Personal Lines Self (Un)Insured

Bil

lion

s

Total = $39.3 Billion

*Excludes medical malpracticeSource: Tillinghast-Towers Perrin, 2006 Update on US Tort Cost Trends.

Total = $121.0 Billion

Total = $159.6 Billion

Total = $231.3 Billion

Tort System Costs,2000-2008F

$179

$233$246

$270

$295

$260

$261

$261

$205

1.82%2.03%

2.22% 2.22%

2.04%2.09% 2.03%2.05%

2.24%

$100

$120

$140

$160

$180

$200

$220

$240

$260

$280

$300

00 01 02 03 04 05 06E 07F 08F

Tor

t S

yste

m C

osts

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

Tor

t C

osts

as

% o

f G

DP

Tort Sytem Costs Tort Costs as % of GDP

After a period of rapid escalation, tort system costs as % of GDP are now falling

Source: Tillinghast-Towers Perrin, 2006 Update on US Tort Cost Trends;2006 is III estimate.

REGULATORY UPDATE

Busy Year for Insurersin Washington

Federal Legislative UpdateFederal Terrorism Reinsurance (TRIA)• TRIA expires 12/31/07. The current federal program offers $100 billion of

coverage subject to a $27.5B industry aggregate retention.

• New Democratic Congress (with Committee chairs from urban Northeast states) predisposed to extend. Despite resistance/lackluster Administration support TRIA will likely extended for a multi-year period, perhaps 6-8 but potentially as long as 15 years (last extension in 2005 was for 2 years)

• Potential changes include extensions of coverage for domestic terrorism losses

(not included currently), and a lower industry retention for nuclear, biological, chemical, or radiological (NBCR) attacks. There could possibly be a modestly higher industry retention for non-NBCR losses, and it needs to be resolved whether liability and group life losses will be covered.

• Original hope for first-half 2007 extension have faded. Now looking at fall or even 11th-hour extension as in 2005.

Sources: Lehman Brothers, Insurance Information Institute

Federal Legislative Update

Natural Disaster Coverage• Some insurers are pushing for federal catastrophic risk fund coverage in the

wake of billions of dollars of losses suffered by insurers from the 2004-2005 hurricane seasons.

• Legislative relief addressing property/casualty insurers’ exposure to natural catastrophes, such as the creation of state and federal catastrophe funds, has been advocated by insurers include Allstate and State Farm recently. However, there is active opposition many other insurers and all reinsurers.

• There are supporters in Congress, mostly from CAT-prone states. Skeptics in Congress believe such a plan would be a burden on taxpayers like the NFIP and that the private sector can do a better job. Unlike TRIA, the industry is not unified on this issue.

• Allowing insurers to establish tax free reserves for future catastrophe losses has also been proposed, but Congress has not yet indicated much support.

Sources: Lehman Brothers, Insurance Information Institute

Federal Legislative UpdateMcCarran-Ferguson Insurance Antitrust Exemption• Under McCarran-Ferguson Act of 1945, insurers have limited immunity under

federal anti-trust laws allowing insurers to pool past claims information to develop accurate (actuarially credible) rates.

• Very low level of understanding of M-F in Washington

• Certain legislators threaten to revoke McCarran-Ferguson because of alleged collusion in the wake of Hurricane Katrina. However, the view among some Washington insiders is that such a move would hurt small insurers with less resources rather than the large insurers perhaps being targeted. The current bills designed to revoke McCarran-Ferguson are S.618 and H.R. 1081.

• The government appointed Antitrust Modernization Commission in an April 2007 report strongly encouraged Congress to re-examine the McCarran-Ferguson Act. Notably, 4 of the commissions 12 members called for a full repeal of the law.

Sources: Lehman Brothers, Insurance Info. Institute

Insurance Information Institute On-Line

If you would like a copy of this presentation, please give me your business card with e-mail address