ownership structure and the public private equity … · ownership structure and the public /...

TRANSCRIPT

Ownership Structure and The Public / Private Equity

Choice*

Emma Schultz Garry Twite† Research School of Finance, Actuarial

Studies and Applied Statistics Department of Finance

University of Melbourne Australian National University Carlton, VIC 3010, Australia Canberra, ACT 0200, Australia [email protected]

May 5, 2015

* This paper has benefited from the useful comments and suggestions provided by Andres Almazan, Aydogan Alti, Fernando Anjos, Jonathan Cohn, Carole Comerton-Forde, Neil Fargher, Jay Hartzell, Jacquelyn Humphrey, Wai-Man (Raymond) Liu, Spencer Martin, Phong Ngo, Clemens Sialm, Gloria Tian, Sheridan Titman, Geoff Warren and seminar participants at the Australian National University, Monash University, University of Newcastle and University of Texas at Austin. † Corresponding author, Department of Finance, Faculty of Business & Economics, The University of Melbourne, Carlton, VIC 3010, Australia; email: [email protected]; phone: +61 3 9035 6172; fax: +61 3 8344 1900.

2

Ownership Structure and The Public / Private Equity Choice

Abstract

We take advantage of both the relatively high concentration of insider ownership in

Australian firms, absent the dominance of founding families, and the widespread issuance

of non-tradable rights to examine the heterogeneous influence of insider and monitor

shareholders on the firm’s public/private choice. By focusing on determinants of the

underwriting arrangements in these issues, we highlight monitoring demand, not control

dilution avoidance, as the key driver of the public/private choice in a general setting

where firms are controlled by non-founding insiders. Importantly, the nature of this

demand is shown to depend on pre-issue ownership concentration: While firms with low

pre-issue monitor concentration use private placements as a means of acquiring

additional monitoring, those with higher concentration use private placements to

substitute insiders for monitors, reducing the level of independent oversight.

JEL: G32

Keywords: Equity Issuance, Private/Public Choice, Insiders, Monitors, Rights Issues

1

1. Introduction

The vast majority of firms will, at some stage, have insufficient internal funding to

finance both ongoing operations and growth investments. At this point, firms turn to

external sources to help overcome their funding shortfall and, to the extent they issue

equity, face a choice between making a public issue1 or private placement (“the

public/private choice”). In this paper, we examine the influence of ownership structure

on this public/private choice. In particular, we consider the tradeoff between the demand

for enhanced monitoring and the avoidance of control dilution by insiders, focusing on

determinants of the underwriting decisions made in relation to non-tradable rights issues

to provide evidence in this regard. As pro-rata allocations made to existing shareholders,

the choice regarding participation in non-renounceable issues rests solely with

shareholders who, in the absence of tradability, can only opt out of a given issue by

letting the rights expire. Consequently, the placement of unsubscribed shares can only be

undertaken by either the underwriter or management, meaning the underwriting decision

is the sole determinant of whether unsubscribed shares are placed privately or publicly.2

By choosing to underwrite the issue, managers transfer responsibility for placing

unsubscribed shares to the underwriting firm, equivalent to a firm commitment offering.

Conversely, by electing not to underwrite a non-tradable issue, managers retain the right

1 Empirical evidence suggests that firms exhibit clear preferences for particular methods of public issuance (Eckbo et al, 2007). Specifically, while most U.S. firms obtain equity financing via firm commitment underwritten seasoned equity offerings (“SEOs”), rights offerings (both standby underwritten and uninsured) continue to be the dominant issuance method in other regions including Australasia and Europe (Eckbo, 2008; and, Massa et al, 2013). Rights issues see current shareholders given a short-term option or “right” to purchase new shares on a pro-rata basis, invariably at a discount to their current market value. 2 This is contrast to SEOs and tradable rights offers, where issues are made to the public from the outset or can be accessed by the public via the purchase of tradable rights, respectively, and are therefore fundamentally public in nature regardless of underwriting arrangements.

2

to place unsubscribed shares with investors of their choosing, that is they choose to make

a private placement.

We build on the existing literature by providing evidence on whether the

observation that family-controlled firms seek to avoid control dilution when issuing

equity (Cronqvist and Nilsson, 2005) extends to the more general setting of firms

controlled by non-founding insiders. Exploring the role of ownership structure in equity

issues made by Australian listed firms allows us to take advantage of their relatively high

concentration of insider ownership, absent the dominance of founding families (Glassop,

2009; Mroczkowski and Tanewski, 2007; and, Masulis et al, 2011), and their use of an

issue type not widely adopted elsewhere, namely the non-tradable rights issue.3

Moreover, studying whether both insider and monitor shareholder ownership affect the

underwriting decisions made in relation to these issues allows us to acknowledge the

heterogeneity of these two shareholder groups as well as the tradeoff made between the

demand for increased monitoring and a desire to avoid control dilution when making

seasoned equity offerings.

We report two main results. Firstly, monitoring demand, not control dilution

avoidance, is the key driver of the public/private choice, with firms having larger and

more concentrated pre-issue monitor shareholdings being more likely to privately place

unsubscribed shares via non-underwritten non-tradable rights issues. However, post-

issue ownership changes for firms electing to make private placements show the nature of

3 The Australian equity market is characterised by both tradable and non-tradable rights issues (referred to as renounceable and non-renounceable issues, respectively, in the Australian context). These issuance methods differ fundamentally in their treatment of the entitlements of current shareholders who elect not to participate in the offer. While current shareholders are able to sell tradable rights, shareholders who do not wish to participate in a non-tradable issue must simply allow the offer to expire. Notwithstanding these differences, tradable and non-tradable issues do not differ materially in terms of their disclosure requirements or the lack of a limit on the maximum allowed level of issue discount.

3

this demand varies markedly with firms’ pre-issue monitor ownership concentration. In

particular, companies with low pre-issue monitor concentration exhibit a positive demand

for monitoring, using private placements as a means of purchase additional oversight of

managers. In contrast, firms with higher pre-issue monitor concentration use these issues

to substitute inside for monitor concentration and, in doing so, reduce the likelihood of

outside shareholder oversight of managers.

Overall, our results highlight monitoring demand, not control dilution avoidance,

as the key driver of the public/private choice in the more general setting of firms

controlled by non-founding insiders. These findings are in stark contrast to those

documented in relation to family-controlled firms, where control dilution avoidance is a

primary determinant of the public-private choice (Cronqvist and Nilsson, 2005).

Importantly, our findings stem from investor-level classification of each type of

owner as monitors or insiders and a research design which mitigate measurement issues

in previous studies stemming from the comparison of fundamentally different issue

methods. With respect to the former, we define monitors to include institutional

shareholders identified within the existing literature to be effective in monitoring the

activities of management4 and individual outsiders whose time-series pattern of

significant ownership in multiple listed firms suggest they behave like professional

investors that are most likely independent of management and, thus, to closely monitor

managerial actions. Conversely, as the name suggests, insiders are the officers and

4Institutional investors include superannuation and pension funds, which have a dominant position within the Australian market. During our sample period, superannuation and pension funds represented 63% of all institutional invested funds, with the residual being equally divided between mutual funds and life insurance. As noted previously, Cremers and Nair (2005) argue that pension funds face fewer conflicts of interest than other institutional investors and they tend to be effective in monitoring the activities of management.

4

directors of the firm they own shares in. Classification is undertaken for each individual

shareholder and also gauges the size and concentration of their shareholdings at the time

the non-tradable offer is made. By studying how both groups affect both the

public/private choice and the outcome of a private placement, we not only acknowledge

their heterogeneity but also recognize the tradeoff made between the demand for

increased monitoring and a desire to avoid control dilution when making seasoned equity

offerings. In focusing on both size and concentration, we employ a more robust measure

of monitoring and control than advanced previously (see, for example, Wu, 2004).

Finally, in terms of research design, existing public/private choice studies

invariably confound issuance method and underwriting decisions, comparing seasoned

equity offerings or tradable rights issues, both underwritten and non-underwritten, with

private placements (see, for example, Wu, 2004; Eckbo and Norli, 2005; and, Cronqvist

and Nilsson, 2005). In contrast, we focus on a single corporate decision, namely the

underwriting choice, made in relation to otherwise identical methods of equity raising

and, in doing so, minimize confounding issues.,

The remainder of the paper is organized as follows. Section 2 describes institutional

structure underlying Australian equity issues during the period of this study. Section 3

introduces our methodology. Section 4 describes the sample. Section 5 presents our

results and Section 6 draws some conclusions.

2. The Australian Institutional Landscape

Rights issues are the dominant method of seasoned equity issuance in Australasia (Eckbo,

2008; and, Massa et al, 2013). Their popularity in Australia can, at least in part, be

5

explained by the Australian Securities Exchange (“the ASX”) listing rules. Specifically,

while ASX Listing Rule 7.1 limits the size of seasoned offerings that can be made

without prior shareholder approval to 15% of issued capital, Exemption 1 renders certain

specific issuance methods, including rights offers, exempt from these limitations. This

method of issuance is made even more attractive by the relatively relaxed disclosure

requirements attached to them as a pro-rata offer type.

Rights issues conducted on the ASX can either be tradable, allowing shareholders

who do not wish to exercise their right to participate in the pro-rata offer to trade this

entitlement on the ASX, or non-tradable. Shareholders not wishing to take up rights in a

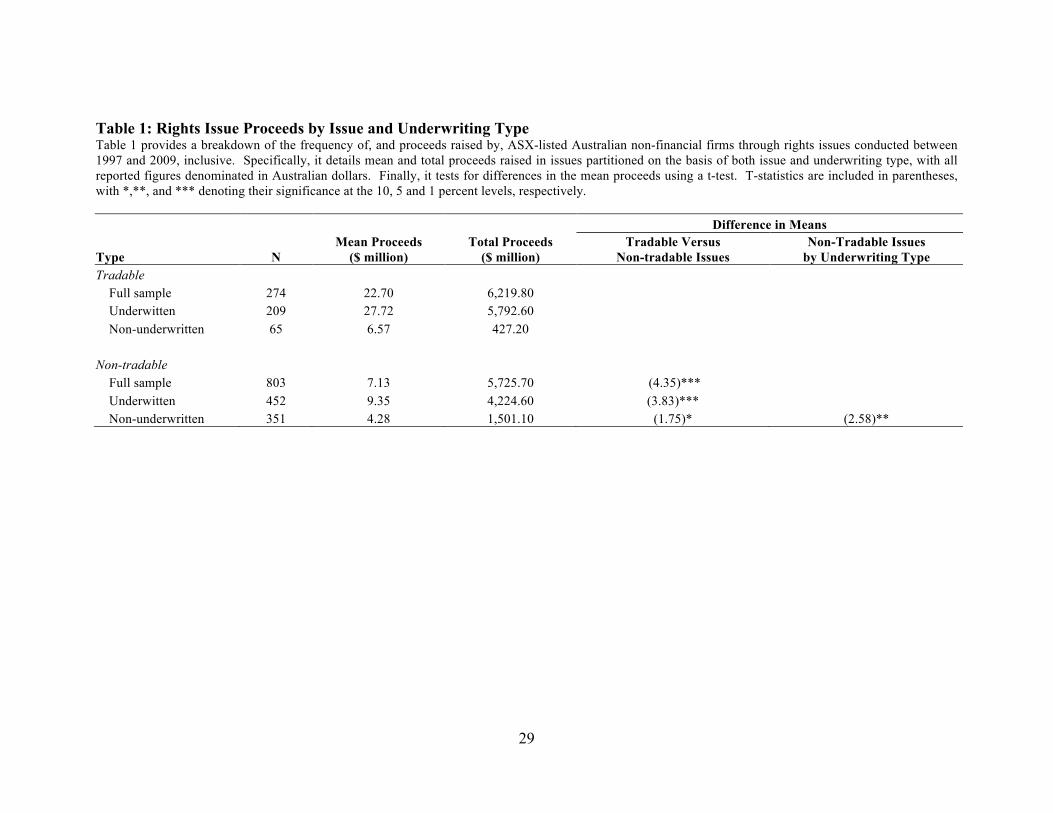

non-tradable issue simply leave their offer to expire. Table 1 provides a breakdown of

rights issues conducted by ASX-listed Australian firms in the period 1997 to 2009,

inclusive, detailing both the frequency of, and proceeds raised by, issues during this

period. Examination of the table reveals that, while non-tradable rights issues were far

more common during our sample period, they were smaller in size: Although there were

803 (274) non-tradable (tradable) issues conducted over the period, they only raised an

average of $7.13 million ($22.70 million) for the issuing firm. Further, as a cautionary

note, non-tradable issues tend to be undertaken by smaller, less-levered firms. More

specifically, total assets (leverage5) for firms undertaking tradable versus non-tradable

issues averaged $121.29 million (0.1898) and $30.06 million (0.0829), respectively.

Despite first impressions, we conjecture that transaction costs incurred by the

issuing company do not vary markedly based on rights issue tradability. In particular,

disclosure requirements are identical for both issue types, and there is no limit imposed

on the maximum permissible issue discount in either case. Indeed, it is for these reasons 5 Measured as the book value of debt over the market value of the firm.

6

that the use of non-tradable rights issues in Australia is so widespread. Further, to the

extent tradable rights are traded on the ASX, and incur additional listing fees for the

issuing firms, they are only traded for very short periods,6 with lapsed rights sold via a

bookbuilding at the conclusion of the trading period. Thus, the incremental transaction

costs for tradable rights issues are minimal.

Three underwriting arrangements are utilized by firms participating in non-tradable

rights issues, namely standby underwriting, best-efforts underwriting and non-

underwriting. The key distinction between standby underwriting and non-underwriting

lies in the right to allocate unsubscribed shares. In the case of standby underwriting, the

underwriter purchases the unsubscribed shares from the firm before placing them. As the

proceeds of standby underwritten offerings are guaranteed by the underwriter and

responsibility for the placement of unsubscribed shares rests with them, these issues are

equivalent to firm commitment offerings. In contrast, non-underwritten issues see

management maintain responsibility for the placement of unsubscribed shares, playing a

significant role in identifying the investors who receive the unsubscribed portion of

shares.7 Best-efforts underwriting differ from standby underwriting agreements in that,

while the underwriter agrees to assist management in both promoting the issue and

allocating unsubscribed shares, they do not agree to purchase the unsubscribed shares

from the issuing firm. For this reason, we classify best-efforts agreements as non-

underwritten issues.8

6 Increasingly, tradable issues are completed on an accelerated basis and, thus, do not involve any exchange trading of rights at all. 7 Within our sample all firms raised the full amount sought exante, either via enforcing the underwriting agreement or private placement. 8 We test the robustness of our results to this classification in Section 5.3.

7

Table 1 highlights the dominance of underwritten non-tradable rights issues in our

sample, with approximately 56% of non-tradable issues conducted in this manner.

[Table 1 about here]

3. Methodology

In examining the determinants of the public/private choice, we consider the relationship

between the likelihood of a firm undertaking a private placement in the form of an non-

underwritten non-tradable rights issue and pre-issue concentration of both monitors’ and

insiders’ ownership as well as insiders’ pre-issue control margin. Thereafter, we consider

changes in ownership concentration measures following the successful completion of the

offering.

3.1 Explanatory Variables

3.1.1 Monitoring Demand

Private placements see large bundles of shares allocated to a small number of investors.

Given empirical evidence that the incentive of shareholders to monitor management

differs based on their independence (Yermack, 1996) and the magnitude of their holdings

relative to those of other shareholders (Fiss, 2006), concentrated independent

shareholders should be best incentivized to monitor the actions of management (see, for

example, Shleifer and Vishny, 1986; and, Wruck, 1989). Therefore, it follows that firms

8

wishing to increase the monitoring of management will use private placements to affect

an increase in the concentration of independent shareholdings.9

We define monitoring shareholders to include managed funds, superannuation,

pension funds and other financial firms identified within the existing literature to be

effective in monitoring the activities of management (see, for example, Cremers and

Nair, 2005) together with individual outsiders whose time-series pattern of significant

ownership in multiple listed firms suggests they behave like professional investors that

are most likely to be independent of management, and, thus, to closely monitor

managerial actions. With respect to the latter, we include shareholders who are not

officers or directors of by the firm and with holdings of at least 5% of the firm’s total

shares in at least 5 firms in any year and/or in a given firm for at least 5 years. We

measure the size and concentration of monitors’ shareholdings using a Herfindahl

measure (“Monitor Herfindahl”) calculated as:

Where Monitor Herfindahli,t is the Herfindahl measure of the size and

concentration of monitor ownership in firm i at the end of the reporting year immediately

preceding the pro-rata issue, t; and, Shareholdingj,i,t is the shareholding of monitor j in

9 Wu (2004) uses data on SEOs conducted by a sample of high-technology post-IPO firms to document a decrease in the blockholdings of shareholders following private placements. Although Wu (2004) selects these firms to ensure a sample with high levels of information asymmetry, evidence suggests that they are also more likely to be subject to financial constraint and / or financial distress (see, for example, Brophy et al, 2009; and, Chaplinsky and Haushalter, 2010). This, in turn, will reduce the importance of monitoring as a motive for the firms undertaking a private placement.

2

, ,,

1, ,

1

nj i t

i t nj

j i tj

ShareholdingMonitor Herfindahl

Shareholding=

=

⎛ ⎞⎜ ⎟⎜ ⎟=⎜ ⎟⎜ ⎟⎝ ⎠

∑∑

9

firm i at this time. With a demand for enhanced monitoring, we expect that the Monitor

Herfindahl will increase following a private placement in the form of a non-underwritten

non-tradable rights issue, Nonunderwritten. Where Nonunderwritten is an indicator

variable equal to one if a rights issue is both non-tradable and non-underwritten, and zero

otherwise.

3.1.2 Control Dilution Avoidance

To the extent that seasoned equity offerings see shares placed with outsiders, they

threaten the private benefits insiders can extract from the firm. Thus, to the extent they

are able, insiders will ensure that new shares are placed privately and in a way that

ensures control dilution does not ensue. Consistent with this conjecture, Cronqvist and

Nilsson (2005) document dilution avoidance as an important determinant of the

private/public choice, with family controlled firms shying away from issuance methods

where this is mostly likely to occur. We extend Cronqvist and Nilsson’s (2005) analysis

to study control dilution avoidance by non-founding insiders in a market characterized by

relatively high concentration of insider ownership where family firms are not the

dominant organizational form (Glassop, 2009; Mroczkowski and Tanewski, 2007; and,

Masulis et al, 2011). In doing so, we argue that these shareholders will be averse to

equity issues which have the potential to adversely affect their control by reducing their

level of ownership concentration, introducing a new blockholder who may monitor their

actions and / or increasing the monitoring activity being undertaken by existing owners.

In our experiment, the potential for such control dilution arises when the underwriter is

responsible for allocating the unsubscribed shares in an underwritten non-tradable issue,

10

as they purchase any unsubscribed shares from the firm prior to placing them.

Conversely, non-underwritten non-tradable issues allow management to place

unsubscribed shares with a party of their choosing.

While we believe insiders’ preference for non-underwritten non-tradable issues

will exist regardless of their level of pre-issue ownership, the extent to which insiders can

avoid control dilution by influencing with whom shares are placed depends critically on

both the size and concentration of their ownership at the time equity is placed.

Specifically, the higher and more concentrated their ownership before the issue, the better

placed they are to ensure issuance methods with the potential to dilute their control are

avoided. That is, the more concentrated pre-issue insider ownership is, the more likely

the firm will undertake a private placement. As with monitor ownership, we measure the

size and concentration of insider holdings with a Herfindahl measure (Inside Herfindahl),

and expect that firms with high pre-issue values of this metric will seek to preserve or

enhance the status quo via these private placements. More specifically, with the

avoidance of control dilution, we expect that Inside Herfindahl (Monitor Herfindahl) will

not decrease (increase) following the completion of a non-underwritten non-tradable

rights issue, Nonunderwritten, in these cases.

In addition, we recognize that the extent to which insiders can avoid control

dilution by influencing with whom shares are placed also depends on the size of their

control margin at the time equity is placed. Specifically, the larger their control margin,

the better placed they are to ensure issuance methods with the potential to dilute their

control are avoided. We measure the control margin as the difference between total

11

insider ownership and total monitor ownership divided by the ownership of the firms’ top

20 shareholders (Insider Control Margin).

3.2 Firm Characteristics Existing literature documents a positive relationship between the level of information

asymmetry faced by a firm and the likelihood it will undertake a private placement,

arguing concentrated private investors are most likely to incur the cost associated with

learning about such firms (see, for example, Hertzel and Smith, 1993; Chemmanur and

Fulghieri, 1999; Wu, 2004; Cronqvist and Nilsson, 2005; and, Gomes and Phillips, 2006).

We control for information asymmetry by including various proxies in our

regressions. Measures previously employed as information asymmetry proxies are

varied but are commonly related to analyst coverage or activity (see, for example, Wu,

2004; and, Gomes and Phillips, 2007). As our sample is characterized by a relatively low

level of, and low cross-sectional variation in, analyst coverage, we utilise other measures

of information asymmetry. Specifically, consistent with Wu (2004), we include bid-ask

spread, defining our measure as the 12-month average of the daily time-weighted average

bid-ask spread (Spread). In addition, consistent with Wu (2004) and Cronqvist and

Nilsson (2005), we employ an age-based measure, equal to the natural logarithm of the

years since incorporation (ln(Age)), in testing. Based on existing evidence, we expect

information asymmetry costs to result in a negative (positive) relationship between

12

ln(Age) (Spread) and whether the firm undertakes a private placement in the form of a

non-underwritten non-tradable rights issue (Nonunderwritten).10

We also include characteristics which the existing literature (Wu, 2004, Cronqvist

and Nilsson, 2005, Gomes and Phillips, 2007, Balachandran et al, 2008) identifies as

affecting the firm’s relative need for, and supply of, funding in the reporting year

immediately preceding their pro-rata issue and, thus, their likelihood of opting for the

issuance method with the greatest chance of raising the requisite monies. Specifically,

with respect to the former, we control for: Size, measured as the natural logarithm of total

assets (ln(Assets)); Growth prospects, measured as the market value of equity scaled by

the book value of equity (Price/Book); and, Capital expenditure, or the ratio of capital

expenditure to total assets (Capex). We control for firms’ supply of funds by including

measures of their: Liquid assets, defined as ratio of cash and marketable securities to total

assets (Cash); Leverage, or the book value of their total debt divided by the sum of the

book value of total debt and the market value of common stock outstanding (Leverage)11;

Profitability, or the ratio of earnings before interest, taxes, depreciation and

amortization12 scaled by total assets (EBITDA); and, Financial constraint, measured using

an indicator variable equal to one if a firm is in the top tertile when firms are ranked by

10 As detailed in Section 5.3, robustness testing also sees us employ both the number of analysts following the firm and an indicator variable equal to one if the firm is followed by one or more analysts as alternative proxies for information asymmetry. 11 Ursel (2006) reports the use of rights issues in the US as largely confined to financially distressed firms. While these findings suggest a potential financial distress bias in our sample, we argue it is unlikely given the widespread use of rights issues in Australia. Regardless, we control for financial distress by including financial leverage in our regressions. 12 We use this in preference to earnings before interest and taxation, EBIT, which has the potential to be distorted by large depreciation charges likely made by the numerous capital-intensive mining firms included in our sample.

13

leverage and it did not pay a cash dividend during the year, and zero otherwise

(Constraint)13.

Finally, similar to Cronqvist and Nilsson (2005), we include an expected take-up

measure in modeling to control for the predicted negative relationship between a rights

offering’s adverse selection costs and the estimated rate of shareholder participation at a

given level of undervaluation (Eckbo and Masulis, 1992). Our expected take-up measure

(Take-up) is equal to the fitted value obtained by regressing the ratio of proceeds raised to

funds sought through the issue (Proceeds), against the percentage discount offered on

shares purchased under the rights issue relative to the market price current at the time of

the announcement of the issue (Discount), shareholdings of the firms’ Top 20 owners

(Top Ownership) and the natural logarithm of the market value of equity (ln(MktCap)).

3.3 Pre-Issue Ownership and the Public/Private Choice

We employ a logistic regression to examine the relationship between the levels of pre-

issue monitor and insider concentration as well as the insider control margin and whether

firms decide to undertake a private placement in the form of a non-underwritten non-

tradable rights issue (Nonunderwritten), fitting a model of the following form:

𝑁𝑜𝑛𝑢𝑛𝑑𝑒𝑟𝑤𝑟𝑖𝑡𝑡𝑒𝑛!,! = 𝛼 + 𝛽𝑀𝑜𝑛𝑖𝑡𝑜𝑟 𝐻𝑒𝑟𝑓𝑖𝑛𝑑𝑎ℎ𝑙!,!!! + 𝛿𝐼𝑛𝑠𝑖𝑑𝑒𝑟 𝐻𝑒𝑟𝑓𝑖𝑛𝑑𝑎ℎ𝑙!,!!! + 𝜃𝐼𝑛𝑠𝑖𝑑𝑒𝑟 𝐶𝑜𝑛𝑡𝑟𝑜𝑙 𝑀𝑎𝑟𝑔𝑖𝑛!,!!! + 𝛾𝐹𝑖𝑟𝑚 𝐿𝑒𝑣𝑒𝑙 𝐶𝑜𝑛𝑡𝑟𝑜𝑙𝑠!,!!! + 𝜗𝐼𝑛𝑑𝑢𝑠𝑡𝑟𝑦 𝐷𝑢𝑚𝑚𝑖𝑒𝑠!,!!! + 𝜀!,!

Where Firm Level Controlsi,t-1 are vectors comprising our information asymmetry

proxies and firm-level accounting variables as previously defined, and Industry 13 As per note 11, we also include an estimate of financial constraint in response to the findings documented by Ursel (2006).

14

Dummiesi,t-1 is a 1-digit industry membership indicator variable. All variables are

measured in the year before the rights issue is announced.

3.4 Changes in Ownership Concentration

We study post-issue changes in the size and concentration of both monitor and insider

shareholdings, considering whether these changes differ systematically by underwriting

type. More specifically, defining the year a firm undertakes a rights issue as t, we first

perform a t-test of differences in the mean changes in both monitor ownership

concentration (ΔMonitor Herfindahl) and insider ownership concentration (ΔInside

Herfindahl) for underwritten versus non-underwritten non-tradable issues between years

t-1 and t+1. If firms use private placements to purchase additional monitoring, we would

expect the mean change in monitor ownership concentration for non-underwritten non-

tradable issues to be significantly larger than for underwritten non-tradable issues.

Conversely, a significantly larger (smaller) mean change in insider (monitor) ownership

concentration for non-underwritten issues relative to underwritten issues would be

consistent with the avoidance of control dilution.

Next we narrow our focus to non-underwritten non-tradable rights issues,

examining whether the tradeoff between the demand for monitoring and the avoidance of

control dilution differs based on the level of pre-issue ownership concentration. To the

extent that private placements are drive by a demand for monitoring, we would expect

that firms with low pre-issue monitor ownership concentration would experience a

significant increase in this concentration as a result of the issue.

15

4. Data

Our sample comprises all rights issues announced by ASX-listed Australian non-financial

firms between 1997 and 2009, inclusive.14 To better understand the dimensions along

which non-tradable offers differ from their tradable equivalents, we also include details

of the latter. We exclude issues made by financial firms, or those with a 1-digit Standard

Industry Classification (“SIC”) code equal to 6, from our sample given fundamental

differences in their operations and regulation. Details of our issues of interest are sourced

from Thomson Reuters SDC Platinum. Thereafter, we source details of Top 20

shareholdings for firms making non-tradable issues from the annual reports available via

Connect4. We categorize shareholders included in these lists as insiders if they are

officers and directors of the issuing firm and monitors if their identity or cross-sectional

and time-series pattern of ownership suggests they will likely monitor the actions of

management. Accounting and share price data for issuing firms are then obtained from

Thomson Reuters Worldscope and Thomson Reuters Datastream, respectively. All

explanatory variables are winsorized at the 0.25th and 99.75th percentiles.

Our final sample comprises 803 non-tradable rights issues made by 562 unique

firms.15 As noted previously, 462 (351) of these issues are underwritten (non-

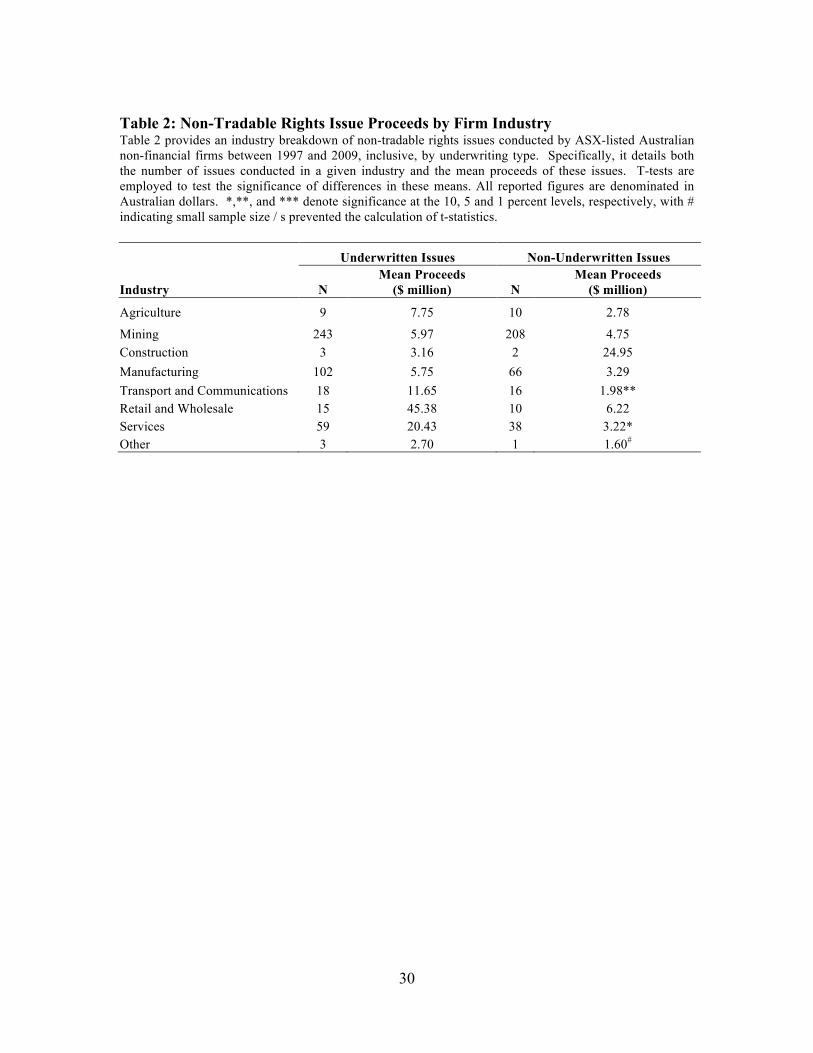

underwritten). Table 2 provides an industry breakdown of the sample of non-tradable

rights issues by underwriting type. Examination of this table yields two conclusions.

14 Cronqvist and Nilsson (2005) remove all rights issues that have a private placement attached to them. Unfortunately, our data sources do not permit the identification and, thus, exclusion of these issues from testing. While we acknowledge the noise these issues introduce, their inclusion in our sample only biases against us finding a significant result for the role of monitoring in the public/private choice. Thus, any significant result we do find is particularly strong. 15 While visual examination suggests an increase in the annual number announced after 2000 in our sample, subsequent investigation confirms this is increase is the result of improved coverage by our chosen databases rather than any changes in regulation. Moreover, with this exception, we observe no clear time-series pattern in the number of issues made.

16

Firstly, for a given industry, non-underwritten non-tradable issues are invariably smaller

and less frequent than underwritten non-tradable issues; and, Secondly, the weighting of

industries for issuing firms is reasonably representative of the market overall. One

notable exception is mining firms, who are slightly over-represented in our sample.

[Table 2 about here]

17

5. Results

Using our sample of non-tradable rights issues, we use two distinct but complementary

approaches to test our predictions regarding the public/private choice. Specifically, we

first consider the relationship between the pre-issue level of ownership concentration, the

insider control margin and the likelihood the firm undertakes a private placement.

Thereafter, we consider post-issue changes in ownership concentration to better

understand the outcomes of making such a placement.

5.1 Pre-Issue Ownership Concentration, the Insider Control Margin and the

Public/Private Choice

Panel A of Table 3 focuses on mean issue characteristics by underwriting type, also

presenting the results of tests for differences in these means. Results suggest that both

proceeds and expected take-up rates are smaller for non-underwritten than underwritten

issues. The fact the issue discount is smaller for non-underwritten non-tradable issues is

consistent with firms using these issues as de-facto private placements. The lower the

discount, the less subscribed the issues will be and, thus, the greater the proportion of

shares that can be placed at the discretion of company management.

Panel B of Table 3 reports mean firm-level, rather than issue-level, characteristics

of issuing firms. It is clear that non-underwritten issues are undertaken by smaller

capital-intensive firms. However, there is no evidence of a statistically significant

difference in information asymmetry between firms making underwritten versus non-

underwritten issues. Further, irrespective of whether the issue is underwritten, we observe

18

higher levels of insider and monitor ownership, together with the level of holdings of the

top 20 shareholders.

Examination of Panel B of Table 3 reveals two interesting features of the data.

Firstly, irrespective of whether the issue is underwritten, monitor shareholders hold a

higher fraction of the firm than insiders and, hence, the insider control margin is negative.

Secondly, results show that the concentration of monitor shareholdings is also higher than

the concentration of insider shareholdings. Interestingly, the pre-issue concentration of

monitor shareholdings and insider control margin are also higher in those firms

undertaking non-underwritten non-tradable issues. In contrast, there is no evidence of a

statistically significant difference in the pre-issue concentration of insider shareholdings

in firms making underwritten versus non-underwritten issues. Taken together, these two

results provide preliminary evidence that the demand for monitoring, rather the desire to

avoid control dilution, drives the public/private choice.

[Table 3 about here]

The role played by the demand for monitoring in shaping firms’ decisions to raise

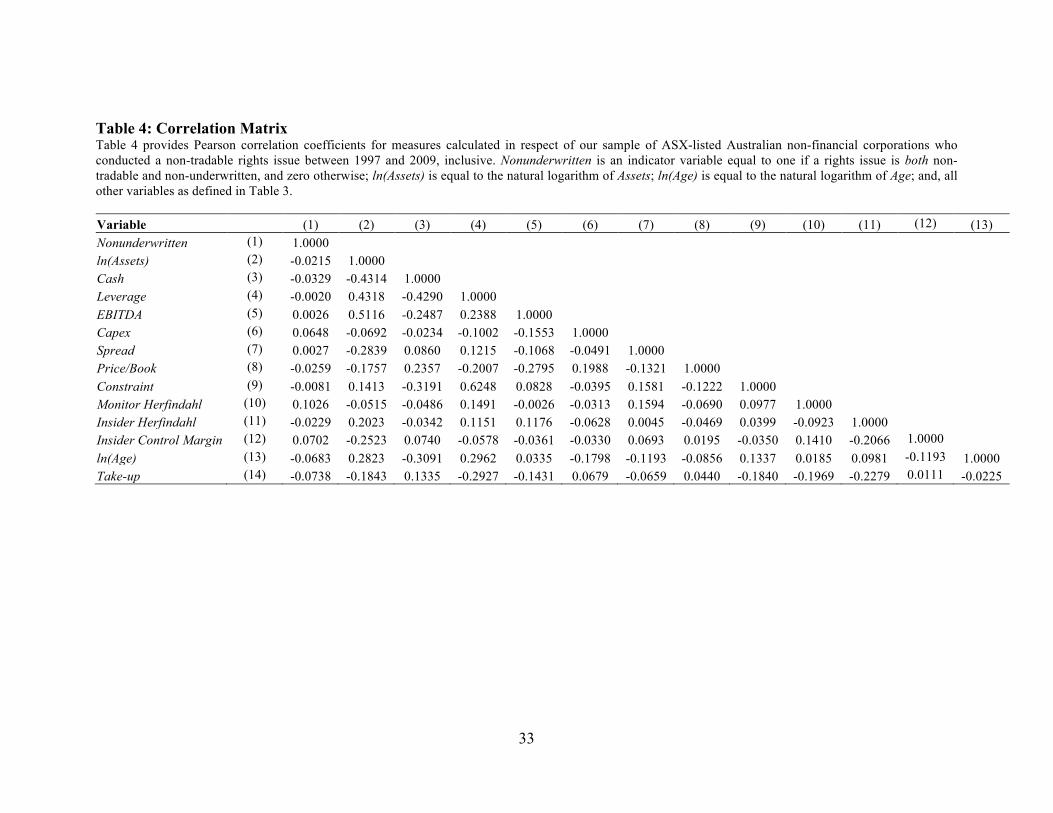

equity publicly versus privately is further supported by the Pearson correlation

coefficients reported in Table 4, which suggest that the underwriting choice is influenced

by the size and concentration of pre-issue monitor shareholdings as well as the insider

control margin. More specifically, higher values of both Monitor Herfindahl and Insider

Control Margin are associated with non-underwritten non-tradable issues, that is, private

placements.

19

Table 4 also confirms our proposed regression analysis is unlikely to be plagued

by collinearity problems. In particular, while we observe the expected correlation

between firm level control variables, our variables of interest (Inside Herfindahl, Monitor

Herfindahl and Insider Control Margin) are not highly correlated with each other.

[Table 4 about here]

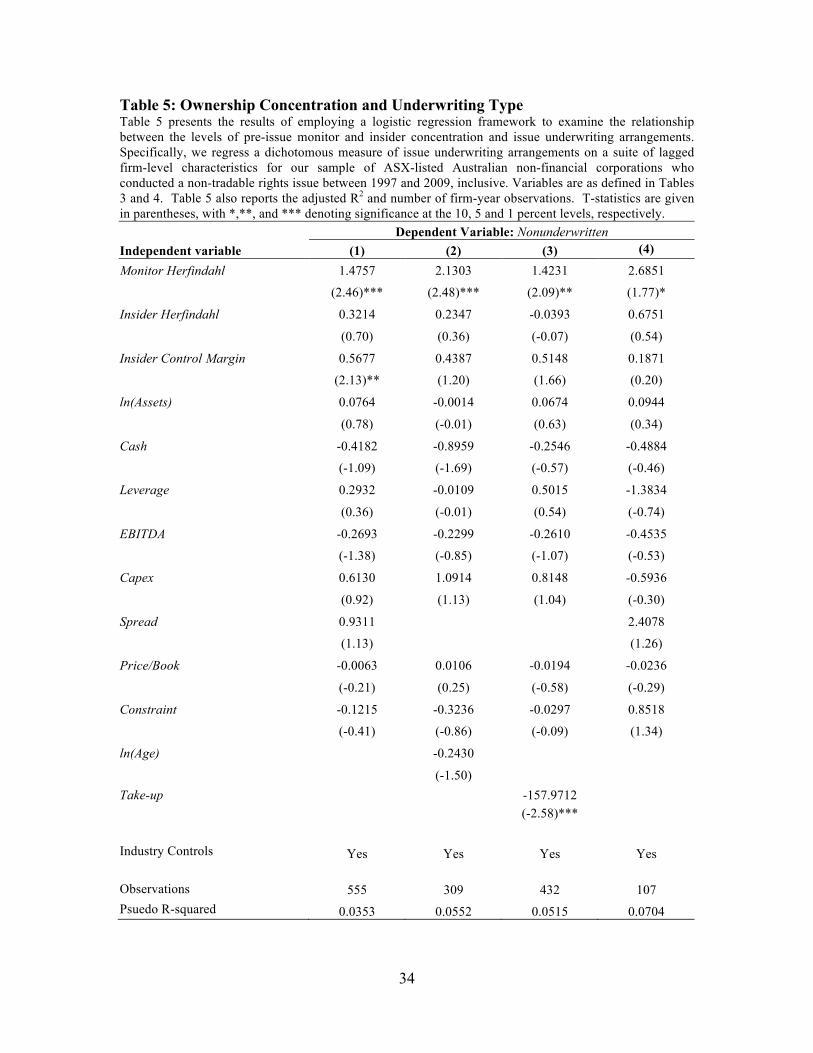

Table 5 presents regressions that estimate the relationship between the levels of

pre-issue monitor and insider concentration as well as the insider control margin and the

public/private choice whilst controlling for information asymmetry and other firm-level

characteristics known to influence both the equity issuance and underwriting decisions. In

all regressions we measure the levels of pre-issue ownership concentration as Monitor

Herfindahl and Insider Herfindahl, while the level of insider control is measured as

Insider Control Margin. Columns 1 and 2 differ in the measure of information

asymmetry they employ: In Column 1 we measure information asymmetry as Spread,

while Column 2 measures it as ln(Age). Column 3 presents the results for a regression

that includes the expected take-up rate, Take-Up, as an explanatory variable. Finally,

Column 4 replicates the regression presented in Column 1 for the subsample of firms

with both Insider Herfindahl greater than the sample mean and Insider Control Margin

greater than zero, that is, a controlling interest held by a small number of insiders.

The results presented in Table 5 confirm that the size and concentration of pre-

issue monitor shareholdings strongly influences the choice of underwriting in non-

tradable issues. In particular, a higher Monitor Herfindahl is associated with the choice of

20

a non-underwritten issue, that is, a private placement. This result persists regardless of

our model specification. In contrast to the existing literature (Cronqvist and Nilsson,

2005), we find no support for the influence of pre-issue insider ownership concentration,

defined to include non-founding insiders, in affecting the public/private choice.

Moreover, while we find weak support for the level of the insider control margin

influencing the choice of underwriting in non-tradable issues, with a higher Insider

Control Margin associated with the choice of a private placement in the form of a non-

underwritten issue in our first model this result does not persist across all our model

specifications. Instead, the result is statistically insignificant in all but the regression

reported in Column 1, including for the subsample of firms with a controlling interest

held by a small number of insiders (Column 4). Instead, for this subsample of firms,

where insiders have the potential to control the firm, we find no support for either pre-

issue insider ownership concentration or control influencing the choice to undertake a

private placement.

[Table 5 about here]

In summary, our strongest finding suggest that firms with larger and more

concentrated pre-issue monitor shareholdings are more likely to allocate unsubscribed

shares via a private placement. Therefore, our findings thus far are consistent with the

conjecture that in the more general setting of firms controlled by non-‐founding

insiders private placements are primarily driven by a demand for monitoring rather than

avoiding control dilution.

21

5.2 Post Issue Changes in Ownership Concentration

We next examine the change in both monitor and insider shareholding concentration

around both non-underwritten non-tradable rights issues (private placements) and

underwritten non-tradable issues (public issues). The results of tests for differences in the

mean change in ownership concentration classified by underwriting type are presented in

Panel A of Table 6. These results reveal a significantly larger post-issue increase in

monitor ownership concentration levels for firms undertaking private placements as

opposed to firms undertaking private public issues. Notwithstanding this, the post-issue

changes in insider ownership concentration do not differ materially based on

underwriting type. Taken together, these findings suggest that the average firm uses

private placements to acquire enhanced monitoring rather than avoid control dilution.

For firms having chosen to undertake a private placement, it remains an open

question as to the effect of the tradeoff between the demand for monitoring and the

avoidance of control dilution on the outcome of the private placement. For this reason

we narrow our focus to examine the relationship between pre-issue ownership

concentration levels and changes in these levels post-issue. Specifically, we rank firms

who undertook non-underwritten non-tradable rights issues based on their pre-issue levels

of monitor ownership concentration, defining firms falling into the first (fourth) quartile

as having low (high) pre-issue ownership concentration. Thereafter, we test whether the

mean post-issue change in both monitor and insider ownership concentration differs for

firms with low versus high pre-issue monitor concentration levels. The results of this

testing are presented in Panel B of Table 6, and provide further evidence consistent with

22

monitoring demand driving the choice to undertake a private placement. Specifically, we

find that monitor concentration increases for firms with low pre-issue concentration

levels. In stark contrast, firms with high pre-issue levels experience a reduction in this

concentration after the issue. This, coupled with the significant increase in post-issue

insider ownership concentration, is consistent with firms enjoying high and concentrated

levels of monitoring in the lead up to the issue using private placements as a way of

substituting insider for monitor shareholders, reducing the likelihood of increased

monitoring activity being undertaken by existing monitors.

[Table 6 about here]

Table 7 presents regressions for firms who undertook non-underwritten non-

tradable rights issues that estimate the relationship between pre-issue monitor

shareholding concentration and changes in both monitor and insider shareholding

concentration around the rights issue whilst controlling for information asymmetry and

other firm-level characteristics known to influence both the equity issuance and

underwriting decisions. We include two additional (indicator) variables in these

regressions, namely High Monitor Herfindahl and Low Monitor Herfindahl. High

Monitor Herfindahl is equal to one if Monitor Herfindahl for a given firm is in the top

quartile of the sample, and zero otherwise, while Low Monitor Herfindahl is equal to one

if Monitor Herfindahl for a given firm is in the bottom quartile of the sample, and zero

otherwise. Examination of the results presented in Table 7 show that for firms

undertaking a private placement, consistent with our univariate results, monitor

concentration increases following the issue for firms with low pre-issue concentration

23

levels. In stark contrast, firms with high pre-issue levels experience a reduction in this

concentration after the issue and a significant increase in post-issue insider ownership

concentration.

[Table 7 about here]

In summary, our results suggest that the influence of the demand for enhanced

monitoring on the choice to undertake a private placement depends upon the pre-issue

monitor concentration levels. At low pre-issue levels of monitor shareholder

concentration firms exhibit a positive demand for enhanced monitoring. However, at

high levels, firms use private placements to substitute insider for monitor shareholders,

reducing the likelihood of increased monitoring activity being undertaken by existing

monitors.

5.3 Robustness Tests

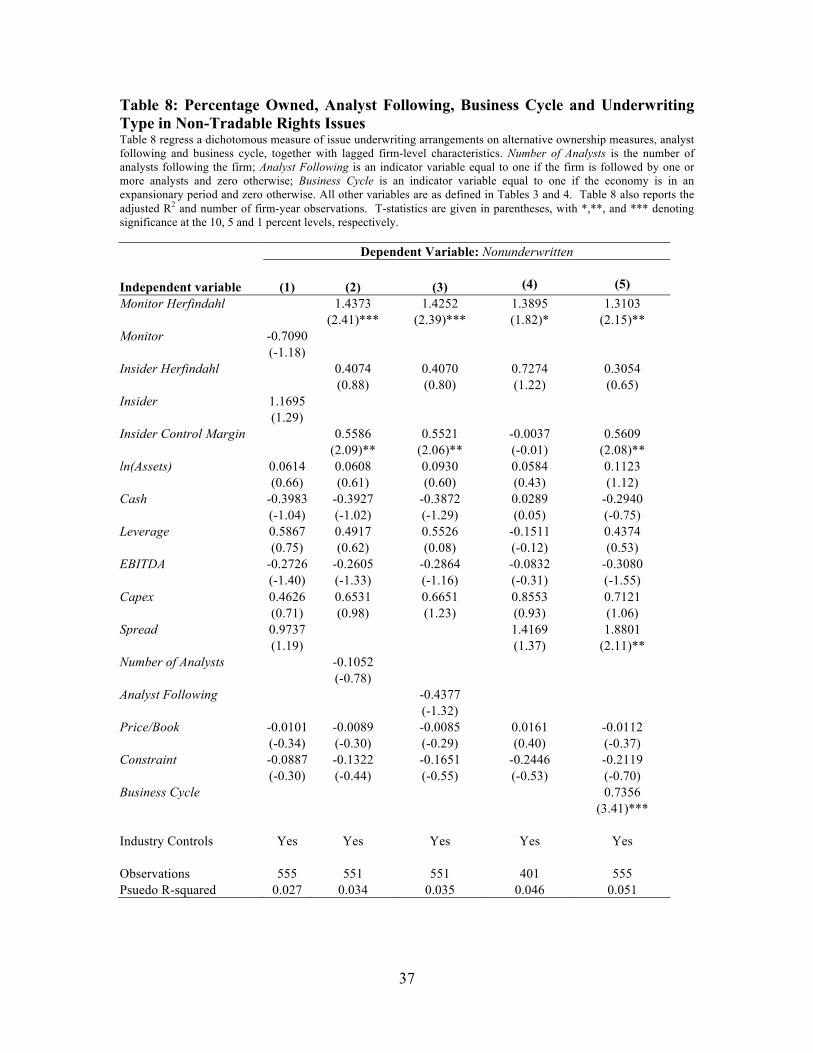

In the first of our robustness tests, we follow Wu (2004) and use ownership percentages

rather than Herfindahl measures of ownership concentration in testing. Results are

presented in Column 1 of Table 8 and provide no support for the percentage of either

monitor or insider shareholdings being significant in influencing the public/private

choice. Coupling these findings with the significance of Monitor Herfindahl in this

regard provides support for monitor shareholders having the greatest incentive to

scrutinize and influence firm operations when their holdings are large and concentrated.

24

Next, we follow Wu (2004) and Gomes and Phillips (2007), employing both the

number of analysts following the firm (Number of Analysts) and an indicator variable

equal to one if the firm is followed by one or more analysts (Analyst Following) as

alternative proxies for information asymmetry. We make use of annual analyst earnings

forecasts from IBES to estimate these proxies. Our results (Columns 2 and 3, Table 8) are

robust to the inclusion of alternative proxies for information asymmetry. Consistent with

the results reported in Table 5, firms with larger and more concentrated pre-issue monitor

shareholdings are more likely to allocate unsubscribed shares via a private placement.

With respect to information asymmetry, we again find no evidence in support of a

positive relationship between information asymmetry and the choice to undertake private

placements within our sample. This result is consistent with the lack of a statistically

significant difference in information asymmetry between firms making underwritten

versus non-underwritten issues reported in Table 3.

To recognize the potential for the inclusion of non-tradable issues with best

efforts arrangements to bias our sample of non-underwritten issues, we exclude them

from our sample and re-perform testing. Our results (Column 4, Table 8) are robust to

the exclusion of best efforts issues, albeit weaker. Firms with larger and more

concentrated pre-issue monitor shareholdings are more likely to allocate unsubscribed

shares via a private placement.

It is possible that market conditions impact on both the level of rights issues and

the supply of underwriters. In particular, we conjecture that there will be more rights

issues and more underwriters willing to underwrite these issues during periods of

economic expansion. We test the impact of theses by including an indicator variable

25

equal to one if the Melbourne Institute Business Cycle Dates suggest the economy is in

an expansionary period and zero otherwise (Business Cycle). Unexpectedly, as depicted

in Column 5 of Table 8, we find evidence that firms are more likely to undertake private

placements in expansionary periods. However, consistent with the results reported in

Table 5, we still find that firms with larger and more concentrated pre-issue monitor

shareholdings are more likely to allocate unsubscribed shares via a private placement.

[Table 8 about here]

6. Conclusions

We take advantage of both the relatively high concentration of insider ownership in

Australian firms, absent the dominance of founding families, and the widespread use of

non-tradable rights issues in the Australian equity market to better understand

determinants of the public/private choice. We first examine the importance of the size

and concentration of pre-issue monitor and insider shareholdings as well as the level of

insider control on firms’ decisions to underwrite these issues. In doing so, we

demonstrate it is the demand for monitoring, and not the avoidance of control dilution nor

the level of insider control, that is pivotal in shaping the firm’s decision to place equity

privately. Initial testing shows that, on average, firms with higher and more concentrated

pre-issue levels of monitor shareholdings are more likely to place unsubscribed shares

privately. More importantly, post-issue changes in ownership reveal that the influence of

the demand for monitoring on the choice of a private placement varies based on firms’

pre-issue monitor concentration. While post-issue monitor concentration increases in

26

firms with low levels of pre-issue monitor concentration, the reverse is true for firms with

high levels. Indeed, the latter substitute inside for monitor ownership concentration,

thereby reducing the level of independent oversight of the firm.

Overall, our strongest finding suggest that firms with larger and more

concentrated pre-issue monitor shareholdings are more likely to allocate unsubscribed

shares via a private placement. The finding of no support for the influence of pre-issue

insider ownership concentration or insider control on the public/private choice, with the

inclusion of firms controlled by non-founding insiders in our definition of insiders,

suggests that the positive influence of insider control on the decision to undertake a

private placement is restricted to family-controlled firms (Cronqvist and Nilsson, 2005).

As per our earlier caveat, non-tradable issues tend to be undertaken by smaller,

less-levered firms. Given this, to the extent that larger firms enjoy increased analyst

following and this coverage substitutes for the monitoring that can be secured by private

placements, our results may not be generalizable to such firms. Notwithstanding this, our

results provide concrete support that the demand for monitoring is the central determinant

in many firms’ decisions to make private issues.

27

References

Balachandran, B., Faff, R., Theobald, M., 2008. Rights offerings, takeup, renounceability, and underwriting status. Journal of Financial Economics 89, 328-346.

Brophy, D., Ouimet, P., Sialm, C., 2009. Hedge funds as investors of last resort? Review of Financial Studies 22, 541-574.

Byrd, J., Hickman, K., 1992. Do outside directors monitor managers? Evidence from tender offer bids. Journal of Financial Economics 32, 195-221.

Chaplinsky, S., Haushalter, D., 2010. Financing under extreme uncertainty: contract terms and returns to private investments in public equity. Review of Financial Studies 23, 2789-2820. Chemmanur, T., Fulghieri, P., 1999. A theory of going-public decision. The Review of Financial Studies 12, 249-279. Cremers, M., Nair, V., 2005. Governance mechanisms and equity prices. Journal of Finance 60, 2859-94. Cronqvist, H, Nilsson, M., 2005. The choice between rights offerings and private equity placements”, Journal of Financial Economics, 78, 375-407. Eckbo, B., 2008. Equity issues and the disappearing rights offer phenomenon. Unpublished working paper. Tuck School of Business at Dartmouth, Hanover. Eckbo, B., Masulis, R., 1992. Adverse selection and the rights offer paradox. Journal of Financial Economics 32, 293–332. Eckbo, B., Masulis, R., Norli, O., 2007. Security offerings. In: Eckbo, B. (Ed.), Handbook of Corporate Finance. Elsevier/North-Holland, Amsterdam, pp. 233-373. Eckbo, B., Norli, O., 2005. The equity flotation method pecking order. Unpublished working paper. Tuck School of Business at Dartmouth, Hanover. Glasop, L., 2009, Australia’s top 100 private family firms, Unpublished working paper, Deakin University. Gomes, A., Phillips, G., 2007. Why do public firms issue private and public securities? Unpublished working paper. Washington University, Saint Louis. Hertzel M., Smith, R., 1993. Market discounts and shareholder gains for placing equity privately. Journal of Finance 48, 459-485. Massa, M., Vermaelen, T., Xu, M., 2013. Rights offerings, trading, and regulation: a global perspective. Unpublished working paper. INSEAD, Fontainebleau. Masulis, R.W., Pham, P.K., Zein, J., 2011, Family Business Groups around the World: Financing Advantages, Control Motivations, and Organizational Choices, The Review of Financial Studies 24, 3556-3600.

Mroczkowski, N., Tanewski, G., 2007, Delineating publicly listed family and nonfamily controlled firms: an approach for capital market research in Australia, Journal of Small Business Management 45, 320–332.

28

Shleifer, A., Vishny, R., 1986. Large shareholders and corporate control. Journal of Political Economy 94, 461-488.

Ursel, N., 2006. Rights offerings and corporate financial condition. Financial Management 35, 31-52.

Wruck, K., 1989. Equity ownership concentration and firm value: evidence from private equity financings. Journal of Financial Economics 23, 2-28.

Wu, Y., 2004. The choice of equity-selling mechanisms. Journal of Financial Economics 74, 93 – 119.

29

Table 1: Rights Issue Proceeds by Issue and Underwriting Type Table 1 provides a breakdown of the frequency of, and proceeds raised by, ASX-listed Australian non-financial firms through rights issues conducted between 1997 and 2009, inclusive. Specifically, it details mean and total proceeds raised in issues partitioned on the basis of both issue and underwriting type, with all reported figures denominated in Australian dollars. Finally, it tests for differences in the mean proceeds using a t-test. T-statistics are included in parentheses, with *,**, and *** denoting their significance at the 10, 5 and 1 percent levels, respectively. Difference in Means

Type N Mean Proceeds

($ million) Total Proceeds

($ million) Tradable Versus

Non-tradable Issues Non-Tradable Issues

by Underwriting Type Tradable

Full sample 274 22.70 6,219.80 Underwitten 209 27.72 5,792.60 Non-underwritten 65 6.57 427.20

Non-tradable Full sample 803 7.13 5,725.70 (4.35)*** Underwitten 452 9.35 4,224.60 (3.83)*** Non-underwritten 351 4.28 1,501.10 (1.75)* (2.58)**

30

Table 2: Non-Tradable Rights Issue Proceeds by Firm Industry Table 2 provides an industry breakdown of non-tradable rights issues conducted by ASX-listed Australian non-financial firms between 1997 and 2009, inclusive, by underwriting type. Specifically, it details both the number of issues conducted in a given industry and the mean proceeds of these issues. T-tests are employed to test the significance of differences in these means. All reported figures are denominated in Australian dollars. *,**, and *** denote significance at the 10, 5 and 1 percent levels, respectively, with # indicating small sample size / s prevented the calculation of t-statistics.

Underwritten Issues Non-Underwritten Issues

Industry N Mean Proceeds

($ million) N Mean Proceeds

($ million)

Agriculture 9 7.75 10 2.78

Mining 243 5.97 208 4.75 Construction 3 3.16 2 24.95 Manufacturing 102 5.75 66 3.29 Transport and Communications 18 11.65 16 1.98** Retail and Wholesale 15 45.38 10 6.22 Services 59 20.43 38 3.22* Other 3 2.70 1 1.60#

31

Table 3: Characteristics of Non-Tradable Rights and Their Issuing Firms Panel A: Issue Characteristics Panel A compares the mean characteristics of underwritten versus non-underwritten non-tradable rights issues made by ASX-listed Australian non-financial firms between 1997 and 2009, inclusive. T-tests are employed to test the significance of differences in these means. Variables are defined as follows: Dilution is the rights issue ratio; Discount is the discount offered on shares purchased under the rights issue relative to the market price current at the time of the issue announcement; Private/Total is the difference between the funds sought and the proceeds raised by the issue scaled by the funds sought; Fees are underwriting and other fees incurred in making the rights issue expressed as a fraction of the issue proceeds; Take-up is the expected take-up rate for the rights issue and is equal to the fitted value obtained by regressing the ratio of Proceeds to funds sought through the issue against Discount, Top Ownership (proportion of firm’s outstanding common stock owned by the top 20 shareholders) and the natural logarithm of the market value of equity; Proceeds is the money raised by conducting the rights issue; and, Proceeds/Book is the ratio of Proceeds to the book value of equity; All reported figures are denominated in Australian dollars with *,**, and *** denoting significance at the 10, 5 and 1 percent levels, respectively.

Underwritten Issues Non-Underwritten Issues

Variable N Mean N Mean

Dilution 452 0.7003 351 0.7018

Issue Discount 327 0.2030 245 0.1291***

Private/Total 452 0.2391 351 0.2577

Fees 254 0.0323 29 0.0200***

Take-up 294 0.1967 230 0.1964**

Proceeds ($ million) 452 9.3500 351 4.2800**

Proceeds/Book 452 0.6793 351 0.4752***

32

Panel B: Firm Characteristics Panel B compares the mean characteristics of ASX-listed Australian non-financial firms making underwritten versus non-underwritten non-tradable rights issues between 1997 and 2009, inclusive. T-tests are employed to test the significance of differences in these means. Variables are defined as follows: Assets is the book value of total assets; Sales is net sales and other operating revenues; Cash is the cash and other marketable securities over total assets; Fixed Assets is the ratio of fixed to total assets; Goodwill is goodwill divided by total assets; Leverage is the book value of total debt divided by the sum of the book value of total debt and the market value of common stock outstanding; Constraint is a financial constraint indicator variable equal to one if a firm is in the top tertile when firms are ranked by leverage and it did not pay a cash dividend during the year, and zero otherwise. Turnover is sales divided by total assets; Income is net income before extraordinary items and dividends over total assets; R&D is research and development expenditure scaled by total assets; Capex is the ratio of capital expenditure to total assets; Depreciation represents the ratio of depreciation charges to total assets; EBITDA is the ratio of earnings before interest, tax, depreciation and amortization to total assets; Dividends is cash dividends scaled by total assets; Price/Book is the market value of equity scaled by the book value of equity; Price/Book+ is the Price/Book ratio for firms with a positive book value of equity; Spread is the 12-month average of the daily time-weighted average bid-ask spread; Monitor is proportion of total shareholding held by monitors; Insider is proportion of total shareholding held by insiders; Monitor Herfindahl is a Herfindahl measure of the concentration of monitors’ shareholdings; Insider Herfindahl is a Herfindahl measure of the concentration of insiders’ shareholdings; and, Insider Control Margin is insider minus monitor ownership divided by the ownership of the firms’ Top 20 shareholders. All variables are lagged one period. All reported figures are denominated in Australian dollars with *,**, and *** denoting significance at the 10, 5 and 1 percent levels, respectively.

Underwritten Issues Non-Underwritten Issues

Variable N Mean N Mean

Assets ($ million) 436 34.3371 333 24.4714*

Sales ($ million) 430 26.5087 327 13.1627***

Cash 436 0.3379 333 0.3187

Fixed Assets 404 0.4495 318 0.4757

Goodwill 419 0.0444 317 0.0471

Leverage 409 0.0826 310 0.0819

Constraint 452 0.1806 351 0.1743

Turnover 430 0.4091 327 0.3285

Income 430 -0.3735 330 -0.3928

R & D 149 0.1113 109 0.0652**

Capex 430 0.0933 329 0.1170**

Depreciation 410 0.0333 314 0.0310

EBITDA 397 -0.3247 298 -0.3217

Dividends 425 0.0023 328 0.0020

Price/Book 409 3.0149 311 2.8447

Price/Book+ 398 3.1240 299 2.9979

Spread 452 0.1056 351 0.1047

Age 251 19.5894 212 17.5707

Monitor 382 0.2742 314 0.2413***

Insider 382 0.1127 314 0.1228

Monitor Herfindahl 363 0.2417 298 0.2715**

Insider Herfindahl 363 0.3187 298 0.2914

Insider Control Margin 374 -0.2698 307 -0.2089**

Top Ownership 406 0.5642 336 0.5504

33

Table 4: Correlation Matrix Table 4 provides Pearson correlation coefficients for measures calculated in respect of our sample of ASX-listed Australian non-financial corporations who conducted a non-tradable rights issue between 1997 and 2009, inclusive. Nonunderwritten is an indicator variable equal to one if a rights issue is both non-tradable and non-underwritten, and zero otherwise; ln(Assets) is equal to the natural logarithm of Assets; ln(Age) is equal to the natural logarithm of Age; and, all other variables as defined in Table 3. Variable (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) (11) (12) (13) Nonunderwritten (1) 1.0000 ln(Assets) (2) -0.0215 1.0000 Cash (3) -0.0329 -0.4314 1.0000 Leverage (4) -0.0020 0.4318 -0.4290 1.0000 EBITDA (5) 0.0026 0.5116 -0.2487 0.2388 1.0000 Capex (6) 0.0648 -0.0692 -0.0234 -0.1002 -0.1553 1.0000 Spread (7) 0.0027 -0.2839 0.0860 0.1215 -0.1068 -0.0491 1.0000 Price/Book (8) -0.0259 -0.1757 0.2357 -0.2007 -0.2795 0.1988 -0.1321 1.0000 Constraint (9) -0.0081 0.1413 -0.3191 0.6248 0.0828 -0.0395 0.1581 -0.1222 1.0000 Monitor Herfindahl (10) 0.1026 -0.0515 -0.0486 0.1491 -0.0026 -0.0313 0.1594 -0.0690 0.0977 1.0000 Insider Herfindahl (11) -0.0229 0.2023 -0.0342 0.1151 0.1176 -0.0628 0.0045 -0.0469 0.0399 -0.0923 1.0000 Insider Control Margin (12) 0.0702 -0.2523 0.0740 -0.0578 -0.0361 -0.0330 0.0693 0.0195 -0.0350 0.1410 -0.2066 1.0000 ln(Age) (13) -0.0683 0.2823 -0.3091 0.2962 0.0335 -0.1798 -0.1193 -0.0856 0.1337 0.0185 0.0981 -0.1193 1.0000 Take-up (14) -0.0738 -0.1843 0.1335 -0.2927 -0.1431 0.0679 -0.0659 0.0440 -0.1840 -0.1969 -0.2279 0.0111 -0.0225

34

Table 5: Ownership Concentration and Underwriting Type Table 5 presents the results of employing a logistic regression framework to examine the relationship between the levels of pre-issue monitor and insider concentration and issue underwriting arrangements. Specifically, we regress a dichotomous measure of issue underwriting arrangements on a suite of lagged firm-level characteristics for our sample of ASX-listed Australian non-financial corporations who conducted a non-tradable rights issue between 1997 and 2009, inclusive. Variables are as defined in Tables 3 and 4. Table 5 also reports the adjusted R2 and number of firm-year observations. T-statistics are given in parentheses, with *,**, and *** denoting significance at the 10, 5 and 1 percent levels, respectively. Dependent Variable: Nonunderwritten Independent variable (1) (2) (3) (4)

Monitor Herfindahl 1.4757 2.1303 1.4231 2.6851

(2.46)*** (2.48)*** (2.09)** (1.77)*

Insider Herfindahl 0.3214 0.2347 -0.0393 0.6751

(0.70) (0.36) (-0.07) (0.54)

Insider Control Margin 0.5677 0.4387 0.5148 0.1871

(2.13)** (1.20) (1.66) (0.20)

ln(Assets) 0.0764 -0.0014 0.0674 0.0944

(0.78) (-0.01) (0.63) (0.34)

Cash -0.4182 -0.8959 -0.2546 -0.4884

(-1.09) (-1.69) (-0.57) (-0.46)

Leverage 0.2932 -0.0109 0.5015 -1.3834

(0.36) (-0.01) (0.54) (-0.74)

EBITDA -0.2693 -0.2299 -0.2610 -0.4535

(-1.38) (-0.85) (-1.07) (-0.53)

Capex 0.6130 1.0914 0.8148 -0.5936

(0.92) (1.13) (1.04) (-0.30)

Spread 0.9311 2.4078

(1.13) (1.26)

Price/Book -0.0063 0.0106 -0.0194 -0.0236

(-0.21) (0.25) (-0.58) (-0.29)

Constraint -0.1215 -0.3236 -0.0297 0.8518

(-0.41) (-0.86) (-0.09) (1.34)

ln(Age) -0.2430

(-1.50)

Take-up -157.9712

(-2.58)***

Industry Controls Yes Yes Yes Yes

Observations 555 309 432 107 Psuedo R-squared 0.0353 0.0552 0.0515 0.0704

35

Table 6: Changes in Monitoring and Insider Herfindahls Table 6 compares the mean changes in Monitoring and Insider Herfindahls around non-tradable rights issues conducted by ASX-listed Australian non-financial firms between 1997 and 2009, inclusive. Changes in both measures are calculated between years t-1 and t+1, with reference to the issue date, t=0. T-tests are used to ascertain whether the change in a given Herfindahl is significantly different from zero and whether there are significant differences between pairs of Herfindahl changes. T-statistics are given in parentheses, with *,**, and *** denoting their significance at the 10, 5 and 1 percent levels, respectively. In Panel A, the sample is partitioned based on underwriting type, underwritten versus non-underwritten. Panel B compares the difference between the change in Monitoring and Insider Herfindahls for the top and bottom quartiles of the sub-sample of non-underwritten non-tradable rights issues ranked by the level of the issuing firm’s pre-issue Monitoring Herfindahl. Panel A: Underwritten versus Non-Underwritten Issues

Underwriting Type Underwritten Non-underwritten Herfindahl N Mean Change N Mean Change Difference Monitor Herfindahl 338 0.0936*** 279 0.1975*** 0.1039*** Insider Herfindahl 338 0.2003*** 279 0.2125*** 0.0122 Panel B: High Versus Low Pre-Issue Monitor Ownership Concentration for Non-Underwritten Issues Pre-Issue Level Monitor Herfindahl Low High Herfindahl N Mean Change N Mean Change Difference Monitor Herfindahl 67 0.6572*** 68 -0.1981*** -0.8553*** Insider Herfindahl 67 -0.0018 68 0.4068*** 0.4086***

36

Table 7: High and Low Pre-Issue Monitor Herfindahls and Changes in Herfindahls Table 7 presents the results of a regression examining the relationship between the levels of pre-issue monitor concentration and changes in Monitoring and Insider Herfindahls around non-tradable rights issues conducted by ASX-listed Australian non-financial firms between 1997 and 2009, inclusive. We define ΔMonitor Herfindahl as the change in monitor ownership concentration for non-underwritten non-tradable issues between years t-1 and t+1 and ΔInside Herfindahl as the change in insider ownership concentration for non-underwritten non-tradable issues between years t-1 and t+1. High Monitor Herfindahl is an indicator variable equal to one if Monitor Herfindahl for a given firm is in the top quartile of the sample, and zero otherwise. Low Monitor Herfindahl is an indicator variable equal to one if Monitor Herfindahl for a given firm is in the bottom quartile of the sample, and zero otherwise. All other variables are as defined in Tables 3 and 4. Table 5 also reports the adjusted R2 and number of firm-year observations. T-statistics are given in parentheses, with *,**, and *** denoting significance at the 10, 5 and 1 percent levels, respectively.

Dependent variable: ΔMonitor Herfindahl ΔInside Herfindahl Independent variable

High Monitor Herfindahl -0.3735 0.2332

(-4.14)*** (2.00)** Low Monitor Herfindahl 0.4499 -0.2363

(4.54)*** (-2.01)** ln(Assets) -0.0788 0.0061

(-1.61) (0.11)

Cash 0.1153 -0.0367

(0.72) (-0.17)

Leverage 0.9270 -0.3773

(2.28)** (-0.94)

EBITDA 0.0522 -0.1421

(0.65) (-1.45)

Capex 0.5346 -0.3651

(1.85)* (-1.27)

Spread -0.4724 0.0245

(-1.67)* (0.08)

Price/Book -0.0057 0.0105

(-0.53) (0.55)

Constraint -0.1900 0.1369

(-1.63) (1.04)

Industry Controls Yes Yes

Observations 229 224 Psuedo R-squared 0.2589 0.1033

37

Table 8: Percentage Owned, Analyst Following, Business Cycle and Underwriting Type in Non-Tradable Rights Issues Table 8 regress a dichotomous measure of issue underwriting arrangements on alternative ownership measures, analyst following and business cycle, together with lagged firm-level characteristics. Number of Analysts is the number of analysts following the firm; Analyst Following is an indicator variable equal to one if the firm is followed by one or more analysts and zero otherwise; Business Cycle is an indicator variable equal to one if the economy is in an expansionary period and zero otherwise. All other variables are as defined in Tables 3 and 4. Table 8 also reports the adjusted R2 and number of firm-year observations. T-statistics are given in parentheses, with *,**, and *** denoting significance at the 10, 5 and 1 percent levels, respectively. Dependent Variable: Nonunderwritten

Independent variable (1) (2) (3)

(4)

(5) Monitor Herfindahl 1.4373 1.4252 1.3895 1.3103

(2.41)*** (2.39)*** (1.82)* (2.15)**

Monitor -0.7090 (-1.18) Insider Herfindahl 0.4074 0.4070 0.7274 0.3054

(0.88) (0.80) (1.22) (0.65)

Insider 1.1695 (1.29) Insider Control Margin 0.5586 0.5521 -0.0037 0.5609 (2.09)** (2.06)** (-0.01) (2.08)** ln(Assets) 0.0614 0.0608 0.0930 0.0584 0.1123

(0.66) (0.61) (0.60) (0.43) (1.12)

Cash -0.3983 -0.3927 -0.3872 0.0289 -0.2940

(-1.04) (-1.02) (-1.29) (0.05) (-0.75)

Leverage 0.5867 0.4917 0.5526 -0.1511 0.4374

(0.75) (0.62) (0.08) (-0.12) (0.53)

EBITDA -0.2726 -0.2605 -0.2864 -0.0832 -0.3080

(-1.40) (-1.33) (-1.16) (-0.31) (-1.55)

Capex 0.4626 0.6531 0.6651 0.8553 0.7121

(0.71) (0.98) (1.23) (0.93) (1.06)

Spread 0.9737 1.4169 1.8801

(1.19) (1.37) (2.11)**

Number of Analysts -0.1052 (-0.78) Analyst Following -0.4377 (-1.32) Price/Book -0.0101 -0.0089 -0.0085 0.0161 -0.0112

(-0.34) (-0.30) (-0.29) (0.40) (-0.37)

Constraint -0.0887 -0.1322 -0.1651 -0.2446 -0.2119 (-0.30) (-0.44) (-0.55) (-0.53) (-0.70) Business Cycle 0.7356 (3.41)***

Industry Controls Yes Yes Yes Yes Yes

Observations 555 551 551 401 555 Psuedo R-squared 0.027 0.034 0.035 0.046 0.051