p2 ch2 the modern business environment · p2 – advanced management accounting ch2 – the modern...

TRANSCRIPT

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 1

Chapter 2 The modern business environment Chapter learning objectives: Lead Component Indicative syllabus content

A.1 Evaluate techniques for analysing and managing costs for competitive advantage.

(b) Evaluate total quality management (TQM) techniques.

• The impacts of just-in-time (JIT) production, the theory of constraints and total quality management on efficiency, inventory and cost.

• The benefits of JIT production, total quality management and the theory of constraints, and the implications of these methods for decision making in the contemporary manufacturing environment.

• Kaizen costing, continuous improvement and cost of quality reporting.

• Process re-engineering and the elimination of non-value adding activities and reduction of activity costs.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 2

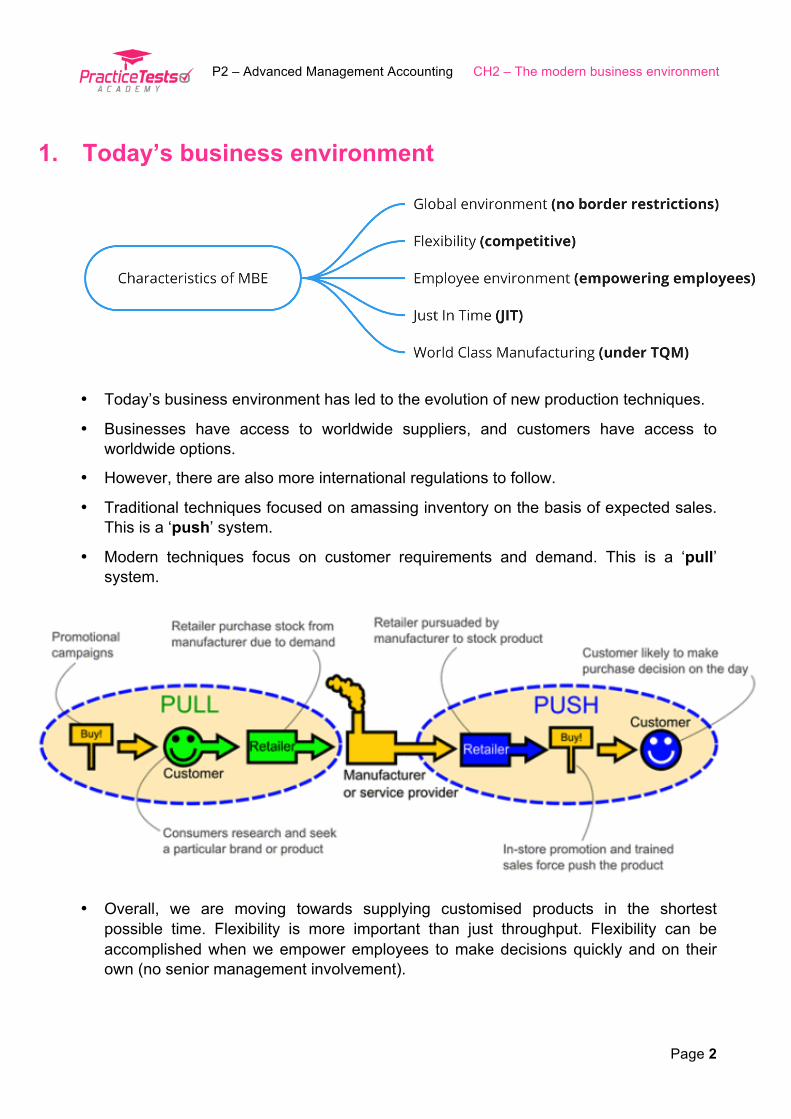

1. Today’s business environment

• Today’s business environment has led to the evolution of new production techniques.

• Businesses have access to worldwide suppliers, and customers have access to worldwide options.

• However, there are also more international regulations to follow.

• Traditional techniques focused on amassing inventory on the basis of expected sales. This is a ‘push’ system.

• Modern techniques focus on customer requirements and demand. This is a ‘pull’ system.

• Overall, we are moving towards supplying customised products in the shortest

possible time. Flexibility is more important than just throughput. Flexibility can be accomplished when we empower employees to make decisions quickly and on their own (no senior management involvement).

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 3

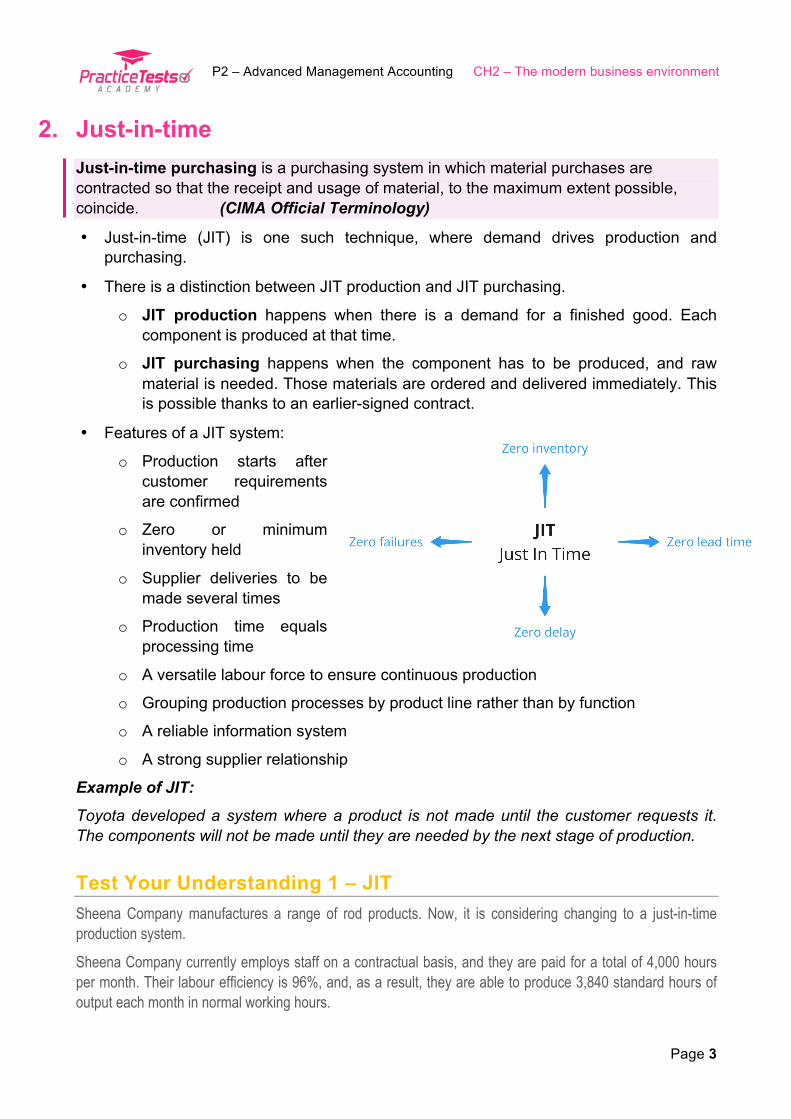

2. Just-in-time Just-in-time purchasing is a purchasing system in which material purchases are contracted so that the receipt and usage of material, to the maximum extent possible, coincide. (CIMA Official Terminology)

• Just-in-time (JIT) is one such technique, where demand drives production and purchasing.

• There is a distinction between JIT production and JIT purchasing.

o JIT production happens when there is a demand for a finished good. Each component is produced at that time.

o JIT purchasing happens when the component has to be produced, and raw material is needed. Those materials are ordered and delivered immediately. This is possible thanks to an earlier-signed contract.

• Features of a JIT system:

o Production starts after customer requirements are confirmed

o Zero or minimum inventory held

o Supplier deliveries to be made several times

o Production time equals processing time

o A versatile labour force to ensure continuous production

o Grouping production processes by product line rather than by function

o A reliable information system

o A strong supplier relationship

Example of JIT:

Toyota developed a system where a product is not made until the customer requests it. The components will not be made until they are needed by the next stage of production.

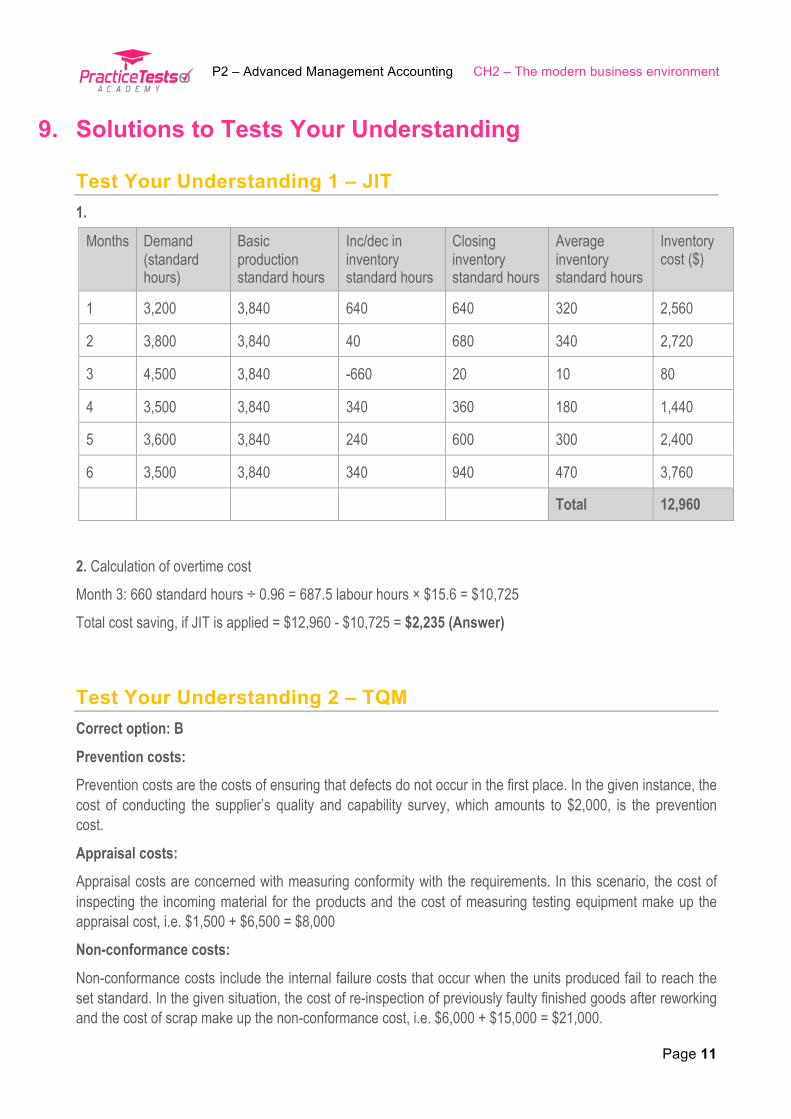

Test Your Understanding 1 – JIT Sheena Company manufactures a range of rod products. Now, it is considering changing to a just-in-time production system.

Sheena Company currently employs staff on a contractual basis, and they are paid for a total of 4,000 hours per month. Their labour efficiency is 96%, and, as a result, they are able to produce 3,840 standard hours of output each month in normal working hours.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 4

Overtime working is utilised to meet additional demand, though Sheena Company tries to avoid overtime hours. This is because the company pays for them at a 20% premium to the normal hourly rate of $12 per hour. Instead, Sheena Co plans production so that inventory levels increase in months of lower demand to enable sales demand to be met in other months.

Sheena has determined that the cost of holding inventory is $8 per month for each standard hour of output that is held in inventory. Assume that other costs (other than labour) are either fixed or not driven by labour hours and that there is no inventory at the start of Month 1 and at the end of Month 6. Assume that production and sales will occur evenly over the month and that the minimum contracted hours will remain the same with JIT.

Sheena has forecast the demand for its products for the six months as follows:

Months Demand (standard hours)

1 3,200

2 3,800

3 4,500

4 3,500

5 3,600

6 3,500

1. With the current production system, calculate the total inventory holding costs for each of the six months and the period in total.

2. Calculate the total production cost savings/expenditure made by changing to a JIT production

system.

3. Total quality management Total quality management (TQM) is ‘an integrated and comprehensive system of planning and controlling all business functions so that products or services are produced that meet or exceed customer expectations. TQM is a philosophy of business behaviour, embracing principles such as employee involvement, continuous improvement at all levels and customer focus, as well as being a collection of related techniques aimed at improving quality, such as full documentation of activities, clear goal setting and performance measurement from the customer perspective.’ (CIMA Official Terminology)

• Principles of total quality management (TQM):

o ‘Get it right the first time’: this aims to prevent the cost of rectifying. The focus is on 100% quality in the first go.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 5

o Continuous improvement: this principle holds that there is always room for improvement, so it aims for further improvement.

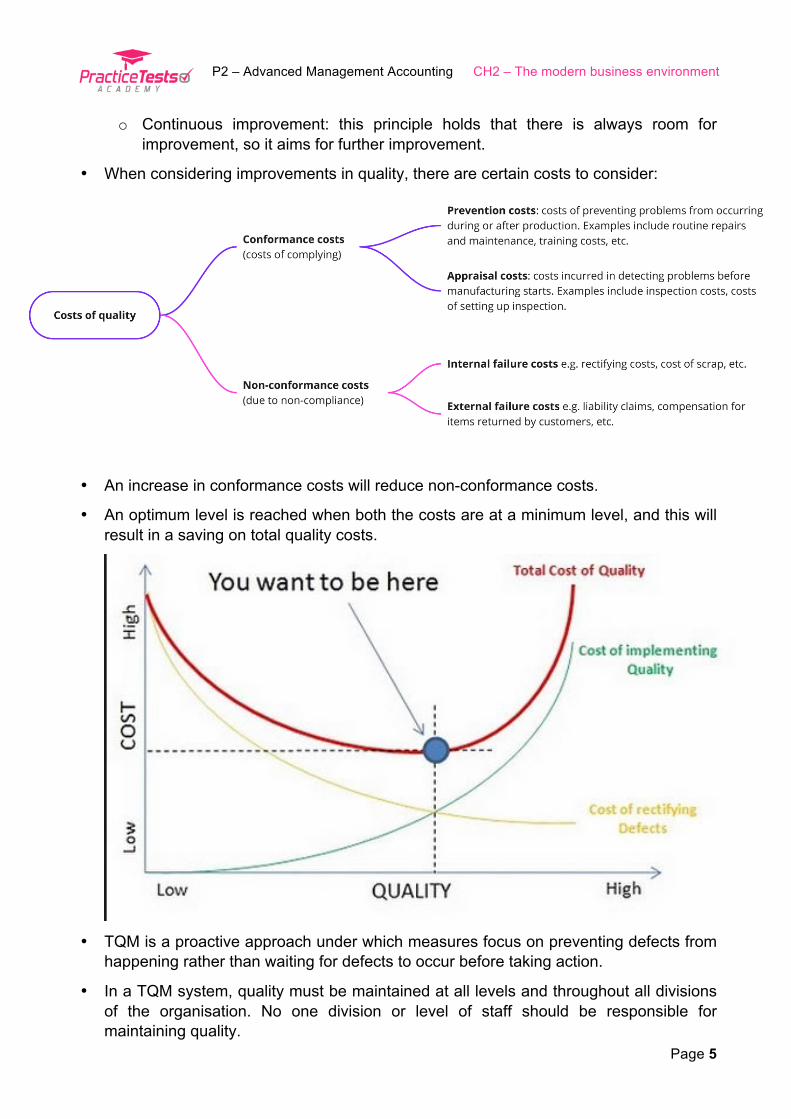

• When considering improvements in quality, there are certain costs to consider:

• An increase in conformance costs will reduce non-conformance costs.

• An optimum level is reached when both the costs are at a minimum level, and this will result in a saving on total quality costs.

• TQM is a proactive approach under which measures focus on preventing defects from

happening rather than waiting for defects to occur before taking action.

• In a TQM system, quality must be maintained at all levels and throughout all divisions of the organisation. No one division or level of staff should be responsible for maintaining quality.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 6

• Quality certification programmes and zero defect programmes should be implemented.

• It aims at understanding the customer requirements by getting closer to them and setting out the expected standards for the customers and employees.

Test Your Understanding 2 – TQM Macro Ltd is a manufacturing company. The management accountant has determined that its monthly costs are made up of the following:

$

Cost of re-inspection of previously faulty finished goods after reworking 6,000

Cost of inspecting the incoming material for the products 1,500

Cost of scrap 15,000

Cost of conducting the supplier’s quality and capability survey 2,000

Cost of measuring testing equipment 6,500

Which of the following options identifies Macro Ltd’s monthly prevention costs, appraisal costs and non-conformance costs?

Options Prevention costs ($) Appraisal costs ($) Non-conformance costs ($)

A 7,500 17,000 6,500

B 2,000 8,000 21,000

C 8,500 7,500 15,000

D 6,000 16,500 8,500

Communication of quality • Establish senior management commitment

• Present TQM

• Hold TQM workshops and training sessions

• Establish quality circles

• Establish standards by benchmarking

• Restructure reward systems

• Information systems to monitor and control

• Cultural change of attitudes and beliefs over the long term

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 7

Quality circles Quality Circles are where a small group of employees, normally working in the same area, volunteer to meet on a regular basis to identify areas for improvement or analyse work-related problems in order to find solutions.

Problems with implementing TQM in an organisation • Can be demotivating because one cannot achieve ‘perfection’

• Barriers to participation – not everyone can be involved

• Relies heavily on the quality of suppliers

• Change management – the culture of the organisation

4. Throughput accounting and TOC • The theory of constraints (TOC) is a production system where the key financial

concept is the maximisation of throughput while keeping conversion and investment costs to a minimum.

• The 5 stages of TOC: identify the constraint => exploit it => subordinate other activities => elevate the constraint => repeat the process.

• Throughput = Sales Revenue less Direct Material Cost

• The aim of throughput accounting is to increase throughput while keeping operational expenses and inventory at a minimum.

• This is achieved by determining the constraints that prevent the maximisation of throughput.

• If bottleneck resources cannot be removed, full utilisation should be ensured.

• Other resources should be operated according to the bottleneck resource to avoid excessive inventory accumulation.

• Formulae for throughput accounting:

o Total factory costs (TFC) = all costs except direct material cost

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 8

o Return per factory hour = !!!"#$!!"#! !"# !"#$!"#$%&' !"#$ !" !!! !"##$%&%'( !"#$!%"

o Cost per factory hour = !"!#$ !"#$%&' !"#$# !"!#$ !"#$ !" !!! !"##$%&%'( !"#$%!&"

o Throughput accounting ratio = !"#$!% !"# !"#$%&' !!"#!"#$ !"# !"#$%&' !!"#

o The focus is on maximising the throughput accounting ratio.

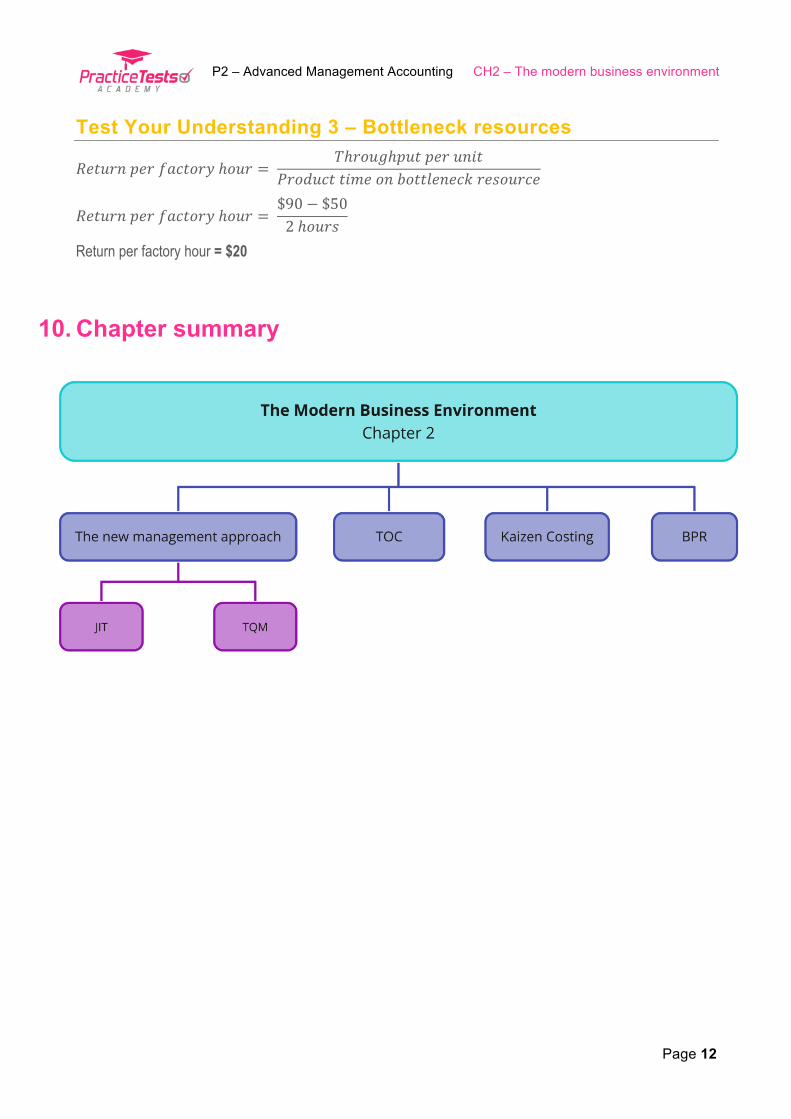

Test Your Understanding 3 – Bottleneck resources Korea Inc manufactures a product requiring 2 hours of machining. Machine time is the bottleneck resource due to the availability of a limited number of machines. The company has 15 machines available, and each machine can be used for up to 40 hours.

The product is sold for $90 per unit, and the direct material cost per unit is $50 per unit. The factory costs are $10,000 per week.

Please calculate the return per factory hour.

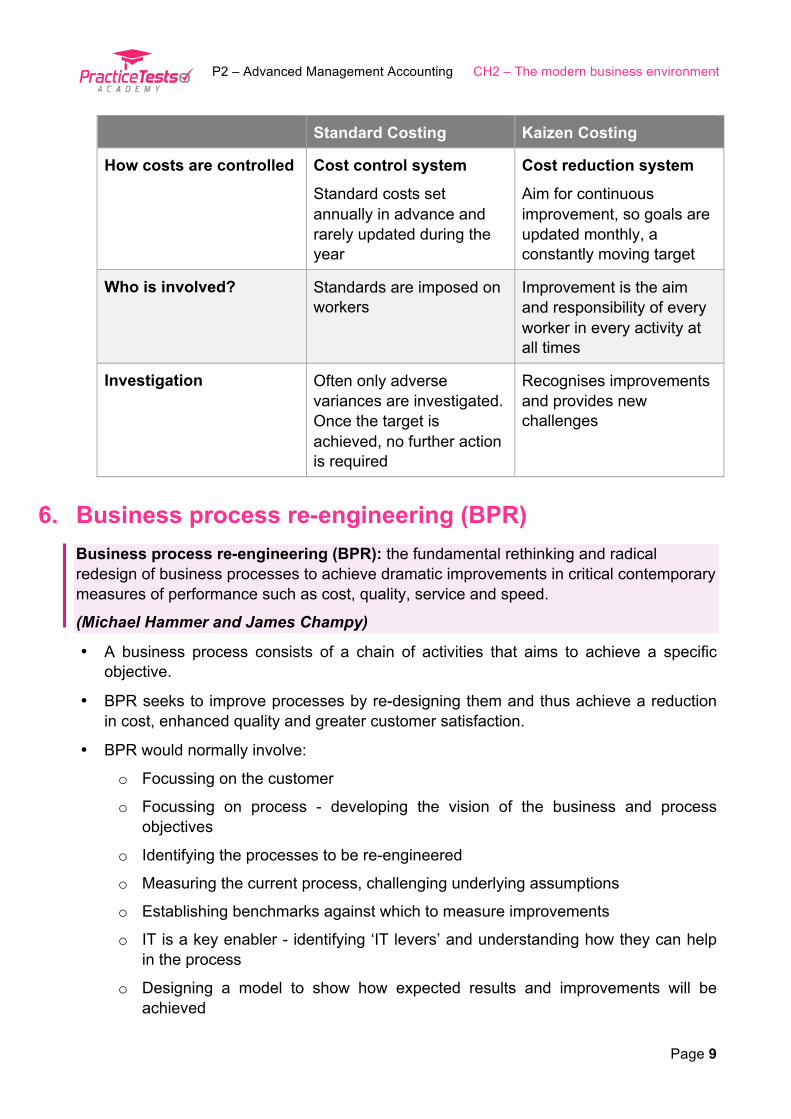

5. Kaizen costing • ‘Kaizen’ is a Japanese term meaning continuous improvement in small incremental

amounts rather than large radical improvements.

• Kaizen costing is used during the manufacturing process.

• The focus will be on reducing the variable costs during the manufacturing phase.

• During the design phase of a product, a target product cost is established.

• Constant reduction in cost is sought during the production of the product.

• The whole workforce should be involved in suggesting improvements.

• Cost reduction targets will be set more frequently and implemented more frequently than with standard costing, usually on a monthly basis.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 9

Standard Costing Kaizen Costing

How costs are controlled Cost control system

Standard costs set annually in advance and rarely updated during the year

Cost reduction system

Aim for continuous improvement, so goals are updated monthly, a constantly moving target

Who is involved? Standards are imposed on workers

Improvement is the aim and responsibility of every worker in every activity at all times

Investigation Often only adverse variances are investigated. Once the target is achieved, no further action is required

Recognises improvements and provides new challenges

6. Business process re-engineering (BPR) Business process re-engineering (BPR): the fundamental rethinking and radical redesign of business processes to achieve dramatic improvements in critical contemporary measures of performance such as cost, quality, service and speed.

(Michael Hammer and James Champy)

• A business process consists of a chain of activities that aims to achieve a specific objective.

• BPR seeks to improve processes by re-designing them and thus achieve a reduction in cost, enhanced quality and greater customer satisfaction.

• BPR would normally involve:

o Focussing on the customer

o Focussing on process - developing the vision of the business and process objectives

o Identifying the processes to be re-engineered

o Measuring the current process, challenging underlying assumptions

o Establishing benchmarks against which to measure improvements

o IT is a key enabler - identifying ‘IT levers’ and understanding how they can help in the process

o Designing a model to show how expected results and improvements will be achieved

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 10

7. Supply chain management • The supply chain is the chain of suppliers and customers that a business deals with. It

consists of all the activities conducted along that chain, starting from the acquisition of raw material up to the eventual consumption of the product or service by the consumer.

• The globalisation of businesses has seen supply chains become longer and increasingly complex.

• A strengthened supply chain will eventually benefit each and every member of the supply chain, and IT can play a very important role in achieving this.

• Areas of supply chain management where IT is becoming vital:

o Purchasing: implementing and linking information systems with those of the suppliers can improve the working relationship with them. It will help reduce costs and increase efficiency.

o Inventory management: information systems can help the business maintain customer records and stay up-to-date with customer information and thus control inventory efficiently. This will help keep inventory levels low.

o Customer orders: a flexible and efficient order processing system will lead to return customers. Online ordering has become quite desirable among customers due to technological enhancement, making such enhancements important for businesses.

o Delivery and logistics: the last node in the supply chain is delivery to the customer. Information technology has introduced tracking systems so that orders can be tracked from manufacturing to final delivery to the customer.

• Outsourcing: organisations have started depending more on outsourcing so that they can focus on their core competencies. A lot of the functions such as sales, design, IT and distribution are usually outsourced to firms that specialise in these areas.

8. Gainsharing arrangements • A gainsharing arrangement returns cost savings to employees.

• In a gainsharing arrangement, the company will guarantee to its customers that they will attain a particular amount of cost saving.

• There is a commitment by the company that it will make up for the difference in cash if the targets are not met.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 11

9. Solutions to Tests Your Understanding

Test Your Understanding 1 – JIT 1.

Months Demand (standard hours)

Basic production standard hours

Inc/dec in inventory standard hours

Closing inventory standard hours

Average inventory standard hours

Inventory cost ($)

1 3,200 3,840 640 640 320 2,560

2 3,800 3,840 40 680 340 2,720

3 4,500 3,840 -660 20 10 80

4 3,500 3,840 340 360 180 1,440

5 3,600 3,840 240 600 300 2,400

6 3,500 3,840 340 940 470 3,760

Total 12,960

2. Calculation of overtime cost

Month 3: 660 standard hours ÷ 0.96 = 687.5 labour hours × $15.6 = $10,725

Total cost saving, if JIT is applied = $12,960 - $10,725 = $2,235 (Answer)

Test Your Understanding 2 – TQM Correct option: B

Prevention costs: Prevention costs are the costs of ensuring that defects do not occur in the first place. In the given instance, the cost of conducting the supplier’s quality and capability survey, which amounts to $2,000, is the prevention cost.

Appraisal costs: Appraisal costs are concerned with measuring conformity with the requirements. In this scenario, the cost of inspecting the incoming material for the products and the cost of measuring testing equipment make up the appraisal cost, i.e. $1,500 + $6,500 = $8,000

Non-conformance costs:

Non-conformance costs include the internal failure costs that occur when the units produced fail to reach the set standard. In the given situation, the cost of re-inspection of previously faulty finished goods after reworking and the cost of scrap make up the non-conformance cost, i.e. $6,000 + $15,000 = $21,000.

P2 – Advanced Management Accounting CH2 – The modern business environment

Page 12

Test Your Understanding 3 – Bottleneck resources

𝑅𝑒𝑡𝑢𝑟𝑛 𝑝𝑒𝑟 𝑓𝑎𝑐𝑡𝑜𝑟𝑦 ℎ𝑜𝑢𝑟 = 𝑇ℎ𝑟𝑜𝑢𝑔ℎ𝑝𝑢𝑡 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡

𝑃𝑟𝑜𝑑𝑢𝑐𝑡 𝑡𝑖𝑚𝑒 𝑜𝑛 𝑏𝑜𝑡𝑡𝑙𝑒𝑛𝑒𝑐𝑘 𝑟𝑒𝑠𝑜𝑢𝑟𝑐𝑒

𝑅𝑒𝑡𝑢𝑟𝑛 𝑝𝑒𝑟 𝑓𝑎𝑐𝑡𝑜𝑟𝑦 ℎ𝑜𝑢𝑟 = $90− $502 ℎ𝑜𝑢𝑟𝑠

Return per factory hour = $20

10. Chapter summary