p4 - interim

TRANSCRIPT

Interim Assessment

KAPLAN PUBLISHING Page 1 of 8

ACCA INTERIM ASSESSMENT

Advanced Financial

Management

JUNE 2009

QUESTION PAPER

Do not open this paper until instructed by the supervisor This question paper must not be removed from the examination hall

Time allowed Reading time: 15 minutes Writing time: 3 hours Section A: Answer BOTH questions Section B: Answer TWO questions only

Kaplan Publishing/Kaplan Financial

ACCA P4 Advanced Financial Management

© Kaplan Financial Limited, 2008 All rights reserved. No part of this examination may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without prior permission from Kaplan Publishing.

Page 2 of 8 KAPLAN PUBLISHING

Interim Assessment

SECTION A

Answer BOTH questions QUESTION 1 Larkin Motors plc (“LM”) is a long-established listed company. Its main business is the retailing of new and used motor cars and the provision of after-sales service. It has sales outlets in most of the major towns and cities in the UK. It also owns a substantial amount of land and property that it has acquired over the years, much of which it rents or leases on medium-long term agreements. Approximately 80% of its non-current asset value is land and buildings. The company has grown organically for the last few years but is now considering expanding by acquisition. The Chief Executive is not in favour of hostile bids as he believes the bidder always pays too much to acquire the target. Any acquisition that LM makes will therefore need to be an agreed bid. Brass Vehicles Limited (“BV”) owns a number of car showrooms in wealthy, semi-rural locations in the North of England. All of these showrooms operate the franchise of a well-known major motor company. BV is a long-established private company with the majority of shares owned by the founding family, many of whom still work for the company. The major shareholders are now considering selling the business if a suitable price can be agreed. The Managing Director of BV, who is a major shareholder, has approached LM to see if it would be interested in buying BV. He has implied that holders of up to 50% of BV’s shares might be willing to accept LM shares as part of the deal. The forecast earnings of LM for the next financial year are £35 million. According to the Managing Director of BV, his company’s earnings are expected to be £4 million for the next financial year. Financial statistics and other information on LM and BV are shown below:

LM BV

Shares in issue (millions) 25 1.5

Earnings per share (pence) 112.5 153

Dividend per share (pence) 50.6 100

Share price (pence) 1,237 n/a

Net asset value attributable to equity (£m) 350 45

Debt ratio 20 0

(outstanding debt as percentage of total market value of company)

Forecast growth rate percentage (constant, annualised) 4 5

Cost of equity 9% n/a BV does not calculate a cost of equity, but the industry average for similar companies is 10%.

KAPLAN PUBLISHING Page 3 of 8

ACCA P4 Advanced Financial Management

Required: Assume you are a financial manager working with LM. Advise the LM Board on the following issues in connection with a possible bid for BV: (a) methods of valuation that might be appropriate and a range of valuations for BV

within which LM should be prepared to negotiate. (12 marks) (b) the financial factors relating to both companies that might affect the bid. (6 marks) (c) the most appropriate form of funding the bid and the likely financial effects on LM. (6 marks) (d) the advantages and disadvantages of growth by agreed acquisition as compared with

organic growth. (6 marks) Note: A report format is NOT required for this question. (Total: 30 marks) QUESTION 2 Shelley Transport Ltd (“ST”) is a private transport and distribution business. It is considering three new investment projects, which are not mutually exclusive. ST has no cash reserves, but could borrow a maximum of £30 million at the present time at a gross interest rate of 10%. Borrowing above this amount might be possible, but at a much higher rate of interest. The initial capital investment required, the NPV and the duration of each project is as follows:

Initial NPV Duration Investment £million Years £million (after tax) Project A 15.4 2.75 6 Project B 19.0 3.60 7 Project C 12.8 3.25 Indefinite

Notes: 1 ST pays corporation tax at 30%. 2 Apart from the initial investment, assume that cash flows arise evenly throughout the

duration of the investments. 3 The projects are not divisible and cannot be postponed. 4 The discount rate considered appropriate for all three investments is 12% net of tax.

Page 4 of 8 KAPLAN PUBLISHING

Interim Assessment

Required: (a) (i) Calculate the profitability index and equivalent annual annuities for all three

projects. Explain the usefulness of these methods of evaluation in the circumstances here, and recommend which project(s) should be undertaken.

(12 marks) (ii) Explain the differences between ‘hard’ and ‘soft’ capital rationing and explain

which type is evident in the scenario here. Discuss, briefly, the advisability of the directors of ST limiting their capital expenditure in this way. (5 marks)

(iii) You later discover that the discount rate used was nominal, but the cash

flows have been calculated in real terms. Explain, without doing any calculations, how the calculation for NPV should

be adjusted and what effect the changes might have on your recommendation. (5 marks)

(b) Assume that Project B, and B only, could attract Government support as follows:

• a non-repayable grant of £3.5 million payable as soon as the project commenced; plus

• subsidised bank lending of 50% of the initial investment (after the government grant), secured on the non-current assets that would be acquired for this project. The capital amount of the debt would be repayable in eight years’ time. Interest (before tax) is at the rate of 8% per annum and will be paid in equal instalments annually at the end of each year.

Discuss, with supporting calculations, whether this new information would change

your recommendation using an APV approach incorporating the NPV in the scenario as the ‘base case’. (8 marks)

(Total: 30 marks)

KAPLAN PUBLISHING Page 5 of 8

ACCA P4 Advanced Financial Management

SECTION B

Answer TWO questions only QUESTION 3 The following are extracts from the corporate governance guidelines issued by a UK plc: (i) All auditors’ fees, including fees for services other than audit, should be fully

disclosed in the annual report. In order to ensure continuity of standards the same audit partner, wherever possible, should be responsible for a period of at least three years.

(ii) The board shall establish a remuneration committee comprising 50% executive

directors, and 50% non-executive directors. A non-executive director shall chair the committee.

(iii) The chairman of the company may also hold the position of chief executive, although

this shall not normally be for a period of more than three years. (iv) The annual report shall fully disclose whether principles of good corporate

governance have been applied. (v) No director shall hold directorships in more than 20 companies. (vi) Directors should regularly report on the effectiveness of the company’s system of

internal control. Required: (a) Discuss the extent to which each of points (i) – (vi) is likely to comply with corporate

governance systems such as the UK Combined Code. (10 marks) (b) Prepare a brief report advising senior managers of your company who are going to

work in subsidiaries in Germany, Japan and the USA of the main differences in corporate governance between the UK and any TWO of the above countries, and possible implications of the differences for the managers. (10 marks)

(Total: 20 marks)

Page 6 of 8 KAPLAN PUBLISHING

Interim Assessment

QUESTION 4 (a) Briefly discuss the meaning and importance of the term ‘delta’ in option pricing. (3 marks) (b) Bioplasm Inc is a pharmaceuticals company that has completed the preliminary

development of a new drug to combat a major disease. Initial clinical trials of the drug have been favourable, and the drug is expected to receive approval from the regulatory authority in the near future.

Bioplasm has taken out a patent on the drug that gives it the exclusive right to commercially develop and market the drug for a period of 15 years. Although it is difficult to produce precise estimates, the company believes that to commercially develop and market the drug for worldwide use will cost approximately $400 million at current prices. The expected present value from sales of the drug during the patent period could vary between $350 million and $500 million. The current long-term government bond yield is 5%. The annual variance (standard deviation squared) of returns on similar biotech companies is estimated to be 0.185. The finance director of Bioplasm can see from the possible NPVs that the company has a difficult decision as to whether or not to develop the drug, and wonders if real option pricing could assist the decision.

Required: Using the Black-Scholes option pricing model for the life of the patent, estimate the call values of the option to commercially develop and market the drug. Provide a reasoned recommendation, based upon your calculations and any other relevant information, as to whether or not Bioplasm should develop the drug. Note: Since the value of the returns from the patent will fall over the period before the drug is commercially developed, it is necessary to adjust the expected present value from sales of the drug. In all relevant parts of the Black-Scholes model, the present value from sales of the drug should be multiplied by exp (–0.067)(15) to reflect this potential reduction in value according to when the drug is developed. (17 marks) (Total: 20 marks)

KAPLAN PUBLISHING Page 7 of 8

ACCA P4 Advanced Financial Management

QUESTION 5 (a) Arshavin plc has made a takeover bid for Berbatov plc. Arshavin plc’s share price has

been performing well in recent months as the market believes its managing director, Mr Khan, has the ability to dramatically improve the company’s earnings. The acquisition of Berbatov plc, an erratic performer in recent years, seems to be a sensible move in commercial terms. However, the market does not react to the terms of the bid as Mr Khan expected and he finds Arshavin plc’s share price falls.

A summary of the financial data before the bid is as follows:

Arshavin plc Berbatov plc

Number of shares in issue 5 million 15 million Earnings available to ordinary shareholders £2.5 million £7.5 million P/E ratio 12.5 7.5

Mr Khan’s estimated financial data post-acquisition:

Estimated market capitalisation £125 million Estimated share price £8.33 Estimated EPS £0.67 Estimated equivalent value of one old Berbatov plc share £5.55

The offer is 10 Arshavin plc shares for 15 shares in Berbatov plc. At the time of the bid announcement, no information is related other than the bid terms and the comment by Mr Khan that he hopes to ‘turn Berbatov round’. The expected rate of return on Arshavin plc’s equity capital is 15% per annum constant.

Required:

(i) Suggest how Mr Khan might have calculated the post-acquisition data.

(ii) Write a short report suggesting a probable post-acquisition share price and advising shareholders in both Arshavin plc and Berbatov plc on whether the bid should proceed.

(14 marks)

(b) It is later announced that the proposed merger is expected to result in immediate administrative savings of £5 million. Sales of redundant assets by the end of the first year are expected to realise £10 million. Net income is expected to increase by £7.5 million per annum for the foreseeable future as a result of a more aggressive marketing policy for Berbatov plc’s business.

Note: You should assume all figures are net of tax. Required:

Explain how this new information would affect your estimation of a probable post-acquisition share price, and comment on how it might affect Berbatov plc’s bargaining position. (6 marks) (Total: 20 marks)

Page 8 of 8 KAPLAN PUBLISHING

Interim Assessment

ACCA

Paper P4

Advanced Financial Management June 2009

Interim Assessment – Answers

To gain maximum benefit, do not refer to these answers until you have completed the interim assessment questions and submitted them for marking.

KAPLAN PUBLISHING Page 1 of 19

ACCA P4 Advanced Financial Management

© Kaplan Financial Limited, 2008 All rights reserved. No part of this examination may be reproduced or transmitted in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without prior permission from Kaplan Publishing.

Page 2 of 19 KAPLAN PUBLISHING

Interim Assessment

ANSWER 1 (a) Valuations for BV Three possible methods of valuation that could be used to value the shares of BV

are:

• net assets basis • dividend basis • earnings basis. Net assets attributable to equity of BV = £45m Number of shares in issue = 1.5m ∴Net asset value per share = £30 Usually, the net assets value method of valuing a company is not very useful since a conventional balance sheet is drawn up using costs (not market values) and excludes many valuable assets (e.g. trained employees, business know-how, etc). However in the case of BV we have a company with a number of owned car showrooms and a valuable franchise. If the showrooms are measured on the balance sheet at their open market value, and if the franchise is included on the balance sheet at cost or fair value, then it is possible that the company’s net asset value will be relevant to LM. The dividend valuation model states that:

Company value = rate growth Annualequity of Cost

total dividend s year'Next−

= 0.050.1

1.05£11.5m−

××

= £31.5m There are a number of points that should be made concerning this valuation: • We have assumed that next year’s dividend will be this year’s dividend (£1

per share) increased by the general forecast growth rate. However, given that earnings are expected to almost double next year (from 1.5m × £1.53 = £2.3m, up to £4m), this estimate of next year’s dividend may be too modest.

• We have assumed a cost of equity of 10%, since this is the industry average for similar companies. Clearly we need to assess whether BV is anything like an ‘average’ company before we can use this figure.

• We have assumed that dividends will grow each year in the future at an annual rate equal to the 5% forecast growth rate for the company as a whole. Dividend policy is a matter for the directors of the company to decide, but in the long run this 5% rate may be reasonable. If LM acquires the company, it will be able to control the dividend policy directly.

KAPLAN PUBLISHING Page 3 of 19

ACCA P4 Advanced Financial Management

The earnings valuation for a company is given by: Company value = Earnings × Appropriate P/E ratio

= £4m × 112.51,237 = £44m

In this valuation, next year’s earnings (as forecast by the Managing Director of BV) have been used. The MD has an interest in being optimistic and overstating the forecast earnings figure. The alternative would be to use this year’s earnings figure of 1.5m × £1.53 = £2.3m, which would produce a much lower valuation. There is no P/E ratio for BV, since it is a private company. We have used the only P/E ratio provided in the question, that for LM.

P/E ratio = 112.5p1,237p

EPSprice Share

= = 11

It would be possible to adjust this P/E ratio arbitrarily either up or down to reflect the different characteristics of LM (a large public company with plenty of land and property) and BV (a smaller private company with good growth prospects), but since this adjustment could be either up or down, the simple decision has been taken to leave it unchanged. Conclusion The following valuations for BV have been produced:

£m Net assets basis 45 Dividend valuation model 31.5 Earnings basis (using current earnings) £2.3 × 11 = 25.3 Earnings basis (using forecast earnings) £4.0 × 11 = 44.0

LM should be prepared to negotiate within the range of £40m to, say, £48m. There seems little prospect of the shareholders of BV selling for less than the £45m net asset value, but perhaps some assets are overstated in the balance sheet.

(b) Financial factors affecting the bid

It is unusual for the net assets basis of valuing a company to exceed the dividend basis and the earnings basis. There are many estimates used in the latter two bases, so perhaps they are inaccurate in this example. As stated in part (i), it would be unlikely that the shareholders of BV would agree to sell their shares for less than the net assets basis, so in this example we can forget the dividend basis and the earnings basis. It is the Managing Director of BV who has approached LM, so the balance of power is such that LM can decide at its leisure whether to bid. LM has a market capitalisation of 25m × £12.37 = £309.25m. It is being asked to bid for a much smaller company,

Page 4 of 19 KAPLAN PUBLISHING

Interim Assessment

worth around £45m, in wealthy locations in the north of England. LM appears to be a volume player in the motor car market, with no apparent experience of semi-rural showrooms. Given LM’s lack of experience, perhaps it should not bother to bid for this much smaller company, or certainly it should not pay an excessive premium over net asset value. Curiously, we see that LM’s net asset value (£350m) also exceeds its market valuation (£309.25m). It is possible that the motor car business is unfavourably valued by the market. It is also possible that the market has overlooked the high asset backing to LM’s shares. It is possible that, if it launches a bid for BV and becomes better known in the market as a result of the accompanying publicity, then LM itself could become a target for takeover bids. What other investment opportunities are available for the £45m (or so) expected to be invested in the acquisition? Do all the BV shareholders want to sell their shares, or will there be a significant minority interest that will want to hold on? LM might not want to acquire a company if less than 100% of the shares can be acquired.

(c) The form of funding the bid

We are looking to finance an acquisition costing in the region of £45m, and must decide whether to offer shares or cash as the consideration. The Managing Director of BV has indicated that holders of up to 50% of BV’s shares might accept shares. LM’s current debt ratio is 20%, thus:

£309.25m debt sLM'debt sLM'+

= 0.2

∴ LM’s current debt = 0.8

£61.85 = £77.3m

The most new gearing possible would be if all the BV shareholders were paid in cash, raised from new borrowings. Thus £45m of fresh debt would be issued.

LM’s new debt ratio = 309.254577.34577.3

+++ = 28%

This does not seem excessive for a large company such as LM, especially considering the excellent asset backing available to secure issues of debt. On the other hand, a new equity issue would reduce the debt ratio, but this is not a pressing priority. In practice, some combination of shares and cash is likely to be negotiated, depending on the requirements and tax positions of individual BV shareholders.

KAPLAN PUBLISHING Page 5 of 19

ACCA P4 Advanced Financial Management

(d) Features of growth by acquisition versus organic growth

The advantages of growth by acquisition are: • much quicker method of increasing market share than growing organically • since the two companies will not have perfectly correlated cash flows,

combining them together will offer diversification opportunity and a reduction in the cost of capital. This should increase the value of the group and therefore increase shareholder wealth

• buying out one’s competitors reduces the competition faced in the market, thereby strengthening one’s price-setting ability.

The disadvantages of growth by acquisition are: • it is usually more expensive for the purchasing company. Research

continually shows that in contested acquisitions it is the shareholders of the target company who gain the greatest share of the benefits arising

• many acquisitions are planned in anticipation of generating synergistic cost savings, but in practice these synergies often fail to appear after the acquisition

• there may be cultural clashes following the acquisition between the two sets of employees. If the skilled employees of the acquiree become demotivated and leave, then much of the skill set that was paid for in the acquisition has been lost.

MARKING SCHEME

Marks

(a) Asset based valuation – calculation 1 – comment 1

Dividend valuation – calculation 2 – comment 3

Earnings valuation – calculation 2 – comment 3

Recommendations – range for negotiation 2 Max 12 (b) One mark per valid point Max 6 (c) One mark per valid point Max 6 (d) One mark per valid point Max 6 Total 30 ______

Page 6 of 19 KAPLAN PUBLISHING

Interim Assessment

ANSWER 2 Key answer tips At first glance this is a straightforward question looking at three investment appraisal techniques – profitability index, equivalent annuities and adjusted present value. The difficulty here lies in mixing the techniques in the same question and using some out of their normal context. You will have used equivalent annual costs to assess asset replacement cycles but may not have considered whether the technique is relevant to a capital rationing situation. (a) (i) Profitability indices

A B C

NPV 2.75 3.60 3.25

Initial investment 15.4 19.0 12.8

Profitability index (PI) = NPV / £ invested

17.86% 18.95% 25.39%

Ranking 3rd 2nd 1st

The correct approach for resolving a problem of capital rationing depends on

whether or projects are mutually exclusive and whether they are divisible. In this scenario we are told that they are not mutually exclusive so

combinations are possible. Furthermore we are told that projects are not divisible so there is little point in looking at a profitability index, which details the benefit to the company of each £1 invested. The profitability index would be useful if it were possible to do, say, A and 60% of B.

That is not the case here. Equivalent annuities

A B C

NPV 2.75 3.60 3.25

Annuity discount factor @12% 4.111 4.564 1/0.12

Equivalent annual cash flow 0.669 0.789 0.390

Ranking 2nd 1st 3rd

Equivalent annuities are useful for comparing projects of different duration when those investments are likely to be repeated – for example in the case of asset replacement when replacement cycles of differing lengths can be compared. There is no indication here that projects can be repeated into perpetuity so equivalent annuities are of little use when the objective is to maximise shareholder wealth. Recommendations Assuming the objective is to maximise shareholder wealth, then projects should be assessed by looking at the combination that gives the greatest NPV. With £30 million available, ST could undertake one of four possible portfolios:

KAPLAN PUBLISHING Page 7 of 19

ACCA P4 Advanced Financial Management

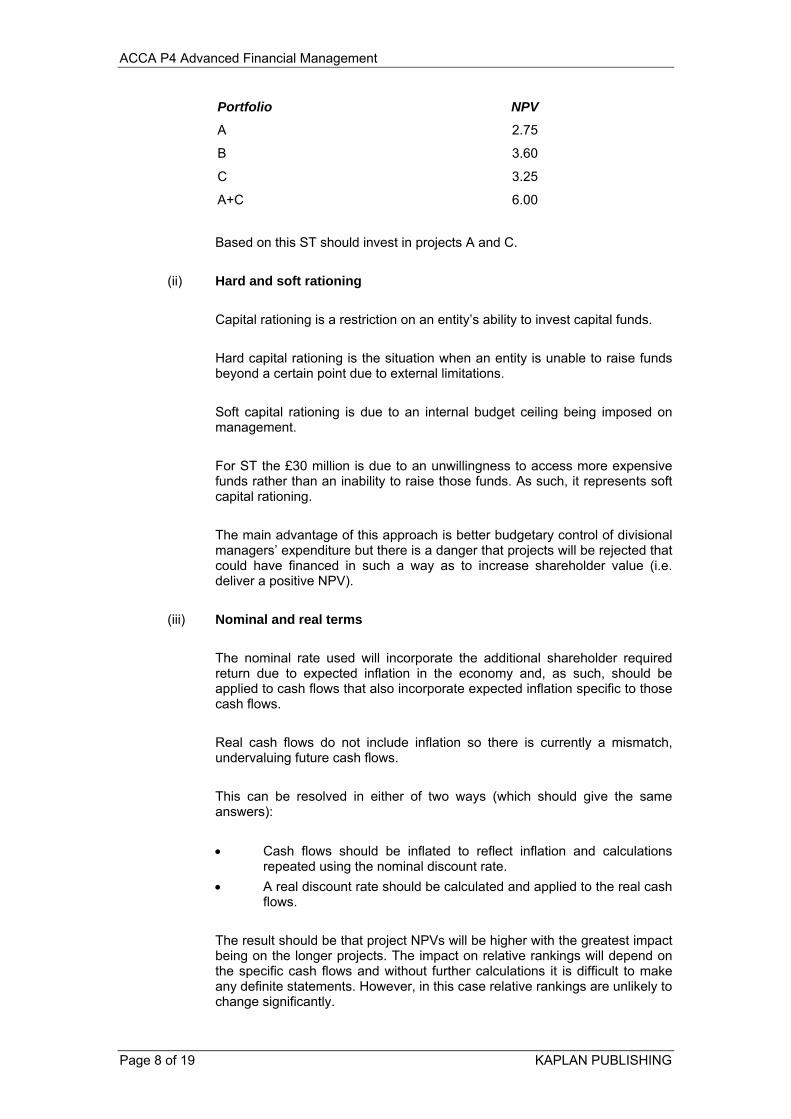

Portfolio NPV

A 2.75

B 3.60

C 3.25

A+C 6.00

Based on this ST should invest in projects A and C.

(ii) Hard and soft rationing Capital rationing is a restriction on an entity’s ability to invest capital funds. Hard capital rationing is the situation when an entity is unable to raise funds

beyond a certain point due to external limitations. Soft capital rationing is due to an internal budget ceiling being imposed on

management. For ST the £30 million is due to an unwillingness to access more expensive

funds rather than an inability to raise those funds. As such, it represents soft capital rationing.

The main advantage of this approach is better budgetary control of divisional

managers’ expenditure but there is a danger that projects will be rejected that could have financed in such a way as to increase shareholder value (i.e. deliver a positive NPV).

(iii) Nominal and real terms The nominal rate used will incorporate the additional shareholder required

return due to expected inflation in the economy and, as such, should be applied to cash flows that also incorporate expected inflation specific to those cash flows.

Real cash flows do not include inflation so there is currently a mismatch,

undervaluing future cash flows. This can be resolved in either of two ways (which should give the same

answers):

• Cash flows should be inflated to reflect inflation and calculations repeated using the nominal discount rate.

• A real discount rate should be calculated and applied to the real cash flows.

The result should be that project NPVs will be higher with the greatest impact

being on the longer projects. The impact on relative rankings will depend on the specific cash flows and without further calculations it is difficult to make any definite statements. However, in this case relative rankings are unlikely to change significantly.

Page 8 of 19 KAPLAN PUBLISHING

Interim Assessment

(b) APV for project B

• Base case NPV = £3.60 million • Present value of financing side-effects

1 Grant: benefit = £3.5 million 2 Subsidised loan. Amount borrowed = 50% × (19.0 – 3.5) = £7.75

million

Narrative CF £

Tax relief on interest (7.75m×8%×30%) 186,000

Interest saved (7.75m×2%) 155,000

Tax relief on interest foregone (7.75m×2%×30%) (46,500)

Net annual benefit 294,500

Annuity discount factor – years 1-8 at 10% 5.335

Overall PV of financing side effects 1,571,158

• APV = 3.60 + 3.50 + 1.57 = £8.67 million • This now makes B worth more than the combination of A and C, so the

decision would change to invest in B instead. • However, this process could be repeated for A and C if project-specific

finance can be found for them that has additional benefits. If this is the case, then the decision may reverse again.

MARKING SCHEME

Marks

(a)(i) Profitability indices 3 Equivalent annual annuities 3 Usefulness of methods 4 Recommendations 2 Max 12 (a)(ii) One mark per valid point Max 5 (a)(iii) One mark per valid point Max 5 (b) Amount of loan 1 Tax relief on interest 1

Interest saved 2

Tax relief on interest foregone 2

APV and comment 2

Max 8

Total 30 ______

KAPLAN PUBLISHING Page 9 of 19

ACCA P4 Advanced Financial Management

ANSWER 3 Tutorial note: The suggested answer focuses on the UK Combined Code, as amended in 2003. However, the question does not specifically ask about corporate governance in the UK, and a well-prepared answer can refer to the governance rules in any other country. The examiner commented that answers which included comments on how points (i) to (vi) might comply with other corporate governance systems were equally acceptable. (a) Many aspects of the extracts in the question would not comply with corporate

governance systems such as the UK Combined Code guidelines.

(i) Audit fees and auditor independence. In the UK, it is a requirement of company law that all audit fees and fees for other services provided by auditors should be fully disclosed. Non-audit fees include fees for tax advice, management consultancy and general accountancy services.

It has been argued that the partner(s) responsible for the audit should be regularly changed so that the audit is perceived to be more objective, and there is less chance of missing important anomalies in the audit process. However, there are no provisions about audit partner rotation in the Combined Code. It should be the responsibility of the audit committee to ensure the independence of the auditors, and to review the appointment/re-appointment and make suitable recommendations to the full board.

(ii) The UK Combined Code states that the remuneration committee should consist of at least three (or two, in the case of smaller companies) members, and these should all be independent non-executive directors. The committee should objectively determine the remuneration and individual packages for each executive director and also the chairman and 'senior management' (but consult with the chairman and/or CEO about the remuneration of the other executive directors).

(iii) The UK Combined Code states that the roles of chairman and chief executive should not be exercised by the same individual. The division of responsibilities between the chairman and chief executive should also be clearly established, agreed by the board and set out in writing. The chairman should be independent, and the CEO should not go on to become chairman in the same company.

(iv) The disclosure of whether principles of good corporate governance have been applied is not normally enough; companies should also fully explain how such principles have been applied. The requirements for preparing a corporate governance report (and 'comply or explain' in this report) are contained in the UK Listing Rules for listed companies.

(v) There is a requirement for directors to meet regularly and to retain full and

effective control over the company. In practice, it is doubtful if anyone holding so many directorships, whether executive or non-executive, could devote sufficient time to each company to effectively fulfill their responsibilities. However, the Combined Code makes no specific reference to the number of directorships any individual may hold. The Code merely states that the letter of appointment of a non-executive director should set out the expected time commitment, and the individual should also make a disclosure to the board, before his or her appointment, of his or her other time commitments. There is also a requirement in the Code for individual directors to undergo a performance appraisal annually. Presumably, any director who does not have the time to perform his duties properly will be identified and asked either to commit more time or to resign.

Page 10 of 19 KAPLAN PUBLISHING

Interim Assessment

(vi) This is likely to comply with the Combined Code, although the board should also review risk management generally, not just the system of internal controls. The Combined Code states that the directors should maintain a sound system of internal control and, at least annually, conduct a review of the effectiveness of the group's system of internal controls and they should report to the shareholders that they have done so. The review should cover all material controls. These include not just financial controls, but also operational controls, compliance controls and the risk management system.

Tutorial note: This question – and solution – does not cover every aspect of the UK Combined Code. Similarly, corporate governance codes in other countries will address other issues in addition to those covered by this question. Perhaps a significant item to remember in the UK is that it is recommended that at least one half of the board of directors in large listed companies (and at least two directors in smaller companies) should be independent non-executive directors. A further item to note for the UK is the introduction of the Directors' Remuneration Disclosure Regulations in 2002, amending the Companies Act 1985 and requiring detailed disclosures about directors' remuneration and remuneration policy.

(b) Report on Corporate Governance in the USA, Germany and Japan

The broad principles of corporate governance are similar in the UK, the USA and Germany, but there are significant differences in how they are applied. In particular, whereas the UK and Germany have voluntary corporate governance codes, the US system is based on legislation (the Sarbanes-Oxley Act).

USA There are many similarities between corporate governance in the UK and USA. However, whereas the UK has historically relied upon a system of self-regulation and voluntary codes of best practice, the USA corporate governance structure is more formalised, often with legally enforceable controls. In the US, certain statutory requirements for publicly traded companies are set out in the Sarbanes-Oxley Act. These requirements include the certification of published financial statements by the CEO and the chief financial officer (finance director), faster public disclosures by companies, legal protection for whistleblowers, a requirement for an annual report on internal controls, and requirements relating to the audit committee, auditor conduct and avoiding 'improper' influence of auditors. The Act also requires the Securities and Exchange Commission and the main stock exchanges to introduce further rules relating to matters such as the disclosure of critical accounting policies, the composition of the board and the number of independent directors. The Act has also established an independent body to oversee the accounting firms. (This is called the Public Company Accounting Oversight Board, or 'Peek-a-Boo'). Managers must be careful to comply with regulations to avoid possible legal action against the company or themselves individually.

Germany As both the UK and Germany are members of the EU, they must both follow EU directives on company law. A major difference that exists in the board structure for companies is that the UK has a unitary board (consisting of executive and non-executive directors together), whereas German companies have a two-tier board of directors. The supervisory board of non-executives (Aufsichrat) has responsibility for corporate policy and strategy, and the management board of executive directors (Vorstand) has responsibility primarily for the day-to-day operations of the company. The supervisory board typically includes representatives from major banks that have historically been large providers of long-term finance to German companies (and are

KAPLAN PUBLISHING Page 11 of 19

ACCA P4 Advanced Financial Management

often major shareholders). The supervisory board does not have full access to financial information, is meant to take an unbiased overview of the company, and is the main body responsible for safeguarding the external stakeholders’ interests. The presence on the supervisory board of representatives from banks and employees (trade unions) may introduce perspectives that are not present in some UK boards. In particular, many members of the supervisory board would not meet the criteria under UK Combined Code guidelines for being considered independent. Japan Although there are signs of change in Japanese corporate governance, much of the system is based upon negotiation or consensual management rather than a legal or even a self-regulatory framework. As in Germany, banks have a significant influence, as have representatives of other external companies as shareholders. It is not uncommon for Japanese companies to have cross holdings of shares with their suppliers, customers, banks, etc, all being represented on each others' boards. There are often three boards of directors: policy boards, responsible for strategy and comprised of directors with no functional responsibility; functional boards, responsible for day-to-day operations; and largely symbolic monocratic boards. The interests of the company as a whole should dictate the actions of the boards. This is in contrast to the UK or US systems where, at least in theory, the board should act primarily in the best interests of the shareholders, i.e. the owners of the company.

The consensual management style should be respected even though at times decision making might seem slow.

MARKING SCHEME

Marks

(a) 1 to 2 marks per relevant point made, subject to a maximum of two marks for each of the six aspects listed (i) – (vi)

Max 10

(b) 1 to 2 marks per relevant point made, subject to a maximum of five marks for each country chosen

Max 10 ______

Total 20 ______

Page 12 of 19 KAPLAN PUBLISHING

Interim Assessment

ANSWER 4 (a) Delta measures the change in the option price (premium) as the value of the

underlying share moves by 1%.

Delta = share underlying the of price the in Change option the of price the in Change

It is measured by N(d1) in the Black-Scholes option pricing model. As the share price falls, delta falls towards zero. Delta may be used to construct a risk-free hedge position, whereby overall wealth will not change with small changes in share price. As the delta value approaches zero the hedged position will become unaffected by changes in share price.

(b) Using the Black-Scholes model for European options:

(1) Time, t = 15. (2) Using the guidance given in the question, Pa (in $ million) is estimated to be

either:

(i) 350 = 350 (1/ ) = 350 (1/2.7319) = 128.11, or )15(067.0e− )15(067.0e

(ii) 500 = 500 (1/2.7319) = 183.02. )15(067.0e−

(3) The exercise price, Pe = 400 (in $ million) (4) The interest rate, r = 0.05.

(5) Volatility, s = 185.0 = 0.430.

These values can now be applied to the Black-Scholes formula values. Call price for a European option = c = PaN(d1) – PeN(d2)e−rt , where:

tst)s5.0r()P/Pln(

d2

ea1

++= and tsdd 12 −=

If Pa is 128.11

1543.0)15)(43.05.005.0()400/11.128ln(d

2

1×++

= = + 0.600

tsdd 12 −= = 1543.0600.0 − = – 1.065

KAPLAN PUBLISHING Page 13 of 19

ACCA P4 Advanced Financial Management

From normal distribution tables: • d1 = 0.600. Normal distribution value = 0.2257, say 0.226. d1 is a positive

value, therefore add to 0.5. N( ) = 0.5 + 0.226 = 0.726 1d

• = – 1.065. Normal distribution value = mid-way between 0.3554 and 0.3577 = 0.35655, say 0.357. is negative, therefore subtract from 0.5.

2d

2d

N( ) = 0.5 – 0.357 = 0.143. 2d

Inputting data into call price = c = PaN(d1) – PeN(d2)e−rt

Call price (in $ million) = 128.11 (0.726) – [400 (0.143)/ ] = 93.01 – 27.02 = 65.99.

)15(05.0e

If Pa is 183.02

1543.0)15)(43.05.005.0()400/02.183ln(d

2

1×++

= = + 0.814

tsdd 12 −= = 1543.0814.0 − = – 0.851

From normal distribution tables:

• = 0.814. Normal distribution value = between 0.2910 and 0.2939, say

0.292. 1d

is a positive value, therefore add to 0.5. 1d

N( ) = 0.5 + 0.292 = 0.792 1d

• = – 0.851. Normal distribution value = above 0.3023, say 0.303. 2d

is a negative value, therefore subtract from 0.5. 2d

N( ) = 0.5 – 0.303 = 0.197. 2d

Inputting data into call price = c = PaN(d1) – PeN(d2)e−rt

Call price (in $ million) = 183.02 (0.792) – [400 (0.197)/ ] = 144.95 – 37.22 = 107.73

)15(05.0e

Recommendation Under both scenarios the call option has a value in excess of the static NPV estimates.

(a) With a $350 million present value from sales and development costs of $400

million, the expected NPV is ($50 million), but the value of the call option is $66 million.

Page 14 of 19 KAPLAN PUBLISHING

Interim Assessment

(b) With a $500 million present value from sales the expected NPV is $100 million, whilst the call option value is $107 million.

If the data are correct then the option pricing model would suggest that the company should develop the patent no matter which present value occurs. However, valuing a long-term option such as this is subject to restrictive assumptions and will be subject to a considerable margin of error. Possible problems include:

(a) The accuracy of the present value forecasts, and the use of the correct

discount rate to assess their risk. (b) The accuracy of the estimated development cost of the drug for commercial

use. This estimate could be subject to substantial error as it relates to a new product and probably to new technology.

(c) The accuracy of the estimated variance. As this is a new drug the variance of

returns from other Biotech companies might not be relevant, and the Black-Scholes model is quite sensitive to this variable. The model also assumes that this volatility will be constant for the 15-year period which is very unlikely.

(d) The Black-Scholes model was developed for European options. As

development of the drug could take place at any time during the 15 year period the option is an American option rather than a European option.

(e) What will happen after 15 years? Although competition will probably eliminate

most abnormal returns the company is likely to have built up a strong brand image and could still generate positive NPVs after this time, which have not been included in the above calculations.

(f) How likely is it that a competitor might develop a superior drug? If this occurs

the projections will be very adversely affected.

Because of the potential margin of error, Bioplasm should be cautious about accepting the values produced by the option pricing model, although they might be used as part of the overall decision process. This should also include the NPV estimates and strategic considerations. The company would also be advised to investigate possible cash flows after the patent period has expired.

KAPLAN PUBLISHING Page 15 of 19

ACCA P4 Advanced Financial Management

MARKING SCHEME

Marks

(a) Definition 1 Equation 1 Use 1 ______ 3 ______ (b) Correct Pa values 2 Estimates of N(d1) and N(d2) 4 Call values 4 Comment on call prices and their implications 3 Discussion of possible problems and conclusion 5 ______ Max 17 ______ Total 20 ______

ANSWER 5 (a) (i) Estimated market capitalisation − £125m

Post-acquisition earnings × Pre-acquisition P/E ratio of the bidding company (7.5m + 2.5m) = £10m × 12.5 times = £125m Estimated share price − £8.33

Market capitalisation £125m Number of shares Arshavin plc: 5m Berbatov plc:

15 × 10/15 10m__

15m Share price £125m/15m = £8.33

Estimated EPS – 67p Total earnings £10m/No of shares 15m = 67p Estimated equivalent value of one old Berbatov share − £5.55

£8.33 × 10 shares in A plc/for every 15 shares in B plc = £5.55

Page 16 of 19 KAPLAN PUBLISHING

Interim Assessment

(ii) REPORT

To: A N Other From: A N Accountant Date: 23 May 20X5 Subject: Pricing of Arshavin plc’s offer for Berbatov plc

The probable post-acquisition share price can be estimated by finding the total market capitalisation of the new group and dividing this by the number of shares in issue following the acquisition. This method assumes that the existing market capitalisations are a fair reflection of the value of the two companies, and ignores any synergistic effects.

Arshavin Berbatov Group

Earnings available to equity £2.5m £7.5m P/E ratio 12.5 7.5 Market capitalisation £31.25m £56.25m £87.5m Number of shares in issue 15m Post merger share price £5.83

The shareholders in Arshavin plc will retain the same number of shares after the acquisition, but their price will have fallen from (£31.25m/5m) = £6.25 to £5.83 per share. This represents a loss in value of £2.1m (5m × (6.25 − £5.83)) to the shareholders. In addition, Arshavin will have to issue a further 10m shares to the shareholders of Berbatov. This means that the shareholders in Arshavin will have lost control of the group, owning only one third of the total number of shares in issue post-acquisition. Thus, on the basis of the information provided this bid does not appear to be in the best interests of the shareholders in Arshavin. However, if Mr Khan is indeed able to bring about a significant improvement in performance of Berbatov plc, then the bid could hold some long term benefits for the shareholders.

The shareholders in Berbatov plc pre-merger share price (£56.25m/15m) = £3.75. This would compare to £5.83 × 10/15 = £3.89 – the equivalent value post-merger of one old Berbatov plc share, which only represents an acquisition premium of £3.89 − £3.75/£3.75 = 3.7%. This does not compare favourably with the average UK acquisition premium of 40%.

Thus, considering the small acquisition premium, the majority of shareholders in Berbatov plc will probably not be in favour of the bid.

It is worth noting that the share for share exchange would have the advantage of CGT postponement and that the Berbatov shareholders will hold the majority of shares in the new group.

KAPLAN PUBLISHING Page 17 of 19

ACCA P4 Advanced Financial Management

(b) The new information will affect the value of the combined group as follows. The improvement in net income of £7.5m will be capitalised at 15% (Arshavin’s cost of capital) to give a value of £50m.

£m

Market capitalisation as calculated above 87.5 Add: One-off administrative savings 5.0 Sale of assets at end of Year 1 £10m × 0.87 (discounted at 15%) 8.7 Improvement in net income £7.5/.15 = 50.0 ____ 63.7 _____ Revised market capitalisation 151.2 _____ Number of shares in issue 15m Post-merger share price £10.08

Total synergy − £63.7m Arshavin plc Berbatov plc £19.15m £44.55m (30%) (70%)

The shareholders in Berbatov acquisition premium would be: £10.08 × 10/15 = £6.72. £6.72 − £3.75/£3.75 = 79.2%. This reflects the percentage increase in wealth for target shareholders. Therefore their share of the total synergy is £56.25 × 0.792 = £44.55. This appears to represent a good deal for the Berbatov shareholders.

However, if a takeover of Berbatov is an attractive proposition to other companies as well as Arshavin this may mean that the shareholders are able to push the price up to what another bidder would be prepared to pay. The precise amount will depend on the size of the increase in value that the other bidders believe they could realise. If there are no other potential offers then the shareholders may not be able to obtain much improvement on Arshavin’s initial offer.

Page 18 of 19 KAPLAN PUBLISHING

Interim Assessment

MARKING SCHEME

Marks

(a) (i) Calculation of the post-acquisition data: Estimated market capitalisation based on bootstrapping 2 Estimated share price 2 Estimated EPS 2 Estimated equivalent value of one old Berbatov plc share 2 (ii) Report: Calculation of post-merger share price 2 Comment about reduction in share price of Arshavin plc 1 Calculation of acquisition premium 1 Comment on low acquisition premium 1 Comment: Berbatov’s shareholders will be the majority

shareholders of CGT comment 1 __

14 (b) Calculation of the PV of the synergies 2 Calculation of the new post-share price 1 Calculation of acquisition premium 1 Valid concluding comments, maximum marks 2 __ 6 __ Total 20 __

KAPLAN PUBLISHING Page 19 of 19