pacra jawad

TRANSCRIPT

0

Assignment

Submitted to

Mr. Hafiz M. Waqar

Submitted By

Arooj Rehmat

1

PACRA REGULATORY MECHANISM

The Pakistan Credit Rating Agency Limited

History:

The trend of establishing local rating agencies started only in the

1970s. Prior to this, the two international rating agencies, namely

standard and poor’s, and Moody’s investor service, dominated the

rating world. However, since the establishment of first known local

rating agency, the Canadian Bond Rating Services in 1972, local

rating agencies have proliferated across the globe, both in the

developed markets (Australia, France and Japan), and also in a large

number of emerging markets. Currently, there are 17 emerging

markets (Argentina, Brazil, Chile, Columbia, India, Israel, Korea,

Malaysia, Mexico, Pakistan, Peru, Philippines, Portugal , South Africa

, Thailand , Tunisia, Venezuela) were duly recognized local rating agencies are in operation. Of these

countries Pakistan joined the club in 1994, with the establishment of PACRA. It is interesting to note that

in several other important emerging markets including Turkey, East European countries and republics of

the former Soviet Union, rating agencies still have to be established or are in the process of being

established. The main motivation for the establishment of local rating agencies is the recognition of their

critical role in promoting or other fixed income securities markets. At the same time there is increasing

realization that rating agencies are likely to impart efficiency to the financial and capital markets.

PACRA stands for Pakistan Credit Rating Agency. It was first credit rating Company established in Pakistan.

It was established in 1994 between the joint venture of IBCA Limited (the international credit rating

agency), International Finance Corporation (IFC) and the Lahore Stock Exchange. The primary function of

PACRA is to evaluate companies’ willingness to fulfill its debt obligations. PACRA is geared to provide a full

range of credit rating services. This includes the rating of corporate entities and fixed income instruments.

The ownership and management structure of PACRA ensures complete independence from any direct or

indirect control of the Government, any private sector business group or financial institution. A rating

assigned by the rating committee, which includes senior management of PACRA, reflects PACRA's

objectively formed opinion of credit risk. Other rating reviews carried out by PACRA include Financial

Strength ratings of modarabas, Mutual Fund ratings and Insurer Financial Strength (IFS) ratings for

insurance companies.

2

PAKISTAN CREDIT RATING REGULATORY FRAMEWORK

Establishment of PACRA in 1994 represents an important milestone in

the development of financial infrastructure in Pakistan. More

significantly, this signifies the fulfillment of all the ingredients

considered necessary for the establishment of local bond (TFC) market

in the country. In order to establish the sanctity and credibility of credit

ratings in the country, the regulators moved quickly for prescribing the

eligibility criteria for the establishment of credit rating companies and

also assumed the legal authority of monitoring the functioning of such

companies on a regular basis. This dual purpose which was achieved by the Corporate Law Authority

through an amendment in the Security and Exchange ordinance 1969, and notification of “Credit Rating

Companies Rules 1995”. The most significant eligibility condition for registration of a credit rating

company is a joint venture arrangement or technical collaboration with an internationally recognized

credit rating institution. PACRA having satisfied all the requirements under the rules stands duly registered

with the CLA. In order to provide to investors in fixed income securities (including TFC’s), the CLA has

made it mandatory for all such securities to be rated if the instrument is to be offered to the general public

and listed on the stock exchange.

Meanwhile, the SBP also recognized the potential benefit of credit rating in terms of augmenting the

supervisory role of SBP for monitoring the performance of the financial sector. It was therefore, made

mandatory for all Modarbas (an Islamic financial institution), leasing companies, as well as investment

bank to obtain credit rating. Under current regulations prescribed by the CLA – all Modarbas issuing COMs,

(CERTIFICATE OF MUSHARIKA) and all the leasing companies issuing COIs (CERTIFICATE OF

INVESTMENT)require to be rated on a continuing basis.

Mission of PACRA

To be accepted as the leading credit rating agency in the country

through highest standards of professionalism and ethics.

3

Risk Evaluation

PACRA ratings reflect an independent, professional opinion of

the credit quality denoting the credit risk associated with a

particular debt instrument or a corporate entity. By providing

a measurement of risk, PACRA’s ratings facilitate investment

decisions. However, PACRA’s rating is not the

recommendation to purchase, sell or hold a security, in as

much as it does not comment on the security’s market price or

suitability for a particular investor.

PACRA’s Product of Rating:

PACRA’s spectrum of rating covers:

Instrument Rating

Structured Finance Rating

Entity Rating

Insurer Financial Strength Rating

Project Grading

Fund Stability Rating

Star Ranking /Fund Performance Ranking

Capital Protection Rating

Asset Manager Rating

Instrument Rating:

Instrument rating covers all non-equity instruments including TFC’s (long and short term), convertibles, debentures and redeemable certificates. PACRA’s rating process assumes that the return offered on such instruments (expected profit, makeup etc) is in the nature of a fixed obligation. Thus, in the case of TFC’s even though the issuing document refers to the return as ‘expected profit’, PACRA, in consonance with the shared perception of the issuer and the investor, deems this to be a contractual obligation for purpose of credit rating.

Structured Finance Rating:

PACRA has also developed the expertise of rating securities or structured finance debt instruments. Such instruments could have varying credit enhancement characteristics for reducing the default risk, the investment risk, or both. Structured Finance ratings focus mainly on evaluating the specific cash flows identified for meeting the repayment obligations and also the security arrangements. PACRA’s ratings are contingent on examining all the underlying documentation that gives effect to the purposed features of the instrument.

4

While all ratings follow an interactive process, the degree of interaction between the client and PACRA is considerably more in such ratings than in standard instrument ratings. Consistent with international practice, PACRA is also prepared to review various options of credit enhancement and advise the client on the preferred option for achieving the desired rating.

Entity Rating:

Entity rating signifies the entity’s level of credit risk and the capacity for timely payment of financial commitments to senior unsecured creditors. The risk level is indicated by the long and short term ratings.

Insurer Financial Strength Rating:

The insurer financial strength (IFS) rating represents an opinion of an issuer’s financial strength and

business continuity from a policy holder's prospective. IFS rating capture the relative ability of the insurer

to meet policy holders' obligations. However, the rating provides no guarantee against default but offers a

well-researched opinion as to the likelihood of the issuer to fail to fulfill its obligations towards policy

holders. IFS rating is applicable to insurance obligations insofar as these are in compliance with the

company's stated policies and procedures.

Project Grading

The Project Grading (PG) is an opinion on a specific project being managed by any real estate entity. PG

differentiates projects on the basis of their individual attributes; the concept is that projects of the same

developer could have different grading; Although DG and PG have a high probability of linear relationship,

this could break to merit a different rating for the project depending upon its unique characteristics.

Fund Stability Rating

This is an opinion on the prospective relative stability in a fund’s return. The rating provides an objective

measure as to the main areas of risk to which the income and money-market funds are exposed. The risk

factors are: Credit Risk, Market Risk, Liquidity Risk, Returns Volatility, and Quality of Management and

Support Systems.

Star Ranking /Fund Performance Ranking

The Star Ranking measures performance of funds in a risk and returns combination, and then ranks the

funds accordingly on the basis of their performance. The ranking is a quantitative measure and funds are

rated within their respective categories. A fund’s particular ranking is computed with reference to its

category and consequently, rankings are comparable only in the same category.

Capital Protection Rating

Capital Protection Rating (CPR) is another rating class for mutual funds. CPR captures the relative extent

to which principal invested in the fund is secure from loss at the time of maturity. CPR is not a view on the

5

fund performance; it is concerned with the fund performance only insofar as it is imperative to meet the

redemption of the principal amount at maturity.

Asset Manager (AM) Rating

Asset Manager (AM) Rating provides investors with an independent opinion on the quality and expertise

deployed by an asset management company and potential vulnerability to operational and investment

management failures. AM Rating differs fundamentally from credit ratings, which refer to the ability to

meet debt obligations. The focus of AM rating is to gauge the fund management capability of the asset

manager, as reflected from its operating platform, human resource base and the infrastructure that it has

erected. AM rating gives a view on whether the asset manager meets or exceeds the overall investment

management best practices, the benchmarks and standards in all criteria under review.

Rating Methodologies

PACRA‘s rating evaluation is reflected in its rating scale which is applicable to long-term and short-term ratings and is internationally recognizable. Fundamentally, the rating scale represents a decreasing order of risk. In determining the level of risk, a diverse range of complex data is collected and analyzed. This data is gathered primilary from the potential issuer or client and supplemented with strategic information obtained from outside independent, reliable sources. The rating process covers analysis of both quantitative and qualitative aspects including operations, finance, management and strategy. The factors considered by PACRA while forming its opinion include:

Industry Risk:

Industry risk is measured by the strength of the industry within the economy and relative to economic trends. This also includes the ease or difficulty of entering the industry, the diversity of earning base and role of regulation and legislation. The specific issues covered include:

Economic importance of the industry Potential for support Employment significance Industrial relations record Significance of legislation: protective and harmful, relationship with Govt. Maturity of the industry International competition Barriers to entry Competitive situation domestically: monopoly, oligopoly, fragmentation Nature of the industry: capital intensity, product life spans, marketing requirements Cyclic factors: demand, supply, implications for price volatility Industry cost and revenue structure: susceptibility to energy prices, interest rate levels, Govt.

policies Important developments and trends in the industry

6

Market Position:

Market position covers the company’s market share in its major

activities and the historical protection of its position and projected

ability for the future. It also covers the company’s historical operating

margins and its ability to maintain and improve them. The specific issues

covered include:

Competitive position within the industry: size, market share & trend, price setting-ability

Major product importance

Product lives and competition

Degree of product diversification

Significance of R&D expenditure and of new product development

Geographic diversity of sales and production

Ownership and Support:

The ownership structure of the company, financial strength of the owners, potential for support and other tangible benefits are covered in this area. The specific issues covered include:

Ownership of the entity

Relationship with owners

Financial strength of owners

Potential for support or for funds with drawls

Structure of relationship

Other benefits: access to technology products

Access to capital markets

Management Evaluation

Management evaluation covers the record to date in operations and financial terms, corporate goals, attitude to risk, control system, experience and record control to peers. The specific issues covered include:

Record to date in financial terms

Corporate goals and outlook: aggressive stance, attitude to risk

Experience, background, credibility

Depth of management: key individuals, succession

Record compared with peers

7

Accounting Quality:

This area covers an overall review of the accounting policies employed and consistency in their application. The specific issues covered include:

Reporting and disclosure requirements

Auditors and audit opinions

Revenue recognition policies: long-term projects

Stock valuation policies

Fixed asset valuation method

Goodwill and intangible treatment

Undervalued assets , such as free hold property

Debt/Equity hybrid instruments

Depreciation methods, rates , lives

Foreign currency treatment

Deferred taxation policy

Accounting for pension obligations

Treatment of finance cost

Contingent liabilities

Overall aggressiveness or prudence of accounting presentation

Unusual accounting policies , movements on reserves

Changing in accounting policies

Changes in group composition

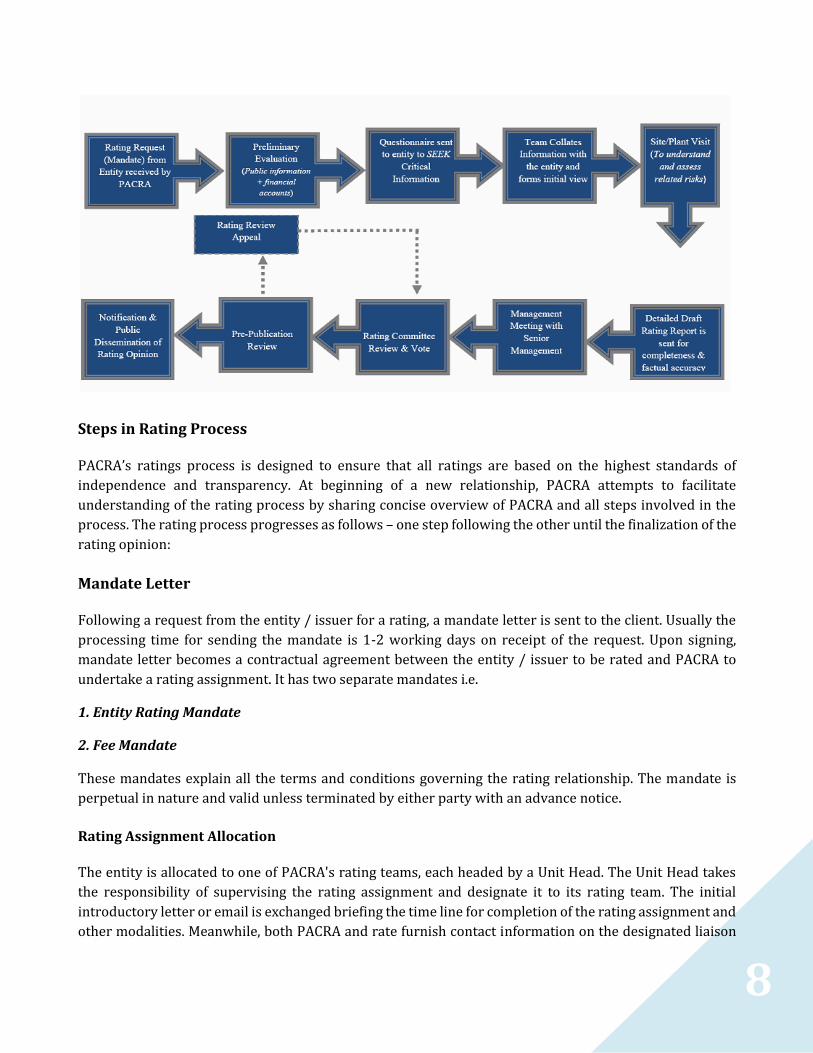

Rating Process

Credit rating is an interactive process relying primarily on information and interaction with the rater. It

is supplemented with information obtained from outside independent sources. The entire process is

aimed at evaluating financial strength of an entity to timely meet its financial obligations. PACRA follows

a rigorous, objective and structured rating process at the onset of rating relationship to arrive at a rating

opinion. The rating process, subscribes to rigorous quality standards. PACRA has developed

comprehensive methodologies for different segments of entities – Banks, NBFCs, Insurance, AMCs, and

Corporate. We evaluate and analyze both qualitative and quantitative aspects and captures factors

affecting the entity in the short-term and long-term. Our analyses broadly focus on ownership and

governance structure of the organization, its management and control environment and evaluation of

business and financial risks.

8

Steps in Rating Process

PACRA’s ratings process is designed to ensure that all ratings are based on the highest standards of

independence and transparency. At beginning of a new relationship, PACRA attempts to facilitate

understanding of the rating process by sharing concise overview of PACRA and all steps involved in the

process. The rating process progresses as follows – one step following the other until the finalization of the

rating opinion:

Mandate Letter

Following a request from the entity / issuer for a rating, a mandate letter is sent to the client. Usually the

processing time for sending the mandate is 1-2 working days on receipt of the request. Upon signing,

mandate letter becomes a contractual agreement between the entity / issuer to be rated and PACRA to

undertake a rating assignment. It has two separate mandates i.e.

1. Entity Rating Mandate

2. Fee Mandate

These mandates explain all the terms and conditions governing the rating relationship. The mandate is

perpetual in nature and valid unless terminated by either party with an advance notice.

Rating Assignment Allocation

The entity is allocated to one of PACRA's rating teams, each headed by a Unit Head. The Unit Head takes

the responsibility of supervising the rating assignment and designate it to its rating team. The initial

introductory letter or email is exchanged briefing the time line for completion of the rating assignment and

other modalities. Meanwhile, both PACRA and rate furnish contact information on the designated liaison

9

person (s) for ensuring smooth and speedy communication. The respective sub team manager and analyst

take care of all aspects of the rating assignment as per the PACRA's guidelines.

Preliminary Analysis & Information Solicitation

A Preliminary study is conducted with a careful review of an entity's published information. From this

review, analysts determine what additional information and data are needed. A detailed questionnaire is

sent to the client for soliciting the required financial & non-financial information over and above that

provided in their financial statements and the notes to their accounts. Upon receipt of the information, an

initial rating assessment is made and discussed internally based on findings of the rating team. This would

be followed by a site visit and management meeting, preferably at entity's head office.

Site Visit

The respective rating team conducts entity's head office and/or plant visit. The objective of which is to

develop a better understanding of the organizational structure, and quality of the process, and conduct

interview of key department heads and establish a sense of control environment prevailing in the entity. A

detailed itinerary in advance is sent for the said visit.

Management Meeting

The purpose of Management Meeting is to assimilate the strategic view of the entity’s top management The

meeting is wide-ranging, covering the entity's ownership, governance, financial position, future prospects,

the economic environment and many other issues that can have a bearing on the rating. The participants

of the meeting include the respective rating team, Unit Head and members of apex rating committee from

PACRA and the senior management of the client including the Chief Executive Officer. Before heading for

the management meeting, a formal agenda is sent, highlighting the areas where we expect to have the views

and opinions of the entity’s top management. We expect to have a formal presentation for this meeting

covering, at a minimum, those areas highlighted in the agenda.

Draft Rating Report Review

Subsequent to the management meeting, a draft detailed rating report is sent to the entity's management

for their feedback on completeness and accuracy of the information contained in the report. If the report

containing anything which is confidential, the client is also expected to communicate the same. The

feedback is expected from the entity within five working days.

Rating Committee

A multi-layered, decision-making process is followed in assigning a rating. In finalizing the rating, the

relevant team prepares a rating proposal based on the information gathered through the questionnaire

and discussion at the Management Meeting and head office/site visit. This is presented to the rating

committee, comprising at least one apex, two permanent members and the rating team. The RC is usually

conducted within one week following the management meeting.

10

Pre-Publication Review

Subsequent to the Rating Committee, PACRA provides rated entities with draft press release and one page

summary report in advance for pre-publication review. This is to avoid issuing any credit analyses that

contain misrepresentations or are otherwise misleading as to the general credit worthiness of an entity /

issuer.

Notification

Once the rating has been finalized, it is formally notified to the entity / issuer. The rating notification is

usually accompanied by a final set of rating report and press release.

Standard Rating Scale & Definitions

ASSET MANAGER RATING SCALE & DEFINITIONS

AM1: Asset manager meets or exceeds the overall investment management industry best practices and

highest benchmarks in all criteria under review.

AM2: Asset manager meets very high investment management industry standards and benchmarks with

noted strengths in several of the rating factors.

AM3: Asset manager meets high investment management industry standards and benchmarks.

AM4: Asset manager demonstrates an adequate organization that meets investment management industry

standards and benchmarks.

AM5: Asset manager does not meet the minimum investment management industry standards and

benchmarks.

CAPITAL PROECTION RATING SCALE & DEFINITIONS

AAA (cp): Exceptionally Strong certainty Capital Protection.

AA (cp): Very strong certainty of capital protection.

A (cp): Strong certainty of protection.

BBB (cp): Adequate certainty of capital protection

BB (cp): weak capital protection

11

DEBT INSTRUMENT RATING SCALE & DEFINITIONS

LONG TERM RATINGS

AAA: Highest credit quality. ‘AAA’ ratings denote the lowest expectation of credit risk. They are assigned only in case of exceptionally strong capacity for timely payment of financial commitments. This capacity is highly unlikely to be adversely affected by foreseeable events. AA: Very high credit quality. ‘AA’ ratings denote a very low expectation of credit risk. They indicate very strong capacity for timely payment of financial commitments. This capacity is not significantly vulnerable to foreseeable events.

A: High credit quality. ‘A’ ratings denote a low expectation of credit risk. The capacity for timely payment of financial commitments is considered strong. This capacity may, nevertheless, be more vulnerable to changes in circumstances or in economic conditions than is the case for higher ratings. BBB: Good credit quality. ‘BBB’ ratings indicate that there is currently a low expectation of credit risk. The capacities for timely payment of financial commitments are considered adequate, but adverse changes in circumstances and in economic conditions are more likely to impair this capacity. This is the lowest investment grade category. BB: Speculative. ‘BB’ ratings indicate that there is a possibility of credit risk developing, particularly as a result of adverse economic change over time; however, business or financial alternatives may be available to allow financial commitments to be met. Securities rated in this category are not investment grade. B: Highly speculative. ‘B’ ratings indicate that significant credit risk is present, but a limited margin of safety remains. Financial commitments are currently being met; however, capacity for continued payment is contingent upon a sustained, favorable business and economic environment. CCC, CC, C: High default risk. Default is a real possibility. Capacity for meeting financial commitments is solely reliant upon sustained, favorable business or economic developments. A‘CC’ rating indicates that default of some kind appears probable. ‘C’ ratings signal imminent default.

SHORT TERM RATINGS

A1+: Obligations supported by the highest capacity for timely repayment. A1:. Obligations supported by a strong capacity for timely repayment. A2: Obligations supported by a satisfactory capacity for timely repayment, although such capacity may be susceptible to adverse changes in business, economic, or financial conditions. A3: Obligations supported by an adequate capacity for timely repayment. Such capacity is more susceptible to adverse changes in business, economic, or financial conditions than for obligations in higher categories. B: Obligations for which the capacity for timely repayment is susceptible to adverse changes in business, economic, or financial conditions.

12

C: Obligations for which there is an inadequate capacity to ensure timely repayment. D: Obligations which have a high risk of default or which are currently in default.

FUND STABILITY RATING SCALE & DEFINITIONS

AAA (f): A fund showing a consistently outstanding performance with very strong capacity to respond to

future opportunities or stress situations.

AA (f): A fund consistently outperforming its peers with strong capacity to respond to future opportunities

or stress situations.

A (f): A fund with stable performance generally in line with its peers with adequate capacity to respond to

future opportunities or stress situations.

BBB (f): A fund with performance comparable to peers but showing a relatively higher volatility and lower

capacity to respond to future opportunities or stress situations.

BB (f): A fund with a below average performance and limited capacity to respond to future opportunities

or stress situations.

INSUERER FINANCIAL STRENGTH (IFS) SCALE & DEFINITIONS

AAA – Exceptionally Strong. Insurers assigned this highest rating are viewed as possessing

exceptionally strong capacity to meet policyholder and contract obligations. For such companies, risk

factors are minimal and the impact of any adverse business and economic factors is expected to be

extremely small.

AA-Very Strong. Insurers are viewed as possessing very strong capacity to meet policyholder and

contract obligations. Risk factors are modest, and the impact of any adverse business and economic

factors is expected to be very small.

A -Strong. Insurers are viewed as possessing strong capacity to meet policyholder and contract

obligations. Risk factors are moderate, and the impact of any adverse business and economic factors is

expected to be small.

BBB -Good. Insurers are viewed as possessing good capacity to meet policyholder and contract

obligations. Risk factors are somewhat high, and the impact of any adverse business and economic

factors is expected to be material, yet manageable.

BB - Moderately Weak. Insurers are viewed as moderately weak with an uncertain capacity to meet

policyholder and contract obligations. Though positive factors are present, overall risk factors are high,

and the impact of any adverse business and economic factors is expected to be significant.

B -Weak. Insurers are viewed as weak with a poor capacity to meet policyholder and contract

obligations. Risk factors are very high, and the impact of any adverse business and economic factors is

expected to be very significant. CCC, CC, C -Very Weak. Insurers rated in any of these three categories

13

are viewed as very weak with a very poor capacity to meet policy holder and contract obligations. Risk

factors are extremely high, and the impact of any adverse business and economic factors is expected to

be insurmountable.

A 'CC' rating indicates that some form of insolvency or liquidity impairment appears probable. A 'C'

rating signals that insolvency or a liquidity impairment appears imminent.

DDD, DD, D -Distressed. These ratings are assigned to insurers that have either failed to make

payments on their obligations in a timely manner, are deemed to be insolvent, or have been subjected

to some form of regulatory intervention. Within the DDD-D range, those companies rated 'DDD' have

the highest prospects for resumption of business operations or, if liquidated or wound down, of having

a vast majority of their obligations to policyholders and contract holders ultimately paid off, though on

a delayed basis (with recoveries expected in the range of 90-100%). Those rated 'DD' show a much

lower likelihood of ultimately paying off material amounts of their obligations in a liquidation or wind

down scenario (in a range of 50-90%). Those rated 'D' are ultimately expected to have very limited

liquid assets available to fund obligations, and therefore any ultimate payoffs would be quite modest (at

under 50%)

REAL ESTATE PROJECT GRADING SCALE & DEFINITIONS

PG1: Very strong project execution capacity. The prospects of execution of the real estate project as per

plan are the most promising and the ability to transfer ownership as per terms is the highest.

PG2: Strong project execution capacity. The prospects of execution of the real estate project as per plan

and the ability to transfer ownership as per terms are highly promising. PG3 Good project execution

capacity. The prospects of execution of the real estate project as per plan and the ability to transfer

ownership as per terms are good. Project execution capacity can be affected moderately by changes in

the real estate sector prospects.

PG4: Adequate project execution capacity. The prospects of execution of the real estate project as per

plan and the ability to transfer ownership as per terms provide adequate comfort. Project execution

capacity can be affected severely by changes in real estate sector prospects.

PG5: Weak project execution capacity. The prospects of execution of the real estate project as per plan

and the ability to transfer ownership as per terms are poor.