page 1 the new auditor’s report and iaasb’s work plan dan montgomery, auditor reporting...

TRANSCRIPT

Page 1

The New Auditor’s Report and IAASB’s Work Plan

Dan Montgomery, Auditor Reporting Implementation Working Group Chair, Former Auditor Reporting Task Force Chair and IAASB Deputy Chair

Johannesburg, South Africa

October 12, 2015

Page 2

I. The New Auditor’s Report

Page 3

Why Change the Auditor’s Report?

• Foundation for the future of global auditor reporting and improved auditor communications

• Essential to the continued relevance of the audit profession globally

– Audit opinion is valued, but could be more informative

– Users want more relevant and decision-useful information about the entity and the financial statement audit

Page 4

New and Revised Auditor Reporting Standards – Key Features

Aud

itor

Rep

ort Audit Opinion – Required to be presented first

Key Audit Matters – Required for listed entities

Going Concern – Additional focus

Other Information – New section

Responsibilities – In the audit; Independence and ethical obligations; Engagement partner (listed entities)

Page 5

Expected Benefits of the New Auditor’s Report

• Enhanced communicative value to users• More robust interactions and communication among

users, auditors and those charged with governance (TCWG)

• Increased attention by management and TCWG to the disclosures referred to in the key audit matters (KAM) section of the auditor’s report

• Increased professional skepticism in areas where KAM are identified

• Increased audit quality or users’ perception of audit quality

Page 6

Decision-Making Framework for Determining KAM

Matters that were communicated with TCWG

Matters that required significant auditor attention

Matters of most significance

in the audit Key Audit

Matters

Page 7

Initial Step in Determining KAM

The auditor will always consider

• Areas of higher assessed risks of material misstatements or significant risks (i.e., risks requiring special audit consideration)

• Significant auditor judgments relating to areas of significant management judgment (e.g., complex accounting estimates)

• Effect on the audit of significant events or transactions

Matters that were communicated with TCWG

Matters that required significant auditor attention

Page 8

Determination of Matters of Most Significance in the Audit – KAM

• KAM is determined by the auditor’s consideration of the– Nature and extent of communication with TCWG

– Importance to intended users’ understanding of the financial statements

– Nature and extent of audit effort needed to address

– Nature of the underlying accounting policy, its complexity or subjectivity

– Nature and materiality, quantitatively or qualitatively, of corrected and accumulated uncorrected misstatements due to fraud or error (if any)

– Severity of any control deficiencies identified relevant to the matter (if any)

– Nature and severity of difficulties in applying audit procedures, evaluating the results of those procedures, and obtaining relevant and reliable evidence

Matters that required significant auditor attention

Matters of most significance in the audit

Page 9

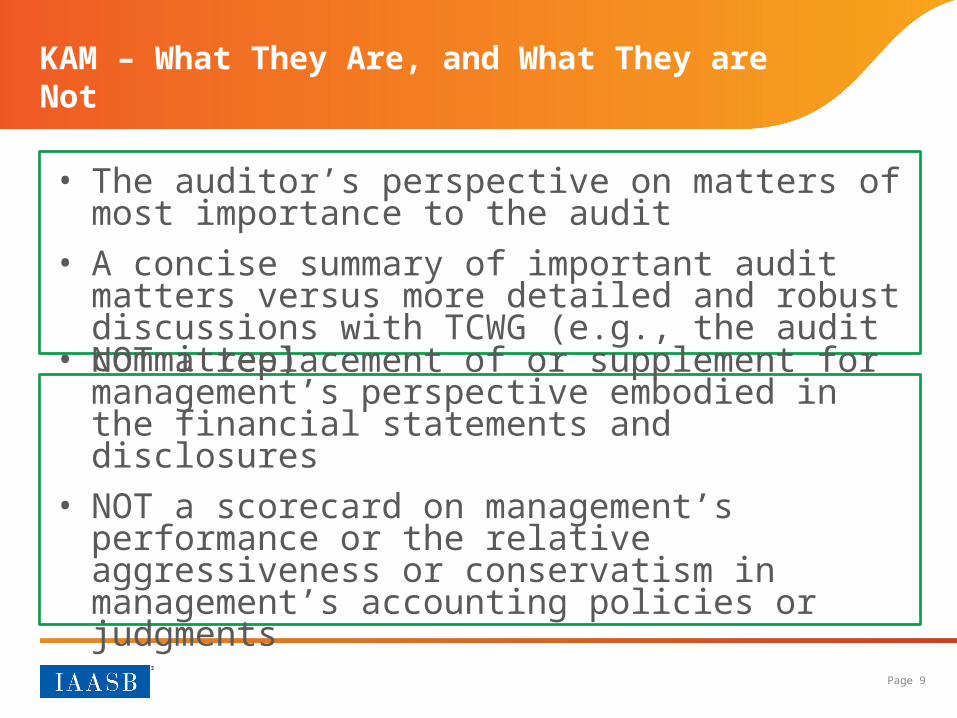

KAM – What They Are, and What They are Not

• The auditor’s perspective on matters of most importance to the audit

• A concise summary of important audit matters versus more detailed and robust discussions with TCWG (e.g., the audit committee)

• NOT a replacement of or supplement for management’s perspective embodied in the financial statements and disclosures

• NOT a scorecard on management’s performance or the relative aggressiveness or conservatism in management’s accounting policies or judgments

Page 10

KAM – Delivering Entity-Specific Information to Users

Consistency and

Comparability

Relevance and Usefulness

Boilerplate; generic language;not relevant to the entity or the audit

Entity- and audit specific information of increased value

Page 11

Are KAM Always Communicated in the Auditor’s Report?

• Auditor is required to include each KAM unless– Law or regulation precludes disclosure– In extremely rare circumstances, the auditor determines that the

matter should not be communicated Adverse consequences of communicating the KAM would reasonably be

expected to outweigh the public interest benefits of such communication

• In certain limited circumstances, there may be no KAM to be communicated

• Concepts of EOM and OM paragraphs are retained – EOM and OM paragraphs cannot be used as a substitute for

communicating a matter determined to be a KAM

Page 12

Enhanced Auditor Reporting on Going Concern

• Changes to ISAs and the auditor's report to focus more on GC– Explicit description of the respective

responsibilities of management and the auditor in all auditor’s reports

– Separate GC section required when material uncertainty exists, with a heading “Material Uncertainty Related to Going Concern”

– New requirement to challenge adequacy of disclosures for GC “close calls”

Page 13

Interaction Between KAM and Going Concern (GC)

• Matters relating to GC, including “close calls”, may be determined to be KAM and communicated in the auditor’s report in accordance with new ISA 701

• When a material uncertainty related to GC exists, it is by nature a KAM, but is reported separately in the “Material Uncertainty Related to Going Concern” section of the auditor’s report

More information about GC is available in the Auditor Reporting Toolkit at: www.iaasb.org/auditor-reporting.

Page 14

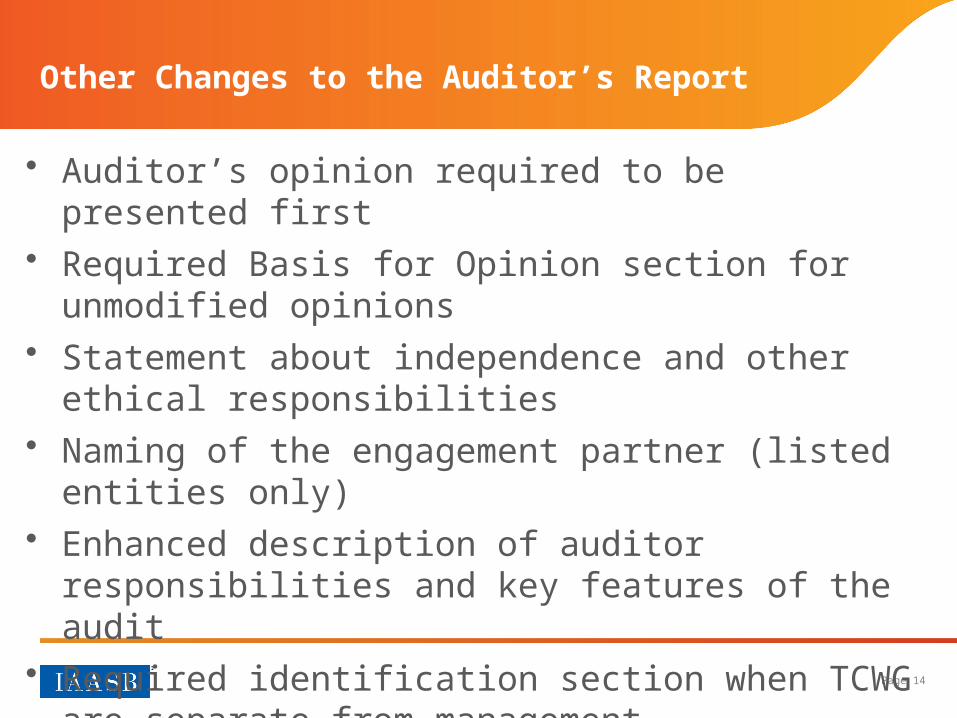

Other Changes to the Auditor’s Report

• Auditor’s opinion required to be presented first • Required Basis for Opinion section for unmodified

opinions• Statement about independence and other ethical

responsibilities• Naming of the engagement partner (listed entities only)• Enhanced description of auditor responsibilities and key

features of the audit • Required identification section when TCWG are

separate from management

Page 15

New Webpage www.iaasb.org/auditor-reporting with easy access to new and revised standards and other resources

• Auditor Reporting Fact Sheet • Auditor Reporting “At a Glance”• Basis for Conclusions• Publications on GC and KAM • Illustrative KAM examples • Plans for webcasts, podcasts and other

potential publications

Resources – Auditor Reporting Toolkit

Page 16

• IAASB-supported “roll-out plan” with objectives of– Promoting awareness

– Informing and educating users

– Learning about experiences of those responsible for adopting and implementing the standards

– Preparing for post-implementation review

• Planned activities – Outreach and other communications

– Auditor Reporting Toolkit

Implementation Support

New and revised Auditor Reporting standards are effective for periods ending on or after December 15, 2016

Page 17

II. IAASB Work Plan – Enhancing Audit Quality

Page 18

Enhancing Audit Quality

• Clarified ISAs and ISQC 1 serve fundamental role in underpinning audit quality, need to evolve in response to – Changes in business environment– Firm’s business models (structures; organization of audits)– ISA Implementation Monitoring findings and other feedback on

current practices– Audit inspection findings– Outreach and other interactions

Key Strategic Objective: Ensure that ISAs continue to form the basis for high-quality, valuable and relevant audits conducted worldwide by responding on a timely basis to issues noted in practice and emerging developments

Page 19

Work Plan for 2015–2016 ― Priority Projects

The IAASB in the Coming Years

2015: (1) Intense exploration, research and outreach One discussion

paper (ITC); (2) Project proposal related to ISA

540

2016: Analysis of comments and dialogue Proposals for

standard setting and other guidance

Enhancing Audit Quality with a Clear Public Interest Perspective

Quality Control

Group Audits

ISA 540, Incl. FI

Professional Skepticism

Page 20

Timing―ITC

• Issuance of ITC (Quality Control; Group Audits; Professional Skepticism) – Dec 2015; Comment period of 150 days ending May 2016; outreach events held while ITC is out for comment and possibly after

• Comment analysis and discussion – May 2016–Sept 2016

• Approval of project proposals (Quality Control and Group Audits), and decision on IAASB way forward re: Professional Skepticism – Sept 2016

• Development of Exposure Drafts (Quality Control and Group Audits) – Sept 2016–mid-2017

Page 21

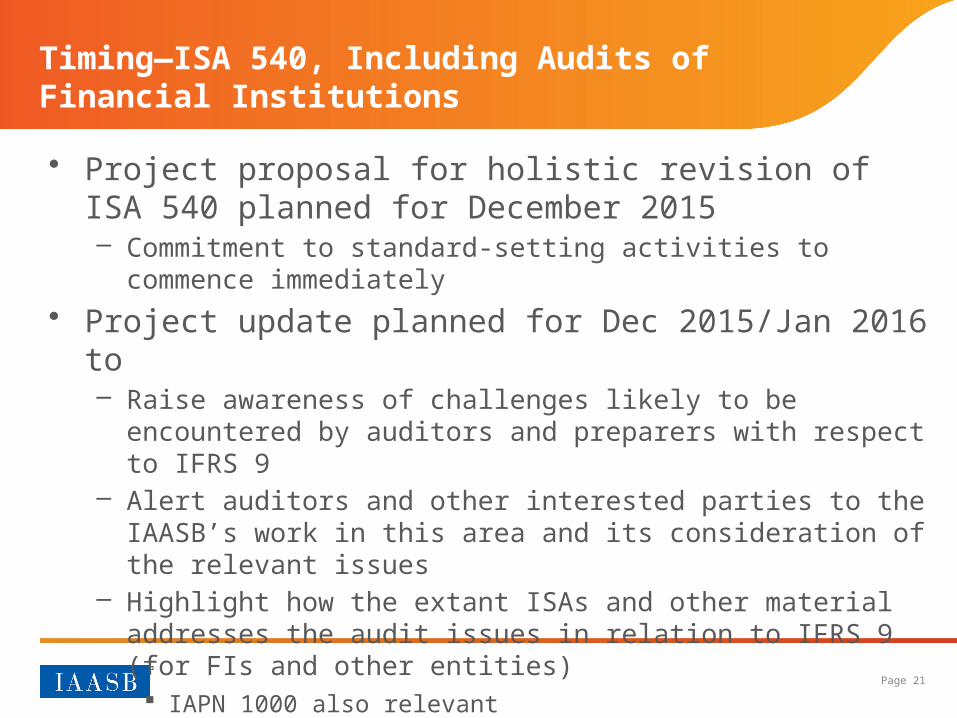

• Project proposal for holistic revision of ISA 540 planned for December 2015– Commitment to standard-setting activities to commence

immediately

• Project update planned for Dec 2015/Jan 2016 to– Raise awareness of challenges likely to be encountered by auditors

and preparers with respect to IFRS 9– Alert auditors and other interested parties to the IAASB’s work in

this area and its consideration of the relevant issues– Highlight how the extant ISAs and other material addresses the

audit issues in relation to IFRS 9 (for FIs and other entities) IAPN 1000 also relevant

– Signal the IAASB’s plans with respect to the issues that are likely to be addressed in the revision of ISA 540 and the proposed timeline

Timing―ISA 540, Including Audits of Financial Institutions

Page 22

• Monitoring of identified and emerging developments in audit, assurance and related services and provide recommendations to the IAASB on topics to be pursued– Data analytics and the effect on the audit, including whether ISAs

could be viewed as restricting innovation – Integrated reporting, including the demand for assurance on

integrated reports

• Services other than audits, in particular for SMEs– “Hybrid engagements” and how agreed-upon procedures may be

used in connection with other services, including the IAASB’s recently revised review and compilation standards

Preparing for the Future