pakko slides-2014

TRANSCRIPT

Dr. Michael PakkoChief Economist and State Economic ForecasterInstitute for Economic Advancement, UALR

The Arkansas Economic Outlook

October 15, 2014

Disclaimer: The views expressed are my own, and do not necessarily reflect the positions of the Federal Reserve Bank of St. Louis, the Federal Reserve System, the University of Arkansas at Little Rock, the University of Arkansas System, or the Institute for Economic Advancement.

Arkansas’ Experience

Source: Federal Reserve Bank of Philadelphia

Arkansas’ Experience

Source: Federal Reserve Bank of Philadelphia

Arkansas’ Experience

• By some measures, Arkansas is faring better than the rest of the nation

E.g., Personal Income, Proprietors’ Income, Dividends & Interest, etc.

• By other measures, Arkansas is lagging behindE.g., Employment, Wages and Salaries, Labor Force Participation

• Common element: Weak Labor Market Conditions(even weaker than we thought)

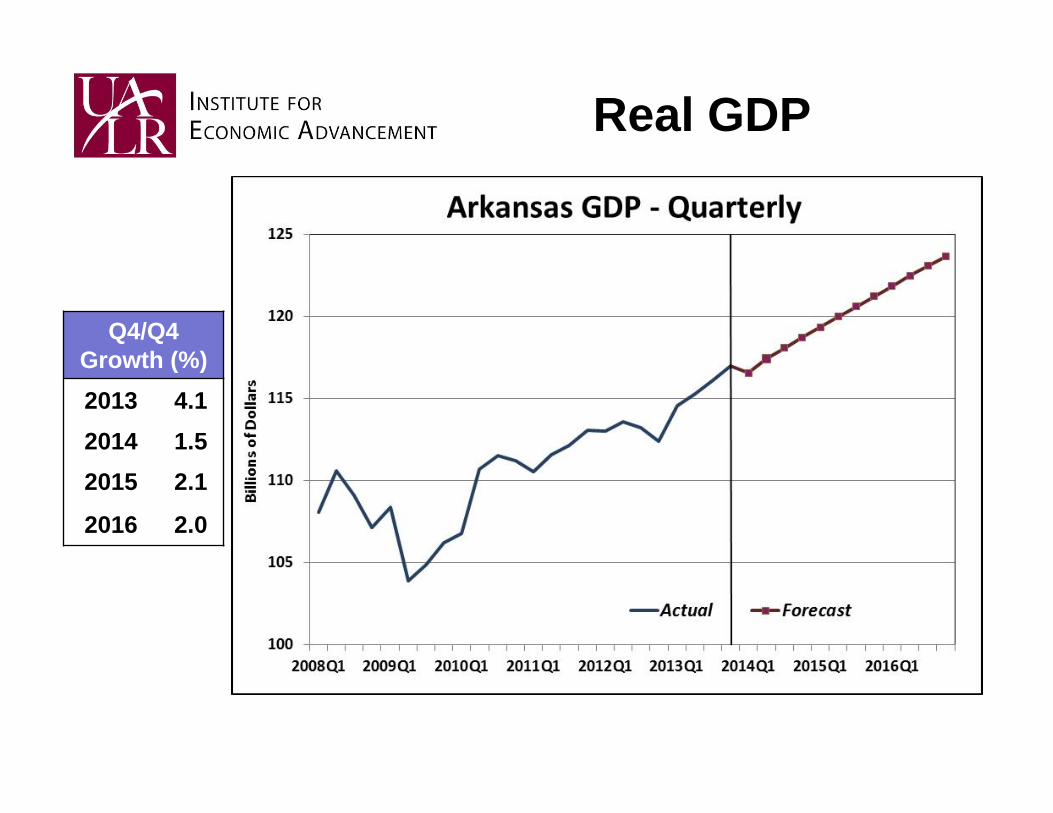

Gross Domestic Product

Source: Bureau of Economic Analysis

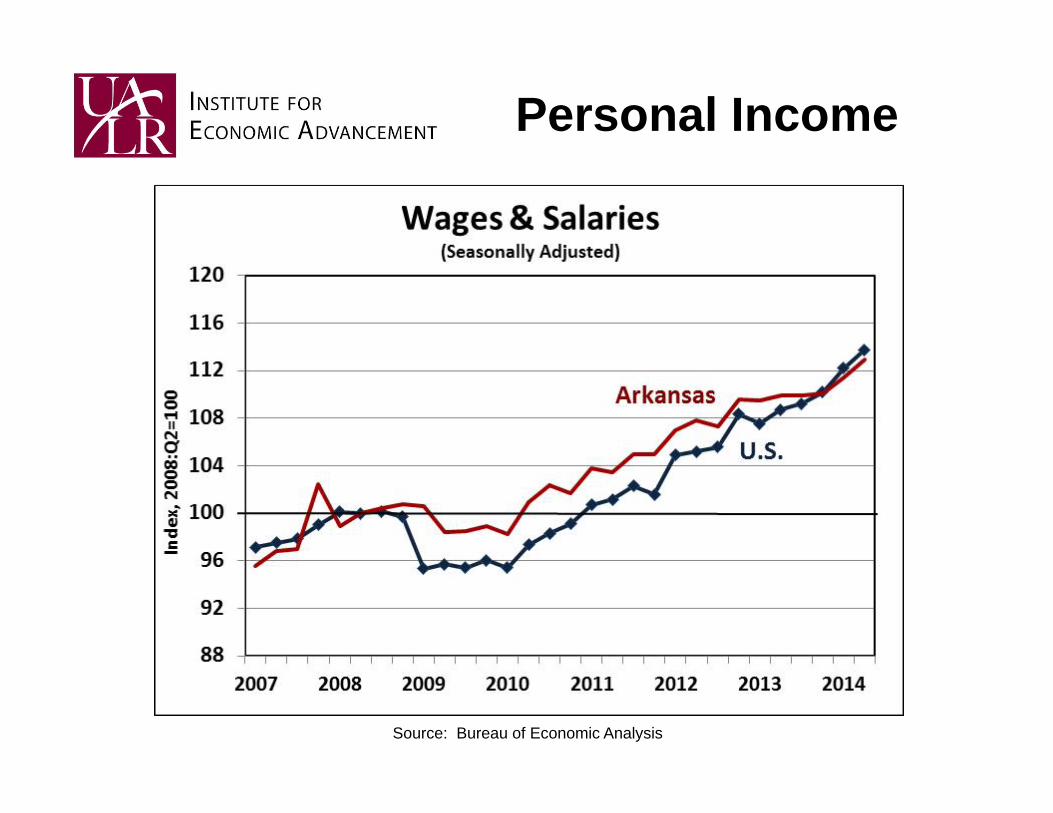

Personal Income

Source: Bureau of Economic Analysis

Personal Income

Source: Bureau of Economic Analysis

Personal Income

Source: Bureau of Economic Analysis

Personal Income

Source: Bureau of Economic Analysis

Personal Income

Source: Bureau of Economic Analysis

Taxable Sales

Sources: Arkansas Department of Finance and Administration, Oil Price Information Service, Institute for Economic Advancement.

Taxable Sales

Sources: Arkansas Department of Finance and Administration, Oil Price Information Service, Institute for Economic Advancement.

Taxable Sales

Sources: Arkansas Department of Finance and Administration, Oil Price Information Service, Institute for Economic Advancement.

Sources: Arkansas Realtors® Association, Institute for Economic Advancement.

Home Sales

Sources: Arkansas Realtors® Association, Institute for Economic Advancement.

Home Sales

Unemployment

Source: Bureau of Labor Statistics.

Unemployment

Source: Bureau of Labor Statistics.

52

54

56

58

60

62

64

2006 2007 2008 2009 2010 2011 2012 2013 2014

Percen

t

Employment/Population Ratios

U.S.

Arkansas

56

58

60

62

64

66

68

2006 2007 2008 2009 2010 2011 2012 2013 2014

Percen

t

Labor Force Participation Rates

U.S.

Arkansas

Unemployment

Source: Bureau of Labor Statistics.

Employment

Source: Bureau of Labor Statistics.

Employment

Source: Bureau of Labor Statistics.

Employment

Source: Bureau of Labor Statistics.

Employment

Source: Bureau of Labor Statistics.

Employment

Source: Bureau of Labor Statistics.

Economic Forecasts"Prediction is very difficult, especially about the future."

‐ Niels Bohr , Nobel prize‐winning physicist.

Forecast Methodology

Model: Arkansas Baseline from Moody’s Analytics.Part of a structural econometric model of the U.S. EconomyLinked to US forecast, with relationships estimated by sectorBaseline forecast from Moody’s macroeconomic U.S. model

Alternative Forecast Paths: Moody’sWells FargoWall Street JournalBlue Chip ConsensusNABE

Employment

Q4/Q4 Growth

2012 ‐0.9K‐0.8%

2013 +7.2K+0.6%

2014 +12.5K+1.1%

2015 +24.6K+2.1%

2016 +24.2K+2.0%

Employment

Q4/Q4 Growth

2012 ‐0.9K‐0.8%

2013 ‐2.4K‐0.2%

2014 +11.1K+0.9%

2015 +24.3K+2.1%

2016 +24.0K+2.0%

Including expectedrevision in 2015

Employment

Q4/Q4 Growth

2012 ‐0.9K‐0.8%

2013 +7.2K+0.6%

2014 +12.5K+1.1%

2015 +24.6K+2.1%

2016 +24.2K+2.0%

Q4/Q4 Growth

2012 ‐0.9K‐0.8%

2013 ‐2.4K‐0.2%

2014 +11.1K+0.9%

2015 +24.3K+2.1%

2016 +24.0K+2.0%

As Published

Expected Revision

Unemployment

End of Year (Q4)

2013 7.5

2014 6.0

2015 5.5

2016 5.3

Real GDP

Real GDP

Q4/Q4 Growth (%)2013 4.12014 1.52015 2.1

2016 2.0

Personal Income

Q4/Q4 Growth (%)2013 -1.92014 4.12015 5.4

2016 5.7

Retail Sales

Q4/Q4 Growth (%)

2013 1.12014 0.62015 5.4

2016 5.6

Home Sales

Sales(Pct. Change)

2012 23.3K‐0.2%

2013 25.7K10.1%

2014 27.8K8.4%

2015 30.6K9.9%

2016 32.4K6.0%

Arkansas EconomistFor more information and analysis of the Arkansas Economy,

visit the Arkansas Economist: www.arkansaseconomist.com