panel sponsored by - milken instituteassets1c.milkeninstitute.org/assets/events/conferences/...asia/...

TRANSCRIPT

2

Panel Sponsored by

3

Blazing New Trails, Battling Old Obstacles

• Biotech Industry Overview• Recent Financial Performance of the Biotech Industry • New FDA Initiatives• R&D Initiatives / Product Pipelines• IP & Patent Protection• Pharmacoeconomics / Reimbursement• Biotech and the Capital Markets• M&A / Consolidation Opportunities• Prognosis for the Biotech Industry

4

Global Biotechnology at a Glance

5324161,8791,4574,284Public and private companies

4413311,7751,1153,662Private companies9185104342622Public companies

Number of companies6,5187,00534,180141,000188,703Number of employees

(19)(507)(608)(4,799)(5,933)Net income ($m)1754744,24411,53216,427R&D expense ($m)

$1,001$1,021$7,533$25,319$34,874Revenues ($m)Public company data

Asia/Pacific

CanadaEuropeU.S.GlobalOctober 1, 2000 – Sept. 30, 2001

5

Share of Global Biotechnology Revenues (2002)

Asia / Pacific

3%

Canada3%

Europe22%

U.S.72%

6

1600

1400

1200

1000

800

600

400

200

0

Number of Biotech Companies

Top Biotech Countries (2002)

U.S.C

anad

a

Ger

man

y

U.K

.

Fra

nce

Au

stra

lia

Sw

eden

Isra

el

Sw

itze

rlan

d

Fin

lan

d

Th

e N

eth

erla

nd

s

Den

mar

k

7

500

400

300

200

100

0

Number of Biotech Companies

Top U.S. Biotech States (2001)

CaliforniaM

assa

chu

sett

s

Mar

ylan

d

No

rth

Car

olin

a

Pen

nsy

lvan

ia

New

Jer

sey

New

Yor

k

Was

hin

gto

n

Geo

rgia

Texa

s

Flo

rid

a

Co

lora

do

8

Market CapitalizationCompression upAggregate market cap for the number of companies shown in eachsegment ($B)

Compression downNumber of companies occupying each market cap segment

$0

$50

$100

$150

$200

$250

$300

<$200M $200-$400M

$400-$600M

$600-$800M

$800M-$1B

$1-$5B $5-$10B >$10B

Mar-00

Dec-02

0

50

100

150

200

250

<$50M $200-$400M

$600M-$800M

$1-$5B >$10B

Mar-00

Dec-02

141346 60 57 35 2329

11 12 7

67

22

11

7

11

2

9

Index Performance

40%

60%

80%

100%

120%

140%

160%

3/28/2001 9/28/2001 3/28/2002 9/28/2002 3/28/2003

NBI

Nasdaq

60%

70%

80%

90%

100%

110%

120%

3/28/2001 9/28/2001 3/28/2002 9/28/2002 3/28/2003

S&P 500

S&P 500 PharmIndex

I. Nasdaq Biotech Index vs. NasdaqComposite

II. S&P 500 vs. S&P PharmaIndex

10

2003200220012000

40

30

20

10

0

Aggregate Amount (US$ Billions)

$37.3

$16.2

$11.6

$1.7

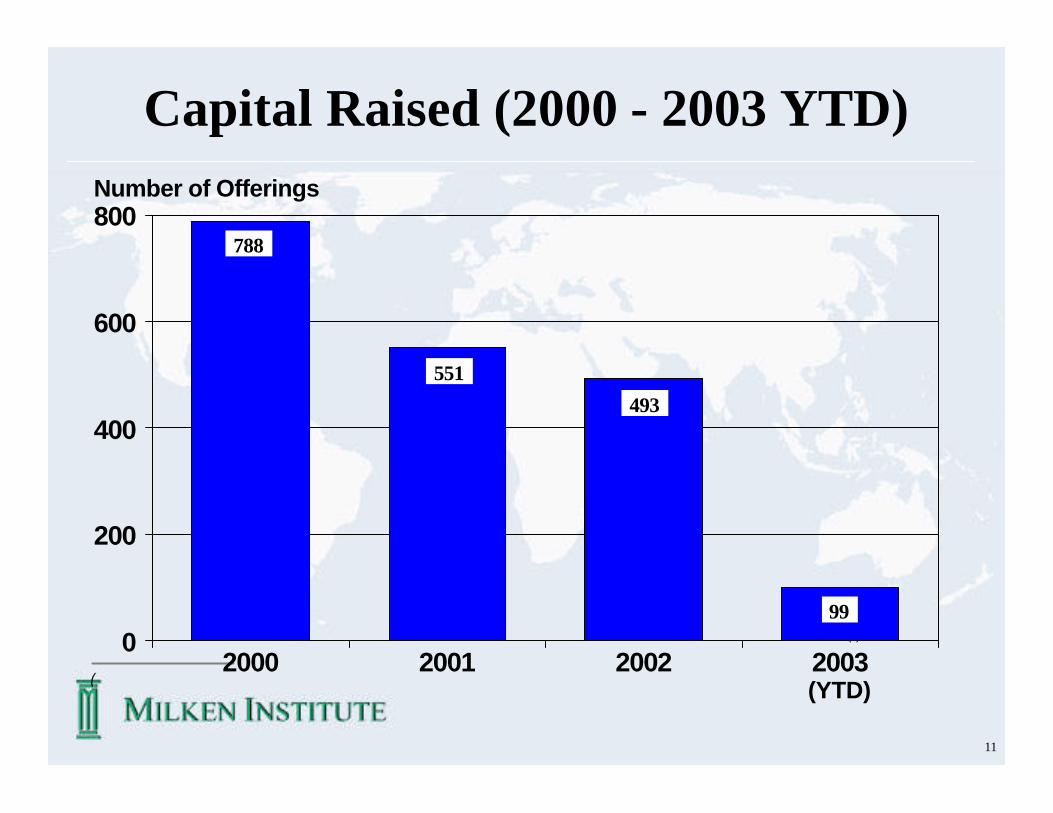

Capital Raised (2000 - 2003 YTD)

(YTD)

11

Capital Raised (2000 - 2003 YTD)

(

(1)

2003200220012000

800

600

400

200

0

Number of Offerings

788

551

493

99

(YTD)

12

2003200220012000

700

600

500

400

300

200

100

0

Number of Issuers

616

458421

99

Capital Raised (2000 - 2003 YTD)

(YTD)

13

Industry Overview• The industry has over 1,800 drugs in

development, including:– 98 new medicines for AIDS– 400 new medicines in development for cancer– 200 medicines in development for children– 120 new medicines of heart disease and stroke– 176 new medicines in development for neurological

diseases– 780 new medicines in development for older

individuals

Life Sciences Overview

14

• The industry has numerous tools and techniques to fight disease, including:– Monoclonal Antibodies– Vaccines– Interferon– Antisense drugs– Gene Therapies– Interleukins– Recombinant Soluble Receptors

Life Sciences Overview

15

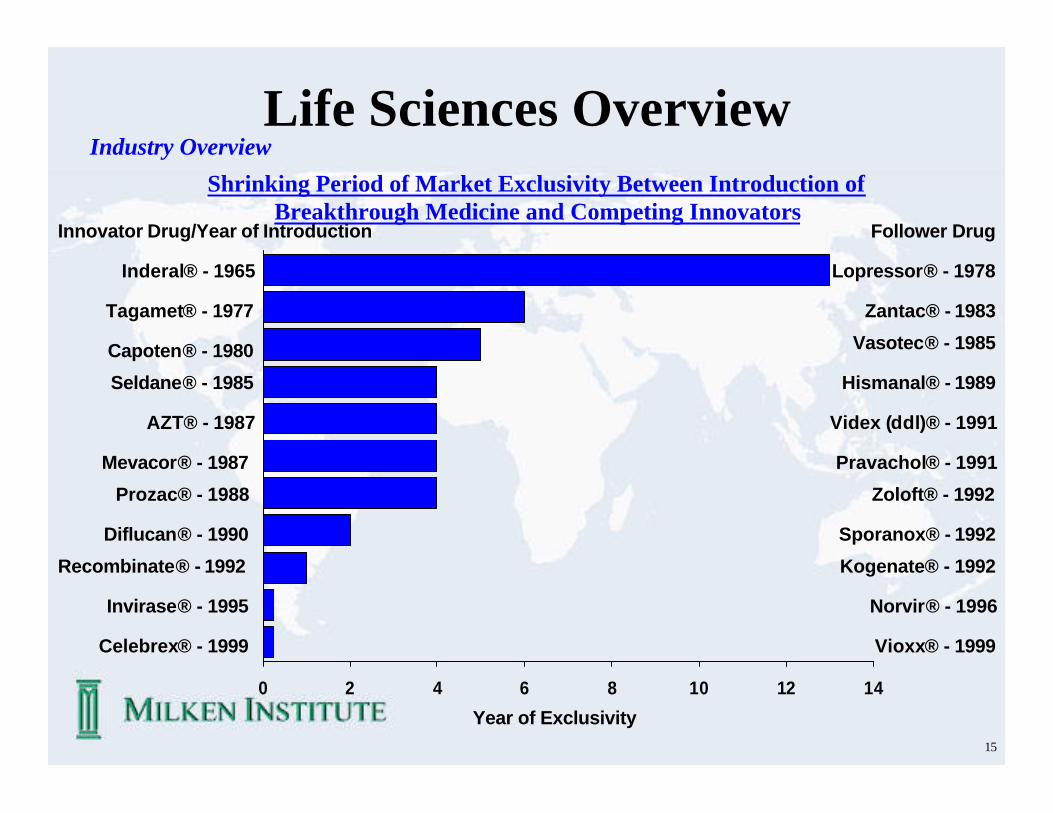

Life Sciences Overview

0 2 4 6 8 10 12 14

Inderal® - 1965

Tagamet® - 1977

Capoten® - 1980

Seldane® - 1985

AZT® - 1987

Mevacor® - 1987

Prozac® - 1988

Diflucan® - 1990

Recombinate® - 1992

Invirase® - 1995

Celebrex® - 1999

Lopressor® - 1978

Zantac® - 1983

Vasotec® - 1985

Hismanal® - 1989

Videx (ddl)® - 1991

Pravachol® - 1991

Zoloft® - 1992

Sporanox® - 1992

Kogenate® - 1992

Norvir® - 1996

Vioxx® - 1999

Follower DrugInnovator Drug/Year of Introduction

Year of Exclusivity

Industry Overview

Shrinking Period of Market Exclusivity Between Introduction of Breakthrough Medicine and Competing Innovators

16

Life Sciences OverviewIndustry Overview

• Access to approved drugs and pipelines is a critical success factor• Life science companies have increasingly used strategic alliances to

increase revenues

– Increasing Frequency of Strategic Alliances % of 2001 Revenues from Licensed Products

121

235 248 269319 324

428 415

480439

495

637 657 637

724

0

100

200

300

400

500

600

700

800

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

45

35 34

24

2018

16 16 15

10

0

5

10

15

20

25

30

35

40

45

50

ABT JNJ BMS PHA AVE AZN PFZ MRK GSK NOV

17

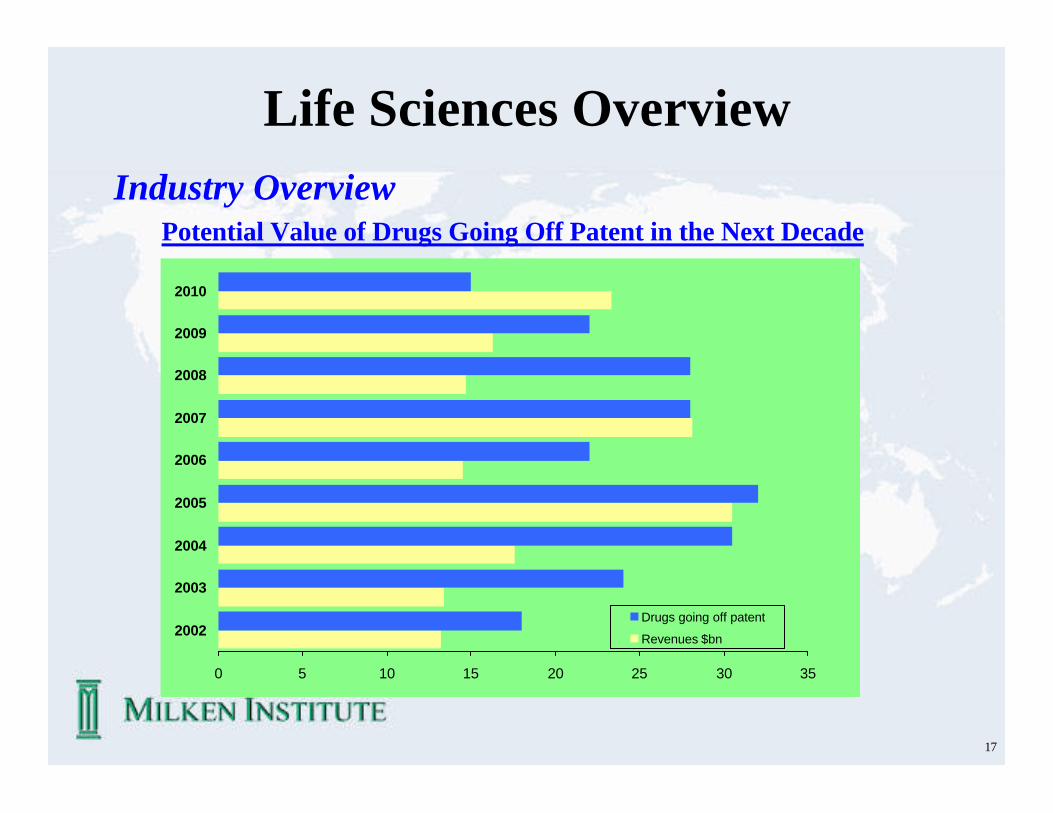

Life Sciences OverviewIndustry Overview

Potential Value of Drugs Going Off Patent in the Next Decade

0 5 10 15 20 25 30 35

2002

2003

2004

2005

2006

2007

2008

2009

2010

Drugs going off patent

Revenues $bn

18

2000199819961994199219901988

35

30

25

20

15

10

5

0

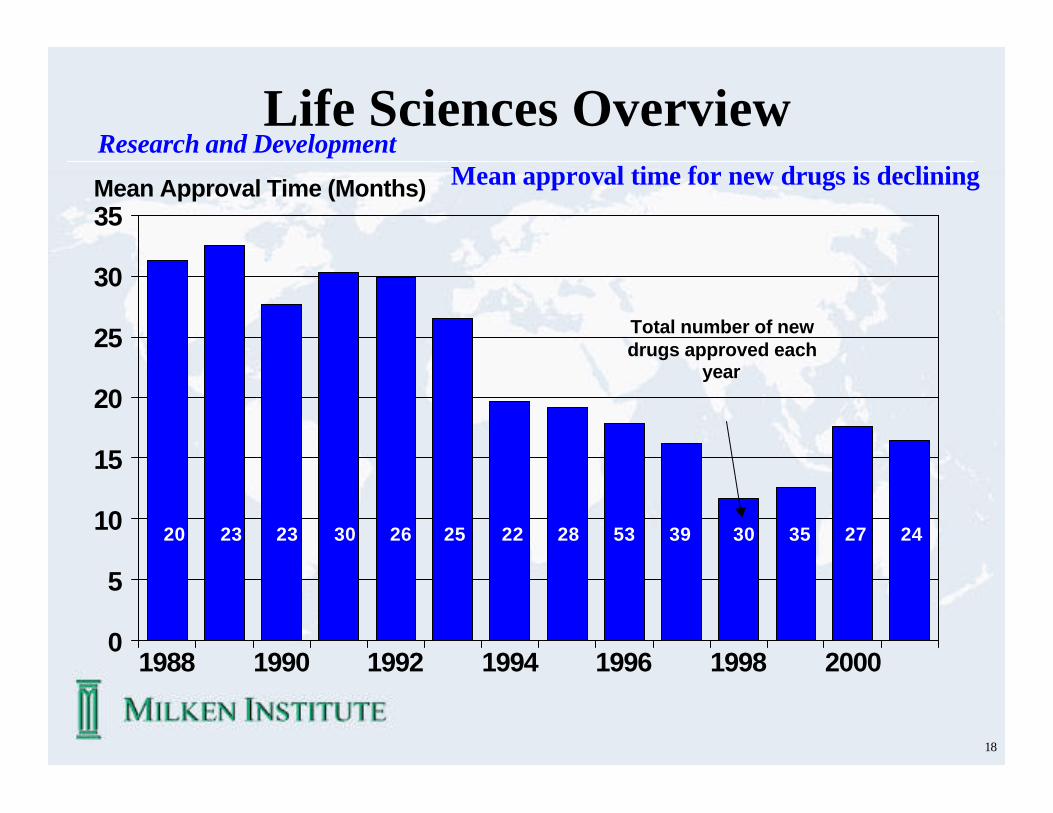

Mean Approval Time (Months)

Life Sciences OverviewResearch and Development

Mean approval time for new drugs is declining

Total number of new drugs approved each

year

20 23 23 30 26 25 22 28 53 39 30 35 27 24

19

Life Sciences Overview

•The pharmaceutical industry is the most research-intensive major industry in the United States•The industry spends over $30 billion in R&D – more than the $20 billion approximate operating budget of the NIH•R&D represents approximately 18% of sales•Average cost of developing a new drug is now more than $800 million•Four drivers of increased costs

–More complex diseases–High attrition rates–More demanding development requirements–Increasing scale and globalization

$54

$231

$802

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

1976 1987 2000

($ in Millions)

5.1 5.9 6.1

2.5

4.4

5.56.3

2.4

2.1

2.81.8

3.2

0

2

4

6

8

10

12

14

16

1960s 1970s 1980s 1990sApproval Phase Clinical Phase Preclinical Phase

Development Time (Years)

8.1

11.6

14.2 14.2

).

Research and Development

20

Rising R&D Yields Fewer Drugs

020098969492908886848280

60

50

40

30

20

10

0

24

20

16

12

8

4

0

Number Percent Change, Year Ago

New Drugs Approved - LR&D - R

21

Biotech Patents Granted in U.S.

U.S. Origin

Foreign Origin

0201009998979695949392919089

6

5

4

3

2

1

0

Number (000s)

22

New FDA Initiative

• Reducing review cycles– Deadlines for informing sponsors on deficiencies in NDAs and

BLAs• Improving quality, efficiency of reviews

– Enhanced reviewer training – Peer review process within FDA– Develop new standards for the review process

• New guidance documents– Cancer, diabetes, obesity– Emerging technologies focused on

• Cell and gene therapy• Pharmacogenomics• Novel drug delivery

23

New FDA Initiative

• Biodefense– “Operation Bioshield” – $6-8 billion earmarked for new products

• Biogenerics– Estrogens– Insulin– Human growth hormone– Liposomes

24

Approval WatchSelected Therapeutics Under Regulatory Review

Company Product Indication Status Partner

Alkermes Risperdal Consta Schizophrenia U.S. J&J

Atrix Leuprogel Advanced prostate cancer U.S./EU MediGene; Sanofi

Biogen Amevive Psoriasis U.S./EUBioMarin Aldurazyme Mucopolysaccharidosis I U.S./EU Genzyme

Corixa Bexxar Non-Hodgkin's lymphoma U.S. GIaxoSmithKline

Cubist Cidecin Complicated skin and skin structure infections

U.S.

CV Therapeutics Ranexa Chronic angina U.S.

Genelabs AnastarSystemic lupus erythematosus EU

Genentech Xolair Asthma U.S. Tanox, NovartisGenentech Raptiva Psoriasis U.S. XomaGenzyme Fabrazyme Fabry's disease U.S.Gilead Coviracil HIV/AIDS U.S.

Guilford Gliadel WaferNewly diagnosed malignant glioma

U.S.

Icos Cialis Erectile dysfunction U.S. Eli LillyMedimmune FIuMist Influenza Wyeth

Prevent chemotherapy-inducednausea and vomiting

Neurobiological Memantine Alzheimer's disease U.S.Forest; Lundbeck; Merz Oxford

Oxford GlycoSciences

Zavesca Gaucher’s disease U.S. Actelion

Pozen MT 100 Migraine EUPozen MT 300 Migraine U.S.

SuperGen OrathecinRefractory pancreatic cancer

U.S.

Transkaryotic Replagal Fabry's disease U.S.Trimeris Fuzeon HIV/AIDS U.S/EU Roche

Vertex GW433908 (VX-175) HIV/AIDS U.S. GIaxoSmithKline

MGI Pharma Palonosetron U.S. Helsinn

25

Upcoming MilestonesSelected Compounds with Data or Regulatory Submissions Expected in 2003

Indication Status Milestone Partner(s)Graft-versus-host disease Ph II/III Data I Q03 SangStatSpasticity in spinal cord injury

Ph III Data mid-03 Elan

Postoperative ileus Ph III Data I Q03 GIaxoSmithKline Brain metastases Ph III Data I H03; submit

NDA 2H03Type II diabetes Ph III Data I H03 AlkermesType I & 11 diabetes Approvable NDA amendment I

Q03 Kidney cancer, melanoma Ph III Interim data end of

03Non-Hodgkin's lymphoma Ph II/III Data I H03 InexVascular imaging with MRI Ph 111 Data spring 03; file

NDA 3Q03Pfizer

Wet age-related macular degeneration

Ph III Data 3Q03

Bristol-Myers;Merck KGaA

Dry eye PhIII Data IQ03Upper respiratory infection Ph III Data 2Q03Complicated skin and skin Ph III Data I H03 structure

infectionsNon-small cell lung cancer Ph III Data March 03 Eli LillyLupus nephritis Ph III Data early 03

Osteoporosis Ph III Data 03 Pfizer Multiple myeloma Ph III Submit NDA and

MAA early 03 Non-small cell lung cancer Ph III Results summer 03 Genentech; Roche Myelodysplastic syndrome Ph III Submit NDA 03Obesity Ph III Data early 03Insomnia Ph III File NDA Feb 03 AventisPulmonary arterial hypertension

Ph II/III Meet w/ FDA end Jan 03

Icos

Esophageal candidiasis Ph III Data I Q03; file NDA April 03

Merck data March 03

Colorectal cancer Refusal-to-file letter

26

Shareholder Value Creation

2 Products11 Clinical Molecules4 Franchises(NOL $300M 2003)

Founding1993

Breakeven Through

Product Sales2003-2005

5 Years Post Breakeven

20%+ Growth2006-2010

10 Years Post Breakeven

20%+ Growth2011

Crossing the Chasms

27

Class I: Truly Precedented(Drug Efficacious in Humans w/ Disease)

Class II: Cellular Pathway is “Validated”(in Humans w/ Disease by a Drug (IIA) or a Mutation (IIB)

Class III: Truly Unprecedented(Validation only in Animals and Human Cell/Tissue by Expression; Putative Mechanism Defined (IIIA) or Undefined (IIIB)

Levels of Precedence For Targets

28

New Biotech Drug and Vaccine Approvals

0200989694929088868482

35

30

25

20

15

10

5

0

Number

29

Number of U.S. Biotech Firms

2001200019991998199719961995199419931992

1600

1400

1200

1000

800

600

400

200

0

Number

30

U.S. Biotech IPOs

0200989694929088868482

70

60

50

40

30

20

10

0

Number

31

Cost and Benefit of Cancer Drugs

* Growth Colony Stimulating Factor

Without G-CSFWith G-CSF

85

80

75

70

65

60

55

50

US$ Thousands

G-CSF* reduces hospital costs for cancer patients

32

Cost and Benefit of Breast Cancer Anticancer Drug

Cost of SurgeryCost of Oral Anticancer Drug

14

12

10

8

6

4

2

0

US$ Thousands

33

Reduction in Labor Costs and Cost of Drug Treatment

500

400

300

200

100

0

Cost per Employee per Month

Decrease in Lost Productivity

Cost and Benefit of Migraine Medication

Migraine medication reduces employers’ labor costs and decreases lost productivity

34

Cost and Benefit of Chicken Pox Vaccination

Without VaccinationWith Vaccination

600

500

400

300

200

100

0

US$ Millions

Loss-of-Work Costs

Medical Costs

Vaccination reduces loss-of-work

35

Savings in ReducedTreatment Cost of

7

6

5

4

3

2

1

US$ Millions per 1,000 Treated Patients

Cost and Benefit of Clot-Busting Drug

Use of Clot-Busting Drug Reduces Patients’ Disability and Results in Net Savings to Health System

Clot-Busting Drug Patient Rehabilitationand Nursing-Home Costs

36

New Medicines in Development for AIDS

AntifungalsAnti-Infectives

ImmunomodulatorsVaccines

AIDS-Rel. CancerAntivirals

40

30

20

10

0

Number

37

New Medicines in Development for Cancer

ProstateSkinColonBreastLung

70

65

60

55

50

Number

38

New Medicines in Development for Children

0 5 10 15 20 25

Vaccines

Cardiovascular Disease

Infectious Bacterial Disease

Psychiatric Disorders

Cystic Fibrosis

Asthma

Skin Disorders

Neurologic Disorders

Genetic Disorders

AIDs and AIDS-Related Disorders

Number

39

New Medicines in Development for Heart Disease and Stroke

0 5 10 15 20

Stroke

Congestive Failure

Peripheral Vascular Disease

Hypertension

Adjunctive Therapies

Hyperlipidemia

Heart Attack

Number

40

New Medicines in Development for Neurologic Diseases

Migraine Stroke

Multiple SclerosisParkinson's

Alzheimer'sBrain Tumors

Pain

45

40

35

30

25

20

15

10

5

Number

41

New Medicines in Development for Older Americans

0 10 20 30 40 50

Parkinson’s Disease

Bladder/Kidney Disorders

Osteoporosis

Skin Conditions

Pain

Gastrointestinal Disorders

Depression

Alzheimer’s Disease/Dementias

Rheumatoid Arthritis

Diabetes

Respiratory/Lung Disorders

Number

42

Rising Cost of Developing a New Drug

200019871976

1000

800

600

400

200

0

US$ Millions

43

Growth in Ethical Pharmaceuticals’ Domestic R&D and R&D Abroad

Domestic

Abroad

00989694929088868482807876747270

25

20

15

10

5

0

US$ Billions

44

R&D Expenditures for Human-Use Pharmaceuticals

2001200019991998

100

80

60

40

20

0

Percent

DomesticAbroad

45

$10.9 Billion

$6.3 Billion

$3.5 Billion

$864 Million

$206 Million

2002*

$27.5 Billion

$0.4 Billion

$3.9 Billion

$15.9 Billion

$7.3 Billion

2000

$3.7 Billion

$11 BillionVenture

$7.0 Billion

$3.6 Billion

Other

$13.8 Billion

$21.4 Billion

Total

$2.8 Billion

$4.4 Billion

Follow Ons

$0.3 Billion

$2.4 Billion

IPOs

20011999

Investment in Biotechnology

46

Investment in Biotechnology

2002200120001999

16

14

12

10

8

6

4

2

0

US$ Billions

IPOS Follow OnsVenture Other

47

1H1032H1021H1022H1011H1012H1001H1002H991H99

25

20

15

10

5

0

30

24

18

12

6

0

US$ Billions Number

Number of Deals

Total Amount

(Adj.)

Merger Trends in the Biotech Industry(Announced Value and Number of Transactions)

48

$1.25 MillionNXY – 059

REN – 1654

Other Assets

$34 Million in Preferred Stock

Small But Important

49

Small But Important

$55.9 MillionAlfimeprase

50

$196 Million

Genomics Leader Branches Out Into Drug Discovery

51

2001 Mega Deals

$1.3 Billion $2 Billion

52

2002 Mega Mega Deal

$16 Billion

53

2003 Mega Deal

$2.4 Billion

54

NMEs/PLAs/BLAs: Trend in Number Approved Reflects Number Filed

2001200019991998199719961995199419931992

70

60

50

40

30

20

10

0

70

60

50

40

30

20

10

0

Approvals Number Filed

Approvals - L

Number Filed - R

55

Prescription Drugs Emerging With a Central Role in US Health Care

200019991998199719961995199419931992

3.0

2.5

2.0

1.5

1.0

0.5

0.0

Number of Dispensed Prescriptions (Billions)

56

1996 -19981991-1995

Prior, Foreign Marketing of New Drugs Approved in the US

US Patients Increasingly First to Have Access/Exposure to New Drugs

<1 yr prior mktg, 31%

U.S. 1st market, 47%

6-10 yrs prior mktg, 5%

>10 yrs prior mktg, 4%1-5 yrs prior

mktg, 14%

<1 yr prior mktg, 12%

U.S. 1st market, 31%

6-10 yrs prior mktg, 10%

>10 yrs prior mktg, 9%1-5 yrs prior

mktg, 37%

57

New Products Revenue Potential: 2003

• Risperdal Consta $500• Symlin $100m• Amevive $400m• Humera $2b• Xolair * $250m• Fabrazyme $150m• Hepsera $200m

• Cialis $500m• Flumist $450m• Iressa $350m • Xanelim * $200m• Palonosetron * $200m• Cidecin $300m• Fuzion (T-20) $300m

58

Genentech – Best Number of “Shots on Goal”

• Rituxan: Rheumatoid Arthritis• Xolair: Asthma• Xanelim (Raptiva): Psoriasis• Tarceva: NSCLC• Avastin: Colorectal Cancer• 2C4: Breast & Solid Tumors

59

Can You Generate a Return in Biotech???

• $5.8 Billion in Revenue Potential being Introduced to the Market during 2003!

• If You Believe the Street Research!!!

60

A Science-Driven Growth Industry

• Developing new drugs for human healthcare using novel technologies

• High-margin products protected by patents or market exclusivity

• Long R&D development phase (7-10 years)• High R&D expenses ($300MM+ per drug)• Regulatory hurdles

61

The Biotech Sector at a Glance

• Emerging Industry - solid fundamentals– Approximately 330 publicly-traded stocks– 70 biologics on the market

• 35 of these 70 approved in past three years

– 369 products in development; 175 in cancer– Vast majority of companies are unprofitable

62

Characteristics of Biotech Stocks

• Aggressive growth• High-risk, volatile stocks• Event-driven:

– Clinical results; regulatory events– Product launches– Product sales and earnings– Corporate collaborations

63

Investment Thesis

“Products and Pipeline” • Sector performance will be driven by

select stocks• Focus on companies with products on the

market or in late stages of development• Identify near-term events to drive price

appreciation

64

Investment Criteria

• Broadly-applicable proprietary technology

• Products address major markets• Experienced management team• Strong financial position• Corporate collaborations• Attractive valuation on a comparative

basis

65

Valuation Approach

• Forward P/E ratios– Hx.Average for the sector: 50-55x

• Forward P/E to growth rates (PEG)– Hx.Average for the sector: 2.0x

• Near-term events– New product approvals; significant clinical

data

66

New Drugs for Prostate Cancer

• Models to study• Learn biology• Targeted gene expression studies• Clinical trial endpoints

67

** As of 5/31/02

Capital Raised by Public Biotech Firms

020098969492908886848280

30

25

20

15

10

5

0

US$ Billions

68

Revenues for Selected Biotech FirmsGenentech, Amgen, Biogen, Chiron and Genzyme

0098969492908886848280

10

8

6

4

2

0

US$ Billions

69

U.S. Biotech IPOs

0200989694929088868482

70

60

50

40

30

20

10

0

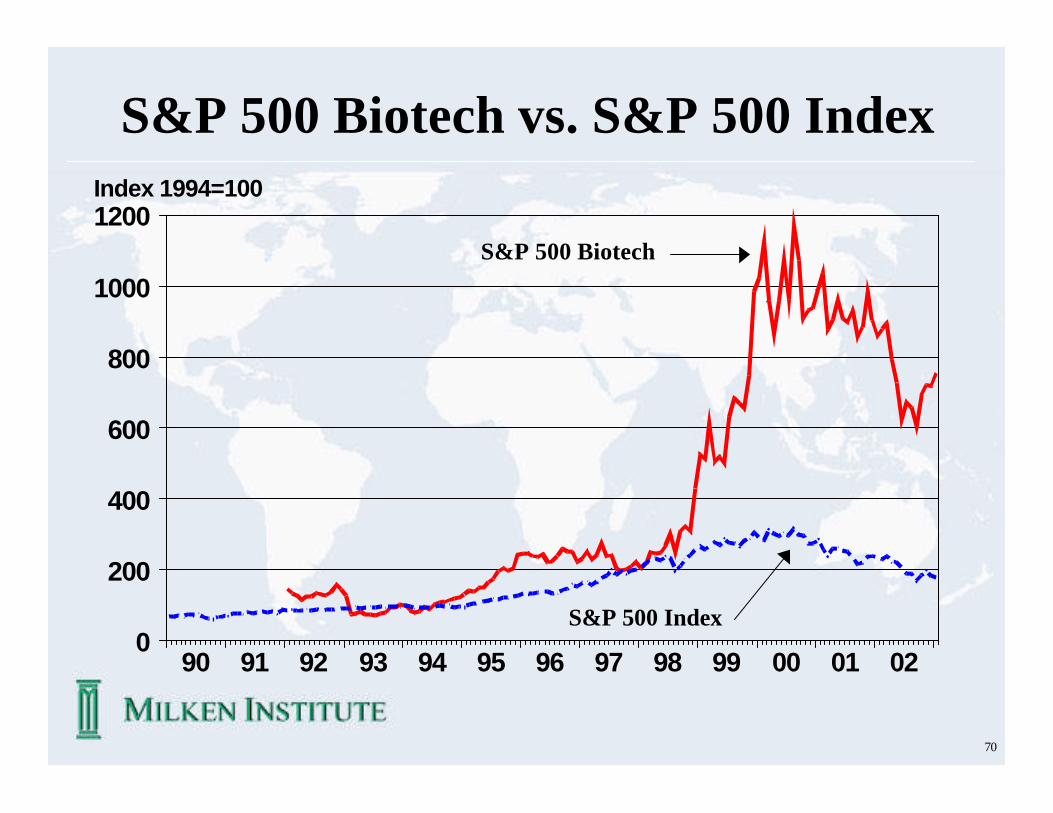

Number

70

02010099989796959493929190

1200

1000

800

600

400

200

0

Index 1994=100

S&P 500 Biotech vs. S&P 500 Index

S&P 500 Index

S&P 500 Biotech

71

Biotech Deals and Dollars Raised

2001200019991998199719961995199419931992

160

140

120

100

80

60

40

20

0

24

21

18

15

12

9

6

3

0

Number US$ Billions

Number of Deals - LAverage Amount Raised - R

72

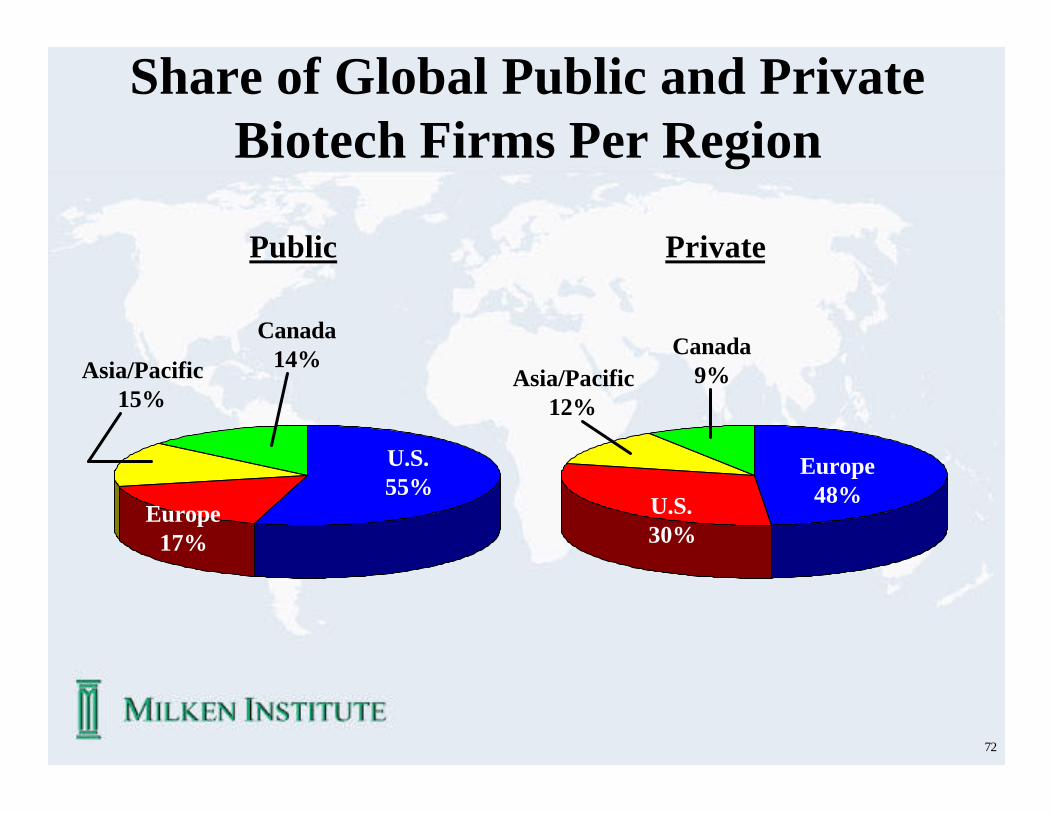

Share of Global Public and Private Biotech Firms Per Region

Asia/Pacific15%

U.S.55%

Europe17%

Canada14%

Asia/Pacific12%

U.S.30%

Europe48%

Canada9%

Public Private