panel unit root and cointegration methods

TRANSCRIPT

Panel unit root and cointegration methods

Mauro Costantini

University of Vienna, Dept. of Economics

Master in Economics

Vienna

2010

Mauro Costantini Panel unit root and cointegration methods

Outline of the talk (1)

Unit root, cointegration and estimation in time

series.

1a) Unit Root tests (Dickey-Fuller Test, 1979);

2a) Cointegration tests: single equation method

(Engle-Granger, 1987);

3a) Estimators: OLS, DOLS (Saikkonen, 1991), FMOLS

(Phillips and Hansen, 1990).

Mauro Costantini Panel unit root and cointegration methods

Outline of the talk (2)

Unit root, cointegration and estimation in panel

data.

1b) Limits of time series approach;

2b) Advantages and Disadvantages of the nonstationary panel

methods.

3b) First and second generation of panel unit root tests,

cointegration and estimation methods.

Mauro Costantini Panel unit root and cointegration methods

Time series unit root tests: regression equation (1)

yt = ρyt−1 + εt (1)

∆yt = βyt−1 + εt (2)

where β = (ρ− 1) and εt is white noise process

(E(ε) = 0,E(ε2t ) = σ2 < ∞,E(etej) = 0, for t 6= j). The test of

H0 : β = 0 (ρ = 1) has a non-standard distribution (Brownian or

Wiener process).

Mauro Costantini Panel unit root and cointegration methods

Asymptotic distribution of Dickey-Fuller tests (2)

Given t observation, the OLS estimator of ρ in (1) is:

ρ =

( T∑

t=1

y2t−1

)−1 T∑

t=1

ytyt−1 (3)

The limiting distribution of the OLS estimator ρ when ρ = 1 is:

T (ρ− 1) ⇒∫ 10 W (r)dW (r)∫ 1

0 W (r)2dr=

(1/2)[W (1)]2 − 1∫ 10 [W (R)]2dr

(4)

The previous distribution can be used for testing the unit root null

hypothesis H0 : ρ = 1, that’s K = T(ρ− 1) or we can normalize it

with the standard of the OLS estimator and construct the

t-statistics.

Mauro Costantini Panel unit root and cointegration methods

Asymptotic distribution of Dickey-Fuller tests (3)

The test statistics is:

tρ =(ρ− 1)

σρ=

(ρ− 1)

s2 ÷∑Tt=1 y2

t−11/2, (5)

where σρ is the usual OLS standard error for the estimated

coefficient and s2 denotes the OLS estimate of the residual

variance:

s2 =

∑Tt=1(yt − ρyt−1)

2

T − 1(6)

as T →∞,

tρ →∫ 10 W (r)dW (r)

[∫ 10 W (r)2dr ]1/2

=1/2[W (1)2 − 1][∫ 1

0 W (r)2dr ]1/2, (7)

Mauro Costantini Panel unit root and cointegration methods

Cointegration: concept (1)

An important property of I(1) variables is that a linear combination

of these two variables that is I(0) may exist. If this is the case,

these variables are said to be cointegrated. The concept of

cointegration was introduced by Granger (1981). Consider two

variables yt and xt that are I(1). Then yt and xt are said to be

cointegrated if there exist a β such that yt − βxt is I(0). We

denoted this as CI (1, 1). More generally, if yt is I(d) and and xt is

I(d), then yt and xt are CI (d , b) if yt − βxt is I (d − b) with b > 0.

Mauro Costantini Panel unit root and cointegration methods

Cointegration: concept (2)

What the previous concept means is that the regression equation:

yt = βxt + µt (8)

makes sense since yt and xt do not drift too far apart each other

over time. Thus, there is a long run equilibrium relationship

between them (see the geometric interpretation of cointegration

below). If yt and xt are not cointegrated, that is yt − βxt = µt is

also I(1), then yt and xt would drift apart from each other over

time. In this case, the relationship between yt and xt that we

obtain by regressing yt on xt would be spurious.

Mauro Costantini Panel unit root and cointegration methods

Cointegration: graphics (1)

Nominal interest rate on a 20 year US saving and loan credit instrument (R20) and AAA Moodys bond rate (R30)

Mauro Costantini Panel unit root and cointegration methods

Cointegration: geometric interpretation (4)

Suppose pit > pjt , demand will go to location j : i.) Shocks to the

economy make us to move out of the equilibrium; ii.) The

adjustment does not have to be instantaneous but eventually; iii.)

Long run equilibrium pit = pjt , this us a linear attractor

45°

1 1 1( )i jp p 2

1 1( )i jp p

3

3 3( )i jp p

4

5

it jtp pjtp

itp

Mauro Costantini Panel unit root and cointegration methods

Cointegration Tests: Engel and Granger model (1)

Consider two series y1t ∼ I(1), y2t ∼ I(1) and a simple

two-equation model:

y1t = βy2t + u1t , u1t = u1t−1 + ε1t , (9)

y1t = αy2t + u2t , u2t = ρu2t−1 + ε2t , |ρ| < 1 (10)

The second equation describes a particular combination of the

series which is stationary. Hence y1t and y2t are C(1,1). The null

hypothesis is taken to be no co-integration or ρ = 1 in (10).

Mauro Costantini Panel unit root and cointegration methods

Cointegration Tests: Engel and Granger model (2)

1. The cointegrating equation (10) is estimated by OLS and the

residuals are saved.

2. Several tests on the residual are provided (i.e. Durbin-Watson,

Dickey-Fuller and Augmented Dickey-Fuller). If the residuals

are nonstationary, the series are no cointegrated. Otherwise,

the series are cointegrated.

For examples, if the residuals are nonstationary, the DW test will

approach to zero and thus the test rejects no co-integration

hypothesis if DW is too big.

Mauro Costantini Panel unit root and cointegration methods

Cointegration Tests: Engel and Granger model (3)

Consider again y1t and y2t that are both I(1). Suppose there is

cointegration, that’s ut in (10) is I(0) and α is the cointegrating

vector (for the case of two variables, scalar). If there is

cointegration, we can show that α is unique. Because, if we have

y1t = γy2t + v2t where v2t is also I(0), by substraction we have

(α− γ)y2t + u2t − v2t is I(0). But u2t − v2t is I(0) which means

(α− γ)y2t is I(0). This is not possible since y2t is I(1).

Mauro Costantini Panel unit root and cointegration methods

Cointegration Tests: Engel and Granger model (4)

The equation-system (9-10), can be re-written in reduced as

follows:

y1t =α

α− βu1t − β

α− βu2t (11)

y2t =1

α− βu1t − 1

α− βu2t (12)

These equation show that both y1t and y2t are driven by a

common I(1) variable. This is known as the common trend

representation of the cointegrated system.

Mauro Costantini Panel unit root and cointegration methods

OLS estimator (1)

If the variables in (10) are not cointegrated, ρ = 1, then the OLS

is quite likely to produce spurious results (high R2, t-statistics that

appear to be significant), but the results are without economic

results (if the residuals have a stochastic trend, any error in period

t never decays, so that the deviation from the model is permanent.

It’s hard to imagine attaching any importance to an economic

model having permanent errors).

Mauro Costantini Panel unit root and cointegration methods

OLS estimator (2)

Stock (1987) show that OLS estimator is superconsistent: α

converge to its true value at the rate T(superconsistency) instead

of the usual rate√

T (consistency). Although α is superconsistent,

Banerjee et al. (1986) and Banerjee et al. (1993) show that

through Monte Carlo studies that there can be substantial sample

biases (the dynamic is missed). This missing information also

causes the DF test in the Engle-Granger approach to be less

powerful than the cointegration test based on the t-statistics in the

Error Correction model (ECM)

Mauro Costantini Panel unit root and cointegration methods

OLS estimator and the dynamic model (ECM)(1)

Consider the following ADL(1,1) model:

yt = α0 + α1yt−1 + β0zt + β1zt−1 + εt (13)

where εt ∼ iid(0, σ2) and |α1| < 1. In a statistic equilibrium (all

changes has ceased), we have E (yt) = E (yt−1) = ... = y∗ and

E (zt) = E (zt−1) = ... = z∗.

Mauro Costantini Panel unit root and cointegration methods

OLS estimator and the dynamic model (ECM)(2)

By getting the expectation of (13), we have:

y∗ = α0 + α1y∗ + β0zt + β1z

∗ (14)

and then

y∗ =α0 + (β0 + β1)z

∗

1− α1≡ k0 + k1z

∗ (15)

or

E (yt) = k0 + k1E (zt) (16)

where k1 is the long-run multiplier of y with respect to z.

Mauro Costantini Panel unit root and cointegration methods

OLS estimator and the dynamic model (ECM)(3)

Now subtract yt−1 from both side of (13) and then add and

subtract β0zt−1 on the right-hand side to get:

∆yt = α0 + (α1 − 1)yt−1 + β0∆zt + (β0 + β1)zt−1 + εt (17)

and finally add and subtract (α1− 1)zt−1 on the right side, yielding

∆yt = α0+(α1−1)(yt−1−zt−1)+β0∆zt+(β0+β1+α1−1)zt−1+εt

(18)

Mauro Costantini Panel unit root and cointegration methods

OLS estimator and the dynamic model (ECM)(4)

Alternatively, we could have added and subtracted (β0 + β1)zt−1

on the right side, to get

∆yt = α0 + (α1 − 1)(yt−1 − k1zt−1) + β0∆zt + εt (19)

where (α1 − 1) represents the short-run adjustment to a

’discrepancy’ (a measure of the speed of adjustment of y to a

discrepancy between y and z in the previous period).

Mauro Costantini Panel unit root and cointegration methods

Dynamic model and cointegration test (1)

Write in a different form (19) with no constant term:

∆yt = a∆zt + b(y − z)t−1 + εt (20)

The parameter b is the error correction coefficient. For yt = lnY

and z = lnZ , a denotes the short run-elasticity of Y with respect

to Z. Without loss of generality, the cointegrating vector for

(yt , zt)′is (1,-1) if yt and zt are cointegrated. We assume, for

simplicity, that the cointegrating vector is known.

Mauro Costantini Panel unit root and cointegration methods

Dynamic model and cointegration test (2)

The variable yt and zt are cointegrated, or not, depending on

whether b < 0 and b = 0. Thus, tests of cointegration rely on

upon some estimate of b. In ECM approach, equation (20) is

estimated by OLS

∆yt = a∆zt + bwt−1 + εt (21)

where the disequilibrium is:

wt = yt − zt (22)

The t-statistics based on b is the ECM statistics, tECM . It is used

to test the null hypothesis that b = 0, i.e, that yt and zt are not

cointegrated with cointegrating vector [1,-1].Mauro Costantini Panel unit root and cointegration methods

Dynamic model and cointegration test (3)

The DF statistics derives form a different regression, so it’s helpful

to establish the relationship between the DF regression equation

and the ECM in (20). Subtract ∆zt from both side of (20) and

re-arrange:

∆(y − z)t = b(y − z)t + [(a− 1)∆zt + εt ] (23)

Mauro Costantini Panel unit root and cointegration methods

Dynamic model and cointegration test (4)

It should be noted that (22) and (23) can be rewritten as:

∆wt = bwt + et (24)

where the disturbance et is

et = (a− 1)∆zt + εt ] (25)

Mauro Costantini Panel unit root and cointegration methods

Dynamic model and cointegration test (5)

OLS estimation of (24) generates:

∆wt = bwt + et (26)

The t-statistics based on b is the DF statistics, TDF . This statistics

is also used for testing whether yt and zt are cointegrated.

Mauro Costantini Panel unit root and cointegration methods

Dynamic model and cointegration test (6)

In contrast to the estimated ECM in (21), the estimated DF

equation (26) ignores potential information contained in ∆zt

Mauro Costantini Panel unit root and cointegration methods

OLS estimator, endogeneity and serial correlation

In addition, the asymptotic distribution of the OLS estimator

depends on nuisance parameters arising from endogenity of the

regressors and serial correlation in the errors. To solve these

problems, two estimators are proposed: FMOLS (fully modified

OLS) and DOLS (dynamic OLS)

Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (1)

Consider the following model:

yt = µ + β′xt + u1t = θ

′zt + u1t , (27)

∆xt = u2t , (28)

for t = 1, ..., T , θ = (µ, β′)′, zt = (1, x

′t)′. For ut = [u1t , u2t ], we

assume that the functional central limit theorem (FCLT) can be

applied as follows:

1√T

[Tr ]∑

t=1

⇒ W (r) =

W1(r)

W2(r)

(29)

for 0 ≤ r ≤ 1, where W (r) is a Brownian motion on [0, 1] with a

variance-covariance matrix Ω (W (·) ∼ BM(Ω)).Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (2)

Note that the long-run variance of ut and its one-sided version can

be expressed as Ω = Σu + Π + Π′

Λ = Σu + Π, with Σu = limT→∞

T−1∑T

t=1 E (utu′t) and

Π = limT→∞

T−1∑T−1

j=1

∑T−jt=1 E (utu

′t+j).

Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (3)

Ω and Λ can be conformably partioned with ut as:

Ω =

ω11 ω12

ω21 Ω22

Λ =

λ11 λ12

λ21 Λ22

Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (4)

It is known that the OLS estimator of θ, denoted by θ, is consistent

but inefficient in general. The centered OLS estimator with a

normalizing matrix DT = diag√

T , TIn weakly converges to

DT (θ − θ) ⇒( ∫ 1

0W2(r)W

′2(r)dr

)−1(∫ 1

0W2(r)dW1(r) + λ21

)

(30)

and we can observe that this limiting distribution contains the

second-order bias from the correlation between W1(·) and W2(·)and the non-centrality parameter λ21.

Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (5)

As explained in Phillips and Hansen (1990) and Phillips (1995),

the former bias arises from the endogeneity of the I(1) regressor xt

while the non-centrality bias comes from the fact that the

regression errors are serially correlated. Phillips and Hansen (1990)

argue that the second-order biases have no effect on the

consistency of the estimators, but result in asymptotic distributions

of scaled estimators, such as T (β − β) in (27), having non-zero

means.

Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (6)

In order to eliminate the second-order bias, Phillips and Hansen

(1990) proposes correcting the single-equation estimates

non-parametrically in order to obtain meadian-unbiased and

asymptotically normal estimates.

Mauro Costantini Panel unit root and cointegration methods

FMOLS estimator (6)

The Fully modified OLS is:

θ+ =

( T∑

t=1

ztz′t

)−1( T∑

t=1

zty+t − TJ+

)(31)

where the transformations:

y+t = yt − ω12Ω

−122 u2t (32)

and

J+ =

0

λ2 − Λ22ˆΩ−122 ω21

(33)

allows for correcting for the endogeneity bias and the

non-centrality bias.Mauro Costantini Panel unit root and cointegration methods

DOLS Estimator (1)

Contrary to nonparametric approach provided by Phillips and

Hansen, the DOLS method proposed by Saikkonen (1991) is based

on parametric regressions. Saikkonen proposes to augment the

leads and lags of the first difference of y2t as regressors and to

estimate

yt = θ′zt +

K∑

j=−K

π′j∆xt−j + u1t , (34)

Mauro Costantini Panel unit root and cointegration methods

DOLS Estimator (2)

The DOLS estimator is defined as the OLS of θ for (84)

θ′=

( T−K∑

t=K+1

zt z′t

)−1( T−K∑

t=K+1

zt y1t

)(35)

where zt and y1t are regression residuals of zt and yt on

wt = (u′2,t+K , ........, u

′2,t−K ), respectively.

Mauro Costantini Panel unit root and cointegration methods

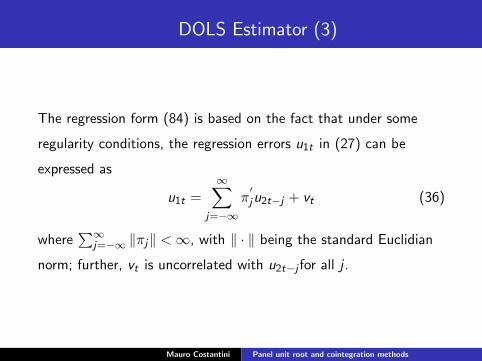

DOLS Estimator (3)

The regression form (84) is based on the fact that under some

regularity conditions, the regression errors u1t in (27) can be

expressed as

u1t =∞∑

j=−∞π′ju2t−j + vt (36)

where∑∞

j=−∞ ‖πj‖ < ∞, with ‖ · ‖ being the standard Euclidian

norm; further, vt is uncorrelated with u2t−j for all j .

Mauro Costantini Panel unit root and cointegration methods

DOLS Estimator (4)

From (36), we observe that

u1t =∑

|j |>K

π′ju2t−j + vt (37)

The uncorrelatedness of vt with all the leads and lags of u2t is an

important property to prove that the DOLS method successfully

eliminates the second-order bias of the OLS Estimator.

Mauro Costantini Panel unit root and cointegration methods

Some limits of time series approach

1. In time series analysis with unit root processes, many of the

estimators and statistics of interest have been shown to have

limiting distributions which are complicated functionals of

Wiener processes.

2. The power deficiencies of pure time series-based tests for unit

roots and cointegration .

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (1)

Finite sample properties

Monte Carlo simulations have shown that the power of the various

Dickey-Fuller and Phillips-Perron tests is very low; unit root tests

do not have power to distinguish between a unit root and near unit

root process (see Dickey and Fuller, 1997). Thus, these test will

too often indicate that a series contains a unit root. Moreover,

they have a little power to distinguish between trend stationary

and drifting processes. In finite sample, any trend stationary

process can be arbitrarily well approximated by a unit root process,

and a unit root process ca be arbitrarily well approximated by a

trend stationary process.

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (2)

Finite sample properties

Consider the following random walk plus noise model:

yt = µt + ηt (38)

µt = µt−1 + εt (39)

where ηt and εt are both independent white-noise process with

variance of σ2η and σ2, respectively. Suppose that we can observe

the yt sequence, but cannot directly observe the separate shocks

affecting yt.

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (3)

Finite sample properties

If σ2 6= 0, yt is the unit root process:

yt = µ0 +T∑

t=1

εt + ηt (40)

If σ2 = 0, then all values of εt are constant, that’s:

εt = εt1 = ... = ε0. Now, define this initial values of ε0 as a0. It

follows that

µt = µ0 + a0t

and yt is trend stationary:

yt = µ0 + a0t + ηt (41)

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (4)

Finite sample properties

The difference between the difference stationary process (40) and

trend process (41) concerns the variance of εt. Since we observe

the composite effect of the two shocks, but not the individual

components ηt and εt, we can see that there is no simple way to

determine whether σ2 is exactly equal to zero, in particular when

the Data Generating Process (DGP) is such that σ2η is large

relative to σ2. In a finite sample, arbitrarily increase σ2η will make

it virtually impossible to distinguish a TS and DS series.

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (5)

Finite sample properties

In addition, it also follows that a trend stationary process can be

arbitrarily well approximate a unit root process. If the stochastic

portion of the the trend stationary process has sufficient variance,

it will be not possible to distinguish between the unit root and the

trend stationary hypothesis.

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (6)

For example, the random walk plus drift model:

yt = a0 + yt−1 + εt ,

can be arbitrarily well represented by the model

yt = a0 + ρyt−1 + εt

by increasing σ2 and allowing ρ to be close to unity. Both these

models can be approximated by (41).

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (7)

For applications

It turns out that for tests of unit root hypothesis versus stationary

alternatives the power depends very little on the number of

observations per se but is rather influenced in an important way by

the span of the data. For a given number of observations, the

power is largest when the span is longest. For a given span,

additional observation obtained using data sampled more

frequently lead only to a marginal increase in power, the increase

becoming negligible as the sampling interval is decreased (Perron,

1990, JBES).

Mauro Costantini Panel unit root and cointegration methods

Low power of unit root tests (8)

In most applications os interest, a data set containing fewer annual

data over a long time period will lead to tests having higher power

than if use was made of a data set containing more observations

over a short time period. These results show that, whenever

possible, tests of unit root hypothesis should be performed using

annual data over a long time period.

Mauro Costantini Panel unit root and cointegration methods

Nonstationary Panel data

With the growing use of cross-country data over time to study

purchasing power parity, growth convergence and international

R&D spillovers, the focus of panel data econometrics has shifted

towards studying the asymptotics of macro panels with large

N(number of countries) and large T (length of the time series)

rather than the usual asymptotics of micro panels with large N and

small T. A strand of literature applied time series procedures to

panels, worrying about nonstationarity, spurious regression and

cointegration.

Mauro Costantini Panel unit root and cointegration methods

Why nonstationary panel data? Advantages...

1. The use of data from countries for which the span of time

series data is insufficient and would in this way preclude the

analysis of many economic hypothesis of interest;

2. The benefits coming from better power properties of the

testing procedure with respect to standard time series

technique;

3. The fact that many issue of economic interest, such as

convergence or purchasing power parity lend themselves

naturally to being analyzed in a panel framework;

4. Unit root and cointegration tests have Normal standard

asymptotic distribution.

Mauro Costantini Panel unit root and cointegration methods

...Disavantages (1)

1. Panel data generally introduce a substantial amount of

unobserved heterogeneity, rendering the parameters of the model

cross section specific;

2. The panel test outcomes are often difficult to interpret if the

null of the unit root or cointegration is rejected. The best that can

be concluded is that ”a significant fraction of the cross section

units is stationary or cointegrated”. The panel tests do not provide

explicit guidance as to the size of this fraction or the identity of

the cross section units that are stationary or cointegrated;

Mauro Costantini Panel unit root and cointegration methods

...Disavantages (2)

3. With unobserved I(1) common factors affecting some or all the

variables in the panel, it is also necessary to consider the possibility

of cointegration between the variables across the groups (cross

section cointegration) as well as within group cointegration;

Mauro Costantini Panel unit root and cointegration methods

...Disavantages (3)

4. Economic applications. For example, panel unit root tests are

not able to rescue purchasing power parity (PPP). The results on

PPP with panels are mixed depending ont the group of countries

studied, the period of study and the type of unit root test used. In

addition, for PPP, series. The null hypothesis of a single time

series is different from the null hypothesis of panel data, so the

panel data tests are the wrong answer to low power of unit root

tests in single time series.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root and cointegration methods: 1 generation

The common feature of first generation of nonstationary methods

is the restriction that all cross-sections are independent. Under this

independence assumption the Lindberg-Levy central limit theorem

or other central limit theorems can be applied to derive the

asymptotic normality of panel test statistics.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root and cointegration methods: 2 generation

The second generation panel methods relax the cross-sectional

independence assumption. In this context, the first issue is to

specify the cross-sectional dependencies, since as pointed out by

Quah (1994). The second problem is that cross-sectional

dependency is very hard to deal with in non-stationary panels. In

this case the usual t-statistics unit root tests have limit

distributions that are dependent in a very complicated way upon

various nuisance parameters defining correlations across individual

units. There does not exist any simple way to eliminate the

nuisance parameters in such systems, and a lot of different testing

procedures have been proposed.

Mauro Costantini Panel unit root and cointegration methods

First generation: Cross-section independent hypothesis

1. Unit root tests: Levin, lin and Chu (2002); Maddala and Wu

(1999) and Im, Pesaran and Shin (1997, 2003)

2. Cointegration tests: residual based tests (Kao, 1999, JE).

3. Estimation and inference: OLS, DOLS and Fully Modified

OLS (Kao and Chiang, 2000)

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests(1)

Homogeneous alternative:

Levin, lin and Chu (LLC) (2002).

Model specifications: yit is generated by one of the following

three models:

∆yit = δiyit−1 + ζit (42)

∆yit = α0i + δiyit−1 + ζit (43)

∆yit = α0i + α1i t + δiyit−1 + ζit , (44)

where −2 ≤ δ ≤ 0 for , i=1,....,N; t=1,....,T, and the errors, ζit are

distributed independently across individuals and follow a stationary

invertible ARMA process.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (2)

In Model 1, the panel unit root test procedure evaluates the null

hypothesis H0 : δ = 0 against the alternative H1 : δ < 0. The series

yi t has an individual-specific mean in Model 2, but does not

contain a time trend. In this case, the panel test procedure

evaluates the null hypothesis that H0 : δ = 0 and α0i = 0, for all i,

against H1 : δ < 0 and α0i ∈ R. Finally, under Model 3, the series

yi t has an individual-specific mean and time trend. In this case,

the panel test procedure evaluates the null hypothesis that

H0 : δ = 0 and α1i = 0, for all i, against the alternative H1 : δ < 0

and α1i ∈ R. LLC (2002) formulate a panel unit root test

procedure which consists of three steps.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (3)

In the first step, the ADF regressions for each individual in the

panel is carried out:

∆yit = δityit−1 +

Pi∑

L=1

θiL∆yit−L + αmidmt + εit (45)

where dmt denotes the vector of deterministic variables and αmi

indicate the corresponding vector of coefficients for the specific

model m (m ∈ 1, 2, 3).1

1The models are identified as follows: m = 1 denotes an ADF with no

constant and trend; m = 2 indicates an ADF with the constant term; m = 3

denotes an ADF with constant and trend.Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (4)

After having determined the order of the ADF regression, LLC run

two auxiliary regressions of ∆yit and yit−1 against ∆yit−L (with

L = 1, . . . , pi ), and generate two orthogonolized residuals, eit and

νit . To control for heterogeneity across individuals, LLC derive the

normalized residuals eit and νit by dividing by the standard error

form equation(6): eit = eitσεi

and νit−1 =νit−1

σεi.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (5)

The second step requires estimating the ratio of the long run to

short run innovation standard deviation, si =σyi

σεi, for each

individual. Finally, the pooled t-statistic is computed:

t∗ρ =tρ − NT SN σ−2

ε STD(ρ)µ∗mT

σ∗mT

(46)

where tρ is the t-statistic in the regression

eit = ρνit−1 + εit , (47)

SN is the estimated average standard deviation

ratio,SN = 1N

∑Ni=1 si , T is the time dimension,

STD(ρ) = σε[∑N

i=1

∑Tt=2+pi

ν2it−1]

− 12 , µ∗

mTand σ∗

mTare the mean

and the standard deviation adjustments.Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (6)

Using Lindberg-Levy central limit theorem and sequential limit

theory (T →∞ followed by N →∞), LLC(2002) obtain the

following limit distribution:

model tρ

1 tρ ⇒ N(0, 1)

2√

1.25tρ +√

1.875N ⇒ N(0, 1)

3√

448277

(tρ +

√3.75N

)⇒ N(0, 1)

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (7)

Heterogeneuos alternative: Im, Pesaran and Shin (1997, 2003)

IPS propose a test based on the average of the ADF statistics

computed for each individual in the panel. The IPS test is based on

∆yi ,t = αi+βiyi ,t−1+ΣKj=1δij∆yi ,t−1+ξi ,t , i = 1, 2, . . . , N; t = 1, 2, . . . , T .

(48)

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (8)

The null hypothesis of a unit root can be now defined as

H0 : βi = 0 for all i against the alternatives H1 : (βi < 0,

i = 1, 2, . . . ,N1 < N and βi = 0, i = N1 + 1, N2, . . . , N). The

alternative hypothesis βi may differ across cross-sectional units.

Formally we assume that under the alternative hypothesis the

fraction of the individual processes that are stationary is non-zero,

namely if limN→∞(N1/N) = δ, 0 < δ ≤ 1. This condition is

necessary for the consistency of the panel unit root tests.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (9)

The IPS test simply uses the average of the N ADF individual

t-statistics, tiT :

tNT =1

N

N∑

i=1

tiT (49)

from which

Zt =N

12 [tNT − E (tT )]

[Var(tT )]12

(50)

where E (tT ) and Var(tT ) are respectively the theoretical mean and

variance of tNT . The Zt statistic has an asymptotic standard

normal distribution under the null of a unit root.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (10)

Fisher’s Test: Maddala and Wu (1999)

MW (1999) proposed a new simple test based on Fisher’s

suggestion which consists in combining p-values from individual

unit root test. Let the p-value of τi be

pi = Pr(τ ≤ τi ) =

∫ τi

−∞f (x)dx (51)

where f (x) is the probability density function of x . The density

function of pi can be obtained by the method of transformation:

g(pi ) = f (τi )|J|, where J = dτidpi

is the Jacobian of the

transformation and |J| is its absolute value.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (11)

Since f (τi ) = dpidτi

, the Jacobian is 1f (τi )

and g(pi ) = 1 for

0 ≤ pi ≤ 1. In other terms, pi is uniformly distributed on the

interval [0, 1](pi ∼ U[0, 1]). Subsequently, we set yi = −2 ln(pi ) .

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (12)

By the method of transformation, the probability density function

of yi is h(yi ) = g(pi )|dpidyi|. Since g(pi ) = 1 and

|dpidyi| = pi

2 = 12e−

yi2 , then we get h(yi ) = 1

2e−yi2 which is the density

of a chi-square with two degrees of freedom. The joint test

statistic, under the null and the additional hypothesis of

cross-sectional independence of the errors terms εit in the ADF

equation, has a chi-square distribution with 2N degrees of freedom:

λ = −2N∑

i=1

ln(pi ) ∼ χ22N (52)

where N is the number of separate samples.

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests (13)

For the Fisher test, MW apply the ADF(p) test for each individual

series. Two models are estimated

∆yi ,t = αi + ρiyi ,t−1 +

p∑

j=1

γij∆yi ,t−j + εit ,

∆yi ,t = αi + δi t + ρiyi ,t−1 +

p∑

j=1

γij∆yi ,t−j + εit .

Mauro Costantini Panel unit root and cointegration methods

Panel Unit Root tests: theoretical considerations

I The IPS and Fisher tests relax the restrictive hypothesis

assumption of the LLC test that the autoregressive parameter

of yit−1 is the same under the alternative hypothesis;

I The Fisher test has the advantage over the IPS test in that it

does not require a balanced panel;

I The Fisher test can use different lag lengths in the individual

ADF regressions and can be applied to any other unit root

test. However, the Fisher test has disadvantage that the

p-values have to be derived by Monte Carlo simulations.

Mauro Costantini Panel unit root and cointegration methods

The size and the power of panel unit root tests: DGP (1)

The Theory and Practice of the Econometrics of Non-Stationary

Panels (Banerjee and Wagner, mimeo):

DGP 1

yit = αi (1− ρ) + ρyit−1 + uit (53)

uit = εit + cεit−1, (54)

with εit ∼ N(0, 1). The parameters chosen in the simulations are

α = [α1, ......., αN ], ρ and c. Note that the formulation of the

intercepts as αi (1− ρ) ensures that in the unit root case (when

ρ = 1) no drift appears.

Mauro Costantini Panel unit root and cointegration methods

The size and the power of panel unit root tests: DGP (2)

Consequently, when ρ = 1 α is equal to zero in the simulations for

computational efficiency. Otherwise, the coefficients αi are chosen

uniformly distributed over the interval 0 to 4, i.e. αi ∼ U[0, 4].

Mauro Costantini Panel unit root and cointegration methods

The size and the power of the panel unit root tests: DGP

(3)

DGP 2

yit = αi + αi (1− ρ)t + ρyit−1 + uit (55)

uit = εit + cεit−1, (56)

with εit ∼ N(0, 1). This formulation allows for a linear trend in the

absence of a unit root and for a drift in the presence of a unit root.

The coefficients αi are, as for the previous case, U[0,4] distributed.

Mauro Costantini Panel unit root and cointegration methods

The size and the power of the panel unit root tests: DGP

(4)

NOTE: The careful reader will have observed that our simulated

DGPs all have a cross sectionally identical coefficient ρ under both

the null and the alternative. Thus, we are in effect in a situation

where we generate data either under the null hypothesis or under

the homogenous alternative. We do this, because only the more

restrictive homogenous alternative can be used for all tests

described in the previous section. This implies to a certain extent

that we do not explore the additional degree of freedom that the

tests against the heterogeneous alternative (IPS and MW) possess.

Mauro Costantini Panel unit root and cointegration methods

The size of panel unit root tests

DGP 1.

a) c=0, T=10,15,20. LLC and MW tests are increasingly oversized

with N increasing. IPS test exhibit satisfactory size behaviour. For

T=50,100. LLC and MW also exhibit satisfactory size behaviour.

b) c=-0.99 (negative serial correlation). Size distortion for any

given T.

DGP 2.

a) c=0. T=10,15. Size distortion for LLC and MW (lesser rate).

T=25, only MW show size distortion.

b) Serially correlated errors (c ≥ −0.2). The size is below 0.1 for

LLC for any combination of N,T.

Mauro Costantini Panel unit root and cointegration methods

The power of the panel unit root tests

DGP 1. For ρ ≤ 0.9, N=10 and T ≤ 100 all test have power equal

to 1. For larger value of ρ ρ ∈ 0.95, 0.99, N ≤ 50 is required to

have power tending to 1 for T ≤ 100 (for both c=0 and c 6= 0).

DGP2. For ρ ≤ 0.9 and T ≤ 100, all test have power equal to 1

for all values of N.

Mauro Costantini Panel unit root and cointegration methods

Panel cointegration tests (1)

Homogeneous hypothesis

Kao (1999) proposes the Dickey-Fuller test and the Augmented

Dickey-Fuller (ADF). Let eit be the estimated residual from the

following regression:

yit = αi + βxit + eit (57)

Mauro Costantini Panel unit root and cointegration methods

Panel cointegration tests (2)

The equation (57) is estimated using LSDV (least square dummy

variable) estimator. The DF test is applied to the estimated

residuals:

eit = γeit−1 + νit (58)

The null hypothesis of no cointegration, H0 : γ = 1, is tested

against the alternative of cointegration for all i=1,....n

(Homogenous hypothesis).

Mauro Costantini Panel unit root and cointegration methods

Panel cointegration tests (3)

Kao (1999) proposed four DF-types tests:

DFγ =

√NT (γ − 1)√

10.2(59)

DFt =

√1.25tγ√1.875N

(60)

DF ∗γ =

√NT (γ − 1) +

(3√

Nσ2ν

σ20ν

)

√3 + 36σ4

ν

5σ40ν

(61)

Mauro Costantini Panel unit root and cointegration methods

Panel cointegration tests (4)

DF ∗t =

tγ +

(√6Nσν/2σ0ν

)

√(σ2

0ν/2σ2ν

)+

(3σ2

ν/10σ20ν

) (62)

While DFγ and DFt are based on the assumption of strict

exogeneity of the regressors with respect to the errors in the

equation, DF ∗γ and DF ∗t are for cointegration with endogenous

regressors.

Mauro Costantini Panel unit root and cointegration methods

Panel cointegration tests (5)

The ADF regression estimated is:

eit = γeit−1 +

p∑

j=1

φj∆eit−j + νit (63)

The ADF test is applied to the estimated residual: where p is

chosen so that the residual νi ,tp are serially uncorrelated. The

ADF test statistic is the usual t-statistic of the equation (63).

Mauro Costantini Panel unit root and cointegration methods

Panel cointegration tests (6)

With the null hypothesis of no cointegration, the ADF test

statistics can be constructed as:

ADF =tADF + (

√6Nσν2σ0ν

)√(

σ20ν

2σ2ν) + (10σ2

0ν)

(64)

where σ2ν = Σµε − ΣµεΣ

1ε, σ2

0ν = Ωµε − ΩµεΩ1ε, Ω is the long-run

covariance matrix and tADF is the t-statistic in the ADF

regression. Kao shows that all DF and ADF test converges to a

standard normal distribution N(0,1).

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (1)

homogeneity hypothesis (i.e. the variances are constant across the

cross-section units.)

Kao and Chiang (2000) analysed the asymptotic distributions for

ordinary least square (OLS), fully modified OLS (FMOLS), and

dynamic OLS (DOLS) estimators in cointegrated regression models

in panel data. They shows that the OLS, FOMLS, and DOLS

estimators are all asymptotically normally distributed.

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (2)

Kao and Chiang consider the following fixed-effect panel regression:

yit = αi + x′itβ + uit i = 1, ...,N, t = 1, ...,T , (65)

where yit are 1× 1, β is a k × 1 vector of the slope parameters,

αi are the intercepts, and uit are the stationary disturbance

terms.

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (3)

Kao and Chiang also assumed that xit are K × 1 integrated

processes of order one for all i, where

xit = xit−1 + εit .

Under these specifications, the previous equation defines a system

of cointegrated regressions, i.e. is cointegrated under the

hypothesis that yit and xit are independent across

cross-sectional units.

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (4)

The innovation vector is wit = (uit , εit). The long-run covariance

matrix, Ω, of wit , can be written as:

Ω =∞∑

J=−∞E (wi ,jwi ,0

′) (66)

= Σ + Γ + Γ′

(67)

=

Ωu Ωuε

Ωεu Ωε

. (68)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (5)

where

Γ =∞∑

J=−∞E (wijwi0) =

Γu Γuε

Γεu Γε

(69)

and

Σ = E (wijwi0) =

Σu Σuε

Σεu Σε

(70)

are partitioned conformably with wit .

Mauro Costantini Panel unit root and cointegration methods

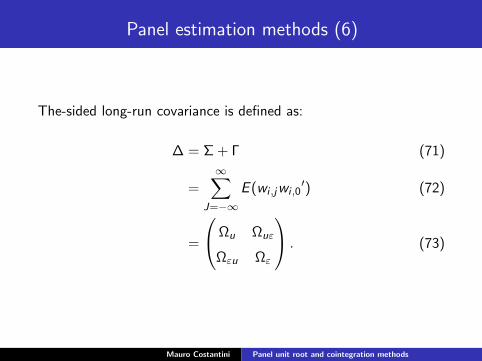

Panel estimation methods (6)

The-sided long-run covariance is defined as:

∆ = Σ + Γ (71)

=∞∑

J=−∞E (wi ,jwi ,0

′) (72)

=

Ωu Ωuε

Ωεu Ωε

. (73)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (7)

Kao and Chiang derived limiting distributions for the OLS, FMOLS

and DOLS estimators in a cointegrated regression. The OLS

estimator of is β is

βOLS = [N∑

i=1

T∑

t=1

(xit − xi )(xit − xi )′]−1[

N∑

i=1

T∑

t=1

(xit − xi )(yit − yi )]

(74)

where xi = 1T

∑Ti=1 xit and yi = 1

T

∑Ti=1 yit represent the

individuals means.

The FMOLS estimator is derived by making corrections for

endogeneity and serial correlations to the OLS estimator βOLS .

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (8)

Let

u+it = uit − ΩuεΩ

−1ε εit (75)

u+it = uit − ΩuεΩ

−1ε εit (76)

and

y+it = yit − ΩuεΩ

−1ε ∆it (77)

y+it = yit − ΩuεΩ

−1ε ∆it (78)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (9)

The endogeneity correction is achieved by modifying the variable

yit in (65), with the transformation:

y+it = yit − ΩεuΩ

−1ε ∆xit (79)

= αi + x′itβ − ΩεuΩ

−1ε ∆xit (80)

where Ωεu and Ωε are consistent estimates of Ωεu and Ωε.

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (9)

The serial correlation correction term takes the form:

∆+εu = (∆εu ∆−1

ε )

(1

ΩεuΩε

)(81)

= ∆εu − ∆εΩ−1ε ∆εu (82)

where ∆εu and ∆ε are kernel estimates of ∆εu and ∆ε .

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (10)

The FMOLS estimator is:

βFMOLS = [N∑

i=1

T∑

t=1

(xit− xi )(xit− xi )′]−1× [

N∑

i=1

( T∑

t=1

(xit− xi )y+it −T ∆+

εu)]

(83)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation methods (11)

The DOLS estimator can be obtained by running the following

regression:

yit = αi + x′itβ

q2∑

j=−q1

cit∆xit+j + νit (84)

Kao and Chiang (2000) showed that the asymptotic distributions

of the OLS, FMOLS and DOLS estimators are normal standard.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependence: Introduction(1)

The cross-sectional independence assumption is quite restrictive in

many empirical applications. More generally, this assumption raises

the issue of the validity of the panel approach in macroeconomic,

finance or international finance. For instance, the issue is to know

if it is useful to test the non-stationarity of the GDP of a particular

country, which is notably linked to the persistence of international

shocks, without considering the relationships between this GDP

and the GDP of the others countries which belong to the same

economic area. Since co-movements in national business cycles are

often observed (Backus and Kehoe, 1992), this issue is far from

being only a technical problem of power and size distortion.

Mauro Costantini Panel unit root and cointegration methods

... How does the independent tests work under a simple

form of cross-section dependence? (1)

Consider the following DGP:

∆yit = −φiµi + φiyit−1 + uit , (85)

The error term uit contains a time-specific effect θt and a specific

component εit : uit = θt + εit , where εit = λiεit−1 + eit .2

2The inclusion of time dummies (common time effect) appears to be a poor

control for cross-sectional dependence, for example, in testing for purchasing

power parityMauro Costantini Panel unit root and cointegration methods

... How does the independent tests work under a simple

form of cross-section dependence? (2)

We assume eit to be jointly normal distributed with:

E (eit) = 0, (86)

and

E (eit , ejs) =

σij for t=s

0 for t 6= s.(87)

Mauro Costantini Panel unit root and cointegration methods

... How does the independent tests work under a simple

form of cross-section dependence? (3)

If we let Σ denote (σij)Ni ,j=1 then non-zero terms on the

off-diagonal terms in Σ represents the existence of

cross-correlations.

Mauro Costantini Panel unit root and cointegration methods

... How does the independent tests work under a simple

form of cross-section dependence? (3)

Example: Σ, N = 2 and T = 3.

i , t 1,1 1, 2 1, 3 2, 1 2, 2 2, 3

1,1 σ21 0 0 σ12 0 0

1,2 0 σ21 0 0 σ12 0

1,3 0 0 σ21 0 0 σ12

2,1 σ12 0 0 σ22 0 0

2,2 0 σ12 0 0 σ22 0

2,3 0 0 σ12 0 0 σ22

Mauro Costantini Panel unit root and cointegration methods

... How does the independent tests work under a simple

form of cross-section dependence? (4)

In general, when there is no cross-sectional correlation in the

errors, the IPS test is slightly more powerful than the Fisher test,

in the sense that the IPS test has higher power when the two have

the same size. Both tests are more powerful than the LL test.

When the errors in the different samples (or cross-section units)

are cross correlated (as would often be the case in empirical work)

none of the tests can handle this problem well.

Mauro Costantini Panel unit root and cointegration methods

... How does the independent tests work under a simple

form of cross-section dependence? (5)

However, the Monte Carlo evidence suggests that this problem is

less severe with the Fisher test than with the LL or the IPS test.

More specifically, when T is large but N is not very large, the size

distortion with the Fisher test is small. But for medium values of T

and large N, the size distortion of the Fisher test is of the same

level as that of the IPS test.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS, cross-sectional

demean and bootstrap method. (1)

1. O’Connel (1998)

The distribution of ρ in LLC (2002) is derived under the

assumption that the variance-covariance matrix is diagonal (no

correlation).

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS, cross-sectional

demean and bootstrap method. (2)

Now, suppose that the correlation matrix taken the following form:

Ω =

1 ω ... ω

ω 1 ... ω

. . ... .

. . ... .

ω ω ... 1

(88)

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (3)

To define the GLS estimator of δi in (42), let Y be the following

matrix T × N

YT×N =

∆y11 ∆y21 ... ∆yN1

∆y12 ∆y22 ... ∆yN2

. . ... .

. . ... .

∆y1T ∆y2T ... ∆yNT

Similarly, let X be the T×N matrix of lagged yit .

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (4)

The GLS estimated of δi is given by:

δi GLS =tr(X

′Y Ω−1)

tr(X ′XΩ−1)(89)

The GLS estimator possesses an appealing feature that aids in the

interpretation of cross-country estimates of δi .

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (5)

Consider the Purchasing power parity. A basic intuition is that a a

set of real exchange rates generated by different choices of

numeraire are linear combinations of the one another. Thus

changing the numeraire does not change the information that is

used in the estimator, only its configuration (i.e its

interdependence). By nature, GLS controls for interdependence.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (6)

As a results, the GLS estimator is invariant to the linear

combination of the real exchange rates that is used as numeraire.

Its not necessary for Ω to be known for this to hold: invariance

carries over to the feasible GLS estimator

δi GLS =tr(X

′Y Ω−1)

tr(X ′X Ω−1)(90)

where Ω is some consistent estimates of Ω.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (7)

2. Cross-sectional demean.

Let yit be a balanced panel generated by (42) with

ζit = αi + θt + εt , where θt is a single common time effect. You

can control for the common time effect θt . If you do, you subtract

off the cross-sectional mean and the basic unit of analysis is

yit = yit − 1

N

N∑

j=1

yjt (91)

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (6)

Potential pitfalls of including common-time effect. Doing so

however involves a potential pitfall. θt , as part of the

error-components model, is assumed to be iid. The problem is that

there is no way to impose independence. Specifically, if it is the

case that each yit is driven in part by common unit root factor, θ is

a unit root process. Then

yit = yit−1 − 1

N

N∑

j=1

yjt

will be stationary. The transformation renders all the deviations

from the cross-sectional mean stationary.Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (7)

This might cause you to reject the unit root hypothesis when it is

true. Subtracting off the cross-sectional average is not necessarily

a fatal flaw in the procedure, however, because you are subtracting

off only one potential unit root from each of the N time-series. It

is possible that the N individuals are driven by N distinct and

independent unit roots. The adjustment will cause all originally

nonstationary observations to be stationary only if all N individuals

are driven by the same unit root.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (8)

3. bootstrap method

The method discussed here is called the residual bootstrap because

we resampling from the residuals. The DGP under the null

hypothesis is:

∆yit = µi +

Ki∑

j=1

φij∆yit−j + εit (92)

Since yt is a unit root process, its firs difference follows an

autoregression. The individual equations of the DGP can be fitted

by Least Squares. If a linear trend is included in the test equation

a constant must be included in (92).Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (9)

To account for dependence across cross-sectional units, estimate

the joint error covariance matrix Σ = E (εtε′t) by

Σ = 1T

∑Tt=1(εt ε

′t) where εt = (ε1t , ..., ˆεNT ) is the vector of OLS

residuals.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (10)

The parametric bootstrap distribution for τ (see (46)) is built as

follows.

1. Draw a sequence of length T + R innovation vectors from

ε ∼ N(0, Σ).

2. Recursively build up pseudo-observations yit , i = 1, . . . , N, t

= 1, . . . , T + R according to (92) with the εt and estimated

values of the coefficients µiand φij .

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panels: GLS (O’Connel, 1998),

cross-sectional demean and bootstrap method. (11)

3. Drop the first R pseudo-observations, then run the LLC test on

the pseudo-data. Do not transform the data by subtracting off the

cross-sectional mean. This yields a realization of τρ in (46)

generated in the presence of cross- sectional dependent errors.

4. Repeat a large number (2000 or 5000) times and the collection

of τρ statistics form the bootstrap distribution of these statistics

under the null hypothesis.

Mauro Costantini Panel unit root and cointegration methods

Cross-section dependent panel unit root tests: factor

models and cross-section averages methods

1. Test based on factors models: Bai and NG, 2004. For these

tests, the idea is to shift data into two unobserved components:

one with the characteristic that is strongly cross-sectionally

correlated (common factor) and one with the characteristic that is

largely unit specific (idiosyncratic component).

2. Test based on cross-section averages: Pesaran (2007). Instead

of basing the unit root tests on deviations from the estimated

common factors, he augments the standard Dickey Fuller or

Augmented Dickey Fuller regressions with the cross section average

of lagged levels and first-differences of the individual series.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (1)

1. Bai and Ng propose to test the common factors and the

idiosyncratic components separately. So, it is possible to know if

the non-stationarity comes from a pervasive or an idiosyncratic

source. Bai and Ng (2004) consider the following model

Yi ,t = Di ,t + λ′iFt + ei ,t , (93)

where Di ,t is a polynomial trend function, Ft is an r × 1 vector of

common factors, and λi is a vector of factor loading. The process

Yi ,t may be non-stationary if one or more of the common factors

are non-stationary, or the idiosyncratic error is non-stationary, or

both.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (2)

In order to test the non-stationarity of the common factors, Bai

and Ng (2004) distinguish two cases: only one common factor

among the N variables (r = 1) and more than one common factor

(r > 1).

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (3)

Among the r common factors, we allow r0 and r1 to be stochastic

common trends with r0 + r1 = r . The corresponding model in first

difference is:

∆yit = λ′i + zit (94)

where zit = ∆eit and f = ∆Fit with E (ft) = 0. Applying the

principal-components approach to ∆yit yields r estimated factors

ft , the associated loadings λt , and the estimated residuals,

zit = yit − λ′i ft .

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (4)

Define for t = 2....,T eit =∑t

s=2 zit (i=1,....N) Ft =∑t

s=2 zit , an

r × 1 vector.

1. If r = 1, let ADF Fe be the t statistics for testing δi0 in the

univariate augmented autoregression (with an intercept):

∆Fit = c + δ0Ft−1 + δ1∆et−1 + δp∆Fit−p + error (95)

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (5)

2. If r > 1, demean Ft and denote F ct = Ft − ¯Ft , where

¯Ft = (T − 1)−1∑T

t=2 Ft . Start with m = r :

A: β⊥ denotes the m eigenvectors associated with the m largest

eigenvalues of T−2∑T

t=2 F ct F c ′

t . Two different statistics may be

considered:

B.I: Let K (j) = 1− j(j+1) , j = 0, 1, ......J

i) Let ξct be the residuals from estimating a first-order VAR in Y c

t .

In addition, let∑c

1 =∑J

j=1 K (j)(T−1∑T

t=2 ξct−j ξ

c ′t )

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (6)

ii) Let vMc be the smallest eigenvalue of:

Φcc(m) = 0.5[

T∑

t=2

(Y ct Y c′

t−1 + Y ct−1Y

c′t )− T (Σc

1 + Σc′1 )](

T∑

t=2

Y ct Y c′

t−1)−1

(96)

iii) Define MQcc (m) = T [νc

c (m)− 1].

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (7)

B.II: For p fixed that does not depend on N and T

i) Estimate a VAR of order p in ∆Y ct to get

∏(L) = Im −

∏1L− ....− ∏

pLp and filter Y ct by

∏(L), we have:

y ct =

∏(L)Y c

t

ii) Let νcf (m) be the smallest eigenvalue of:

Φfc(m) = 0.5[

T∑

t=2

(y ct y c′

t−1 + y ct−1y

c′t )](

T∑

t=2

y ct y c′

t−1)−1 (97)

iii) Define the statistics MQcf (m) = T [νc

f (m)− 1].

C: If H0 : r1 = m is rejected, set m = m − 1 and return to step A.

Otherwise, r1 = m and stop.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (8)

To test the stationarity of the idiosyncratic component, Bai and

Ng (2004) propose to pool individual Augmented Dickey-Fuller

(ADF ) t-statistics with de-factored estimated components eit in

the model with no deterministic trend

∆ei ,t = δi ,0ei ,t−1 +

p∑

j=1

δi ,j∆ei ,t−j + µi ,t . (98)

Let ADF ce (i) be the ADF t-statistic for the i-th cross-section unit.

The asymptotic distribution of the ADF ce (i) coincides with the

Dickey-Fuller distribution for the case of no constant. However,

these individual time series tests have the same low power as those

based on the initial series.Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: factor models (9)

Bai and Ng (2004) propose pooled tests based on Fisher type

statistics defined as in Choi (2001) and Maddala and Wu (1999).

Let Pce (i) be the p-value of the the ADF t-statistics for the i-th

cross-section unit, ADF ce (i), then the standardized Choi’s type

statistics is:

Z ce =

−2∑N

i=1 log Pce (i)− 2N√

4N. (99)

The statistics (99) converge for (N, T →∞) to a standard normal

distribution.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: cross-section averages methods,

Pesaran (2007) (1)

Pesaran proposed to augment the standard DF (or ADF)

regression with the cross section averages of lagged levels and

first-differences of the individual series.

If residuals are not serially correlated, the regression used for the

ith country is defined as:

∆yit = αi + ρiyi ,t−1 + ci yt−1 + di∆yt + eit . (100)

where yt−1 = (1/N)∑N

i=1 yit−1 and ∆yt = (1/N)∑N

i=1 ∆yit

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: cross-section averages methods (2)

Let us denote ti (N, T ) the t-statistic of the OLS estimate of ρi .

The Pesaran’s test is based on these individual cross-sectionally

augmented ADF statistics, denoted CADF. A truncated version,

denoted CADF∗, is also considered to avoid undue influence of

extreme outcomes that could arise for small T samples.

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: cross-section averages methods (3)

In both cases, the idea is to build a modified version of IPS t-bar

test based on the average of individual CADF or CADF∗ statistics

(respectively denoted CIPS and CIPS):

CIPS(N, T ) = N−1N∑

i=1

ti (N, T ) (101)

CIPS∗(N, T ) = N−1N∑

i=1

t∗i (N, T ) (102)

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: cross-section averages methods (4)

where the truncated CADF statistics is defined:

t∗i (N, T ) =

K1 if ti (N, T ) ≤ K1

ti (N, T ) if K1 < ti (N,T ) < K2

K2 if ti (N, T ) ≥ K2

(103)

The constants K1 and K2 are fixed such that the probability that

ti (N, T ) belongs to [K1, K2] is near to one. In a model with

intercept only, the corresponding simulated values are respectively

-6.19 and 2.61

Mauro Costantini Panel unit root and cointegration methods

Panel unit root tests: cross-section averages methods (5)

Pesaran consider also the case of serially correlated residuals. For

an AR(p) error specification, the relevant individual CADF

statistics are computed from a pth order cross-section/time series

augmented regression:

∆yit = αi + ρiyi ,t−1 + ci yt−1 +

p∑

j=0

di ,j∆yt +

p∑

j=0

βi ,j∆yit−j + µit .

(104)

Mauro Costantini Panel unit root and cointegration methods

Cointegration tests: cross-section dependence(1)

Gengenbach, Palm and Urbain (2006) propose the following

testing procedure which consist of two steps:

1. A preliminary PANIC analysis on each variable Xi ,t and Yi ,t to

extract common factors is conducted. Tests for unit roots are

performed on both the common factors and the idiosyncratic

components using by Bai and Ng (2004) procedure.

Mauro Costantini Panel unit root and cointegration methods

Cointegration tests: cross-section dependence (2)

2. a) If I(1) common factors and I(0) idiosyncratic components are

detected, then a situation of cross-member cointegration is found

and consequently the non-stationarity in the panel is entirely due

to a reduced number of common stochastic trends. Cointegration

between Yi ,t and Xi ,t can only occur if the common factors for Yi ,t

cointegrate with those of Xi ,t .

b) If I(1) common factors and I(1) idiosyncratic components are

detected, then defactored series are used. In particular, Yi ,t and

Xi ,t are defactored separately. Testing for no-cointegration

between the defactored data can be conducted using standard

panel tests for no cointegration such as those of Pedroni’s (1999,

2004) unit root tests.Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (1)

Bai and Kao (2006) consider the following fixed-effect panel

regression:

yit = αi + x′itβ + eit i = 1, ...,N, t = 1, ...,T , (105)

where yit are 1× 1, β is a k × 1 vector of the slope parameters,

αi are the intercepts, and eit are the stationary disturbance

terms. They assumed that xit is K × 1 integrated processes of

order one for all i, where

xit = xit−1 + εit .

Under these specifications, the previous equation defines a system

of cointegrated regressions, i.e. yit is cointegrated with xit .Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (2)

To model for cross-sectional dependence, Bai and Kao (2006)

assume that the error term follows a factor model (Bai and NG,

2006):

eit = λ′iFt + µit , (106)

where Ft is a r × 1 vector of common factor a, λi is a r × 1 vector

of factor loadings and uit is the idiosyncratic component of eit ,

which means:

E (eitejt) = λ′iE (FtF

′t )λj , (107)

i.e. eit and ejt are correlated due to the common factors Ft .

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (3)

The OLS estimator of β is :

βOLS =

[ N∑

i=1

T∑

t=1

yit(xit − xi )′][ N∑

i=1

T∑

t=1

(xit − xi )(xit − xi )′]−1

(108)

As regards the limiting distribution, we have:

√nT

(βOLS − β

)−√nδnT ⇒ N

(0, 6Ω−1

ε AΩ−1ε

)(109)

as (n,T →∞), with nT → 0,

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (4)

where

A = limn→∞

1

n

n∑

i=1

(λ′iΩF .εiλiΩεi + Ωµ.εiΩεi

)

and

δnT =1

n

[ n∑

i=1

λ′i

(ΩFεiΩ

1/2εi

(∫WidW

′i

)Ω−1/2εi + ∆Fεi

)+

ΩµεiΩ1/2εi

(∫WidW

′i

)Ω−1/2εi + ∆µεi

]×

[1

n

N∑

i=1

T∑

t=1

1

T 2(xit − xi )(xit − xi )

′]−1

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (5)

and

Wi = Wi −∫

Wi , andΩε = limn→∞

1

n

n∑

i=1

Ωεi

and

Ωi =

ΩFi ΩFµi ΩFei

ΩµFi Ωµi Ωµεi

ΩεFi Ωεµi Ωεi

(110)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (6)

The FMOLS estimator of β is constructed by modifying the

variable yit in (105)

y+it = yit −

(λ′iΩFεi + Ωµεi

)Ω−1

εi ∆xit (111)

The serial correlation correction term takes the form:

∆+bεi = ∆bεi − ΩbεiΩ

−1εi ∆εi =

∆+

Fεi

∆+µεi

(112)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (7)

The infeasible estimator is:

βFM =

[ N∑

i=1

( T∑

t=1

y+it (xit − xi )

′ − T

(λ′i∆

+Fεi + ∆+

Fεi

))]

[ N∑

i=1

T∑

t=1

(xit − xi )(xit − xi )′]−1

(113)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (8)

The limiting distribution of the infeasible estimator is:

√nT

(βFM − β

)⇒ N

(0, 6Ω−1

ε CΩ−1ε

)(114)

as (n, T →∞), with nT → 0,

where

A = limn→∞

1

n

n∑

i=1

(λ′iΩF .εiλiΩεi + Ωµ.εiΩεi

)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence (9)

The feasible FMOLS is obtained by substituting λi , Ft , σi and Ωi ,

with λi , Ft , σi and Ωi , The asymptotic distribution is:

√nT

(βFM − βFM

)⇒ 1

n√

T

n∑

i=1

( t∑

i=1

e+it (xit − xi )

′)− T ∆+

bεn

)−

( t∑

i=1

e+it (xit − xu)

′)− T∆+

bεn

)

=

[1

n√

T

n∑

i=1

( t∑

i=1

(e+it − e+

it )(xit − xi )′)− T (∆+

bεn −∆+bεn

)]

[1

nT 2

n∑

i=1

t∑

i=1

(xit − xi )(xit − xi )−1

]−1

(115)

as (n,T →∞), with nT → 0,Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence

(10)

In the literature, the FM-type estimators usually were computed

with a two-step procedure, by assuming an initial consistent of β,

say βOLS . Then, one can constructs estimates of the long-run

covariance matrix, Ω(1), and loading, λ(1)i . The 2S-FM, denoted by

β2S , is obtained using Ω(1) and λ(1)i :

β(1)2S =

[ N∑

i=1

( T∑

t=1

y+(1)it (xit − xi )

′ − T

(λ′(1)i ∆

+(1)Fεi + ∆

+(1)Fεi

))]

[ N∑

i=1

T∑

t=1

(xit − xi )(xit − xi )′]−1

(116)

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence

(10)

Bai and Kao (2006) propose the CUP-FM estimator. The

CUP-FM estimator is constructed by estimating parameters,

long-run covariance matrix an loading recursively. Thus βFM , Ω(1)

and λ(1)i are estimated repeatedly, until convergence is reached.

Mauro Costantini Panel unit root and cointegration methods

Panel estimation: cross-sectional dependence

(11)

The CUP-FM estimator is defined as:

βCUP =

[ N∑

i=1

( T∑

t=1

y+(1)it (βCUP)(xit − xi )

′

−T

(λ′i

(βCUP

)∆+

Fεi

(βCUP

)+ ∆+

Fεi

(βCUP

)))]

[ N∑

i=1

T∑

t=1

(xit − xi )(xit − xi )′]−1

(117)

Mauro Costantini Panel unit root and cointegration methods