paper 1: accounting - icai knowledge gateway · accounting standards ca shruthi bn ... methods of...

TRANSCRIPT

Accounting StandardsC A S h r u t h i B N

Paper 1: Accounting

Contents:

AS 6 AS 10 As 9

AS – 6 Depreciation Accounting

DEPRECIATION – Meaning It is a measure of wearing out, consumption or other loss of value

of a depreciable asset arising from use and passage of time.

Depreciable AssetsThey are those assets which are: Are expected to be used for more than one accounting period Have a limited useful life Are held for use in production of goods and services

2

Applicability of AS 6

AS 6 is not applicable to the following: Forests, Plantations Wasting Assets, Minerals and Natural gas Expenditure on R&D Goodwill Live stock

3

Calculation of Depreciation

Depreciation = Historical cost/revalued amount –Estimated scrap value of depreciable assets

Estimated useful life of depreciable assets

Cost of depreciable assets is the total cost spent in connection with its acquisition, installation and commissioning. Estimated useful life is the period over which it is expected to be used by the enterprise. Generally useful life is shorter than physical life. Estimated scrap value is the price fetched when the depreciable asset is sold or scrapped at the end of its useful life.

Depreciable Amount = Historical cost/revalued cost –estimated scrap value

4

Methods of Depreciation

As Per AS6 Straight Line Method and Written down value method

Selection of appropriate method depends on Type of asset Nature of the use of such asset Circumstances prevailing in the business, etc.

5

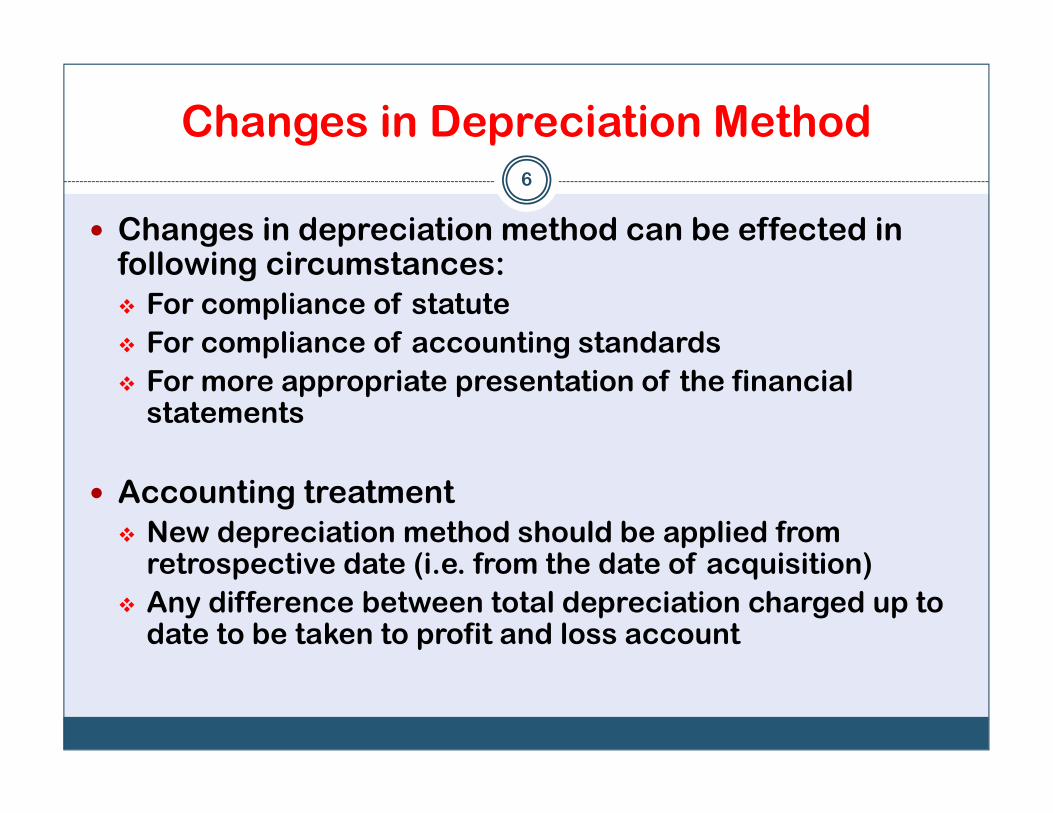

Changes in Depreciation Method

Changes in depreciation method can be effected in following circumstances: For compliance of statute For compliance of accounting standards For more appropriate presentation of the financial

statements

Accounting treatment New depreciation method should be applied from

retrospective date (i.e. from the date of acquisition) Any difference between total depreciation charged up to

date to be taken to profit and loss account

6

Change in Estimated Useful life

Such changes to be given prospective effect in the books of account

Change in estimated useful life Outstanding depreciable amount on the date of change to be

allocated over revised useful life of assets

Example P/M has useful life of 5 yrs. Depreciable amount is Rs 40 lakhs.

The company has charged SLM depreciation . At the end of 6th

year, the balance useful life was re-estimated at 8 years.

Depreciation charge from 7th year = 40 – 40/10*6 = 2

8

7

Change in Historical Cost and Estimated Scrap Value

Change in the historical cost may occur due to revaluation, price adjustment, etc.

Increase or decrease in historical cost is added/ deducted from the outstanding depreciable amount on the date of change.

Such adjusted depreciable amount is allocated over remaining useful life of the depreciable asset

Above principle has to be applied for change in estimated scrap value

8

Depreciation Charge on Addition/ Extensionto an Existing Asset

Addition/extension If addition/extension is an integral part of existing asset, then it is

depreciated over the remaining useful life of the existing asset In a reverse case, it is depreciated over the estimated useful life of

additional assets.

When the depreciable asset is discarded, demolished or destroyed book value after netting off sale proceeds to be debited/ credited to profit and loss account.

9

Disclosure

Accounting policy with respect to depreciation

Total cost of each class of assets, depreciation for the period and accumulated depreciation

Following disclosure is given in the balance sheet:Gross block of fixed assets XXX

Less: Accumulated depreciation XXX

Net block of fixed assets XXX

Depreciation method and rated/useful life

Change in depreciation method

10

Question No. 1

What would need to be done in books of account for change in the depreciation method?(a) Effect of change in depreciation method to be provided

prospectively(b) Retrospective effect to be given for such change from

the date of acquisition of the asset(c) No effect to be given in the books(d) Change in the depreciation method is not possible as

the method chosen first should be applied consistently from period to period

11

Question 1 Answer

Answer: (b)

12

Question No. 2

ABC Ltd uses horses to transport material from one place to another place on hilly area for construction activity. It purchases horses worth Rs 80,000 for transporting material on 1.4.2010. Useful life of horses was estimated at 5 years, therefore company decided to write off depreciation on horses as per SLM over 5 years as per AS 6. Whether the treatment is correct?(a) Yes(b) No(c) Can’t say

13

Question 2 Answer

Answer : (b)

14

Question No. 3

A plant was depreciated under two different methods as under-

If the company followed WDV for first four years and decides to switch over to SLM, what would be the amount of resultant surplus/deficiency?(a) Deficiency of 13.15 to be debited to profit and loss account(b) Deficiency of 13.15 to be credited to profit and loss account(c) Surplus of 13.15 to be debited to profit and loss account(d) Surplus of 13.15 to be credited to profit and loss account

Year SLM WDV

1st year 3.9 10.69

2nd year 3.9 7.9

3rd year 3.9 5.84

4th year 3.9 4.32

Total 15.60 28.75

5th year 3.9 3.19

15

Question 3 Answer

Answer : (d)

16

Question No. 4

Can land be depreciated?(a) Yes, as it is a fixed asset(b) No

17

Question 4 Answer

Ans: (b) as land is not a depreciable asset and may not satisfy the conditions laid out for depreciable assets (i.e. does not have a limited useful life)

18

AS 10 - Accounting for Fixed Assets

Fixed assets – Meaning

It is an asset which is Held with intention of being used for the purposes of producing or

providing goods and service Not held for sale in the normal course of business Expected to be used for more than one accounting periodExamples: land and building, plant, machinery, furniture, etc.

This accounting standard is not applicable to the following items Forests, plantations and similar regenerative natural resources Wasting assets like minerals Expenditure on real estate development Live stock

19

Fixed Assets – Measurement

Fixed assets can be accounted at Historical cost/ Revalued price

Historical Cost includes Purchase price Import duties and non-refundable duties Directly attributable cost of bringing the asset to the

working condition for its intended use such as delivery and handling cost, installation and commissioning charges, architect’s fees, price adjustments, etc

20

Historical Cost for Self Constructed Assets

Historical cost includes All costs which are directly related to the specific assets All attributable costs to the construction activity Any internal profit included in the cost should be

eliminated

21

Cost of the Asset Acquired in Exchange of Existing Assets

Scenario 1: Fixed assets exchanged are not similar Assets acquired should be recorded at either fair market value

of the asset given up or fair market value of the asset acquired, which ever is more clearly evident.

Scenario 2: Fixed assets exchanged are similar Assets acquired should be recorded at either fair market value

of the asset given up or fair market value of the asset acquired, if this is more clearly evident or net book value of the asset given up

Scenario 3: fixed assets acquired in exchange of shares or other securities Assets should be recorded at either fair market value of asset

purchased or fair market value of shares or securities, whichever is clearly available.

22

Revaluation of Fixed Assets –Accounting Treatment

First time upward revaluation Fixed asset account ….. Dr Revaluation Account …. Cr

First time downward revaluation Profit and loss account … Dr Fixed assets account … Cr

23

Revaluation of Fixed Assets –Accounting Treatment

First time downward revaluation and subsequent upward revaluation First time – Same as before Subsequent upward revaluation :

Fixed assets account … Dr Profit and loss account… Cr (only to the extent of amount written in first

time downward revaluation) Revaluation reserve account … Cr (for the balance amount)

First time upward revaluation and subsequent downward revaluation First time – same as before Subsequent downward revaluation:

Revaluation reserve account .. Dr (only to the extent of balance available with respect to the asset being revalued first time)

Profit and loss account … Dr (for balance amount or full amount) Fixed asset account … Cr

24

Special circumstances

Assets acquired on hire purchase To be recorded at cash price. Recording will be done as

per AS 19

Jointly held assets Cost of the asset to be recorded proportionate to the

right entity has to utilize the asset

Fixed assets acquired at consolidated price Cost of each asset to be determined on a fair basis as

per valuation by competent valuers.

25

Other matters

Improvements or repairs to fixed assets to be added to the cost of fixed assets if there is an increase in the expected future benefits from the assets, else charged to profit and loss account

Addition or extension to an existing fixed asset If it forms an integral part, the cost to be added to the gross

block of existing assets, else to be accounted separately.

Profit or loss on disposal/retirement of assets to be taken to profit and loss account.

26

Disclosure

Gross and net book values at the beginning and end of the financial year

Expenditure on construction of fixed assets Revalued amount

27

Question No 5

A company has purchased plant and machinery in the year 2007-08 for Rs 45 lakhs. A balance of Rs 5 lakh is still payable to the suppliers for the same. The supplier waived off the balance amount during the financial year 20010-11. What is the correct treatment of Rs 5 lakh?

(a) Treat it as income and credit it to profit and loss account. (b) As there is no cash flow involved, Rs 5 lakh need not be

accounted (c) Rs 5 lakh to be deducted from the cost price of the asset(d) Rs 5 lakh to be deducted from the cost price of the asset over

the useful life of the asset.

28

Question No 5

Answer : (c)

29

Question No 6

ABC Ltd is constructing a fixed asset. The cost of the project is Materials : Rs 500,000 Direct expenses : Rs 100,000 Total wages of the company during the year Rs 120000 of which 1/12 is

chargeable to the project Depreciation on asset used for the project Rs 12,000 Profit on sale of scrapped material Rs 10,000

What is the cost of fixed assets?(a) 732,000(b) 722,000(c) 622,000(d) 612,000

30

Question 6 Answer

Answer: (d) Cost = 500,000+100,000+120,000/12+12,000-10,000

31

Question No 7

A company has credited the surplus arising in revaluation of land and building to the profit and loss account to the extent of depreciation charged theron in the previous year. It is argued by the company that to this extent, depreciation need not have been charged in these years. Whether the accounting treatment is correct?

(a) Yes, as AS 10 permits credit to the profit and loss account to the extent of depreciation amount

(b) No, AS 10 does not permit such credits to profit and loss account unless it is a case of subsequent upward revaluation.

32

Question No 7

Answer: (b)

33

AS 9 – Revenue recognition

This standard explains when the revenue should be recognized in the profit and loss account and also the circumstances in which revenue recognition has to be postponed

Revenue means gross inflow of cash, receivable or other consideration arising in the course of ordinary activities of an enterprise

An enterprise generated revenue from The sale of goods Rendering of services Use of the enterprises resources by others yielding

interest, dividend and royalties.

34

Sale of Goods

Revenue from sale of goods to be recognized when all the three conditions are fulfilled Seller has transferred the ownership of goods to the

buyer for a price. OR all significant risks and rewards of ownership have been transferred to the buyer

Seller does not retain any effective control of ownership of the transferred goods

There is no significant uncertainty in collection of the amount of consideration

35

Sale of Goods – Certain Principles

Circumstance Revenue recognition

1 Delivery of goods is delayed at buyer’s request

Where buyer has taken the title to goods and accepts billing, revenue to be recognized immediately

2 Sale on approval basis Revenue to be recognized when the buyerconfirms his desire to buy such goods by communication

3 Warranty sales Sales recognized immediately, but a provision to be made to cover the unexpired warranty as per AS 29

4 Consignment sales Revenue should be recognized only when the goods are sold to third party

5 Installment sales Cash price to be recognized as revenue immediately. However, interest portion has to be recognized over a period of time.

36

Services

Revenue from rendering services Following two methods can be followed

Completed service contract method where revenue is recognized only upon completion of the service contract and there exists no uncertainty about the collection of amount of service charges

Proportionate completion method where revenue is recognized with reference to performance of each act. No significant uncertainty in collection of the revenue to exist.

37

Revenue from use of Enterprise Resources

Sl. No. Particulars Revenue Recognition Criteria

1 Royalties On accrual basis as per terms of the agreement

2 Dividend When the declaring company declares dividend

3 Interest Recognized on time proportion basis

38

Postponement of revenue recognition

Where there exists significant uncertainty in collection of the revenue, revenue recognition should be postponed

When uncertainty of collection of revenue arises subsequently after the revenue recognition, make a provision for the uncertainty in collection.

39

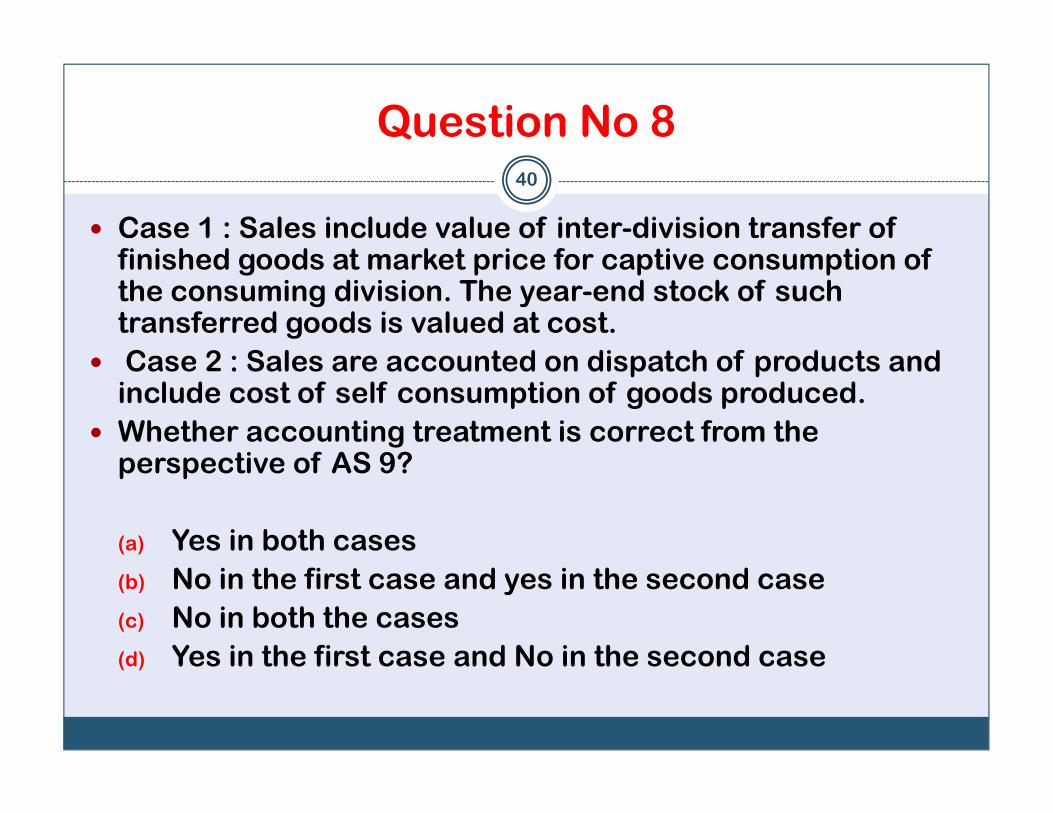

Question No 8

Case 1 : Sales include value of inter-division transfer of finished goods at market price for captive consumption of the consuming division. The year-end stock of such transferred goods is valued at cost.

Case 2 : Sales are accounted on dispatch of products and include cost of self consumption of goods produced.

Whether accounting treatment is correct from the perspective of AS 9?

(a) Yes in both cases(b) No in the first case and yes in the second case(c) No in both the cases (d) Yes in the first case and No in the second case

40

Question 8 Answer

Answer: (c) ICAI has announced that inter-divisional transfers are not sales. Further, in the case of self-consumption, there is not transfer of risk to a third party.

41

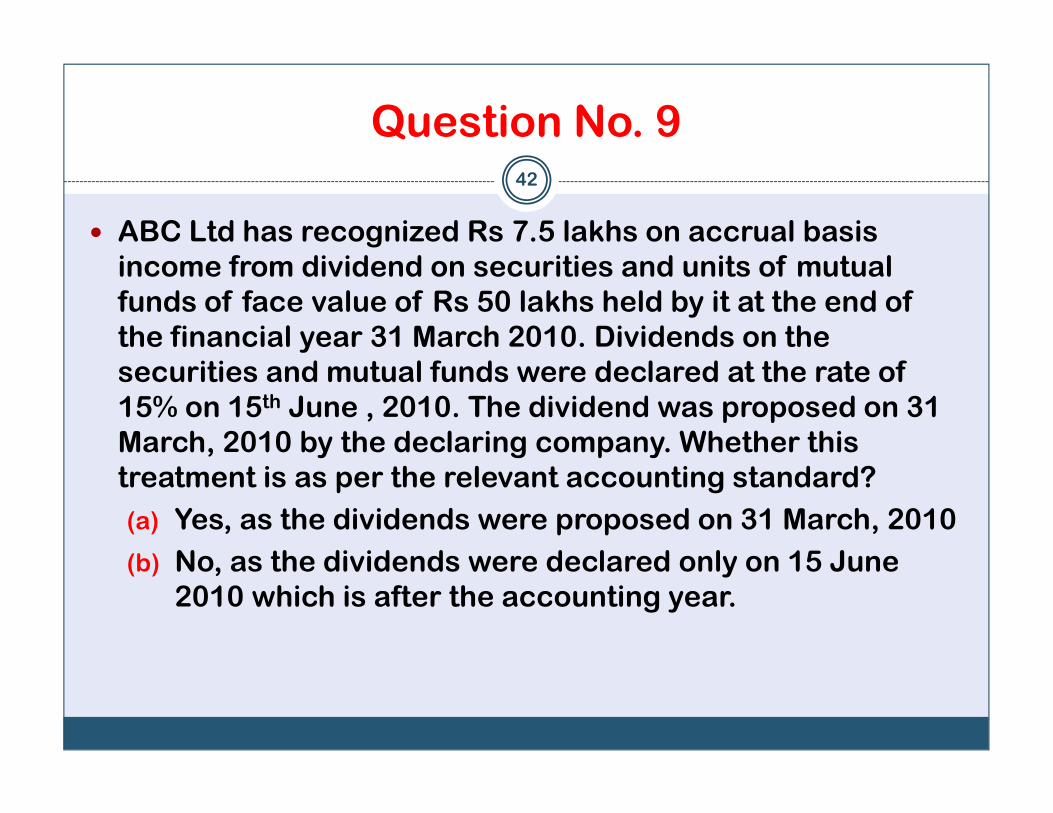

Question No. 9

ABC Ltd has recognized Rs 7.5 lakhs on accrual basis income from dividend on securities and units of mutual funds of face value of Rs 50 lakhs held by it at the end of the financial year 31 March 2010. Dividends on the securities and mutual funds were declared at the rate of 15% on 15th June , 2010. The dividend was proposed on 31 March, 2010 by the declaring company. Whether this treatment is as per the relevant accounting standard?(a) Yes, as the dividends were proposed on 31 March, 2010(b) No, as the dividends were declared only on 15 June

2010 which is after the accounting year.

42

Question 9 Answer

Answer: (b) As per AS 9, income from dividend would need to be recognized only when it is declared.

43

THANK YOU44