pareto efficient taxation - ocw.mit.edu · pareto efficient income taxation. iván werning. mit....

TRANSCRIPT

Pareto Efficient Income Taxation

Iván Werning

MIT

April 2007

NBER Public Economics meeting

Pareto Efficient Income Taxation - p. 1

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 2

Introduction

Q: Good shape for tax schedule ?

Introduction

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 2

Q: Good shape for tax schedule ? Mirrlees (1971), Diamond (1998), Saez (2001)

positive: redistribution vs. efficiency

normative: Utilitarian social welfare function

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 2

Introduction

Q: Good shape for tax schedule ? Mirrlees (1971), Diamond (1998), Saez (2001)

positive: redistribution vs. efficiency

normative: Utilitarian social welfare function

this paper: Pareto efficient taxation

positive: redistribution vs. efficiency

normative: Utilitarian social welfare function Pareto Efficiency

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 3

Old Motivation: “New New New...”

Why not Utilitarian? (

i Ui)

practical: cardinality U i → W (U i) (or even W i(U i)) ... which Utilitarian?

conceptual: political process: social classes Coasian bargain ...but max

U i ?

philosophical: other notions of fairness and social justice

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 3

Old Motivation: “New New New...”

Why not Utilitarian? ( i Ui)

practical: cardinality U i → W (U i) (or even W i(U i)) ... which Utilitarian?

conceptual: political process: social classes Coasian bargain ...but max U i ?

philosophical: other notions of fairness and social justice

Pareto efficiency weaker criterion

!

!

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

����������

�����������

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

�����L

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 4

Pareto Frontier

V�

VL

�����L

Ȝ������ Ȝ���L

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 5

Contribution

invert Mirrlees model...

...express in tractable way

...use it: some applications

Results

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 6

#0 restrictions generalize “zero-tax-at-the-top” #1 Any T (Y ). . .

efficient for many f(θ)

inefficient for many f(θ) . . . anything goes

#2 Given T0(Y ) g(Y ) f(θ) (Saez, 2001) efficient set of T (Y ): large

inefficient set of T (Y ): large

#3 Simple test for efficiency of T0(Y )

Results

Introduction ❖ Introduction ❖ Motivation ❖ Contribution ❖ Results

Model

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 7

#4 Simple formulas...

bound on top tax rate

efficiency of a flat tax

#5 Increasing progressivity maintains Pareto efficiency

#6 observable heterogeneity not conditioning can be efficient

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

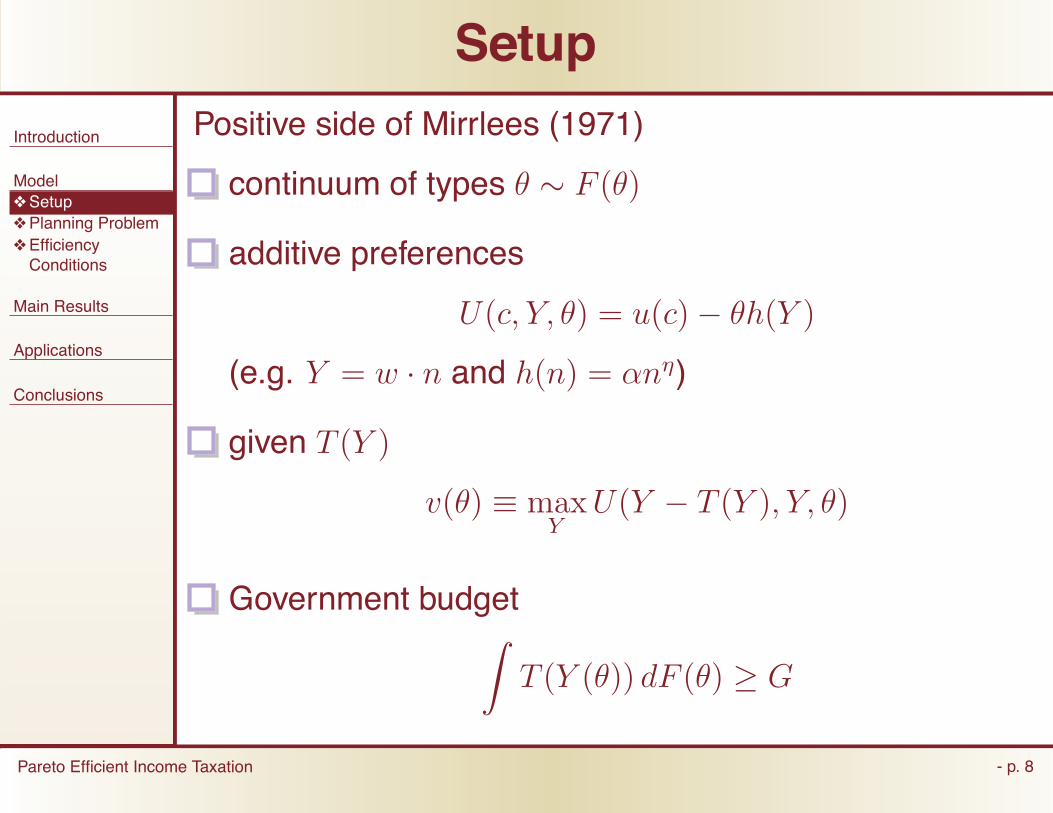

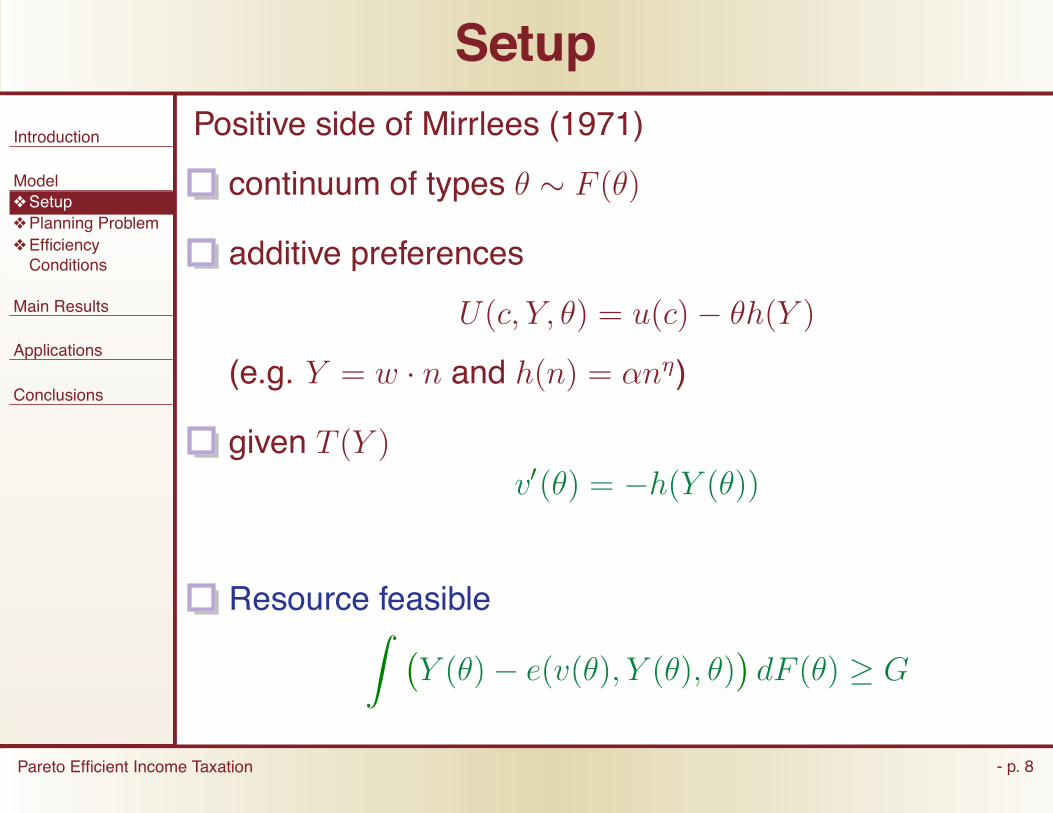

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

given T (Y )

v(θ) ≡ max Y

U(Y − T (Y ), Y, θ)

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

given T (Y )

v(θ) ≡ max Y

U(Y − T (Y ), Y, θ)

Government budget � T (Y (θ)) dF (θ) ≥ G

�

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

given T (Y )

v(θ) ≡ max Y

U(Y − T (Y ), Y, θ)

Resource feasible � Y (θ) − c(θ)

� dF (θ) ≥ G

"

� � �

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

given T (Y )

v ′(θ) = Uθ(Y (θ) − T (Y (θ)), Y (θ), θ)

Resource feasible

Y (θ) − c(θ) dF (θ) ≥ G "

# $

′

� � �

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

given T (Y ) v (θ) = −h(Y (θ))

Resource feasible

Y (θ) − c(θ) dF (θ) ≥ G $#

"

!

′

� � �

Setup

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 8

Positive side of Mirrlees (1971)

continuum of types θ ∼ F (θ)

additive preferences

U(c, Y, θ) = u(c) − θh(Y )

(e.g. Y = w · n and h(n) = αnη)

given T (Y ) v (θ) = −h(Y (θ))

Resource feasible

Y (θ) − e(v(θ), Y (θ), θ) dF (θ) ≥ G "

# $

!

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 9

Planning Problem

Dual Pareto Problem

maximize net resources

subject to, v(θ) ≥ v(θ)

incentives

� � �Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 9

Planning Problem

Dual Pareto Problem

max Y ,v

Y (θ) − e(v(θ), Y (θ), θ) dF (θ)

subject to, v(θ) ≥ v(θ)

incentives

"

# $

� � �

′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 9

Planning Problem

Dual Pareto Problem

max Y ,v

Y (θ) − e(v(θ), Y (θ), θ) dF (θ)

subject to, v(θ) ≥ v(θ)

v (θ) = −h( Y (θ))

$

"

#

!

� � �

′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 9

Planning Problem

Dual Pareto Problem

max Y ,v

Y (θ) − e(v(θ), Y (θ), θ) dF (θ)

subject to, v(θ) ≥ v(θ)

v (θ) = −h( Y (θ))

Y (θ) nonincreasing

#

"

$

!

� � ��

′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

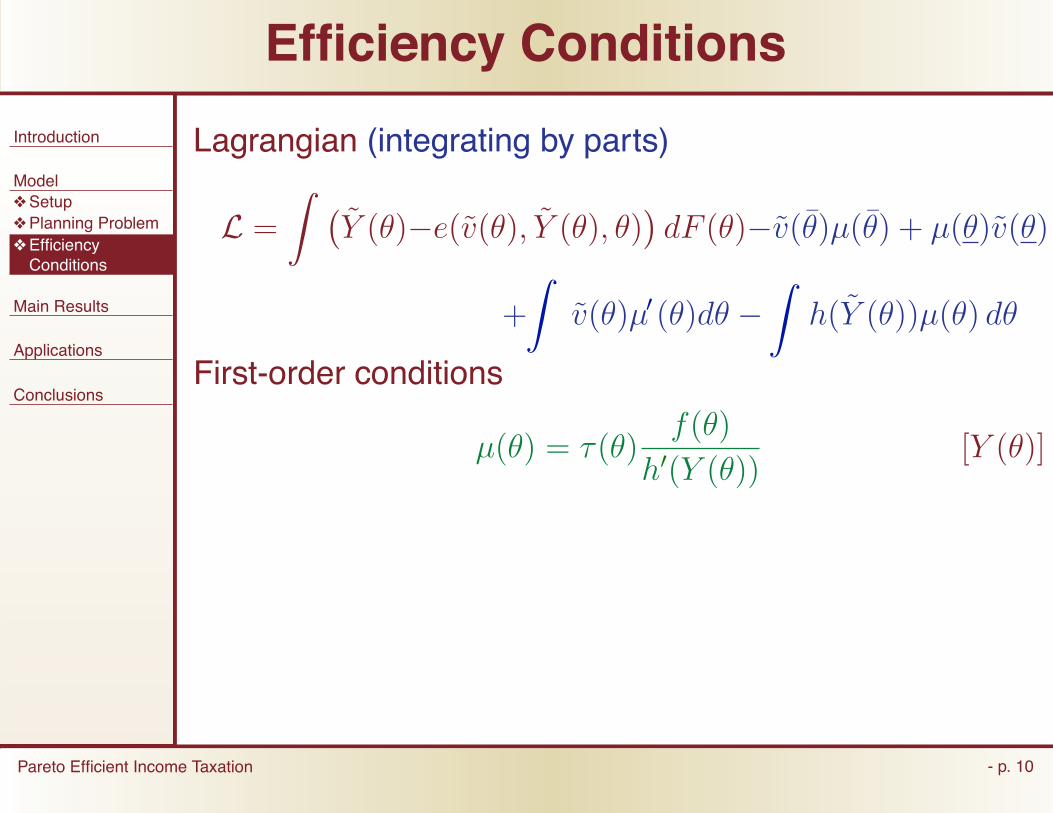

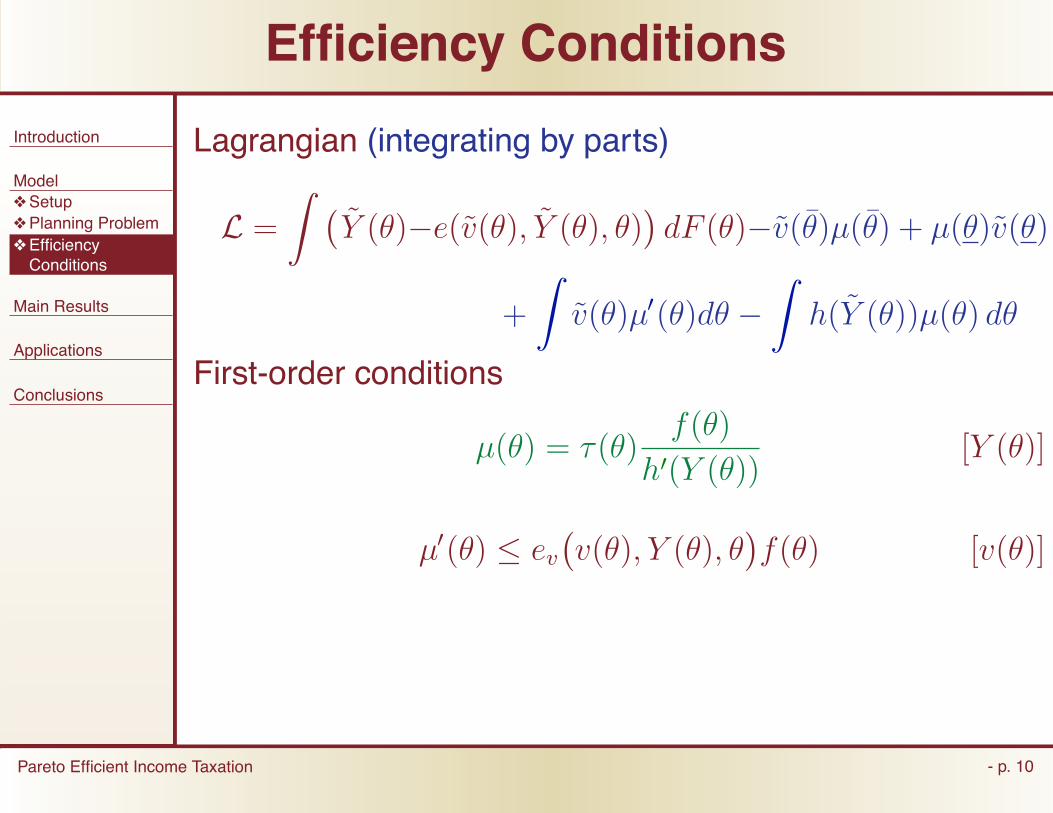

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)

− � v (θ) + h( Y (θ))

� μ(θ) dθ

"

#

"

$

!

� � ��

′

�

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian (integrating by parts)

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)−v(θ)μ(θ) + μ(θ)v(θ)

+ v(θ)μ (θ)dθ − h( Y (θ))μ(θ) dθ

$

"

#

""

!

� � ��

′

�

� �′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian (integrating by parts)

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)−v(θ)μ(θ) + μ(θ)v(θ)

+ v(θ)μ (θ)dθ − h( Y (θ))μ(θ) dθ

First-order conditions

1 − eY (v(θ), Y (θ), θ) f(θ) = μ(θ)h (Y (θ)) [Y (θ)]

""

$

$

"

#

#

!

!

� � ��

′

�

′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian (integrating by parts)

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)−v(θ)μ(θ) + μ(θ)v(θ)

+ v(θ)μ (θ)dθ − h( Y (θ))μ(θ) dθ

First-order conditions

τ(θ)f(θ) = μ(θ)h (Y (θ)) [Y (θ)]

"

# $

""

!

!

� � ��

′

�

′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian (integrating by parts)

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)−v(θ)μ(θ) + μ(θ)v(θ)

+ v(θ)μ (θ)dθ − h( Y (θ))μ(θ) dθ

First-order conditions

μ(θ) = τ(θ) f(θ)

h (Y (θ)) [Y (θ)]

"

"

"

# $

!

!

� � ��

′

�

′

′� �

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian (integrating by parts)

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)−v(θ)μ(θ) + μ(θ)v(θ)

+ v(θ)μ (θ)dθ − h( Y (θ))μ(θ) dθ

First-order conditions

μ(θ) = τ(θ) f(θ)

h (Y (θ)) [Y (θ)]

μ (θ) ≤ ev v(θ), Y (θ), θ f(θ) [v(θ)]

$

""

"

#

$#

!

!

!

� � ��

′

�

′

′� �

′ ′

Introduction

Model ❖ Setup ❖ Planning Problem ❖ Efficiency Conditions

Main Results

Applications

Conclusions

Pareto Efficient Income Taxation - p. 10

Efficiency Conditions

Lagrangian (integrating by parts)

L = Y (θ)−e(v(θ), Y (θ), θ) dF (θ)−v(θ)μ(θ) + μ(θ)v(θ)

+ v(θ)μ (θ)dθ − h( Y (θ))μ(θ) dθ

First-order conditions

μ(θ) = τ(θ) f(θ)

h (Y (θ)) [Y (θ)]

μ (θ) ≤ ev v(θ), Y (θ), θ f(θ) [v(θ)]

τ(θ)

�

θ τ (θ) τ(θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ (θ)

#

"

# $

$

"

"

!

!

! !

�′ ′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 11

Efficiency Conditions

Proposition. T (Y ) is Pareto efficient if and only

τ(θ) θ τ (θ) τ (θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ(θ)

τ(θ) ≥ 0 and τ(θ) ≤ 0.

'

! !

�′ ′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 11

Efficiency Conditions

Proposition. T (Y ) is Pareto efficient if and only

τ(θ) θ τ (θ) τ (θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ(θ)

τ(θ) ≥ 0 and τ(θ) ≤ 0.

note: “zero-tax-at-top” special case

'

! !

�′ ′

′

�′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 11

Efficiency Conditions

Proposition. T (Y ) is Pareto efficient if and only

τ(θ) θ τ (θ) τ (θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ(θ)

τ(θ) ≥ 0 and τ(θ) ≤ 0.

note: “zero-tax-at-top” special case

more general condition:

τ (θ)f(θ) h (Y (θ))

+ θ

θ

1

u (c(θ)) f(θ) dθ is nonincreasing

'

"

! !

! !

�′ ′

Intuition

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 12

define

T (Y ) ≡

T (Y (θ)) − ε Y = Y (θ)

T (Y ) Y = Y (θ)

Proposition. T > T

τ(θ) θ τ (θ) τ(θ)

+ 2 d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 3(1 − τ(θ))

is violated at θ

'

! !

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

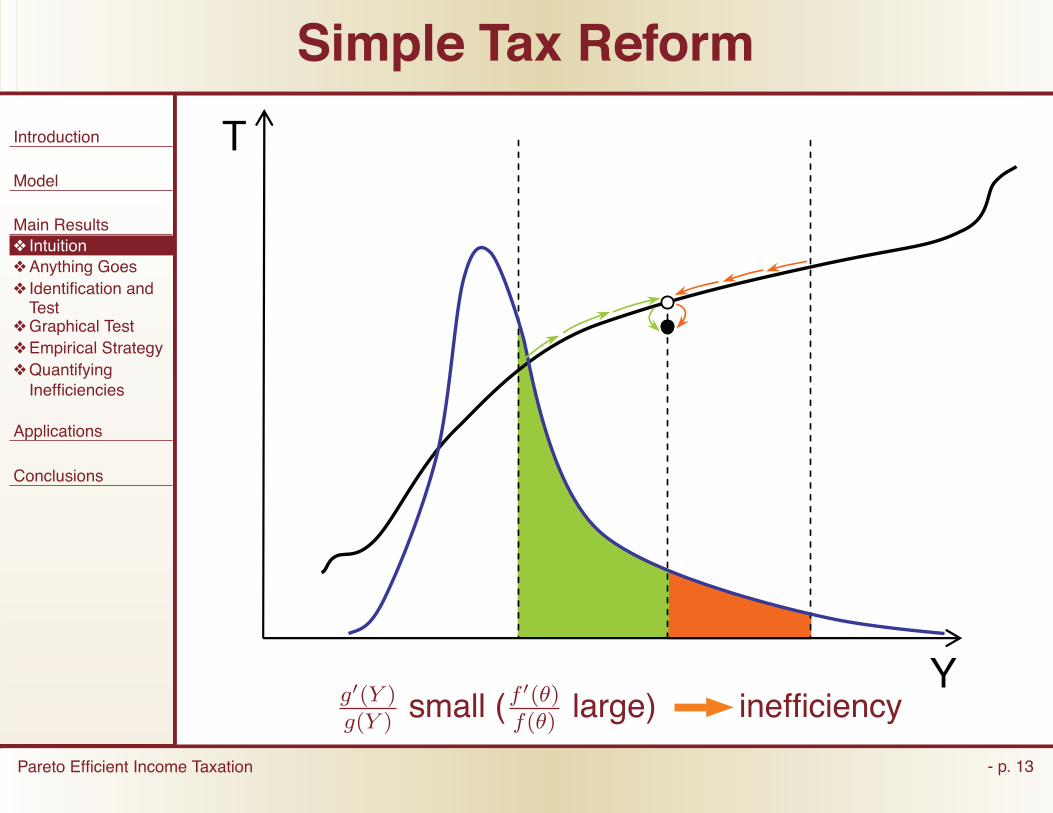

Pareto Efficient Income Taxation - p. 13

Simple Tax Reform

Y

T

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 13

Simple Tax Reform

Y

T

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 13

Simple Tax Reform

Y

T

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 13

Simple Tax Reform

Y

T

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 13

Simple Tax Reform

Y

T

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 13

Simple Tax Reform

Y

T

g'(Y ) g(Y ) small (

f '(θ) f(θ) large) inefficiency

Laffer

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 14

lower taxes increase revenue

Pareto improvements “Laffer” effect

Proposition. T1(Y ) > T0(Y ) T1(Y ) ≤ T0(Y )

�′ ′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 15

Anything Goes

τ(θ) θ τ (θ) τ(θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ (θ)

Proposition. For any T (Y )

exists set {f(θ)} Pareto efficient

exists set {f(θ)} Pareto inefficient

'

! !

�′ ′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 15

Anything Goes

τ(θ) θ τ (θ) τ(θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ (θ)

Proposition. For any T (Y )

exists set {f(θ)} Pareto efficient

exists set {f(θ)} Pareto inefficient

without empirical knowledge anything goes

'

! !

�′ ′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 15

Anything Goes

τ(θ) θ τ (θ) τ(θ)

+ d log f(θ)

d log θ −

d log h (Y (θ)) d log θ

�

≤ 1 − τ (θ)

Proposition. For any T (Y )

exists set {f(θ)} Pareto efficient

exists set {f(θ)} Pareto inefficient

without empirical knowledge anything goes

need information on f(θ) to restrict T (Y )

'

! !

′

′

′

′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 16

Identification and Test

observe g(Y ) identify (Saez, 2001)

θ(Y ) = (1 − T (Y )) u (Y − T (Y ))

h (Y )

f(θ(Y )) = g(Y ) θ (Y )

!

!

!

!

′

′

′

′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 16

Identification and Test

observe g(Y ) identify (Saez, 2001)

θ(Y ) = (1 − T (Y )) u (Y − T (Y ))

h (Y )

f(θ(Y )) = g(Y ) θ (Y )

efficiency test...

d log g(Y ) d log Y

≥ a(Y )

... for tax schedule in place

!

!

!

��

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 17

Graphical Test

define Rawlsian density:

α(Y ) = exp

Y 0 a(z) dz

�

∞ 0 exp

Y 0 a(z) dz

�

graphical test:

g(Y ) α(Y )

nondecreasing

0.5 1 1.5 2 2.5 3 3.5 4 4.5 5 5.5 6 0

0.05

0.1

0.15

0.2

0.25

0.3

%

%

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 18

Empirical Implementation

needed 1. current tax function T (Y )

2. distribution of income g(Y )

3. utility function U(c, Y, θ)

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 18

Empirical Implementation

needed 1. current tax function T (Y )

2. distribution of income g(Y )

3. utility function U(c, Y, θ)

in principle: #1 and #2 easy #3 usual deal

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 18

Empirical Implementation

needed 1. current tax function T (Y )

2. distribution of income g(Y )

3. utility function U(c, Y, θ)

in principle: #1 and #2 easy #3 usual deal

Diamond (1998) and Saez (2001)

′

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 18

Empirical Implementation

needed 1. current tax function T (Y )

2. distribution of income g(Y )

3. utility function U(c, Y, θ)

in principle: #1 and #2 easy #3 usual deal

Diamond (1998) and Saez (2001)

some challenges... 1. econometric: need to estimate g (Y ) and g(Y )

2. conceptual: static model lifetime T (Y ) and g(Y ) (Fullerton and Rogers)

!

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 19

Output Density

IRS’s SOI Public Use Files for Individual tax returns

lifetime g(Y )?

lifetime T (Y ) schedule?

Y i = 1 n Y i t

smooth density estimate assumed T (Y ) = .30 × Y

!

( )

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 19

Output Density

IRS’s SOI Public Use Files for Individual tax returns

lifetime g(Y )?

lifetime T (Y ) schedule?

Y i = 1 n Y i t

smooth density estimate assumed T (Y ) = .30 × Y

0 0.5 1 1.5 2 2.5

x 105

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2 x 10

−5

Average Income (in 1990 dollars)

nsity (bandwidth = 10,000) of Average Income Over Varying Time Periods in the Un

>= 10 years during 1979−1990 1982−1986 1987−1990

Figure 1: Density of income

g(Y )

0 2 4 6 8 10 12 14 16 18

x 104

−12

−10

−8

−6

−4

−2

0

2

Average Income (in 1990 dollars)

ernel Density (bandwidth = 10,000) of Average Income Over Varying Time Periods in

>= 10 years during 1979−199 1982−1986 1987−1990

Figure 2: Implied elasticity Y g'(Y )

!

Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 19

Output Density

IRS’s SOI Public Use Files for Individual tax returns

lifetime g(Y )?

lifetime T (Y ) schedule?

Y i = 1 n Y i t

smooth density estimate assumed T (Y ) = .30 × Y

0 2 4 6 8 10

x 104

0

0.5

1

1.5

2

2.5

3

x 10−5Rawlsian Test against 1987−1990 Average Income Data (sigma = 0, eta = 2, T = .3

0 1 2 3 4 5 6 7 8 9 10

x 104

0

1

2

3

4

5

x 10−5Rawlsian Test against 1987−1990 Average Income Data (sigma = 1, eta = 3, T = .3Y

!

� � � � � �Introduction

Model

Main Results ❖ Intuition ❖ Anything Goes ❖ Identification and Test

❖ Graphical Test ❖ Empirical Strategy ❖ Quantifying Inefficiencies

Applications

Conclusions

Pareto Efficient Income Taxation - p. 20

Quantifying Inefficiencies

efficiency test qualitative

quantitative. . .

Δ ≡ Y ∗(θ) − c ∗(θ) dF (θ) − Y (θ) − c(θ) dF (θ)

does not count welfare improvements

v(θ) > v(θ)

"

#

"

#

′

Introduction

Model

Main Results

Applications ❖ Top Tax Rate ❖ Flat Tax ❖ Progressivity ❖ Heterogeneity

Conclusions

Pareto Efficient Income Taxation - p. 21

Top Tax Rate

u(c) = c1−σ/(1 − σ) and h(Y ) = αY η

suppose top tax rate

τ ≡ lim θ→0

τ(θ) = lim Y →∞

T (Y )

exists

!

′

Introduction

Model

Main Results

Applications ❖ Top Tax Rate ❖ Flat Tax ❖ Progressivity ❖ Heterogeneity

Conclusions

Pareto Efficient Income Taxation - p. 21

Top Tax Rate

u(c) = c1−σ/(1 − σ) and h(Y ) = αY η

suppose top tax rate

τ ≡ lim θ→0

τ(θ) = lim Y →∞

T (Y )

exists

efficiency condition bound

τ ≤ σ + η − 1 ϕ + η − 2

.

where ϕ = − limT →∞ d log g(Y )/d log Y .

!

′

Introduction

Model

Main Results

Applications ❖ Top Tax Rate ❖ Flat Tax ❖ Progressivity ❖ Heterogeneity

Conclusions

Pareto Efficient Income Taxation - p. 21

Top Tax Rate

u(c) = c1−σ/(1 − σ) and h(Y ) = αY η

suppose top tax rate

τ ≡ lim θ→0

τ(θ) = lim Y →∞

T (Y )

exists

efficiency condition bound

τ ≤ σ + η − 1 ϕ + η − 2

.

where ϕ = − limT →∞ d log g(Y )/d log Y .

Saez (2001): ϕ = 3

!

Top Tax Rate 1

Introduction

0.9Model

Main Results 0.8

Applications ❖ Top Tax Rate 0.7

❖ Flat Tax ❖ Progressivity

0.6 ❖ Heterogeneity

Conclusions 0.5

0.4

0.3

0.2

0.1

0 0 1 2 3 4 5 6 7 8 9

elasticity 1/η+1

upper bound on τ

Pareto Efficient Income Taxation - p. 22

10

Flat Tax

Introduction

Model

Main Results

Applications ❖ Top Tax Rate ❖ Flat Tax ❖ Progressivity ❖ Heterogeneity

Conclusions

Pareto Efficient Income Taxation - p. 23

linear tax necessary condition

τ ≤ σ + η − 1

−d log g(Y ) d log Y + η − 2

linear tax sufficient condition

τ ≤ η − 1

−d log g(Y ) d log Y + η − 1

Introduction

Model

Main Results

Applications ❖ Top Tax Rate ❖ Flat Tax ❖ Progressivity ❖ Heterogeneity

Conclusions

Pareto Efficient Income Taxation - p. 24

Progressivity

Quasi-linear u(c) = c

result: can always increase progressivity

Introduction

Model

Main Results

Applications ❖ Top Tax Rate ❖ Flat Tax ❖ Progressivity ❖ Heterogeneity

Conclusions

Pareto Efficient Income Taxation - p. 25

Heterogeneity

groups = 1, . . . , N

f i(θ) and U i(c, Y, θ)

unobservable i single T (Y )

average efficiency condition

observable i multiple T i(Y )

N efficiency conditions

observation: T i(Y ) = T (Y ) may be Pareto efficient

never optimal for Utilitarian

Conclusions

Introduction

Model

Main Results

Applications

Conclusions ❖ Conclusions

Pareto Efficient Income Taxation - p. 26

Pareto efficiency simple condition

generalizes zero-tax-at-the-top result

Pareto inefficient Laffer effects

flat taxes may be optimal...

...more progressivity always efficient

��������� ���� �������������������

���������� ���!���������"� �#$�#

"� ��%� ����������������&����������� �� ��� ��� ��� ����%�'��(�)��������������������������� ���