particularities of risk management for funds of hedge funds

TRANSCRIPT

A member of the Man GroupJune 2008

Particularities of Risk Management for Funds of Hedge Funds

Pierre-Yves Moix, Chief Risk Officer of Man Investments

2

Disclaimer and important information

This presentation is communicated by Man Investments Ltd. which is authorised and regulated by the Financial Services Authority. This material is for information purposes only. It is proprietary information of Man Investments Ltd. and its affiliates and may not be reproduced or otherwise disseminated in whole or in part without prior written consent from Man Investments Ltd. Information contained herein is provided from the Man database except where otherwise stated.

www.maninvestments.com

3

Context

Strategy risk management

Proactive risk management

Continuous risk management

Operational risk management

Liquidity risk management

Conclusion

4

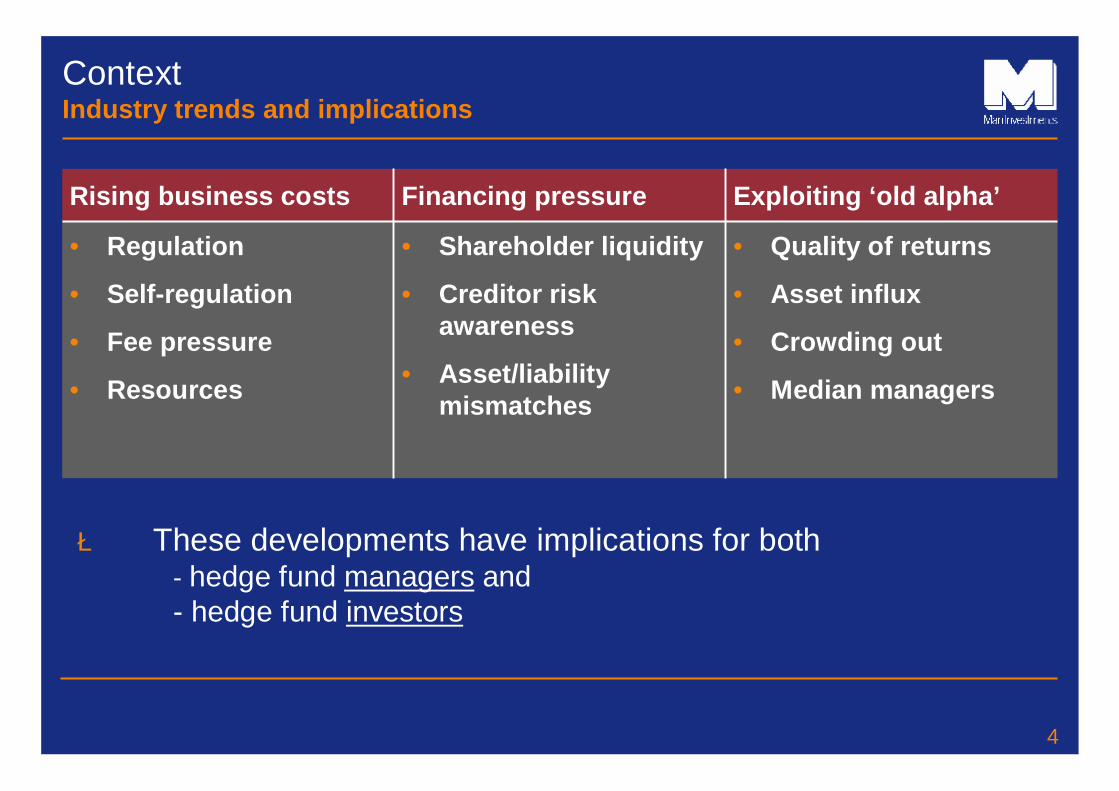

ContextIndustry trends and implications

• Quality of returns

• Asset influx

• Crowding out

• Median managers

• Shareholder liquidity

• Creditor risk awareness

• Asset/liability mismatches

• Regulation

• Self-regulation

• Fee pressure

• Resources

Exploiting ‘old alpha’ Financing pressureRising business costs

è These developments have implications for both - hedge fund managers and - hedge fund investors

5

ContextIt’s not all about market/strategy risk I/II

Liquidity risk

Operational risk (complexity)

Financing risk(leverage)

The other dimensions of risks

Schematic illustration

6

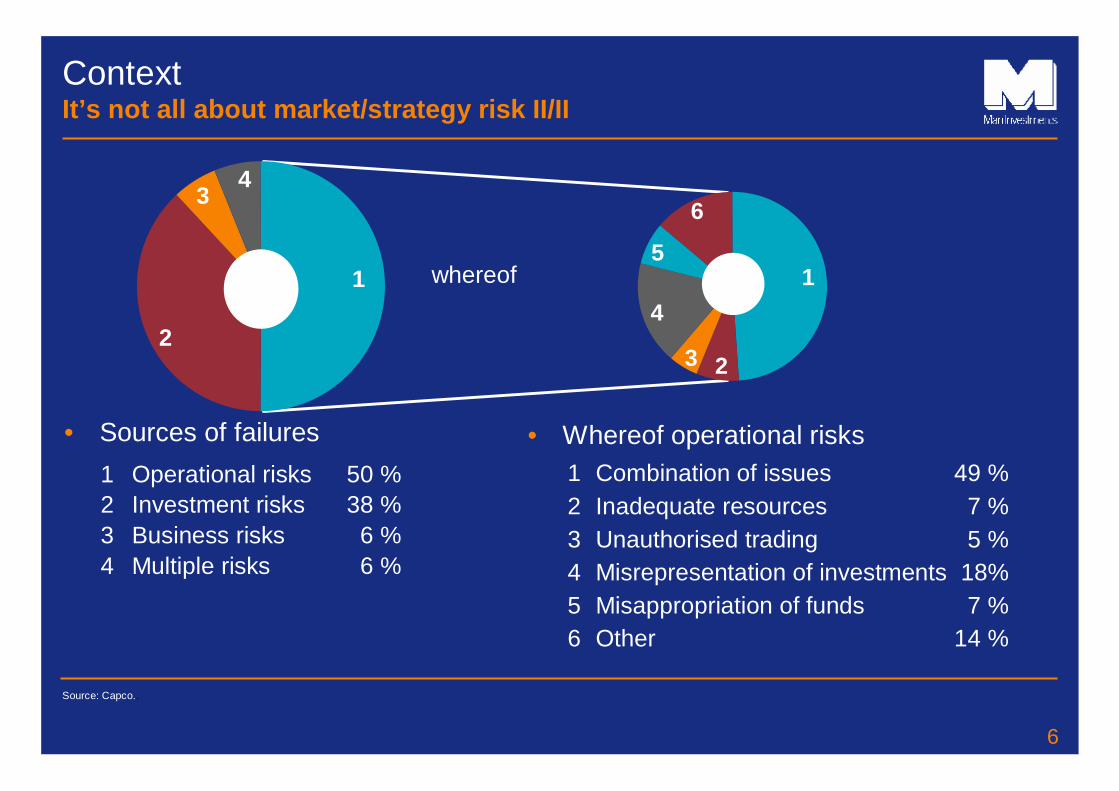

ContextIt’s not all about market/strategy risk II/II

Source: Capco..

6 %Multiple risks46 %Business risks3

38 %Investment risks250 %Operational risks1

• Sources of failures1 Combination of issues 49 %2 Inadequate resources 7 %3 Unauthorised trading 5 %4 Misrepresentation of investments 18%5 Misappropriation of funds 7 %6 Other 14 %

• Whereof operational risks

13

4

53

4

5

whereof1

3

2

4

1

3 2

4

5

6

7

Context

Strategy risk management

Proactive risk management

Continuous risk management

Operational risk management

Liquidity risk management

Conclusion

8

Strategy risk managementOverview

SlideID-16431

Asset allocation• Managing tails and correlations

• Inclusion of financial crisis scenarios

Portfolio management• Diversification advantage

• Managing liquidity gaps

Hedge fund selection• Structural choices and related degree of

transparency require different risk management tools, i.e. fund versus managed account investments

Fund / MAC

Risk management

Styles’ risk/return characteristics

Allocation optimiser

Approved funds

Asset allocation

Portfolio construction

9

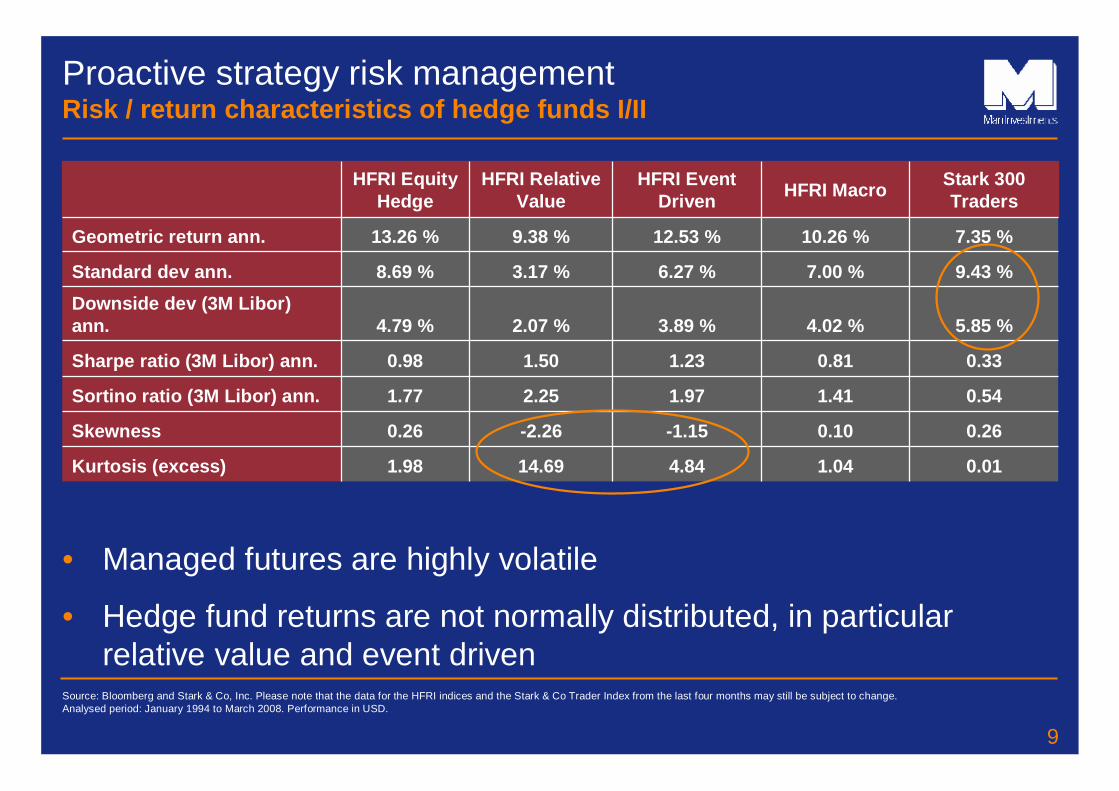

Proactive strategy risk managementRisk / return characteristics of hedge funds I/II

• Managed futures are highly volatile

• Hedge fund returns are not normally distributed, in particular relative value and event driven

Source: Bloomberg and Stark & Co, Inc. Please note that the data for the HFRI indices and the Stark & Co Trader Index from the last four months may still be subject to change. Analysed period: January 1994 to March 2008. Performance in USD.

0.011.044.8414.691.98Kurtosis (excess)

0.260.10-1.15-2.260.26Skewness

0.541.411.972.251.77Sortino ratio (3M Libor) ann.

0.330.811.231.500.98Sharpe ratio (3M Libor) ann.

5.85 %4.02 %3.89 %2.07 %4.79 %Downside dev (3M Libor) ann.

9.43 %7.00 %6.27 %3.17 %8.69 %Standard dev ann.

7.35 %10.26 %12.53 %9.38 %13.26 %Geometric return ann.

Stark 300 TradersHFRI MacroHFRI Event

DrivenHFRI Relative

ValueHFRI Equity

Hedge

10

Proactive strategy risk managementRisk / return characteristics of hedge funds II/II

èOmega includes all higher momentsSource: Bloomberg.Analysed period: January 1994 to March 2008.Please note that the HFRI index data over the past 4 months may be subject to change.

Threshold -8 % -6 % -4 % -2 % 0 % 2 % 4 % 6 % 8 %Lo

g (o

meg

a)

-15

-10

-5

0

5

10

15

20HFRI Fund of Funds Composite IndexNormal equivalent

11

Proactive strategy risk managementCorrelations I/III

èManaged futures are uncorrelated

èComparatively high correlation of event driven with equity hedged and to a lesser extent with relative value strategies

1.00.50.0-0.10.0Stark 300 Traders

0.51.00.60.40.6HFRI Macro

0.00.61.00.70.8HFRI Event Driven

-0.10.40.71.00.6HFRI Relative Value

0.00.60.80.61.0HFRI Equity Hedge

Stark 300 TradersHFRI MacroHFRI Event

Driven

HFRI Relative

Value

HFRI Equity Hedge

Source: Bloomberg and Stark & Co, Inc. Please note that the data for the HFRI indices and the Stark & Co Trader Index from the last four months may still be subject to change. Analysed period: January 1994 to March 2008. Performance in USD.

12

Proactive strategy risk managementCorrelations II/III

• Hedge funds should provide diversification for traditional investments

• Currently, high correlations across styles and with regard to traditional investments

– Is this unusual?

– Is there an explanation?

24M rolling measured correlations

1996 1997

1998 1999

2000 2001

2002 2003

2004 2005

2006 2007

2008 Ann

ualis

ed re

turn

-40 %

-30 %

-20 %

-10 %

0 %

10 %

20 %

30 %

40 %

Cor

rela

tion

-1.0

-0.8

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

World equitiesHFRI RVAHFRI EHHFRI EDHFRI MacroStark MF

Source: Bloomberg and Stark & Co, Inc. Please note that the data for the HFRI indices and the Stark & Co Trader Index from the last four months may still be subject to change. Analysed period: January 1996 to March 2008. Performance in USD.

13

Proactive strategy risk managementCorrelations III/III

• Managed futures have non-linear links to traditional investments

• Alternative risk factors are needed to explain hedge fund returns

Source: Bloomberg and Stark & Co, Inc. Period of analysis: January 1994 – March 2008. Please note that the HFRI index and Stark & Co Trader Index data over the past 4 months may be subject to change. World stocks are proxied by MSCI World Total Return Index, world bonds by Citigroup WGBI all maturities

Stark MF

Worst months Quintile 2 Quintile 3 Quintile 4 Best months

Cor

rela

tion

-0.6-0.5-0.4-0.3-0.2-0.10.00.10.20.30.40.50.6

Correlations with world stocksCorrelations with world bonds

Stark MF

MSCI World monthly return

-10 %

-5 %

0 %

5 %

10 %

15 %

-10 % -5 % 0 % 5 % 10 % 15 %

Star

k M

F m

onth

lyre

turn

Stark MF Poly. (Stark MF) Linear (Stark MF)

Stark MF

-10 %

-5 %

0 %

5 %

10 %

15 %

-10 % -5 % 0 % 5 % 10 % 15 %

Citigroup WGBI monthy return

Star

k M

F m

onth

lyre

turn

Stark MF Poly. (Stark MF) Linear (Stark MF)

14

Context

Strategy risk management

Proactive risk management

Continuous risk management

Operational risk management

Liquidity risk management

Conclusion

15

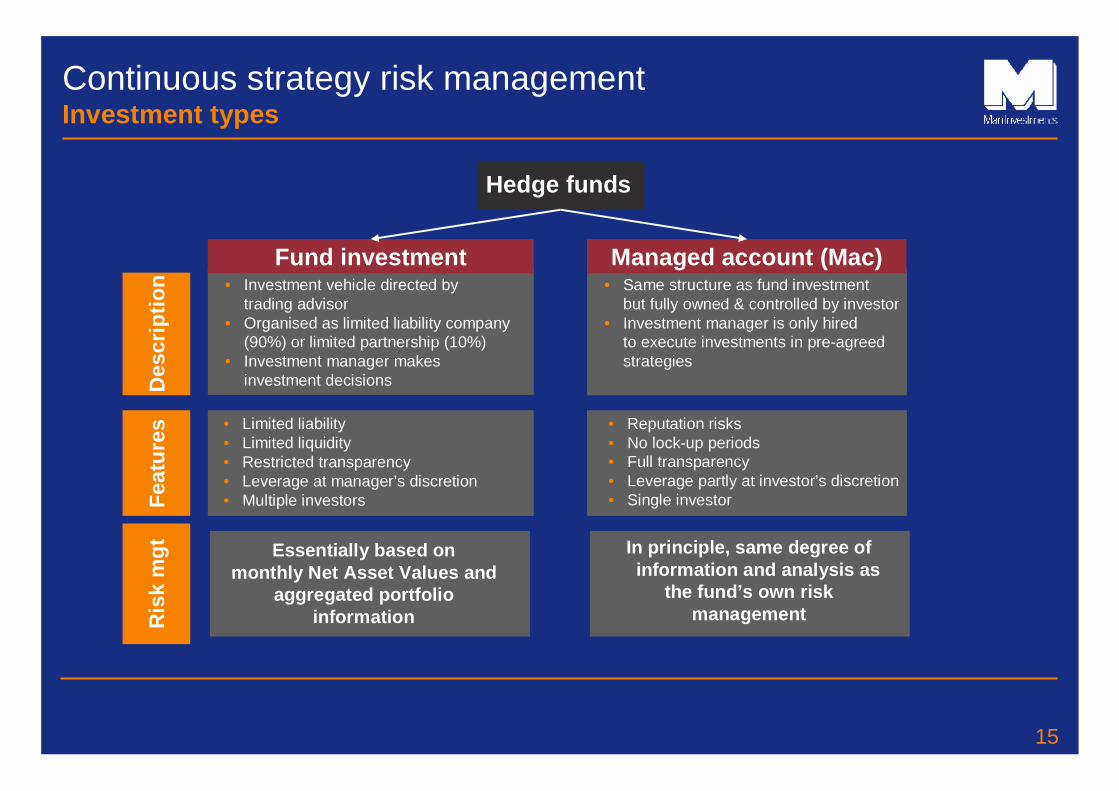

Continuous strategy risk managementInvestment types

Hedge funds

Fund investment• Investment vehicle directed by

trading advisor• Organised as limited liability company

(90%) or limited partnership (10%) • Investment manager makes

investment decisions

• Limited liability• Limited liquidity• Restricted transparency• Leverage at manager’s discretion• Multiple investors

Managed account (Mac)

• Reputation risks • No lock-up periods• Full transparency• Leverage partly at investor’s discretion• Single investor

• Same structure as fund investmentbut fully owned & controlled by investor

• Investment manager is only hired to execute investments in pre-agreed strategies

Des

crip

tion

Feat

ures

Ris

k m

gt Essentially based on monthly Net Asset Values and

aggregated portfolio information

In principle, same degree of information and analysis as

the fund’s own risk management

16

Continuous strategy risk managementThe three levels of transparency

• Managers who pursue more liquid strategies, with a shorter track record and a higher strategy capacity tend to provide position information

• Managers who pursue less liquid strategies, with longer track records and a smaller strategy capacity tend to provide NAV & exposure information

Positions

NAV

Exposure &performance attribution

17

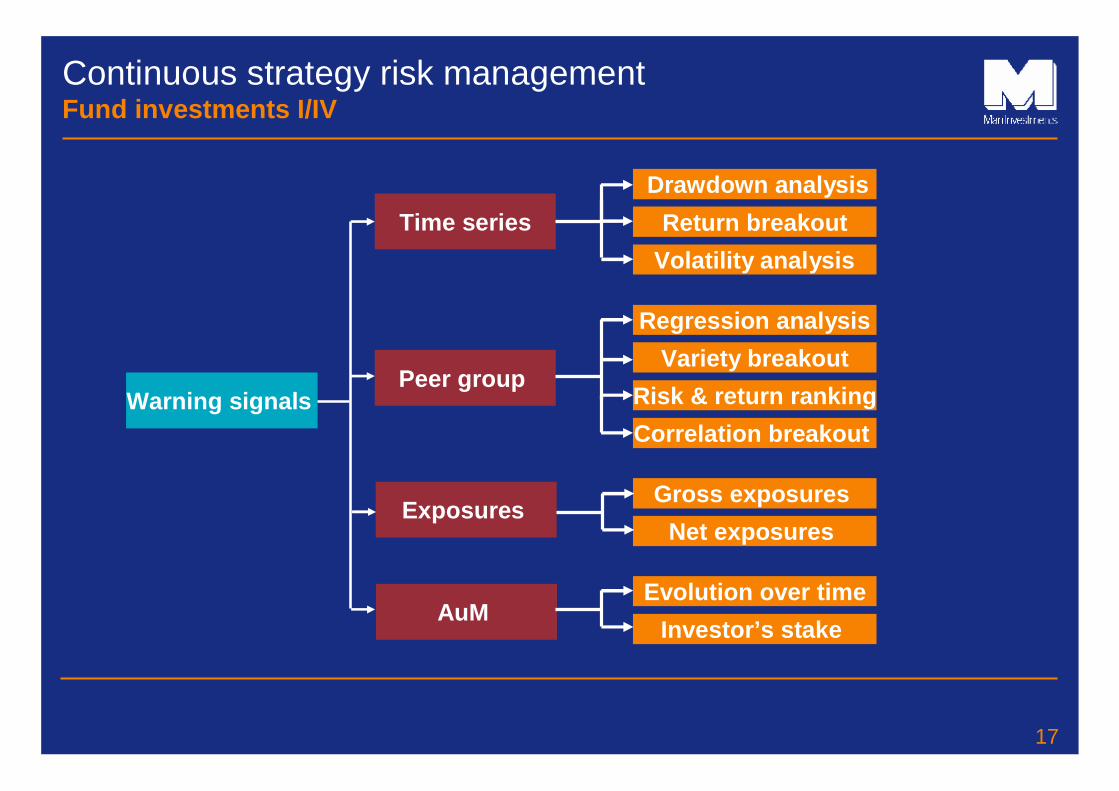

Continuous strategy risk managementFund investments I/IV

Warning signals

Time series

Peer group

Drawdown analysisReturn breakout

Regression analysis

Correlation breakout Risk & return ranking

Variety breakout

Gross exposures

Volatility analysis

Exposures Net exposures

Evolution over timeInvestor’s stake

AuM

18

Continuous strategy risk managementFund investments II/IV

Source: RMF Investment Management and Bloomberg. There is no guarantee of trading performance and past performance is not necessarily a guide to future results.

Under water chart

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

500

600

700

800

900

1000

HFRI Relative Value Arbitrage IndexMSCI World

Relative value fundYear 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8

19

Continuous strategy risk managementFund investments III/IV

Source: RMF Investment Management and Bloomberg. There is no guarantee of trading performance and past performance is not necessarily a guide to future results.

Time series of monthly returns

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

-4 %

-2 %

0 %

2 %

4 %

6 %

8 %

Relative value fundRisk bound 2 stdev (ltd)Risk bound 2 stdev (12 month)

warning signals

warning signals

20

Continuous strategy risk managementFund investments IV/IV

Source: RMF Investment Management. There is no guarantee of trading performance and past performance is not necessarily a guide to future results..

Ranking of peer group 12 months downside deviation

Peer group rankingNumber of funds

Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

0 %

20 %

40 %

60 %

80 %

100 % Num

berof fundsin peergroup0

10

20

30

40

50

60

21

Continuous strategy risk managementManaged Accounts I/III

Limits, Restrictions

VaR

Equity leverage

Risk

P&L

Outliers

Drawdowns

Other

Margin to equity ratio

Approved instruments,markets, sectors

Risk factor sensitivities,stress tests

Backtesting exceptions

If contractually agreed

Soft exceptionHard exception

22

Continuous strategy risk managementManaged Accounts II/III

23

Continuous strategy risk managementManaged Accounts III/III

MAC XXXMAC YYYMAC ZZZ

….

24

Context

Strategy risk management

Proactive risk management

Continuous risk management

Operational risk management

Liquidity risk management

Conclusion

25

Operational risk management Operational due diligence (OpDD) approaches compared

• Basic OpDD approaches– Governance focus

– Quantitative data

– Less qualitative assessment required

• Fundamental OpDD approaches

– Value chain/management control focus

– Quantitative & qualitative data

– Requires assessment/ interpretation

Investor

Investment firm

Basicapproaches

Investment process

Investor

Investment firm

Fundamentalapproaches

26

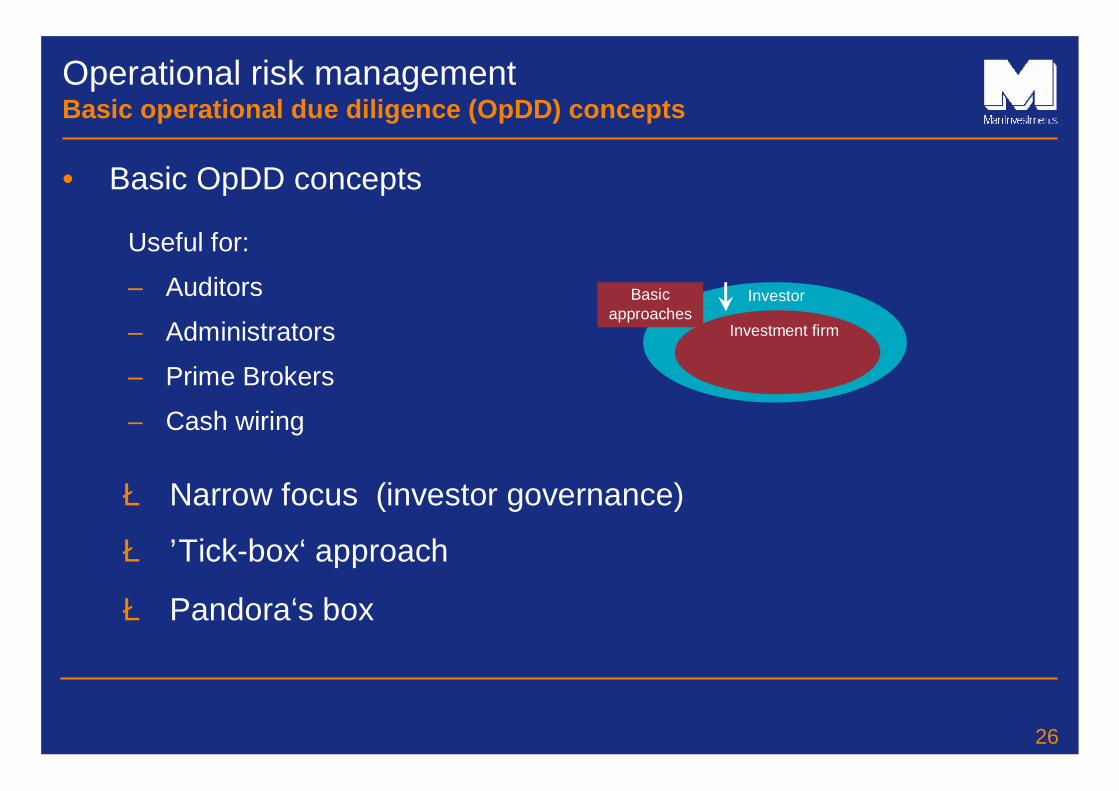

Operational risk managementBasic operational due diligence (OpDD) concepts

• Basic OpDD concepts

Useful for:

– Auditors

– Administrators

– Prime Brokers

– Cash wiring

è Narrow focus (investor governance)

è ’Tick-box‘ approach

è Pandora‘s box

Investor

Investment firm

Basicapproaches

27

Operational risk management Fundamental operational due diligence (OpDD) concepts

• Fundamental OpDD concepts

è Broader focus (value chain)

è Skill-based approach

è Framework-based

Investment process

Investor

Investment firm

Fundamentalapproaches

Typical focus areas:

– Governance

– Roles & responsibilities

– Controlling and accounting

– Outsourcing

28

• Combining the operational risk dimensions with the scope of the due diligence

Operational risk managementFundamental operational due diligence concepts

è Methodology of ‘Slicing-and-dicing’

+ =• Establishes

common understanding

• Dimensions of operational risks

Operational risk definition

Operational risk model

• Defines the scope of the operational due diligence

Operational risk assessment matrix

29

• Operational risk definition – four dimensions• Processes Activities to achieve desired outcomes

• People Human resources to service processes and systems

• Systems Technologies to support processes and people

• External events Incidences disrupting internal activities

Assessing operational riskOperational risk definition by the Basle Committee

èProcesses, people and systems are internal risk dimensions and can be compared across organisations

èExternal events are not fully controllable and are context-specific

30

Assessing operational risk Operational risk model

Functional responsibilitiesTrading

Legal and complianceRisk management

Operations and controllingTrade processing and settlement monitoring

Accounting and MIS reportingPortfolio valuation and performance measurement

Business managementGovernance, policies and procedures

Infrastructure, IT and business continuityOrganisational structure and human resources

• Sources of operational risks for hedge funds

Internal sourcesExternal sources

Fund administrator

Valuation agent

(Prime) Broker(s)

Otherse.g. lawyers, consultants

Outsourcing 1

2

3

4

31

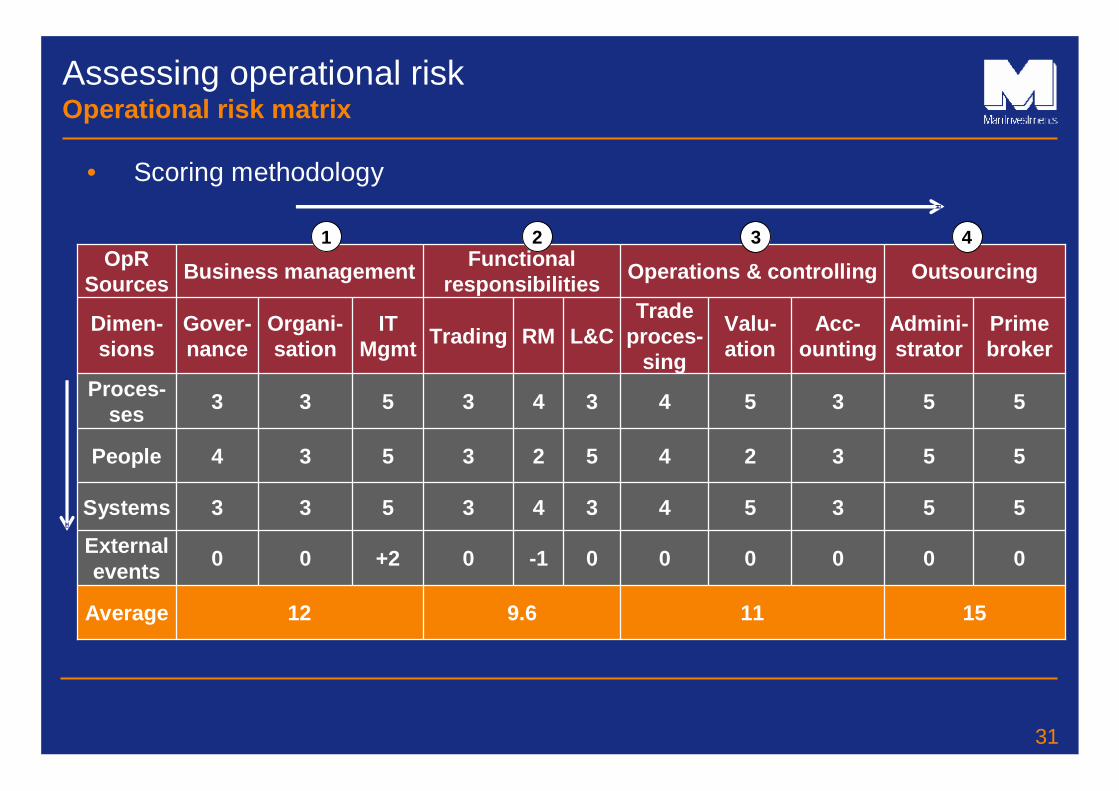

Assessing operational riskOperational risk matrix

• Scoring methodology

15119.612Average

000000-10+200External events

55354343533Systems

55324523534People

55354343533Proces-ses

Prime broker

Admini-strator

Acc-ounting

Valu-ation

Trade proces-

singL&CRMTrading IT

MgmtOrgani-sation

Gover-nance

Dimen-sions

OutsourcingOperations & controllingFunctional responsibilitiesBusiness managementOpR

Sources

1 2 3 4

32

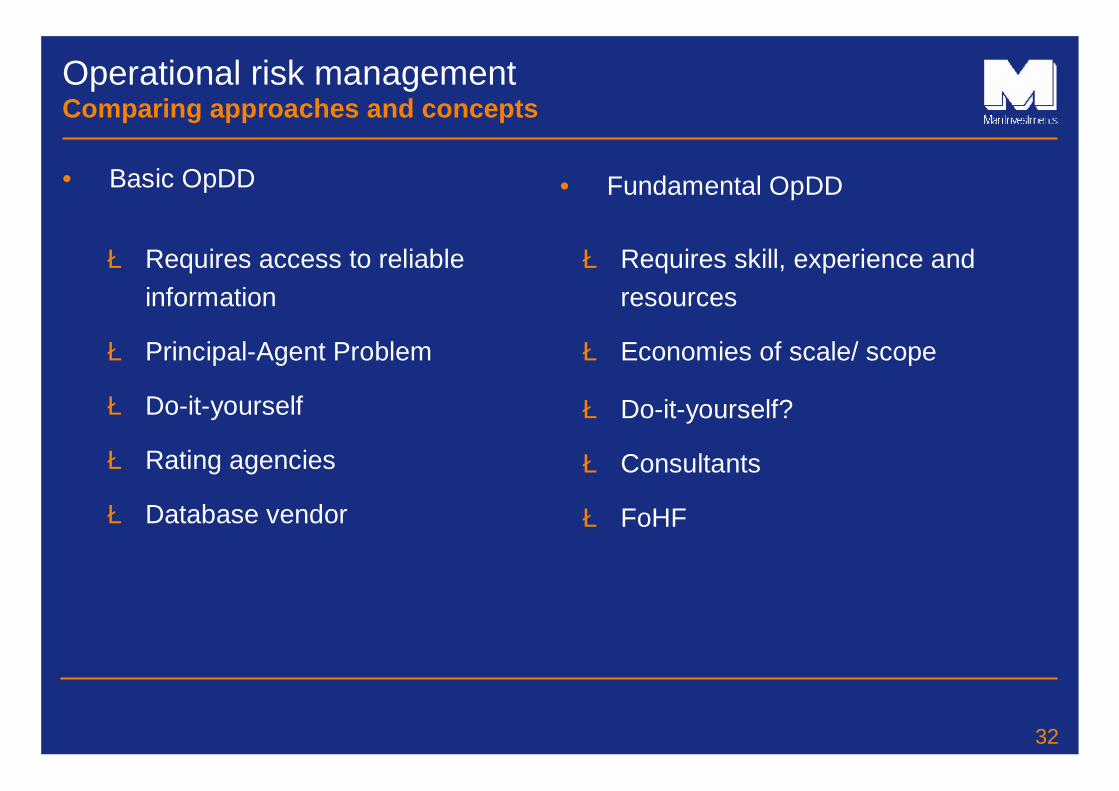

Operational risk management Comparing approaches and concepts

• Basic OpDD • Fundamental OpDD

è Requires access to reliable information

è Principal-Agent Problem

è Requires skill, experience and resources

è Economies of scale/ scope

è Do-it-yourself

è Rating agencies

è Database vendor

è Do-it-yourself?

è Consultants

è FoHF

33

Context

Strategy risk management

Proactive risk management

Continuous risk management

Operational risk management

Liquidity risk management

Conclusion

34

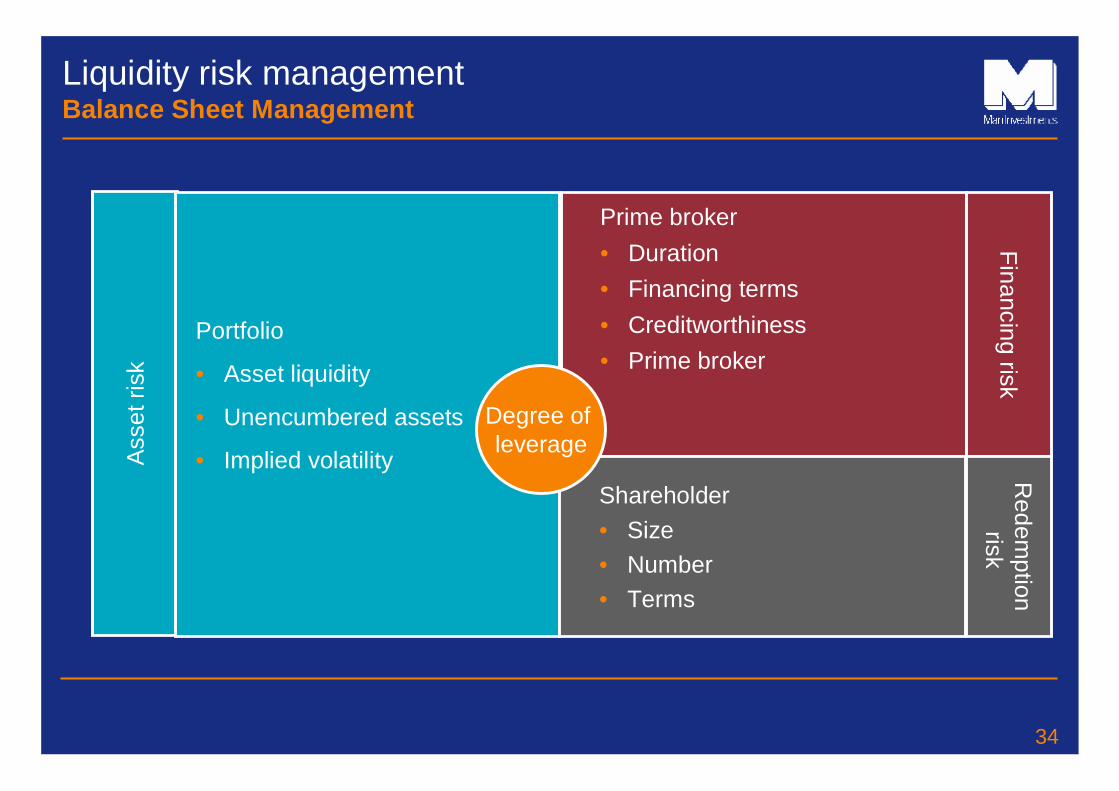

Ass

et ri

sk

Portfolio

• Asset liquidity

• Unencumbered assets

• Implied volatility

Prime broker• Duration• Financing terms• Creditworthiness• Prime broker

Financing risk

Shareholder• Size• Number• Terms

Redem

ptionrisk

Degree of leverage

Liquidity risk managementBalance Sheet Management

35

Liquidity risk managementRedemption timeline of a hedge fund

End of lockupperiod

Hard lockup period

Notice period

No redemption is allowed

Redemption period

Time

Bal

ance

pay

out

settl

emen

t dat

e

Sub

scrip

tion

date

Cal

cula

tion

date

Sta

rt of

bal

ance

pay

out p

erio

d

Initi

al p

ayou

t se

ttlem

ent d

ate

Red

empt

ion

date

Initial payout period

Balance payout period

Not

ice

date

Cash flows from hedge fund redemption

èExpected cash flows from a hedge fund redemption taking into account lock up, notice period, redemption frequency, and payoutterms

36

Liquidity risk managementRedemption strategies for a portfolio of hedge funds

t t + 1 t + 2 ….

Hedge fund redemptions Cumulative gapClient redemptions

• Hedge funds redeemed proportionally

è Structural liquidity mismatch in fund of hedge funds creates a cash flow gap

• Most liquid hedge funds redeemed first

t t + 1 t + 2 ….è Cash flow gap is minimised

37

Liquidity risk management Scenario analysis

XYZ Breakdown 14.4% 36.1% 35.3% 8.9% 5.4%

Notice period: 90 day(s) Redemption frequency: Quarterly First payment date: Cumulative 14.4% 50.5% 85.8% 94.6% 100.0%

Legal monthly liquidity: 28.1% Fraction of portfolio with LockUp: 37%

Assets 2,128,445,329 2,128,445,329 Liabilities Liquid ity gaps analysisPortfolio 2,040,781,862 2,073,436,926 Net Assets

>>> Cash 87,663,466 55,008,403 Loans

Direct available credit line(*) 195,000,000Other sources of credit line noneAdditional USD credit line (manual) -Aggregation methodology Bottom UpRedemption strategy Proportional

Use of cash 15.00% 13,149,520

Redemptions of assets 15.00% 306,117,279

Sum of draws of credit facility 39,000,000

Sum of repayments of credit facility -39,000,000

Repayment of current loans 15.00% -8,251,260

Client redemptions 15.00% -311,015 ,539

Deficiency of cash, Gap, during redemption process no gap no gap no gap no gap no gap 2.0% 0.1% no gap no gap no gap no gapExcess of cash during redemption process - - - - - 6.3 0.3 - - - -

Quarterly(*)Direct credit line is granted to the product itself, - - - - - 100.0% - - - - - -full amount availability is subject to conditions - - - - - 311 - - - - - -

Nb HF before Nb HF after Cumulated liquid ity profile (** )

redemption redemption CAA (no TAA)

[77] - Asset allocation - [77] Alloc. afterCash redemption[17] - Equity hedged - [17] 20.80% 14.35% 20.80% w

[21] - Relative value - [21] 28.68% 20.02% 28.68% w

[17] - Event driven - [17] 21.11% 18.76% 21.11% w

[11] - Global macro - [11] 17.60% 15.34% 17.60% w

[11] - Managed futures - [11] 11.81% 7.40% 11.81% w

[0] - Other - [0] 24.13%Use of credit facility

incl. CL 10.3% 22.3% 46.4% 60.4% 64.5% 98.0% 99.9% 100.0% 100.0% 100.0% 100.0% 100.0%

(**)Total amount recovered divided by total amount due to investors and credit providers excl. CL 10.3% 22.3% 46.4% 60.4% 64.5% 85.8% 87.7% 87.9% 87.9% 87.9% 88.2% 94.7%

-

Product XYZ

Liquidity Analysis

20.00%

no gap

as of 31 Jan 2008

Veryliquid <3M

Liquid

<6M

Illiquid

<12M

Veryilliquid

>1Y

Highlyliquid <1M

Cumulative Gap: (%)(MUSD)

Redemption to clients: (%)(MUSD)

Current allocation

Switch to target alloc.

Jul 2008

Cha

nge

-400

-300

-200

-100

0

100

200

300

Feb-08 Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 Jan-09

0%

20%

40%

60%

80%

100%

120%

38

Context

Strategy risk management

Proactive risk management

Continuous risk management

Operational risk management

Liquidity risk management

Conclusion

39

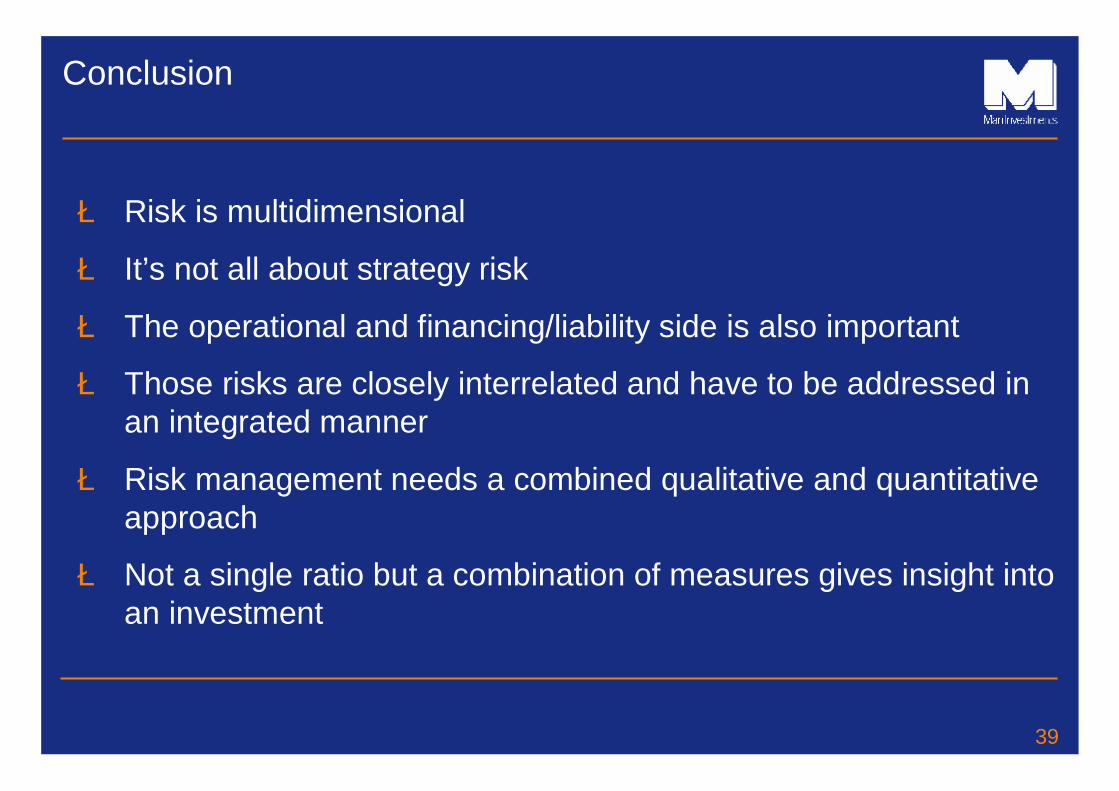

Conclusion

è Risk is multidimensional

è It’s not all about strategy risk

è The operational and financing/liability side is also important

è Those risks are closely interrelated and have to be addressed inan integrated manner

è Risk management needs a combined qualitative and quantitative approach

è Not a single ratio but a combination of measures gives insight into an investment