partnership exchanges: structuring drop and swap and

TRANSCRIPT

Partnership Exchanges: Structuring "Drop

and Swap" and "Mixing Bowl" Transactions Minimizing IRS Challenges and Maximizing Favorable Tax Treatment

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

THURSDAY, AUGUST 21, 2014

Presenting a live 90-minute teleconference with interactive Q&A

Maher Haddad, Attorney, Baker & McKenzie, Chicago

Mark E. Wilensky, Counsel, Meltzer, Lippe, Goldstein & Breitstonen, LLP, Mineola, N.Y.

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-873-1442 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can address

the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

For CLE credits, please let us know how many people are listening online by

completing each of the following steps:

• Close the notification box

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

For CPE credits, attendees must listen throughout the program, including the Q &

A session, and record verification codes in the corresponding spaces found on the

CPE Proctor form, in order to qualify for full continuing education credits.

Strafford is required to monitor attendance.

Please refer to the instructions emailed to registrants for additional information.

If you have any questions, please contact Customer Service at 1-800-926-7926

ext. 10.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Partnership Exchanges: Structuring "Drop and Swap" and “Mixing Bowl” Transactions

By: Mark E. Wilensky, Esq. Meltzer, Lippe, Goldstein & Breitstone, LLP

Mineola, New York [email protected]

516-747-0300 x284

&

Maher Haddad, Esq. Baker & McKenzie LLP

Chicago, IL [email protected]

312-861-2666

© 2014 Meltzer, Lippe, Goldstein

& Breitstone, LLP.

All rights reserved.

Strafford Webinar

6

7

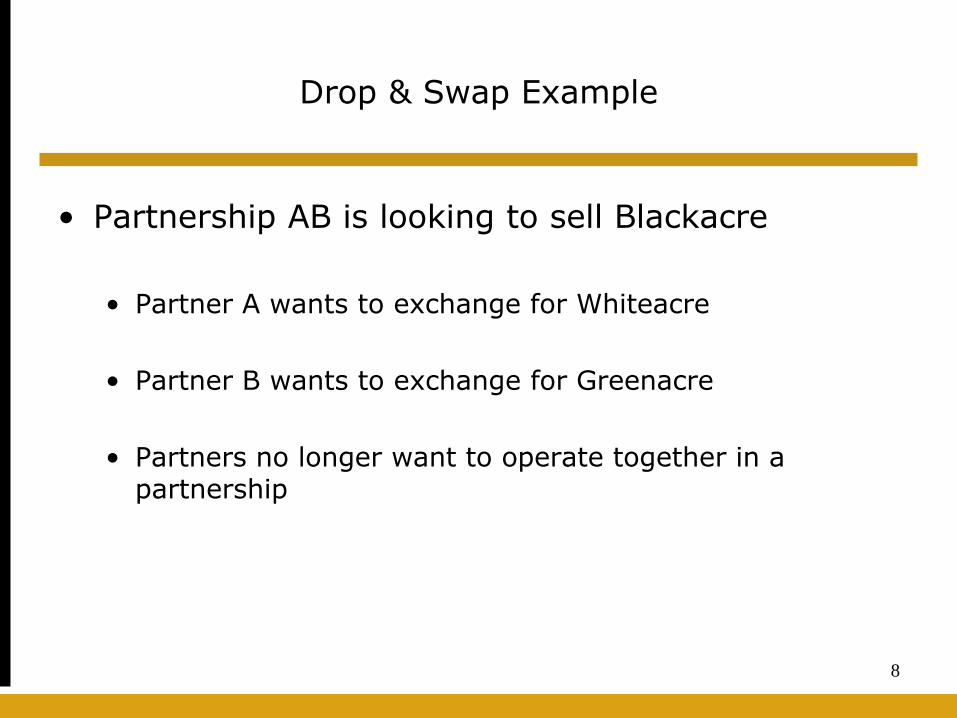

Drop & Swap Example

• Partnership AB is looking to sell Blackacre

• Partner A wants to exchange for Whiteacre

• Partner B wants to exchange for Greenacre

• Partners no longer want to operate together in a partnership

8

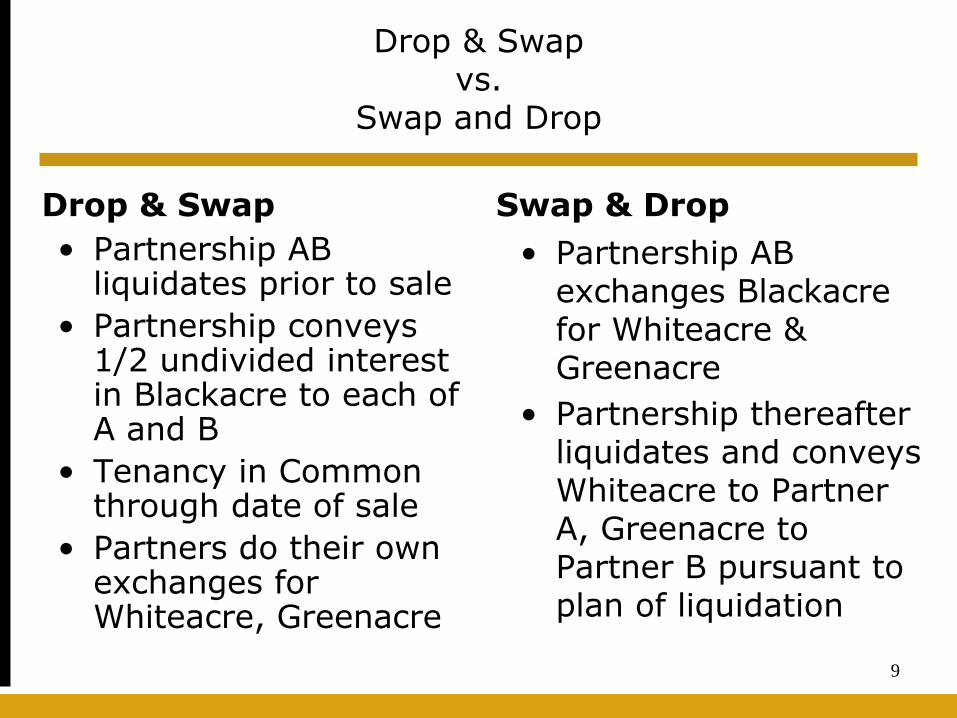

Drop & Swap vs.

Swap and Drop

Drop & Swap

• Partnership AB liquidates prior to sale

• Partnership conveys 1/2 undivided interest in Blackacre to each of A and B

• Tenancy in Common through date of sale

• Partners do their own exchanges for Whiteacre, Greenacre

Swap & Drop

• Partnership AB exchanges Blackacre for Whiteacre & Greenacre

• Partnership thereafter liquidates and conveys Whiteacre to Partner A, Greenacre to Partner B pursuant to plan of liquidation

9

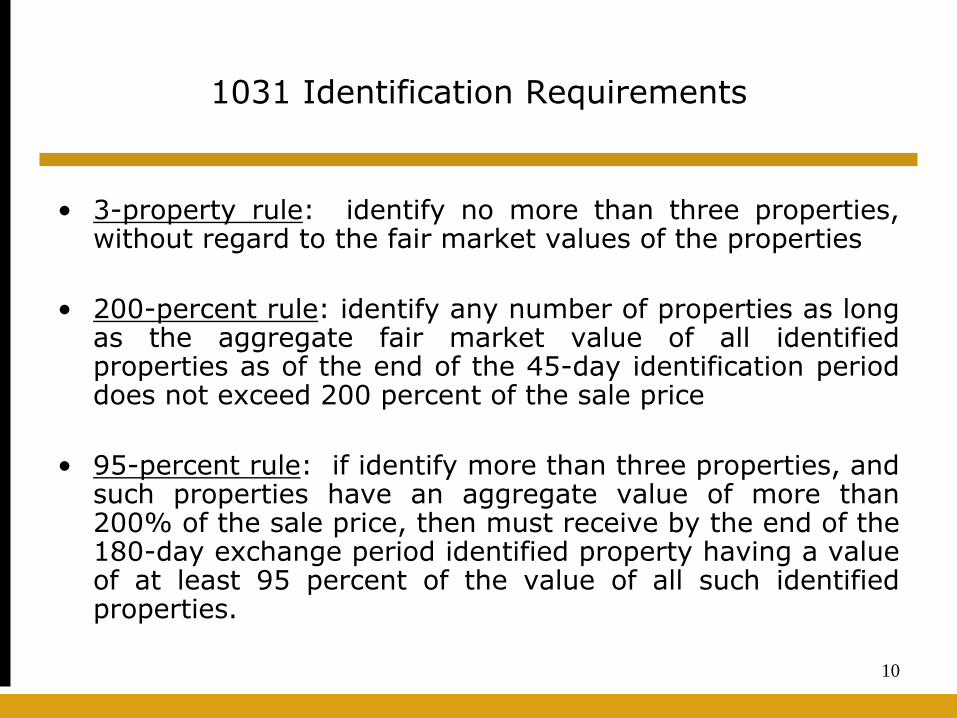

1031 Identification Requirements

• 3-property rule: identify no more than three properties, without regard to the fair market values of the properties

• 200-percent rule: identify any number of properties as long as the aggregate fair market value of all identified properties as of the end of the 45-day identification period does not exceed 200 percent of the sale price

• 95-percent rule: if identify more than three properties, and such properties have an aggregate value of more than 200% of the sale price, then must receive by the end of the 180-day exchange period identified property having a value of at least 95 percent of the value of all such identified properties.

10

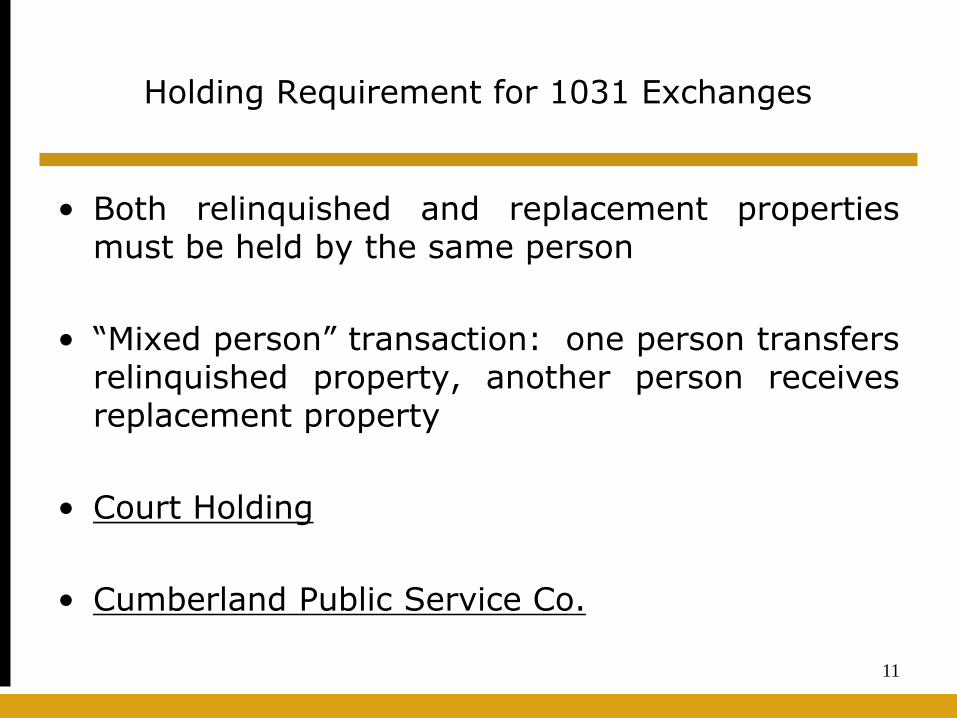

Holding Requirement for 1031 Exchanges

• Both relinquished and replacement properties must be held by the same person

• “Mixed person” transaction: one person transfers relinquished property, another person receives replacement property

• Court Holding

• Cumberland Public Service Co.

11

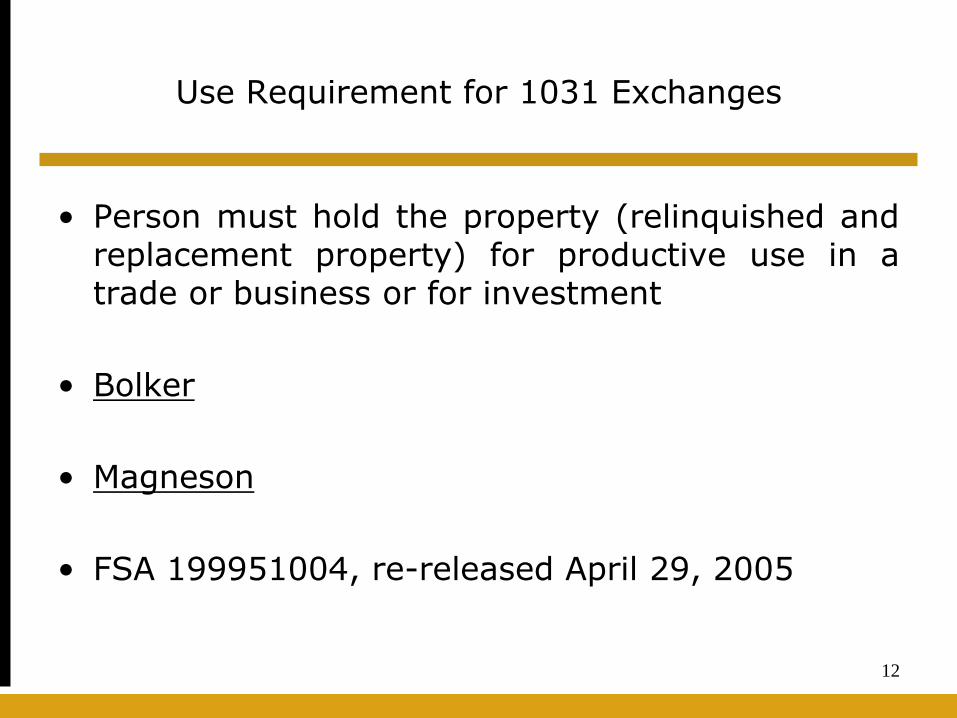

Use Requirement for 1031 Exchanges

• Person must hold the property (relinquished and replacement property) for productive use in a trade or business or for investment

• Bolker

• Magneson

• FSA 199951004, re-released April 29, 2005

12

1031 Not Applicable To Exchanges of Partnership Interests

• Distinguishing tenancy in common from partnership for tax purposes

• Co-ownerships vs. joint business enterprise

• 761 election out of Subchapter K

• IRS Revenue Procedure 2002-22

13

Slide Intentionally Left Blank

Reporting Requirements

• Reporting distribution of TIC interests or distribution of property received in a like kind exchange on Form 1065

• Reporting ownership of tenant-in-common interests on individual 1040s

• IRS Form 8824

15

The 11th Hour Drop & Swap

• Partnership AB is already in contract for the sale of Blackacre, or otherwise about to enter into contract

• Independent business purpose for the distribution of TIC interests?

• Chase

16

Mixing Bowl Example

• A and B each own non-identical interests in a portfolio of 20 real estate LLCs

• Assume the aggregate FMV of all 20 properties is $100 million, and A’s aggregate interest is $40 million and B’s aggregate interest is $60 million

• Assume all 20 properties have built-in gain

• A and B want to separate their investments, with each owning 100% of some of the properties

17

Mixing Bowl Example (con’t)

• A and B each contribute all of their interests in each real estate entity to “Holdings LLC”

• Holdings LLC, as a result, owns 100% of each of 20 real estate LLCs

• A receives a 40% interest in Holdings LLC, and B receives a 60% interest in Holdings LLC

• After, alternatively, two or seven years, Holdings LLC liquidates

18

Mixing Bowl Example (con’t)

• Pursuant to the plan of liquidation, Holdings LLC revalues the real estate LLCs at $110 million and distributes all of its properties as follows:

• a 100% interest in 8 real estate LLCs to A having a value of $42 million plus $2 million cash

• A 100% interest in 12 real estate LLCs to B having a value of $68 million

• Cash, subject to true up

19

Slide Intentionally Left Blank

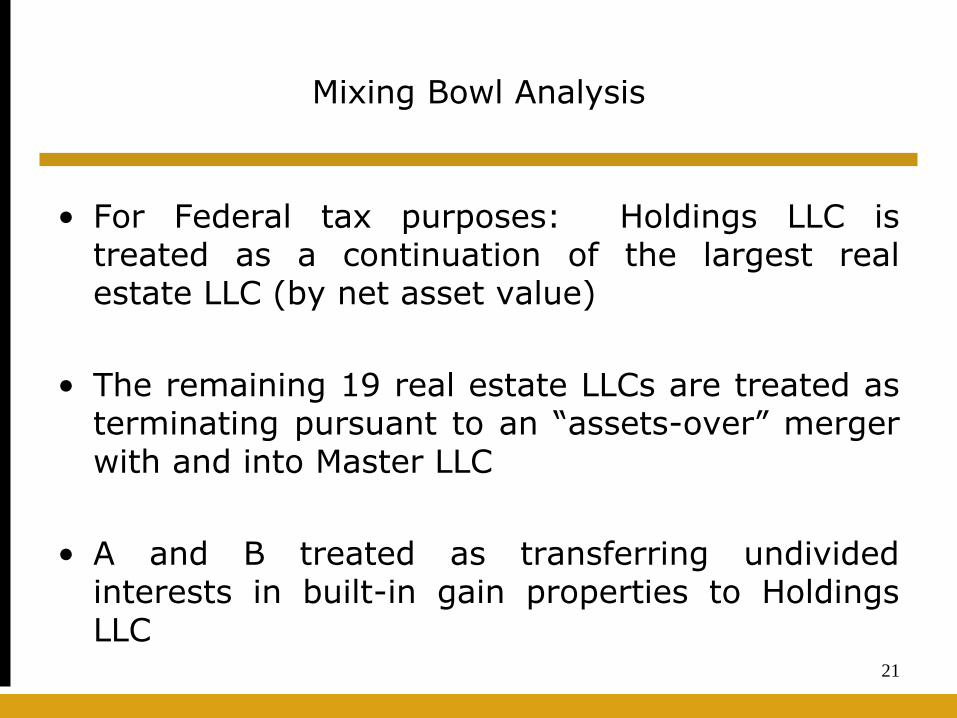

Mixing Bowl Analysis

• For Federal tax purposes: Holdings LLC is treated as a continuation of the largest real estate LLC (by net asset value)

• The remaining 19 real estate LLCs are treated as terminating pursuant to an “assets-over” merger with and into Master LLC

• A and B treated as transferring undivided interests in built-in gain properties to Holdings LLC

21

Mixing Bowl Analysis (con’t)

22

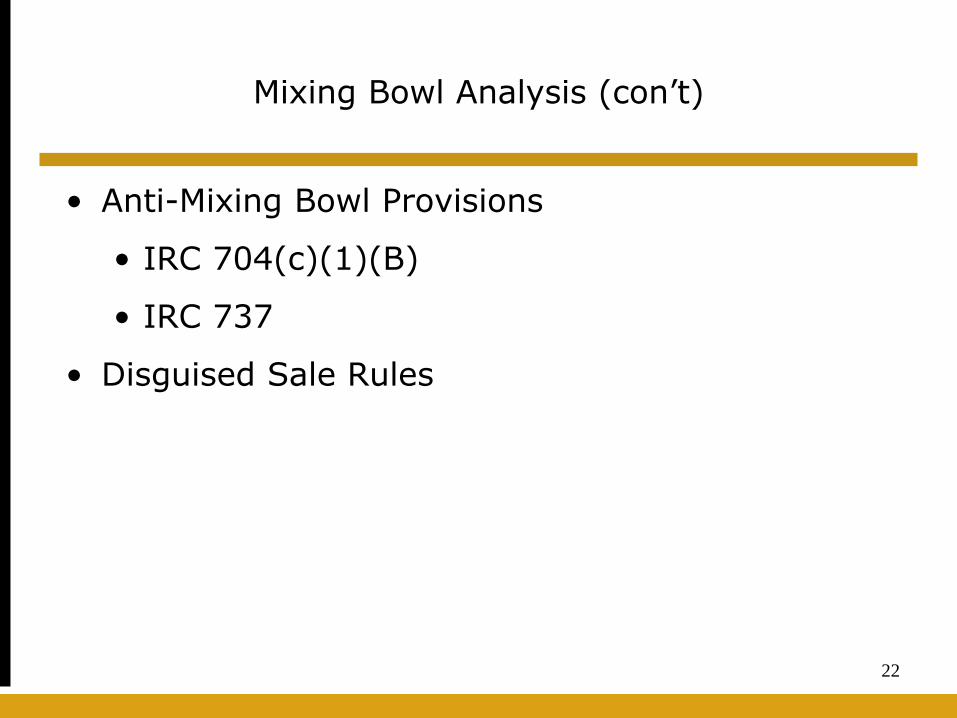

• Anti-Mixing Bowl Provisions

• IRC 704(c)(1)(B)

• IRC 737

• Disguised Sale Rules

Anti-Mixing Bowl Rule #1: IRC 704(c)(1)(B)

23

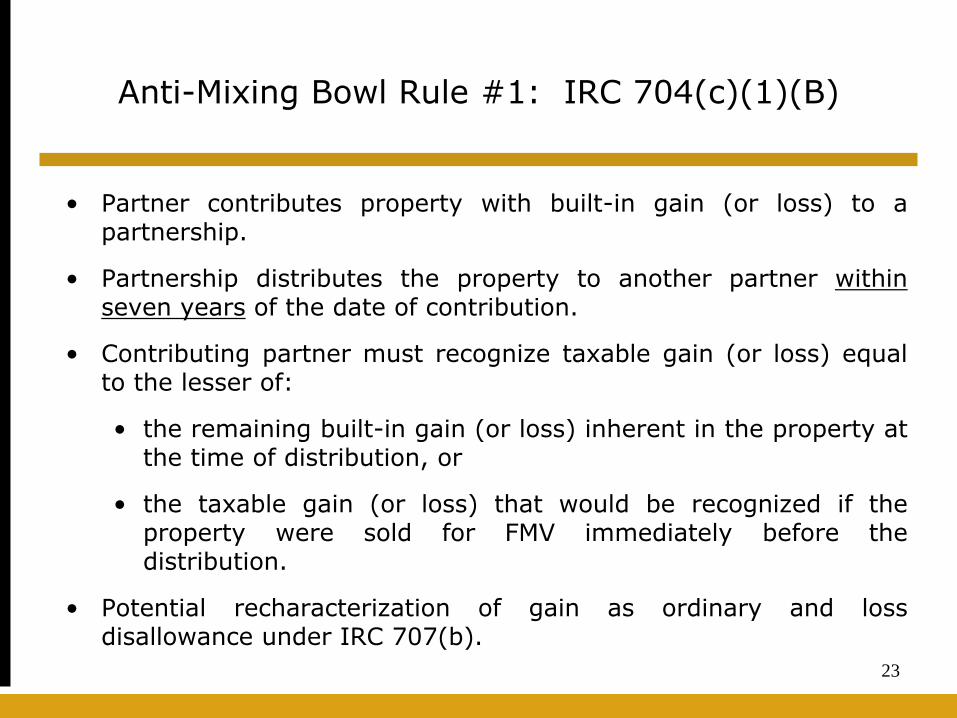

• Partner contributes property with built-in gain (or loss) to a partnership.

• Partnership distributes the property to another partner within seven years of the date of contribution.

• Contributing partner must recognize taxable gain (or loss) equal to the lesser of:

• the remaining built-in gain (or loss) inherent in the property at the time of distribution, or

• the taxable gain (or loss) that would be recognized if the property were sold for FMV immediately before the distribution.

• Potential recharacterization of gain as ordinary and loss disallowance under IRC 707(b).

Anti-Mixing Bowl Rule #2: IRC Section 737

24

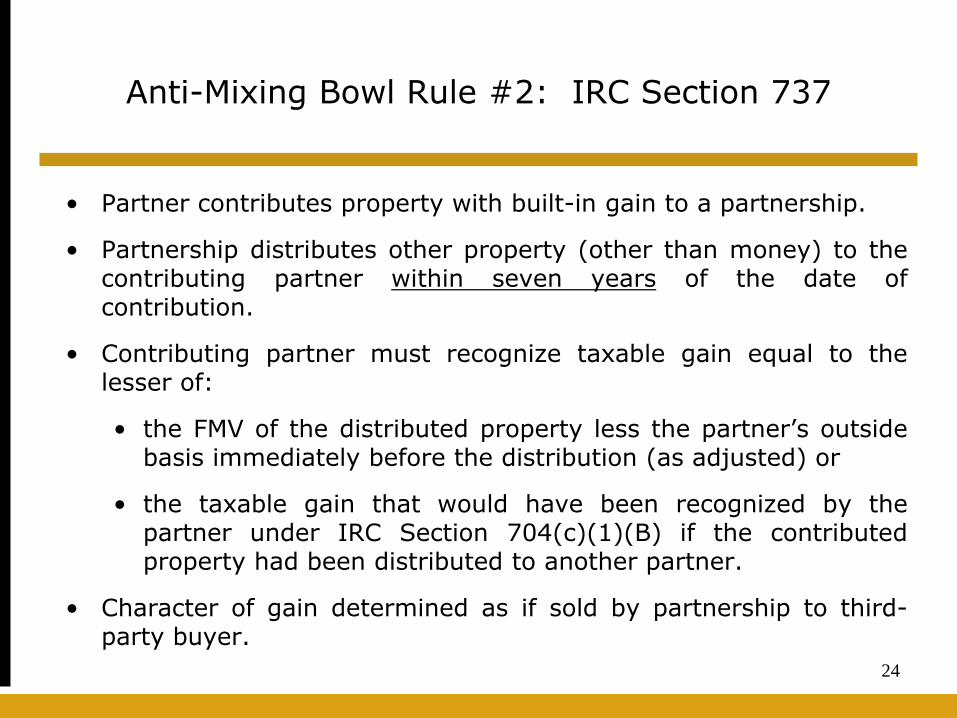

• Partner contributes property with built-in gain to a partnership.

• Partnership distributes other property (other than money) to the contributing partner within seven years of the date of contribution.

• Contributing partner must recognize taxable gain equal to the lesser of:

• the FMV of the distributed property less the partner’s outside basis immediately before the distribution (as adjusted) or

• the taxable gain that would have been recognized by the partner under IRC Section 704(c)(1)(B) if the contributed property had been distributed to another partner.

• Character of gain determined as if sold by partnership to third-party buyer.

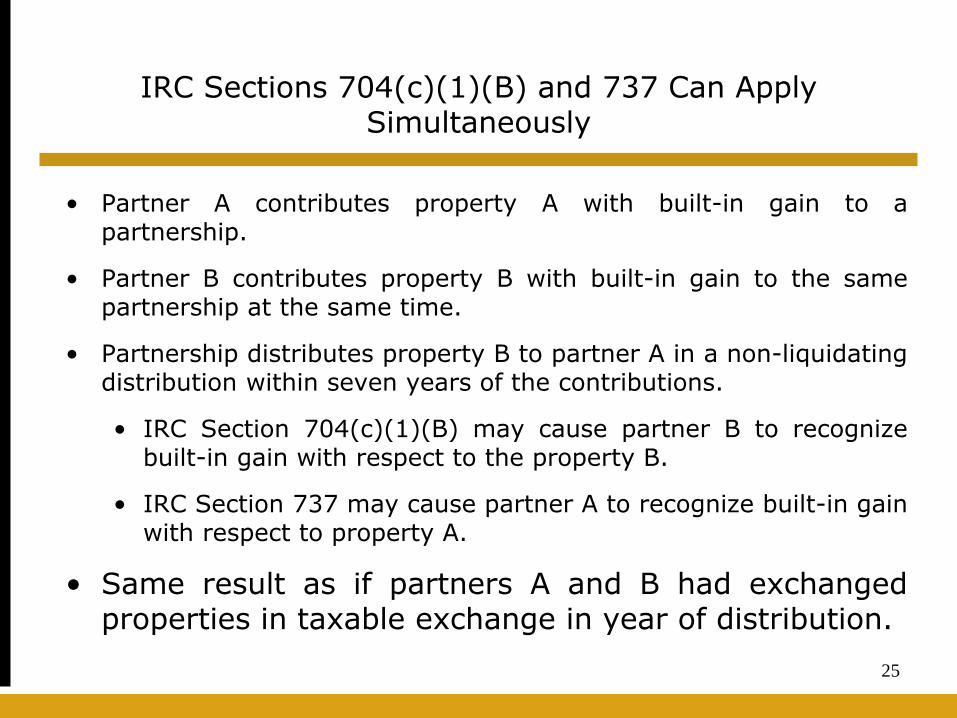

IRC Sections 704(c)(1)(B) and 737 Can Apply

Simultaneously

25

• Partner A contributes property A with built-in gain to a partnership.

• Partner B contributes property B with built-in gain to the same partnership at the same time.

• Partnership distributes property B to partner A in a non-liquidating distribution within seven years of the contributions.

• IRC Section 704(c)(1)(B) may cause partner B to recognize built-in gain with respect to the property B.

• IRC Section 737 may cause partner A to recognize built-in gain with respect to property A.

• Same result as if partners A and B had exchanged properties in taxable exchange in year of distribution.

Slide Intentionally Left Blank

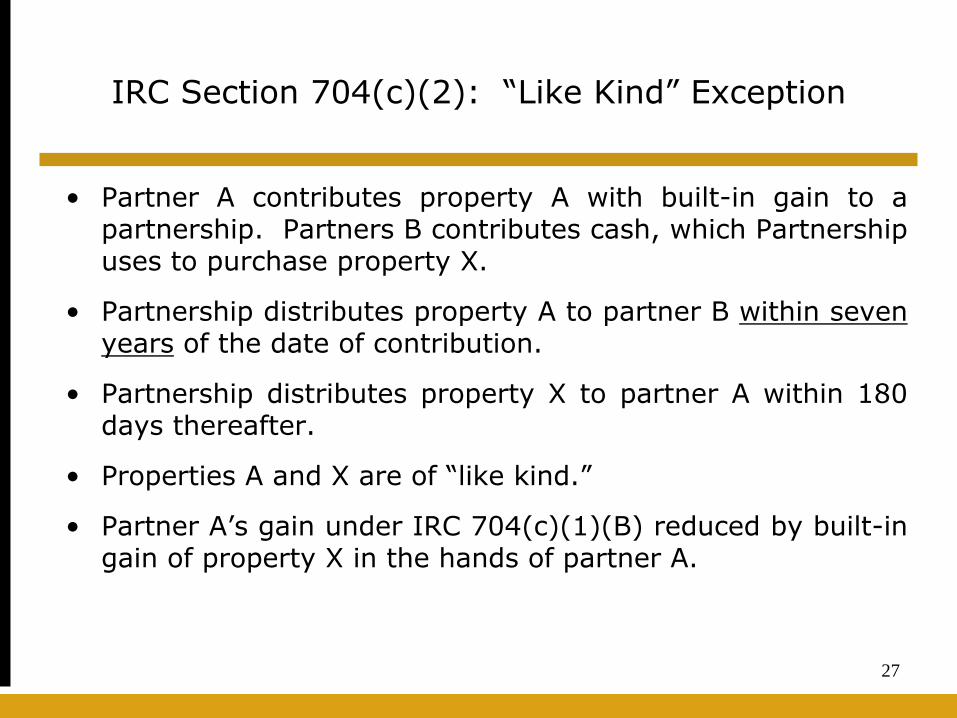

IRC Section 704(c)(2): “Like Kind” Exception

27

• Partner A contributes property A with built-in gain to a partnership. Partners B contributes cash, which Partnership uses to purchase property X.

• Partnership distributes property A to partner B within seven years of the date of contribution.

• Partnership distributes property X to partner A within 180 days thereafter.

• Properties A and X are of “like kind.”

• Partner A’s gain under IRC 704(c)(1)(B) reduced by built-in gain of property X in the hands of partner A.

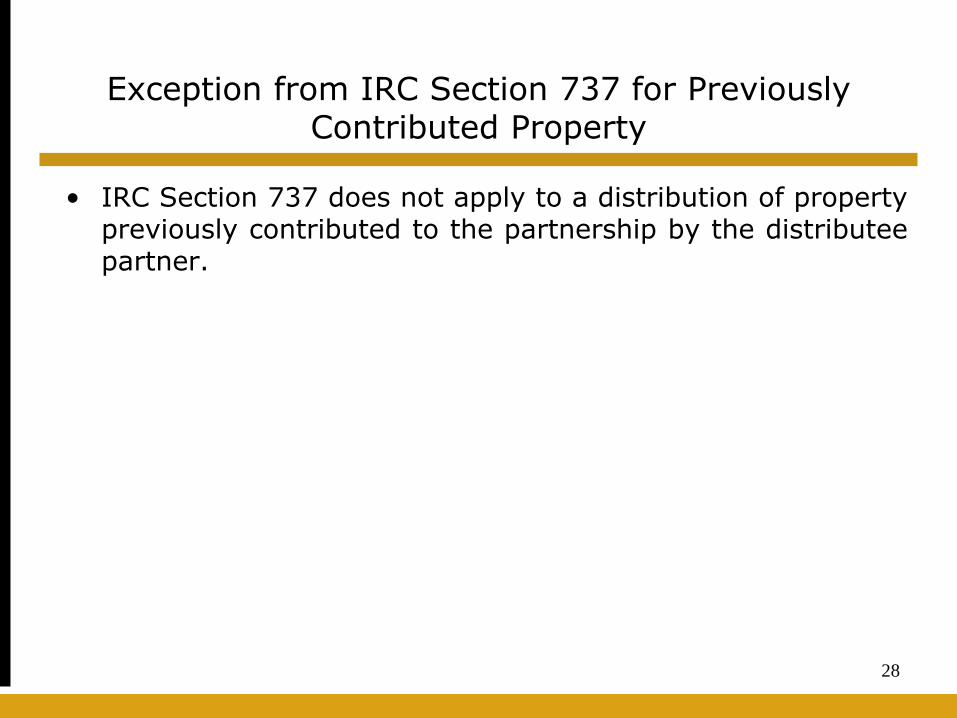

Exception from IRC Section 737 for Previously Contributed Property

28

• IRC Section 737 does not apply to a distribution of property previously contributed to the partnership by the distributee partner.

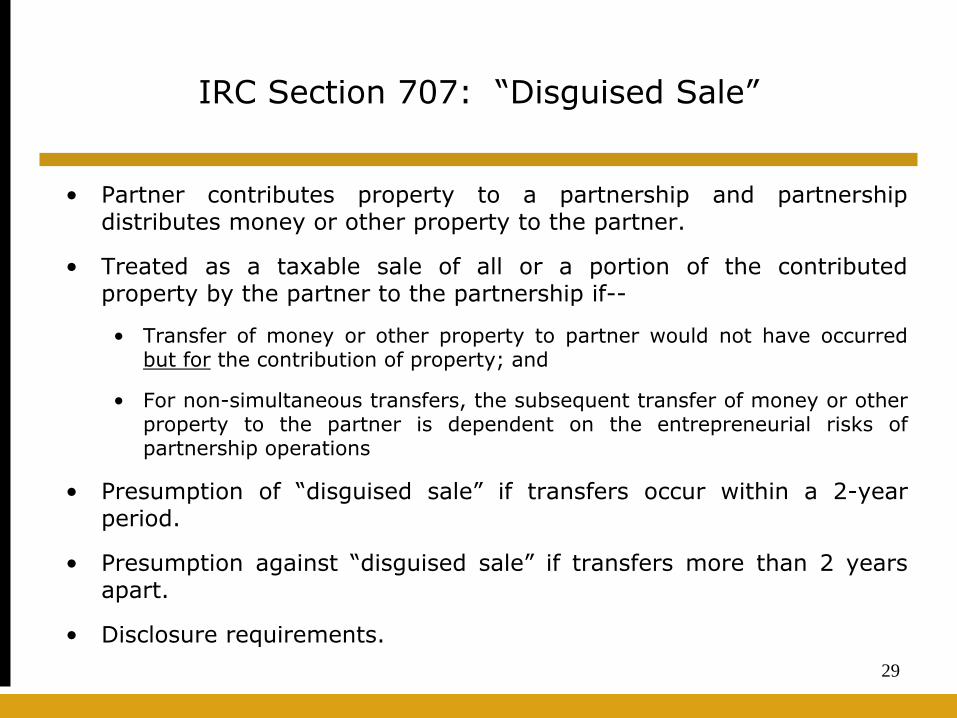

IRC Section 707: “Disguised Sale”

29

• Partner contributes property to a partnership and partnership distributes money or other property to the partner.

• Treated as a taxable sale of all or a portion of the contributed property by the partner to the partnership if--

• Transfer of money or other property to partner would not have occurred but for the contribution of property; and

• For non-simultaneous transfers, the subsequent transfer of money or other property to the partner is dependent on the entrepreneurial risks of partnership operations

• Presumption of “disguised sale” if transfers occur within a 2-year period.

• Presumption against “disguised sale” if transfers more than 2 years apart.

• Disclosure requirements.

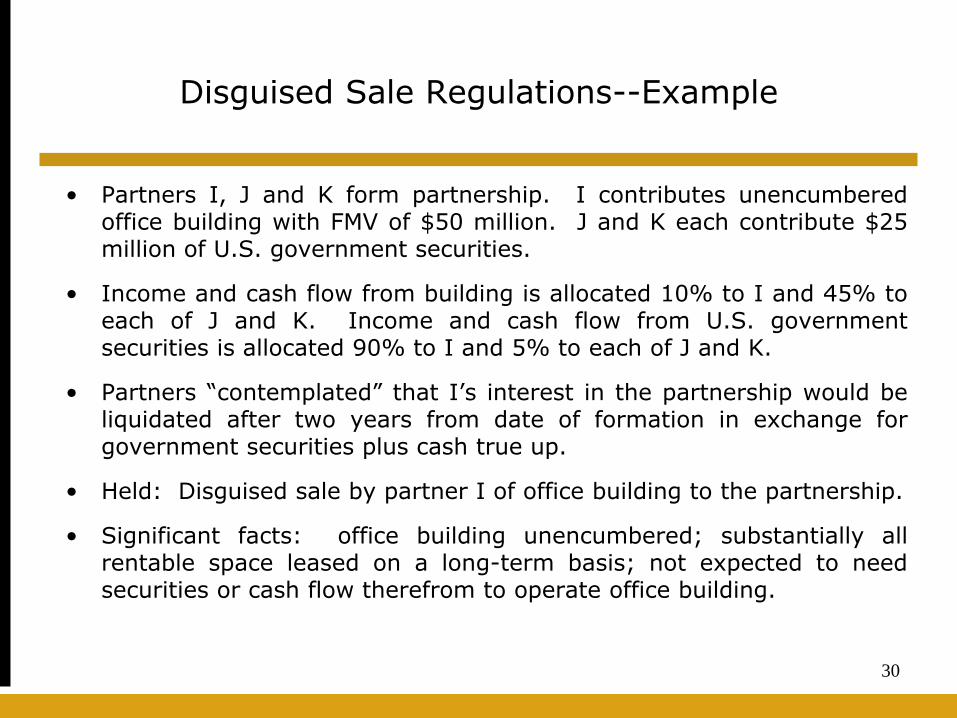

Disguised Sale Regulations--Example

30

• Partners I, J and K form partnership. I contributes unencumbered office building with FMV of $50 million. J and K each contribute $25 million of U.S. government securities.

• Income and cash flow from building is allocated 10% to I and 45% to each of J and K. Income and cash flow from U.S. government securities is allocated 90% to I and 5% to each of J and K.

• Partners “contemplated” that I’s interest in the partnership would be liquidated after two years from date of formation in exchange for government securities plus cash true up.

• Held: Disguised sale by partner I of office building to the partnership.

• Significant facts: office building unencumbered; substantially all rentable space leased on a long-term basis; not expected to need securities or cash flow therefrom to operate office building.