payment week - andrew barnes, managing director__citi ventures

TRANSCRIPT

MAY 11 - 16, 2014 Visit PaymentWeek.com

Exclusive Q&A with Avangate’s CMO/SVP Mike Ni

The No Checkout – What’s the Big Deal?

ALSO INSIDE:

Square Wants You to Skip Lines with Its New Order App

2F E A T U R E D A R T I C L E S

Felix ShipkevichFOUNDER

Jason MongielloDIRECTOR OF MARKETING

GRAPHIC DESIGNER

Kevin XuEDITOR

CONTENT STRATEGIST

Andrew BarnesMANAGING EDITOR,

EMERGING PAYMENTS

Kyle DowlingCONTRIBUTING WRITER

Jane GenovaCONTRIBUTING WRITER

Michael FosterCONTRIBUTING WRITER

Helen Wallis CONTRIBUTING WRITER

David CrossCONTRIBUTING WRITER

Corporate Office65 Broadway

Suite 508New York, NY 10006

For Advertising Rates:[email protected]

2014 Lamil Media Inc. All rights reserved. The content of this publication may not be reproduced by any means, in whole or in part, without the prior written consent of the publisher. Requests to reuse materials published in Payment Week should be directed towards our

editor.

M A R K E T P L A C E

T E C H

E M E R G I N G P A Y M E N T S

Digging Deeper with Citi Ventures: Helping Startups Climb the Mountain of Payments

Lisa Stanton, President of the Americas at Monitise talks about the differences in U.S. and Asia markets, developing new domestic commerce networks, and building out partnerships with huge financial

players.

S P O T L I G H T A R T I C L E

4 - It’s Time You Were Introduced to Social Media Payments

3 - LevelUp Wheeling and Dealing with Zuppler and Revention

I N D U S T R Y V O I C E S

6 - Financial Institutions Find Value in Bitcoin7 - Doge Vault Shuts Down as Dogecoiners Struggle to Keep Supporters in Good Spirits

M A Y 1 1 - 1 6 , 2 0 1 4

8 - The No Checkout – What’s the Big Deal?

10 - Stadium and Event Purchases Made Easier with DataCash and Sports Fusion Collaboration

13 - Square Wants You to Skip Lines with Its New Order App

11 - Consumer Tips: The Double-Edged Sword of Credit Card Rewards

21 - Digging Deeper with Citi Ventures: Helping Startups Climb the Mountain of Payments

14 - Exclusive Q&A with Avangate’s CMO/SVP Mike Ni

T E C H

3

Mobile

LevelUp Wheeling and Dealing with Zuppler and Revention By: Kevin Xu

LevelUp, QR code-based mobile payments and loyalty platform, is making major moves this week.

The company has inked partnerships with Zuppler and Revention to target both consumer and merchant-side payments to bolster their numbers.

Zuppler, a Pennsylvania-based mobile and online food ordering service, will allow their customers to pay with LevelUp, and in turn, receive loyalty rewards and incentives through LevelUp-enabled restaurants.

In total, Zuppler and LevelUp have on board 18,000 restaurants and over 2 million customers.

Revention, a point-of-sale hardware and software provider, will enable LevelUp support for their merchants across their line of solutions.

This means that merchants using Revention platforms can choose to support LevelUp payments and offer loyalty rewards to drive repeat purchases.

LevelUp, based in Boston, has seen a steady uptick in users throughout the last few months. It reported an increase of active users (defined by five or more purchases made per month) from 80,000 in January, to 110,000 currently.

LevelUp boasts a total user count of 1.5 million thanks in part to its partnership with Dunn Bros. Coffee, and providing white-labeled solutions to partners.

It also cut processing fees from 2 percent of every transaction, to 1.95 percent, thanks to streamlining the way they carry out payment processing.

While it admittedly isn’t a significant margin, every bit helps in trying to onboard more merchants, especially for SMBs, a segment that LevelUp is particularly popular with.

The company’s ultimate goal is to push transaction fees to 0 percent, and make money on facilitating loyalty rewards.

Image credit: LevelUp

4T E C H

4

Social Media

It’s Time You Were Introduced to Social Media Payments By: Kyle Dowling

If you haven’t heard the term social media payments, don’t worry, you’re not alone; but chances are you will most likely in the not so

distant future.

The newly introduced term encompasses the rapidly growing utilization of a payments program in today’s ever so popular social media environment.

And like so many things, it all seems to be starting with Facebook… with Apple coming up just behind.

Some time ago, the social media mega-giant announced they would be starting up their own payments plan, a program that would allow users to purchase items directly through a Facebook payments system with other users by keeping money on the social media platform, even with mobile payments. In short, think of it as Facebook’s PayPal.

Due to the growth in the mobile payments industry, many believe the mobilization of business has now changed an array of industries, morphing e-commerce to m-commerce – a new stage where even the highest ranking and respected organizations are striking to take their business mobile.

In the payments industry, it’s go mobile or go home.

Over the years, as the time it has taken to transfer data through mobile has decreased, the demand for more mobile payments have increased vastly.

Payment systems such as PayPal and Authorize.net pioneered an industry that has forever changed the way we do business.

Each and every month, more and more apps are created, utilized and eventually sold for an immense

T E C H

5

profit, proving that they are an essential part of our day-to-day lives.

According to Deborah Baxley, Principal at Capgemini Financial Services, “Pioneers like PayPal, Uber and Airbnb leverage the power of mobile and social to create trust in marketplaces and enable a type of commerce that had been impossible previously.”

Programs such as WhatsApp, Viber, and Gilt, are all taking shape to form our new, mobile economy. We can now get whatever we want without ever having to leave our homes.

What started out as a way to exchange mere messages, videos, images, thoughts and ideas – a personal exchange – has grown so far to become an actual industry, a place where not only are the aforementioned personal exchanges are met, but also monetary exchanges for the very things we find ourselves needing to survive.

With that in mind, perhaps the next evolution of social media platforms is to facilitate payments, while our ways to pay become increasingly social.

6E M E R G I N G P A Y M E N T S

6

Digital Currencies

Financial Institutions Find Value in Bitcoin By: Daniel Cross

Image credit: Antana Coins

Despite temporary setbacks in hacking concerns and price stability, bitcoin is quickly becoming mainstream, and financial

institutions are taking notice.

Banks have begun to take notice of how cryptocurrencies are able to move money cheaply and quickly, legitimizing it in the eyes of large financial institutions. JP Morgan even sent in patent applications for its own version of a digital currency closely resembling bitcoin late last year (which were rejected).

Bitcoin’s software works by making a public record of transactions.

Payments made with bitcoins are almost immediately registered and recorded which means that the same bit of currency can’t be duplicated. Transactions are verified by the use of computers who are then awarded new bitcoins — the basis of bitcoin mining.

Fiserv, a global provider of IT management and e-commerce systems for the financial services industry is considering ways to replicate bitcoin’s

open ledger system to move funds securely across its network.

While the use of the cryptocurrency itself may not be implemented, the underlying design of encryption involved in transfers could be the next innovation for major banks to compete in the near future.

Credit cards and international wire transfers may soon find themselves out of business thanks to the information technology that bitcoin utilizes. Payment systems that don’t clear immediately and come with fees are quickly being supplanted by mobile money remittance services, and slowly, digital currencies.

The cloud of doubt cast over digital currencies surviving government regulations may put online monies like bitcoin out of service, but its technology may be what survives the aftermath.

As financial institutions come to realize the value of this new technology, current systems like Automated Clearing House (ACH) fund transfers may soon be replaced by public ledgers used by bitcoin and other digital currencies.

E M E R G I N G P A Y M E N T S7

7

Digital Currencies

Doge Vault Shuts Down as Dogecoiners Struggle to Keep Supporters in Good Spirits By: Michael Foster

Online wallet Doge Vault has shut down, with the site officially stating their “online wallet service was compromised by attackers.”

Early reports said hackers had infiltrated and destroyed the online wallet’s data, and it is not clear how many coins were lost by the service’s users.

While Dogevault has encouraged members to email them for a status update, little additional information is currently available.

While it is impossible to know if all dogecoins have been permanently lost, the attack on Doge Vault is the second such attack of an online wallet service in less than three months, leaving unanswered questions and greater doubts about the future of cryptocurrencies.

Near the end of February, one of the most popular online exchange for bitcoins, Mt. Gox suddenly announced they were shutting down and filing for bankruptcy, causing that currency to lose nearly a third of its value.

Since the fall of Mt. Gox, Dogecoin has quickly become a favorite amongst alternative cryptocurrency enthusiasts, with even Reddit’s CEO embracing the currency and dismissing Bitcoin’s fans as “basically crazy libertarians.”

The alternative digital currency, which took inspiration from an internet meme featuring Shiba Inu dogs with grammatically head-scratching captions written in comic sans, has found traction as a form of online tipping on message boards and forums.

Dogecoin’s ardent supporters have tried to introduce its currency to a larger mainstream audience through several promotions, such as a recent promotion of NASCAR driver Josh Wise, giving both the currency and Wise major mainstream news exposure.

While Dogecoin’s supporters are attempting to bolster the spirits of their fellow currency users, affectionately called “Shibes,” more cynical critics are quick to point out that the plan has so far been unsuccessful, with die-hard NASCAR fans telling reporters they think Dogecoin is possibly German money or “it’s currency that dogs use.”

8E M E R G I N G P A Y M E N T S

8

Card Solutions

The No Checkout – What’s the Big Deal? By: Jane Genova

The idea of consumers shopping at brick and mortar stores without

checking out is making the rounds.

This is not self check out. It’s “no checkout.”

One phrase associated with it has even become sticky: “It feels like stealing.” But eventually “stealing” could become a standard option in stores.

However, the media attention ducks a tough reality. In itself, no new introduction in the payment system will do much to transform the distressed brick and mortar retail sector.

Essentially, with no checkout, electronic virtual networks link the identity of customers and how they prefer to be billed with the merchandise selected.

For example, a shopper tries on a dress, likes it and wears it out of the store without scanning or having it scanned at a checkout. And that’s about all most customers need to know regarding the sensors which are picking up, transmitting, and aggregating data.

It’s hardly futuristic.

For a number of years, it’s been leveraged in Apple retail through the iPhone.

Also, the transaction will not likely “feel” like stealing. Shoppers sophisticated enough to be using it are well aware that there is a bill waiting for them in cyberspace.

In addition, in some sectors, electronic ways of payment have become commodities. They are expected or represent the

price of entry. Not having them could put them at a competitive disadvantage but their presence isn’t necessarily experienced by customers as competitive differentiation.

For instance, in the flat fast food industry, some chains such as Burger King and Wendy’s have been embracing mobile payments. Their objective is to win back market share from casual restaurants and convenience stores. Not too many stock analysts are bullish that the tactic will be effective.

This isn’t to say there are no benefits to retailers who want to enable a no checkout system.

At the top of the list is reducing operational costs. Those extend from the amount of floor space needed to personnel headcount. Another is a faster and more

E M E R G I N G P A Y M E N T S9

9

efficient service by eliminating a step from shopping. Accuracy could be increased. The presence of a constantly enabled network could deter theft, both by shoplifters and employees.

In addition, customers who have come to dislike the cross-selling at human checkout points get to avoid it completely.

But much more than a sophisticated payment system is needed to address the challenges brick and mortar is dealing with. This is the era of the omnichannel in retail.

The customer shopping experience has become fluid, including both online and brick and mortar. They go to the physical store for a myriad of reasons.

If it’s to actually purchase something, too often, unlike online, it is isn’t available. Brick and mortar inventory systems tend not to have kept up with those online.

Should the visit to the store be to have staff provide information and insight about the products or services, they might be disappointed. Expectations have been raised by the kind of expertise available at Apple and other leading retailers who pride themselves on the knowledge their employees possess about the products and services that they’re offering.

The purpose might be to take advantage of discounts only provided at the store. However, it might be customers who inform

clerks about them and who have to be alert that they are rung up accurately.

The benefits of no checkout can be incorporated in solving some of these problems. For instance, funds saved can be invested in improving the inventory system. Personnel freed up can be developed as experts for special lines of products and services.

The bottom line may well be that the payment function can’t exist as a silo in the retail organization.

Mega successful Starbucks frames payment introductions as simply an aspect of their all-encompassing plan to enhance the customer experience.

Shouldn’t that be the goal of all businesses?

10E M E R G I N G P A Y M E N T S

10

Card Solutions

Stadium and Event Purchases Made Easier with DataCash and Sports Fusion Collaboration By: Daniel Cross

Sports clubs and organizations primarily make money off of the games they host from ticket sales and merchandise, but a new opportunity

has emerged that will drive revenue streams even higher.

Alternate activities such as stadium tours, restaurant bookings, parking, day-events, and other miscellaneous enterprises are now easier than ever to manage. Up-to-date IT systems allow customers to make purchases and book events in a safe and simple manner.

The normally partitioned stand-alone services associated with stadiums and sports venues has become one dynamic system thanks to the partnership between MasterCard’s DataCash global payment processing service and Sports Fusion, a European sports IT company.

Fast and secure payment transactions take place online, in-store, and at events with DataCash now

fully integrated into Sports Fusion’s IT management platform. Sports businesses and event organizations benefit from custom creative solutions to give customers the best possible experience.

Brands like Liverpool Football Club and Chelsea Football Club, some of the biggest and most popular names in the world, are taking advantage of the added benefits provided by DataCash and Sports Fusion.

A continuous stream of purchases come from customers from the moment they arrive at a stadium and are now able to be serviced under one roof.

The worldwide popularity of European football means that teams will be able to expand their brands to other countries with DataCash’s global presence. Currency exchanges are simplified which will add even more fans to the sports clubs and ultimately to their bottom line.

E M E R G I N G P A Y M E N T S11

11

Card Solutions

Consumer Tips: The Double-Edged Sword of Credit Card Rewards By: Jane Genova

With the economic recovery picking up momentum, credit card issuers are gunning for increased market share. One

prevalent marketing strategy is stepped-up credit card rewards programs.

Some economists predict that Q2 2014 GDP growth could hit 4%. That’s an amazing turnaround from the anemic Q1 2014 GDP Growth of 1%.

Financial institutions issuing credit cards are expecting a surge in the number and amount of purchases on credit cards. To capture that activity, they are focusing on making their rewards align with what different kinds of consumers want. However, consumers will have to be wary of some of the rewards programs.

A typical problem is that the terms and conditions of many programs are convoluted.

At first glance, consumers may be attracted to

5 percent cash back on quarterly purchases of everyday items such as gasoline and dining at certain restaurants. The catch though, is that consumers may have to opt-in every quarter for that.

They must also be aware that there are usually limits on the amount of purchases that are eligible for cash. If they aren’t paying attention, they might charge way more than the limit, with no reward.

Another kind of confusing set of terms and conditions could be the reward which provides, for example, $500 back for travel.

But to qualify for this, consumers have to charge $3000 on their cards during a three month timeframe. If consumers aren’t tracking the numbers closely, they could wind up charging too little or too much to make the reward pay off for them.

Related to that is the growing proliferation of

12E M E R G I N G P A Y M E N T S

12

different categories of “deals” among various cards. Consumers seriously focused on taking maximum advantage of rewards might wind up applying for many cards and carrying them all in their wallets.

Some may apply for multiple cards with rewards that pertain to shopping for groceries and travel rewards for example, and with an increased ability to spend, comes an increased necessity for fiscal responsibility.

There is also the ever-present peril of introductory offers which, of course, eventually expire.

However, consumers can game that system by enjoying the reward and never using that particular credit card again. That’s analogous to doing serial transfers of credit card balances at zero interest and never having to eventually pay the high interest rates which kick in after the promotional offer.

Consumers also have to be wary about signing up

for a credit card which offers attractive rewards, with the annual fee waived for the first year. Come the second year, consumers may or may not notice the annual fee tacked on to their credit card bill. That can range anywhere from $95 to $175.

Obviously, the “price” for rewards has to be calculated in a number of ways. At the top of the list is the human cost of time and energy invested in monitoring offers and following the letter of the “law” for different rewards programs.

Next is the temptation of having too much credit available because of signing up for so many cards.

A mindset that spending equals goodies is not necessarily a terrible one to have. Card issuers get on board more members who spend more, and consumers get more bang for their buck, but these same consumers must remain vigilant in their spending habits.

13M A R K E T P L A C E

13

Industry Leaders

Square Wants You to Skip Lines with Its New Order App By: Kevin Xu

Square is shifting gears in the mobile wallet wars.

The payments company is scrapping its Wallet mobile app and replacing it with a new payment app called Order.

It’s currently available for iOS and is in beta for Android users.

While functionally the same in enabling consumers to pay for goods and services at Square-partnered retail locations, Order is shifting the focus to the increasingly popular food and beverage scene.

Order’s main selling point is that it will allow customers to order and pay ahead for their coffee or meals, and pick them up when they want at merchants participating in Square Pickup, skipping lines and eliminating the need to ever have to wait again.

It’s no surprise then that Square is launching Order in the hustle and bustle cities of New York and San Francisco, where ordering food through online or mobile is particularly popular, and there are plans

to bring Order to cities nationwide.

One caveat – Square will be directly competing with online food-ordering companies such as GrubHub Seamless.

It’s a risk that Square may want to take if it can bolster its offerings and present itself to merchants as more than just a mobile credit card reader provider.

Square’s merchant services and tools already include Dashboard, Square Register, Stand, and Market.

If Square can add and find success in consumer-facing services such as Order, and its person-to-person payment service, Cash, it may lead to more merchants and retailers processing payments through Square since there’s a promise of driving more (efficient) business.

Square will initially take a 2.75 percent cut on purchases made through Order, and after July 1st, it will be up to 8 percent.

Image credit: Antana Coins

I N D U S T R Y V O I C E S

14

Interviews Exclusive Q&A with Avangate’s CMO/SVP Mike Ni By: Kevin Xu

We got to chat with Avangate’s Mike Ni, who discussed why cloud technology is so disruptive in payments, building out

a B2B and B2C platform on a global scale, and a Bitcoin tease.

Hi Mike, let’s get a breakdown on Avangate.

At Avangate, we are a commerce platform. A lot of people blend or blur the line between payment processing provider, service provider and commerce.

But just to provide a little more definition, we look at commerce as really five key blocks. Not only global payment, which we do in terms of helping customers go globally, but for the other key modules that are part of our whole platform. One is how do you sell and even optimize that online selling, right, and sell service? How do you reach out to management? How do you sell through a reseller?

The new, rich media we are forming, there’s a lot going on online. How do you actually manage to bridge the online and offline world? How do you actually manage not only your own affiliate, but we have a whole network of over 40,000 affiliates in the software and services world. Then finally, subscription billing.

Very fundamental to not only the new economy, but frankly, services in particular like subscription, freemium, fractional ownership. These are all things that become fundamental to this business model surrounding services. So that’s sort of in a nutshell all on our cloud-based platform. We have over 3,400 customers on our platform leveraging us for payments and commerce.

Can you speak to your rate of growth?

I N D U S T R Y V O I C E S

15

We’ve been around I think since 2006, when we first launched. When we were going for a round of funding by Francisco Partners – they see this world moving very rapidly around services, digital commerce, and digital goods – and as such, helped not only fund us for growth, but actually bought out our previous investors as well.

Of course, part of this movement as a company, we’ve been signing not only partners, but also winning a bunch of awards for growth, for leadership in building an e-commerce platform, as well as made partners or vendors for commerce last year. Of course, we’ve been closing customers, both B2C and B2B, folks for online financial services via subscription, as well as HP, as they make their shifts towards selling their own product as a cloud service.

And part of this gets into the trend behind what we see as this huge shift towards services as a whole, which is products are dead, right?

What we see more and more is that with customers being able to have a lot of choice, products increase and commoditize, frankly. People are increasingly looking to add on service contracts, turning their products into a service, being able to add and innovate around the visual aspects of their business to drive up the margins of their business.

We see this across multiple customers who are making this shift and us helping them do so. And it’s a massive growth, right, across multiple industries.

We started in software, which is like a Kaspersky World, and have quickly moved from there as those turn into cloud services, which like iYogi and TechLive Connect, are consumer tech support, right? Purely service contract. How do I actually get someone to help me pay for that service? So a very rapid change for us in an industry that we see

changing very rapidly.

I see a general trend in cloud computing; cloud technology being the next movement, driver of business. How are you leveraging this technology to help B2B, B2C companies?

Sure. Two things going on. Or let’s start with three things.

Number one, the cloud has changed how people are buying. Because what’s happening is, the cloud made it easier to consume in smaller bits.

Let’s take HP for an example, right? What’s happened was they were making consumer sales or inside sales and they had mid-market sales guys and above. In one year, they saw the small end of the business starting to trend downwards.

And they said, “It’s okay. We’re more of an enterprise play.” But what was really happening was the cloud had changed what people were buying. People were buying one or two, five. They were buying in smaller chunks.

And those customers, when you get in, has a foot in the door, who get the RFPs for the bigger deals. So you see, big companies needed to make a shift because the cloud fundamentally changed what B2B customers are buying. In the same way, sort of like MyFICO, for instance.

If you look at the cloud here, when you look at how people engage online, how did they discover a service. And how do you now offer it to them so that you can give them guidance on how to manage their credit scores.Help them with a monitoring service that helps alert them, right?

These are all services that were not possible

I N D U S T R Y V O I C E S

16

without the cloud. When we talk about not only being able to package that, but then to be able to sell it, right, you talk about being able to sell it online, being able to create multiple packages very quickly, and then turn on and off on different times. Now let me tell you why this is difficult and why companies need to turn to a commerce solution.

For instance, almost any of these companies, they had an ERP system in the backend that they’re building on. So when I was a product manager in one of these companies, it would take me two months to add a new product to the ERP system’s bill of materials, and then have finance build the track report on it. Two months, right?

What is fundamentally needed was a way for the line of business folks to be able to quickly create 25 in a week, do A/B testing, put them out there to different segments, put them out in different channels, and see how these things sell through which channels at what price point. The world, especially on cloud services, has moved away from traditional sales approaches and moved much more towards self-discovered consumption, purchasing on the side.

Therefore, the online aspects of this are incredibly important, right. Especially when it comes to services. Let’s take Bloomberg for instance.

The fact is, unlike going to a store where I’ll look and compare a price, and maybe I’ll go home and buy it on Amazon. Then sometimes, sometimes I’ll even buy it on a device. When you see the data, it doesn’t quite happen that way. In reality, services are consumed on the spot. “I want a ride now, right? I’m reading content now. I’m accessing a database and I need access, and therefore I will pay now wherever I am.”

So they need to combine at every point of

engagement with the customer into a point where I can service them by actually either exchanging some value with them. Sometimes that’s money. Sometimes that’s just signing up for a free trial or for a freemium, where upon usage, I’ll bill them later.

The whole engagement approach requires that every point of engagement with my customers or prospects actually changes.This is where payments have actually gotten a huge boost. In the same way that we’ve been growing in this world, payments have actually been dragged into this world as well, because of the dynamics of how people need to pay are actually very much in the moment, where every device can be a point-of-sale device.

But in reality, if you look at what people are really needing, because now, folks like HP, were building all this infrastructure around it. In reality, what they needed was more than just payment.

That’s why when you look at even what’s going on in the industry today, whether it’s Square and the articles around being low margin, or whether you see folks like Stripe.

The first thing they did after raising a fairly substantial round is say, “I’m going to build a whole bunch of items above payments to try to get a little more sticky and to ask more margins.”

So what you’re seeing is demand for the solution, so an ecosystem around payments – which is a total solution, which is commerce.

This is where we think there’s a huge wave of innovations in around services that is touching the payments industry. But clearly, payments is part of a solution where payments will be working with a commerce solution like us to be able to help grow this industry.

I N D U S T R Y V O I C E S

17

What are some of the services that you provide in making global payments easier, relating to cloud technology?

When you look at what’s needed, let’s talk about from the payments up.

When we look at payments, we say it’s around smarter payment. I know some people have been starting to use that word. It’s something that we’ve been talking about for a while. Why do you need smarter payments? Actually, let’s start with the top line.

There’s three things that we typically help our customers with. One is really servicing the customer at every touch point. Number two, it’s around being able to simplify and scale their operations, their business as they grow. And people are really focusing on how fast markets are moving, how to focus on their business without having to build all this building infrastructure, without paying for the backend infrastructure.

So we’ll get back to that as well. I think the first thing to start with is smarter payment. What do we provide there to help them? Well, first and foremost, it’s around just, how do you actually get signed up and leverage all the payments, as many of the payments methods you need around the world?

We have to provide the platform and relationships that allow them to start selling.

That’s the first thing. We help them to go global. Number two, especially given the world of services, retention, the subscription, which is incredibly important.

So for us, it’s around how do we actually provide an intelligent payment routing? How do we actually understand not only the simple retry but how to

increase optimization rate?

A combination of cunning, logic, a combination of account updaters, retry mechanisms, as well as failovers to multiple processors where we can actually get the best of all the different relationships we have underneath.

Again, by extracting out payments for the customers, we allow them to increase their retention and conversion. This is about getting a little smarter. Of course, we’re talking about alternative payments. Why should a customer have to follow a particular currency or whatever the new currency of the week is. We are constantly adding alternative payment methods, whether it’s PayNearMe, or Boleto, down in Latin America.

We’re constantly reaching through to alternative methods that become a single API, so that vendors don’t have to worry about it. They can select and turn on just from the control panel. That provides a huge amount of IA market. Now that’s around smarter payments.

The second thing we do is go kind of backwards, is going back through to how do we help customers service at every touch point?

How do I extend my trial by a month? How do you actually give a 20% discount in the next three months of your subscription because you had a payment issue? How do I upsell and cross-sell you in the call center?

What we saw were literally customers spending over half a year to try to wire payment into all of their touch points and to do the logic of how to actually do subscription billing, how to actually upgrade, downgrade. So payments is trying to provide some of these core tools, but you still have to build around all the APIs to get it done.

I N D U S T R Y V O I C E S

18

What we have is it’s all pre-wired, so that customers don’t have to do it themselves. So you talk about pre-wiring not only in a way that allows me to service a customer and do all these processes, right, but to also do them at every touch point consistently. Self-service in the call center with a direct salesperson.

Finally, it’s around the middle box we call sort of simplified scale. This is where there’s a huge amount of infrastructure.

HP was nine months into their project of wiring their own gateway, by the way. They have payment inside of HP. They had everything. They have their own gateway. They have multiple payments relationship. They were nine months into a project, putting, trying to build around billing, multiple ways of managing entitlement.

This is what’s interesting about services. When you talk about cloud, digital goods are infinitely configurable. Why is that different than a product? A product, you’re going to go buy it, right? There’s one of them in a store. Maybe I’ll give you two different types, a small one and a big one. With services, you could have a hundred different combinations of entitlement. On Mondays, you can read this. On Tuesday night, you can read it.

I mean, you can come up with any combination of craziness. To me, they’re going to want that combination because it personalizes them. When you look at the rules… and now how do I wire together by ordering through the front-end? How do I wire together to tell my ERP system the right thing to do? How do I bill it on a regular basis? How do I define these products?

How do I actually create all these different price points and different models and just get them out there to test, for scaling, experimenting?

To do this would take a large amount of time to wire your old systems together, as we found almost all our customers were doing.

In fact, Constellation Research did a recent study. Over 33 different systems participate in a single order. What you’re doing is with someone like us, it’s not replacing the system, not taking away your ordering system, et cetera. It’s around orchestrating them and being able to create a virtual bundle that I can sell to my customers.

This revolution that happened in telcos now – which only big companies could afford at that point in time – is now happening in multiple companies around the world. We’re working with hardware manufacturers that have recognized that their hardware is getting lower and lower margins, but they can install software on top it. The analogy I use is like a Tesla. There’s a $40,000 to $60,000 difference, depending on how much stuff’s in there. Majority of that difference in performance is software; the sustained hardware, sustained cost.

How do I, as a hardware provider, become a platform for add-ons? As Bezos said, “Every hardware platform better have a ecosystem with add-on solutions to grow your total solutions value.”

How are finding new and innovative ways to pay driving change?

Already, payments is revealing those huge innovations happening, because everything can be wired for being a point of sale. More and more, services are buying at that point of sale. It’s not just where now I’m using a cash register. It’s really a service in itself, which is much larger than products in this industry are being sold and productized online.

I N D U S T R Y V O I C E S

19

The question is, is payments enough? When you look at what’s needed, what we’re seeing over and over again is customers understand how much they end up having to do themselves.

They actually need to go up from payment and look for solutions to bring together the touch point, putting together the billing and the commerce pieces, putting together smarter levels of payment to help them manage the chargeback, to help them manage the financial reconciliation, to help them manage having to go global and manage global compliance.

Just a little bit off-topic, does that include supporting Bitcoin payments?

Bitcoin… not yet.

Not yet? Do you have plans in the works to do that?

Yes. So part of this is… services, yes. We’ll just leave it at that.We’re bringing on new innovation, and cryptocurrency is one that we see as fundamental innovation in the industry and one that is welcome. So innovation and things to turn it around I think are ones that not only are we looking at, but our vendors are looking towards as well.

So all this innovation of Bitcoin actually, fundamentally, you find a way to lower the cost. In fact, if you look at… I think a major card provider was saying it may not be Bitcoin that thrives at the end of the day, and of course, they may wish that. But the infrastructure, the technology and protocol is something that we can actually start using in our networks as well, right, and that will lower the cost. It’s a great innovation.

We’ll see if the old guard can update their platform

and learn from that. I think the second thing is that you see effort. The resellers are creating their own network, right, on mobile. They see that potentially, mobile payments, mobile POS becoming an approach towards bypassing the card networks and become big enough that they can actually challenge the hegemony of the card networks and the price they pay.

A little bit about you. What’s your history and how did you get involved in Avangate?

Sure. I’ve been in the Valley here for about 20 years, both in… and actually, all in software; both at large as well as small companies.

So I’ve been a VP, executive at Oracle, PeopleSoft, Amdocs. So those experiences really… looking at not only customer management but billing, as well as being in a variety of startups, both venture and PE-backed.

I’ve been lucky, knock on wood. I’ve survived the mass exits in most of these and see this as just a huge opportunity to move forward.

I’ve primarily been in customer management; like I said, middleware. And as such, my background matches very well with B2B and B2C. Now, I would say that when you look at this industry, why Avangate and the industry itself is undergoing such a massive change in product services.

And like I said, the cloud touches every industry. The fact is that Nike+is a product company. But did you see their investment? Nike+ is just a platform. Did they expect to make a lot of money there? No. They invested in 30 startups that are creating services on top of Nike+.

Look at each new thing. The things themselves may

I N D U S T R Y V O I C E S

20

not be the big drivers of revenue. In fact, many don’t see it. They see it as a huge generation of data.I mean, it’s not just the startups around Nike+. It is the e-book publishers.

You got folks who are publishing to folks who love to generate their own backyard garden and feed themselves and get off the power grid. You have all types of interesting folks who are self-publishing,

creating not only content, but also services because of the cloud. It makes it so cheap to get it out there. And we become a platform that grows with them. Because we only take money when they make money. So that we see a huge growth in all these vendors leveraging the cloud, leveraging the tools we have that are necessary for a service type of business to grow. So it’s a lot of fun.

Mike Ni, CMO/SVP Marketing and Products

Michael Ni brings over 20 years of experience as a marketing and product executive in bringing success-ful innovation-driven businesses to market – from startup to Fortune 500 companies.

Michael’s business experience spans across software, telecommunications, consumer packaged goods and digital media.

Prior to joining Avangate, Michael served as VP Products at Amdocs, where he drove the definition and development of next generation customer management, retail and commerce applications. In addition, he has held executive positions at leading CRM/ERP vendors, technology startups, and in strategy con-sulting. These roles include GM/Managing Director at MyWire, a venture-backed new media company; VP of Product at Oracle / PeopleSoft, where he drove the definition and development of the “Fusion” next-generation applications platform; VP of Product and Operations at venture-funded OnePage, Inc. (acquired by Sybase, Inc.) as well as Marketing Strategy Consultant at PriceWaterhouseCoopers.

Michael received an MBA from Harvard Business School, an MS from Stanford University and a BS in Me-chanical Engineering/Robotics from Massachusetts Institute of Technology.

I N D U S T R Y V O I C E S

21

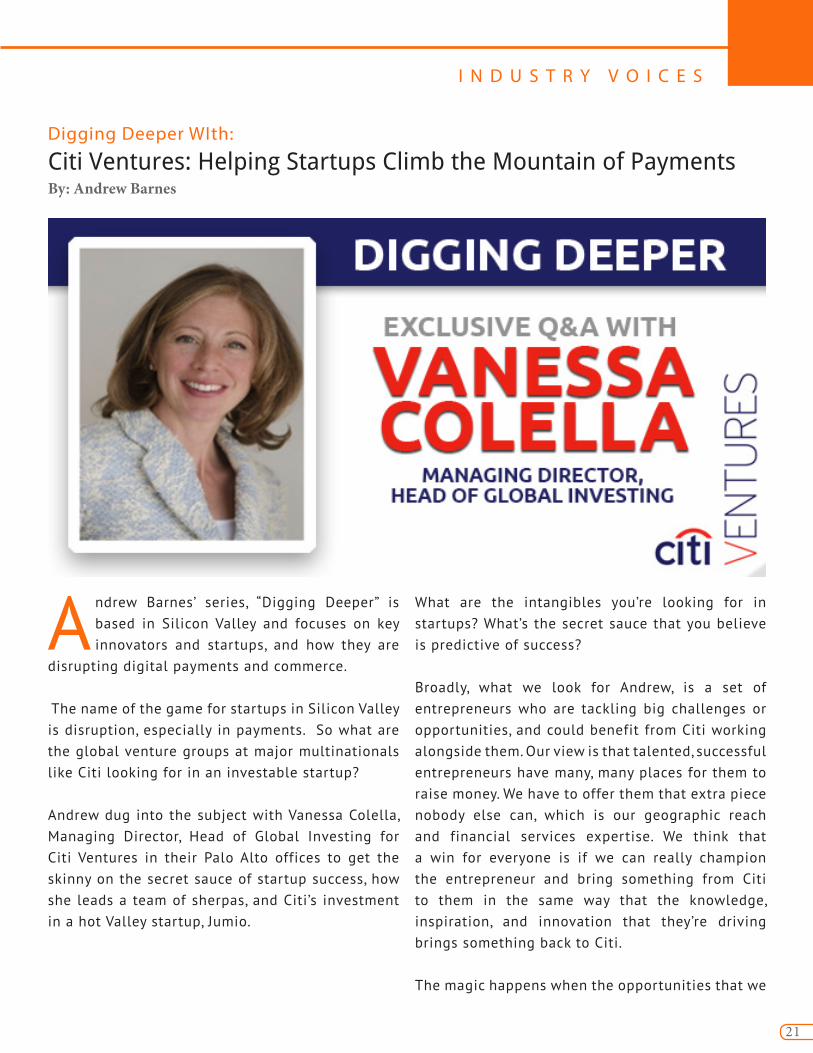

Digging Deeper WIth:

Citi Ventures: Helping Startups Climb the Mountain of Payments By: Andrew Barnes

Andrew Barnes’ series, “Digging Deeper” is based in Silicon Valley and focuses on key innovators and startups, and how they are

disrupting digital payments and commerce.

The name of the game for startups in Silicon Valley is disruption, especially in payments. So what are the global venture groups at major multinationals like Citi looking for in an investable startup?

Andrew dug into the subject with Vanessa Colella, Managing Director, Head of Global Investing for Citi Ventures in their Palo Alto offices to get the skinny on the secret sauce of startup success, how she leads a team of sherpas, and Citi’s investment in a hot Valley startup, Jumio.

What are the intangibles you’re looking for in startups? What’s the secret sauce that you believe is predictive of success?

Broadly, what we look for Andrew, is a set of entrepreneurs who are tackling big challenges or opportunities, and could benefit from Citi working alongside them. Our view is that talented, successful entrepreneurs have many, many places for them to raise money. We have to offer them that extra piece nobody else can, which is our geographic reach and financial services expertise. We think that a win for everyone is if we can really champion the entrepreneur and bring something from Citi to them in the same way that the knowledge, inspiration, and innovation that they’re driving brings something back to Citi.

The magic happens when the opportunities that we

I N D U S T R Y V O I C E S

22

see as a 202-year-old corporation, and opportunities that these entrepreneurs see as a couple-year-old companies, intersect.

You referenced traction. Give me an idea of what qualifies as traction in a marketplace?

Any business starts out with an idea that gets prototyped, built, and tested with clients or in pilots. It’s really easy to get very excited about the ideas. We say to entrepreneurs that it is hard for us to bring value at the idea stage, so by traction I mean a working product that is either being piloted or ready to be piloted in market.

Entrepreneurs and startups tend to pivot as they’re figuring out how their idea works in the marketplace, the available white space, and the problem they want to solve. As they learn there tend to be pivots early on.

We find that we can be most helpful to an entrepreneur, and they can find the most success in working with Citi when they’ve already gone through some of those early pivots and they’re now settled on the product and the market that they are going after. That’s what we look for when we talk about early traction.

I suspect that when you’ve got internal constituencies you can’t be championing X and all of a sudden it changes the Y. The process of re-socializing and re-integrating isn’t pretty is it?

Yes. Here’s how I describe it to people. Part of my team acts as Sherpas. Our job is to help make the magic happen, and that magic is leading a startup at the right time to a place where they might be able to engage with us to pilot something or test

something in a way that is an opportunity for Citi and an opportunity for them.

Like a Sherpa, our job is not to say, “There is the mountain. Go climb it and when you get to the top, call Bob.” Our job is to figure out the time of year, the week, and the time of day to start that climb. Identify who you need along the way to ensure success. Figure out the supplies needed to make sure that when that critical meeting happens, it is the most productive for Citi and for startups who are resource constrained and can’t burn cycles figuring out who to talk to in a big company.

We take that part of our job really seriously and sometimes, that means that we invest in a company and we don’t engage with them right away because we know that they’re working on something and it isn’t quite the right time. Other times, it means that we engage with a company well before we ever invest because we think it would be a great thing to understand what they’re doing in order to solve a challenge that we’ve got a Citi. And then we may or may not invest in them down the road.

Say I’m a startup and you’ve got an interest in me. You make an investment. Is my access primarily with someone on your team who is front running the interface in Citi or am I interfacing directly with units within Citi over time? How does that look?

That’s a great question. Our aim is never to be a bottleneck where you can’t call somebody at Citi without talking to us first. During that first climb, there can be quite a bit of interaction as we’re introducing the startups to people at the right level within Citi. We’re making sure that both sides are speaking the same language and that there’s an understanding of how we might be able to work together.

I N D U S T R Y V O I C E S

23

Of course Citi is a huge company. We operate many different businesses serving nearly 160 countries, so as a company starts to get traction within Citi, they start to have contacts within the organization. We’re always there to be a resource but that second, third, fourth climb, they already kind of know the route and it becomes much easier for them to interact directly with the business.

What about reaching beyond Citi, to other companies that might be good for their business?

We think the network is extraordinarily important. Our team consists of professional people from across the venture capital ecosystem. We think it’s important to understand what the network is like for an entrepreneur and we believe that this isn’t about just the startup and Citi. No startup is going to be successful only talking to Citi.

This is all about how we can we help get them going, and there’s other people that we know in common that would be good for them to be involved with. For example Andrew, what you find if I take service security as an example, is that we aren’t looking to acquire these companies. We’re looking for security companies to be successful so that overall, they’re increasing the safety and soundness of our financial system.

We’re very happy when they find success with us and then they go on to be successful with other companies because we are all in a race to stay ahead of the bad guys.

Right, and you’ve achieved the strategic objective of bringing in best practices while also improving your investment from an ROI standpoint as well, correct?

That’s right. What we really measure in terms of ROI here is strategic and different than some corporate venture units. I always say, and as every entrepreneur knows, that a bankrupt startup is not strategic. I think it’s a false dichotomy when people talk about measuring financial return or strategic return because if the company is not in business, I can guarantee you it’s not strategic.

Let me drill down on that last comment and how you might be different from other investors. Can you talk to this?

Yes. I think we are unique in a couple ways. Probably the most obvious way is that Citi has an unparalleled global footprint. There’s not many corporates, particularly on the financial side, which can help with access to the kind of markets and regions that we can.

I also think that we’re trying to be unique with the notion that we are not a one-and-done kind of operation. Frankly, if we have a startup who does one successful pilot with us and has a commercial deal with one of our business units in one region, we shouldn’t view that as a success for Citi and for that startup unless it is a completely centralized piece of technology because the reality is that there probably are many places around Citi that that same technology could be quite impactful.

We always look for scale. We look for entrepreneurs who are interested in scaling their businesses because we think that that’s something that we can help bring to the table and help them through that beginning process. Dealing with large companies can be a bureaucratic challenge and so if we can help build skills and capabilities to make that easier, then that helps accelerate the success of the company.

I N D U S T R Y V O I C E S

24

From an economic standpoint, is there a difference between yourself and corporates?

We don’t do seed investing. There are some other corporates that do very early seed investing. That would be slightly different. Obviously as a bank, we work very closely with our regulatory, compliance, and legal colleagues because there are some limitations on how much of a stake we could take in a company.

Down the road from us is Jumio, another Silicon Valley startup in which you have invested. What do you love about what they’re doing in the marketplace?

We’re excited about companies that are thinking about ways to improve the customer’s ability to interact. In Jumio’s case, you don’t have to type in all of your information, it gets pulled in and then filled out so that you can say, “Yup, you got it right. That’s all the information and it’s correct.”

For us, it’s exciting because fundamentally it’s a great experience if you’re a consumer. It is easier than having to key in all of your information especially if you’re on a mobile phone, which is so challenging. As with Jumio, we look for how these companies and these technologies make for a better experience for our customers.

You’ve lived in a bunch of places. What’s different about Silicon Valley and what about it had you put your venture investing office here?

The thing I love about the Valley is its optimism. People in the Valley view challenges or problems as opportunities to make it better, to make the world a better place, to make the experience better, to

change things, to add value. I think that optimism is just infectious. It helps us all think more broadly and differently about how we tackle problems and how we make them into opportunities.

A question on financial inclusion. Also called the emerging middle class, unbanked and underserved. How do you view this sector and are you putting investment dollars because you see opportunities for Citi?

Two things, first of all, Citi has been quite involved in a lot of early micro lending and pilots. That’s something that we take very seriously and have been active in for a long, long time.

In terms of investing in particular, what I find fascinating is the consumerization of IT, the cloud, and the advances in user experience have made it much less expensive to deliver many different types of services to different people. We might not talk about it as inclusion per se. But the fact that those services can be created, built, deployed, and delivered for less money than what’s previously possible expands the number of people able to take advantage of those services.

I think we’re seeing that become a reality in financial services. You see it with companies who are helping people look at how much to spend and how much to save. You see it with companies that are automating things like investing. For instance, if I only have $5,000 to invest, I may not want to hire a financial adviser because that is probably going to eat away at the core of what I’m saving. There are ways that I can responsibly invest that money in a much more automated fashion.

You really see it across the board. Innovation ultimately has the potential to disrupt a lot of the

I N D U S T R Y V O I C E S

25

historic value chain in payments. For instance, whether or not one can afford to hold a particular payment vehicle.

Some people might say that financial inclusion is a particular focus. We think it’s a mega trend in financial services and it’s based on the technology trends that you’re seeing from the cloud and how software is spurring products and services that previously have been far more expensive to deliver.

Palo Alto or San Francisco, what is a favorite restaurant for you? For instance, “Whenever I’m in need of X, I go to Y.”

Well, I have an infant so frequenting a restaurant is not as often as it used to be. These days such meals are standing next to the high chair thinking out how much chicken is going to go into his mouth versus on the floor. But when we do get out, we usually try and find some sushi.

Fair enough. I’ve got a two year old so I can certainly relate to that.

It’s all the stuff that people said you were going to find interesting and before you had one, you thought those people are weird. And then a you have child and it’s fun.

It’s like I never thought a place like Sam’s Chowder House on University Avenue would be such a great place to go but it is.

Exactly.

Great talking with you today Vanessa. Thanks for your

time and I look forward to our next conversation.

Great talking to you as well Andrew.

I N D U S T R Y V O I C E S

26

About Citi VenturesCiti Ventures is Citi’s global corporate venturing and innovation arm, chartered to collaborate with internal and external partners to conceive, partner, launch, and scale new ventures that have the potential to enhance and transform the financial services industry, drive client success, and generate new value for Citi. Citi, the leading global financial services company, has approximately 200 million customer accounts and does business in more than 160 countries and jurisdictions. Citi provides consumers, corporations, and governments with a broad range of financial products and services, including consumer, corporate and investment banking, securities brokerage, global transaction and wealth management services.

Vanessa Colella, Managing Director, Head of Global InvestingVanessa Colella leads Venture Investing for Citi. Her team identifies and invests in start-ups that are changing the game in the areas of data, security, payments, and fin tech and works with entrepreneurs to help them pilot and commercialize their technologies at Citi. She joined Citi Ventures in April 2013 coming to the team from Citi’s Consumer Business as Head of North America Marketing for the previous three years. Vanessa previously was head of data and insights at Yahoo!, a partner at McKinsey and Co. and an Entrepreneur in Residence with US Venture Partners. A charter member of Teach for America, Vanessa received her BS in Biology from the Massachusetts Institute of Technology and subsequently returned there for her graduate studies at the Media Lab, earning both her MS and PhD degrees. Vanessa resides in San Francisco with her husband and their son.

Andrew Barnes, Managing Director, Emerging PaymentsBarnes is a self-confessed payments “geek” and recognized entrepreneur-intrapreneur working in Silicon Valley. He leverages his business development track record and network in tech, startups, retail, and FI’s to profile opportunities and solve challenging revenue problems in payments and mobile commerce. Barnes has held executive positions internationally with Sprint, Global One, and 2Roam Mobile. He founded the National NNN Investment Group and is an Advisor to the Electronic Transactions Association (ETA). Barnes has an MBA from Waseda in Tokyo and a BA from Penn State. He can be reached at @AndrewinSV and Linkedin.