hotels in india— trends & opportunities continued incredible india campaign has had a strongly...

TRANSCRIPT

HVS International Hotels in India - Trends & Opportunities 2001 1

HOTELS IN INDIA—TRENDS & OPPORTUNITIES

2005 Edition

This edition has been published by the New Delhi Office of HVS International www.hvsinternational.com

IntroductionOver the last two years thehospitality industry has witnessedactive interest and has transformedthe country as a hugedevelopment destination. Thispublication assesses current trendsand presents future opportunitiesfor the hotel industry in India. Asalways, apart from conductingspecific research for thispublication, we have includedmacro data provided by theDepartment of Tourism. Thepublication briefly discusses thetourism industry in India in thecontext of the present economicscenario and presents the resultsof our survey on the performanceof branded hotels, analysed byeach segment of the hotel market,as well as by major cities. Ourstudy also provides an overviewof supply and demand conditionsin the hotel market in India. As in

previous editions of this report,we have, once again, presentedour assessment of industry trendsand development opportunities;this is included as part of the‘Future Trends’ section.

In addition to this document, wepublish The Indian Hotel IndustrySurvey on an annual basis, inassociation with the Federation ofHotel & Restaurant Associationsof India (FHRAI). This publication,the only one of its kind in India,provides detailed financial andoperating information on the hotelindustry, analysed by starcategory, across all major cities inthe country. The next edition(2004/05) will be available by theend of the year.

This is the ninth edition of HVSInternational’s Hotels in India -Trends and Opportunities

publication, providing us with aunique opportunity to understandindustry dynamics through tenyears of performance trendsrepresenting periods of peaks andvalleys. This year, 235 hotels,having a total room count of 31,234rooms, participated in our survey.The overall room count hasincreased, reflecting the openingof new hotels with largeinventories. Table 1 illustratessurvey participation for the years1999/2000 to 2004/05.

The Indian Economy - AnOverviewFollowing a growth of 8.5% in2003/04, the Indian economyperformed extremely well during2004/05, with GDP growing at6.9%. Despite the anticipatedgrowth inGDP inreal termsfor 2004/05 beingless thanthat for2003/04, it is among the highestachieved since Independence. Inthe first quarter of the currentfiscal (2005/06), the economyregistered an impressive growthof 8.1%. Domestic politicalstability and a benign worldeconomic environment haveprovided a backdrop conducive todevelopment, while a stronggrowth momentum in the Industry(especially manufacturing) andServices sectors has provided the

Also in this issue :FROM POACHINGSALMON TOPOACHING HOTELEMPLOYEES!

������������� ������ ������

2 Hotels in India - Trends & Opportunities 2001 HVS International

impetus necessary to sustain astrong performance in the short tomedium term. Another positivefeature has been the continuedmaintenance of relative stability ofprices and control on inflationdespite a rising world fuel priceregime. While the Reserve Bankof India has projected a GDPgrowth of 7.0% for 2005/06,following the economy’s firstquarter performance, projectionsmade by independent agenciesanticipate a GDP increase of 7.5-8.0%.

While agriculture and alliedactivities are the main source oflivelihood for 58% of India’spopulation, the share of thissector in the overall economy hasdeclined steadily over the past fewdecades, from 36.6% of GDP in1983/84 to 22.8% in 2003/04.

The Index of IndustrialProduction, which measures theoverall industrial growth rate, was10.1% in October 2004, comparedto 6.2% in October 2003. The shareof Industry in the overall economyhas remained stable over the pastfew decades from 25.8% of GDPin 1983/84 to 26.4% in 2003/04.

The Services sector hasmaintained a steady growthpattern since 1996/97, except fora decline in 2000/01. The share ofServices in the overall economyhas increased greatly over the pastfew decades, from 37.6% of GDPin 1983/84 to 50.7% in 2003/04.Trade, hotels, transport &communications witnessed theirhighest-ever growth of 10.9% in2004, followed by financialservices. Together, they constituteabout one-half of the Servicessector. This sector is presently thelargest contributor of room nightsfor hotels in India, and its

continued growth has greatlyinfluenced the current boom indemand, particularly in theNational Capital Region(comprising Delhi, Gurgaon,NOIDA and some othersurrounding areas), as well as inBangalore, Hyderabad, Pune,Chennai and Mumbai.

Our estimates indicate that India’sGDP growth over the next fewyears would continue to be drivenby Services and international trade.Within Services, the key sectorsthat would spearhead growth areaviation, retail and commercialreal estate, ITeS, telecom,insurance, and financial services.This growth in Services is expectedto further increase demand forhotel rooms of all categories acrossthe country.

The economy’s continuedbuoyancy and several otherdevelopments – government-ledinitiatives to improve India’sdeficient infrastructure, tax andother reforms, privatisation anddisinvestment policies andincrease in FII and FDI in certainkey sectors, namely, real estateand banking, have resulted inincreased foreign investments intothe country. The Economist (Jan2005) in its FDI Confidence Index,on the basis of an annual surveyby A.T. Kearney, reported thatIndia now ranks second, afterChina, as a location for foreigninvestment in manufacturing. Thisis a rise from the sixth place atwhich it was ranked a year ago.India’s foreign exchange reserves,stand at an estimated level ofnearly US$143 billion, as ofSeptember 2005.

Inflation, which was at a four-yearhigh of 8.0% in early September2004, was 3.75% in September

2005. High international oil prices,the highest ever with crude oiltrading at US$70 a barrel (inSeptember 2005) and fluctuatingbetween US$60 and US$70, areexpected to lead to significantwidening of the merchandise tradedeficit. The Rupee is expected toremain stable against the USDollar in 2005/06 with thewidening of the US fiscal tradedeficit.

Trends & Developmentsin TourismThe year 2004 has been the bestyear till date for inbound travel,with foreign visitor arrivalsreaching a record 3.40 million,resulting in international tourismreceipts of US$4.8 billion. Thisimpressive performance in touristarrivals is attributable to a strongsense of business and investmentconfidence in India: inspired bysteady growth in the Indianeconomy, a strong performance ofthe domestic corporate sector, aswell as initiatives taken to makepeace with Pakistan, strengthenties with other nations and opensectors of the economy to privatesector/foreign investment.Significantly, the bulk ofinternational arrivals in India, bothin 2003 and 2004, have beenbusiness travellers.

The continued focus on liberalisingthe Indian aviation sector hasprovided a further impetus totravel. Domestic air passengertraffic grew by 24.2% in 2004/05compared to 2003/04.International passenger trafficobserved a growth of 16.7% in thesame period. The increase ininternational flights, seat capacityand frequency into the country andthe decision to allow privateairlines like Jet Airways and AirSahara to fly abroad will also have

HVS International Hotels in India - Trends & Opportunities 2001 3

a positive impact on tourist andbusiness arrivals in India, as it willprovide additional seats to keydestinations. Increase in charterflights into India and new airlinesproviding additional seats fortravel within the country areexpected to have a significantimpact on increasing affordable airtravel within the country.Furthermore, India’s growingrecognition as an exciting place tovisit (‘The Readers Travel Awards2005’, conducted by Condé NastTraveller has placed India atnumber five among the world’smust-see countries, up fromnumber nine in 2003) has helpedboost its image as a leisuredestination.

While the encouraging trend inforeign tourist arrivals hasattracted much attention, verylittle has actually been said aboutdomestic tourism. Domestictourism, according to ourestimates, grew by 40% on anannual basis over the last threeyears and is currently estimatedat 230 million travellers. A rise indisposable income across mostincome segments, and acorresponding increase in thepropensity to spend, together withmore affordable air travel, have

fuelled this growth. Risingaffluence and higher incomes arealso expected to enhance theconcept of travelling for leisure.Domestic travel, both businessand leisure, also benefited from astrong performance of thecorporate sector in India, and theoverall sense of optimism withregard to the economy.

The current government, like itspredecessor, is adopting aproactive strategy towards thedevelopment of tourism in India.The continued Incredible Indiacampaign has had a stronglypositive impact on tourist arrivals.Definite efforts are being made tocommunicate the Brand Indiamessage: as the host, India madeits presence strongly felt at theWTTC-promoted Global Travel &Tourism Summit held in NewDelhi in early April this year(2005).

There is also an increasing focuson promoting traditional touristdestinations in the country and onprioritising new attractions andtravel circuits. Niche marketing inareas such as medical and healthtourism, is expected to be a majorgrowth driver. These segmentsgenerated 150,000 visitors in 2003,a number that is expected to

increase to 1 million, and bring inrevenues up to US$5 billion in afew years.Prospects for tourism in India,both inbound and domestic, arebright, with many opportunities.According to recent estimates ofthe World Travel & TourismCouncil (as of early 2005), Indiantourism demand will grow at 8.8%over the next ten years, whichwould place India as the second-most rapidly growing tourismmarket in the world afterMontenegro and before China.This is expected to result in agrowth of 7.1% in total travel andtourism GDP and an increase of0.9% in travel and tourismemployment.

Table 2 reflects key statistics forthe Indian tourism industry.

Survey ResultsThe HVS International survey hasbeen computed by dividing therespondent branded hotels intotheir respective classificationsaccording to star grading. Asbefore, we have examined theperformance of ten major citiesacross India, wherever areasonable sample allowed. Whilemost of the data provided to us isin Indian Rupees, we have

������������� ���������������

4 Hotels in India - Trends & Opportunities 2001 HVS International

presented survey results in USDollars as well.

For the second year in a row mostmarkets across categorieswitnessed robust increase both interms of occupancy and averagerate. The demand for qualityaccommodation from all marketsegments, especially thecommercial and extended-staymarkets, continued to be higherthan the additions to supplyresulting in acute demand-supplyimbalance in certain cities, such asBangalore, Mumbai and Delhi(NCR). This demand-supplyimbalance enabled hotels in thesecities to charge higher tariffs acrossall market segments. As a result,the industry saw a 12-monthgrowth of 20.7% in average rate(in 2004/05), compared to a 12-month occupancy growth of 7.1%.Table 3 reflects room occupancyby hotel classification for theperiod 1995/96 to 2004/05. Table4 presents average rateperformance in Rupees for thesame period while Table 5 reflectsaverage rate results in US Dollars.Table 6 presents RevPARperformance in Rupees for theperiod 1995/96 to 2004/05 andTable 7 presents the same in USDollars.

Over the past five years, additionsto room supply have mostly been

contributed by developments inthe budget and mid-marketsegments. The increasedrepresentation of branded hotelsin these segments during weakdemand periods resulted in adownward spiralling of averagerates, thus lowering overallaverage rate figures for theindustry. The year 2004/05 wasmarked by an improvement inaverage rate – spurred by strongrate growth trends in the budgetand mid-market segments. Thehighest annual growth in averagerate, in Rupee terms, waswitnessed in the four-star (25.7%)and five-star (24.2%) categoriesfollowed by the five-star deluxecategory (19.2%). The average ratefor three-star properties showeda lower increase (12.5%). It mayalso be noted that, over a ten-yearperiod, the compounded averagerate growth in Rupee terms hasbeen strongest in the four-starcategory followed by five-star andthree-star hotels. Our marketresearch indicates that hotelsacross all categories havewitnessed an improved foreign-domestic guest ratio and,therefore, despite a strongerRupee, the growth in average ratein US Dollar terms has been higheracross all categories.

Average occupancy witnessed anacross-the-board growth, for the

third consecutive year. Strongyear-round demand from thecommercial travel segmentcompounded by higher demandfrom segments such as leisure andMICE substantially reduced theimpact of seasonality overweekends and slow seasons and,therefore, occupancies have beenon a steady growth curve. Theemergence of relatively newfeeder markets and consistentdemand from niche markets, suchas the extended-stay segment,have resulted in a higher level ofbase demand that ensures aminimum level of occupancy. Thisdemand has been extremelyadvantageous, as it enabled hotelsto indulge in proactive yieldmanagement, rate contracting andmicro segment planning.

Five-star deluxe hotels witnessedthe largest increase in occupancy(8.8%), followed by five-star hotels(7.3%). Growth for the four-starand three-star categories was 5.7%and 2.7%, respectively.Occupancy levels have shown asmaller increase this year(compared to 2003/04), asmarkets now have a higher baseagainst which to benchmark theirgrowth.

In terms of RevPAR (RoomsRevenue per Available Room), allstar categories experienced

����������������������������������������� ���������������� ��!���������

HVS International Hotels in India - Trends & Opportunities 2001 5

�����"����������������������������������� ���������������� ��!�#$�����������%&�����������'

�����(����������������������������������� ���������������� ��!�#$�����������%)��* �����'

�����+����������������������������������� ���������������� ��!���$,#��%&�����������'

�����-����������������������������������� ���������������� ��!���$,#��%)��* �����'

6 Hotels in India - Trends & Opportunities 2001 HVS International

healthy growth in 2004/05. Five-star hotels experienced themaximum growth in Rupee terms(33.3%) followed by four-starhotels (32.9%) and five-star deluxehotels (29.7%). The three-starsegment witnessed the leastimprovement (15.5%). In USDollar terms the five-star segmentshowed the highest increase(36.6%), followed by the four-star(36.1%) and five-star deluxe(32.9%) segments.

Table 8 illustrates hotel occupancyfor ten key cities in India, between1995/96 and 2004/05. Tables 9and 10 show average rates for eachof these hotel markets, expressedin Rupees and US Dollars,respectively. Tables 11 and 12present the correspondingRevPAR data for each city. In2004/05, Ahmedabad saw thehighest occupancy growth(16.8%), followed by Agra (16.4%)and Jaipur (14.3%). For the secondyear in a row Agra and Jaipur,both part of the much-popularGolden Triangle, witnessed theirhighest occupancy increase,thanks to sustained demand fromdomestic travellers and higherforeign tourist arrivals.

Demand for the Goa marketcontinues to remain strong whenwe take into account the supplyaddition during 2002/03.Occupancy growth in Goa was5.9% in 2004/05. The NCRcurrently has among the largestnumber of branded hotel roomsin the country and occupancy grewby an impressive 8.1%, indicatingstrong demand trends across allmarket segments and feedermarkets. Mumbai, on the otherhand, witnessed a 3.9% increase.During 2004/05, marketwideoccupancy for Mumbai showed amuch flatter growth; this can be

attributed to a larger roominventory, owing to an increase insupply, especially in the brandedfive-star deluxe and five-starcategories. Contrary to marketperceptions, the cyber cities ofBangalore and Hyderabad had thelowest annual growth inoccupancy amongst the ten cities.Bangalore witnessed a smallincrease of 2.5% while theHyderabad market grew only at2.2%. The lack of room availabilitycontinues to be acute in thesemarkets resulting in a huge levelof unaccommodated demand,which is now being catered to bystandalone hotels and servicedapartments. Also, the existingrates in markets such as Bangaloreare compelling a large section ofcorporate travellers to makeadjustments in terms of their hotelpreferences.

In terms of average rate (Rupeeterms), Bangalore continues to bethe rate leader for the secondconsecutive year, witnessing a rategrowth of 63.1% in 2004/05. Ridingon strong corporate and extended-stay demand, Hyderabadwitnessed a rate increase of 25.7%.Moreover, for the first time in tenyears, highly seasonal marketssuch as Ahmedabad, Agra, Jaipurand Goa all witnessed an annualgrowth of 20.0% or higher. This isan astonishing achievement andpoints to the strong potentialoffered by secondary markets andleisure destinations for new hoteldevelopment, in the presentscenario of robust demand trendsand very low room inventory.

The four main metro cities - Delhi,Mumbai, Chennai and Kolkata -continued to witness a steadyimprovement in average rate forthe second year in a row. Averagerate growth in Delhi was 21.8%

while rates in Mumbai went up by13.8%. Chennai and Kolkata, whichhave traditionally remained pricesensitive markets, witnessed amodest growth of 10.2% and 6.4%,respectively. In US Dollar terms,growth in average rate in 2004/05was highest for Bangalore (67.6%),followed by Hyderabad (30.0%).Agra, Ahmedabad, Goa andJaipur witnessed growth in the20.0% range. The Kolkata andChennai markets registered thelowest increase.

Based on the development statusof various hotel projects across theten cities studied, our assessmentis that over the next 24-36 months,most hotels across star categorieswill be able to maximize yieldsand prices will move up. Ourresearch indicates that the majorityof hotel markets in India follow aone-year lag period before ratesstart moving upwards; for thenext three years, most marketshave the potential to registeraverage annual growth in therange of 20-25%. The plannedaddition to supply will start a raterationalisation process and ratesare likely to flatten starting the lastquarter of 2007.

In terms of RevPAR growth in2004/05, Bangalore (67.3%) was innumber one position, followed byAgra (44.4%), Ahmedabad (42.8%)and Jaipur (38.2%). The emergenceof secondary markets as RevPARleaders has taken place for the firsttime, pointing to the potential ofthese locations for hoteldevelopment. The four metrocities also performed well in termsof RevPAR, with the NCR marketappreciating by 31.6%, Mumbaigrowing by 18.2%, and Chennaiand Kolkata showing an increaseof 18.6% and 17.7%, respectively.

HVS International Hotels in India - Trends & Opportunities 2001 7

In the short term, RevPARperformance in primary marketsthat include the four metros,Bangalore and Hyderabad is likelyto be a function of rateimprovements in each individualmarkets. These cities have realisedtheir peak potential in terms of

occupancy growth, and furtherincreases are likely to follow amuch flatter growth trajectory.Due to the limited availability ofrooms, these markets will witnesshigher average rate growth.RevPAR performance in secondarydestinations, both commercial and

leisure, will depend upon demandgrowth from key markets andoccupancy improvement is likelyto be the most important driver.Secondary markets, typically,have substantially higher ratesensitivity, resulting in longer ratematurity periods.

�����.�����������������������������������/�0 �������!���������

�����1�����������������������������������/�0 �������!�#$�����������%&�����������'

8 Hotels in India - Trends & Opportunities 2001 HVS International

������2�����������������������������������/�0 �������!�#$�����������%)��* �����'

������������������������������������������/�0 �������!���$,#��%&�����������'

������������������������������������������/�0 �������!���$,#��%)��* �����'

HVS International Hotels in India - Trends & Opportunities 2001 9

Hotel SupplyIn the past year, much has beentalked about the insufficientinventory of quality accom-modation across India. The recentboom witnessed many hotelmarkets in India and expectationsof strong room night demand inthe forthcoming years has broughtabout a renewed interest on thepart of real estate developers inhotel projects. In the last one year,several new hotels have beenannounced in high-growthmarkets such as Bangalore,Hyderabad and Gurgaon. Marketsurveys conducted recently byHVS at the above three locationshave identified 65 hotel projects,under various stages ofdevelopment, that will togetherprovide an additional inventory of

approximately 13,500 rooms.Taking into account the nature ofdemand, customer demographics,key feeder markets and marketsegmentation we believe thatBangalore, Hyderabad andGurgaon would be close tosaturation, should all the plannedsupply actually be developed. Thecumulative addition to supply forMumbai, Chennai and Kolkata islikely to be 35 hotels with aninventory of 8,000 rooms. Thedemand for hotel accommodationin the latter three markets has beendetermined using a mixedportfolio of market segments anddiverse key feeder markets. Thelack of seasonality also improvesthese cities’ overall potential andour estimate is that the plannedsupply will be readily absorbed,

taking into account projections ofdouble-digit annual demandgrowth over a three to five yearhorizon. In Mumbai, for example,while new hotels havecommenced operations in the lastthree to four years, strongdemand conditions have ensuredconsistent marketwide growth,both in terms of average rate andoccupancy. According to ourestimates, the combined inventoryin branded business and luxuryhotels across the ten cities standsat 22,400 rooms. We expect thissupply to increase by 85-90% inthe next five years.

An encouraging development in2004/05 has been the number ofhotel projects announced insecondary cities such as Pune,Jaipur, Agra and Ahmedabad.Unlike metro cities, which areexpected to witness new roomadditions to an existing maturelevel of room inventory, thesecondary markets will grow froma much smaller base. Thus, supplyadditions are not likely to impactmarket occupancies, owing tolarge levels of unaccommodateddemand that would be absorbedby the planned supply. A classicexample is that of Goa, where thetotal room inventory in thebranded hotel segment literallydoubled, between 2002 and 2003.Industry observers had indicatedthat marketwide performancewould suffer tremendously.Instead, the addition to supplywas matched with strong yearround demand from domesticinbound travel and MICEsegments, the market continued toperform well and is now on aconsistent growth curve.

Going forward, the biggestchallenge, given the presentsupply scenario, will be the

���������*�������� �� ��34�����������,� � ����5������� ��������/�0 ������

10 Hotels in India - Trends & Opportunities 2001 HVS International

availability of quality sites forhotel projects. Site location,accessibility, visibility andproximity to key demand areasare critical factors for long termsfeasibility of hotels and lack ofgood sites would have a negativeimpact on the supply front. Thereal estate market, too, has seenits best times in the last two years,and existing land prices acrossmost cities are somewhatprohibitive, especially forstandalone property developers.

Future TrendsHaving researched variousmarkets and conducted surveysfor the past nine years, we havehad a unique opportunity tounderstand hotel industry trendsthat have now witnessed acomplete cycle. The industry wasat its peak during 1995/96 andmaintained a consistent trend overthe following three years. In 1999,India carried out a nuclearweapons test; this was soonfollowed by the Kargil conflictbetween India and Pakistan.Relations between the twocountries were unfriendly and thisuncertainty had a huge impact ontravel. From 2001 onwards, aseries of international events suchas 9/11, the SARS outbreak andthe US war in Iraq further affectedcommercial demand andinternational tourist traffic. Hotel

markets across most of the worldwitnessed an occupancy decline;however, in India, this impact wasfor a relatively smaller timeperiod. Strong demand fromdomestic leisure travel andcontinued travel within India,especially business travel, enabledhotel demand to grow. In 2003/04, most hotel markets hadrecovered, across all starcategories, and were recordingimpressive growth in terms ofoccupancy. In the last 12-18months, hotel operators have beenable to optimize demand andimplement proactive ratemanagement strategies. Theaverage rate performance in themajority of markets clearly reflectsthis. With projections of strongdemand growth and limitedaddition to supply expected, mostcities are likely to maintain highoccupancies and witness averagerate growth in the range of 25-30%,annually, for the next three years.

Table 14 presents key operatingstatistics for five-star deluxe andfive star hotels in key cities, forthe period April to August 2005.Comparisons with thecorresponding period last yearhave also been presented, toillustrate the extent of change.

Performance trends for the firstfive months of 2005 are

encouraging. Most markets thathave registered strong growth arecontinuing to show marginalincrease in occupancyaccompanied by very strong rateperformance. In 2004/05,occupancy growth in Kolkata andChennai was much flatter; thesemarkets showed impressive gainsmore recently, in the first quarterof 2005. Rate growth in thesemarkets does not mirror demandgrowth; as mentioned earlier,Kolkata and Chennai havetraditionally been rate sensitivemarkets and we estimate that bothcities will see strong rate growthfrom the third quarter of 2005.

Occupancy growth for Hyderabadhas been small and Bangaloreactually had a small decline inoccupancy despite a decrease inroom supply due to renovations.However, it is the same demand-supply imbalance that continuesto allow hotels in Bangalore tocharge rates in the US$250 toUS$300 range and our estimate isthat in the next financial year, ratesin both markets (Bangalore andHyderabad) will grow atapproximately 20-25%. With newsupply being phased in startingearly 2007, there will be rateconsolidation, and both rate andoccupancy are expected tostabilise by 2008.

�������"������������*������#����������#�����6�#�����22(�$�7�#�����6�#�����22"

HVS International Hotels in India - Trends & Opportunities 2001 11

Interestingly, Goa remains themost underestimated marketamong the major cities and wehave been recommending thismarket for development for thepast 2-3 years. It continues to seethe highest demand growth in thecurrent year with reasonablystrong average rate increase. Interms of RevPAR the market, inthe first five months of 2005, hasgrown by 55.2%, second only toNew Delhi (64.3%) and slightlyahead of Hyderabad (52.6%).

Mumbai and Delhi continue towitness strong commercialdemand and we expect annualoccupancy growth in the region of12-15% accompanied by 20-25%growth in average rates in 2005/06. The Commonwealth Games tobe hosted in New Delhi in 2010 isalso likely to induce strongdemand and greatly assist in theabsorption of additional supply inthe market.

A buoyant economy, robustcorporate results and a boomingstock market are strong indicatorsfor surging domestic leisuredemand. Foreign tourist arrivalshave grown by 16.0% for first eightmonths of 2005. The period fromOctober to January is consideredthe peak season across mostleisure destinations and demandis likely to further improve duringthis period. Continued demandgrowth from the domestic as wellas the foreign travel circuits willlead to higher occupancies andrates across all key leisuredestinations. We also stronglybelieve that for the next five years,secondary markets will benefit themost, with improved airconnectivity to other cities and thedevelopment of national highwayinfrastructure. With limited roominventory base and very littlesupply addition, existing hotels inthese markets will gain the most.

OpportunitiesOur research and market analyseslead us to conclude that hotelspositioned between budget andmid-market levels and having aninternational brand affiliationcontinue to provide the mostattractive opportunities, acrossmost secondary markets. Over thelast 12-18 months high growthmarkets such as Bangalore,Hyderabad and Gurgaon haveseen aggressive hoteldevelopment activity, and thesecities could face a scenario ofoversupply in three to four years.A wise strategy for these citieswould be to observe the progressof projects under development, aswell as demand trends, before aninvestment decision is taken.

The four main metros and Goacontinue to present the bestopportunity for luxury hoteldevelopment. While these marketshave the largest room inventorymuch commercial development istaking place, especially in the citysuburbs. There is a strong positivecorrelation between hotel demandand commercial development, andfactors such as airline seat capacityexpansion, growing number ofdomestic budget airlines andimproved frequency will furtherenhance demand from thetransient and airline marketsegments.

A keen observer of the hotelmarket would agree that India hasbeen guilty of following a herdmentality when it comes to hotellocations. Almost all developmentstrategies are directed towardsprojects in the main city centre ofhigh growth markets. Over thenext three to five years, the biggestsurge in demand is expected tocome from commercial zones thatare being developed in metro

suburbs and secondary markets.This provides a uniqueopportunity for hotels. Areas suchas Whitefield in Bangalore, NaviMumbai, Manesar near Gurgaon,the International Airportcommercial zone in Hyderabad,Rajarhat and Salt Lake City inKolkata, Kharadi and KalyaniNagar in Pune, and theA h m e d a b a d - G h a n d i n a g a rhighway will witness large levelsof commercial development andare attractive locations for newhotel projects.

The lead time for developing ahotel project in India isapproximately 24-36 months andit is important to understand thecommercial development trends ina market. Mixed-use developmentprojects that include a hotel, retailand commercial space have gainedmomentum in the last 24 monthsand will continue to be anattractive option for developmentsin large land parcels. Key touristdestinations, such as Jaipur andother cities of historicalimportance in Rajasthan,Himachal Pradesh, Goa andKerala will witness integratedtourism projects. The relativelynewer concept of weekend travelis poised to gain furthermomentum with a growingeconomy and higher disposableincomes, and leisure destinationsin close proximity to metro citieswill benefit from this trend.Moreover, the developments andexpansions planned in the IT &ITeS and BPO segments remainencouraging. The entry of newcompanies, typically, generatessignificant room night demandduring the start-up period, asprocesses are set up andexecutives travel for training. Thiscategory of hotel customerensures a relatively strong base ofdemand due to a comparativelyhigher average length of stay.

12 Hotels in India - Trends & Opportunities 2001 HVS International

In most hotel markets, insufficientavailability and high room ratescreate conditions that are notconducive for large internationalconferences to be held. Logisticalbottlenecks in these markets alsopose a problem. Post 2007, onceseveral markets see an increase insupply, most hotels would adoptan aggressive marketing strategyfor the MICE segment anddemand from this category islikely to rebound strongly.

In India, as in other markets acrossthe world, large additions to roomsupply in hotels calls forinvestments worth millions ofdollars. Availability of finance forfunding hotel projects has,traditionally, been an importantarea of concern. However,promising demand conditions andthe industry’s strong growth

potential has radically changed theway most financial institutions,banks and foreign investmentfunds look at India today. In thelast six months, HVS Internationalhas had the opportunity to interactwith the representatives of at leasttwelve foreign investment funds,and we believe that finance is nolonger a big issue for a viableproject in a good location. Hotelmanagement companies andinternational brands are also opento considering equity participationin projects, opening newopportunities for the industry.

The outlook for the hospitalitymarket in India is optimistic andwill continue to remain so, in ouropinion. The economy’s buoyancy,initiatives to improveinfrastructure, growth in theaviation and real estate sectors

and easing of restrictions onforeign investment and, perhaps,most importantly, efforts to makepeace with neighbouring Pakistanwill fuel demand for hotels acrossstar categories in the majority ofmarkets. India’s hotel industry isincreasingly being viewed asinvestment-worthy, both withinthe country and outside, andseveral international chains arekeen to establish or enhance theirpresence here. We anticipate that,over the next three to five years,India will emerge as one of theworld’s fastest growing tourismmarkets and will be hard toignore.

Tables 15 to 17 provide a graphicalrepresentation of operatingstatistics for key cities in India forthe period 1995/96 till 2004/05.

������(��������������/�0 ������� %�11(81+� 6��22"82(

HVS International Hotels in India - Trends & Opportunities 2001 13

������+��#$��������������/�0 ������� %�11(81+� 6��22"82('

������-����$,#�����/�0 ������� %�11(81+� 6��22"82('

14 Hotels in India - Trends & Opportunities 2001 HVS International

FROM POACHINGSALMON TOPOACHING HOTELEMPLOYEES!

A series of ambitious economicreforms aimed at deregulating thecountry and stimulating foreigninvestment has moved India firmlyinto the front ranks of rapidlygrowing Asia Pacific region.Today, India is one of the mostexciting emerging markets in theworld. Skilled managerial andtechnical manpower that matchthe best available in the world andan educated middle class whosesize exceeds the population of theUSA or the European Union,provide India with a distinctcutting edge in global competition.This increasing transformationmeans a more complex economythat demands more sophisticatedtalent, with global acumen, multi-cultural fluency, technologicalliteracy, entrepreneurial skills andthe ability to manage increasingly'delayered' organizations.

In today's competitive marketenvironment it is widely knownthat organizations compete head-to-head with rival firms for controlof customers, market share andrevenue to achieve a leadershipposition in their chosen mode ofoperations. With Indian industryall set for the next big leap, thegaps in manpower demand andsupply are beginning to show.Poaching of priced talent isrampant and companies acrossthe board from media to telecomare being bled white. Be it thenascent biotech industry or otherpromising sectors, compellingbusiness pressures anddemanding deadlines arefacilitating this 'guerrilla warfare'

by a subtle name – poaching. TheIndian hospitality industry is noexception and is also witnessing alarge exodus of employees toother industries that find highperforming hotel employees acherry pick!

Here's our summary evaluation ofthe issue at hand….

Today, the coming together ofdifferent corporate psychologiesin a competitive businessenvironment makes a hotelprofessional move from one hotelto another and on a larger canvasmakes him move out of the hotelindustry to other sectors. Thereasons could be many…adifferent work challenge, theexpectation of faster careergrowth, aspirations for betterwork-life balance, a hospitalitycareer being a poor fit with one'spersonality, or a combination ofsome of these factors. Last but notthe least, the temptation of betterpay is, more often than not, aprime driver. Research shows thatmoney is like Prozac. Neithernecessarily makes you happy,however assists in preventingdifferent forms of unhappiness -----in the case of the former, lessfinancial anxiety, affording betterhousing, better and bigger car,good schooling for the children,metro locations and softer loans.To summarize, it's a fine mix ofemployee aspirations, the mirageof other sectors and the finesse ofan executive search firm that leadsto poaching from hotels!

So who are the 'poachers'? Agrowing list of industries andsectors, that are witnessing hecticactivity, expansions and arepassing through a boom. A briefsectoral analysis is presented.

Retail - Market liberalization andan increasingly assertivemetropolitan consumerpopulation is now sowing theseeds of a prolonged retailtransformation in India. The retailboom witnessed in India over thelast 18-24 months has startedbringing in bigger Indian andmultinational operators on to theIndian retail scene. Internationalbrands such as Wal-Mart, Tescoand Carrefour are eyeing India astheir next expansion destination.According to a recent studyundertaken by the AssociatedChambers of Commerce andIndustry of India (ASSOCHAM),organized retail is expected toregister an annual growth of 6.0%over the next five years and touchtotal business of US$17bn againstits current business volume ofUS$6bn. According to India RetailReport 2005 conducted by KSATechnopak, India's distinctadvantage is that it is amongst theleast saturated of all major globalmarkets in terms of penetration ofmodern retailing formats.Amusement park, conventioncentre, serviced apartments andhotel are some mixed-useconcepts that are being combinedwith retail to present a completeproduct mix. The opening up ofthe retail sector in India throwsmajor challenges to the hotels fora majority of retail functions areidentical and it enables the retailplayers to go higher in thehierarchy of poaching, targetingmid to top level executives acrosskey functional areas.

Aviation - International anddomestic travel in India is growingby leaps and bounds. It has beenestimated that the aviation sectorin India is likely to witness a 20.0%YOY growth over the next fiveyears in passenger traffic from the

HVS International Hotels in India - Trends & Opportunities 2001 15

existing almost. The entry ofseveral low cost airlines in thedomestic market, the "Open SkyPolicy" that provides anopportunity for domestic carriersto fly to international destinationsand keen focus by the centralgovernment on airportinfrastructure development arekey growth drivers for the sector.In the aviation sector today, apartfrom trained pilots, engineers andoperational staff, there is also agreat need for trained staff that canmanage key functions such asreservations, yield management,guest relations, sales andmarketing. Attractive perks androle enhancement make hotelemployees a soft target forpoaching since they come withspecific expertise, are highlypresentable, well spoken and aretrained in customer service andguest interactions.

Business Process Outsourcing -According to NASSCOM, theprojected revenue of the BPOindustry in India is expected totouch US$12bn in 2006. The sector

hired an average of 400 people onevery working day of the year in2004/05. With annual growthprojected at 11.0%, the sector isexpected to employ over 1.2million people by 2008. VariousBPOs in India have enhanced theirservice portfolio by handlingknowledge-based activities likebudgeting or resource planning,giving their customers access to acomplete menu of end-to-endprocesses in functional areas likeHR, finance and customer caregrowth. With their economicsuccess BPOs are now moving upthe value chain and many suchoutfits are being transformed intoKnowledge Process Outsourcingcompanies or KPOs. The globalKPO sector is expected to grow ata CAGR of over 45% to reachUS$17 billion by 2010. India, withits highly qualified professionalswell versed with the Englishlanguage, is emerging as thelocation of choice for a widevariety of KPO work.

BPO industry is on a spree to hirehotel industry graduates. The

hospitality industry in India todayemploys a large number of youngexecutives in different areas ofhotel operations. Theseemployees are well trained indifferent aspects of guest serviceand interaction, have excellentservice orientation and commandover English. There is also demandfor good chefs, stewards andhousekeepers to undertakefacilities management relatedfunctions. Flexible workschedules, an informal workenvironment and good pay aresome aspects that facilitate themovement of employees fromhotels to the BPO industry.

Real Estate - The commercial andresidential real estate industry inIndia is moving closer to thepeople. No longer a purview oflarger-than-life egos and insatiabledevelopers, the real estateindustry is more focused on thewants and needs of the consumer.The industry is emphasizing moreon branding, and on the marketingof buildings as products that canprovide 'experiences'. The real

34�������

16 Hotels in India - Trends & Opportunities 2001 HVS International

estate industry has been successfulin attracting quite a lot of hotelprofessionals since they areassumed to excel in selling'intangibles' and provide thatunique experience to itsdemanding customers. Stories ofpoaching are also rife in emergingsectors like media, finance andinvestment banking, andinsurance.

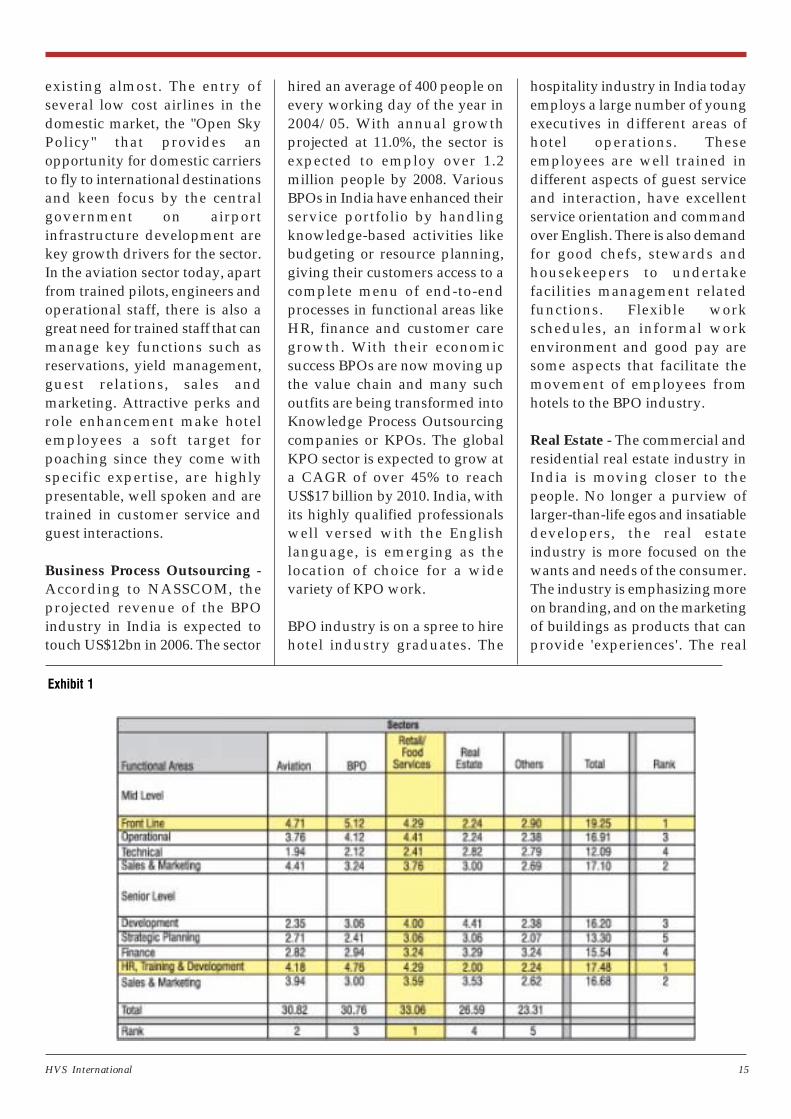

HVS conducted a survey in orderto analyse the quantum of threatwith the emergence of the abovenew sectors. We researched on

two specific variables. The firstvariable was defined as the sectorsthat present the highest threat ofpoaching and the second wasdefined as the functional areas ina hotel that are vulnerable to beingpoached by these sectors. Thesefunctional areas were broadlyclassified into mid-level functionsand top-level functions. Eachfunction was further sub -classified, based on jobresponsibility and specific skillsets. Points were assigned bysector for each job responsibility.The points were assigned on a

continuum of 1 to 6, where 6represents the highest threat ofpoaching. The sum of points foreach variable was ranked and theassigned rank was used as abenchmark to evaluate the risk.

Our research indicates that theretail and food services industrypresent the highest threat ofpoaching from the hospitalityindustry followed closely byaviation and BPO. In mid-levelfunctional areas the front line stafffaces the highest threat of beingpoached followed by sales and

HVS International Hotels in India - Trends & Opportunities 2001 17

marketing and operational staff.In senior level functional areas,HR, Training & Developmentexecutives present the highestthreat of being poached followedby executives responsible for salesand marketing related functions.

In reality, our business truth issimple the quality of yourrelationships protects you fromcompetitive as well as non-competitive poaching. Changingtimes call for dynamic and everemerging strategies. The practicesof innovative managementtechniques and invigorating HRstrategies have resulted in majororganizational transformations.Individual improvements andlifetime commitments fromemployees are possible, it's justthe question of how sincere theefforts of the organization are andhow involved are the people whomatter when it comes to decisionmaking and formulation ofstrategies. We need to revise ourselection and hiring processes toidentify candidates with the rightaptitude and skills for hotel as aprofession and its demandingpressures. The training cultureshould also be customized so asto reflect values of loyalty andcommitment in an individualtowards the organization andempower him to take on thechallenges of working underimmense pressure. Today, weneed leaders who are capable ofperformance management-creating a system of settingattainable goals, providingfeedback and mentoring,reviewing progress and creatingdevelopmental plans and acompetitive compensationstructure. HVS, through itsvarious surveys, has alsoobserved that people who had left

hotels during the boom in the ITindustry are coming back tohotels, probably because ofincreased pressure in the ITindustry or rather maybe becausetheir passion for hotels isinsatiable!

Probably the hotel industry shouldfocus its energies in creating andretaining trained manpower ratherthan joining the poaching rat race.

AcknowledgementsThe Hotels in India - Trends &Opportunities report has beendeveloped for the benefit ofemployees, developers, investorsand operators with an interest inthe tourism industry in India. Thestudy has been made possibleonly with the contribution andsupport of all the domestic andinternational hotel chains, to whoHVS International would like toexpress its gratitude andappreciation.

If you or any of your colleagueswould like to receive compli-mentary copies of this publication,or HVS Executive Search infor-mation, kindly send your e-mailaddress along with full contactdetails to Chandrima Budakoti [email protected] .Alternatively, please visit ourwebsite www.hvsinternational.com andregister yourself.

About HVSHVS International is the world’sleading full-service consulting andappraisal firm devoted exclusivelyto the hospitality industry.Founded in 1980 in the UnitedStates, the company has 22 officesacross the globe. Since 1980, HVShas consulted with over 10,000hotels in more than 70 different

countries worldwide. The SouthAsia office is based out of NewDelhi, India.

HVS International has beenoperating in India for eight years.The HVS team has worked onprojects ranging from feasibilityand marketing studies; valuationof hotels; residual land values;operator search & managementcontract negotiations;development strategies for newbrands; research reports andinvestment services. Our clients inIndia include Indian Hotels, EIHLtd, ITC Hotels, Hotel LeelaVenture Ltd, Forte Plc,Intercontinental Hotels & Resorts,Mandarin Oriental, CarlsonHospitality, Hyatt International,Hilton International, ChoiceInternational, Silver link Holding,Lehman Bros., ICICI Bank, SunGroup, Emaar (Dubai) andKingdom Holding, among others.

In May 2001, we launched HVSExecutive Search, to cater to thestaffing needs of the hospitalityand related services sectors likereal estate, media, telecom andaviation. Apart from being the firstretained search firm for thehospitality industry in India, HVSExecutive Search also providesservices in areas of HR Consultingand Compensation Survey &Design. In addition to its NewDelhi office, HVS ExecutiveSearch has offices in New York,London and Hong Kong.

HVS Executive Search has alsolaunched two websites:2020skills.com andhospitalitycareernet.com. 2020Skills is an internet - basedassessment tool specificallydesigned for service industry

18 Hotels in India - Trends & Opportunities 2001 HVS International

About the Authors

Manav Thadani joined HVS International’s New York office as aConsultant and Valuation Analyst in September 1995. Prior to joiningHVS, he gained six years of operational experience in various hotels inNew York City. In early 1997, Manav planned the opening of HVSInternational’s first Asian office in India, which was established in NewDelhi later in the year.

Manav holds a Masters degree in Food Service Management from NewYork University (NYU), prior to which he completed his undergraduateeducation in hotel management at NYU.

Siddharth Thaker, joined HVS International, New Delhi in August 2004as Consulting and Valuation Analyst. Formerly, he worked as RevenueManager with Le Meridien Hotels & Resorts at UAE, Tashkent andKuwait. Prior to Le Meridien Hotels & Resorts, he worked with the TajGroup of hotels for two years. He has conducted feasibility and marketstudies and performed hotel valuations for major hotel chains and clients.

Siddharth holds a MMS degree with specialization in advanced financialmanagement and a Bachelors degree in economics and financialaccounting from Bombay University.

Ambika Mehta joined HVS International’s New Delhi office as ResearchAssociate in May 2003. She is currently working as Senior Associatehandling search assignments for international clients, for which she worksin close coordination with the HVS Executive Search divisions acrossthe globe. She also executes the Expatriate positions for the New Delhioffice. Prior to joining HVS, Ambika worked for about a year asManagement Trainee with Omam Consultants.

Ambika holds a Bachelor of Arts degree in Psychology (with Honours)from Lady Shriram College, Delhi University. In 2002, she earned anMBA degree specializing in HR from Benaras Hindu University.

professionals, for assessingperformance characteristics andcultural compatibility. 2020 Skillswas authored by professorsFlorence Berger and JudyBrownell of the Cornell UniversitySchool of Hotel Administration

and HVS Executive search. Theassessment profile has threeunique levels: senior, mid-management, and line. The sitecan be accessed atw w w . 2 0 2 0 s k i l l s . c o m .www.hospitalitycareernet.com is

a web site that provides state-of-the-art solutions for employmentnews, career advice, compen-sation assessment, and more. It hasbecome one of the most efficientways to recruit, hire, and retainprofessionals.

HVS International Hotels in India - Trends & Opportunities 2001 19

20 Hotels in India - Trends & Opportunities 2001 HVS International

OFFICES:Asia - PacificIndiaC-67, Anand Niketan,New Delhi 110 021(91) (11) 5166 3031(91) (11) 5166 3032 fax

Hong Kong183 Jade VillaNgau Liu Chuk Yeung RoadSaikung(852) 2791 5868(852) 2792 2358 fax

Singapore79, Anson Road#11-05Singapore 079906(65) 6293 4415(65) 6293 5426 fax

Sydney5 Elizabeth StreetSuite 101,Level 1Sydney, NSW 2000(61 2) 9233 1125(61 2) 9233 1147 fax

EuropeLondon7-10 Chandos StreetCavendish SquareLondon W1G 9DQ(44) (20) 7878 7700(44) (20) 7436 3386 fax

MadridC/Capitan Haya, (planta 15)28020, MadridSpain(34) 91 417-6937(34) 91 556-2880 fax

North AmericaNew York372 Willis AvenueMineola, NY 11501(516) 248-8828(516) 742-3059 fax

Denver1777 South Harrison StreetSuite 906Denver, CO 80210(303) 512-1222(303) 691-3799 fax

Dallas2601 Sagebrush DriveSuite 101Flower Mound, TX, 75028(972) 899-5400(972) 899-1022 fax

Vancouver4235 Prospect RoadNorth Vancouver, BCCanada V7N 3L6(604) 988-9743(604) 988-4625 fax

Toronto6, Victoria StreetToronto ON M5E 1L 4,Canada(1) (416) 686 2260(1) (416) 686 2264 fax

Miami8925 SW 148th StreetSuite 216Miami, FL 33176(305) 378-0404(305) 278-4484 faxm

San Francisco116 New MontgomeryStreet, Suite 620San Francisco, CA 94105(415) 896-0868(415) 896-0516 fax

Boulder2229 BroadwayBoulder, CO, 80302(303) 443-3933(303) 443-4186 fax

Washington DCSuite 1021300 Piccard DriveRockville, MD, 20850(240) 683-7123(240) 683-7120 fax

ChicagoSuite 1A445 West Erie StreetChicago, II, 60610(312) 587-9900(312) 587-9908 fax

Phoenix4913 E Mitchell drivePhoenix, AZ, 85018(602) 667-6655(602) 269-1864 fax

Weston, CD262 Lyons Plain RoadRiversbendWeston, CT, 06883(203) 226-6000(203) 221-0068 fax

Boston4th Floor607 Boylston StreetBoston, MA, 02116USA(617) 424-1515

South AmericaBuenos AiresSan Martin 640-40 Piso(1004) – Buenos AiresArgentina54-11-4515-146154-11-4515-1462 fax

São PauloAv Brig Faria Lima1912 cj 7F01452-001-Sao Paulo/SPBrazil55-11-3093-274355-11-3093-2783 fax

DIVISIONS

• Consulting Services

• Executive Search

• Investment Services & Brokerage

• Food & Beverage Services

• Asset Management & OperationalAdvisory Services

• HVS/Ference Group:

Operational & Management StrategyDevelopment

• Timeshare Consulting & ResortDevelopment Services

• Valuation Services

• Gaming Services

• HVScompass (Interior Design)

• Convention, Sports & EntertainmentFacilities Consulting

• Marketing Communications

• Technology Strategies

• Hotel Parking Solutions

• Golf Services