pension credit law centre ni october 2009. pension credit two elements guarantee credit savings...

TRANSCRIPT

Pension Credit

Law Centre NI October 2009

Pension Credit

Two Elements

Guarantee credit

Savings credit

Guarantee Credit

aged over 60 living in Great Britain habitually resident in Great

Britain right to reside not subject to immigration

rules

Calculating Guarantee Credit

appropriate minimum guarantee

total income

compare

Appropriate Minimum Guarantee

Standard minimum guarantee

Single £130.00

Couple £198.45

Additional amountsSevere disabilitySingle £52.85Couple one qualifies £52.85Couple both qualify £105.70

CarerSingle £29.50Couple one qualifies £29.50Couple both qualify £59.00

Appropriate Minimum Guarantee

Housing costs

Eligible housing costs mortgage interest interest on loans for repairs and

improvements ground rent service charges

Must be liable to meet the housing costs dwelling normally occupied by person claiming limited to £100,000 or £200,000 (but may

claim a transitional amount)

Non-dependent reductions

Gross income weekly

deduction£382 or more £47.75£306 - £381.99 £43.50£231 - £305.99 £38.20£178 - £230.99 £23.35£120 - £177.99 £17.00Less than £120 £ 7.40

No non-dependent deductions for non-dependent who is: Under 20 for whom person, partner is

“responsible” 16 or 17 years old under 25 in receipt of Income Support or JSA

(IB), or C/ESA or IR ESA assessment phase full-time student receiving Work-based Learning for Young

People Allowance temporarily absent from home for more than

52 weeks co-owner or joint tenant normally residing elsewhere in receipt of Pension Credit

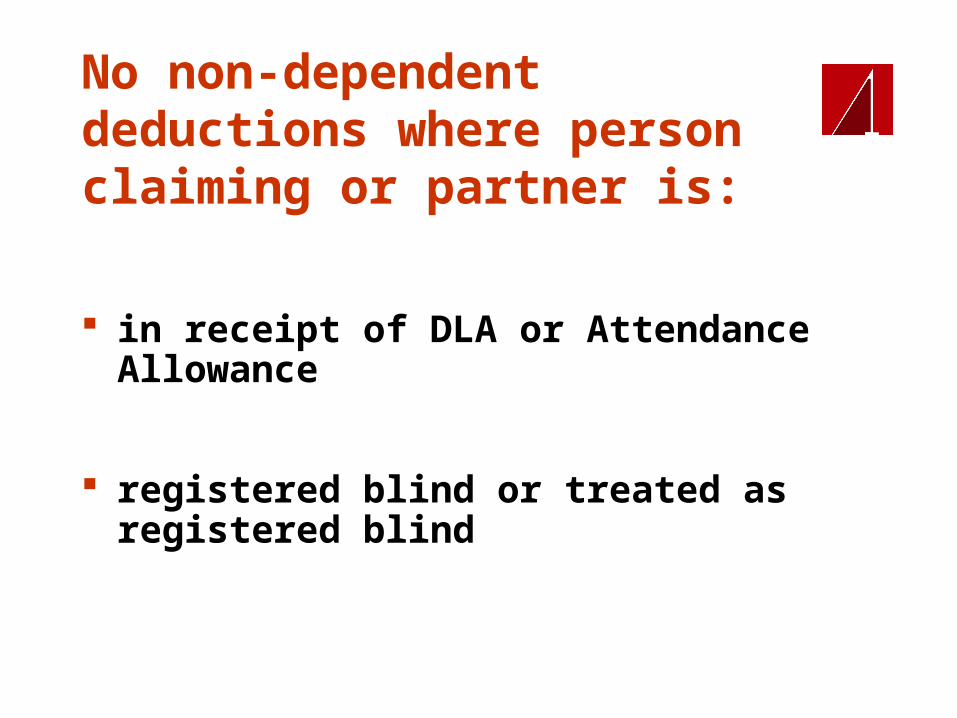

in receipt of DLA or Attendance Allowance

registered blind or treated as registered blind

No non-dependent deductions where person claiming or partner is:

Income

EarningsNet earnings = gross minus tax

minusNational Insurance minus half of anypension contribution

Earnings cont…

Earnings Disregard£20 where a person or partner: is a lone parent is a part-time fire fighter, auxiliary

coastguard, part-time crew of lifeboat or member of T.A., part-time RIR or part-time PSNI

is entitled to a Carers additional amount in receipt of IB, SDA, DLA, Attendance

Allowance, mobility supplement, disability or severe disability element of WTC

in certain circumstances has previously had a £20 disregard

Earnings cont…

Others

Couple £10

Single £5

Benefits and Tax CreditsIgnore DLA Attendance Allowance Constant Attendance Allowance or Exceptionally

SDA Child special allowance Guardians Allowance increases in benefits for children Social Fund payments Child Benefit Christmas bonus Child Tax Credit Housing Benefit Bereavement Payments

Disregard £10

War Disablement Pension War Widow(er)’s or surviving civil partner’s

Pension pensions paid as result of death or

disablement of member of the services compensation for non-payment of War

Pensions Similar pensions paid by other countries Pensions paid to victims of Nazi persecution Widowed Parents and Widowed Mothers

Allowance

Count in full

Retirement Pension Shared additional pension Graduated Retirement Pension Occupational and personal pensions Income from overseas arrangement,

retirement annuity contract, annuities or insurance policies

Working Tax Credit Payment made under the Financial

Assistance Scheme

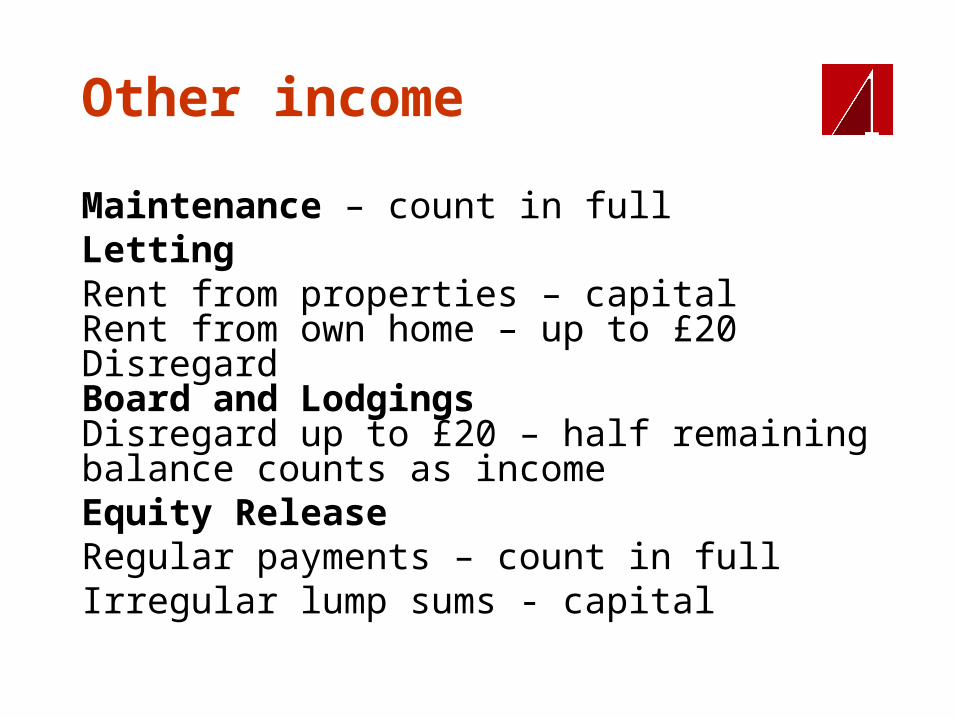

Other income

Maintenance – count in fullLettingRent from properties – capitalRent from own home – up to £20DisregardBoard and LodgingsDisregard up to £20 – half remainingbalance counts as incomeEquity ReleaseRegular payments – count in fullIrregular lump sums - capital

Capital

No upper capital limit

Capital below £6,000 is ignored £10,000 if in care £10,000 for all from 2nd November 2009

Income from capital£1 for every £500 or part of £500 over£6,000/£10,000

Assessed Income PeriodRetirement provision defined as:

Retirement Pension income

Income from annuity contracts

Income from capital

Assessed Income Period Over 65 (partner over 60)

– remains the same for 5 years (or 7 if transferred from Income Support on 6 October 2003)

Over 75 (partner over 60) – remains the same

indefinitely

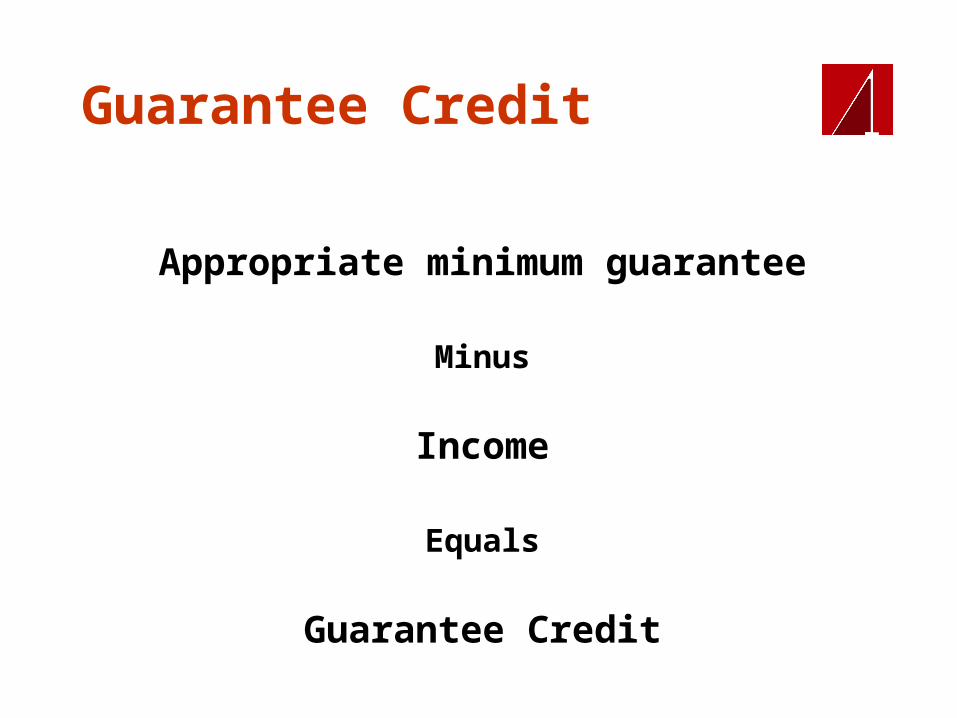

Guarantee Credit

Appropriate minimum guarantee

Minus

Income

Equals

Guarantee Credit

Example 1

Ms B is single, age 74, lives alone in

private rented accommodation. Her

only income is her retirement pension

of £95.25 and Attendance Allowance

Example 1 cont…

Guarantee creditStandard minimum guarantee £130.00Additional amount: severe disability £ 52.85Appropriate minimum guarantee £182.85Income: retirement pension £ 95.25Appropriate minimum guarantee £182.85Less income £ 95.25Guarantee Credit £ 87.60 Mrs B is entitled to a guarantee credit of £87.60

Savings Credit

Aged 65 or over or have a partner who

is 65 or over

Can be paid in addition to guarantee

credit or in its own right

Calculating Savings CreditSix Steps Calculate income Calculate appropriate minimum

guarantee Calculate qualifying income Select savings credit threshold Compare qualifying income and

threshold Compare income with appropriate

minimum guarantee

Steps 1 and 2

Step 1 Calculate income – same as for

guarantee credit Step 2 Calculate appropriate minimum

guarantee – same as for guarantee credit

Step 3 Calculate qualifying income –

Income fromStep 1 minus any:– Working Tax Credit– Incapacity Benefit– JSA (C) – SDA– Maternity Allowance– Maintenance– ESA (C)

Step 4

Select threshold

Single £ 96.00 Couple £153.40

Step 5

Calculate maximum savings credit by comparing qualifying income and threshold

Less than threshold no entitlement More than threshold calculate 60% of the

differenceMaximum Savings Credit– Single £20.40– Couple £27.03

If the 60% is above the maximum then it iscapped at maximum

Step 6

Compare income to appropriate minimum guarantee

Income less than appropriate incomeguarantee entitlement is the amount calculated at Step 5

Income more than appropriate income guarantee calculate 40% of difference

Deduct from amount calculated at Step 5 to get entitlement to savings credit

If 40% is more than amount at step 5 then no entitlement to savings credit

Example 2

June is aged 72 and lives alone. Her

income includes her state retirement

pension of £95.75 and a private pension of £40.45 per week. She lives in rented

accommodation.

Example 2 cont…

Step 1: Calculate incomeRetirement pension £95.25Private pension £40.45Total (A on flowchart) £135.70

Step 2: Calculate appropriate minimum guarantee

Single (B on flowchart) £130.00

Example 2 cont…

Step 3: Calculate qualifying incomeNo exempt income therefore qualifyingincome is the same as her income

(£135.70)(C on flowchart)

Step 4: Select threshold (D)Single £96.00

Example 2 cont…

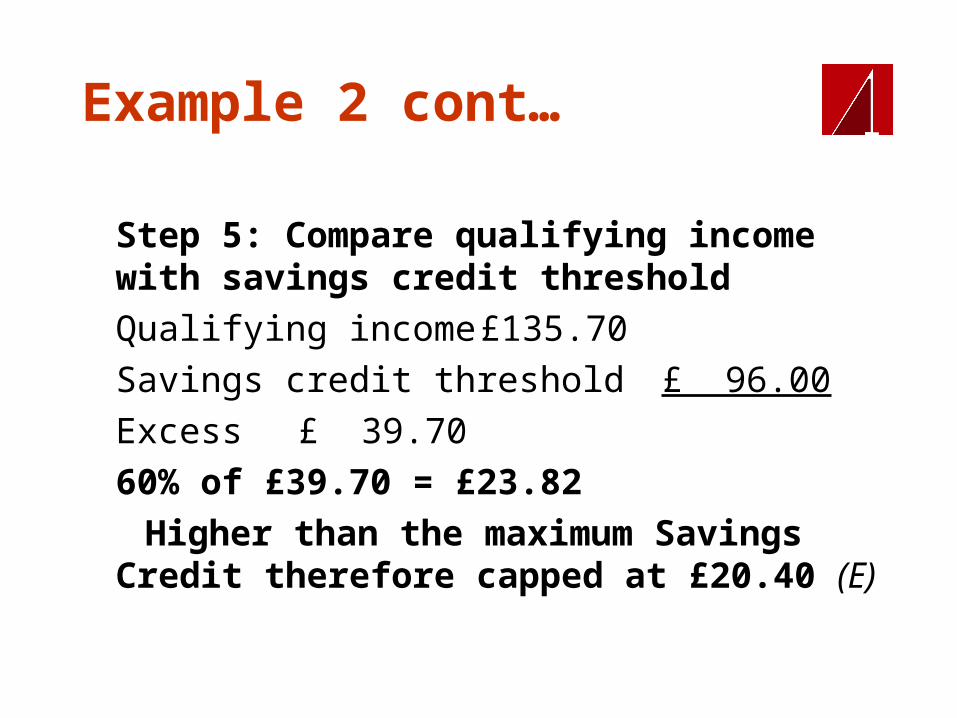

Step 5: Compare qualifying income with savings credit thresholdQualifying income £135.70Savings credit threshold £ 96.00Excess £ 39.7060% of £39.70 = £23.82

Higher than the maximum Savings Credit therefore capped at £20.40 (E)

Example 2 cont…

Step 6: Compare income with appropriate minimum guaranteeIncome £135.70Appropriate minimum guarantee £130.00Excess £ 5.70 (F)

Income more than minimum guarantee then calculate 40% of the excess

Example 2 cont…

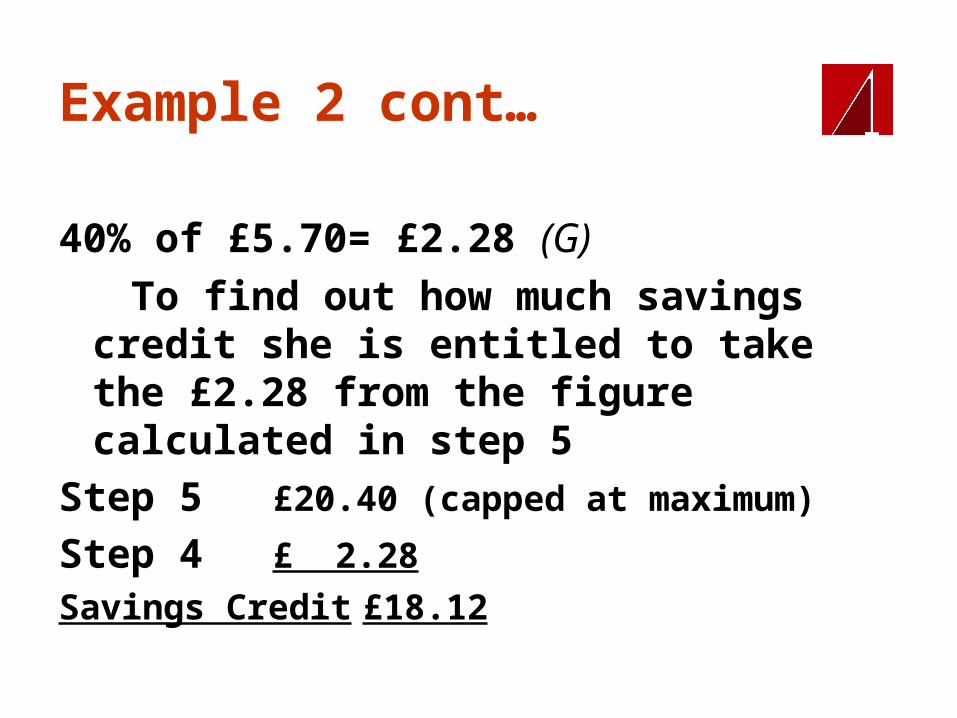

40% of £5.70= £2.28 (G) To find out how much savings credit

she is entitled to take the £2.28 from the figure calculated in step 5

Step 5 £20.40 (capped at maximum)

Step 4 £ 2.28

Savings Credit £18.12

Passporting Benefit Passported BenefitIncome SupportJobseekers Allowance (IB)Pension Credit (Guarantee Credit)IR ESA

Free school mealsSocial Fund:CCG

–Budgeting Loans–Funeral Expenses–Maternity Expenses–Cold Weather Payments

Health BenefitsHousing Renovation Grants

Passporting Benefit

Passported Benefit

Pension Credit (Savings Credit) from

SOCIAL FUND – as above

Child Tax CreditWorking Tax Credit

Health BenefitsSocial Fund:

–Funeral Expenses–Maternity Expenses

Child Tax Credit and Working Tax Credit not in payment (gross income below £16,040

Free school meals

Housing Benefit Social Fund:–Funeral Expenses