pensions core course 2013: measures to increase coverage in the 2008 chilean pension reform

TRANSCRIPT

MEASURES TO INCREASE

COVERAGE IN THE 2008

CHILEAN PENSION REFORM

Gonzalo Reyes

Sr Social Protection Economist, LCSHS

The World Bank

Contents

• The situation in 2006.

• Rationale for a reform

• Reasons for coverage gap.

• Measures of the 2008 Pension Reform

• Some initial Results

• Conclusions

The situation as of 2006 • Private pension system going into its 25th anniversary.

• All workers entering the market since May 1981 mandatorily enrolled in FDC, privately managed pension system.

• Existing workers as of May 1981 could choose to join the new system with no option to move back to the old PAYG DB pension system. • Historical contributions converted into an initial balance in new

individual account through a “recognition bond”.

• Minimum pension guarantee for those with 20 years of contributions.

• Means – tested Social Assistance Pension for people 65 and older (PASIS).

• Institutional arrangement: • Private PFM New DC system

• Public Social Security Institution Legacy DB system

• Ministry of Planning (Social Development) Social Assistance Pensions

Evolution of membership in the new

system.

Number of total members of the pension system exceeded total Labor

Force, but only half of them were making a contribution.

Source: Rofman et al. (2008)

Context: High coverage for LAC standards.

Total number of contributors as % of employed population

Total number of contributors as % of wage earners

Source: Rofman et al. (2008)

Coverage of the elderly

Lower coverage of the elderly than in other high formality countries, with

important role played by Social pensions, especially for women.

Source: Rofman et al. (2008)

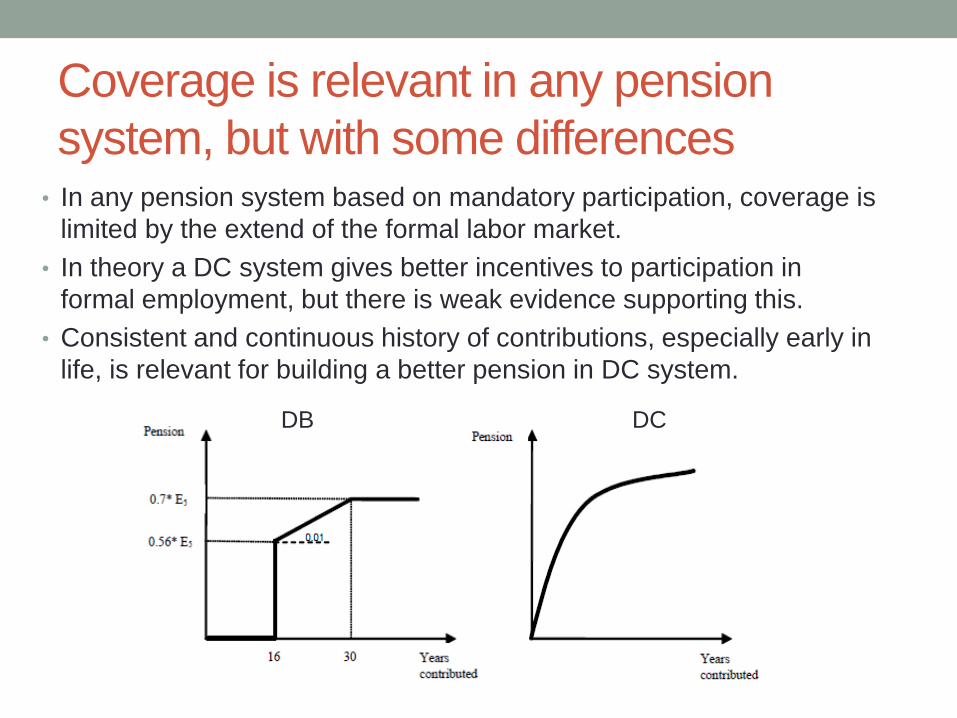

Coverage is relevant in any pension

system, but with some differences • In any pension system based on mandatory participation, coverage is

limited by the extend of the formal labor market.

• In theory a DC system gives better incentives to participation in

formal employment, but there is weak evidence supporting this.

• Consistent and continuous history of contributions, especially early in

life, is relevant for building a better pension in DC system.

DB DC

Coverage: Diagnostics. • There is considerable mobility across employment status for people in

the working age group.

• On average, people spend close to 50% of their potential working life

in the formal salaried sector

• The main reason for men not to contribute is being a self-employed

worker, while for women is being out of the labor force.

Distribution of Potential labor life Distribution of Periods without contributions

Self-employed Formal Informal Unemployed Out of LF

Source

Male Female Male Female

Coverage: Contribution Density • As a result, the average density of contributions is close

to 50%, with great heterogeneity in its distribution.

Source: SAFP based on sample of Contributions history

Women Men

Contribution Density for Labor History

05

10

15

% d

e a

filia

do

s

0 20 40 60 80 100densidad de cotizaciones (%)

05

10

15

% d

e a

filia

do

s

0 20 40 60 80 100densidad de cotizaciones (%)

Average:56% Average:48%

Coverage: Contribution Density: 19-29 yrs of

age

Despite the importance of early contributions, the situation is worse among the young population

Women Men

As a Result: Low expected pensions

• 40-50% receiving pensions below the minimum pension

• Few participants qualify for guaranteed minimum pension

Strategies to Increase Coverage

• For individuals with no savings capacity: • Stronger social safety net

• Special measures for targeted groups (e.g. women)

• For individuals with limited savings capacity • Improve incentives to save

• Provide complementary benefits

• For individuals with savings capacity, not currently covered: • Mandate participation

• Increase compliance

Integrated pension system, since these are not three disjoint groups: People move among them in their working lives!

2008 Pension Reform Measures to

Increase Coverage • Create a New Solidarity Pillar

• Basic Solidarity Pension for individuals who could not contribute

• Solidarity Complement for individuals who financed small pensions, with claw-back provision.

• Mandate self-employed workers to contribute and improve contribution enforcement

• Annual Contribution through tax declaration process for specific portion of self-employed workers (formal)

• New methods and attributions to detect non-compliance of contribution payments by employers.

• Strengthen contributory system.

• Subsidy for young workers first 24 contributions paid before age 35.

• Subsidy for voluntary contributions

• Creation of Voluntary Private Occupational Plans

• Provide equal conditions for men and women

• Bonus per child for women, equivalent to 1 year contributions

• Life and Disability Insurance fees separated by gender

• Redistribution of savings in case of divorce

New Solidarity Pillar

75

255

255

45°

(Units are thousand Chilean $ per month)

Requirements:

- Belong in 60% of

poorest households.

- 20 years residency.

Benefits are individually

based, compatible with

other individual in same

household receiving

benefit.

Voluntary pillar

• Increase voluntary savings

• Collective voluntary savings (Occupational plans, like 401k in USA) • Matching contributions paid by employers.

• 15% Subsidy to voluntary savings paid by the State

Número de cotizantes de Marzo 2008 con saldo por cotizaciones voluntarias o

depósitos convenidos, según ingreso imponible

-

20.000

40.000

60.000

80.000

100.000

120.000

140.000

Menos de

$100 mil

$100 - $200

mil

$200 - $300

mil

$300 - $400

mil

$400 -$500

mil

$500 -$600

mil

$600 -$700

mil

$700 -$800

mil

$800 -$900

mil

$900 mil - 1

millón

Más de 1

millón

Ingreso imponible de los cotizantes (pesos)

Nú

mero

de c

oti

zan

tes

By design, only high income individuals take advantage of tax exemptions

for voluntary savings.

Contributors with Voluntary savings by income level (March

2008)

SOME RESULTS.

Coverage of the working group.

• General positive trend in contributory coverage

Contributors as a percentage of Employed

population.

Source: Own calculations based on S.Pensiones and INE

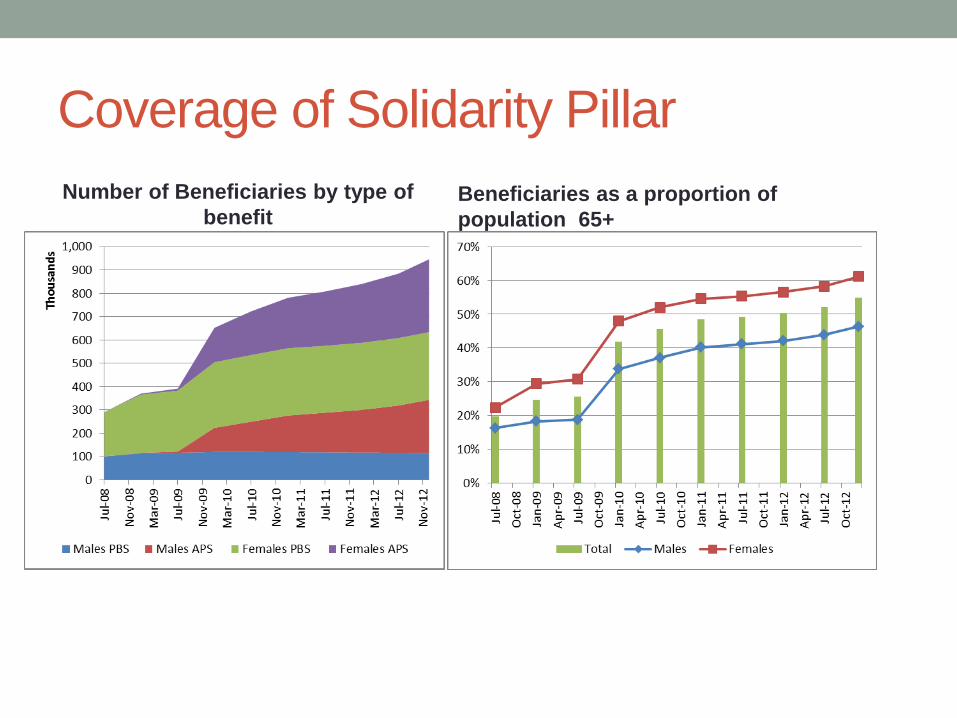

Coverage of Solidarity Pillar

Number of Beneficiaries by type of

benefit Beneficiaries as a proportion of

population 65+

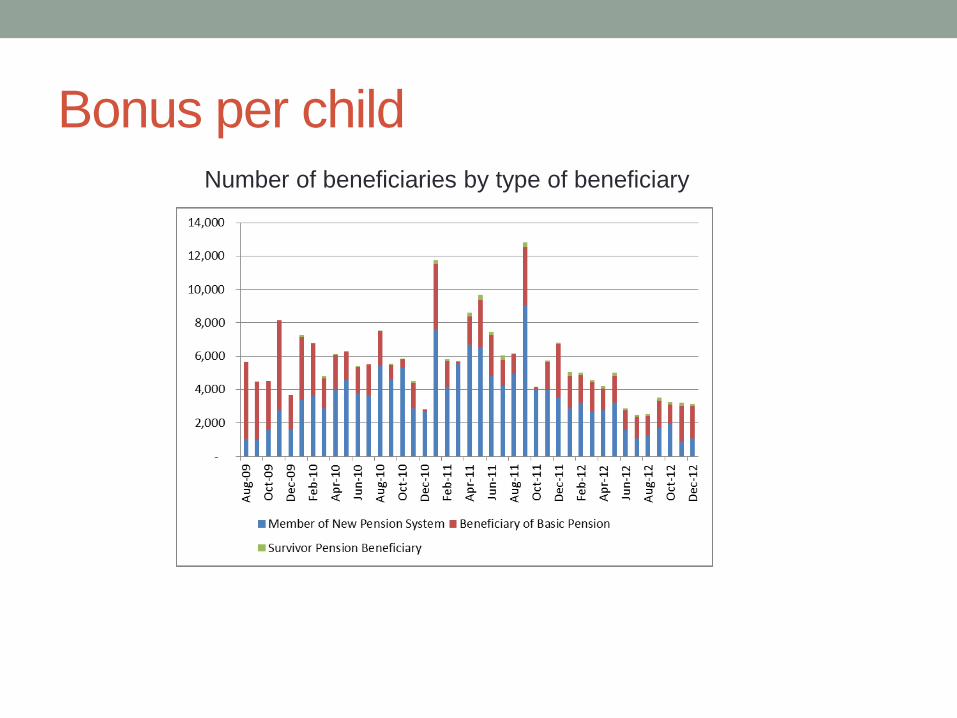

Bonus per child Number of beneficiaries by type of beneficiary

Fiscal Costs

• Solidarity pillar is main driver of fiscal costs.

• Important initial expenditure on Maternal Bonus (stock of retired mothers).

• Cost of Assistance Pensions in 2007 approx. 0.3% of GDP Additional cost of Reform: 0.4 – 0.5% of GDP, in line with original estimates.

• It is expected that the reform will have a total cost of 1% of GDP by 2025, with 0.8% corresponding to the new solidarity pillar.

0.70%

0.71%

0.72%

0.73%

0.74%

0.75%

0.76%

0.77%

0.78%

0.79%

0.80%

0

100

200

300

400

500

600

2S 2010 1S 2011 2S 2011 1S 2012 2S 2012

Solidarity Pillar: old Age Solidarity Pillar: Disability

Contribution subsidies Bonus per child

Cost as % GDP

Bn. Cl$ % of

GDP

Conclusions

• Coverage and adequacy gap due to high mobility in and out of formal employment.

• Gender inequality exacerbated by DC pension system

• Strong rationale for integration between non-contributory and contributory systems.

• Improve incentives to participate voluntarily and provide protection while maintaining link between contributions and benefits.

• Results underlie relevance of integrated approach and gender equity measures.

• Still early for impact of self-employed mandate, but already clear that occupational plans did not have an impact.