personnel and payroll - the grid · financial handbook for schools hertfordshire county council...

TRANSCRIPT

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 1 RESO3529 – Issue 3 : April 2003

SECTION 13 PERSONNEL AND PAYROLL

TABLE OF CONTENTS

Page

Contacts for Section 13 3

13.1 Introduction 513.2 Payroll process 513.3 Employment status of persons engaged by the school 613.4 Taxable expenses and benefits in kind 613.5 Authorised signatories 713.6 Inland Revenue 713.7 Review of payroll reports 813.8 Inland Revenue concession or payments to performers, guest

lecturers and speakers8

13.9 Payroll provider 813.10 Information and returns required from schools with external payroll

arrangements9

Appendix A Employed or self-employed 13Appendix B General agreement with the Inland Revenue on payments to

performers, guest lecturers and speakers etc.21

Appendix C Guidelines for schools’ travel and subsistence expenses 23Annex A Reimbursement of travel expenses 35

Appendix D Authorised signatory listing 39Appendix E Requirements for a payroll provider 41Appendix F Monthly and annual returns required from schools with external

payroll arrangements43

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 2 RESO3529 – Issue 3 : April 2003

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 3 RESO3529 – Issue 3 : April 2003

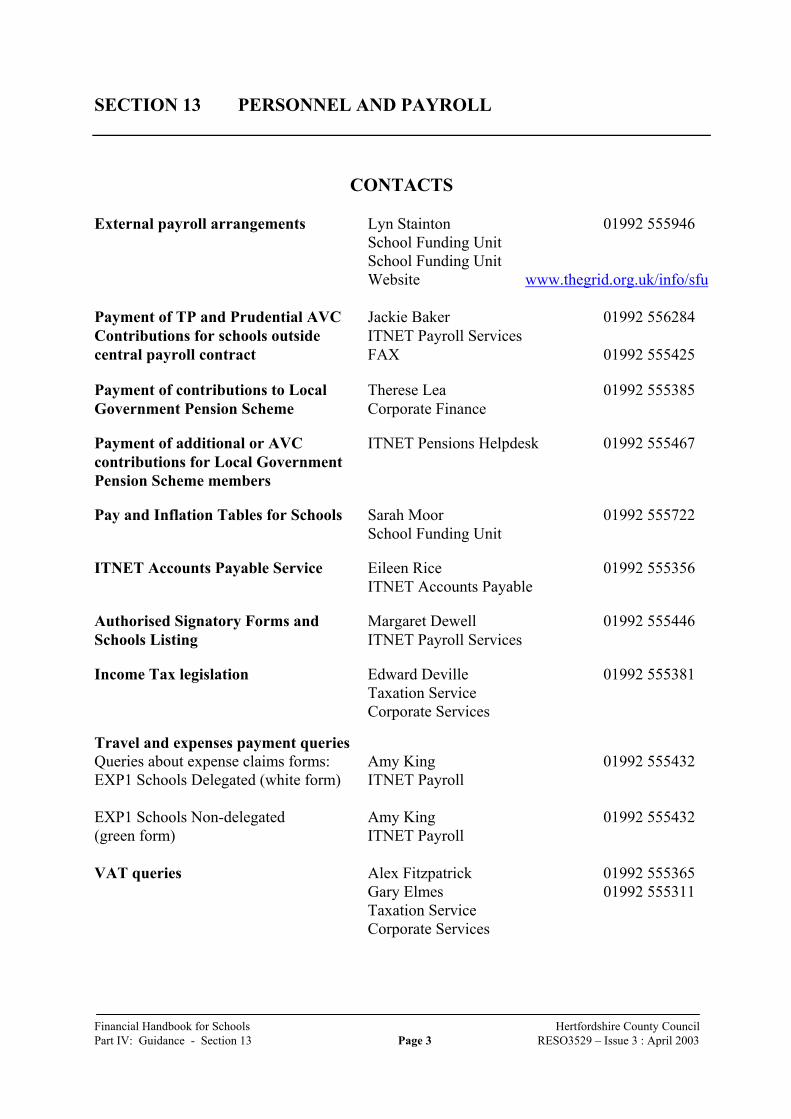

SECTION 13 PERSONNEL AND PAYROLL

CONTACTS

External payroll arrangements Lyn Stainton 01992 555946School Funding UnitSchool Funding UnitWebsite www.thegrid.org.uk/info/sfu

Payment of TP and Prudential AVC Jackie Baker 01992 556284Contributions for schools outside ITNET Payroll Servicescentral payroll contract FAX 01992 555425

Payment of contributions to Local Therese Lea 01992 555385Government Pension Scheme Corporate Finance

Payment of additional or AVC ITNET Pensions Helpdesk 01992 555467contributions for Local GovernmentPension Scheme members

Pay and Inflation Tables for Schools Sarah Moor 01992 555722School Funding Unit

ITNET Accounts Payable Service Eileen Rice 01992 555356ITNET Accounts Payable

Authorised Signatory Forms and Margaret Dewell 01992 555446Schools Listing ITNET Payroll Services

Income Tax legislation Edward Deville 01992 555381Taxation ServiceCorporate Services

Travel and expenses payment queriesQueries about expense claims forms: Amy King 01992 555432EXP1 Schools Delegated (white form) ITNET Payroll

EXP1 Schools Non-delegated Amy King 01992 555432(green form) ITNET Payroll

VAT queries Alex Fitzpatrick 01992 555365Gary Elmes 01992 555311Taxation ServiceCorporate Services

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 4 RESO3529 – Issue 3 : April 2003

Audit Commission data Susan Groom 01992 555329matching information Internal Audit

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 5 RESO3529 – Issue 3 : April 2003

SECTION 13 PERSONNEL AND PAYROLL

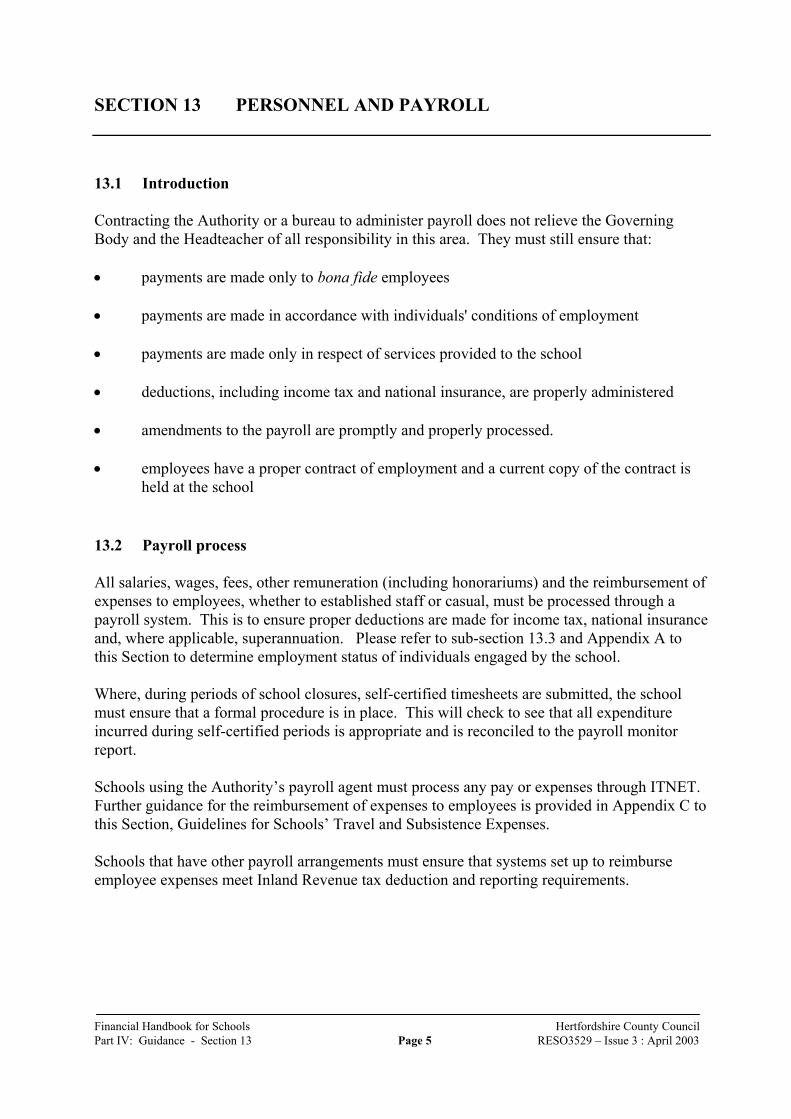

13.1 Introduction

Contracting the Authority or a bureau to administer payroll does not relieve the GoverningBody and the Headteacher of all responsibility in this area. They must still ensure that:

• payments are made only to bona fide employees

• payments are made in accordance with individuals' conditions of employment

• payments are made only in respect of services provided to the school

• deductions, including income tax and national insurance, are properly administered

• amendments to the payroll are promptly and properly processed.

• employees have a proper contract of employment and a current copy of the contract isheld at the school

13.2 Payroll process

All salaries, wages, fees, other remuneration (including honorariums) and the reimbursement ofexpenses to employees, whether to established staff or casual, must be processed through apayroll system. This is to ensure proper deductions are made for income tax, national insuranceand, where applicable, superannuation. Please refer to sub-section 13.3 and Appendix A tothis Section to determine employment status of individuals engaged by the school.

Where, during periods of school closures, self-certified timesheets are submitted, the schoolmust ensure that a formal procedure is in place. This will check to see that all expenditureincurred during self-certified periods is appropriate and is reconciled to the payroll monitorreport.

Schools using the Authority’s payroll agent must process any pay or expenses through ITNET.Further guidance for the reimbursement of expenses to employees is provided in Appendix C tothis Section, Guidelines for Schools’ Travel and Subsistence Expenses.

Schools that have other payroll arrangements must ensure that systems set up to reimburseemployee expenses meet Inland Revenue tax deduction and reporting requirements.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 6 RESO3529 – Issue 3 : April 2003

13.3 Employment status of persons engaged by the school

The Authority, and all schools and other establishments funded by the Authority, have a duty toidentify any individuals to whom they make payments who should be regarded as an employee.The onus is on the potential employer to determine whether the nature of the engagement hasthe characteristics of an employment – if so the individual engaged must be treated as anemployee. The effect of the PAYE Regulations is to place the responsibility for making thisdecision and settling any tax and national insurance liabilities on the employing party, not onthe individual. This applies whether or not that person later declares those earnings. Therefore,making the wrong initial judgement could have a serious impact in grossing up the schools'costs.

Appendix A to this Section provides guidance on how to determine whether an individual isemployed or not. It is important to note that an individual’s self-declared status as “self-employed” (even when supported by his/her accountant or Tax Office) should not be solelyrelied upon. Schools must rigorously follow the guidance set out in Appendix A to determineemployment status and are recommended to keep a record of the reasons for their decision. Ifthere is any doubt at all, then the individual must be asked to complete the questionnaire at theend of Appendix A and submit this to the County Council’s Tax Inspector for a ruling on thecase.

13.4 Taxable expenses and benefits in kind

Schools must be aware that certain expenses paid to employees may be taxable, dependingupon the nature of the expenses, the level of those expenses and the circumstances in whichthey are paid. For example, travel costs between home and the normal place of work areprivate, and any reimbursement is ordinarily taxable. With reimbursed business travel, any excess ofmileage rates above those accepted by the Inland Revenue attract tax and, where relevant,Employers’ and Employees’ Class 1 National Insurance.

Equally any benefits in kind provided to employees may attract tax and Employers’ Class 1ANational Insurance. These include for example:

• accommodation provided at less than market rent (although there are exceptions wherean employee is required to live on site to fulfil his/her duties)

• use of school vehicles for private use

• clothing provided to employees, except where this meets specific conditions to beclassed as a uniform. In particular, if the clothing is in any way suitable for social orexternal use, it should bear a permanent, fixed logo bearing the name of the school.This should avoid tax and national insurance contribution issues

• school equipment and facilities made available to employees for private use. However,important exceptions include:

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 7 RESO3529 – Issue 3 : April 2003

- insignificant private use of equipment and machinery on school premises. Forexample, modest and sporadic use of photocopiers and PCs

- private use of employer-owned computer equipment with an original cost of£2,500 or less

- private use of employer owned mobile telephones.

These exceptions apply for tax and national insurance contribution purposes and are obviouslysubject to normal, disciplinary procedures as to the use of Authority equipment.

Facilities and equipment used privately at home, (other than those excepted above) will also beliable to tax and national insurance. This particularly applies to fixed, home telephones wherethe bill is paid by the school.

Essentially, any other goods, services or facilities made available to employees at less than theirmarket value may be deemed to be a taxable benefit. Accordingly any such benefits should bepaid via the EXP1 expenses claim and identified as taxable, where appropriate, or otherwisedeclared to the Inland Revenue. Expense claim forms must be processed via the school’spayroll provider, and the EXP1 expense claim form has been developed for this purpose forschools within the HCC ITNET payroll service contract. Schools that have other payrollarrangements must ensure that a similar mechanism is set up with their payroll provider toensure that, where appropriate, tax and national insurance contributions are correctly deducted.These schools are strongly advised to obtain a dispensation from the Inland Revenue for thepayment of any expenses other than through their payroll provider, and they must makearrangements with their payroll provider to process any taxable expenses as such.Schools will be liable for any unpaid tax, national insurance and penalties thereon.

13.5 Authorised signatories

Headteachers must maintain a list of authorised signatories for payroll administration. Forschools using the Authority’s payroll agent, a copy must be sent to ITNET. ITNET carry out anannual review of authorised signatories. However, schools should ensure that any changes arenotified to ITNET immediately to ensure the authorised listing is kept up to date.

Further guidance and a copy of the form for notifying changes to authorised signatories arereproduced in Appendix D to this Section.

For schools that have other payroll arrangements, a copy must be sent to the payroll bureau orprovided to payroll administration staff.

13.6 Inland Revenue

In employing staff, the Governing Body must, by law, declare to the Inland Revenue paymentsmade to its staff. It follows that, where contractual arrangements are made on behalf of the

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 8 RESO3529 – Issue 3 : April 2003

Authority, these should be paid through a payroll system. The necessary deductions andemployer's contributions must be calculated, and the school charged with the full cost. It is notcorrect to assume that the employee is responsible for declaring this income for his or her owntax purposes.

The liability of the County Council extends to paying to the Inland Revenue any tax or nationalinsurance due that has not been deducted, and this would be passed on to the school. Inaddition, under the Authority's Scheme for Financing Schools, any fines, penalties orsurcharges levied on the County Council in such circumstances can be charged against theschool's budget.

13.7 Review of payroll reports

Whether paying its own staff or using a payroll bureau (the bureau will provide a payrolltransaction report) the school should ensure through monthly reviews that all, and only, bonafide staff are included, and that all payroll changes are correct. The payroll transaction reportshould be signed and dated to evidence this check.

The school should also check, at least annually, that gross pay agrees with contracts or otherauthorised documents, and that deductions have been correctly determined.

13.8 Inland Revenue concession for payments to performers, guest lecturers andspeakers

Difficult situations can arise when schools purchase services from external suppliers, if theschool does not know whether they are employed or self-employed for tax purposes. It hasbeen recognised by the Inland Revenue that this situation creates work for schools and theaffected departments within the County Council. To try to help with this, Hertfordshire CountyCouncil has negotiated a ‘concession’ in this area where, in the appropriate circumstances, apayment of up to £350 can be paid to an individual gross, without considering his or hertaxation status. This does not, of course, apply where a short term employment contract isintended. This concession is only available to schools within HCC’s contract with ITNET forpayroll services. All schools with external payroll arrangements must separately negotiate asimilar concession with Inland Revenue.

Appendix B to this Section sets out the detailed conditions for this concession; please referto it and Appendix A before seeking to apply this concession.

13.9 Payroll provider

The Governing Body must seek the advice of the Assistant Director (Resources) before enteringinto contractual arrangements with a payroll bureau other than the County Council's payrollagent (ITNET), or if it is proposing the use by the school of a computerised payroll software package. The school or payroll bureau would need to comply with the requirements set out in

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 9 RESO3529 – Issue 3 : April 2003

Appendix E to this Section.The Authority’s Best Value Guide no 4, Good Value in Purchasing Payroll, providesinformation and advice in the selection of a payroll provider. This publication can bedownloaded from the School Funding Unit website. See contacts for this Section.

The contract with such a provider should include:

• job specifications• details on the ownership of programs and data files• identification of who is responsible for

– control and accuracy of data– authorising the bureau to make changes to the data– providing back-up arrangements in the event of systems breakdown

• provision for access for the school's staff and auditors• funding dates if the bureau originates payments• provision for the payment of income tax, national insurance, statutory sick and

maternity pay, superannuation (teachers' and local government) and other deductions.

The Governing Body should review any current contract arrangement regularly and critically.

13.10 Information and returns required from schools with external payrollarrangements

Teachers’ Pensions Regulations

Under the Teachers' Pensions Regulations the Authority is regarded as the employer forpension purposes for all maintained schools. In essence this means that the Authority isresponsible for sending monthly contribution payments, annual salary and service returns andappointment and leaver notifications to Capita, Teachers' Pensions. The responsibility alsocovers payments of Additional Voluntary Contributions (AVCs) to Prudential. This does notaffect the employer/employee relationship in Foundation and Voluntary Aided schools.

The specification for payroll services provided to schools by an external agency must includeprovision for audit access to provide assurance that the correct level of contributions is beingmade over to the Authority.

The arrangements for the consolidation of TP and Prudential AVC payments for schools usingan external payroll provider are as follows:

Monthly • The external payroll provider must supply ITNET with a report by the last working day

of each month in the formats attached in Appendix F to this Section. The detail mustinclude the total:

– superannuable pay

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 10 RESO3529 – Issue 3 : April 2003

– total number of teachers– employees' contributions– additional contributions– employers' contributions– arrears paid (Elected Further Employment elections)– arrears paid (letters previous years)– refunds made (previous years only)– short term pensions– TR22 election amounts deducted– teachers' Prudential AVCs

Payment arrangements:

- BACS: ITNET will debit the school bank account and credit the HCC bankaccount (both transactions by BACS) with the amounts shown in the monthlyreport on the last working day before the 7th of the following month.

- Standing Order: Payment should credit the HCC bank account on the lastworking day before 7th of the following month.

- Cheque: Payment should be received by ITNET by the 3rd working day of thefollowing month.

• ITNET will maintain records of monthly payments for year-end purposes.

Late Returns

• Returns received after the last working day will be processed with the followingmonth’s contributions.

• Teachers' Pensions charge a penalty of 8% per day for late payment.

• Teachers paying Prudential AVCs will loose interest on contributions if payment isreceived late.

• Any penalty charges levied by TP or Prudential AVCs for underpayment will berecharged to the school, where this is the result of underpayment by the school or theschool's payroll provider.

Annual

• The external payroll provider must supply a detailed employee listing of the followingyear-end details for TP payments to ITNET by the last working day of April:

– superannuable pay– total number of teachers– employees' contributions– additional contributions

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 11 RESO3529 – Issue 3 : April 2003

– employers' contributions– arrears paid (Elected Further Employment elections)– arrears paid (letters previous years)– refunds made (previous years only)– short term pensions– TR22 election amounts deducted

This information must be provided in the format attached at Appendix F to this Section.

Copies of letters received from the TP for additional contributions and previous years'adjustments must also be included.

• An initial reconciliation will be carried out by ITNET. Schools will be notified if year-end returns do not agree with monthly statements, or if contributions do not agree withsuperannuable pay. The school will be responsible for resolving any discrepancies bythe last working day of May.

• Once the reconciliation is complete, all details will be included in HCC's annual return(PENTR17A) to Capita, Teachers' Pensions.

Late Returns

• Teachers' Pensions charge a penalty of 8% per day interest for underpayment at year-end.

• Any penalty charges levied by TP or Prudential AVCs for underpayment will berecharged to the school, where this is the result of underpayment by the school or theschool's payroll provider.

This information is only acceptable in paper form. The monthly returns may be faxed toITNET but a copy of the original must also be sent. See contacts for this Section.

Annual Teachers’ Service and Salary Return for Teachers’ Pensions

Teachers’ Pensions require that the Authority provide an annual return confirming the serviceof all teachers employed within the Authority. Therefore, Human Resources and ITNET willcontact schools with external payroll arrangements in February of each year to request theinformation in the format prescribed by Teachers’ Pensions.

Local Government Pension Scheme

All non-teaching staff have the option of joining the Local Government Pension Scheme.Hertfordshire County Council administers the scheme, and all contributions to the schemeshould be paid over monthly. The arrangements are as follows:

Monthly

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 12 RESO3529 – Issue 3 : April 2003

• The school or external payroll provider must supply Corporate Finance with a formdetailing employee’s and employer’s local government pension contributions by the 19th

of the month following deductions from the individual’s salary. See Appendix F for aformat of the monthly form. Corporate Finance will issue new forms every March,which should be used as a master and photocopied as necessary.

• The school or external payroll provider should pay over all contributions by the 19th ofthe month following the deductions from individuals’ salaries. Contributions can bepaid by cheque (made payable to Hertfordshire County Council) or by BACS. Eachpayment should be accompanied by the monthly form.

• The employer’s contribution rate varies every year, and the school will be informed ofthe rate for the new financial year in March each year by Corporate Finance.

• If an employee is purchasing added years, these contributions should also be paid overto the County Council and filled into the relevant box on the monthly form.

• However, if an employee is making AVC (Additional Voluntary Contributions) theseshould be paid directly to Equitable Life or Standard Life and not sent to the CountyCouncil. See contacts to this Section for further details.

Annually

• Corporate Finance will provide the school with a year end form in March each year,which should be completed and returned by the end of May. This summarises thepayments during the year to facilitate reconciliation.

• In addition, the school will need to provide ITNET Pensions with the details ofindividual employees’ contributions during the year to enter onto the Pensions database. The information required for each individual is: name, national insurancenumber, NI earnings, employees contributions, added years contributions (if applicable)and date started or left, if this happened during the year. See contacts to this Section forfurther details.

Audit Commission data matching

The County Council participates in the annual National Fraud Initiative undertaken by theAudit Commission. This initiative is a data matching exercise designed to reduce the search forfraudulent claims made upon Authorities.

Schools that have external payroll arrangements are required to participate by providinginformation on an annual basis. The Chief Internal Auditor will contact schools and provideguidance about the information required, format and timescales for this process. See contactslist for this Section for further information.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 13 RESO3529 – Issue 3 : April 2003

APPENDIX A EMPLOYED OR SELF-EMPLOYED?SECTION 13

1. Employment Status

Introduction

Where a school engages individuals – other than contracted staff – to carry out officialactivities for which a payment is made from the General Account, the school needs to considerthe payee status of the individual for purposes of income tax and national insurance.

A self-employed person is responsible for his/her own income tax and national insurancepayments.

However, it is the employer (the school) who is responsible for the correct calculation anddeduction of income tax and national insurance from the pay of an employee, and is also liableto pay an employer's national insurance contribution. Failure to account for the above willresult in the school being charged with the unpaid monies, plus any fines, penalties orsurcharges levied.

The law does not define 'employment' and 'self-employment' and the school cannot simplychoose to call a job 'employment' or 'self-employment'.

The issue is determined by considering the circumstances of the working arrangements.

In summary, employment status affects who is responsible to the Inland Revenue for thepayment of income tax and national insurance.

Employed or Self-employed?

The circumstances of the working arrangements are central to the issue. A majorconsideration is the type of contract or agreement. Such a contract need not be in writing; itcan be oral or expressed or implied by the working arrangements. There are two types ofcontract:

• a contract of service• a contract for service.

Neither contract has a precise legal definition. Inland Revenue rely on 'tests' which haveemerged from case law and apply these to the facts of individual cases. Unfortunately, the testsare not exhaustive and therefore do not apply to all possible situations.

These tests aim to establish whether or not a 'master/servant' relationship exists. Control is seenas significant in the determination of status.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 14 RESO3529 – Issue 3 : April 2003

It is not sufficient for a person to call themselves self-employed, even if that self-employedstatus is recognised by his or her tax office.

An individual can be employed and self-employed at the same time in different jobs. Each and every contract that an individual undertakes must, therefore, be considered on its ownmerits by reference to the conditions and requirements of that particular engagement.

PAYE considerations do not generally apply to genuine limited companies which are engagedby the school.

However, because unincorporated traders sometimes use the phrase “company” in a colloquialfashion, it is important to exercise care in making gross payments in such an engagement.

• Check that the purported company truly exists.

• Enter into a contract only with the company and not with its shareholders or directors intheir personal capacity.

• Make payments on the production of an invoice only to the company.

Tests: Individuals

a. People with a contract of employment (commonly called a contract of service) aredeemed, for purposes of income tax and national insurance, to be employees. As statedabove, a contract of service need not be in writing: it can be oral or expressed or impliedby the working arrangements.

If the answer 'yes' arises from a majority of the following questions, the individualengaged is likely to be an employee and therefore, employed.

• Does the person provide education, in the role of a teacher, lecturer or instructor?

• Does the individual undertake the work, rather than hire someone else?

• Is the individual supervised (in other words instructed what to do or when andhow to do it)?

• Is the individual paid a rate by the hour, the day, etc.?

• Does the individual work set hours determined by the school?

• Does the individual work at a place or places decided by the school?

• Does the school supply the equipment needed to perform the work?

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 15 RESO3529 – Issue 3 : April 2003

In these circumstances, the payment must be processed through the payroll system toensure proper deductions are made for income tax, national insurance and, whereapplicable, superannuation.

b. On the other hand, people who supply services as independent contractors (under whatis sometimes called a contract for service) are regarded as self-employed.

If the answer 'yes' arises from a majority of the following questions, the individualengaged is likely to be self-employed.

• Is the individual not subject to the control, or to the right of control, of theschool as to what he or she does, and when and how he or she does it?

• May the individual work elsewhere than on the school's premises or at a place orplaces decided by the school?

• Is the work not person-specific? In other words, must the work be done by aperson the school can specify; or may the person involved send a substitute orinvite other people to do the work that he or she has agreed to undertake?

• Is the individual taken on to perform a service which could not be described as'part and parcel' of the employer’s business or organisation'?

• Is a fee paid for the job (rather than a rate per hour, day or week, etc.)?

• Does the individual provide the main items of equipment needed to perform thejob, not just small tools that many employees provide for themselves?

• Does the individual have to correct unsatisfactory work at no cost to the school?

• Could the individual make a loss on the contract?

• Is the individual's business registered for VAT?

Examples:

As a guide only, the following rulings are provided.

Employed

Peripatetic music teacherPiano accompanistTutor or lecturerSwimming instructor

Self-employed

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 16 RESO3529 – Issue 3 : April 2003

Craftsmen (competent)

It is a question of applying the tests to the facts of a particular case and arriving at a balance ofprobabilities from the evidence. In some cases, satisfying or alternatively failing just one of thetests will be overwhelming in establishing the position. In other cases, an even number of testswill be in conflict and the decision will be finely balanced.

If in doubt, follow the questionnaire procedure in the next section.

Dispute as to whether Employed or Self-employed

Where there is doubt, the school – until advised otherwise by the Authority's tax office – musttreat the individual's engagement as an employment and therefore process any paymentsthrough the payroll system.

Also, to establish schedule of charge for taxation, the school must request the individual tocomplete the questionnaire reproduced at the end of this Appendix.

For its part, the Authority assents to the use of the questionnaire procedure by the InlandRevenue as providing, in difficult circumstances, its best protection against unexpected PAYEarrears. Persons completing the questionnaire should note that the answers given are theirresponsibility, as is the taking of necessary advice in relation to both the questions asked andany consequent discussions with the Inland Revenue.

The completed questionnaire quoting reference 9517/H1/WW must be forwarded to:

H.M. Inspector of TaxesInland RevenueChapel Wharf AreaTrinity Bridge House2 Dearman’s PlaceSalford M3 5BS

2. What to do next?

Employer

Where an employer/employee relationship applies, all payments to the individual concernedmust be made through the payroll system.

Payroll appointment processes should be followed and claims submitted for payment throughstandard authorisation procedures.

The actions required can be summarised as follows.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 17 RESO3529 – Issue 3 : April 2003

Appointment Form/P45 or P46

The purpose of the appointment form is to create a payroll record. The school must complete anappointment form and obtain from the individual their Inland Revenue P45 form (issued bytheir previous employer). If there is no P45 the individual must complete Inland Revenue P46form (PAYE: Employer's notice to tax office) to ascertain the individual's tax code status.

Either the P45 or the P46 must be attached to the appointment form and sent to CSF HumanResources at County Hall, Hertford.

Treatment of Income Tax

Tax will be determined by reference to the P45.

If a P46 is completed, an emergency tax code will initially be used. However, if the individualis unable to sign statements 'A' or 'B', because they have other paid employment or pension,then basic rate tax will be deducted.

The P46 will then be forwarded to the Authority's Inspector of Taxes office, for determinationof tax status.

Treatment of National Insurance

In the main, deductions depend upon the level of earning. No deductions are made if earningsare below a threshold, which is reviewed annually by the Department of Social Security. Thefull rate is applied above the threshold.

Alternatively:

a. a reduced rate is applied if a validly held 'married women's reduced rate certificate' isproduced by the individual; or

b. no national insurance liability arises for individuals over state retirement age, subject tothe employer's receipt of a 'non-liability NI' certificate.

Method of payment

The standard method of payment is a cheque, sent to the home address of the individual.

Alternatively, monies can be paid direct into the individual's bank account (electronic fundtransfer), if details are provided.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 18 RESO3529 – Issue 3 : April 2003

Employment contract and pay documents

Category of employee Appointment form Periodic pay formPeripatetic music teacherPiano accompanistTutor or lecturerSwimming instructor

PAY 1 A/ED PAY 1 A/ED PAY 1 A/ED PAY 1 A/ED

FIN 19aFIN 9PAY 8PAY 8

Self-employed

Payment for work where the matter is clear cut, for example a building or electrical contractor.

Payments to contractors and subcontractors who undertake repair and maintenance, where theinvoice contains a labour element, are subject to the Construction Industry Scheme (CIS)regulations. For guidance, please refer to Part IV, Section 14 of this Handbook.

3. Other considerations

Out-of-school activity

Where the school is facilitating an out-of-school activity, and payments to the individualconducting the activity are effectively made by the parents, the school would not be theemployer, provided that the monies are not represented as having been due from and a liabilityof the school.

An out-of-school activity is 'exempt', therefore, only if:

a. it takes place out of school hours

b. the school is not involved in collecting monies and paying these over to the provider ofthe activity or is clearly not directing that activity.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 19 RESO3529 – Issue 3 : April 2003

QUESTIONNAIRE TO ESTABLISH SCHEDULE OF CHARGE FOR TAXATIONPURPOSES (EMPLOYER’S PAYE REF: 951/H1/WW)

Dear Sir or Madam

If you consider that your recent engagement with the School is a self-employment, as opposedto an employee appointment, please complete the following information questions to enable thisaspect to be fully considered.

I would stress that, if you have a contract of employment either written or verbal with youremployer, any income (salary, expenses and benefits in kind) from such a contract willconstitute emoluments that will fall within the Schedule E charge (Inland Revenue'srequirements for employed individuals). As such, they will be correctly subject to PAYE (PayAs You Earn). If no such contract exists and there are other arrangements, details of which willbe revealed by the following questions, your employer is required, as an interim measure, tooperate PAYE against those emoluments pending further advice from this office.

1. Full name

2. Home address

3. Tax District and reference to which your returns are sent. (HCC's reference is951/H1/WW)

4. National Insurance number

5. What arrangements have you made or do you intend making with regard to payment ofNI contributions? If you have consulted the Inland Revenue (NI Contributions) Officealready with regard to the type of contributions relevant to this engagement, what wastheir response and could I see copies of any correspondence?

6. Location of this engagement.

7. Date of commencement and length of the engagement.

8. Have you previously worked for Hertfordshire County Council Education Authority, ifso, how do your present terms of engagement differ at all?

9. What exactly is the nature of the work you have undertaken?

10. How did you obtain the job? Was it advertised? If so, did you attend an interview orwhat were the other circumstances of your engagement?

11. Is there a written contract or correspondence concerning your engagement; if so, may I see copies?

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 20 RESO3529 – Issue 3 : April 2003

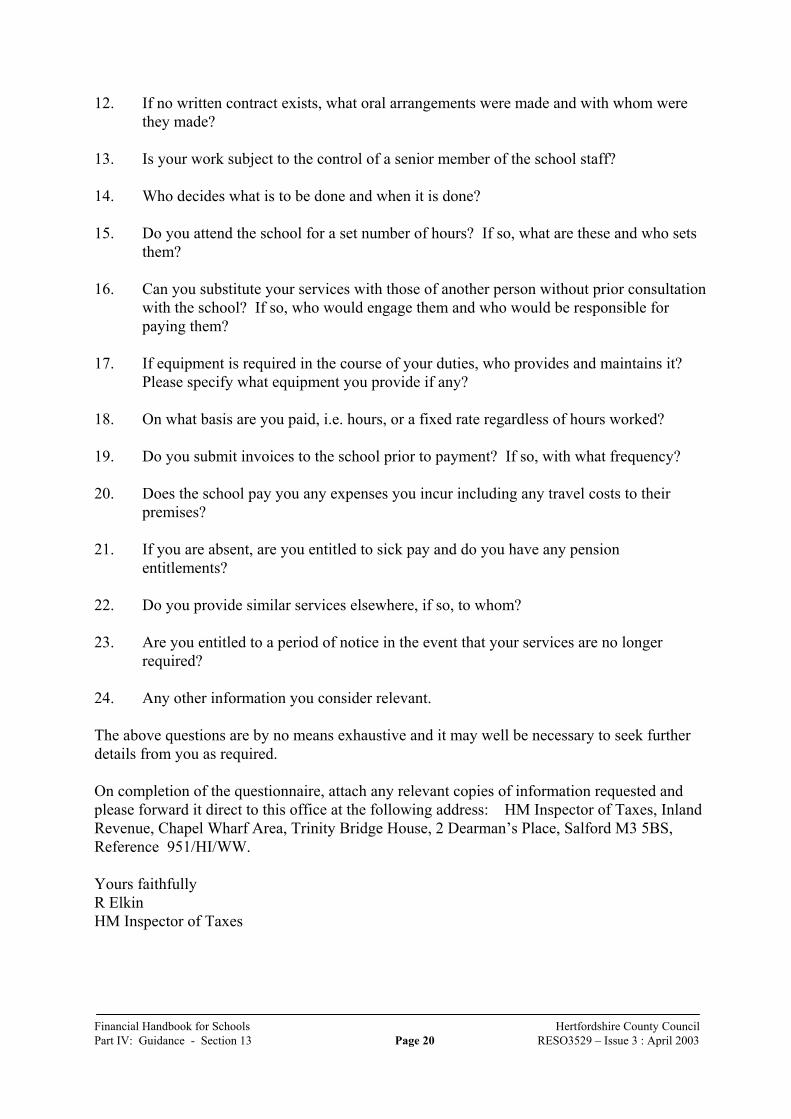

12. If no written contract exists, what oral arrangements were made and with whom were they made?

13. Is your work subject to the control of a senior member of the school staff?

14. Who decides what is to be done and when it is done?

15. Do you attend the school for a set number of hours? If so, what are these and who sets them?

16. Can you substitute your services with those of another person without prior consultationwith the school? If so, who would engage them and who would be responsible forpaying them?

17. If equipment is required in the course of your duties, who provides and maintains it?Please specify what equipment you provide if any?

18. On what basis are you paid, i.e. hours, or a fixed rate regardless of hours worked?

19. Do you submit invoices to the school prior to payment? If so, with what frequency?

20. Does the school pay you any expenses you incur including any travel costs to theirpremises?

21. If you are absent, are you entitled to sick pay and do you have any pension entitlements?

22. Do you provide similar services elsewhere, if so, to whom?

23. Are you entitled to a period of notice in the event that your services are no longer required?

24. Any other information you consider relevant.

The above questions are by no means exhaustive and it may well be necessary to seek furtherdetails from you as required.

On completion of the questionnaire, attach any relevant copies of information requested andplease forward it direct to this office at the following address: HM Inspector of Taxes, InlandRevenue, Chapel Wharf Area, Trinity Bridge House, 2 Dearman’s Place, Salford M3 5BS,Reference 951/HI/WW.

Yours faithfullyR ElkinHM Inspector of Taxes

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 21 RESO3529 – Issue 3 : April 2003

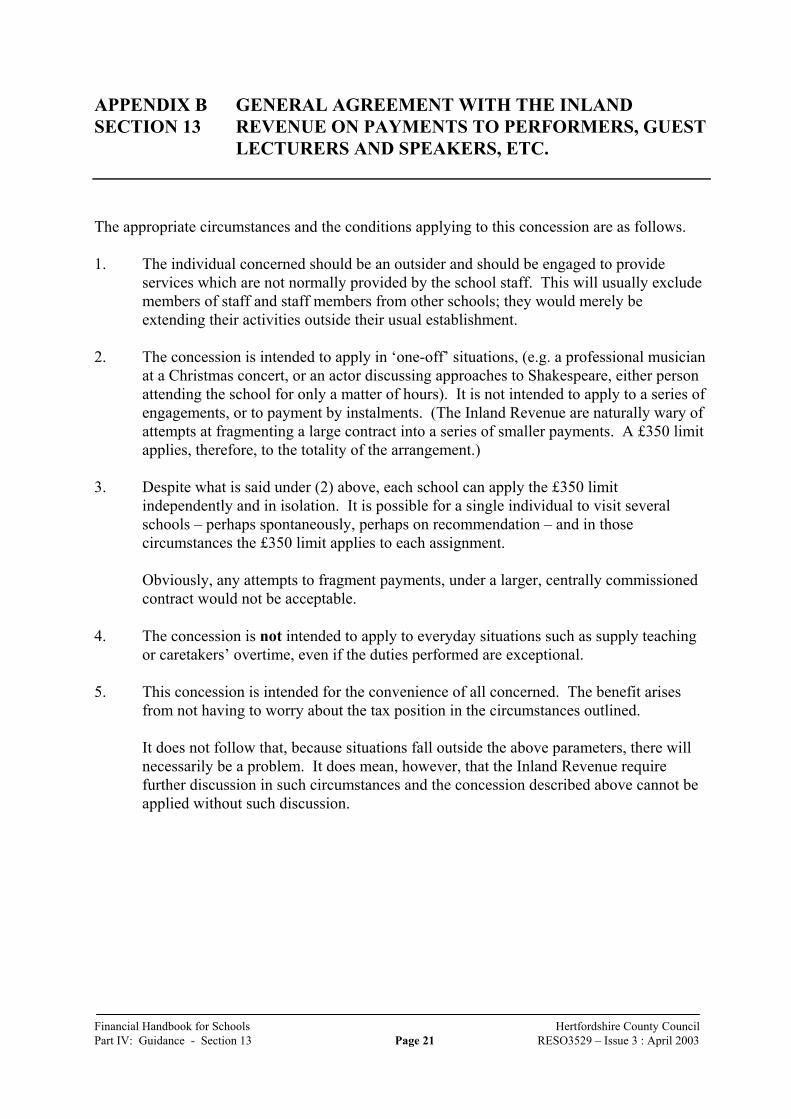

APPENDIX B GENERAL AGREEMENT WITH THE INLAND SECTION 13 REVENUE ON PAYMENTS TO PERFORMERS, GUEST

LECTURERS AND SPEAKERS, ETC.

The appropriate circumstances and the conditions applying to this concession are as follows.

1. The individual concerned should be an outsider and should be engaged to provideservices which are not normally provided by the school staff. This will usually excludemembers of staff and staff members from other schools; they would merely beextending their activities outside their usual establishment.

2. The concession is intended to apply in ‘one-off’ situations, (e.g. a professional musicianat a Christmas concert, or an actor discussing approaches to Shakespeare, either personattending the school for only a matter of hours). It is not intended to apply to a series ofengagements, or to payment by instalments. (The Inland Revenue are naturally wary ofattempts at fragmenting a large contract into a series of smaller payments. A £350 limitapplies, therefore, to the totality of the arrangement.)

3. Despite what is said under (2) above, each school can apply the £350 limitindependently and in isolation. It is possible for a single individual to visit severalschools – perhaps spontaneously, perhaps on recommendation – and in thosecircumstances the £350 limit applies to each assignment.

Obviously, any attempts to fragment payments, under a larger, centrally commissionedcontract would not be acceptable.

4. The concession is not intended to apply to everyday situations such as supply teachingor caretakers’ overtime, even if the duties performed are exceptional.

5. This concession is intended for the convenience of all concerned. The benefit arisesfrom not having to worry about the tax position in the circumstances outlined.

It does not follow that, because situations fall outside the above parameters, there willnecessarily be a problem. It does mean, however, that the Inland Revenue requirefurther discussion in such circumstances and the concession described above cannot beapplied without such discussion.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 22 RESO3529 – Issue 3 : April 2003

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 23 RESO3529 – Issue 3 : April 2003

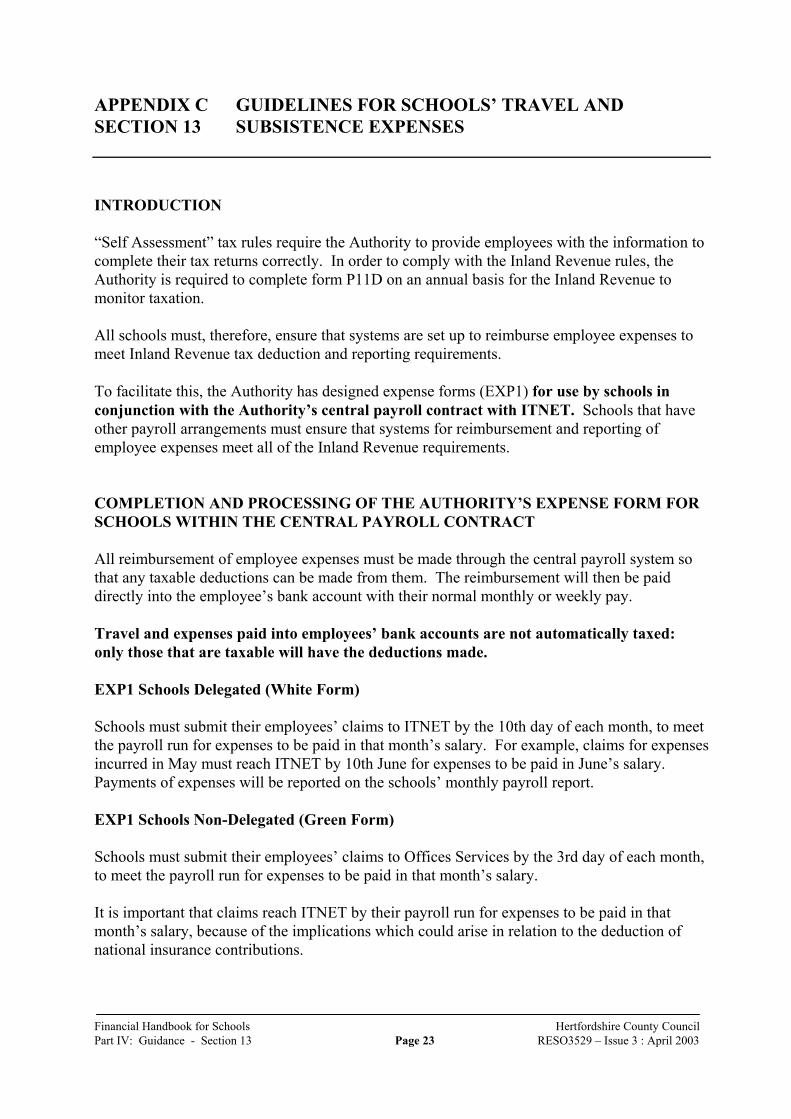

APPENDIX C GUIDELINES FOR SCHOOLS’ TRAVEL ANDSECTION 13 SUBSISTENCE EXPENSES

INTRODUCTION

“Self Assessment” tax rules require the Authority to provide employees with the information tocomplete their tax returns correctly. In order to comply with the Inland Revenue rules, theAuthority is required to complete form P11D on an annual basis for the Inland Revenue tomonitor taxation.

All schools must, therefore, ensure that systems are set up to reimburse employee expenses tomeet Inland Revenue tax deduction and reporting requirements.

To facilitate this, the Authority has designed expense forms (EXP1) for use by schools inconjunction with the Authority’s central payroll contract with ITNET. Schools that haveother payroll arrangements must ensure that systems for reimbursement and reporting ofemployee expenses meet all of the Inland Revenue requirements.

COMPLETION AND PROCESSING OF THE AUTHORITY’S EXPENSE FORM FORSCHOOLS WITHIN THE CENTRAL PAYROLL CONTRACT

All reimbursement of employee expenses must be made through the central payroll system sothat any taxable deductions can be made from them. The reimbursement will then be paiddirectly into the employee’s bank account with their normal monthly or weekly pay.

Travel and expenses paid into employees’ bank accounts are not automatically taxed:only those that are taxable will have the deductions made.

EXP1 Schools Delegated (White Form)

Schools must submit their employees’ claims to ITNET by the 10th day of each month, to meetthe payroll run for expenses to be paid in that month’s salary. For example, claims for expensesincurred in May must reach ITNET by 10th June for expenses to be paid in June’s salary.Payments of expenses will be reported on the schools’ monthly payroll report.

EXP1 Schools Non-Delegated (Green Form)

Schools must submit their employees’ claims to Offices Services by the 3rd day of each month,to meet the payroll run for expenses to be paid in that month’s salary.

It is important that claims reach ITNET by their payroll run for expenses to be paid in thatmonth’s salary, because of the implications which could arise in relation to the deduction ofnational insurance contributions.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 24 RESO3529 – Issue 3 : April 2003

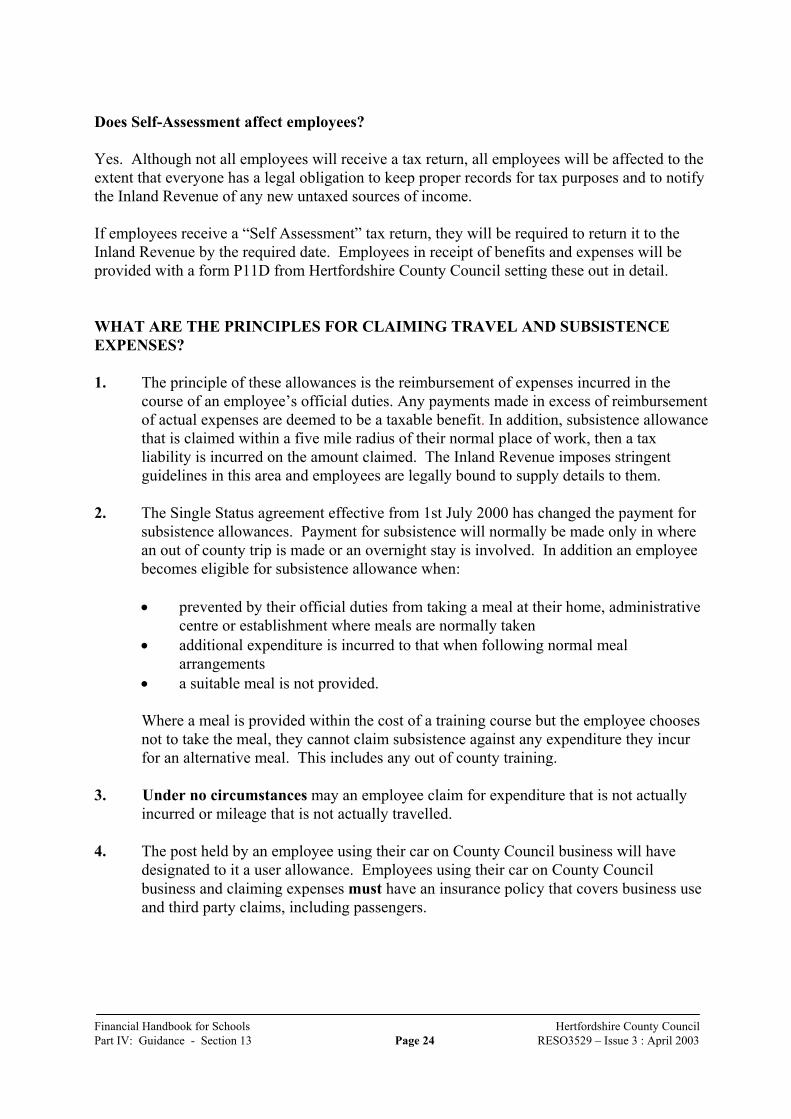

Does Self-Assessment affect employees? Yes. Although not all employees will receive a tax return, all employees will be affected to theextent that everyone has a legal obligation to keep proper records for tax purposes and to notifythe Inland Revenue of any new untaxed sources of income. If employees receive a “Self Assessment” tax return, they will be required to return it to theInland Revenue by the required date. Employees in receipt of benefits and expenses will beprovided with a form P11D from Hertfordshire County Council setting these out in detail. WHAT ARE THE PRINCIPLES FOR CLAIMING TRAVEL AND SUBSISTENCEEXPENSES? 1. The principle of these allowances is the reimbursement of expenses incurred in the

course of an employee’s official duties. Any payments made in excess of reimbursementof actual expenses are deemed to be a taxable benefit. In addition, subsistence allowancethat is claimed within a five mile radius of their normal place of work, then a taxliability is incurred on the amount claimed. The Inland Revenue imposes stringentguidelines in this area and employees are legally bound to supply details to them.

2. The Single Status agreement effective from 1st July 2000 has changed the payment for

subsistence allowances. Payment for subsistence will normally be made only in wherean out of county trip is made or an overnight stay is involved. In addition an employeebecomes eligible for subsistence allowance when:

• prevented by their official duties from taking a meal at their home, administrativecentre or establishment where meals are normally taken

• additional expenditure is incurred to that when following normal mealarrangements

• a suitable meal is not provided.

Where a meal is provided within the cost of a training course but the employee choosesnot to take the meal, they cannot claim subsistence against any expenditure they incurfor an alternative meal. This includes any out of county training.

3. Under no circumstances may an employee claim for expenditure that is not actuallyincurred or mileage that is not actually travelled.

4. The post held by an employee using their car on County Council business will have

designated to it a user allowance. Employees using their car on County Councilbusiness and claiming expenses must have an insurance policy that covers business useand third party claims, including passengers.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 25 RESO3529 – Issue 3 : April 2003

5. Wherever possible employees should travel by train or bus at 2nd class passenger rate orcar share when making the same journey. Staff may choose to travel by first classpublic transport but they will only be reimbursed the cost of 2nd class travel.

CAR MILEAGE PAYMENTS AND TAX Business journeys are defined as those journeys made by the employee, during the course oftheir official duties, to somewhere other than their permanent place of work. Home to work journeys are defined as those which start from home and finish at the employee’spermanent work place and/or start from the permanent work place and finish at home. It isHertfordshire County Council’s policy not to pay costs incurred by employees for their home towork travel. Where an employee makes a business journey from home to somewhere other than theirpermanent work place, or vice versa, Hertfordshire County Council requires the employee todeduct their normal home to permanent work place expenses, thus only claiming the additionalexpenses incurred. • Note the exception to this is where an employee makes a second journey of the day to

their permanent place of work e.g. evening meetings or a journey on a day that they donot normally work. In this instance the employee can claim the mileage from home totheir permanent place of work. However, the Inland Revenue will treat any payment forany second trip from home to permanent place of work as taxable and any paymentmade in relation to such journeys will be taxed.

And/or • Where an employee is required to make a second journey or a journey on a day that they

do not normally work and it is to somewhere other than their permanent place ofwork. This journey from home to work can be claimed without offset of normalcommuting and is not taxable.

And/or • Single status has changed the payments in relation to excess travel and travel time

allowance for an employee who has been re-deployed as follows:

The previous two schemes have been replaced with a single payment (which will bemade in two instalments over two consecutive tax years if the employee requests, toavoid pushing annual earnings over a tax threshold). The value of the payment dependson the difference between existing home to work return journey and the new journey.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 26 RESO3529 – Issue 3 : April 2003

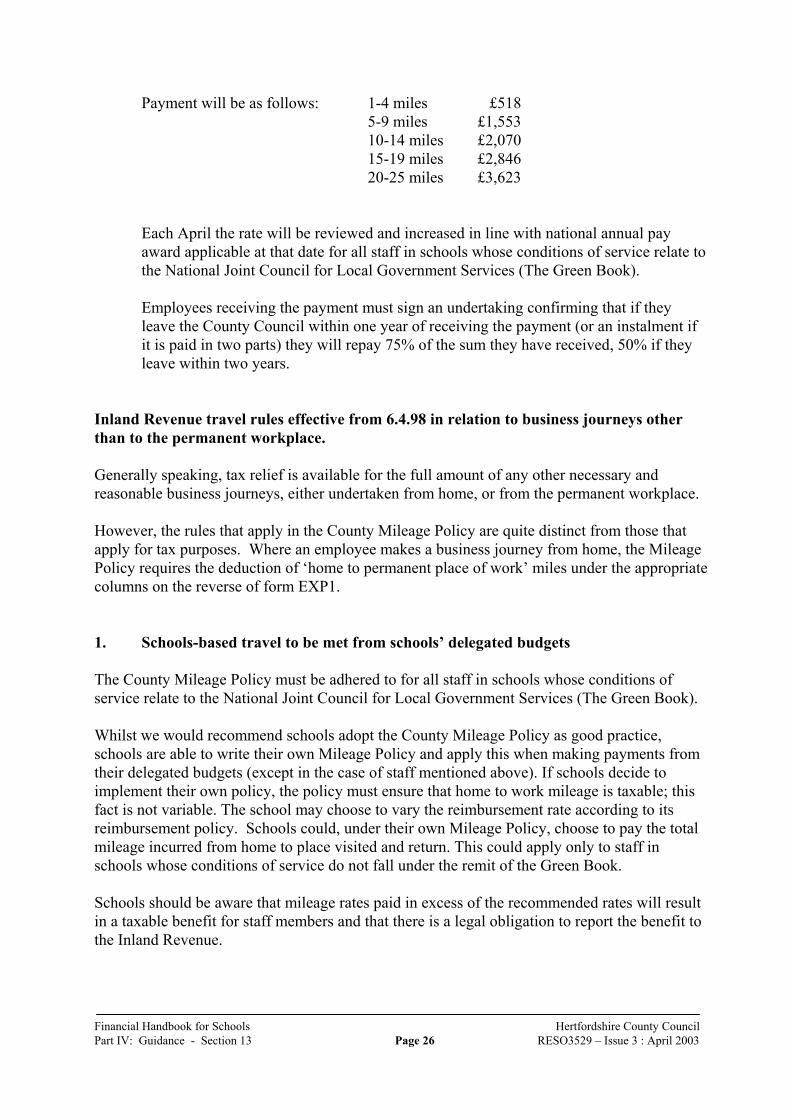

Payment will be as follows: 1-4 miles £5185-9 miles £1,55310-14 miles £2,07015-19 miles £2,84620-25 miles £3,623

Each April the rate will be reviewed and increased in line with national annual payaward applicable at that date for all staff in schools whose conditions of service relate tothe National Joint Council for Local Government Services (The Green Book).

Employees receiving the payment must sign an undertaking confirming that if theyleave the County Council within one year of receiving the payment (or an instalment ifit is paid in two parts) they will repay 75% of the sum they have received, 50% if theyleave within two years.

Inland Revenue travel rules effective from 6.4.98 in relation to business journeys otherthan to the permanent workplace.

Generally speaking, tax relief is available for the full amount of any other necessary andreasonable business journeys, either undertaken from home, or from the permanent workplace.

However, the rules that apply in the County Mileage Policy are quite distinct from those thatapply for tax purposes. Where an employee makes a business journey from home, the MileagePolicy requires the deduction of ‘home to permanent place of work’ miles under the appropriatecolumns on the reverse of form EXP1.

1. Schools-based travel to be met from schools’ delegated budgets

The County Mileage Policy must be adhered to for all staff in schools whose conditions ofservice relate to the National Joint Council for Local Government Services (The Green Book).

Whilst we would recommend schools adopt the County Mileage Policy as good practice,schools are able to write their own Mileage Policy and apply this when making payments fromtheir delegated budgets (except in the case of staff mentioned above). If schools decide toimplement their own policy, the policy must ensure that home to work mileage is taxable; thisfact is not variable. The school may choose to vary the reimbursement rate according to itsreimbursement policy. Schools could, under their own Mileage Policy, choose to pay the totalmileage incurred from home to place visited and return. This could apply only to staff inschools whose conditions of service do not fall under the remit of the Green Book.

Schools should be aware that mileage rates paid in excess of the recommended rates will resultin a taxable benefit for staff members and that there is a legal obligation to report the benefit tothe Inland Revenue.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 27 RESO3529 – Issue 3 : April 2003

2. Travel expenses to be met from non-delegated budgets

The County Council Mileage Policy will be followed for all claims made for travel andsubsistence met from this budget.

It will therefore be a requirement that home to permanent place of work miles are deductedunder the appropriate columns of the EXP1 Schools Non-Delegated (Green Form).

3. Record keeping

It is important for all employees to keep a careful record of their overall business mileage andnot merely that element of the mileage which the school and/or Hertfordshire County Council isprepared to reimburse.

Such records will facilitate any claims that they make to the Inland Revenue for additionalrelief, which they may be entitled to where the Inland Revenue provisions differ from that ofthe employer.

TRAVELLING ARRANGEMENTS FOR OUT OF COUNTY TRIPS

It is not possible to prescribe what these will be since they will vary on each occasiondepending on the reason for the journey.

It is the County Council’s policy to encourage the use of public transport. Journeys to Londonshould usually be by train. Remember to use railcards, particularly Network card, wheneveryou can. Employees should agree the best travel option for the journey with their manager priorto making the journey.

Wherever possible employees should arrange to travel together when going by car. The driveris able to claim the current passenger rate per mile per passenger carried only if the journey ispaid at the public transport rate.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 28 RESO3529 – Issue 3 : April 2003

COMPLETING FORM EXP1 SCHOOLS DELEGATED (WHITE) AND EXP1SCHOOLS NON-DELEGATED (GREEN)

EXP1 Schools Delegated (White)

Employees must use this form where the expenses incurred are to be paid from the school’sbudget. E.g. all day-to-day school based travelling expenditure would be met from the schoolbudget. Annex A to this Appendix provides details of travelling expenditure to be met from theschools’ budget.

EXP1 Schools Non-delegated (Green)

Employees must use this form where the expenses are not paid from the school’s budget, butfrom the non-delegated budget held centrally and managed by the Office Services Manager atCounty Hall. Annex A to this Appendix provides details of travelling expenditure to be metfrom non-delegated centrally held budgets.

Mileage employees can claim

• Journeys which start and finish at the school. Claim all miles. • Journeys made on the way to or from the school. Total all the miles travelled and

deduct your normal home to school miles. Claim any excess on business miles.

Example: Base Letchworth Home HitchinJourney made From home (Hitchin) to Stevenage = 8 miles

Then from Stevenage to base (Letchworth) = 11 milesTotal = 19 miles minus Hitchin to Letchworth 3 miles

Claim 16 business miles

• Out of the school all day. Total all your miles travelled and deduct your normal home toschool and return miles. Claim any excess business miles.

Example: Base HertfordHome WareJourney made From Ware to Bishops Stortford = 15 miles, Bishops Stortford

To Stevenage = 23 miles, Stevenage to Hoddesdon = 15 miles,Hoddesdon to Ware = 6 milesTotal = 59 miles minus Ware to Hertford and return 8 miles

Claim 51 business miles • Evening and weekend meetings. Claim from home to place/s visited. NB Remember

the journey will be taxable if to the permanent workplace, not otherwise.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 29 RESO3529 – Issue 3 : April 2003

• Attending training courses, seminars, conferences. Deduct your normal home to schooltravel. Claim the balance. Training miles paid at the public transport rate.

• Disturbance mileage. (Applicable to staff who have been redeployed and are claiming

excess miles). Claim according to prior written agreement. Claim forms must be completed in full and correctly approved and authorised. Failure to do sowill result in ITNET returning the claim form to the school for amendment. Mandatory items to be completed as follows: • Full name• Home address and postcode• School• Job title• Payroll reference number Staff will find this on their pay slip• National Insurance Number Staff will find this on their pay slip• Category of user Casual/Essential/Lease car/non-designated.• Car make and model• Actual CC Precise details are needed for tax calculations• Vehicle registration• Vehicle Insurance HCC requires that staff using their vehicles for

official business journeys must be covered forbusiness use on their insurance. There is an elementof the mileage rate paid that contributes towards this.Staff are required by law to carry valid insurancefor all journeys.

• All unused lines on reverse side of form must be crossed through to ensure that no otherentries can be added.

Expenditure code(s) For Schools’ delegated travel the following accountcodes are the only ones under which paymentsshould be made.

2409 Travel and subsistence 241 Travel and subsistence – Training 3401 Subsistence3405 Governor travel and subsistence343 Other Indirect Employee Costs

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 30 RESO3529 – Issue 3 : April 2003

The cost centre is the seven-character reference asfollows:

E010xxx Nursery E050xxx Education Support Centres E070xxx Special E320xxx Primary E330xxx Middle/Secondary

Note: “xxx” represents the school number andshould be replaced with your school number (e.g.030, 299, 591, 634, 910 etc.

For non-delegated travel EXP1 (Green) please leaveexpenditure codes blank to be completed by OfficeServices.

• Authorised for payment For EXP1 Schools Non-delegated (Green) this should be left blank for completion by OfficeServices.

For EXP1 Schools Delegated (White) for all staff(excluding Headteacher claims), this should beauthorised by the Headteacher or other authorisedsignatory with delegated powers. For theHeadteacher’s claim, the form should be approvedby a member of the Governing Body. Please refer toPart IV, Section 10 of this Handbook for furtherguidance about approving the payment ofHeadteachers’ expenses. The claim form shouldthen be authorised for payment by an authorisedsignatory with delegated powers.

• Approved signature For EXP1 Schools Non-delegated (Green) this

must be left blank for approval by Office Services.

For EXP1 Schools Delegated (White) by designatedofficer within the school. Signature of claimant mustbe completed in both sections of the form.

• Signature of claimant Must be completed in both sections of the form. Sections to be completed as a matter of good practice • Claim period This will help identification for school’s budget

monitoring.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 31 RESO3529 – Issue 3 : April 2003

• Column A - Date of journey For audit purposes this date must tally with the employee’s diary.

Columns that must be completed in order to process for payment through ITNET • Column B - Started from Important to enable correct payment of miles to be

made and determine taxable and non-taxablemileage.

• Column C - Places visited Need to be clear about where employee went and

the reasons why to enable correct mileage rate to bepaid. This information should also be recorded in theemployee’s diary for audit purposes.

• Column D - Finished at As column B

• Column E - Total miles This must be the total miles travelled.

• Column F - Home to school In this column enter the miles you must deduct forhome to school travel.

• Column G - Miles claimed These will be the balance of column E minuscolumn F.

• Column H - Training miles Enter any miles travelled and being claimed for in relation to training, attendance at conferences,seminars. This will be column E less column F

• Column I - Public transport miles All non-designated travel and out of county miles are paid at single mileage rate and must be entered inthis column. These will be the balance of column Eminus column F. In some instances it may also beminus column H.

• Column J - Number of passengers Passenger miles are only paid when public transportrates are being paid for the journey.

• Column K – Disturbance and This column must be used to claim any home to home to work miles work miles for additionaljourneys outside normal working hours, topermanent work place, or approved disturbancemiles. Remember these are taxable.

• Column L - Fares and car parking Can be claimed in full and receipts must be attached.

• Column M - Subsistence Enter subsistence amount claimed. Remember to

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 32 RESO3529 – Issue 3 : April 2003

enter the reason for the claim in column C. Receiptsfor all expenses must be attached.

• Column N - Other and cycle miles All claims for items not covered in column G to column M should be shown here.

• Telephone calls Staff must ensure when claiming that they submit aVAT recoverable invoice for business calls madefrom home.

• Totals of columns Any miles in columns F to K on each line completedmust add up to the number of miles at column E.Ensure that each column is totalled at the bottom ofthe column. Total mileage to date (1) will beprevious mileage figure (from 1 April in the currentyear) + column G figure. Total mileage to date (2)will be previous disturbance mileage (from 1 Aprilin the current year) + column K miles. The final boxwill be the total of 1 and 2 and this is the figure to beentered on the next claim in the “previous miles from1 April” section.

• Normal place of work box Number of miles from home to permanent work base(bottom right corner of claim) must be entered hereto ensure correct calculations on deductions of hometo permanent work base miles.

• Excess travel time allowance To be completed as appropriate in individually approved cases. (Usually in accordance withredeployment policy.)

The information from the reverse of the form is transferred to the corresponding rows on thefront of the form. Current mileage rates inserted and calculations made to complete grosscolumn, VAT element, VAT amount and net amount. Please make sure that the information istransferred accurately to the front of the form. EXAMPLE • Row 1 miles claimed would be the figure in column G.• Enter the appropriate mileage rate.• Multiply the mileage rate by the number of miles in the mileage column to give you the

gross figure.• Enter the VAT element on the mileage rate in the appropriate column.• Multiply the VAT element by the number of miles, divide the answer by 100, this will

give the VAT amount to be entered in the column. This figure is then subtracted fromthe gross figure to give the net figure.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 33 RESO3529 – Issue 3 : April 2003

• The figures must then be entered onto the tear off portion, in the corresponding rows,with a cost code and account code next to every entry for EXP1 Schools Delegated(White). For EXP1 Schools Non-delegated (Green) the cost centre and account is to beleft blank to be completed by Office Services.

• In some instances it may be necessary to split the cost over more than one account. Thiscan be done, but the information must be fitted into the box.

• Ensure all columns are totalled.• The claim should now be fully completed and can be sent to ITNET for payment.

WHAT HELP IS AVAILABLE?

• Please contact Amy King, ITNET Payroll on 01992 555432 if you have paymentqueries about EXP1 Schools Delegated – the white form.

• Please contact Amy King, ITNET Payroll on 01992 555432 if you have any queries

about EXP1 Schools Non-delegated – the green form. • VAT queries should be directed to Gary Elmes on 01992 555311 or Alex Fitzpatrick on

01992 555365. • Income Tax queries should be directed to Edward Deville on 01992 555381.

GOOD FINANCIAL PRACTICE

Schools are advised to do the following:

Retain copies of information claimed on EXP1 Schools Delegated (white) and EXP1 SchoolsNon-delegated (green) claim forms for a period of six audited years plus the current year.

Ensure that anyone using their car to make journeys for official school business has their carinsured for business use.

Claims from non-employees, e.g. external candidates’ interview expenses may be paid locallyin school using the form A50 or T1. The form should then be retained in schools for six years.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 34 RESO3529 – Issue 3 : April 2003

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 35 RESO3529 – Issue 3 : April 2003

ANNEX A REIMBURSEMENT OF TRAVEL EXPENSES

The following chart sets out recommended reimbursement mileage rates for school basedtravel that is met from the schools’ delegated budget.

Activity/journey Rate Applicable

School trips or journeys, (including planning and preparationvisits)

Single Status Rate

School sporting events, (whether held at the school or at othervenues, e.g. inter-school events)

Single Status Rate

Any journey connected with out-of-school activities, (such asvisits to swimming pools, music centres, teachers centres)

Single Status Rate

Transport of ancillary or relief staff Single Status Rate

Any visits to other education establishments within theCounty (e.g. Primary/Secondary liaison, school/collegeliaison)

Single Status Rate

Official visits to pupils’ homes Single Status Rate

Carrying sick/injured pupils home, to doctor or to hospital Single Status Rate

Journeys connected with pupil work experience (includingpreparation and follow up visits, travel to venues offeringformal, simulated work experience)

Single Status Rate

Collection of equipment from, for example, Hertsmedia Single Status Rate

All training events Public Transport

Interview expenses for teachers attending interview at yourschool (this includes travel and subsistence claims)

Public Transport

Attendance at case conferences for pupils attending yourschool

Single Status Rate

Visits to other schools where pupils are placed temporarily(e.g. special schools or units)

Single Status Rate

Visits to school annexes for teaching purposes (split-sitetravel)

Single Status Rate

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 36 RESO3529 – Issue 3 : April 2003

Visits to other schools for joint planning and teachingactivities

Single Status Rate

The banking of money on behalf of the school or Authority Single Status Rate

Journeys from home to work for ‘directed’ activities outsidenormal school hours, connected with attendance at staffmeetings, parent consultation meetings, PTA Committeemeetings and Governing Body meetings. Travel from home towork and work to home is subject to the deduction of incometax and payment is made through payroll.

Public Transport

Travel expenses to be met from non-delegated budgets

Journeys and expenses connected with the following activities will be met from non-delegatedbudgets.

Travel for ‘official’ County business

Reimbursement of the cost of travel for ‘official’ County business listed below to eventsorganised by or on behalf of the authority. Where journeys do not fall into one of the categoriesbelow the school must meet the costs.

Activity/Journey Rate Applicable

Official attendance at events on behalf of the Authority, (e.g.funerals or special events at the invitation of local industry orother agencies.

Single Status Rate

Extraordinary meetings of education-related organisations atdistrict, divisional, County or national level. These must be ofclear benefit to the Authority (e.g. Hertfordshire Teachers’organisations, Herts Sports Association Committee or othersporting activities not at school level). This does not includeTrade Unions or Associations, or routine divisional meetingsof heads not arranged by the Authority.

Single Status Rate

Meetings or exhibitions arranged by or at the request of theAuthority.

Single Status Rate

Travel to official, LEA sponsored in-service training activitieswhere participation is as a tutor or direct contributor. Thisdoes not include as a recipient of training.

Single Status Rate

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 37 RESO3529 – Issue 3 : April 2003

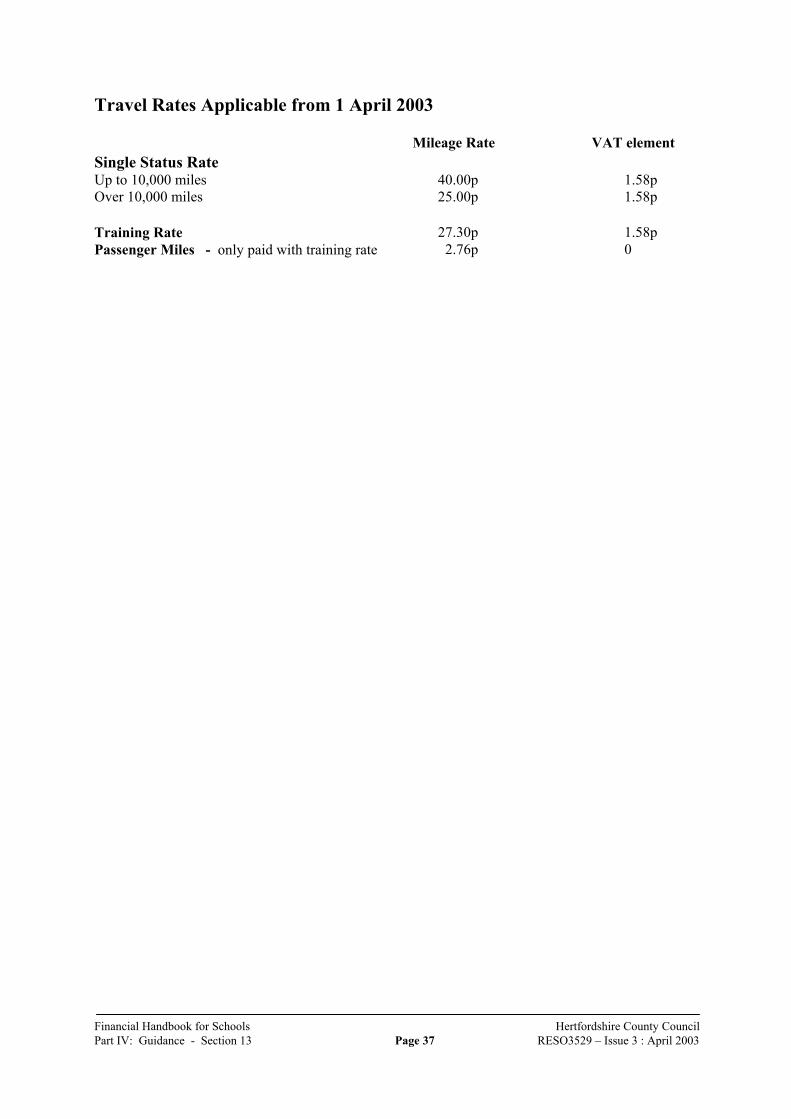

Travel Rates Applicable from 1 April 2003

Mileage Rate VAT elementSingle Status RateUp to 10,000 miles 40.00p 1.58pOver 10,000 miles 25.00p 1.58p

Training Rate 27.30p 1.58pPassenger Miles - only paid with training rate 2.76p 0

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 38 RESO3529 – Issue 3 : April 2003

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 39 RESO3529 – Issue 3 : April 2003

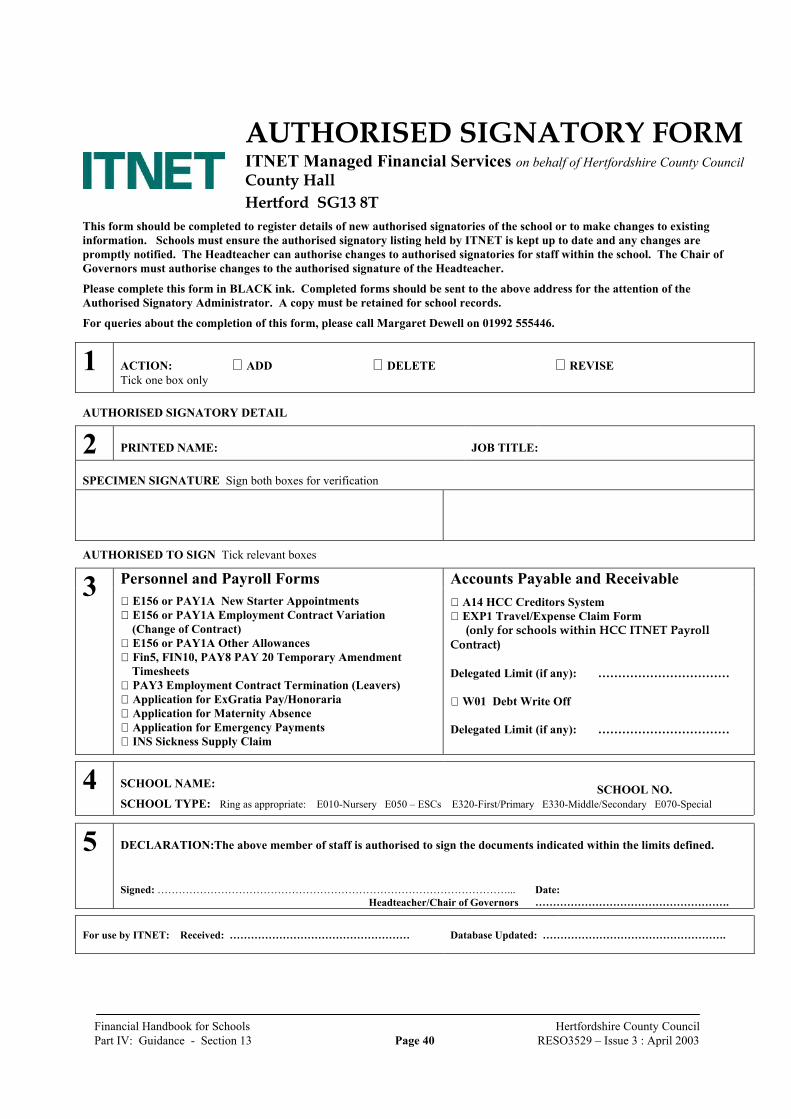

APPENDIX D AUTHORISED SIGNATORY LISTINGSECTION 13

1. It is a fundamental principle of internal control that all transactions should be authorisedin line with the County Council’s financial regulations. ITNET maintains, on behalf ofthe Authority, a full list of schools’ authorised signatories and uses the list to check theauthorisation of payroll, accounts payable and accounts receivable items.

2. Authorised signatories will be those employees of the school that have been delegatedresponsibilities in accordance with the school’s Schedule of Delegation for authorisingpayments. Please refer to the Financial Handbook for Schools, Part IV, Section 1 forfurther details.

3. Each authorised signatory within the school must complete a copy of the attached formand provide two specimen signatures in the boxes provided. The form must then beauthorised by the Headteacher or, where the form relates to the Headteacher, by theChair of Governors.

4. Completed forms should be returned to:

Margaret DewellITNET Payroll ServicesCounty HallHertford SG13 8TN

A copy must be retained within the school for future reference.

5. Schools should ensure that the authorised signatory listing held by ITNET is kept up todate and changes are notified as and when they occur. The form overleaf can be usedfor this purpose.

6. ITNET will check the authorisation of payroll, accounts payable and accountsreceivable items against the authorised signatory listing for the school. Due to thevolume of transactions processed on behalf of schools, these checks will be carried outon a rolling programme of sample checking of transactions.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 40 RESO3529 – Issue 3 : April 2003

AUTHORISED SIGNATORY FORMITNET Managed Financial Services on behalf of Hertfordshire County CouncilCounty HallHertford SG13 8T

This form should be completed to register details of new authorised signatories of the school or to make changes to existinginformation. Schools must ensure the authorised signatory listing held by ITNET is kept up to date and any changes arepromptly notified. The Headteacher can authorise changes to authorised signatories for staff within the school. The Chair ofGovernors must authorise changes to the authorised signature of the Headteacher.

Please complete this form in BLACK ink. Completed forms should be sent to the above address for the attention of theAuthorised Signatory Administrator. A copy must be retained for school records.

For queries about the completion of this form, please call Margaret Dewell on 01992 555446.

1 ACTION: ADD DELETE REVISETick one box only

AUTHORISED SIGNATORY DETAIL

2 PRINTED NAME: JOB TITLE:

SPECIMEN SIGNATURE Sign both boxes for verification

AUTHORISED TO SIGN Tick relevant boxes

Accounts Payable and Receivable3 Personnel and Payroll Forms E156 or PAY1A New Starter Appointments E156 or PAY1A Employment Contract Variation(Change of Contract) E156 or PAY1A Other Allowances Fin5, FIN10, PAY8 PAY 20 Temporary Amendment Timesheets PAY3 Employment Contract Termination (Leavers) Application for ExGratia Pay/Honoraria Application for Maternity Absence Application for Emergency Payments INS Sickness Supply Claim

A14 HCC Creditors System EXP1 Travel/Expense Claim Form

(only for schools within HCC ITNET PayrollContract) Delegated Limit (if any): ……………………………

W01 Debt Write Off

Delegated Limit (if any): ……………………………

4 SCHOOL NAME: SCHOOL NO.

SCHOOL TYPE: Ring as appropriate: E010-Nursery E050 – ESCs E320-First/Primary E330-Middle/Secondary E070-Special

5 DECLARATION:The above member of staff is authorised to sign the documents indicated within the limits defined.

Signed: ………………………………………………………………………………………...Headteacher/Chair of Governors

Date:……………………………………………….

For use by ITNET: Received: …………………………………………… Database Updated: …………………………………………….

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 41 RESO3529 Issue 3 : April 2003

APPENDIX E REQUIREMENTS FOR A PAYROLL PROVIDERSECTION 13

1. Statutory commitments

• Income tax and national insurance: as defined in the Inland Revenue’s YearEnd Pack. In particular, The Employer’s Quick Guide to PAYE; TheEmployer’s Further Guide to PAYE (CWG2) and Booklet 480, Expenses andBenefits: A Tax Guide.

• National insurance contributions: as defined in the Employer’s Manual on National Insurance Contributions

• Statutory Sick Pay (SSP): as defined in the Employer’s Manual on Statutory Sick Pay

• Statutory Maternity Pay (SMP): as defined in the Employer’s Manual on Statutory Maternity Pay

• Working Families Tax Credit and Disabled Person’s Tax Credits (see Year EndPack)

• Recovery of Student Loans (see Year End Pack).

2. Conditions of Service

• Apply the relevant Scheme of Conditions of Service in relation to all payment matters, or any local variations as defined by the LEA.

3. Teachers Pensions Scheme

• Calculate and collect contributions in accordance with the DfES requirements.• Pay over the collected contributions to the LEA for submission to the DfES

monthly.• Calculate and pay amounts due to teachers' dependants under the Short Term

Pension Regulations and make the recovery from the DfES.• Provide the relevant year-end returns relating to contributions, required by the

DfES.

4. Local Government Pension Scheme

• Calculate and collect contributions in accordance with the Regulations.• Pay over the collected contributions to the Local Government Pension Scheme

monthly.• Produce an annual schedule of contributions.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 42 RESO3529 Issue 3 : April 2003

5. Other deductions

Calculate, collect and pay over, the collected contributions for:

• court orders - attachment of earnings- child maintenance- debt recovery- council tax

• voluntary subscriptions(as requested)

- National Union of Teachers- Local Government Officers Association- National Union of Public Employees

• Teachers' Benevolent Fund• UNISON Benevolent Fund• rent (of county council property)• loan repayments.

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 43 RESO3529 Issue 3 : April 2003

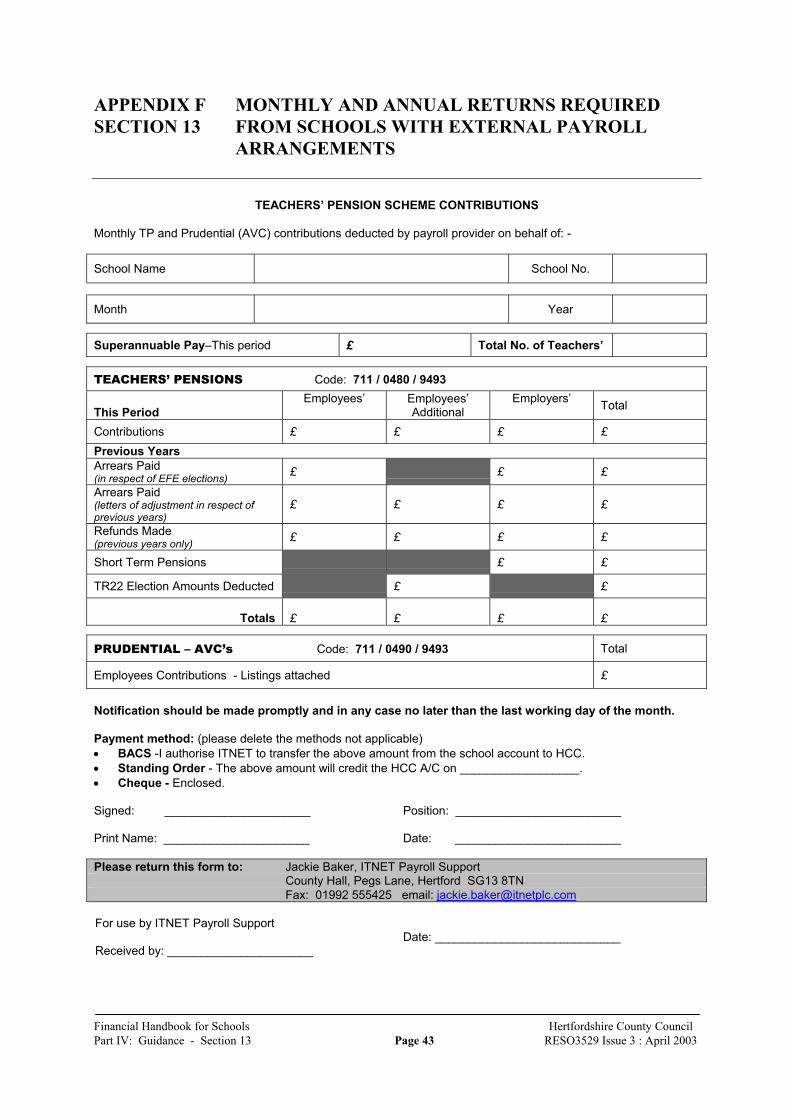

APPENDIX F MONTHLY AND ANNUAL RETURNS REQUIREDSECTION 13 FROM SCHOOLS WITH EXTERNAL PAYROLL

ARRANGEMENTS

TEACHERS’ PENSION SCHEME CONTRIBUTIONS

Monthly TP and Prudential (AVC) contributions deducted by payroll provider on behalf of: -

School Name School No.

Month Year

Superannuable Pay–This period £ Total No. of Teachers’

TEACHERS’ PENSIONS Code: 711 / 0480 / 9493

This PeriodEmployees’ Employees’

AdditionalEmployers’ Total

Contributions £ £ £ £Previous YearsArrears Paid (in respect of EFE elections) £ £ £

Arrears Paid(letters of adjustment in respect ofprevious years)

£ £ £ £

Refunds Made (previous years only) £ £ £ £

Short Term Pensions £ £

TR22 Election Amounts Deducted £ £

Totals £ £ £ £

PRUDENTIAL – AVC’s Code: 711 / 0490 / 9493 Total

Employees Contributions - Listings attached £

Notification should be made promptly and in any case no later than the last working day of the month.

Payment method: (please delete the methods not applicable)• BACS -I authorise ITNET to transfer the above amount from the school account to HCC.• Standing Order - The above amount will credit the HCC A/C on __________________.• Cheque - Enclosed.

Signed: ______________________ Position: _________________________

Print Name: ______________________ Date: _________________________

Please return this form to: Jackie Baker, ITNET Payroll SupportCounty Hall, Pegs Lane, Hertford SG13 8TNFax: 01992 555425 email: [email protected]

For use by ITNET Payroll Support

Received by: ______________________Date: ____________________________

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 44 RESO3529 Issue 3 : April 2003

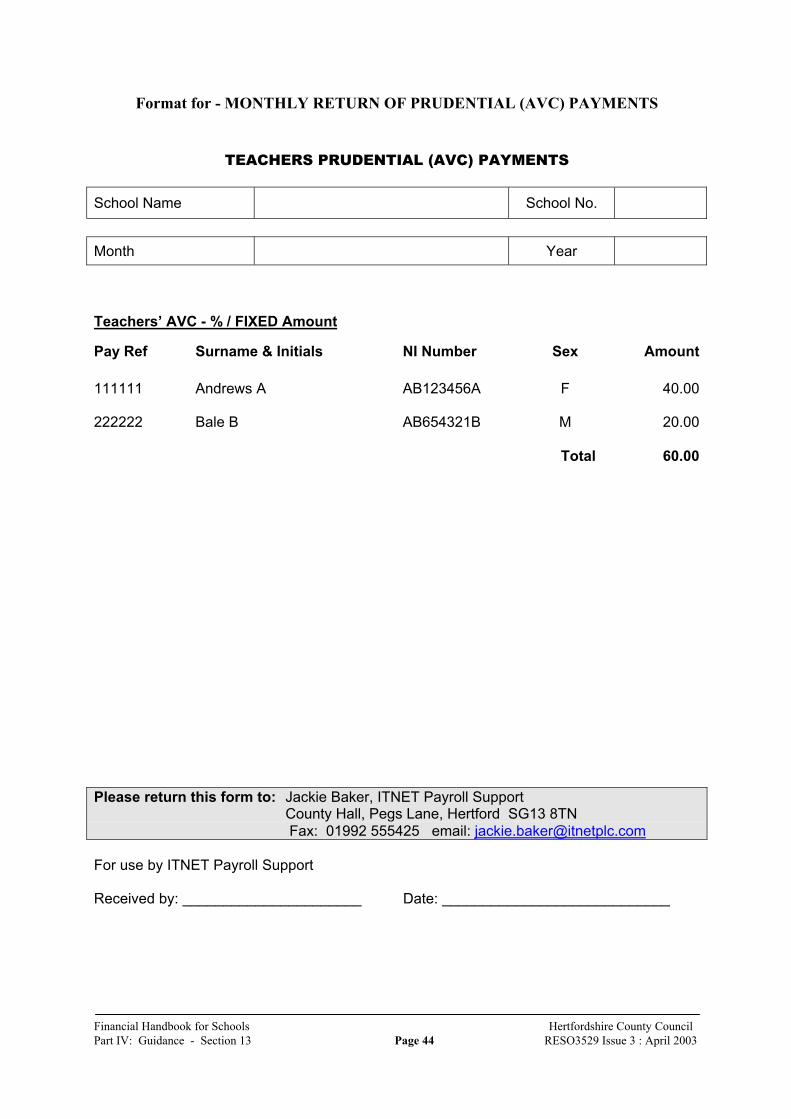

Format for - MONTHLY RETURN OF PRUDENTIAL (AVC) PAYMENTS

TEACHERS PRUDENTIAL (AVC) PAYMENTS

School Name School No.

Month Year

Teachers’ AVC - % / FIXED Amount

Pay Ref Surname & Initials NI Number Sex Amount

111111 Andrews A AB123456A F 40.00

222222 Bale B AB654321B M 20.00

Total 60.00

Please return this form to: Jackie Baker, ITNET Payroll SupportCounty Hall, Pegs Lane, Hertford SG13 8TN

Fax: 01992 555425 email: [email protected]

For use by ITNET Payroll Support

Received by: ______________________ Date: ____________________________

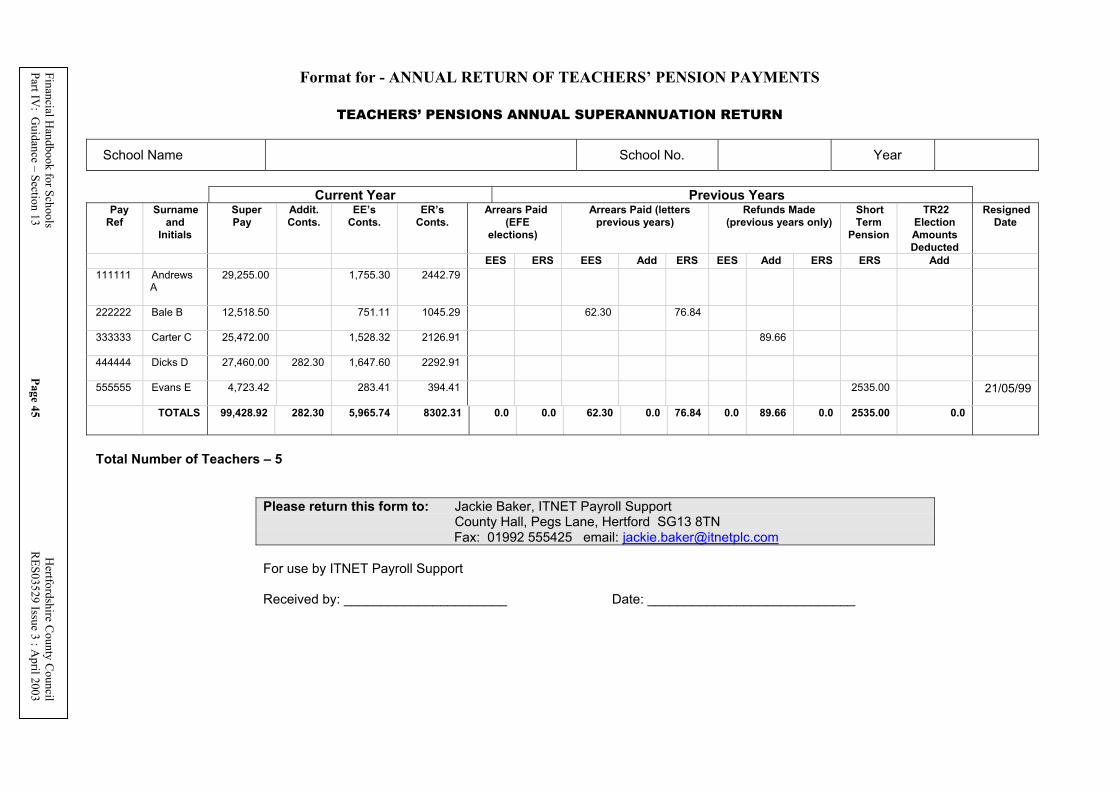

Format for - ANNUAL RETURN OF TEACHERS’ PENSION PAYMENTS

TEACHERS’ PENSIONS ANNUAL SUPERANNUATION RETURN

School Name School No. Year

Current Year Previous YearsPay

RefSurname

andInitials

SuperPay

Addit.Conts.

EE’sConts.

ER’sConts.

Arrears Paid (EFE

elections)

Arrears Paid (lettersprevious years)

Refunds Made(previous years only)

ShortTerm

Pension

TR22ElectionAmountsDeducted

ResignedDate

EES ERS EES Add ERS EES Add ERS ERS Add111111 Andrews

A29,255.00 1,755.30 2442.79

222222 Bale B 12,518.50 751.11 1045.29 62.30 76.84

333333 Carter C 25,472.00 1,528.32 2126.91 89.66

444444 Dicks D 27,460.00 282.30 1,647.60 2292.91

555555 Evans E 4,723.42 283.41 394.41 2535.00 21/05/99

TOTALS 99,428.92 282.30 5,965.74 8302.31 0.0 0.0 62.30 0.0 76.84 0.0 89.66 0.0 2535.00 0.0

Total Number of Teachers – 5

Please return this form to: Jackie Baker, ITNET Payroll SupportCounty Hall, Pegs Lane, Hertford SG13 8TN

Fax: 01992 555425 email: [email protected]

For use by ITNET Payroll Support

Received by: ______________________ Date: ____________________________

Financial Handbook for Schools

Hertfordshire C

ounty Council

Part IV: G

uidance – Section 13 Pa ge 45

RES03529 Issue 3 : A

pril 2003

Financial Handbook for Schools Hertfordshire County CouncilPart IV: Guidance - Section 13 Page 46 RESO3529 Issue 3 : April 2003

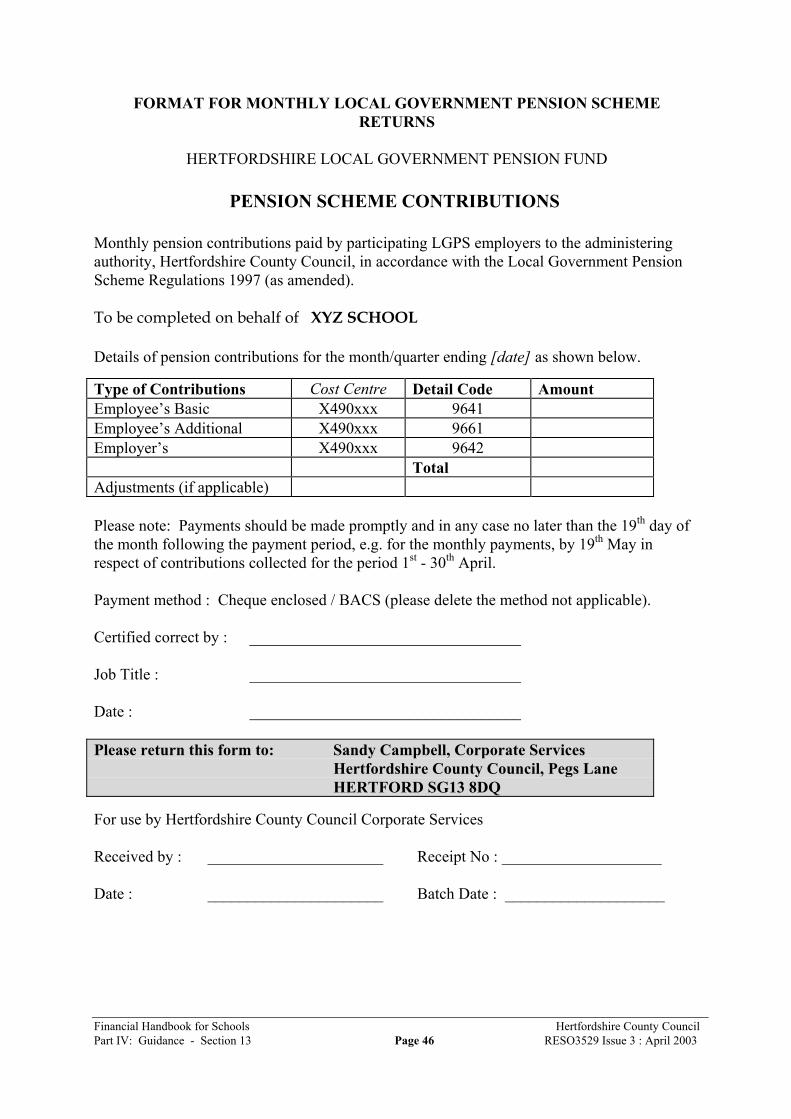

FORMAT FOR MONTHLY LOCAL GOVERNMENT PENSION SCHEMERETURNS

HERTFORDSHIRE LOCAL GOVERNMENT PENSION FUND

PENSION SCHEME CONTRIBUTIONS

Monthly pension contributions paid by participating LGPS employers to the administeringauthority, Hertfordshire County Council, in accordance with the Local Government PensionScheme Regulations 1997 (as amended).

To be completed on behalf of XYZ SCHOOL

Details of pension contributions for the month/quarter ending [date] as shown below.

Type of Contributions Cost Centre Detail Code AmountEmployee’s Basic X490xxx 9641Employee’s Additional X490xxx 9661Employer’s X490xxx 9642

TotalAdjustments (if applicable)