phase-out of libor: impact on floating rate loans and...

TRANSCRIPT

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

Presenting a 90-minute encore presentation featuring live Q&A

Phase-Out of LIBOR: Impact on Floating

Rate Loans and Derivatives; Implementing

Alternative Reference Rates

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

WEDNESDAY, JANUARY 3, 2018

Cheryl I. Aaron, Senior Counsel, Michael Best & Friedrich, Washington, D.C.

Mark Heimendinger, Of Counsel, Lowndes Drosdick Doster Kantor & Reed, Orlando, Fla.

James S. Toscano, Shareholder, Lowndes Drosdick Doster Kantor & Reed, Orlando, Fla.

Tips for Optimal Quality

Sound Quality

If you are listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, you may listen via the phone: dial

1-866-871-8924 and enter your PIN when prompted. Otherwise, please

send us a chat or e-mail [email protected] immediately so we can

address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

Continuing Education Credits

In order for us to process your continuing education credit, you must confirm your

participation in this webinar by completing and submitting the Attendance

Affirmation/Evaluation after the webinar.

A link to the Attendance Affirmation/Evaluation will be in the thank you email

that you will receive immediately following the program.

For additional information about continuing education, call us at 1-800-926-7926

ext. 35.

FOR LIVE EVENT ONLY

Program Materials

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ symbol next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

© 2017 All rights reserved. Lowndes, Drosdick, Doster, Kantor & Reed, P.A.

LOCAL ROOTS. BROAD REACH.SM

Phase-Out of LIBOR

Mark E. Heimendinger

Lowndes, Drosdick, Doster, Kantor & Reed, P.A.

www.lowndes-law.com

© 2017 All rights reserved. Lowndes, Drosdick, Doster, Kantor & Reed, P.A. LOCAL ROOTS. BROAD REACH.SM

Phase-Out of LIBOR

Mark E. Heimendinger

Lowndes, Drosdick, Doster, Kantor & Reed, P.A.

www.lowndes-law.com

Reasons for the Phase-out - Background

LIBOR rate fixing scandal

Wheatley Review published September 20121

ICE Benchmark Administration took over administration of LIBOR February 2014

Alternative Reference Rates Committee convened November 2014

ICE Benchmark Administration LIBOR Roadmap published March 20162

Secured Overnight Financing Rate (SOFR) chosen by ARRC to replace LIBOR

Andrew Bailey announcement July 20173

7

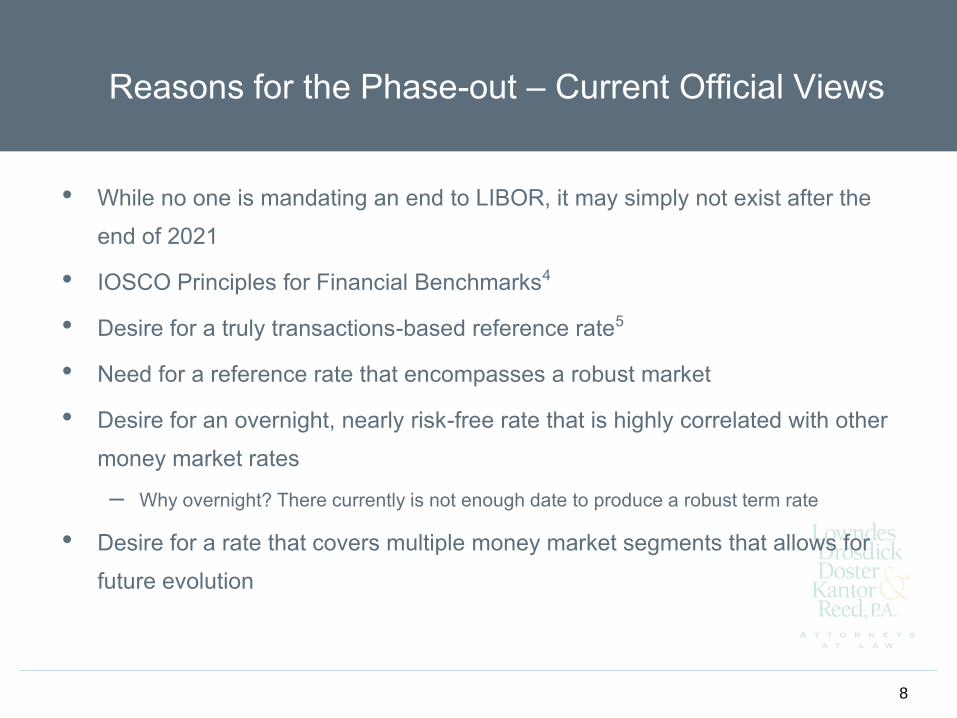

Reasons for the Phase-out – Current Official Views

• While no one is mandating an end to LIBOR, it may simply not exist after the

end of 2021

• IOSCO Principles for Financial Benchmarks4

• Desire for a truly transactions-based reference rate5

• Need for a reference rate that encompasses a robust market

• Desire for an overnight, nearly risk-free rate that is highly correlated with other

money market rates

– Why overnight? There currently is not enough date to produce a robust term rate

• Desire for a rate that covers multiple money market segments that allows for

future evolution

8

Reasons for the Phase-out – Dissenting Views?

• Conflict between creating the “perfect” reference rate vs. “good enough”

• Currently around $160 trillion in transactions quoted in U.S. dollar LIBOR with

approximately 90% of that made up by derivatives6

• Jeffrey Sprecher of ICE stated in October that LIBOR will be difficult to replace and

SOFR doesn’t address term rates7

• CME chief executive Terry Duffy has said he expects LIBOR to continue to be used

alongside the new rates after 20218

• Nearly 80% of the 164 respondents to a recent Bank of America Merrill Lynch survey

released in October believe that LIBOR should continue9

9

Timeline - Paced Transition Plan10

• Infrastructure for futures and/or Overnight Index Swaps (OIS) trading in the new rate is put into

place by ARRC members (2nd half of 2018)

• Trading begins in futures and/or bilateral, uncleared, OIS that reference SOFR (end of 2018)

• Trading begins in cleared OIS that reference SOFR in the current Effective Federal Funds

Rate (EFFR) Price Alignment Interest (PAI) and discounting environment (end of 2018)

• CCPs begin allowing market participants a choice between clearing in new or modified swap

contracts (swaps benchmarked to EFFR, LIBOR and SOFR) into current PAI and discounting

environment or one that uses SOFR for PAI and discounting (1st quarter 2020)

• CCPs no longer accept new swap contracts for clearing with EFFR as PAI and discounting

except for the purpose of closing out or reducing outstanding risk in legacy contracts. Existing

legacy contracts continue to exist but roll off as they hit maturity (2nd quarter 2020)

• Creation of a term reference rate based on SOFR derivatives markets once liquidity has

developed sufficiently to produce a robust rate (end of 2021)

10

Impact on Commercial Lending

• Paced Transition Plan focuses on derivatives

• SOFR is solely an overnight rate and no replacement is anticipated until the end of

2021

• Legacy fallback language contemplates a temporary unavailability of LIBOR not a

permanent replacement

• While ISDA is taking a leading role in derivatives and is working to make sure its rate

works with term products, the market participants must recognize the need to act

11

Impact on Commercial Lending

• Current fallback language is not adequate

– Base rate loans often more expensive than LIBOR

– Need for polling of reference banks

– Problem of value transfers (the choice of alternative rate not adequate without a spread change in

light of difference between LIBOR and a risk-free rate such as SOFR)

– Some provide for conversion to fixed rate based on last quoted LIBOR rate if polling rates not

received

• Wait and see or act now? If you wait until the end of 2021 it may be too late.

– ARRC’s term reference rate is not anticipated to be available until the end of 2021

– ARRC is leaving this to the market – no current legislative or “global” fix available

– What will the lending market be like in 2021?

12

Impact on Commercial Lending

• Review your legacy contracts

– Identify LIBOR-based loans with terms that extend beyond 2021 or with extension options that

extend beyond 2021

– Calculate exposure to this issue

– Identify any securitized loans first. These may not be possible to amend

• Review language and anticipate problems now

• Defeasance?

– Identify any loans with multiple lenders. These will take time to negotiate. Is the agent authorized to

make changes or will changes require 100% lender approval?

– Contact and begin speaking with lenders/borrowers?

13

Impact on Commercial Lending

• Need new fallback language that is flexible enough to anticipate a new (as yet

unidentified) term reference rate

– Clear trigger for use of replacement

– Flexible enough to generally identify a new accepted benchmark rate but specific enough to allow

for mechanical application to allow for securitization and avoid disputes

– Anticipates the difference in magnitude between LIBOR and new reference rate

– Avoids value transfer

– Minimizes market disruption

– Is not subject to manipulation

14

Impact on Commercial Lending

In the event that Lender determines that LIBOR cannot be determined or is no longer offered and provides notice thereof at least one

business day before the interest determination date with respect to the loan interest accrual period, then, commencing with the first day of

such loan interest accrual period, the interest rate will be converted to an interest rate based on the Prime Rate plus an Alternative Rate

Spread. If, prior to a conversion to an interest rate based on the Prime Rate as described above, Lender has determined in its sole but good

faith discretion that LIBOR has been succeeded by another floating rate index that is has an accrual period that is consistent with the loan

interest accrual period, is commonly accepted by market participants in CMBS loans, has been recognized by ISDA for hedging products,

and which has begun to be regularly quoted by a recognized reporting service (the “Alternate Index Rate”), and Lender provides notice

thereof at least one day before the interest determination date with respect to the loan interest accrual period, then, commencing with the first

day of such loan interest accrual period, the interest rate will be converted to an interest rate based on the Alternate Index Rate plus an

Alternative Rate Spread.

“Alternative Rate Spread” shall mean the difference (expressed as the number of basis points) between (a) the interest rate determined in

respect of the loan interest accrual period for which LIBOR was last applicable to the Loan, and (b) the Alternative Index Rate on such date.

- Issues with taking a “snapshot” in time of LIBOR and the Alternative Reference Rate

- Subject to manipulation by large participants?

- Lack of perfect correlation between LIBOR and the Alternative Reference Rate likely to lead to mispricing

- Perhaps focus on a stated number of multiple data points or historical average over a stated period

15

Impact on Securitized and Packaged Consumer Loans

• Approximately $1.8 trillion in outstanding securitizations that reference U.S. dollar

LIBOR.7

• Typical LIBOR provision gives the lender/noteholder direct authority to pick an

alternative reference rate if LIBOR becomes unavailable. Fannie mortgages, for

example, simply require a “comparable” rate.

• These provisions almost universally simply call for the replacement rate and do not

anticipate a change to the spread.

• Cannot negotiate with millions of (consumer) borrowers and, even if you could, legacy

servicing and trust agreements do not accommodate this issue.

• As it stands, ARRC has not proposed a solution. Will the GSEs and regulators act?

16

End Notes

1https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/191762/wheatley_review

_libor_finalreport_280912.pdf

2https://www.theice.com/publicdocs/ICE_LIBOR_Roadmap0316.pdf

3https://www.fca.org.uk/news/speeches/the-future-of-libor

4https://www.iosco.org/library/pubdocs/pdf/IOSCOPD415.pdf

5https://www.newyorkfed.org/medialibrary/media/newsevents/speeches/2017/Frostpresentation.pdf

6https://www.newyorkfed.org/medialibrary/microsites/arrc/files/2017/Bowmanpresentation.pdf

7https://www.risk.net/derivatives/5345891/ices-sprecher-criticises-libor-replacement-push

8https://www.risk.net/derivatives/5356091/the-fraught-search-for-a-libor-fallback

9https://www.reuters.com/article/us-libor-survey-bankofamerica/many-investors-want-libor-to-stay-with-

improvements-bank-of-america-survey-idUSKBN1CV25F; see also

https://www.newyorkfed.org/medialibrary/microsites/arrc/files/2017/Bowmanpresentation.pdf

10https://www.newyorkfed.org/medialibrary/microsites/arrc/files/2017/OConnorpresentation.pdf

17

LOCAL ROOTS. BROAD REACH.SM

Questions?

Mark E. Heimendinger

Of Counsel

Lowndes, Drosdick, Doster, Kantor & Reed, P.A.

407-418-6271 | Orlando, FL

18

Phase-Out of LIBOR

Cheryl I. Aaron

LIBOR in Derivatives Contracts

michaelbest.com

• LIBOR is used as a reference rate in $160 trillion (notional) of

derivatives contracts

• In many interest rate swaps, counterparties rely on a LIBOR-based

rate to hedge against the floating rate risk in a loan or credit facility

• The vast majority of swaps and other types of derivative products

incorporate the terms of the International Swaps and Derivatives

Association (“ISDA”) Master Agreement

• As written, the LIBOR replacement language in the ISDA Master

Agreement is insufficient

• The 2006 ISDA Definitions create a fallback where LIBOR is

unavailable, in which case the Calculation Agent can collect alternate

rates from other major banks and use the arithmetic mean to

determine the replacement

20

LIBOR in Derivatives – what to do now?

michaelbest.com

• First Step: portfolio review • Examine your company’s derivatives portfolio (ideally as part of a

review of all financial contracts), and determine which contracts

reference LIBOR

• Second Step: divide derivatives into 3 categories 1. Already-executed transactions that expire by the end of 2021

• No need to act – counterparties can rely on LIBOR

2. Already-executed transactions that expire after 2021

• Amend, incorporate appropriate fallback terms, allocate associated

risks/losses, and align with related loan fallback terms (as applicable)

3. Transactions that have not yet been executed

• Incorporate appropriate fallback terms, align with related loan fallback

terms (as applicable); potentially choose alternative reference rate

21

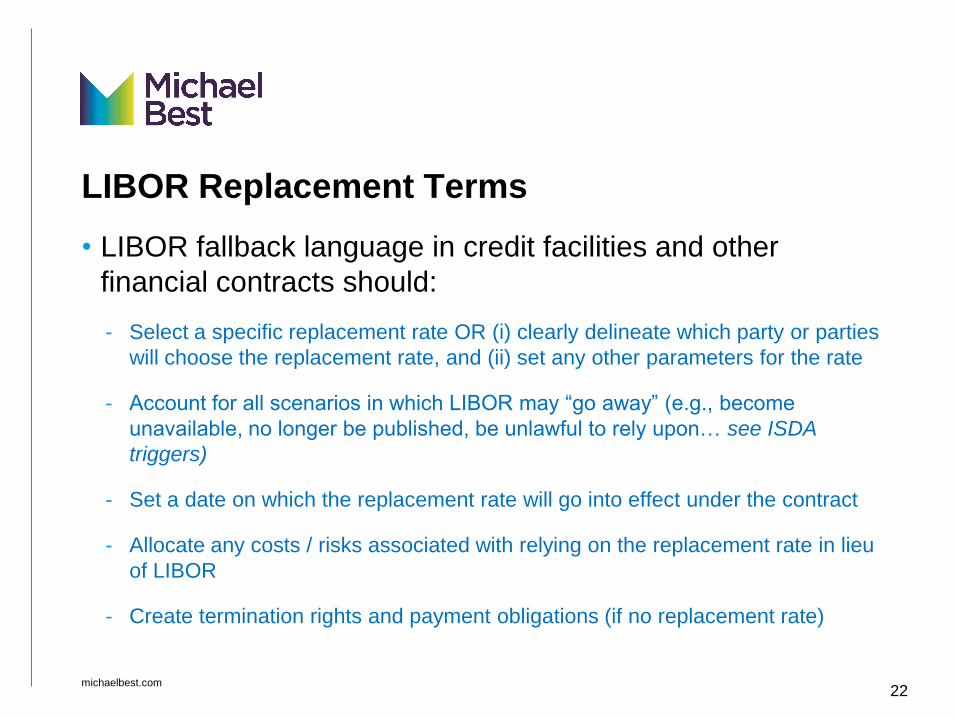

LIBOR Replacement Terms

michaelbest.com

• LIBOR fallback language in credit facilities and other

financial contracts should:

- Select a specific replacement rate OR (i) clearly delineate which party or parties

will choose the replacement rate, and (ii) set any other parameters for the rate

- Account for all scenarios in which LIBOR may “go away” (e.g., become

unavailable, no longer be published, be unlawful to rely upon… see ISDA

triggers)

- Set a date on which the replacement rate will go into effect under the contract

- Allocate any costs / risks associated with relying on the replacement rate in lieu

of LIBOR

- Create termination rights and payment obligations (if no replacement rate)

22

The ISDA Solution

michaelbest.com

• ISDA is in the process of creating a universal LIBOR transition solution for

derivatives and other financial contracts

• At present, ISDA is:

1. Developing a roadmap for the transition (expected December 2017)

2. Drafting a report that will include the results of a market survey on the use of

LIBOR, will identify potential transition issues for existing and new contracts,

and will make recommendations for possible solutions (expected March 2018)

• Going forward, ISDA expects to:

1. Develop strategies related to term structures for the LIBOR replacement rate

and the credit spread that will arise

2. Amend the 2006 ISDA Definitions to incorporate the fallback terms

3. Create a Protocol to incorporate the fallbacks into already-executed

transactions

23

The ISDA Solution

michaelbest.com

• ISDA has identified the following “triggers” for use of its fallback language:

1. A public statement by the ICE Benchmark Administration of its insolvency, with

no successor administrator

2. A public statement by the ICE Benchmark Administration that it will cease

publishing USD LIBOR permanently or indefinitely, and there is no successor

administrator to continue publication

3. A public statement by the UK Financial Conduct Authority that USD LIBOR has

been permanently or indefinitely discontinued

4. A public statement by the UK Financial Conduct Authority that USD LIBOR

may no longer be used

• The trigger timing is upon cessation of USD LIBOR, not at the time of the

announcement

24

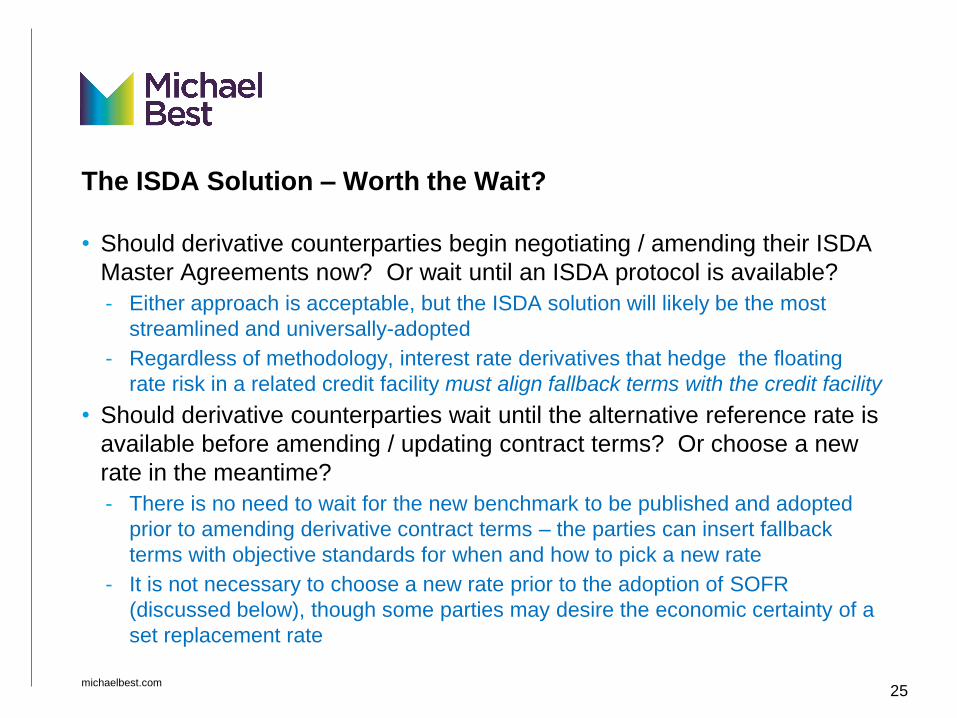

The ISDA Solution – Worth the Wait?

michaelbest.com

• Should derivative counterparties begin negotiating / amending their ISDA

Master Agreements now? Or wait until an ISDA protocol is available?

- Either approach is acceptable, but the ISDA solution will likely be the most

streamlined and universally-adopted

- Regardless of methodology, interest rate derivatives that hedge the floating

rate risk in a related credit facility must align fallback terms with the credit facility

• Should derivative counterparties wait until the alternative reference rate is

available before amending / updating contract terms? Or choose a new

rate in the meantime?

- There is no need to wait for the new benchmark to be published and adopted

prior to amending derivative contract terms – the parties can insert fallback

terms with objective standards for when and how to pick a new rate

- It is not necessary to choose a new rate prior to the adoption of SOFR

(discussed below), though some parties may desire the economic certainty of a

set replacement rate

25

Choosing an Alternative Reference Rate

michaelbest.com

• What makes a good financial benchmark?

- Integrity and continuity. The benchmark should be based on an underlying

market with sufficient liquidity, transaction volume and resilience

- Soundness and robustness. The benchmark should have standardized terms,

transparent data, and readily available historical data (IOSCO Principles)

- Accountability. The benchmark should have evidence of a process that ensures

compliance with the IOSCO Principles

- Governance. The benchmark should have governance structures that promote

its integrity

- Ease of implementation. The benchmark should allow for relative ease in

transitioning to the new rate, including an assessment of the anticipated

demand for hedging and trading, and the potential for a term market in the

underlying rate

26

The Alternative Reference Rate Committee

michaelbest.com

• In 2014, FSOC recommended that U.S. regulators identify an alternative

to USD LIBOR, based on perceived shortcomings

• Later that year, the Federal Reserve Board convened the Alternative

Reference Rates Committee (ARRC) to identify a new financial

benchmark that:

- is based on actual transactions

- aligns with the IOSCO Principles for Financial Benchmarks

• The ARRC is a public-private partnership, comprising representatives of

the Federal Reserve, Federal Reserve Bank of NY, and various banks

• In June 2017, after considering six potential replacement rates, the ARRC

selected the Secured Overnight Financing Rate (SOFR) as its

recommended alternative to USD LIBOR

27

Secured Overnight Financing Rate (SOFR)

michaelbest.com

• What is SOFR?

- Includes overnight, Treasury-backed repo transactions

- All transactions take place in BNY’s triparty repurchase system or are cleared

on one of two Fixed Income Clearing Corporation platforms

- Will be published daily at 8:30am ET based on prior day’s trading activity

• The Federal Reserve requested public comment on its proposal to

compute SOFR in August 2017 (the comment period ended on Oct. 30th)

• The Federal Reserve Bank of New York, along with the Office of Financial

Research, expect to begin publishing SOFR in 2Q 2018

28

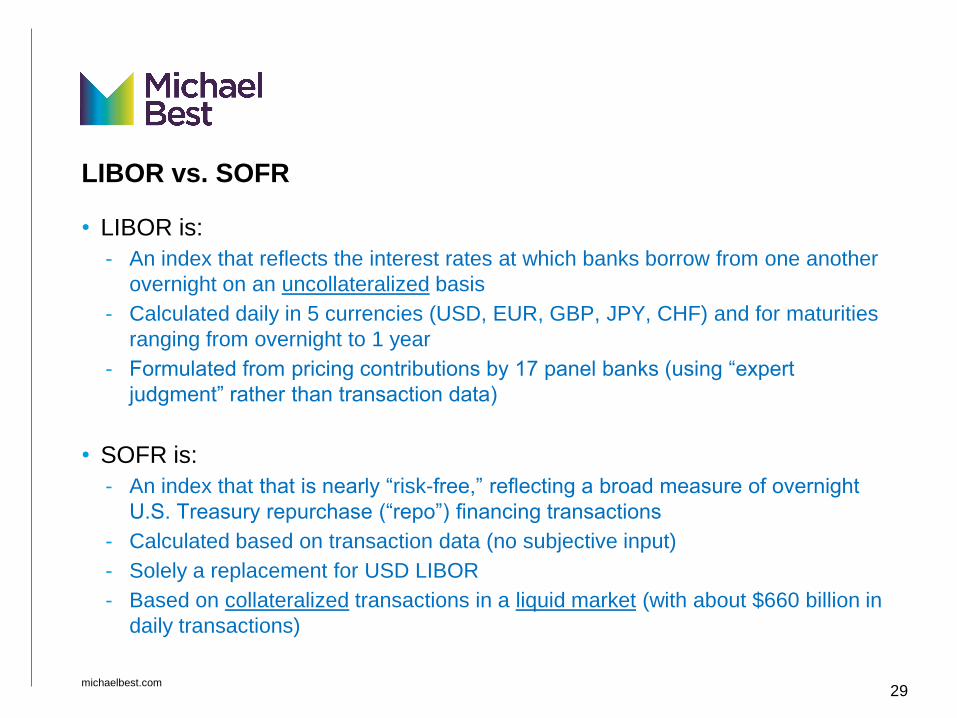

LIBOR vs. SOFR

michaelbest.com

• LIBOR is:

- An index that reflects the interest rates at which banks borrow from one another

overnight on an uncollateralized basis

- Calculated daily in 5 currencies (USD, EUR, GBP, JPY, CHF) and for maturities

ranging from overnight to 1 year

- Formulated from pricing contributions by 17 panel banks (using “expert

judgment” rather than transaction data)

• SOFR is:

- An index that that is nearly “risk-free,” reflecting a broad measure of overnight

U.S. Treasury repurchase (“repo”) financing transactions

- Calculated based on transaction data (no subjective input)

- Solely a replacement for USD LIBOR

- Based on collateralized transactions in a liquid market (with about $660 billion in

daily transactions)

29

Other LIBOR Alternatives

michaelbest.com

• United Kingdom: The Sterling Overnight Index Average (SONIA) will

replace GBP LIBOR

- SONIA is administered by the Bank of England, and is based on actual

transactions in the UK overnight unsecured market

• Japan: The Tokyo Overnight Average Rate (TONAR) will replace JPY

LIBOR, JPY TIBOR and Euroyen TIBOR

- TONAR is calculated and published by the Bank of Japan, and is based on

actual transactions in the Tokyo overnight unsecured market

• Switzerland: The Swiss Average Rate Overnight (SARON) will replace

CHF LIBOR

- SARON is administered by the Swiss National Bank, and is a secured overnight

interest rate average based on the Swiss France interbank market

• EU: The replacement rate for EU LIBOR and Euribor has not yet been

determined

30

The Future of Benchmarks in Derivatives

michaelbest.com

• Despite references to the “end,” “demise” “phaseout,” etc. of LIBOR, the

benchmark may very well continue to exist past 2021

- The UK Financial Conduct Authority did not create a requirement for ICE

Benchmark Administration to stop publishing LIBOR

- Instead, it will no longer compel the LIBOR panel banks to submit pricing data to

the publisher after 2021

• Regardless, LIBOR is no longer the reliable benchmark that it once was,

and derivatives counterparties should not plan on using it past 2021

• Derivatives market participants should expect the transition from LIBOR

to be a massive undertaking, but with advance planning and a thorough

understanding of the new reference rate, the shift may be a smooth one

31

Thank You

michaelbest.com 32

Cheryl I. Aaron

Senior Counsel

Michael Best & Friedrich, LLP

202.595.7934

The Demise of LIBOR:

A Litigation Perspective

James S. Toscano

I. Assumption is that LIBOR goes away

* Given how LIBOR is determined, if the process

for establishing it no longer exists, there is

no objective way to calculate what LIBOR

would be going forward for purposes of

comparison

34

II. CONTRACT LAW GOVERNS

• Loan Credit Agreements

• Adjustable Rate Mortgages

• Home Equity Lines of Credit

• Auto Loans

• Student Loans

• Credit Cards

35

III. HOW DO CONTRACTS ADDRESS

CHANGES IN LIBOR?

Sampling of Provisions: • Successor Provisions: LIBOR continues, but under some authority other than

the ICE Benchmark Administration or is published in a different way.

• Provisions allowing some unilateral flexibility yet still tied to LIBOR: Allows

one party some flexibility to select among LIBOR averages and indecies or to

select some rate still tied in some way to the underlying LIBOR rate.

• Reference Bank Provisions: Provides that a specific interest rate offer from a

specified private bank or the average of rates offered by several identified

banks would be the replacement rate for the LIBOR rate if LIBOR is

unavailable.

• Unilateral Selection: The creditor party is allowed unilaterally to select a

comparable replacement if LIBOR is no longer available.

36

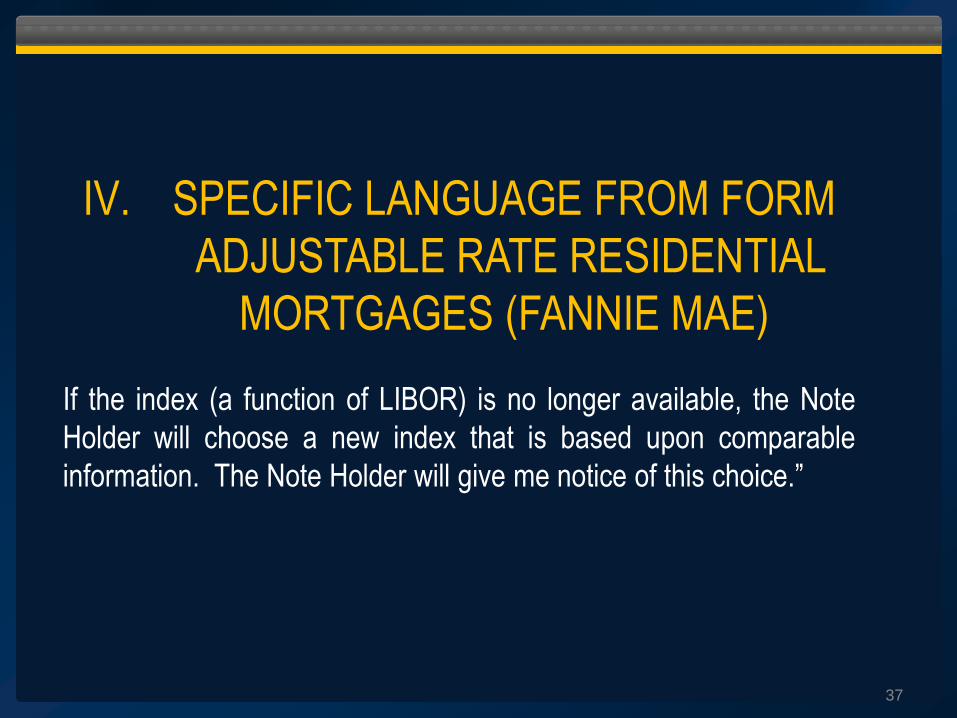

IV. SPECIFIC LANGUAGE FROM FORM

ADJUSTABLE RATE RESIDENTIAL

MORTGAGES (FANNIE MAE)

If the index (a function of LIBOR) is no longer available, the Note

Holder will choose a new index that is based upon comparable

information. The Note Holder will give me notice of this choice.”

37

V. WHAT IS “COMPARABLE INFORMATION?”

• Vague and Ambiguous?

• Interpreted Against the Drafter/Note Holder?

• Essential Term?

• Meeting of the Minds?

38

VI. LEVERAGE/BALANCE OF POWER

• Should have less of an impact on Senior Loan Market –

better able to monitor situation and negotiate resolution.

• Some Commercial Credit Agreements have fallback

language that allows the Issuer to choose other indices

such as the Prime Rate, Federal Funds Rate or the

Treasury “Repo Rate” – temporary fix.

• Those on more equal footing are more likely to work it

out/be able to protect their interests.

39

VII. WHAT ABOUT THE INDIVIDUAL BORROWER

BOUND BY UNILATERAL SELECTION PROVISION?

Unlikely replacements:

• 1 year Treasury Index/Monthly Treasury Average

• Certificate of Deposit Index

• Constant Maturity Treasury

40

VIII. POTENTIAL NEW BENCH MARK

• Alternative Reference Rates Committee

• Fannie Mae and Freddie Mac

41

IX. WHAT TO DO?

42