pitchbook a4us template - aceanalyser.comaceanalyser.com/analyst meet/132754_20090630.pdf · 2. gmr...

TRANSCRIPT

2009

Investor Presentation

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

Key Investment Highlights

V2 June 09

7132 20

1 2

201

150.37

76 6218 8

492

Power Roads Railways Ports Airports Total

X Plan (2002-2007) XI Plan (2007-2012)

The Indian Government has recognized Infrastructure as a key Impediment to Growth and hence encouraging Private Participation

Need to sustain the economic growthNeed to sustain the economic growth

Infrastructure spend plan targets for the XI plan were revised from 4.6% to 7.5% of GDP

Increased plan allocation for infrastructureIncreased plan allocation for infrastructure Encouraging private participationEncouraging private participation

USD bn

Source: Asian Development Outlook, 2007 ; Consultation Paper, Planning Commission, 2007; Govt of India

GDP growth

High GDP growth leads to increasing domestic consumption and higher capital expenditure

0 200 400 600

Power

Roads

Airports

Railways

Ports

Total

Others Private Sector Participation

Private Sector Participation is estimated at 29.6% of total spending in the XI plan

1

Key Investment Highlights

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

GMR Group: A Diversified Conglomerate

The GMR Group was established in 1976 and is a listed company on Bombay Stock Exchange (BSE) and National Stock Exchange (NSE).

GMR Group has rapidly expanded into Infrastructure and other businesses:

Airports

GMR Industries LtdSugar plant in Sankili in AP having cane crushing capacity of 5000 tonnes per dayConstructed and Commissioned Integrated Sugar complex in Haliyal having cane crushing capacity of 3,500 tonnes per day

Corporate Social Responsibility

GMR Varalakshmi FoundationThe Foundation has been working with communities in the quest of improving lives and livelihoods since 1991It focuses on Education, Health, Hygiene and Sanitation, Livelihood and Empowerment and Community Development

The Group was also engaged in the Banking (ING Vysya) & IT (iGate), which were divested with shift in focus to infrastructure.

Agro Based Business

Infrastructure

2

Energy HighwaysUrban

Infrastructure

Sports FranchiseeIPL – Delhi Daredevils

Sports Infrastructure, Development and Management – Delhi Daredevils

3,300 acres SEZ in Tamil Nadu250 acres Aviation specific SEZ on Eastern side of Hyderabad Airport250 acres Multiproduct General SEZ on Western side of Hyderabad Airport 250 acres at Delhi Airport1000 acres at Hyderabad Airport

GMR Infrastructure: Flagship company of the GMR Group

AIRPORTS

ENERGY

HIGHWAYS

URBAN INFRASTRUCTURE

Power Projects (13 Nos) Operational (3 Nos – 823 MW) Under development (10Nos-6200MW)Gross Capacity of 7023 MW

Road Projects (7 Nos: 602 km)Annuity – 255 km Toll – 347 km6 project operational

3

GMR Infrastructure Limited (GIL)

Delhi Airport Development Hyderabad Airport Development

AIRPORTS

Istanbul Airport Development

ENERGY

InterGen N.VNet Capacity – MWAssets in Operation – 7,658 MW located in UK (2,385 MW), Mexico (2,223 MW), Netherlands (820 MW) Philippines (460 MW) & Australia (1,770 MW) Assets in Construction – 428 MW Assets in Development – 2849 MW

Indi

an B

usin

esse

s

International Businesses

Infrastructure Developer, Owner & Operator

GMR Infrastructure: Indian Corporate Structure

GMR Infrastructure Limited (GIL)

ENERGY HIGHWAYS AIRPORT

GMR Tambaram-Tindivanam Expressways Private Limited (GTTEPL) - 93 KMs

GMR Tuni-Anakapalli Expressways Private Limited (GTAEPL) - 59 KMs

GMR Ambala-Chandigarh Expressways Private Limited (GACEPL) -35 KMs

GMR Jadcherla Expressways Pvt Limited (GJEPL) - 58 KMs

GMR Pochanpalli Expressways Private Limited (GPEPL) - 103 KMs

GMR Ulundurpet Expressways Private Limited (GUEPL) - 73 KMs

GMR Energy Limited (GEL) 220 MW

GMR Power Corporation Private Limited

(GPCL) 200 MW

Vemagiri Power Generation Limited (VPGL) -388.5 MW

GMR (Badrinath) Hydro Power Generation Pvt Limited (GBHP) 300 MW

GMR Kamalanga Energy Limted 1050 MW

Delhi International Airport Private Limited (DIAL)

100%

51.0%

100%

100%

100%

74.0%

100%

100%

74.0%

100%

100%

50.1%

63.0%

Operating Companies Under Development

Percentage of holding represents our Direct and Indirect Shareholding

Operating cum Development

GMR Londa Hydro Power Ltd. – 160 MW

100%

GMR Bajoli Holi Hydropower Private Limited–180MW

100%

50.1%

Sabiha Gokcen International Airport (SGIA),Instanbul, Turkey

40%

GMR Krishnagiri SEZ Limited

100%

89%

GMR Hyderabad Aerotropolis Limited (GHAPL) ##

63%

GMR Hyderabad International Airport Limited (GHIAL)

Delhi Aerotropolis Private Limited (DAPL) ##

URBAN INFRASTRUCTURE

GMR Mining and Energy Pvt Limited

GMR Aviations Private Limited (GAPL)

OTHERS

GMR Holdings Private Limited

GMR Hyderabad Aviation SEZ Limited (GHASL) ##

GMR Hyderabad Multiproduct SEZ Limited (GHMSEL) ##

63%

63%

Himtal Hydropower Company Pvt Ltd (Himtal) – 250MW

80%

GMR Energy Trading Limited

51%

GMR Upper Karnali Hydropower PublicLtd – 300MW

73.00%

The balance stake of upper karnali held 22.5% by ITD and 27% by NEA 5

GMR Infrastructure International (Isle of Man)

100%

## DAPL and GHAPL (shown under Property Development) are 100% Subsidiaries of DIAL & GHIAL respectively

GMR Chattisgarh Energy Private Ltd (1200 MW)

100%

GMR Infrastructure: International Corporate Structure

GMR Infrastructure Limited (GIL)

6

GMR Infrastructure International(Isle of Man)

100%

Ons

hore

GMR Holdings Private Limited (GHPL)

74.93%

Off

shor

e

InterGen N.V.(Netherlands)

Malta HoldCo.(Borrowing Company)

Malta HoldCo.(Bidding Company)

OCDs

50%

Potential ListCos.

100%

95%

5%

Loan Facility

100%

CCDs

GMR Energy (Global)(Isle of Man)

OCDs

GMR Infrastructure: A Compelling Investment Story

Leading Indian Infrastructure Player:Over INR 500 bn Investments planned over next five years

PPP model to play significant role in the Infrastructure sector

GMR is well positioned to benefit from this large Growth Opportunity

Entry in the MSCI India index reinforces the Company’s Credentials in Infrastructure Development

1

Broad Based Infrastructure player:- Assets PortfolioSignificant presence across high growth sectors like Airports, Power and Roads

Consistently enjoyed early mover advantage in all the Business Segments

2

Strong track record & established Player: Extensive experience of Developing and Executing projects

Established a Reputation of Reliability and Timely Project completion

3

Balanced revenue mix:Healthy mix of fixed and variable revenue streams across Airports, Power and Roads

4

Strong Management Team:Experienced Management team backed by strong Global Partnership

5

Significant Growth Opportunities:Plans to tap into new opportunities in India and Abroad in the infrastructure space

6

7

GMR Group: Partnership with Best in Class Global Players

Europe’s largest Cargo hub

Europe’s 2nd largest Passenger Airport

Operator and Manager of Malaysia’s 39 airports which comprise International, Domestic and Short Take-Off and Landing (STOL) ports

Largest Airport Retailer in Malaysia with 40 outlets in 4 airports

India’s Premier Infrastructure Finance Organization - over 332 projects financed in Power, Roads, Urban Infrastructure

One of the Worlds largest diversified Organizations with a Market Capitalization of about USD400bn

Korea’s Largest Integrated Electric utility which controls approx 88% of Koreas generating capacity

Global leader in Heavy Industries with Global presence in Shipbuilding, Offshore & Engineering, Industrial Plant & Engineering, Engine & Machinery and Construction Equipment

Malaysia's leading conglomerate in Infrastructure-Building, is a wholly-owned subsidiary of Khazanah Nasional Berhad, an Investment arm of the Government

Air

port

sPo

wer

Road

s

One of the leading Engineering and Construction companies in Turkey

8

Net Revenue EBITDA

EBITDA Margin

4

GMR Infrastructure: Key Financials for FY 09

Key Investment Highlights

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

Passenger Traffic: Growth in India

9

Passenger Traffic In Leading Airports of India

10

Delhi and Hyderabad Airports control 26% of Domestic & 29% of International Passenger Traffic

Domestic PAX Distribution in FY 2009 (Total PAX = 77.3 Mn)

International PAX Distribution in FY 2009 (Total PAX = 31.6 Mn)

Passenger Traffic (In Millions)

Cargo Traffic In Leading Airports of India

11

Delhi and Hyderabad Airports control 27% of Domestic & 28% of International Cargo Traffic

Domestic Cargo Distribution in FY 2009 (Total Cargo= 548 Thousand MT )

International Cargo Distribution in FY 2009(Total Cargo= 1149 Thousand MT )

Hyderabad Airport: Development of fastest growing Airport in India

Consortium PartnersConsortium Partners

12

Sponsor Shareholding

63.0%

11.0%

13.0%

13.0%

India’s First

PPP Green Field AirportOperationalized

on23rd of March 2008

Phase I

Development Highlights

Project OverviewProject Overview

Project Features

Concession Period of 30+30 years from 2008 to 2038

Land Available 5,500 acres

Concession fee 4% of revenue (deferred till 11th year)

Project Cost (Phase 1) USD 608 Mn (INR 29.20 Bn)

Means of Finance (In INR Bn) Equity :3.78; Debt:21.20; Grant: 1.07; Interest Free loan : 3.15

Air Side Facilitiesa) One of the longest Runways (4,260 m) with parallel Taxiwayb) 42 Aircraft parking stands

•30 Remote stands •12 Aerobridge facility c) 5 Cargo Parking Stands

Land Side facilitiesa) 146 Check-in counters ( self check-in – 16)b) 46 Immigration countersc) 3 nos. of 90 meter & 1 no. 70 meter Baggage carouselsd) Car Park facility (3700 cars)

Development to be done in 4 Phases

Proposed Capacities Phase I Phase IV

PAX (in Mn ) 12 40

Cargo (Metric Tonnes) 1,00,000 3,50,000

Number of Runways 1 2

Passenger Terminal Building Area

1.17 Mn Sq.ft 3.9 Mn Sq.ft

Master Planners Consortium comprising of Cowi of Norway, Avia Plan of Denmark & Stup of Mumbai

Airside and Landside Works Contractor

Larsen & Toubro

Airport Service Quality Rating (ASQ) given by Airports Council International (ACI)

Rating of 4.40 (scale 1 to 5) in service standards

Hyderabad Airport: Commercial Arrangements and Developments

Aeronautical OperationsAeronautical Operations Non-Aeronautical OperationsNon-Aeronautical Operations

UDF Development Fees (UDF)

Profile ChargesCommencement

Date

Domestic Passengers

Rs 375 (inclusive of all Taxes) per Departing Domestic Passenger

23rd August 2008

International Passengers

Rs 1000 (inclusive of all Taxes) per Departing International Passenger

23rd April 2008

Area Partner

Cargo operation JV with Menzies plc, UK

In-flight kitchens LSG Sky Chefs & Sky Gourmet

Fuel farm operator Reliance industries Ltd

Fuel farm suppliers Reliance, IOCL, BPCL, HPCL & Shell

Ground Handling Menzies Aviation & Bobba, Air India & SATs

Duty-free retail Nuance 2525 sq.mt.)

MRO JV with Malaysia Airlines

Airport advertisement Laqshya

F&B HMS Host

Lounge management Plaza Premium Lounge (3Nos)

Hospitals Apollo Hospitals (17 Beds)

Car Parking Tenaga Car parking of Malaysia

Telecom Services Tata Teleservices

Book Stores Landmark and Odyssey

Forex Counters Weizmann and Travelex

Health Health & Glow & Dabur

Airport Authority of India (AAI) Prescribed Charges

•

Passenger Service Fees (PSF)

•

Landing Charges

•

Parking Charges

•

X-Ray Baggage Charges

•

Housing Charges

13

Hyderabad Airport: Surface Connectivity

Airport Roads Connectivity

Airport Location: 25 km / 19 miles from Begumpet

The major access points to the new airport include:

a) Four-lane National Highway NH-7 with service lanes (on its west)

b)Four-lane Srisailam State Highway (on its east)

c) Proposed eight-lane 24.38 km access controlled Outer Ring Road

(ORR)

d) Widening of 52-km Inner Ring Road with many flyovers with six lanes

Four-lane 11.6 km long P V Narasimha Rao Elevated Expressway

e) Multiple traffic management initiatives to decongest city roads

f) Alternate four-lane road P7 to decongest Srisailam Highway

g)Other alternate modes being worked out with State government

include: Multi-Modal Transportation System (MMTS)

Mono Rail Transport System (MRTS)

h) Proposed Dedicated Airport Train from city to Airport 40 km stretch

to be covered in around 25 minutes

Airport Commuting Facilities

a) 700 Radio taxis with GPS Vehicle tracking system & 100

executive cars

b) 28 brand new custom designed buses service with Passenger

friendly amenities as part of Aero Express bus service

14

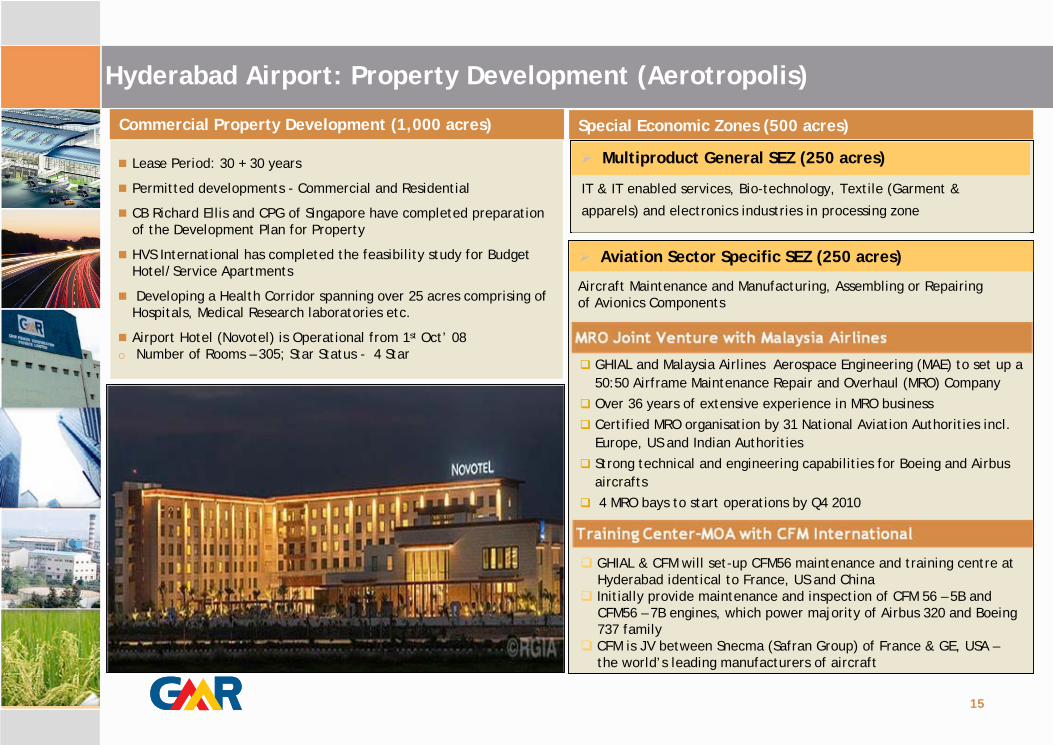

IT & IT enabled services, Bio-technology, Textile (Garment &

apparels) and electronics industries in processing zone

Lease Period: 30 + 30 years

Permitted developments - Commercial and Residential

CB Richard Ellis and CPG of Singapore have completed preparationof the Development Plan for Property

HVS International has completed the feasibility study for BudgetHotel/Service Apartments

Developing a Health Corridor spanning over 25 acres comprising of Hospitals, Medical Research laboratories etc.

Airport Hotel (Novotel) is Operational from 1st Oct’ 08o Number of Rooms – 305; Star Status - 4 Star

Commercial Property Development (1,000 acres)

Hyderabad Airport: Property Development (Aerotropolis)

GHIAL and Malaysia Airlines Aerospace Engineering (MAE) to set up a 50:50 Airframe Maintenance Repair and Overhaul (MRO) CompanyOver 36 years of extensive experience in MRO business

Certified MRO organisation by 31 National Aviation Authorities incl. Europe, US and Indian Authorities

Strong technical and engineering capabilities for Boeing and Airbus aircrafts4 MRO bays to start operations by Q4 2010

GHIAL & CFM will set-up CFM56 maintenance and training centre at Hyderabad identical to France, US and ChinaInitially provide maintenance and inspection of CFM 56 – 5B and CFM56 – 7B engines, which power majority of Airbus 320 and Boeing 737 familyCFM is JV between Snecma (Safran Group) of France & GE, USA –the world’s leading manufacturers of aircraft

Special Economic Zones (500 acres)

Multiproduct General SEZ (250 acres)

Aviation Sector Specific SEZ (250 acres)

Aircraft Maintenance and Manufacturing, Assembling or Repairing of Avionics Components

15

Hyderabad Airport: Glimpses

16

Hyderabad Airport: Business Development Initiatives

Currently:12 Foreign Airlines ( British Airways, Lufthansa, KLM, Singapore Airlines,

Thai Airways, Malaysia Airlines, Emirates, Gulf Air, Qatar Airways, etc.)

10 Domestic Airlines (Air India, Jet Airways, Kingfisher Airlines, Indigo, Spicejet, etc.)

Expected:Etihad Airways to start operations from June’09

In dialogue with China Eastern, Delta Airlines, Tiger Airways, Turkish Airlines, Kenyan Airlines, Iran Airlines

Planned:Initiated dialogues with NACIL, Jet Airways and Kingfisher Airlines to

create a hub in Hyderabad

GHIAL is one of the first Airports in South and South East Asia to be certified as ISO 27001 (Information Security Management System) complaint

Established “Internal Passenger Satisfaction Feedback” system through touch screen KIOSK to understand and analyze the passenger satisfaction levels

Introduced Web-based Suggestion Scheme

Enrolled to participate in ACI-ASQ Customer Satisfaction Benchmarking Program

Initiated Scientific Problem Solving methodology to address the process improvement and cost rationalization issues

Airlines OperationsAirlines Operations Quality InitiativesQuality Initiatives

17

Plan to set up a world class centre for perishable cargo

Animal Quarantine for movement of Laboratory animals, Pets and live stocks has been setup effective April 2009

Recent DevelopmentsRecent Developments

Airline Operations

British Airways started operations from 7th Dec’ 08Air Arabia started operations from 26th Oct’08

Recent RecognitionsRecent Recognitions

GHIAL won the Leadership in Energy and Environmental Design (LEED) “silver rating” by US Green Building (US GBC) and becomes the first airport in Asia and the third Airport globallyto have been recognized by this award

Passenger Terminal Building of GHIAL won the Outstanding Concrete Structure award 2008 of Andhra Pradesh by Indian Concrete Institute

Recognition from ORBIS for Airport Related CSR Activities

The Passenger Traffic has grown at a CAGR of 23% over the past 5 years.

For the period ended FY 09, the Composition of Domestic to International Passengers has been 75:25.

The Cargo Traffic has grown at a CAGR of 15% over the past 5 years

For the period ended FY 09, the Composition of Domestic to International Cargo has been 45:55.

The Air Traffic Movements have grown at a CAGR of 24% over the past 5 Years.

For the period ended FY 09, the Composition of Domestic to International ATMs has been 85:15.

Aircraft Movements (In Thousands)Aircraft Movements (In Thousands) Cargo Tonnage (In Thousand Tonnes)Cargo Tonnage (In Thousand Tonnes)

Total Passengers (In Millions)Total Passengers (In Millions)

32% Growth

41% Growth

35% Growth

19% Growth -2.4% Growth

27% Growth

42% Growth

43% Growth

21% Growth -11% Growth

Hyderabad Airport: Historical Growth Pattern

26% Growth6% Growth

28% Growth14% Growth 6% Growth

18

ATM PerformanceATM PerformanceTotal Passengers (in Thousands)Total Passengers (in Thousands)

Cargo Tonnage (inTonnes) Cargo Tonnage (inTonnes)

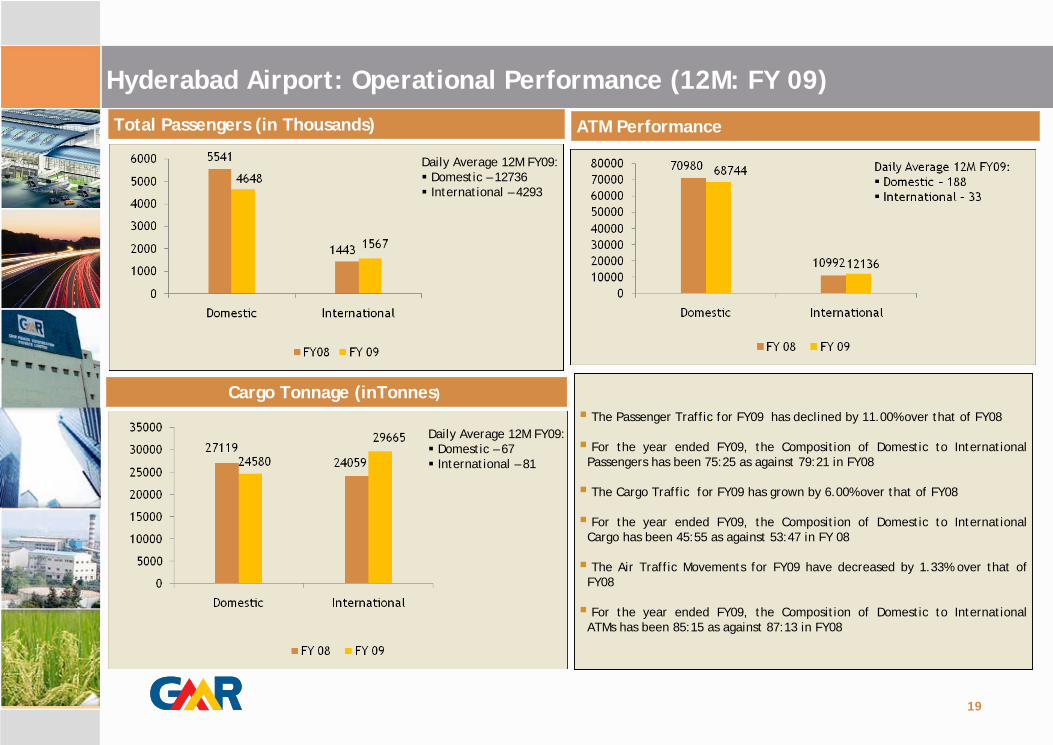

Hyderabad Airport: Operational Performance (12M: FY 09)

The Passenger Traffic for FY09 has declined by 11.00% over that of FY08

For the year ended FY09, the Composition of Domestic to International Passengers has been 75:25 as against 79:21 in FY08

The Cargo Traffic for FY09 has grown by 6.00% over that of FY08

For the year ended FY09, the Composition of Domestic to International Cargo has been 45:55 as against 53:47 in FY 08

The Air Traffic Movements for FY09 have decreased by 1.33% over that of FY08

For the year ended FY09, the Composition of Domestic to International ATMs has been 85:15 as against 87:13 in FY08

19

Daily Average 12M FY09:Domestic – 12736 International – 4293

Daily Average 12M FY09:Domestic – 67International – 81

Total Passengers (in Thousands)Total Passengers (in Thousands) ATMs PerformanceATMs Performance

Cargo Tonnage (InTonnes) Cargo Tonnage (InTonnes)The Passenger Traffic for FY09 Q4 has declined by 0.68% over that of FY09 Q3,

as compared to a 2.13% decrease in FY09 Q3 over that of FY09 Q2

For the period ended FY09 Q4, the Composition of Domestic to International Passengers has been 75:25 as against 73:27 in FY09 Q3 and 74:26 in FY09 Q2

The Cargo Traffic for FY09 Q4 has declined by 5.2% over that of FY09 Q3, as compared to a 4% decline in FY09 Q3 over that of FY09 Q2

For the period ended FY09 Q4, the Composition of Domestic to International Cargo has been 46:54 as against 45:55 in FY09 Q3 and FY09 Q2

The Air Traffic Movements for FY09 Q4 has decreased by 2.20% over that of FY09 Q3, as compared to a 3.85% increase in FY09 Q3 over that of FY09 Q2

For the period ended FY 09 Q3, the Composition of Domestic to International ATMs has been 84:16 as against 83:17 in FY 09 Q3 and 85:15 in FY09 Q2

Hyderabad Airport: Quarterly Operational Performance (Q4: FY 09)

20

INR mn FY09

Gross Revenues 3,860

Aeronautical Revenues 2,058

Non-Aeronautical Revenues 1,802

Less: Annual Fee to AAI 163

Net Revenues 3,697

Operating Expenses 2,266

EBIDTA 1,431

Other Income 36

Interest and Finance Charges 1,536

Depreciation 1,122

PBT (1,191)

PAT (1,210)

Cash Profits (88)

Gross Revenue (Quarterly)

1,0111,077

EBIDTA (Quarterly)

Hyderabad Airport: Financial Performance

21

In Rs millions

1,041

Delhi Airport: Modernization and Development of Premier Airports in India

Consortium PartnersConsortium Partners

Sponsor Shareholding

54.0%

10.0%

10.0%

26.0%

Financing Plan (Phase I)Financing Plan (Phase I)

Source Contribution ($ Mn)

Contribution (INR Mn)

Equity including internal accruals (*)

260 12,500

Development Fees 381 18,270

Interest Free Deposits 190 9,120

Loan from FIs/Banks 1,039 49,860

Total Estimated Project Cost 1,870 89,750

22

ModernizationOf

Existing Terminals (T1 & T2)Completed

In December 2008

ConstructionOf

Greenfield Terminal(T3)To be Completed

ByMarch 2010 Project Overview

Concession period of 30+30 years from 2006 to 2036Revenue Share 45.99 % shared with AAILand 5,100 acres

Estimaited Project Cost (Phase I)

USD 1,870 Mn (INR 89.75 Bn)

Development to be done in 5 PhasesProposed Capacities Phase1 Phase VCompletion Date 2010 2035Pax capacity 46 Mn 100 Mn Cargo capacity 0.5 Mn tons 3.6 Mn tons Runways 2 4Passenger Terminal Building Area 5.5 Mn Sq.ft 17.2 Mn Sq.ft

Design Engineers Mott McDonald Third Runway & Terminal 3 L&T Owners Engineers

TCE, Lahmeyer and Parsons Brinckerhoff

Development Highlights

* - Additional equity brought in by shareholders Rs 12500 Mn towards the project GMR acquired 3.9% stake from IDF

and issued fresh 13 mn shares of GIL in June 09

New Terminal with handling capacity of 10 Mn pax

• Area of 350,000 sq. ft.

• 72 Check in counters

• 16 Security Channels

• In line Baggage screening

Delhi Airport: Construction of Phase 1A Finalized Landside Facilities

T 2 Terminal Refurbishment

Refurbishment of International Terminal with increase in annual capacity from 5 mn pax to 8 mn pax

3-level In-line baggage screening and Handling system Increase in length of 4 Baggage Reclaim beltsEntry gates increased from 4 to 8Check in counters increase from 78 to 100Check in Concourse expansion from 4,500 sqm to 6,500 sqm No of X-ray units increase from 8 to 15Emigration counters increase from 28 to 52Immigration Counters increase from 28 to 48 Security Channels increase from 10 to 228 new In-line Baggage Screening Systems

Airside Facilities

3rd Runway of 4,430 meters and New Rapid Exit Taxiways commissioned and operational

Fire stations, New Crash Fire Tenders & associate infrastructure

New Airside Cleaning Equipments, Automated Grass cutting and Improved Lighting and Signage

23

• Capacity expansion to 8 Mn pax

Terminal T 1

Domestic Departure Terminal (A & D)

New Departure TerminalInaugurated on 26th February 2009

Commenced Operations

Domestic Arrival Terminal (C)

100% Complete and Operational

Terminal T 2 Refurbishment

100% Complete and Operational

All Major Procurement Contracts AwardedTotal Manpower at Site- DIAL & Project Management Contractor : 360- Subcontractor: 25,000 at present

Capital Work in Progress (T3 Terminal)Capital Work in Progress (T3 Terminal)

Financial Arrangement Financial Arrangement

24

DIAL working on aggressive Commissioning Schedule DIAL working on aggressive Commissioning Schedule

Airport Capacity Time

Changi Airport 22 Million 76 Months

Heathrow T5 25 Million 60 Months

Beijing Airport T3 45 Million 60 Months

IGI Airport T3 34 Million 37 Months

The Financial Closure document was signed on 7th Dec ‘07Rupee Term Loan of Rs.3650 Crores from 10 Domestic Banks

- Tenure – 17 years Door-to-door

- PLR Linked Interest Rate (Currently 10.0%-10.5%) with a reset

clause of every 3 years.

Foreign Currency Loan of USD 350 Million from 8 Banks

- Tenure – 13 years Door-to-door

- Interest Rate: Libor + 185 bps

Total Capital Expenditure till 31st March ‘09 is Rs.6,200 Crores Rupee Loan Disbursed: Rs.3,111 Crores with Debt to Equity ratio of

1.25:1 at all times

Shareholders Funds infused comprising of Equity Rs. 1200 crores,

Advance against Lease Deposits – Rs 1250 crores

Key Features Phase 1B Development ( Completion by Mar 2010) Key Features Phase 1B Development ( Completion by Mar 2010)

Airside Facilities

75 Aerobridges

48 Contact Stands

20 remote parking bays

General Aviation facilities

Landside Facilities

168 Nos Check in Counters

14 Nos In-line Baggage Reclaim belts.

Terminal Building T3 of 5.2 million sq. ft with annual capacity of

34 Million

90 Walklators, 47 Escalators, 70 Lifts & 200 Washrooms

Multi-level Car Parking, Taxi Staging & Bus Parking – 4,300 lots

Lounge Area of 10.000 sq. m.

High Speed Rail Link – DMRC

Expansion/Up gradation of Utilities (Sewerage, Power, Water)

Delhi Airport: Construction Status of Terminal T3 (Phase 1B)

Particulars FY 09 Q2 FY 09 Q3

Main Passenger Terminal Building 51% 62.31%

Integrated Terminal Piers Civil works

55% 65.20%

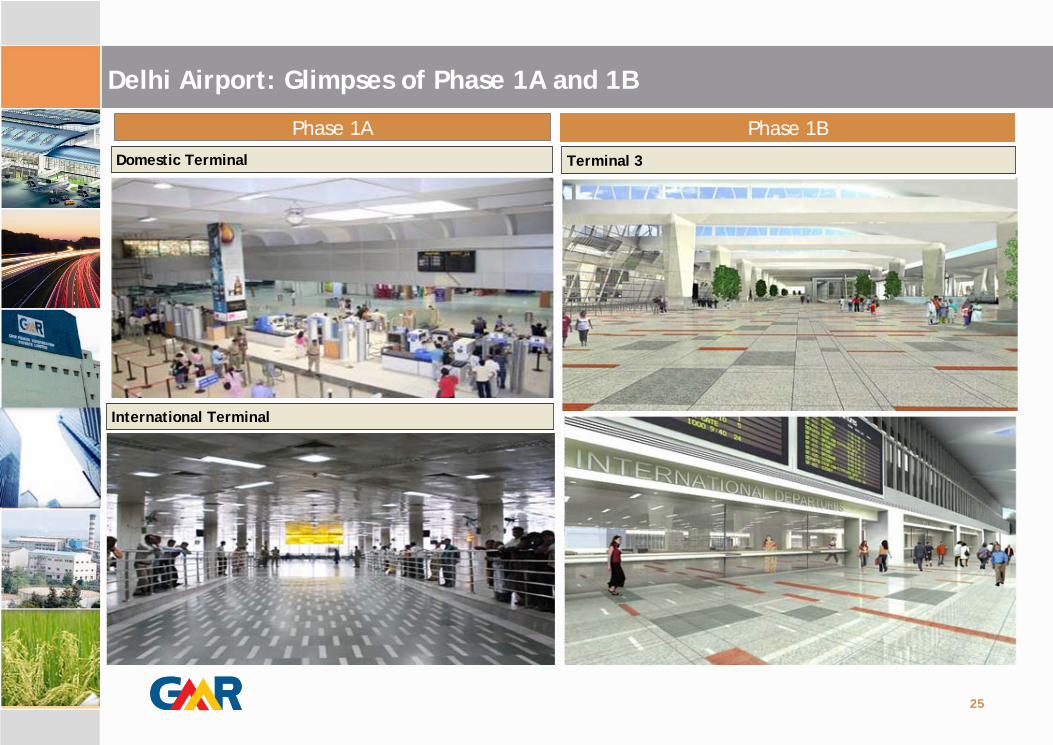

Delhi Airport: Glimpses of Phase 1A and 1B

Domestic TerminalDomestic Terminal

International TerminalInternational Terminal

25

Phase 1A Phase 1B

Terminal 3Terminal 3

Delhi Airport: Master plan for World Class Passenger Terminal by 2010, well- in-time for Commonwealth Games

Phase I Master Plan1 Phase I Master Plan1

Efficient planning to minimize impact on existing operations

26

*Figure not to scale

New Integrated Terminal (T3) by 2010

Land Bank of 250 acres

New Runway (3)

4,430 Mts

Existing Domestic Terminal (T1)

Existing International Terminal Building

Metro RailDeveloper – DMRC Operator – RelianceNo. of Stations – 6

1. New Delhi Railway Station2. Shivaji Stadium3. Moti Bagh4. Aerocity Station (inside

airport) 5. Airport Station (inside Airport)6. Dwarka Sector 2

Delhi Airport: Commercial Arrangements and Developments

Area Partner

Duty free Retail Alpha Airport till 2010

Duty free Retail (T3) Aer Rianta (2010 onwards)

Advertisement Times Innovative Media Pvt Ltd till 2010

Ground Handling Menzies Bobba and Combata, WFS and Bird Group

Cargo Handling Bird Group and World Flight Services (WFS)

Car Parking Garuda Aviation Services Pvt. Ltd. (T2)Mahesh & Sunny Car Park (T1)

In Flight Kitchen Ambassador

Hospitals Apollo

Food & Beverages (T3) SSP Catering India Ltd.; Devyani International Ltd.; Travel Food Services Pvt. Ltd.

27

Airport Development Fees (ADF)

Profile Charges

Domestic Passengers Rs 200 (inclusive of all Taxes) per Departing Domestic Passenger

International Passengers Rs 1300 (inclusive of all Taxes) per Departing International Passenger

Amount collected through DF would not in any case exceed a

ceiling of Rs.1827/- crores exclusive of Taxes (NPV as on 1.3.2009)

ADF would be charged for a period of 36 months w.e.f 01.03.2009

ADF would not be subjected to Revenue sharing

Aeronautical Charges Hike

A 10% hike in Aeronautical Charges (Landing charges, Parking charges, Passenger Service Fees, X-Ray baggage charges, Housing charges) has been approved with effect from 16th February 2009

Aeronautical OperationsAeronautical Operations Non-Aeronautical OperationsNon-Aeronautical Operations

Airport Authority of India (AAI) Prescribed Charges

•

Passenger Service Fees (PSF)

•

Landing Charges

•

Parking Charges

•

X-Ray Baggage Charges

•

Housing Charges

Airline OperationsAirline Operations

Currently

58 Foreign Airlines (Air Arabia, Air France, Air China International Corp., Air France, American Airlines, Austrian Airlines, British Airways, Emirates, Gulf Air, Malaysia Airlines, Lufthansa, Kuwait Airways etc.)

10 Domestic Airlines (Jet Airways, Kingfisher Airlines, Spice Jet, Indian Airlines, Indigo etc.)

Quality InitiativesQuality Initiatives

Received a Rating of 3.26 for Quality standards on the ASQ Rating Scale

OMDA schedule 3 compliance:•

Objective Service Quality requirement as per OMDA •

Identified processes are monitored ,measured as per target set by AAI and action initiated for improvement in grey areas.

ISO9001:2000 Quality Management System:

•

Ensure having basic system in place

•

Continual improvement of processes

•

OMDA compliance

Delhi Airport: Business Development Initiatives

28

The Passenger Traffic has grown at a CAGR of 17% over the past 5 years.

For the period ended FY 09, the Composition of Domestic to International Passengers has been 66:34.

The Cargo Traffic has grown at a CAGR of 8% over the past 5 years .

For the period ended FY 09, the Composition of Domestic to International Cargo has been 30:70.

The Air Traffic Movements have grown at a CAGR of 12% over the past 5 Years.

For the period ended FY 09, the Composition of Domestic to International ATMs has been 73:27.

Aircraft Movements (In Thousands)Aircraft Movements (In Thousands) Cargo Tonnage (In Thousand Tonnes)Cargo Tonnage (In Thousand Tonnes)

Total Passengers (In Millions)Total Passengers (In Millions)

13% Growth

22% Growth

20% Growth

14% Growth-6% Growth

23% Growth

27% Growth

26% Growth

17% Growth -4.7% Growth

Delhi Airport: Historical Growth Pattern

17% Growth11% Growth 2% Growth

11% Growth -1.6% Growth

29

Total Passengers (in Thousands)Total Passengers (in Thousands) ATMs PerformanceATMs Performance

Cargo Tonnage (InTonnes) Cargo Tonnage (InTonnes)

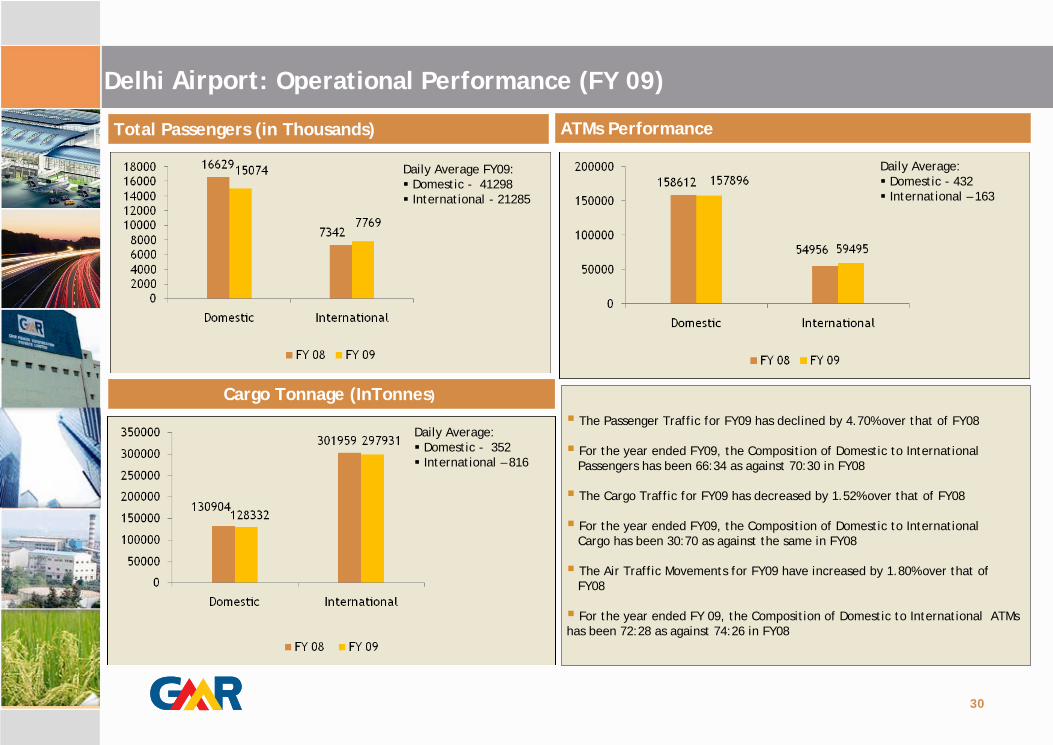

The Passenger Traffic for FY09 has declined by 4.70% over that of FY08

For the year ended FY09, the Composition of Domestic to International Passengers has been 66:34 as against 70:30 in FY08

The Cargo Traffic for FY09 has decreased by 1.52% over that of FY08

For the year ended FY09, the Composition of Domestic to International Cargo has been 30:70 as against the same in FY08

The Air Traffic Movements for FY09 have increased by 1.80% over that of FY08

For the year ended FY 09, the Composition of Domestic to International ATMs has been 72:28 as against 74:26 in FY08

Delhi Airport: Operational Performance (FY 09)

Daily Average FY09:Domestic - 41298International - 21285

Daily Average:Domestic - 432 International – 163

Daily Average:Domestic - 352International – 816

30

Total Passengers (in Thousands)Total Passengers (in Thousands) ATMs PerformanceATMs Performance

Cargo Tonnage (InTonnes) Cargo Tonnage (InTonnes)

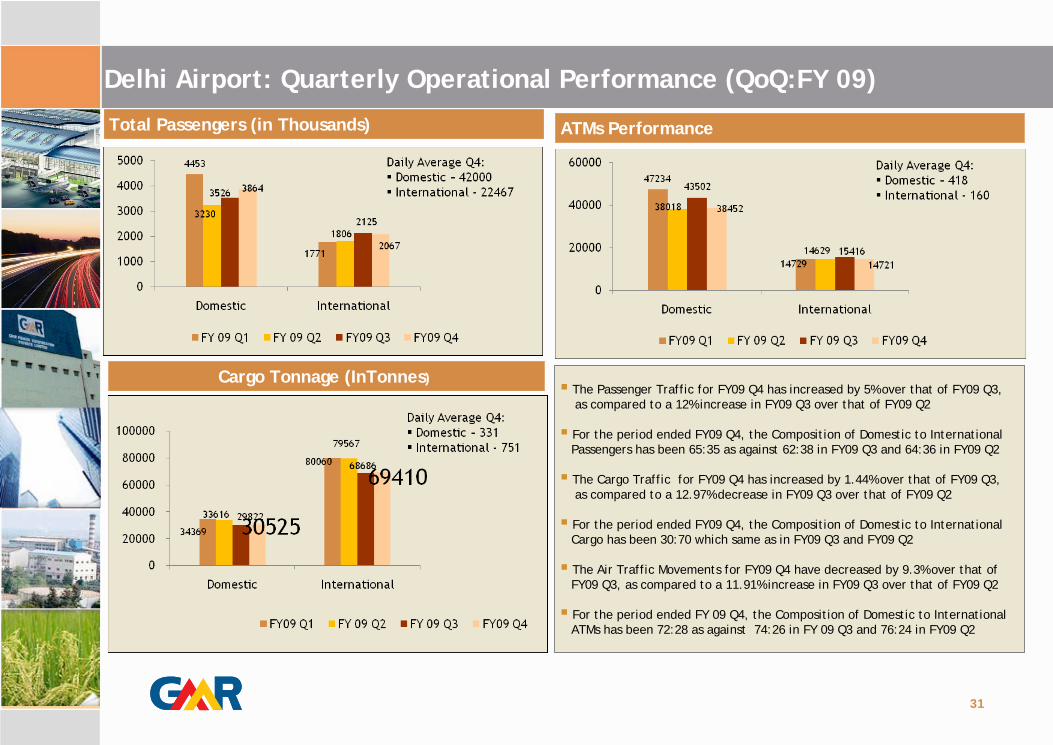

Delhi Airport: Quarterly Operational Performance (QoQ:FY 09)

31

The Passenger Traffic for FY09 Q4 has increased by 5% over that of FY09 Q3, as compared to a 12% increase in FY09 Q3 over that of FY09 Q2

For the period ended FY09 Q4, the Composition of Domestic to International Passengers has been 65:35 as against 62:38 in FY09 Q3 and 64:36 in FY09 Q2

The Cargo Traffic for FY09 Q4 has increased by 1.44% over that of FY09 Q3, as compared to a 12.97% decrease in FY09 Q3 over that of FY09 Q2

For the period ended FY09 Q4, the Composition of Domestic to International Cargo has been 30:70 which same as in FY09 Q3 and FY09 Q2

The Air Traffic Movements for FY09 Q4 have decreased by 9.3% over that of FY09 Q3, as compared to a 11.91% increase in FY09 Q3 over that of FY09 Q2

For the period ended FY 09 Q4, the Composition of Domestic to International ATMs has been 72:28 as against 74:26 in FY 09 Q3 and 76:24 in FY09 Q2

Commercial development at airport envisages development of an alternate commercial hub, right in the heart of NCR.

Master plan, by YRM & PF, details out a world class development comparable to the best & most sought after business districts in the world.

Location vis-a-vis the National Capital Territory would lend a dual advantage of extremely central location with effective connectivity and proximity to demand

Hospitality District, the first phase of development, would mainly constitute of hospitality assets across segments / categories & address the acute shortage of quality hospitality & conferencing facilities in NCR

Delhi Airport: Delhi Aerocity

IGI airport is spread over 5100 acres of land out of which 5% (250 acres) can be used for commercial development by DIAL

Land Bank to be divided into Multiple Land Parcels, which would be developed in a phased manner

~ 80% of our land bank is located next to NH-8, straddling across the main access to airport in form of large, contagious land parcels.

Land Bank Available at IGI, New DelhiLand Bank Available at IGI, New Delhi

Majority of Land Bank

NH 8

Gurgaon

Radisson

*LP = Land Parcel

Development Vision – Delhi AerocityDevelopment Vision – Delhi Aerocity

Hospitality District

Core Airport infrastructure

32

Delhi Aerocity – Phase I: Hospitality District

Hospitality District – HighlightsHospitality District – Highlights

33

First of its kind development with hotels from luxury to budget categories.

Multimodal connectivity through metro & expressway to NCR

Boasts of possibly the first Planned High Street of the country along a 800 m long landscaped, pedestrian walk way

Highly secure environment, integrated with airport security cover

Bid submission window closed on 15th December’ 08 and has attracted bids from reputed national & international hospitality players

Key Statistics

Metro station

Total Area Bid out: 22 acres (7 land parcels) to Hyatt, Accor, Lemon Tree, Dusit, Aria Hotels and Hyatt

Transaction Structure approved by AAI as follows:Annual License Fees to be quoted in Rs. Per Sq.Ft. with an Escalation of 5.5% year-on-year basisRefundable Security Deposit equivalent to 3 years average of the aggregateAnnual License Fees for the tenure of the Lease agreementsDeposits received:Upfront Lease Deposit – INR 5960 Mn ( 276 Mn per acre)Infrastructure Deposit - INR 2866 Mn (133 Mn per acre)

45 acres for Development (13 Asset areas)Total GBA (FSI) = 6.12 mn sft

Hospitality = 10 assets (5.04 mn sft)Commercial = 3 assets (1.08 mn sft)

Scope of Development

DIAL has been allowed additional eighteen usages catering from Commercial, Office to Residential which is incidental and supplemental to the airport usage.

Delhi Airport: Annual Financial Performance

INR mn 2009 2008 2007

Gross Revenues 9,477 8,706 5914

Aeronautical Revenues 3,421 3,219 2723

Non-Aeronautical Revenues 6,056 5,487 3191

Less: AAI Revenue Share 4,406 4,027 2720

Net Revenues 5,071 4,679 3194

Operating Expenses 4,444 3,748 2602

EBIDTA 627 931 592

Other Income 50 48 23

Interest and Finance Charges 494 5 101

Depreciation 525 91 39

PBT (342) 883 475

PAT (235) 567 293

Cash Profit 290 658 332

Cash Accruals 160 950 -

34

INR mn Q4 FY09 Q4 FY08

Gross Revenues 2,391 2,495

Aeronautical Revenues 866 818

Non-Aeronautical Revenues 1,525 1,677

Less: AAI Revenue Share 1,110 1,160

Net Revenues 1,281 1,335

Operating Expenses 1,156 1,177

EBIDTA 125 158

Other Income (20) 25

Interest and Finance Charges 258 2

Depreciation 232 37

PBT (385) 144

PAT (26) 7

Cash Profit 206 44

Delhi Airport: Quarterly Financial Performance

2304 2500

Gross Revenue

EBIDTA

Sabiha Gokcen International Airport at Istanbul in Turkey

Project OverviewProject Overview

36

Consortium Partners Consortium Partners Commercial PartnershipsCommercial Partnerships

Concession period of 20 years from May 2008 onwardsConcession Period 20 years (including construction period of 30

months*)

Concession Fee In lieu of revenue share, EUR1.93bn, to be paid in 20 years with no fee payable in first 3 years

Estimated capex Euro 451 millionsMeans of Finance Equity: €115; Debt: €336Airport Operations taken over on 1st May 2008

Financial Closure June 2008EPC Contractor GMR – Limak Joint VentureMaster Planner Ove Arup

F & B Contract H&CCarparks Self Operated

Cargo Warehouse Operations

System Logistics

Ground Handling Operations

Operated by subsidiary

Duty Free Business Setur, KOC Group

Construction of New Terminal Building

GMR – Limak Joint Venture

Sponsor Shareholding

40%

40%

20%

Capacity Expansionto

25 million Paxto be completed

byend 2009

Project FeaturesProject Features

International Terminal- Enclosed Area 20,000 sqm

Domestic Terminal- Enclosed Area 3,500 sqm

Capacity 6.0 mnCargo Terminal

- Enclosed Area 7,500 sqm-Capacity 145,000 tons- Cold air rooms 5Nos

Runways and Parallel Taxiway45 m x 3,000 m

Apron Parking Capacity 44 Planes

67% Capital Work in Progress achieved as on 30th April 2009

Total Passengers (in Thousands)Total Passengers (in Thousands)

Air Traffic MovementsAir Traffic Movements

Sabiha Gokcen International Airport: Operational Performance

37

2563

1229

2790

1569

0

500

1000

1500

2000

2500

3000

Domestic International

2007

2008

23811

15944

25731

19007

0

5000

10000

15000

20000

25000

30000

Domestic International

20072008

The Passenger Traffic for FY 08 has increased by 15% over that of FY08

For the year ended FY08, the Composition of Domestic to International Passengers has been 64:36 as against 68:32 in FY07

The Air Traffic Movements for FY08 have increased by 12.52% over that of FY07

For the year ended FY 08, the Composition of Domestic to International ATMs has been 58:42 as against 60:40 in FY07

Daily Average CY 08:Domestic – 7644International - 4300

Daily Average CY 08:Domestic – 71International - 52

Total Passengers (in Thousands)Total Passengers (in Thousands) ATMs PerformanceATMs Performance

The Passenger Traffic for CY09 Q1 has increased by 29% over that of CY08 Q1.

For the period ended CY09 Q1, the Composition of Domestic to International Passengers has been 72:28 as against 67:33 in CY08 Q1.

The Air Traffic Movements for CY09 Q1 has increased by 7% over that of CY08 Q1.

For the period ended CY 09 Q1, the Composition of Domestic to International ATMs has been 84:16 as against 64:36 in CY 08 Q1 and 61:39 in CY08 Q1

38

Sabiha Gokcen International Airport: Operational Performance

807

314

Development plan for the Sabiha Gokcen International Airport in IstanbulDevelopment plan for the Sabiha Gokcen International Airport in Istanbul

Sabiha Gokcen International Airport

38

Car Park

NewTerminal

Hotel

VIP

Existing Terminals

Sabiha Gokcen International Airport: Future Business Prospects

Key Development Opportunities

0

20

40

60

2009 2015 2027

3.33 5.1713.44

3.049.42

29.28

6.37

14.59

42.72

Passenger Traffic (in Mn)

Domestic International Total

0

100

200

300

400

2009 2015 2027

30 47

111

2573

207

55

120

318Air Traffic Movements (‘000)

Domestic International Total

39

Catchment Population

Istanbul’s Anatolian side has its own population of 5-6 Mn

Industrial and Residential areas like Kocaeli, Bursa and Izmit around the airport has a 20 Mn plus population

Techno park (90 hectares) and conference/Hotel facilities (20 acres) would contribute to the traffic

Racing F1 track in the vicinity has been a major attraction for the past 2 years coupled with stress on tourism

Takeoff Prospects

Ataturk Airport (the other Istanbul Airport) caters to 149 destinations compared to 64 by SGIA leaving good scope for newer routes

Ataturk is constrained by capacity leading to delays

Quick turnaround and no slot restriction

SGIA is best positioned to handle its catchment area and spillover from AtaturkMajor international destinations in Germany, UK, Scandinavia, Russia and CIS countries would contribute to growth as many turk migrants reside over there, besides tourist traffic

Sabiha Gokcen International Airport: Turkey Overview

40

Turkey’s Economic Overview

15th largest economy and among the top ten emerging markets

Total population of about 73 million with nominal GDP of about USD 657 bn (2007)

Istanbul has a population of about 14 Mn with 35% residing on the Anatolian side

Turkey’s Aviation Sector

Passenger traffic growing at 25% plus per annum since 2003 fuelled by Low cost Carriers.

Turkey comprises of 52 Airports having the State Authority responsible for operations

Tourist Traffic to Turkey is about 23 Mn pax (5.5 Mn pax from Istanbul in 2007)

The Annual Passenger Traffic in Turkey has been 66 Mn pax (Domestic – 29 Mn and International 37 Mn – CAGR 15%

Gross Revenue

EBIDTA

SGIA : Financial Performance

41

INR mnINR mn FY09*

Gross Revenues 2,669

Aeronautical Revenues -

Non-Aeronautical Revenues 2,669

Less: Revenue Share -

Net Revenues 2,669

Operating Expenses 2,573

EBIDTA 96

Other Income (67)

Interest and Finance Charges 14

Depreciation 394

PBT (379)

PAT (319)

Cash Profit 75

* 40% share of GIL

Outline of Emerging Opportunities in Airports Sector in India

Addition of Fleet Size in IndiaAddition of Fleet Size in India

42

Category Numbers

International 16

Major Domestic 22

Custom 8

Other Domestic 74

Total 120

Airport Categorization in IndiaAirport Categorization in India

Airport Infrastructure DevelopmentAirport Infrastructure Development

•The XI plan targets Infrastructure spend of USD 8bn on Airports

•

Total No. of Airlines Operating in India: 71,Domestic: 11, International: 60

•

Delhi, Hyderabad, Bangalore and Mumbai airport have already been

privatized

•

Kolkata and Chennai are being developed by AAI

•

35 non-metro airports are under the AAI’s up gradation plan

•

Airports Economic Regulatory Authority of India Act, 2008 has come into

force w.e.f. 01.01.2009

•

Development of Merchant Airport Policy is under consideration

Presently, the various airlines are operating only through 61 airports. The remaining are lying unutilised, at best handling occasional aircraftoperations.Out of the International Airports 12 are with AAI, 5 are under Joint Venturesand 2 are Greenfield Airports

Airlines Operating in IndiaAirlines Operating in India

Key Investment Highlights

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

Operational Power Projects

GMR Energy Limited

GMR Power Corporation Pvt. Ltd.

Vemagiri Power Generation Ltd.

Facility Mangalore, Karnataka Relocation Plan

Contracted Capacity 220 MW (235 MW post conversion) Barge-mounted power plant would be converted to gas fired power plant & relocated to Kakinada (AP) from Jan 2010Expected to be operationalized by March, 2010EGoM has cleared Gas allocation for 70% of plant requirement from KG Basin

Fuel Naptha

COD 2001

PPA 7yr PPA finished in 2008; currently merchant operation

Facility Chennai, Tamil Nadu Strengths

Contracted Capacity 200 MW GMR Energy holds 51% stakeISO 14001 and OHSAS 18001 compliantDr. M.S. Swaminathan Award for being an environment friendly project

Fuel Low Sulphur Heavy Stock

COD 1999

PPA15 Years till 2014; minimum offtake at 68.5% PLFTake or pay fixed charges

Facility Vemagiri, Andhra Pradesh Strengths

Contracted Capacity Contracted –

370 MW (Installed Capacity

–

388.5MW)PPA with APTRANSCO is being amended for selling 20% of contracted capacity (74 MW) on Merchant Basis and for reducing PPA tenure to 15 years.Gas Sale & Purchase Agreement executed with RIL and Gas being supplied from KG Basin since April 2009

Fuel Natural Gas

COD 2006

PPA23 Years at 80% PLF Take or pay of fixed

charges

43

Facility Kamalanga Chhattisgarh Vemagiri (Expansion)

Location Orissa Raipur Andhra Pradesh

Capacity 1,050 MW (3 X 350 MW) 1,200 MW 740 MW

Fuel Coal Coal Natural Gas

Type of Project BOO (MoU with Govt of Orissa) BOO (MoU with Govt of Chhattisgarh) BOO

Expected CoD 2012 2013 2012

Land Acquisition

Total Land required for the project is 1,105 acres. The land acquisition is expected to be acquired by June/July 2009.Rs. 600 Mn has been deposited with Industrial Development Corporation of Orissa for acquisition of Private Land

State Govt has granted approval for 1050 acres of land of which 200 acres of private land have been acquired.Further land would be acquired by end-July 2009.

Adequate land available for expansion in existing VPGL plant facilities

Fuel Supply Arrangement

Coal linkage of 500 MW obtained from Mahanadi Coal Fields. Tapering coal linkages for balance 550 MW has been approved112 mn MT coal from Rampia & Dip Side Rampia coal block allocated to GMR Energy.

State Govt. has recommended to the Ministry of coal for coal linkage.

Representation made to Ministry of Petroleum and Natural Gas for gas allocation

Power Off-take arrangement

PPA with GRIDCO for 25% power and remaining to PTC PTC entered in agreement with Haryana for 300 MWPlan to sell 20% power on Merchant basis

Plan to sell power through mix of long term PPA & merchant powerPPA with CSEB which has right to purchase upto 30% power during first 20 yearsPlan to sell 30% power on Merchant basis

Plan to sell 100% power on merchant basis

Environmental Clearance

Environment & pollution clearance obtained Presentation made to MoEF. Final approval expected by August 2009.

Terms of Reference for conducting EIA has been approved by MoEF

Project status

Financial Closure achieved for outlay of US$950 Mn EPC contract awarded to SEPCO, China in Sept 2008Department of Water Resources has allocated 30 Cusecs of water from River Brahamini.

Implementation Agreement signed with Govt. of Chhattisgarh.GoC has principally agreed to allocate 32 MCM from river Mahanadi.Notice Inviting Tenders released for BTG and BOP. Offers received and are under evaluation.

DPR prepared by Tata Consulting Engineering LtdNotice Inviting Tenders on ICB basis have been published.Award of EPC expected by August, 2009.

Pipeline of Power Projects Under Development

Power Assets Under DevelopmentPower Assets Under Development

44

Pipeline of Power Projects Under Development

Power Assets Under DevelopmentPower Assets Under Development

Facility Alaknanda Talong Bajoli Holi Upper Karnali Upper Marsyangdi

Location Uttaranchal Arunachal Pradesh Himachal Pradesh Nepal Nepal

Capacity 300 MW 160 MW 180 MW 300 MW 250 MW

Type of Project

Run of River on BOOT basis for 45 years from Implementation Agreement

Run of the River on BOOT basis for a concession period of 40 years from COD

Run of the River on BOOT basis for a concession period of 40 years from COD

Run of the River BOOT basis for concession period of 30 years from Generation License

Run of the River BOOT basis for concession period of 30 years from Generation License

Expected COD 2013 2014 2015 2015 2015

Land Acquisition

Land requirement is approx. 200 Acres and land acquisition is in progress

Approx. 850 acres land required Acquisition will start after DPR and MoEF clearance

Land requirement is 120 acres

Permanent Site establishment is in place

Permanent Site establishment is in place

Power OfftakePlan to have short term PPA with states in North India

Plan to have short term PPA with states in North India

Plan to have short term PPA with states in North India

Plan to export Power to sell on short term PPA to states in North India

Plan to export Power to sell on short term PPA to states in North India

Environmental Clearances

Final clearance obtained form MoEF in Mar 2008No R&R issues

Terms of Reference for Environment study approved by MOEF No R&R issues envisaged

Terms of Reference for Environment study approved by MOEFNo R&R issues envisaged

Environmental clearance expected by Nov 2010

Project statusDPR approved by CEAAppointed E&Y as consultant for CDMTender for main civil works floated and bids received are under evaluationFinancial Closure expected by March 2010.

AF Colenco of Switzerland has been appointed as the principal engineer. DPR has been preparedHydrological Studies have been submitted to CEA.

SNC– Lavalin acting as Principal Engineer and ConsultantDPR is being prepared.Financial Closure expected by Mar 2011

DPR is being preparedSchEMS appointed as EIA consultantsInitial review indicate that the project capacity can be increased to 900 MW with total annual energy of 4,052 MU

DPR is being prepared.Coyne-ET-Belliar appointed as DPR ConsultantsSchEMS appointed as EIA consultantsInitial review indicate that the project capacity can be increased to 560 MW with total annual energy of 2,476 MU

45

7,023 MW of power projects spread across the country7,023 MW of power projects spread across the country

Operating assets3 Projects(823 MW)

Under implementation/ Development10 Projects(6,200 MW)

Bajoli Holi180 MW

HydroAlaknanda300 MW1

Hydro

Orissa1,050 MWFuel type - Coal

Chattisgarh1,200 MW

Fuel Type : Coal

Vemagiri388 MWFuel type – Gas

Chennai200 MWFuel type – Sulphur

Mangalore235 MW

Fuel type – Naphtha

Upper Karnali300 MWHydro

Upper Marsyangdi250 MWHydro

Vemagiri Expansion740 MWFuel type – Natural Gas

Coastal Power Plant – Gujarat1320 MW

Fuel type - Coal

Coastal Power Plant – Andhra Pradesh700 MWFuel type - Coal

Project Pipeline (Gross Capacity MW)Project Pipeline (Gross Capacity MW)

Talong 160 MWHydro

GMR Energy : Overview of Power Assets

46

GMR acquired 33.5% stake for US$ 30 Mn on February 23, 2009HEG is having coal mines in South Africa with interest in Uranium explorationHEG investments include a 39% stake in Homeland Uranium with assets in Niger & USA and an 8% stake in Altona with coal assetsin Australia

HEG owns Mining License for

–

Kendal (74%, total mineable reserve 25 mn tons),

–

Eloff (50% with an option to increase to 74% for US$ 15 mn, total reserve 259-275 mn ton)

–

Northfeild (100% share – 1 mn ton) Annual steady rate run on mine production from

–

Kendal expected to be 1.8 mn ton

–

Eloff expected to be 12 mn ton

–

Northfield expected to be 0.3 mn tonPre-feasibility report on Eloff Project prepared by Exxaro, SA and Validated by Norwest, USAJORC standard certified resource & reserve and feasibility reports completed and mining application has been made.Plan to sell coal in spot market at mine gate to global players like Glencore

Acquired 100% stake for ~ US$ 80 mn (Staggered payment linked to start of production)

Entity has Coal Contract of Works (CCoW) license (given by federal Govt. and approved by the Parliament), has highest degree of certainty and gives mining rights of 30 years from date of issuance

Mine has resources of 288 mn ton and mineable reserves of 104 mn tons

Development period to be 2 years

Annual steady state run on mine production expected to be 6 mn ton (Life 19 Years)

Plan to export coal to India

Coal mined is expected to hauled by Road to Barge loading facility on Musi River

Crushed coal from this facility to be loaded on barges

Barges are expected to transport coal for ~320 kms to trans shipment point where the coal will be loaded on Capesize ships

Towards Securing fuel supply for Power Plants

Indonesia coal mine Homeland Energy Group(HEG)

Based on Imported Coal, planned 2020 MW Coastal Projects including 1320 MW in Gujarat and 700 MW in Andhra Pradesh

47

Power Projects: Strategy to Transform itself into an Integrated Power Producer in India

Leverage expertise to capture future growth opportunities

Diversify into allied power infrastructure businesses

1 2

Add further power assets diversified across fuel types in India.

Bid for UMPPs where fuel supply has been secured.

Invest in IPPs in neighboring developing countries with

Need for infrastructure expansion

Government support

Explore brown field opportunities through acquisitions of development rights and operating assets.

Actively explore opportunities in domestic power distribution.

State of Gujarat, Karnataka & Maharashtra have initiated private participation.

Evaluate power transmission opportunities in India.

Explore Joint Ventures and/or acquisition to realise value.

Explore options for alternate fuel to reduce reliance on any one type of fuel.

In discussion with Companies from Spain and Turkey to venture into the Solar Energy Business in India.

48

GMR Power Assets: Annual Financial Performance

49

INR mn 2009 2008 2007 2006

Gross Revenues 21,527 15,530 12,981 10,225

Contracted 20,207 15,530 12,981 10,225

Merchant 1,320 0 0 0

Net Revenues 21,527 15,530 14,029 10,107

Operating Expenses 16,186 12,031 8,915 5,836

EBIDTA 5,341 3,499 5,114 4,271

Other Income 114 511 128 4

Interest and Finance Charges 955 1,065 1,549 995

(Gains)/loss on FE Fluctuation - - -4 4

Depreciation 1,172 1,175 2,578 1,979

PBT 3,328 1,770 1,119 1,297

PAT 3,045 1,585 893 1,172

Cash Profit 4,217 2,760 3,467 3,155

Cash Accruals 1,990 -1,440

GMR Power Assets: Quarterly Financial Performance

INR mn

INR mn Q4 FY09 Q4 FY08

Gross Revenues 6,528 6,281

Contracted 5,598 6,281

Merchant 930 -

Net Revenues 6,528 6,281

Operating Expenses 5,450 5,230

EBIDTA 1,078 1,051

Other Income 2 106

Interest & Finance Charges 243 309

Depreciation 283 380

PBT 554 468

PAT 476 534

Cash Profit 760 916

Gross Revenue

EBIDTA

50

Huge Capacity additions have been planned in power generation in 11th Five Year Plan to the tune of 79 GW as against 135 GW currently installed.

Total investment opportunity of about US$ 150 billion over a 5 year horizon

De regulated power sector to contribute about 40% of additional capacity by 2012

Hydel power potential of 150,000 MW is untapped as assessed by the Government of India

Future Outlook of Power Sector

Source: UNDP, Human Development Indicators,2006 ; CEA and Crisil Research Power Annual Review 51

Low

Con

sum

ptio

n pe

r ca

pita

Per Capita Consumption in India is extremely low as compared to other countries

Capacity Additions Expected

Mega Watts (In 000’s)

Scope for Public Private Participation

Installed Capacity Breakup FY09 (Total Capacity = 148 GW)

Per Capita Consumption (Thousand Kwh/ year)* Renewable Energy Solutions (Ministry of New & Renewable Energy)

Coal Gas Diesel Nuclear HydroRES

(MNRE)

State 43 4 1 0 27 2

Private 5 5 1 0 1 11

Central 30 7 0 4 9 0

Total 78 16 2 4 37 13

Demand-Supply Gap to Catalyze Growth

Historically Capacity Addition has not kept pace with Demand, Leading to Significant Shortages

(1) Ministry of Power

Demand-Supply Gap Aggravated as Capacity Addition by Government has been far below Planned Targets and

Limited Involvement of Private SectorHistorically Characterized by Huge Energy Shortages(1)

52

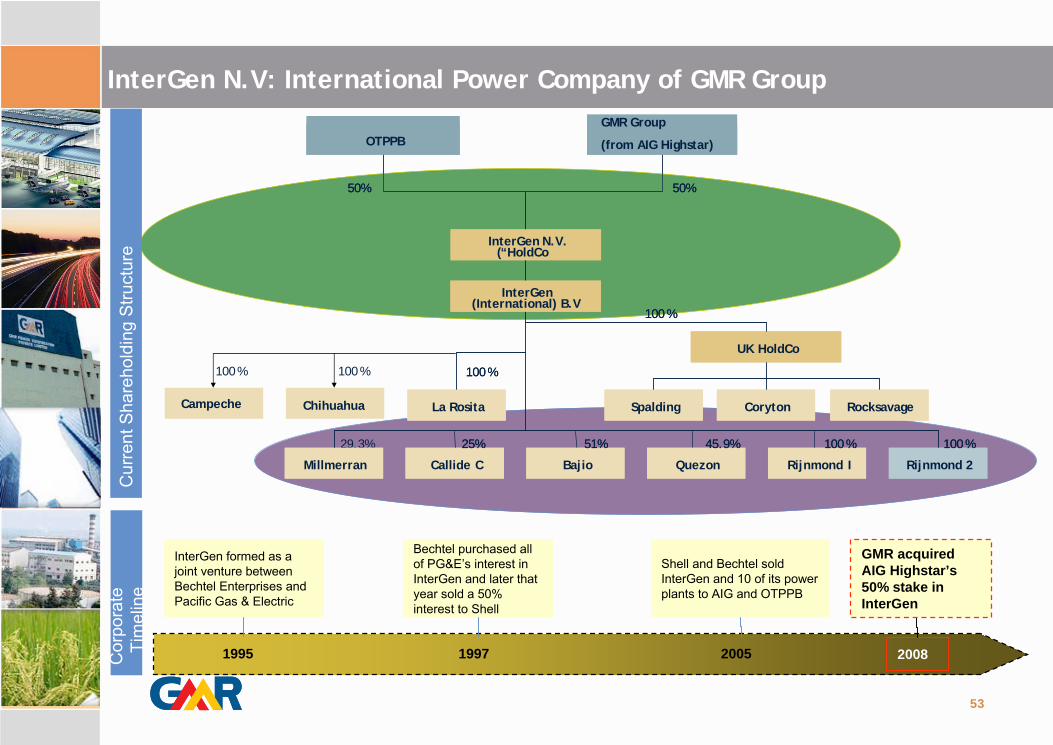

InterGen N.V: International Power Company of GMR Group

50%

OTPPB Highstar

29.3%

UK HoldCo

Coryton RocksavageSpaldingLa Rosita

Millmerran Rijnmond

50%

InterGen N.V.(“HoldCo

InterGen(International) B.V

Callide C Bajio Quezon Rijnmond I

100 %

100 %

25% 51% 45.9% 100 % 100 %

50%

OTPPBGMR Group

(from AIG Highstar)

UK HoldCo

Coryton RocksavageSpaldingLa Rosita

Millmerran Rijnmond 2

50%

InterGen N.V.(“HoldCo

InterGen(International) B.V

Callide C Bajio Quezon Rijnmond I

100 %

100 %

25% 51% 45.9% 100 % 100 %

ChihuahuaCampeche

100 %100 %

InterGen formed as a joint venture between Bechtel Enterprises and Pacific Gas & Electric

Bechtel purchased all of PG&E’s interest in InterGen and later that year sold a 50% interest to Shell

Shell and Bechtel sold InterGen and 10 of its power plants to AIG and OTPPB

1995 1997 2005 2008Cor

pora

te

Tim

elin

e

GMR acquired AIG Highstar’s 50% stake in InterGen

Cur

rent

Sha

reho

ldin

g St

ruct

ure

53

Operating assets■Rijnmond

820 MW

(100%)Assets in construction■Rijnmond II

428 MW(100%)Total 1,248 MW

Netherlands

Operating assets■Quezon

460 MW (45.87%)

Total 460 MW

Philippines

Operating assets■Millmerran

850 MW

(29.3%)

■Callide

920 MW

(25%)

Total 1,770 MW

Australia

Operating assets■Bajio

600 MW

(51%)

■La Rosita

1,100 MW

(100%)

■Campeche facility

252 MW

(100%)

■Chihuahua facility

259 MW

(100%)

Total 2,223 MW

Also includes Libramiento pipeline

Mexico

Operating assets■Rocksavage

748 MW

(100%)

■Coryton

777 MW

(100%)

■Spalding

860 MW

(100%)

Total 2,385 MW

United Kingdom

PhilippinesMexico

Australia

U.KNetherlands

Operating assets

7,658 MWAssets in construction

428 MWTotal 8,086 MWInterGen Equity

6,231 MWGMR Equity 3,116 MW

InterGen Net Capacity (net of aux)

1

Diagram legend

■CCGT

■ Coal

Details of InterGen N.V International Power Assets

C

C Contracted

54

C

C

C

C

C

C

C

C

InterGen has 7658 MW of Assets under Operation with another 428 MW under constructionInterGen also has a current development pipeline of 2,849 MW

• Opportunities in India are slow to materialise

• Competition getting fiercer at home

• Significant growth opportunities in markets overseas

• GMR has the distinctive development skills needed in emerging markets

Avenue for Growth Portfolio Diversification

• Spread risk exposure across geographies

• GMR feels a clear need for pure breed entrepreneur -

developer

Group Profile

• Aim to be well known brand, in global top 10 in key sectors

Learn from other more Skilled Markets

• Bring back new approaches and technology from global exposure

•

Exposure to nuclear technology, getting coal from overseas etc.

Access to International Talent

• Attract talent s, who do not to want to move to India

• Provide international opportunities for Indian staff

Access to International Capital

• Ability to raise capital internationally

• Desire to list on e.g., London Stock Exchange

GMR’s International

aspiration is to achieve $10b assets under

management in 5 years

InterGen N.V: Strategic Rationale & Value Proposition

Going Global complements GMR through de-risking its Portfolio, Leveraging its Partnership and its fFinancial acumen

55

Portfolio of existing assets - high quality and location in attractive markets

Strong development pipeline

International IPP market surging due to requirements for new generation capacity

Recognised management team (unique opportunity to get a team with international experience and solid track record in project development and asset operation)

Unique opportunity to develop/ acquire skills (merchant, tolling, contracted plants)

Leverage/ capitalise on GMR Group’s & InterGen teams combined capabilities to expand through building new generation capacities and replacing other ageing plants

InterGen N.V: Fits well with GMR’s Strategic Intent…

…acquisition elevates GMR to be a Global Power Generatorand elevates GMR as the largest private sector power developer in the country

56

Neil H Smith (President & Chief Executive Officer)

— Lead responsibility for development, financing, construction, operations of all InterGen projects

— Bachelor of Science in Political Science from Emory University; MBA from Harvard Business School

Tim Menzie (Chief Operating Officer)

— Responsibilities include directing all the operations and commercial management activities

— Bachelor’s degree in Business Administration from Westfield State College and Masters of Science in Taxation degree from Bentley College.

Martin Rees (Chief Financial Officer)

— Directs InterGen’s project finance, corporate finance, financial reporting, tax, treasury and information technology functions

— BA in accounting from University of Kent; member of Association of Corporate Treasurers

Susan E Gonzalez (General Counsel)

— Responsibilities include general legal services, compliance, risk management, M&A support

— BA from University of Michigan; Juris Doctor degree from Suffolk University; Certificate in Comparative Law from University Jean Moulin in Lyon, France

Professionally managed Company with strong internal controls and processes

1

2

InterGen N.V: Management Team

57

Equal representation to both OTPPB and GMR

Management is exercised through two bodies:Supervisory Board— 10 members— Equal representation by OTPPB and GMR— Veto rights to both parties on key

decisionsManagement Board— 4 members— OTPPB and GMR have right to nominate 2

members each

Day-to-day operations are run by the Management Board

All key decisions, including key appointments, investment decisions, borrowings etc, decided by the Supervisory Board

InterGen has a strong and well qualified management team in place

— Hands-on management team, very well perceived in the market

— Strong development pedigree – “grown up” in industry from developers (J Makowski, Calpine)

— 600 employees

InterGen N.V: Key Financials (CY2008)

(1) Revenue stated is before MTM Deduction(2) Revenue Consists of only Tier I plants

(3) Proportionate & Adjusted EBITDA

(USD Mn) CY 08 CY 07

Generation 31,8 GWh 30,9 GWh

Revenue(2) 1397 1113

EBIDTA(3)– Tier I 429 407

EBIDTA(3)

– Tier II 214 243

Corporate & Development

(39) (35)

Consol EBIDTA(3) 604 615

58

Key Investment Highlights

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

All road projects commissioned on schedule

Particulars GTAEPL GTTEPL GACEPL GJEPL GPEPL GUEPL* GHVEPL

Location Tuni-Anakapalli Tambaram- Tindivanam

Ambala-Chandigarh Faruknagar- Jadcherla

PochanpalliTindivanam- Ulundurpet

Hyderabad –

Vijayawada

Road Length 59 kms 93 kms 35 kms

Construct - 46 kms + O&M

Sweetener - 12 kms

Construct - 86 kms + O&M Sweetener

- 17 kms

Construct - 73 kms

Construct –

181 kms

Concession Period

17.5 years incl. construction period

of 2.5 yrs.

17.5 years incl. construction

period of 2.5 yrs.

20 years incl. construction period

of 2.5 years

20 years incl. construction period of 2.5

years

20 years incl. construction

Period of 2.5 years

20 years incl.

Construction Period of 2.5

years

25 years from

Date of

appointment

Concession Duration

May. 2002 – Nov. 2019

May. 2002 – Nov. 2019

May. 2006 – May. 2026

Aug. 2006 – Aug. 2026

Sep. 2006 – Sep . 2026

Oct. 2006 – Oct. 2026

-

Project Cost(Rs.Mn)

3040 3900 4985 4713 6900 795022,000

(Approx.)

Financial Closure

June 2002 June 2002 May 2006 August 2006 September 2006 October 2006 -

Commercial Operation Date

Oct 2004 Oct 2004 Nov 2008 Feb 2009 March 2009 Apr 2009 -

Concession Type

Annuity Annuity Toll Toll Annuity Toll Toll

CompletedUnder

Construction

Road Projects

59

* Construction completed , will commence commercial operational shortly

Short listed for submission of Price Bid ( 658 Kms)

RFQ Applications have been submitted for the following projects:

Project Kms Est.Cost RsM

Jaipur – Tonk – Deoli 149 7,290

Chennai ORR 30 8,640

Samikhali – Gandhidham 56 8,050

Udaipur - Ahmedabad 243 25,450

Total 478 49,430

Project Kms Est.Cost RsM

Gandhidham – Mundra Port 71.40 10,310 Ahmedabad – Godhra 117.60 10,250 Godhra – Guj / MP Border 83.85 7,470Haridwar – Dehradun 37.40 4,900Hungund – Hospet 97.89 10,470Kishangarh – Udaipur 315.00 25,340Krishnagiri – Walahjpet 148.00 12,500Rohtak – Bawal 82.53 6,690Hyderabad – Bangalore 22.11 4,500Bijapur – Hungund 97.22 8,580Chengapalli – Kerala/TN Border 55.00 8,520Pune – Satara 142.35 17,250Tumkur – Chitradurga 114.00 8,500Total 1,384.35 1,35,280

Leveraging expertise to explore Opportunities across Land Transportation Sector

60

Road Assets: Glimpses

Jadcherla Road

Ulundurpet Road Pochanpalli Road

Ambala – Chandigarh Road (Completed)

61

Roads Sector: Significant Opportunity for Private Sector Participation

India has one of the largest Road Networks in the World India has one of the largest Road Networks in the World

Source: Report of the Core Group on the Financing of the National Highway Development Program

Total length = 3.3 million km

2% 4%14%

80%

National Highways

State Highways

Major district roads

Rural & other roads

Supportive Regulatory FrameworkSupportive Regulatory Framework

Government will carry out all preparatory work including land acquisition and utility removal .

Right of way (ROW) to be made available to concessionaires free from all encumbrances.

NHAI / GOI to provide capital grant up to 40% of project cost to enhance viability on a case to case basis

100% tax exemption for 5 years and 30% relief for next 5 years, which may be availed of in 20 years.

Concession period allowed up to 30 years

Arbitration and Conciliation Act 1996 based on UNICITRAL provisions.

In BOT projects entrepreneur are allowed to collect and retain tolls

Duty free import of specified modern high capacity equipment for highway construction.

FDI up to 100% in road sector

62

Current status of Road network in IndiaCurrent status of Road network in India

National highways constitute only 2% of road network but carry ~40% of the total road traffic

Vehicle traffic has been growing at a pace of 10% per annum over the last 5 years

The roads and highways in India account for about 80 per cent of the total passenger traffic and about 60 per cent of the total freight traffic in the country

The government has embarked on the ambitious National Highway Development Project covering 13,000 km with a cost of Rs.54, 000 crore.

Roads Sector: Significant Opportunity for Private Sector Participation

NHDP has planned expenditure of ~USD 55bnNHDP has planned expenditure of ~USD 55bn

20,000km10,000km13,146km 6,500km 1,000km N/A

Opportunity for Private Sector Participation worth $23bn (08-12E)Opportunity for Private Sector Participation worth $23bn (08-12E)

Total=USD 55bn

58%42%

Private sector contribution Contribution from other sources

NHDP Phase I GQ (5,846 km) and NS-EW Corridor (981km)

NHDP Phase II NS-EW Corridor (6,161 km) and other National Highways of 486 km length.

NHDP Phase-IIIUpgradation and 4 laning of 4,035 km of National Highways. upgradation and 4 laning of 8074 km

NHDP Phase-IVUpgradation of 2000 Km of Highways into 2 lane highways

NHDP Phase V Six laning of 6,500 km of existing 4 lane highways includes 5,700 km of GQ and other stretches.

NHDP Phase VI 1000 km of expressways

NHDP Phase VII700 km of Ring Roads, Bypasses and flyovers and selected stretches

Phase wise Scope of NHDP Phase wise Scope of NHDP

Phase wise StatusPhase wise Status

63

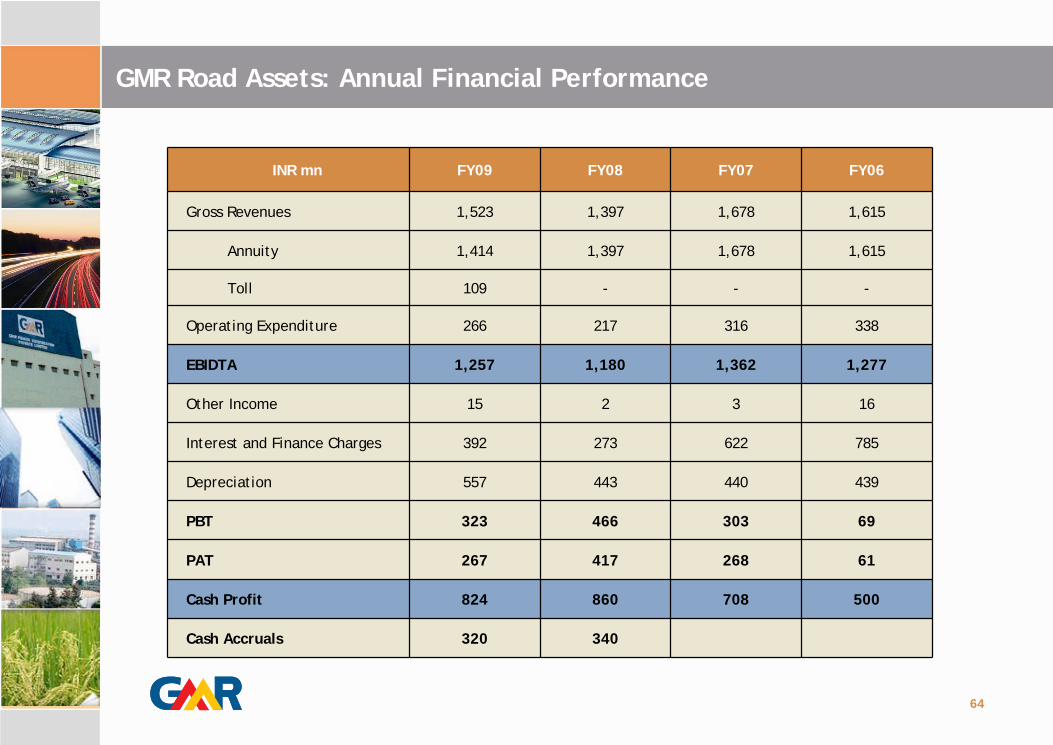

GMR Road Assets: Annual Financial Performance

INR mn FY09 FY08 FY07 FY06

Gross Revenues 1,523 1,397 1,678 1,615

Annuity 1,414 1,397 1,678 1,615

Toll 109 - - -

Operating Expenditure 266 217 316 338

EBIDTA 1,257 1,180 1,362 1,277

Other Income 15 2 3 16

Interest and Finance Charges 392 273 622 785

Depreciation 557 443 440 439

PBT 323 466 303 69

PAT 267 417 268 61

Cash Profit 824 860 708 500

Cash Accruals 320 340

64

GMR Road Assets: Quarterly Financial Performance

INR mn

INR mn Q4 FY09 Q4 FY08

Gross Revenues 464 349

Annuity 365 349

Toll 99 -

Operating Expenditure 70 45

EBIDTA 394 304

Other Income 10 1

Interest & Finance Charges 178 55

Depreciation 179 111

PBT 47 139

PAT 34 125

Cash Profit 213 236

Gross Revenue

EBIDTA

65

Krishnagiri Special Economic Zone: Recent Foray

Entire land of 3300 acres has been Identified

1500 acres of Land acquired

Balance 1800 acres of Land acquisition is in progress

Free from homestead, minimal Relocation & Rehabilitation.

Project Overview Land Acquisition by end of the current FY

Final Notification of SEZ

Completion of Development Plan for covering:

(a) Master Plan and Infrastructure Plan

(b) Business Plan

(c) Demand Assessment

Preparation of Detailed Project Report

Planned Action for next 12 months

66

Setup a Construction Division Team of 124 personnel to mitigate execution risks

Bangalore

Krishnagiri

Location advantages A Strategic Location with distinct Comparative Advantages

Targeted Industries

67

Krishnagiri Special Economic Zone: Locational Advantages

Industrial Legacy because of proximity to Hosur Town which is an automobile hub

Developed Infrastructure by way of Power supply, connectivity etc.

Forward & Backward Linkages due to proximity to Bangalore.

Availability of skilled human resources due to traditional engineering & textile workers pool.

New Technology IndustriesWind Power, Solar Thermal Systems, Photo Voltaic Systems, Aircraft Part Manufacturing.

Knowledge IndustriesIT & ITES, Contract Manufacturing, Nanotechnology, Bioinformatics, Clinical Trials, Health Tourism, Manufacturing & Drug discovery.

Traditional IndustriesAuto & Auto Components, Processed Foods, Light Engineering, Floriculture, Plastics, Garments, Electronics, Logistics.

Key Investment Highlights

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

GMR Infrastructure: Board of Directors

GM Rao

Group Chaiman

Srinivas Bommidala

Chairman - Urban Infrastructure & Highways

GBS Raju

Chairman – Corporate & International Business

G Kiran Kumar

Chairman - Airports

B V N Rao

Chairman – Energy & Agro

GMR Holding BoardGMR Holding Board

K. Balasubramanian

Member Group Holding Board

GMR Infra BoardGMR Infra Board

G. M. Rao

Srinivas Bommidala

G. B.S. Raju

G. Kiran Kumar

B.V. Nageswara Rao

K.Balasubramanian

O B Raju

Arun K. Thiagarajan

K.R. Ramamoorthy

Prakash G. Apte

R.S.S.L.N. Bhaskarudu

Udaya Holla

Uday M. Chitale

P M Kumar

Executive Director,

GMR Holdings Board

68

DIALDIAL

Energy SectorEnergy Sector

Urban Infrastructure & Highways SectorUrban Infrastructure & Highways Sector

Raajkumar, CEO

K V V Rao, Director & President

G.Subba Rao, President Hydro Energy

Ashish Basu, EVP–Commercial & Contracts

R. K Goel, Project Director-Transmission

S N Barde, EVP–O & M

Avinash R Shah, EVP-Business Development

O.B.Raju , MD & CEO-Highways

V Jayaraman, COO–Property Development

Gopala Krishna Kishore, COO-SEZ

D.R Santhana Krishna, CFO - Highways

Kamalakararao Y, CFO-SEZ & Property

P.S. Nair, CEO

Andrew Harrison, COO (T 3 Terminal)

Peter Noyce – COO (T1 & T2 Terminal)

I Prabhakara Rao, CEO-&EVP Airport Development

Gavin Makechnie, Chief Commercial officer

M.S.Narayanan, Head- Finance

A.S.K. Reddy – Head, HR

Ranjit Murugason, CEO

Madhu Terdal, COO

Cenk Alpsoy– CEO, Turkey

Quek Peng Ng, Head – South East Asia

Dean Marks – Head, HR

International Business DevelopmentInternational Business Development

Corporate ServicesCorporate Services

69

GHIALGHIAL

P. Sripathy, CEO

Rajinder Jalpuri, Deputy, COO

A. Vishwanath, Chief Commercial Officer

G.R.K Babu, Head-Finance

Mohan Prasad – HR, Head

GMR Infrastructure: Management Team

Airports Sector

Mr. G Kiran Kumar – Chairman

Mr. B V N Rao- Chairman

Mr. Srinivas Bommidala- Chairman Mr. GBS Raju- Chairman

Corporate FunctionsCorporate Functions

GADLGADL

Govindan Sridharan, CEO

Finance & Systems

Subba Rao, Group CFO

Ashutosh Agarwala, CFO-SFD

Johny Paramian, Group CIO

Legal & Secretarial

Y M Shivamurthy, Group President Legal

Mr. C.P.Sounderarajan, Company Secretary

Other Shared Services

G.K.Raghunandanan, CEO-Procurement

Mr Sheshan Ranganathan, Head-Strategic Planning

Dr.Vijay Vancheswar, Head Communications

Deepak Bharara–Group FMS Head & Head HR GGCL

Key Investment Highlights

2 GMR : Leading Infrastructure Player

3 Airports : Building Gateways To India

4 Power : Lighting the World

5 Urban Infrastructure & Highways : Paths To Progress

6 Strong Management Team

7Financial Highlights

India : Secular Growth In Infrastructure1

Stock Prices & Shareholding Pattern

8

GIL Shareholding Pattern

Floating Shareholding(25.07% equity of the company) – As on May 29, 2009

58

35.54%

36.67%

6.17%

21.62%