pkes/perg introductory workshop a monetary theory … · pkes/perg introductory workshop a monetary...

TRANSCRIPT

PKES/PERG Introductory Workshop

A Monetary Theory of Production

Jo MichellUWE, Bristol

1 / 21

A Monetary Theory Of Production

In my opinion the main reason why the problem ofcrises is unsolved, or at any rate why this theory is sounsatisfactory, is to be found in the lack of what mightbe termed a monetary theory of production.The distinction which is normally made between abarter economy and a monetary economy depends uponthe employment of money as a convenient means ofeffecting exchanges — as an instrument of greatconvenience, but transitory and neutral in its effect.. . . It is not supposed to affect the essential nature ofthe transaction from being, in the minds of thosemaking it, one between real things, or to modify themotives and decisions of the parties to it. Money, thatis to say, is employed, but is treated as being in somesense neutral.

J. M. Keynes, 1933

2 / 21

Money in (heterodox) economics

I Money matters; it is not a veil over real transactions

I Banks, financial systems and structures matter.

I Monetary analysis didn’t start with Keynes: Classicalpolitical economy; Marx; Wicksell; Hayek; DennisRobertson, Schumpeter and others.

I But important contributions from Keynes and his followers

I Emphasis on time, uncertainty, history, institutionalstructure

I No single heterodox or Post Keynesian theory of money;debates within PK econ and with other schools

3 / 21

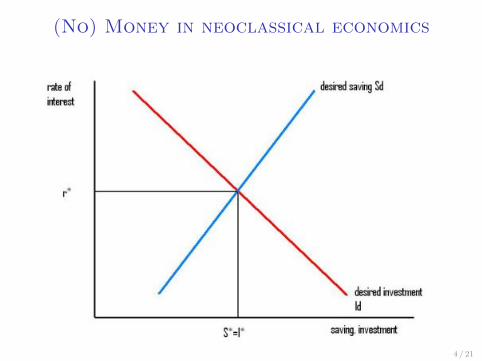

(No) Money in neoclassical economics

4 / 21

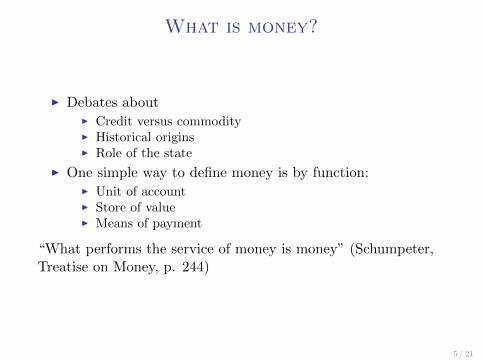

What is money?

I Debates aboutI Credit versus commodityI Historical originsI Role of the state

I One simple way to define money is by function:I Unit of accountI Store of valueI Means of payment

“What performs the service of money is money” (Schumpeter,Treatise on Money, p. 244)

5 / 21

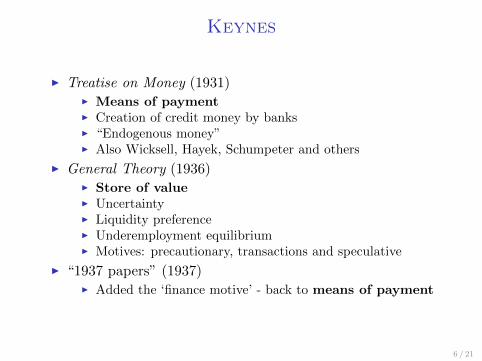

Keynes

I Treatise on Money (1931)I Means of paymentI Creation of credit money by banksI “Endogenous money”I Also Wicksell, Hayek, Schumpeter and others

I General Theory (1936)I Store of valueI UncertaintyI Liquidity preferenceI Underemployment equilibriumI Motives: precautionary, transactions and speculative

I “1937 papers” (1937)I Added the ‘finance motive’ - back to means of payment

6 / 21

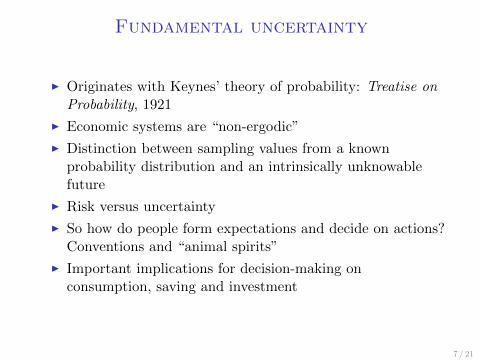

Fundamental uncertainty

I Originates with Keynes’ theory of probability: Treatise onProbability, 1921

I Economic systems are “non-ergodic”

I Distinction between sampling values from a knownprobability distribution and an intrinsically unknowablefuture

I Risk versus uncertainty

I So how do people form expectations and decide on actions?Conventions and “animal spirits”

I Important implications for decision-making onconsumption, saving and investment

7 / 21

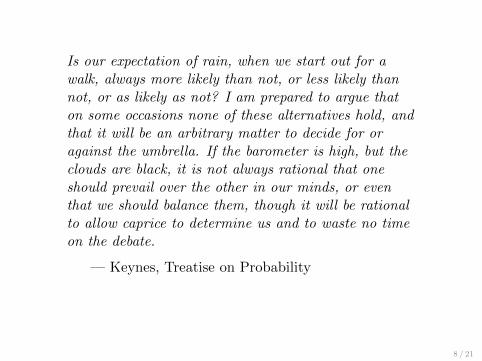

Is our expectation of rain, when we start out for awalk, always more likely than not, or less likely thannot, or as likely as not? I am prepared to argue thaton some occasions none of these alternatives hold, andthat it will be an arbitrary matter to decide for oragainst the umbrella. If the barometer is high, but theclouds are black, it is not always rational that oneshould prevail over the other in our minds, or eventhat we should balance them, though it will be rationalto allow caprice to determine us and to waste no timeon the debate.

— Keynes, Treatise on Probability

8 / 21

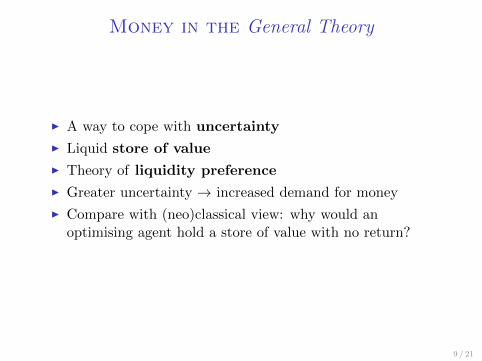

Money in the General Theory

I A way to cope with uncertainty

I Liquid store of value

I Theory of liquidity preference

I Greater uncertainty → increased demand for money

I Compare with (neo)classical view: why would anoptimising agent hold a store of value with no return?

9 / 21

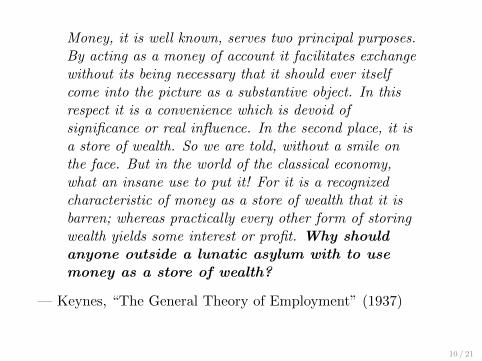

Money, it is well known, serves two principal purposes.By acting as a money of account it facilitates exchangewithout its being necessary that it should ever itselfcome into the picture as a substantive object. In thisrespect it is a convenience which is devoid ofsignificance or real influence. In the second place, it isa store of wealth. So we are told, without a smile onthe face. But in the world of the classical economy,what an insane use to put it! For it is a recognizedcharacteristic of money as a store of wealth that it isbarren; whereas practically every other form of storingwealth yields some interest or profit. Why shouldanyone outside a lunatic asylum with to usemoney as a store of wealth?

— Keynes, “The General Theory of Employment” (1937)

10 / 21

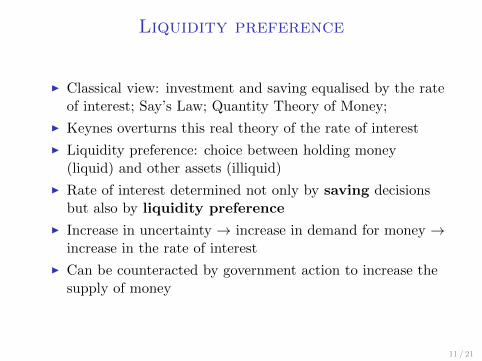

Liquidity preference

I Classical view: investment and saving equalised by the rateof interest; Say’s Law; Quantity Theory of Money;

I Keynes overturns this real theory of the rate of interest

I Liquidity preference: choice between holding money(liquid) and other assets (illiquid)

I Rate of interest determined not only by saving decisionsbut also by liquidity preference

I Increase in uncertainty → increase in demand for money →increase in the rate of interest

I Can be counteracted by government action to increase thesupply of money

11 / 21

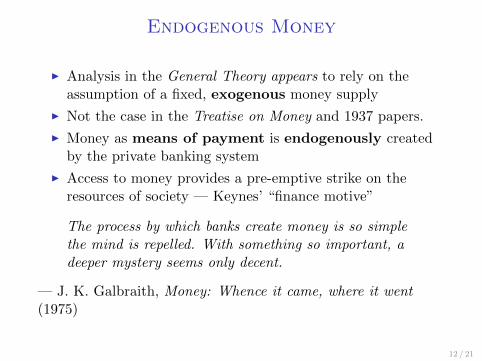

Endogenous Money

I Analysis in the General Theory appears to rely on theassumption of a fixed, exogenous money supply

I Not the case in the Treatise on Money and 1937 papers.

I Money as means of payment is endogenously createdby the private banking system

I Access to money provides a pre-emptive strike on theresources of society — Keynes’ “finance motive”

The process by which banks create money is so simplethe mind is repelled. With something so important, adeeper mystery seems only decent.

— J. K. Galbraith, Money: Whence it came, where it went(1975)

12 / 21

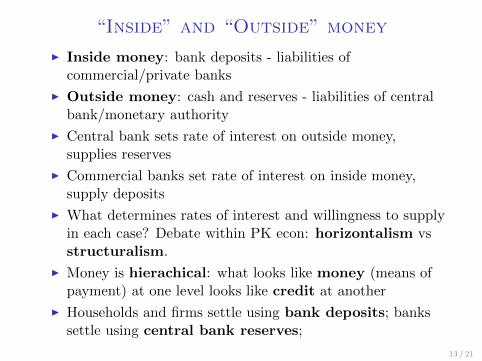

“Inside” and “Outside” money

I Inside money: bank deposits - liabilities ofcommercial/private banks

I Outside money: cash and reserves - liabilities of centralbank/monetary authority

I Central bank sets rate of interest on outside money,supplies reserves

I Commercial banks set rate of interest on inside money,supply deposits

I What determines rates of interest and willingness to supplyin each case? Debate within PK econ: horizontalism vsstructuralism.

I Money is hierachical: what looks like money (means ofpayment) at one level looks like credit at another

I Households and firms settle using bank deposits; bankssettle using central bank reserves;

13 / 21

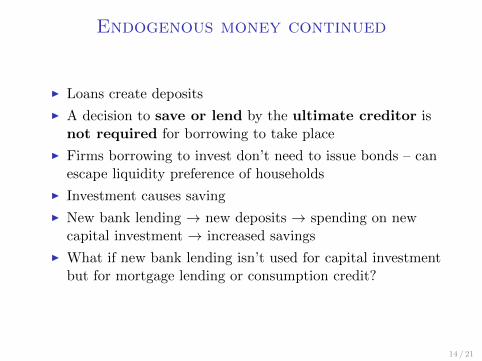

Endogenous money continued

I Loans create deposits

I A decision to save or lend by the ultimate creditor isnot required for borrowing to take place

I Firms borrowing to invest don’t need to issue bonds – canescape liquidity preference of households

I Investment causes saving

I New bank lending → new deposits → spending on newcapital investment → increased savings

I What if new bank lending isn’t used for capital investmentbut for mortgage lending or consumption credit?

14 / 21

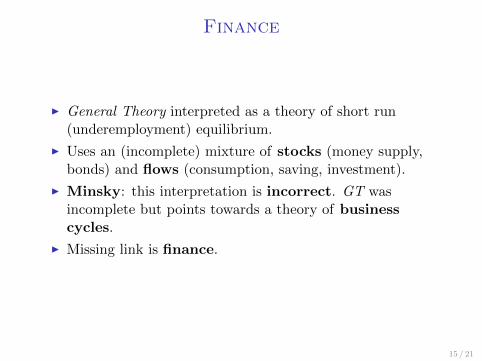

Finance

I General Theory interpreted as a theory of short run(underemployment) equilibrium.

I Uses an (incomplete) mixture of stocks (money supply,bonds) and flows (consumption, saving, investment).

I Minsky: this interpretation is incorrect. GT wasincomplete but points towards a theory of businesscycles.

I Missing link is finance.

15 / 21

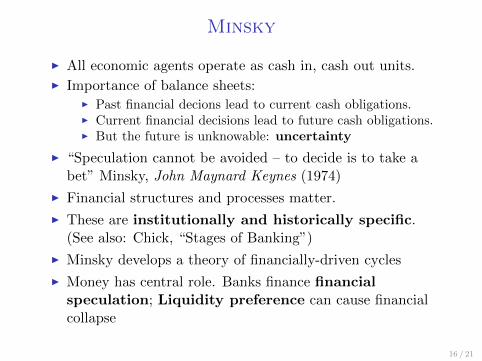

Minsky

I All economic agents operate as cash in, cash out units.

I Importance of balance sheets:I Past financial decions lead to current cash obligations.I Current financial decisions lead to future cash obligations.I But the future is unknowable: uncertainty

I “Speculation cannot be avoided – to decide is to take abet” Minsky, John Maynard Keynes (1974)

I Financial structures and processes matter.

I These are institutionally and historically specific.(See also: Chick, “Stages of Banking”)

I Minsky develops a theory of financially-driven cycles

I Money has central role. Banks finance financialspeculation; Liquidity preference can cause financialcollapse

16 / 21

Comparision with conventional wisdom

I Monetarism: central bank controls “inside” money directlybecause of table multiplier relationship with “outside”money.

I In the long run, output and employment are determined bythe supply side

I The economy tends towards full employment equilibrium inthe long-run

I From QTM, money supply determines prices

I CB should adjust quantity of reserves (outside money) inorder to target monetary aggregates and therefore inflation.

17 / 21

Comparision with conventional wisdom

I New Consensus replaced monetarism but retained manykey assumptions and conclusions

I In the long run, output and employment are determined bythe supply side

I The economy tends towards full employment equilibrium inthe long-run

I Central bank sets price of money - rate of interest

I This is actually a real rate of interest. There is no moneyin the models.

I “True” (natural) rate of interest determined in standardneoclassical way.

I Money, banks, credit, finance etc. all absent fromworkhorse DSGE model.

I Assumed irrelevant because of arbitrage by rationalactors in markets. Can “safely” be ignored.

18 / 21

Heterodox monetary theory now

I Many of key assertions shown to be correct.

I Bank of England now accepts the endogenous money view.

I Widely accepted that financial structure matters.

I Important implications and applications:I Quantitative easing etcI Secular stagnationI Income and wealth inequalityI Household debtI Cross-border capital flowsI Shadow banking system

19 / 21

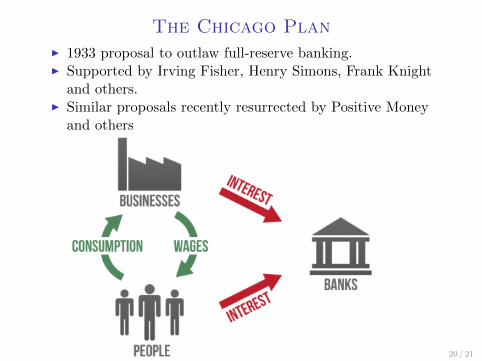

The Chicago PlanI 1933 proposal to outlaw full-reserve banking.I Supported by Irving Fisher, Henry Simons, Frank Knight

and others.I Similar proposals recently resurrected by Positive Money

and others

20 / 21

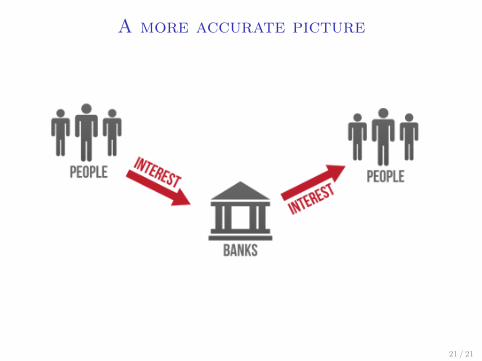

A more accurate picture

21 / 21

A Monetary Theory Of Production

Accordingly I believe that the next task is to work outin some detail a monetary theory of production, tosupplement the real-exchange theories which we alreadypossess. At any rate that is the task on which I amnow occupying myself, in some confidence that I amnot wasting my time.

J. M. Keynes, 1933

22 / 21