plaintiffs memorandum in opposition...

TRANSCRIPT

STATE OF MINNESOTA DISTRICT COURT

COUNTY OF RAMSEY SECOND JUDICIAL DISTRICT

Howard Swanson, Lambert Niesen, Steven Bornus, Richard Maus, James R. Otto, and William H. Kuretsky,

Plaintiffs,

vs.

State of Minnesota , Public Employees’ Retirement Association of Minnesota, Minnesota State Retirement System, Teachers Retirement Association of Minnesota, Governor Tim Pawlenty (in his official capacity), Thomas L. Marshall (in his official capacity), Mary Most Vanek (in her official capacity), Mary Brenner (in her official capacity), David Bergstrom (in his official capacity), Martha Lee Zins (in her official capacity), and Laurie Fiori Hacking (in her official capacity),

Defendants.

Court File No. 62-CV-10-5285

The Honorable Gregg A. Johnson Case Type: 14 Other Civil

PLAINTIFFS’ MEMORANDUM IN OPPOSITION TO

DEFENDANTS’ MOTION FOR SUMMARY JUDGMENT

i

TABLE OF CONTENTS

TABLE OF CONTENTS ................................................................................................................ i

TABLE OF AUTHORITIES .......................................................................................................... ii

Statement of the Issues .....................................................................................................................1

STATEMENT OF ADDITIONAL RECORD FOR MOTION .......................................................2

STATEMENT REGARDING UNDISPUTED AND DISPUTED FACTS ....................................2

I. INTRODUCTION. ..............................................................................................................4

II. PROCEDURAL HISTORY. ................................................................................................9

III. FACTUAL BACKGROUND ............................................................................................10

A. General Background Regarding Public Pensions ..................................................10

1. Types of Pensions ......................................................................................10

2. Determining Initial Pension Benefits and Providing Increases in Public Pension Defined Benefit Plans ...................................................................12 3. Determining and Evaluating the Plans’ Funding .......................................13

B. The Retirement Systems’ Postretirement Adjustments .........................................14

1. Applicable Principles from the LCPR Principles of Pension Policy .........14

2. The Statutory Underpinnings of the Postretirement Adjustments .............15

3. The Postretirement Adjustment Formulas from 1992 through 2009 .........16

4. The Retirement Systems’ Communications with its Members Regarding the Postretirement Adjustments .................................................................17 C. The 2009 and 2010 Pension Legislation ................................................................18

1. The 2009 Pension Legislation ....................................................................18

2. The 2010 Pension Legislation ....................................................................19

a. Impact of Reduction on the Retirees’ Pension Benefits ................20

ii

b. Events Preceding Passage of the 2010 Legislation ........................21

IV. LEGAL ARGUMENT .......................................................................................................24

A. Legal Standards ......................................................................................................24

B. If Defendants’ Motion Is Not Denied On The Current Record, The Court Should Stay Disposition Of The Motion To Allow Plaintiffs To Engage in Discovery. ..............................................................................................................25 C. Even Based On This Limited Record, Defendants Have Failed To Establish As A Matter of Law That The 2009 And 2010 Pension Legislation Do Not Violate The Contract Clauses Of The United States And Minnesota Constitutions ..........................................................................................................27 1. The Contract Clauses of the United States and Minnesota Constitutions Protect Contractual Relationships Like Those at Issue Here .................... 27 2. Previous Legislatures had the Power to Bind Future Ones with regard to Pension Obligations. ..................................................................................28 3. Retirees have a Contractual Right to Receive Postretirement Adjustments Pursuant to the Statutory Formula in Effect at the Time of Retirement. ...................................................................................30 a. The statutory language provides no discretion in the payment of postretirement benefits. .................................................................30 b. Where the statutory language providing a monetary retirement benefit is mandatory, Minnesota’s courts have found that a contract exists ............................................................................... 33 c. Defendants’ representations and conduct in implementing the postretirement adjustments are consistent with plaintiffs’ interpretation of the statutes .......................................................... 37 4. Questions of Fact Exist Whether the 2009 and 2010 Pension Legislation Substantially Impair the Rights of Retirees to Receive Future Postretirement Adjustments Pursuant to the Formula in Effect Upon their Retirements. .......................................................................................40 5. Questions of Fact Exist Whether the 2009 and 2010 Pension Legislation is “reasonable and necessary to serve an important public purpose” .......43

iii

D. Defendants have Failed to Establish as a Matter of Law that the 2010 Pension Legislation Does Not Violate The Takings Clauses Of The United States and Minnesota Constitutions. .......................................................................................49 1. The Takings Clauses of the United States and Minnesota Constitutions. .49 2. Retirees have a Protected Property Interest in the Postretirement Adjustment Formula in Effect at the Time of their Retirement. ................50 E. Plaintiffs May Bring Claims Under 42 U.S.C. § 1983 Against The Individual Defendants For Injunctive Relief and Obtain Monetary Damages Against The Defendants Through A Direct Action Under The Federal Takings Clause. ..........54 F. Defendants’ Challenges to Plaintiffs’ Class Action Allegations Are Premature and Without Merit ..................................................................................................55 V. CONCLUSION ........................................................................................................................58

iv

TABLE OF AUTHORITIES

Cases

AFL-CIO v. Sundquist, 338 N.W.2d 560 (Minn. 1983) .......................................................... 37, 40

AFSCME v. City of Benton, Arkansas, 513 F.3d 874 (8th Cir. 2008) .......................................... 47

Allied Structural Steel Co. v. Spannaus, 438 U.S. 234 (1978) ......................................... 27, 44, 47

Alsbrook v. City of Maumelle, 194 F.3d 999 (8th Cir. 1999) ....................................................... 54

Ario v. Metropolitan Airports Comm’n, 367 N.W.2d 509 (Minn. 1985) ..................................... 56

Arkansas Day Care Ass'n, Inc. v. Clinton, 577 F.Supp. 388 (D. Ark. 1983) ............................... 54

Ass’n of Surrogates & Supreme Court Reporters v. State of New York, 940 F.2d 766 (2d Cir. 1991)...................................................................................................... 44

Bailey v. State, 500 S.E.2d 54 (N.C. 1998) ................................................................................... 42

Booth v. Sims, 456 S.E.2d 167 (W. Va. 1995) ................................................................. 29, 36, 42

Branch v. U.S., 69 F.3d 1571 (Fed. Cir. 1995) ............................................................................. 52

Brayton, et al v. Pawlenty, et al., File No. 62-CV-09-1163 (Ramsey County District Court) ........................................................ 8

Burks v. Teasdale, 603 F.2d 59 (8th Cir. 1979) ............................................................................ 54

Carlstrom v. State, 694 P.2d 1 (Wash. 1985) ............................................................................... 46

Christensen v. Minneapolis Municipal Employees Ret. Board, 331 N.W.2d 740 (Minn. 1983)........................................................................................... passim

Commonwealth Edison v. U.S., 46 Fed.Cl. 29 (Fed. Cl. 2000) .............................................. 52, 53

Continental Illinois Nat. Bank and Trust of Chicago v. State of Washington, 696 F.2d 692 (9th Cir. 1983) .................................................................................................... 47

DLH, Inc. v. Russ, 566 N.W.2d 60 (Minn. 1997) ......................................................................... 24

Donnay v. Boulware, 275 Minn. 37, 144 N.W.2d 711 (1966) ...................................................... 24

Donohue v. Paterson, 2010 WL 2178749 (N.D. N.Y. May 12, 2010) ........................................ 42

Dougherty v. Dougherty, 950 A.2d 592 (Conn. App. 2008) ........................................................ 32

Energy Reserves Group, Inc. v. Kansas Power & Light Co., 459 U.S. 400 (1983) ..................... 43

Florida Rock Industries v. United States, 18 F.3d 1560 (Fed.Cir.1994) ...................................... 50

v

Glen Lewy 1990 Trust v. Investment Advisors, Inc., 650 N.W.2d 445 (Minn. Ct. App. 2002) ............................................................................. 56, 57

Hartung v. Billmeier, 66 N.W.2d 784 (Minn. 1954) .............................................................. 34, 35

Honeywell, Inc. v. Minn. Life and Health Ins. Guar. Assoc., 110 F.3d 547 (8th Cir. 1997) .................................................................................................... 28

Hughes Aircraft Co. v. Jacobson, 525 U.S. 432 (1999) ............................................................... 10

In re Eilbert, 162 F.3d 523 (8th Cir. 1998) ................................................................................... 29

Jacobsen v. Anheuser-Busch, Inc., 392 N.W.2d 868 (Minn. 1986) ........................................ 28, 43

Johnson v. City of Minnesota, 667 N.W.2d 109 (Minn. 2003) ..................................................... 50

Koster v. City of Davenport, Iowa, 183 F.3d 762 (8th Cir. 1999) ................................................ 28

Lingle v. Chevron U.S.A., Inc. 544 U.S. 528 (2005)..................................................................... 50

Manning v. N.M. Energy, Minerals & Natural Resources Dept., 144 P.3d 87 (N.M. 2006) .......................................................................................................... 54

Massachusetts Community College Council v. Commonwealth, 649 N.E.2d 708 (Mass. 1995) ................................................................................................... 41

Minnesota Education Association v. State, 282 N.W.2d 915 (Minn. 1979) ................................. 30

Murray v. City of Charleston, 96 U.S. 432 (1887) ....................................................................... 29

N.J. v. Wilson, 7 Cranch 164 (1812) ............................................................................................. 29

Nicholson v. United States, 77 Fed.Cl. 605 (Fed. Cl. 2007) ......................................................... 53

Offerdahl v. Univ. of Minn.Hosps, & Clinics, 426 N.W.2d 425 (Minn.1988) ............................. 24

Opinion of Justices (Furlough), 609 A.2d 1204 (N.H. 1992) ....................................................... 48

Palazzolo v. Rhode Island, 533 U.S. 606 (2001) .......................................................................... 49

Parella v. Retirement Bd. of Rhode Island Employees’ Retirement System, 173 F.3d 46 (1st Cir. 1999) ................................................................................................. 28, 51

Penn Central Transp. Co. v. New York City, 438 U.S. 104 (1978) ........................................ 49, 50

Phillips v. Washington Legal Foundation, 524 U.S. 156 (1998) .................................................. 51

Pasadena Police Officers Association v. City of Pasadena, 147 Cal.App.3d 695 (1983) ................................................................................................ 37, 42

Police Pension and Relief Board of the City and County of Denver v. McPhail, 338 P.2d 694 (Colo. 1959) ........................................................................................................ 36

vi

Professional Firefighters Ass’n of Omaha, Local 385 v. City of Omaha, 2010 WL 2426466 (D. Neb. June 10, 2010) ....................................................................... 47, 51

Rathbun v. W.T. Grant Co., 219 N.W.2d 641 (Minn. 1974) ........................................................ 58

Rice v. Perl, 320 N.W.2d 407 (Minn. 1982) ................................................................................. 25

Smith v. United HealthCare, 2002 WL 192565 (D.Minn. Feb. 5, 2002) ..................................... 57

Smith, et al., v. Woodwind Homes, Inc., 605 N.W.2d 418 (Minn. Ct. App. 2000) ................. 24, 25

State ex rel. Cannon v. Moran, 331 N.W.2d 369 (1983) .............................................................. 42

State ex rel. Humphrey v. Philip Morris Inc., 551 N.W.2d 490 (Minn. 1996) ............................. 33

State v. Great Northern Railway, Co., 106 Minn. 303 (1908) ...................................................... 30

Streich v. American Family Mut. Ins. Co., 399 N.W.2d 210 (Minn. Ct. App. 1987) ................... 56

Sylvestre v. Minnesota, 214 N.W.2d 658 (Minn. 1973) ........................................................ passim

U.S. Trust Co. v. N.J., 431 U.S. 1 (1977)............................................................................... passim

U.S. v. Clarke, 445 U.S. 253 (1980) ............................................................................................. 54

U.S. v. Sperry Corp., 493 U.S. 52 (1989) ..................................................................................... 52

United Firefighters of Los Angeles City v. City of Los Angeles, 210 Cal.App.3d 1095 (1989) .............................................................................................. 37, 41

United States v. General Motors Corp., 323 U.S. 373 (1945) ...................................................... 50

Univ. of Hawaii Professional Assembly v. Cayetano, 183 F.3d 1096 (9th Cir. 1999) ................. 42

Vieths v. Thorp Finance Co., 232 N.W.2d 776 (Minn. 1975) ...................................................... 25

Webb’s Fabulous Pharmacies, Inc. v. Beckwith, 449 U.S. 155 (1980) ........................................ 51

Wensmann Realty v. City of Eagan, Inc., 734 N.W.2d 623 (Minn. 2007) .................................... 49

Westling v. County of Mills Lake, 581 N.W.2d 815 (Minn. 1998) ............................................... 49

White Motor Corp. v. Malone, 599 F.2d 283 (8th Cir. 1979) ....................................................... 44

Will v. Michigan Dep’t of State Police, 491 U.S. 58 (1989) ......................................................... 54

Constitutional Provisions

Minn. Const. art. I, § 11 .................................................................................................................. 6

Minn. Const. art. I, § 13 .................................................................................................................. 7

vii

U.S. Const. art. I, § 10............................................................................................................... 6, 27

U.S. Const. Amend. V .................................................................................................................... 7

Statutes

1980 Minn. Laws, ch. 342, § 22 ................................................................................................... 35

1984 Minn. Laws, ch. 564, § 51 ................................................................................................... 37

1992 Minn. Laws 530, §§ 1-2 (effective July 1, 1992) ................................................................. 16

1997 Minn. Laws, ch. 233, art I .................................................................................................... 17

2010 Minn. Laws, ch. 359 art. 1 ................................................................................................... 20

Minn. Stat § 356.415 (2010) ......................................................................................................... 18

Minn. Stat. § 11A.18 (2008) ......................................................................................................... 16

Minn. Stat. § 352.115 .................................................................................................................... 32

Minn. Stat. § 353.29 ...................................................................................................................... 32

Minn. Stat. § 356.001, subd. 1 (2009) .......................................................................................... 15

Minn. Stat. § 356.415 .................................................................................................................... 31

Minn. Stat. § 356A.01, Subd. 21 (2009) .................................................................................... 16

Minn. Stat. § 356A.05(a) (2008) ................................................................................................... 16

Minn. Stat. § 645.08 (2009) .......................................................................................................... 33

Minn. Stat. § 645.16 ...................................................................................................................... 37

Minn.Stat. § 645.16 (2009) ........................................................................................................... 33

29 U.S.C. § 1002 ........................................................................................................................... 10

42 U.S.C. § 1983 ........................................................................................................................... 54

Other Authorities

“The Most-Cited Law Review Articles Revisited” 71 Chicago-Kent L.R. 751 (1996) ................ 50

BLACK'S LAW DICTIONARY .............................................................................................. 29, 31, 32

Charles A. Reich, "The New Property," 73 Yale L.J. 733 (1964) ................................................ 51

History of Military Pension Legislation in the United States, 12 Columbia University Press, 1900 .......................................................................................... 4

viii

James W. Ely Jr., “Economic Liberties and the Original Meaning of the Constitution,” 45 San Diego L.R. 673 (2008). ............................................................................................................ 27

J. Hetland & O. Adamson, 2 Minnesota Practice 588 (1970) 26

Stephen R. Bruce, Pension Claims Rights and Obligations 187 (2d ed. 1993) ............................ 32

1

Statement of the Issues

1. Where the statutory language provides that Retirees are entitled to postretirement

adjustments calculated according to the formula in effect at their retirement, where the

communications of Defendants guaranteeing those adjustments are consistent with that language,

where the Defendants have the responsibility of funding their defined benefit plans, and where

some Retirees even relinquished their defined contribution accounts in exchange for annuities

that were to include the postretirement adjustments, do current Retirees have a contractual

entitlement to postretirement adjustments based on the formula (or its equivalent) in effect at the

time of their retirement?

2. Where courts have routinely found that governmental claims of “economic

necessity” do not justify impairment of a contract between citizens and the government, where

the pension funds here were not in crisis and where reasonable and feasible options were

available to address the fiscal stability of Minnesota’s pension funds, did the Minnesota

Legislature violate the Contract Clauses of the United States and Minnesota Constitutions when

it decreased or eliminated current Retirees’ postretirement adjustments based on the formula (or

its equivalent) in effect at the time of their retirement?

3. Where well-established law recognizes that a Takings Clause violation occurs if

money taken is protected by a property right, did the Minnesota Legislature violate the Takings

Clauses of the United States and Minnesota Constitutions when it decreased or eliminated

current Retirees’ postretirement adjustments based on the formula (or its equivalent) in effect at

the time of their retirement?

2

4. Where well-established law recognizes that defendants can be sued in their

individual capacity when plaintiffs have sued for injunctive relief and that official-capacity

actions for prospective relief are not treated as actions against the state, did Defendants fail to

provide a basis for dismissing Plaintiffs Section 1983 claims?

5. Where a single set of government actions had a dramatic negative impact on the

postretirement adjustments to which Plaintiffs and the proposed class are entitled, and where

Plaintiffs have shown on a preliminary basis how they will meet the requirements of Minn. R.

Civ. P. 23, have Plaintiffs demonstrated the viability of this lawsuit as a class action?

6. Where no formal discovery has occurred and Plaintiffs have demonstrated that

discovery will yield material facts relevant to their claims, are Plaintiffs entitled to discovery if

the Court is not inclined to deny Defendants’ motion on the record presented?

STATEMENT OF ADDITIONAL RECORD FOR MOTION

1. Affidavit of Susan M. Coler, with Exhibits 1-25 and Summary Exhibits 1-4

2. Affidavit of Claude Poulin, with Exhibits A-B

STATEMENT REGARDING UNDISPUTED AND DISPUTED FACTS

Section III below titled “Factual Background” provides the Court with many additional

undisputed facts relevant to the issues in this case, including citations to statutory language and

to documents originating from the Defendants, as well as factual information available in the

public record.

Plaintiffs’ discussion of disputed facts is integrated into Section III and is further

discussed in Section IV, Plaintiffs’ arguments to the Court. Nonetheless, below is a listing that

includes the primary material disputed facts relevant to this motion. Citations to the factual basis

3

on which Plaintiffs assert that these facts are disputed are provided in Section III, “Factual

Background.”

Disputed: Whether the Retirees are contractually entitled to postretirement adjustments based on the formula in effect (or its equivalent) at the time they retired. See § III, Disputed: Whether the 2009 and 2010 Legislation at issue here decreased benefits to which Retirees are entitled. Disputed: Whether, during the period from 1992 through 2008, the Legislature has provided compensation for possible decreases resulting from actual changes in the statutory formula by which Retirees’ monthly annuities are increased. Disputed: Whether Defendants’ communications and conduct with respect to postretirement adjustments support Retirees’ contractual entitlement to postretirement adjustments based on the formula in effect (or its equivalent) at the time they retired. Disputed: Whether the imposition of “shared sacrifice” on the Retirees is illegal. Disputed: Whether the impairment of contract imposed on the Retirees is substantial. Disputes: Whether the impairment of contract imposed on the Retirees is reasonable and necessary to serve an important public purpose. Disputed: Whether the fiscal stability of the pension funds warranted the impairment of contract imposed on the Retirees. Disputed: Whether feasible and reasonable options exist to protect and improve the fiscal stability of the pension funds without the impairment of contract imposed on the Retirees. Disputed: Whether the Retirees’ receipt of postretirement adjustments according to the formula in place at the time they retired (or its equivalent) is a property right. Disputed: Whether the Defendants’ decrease of postretirement adjustments to which Retirees are entitled constitutes a basis for injunctive relief appropriate for redress under Section 1983.

4

I. INTRODUCTION

“Whether it be in the field or in the halls of the legislature it is not consonant with the American traditions of fairness and justice to change the ground rules in the middle of the game.” – Sylvestre v. Minnesota, 214 N.W.2d 658, 665 (Minn. 1973) (quotation omitted). This case concerns an enormous game changer. Plaintiffs and the Class they represent

(collectively, “Retirees”), approximately 130,000 retired Minnesota public sector employees,

were promised certain pension benefits and counted on those benefits to sustain them throughout

retirement. That promise has now been broken.

Retirees include former public school teachers who taught millions of Minnesota's

children; retired state judges who interpreted and enforced the state’s laws; retired police officers

who put themselves in harms’ way to protect Minnesota’s citizens; and other retired state, county

and local government workers who ensured the proper functioning of all sectors of Minnesota

government. Retirees are members of one of Minnesota’s three statewide public pension

systems, (collectively, “Retirement Systems”).1 Former state employees belong to the Minnesota

State Retirement System (MSRS); former local government employees belong to the Public

Employees Retirement Association of Minnesota (PERA); and most former Minnesota teachers

belong to the Teachers Retirement Association of Minnesota (TRA).

Retirees worked in public service for many years, often at a lower wage than they could

have earned in the private sector. Throughout their employment, they made mandatory

contributions to the Retirement Systems. Under Minnesota law, Retirees became vested in their

full pension benefits when they retired. These vested benefits include the right to receive

1 The public pension is not a modern construct, but is as old as ancient Rome. Caesar used a public pension to ensure that soldiers who had returned to Rome would remain faithful to the Republic. William Henry Glasson, History of Military Pension Legislation in the United States, 12 Columbia University Press, 1900 at 24-42.

5

pension increases based on the statutory postretirement adjustment formula that was in effect at

the time that they retired. Indeed, the Retirement Systems repeatedly assured Retirees that they

could count on the annual increase, and that it was “guaranteed.”

Despite these assurances, the Minnesota Legislature in 2009 and 2010 enacted

legislation (the “Pension Legislation”) that reduced Retirees’ promised pension benefits. In

2009, the legislature dramatically modified the postretirement adjustment formula by substituting

a flat 2.5% increase for the previously guaranteed inflation and investment components. In

2010, the legislature took away the guaranteed 2.5% increase and reduced the postretirement

adjustment formula to a range from 0 to 2.0%. While Defendants’ claim that the 2010

adjustments are “temporary,”2 some reductions will undoubtedly remain for a long period of

time. By doing this, the Legislature unilaterally “changed the ground rules” on Retirees, not in

the “middle of the game” while they were still employed, but after they had retired, long after the

game was over.

Prior to any discovery, and having provided only selected documents, Defendants have

now prematurely moved for summary judgment, seeking a determination that they had a right to

reduce Retirees’ pension benefits as they did. The Court should deny Defendants’ motion

outright even on this slim record because the statutory language is clear with respect to the

Retirees’ entitlement to their pension annuities including postretirement adjustments and there

are numerous disputed questions of material fact. Or the Court should take up Defendants’

motion only after the parties have had an opportunity to take the pertinent discovery.

2 See p. 38 of August 18, 2010 Memorandum of Defendants In Support Of Motion For Summary Judgment. Defendants’ Memorandum will be cited in this brief as Def. Mem. at ---.

6

To obfuscate their illegal conduct, Defendants present the Court with a lengthy

description of how pension plan fiduciaries managed pension funds over the last forty years. For

the most part, this description is irrelevant to the issues to be decided.

The bulk of the plans at issue here are defined benefit plans. Like any sponsor of a

defined benefit plan, Minnesota’s public employers accepted the risk and burden of amassing the

funds to fulfill its guarantee of a particular “benefit,” including statutorily promised annuities

with postretirement increases, to public employees upon retirement. Employees were never told

that after retirement the state could shift the risk to them. To the contrary, Retirees were assured

that their benefits were guaranteed. By cutting Retirees’ vested benefits, the State has shifted to

Retirees part of the investment risk that it promised to fully assume and until now did fully

assume. Those Retirees in defined contribution plans (e.g. the MSRS Unclassified Plan) – who

elected upon retirement to trade in their individual accounts for essentially the same monthly

benefits and statutory increases as the rest of the Retirees -- experienced an even more egregious

takeaway: the individual annuities that they essentially “purchased” from the State are now being

reduced, without any refund to them of any part of the purchase price.

The Minnesota and United States Constitutions obligate Defendants to fulfill their side of

the bargain and provide Retirees with the postretirement adjustments in effect at the time that

they retired. Specifically, Defendants have violated the Contract Clause of the U.S. Constitution,

which declares that “[n]o state shall…pass any…law impairing the obligations of contracts…”

(U.S. Const. art. I, § 10); the Contract Clause of the Minnesota Constitution, which in pertinent

part provides that no law “…impairing the obligation of contracts shall be passed…” (Minn.

Const. art. I, § 11); the Takings Clause of the United States Constitution, which states that

“private property [shall not] be taken for public use, without just compensation” (U.S. Const.

7

Amend. V); and the Takings Clause of the Minnesota Constitution, which provides that “Private

property shall not be taken, destroyed or damaged for public use without just compensation”

(Minn. Const. art. I, § 13).

With respect to the 2009 Pension Legislation, Defendants have provided no facts that the

elimination of the investment component of the postretirement adjustment was necessary. With

regard to the 2010 Pension Legislation, Defendants claim that extreme exigencies justified their

actions, but Retirees will establish that the situation did not warrant the drastic action taken and

that Defendants could have taken other actions to shore up the Retirement Systems’ funding

levels without breaking their promise to Retirees. Because this issue comes before the Court on

summary judgment, however, Retirees do not need to make their case now; they need only show

that there are genuine disputed issues as to whether the situation was as dire as claimed by the

Defendants, and whether the Defendants had viable alternatives that did not involve violation of

Retirees’ vested rights. Retirees easily meet this requirement to defeat Defendants’ motion for

summary judgment.

At this stage, the Court should also reject Defendants’ arguments that the promised

postretirement adjustments are somehow separate from the vested annuity without future

adjustments, or that Retirees have a right only to those postretirement amounts that they already

have received. The plain language of the governing statutes and plan documents refutes these

arguments. However, should the Court determine that the operative language is ambiguous, it

would be obliged to examine extrinsic factual evidence concerning plan interpretation and the

conduct of plan administrators over the past two decades before deciding these issues. Plaintiffs

offer documents available to them showing that the Retirement Systems’ administrators acted in

a manner consistent with their view of the statutory language (such as documents saying the

8

adjustments were “guaranteed”), but they have not had an opportunity to engage in any

affirmative discovery. This discovery should occur before any ruling.

Finally, Defendants attempt to justify the 2010 Pension Legislation by claiming that

Retirees were bound to participate in what Defendants term “shared sacrifice” for the benefit of

the pension funds that Defendants have failed to properly maintain. Defendants imply that

Retirees are somehow selfish for seeking to enforce the bargain that Defendants made and on

which Retirees relied for financial security in their retirement. Defendants fall back on this

“shared-sacrifice” equitable argument because there is no legal basis for transferring to the

Retirees any of the obligation to help shore up the funding levels of the Retirement Systems’

plans once they have started receiving benefits.

In her decision holding that the unallotment process is unconstitutional, District Court

Judge Gearin observed that government faces policy decisions that are challenging and

sometimes painful. While such decisions are not normally the business of the Court, they are if

they “…are made in a way that violates the constitution.” Order, Brayton, et al v. Pawlenty, et

al., File No. 62-CV-09-1163 (Ramsey County District Court), attached to the Affidavit of Susan

M. Coler (“Coler Aff.”) as Ex. 1 at 10.3 Here, Defendants’ decision to eliminate a portion of

promised benefits in the name of “shared sacrifice” violates both the federal and state

constitutions. Accordingly, this Court may and should step in.

In sum, while Defendants strive to distract the Court from their illegal conduct through

lengthy discussions of the tribulations faced by plan administrators and calls for “shared

sacrifice,” these points have no bearing on the fundamental question of whether the 2009 and

2010 Pension Legislation was constitutional. While that question requires resolution of a series 3 Unless otherwise indicated, all exhibits are attached to the Coler Aff. and are referenced as “Ex. --.”

9

of factual disputes, Plaintiffs have not been allowed any discovery. The Court should deny or

postpone ruling on Defendants’ summary judgment motion and allow discovery to proceed.

II. PROCEDURAL HISTORY

Plaintiffs commenced this lawsuit on May 17, 2010, two days after Governor Pawlenty

signed the 2010 Pension Legislation into law. Coler Aff. ¶ 2. Plaintiffs filed an Amended

Complaint on July 1, 2010, which Defendants answered on July 30, 2010. Id. In early

conversations among counsel, Defendants announced their intention to file a motion for

summary judgment and, at a status conference, asked the Court for the earliest possible filing

date. Coler Aff. ¶ 4. In a telephone conference held August 2, 2010, Plaintiffs’ counsel urged

Defendants to allow Plaintiffs a short but reasonable period of discovery before propounding

their motion. Id., ¶ 5. Plaintiffs provided Defendants with written citations supporting their

position. Id., Ex. 2 Defendants rejected Plaintiffs’ effort to obtain discovery and stated that

they would proceed with their motion for summary judgment. Id.,

Attempting to obtain at least minimal basic discovery as soon as possible, Plaintiffs

served Defendants with Requests for Production of Documents on August 10, 2010, Coler Aff., ¶

6, Ex. 3; responses are due September 9, 2010, two days after the September 7, 2010 due date for

this brief. Coler Aff., ¶ 6. On August 19, 2010, Plaintiffs served notices pursuant to Minn. R.

Civ. P. 30.02(f) for depositions to occur in October. Id., Ex. 4.

Meanwhile, on August 18, 2010, Defendants served their summary judgment submission;

it includes a 57-page brief, over 70 exhibits, and four affidavits; Plaintiffs had less than three

weeks – until September 7, 2010 – to respond.

10

III. FACTUAL BACKGROUND A. General Background Regarding Public Pensions

1. Types of Pensions

There are two types of pension plans: defined contribution and defined benefit plans. “A

defined contribution plan is one where employees and employers may contribute to the plan, and

the employer's contribution is fixed and the employee receives whatever level of benefits the

amount contributed on his behalf will provide.” Hughes Aircraft Co. v. Jacobson, 525 U.S. 432,

439 (1999) (quotation omitted). A defined contribution plan is essentially made up of individual

accounts for plan participants; indeed, it is also called an “individual account” plan. Section

3(34) of the Employee Retirement Income Security Act of 1974 (“ERISA”), 29 U.S.C. §

1002(34). A 401(k) plan is a typical defined contribution plan. “A defined benefit plan, on the

other hand, consists of a general pool of assets rather than individual dedicated accounts. Such a

plan, as its name implies, is one where the employee, upon retirement, is entitled to a fixed

periodic payment.” Hughes, 525 U.S. at 439 (quotation omitted). Almost all of the pension plans

in the Retirement Systems are defined benefit plans.

A critical distinction between defined contribution plans and defined benefit plans – and

a critical point in this case – concerns assumption of risk. In a 2007 report, the State of

Minnesota’s Office of Legislative Auditor explains this important point:

In defined benefit plan, the employer takes on the investment risk. Contributions made throughout the employee’s tenure are invested to pay the promised benefit. If assets are insufficient to pay the specific promised benefits, the employer assumes the market risk and generally makes up the difference. On the other hand, in defined contribution plans, the individual employee bears the investment risk. That is, the retiree’s pension income is directly affected by the investment performance of his or her pension account.

11

Ex. 5 at 4. In other words, where, as here, the operative plans involve defined benefits, the

employer is responsible for funding the plan, and bears the investment risk. Affidavit of Claude

Poulin, F.S.A., M.A.A.A., E.A., (“Poulin Aff.”), ¶ 14. In contrast, defined contribution plans

like 401(k)’s are never “underfunded” as participants simply receive the sum of their

contributions, the employer match (if applicable), and the gains (or losses) resulting from their

investment strategy.

As have other states, Minnesota funds its defined benefit plans through a combination of

statutorily determined contributions by both the employing public entity and by current

employees. See e.g., for MSRS: Minn. Stat. 352.021, subd. 2 (2009) (“Every person who

becomes a state employee . . . is covered by the general state employees retirement plan.

Acceptance of state employment or continuance in state service is deemed to be consent to have

deductions made from salary for deposit to the credit of the account of the state employee in the

retirement fund.”); Minn. Stat. § 352.04, subd. 1 (2009) (creating retirement fund where

employee contributions, employer contributions, and other amounts authorized by law must be

deposited); id. , subds. 2-3 (articulating the amount of employee and employer contributions as a

percent of salary).

“Nearly all employees of state and local government are required to make contributions

to defray the cost of their retirement benefit.” Ex. 6 at 8 (Keith Brainard, “Public Fund Survey

Summary of Findings for FY 2008,” NASRA). Contribution rates for employees and many

employers are set as a fixed percentage of pay. About one-fourth of state and local governments

do not participate in Social Security. Contribution rates in those “non-coordinated” plans are

higher, “because benefits usually also are higher to offset the lack of Social Security.” Id.

12

In 2008, before many states raised their contribution rates, the nationwide median

employer contribution rate for workers who participate in Social Security was 8.7%. Id. The

employer contributions in 2008 for many “coordinated” plans in the Midwest and the Plains

states far exceeded the national median: Arkansas PERS – 12.54%; Idaho PERS – 10.39%;

Illinois SERS – 16.56%; Missouri SERS - 12.75%; Oklahoma PERS – 12.46%. Ex. 7 at 22-23

(“2008 Comparative Study of Major Public Employee Retirement Systems,” Wisconsin

Legislative Council (revised May 2010)).

2. Determining Initial Pension Benefits and Providing Increases in Public Pension Defined Benefit Plans

Employees enrolled in defined benefit plans begin receiving pension benefits once they

meet the particular plan’s eligibility requirements and terminate their employment. Typically,

and here, a retiree’s base benefit is calculated by multiplying a formula multiplier by the

employee’s salary and by the number of service years. For example, the current MSRS

Coordinated Plan formula for a person at normal retirement at age 65 is [1.7%] x [average

compensation] x [years of service]. Bergstrom Ex. 23 at 30.4 Thus, an employee who retires

after 20 years of service and whose average compensation is $36,000 would receive a base

benefit of $1,020 per month or $12,240 a year. Compared to most other state pension system,

the Retirement Systems’ initial payment level is low.5 Ex. 5 at 72-73; Ex. 7 at 26, 28-29.

4 The Bergstrom, Hacking, Klausing and Vanek Exhibits were attached to their affidavits filed with Defendants’ Memorandum. 5 In a 2007 report, the State of Minnesota’s Office of Legislative Auditor found that Minnesota’s lower initial pension benefits resulted from the use of a lower benefit multiplier, the manner in which an employee’s “average salary” is determined, larger reductions for those who retire before age 65, and because “Minnesota is one of 10 states that does not exempt pension income from state income taxes.” Ex. 5 at 70-73; see Ex. 6 at 32, 34-35.

13

Nearly all major public pension systems in the United States provide some form of

periodic pension increase to compensate retirees for the anticipated effects of inflation. These

increases can be in one of several forms, including a fixed annual percentage increase, an

increase tied to the Consumer Price Index (usually with a cap), an increase based on investment

returns beyond a designated level, or an increase enacted by the state legislature. Compared to

most other state pension systems (at least since 2002), Minnesota has been providing less in

postretirement adjustments to retirees.6 Ex. 5 at 7; p. 7; Ex.7 at 32, 34-35.

3. Determining and Evaluating the Plans’ Funding

It is common practice for trustees of public pension plans to determine annually whether

plan assets are sufficient to meet plan obligations. This occurs by instructing an actuary to

produce an “actuarial valuation” that estimates the plan’s position at a specific point in time.

Actuarial projections are based on two types of assumptions – economic and demographic.

Economic assumptions include assumptions as to investment returns, which are used to

determine the present value of future liabilities, and assumptions as to salary increases, used to

project current pay until retirement. Demographic assumptions include the likelihood of retirees’

termination of employment, retirement, disability or death at any particular point in time. Ex. 8

at 1 (“Actuarial Valuation Basics,” Massachusetts Public Employee Administration Commission

(2008)).

There are two methods of plan asset valuation. The “Market Value of Assets” (MVA)

method represents a “snap shot” of the value of the plan on a particular day and is calculated by

determining the present value of future expected cash flows, discounted by the market rate of 6 The Legislative Auditor found that of the 42 pension systems providing for automatic increases, 24 had more generous postretirement benefit increase formulas, 10 had the same or equivalent formulas, and 8 had generally lower formulas than Minnesota’s post-retirement formula. Ex. 5 at 73.

14

investment return. Use of the MVA does not take into account short-term market fluctuations,

and may make it difficult to value fund assets on a consistent basis. To alleviate this problem

and reduce the impact of short-term asset volatility, actuaries calculate the plan’s “Actuarial

Value of Assets” (AVA) which “smoothes” the investment returns over a period of time, usually

up to five years. Thus, when the returns are higher than assumed, smoothing defers gains in the

AVA. When the returns are less than assumed, smoothing defers losses in the AVA. Ex. 9 at 8

(“Montana Municipal Police Officers’ Retirement System June 30, 2009 Actuarial Valuation”).

Pension Plans do not have to be fully funded to be actuarially sound. Many experts

consider AVA ratios above 80% as sound for public pensions. Ex. 10 at 15 (GAO, “State and

Local Government Retiree Benefits – Current Funded Status of Pension and Health Benefits”).

MVA ratios are informative but a lower MVA “doesn’t fully disclose the long-term funding

trend of the System,” according to Milliman, the actuary for Minnesota’s Legislative Committee

on Pensions and Retirement. Klausing Aff., Ex. 1 at 5 (July 1, 2009 Actuarial Review of the

Retirement Systems).

B. The Retirement Systems’ Postretirement Adjustments

1. Applicable Principles from the LCPR Principles of Pension Policy

Since 1955, the Legislative Commission on Pensions and Retirement (“LCPR”) has had

in place a set of “Principles of Pension Policy” to be used “as the basis for evaluating proposed

public pension legislation.” Klausing, Ex. 6 at 5-8. As the LCPR recognizes, “[p]roblems can

be avoided or minimized if a sound set of principles is used as a guideline in developing the

various public pension funds and plans.” Id. at 5.

With respect to postretirement benefits and how the Legislature should address funding

shortfalls, the Principles state:

15

• “Postretirement benefit adequacy should function to replace the impact of economic inflation over time in order to maintain a retirement benefit that was adequate at the time of retirement.”

• “In recommending benefit plan modifications, the imposition of reductions in overall

benefit coverage for existing pension plan members should not be recommended.” • “The imposition of a reduction in overall benefit coverage may be imposed for new

pension plan members in order to achieve sound pension policy goals.”

• “A reduction in some aspect or aspects of benefit coverage may be recommended in combination with a proposed benefit increase or benefit increases in implementing sound pension policy goals.”

Id. at 5-6 (emph. added).

2. The Statutory Underpinnings of the Postretirement Adjustments

The Minnesota Legislature has provided Retirees with an initial pension annuity and

postretirement adjustments to that annuity by statute. See Summary Exhibits (“S. Ex.”) 1-4

(providing relevant statutory citations from 1992-2010). The statutory language states that

Retirees are “entitled” to both an annuity and an annual adjustment to that annuity that is made

“automatically.” Id. The statutes further articulate in mandatory terms the formulas by which

both the annuity and the adjustments “must” or “shall” be determined. Id. To avoid unnecessary

duplication, a detailed analysis of the statutory language of the pension annuities postretirement

adjustments is provided in the Argument below at § IV.C.3.a.

The Legislature has further declared that the public pension plans exist for the “exclusive

benefit” of members and beneficiaries. They were created “to provide for the retirement of their

members and to provide funds for the beneficiaries of members in the event of death of a

member.” Minn. Stat. § 356.001, subd. 1 (2009). The exclusivity of the benefit is clear: “no part

of the moneys of the plans and funds may revert to the plan or fund or be used for or diverted to

purposes other than the exclusive benefit of the members or their beneficiaries.” Id.

16

Accordingly, the Legislature assigned the plan fiduciaries the duty to provide authorized

benefits to plan participants and beneficiaries, incur and pay administrative expenses, and

“manage a covered pension plan in accordance with the purposes and intent of the plan

document.” Minn. Stat. § 356A.05(a) (2008). To this end, the fiduciaries are obligated by

statute to carry out their duties “in a manner consistent with law and the plan document.” 7 Id. at

(b) (emphasis added; italicized phrase omitted in Def. Mem. at 8).

3. The Postretirement Adjustment Formulas from 1992 through 2009

In 1992, the Legislature enacted a formula for postretirement adjustments that provided a

benefit designed to both (1) compensate for the effects of inflation (the inflation-adjustment

component) and (2) allow retirees to share in any earnings (the investment-based component).

See 1992 Minn. Laws 530, §§ 1-2 (effective July 1, 1992). That two-component formula

remained in place through 2009.

Initially, the inflation-adjustment component provided for an increase in annual benefits

equal to 100% of the inflation rate as measured by the Consumer Price Index (“CPI-W”) up to a

maximum of 3.5%. Id. The separate investment-based component would be paid only if

investment returns, averaged over a five-year period, exceeded the amount needed to pay: (1) the

inflation-based component (2.5% maximum), and (2) the 5% annual actuarial earnings

assumption. In addition, all accumulated investment losses from prior periods were required to

be recovered before the investment-based portion of this calculation was to be paid. Minn. Stat.

§ 11A.18 (2008). In 1997, the inflation-adjustment component was decreased from 3.5% to 7 Plan documents are defined by statute as “a written document or series of documents containing the eligibility requirements and entitlement provisions constituting the benefit coverage of a pension plan, including any articles of incorporation, bylaws, governing body rules and policies, municipal charter provisions, municipal ordinance provisions, or general or special state law.” Minn. Stat. § 356A.01, Subd. 21 (2009).

17

2.5%, and the actuarial earnings assumption was increased from 5 to 6%. Consistent with the

“Principles of Pension Policy” stating that any reduction should be in combination with a

proposed benefit increase, the Legislature implemented a permanent one-time increase designed

to be “actuarially equivalent” to the previous statutory formula. See 1997 Minn. Laws, ch. 233,

art I, §§ 5, 58, 72.

Retirees received postretirement adjustments including both components through 2002,

but after that received only the inflation-adjustment component because the funds did not have

sufficient returns to meet the formula requirements allowing payment of the investment-based

component. Bergstrom Ex. 8 at 13. (April 20, 2007 Memo to Post Fund Committee from the

Retirement Systems’ Executive Directors).

4. The Retirement Systems’ Communications with its Members Regarding the Postretirement Adjustments

Because Plaintiffs have not obtained any discovery from Defendants, they have not yet

performed a systematic or comprehensive review of communications from the Retirement

Systems to public employees and retirees concerning the postretirement adjustments. Relevant

documents that Plaintiffs have obtained independently suggest that the Retirement Systems

regularly assured employees and Retirees that they could count on continuing to receive their

promised postretirement adjustments under the 1992/1997 two-component formula throughout

retirement.

For example, in brochures provided to members, PERA referred to the investment-based

adjustment as the “Permanent Investment Component” and to the inflation-based adjustment as

the “Permanent Inflation Component.” Ex. 11 (“Increases in Your PERA Pension,” January

2004). That same brochure described the inflation-adjustment component as “a permanent

feature . . . It is paid regardless of investment gains or losses experienced by the Post Fund.” Id.

18

Likewise, on the back cover of a 1991 handbook for police and fire members, PERA stated that

“benefits are based on the laws in effect at the time you terminate your public service.” Ex. 12

(“Your Benefits With PERA,” November 1991). Similarly, in a 2005 letter, Defendant and

MSRS Executive Director Bergstrom informed a retiree: “Our increase is based on two

components. The inflation component guarantees that we increase benefits based on the

Consumer Price Index (CPI) up to 2.5 percent.” Ex. 13 (February 2, 2005 Bergstrom Letter to

James Otto). See also, Ex. 14 (“Minnesota Post Retirement Investment Fund,” November 1999

TRA Pamphlet) (“The cost-of-living component is paid up to a maximum of 2.5 percent . . . It is

paid each year regardless of the amount of investment return.”).

In addition, the selected documents that Defendants filed with their motion include

several that describe the postretirement adjustments as “guaranteed” or words to that effect. See

e.g., Bergstrom Ex. 4 at 3 (January 25, 2007 Post Fund Minutes referencing “the current

guaranteed 2.5% cost of living adjustment”); Vanek Ex. 1 at 11 (December 5, 2006 Memo from

Executive Directors of Retirement Systems to Boards of Directors, noting that the 8.5 percent

return assumed by the Post Fund is required “to cover the guaranteed inflation based annual

adjustment”); Hacking Ex. 7 at 1 (January 2007 Post Fund Q&A, noting that “each year” the

inflation-based adjustment “is granted regardless of investment performance”).

C. The 2009 and 2010 Pension Legislation

1. The 2009 Pension Legislation

In 2009, as part of the legislation abolishing the Minnesota Post Retirement Investment

Fund (“Post Fund”), the dual-component formula was eliminated and replaced with a 2.5%

annual increase. 2009 Minn. Laws, Ch. 191 (codified at Minn. Stat § 356.415 (2010)). The

2.5% annual increase was applied on January 1, 2010 to all retired members of the Retirement

19

Systems, regardless of date of retirement. Klausing Ex. 18 at 3 (Minnesota State Board of

Investment 2009 Annual Report).

Plaintiffs are not aware of any analysis undertaken by Defendants of whether the flat

2.5% increase constituted a decrease in the postretirement adjustment over time as compared to

the previous formula – CPI capped at 2.5% plus the potential investment component. It is

apparent that the Retirement Systems viewed awarding the CPI capped at 2.5% as the actuarial

equivalent of a 2.5% flat increase. Bergstrom Aff., Ex. 26 at 8 (Post Fund Proposal – 2008

Legislative Session) (“2.5 percent annual increase is built into the current actuarial funding

structure”). However, the 2009 legislation does appear to be a reduction over time because of

the complete elimination of the investment component that had provided substantial increases in

past years. See Bergstrom Ex. 2 at 3 (MSRS Messenger (newsletter), Spring 2007, showing

increases from 1997 through 2007 ranging from .07% to 11%). Plaintiffs are unable to

determine without additional discovery whether the 2009 modification in fact compensates the

Retirees for projected losses they will incur as a result of the change, but it appears that, as a

result of the 2009 change, the Retirees lost the investment component and received nothing in

return.

2. The 2010 Pension Legislation

In 2010, the Minnesota Legislature changed the postretirement adjustment formula again.

The formulas were individual to the Retirement Systems, but uniformly constituted reductions in

the postretirement adjustment that had been passed in 2009.

MSRS – for all plans (except State Patrol), reducing the automatic postretirement increase from 2.5% to 2.0% and for State Patrol Plan, reducing the automatic postretirement increase from 2.5% to 1,5% until the funding of the plan reaches 90% (MVA) when it will return to 2.5%.

20

PERA – for the General Plan and Local Government Correctional Service Plan, reducing the automatic postretirement increase from 2.5% to 1.0% until the funding of the plan reaches 90% (MVA) when it will return to 2.5%; for the Police and Fire Plan, reducing the automatic postretirement adjustment from 2.5% to 1.0% for 2011 and 2012 and then increase it to CPI with a cap of 1.5% until the funding of the plan reaches 90% (MVA) when it will return to 2.5%. TRA – suspending the automatic postretirement increase for two years and then reducing the automatic postretirement increase from 2.5% to 2.0% until the funding of the plan reaches 90% (MVA) when it will return to 2.5%

2010 Minn. Laws, ch. 359 art. 1, §§76-81 (“2010 Pension Legislation”). a. Impact of Reduction on the Retirees’ Pension Benefits. TRA’s actuary believes that – even with the 2010 Pension Legislation – the TRA funding

level will not be restored to 90% at any time during the next 35 years. Hacking Ex. 12 at 4

(March 16, 2010 Memorandum from Hacking to House Committee). From the documents filed

with this motion, Plaintiffs have not been able to identify similar information for the other funds.

If it is assumed that most of the other funds will be below 90% MVA for at least 25 years,

Plaintiffs estimate that retirees of the following plans will receive the following percentage

reductions in benefits over that time: MSRS (except for State Patrol Plan) - 7% less; MSRS State

Patrol Plan – 13.3%; PERA General Plan - 19.2%; and PERA Police and Fire Plan - 14.2%.

Coler Aff. at ¶¶ 9-10. Plaintiffs further estimate that TRA retirees, who will also receive no

adjustments in 2011 and 2012, will see their benefits reduced by 10.5% over the next twenty-five

years.Id. This translates into the loss of at least tens of thousands of dollars for retirees with

relatively few years of service8 and up to several hundred thousands of dollars for retirees with

8 For the “hypothetical” retiree who retired in 2009 and received the average benefit for new retirees with at least 10 years of service, the retiree’s benefits will be reduced by the following over the next 25 years: MSRS State Employees Plan -- $22,487; MSRS State Patrol Plan -- $124,374; PERA General Plan -- $40,470; PERA Police & Fire Plan -- $98,576; and TRA Plan -- $42,254. Coler Aff. at ¶ 11.

21

over 30 years of service.9 It does not appear from the documents submitted by Defendants that

the Pension Boards, the LCPR or the Legislature were provided or considered calculations of this

type during their deliberations.

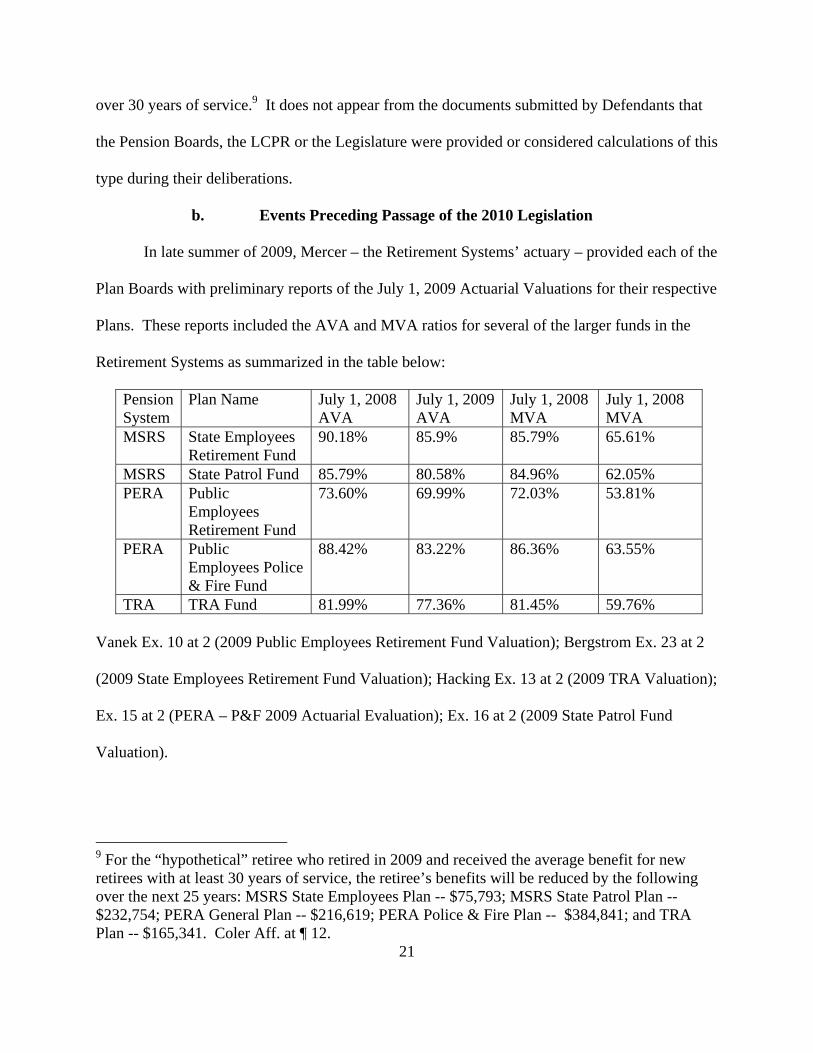

b. Events Preceding Passage of the 2010 Legislation In late summer of 2009, Mercer – the Retirement Systems’ actuary – provided each of the

Plan Boards with preliminary reports of the July 1, 2009 Actuarial Valuations for their respective

Plans. These reports included the AVA and MVA ratios for several of the larger funds in the

Retirement Systems as summarized in the table below:

Pension System

Plan Name July 1, 2008 AVA

July 1, 2009 AVA

July 1, 2008 MVA

July 1, 2008 MVA

MSRS State Employees Retirement Fund

90.18% 85.9% 85.79% 65.61%

MSRS State Patrol Fund 85.79% 80.58% 84.96% 62.05% PERA Public

Employees Retirement Fund

73.60% 69.99% 72.03% 53.81%

PERA Public Employees Police & Fire Fund

88.42% 83.22% 86.36% 63.55%

TRA TRA Fund 81.99% 77.36% 81.45% 59.76% Vanek Ex. 10 at 2 (2009 Public Employees Retirement Fund Valuation); Bergstrom Ex. 23 at 2

(2009 State Employees Retirement Fund Valuation); Hacking Ex. 13 at 2 (2009 TRA Valuation);

Ex. 15 at 2 (PERA – P&F 2009 Actuarial Evaluation); Ex. 16 at 2 (2009 State Patrol Fund

Valuation).

9 For the “hypothetical” retiree who retired in 2009 and received the average benefit for new retirees with at least 30 years of service, the retiree’s benefits will be reduced by the following over the next 25 years: MSRS State Employees Plan -- $75,793; MSRS State Patrol Plan -- $232,754; PERA General Plan -- $216,619; PERA Police & Fire Plan -- $384,841; and TRA Plan -- $165,341. Coler Aff. at ¶ 12.

22

Shortly after receiving the actuarial valuations, the Boards decided to take immediate

action with respect to funding levels and moved quickly to the “solution” of cutting benefits of

current retirees by lowering the postretirement adjustment formula. For example, at their

September 2009 meeting, TRA Board members were already talking about a “shared sacrifice”

approach. Hacking Ex. 10 at 1 (November 6, 2009 TRA Board Minutes). Similarly, even

before their actuaries provided them with models for reducing the postretirement increases, the

PERA Board voted at its October 2009 meeting to cut the benefits to the current retirees. Vanek

Ex. 6 at 5 (October 8, 2009 PERA Board Minutes).

At the same time, the Retirement Systems reported to their constituents that the pension

funds were not in a crisis situation. See e.g., Hacking Ex. 7 at Ex. 3A-5 at 4 (October 2009 Q &

A – Q: Is there a risk that TRA will not be able to pay monthly benefits?" A: "No, not for many

years. There is no imminent danger threatening benefit payments."); Vanek Ex. 12 at 1 (Autumn

2009 "The PERA Benefit" (newsletter) – "With assets of over $14 billion for all our plans,

current benefits are not in jeopardy--the problems that must be addressed lie in the future.")

During the period that the 2010 Legislation was being considered, the State Board of

Investment reported excellent investment returns in the Retirement Systems’ jointly-managed

defined benefit plans. See Ex. 17 (SBI December 14, 2009 and February 14, 2010 Minutes, SBI

Combined Funds Performance, 3/3/10). MSRS acknowledges on its website that since “June 30,

2009, the Plan has experienced significant recovery with strong investment gains of about 15

percent . . . [that] have helped stabilize the funding and the Plan is now over 70 percent funded.”

Ex. 18 (MSRS Web Page).

During their formulation of their final proposals to the Legislature, the Pension Boards

were also provided with information about changes that other states had recently enacted or were

23

considering to shore up their pension plans. See, e.g.,Vanek Ex. 10 at 3 (December 2009 “Public

Employees Retirement Fund Actuarial Valuation Report as of July 1, 2009”). Options that the

Pension Boards were aware of but rejected included lowering benefit levels for new hires or

raising employer or employee contribution rates to levels on par with most other states, or even

to their own historical levels.

For example, documents show that the MSRS Board summarily rejected options

involving increased employer and current employee contributions due to the recent history of

State budget cuts. In discussing why MSRS was not recommending an increase to contribution

rates for the MSRS General and Correctional Plans, MSRS Executive Director Bergstrom stated

in a March 2010 memo to the Legislature:

The employees and employers have already been asked to increase contribution rates over the past years. Asking employees to shoulder an additional burden when they have not received, nor are likely to receive, salary increases was not a viable alternative. The serious deficits facing the State of Minnesota, and specifically state agencies, make it unpalatable to increase employer contributions.

Bergstrom, Ex. 22 at 2 (March 13, 2010 Bergstrom Memorandum to Rep. Pewlowski) (emphasis

added);10 see also Vanek Ex. 8 at 4 (December 10, 2009 Minutes of PERA Board of Trustees in

which a trustee stated that COLA should be suspended because “actives are not getting a wage

increase, they are paying more for insurance and in some cases are being furloughed”).

In this context, the “shared sacrifice” model cutting current retiree benefits provided a

seemingly easy new “option” that was hastily proposed and adopted by the Legislature. This

lack of consideration and the abbreviated process may be contrasted to another component of the

2010 Legislation that mandated the Retirement Systems to undertake a year-long process to

10 Bergstrom is referring to the increase of the employer and employee contributions from 4% to 5% over the past four years. Bergstrom, Ex. 22 at 2.

24

study the long-term health of their pension plans. See 2010 Laws, ch. 359, art. I, § 86. The

Retirement Systems have published a proposed approach to undertake this study, which includes

a study, actuarial analysis conducted by the Retirement Systems’ actuary and reviewed by the

LCPR actuary, solicitation of input from “stakeholder groups and other interested parties, and

publication of a draft report that will be circulated to all groups and interested parties for

comment before a final report is issued. Ex. 19 (Retirement Systems Proposed Design Study).

IV. LEGAL ARGUMENT

A. Legal Standards

Rule 56 of the Minnesota Rules of Civil Procedure establishes the standard for summary

judgment. On a motion for summary judgment, Plaintiffs are simply required to present specific

facts showing that there is a genuine issue for trial. Minn. R. Civ. P. 56.05. The Minnesota

Supreme Court has cautioned that summary judgment should be applied carefully: “Summary

judgment is a blunt instrument and should not be employed to determine issues which suggest

that questions be answered before the rights of the parties can be fairly passed upon. It should be

employed only where it is perfectly clear that no issue of fact is involved . . .” Donnay v.

Boulware, 275 Minn. 37, 45, 144 N.W.2d 711, 716 (1966).

“The district court’s function on a motion for summary judgment is not to decide issues

of fact, but solely to determine whether factual issues exist.” DLH, Inc. v. Russ, 566 N.W.2d 60,

70 (Minn. 1997). In so doing, the evidence must be viewed in the light most favorable to the

party opposing the motion. Smith, et al., v. Woodwind Homes, Inc., 605 N.W.2d 418, 422 (Minn.

Ct. App. 2000) (citing Fabio v. Bellomo, 504 N.W.2d 758, 761 (Minn.1993)). All doubts and

factual inferences must be resolved in favor of the non-moving party. Offerdahl v. Univ. of

Minn.Hosps, & Clinics, 426 N.W.2d 425, 427 (Minn.1988). Ultimately, the moving party has

25

the burden of showing the absence of any genuine issue of material fact. Smith, 605 N.W.2d at

422 (citing Minn. R. Civ. P. 56.03).

Additionally, summary judgment must not operate to deny a litigant an opportunity to

discover and present facts. Vieths v. Thorp Finance Co., 232 N.W.2d 776, 778 (Minn. 1975). In

short, summary judgment may only be granted if (1) both parties have had an opportunity to

discover and present facts, and (2) there is no genuine issue of material fact.

B. If Defendants’ Motion Is Not Denied On The Current Record, The Court Should Stay Disposition Of The Motion To Allow Plaintiffs To Engage in Discovery.

Even with limited time and lack of access to the complete record relevant to the issues in

this case, Plaintiffs demonstrate below that genuine issues of material fact compel denial of

Defendants’ motion. However, if the Court is not persuaded to deny this motion outright,

Plaintiffs seek a continuance to allow for additional discovery before any decision is made.

Minn. R. Civ. P. 56.06 provides:

Should it appear from the affidavits of a party opposing the motion that the party cannot for reasons stated present, by affidavit, facts essential to justify the party's opposition, the court may refuse the application for judgment or may order a continuance to permit affidavits to be obtained or depositions to be taken or discovery to be had or may make such other order as is just.

Continuances to conduct discovery should be “liberally granted.” Rice v. Perl, 320 N.W.2d 407,

412 (Minn. 1982). “This is especially true when the party seeking the continuance is doing so

because of a claim of insufficient time to conduct discovery.” Id.

Normally the court will grant additional time to the nonmoving party to obtain the facts if the reason is a matter of insufficient time. A continuance or permission to engage in further discovery should not be denied to a party except in the most extreme circumstances. * * * As a practical matter, the court should be liberal in granting additional time for purposes of preparing affidavits or discovery if a party has any real reason to believe that facts can be established by such means.

26

Id. (quoting J. Hetland & O. Adamson, 2 Minnesota Practice 588 (1970)). In other words, two

key factors in deciding to continue discovery are (1) whether the non-moving party was diligent

in seeking discovery and (2) whether that party has a good faith belief that discovery will

uncover material facts. Id.

This case was filed just four months ago. Plaintiffs filed document requests within two

weeks of receiving Defendants’ answer to their complaint, and deposition notices not long after

that. Plaintiffs tried to persuade the Defendants to engage in a relatively short period of

discovery before filing their summary judgment motion but their efforts were rebuffed.

Plaintiffs’ diligence is indisputable. Defendants’ responses to Plaintiffs’ first set of document

requests are not due until after the deadline for this response. In responding to Defendants’

motion for summary judgment, Plaintiffs have had less than three weeks to analyze the

documents served by Defendants with their motion.

Based on the documents submitted with Defendants’ motion, and additional documents in

the public record and provided by Plaintiffs and class members, Plaintiffs’ counsel believe that

additional relevant and probative documents exist besides those that Defendants filed with their

motion. Coler Aff., ¶¶ 7-8. Plaintiffs’ arguments further demonstrate that deposition and expert

testimony will be probative of the issues to be decided. Id.; see Affidavit of Claude Poulin, filed

with this Brief. As required by Minn. R. Civ. P. 56.06, and to the extent possible given the early

stage of this litigation, Plaintiffs provide affidavit testimony as to the discovery sought, the

sources of that evidence, and their good faith belief that discovery will uncover additional

material facts. Id., and Exs. 2-3.

In sum, Plaintiffs assert that even the current record demonstrates that genuine issues of

material fact warrant outright denial of Defendants’ motion. However, if the Court is not

27

inclined to deny Defendants’ motion outright, then Plaintiffs ask it to order a continuance

sufficient to allow Plaintiffs a reasonable opportunity to discover documents and information

probative of their claims. Plaintiffs have made the showing necessary for a continuance under

Minn. R. Civ. P. 56.06: (1) they have been diligent in seeking discovery, and (2) they have a

good faith belief that discovery will uncover material facts.

C. Even Based On This Limited Record, Defendants Have Failed To Establish As A Matter of Law That The 2009 And 2010 Pension Legislation Do Not Violate The Contract Clauses Of The United States And Minnesota Constitutions

1. The Contract Clauses of the United States and Minnesota Constitutions Protect

Contractual Relationships Like Those at Issue Here “No State shall . . . pass any . . . Law impairing the Obligation of Contracts.” U.S. Const.

art. I, § 10, cl. 1.

The Contract Clause is one of the United States Constitution’s few express bans on the

state, and its unique history suggests not only a present importance, but also an importance to the

founding and development of America.11 The United States Supreme Court observed that the

framers placed a high value on the protection of contracts: “Contracts enable individuals to

order their personal and business affairs according to their particular needs and interests. Once

arranged, those rights and obligations are binding under the law, and the parties are entitled to

rely on them.” Allied Structural Steel Co. v. Spannaus, 438 U.S. 234, 245 (1978).

11 The clause resulted from the tenuous economic state of the Republic following the Revolution, and the uncertainty created by the states’ attempts at remedying the problem. These state measures included the enactment of laws that stayed collection of debts, laws that changed contracts to allow installments, laws allowing the payment of debts in commodities, state printing of new paper money, and laws designating the new paper money as legal tender for payment of debts. The framers of the Constitution recognized the instability caused by such contractual uncertainty, and understood the direct link between personal autonomy and the inviolability of contracts; therefore they sought to create a blanket assurance that private and public contracts would have the full force of law. James W. Ely Jr., “Economic Liberties and the Original Meaning of the Constitution,” 45 San Diego L.R. 673, 698-700 (2008).

28

“The modern Contract Clause analysis involves three components: “‘(1) Does a

contractual relationship exist, (2) does the change in the law impair that contractual relationship,

and if so, (3) is the impairment substantial?’” Koster v. City of Davenport, Iowa, 183 F.3d 762,

766 (8th Cir. 1999) (quoting Honeywell, Inc. v. Minn. Life and Health Ins. Guar. Assoc., 110

F.3d 547, 551 (8th Cir. 1997) (en banc)). “If a substantial impairment of a contractual

relationship exists, the legislation nonetheless survives a constitutional attack if the “impairment

is ... justified as ‘reasonable and necessary to serve an important public purpose.’” Id. (quoting

Parella v. Retirement Bd. of the R.I. Employees’ Retirement Sys., 173 F.3d 46, 59 (1st Cir.

1999)); see U.S. Trust Co. v. N.J., 431 U.S. 1, 25 (1977).

The Minnesota Constitution provides similar protections. Minnesota’s Contract Clause

provides: “No bill of attainder, ex post facto law, or any law impairing the obligation of contracts

shall be passed . . .” Minn. Const. art I, § 11. To establish a violation of the Minnesota Contract

Clause, “a court initially considers whether the state law has, in fact, operated as a substantial

impairment of a contractual obligation.” Jacobsen v. Anheuser-Busch, Inc., 392 N.W.2d 868,

872 (Minn. 1986). If a substantial impairment is found, “those urging the constitutionality of the

legislative act must demonstrate a significant and legitimate public purpose behind the

legislation.” Id.

2. Previous Legislatures had the Power to Bind Future Ones with regard to Pension Obligations.

Before turning to the three-part modern Contracts Clause analysis, Plaintiffs address

Defendants’ contention that the Minnesota Legislature in 1991 did not have the power to bind

future legislatures to utilize a specific statutory postretirement adjustment formula to increase the

Retirees’ pensions. See Def. Memo at 34. Defendants’ argument is without merit because the

State has not contracted away an essential attribute of its sovereignty.

29

Under its reserved powers, a state may not enter into a contract that limits its power to act