planned giving council of northeast florida annual symposium a 360 degree tour of planned giving...

TRANSCRIPT

Planned Giving Council of Northeast Florida

Annual Symposium

A 360 Degree Tour of Planned Giving

Audrey L. Johnson, CTFAVice PresidentWells Fargo Private Bank, Philanthropic [email protected]

Agenda

• Philanthropic Process

• Planned Giving: The Opportunity and Dilemma

• The Gifts: Donor Version

• Case Study: Confronting the Dilemma to Obtain the Opportunity

• Closing Thoughts/Resources

Philanthropy is Personal

• Make a difference • Feel financially secure• Support a cause• Leave/further a legacy • Involve family • Support the community • Set an example• Personal beliefs• Volunteer for the organization• Being asked• Business Interests

There are many reasons why individuals make charitable donations.

Philanthropic Planning Process

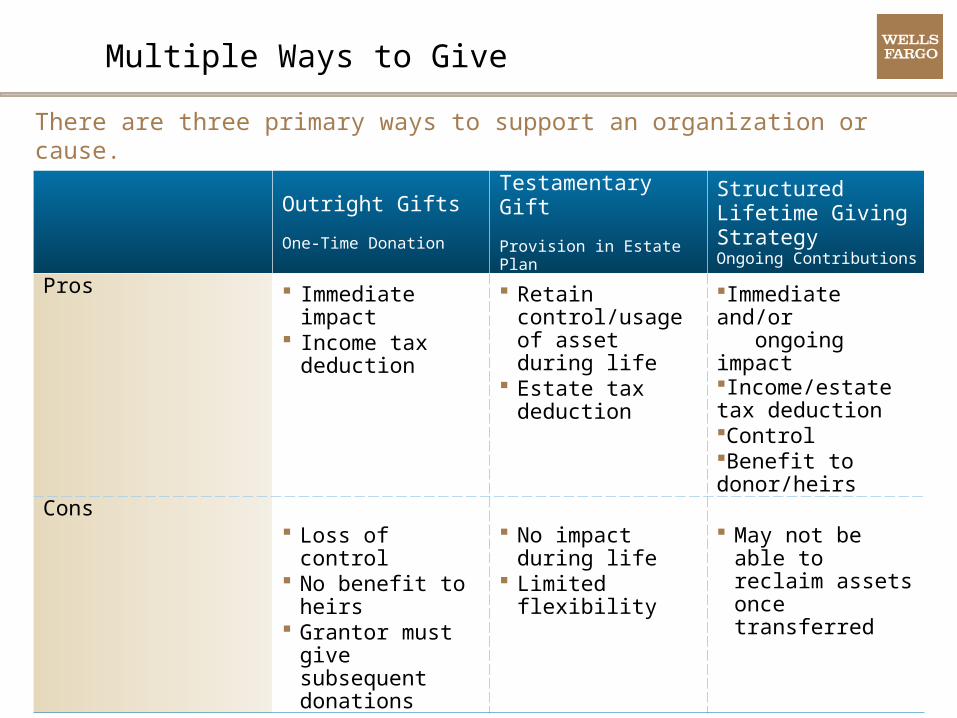

Multiple Ways to Give

There are three primary ways to support an organization or cause.

Outright Gifts

One-Time Donation

Testamentary Gift

Provision in Estate Plan

Structured Lifetime Giving StrategyOngoing Contributions

Pros Immediate impact

Income tax deduction

Retain control/usage of asset during life

Estate tax deduction

Immediate and/or

ongoing impact Income/estate tax deduction ControlBenefit to donor/heirs

Cons Loss of control No benefit to

heirs Grantor must

give subsequent donations

No impact during life

Limited flexibility

May not be able to reclaim assets once transferred

Planned Giving: The Opportunity and

Dilemma

Traditional Planned Giving Vehicles

• Bequests

• Charitable Gift Annuities

• Charitable Remainder Trusts

• Charitable Lead Trusts

Planned Giving: The Opportunity

• The next step in major gift fundraising and relationship building with your donors

• A great win-win opportunity

• A complement to your annual and major giving programs, and normally a major component of a comprehensive campaign

• Great opportunity to combine mission with values

• Other charitable organizations have planned giving programs and are receiving additional support through these programs

• Can be complicated

• Needs to be monitored

• Can involve many parties

• Deferred by design

• Requires consistency to be effective

• Charitable organizations may be missing opportunities for support by not having a planned giving program but infrastructure is required for the program to develop

Planned Giving: The Dilemma

The Gifts: Donor Version

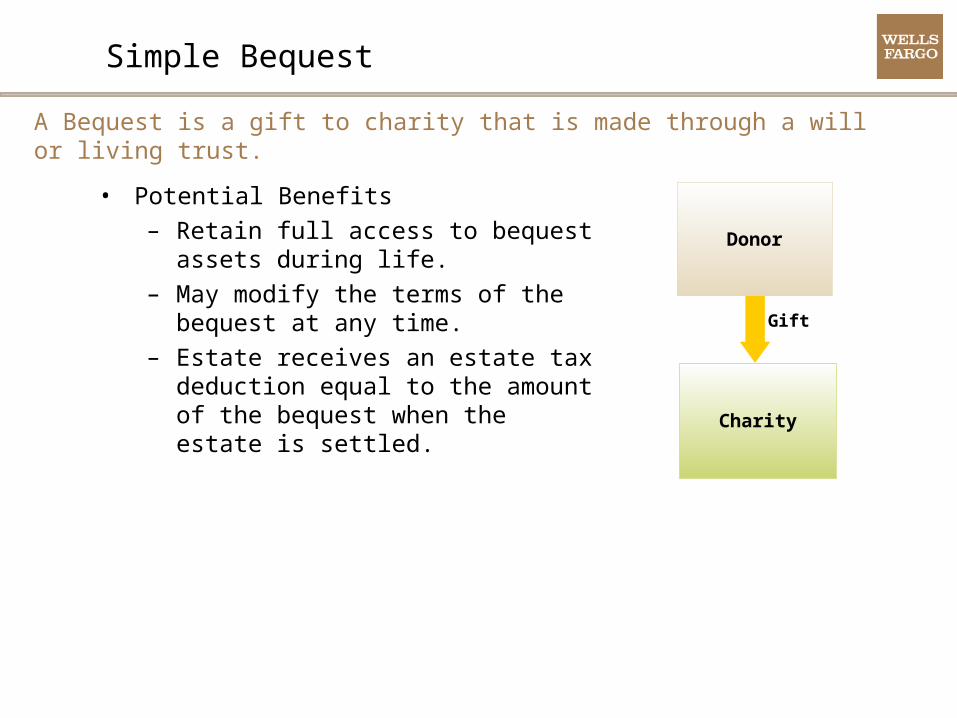

Simple Bequest

• Potential Benefits– Retain full access to bequest

assets during life.– May modify the terms of the

bequest at any time.– Estate receives an estate tax

deduction equal to the amount of the bequest when the estate is settled.

A Bequest is a gift to charity that is made through a will or living trust.

Donor

Gift

Donor

Charity

Types of Bequests

• Specific Bequest: specific dollar amount or specific asset.

• Percentage Bequest: a percentage of the donor’s estate or undivided interest in an asset.

• Residuary Bequest: after satisfying other bequests, donor gives residue or remainder of estate.

• Contingency Bequest: if other bequests cannot be honored, then those bequests go to charitable organization.

Charitable bequests can also take the form of beneficiary designations for IRA’s, qualified retirement plans, life insurance policies, and bank/brokerage account instructions to “pay/transfer on death” to charity.

Charitable Gift Annuity

• Potential Benefits– Receive an immediate or deferred

annuity– Receive an immediate income

tax deduction (based on the value of future interest)

– Not immediately subject to capital gains tax

– Removes assets from your taxable estate

– Converts non-income producing assets into a reliable fixed-income stream

– Initial gift amount is usually smaller than with other options

A Charitable Gift annuity creates a contract between donor and the charity. In exchange for your gift, the charity guarantees payment of the annuity amount.

Donor

Income

Principal Upon Death

Charitable Gift Annuity

Donor

Charity

Charitable Remainder Trust

• Potential Benefits– Receive an immediate income

tax deduction (on the remainder charitable interest)

– Not subject to capital gains on the sale of contributed assets

– Removes gifted assets from your taxable estate

– Pays income to you and/or a designated third party during lifetime

A Charitable Remainder Trust (“CRT”) splits beneficial ownership between a current income interest and a future charitable interest.

Donor

Gift Income

TrustRemainder

CRT

Donor

Charity

Charitable Lead Trust

• Potential Benefits– Leverages the gifting

program with a discounted gift value

– Removes gifted assets from your taxable estate

– Provides an income tax deduction on the amount gifted to charity

– Charity receives stream of income throughout your life or for a fixed number of years

– Remainder of funds go to family or a designated third party

A Charitable Lead Trust (“CLT”) splits beneficial ownership between a current charitable interest and a future non-charitable beneficiary.

Donor

Gift

Income

TrustRemainder

CLT

Donor

Charity

Beneficiaries

Case Study: From Dilemma to Opportunity

Dilemma #1 – Planned Giving is Complicated

How do we deal with the complex nature of planned giving?

Organizations should have policies and procedures in place to control the madness, know the needs of your donors and know the rules.

The purpose of policies and procedures is not necessarily to make each parties’ job easier, but instead to make the overall process run more efficiently.

Show me policies and procedures that everyone likes and I’ll show you a set of lousy policies and procedures.

Opportunity – Develop Policies & Procedures

Important Policies for a Planned Giving Program

• Board Resolution(s)• Gift Acceptance Policy• Investment Policy Statement• Severance Policy• Policy for Counting Gifts

– Naming opportunities– Endowment levels

Opportunity – Connect with the Donor

• Planned Giving Software has improved significantly over the years– Charts/ Diagrams– Projections– Investment Assumptions– Mortality/Actuarials– Taxation

• Great for explaining to advisors, but could be overkill for donors and their family.

• Simplify the Message /Focus on the Donor

Explaining the traditional planned gifts to Donors

PENNSYLVANIA

NEW YORKCT

MA

VT

NH

MAINE

ALASKA

WYOMING

COLORADO

ARIZONA

NEW MEXICO

TEXAS

OKLAHOMA

KANSAS

NEBRASKA

SOUTH DAKOTA

NORTH DAKOTA MINNESOTA

WISCONSIN

IOWA

ILLINOISIN

KENTUCKY

GEORGIA

MISSOURI

LA

HAWAII

MICHIGAN

CALIFORNIA

UTAH

NEVADA

IDAHO

OREGON

WASHINGTON

MONTANA

WV

NJOHIO

MD

DE

RILong Island

ARKANSAS

MS

FL

ALABAMA

NC

SC

DC

TENNESSEE

VIRGINIA

Red = Registration StateOrange = Notice StateGreen = Exempt StatePurple = Silent State

Opportunity – Know the Rules

Charitable Gift Annuity Regulatory Map

2222

Dilemma #2 – Planned Giving Involves Many Parties

Who needs to be involved and why?

Gift of property

Donor

CharitableGift

AnnuityCHARITY

Remainder toCHARITY

Income tax deductionFixed payments

How it works

You transfer cash, securities, or other property to CHARITY.

You receive an income tax deduction and may save capital gains tax.

CHARITY pays a fixed amount each year to you or to anyone you name for life. Typically,a portion of these payments is tax-free.

When the gift annuity ends, its remaining principal passes to CHARITY.

Opportunity – Understand the roles and responsibilities

Investment Committee

Board of DirectorsFinance

AccountingDevelopment

Legal

CPAAttorney

Financial Planner

Federal Government/

Internal RevenueService

State Department of Insurance

Other Charities

Beneficiaries

Appraiser

Auditors

BankFiduciary

Trust Company

The Potential Players in a Planned Giving Program

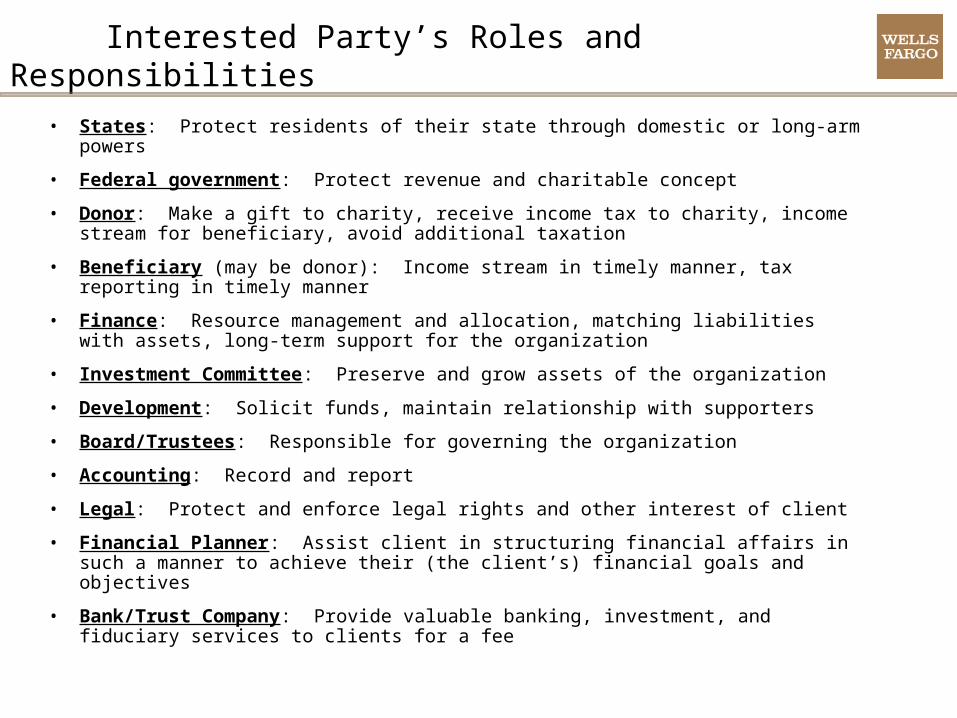

Interested Party’s Roles and Responsibilities

• States: Protect residents of their state through domestic or long-arm powers

• Federal government: Protect revenue and charitable concept

• Donor: Make a gift to charity, receive income tax to charity, income stream for beneficiary, avoid additional taxation

• Beneficiary (may be donor): Income stream in timely manner, tax reporting in timely manner

• Finance: Resource management and allocation, matching liabilities with assets, long-term support for the organization

• Investment Committee: Preserve and grow assets of the organization

• Development: Solicit funds, maintain relationship with supporters

• Board/Trustees: Responsible for governing the organization

• Accounting: Record and report

• Legal: Protect and enforce legal rights and other interest of client

• Financial Planner: Assist client in structuring financial affairs in such a manner to achieve their (the client’s) financial goals and objectives

• Bank/Trust Company: Provide valuable banking, investment, and fiduciary services to clients for a fee

2525

Dilemma #3 – Planned Giving must be Monitored

How do we structure an effective planned giving program?

Donor Development Staff

Finance/ Accounting

Office

Wells Fargo/Fiduciary Partner

Gift Development

Discuss Objectives & Request Information

Identify Prospects

Discuss solutions that your organization can provide to help Donor achieve objectives.

Maintain records of Donor interaction

Budget Support Provide technical support to Development Staff

Discuss ways to achieve Donor objectives

Make Development Staff and Finance Office aware of products and resources that may help facilitate gift

Establishing Charitable Gift

Review gift illustration with trusted advisor

Determine best funding assets

Request more illustrations if necessary

Fund gift

Execute Gift Agreement

Collect necessary Donor information

Review Gift Acceptance Policy

Work with Donor and Advisor to transfer assets

Send gift confirmation to Donor

Review proposed gift transaction

Authorize or facilitate necessary transactions

Review and Execute Gift Documents

Review and Execute Banking Documents

Work with Development Staff and Finance Office to establish necessary accounts

Provide Asset Delivery Instructions

Receive assets into appropriate account

Review Gift Agreements

Opportunity – Develop a Strategy and Utilize Resources

Sample Detailed Flowchart

Donor Development Staff

Finance/ Accounting Office

Wells Fargo/Fiduciary Partner

GiftAdministratio

n

Provide Development/ Wells Fargo with current payment information and mailing address

Set reminders to check-in with donor at least annually

Communicate important news opportunities with Donor

Follow up with Donor to address concerns identified by Finance Office and Wells Fargo

Review financial reports (i.e. FASB, Reserves, Investment Performance, Fund Accounting)

Work with Wells Fargo to develop Investment Policy Statement

Monitor Investment Performance

Set-up gift on PG Calc GiftWrap or appropriate trust system

Send payments and monitor payments in accordance with Gift Agreements

Provide Financial and Transactional Reports to Finance Office

Prepare and submit tax reports to Donor, Finance, and Government

Make sure gift assets are prudently invested in accordance with Investment Policy Statement

Conduct ongoing Due-Diligence on Investment Managers

Terminating The Gift

Estate notifies charity of death

Notify Wells Fargo of donor’s death

Provide instructions for distribution of gift residual

Close out gift on PG Calc GiftWrap or appropriate trust system

Distribute funds in accordance with instructions provided by Finance Office

File final tax report

Sample Detailed Flowchart (cont.)

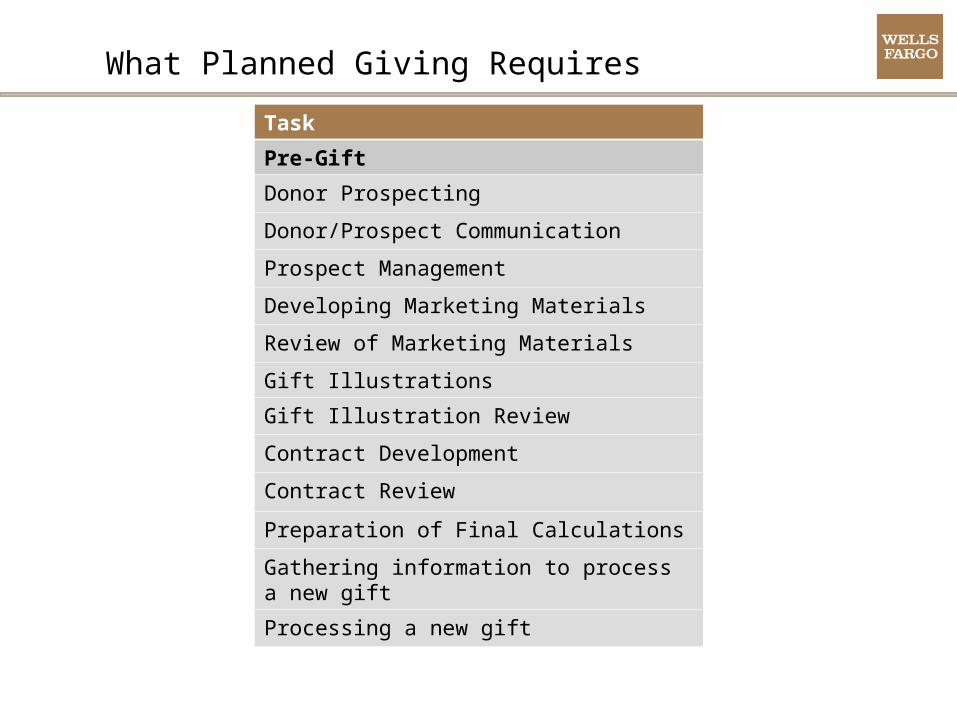

What Planned Giving Requires

Task

Pre-Gift

Donor Prospecting

Donor/Prospect Communication

Prospect Management

Developing Marketing Materials

Review of Marketing Materials

Gift Illustrations

Gift Illustration Review

Contract Development

Contract Review

Preparation of Final Calculations

Gathering information to process a new gift

Processing a new gift

What Planned Giving Requires (cont.)

Gift Administration

Generation of Periodic Annuity Payments

Recordkeeping (Physical and Electronic)

Research (client issues)

Monitoring/Reporting Outstanding Payment Distributions

Reconciling Outstanding Payment Distributions

Notification of death of a beneficiary

Notification of beneficiary address update

Reserve Calculations

FASB Calculations/Letters

SSAE 16 Audit Information

Distribution of 1099s/K-1 Letters

Fund Accounting

Tax Preparation

Task

What Planned Giving Requires (cont.)

Task

Policy Development

Investment Policy Statement (Development and Updates)

Gift Acceptance Policy

Investment Management

Investment Services

Rebalancing Assets according to Investment Policy

Compliance

State Compliance (Registration and Annual Reporting)

Training and Technical Support

Client Staff Training

Consulting on Gift Strategies

Program Strategy Sessions

Sample Calendar for a Charitable Gift Annuity ProgramJanuary:• Collect information for annual reports• Send out Form 1099 to annuitants by

1/31• Communicate with annuitants that their

tax information is in the mail, thank

donors for support

February:• Send Form 1096 to IRS by 2/28• Send any necessary payments to annuitants• Have a joint finance/development meeting to

wrap-up previous years results and review

expectations for current year• Complete annual report for State Department of

Insurance

March:• Investment committee meeting to review previous

year’s results• Submit annual report to State Department of

Insurance (if required), CY + 90 days• Send any necessary payments to annuitants• If 3/31 FYE, notify bank of need for annualized bank

statement for past 12 months & liability/reserve

reports

April:• Marketing to donors/annuitants• Send any necessary payments to

annuitants• Quarterly executive summary on CGA

program (1st Qtr. Results)• Submit annual report to State

Department of Insurance (if required)

CY+120

May• Send any necessary payments to annuitants• Send letter requesting an update on seasonal

addresses

June• Send any necessary payments to annuitants• If 6/30 FYE, notify bank of need for an annualized

bank statement for past 12 months &

liability/reserve reports.

July• Send any necessary payments to

annuitants • Collect information for annual reports (if

required)

August• Send any necessary payments to annuitants

September• Year end marketing to donors/annuitants• Send any necessary payments to annuitants• If filings required for a 9/30 FYE, notify bank of need

for an annualized bank statement for past 12

months.• If 9/30 FYE, notify bank of need for liability/reserve

reports

October:• Send any necessary payments to

annuitants• Verify banking and address

information for annuitants

November:• Send any necessary payments to annuitants• Marketing to donors/annuitants

December• Send any necessary payments to annuitants• Verify service provider staffing and holiday

schedule• If CYE, notify bank of need for an annualized bank

statement for past 12 months & liability/reserve

reports

Closing Thoughts and Resources

Closing Thoughts/Best Practices

The planned giving opportunity is worth the dilemma. Incorporate tools to address the challenges:

• Develop a gift acceptance policy with the scope of the planned giving program, age and gift minimums, and remainder severance policy

• Develop an investment policy statement for planned giving assets

• Develop a planned giving marketing strategy

• Educate board and staff; Educate donors; Educate advisors

• Invest 100% of the gift annuity amount

• Invest with fiduciary scope for planned giving assets

• Register with states for CGA programs; file annual report if necessary

• Keep accurate records, including donor due diligence

• Perform due diligence audit on CRT and CGA assets, investment management, and tax reporting

• Stewardship and Diligence: be sure to keep in touch with donors/ beneficiaries

• Benchmark, benchmark, benchmark

• Review policies and revise when necessary

• Share program impact

Planned Giving Resources

American Council on Gift Annuitieswww.acga-web.org

BoardSourcewww.boardsource.org

The Center on Philanthropy at Indiana Universitywww.philanthropy.iupui.edu

Giving USAwww.giving.usa.org

Planned Giving Design Centerwww.pgdc.org

Questions/Thank you

It has been a pleasure to spend this time with you.

If there are any questions, please contact me at:

[email protected] or 336.732.2987

Disclosures

Wells Fargo Wealth Management provides products and services through Wells Fargo Bank, N.A. and its various affiliates and subsidiaries.

The information and opinions in this report were prepared by Wells Fargo Wealth Management.Information and opinions have been obtained or derived from sources we consider reliable, but we

cannot guarantee their accuracy or completeness. Opinions represent Wells Fargo Wealth’s opinion as of the

date of this report and are for general information purposes only. Wells Fargo Wealth does not undertake to advise

you of any change in its opinions or the information contained in this report. Wells Fargo & Company affiliates

may issue reports or have opinions that are inconsistent with, and reach different conclusions from, this

report.

Wells Fargo & Company and its affiliates do not provide legal advice. Please consult your legal and tax advisors to

determine how this information may apply to your own situation. Whether any planned tax result is realized by

you depends on the specific facts of your own situation at the time your taxes are prepared.