plastics & packaging investment banking sector...

TRANSCRIPT

William Blair’s investment banking group combines signi�icant transaction experience, rich industry knowledge, and deep relationships to deliver successful advisory and �inancing solutions to our global base of corporate clients. We serve both publicly traded and privately held companies, executing mergers and acquisitions, growth �inancing, �inancial restructuring, and general advisory projects. This comprehensive suite of services allows us to be a long-term partner to our clients as they grow and evolve. From 2010 - 2013, the investment banking group completed 250 merger-and-acquisition transactions worth more than $52 billion in value, involving parties in 27 countries and four continents, was an underwriter on over 20% of all U.S. initial public offerings and arranged more than $11.5 billion of debt �inancing.

About William Blair Investment Banking

Sector Update August 2014

Plastics & Packaging Investment Banking Sector Report In this Issue: – Sector Trends and Insights – M&A Activity– Valuation Analysis

Plastics & Packaging Investment Banking

Elliot Farkas Managing Director [email protected] +1 312 364 8157

Paul M. Hindsley Managing Director [email protected] +1 312 364 8576

William Blair

Plastics & Packaging Insights Investment Banking Team Biographies

Investment Banking Team Biographies

William Blair & Company Plastics & Packaging Investment Banking

Elliot Farkas, managing director, has been a member of the William Blair & Company corporate finance department since 2006 and is based in Chicago. Elliot has more than 13 years of experience advising on buy and sell-side mergers and acquisitions, fairness opinions, private placements, recapitalizations, and public offerings and has completed over 75 transactions. Before joining the firm, Elliot worked at Robert W. Baird & Co. in the manufactured products investment banking group and at PricewaterhouseCoopers in the transaction services and audit and assurance advisory groups.

Elliot received an M.B.A. in finance from the University of Michigan and a B.S.B.A. in accounting from The Ohio State University. He is also a CPA.

+1 312 364 8157

Paul M. Hindsley, managing director in the consumer and industrial groups, has been a member of the William Blair & Company corporate finance department since 1997. Paul has 32 years of experience advising on mergers and acquisitions, private placement of equity and debt securities, and public offerings and has completed over 250 transactions. Before joining the firm, Paul worked at Nesbitt Burns Securities and Harris Bank as a senior banker for middle-market companies.

Paul received a B.A. from Duke University and an M.B.A. from Northwestern University.

+1 312 364 8576

Philip W. Reitz, managing director, joined William Blair & Company in 1989. As part of the commercial & industrial group, Phil specializes in merger and acquisition advisories for industrial companies. In addition, Phil has advised clients on numerous public equity underwritings and private equity and debt placements.

Phil has a B.A. from Northwestern and an M.B.A. from Stanford where he was an Arjay Miller Scholar (top ten percent of class).

+1 312 364 8688

William Blair

Plastics & Packaging Insights Selected Recent William Blair Plastics & Packaging Transactions

Selected Recent William Blair Plastics & Packaging Transactions

Not Disclosed

has been acquired by

The Lubrizol Corporation

July 2014

Not Disclosed

has been acquired by

Olympus Partners

May 2014

Not Disclosed

has sold select assets to

WNA, Inc.

March 2014

Not Disclosed

has been acquired by

Wabtec Corporation

September 2013

Not Disclosed

has been acquired by

Pactiv, LLC

March 2013

Not Disclosed

has been acquired by

Schattdecor AG

January 2013

Not Disclosed

a division of Pregis

has been acquired by

Monitor Clipper Partners

October 2012

Not Disclosed

has been acquired by

Graham Partners

September 2012

Not Disclosed

North American Operations

has been acquired by

Arclin, Inc.

July 2012

$79,120,000

Initial Public Offering

February 2012

$247,500,000

has been acquired by

Odyssey Investment Partners, LLC

August 2012

$248,000,000

has been acquired by

Snow Phipps Group, LLC

July 2012

$72,450,000

Initial Public Offering

February 2012

$135,500,000

Subsidiaries of Contex Group A/S

have been acquired by

3D Systems Corporation

January 2012

€160,000,000

A division of Pregis Corporation

has been acquired by

Sun Capital Partners

December 2011

$181,700,000

has been acquired by

Phillips Plastics Corporation

August 2011

Not Disclosed

a portfolio company of

Mason Wells

has been acquired byHighlander Partners

December 2010

Not Disclosed

has been acquired by

WynnchurchCapital, Ltd.

December 2010

Not Disclosed

has been acquired by

Filtrona plc

November 2010

Not Disclosed

Senior Debt Placement/Recapitalization

December 2009

$115,000,000

a subsidiary of Filtrona plc

has been acquired by

Saw Mill Capital

March 2009

Not Disclosed

has been acquired by

Vesta Inc.

March 2009

Not Disclosed

has been acquired by

Parker Hannifin

April 2008

Not Disclosed

has completed a recapitalization with

Pouschine Cook Capital Management Inc.

December 2007

William Blair

Plastics & Packaging Insights Selected William Blair Plastics & Packaging Transactions

Selected William Blair Plastics & Packaging Transactions

Pregis Corporation Case Study

William Blair & Company acted as financial advisor to Pregis Corporation, a portfolio

company of AEA Investors, in connection with its sale to Olympus Partners. Terms of the transaction were not disclosed.

Based in Deerfield, Illinois, Pregis Corporation is a leading global provider of innovative protective packaging materials and systems. The company offers solutions for a wide variety of consumer and industrial market segments, including food, beverage, healthcare, medical devices, agricultural, e-commerce, retail, automotive, furniture, electronics, construction, and military/aerospace. Pregis’ high growth systems business provides a high margin, recurring revenue stream.

AEA is a private equity firm focused on middle-market companies and is based in New York. AEA focuses on control buyouts in four industry sectors: value-added industrial products, specialty chemicals, consumer products, and related services.

Olympus Partners is a private-equity firm focused on providing equity capital for middle-market management buyouts and for companies needing capital for expansion. Olympus is an active, long-term investor across a broad range of industries, including consumer products, healthcare, financial services, and business services.

Pactiv Divestiture Case Study

William Blair & Company acted as financial advisor to Pactiv LLC, a portfolio company

of Rank Group, in connection with the sale of select plastics assets to Waddington North America Inc. (WNA). Terms of the transaction were not disclosed.

Based in Lake Forest, Illinois, Pactiv is a global packaging operation of more than 11,000 employees with more than 50 manufacturing plants, mixing centers, and distribution centers.

Based in Covington, Kentucky, WNA is a leading manufacturer of disposable drinkware, dinnerware, serving ware, cutlery, and custom packaging with a broad line of upscale products. WNA is owned by Olympus Partners, a private-equity firm founded in 1988 that makes equity investments in middle-market leveraged buyouts and minority ownership financings.

Having sold Spirit Foodservice, Inc. to Pactiv in March 2013, William Blair & Company’s packaging bankers were aware that certain acquired product lines were less of a strategic fit with Pactiv and that WNA had expressed interest in those assets in an earlier sale process. William Blair made the introduction, developed the valuation that was acceptable to both parties, and assisted in negotiating the final terms of the transaction.

Not Disclosed

William Blair & Company is pleased to announce that

A portfolio company of AEA

has been acquired by

William Blair & Company acted as financial advisor to Pregis Corporation

in the above Transaction

May 2014

Not Disclosed

William Blair & Company is pleased to announce that

A portfolio company of Rank Group

has sold select assets to

William Blair & Company acted as financial advisor to Rank Group and

Pactiv in the above Transaction

March 2014

William Blair

Plastics & Packaging Insights Table of Contents

Table of Contents

Industry Review and Outlook ................................................................................................................................................................................................................... 1

Recent Notable Plastics & Packaging Transactions ........................................................................................................................................................................ 3

Current Industry Trends .......................................................................................................................................................................................................................... 10

Public Plastics & Packaging Company Valuations ........................................................................................................................................................................ 14

William Blair

Plastics & Packaging Insights Industry Review and Outlook 1

Industry Review and Outlook

M&A Activity

M&A activity in the plastics and packaging sector increased dramatically in the first half of 2014, with transaction activity rising 55% from the first half of 2013, after an 18% increase in the second half of 2013. The first half of 2014 plastics and packaging sector deal volume was notably better than the overall global M&A market, which increased roughly 0.5% (the middle market declined 1.4%) during the same period. Transaction activity was strongest during the second quarter of 2014, up 18% sequentially over the first quarter and up 64% over the second quarter of 2013. We noted a marked increase in overall market activity in the first half of 2014 and expect this momentum to carry into the second half of the year.

Global Plastics & Packaging Sector Transaction Volume(1)

(number of deals)

Global Plastics & Packaging Sector Transaction Value(1)

($ in millions)

(1) Aggregate volume and value includes all announced deals. Sources: Dealogic and William Blair’s Mergers and Acquisitions market analysis.

Aggregate transaction value was also up significantly year-over-year, principally due to an increase in large-sized deals, many of which were absent in 2013. Deal value in 2014 was driven by a large number of $750 million-plus transactions, such as the Carlyle Group’s acquisition of Signode Packaging Systems ($3.2 billion), Clayton Dubilier & Rice’s acquisition of Mauser ($1.7 billion), and Montagu’s acquisition of Rexam’s pharmaceutical devices and prescription packaging division ($805 million). Other notable transactions in 2014 were Golden Gate Capital’s purchase of Phillips-Medisize ($800 million), as well as Pritzker Group’s purchase of Technimark ($450 million) and Olympus Partners’ purchase of Pregis for an undisclosed amount. We believe that plastics and packaging M&A activity will remain strong into 2014 as the domestic and global economies continue to improve and as factors such as debt financing multiples, private-equity capital, and the need for strategic growth continue to drive M&A activity.

258 233 252 266

343 336 307 272 301

269 278 270

134 111 159 172

0

100

200

300

400

500

600

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2H '12 1H '13 2H '13 1H '14

Median: 271

+18.7%

+55.0%

$9,938 $8,362

$16,941 $19,717

$17,192

$47,281 $43,882

$12,093 $18,583

$21,387 $15,998

$9,655 $6,760 $2,719

$6,936

$17,467

$0

$10,000

$20,000

$30,000

$40,000

$50,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2H '12 1H '13 2H '13 1H '14

Median: $17,067

+2.6%

>6x

William Blair

Plastics & Packaging Insights 2 Industry Review and Outlook

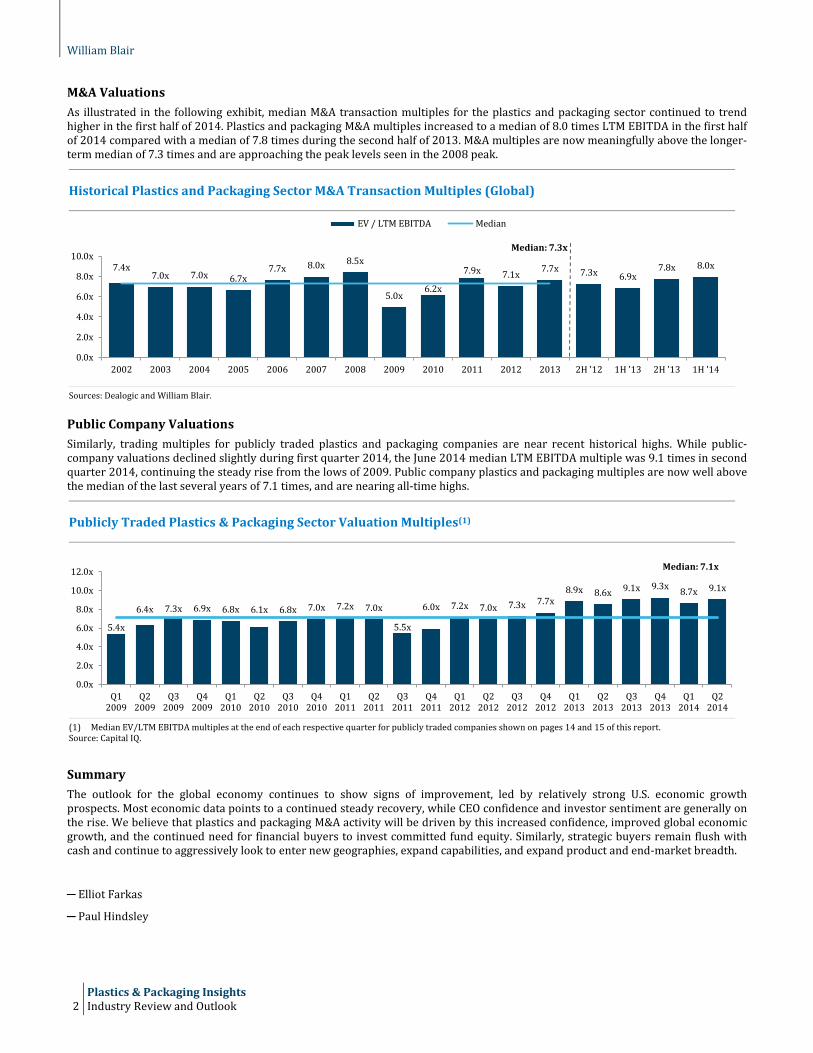

M&A Valuations

As illustrated in the following exhibit, median M&A transaction multiples for the plastics and packaging sector continued to trend higher in the first half of 2014. Plastics and packaging M&A multiples increased to a median of 8.0 times LTM EBITDA in the first half of 2014 compared with a median of 7.8 times during the second half of 2013. M&A multiples are now meaningfully above the longer-term median of 7.3 times and are approaching the peak levels seen in the 2008 peak.

Historical Plastics and Packaging Sector M&A Transaction Multiples (Global)

Sources: Dealogic and William Blair.

Public Company Valuations

Similarly, trading multiples for publicly traded plastics and packaging companies are near recent historical highs. While public-company valuations declined slightly during first quarter 2014, the June 2014 median LTM EBITDA multiple was 9.1 times in second quarter 2014, continuing the steady rise from the lows of 2009. Public company plastics and packaging multiples are now well above the median of the last several years of 7.1 times, and are nearing all-time highs.

Publicly Traded Plastics & Packaging Sector Valuation Multiples(1)

(1) Median EV/LTM EBITDA multiples at the end of each respective quarter for publicly traded companies shown on pages 14 and 15 of this report. Source: Capital IQ.

Summary

The outlook for the global economy continues to show signs of improvement, led by relatively strong U.S. economic growth prospects. Most economic data points to a continued steady recovery, while CEO confidence and investor sentiment are generally on the rise. We believe that plastics and packaging M&A activity will be driven by this increased confidence, improved global economic growth, and the continued need for financial buyers to invest committed fund equity. Similarly, strategic buyers remain flush with cash and continue to aggressively look to enter new geographies, expand capabilities, and expand product and end-market breadth.

─ Elliot Farkas

─ Paul Hindsley

7.4x7.0x 7.0x 6.7x

7.7x 8.0x 8.5x

5.0x6.2x

7.9x 7.1x7.7x 7.3x 6.9x

7.8x 8.0x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2H '12 1H '13 2H '13 1H '14

Median: 7.3x

EV / LTM EBITDA Median

5.4x

6.4x 7.3x 6.9x 6.8x 6.1x 6.8x 7.0x 7.2x 7.0x

5.5x

6.0x 7.2x 7.0x 7.3x 7.7x8.9x 8.6x 9.1x 9.3x

8.7x 9.1x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

Q12009

Q22009

Q32009

Q42009

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Median: 7.1x

William Blair

Plastics & Packaging Insights Recent Notable Plastics & Packaging Transactions 3

Recent Notable Plastics & Packaging Transactions

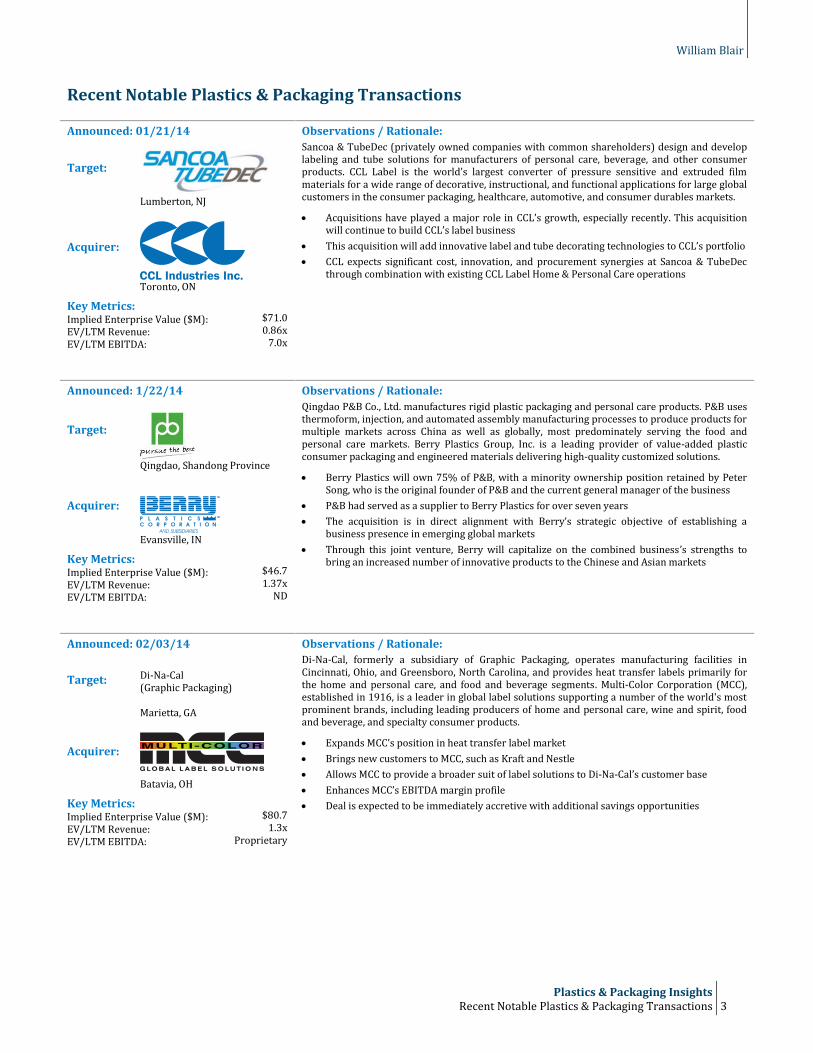

Announced: 01/21/14 Observations / Rationale:

Target:

Sancoa & TubeDec (privately owned companies with common shareholders) design and develop labeling and tube solutions for manufacturers of personal care, beverage, and other consumer products. CCL Label is the world's largest converter of pressure sensitive and extruded film materials for a wide range of decorative, instructional, and functional applications for large global customers in the consumer packaging, healthcare, automotive, and consumer durables markets.

Acquisitions have played a major role in CCL’s growth, especially recently. This acquisition will continue to build CCL’s label business

This acquisition will add innovative label and tube decorating technologies to CCL’s portfolio

CCL expects significant cost, innovation, and procurement synergies at Sancoa & TubeDec through combination with existing CCL Label Home & Personal Care operations

Lumberton, NJ

Acquirer:

Toronto, ON Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$71.0 0.86x

7.0x

Announced: 1/22/14 Observations / Rationale:

Target:

Qingdao P&B Co., Ltd. manufactures rigid plastic packaging and personal care products. P&B uses thermoform, injection, and automated assembly manufacturing processes to produce products for multiple markets across China as well as globally, most predominately serving the food and personal care markets. Berry Plastics Group, Inc. is a leading provider of value-added plastic consumer packaging and engineered materials delivering high-quality customized solutions.

Berry Plastics will own 75% of P&B, with a minority ownership position retained by Peter Song, who is the original founder of P&B and the current general manager of the business

P&B had served as a supplier to Berry Plastics for over seven years

The acquisition is in direct alignment with Berry’s strategic objective of establishing a business presence in emerging global markets

Through this joint venture, Berry will capitalize on the combined business’s strengths to bring an increased number of innovative products to the Chinese and Asian markets

Qingdao, Shandong Province

Acquirer:

Evansville, IN Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$46.7 1.37x

ND

Announced: 02/03/14 Observations / Rationale:

Target:

Di-Na-Cal (Graphic Packaging)

Di-Na-Cal, formerly a subsidiary of Graphic Packaging, operates manufacturing facilities in Cincinnati, Ohio, and Greensboro, North Carolina, and provides heat transfer labels primarily for the home and personal care, and food and beverage segments. Multi-Color Corporation (MCC), established in 1916, is a leader in global label solutions supporting a number of the world's most prominent brands, including leading producers of home and personal care, wine and spirit, food and beverage, and specialty consumer products.

Expands MCC’s position in heat transfer label market

Brings new customers to MCC, such as Kraft and Nestle

Allows MCC to provide a broader suit of label solutions to Di-Na-Cal’s customer base

Enhances MCC’s EBITDA margin profile

Deal is expected to be immediately accretive with additional savings opportunities

Marietta, GA

Acquirer:

Batavia, OH Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$80.7

1.3x Proprietary

William Blair

Plastics & Packaging Insights 4 Recent Notable Plastics & Packaging Transactions

Announced: 02/7/14 Observations / Rationale:

Target:

(Black Diamond Capital)

Constar manufactures and supplies polyethylene terephthalate plastic (PET) containers for food and beverage companies in the United States and internationally. It offers hot fill bottles for enhanced waters, juices, energy drinks, and RTD teas. Plastipak Packaging, Inc. develops and manufactures packaging products for the food and beverage and the cleaning supplies industries.

Constar’s North American assets were acquired out of bankruptcy, the third time Constar has been through bankruptcy

Constar's talent and technology will allow Plastipak to bring to its customers a complete portfolio of solutions in rigid beverage packaging

Trevose, PA

Acquirer:

Plymouth, MI Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$102.5

0.54x ND

Announced: 2/13/14 Observations / Rationale:

Target:

(Paper Packaging Division)

Bemis Paper Packaging Division is a supplier of multiwall paper bags for food and other applications. Hood Packaging supplies paper flexible packaging and bags, consumer plastic packaging, and industrial plastic packaging from its facilities across the United States and Canada.

The sale will allow Bemis to focus on strategic opportunities in high barrier, multilayer flexible packaging, medical and pharmaceutical packaging, and other plastics packaging solutions as well as developing geographic markets

Bemis’s Paper Packaging Division’s multiwall paper business was focused on food and consumer goods

The multiwall paper segment is mature and undergoing consolidation led by firms like privately held Hood Packaging and publicly held Graphic Packaging

(Bemis Company, Inc.) Neenah, WI

Acquirer:

(Hood Companies, Inc.)

Madison, Mississippi and Burlington, Ontario

Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

ND ND ND

Announced: 2/19/14 Observations / Rationale:

Target:

Benson Box Ltd. manufactures and supplies printed folding cartons for the food and pharmaceutical industries in the United Kingdom and other European countries. Graphic Packaging Holding Company (NYSE: GPK) is a leading provider of packaging solutions for a wide variety of products to food, beverage, and other consumer products companies.

Benson Group brings more than 200 customers and roughly 940 employees to Graphic Packaging, and operates four folding-carton facilities in the United Kingdom that convert about 80,000 tons of paperboard annually

Acquisition enhances Graphic Packaging's European platform by broadening its offerings in food and consumer products and extending the business into the store brand market

Combination creates a $700 million-plus business in Europe. Acquisition is Graphic’s third in the European folding-carton market in the last three years

It is expected to generate $5 million to $7 million of synergies over the next 18 months

Bardon, UK

Acquirer:

Atlanta, GA Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$165.0

0.83x 6.6x

William Blair

Plastics & Packaging Insights Recent Notable Plastics & Packaging Transactions 5

Announced: 3/11/14 Observations / Rationale:

Target: Capri Packaging Inc.

Capri Packaging Inc. manufactures printed flexible plastic packaging products. Capri Packaging Inc. operated as a subsidiary of Schreiber Foods Inc. TC Transcontinental is the largest printer and leading provider of media and marketing activation solutions in Canada. It specializes in print and digital media, the production of magazines, newspapers, books and custom content, mass and personalized marketing, interactive and mobile applications, and door-to-door distribution.

The transaction represents a strategic move for Transcontinental into a new promising area, flexible packaging, where it can significantly leverage its manufacturing competencies

The printed flexible packaging industry was identified as a natural fit given that the production process is very similar to Transcontinental's printing operations and the market offers many opportunities for growth

As part of the transaction, the seller, Schreiber Foods, Inc., has signed a 10-year agreement to secure Capri Packaging as a strategic supplier of printed flexible packaging, which represents about 75% of Capri's total revenues

Transcontinental is expected to continue to build its new flexible packaging platform and diversify its customer base in flexibles

Clinton, MO

Acquirer:

St. Leonard, Quebec Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$133.0

1.85x ~7.8x

Announced: 03/13/14 Observations / Rationale:

Target:

(Medical Action Industries NASD:MDCI)

Medegen develops medical devices and components, and provides contract manufacturing services to healthcare, medical device, and pharmaceutical industries in the United States and internationally. Inteplast Group's three divisions—AmTopp, Integrated Bagging Systems, and World-Pak—offer a diverse product line including BOPP film, stretch film, and XF cross-laminated film; grocery, merchandise, and garment bags; trash can liners and other plastic bags and supplies; fluted plastic sheets; and free foam and celuka PVC sheets.

Medegen will enhance Inteplast's existing portfolio of disposable medical and hospital products

Transaction will reduce Medegen’s exposure to volatility in resin pricing and enables it to focus additional time and resources on building stockholder value through the optimization of its core business units

Inteplast was attracted to Medegen’s technical expertise and market leadership

Gallaway, TN

Acquirer:

Livingston, NJ Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$78.6

ND ND

Announced: 03/24/14 Observations / Rationale:

Target:

Rexam’s Healthcare Containers and Closures business produces bottles, closures and specialty products for pharmaceutical and OTC applications. The transaction includes eight manufacturing locations—five in the United States and one each in Mexico, France, and India—with total employees of about 1,500. Berry Plastics Group, Inc. is a leading provider of value-added plastic consumer packaging and engineered materials delivering high-quality customized solutions.

The acquisition will increase Berry’s sales in healthcare packaging to more than $500 million

The U.S. portion has a highly synergistic fit with Berry’s existing healthcare product portfolio, while the facilities located outside the United States will allow Berry to increase its presence in the attractive global healthcare market

Berry expects the acquisition will be deleveraging after synergies (post-synergy multiple is estimated to be less than 5.5 times)

(US, Mexico, India Healthcare C&C business) London, UK

Acquirer:

Evansville, IN Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

~$135.0

~0.52x ~7.0x

William Blair

Plastics & Packaging Insights 6 Recent Notable Plastics & Packaging Transactions

Announced: 04/01/14 Observations / Rationale:

Target:

Boltaron is a leading North American producer of thermoplastic sheet for components used in aircraft and mass-transit vehicle interiors, as well as for applications in the construction, chemical process, and semiconductor industries. Simona manufactures and warehouses thermoplastics. The company offers polymeric sheet and semifinished plastics.

Simona gains diversified capabilities, a major position in high-value engineering plastics, and a sales network with proven success in marketing high-value sheet to engineering specifiers of aerospace and other high-value components

Through the acquisition, Simona also gains the only manufacturing facility in North America with extrusion, calendaring, and press laminating under one roof, allowing the production of specialized film and sheet products in thicknesses ranging from .076 to 76.0 mm, as well as multilayer composites having unique properties

Collectively, the combined entity will now span the entire market with high-volume commodity grades up to high-performance aerospace grades

Acquisitions reaffirms Simona’s strategy of expansion in the U.S. plastics market

Newcomerstown, OH

Acquirer:

Kirn, Germany Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

ND ND ND

Announced: 4/22/14 Observations / Rationale:

Target:

Pregis Corporation is a leading global provider of innovative protective packaging materials and systems. The company offers solutions for a wide variety of consumer and industrial market segments, including food, beverage, healthcare, medical devices, agricultural, e-commerce, retail, automotive, furniture, electronics, construction, and military/aerospace. Olympus Partners is a private-equity firm focused on providing equity capital for middle-market management buyouts and for companies needing capital for expansion.

Represents final transaction following AEA’s carve-out of Pregis from Pactiv in 2005

Pregis’ high growth, high margin systems business was attractive to buyers, particularly those with a strong thesis around e-commerce growth

Pregis’s primary products include systems, bubble wrap, and foam for inside-the-box applications

Pregis’s partnership with Olympus will accelerate the realization of the company’s strategic vision through enhanced product development, market diversification, and continued acquisitions

(AEA) Deerfield, IL

Acquirer:

Stamford, CT Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

Proprietary Proprietary Proprietary

Announced: 04/22/14 Observations / Rationale:

Target:

(HIG Capital)

Vaupell was founded in Seattle, Washington, in 1947 and supplied the first plastic parts to Boeing. Vaupell designs, engineers, and produces custom, high-performance engineered plastic and composite components and assemblies for demanding applications. Sumitomo Bakelite manufactures and sells semiconductor materials, and circuit and plastic products, in Asia, North America, and Europe.

Sumitomo Bakelite has expanded its High Performance Plastics (HPP) business into areas in which it can leverage accumulated technologies related to the automotive industry

Sumitomo Bakelite had been looking to enter the aerospace interiors business, given that it could apply its accumulated technologies and take advantage of the growing demand for plastics in aircraft to save weight and reduce fuel consumption

During H.I.G.’s ownership, Vaupell made two sizeable acquisitions, expanded its product line and capabilities, invested in new technologies, and made strategic investments to support its customers by opening new facilities in Everett, Washington, and Shenzhen, China

Seattle, WA

Acquirer:

Tokyo, Japan Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$265.0

2.15x Proprietary

William Blair

Plastics & Packaging Insights Recent Notable Plastics & Packaging Transactions 7

Announced: 4/28/14 Observations / Rationale:

Target:

Technimark is a global manufacturer of custom rigid plastic packaging and components, primarily for the consumer packaged goods, household care, and specialty industrial markets. The Pritzker Group is a private-equity and venture capital firm specializing in acquisitions, management-led buyouts, family and founder liquidity, family- or entrepreneur-owned businesses, corporate divestitures, growth capital, industry consolidations, debt, add-on acquisitions, and middle-market investments.

Technimark provides a full range of services, including packaging design and production materials, receiving, and distribution

Pritzker Group was attracted to Technimark’s market leadership position, strong management team, and growth prospects

Pritzker Group will provide Technimark with the long-term resources it needs to continue expanding its geographic footprint and product capabilities

The Wellington family, founders of Technimark, invested alongside Pritzker, and will continue to manage the company

(Quad-C) Asheboro, NC

Acquirer:

Chicago, IL Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$450.0

1.16x ~8.5x

Announced: 5/1/14 Observations / Rationale:

Target:

Pretium Packaging, LLC is one of the nation’s largest manufacturers of customized, high performance rigid blow-molded plastic bottles and containers. Pretium utilizes its national manufacturing footprint, design and engineering capabilities, and full range of process capabilities to provide customized solutions to its customers in the food and specialty beverage, private-label, pharmaceutical, personal care and household and industrial sector. Genstar Capital is a private-equity firm specializing in management buyouts, recapitalizations, and add-on acquisitions of middle-market public or private companies.

Pretium distinguishes itself through service, flexibility, speed-to-market, and engineering capabilities. The company sells to a diversified customer base ranging from Fortune 500 companies to smaller privately owned businesses

Pretium fits well with Genstar’s investment thesis for the packaging industry

The acquisition enables Pretium to further pursue growth investments and strategic acquisitions to expand product capabilities and enter new end-markets and geographies

(Castle Harlan) Chesterfield, MO

Acquirer:

San Francisco, CA Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$331.0 ~2.06x

~8.8x

Announced: 05/01/14 Observations / Rationale:

Target:

Ace is one of the Far East's leaders in the manufacture of plastic injection-molded components and injection-molding tools for niche segments in the packaging, lifestyle, medical, power, and automotive end markets. Based in Hong Kong, ACE operates five advanced production plants in mainland China with about 3,300 employees. RPC is an international rigid plastic packaging supplier to the food and non-food, consumer, and industrial markets. It operates through its injection molding, thermoforming, and blow molding segments.

ACE's focus on high-growth niche segments and portfolio of high quality innovative products supported by significant market and product expertise with complementary mold-making capabilities were attractive to RPC

ACE had also been a long-term supplier of molds for RPC

RPC funded the purchase through the issue of new shares, new debt, and existing cash reserves

Opportunity for RPC to establish a meaningful platform in Asia

Ability to enhance ACE’s stand-alone growth strategy by leveraging RPC’s network

Kwai Chung, Hong Kong

Acquirer:

Rushden, UK Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$427.3

2.38x 7.4x(1)

(1) Up to 10.5x with earn-out consideration

William Blair

Plastics & Packaging Insights 8 Recent Notable Plastics & Packaging Transactions

Announced: 05/07/14 Observations / Rationale:

Target:

(Kohlberg & Co.)

Phillips-Medisize is a leading global provider of design and manufacturing services to the pharmaceutical, medical device, diagnostic, and specialty commercial markets. The Company receives about 75% of total revenue from drug delivery, medical device, primary pharmaceutical packaging, and diagnostic products. Golden Gate Capital is a private-equity firm specializing in leveraged buyouts, recapitalizations, restructuring, corporate extractions, carve-outs, distressed, bankruptcy restructurings, refinancing, public-to-private transactions, and public equities.

Golden Gate's financial support, successful record of backing manufacturing companies, and deep industry relationships will help perpetuate the company's strong momentum

Phillips-Medisize represents an opportunity for Golden Gate to invest in a strong design and manufacturing service platform with global scale and a proven track record of delivering an exceptionally broad and deep set of capabilities to customers

Phillips-Medisize is well positioned to grow in the rapidly expanding medical outsourcing market

Hudson, WI

Acquirer:

San Francisco, CA Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$800.0 ~1.33x ~10.0x

Announced: 06/4/14 Observations / Rationale:

Target:

Ferro Corporation is a leading global supplier of technology-based performance materials and chemicals. The specialty plastics segment's products include color additives and concentrates with a focus on high-margin color, combination, and additive masterbatches; filled and reinforced plastics with a strong position in glass-filled polypropylene and custom formulating capabilities; advanced polymer compounds and alloys including melt-processable rubber, molding and extrusion materials, and custom compounds. A. Schulman, Inc. is a leading international supplier of high-performance plastic compounds and resins.

Acquisition is an excellent strategic complement to A. Shulman’s existing capabilities and reflects ongoing efforts to expand their product offering and geographic reach in target markets

A. Schulman anticipates achieving about $5.5 million in synergies within 12 to 18 months following the close of the transaction, driven primarily by sourcing activities and plant efficiency actions

The specialty plastics assets included in the pending transaction generated sales of $154 million in 2013, with about two-thirds of these in the United States

Strategically combining the two businesses provides the existing customers of the specialty plastics segment with an expanded product portfolio, technical solutions, and global resources with the full support of the A. Schulman team

(Specialty Plastics Business) Mayfield Heights, OH

Acquirer:

Fairlawn, OH Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

$91.0 0.59x

ND

Announced: 6/17/14 Observations / Rationale:

Target:

/

Ecoplast Corporation is a leading supplier of recycled and custom compounded resins in the United States. Envision Plastics Industries LLC produces post-consumer high-density polyethylene resins for food, beverage, personal care, consumer healthcare, and general-purpose industries in North America. Consolidated Container Company is a leading developer and manufacturer of rigid plastic packaging solutions in the United States. CCC specializes in customized mid- and short-run packaging solutions, serving a diverse customer base in the dairy, household chemicals, food, industrial/specialty chemicals, water, and beverage/juice markets.

This is the first time Consolidated Container Company will actually process its own recycled plastics

CCC is in a position to help accelerate the growth of Envision and Ecoplast by leveraging its market presence

Envision and Ecoplast will operate as a stand-alone business led by the existing management team

Fontana, CA / Reidsville, NC

Acquirer:

(Bain Capital) Atlanta, GA

Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

ND ND ND

William Blair

Plastics & Packaging Insights Recent Notable Plastics & Packaging Transactions 9

Announced: 6/17/14 Observations / Rationale:

Target:

Duro Bag is a manufacturer and marketer of retail and luxury paper bags, for foodservice, grocery, wholesale-distribution, and other industries. The company produces grocery bags, handle bags, compostable paper lawn and leaf bags, and various specialty bags, including lunch bags, pharmacy bags, Freshness Paper bread bags, foodservice bags, as well as a broad range of premium paper shopping bags for luxury retailers in North America. Hilex Poly is an industry-leading manufacturer of flexible packaging products, ranging from bags for grocery, retail, and food service markets, to can liners and specialty films.

The acquisition of Duro Bag will enable Hilex to expand its portfolio of 100% recyclable products to include paper as well as broaden its reach to other market segments

Hilex continues to focus on developing products that are recyclable, sustainable, and environmentally friendly

Duro Bag, which bills itself as the largest paper bag manufacturer in North America, has 2,500 employees, including 800 in Greater Cincinnati. It operates 10 manufacturing facilities around the country

The combined company will have more than 3,000 manufacturing jobs in the United States and more than 600 in Canada and Mexico

Florence, KY

Acquirer:

(Wind Point Partners)

Hartsville, SC Key Metrics: Implied Enterprise Value ($M): EV/LTM Revenue: EV/LTM EBITDA:

ND ND ND

William Blair

Plastics & Packaging Insights 10 Current Industry Trends

Current Industry Trends

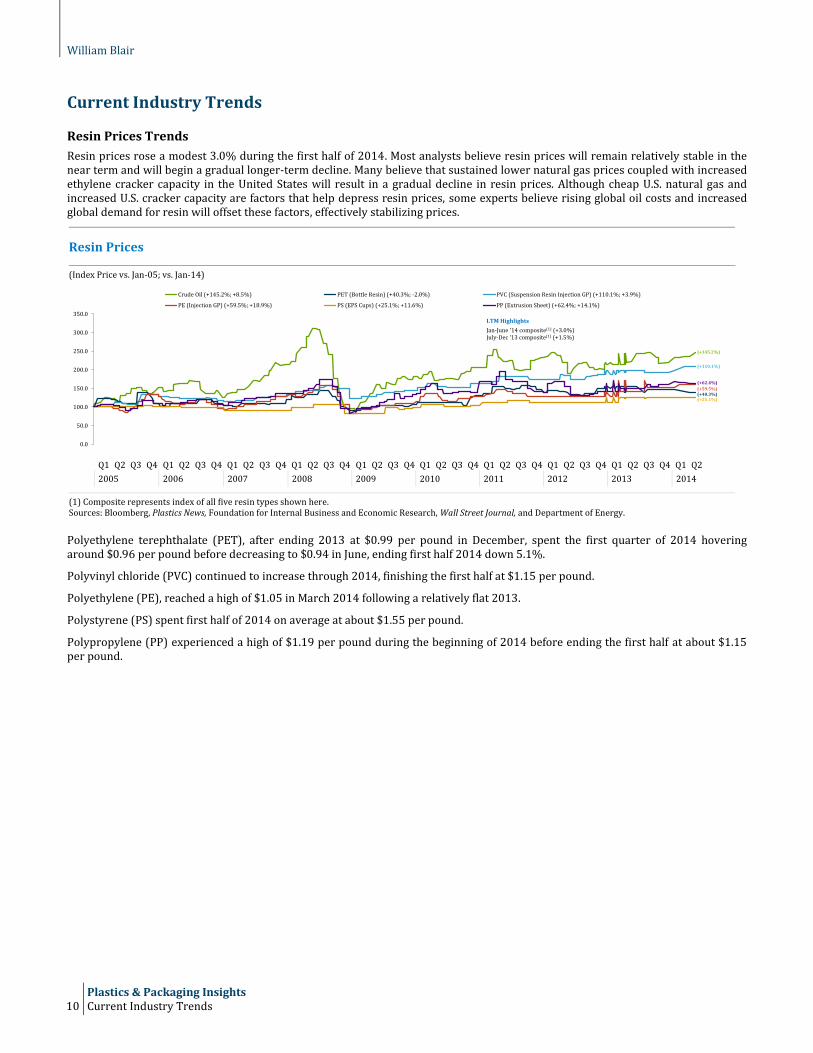

Resin Prices Trends

Resin prices rose a modest 3.0% during the first half of 2014. Most analysts believe resin prices will remain relatively stable in the near term and will begin a gradual longer-term decline. Many believe that sustained lower natural gas prices coupled with increased ethylene cracker capacity in the United States will result in a gradual decline in resin prices. Although cheap U.S. natural gas and increased U.S. cracker capacity are factors that help depress resin prices, some experts believe rising global oil costs and increased global demand for resin will offset these factors, effectively stabilizing prices.

Resin Prices

(Index Price vs. Jan-05; vs. Jan-14)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

(1) Composite represents index of all five resin types shown here. Sources: Bloomberg, Plastics News, Foundation for Internal Business and Economic Research, Wall Street Journal, and Department of Energy.

Polyethylene terephthalate (PET), after ending 2013 at $0.99 per pound in December, spent the first quarter of 2014 hovering around $0.96 per pound before decreasing to $0.94 in June, ending first half 2014 down 5.1%.

Polyvinyl chloride (PVC) continued to increase through 2014, finishing the first half at $1.15 per pound.

Polyethylene (PE), reached a high of $1.05 in March 2014 following a relatively flat 2013.

Polystyrene (PS) spent first half of 2014 on average at about $1.55 per pound.

Polypropylene (PP) experienced a high of $1.19 per pound during the beginning of 2014 before ending the first half at about $1.15 per pound.

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

Crude Oil (+145.2%; +8.5%) PET (Bottle Resin) (+40.3%; -2.0%) PVC (Suspension Resin Injection GP) (+110.1%; +3.9%)

PE (Injection GP) (+59.5%; +18.9%) PS (EPS Cups) (+25.1%; +11.6%) PP (Extrusion Sheet) (+62.4%; +14.1%)

LTM Highlights

Jan-June '14 composite(1) (+3.0%)July-Dec '13 composite(1) (+1.5%)

(+145.2%)

(+59.5%)

(+110.1%)

(+62.4%)

(+25.1%)(+40.3%)

William Blair

Plastics & Packaging Insights Current Industry Trends 11

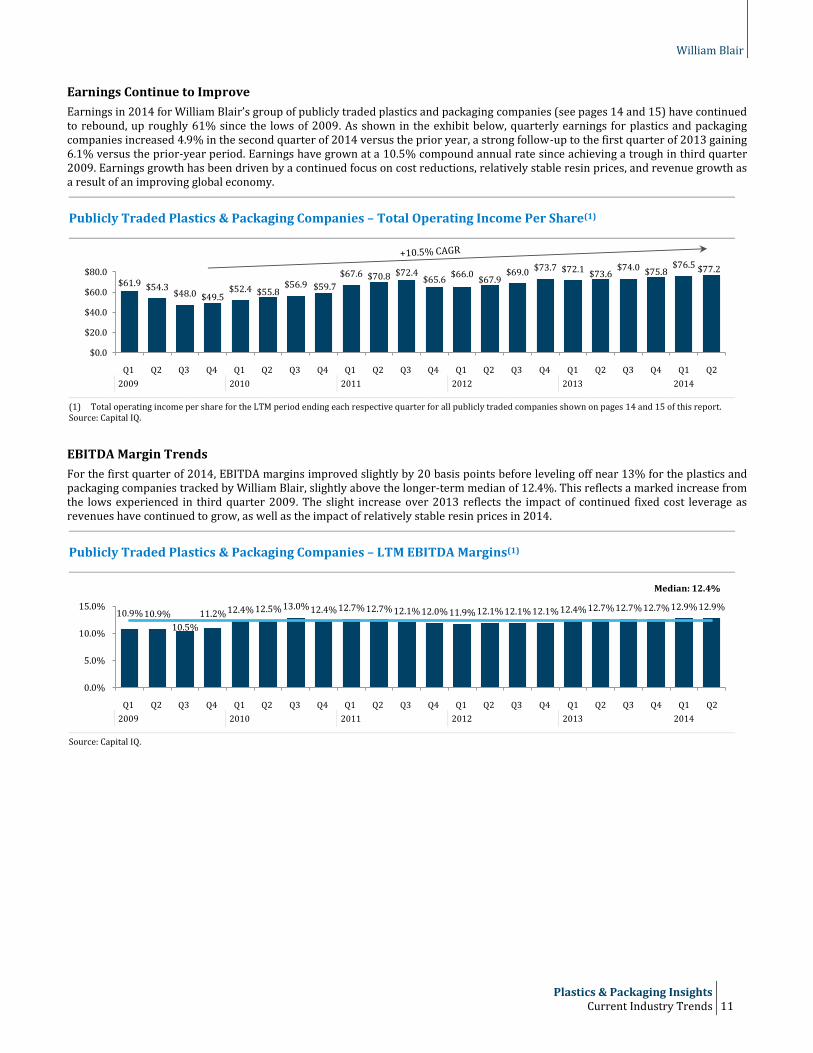

Earnings Continue to Improve

Earnings in 2014 for William Blair’s group of publicly traded plastics and packaging companies (see pages 14 and 15) have continued to rebound, up roughly 61% since the lows of 2009. As shown in the exhibit below, quarterly earnings for plastics and packaging companies increased 4.9% in the second quarter of 2014 versus the prior year, a strong follow-up to the first quarter of 2013 gaining 6.1% versus the prior-year period. Earnings have grown at a 10.5% compound annual rate since achieving a trough in third quarter 2009. Earnings growth has been driven by a continued focus on cost reductions, relatively stable resin prices, and revenue growth as a result of an improving global economy.

Publicly Traded Plastics & Packaging Companies – Total Operating Income Per Share(1)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2009 2010 2011 2012 2013 2014

(1) Total operating income per share for the LTM period ending each respective quarter for all publicly traded companies shown on pages 14 and 15 of this report. Source: Capital IQ.

EBITDA Margin Trends

For the first quarter of 2014, EBITDA margins improved slightly by 20 basis points before leveling off near 13% for the plastics and packaging companies tracked by William Blair, slightly above the longer-term median of 12.4%. This reflects a marked increase from the lows experienced in third quarter 2009. The slight increase over 2013 reflects the impact of continued fixed cost leverage as revenues have continued to grow, as well as the impact of relatively stable resin prices in 2014.

Publicly Traded Plastics & Packaging Companies – LTM EBITDA Margins(1)

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2

2009 2010 2011 2012 2013 2014

Source: Capital IQ.

$61.9 $54.3$48.0 $49.5

$52.4 $55.8$56.9 $59.7

$67.6 $70.8 $72.4$65.6

$66.0$67.9

$69.0 $73.7 $72.1$73.6

$74.0 $75.8$76.5 $77.2

$0.0

$20.0

$40.0

$60.0

$80.0

10.9% 10.9%

10.5%

11.2% 12.4% 12.5% 13.0% 12.4% 12.7% 12.7% 12.1% 12.0% 11.9% 12.1% 12.1% 12.1% 12.4% 12.7% 12.7% 12.7% 12.9% 12.9%

0.0%

5.0%

10.0%

15.0%

Median: 12.4%

William Blair

Plastics & Packaging Insights 12 Current Industry Trends

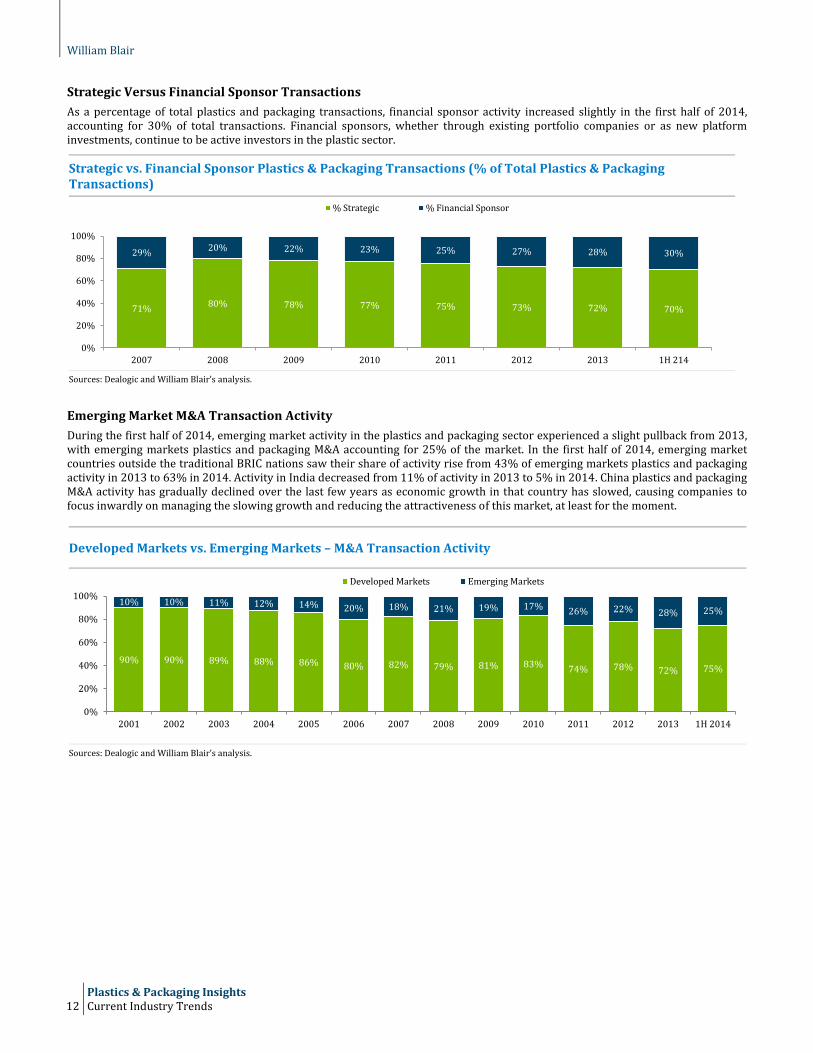

Strategic Versus Financial Sponsor Transactions

As a percentage of total plastics and packaging transactions, financial sponsor activity increased slightly in the first half of 2014, accounting for 30% of total transactions. Financial sponsors, whether through existing portfolio companies or as new platform investments, continue to be active investors in the plastic sector.

Strategic vs. Financial Sponsor Plastics & Packaging Transactions (% of Total Plastics & Packaging Transactions)

Sources: Dealogic and William Blair’s analysis.

Emerging Market M&A Transaction Activity

During the first half of 2014, emerging market activity in the plastics and packaging sector experienced a slight pullback from 2013, with emerging markets plastics and packaging M&A accounting for 25% of the market. In the first half of 2014, emerging market countries outside the traditional BRIC nations saw their share of activity rise from 43% of emerging markets plastics and packaging activity in 2013 to 63% in 2014. Activity in India decreased from 11% of activity in 2013 to 5% in 2014. China plastics and packaging M&A activity has gradually declined over the last few years as economic growth in that country has slowed, causing companies to focus inwardly on managing the slowing growth and reducing the attractiveness of this market, at least for the moment.

Developed Markets vs. Emerging Markets – M&A Transaction Activity

Sources: Dealogic and William Blair’s analysis.

71%80% 78% 77% 75% 73% 72% 70%

29%20% 22% 23% 25% 27% 28% 30%

0%

20%

40%

60%

80%

100%

2007 2008 2009 2010 2011 2012 2013 1H 214

% Strategic % Financial Sponsor

90% 90% 89% 88% 86% 80% 82% 79% 81% 83%74% 78% 72% 75%

10% 10% 11% 12% 14% 20% 18% 21% 19% 17%26% 22% 28% 25%

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H 2014

Developed Markets Emerging Markets

William Blair

Plastics & Packaging Insights Current Industry Trends 13

Emerging Markets Plastics & Packaging M&A Activity

Brazil 0% 4% 4% 0% 8% 9% 13% 9% 6% 6% 5% 7% 3% 2%

Russia 0% 4% 11% 0% 0% 7% 2% 6% 4% 4% 5% 5% 7% 2%

India 9% 15% 4% 10% 5% 12% 10% 6% 7% 13% 21% 10% 11% 5%

China 13% 19% 18% 19% 22% 24% 26% 38% 33% 47% 40% 38% 37% 28%

Other(1) 78% 58% 64% 71% 65% 48% 49% 42% 50% 30% 29% 40% 43% 63%

Note: Selected countries derived from the Dow Jones list of emerging countries. (1) Other countries include: Argentina, Bulgaria, Chile, Colombia, Czech Republic, Egypt, Estonia, Hungary, Indonesia, Jordan, Lithuania, Malaysia, Mexico, Pakistan, Oman, Peru, Philippines, Poland, Qatar, Romania, South Africa, Thailand, Turkey, and United Arab Emirates. Sources: Dealogic and William Blair’s analysis.

Emerging market activity. A few select examples of recent emerging markets M&A activity are profiled below:

Mondi, a South African-based producer of paper and packaging products, acquired U.S.-based Graphic Packaging International’s Bags and Kraft Paper Business, for $105 million.

Polymer Group, a manufacturer of engineered textile products, acquired Brazil-based Companhia Providencia Industria, a manufacturer of nonwoven fabrics, for $439 million.

Ravago, a distributor of plastic composite materials, acquired Turkey-based Tekpol, a polyurethane manufacturer, for $49 million.

Kraton Performance Polymers, a manufacturer of engineered polymers, acquired Taiwan-based LCY Chemical Corp., a manufacturer of copolymers, for $696 million.

Amcor, an Australian manufacturer of plastics and packaging, acquired Indonesia-based Bella Prima Packaging, a producer of films and laminated packaging materials, for $25 million.

0%

20%

40%

60%

80%

100%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 1H 2014

Other China India Russia Brazil

William Blair

Plastics & Packaging Insights 14 Public Plastics & Packaging Company Valuations

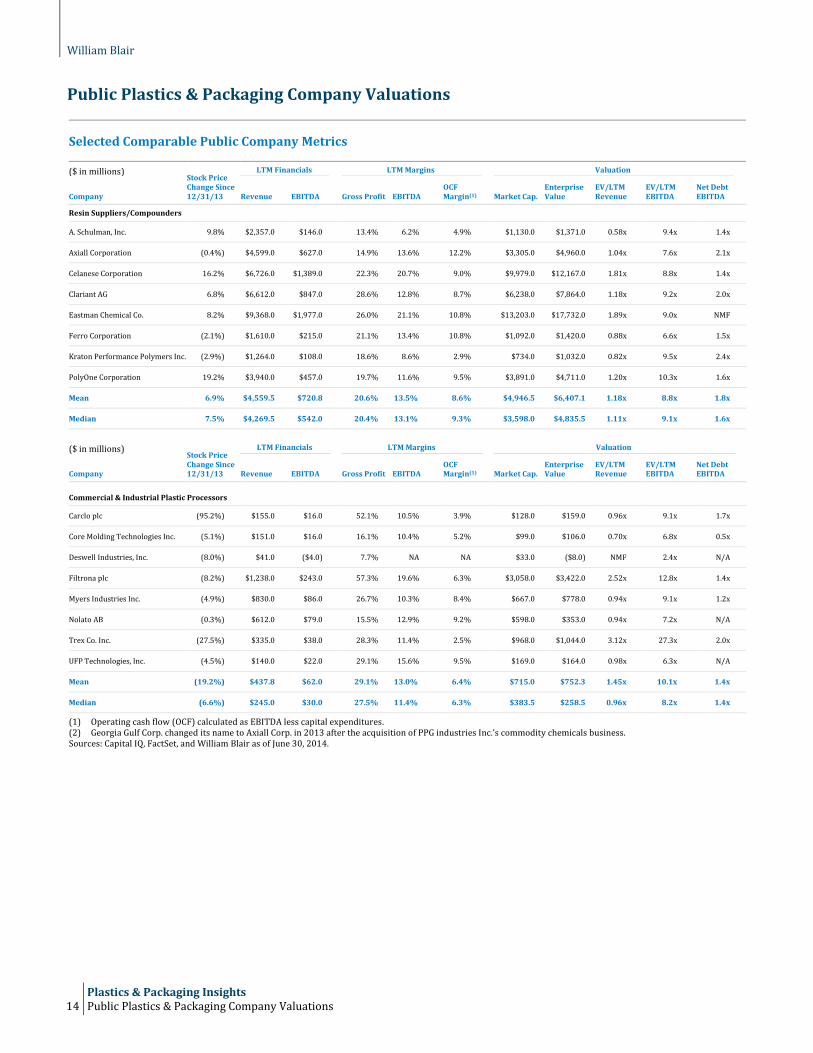

Public Plastics & Packaging Company Valuations

Selected Comparable Public Company Metrics

($ in millions) Stock Price Change Since 12/31/13

LTM Financials LTM Margins Valuation

Company Revenue EBITDA Gross Profit EBITDA OCF Margin(1) Market Cap.

Enterprise Value

EV/LTM Revenue

EV/LTM EBITDA

Net Debt EBITDA

Resin Suppliers/Compounders

A. Schulman, Inc. 9.8% $2,357.0 $146.0 13.4% 6.2% 4.9% $1,130.0 $1,371.0 0.58x 9.4x 1.4x

Axiall Corporation (0.4%) $4,599.0 $627.0 14.9% 13.6% 12.2% $3,305.0 $4,960.0 1.04x 7.6x 2.1x

Celanese Corporation 16.2% $6,726.0 $1,389.0 22.3% 20.7% 9.0% $9,979.0 $12,167.0 1.81x 8.8x 1.4x

Clariant AG 6.8% $6,612.0 $847.0 28.6% 12.8% 8.7% $6,238.0 $7,864.0 1.18x 9.2x 2.0x

Eastman Chemical Co. 8.2% $9,368.0 $1,977.0 26.0% 21.1% 10.8% $13,203.0 $17,732.0 1.89x 9.0x NMF

Ferro Corporation (2.1%) $1,610.0 $215.0 21.1% 13.4% 10.8% $1,092.0 $1,420.0 0.88x 6.6x 1.5x

Kraton Performance Polymers Inc. (2.9%) $1,264.0 $108.0 18.6% 8.6% 2.9% $734.0 $1,032.0 0.82x 9.5x 2.4x

PolyOne Corporation 19.2% $3,940.0 $457.0 19.7% 11.6% 9.5% $3,891.0 $4,711.0 1.20x 10.3x 1.6x

Mean 6.9% $4,559.5 $720.8 20.6% 13.5% 8.6% $4,946.5 $6,407.1 1.18x 8.8x 1.8x

Median 7.5% $4,269.5 $542.0 20.4% 13.1% 9.3% $3,598.0 $4,835.5 1.11x 9.1x 1.6x

($ in millions)

Stock Price Change Since 12/31/13

LTM Financials LTM Margins Valuation

Company Revenue EBITDA Gross Profit EBITDA OCF Margin(1) Market Cap.

Enterprise Value

EV/LTM Revenue

EV/LTM EBITDA

Net Debt EBITDA

Commercial & Industrial Plastic Processors

Carclo plc (95.2%) $155.0 $16.0 52.1% 10.5% 3.9% $128.0 $159.0 0.96x 9.1x 1.7x

Core Molding Technologies Inc. (5.1%) $151.0 $16.0 16.1% 10.4% 5.2% $99.0 $106.0 0.70x 6.8x 0.5x

Deswell Industries, Inc. (8.0%) $41.0 ($4.0) 7.7% NA NA $33.0 ($8.0) NMF 2.4x N/A

Filtrona plc (8.2%) $1,238.0 $243.0 57.3% 19.6% 6.3% $3,058.0 $3,422.0 2.52x 12.8x 1.4x

Myers Industries Inc. (4.9%) $830.0 $86.0 26.7% 10.3% 8.4% $667.0 $778.0 0.94x 9.1x 1.2x

Nolato AB (0.3%) $612.0 $79.0 15.5% 12.9% 9.2% $598.0 $353.0 0.94x 7.2x N/A

Trex Co. Inc. (27.5%) $335.0 $38.0 28.3% 11.4% 2.5% $968.0 $1,044.0 3.12x 27.3x 2.0x

UFP Technologies, Inc. (4.5%) $140.0 $22.0 29.1% 15.6% 9.5% $169.0 $164.0 0.98x 6.3x N/A

Mean (19.2%) $437.8 $62.0 29.1% 13.0% 6.4% $715.0 $752.3 1.45x 10.1x 1.4x

Median (6.6%) $245.0 $30.0 27.5% 11.4% 6.3% $383.5 $258.5 0.96x 8.2x 1.4x

(1) Operating cash flow (OCF) calculated as EBITDA less capital expenditures. (2) Georgia Gulf Corp. changed its name to Axiall Corp. in 2013 after the acquisition of PPG industries Inc.’s commodity chemicals business. Sources: Capital IQ, FactSet, and William Blair as of June 30, 2014.

William Blair

Plastics & Packaging Insights Public Plastics & Packaging Company Valuations 15

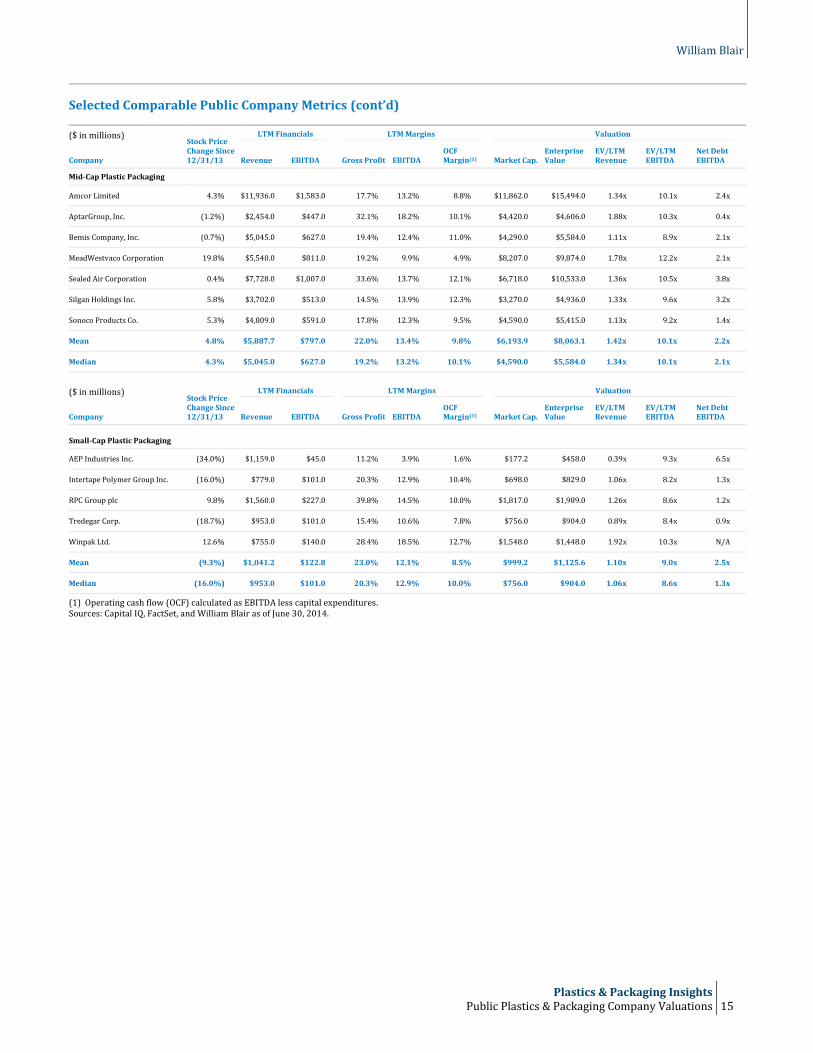

Selected Comparable Public Company Metrics (cont’d)

($ in millions) Stock Price Change Since 12/31/13

LTM Financials LTM Margins Valuation

Company Revenue EBITDA Gross Profit EBITDA OCF Margin(1) Market Cap.

Enterprise Value

EV/LTM Revenue

EV/LTM EBITDA

Net Debt EBITDA

Mid-Cap Plastic Packaging

Amcor Limited 4.3% $11,936.0 $1,583.0 17.7% 13.2% 8.8% $11,862.0 $15,494.0 1.34x 10.1x 2.4x

AptarGroup, Inc. (1.2%) $2,454.0 $447.0 32.1% 18.2% 10.1% $4,420.0 $4,606.0 1.88x 10.3x 0.4x

Bemis Company, Inc. (0.7%) $5,045.0 $627.0 19.4% 12.4% 11.0% $4,290.0 $5,584.0 1.11x 8.9x 2.1x

MeadWestvaco Corporation 19.8% $5,540.0 $811.0 19.2% 9.9% 4.9% $8,207.0 $9,874.0 1.78x 12.2x 2.1x

Sealed Air Corporation 0.4% $7,728.0 $1,007.0 33.6% 13.7% 12.1% $6,718.0 $10,533.0 1.36x 10.5x 3.8x

Silgan Holdings Inc. 5.8% $3,702.0 $513.0 14.5% 13.9% 12.3% $3,270.0 $4,936.0 1.33x 9.6x 3.2x

Sonoco Products Co. 5.3% $4,809.0 $591.0 17.8% 12.3% 9.5% $4,590.0 $5,415.0 1.13x 9.2x 1.4x

Mean 4.8% $5,887.7 $797.0 22.0% 13.4% 9.8% $6,193.9 $8,063.1 1.42x 10.1x 2.2x

Median 4.3% $5,045.0 $627.0 19.2% 13.2% 10.1% $4,590.0 $5,584.0 1.34x 10.1x 2.1x

($ in millions)

Stock Price Change Since 12/31/13

LTM Financials LTM Margins Valuation

Company Revenue EBITDA Gross Profit EBITDA OCF Margin(1) Market Cap.

Enterprise Value

EV/LTM Revenue

EV/LTM EBITDA

Net Debt EBITDA

Small-Cap Plastic Packaging

AEP Industries Inc. (34.0%) $1,159.0 $45.0 11.2% 3.9% 1.6% $177.2 $458.0 0.39x 9.3x 6.5x

Intertape Polymer Group Inc. (16.0%) $779.0 $101.0 20.3% 12.9% 10.4% $698.0 $829.0 1.06x 8.2x 1.3x

RPC Group plc 9.8% $1,560.0 $227.0 39.8% 14.5% 10.0% $1,817.0 $1,989.0 1.26x 8.6x 1.2x

Tredegar Corp. (18.7%) $953.0 $101.0 15.4% 10.6% 7.8% $756.0 $904.0 0.89x 8.4x 0.9x

Winpak Ltd. 12.6% $755.0 $140.0 28.4% 18.5% 12.7% $1,548.0 $1,448.0 1.92x 10.3x N/A

Mean (9.3%) $1,041.2 $122.8 23.0% 12.1% 8.5% $999.2 $1,125.6 1.10x 9.0x 2.5x

Median (16.0%) $953.0 $101.0 20.3% 12.9% 10.0% $756.0 $904.0 1.06x 8.6x 1.3x

(1) Operating cash flow (OCF) calculated as EBITDA less capital expenditures. Sources: Capital IQ, FactSet, and William Blair as of June 30, 2014.

William Blair

Plastics & Packaging Insights 16 Public Plastics & Packaging Company Valuations

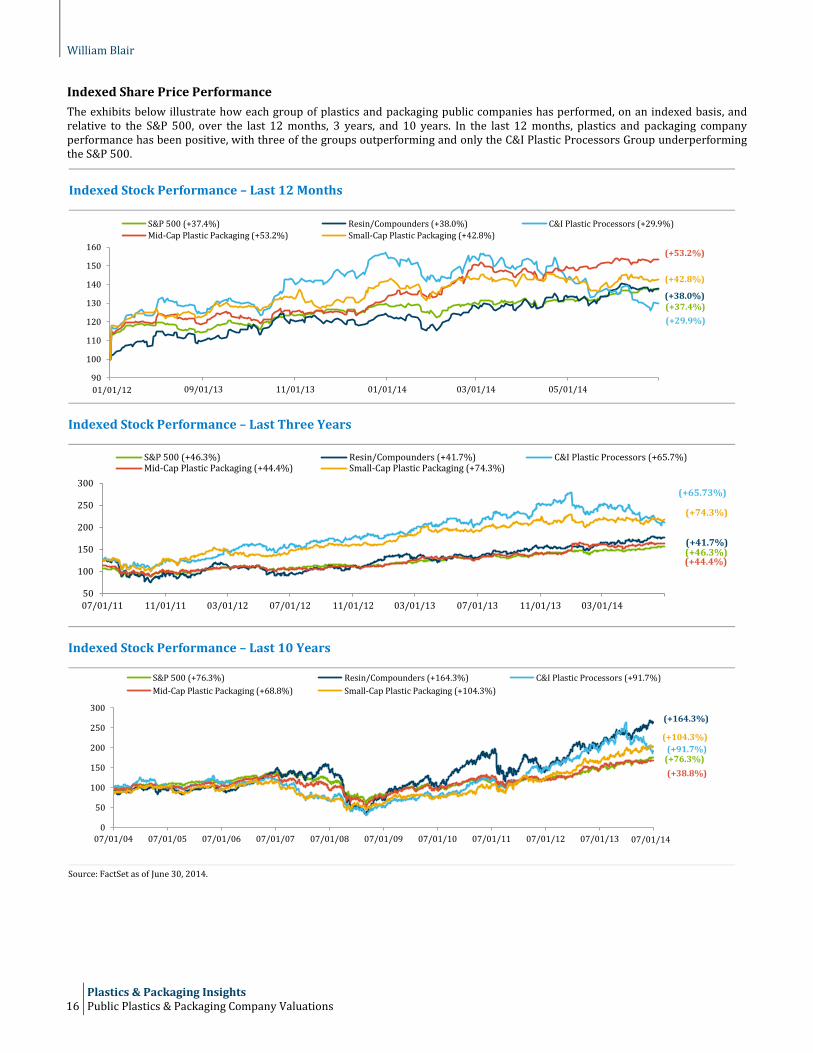

Indexed Share Price Performance

The exhibits below illustrate how each group of plastics and packaging public companies has performed, on an indexed basis, and relative to the S&P 500, over the last 12 months, 3 years, and 10 years. In the last 12 months, plastics and packaging company performance has been positive, with three of the groups outperforming and only the C&I Plastic Processors Group underperforming the S&P 500.

Indexed Stock Performance – Last 12 Months

Indexed Stock Performance – Last Three Years

Indexed Stock Performance – Last 10 Years

Source: FactSet as of June 30, 2014.

90

100

110

120

130

140

150

160

07/01/13 09/01/13 11/01/13 01/01/14 03/01/14 05/01/14

S&P 500 (+37.4%) Resin/Compounders (+38.0%) C&I Plastic Processors (+29.9%)

Mid-Cap Plastic Packaging (+53.2%) Small-Cap Plastic Packaging (+42.8%)

(+53.2%)

(+37.4%)

(+42.8%)

(+38.0%)

(+29.9%)

01/01/12

50

100

150

200

250

300

07/01/11 11/01/11 03/01/12 07/01/12 11/01/12 03/01/13 07/01/13 11/01/13 03/01/14

S&P 500 (+46.3%) Resin/Compounders (+41.7%) C&I Plastic Processors (+65.7%)Mid-Cap Plastic Packaging (+44.4%) Small-Cap Plastic Packaging (+74.3%)

(+46.3%)

(+74.3%)

(+65.73%)

(+44.4%)

(+41.7%)

0

50

100

150

200

250

300

07/01/04 07/01/05 07/01/06 07/01/07 07/01/08 07/01/09 07/01/10 07/01/11 07/01/12 07/01/13

S&P 500 (+76.3%) Resin/Compounders (+164.3%) C&I Plastic Processors (+91.7%)

Mid-Cap Plastic Packaging (+68.8%) Small-Cap Plastic Packaging (+104.3%)

(+76.3%)(+91.7%)

(+104.3%)

(+38.8%)

(+164.3%)

07/01/14

William Blair

Plastics & Packaging Insights Public Plastics & Packaging Company Valuations 17

Historical Trading Values

The following exhibits summarize the median enterprise-value–to–trailing-12-month EBITDA multiples for each group of selected public companies. The data highlights quarterly metrics since 2006. As highlighted below, while the broader market decline in third quarter 2011 depressed valuations to near recession levels, plastics and packaging companies have subsequently rebounded strongly and now generally trade above longer-term median levels.

Resin Suppliers/Compounders

Commercial and Industrial Plastic Processors

Mid-Cap Plastic Packaging

Small-Cap Plastic Packaging

Sources: Capital IQ, FactSet, and William Blair.

7.5x7.2x6.7x7.2x7.6x8.4x7.2x7.2x7.2x7.0x6.2x

5.2x5.2x6.2x

8.6x7.5x6.8x

4.8x

6.9x6.8x6.9x6.3x

4.6x

5.3x6.7x6.1x6.9x

9.2x10.4x

9.5x9.8x

10.2x8.7x9.1x

0.0x2.0x4.0x6.0x8.0x

10.0x12.0x

Median: 7.1x

7.6x7.0x7.9x

8.6x8.9x

8.4x8.1x6.6x6.0x 5.7x

5.0x3.0x

3.8x

5.9x

6.8x6.7x

6.2x

7.9x

5.9x

7.0x6.7x6.1x

5.1x5.3x

6.4x6.6x6.4x

6.3x6.7x

8.7x7.3x

7.0x7.7x

8.2x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0xMedian: 6.7x

8.5x8.1x8.1x

8.6x8.7x8.8x8.1x

7.7x7.8x

7.2x7.4x

6.7x6.3x

6.8x7.2x7.2x7.3x6.8x7.5x7.4x7.4x7.6x6.8x7.2x8.0x8.0x7.7x8.0x

8.9x8.7x

9.1x10.2x

10.1x10.1x

0.0x2.0x4.0x6.0x8.0x

10.0x12.0x

Median: 7.7x

7.2x7.0x

7.1x8.5x

8.3x7.5x6.8x5.9x6.5x5.9x5.6x

6.1x5.7x

4.6x

5.7x5.6x5.6x5.7x7.2x

6.8x7.1x6.5x

5.5x

6.5x6.6x7.0x7.3x6.7x8.1x

7.9x

9.6x9.3x8.7x8.6x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0xMedian: 6.8x

William Blair

William Blair is a trade name for William Blair & Company, L.L.C. and William Blair International, Limited. William Blair & Company, L.L.C., is a Delaware company and is regulated by the Securities and Exchange Commission, The Financial Industry Regulatory Authority, and other principal exchanges. William Blair International Limited is authorised and regulated by the Financial Services Authority ("FSA") in the United Kingdom. William Blair & Company® only offers products and services where it is permitted to do so. Some of these products and services are only offered to persons or institutions situated within the United States and are not offered to persons or institutions outside of the United States. This material has been approved for distribution in the United Kingdom by William Blair International Limited, and is directed only at, professional clients and eligible counterparties (as defined in COBS 3.5 and 3.6 of the FSA Handbook). This advertisement is not intended to be investment advice. William Blair & Company | 222 West Adams Street | Chicago, Illinois 60606 | +1 312 236 1600 | williamblair.com

August 21, 2014

Plastics & Packaging Insights 18 Disclosures

Disclosures

William Blair’s investment banking group combines signi�icant transaction experience, rich industry knowledge, and deep relationships to deliver successful advisory and �inancing solutions to our global base of corporate clients. We serve both publicly traded and privately held companies, executing mergers and acquisitions, growth �inancing, �inancial restructuring, and general advisory projects. This comprehensive suite of services allows us to be a long-term partner to our clients as they grow and evolve. From 2010 - 2013, the investment banking group completed 250 merger-and-acquisition transactions worth more than $52 billion in value, involving parties in 27 countries and four continents, was an underwriter on over 20% of all U.S. initial public offerings and arranged more than $11.5 billion of debt �inancing.

About William Blair Investment Banking

Sector Update August 2014

Plastics & Packaging Investment Banking Sector Report In this Issue: – Sector Trends and Insights – M&A Activity– Valuation Analysis

Plastics & Packaging Investment Banking

Elliot Farkas Managing Director [email protected] +1 312 364 8157

Paul M. Hindsley Managing Director [email protected] +1 312 364 8576