platforms for the development of digital television broadcasting and the internet in japan...

Post on 19-Dec-2015

213 views

TRANSCRIPT

Platforms for the Development of Digital Television Broadcasting and the Internet in Japan

Fourteenth Northeast Asia Economic Forum

Shenyang, China

20-21 September 2005

Hajime ONIKI

Osaka-Gakuin University, [email protected]

www.osaka-gu.ac.jp/php/oniki/

9/20-21/2005 H. Oniki

2

I. Introduction A. Overview of IT, DTV, and the Internet in Japan

Source of all statistical graphs in this presentation: MIC, Information and Communication in Japan (2005 White Paper), June 2005.

9/20-21/2005 3

Communications Industry: GDP (Value Added, 1995 prices)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Bill J PY

9/20-21/2005 4

Commnunications Industry (Pecentage of Value Added in GDP)

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1995 1996 1997 1998 1999 2000 2001 2002 2003

%

9/20-21/2005 5

IT Investment of All Industries (1995 Prices)

0

5,000

10,000

15,000

20,000

25,000

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Bill J PY

9/20-21/2005 6

Percentage of IT Investment in Total Investment of AllIndustries

0.0

5.0

10.0

15.0

20.0

25.0

30.0

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

%

9/20-21/2005 7

0

200

400

600

800

1000

1200

1400

1600

1800

1991 1992 19931994 1995 1996 1997 1998 1999 20002001 2002 2003

J apanUSKorea

Growth of IT Investment of all Industries: J apan, Korea, US

(1991=100)

9/20-21/2005 8

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,000

1996 1997 1998 1999 2000 2001 2002 2003 2004

固定通信移動通信

Mill. Telecommunications Subscribers

WirelineWireless

9/20-21/2005 9

Internet Users

0

10

20

30

40

50

60

70

80

90

1997 1998 1999 2000 2001 2002 2003 2004

Million

9/20-21/2005 10

Percentage of Internet Users in the Population

0

10

20

30

40

50

60

70

1997 1998 1999 2000 2001 2002 2003 2004

%

9/20-21/2005 11

World Internet Users

0

100

200

300

400

500

600

700

800

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

Mill.

9/20-21/2005 12

1.1 1.1 1.1 1.2 1.6 1.8

48.940.1 40.1 37.5 34.9 32.4

20.527.3 28.3 30.4 33.9 36.1

26.9 28.6 28.4 29.0 27.7 27.7

2.5 2.9 2.1 1.8 1.9 2.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1998 1999 2000 2001 2002 2003

OceaniaEuropeAsiaAmericasAfirica

Area Composition of Internet Users

9/20-21/2005 13

Average Anuual Expenditures on Communications by Households

78,12383,565

90,046

99,266 102,611109,701

118,327124,362

132,864141,372

145,332

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

J PY/ Year

9/20-21/2005 14

Percentage of Communications Expenditures by Householdsin Total Expenditures

2.1 2.3 2.5 2.6 2.8 3.1 3.4 3.6 3.9 4.0

012345678

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

(%)

9/20-21/2005 H. Oniki

15

Impact of the introduction of Digital Television (DTV) in Japan

Possibilities of processing DTV content by using the power of computer and storage technologies

DTV’s competition and coordination with the Internet

I. Introduction B. Objective of this presentation

9/20-21/2005 H. Oniki

16

II. Digital Broadcasting and the Internet in Japan A. Start of DTV in Japan (1/2)

1. Terrestrial DTV

Digital terrestrial television started at the end of 2003.

By 2011 analog television will be terminated.

regulated by Ministry of Internal Affairs and

Communication (MIC)

9/20-21/2005 H. Oniki

17

II. Digital Broadcasting and the Internet in Japan A. Start of DTV in Japan (2/2)

2. Other DTV’s

1996: CS broadcasts

1998: cable TV

2000: BS broadcasts

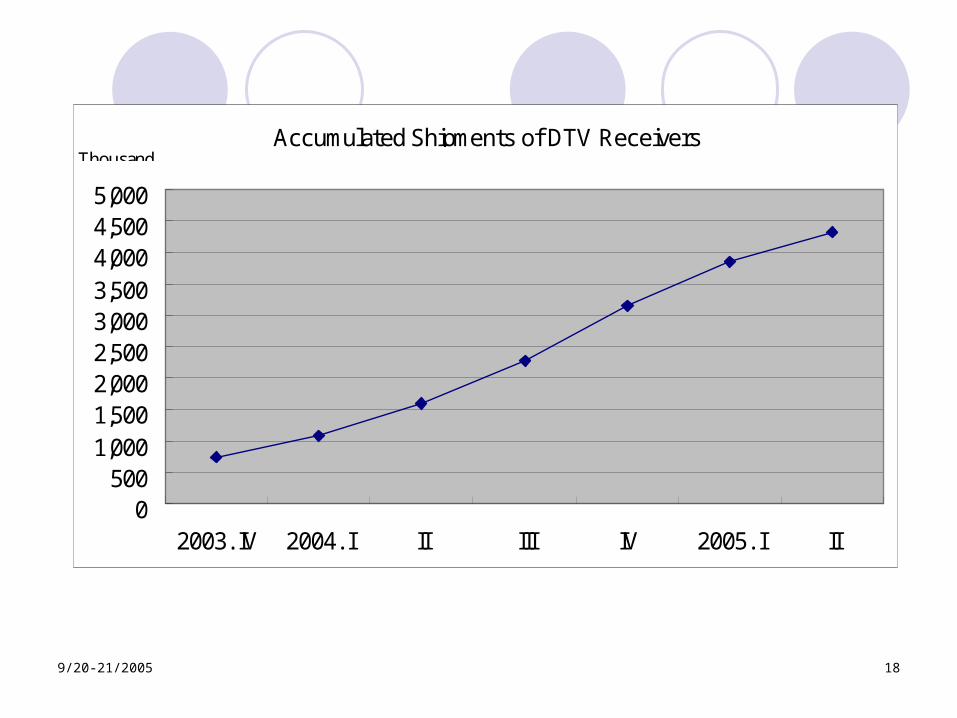

9/20-21/2005 18

Accumulated Shipments of DTV Receivers

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

2003. IV 2004. I II III IV 2005. I II

Thousand

9/20-21/2005 H. Oniki

19

II. Digital Broadcasting and the Internet in Japan B. Terrestrial TV in Japan (1/4)

1. Statistics

Terrestrial TV’s revenue:

80% of all revenue for broadcasting

Per capita (per consumer) annual revenue: JPY30,000

(US$250)

Japanese households watch TV 3 hours per day.

9/20-21/2005 20

Total Annual Revenue in Broadcast Industry

29,000

30,000

31,000

32,000

33,000

34,000

35,000

36,000

37,000

38,000

39,000

1996 1997 1998 1999 2000 2001 2002 2003

100Mill J PY

9/20-21/2005 21

0:00

1:00

2:00

3:00

4:00

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

NHK総計

民放総計

Hours/ Day Television Watching by Households

PublidStattion(NHK)CommercialStation

9/20-21/2005 H. Oniki

22

II. Digital Broadcasting and the Internet in Japan B. Terrestrial TV in Japan (2/4)

2. Regulation

DTV considered to replace analog with digital content

not a new service

few changes in rules or regulations

no new entry

9/20-21/2005 H. Oniki

23

II. Digital Broadcasting and the Internet in Japan B. Terrestrial TV in Japan (3/4)

3. Economics

monopolistic status

no new licenses

average profits quite high

broadcasters in urban areas can bear costs for DTV transition

those located in rural areas may not

9/20-21/2005 H. Oniki

24

II. Digital Broadcasting and the Internet in Japan B. Terrestrial TV in Japan (4/4)

4. Impact of DTV transition explained from

technological aspect

a. noise reduction

b. realization of HDTV

c. spectrum saving

d. possibility of interactive TV

9/20-21/2005 H. Oniki

25

II. Digital Broadcasting and the Internet in Japan C. Impact of DTV

Possible to process DTV content after they are broadcast

desirable to prepare environment for content

processing

DTV and the Internet may be competitive and

complementary

Convergence of broadcasting and telecommunications.

9/20-21/2005 H. Oniki

26

III. Platforms for Efficient Utilization of DTV A. Restrictions on content utilization with DTV in Japan (1/2)

1. Rigid restrictions on utilizing content

All DTV programs are broadcast scrambled

B-CAS card required for viewing

Copy-once requirement

9/20-21/2005 H. Oniki

27

III. Platforms for Efficient Utilization of DTV A. Restrictions on content utilization with DTV in Japan (2/2)

2. Implications

Possible for a broadcaster to introduce pay TV

no broadcaster intends to introduce pay TV

“TiVo” in U.S.

Potential benefits of applications software for DTV content blocked by restrictions

<Figure 1>

9/20-21/2005 28

Copyright protection

Optimal state

Present state

Figure 1: Tradeoff of Copyright Protection and Applications Development

Applications development

9/20-21/2005 H. Oniki

29

III. Platforms for Efficient Utilization of DTV B. Platforms for DTV applications (1/6)

1. Present state of DTV

lot of content but no applications software

like computers in earlier days

little applications software but with a lot of analog

content

9/20-21/2005 H. Oniki

30

III. Platforms for Efficient Utilization of DTV B. Platforms for DTV applications (2/6)

2. Preparing environment for transactions of

content with a copyright

Business codes

Database and network system

9/20-21/2005 H. Oniki

31

III. Platforms for Efficient Utilization of DTV B. Platforms for DTV applications (3/6)

3. Transactions system for DTV content

Transacting goods and services

market mechanism

differences between (ordinary) goods and services

and content

Content can be copied with or without modification.

9/20-21/2005 H. Oniki

32

III. Platforms for Efficient Utilization of DTV B. Platforms for DTV applications (4/6)

4. Degree of complexities in transactions of

content

Cost of transacting digital content is high.

9/20-21/2005 H. Oniki

33

III. Platforms for Efficient Utilization of DTV B. Platforms for DTV applications (5/6)

5. System for transactions of digital content to be built on copyright laws

Many “rights” in relation to content

Status of rights to be attached to content

Information set: descriptor

Database of descriptors of content

Record of transactions of real estate

9/20-21/2005 34

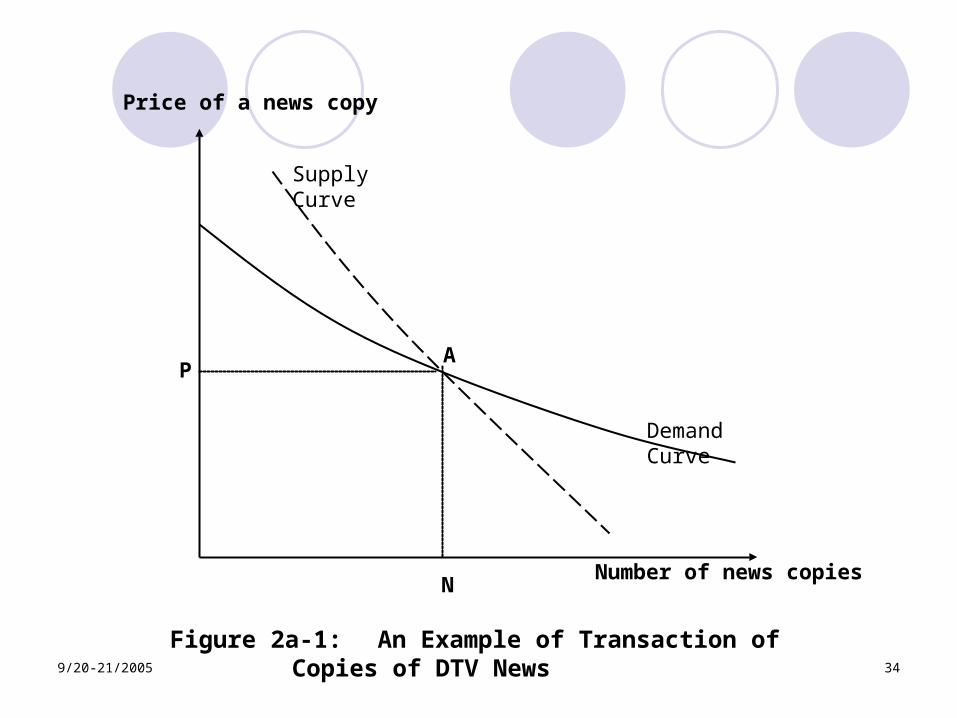

Number of news copiesN

Price of a news copy

Supply Curve

Demand Curve

AP

Figure 2a-1: An Example of Transaction of Copies of DTV News

9/20-21/2005 35

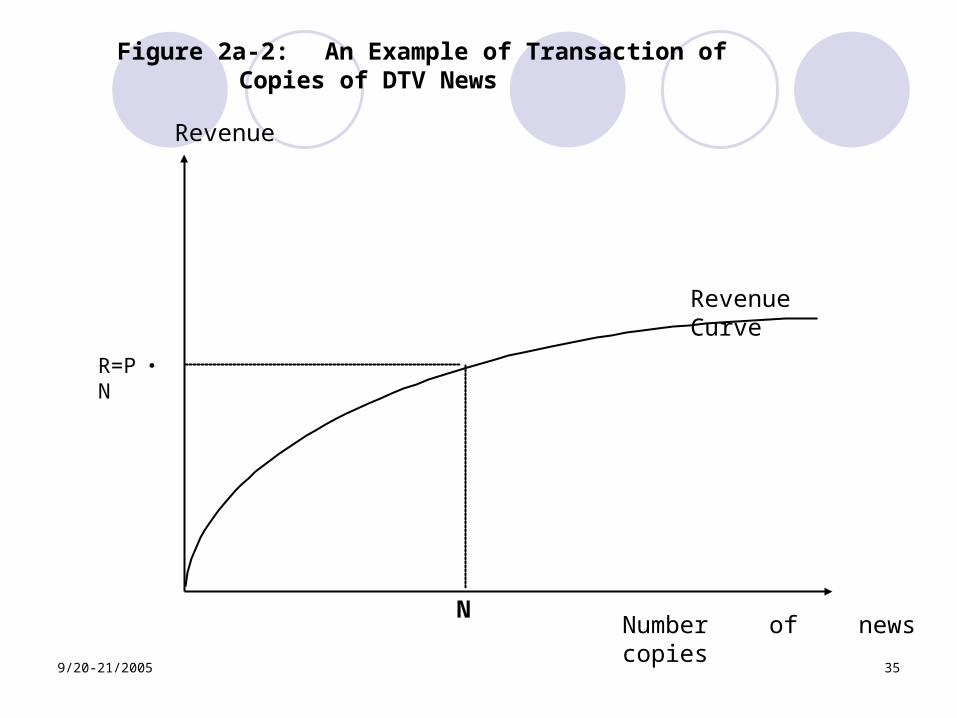

Revenue Curve

R=P ・N

Revenue

Number of news copiesN

Figure 2a-2: An Example of Transaction of Copies of DTV News

9/20-21/2005 H. Oniki

36

III. Platforms for Efficient Utilization of DTV B. Platforms for DTV applications (6/6)

6. Example of simple descriptor of DTV

news content

<Figure 2b>

9/20-21/2005 37

Descriptor of Video Copy for Transaction

1. Video CharacteristicsTitle: Morning News Class.: General NewsBroadcast by: XYZ Network, Inc. at: Tokyo and other locationson: 02/15/2005 time: 9:00-10:00AM duration: 45 minCommercials: not included2. Supply-Price SchedulePrice per Copy (yen) No. of Copies registered for sale 1.000 ~ 5,000 700 ~ 1,000 500 ~ 2,000 310 ~ 5,000 220 ~ 10,000 160 ~ 20,000 100 ~ 50,000 80 50,000 ~ Figure 2b-1: Example of Descriptor of News Video for Sale

9/20-21/2005 38

Descriptor of Video Copy for Transaction

3. Current Registration for Purchasing a CopyNo. of Copies for Effective Purchase: 2513No. of Copies Delivered: 0Price Currently Bid: 310 yensClosing Time of Current Offer: Noon, 2/16/20054. Conditions for Copy Utilization

•Must use equipment with B-CAS compliance•Utilization Type: A2

•May retain single copy for viewing; Duplicate copies not allowed.

(2)May cut and use any portion(s) of video, but only one cut is allowed. Duplicating cut portion(s) not allowed. Cut portion(s) will be removed from the original video; the original video will be shortened by the (total) length of cut portion(s).

(3)Any video to which cut portion(s) of the original video are pasted may not be duplicated; such shall be used under the copy-once restriction.

Figure 2b-2: Example of Descriptor of News Video for Sale

9/20-21/2005 H. Oniki

39

III. Platforms for Efficient Utilization of DTV C. Status of broadcasters (1/2)

1. Monopoly in the supply of broadcast content

little incentive to let DTV content be utilized

with applications software for the benefit of

consumers

9/20-21/2005 H. Oniki

40

III. Platforms for Efficient Utilization of DTV C. Status of broadcasters (2/2)

2. Recent trend:

Content on IP-TV (August 2005)

by commercial broadcasters

Disclosure obligation of DTV content by direct governmental regulations

Information and Communication Council (July 2005)

DTV content to be supplied via the Internet

9/20-21/2005 H. Oniki

41

IV. Competition and Coordination of DTV and the Internet A. Vertical Structure of DTV and the Internet (1/2)

1. Vertical structure in communications

industry

Division of labor viewed vertically

<Figure 3>

9/20-21/2005 42

ServicesTeleph

onyInterne

tCable TV

Broadcast

Mode of Supply

Contents

(Contents of

telephone and fax)

E-mails,Web

BroadcastContents

CompetitiveNetworking Voice

TransmissionIP-Packet

TransmissionCable

TransmissionBroadcasting

Media

Electric current, Optical rays Spectrum

Twisted and coaxial cables,Optical fibers

(Antennas)

MonopolizedEquipmentStructures

andSpaces

Tunnels, Tubes, Poles, etc. Terrestri

al spectru

m spacesTerrestrial (physical) spaces

Infrastructure Wired

Wireless

Figure 3: The Layers Structure of the Services for Information Transmission

9/20-21/2005 H. Oniki

43

IV. Competition and Coordination of DTV and the Internet A. Vertical Structure of DTV and the Internet (2/2)

2. Competition and growth

Activities competing and substituting within single

layer

twisted copper pair to optical fibers

telephony from traditional voice transmission to new

IP-packet transmission

Best to promote competition layer-wise

9/20-21/2005 44

Annual Sales of Media Contents

4.6 4.8 4.9

1.0 0.9 0.9

5.3 5.1 5.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2000 2002 2007

TextVoiceVideo

Trill J PY

9/20-21/2005 45

No. of Broadband Subscribers

02468

101214161820

1999 2000 2001 2002 2003 2004

Wireless FWA( )FTTHVia CableDSL

Mill.

9/20-21/2005 46

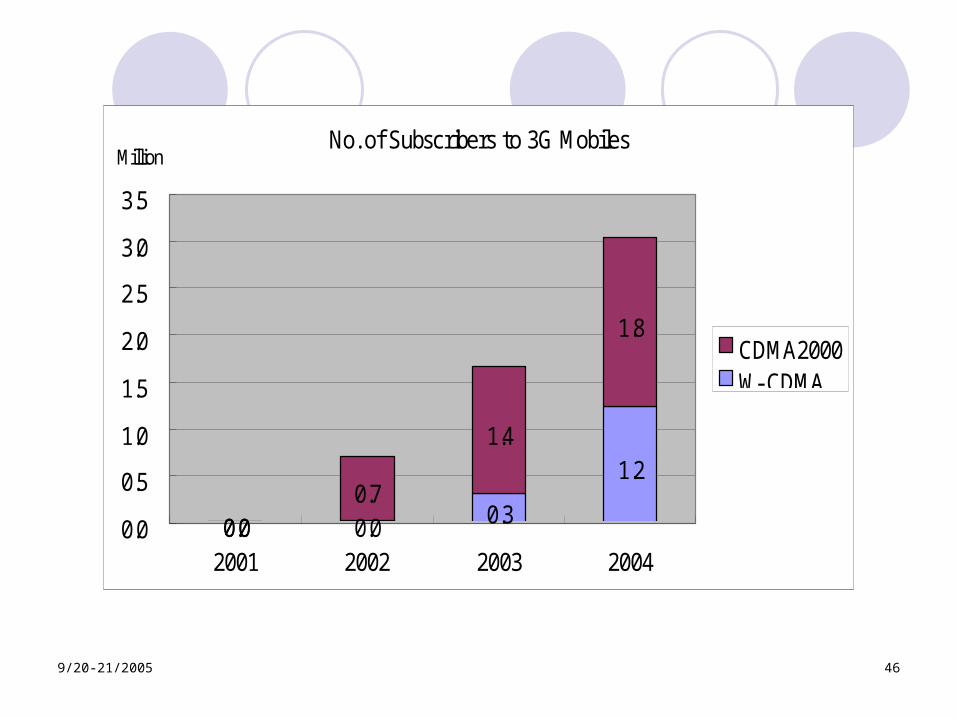

No. of Subscribers to 3G Mobiles

0.0 0.0 0.3

1.2

0.00.7

1.4

1.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2001 2002 2003 2004

CDMA2000W- CDMA

Million

9/20-21/2005 H. Oniki

47

IV. Competition and Coordination of DTV and the Internet B. Monopoly in the infrastructure layer (1/3)

Legal and economic basis of supply of infrastructure

layer not clearly established

1. Wired communication

NTT supplies large portion of communications

infrastructure

“given” at the time of privatization

9/20-21/2005 H. Oniki

48

IV. Competition and Coordination of DTV and the Internet B. Monopoly in the infrastructure layer (2/3)

2. Wireless communication

Spectrum assigned by MIC without charging

economic values

far from being competitive or with free entry

9/20-21/2005 H. Oniki

49

IV. Competition and Coordination of DTV and the Internet B. Monopoly in the infrastructure layer (3/3)

3. Implications of monopoly

Monopolistic profits

Internal cross-subsidization in upper-layer

competition

9/20-21/2005 H. Oniki

50

IV. Competition and Coordination of DTV and the Internet C. Policies for fair competition at level-playing field (1/6)

1. Designation of “monopoly-front service”

to be determined by the government

regulate supply of services located at front level

so that monopolized group function as if a

competitive group

9/20-21/2005 H. Oniki

51

IV. Competition and Coordination of DTV and the Internet C. Policies for fair competition at level-playing field (2/6)

2. Vertical separation

Monopolistic operator be vertically separated from

competitive activities

structurally or in accounting

No regulation on competitive activities

supply of monopoly-front service be open to all purchasers

9/20-21/2005 H. Oniki

52

IV. Competition and Coordination of DTV and the Internet C. Policies for fair competition at level-playing field (3/6)

3. Regulation of monopoly

Monopolistic operator must act as price taker in supply

of infrastructure

<Figure 4>

9/20-21/2005 53

Supply of infrastructure Sservices

Price of

infrastructure services

Demand

Equilibrium

prices

Figure 4: Equilibrium Price of Infrastructure Service

9/20-21/2005 H. Oniki

54

IV. Competition and Coordination of DTV and the Internet C. Policies for fair competition at level-playing field (4/6)

4. Implications

Most difficulties and complexities in communications

industry arise from that every activity must use some

infrastructure (including space), which cannot be

supplied competitively without governmental

regulations.

<Figure 5>

9/20-21/2005 55

Services Economic unitsMode of supply

Final demand

Consumers, Firms, Governments, Public entities, etc

Competitive

Content supply

Content suppliers (newspapers, publishers, producers of music and video contents, news agencies, advertising

agencies, etc.)

Web, E-mails, and

other data

Information Transmission

Network-service providers(broadcast, telephone, access,

backbone, Internet, etc.)

Infrastructure

Supply of infrastructure for information transmission

(wired, wireless)

Monopolized

Figure 5: The Structure of IT Industries under Vertical Separation

9/20-21/2005 H. Oniki

56

IV. Competition and Coordination of DTV and the Internet C. Policies for fair competition at level-playing field (5/6)

5. Public corporations for infrastructure supply

a. Short-run behavior of monopolistic operator to simulate short-run service market

b. Long-run behavior of monopolistic operator

to simulate competitive capital market

Prohibited from maximizing rate of return from investment

9/20-21/2005 H. Oniki

57

IV. Competition and Coordination of DTV and the Internet C. Policies for fair competition at level-playing field (6/6)

6. Policy recommendations

Enforce monopoly-front and the price-taker

requirements

9/20-21/2005 58