podcast #2. february 2021 ed sullivan, svp & chief economist

TRANSCRIPT

Cement Outlook BriefingPodcast #2. February 2021

Ed Sullivan, SVP & Chief Economist

Presentation Focus

1. Macroeconomic Data & Covid-19 Relief Impacts

2. IHME Covid-19 Projections

3. The Vaccine Scenario & Achieving Herd Immunity

4. Inflation Threats

5. Winter 2020-2021 Segment Projections

Macroeconomic Data

Unemployment ClaimsNew, Weekly

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

August 4th: 1,181 Deaths Inflection Point:

November 15th: 1,159 DeathsLow Point:

October 17th: 706 Deaths

Current 7 Day Moving Average: 3,183 Deaths

Note: IHME expects daily death rate will remain near current levels

through mid-February.

This is followed by a 1,000 decline in the rate each

subsequent month through April.

This suggests Covid-19 remains an elevated drag on economic

recovery

“Low Wage” Unemployment Exceeds 20%

Consumer SentimentComposite, University of Michigan

0

20

40

60

80

100

120

Covid-19 ImpactFebruary 101.

April 71.

Current: 79Lingering Covid-19

levels has prevented a meaningful recovery.

Note: With high sustained Covid-19 death rates

expected through April, consumers will remain cautious.

Consumer spending accounts for 2/3 of every $ generated in US GDP.

Slow growth and disappointing rates of improvement will characterize the economy.

At least through the first half of 2021.

Back to Normal IndexMoody’s-CNN Survey 100=March 1st

0

20

40

60

80

100

120

1-Mar-20 1-Apr-20 1-May-20 1-Jun-20 1-Jul-20 1-Aug-20 1-Sep-20 1-Oct-20 1-Nov-20 1-Dec-20 1-Jan-21

Current-18%

-40%

37 monthly & high frequency variables included in the index from home prices, rail traffic, business confidence, seated diners, etc.

August 15th:-21%Key Point.

Covid Relief programs prevent the economy from slipping into further decay. They enable a recovery. By themselves, they are not expected

to generate growth.

The Next Round of Covid-19 Relief: Key Spending

• Direct Payments• State Aid• Unemployment Sweetener• Re-open Schools• Child Tax Credit• Underfunded Pension• Covid-19 Testing• FEMA Disaster Support• Minimum Wage• Metro Transit

$422 Billion$350$246$129$109$82$49$45$47$28

Covid Data & Projections

IHME Daily Death Rate Projections7 Day Moving Average

0

500

1000

1500

2000

2500

3000

3500

4000

4500 CurrentCurrently, IHME projects that the daily death rate

will not decline to past peak (Mid-

April 2020) levels until early March.

Revised IHME Projections

The Vaccine Scenario

Vaccine Impact on the EconomyOnce the Vaccine is Mass Distributed….and herd immunity levels reached…..

It will:

• Result in a dramatic surge in consumer confidence.

• Encourage a return to many, but not all, Pre-Covid activities• Dining, movies, shopping, face-to-face interactions.

• Business will reopen, new businesses will emerge to fill voids created by the virus.• Perhaps encouraged by SBA support

• Investment uncertainty will decline.

• Economy will expand rapidly.

• Jobs growth will be strong.

This is largely based on consumers returning to pre-Covid patterns.

Given the severity and duration of the disruption…restoration of consumer patterns may occur over several quarters to materialize…

The process begins with consumers sense of safety and the achievement of herd immunity.

US Vaccine Supply

0

50

100

150

200

250

300

350

400

Q 4 2020 Q1 2021 Q2 2021 Q3 2021Old Production New Production

Notes: Q 4 Performance: Production-to-Contract: 67%, Doses Delivered-to-Vaccination: 33%Forward Assumptions: Production-to-Contract: 85%, Doses Delivered-to-Vaccination: 85%

Notes: Pfizer announced dramatic reduction in

processing from start to vial ready from 110 days to 60 days. This essentially increases Pfizer

production/supply by 45%.

Johnson & Johnson announced it will begin production in Q2.

Daily Rate of Vaccinations

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Q 4 2020 Q1 2021 Q2 2021 Q3 2021

Notes: With the news of increased vaccine production, the issue begins to shift from vaccine supply to convincing

enough of the population to get the vaccination.

Million Vaccination Doses Daily

Implied Herd Immunity Dates:

70% August 2nd

75% August 12th

80% August 22nd

85% September 2nd

Winter Forecast Assumption:

White Knight shows up mid-to-late third quarter, compared to early third quarter

assumed in the Winter Forecast.

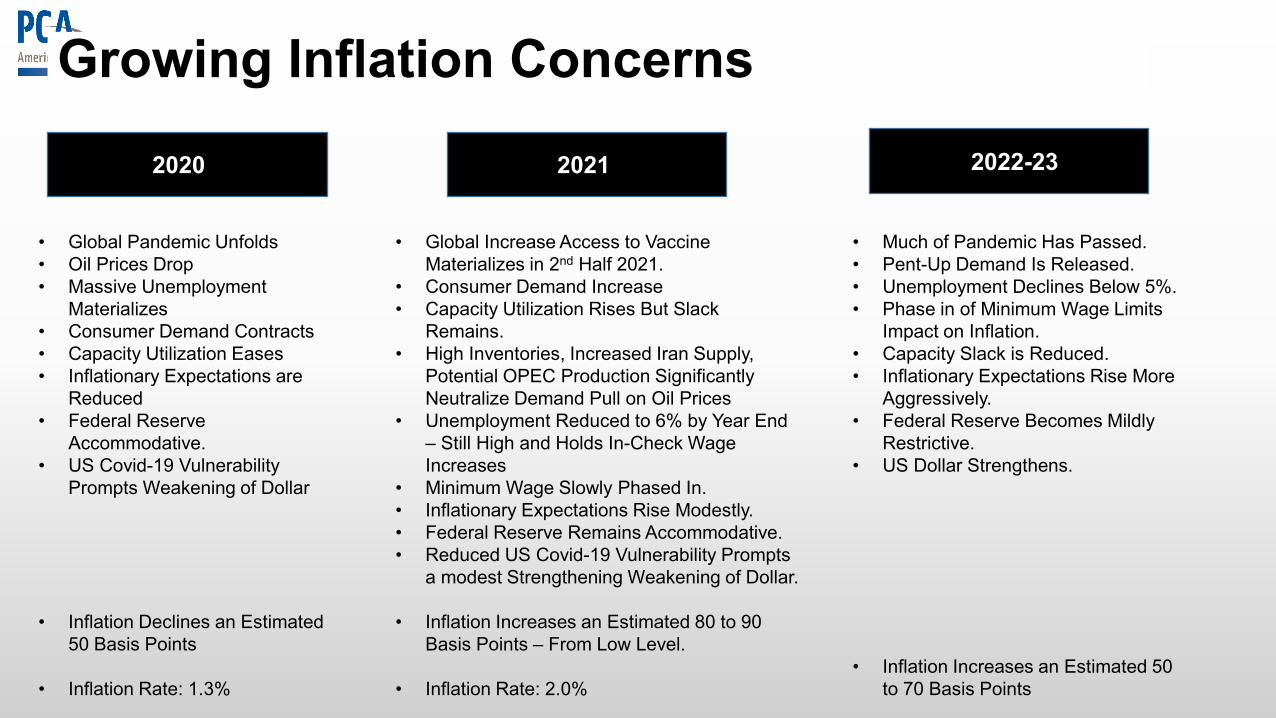

Growing Inflation Concerns

Growing Inflation Concerns

2020

• Global Pandemic Unfolds• Oil Prices Drop• Massive Unemployment

Materializes• Consumer Demand Contracts• Capacity Utilization Eases• Inflationary Expectations are

Reduced• Federal Reserve

Accommodative.• US Covid-19 Vulnerability

Prompts Weakening of Dollar

• Inflation Declines an Estimated 50 Basis Points

• Inflation Rate: 1.3%

2021 2022-23

• Global Increase Access to Vaccine Materializes in 2nd Half 2021.

• Consumer Demand Increase• Capacity Utilization Rises But Slack

Remains.• High Inventories, Increased Iran Supply,

Potential OPEC Production Significantly Neutralize Demand Pull on Oil Prices

• Unemployment Reduced to 6% by Year End – Still High and Holds In-Check Wage Increases

• Minimum Wage Slowly Phased In. • Inflationary Expectations Rise Modestly. • Federal Reserve Remains Accommodative.• Reduced US Covid-19 Vulnerability Prompts

a modest Strengthening Weakening of Dollar.

• Inflation Increases an Estimated 80 to 90 Basis Points – From Low Level.

• Inflation Rate: 2.0%

• Much of Pandemic Has Passed.• Pent-Up Demand Is Released.• Unemployment Declines Below 5%.• Phase in of Minimum Wage Limits

Impact on Inflation.• Capacity Slack is Reduced.• Inflationary Expectations Rise More

Aggressively.• Federal Reserve Becomes Mildly

Restrictive.• US Dollar Strengthens.

• Inflation Increases an Estimated 50 to 70 Basis Points

Residential Projection

0

1

1

2

2

3

3

4

4

5

5

Residential Cement Consumption Mortgage Interest Rates% Average SF Monthly Payment

950

1,000

1,050

1,100

1,150

1,200

1,250

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

2017 2018 2019 2020 2021 2022 2023 2024 2025

Residential Cement Consumption Residential Cement ConsumptionMetric Tons

0%

1%

2%

3%

4%

5%

2,017.00 2,018.00 2,019.00 2,020.00 2,021.00 2,022.00

Residential Cement Consumption Growth%, Y-O-Y

Nonresidential Projection

-30%

-25%

-20%

-15%

-10%

-5%

0%

Total

Nonresidential ConstructionReal PIP, Y-O-Y Change

IndustrialHotel

Office

Scarring & Bankruptcies

Vacancy Rates Increase

Sq Feet Vented onto MarketNOI Declines

Banks Tighten Lending

Standards

Nonresidential Construction

Decline

Working Capital Factor:

The longer below “normal” economic conditions persist – the more pressure occurs on

working capital and ability to stay open.

Structural Factors Contribute to Vacancy

Rates:

• Work-At-Home• E-Retail

• Virtual Meeting• E-Learning

• Urban Trend Slows

Bank Lending Officer Survey:

More Banks Tightening Lending

Standards Since 2008

Nonresidential Recovery Process

Nonresidential is not expected to contribute to growth until 2023

Public Projection

Revenue Decline

Less than 2% Decline

6% Decline or More

State Revenues: 2021

4.1 to 5.9% Decline

2.1 to 4% Decline

ME

RI

MA

VTNH

AL GA

SC

TN

FL

MS

LA

TX

OKNM

KS

MN

IA

MO

AR

WY

CO

ND

SD

NE

WA

ID

MT

OR

NVUT

AZ

CA

WI

ILIN

MI

OH

WVVA

NC

MD

DE

PA

NY

CT

NJ

• Depressed economic activity reduces tax collections.

• In context of Balance Budget Amendments, states either raise revenue collections via taxes or cut spending.

• Tax increases are out given the economic distress.

• Entitlement programs and support are least likely to be cut.

• Public construction programs become vulnerable.

• Without specific state relief in the Covid-19 Federal support program – public spending becomes a key downside risk factor for 2021 cement consumption.

• PCA Winter forecast positions public so that up and downside risks are balance.

• Currently, the next Federal Covid-19 support program may direct $300 Billion for state support. This represents upside risk to the current forecast.

Biden Plan & Moving Forward Act

PCA combines information from the Biden infrastructure plan and the Moving Forward Act passed by the House to garner potential

details. From there, cement intensities are assigned.

Very rough estimates suggest massive - UNPRECEDENTED

increases in annual cement consumption beginning in 2023.

The “Face Value” plan is more than 8 times the size of PCA’s

“placeholder of $235 billion over 10 years.

Key Point.The proposed program, as we see

it, is more massive than any previous infrastructure program.

Winter Projection

50,000

60,000

70,000

80,000

90,000

100,000

110,000

120,000

2017 2018 2019 2020 2021 2022 2023 2024 2025

Total Cement Consumption Total Cement ConsumptionMetric Tons

-1%

0%

1%

2%

3%

4%

5%

2017 2018 2019 2020 2021 2022 2023 2024 2025

Cement Consumption Growth%, Y-O-Y

Residential Strength Continues.Nonresidential weakness.Public reflects State fiscal exposure

2022-2023 Growth Acceleration reflects a Biden Infrastructure “Placeholder”

of $260 Billion Ten Year Program.

Cement Outlook BriefingPodcast #2. February 2021

Ed Sullivan, SVP & Chief Economist