poland - university of minnesota duluthjvileta/documents/businessforecastreportpolandbmi.pdfswot...

TRANSCRIPT

Published by BUSINESS MONITOR INTERNATIONAL LTD

BUSINESS FORECAST REPORT

Q4 2013www.businessmonitor.com

POLANDINCLUDES 10-YEAR FORECAST TO 2022

The Recovery Has Arrived

ISSN 1745-0667Published by Business Monitor International Ltd.

Copy Deadline: 16 August 2013

2 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013 P

OLA

ND

– M

AC

RO

EC

ON

OM

IC IN

DIC

ATO

RS

20

12e

201

3f 2

014f

201

5f 2

016f

201

7f 2

018f

201

9f 2

020f

202

1f 2

022f

Nom

inal

GD

P, U

S$b

n [1

]49

8.6

522.

351

1.6

569.

561

6.8

657.

670

5.5

747.

979

9.4

847.

690

2.5

Nom

inal

GD

P, P

LNbn

[2]

1,62

2.1

1,64

9.3

1,71

2.0

1,80

5.9

1,92

7.4

2,05

4.9

2,18

7.2

2,31

2.4

2,45

8.3

2,60

6.3

2,77

5.3

Nom

inal

GD

P, E

UR

bn [2

]39

2.6

392.

740

2.8

463.

051

4.0

548.

058

7.9

623.

366

6.2

706.

375

2.1

GD

P p

er c

apita

, US

$ [2

]13

,048

13,6

6613

,385

14,9

0116

,138

17,2

0818

,470

19,5

8920

,951

22,2

3023

,696

GD

P p

er c

apita

, EU

R [2

]10

,274

10,2

7510

,539

12,1

1513

,448

14,3

4015

,391

16,3

2417

,459

18,5

2519

,746

Rea

l GD

P g

row

th, %

cha

nge

y-o-

y [2

]2.

01.

22.

32.

83.

73.

63.

52.

83.

33.

03.

5

Priv

ate

final

con

sum

ptio

n, %

of G

DP

[2]

60.6

59.9

59.3

58.9

58.8

58.6

58.4

58.0

57.8

57.5

57.4

Priv

ate

final

con

sum

ptio

n, re

al g

row

th %

y-o

-y [2

]1.

10.

01.

32.

03.

53.

33.

02.

03.

02.

53.

3

Gov

ernm

ent fi

nal c

onsu

mpt

ion,

% T

otal

GD

P [2

]17

.617

.517

.417

.617

.617

.617

.617

.717

.817

.917

.9

Gov

ernm

ent fi

nal c

onsu

mpt

ion,

real

gro

wth

% y

-o-y

[2]

-0.8

0.6

2.0

3.6

3.6

3.6

3.6

3.6

3.6

3.6

3.6

Fixe

d ca

pita

l for

mat

ion,

% o

f GD

P [2

]20

.220

.120

.420

.520

.721

.021

.321

.621

.721

.922

.0

Fixe

d ca

pita

l for

mat

ion,

real

gro

wth

% y

-o-y

[2]

2.1

0.8

4.0

3.0

5.0

5.0

5.0

4.0

4.0

4.0

4.0

Pop

ulat

ion,

mn

[3]

38.2

38.2

38.2

38.2

38.2

38.2

38.2

38.2

38.2

38.1

38.1

Une

mpl

oym

ent,

% o

f lab

our f

orce

, eop

[4]

13.0

14.2

12.5

11.5

10.5

8.2

8.0

7.8

7.5

7.5

7.0

Con

sum

er p

rice

inde

x, %

y-o

-y, a

ve [4

]4.

10.

51.

52.

73.

03.

03.

03.

03.

03.

03.

0

Lend

ing

rate

, %, a

ve [5

]8.

58.

08.

08.

08.

08.

08.

08.

08.

08.

08.

0

Cen

tral B

ank

polic

y ra

te, %

eop

[6]

4.25

2.50

2.50

4.00

4.00

4.00

4.00

4.00

4.00

4.00

4.00

Exc

hang

e ra

te P

LN/U

S$,

ave

[7]

3.25

3.16

3.35

3.17

3.12

3.12

3.10

3.09

3.08

3.08

3.08

Exc

hang

e ra

te P

LN/E

UR

, ave

[7]

4.13

4.20

4.25

3.90

3.75

3.75

3.72

3.71

3.69

3.69

3.69

Bud

get b

alan

ce, U

S$b

n [8

]-1

9.3

-20.

6-1

8.4

-18.

3-1

4.9

-13.

3-1

6.8

-23.

6-2

5.1

-26.

6-2

8.2

Bud

get b

alan

ce, %

of G

DP

[8]

-3.9

-4.0

-3.6

-3.2

-2.4

-2.0

-2.4

-3.2

-3.1

-3.1

-3.1

Goo

ds a

nd s

ervi

ces

expo

rts, U

S$b

n [6

]22

3.5

248.

126

7.7

287.

831

1.7

345.

737

6.8

410.

744

7.7

488.

053

1.9

Goo

ds a

nd s

ervi

ces

impo

rts, U

S$b

n [6

]22

4.2

241.

826

0.9

283.

030

6.5

331.

036

0.8

393.

342

8.6

467.

250

9.3

Bal

ance

of t

rade

in g

oods

and

ser

vice

s, U

S$b

n [6

]-0

.66.

36.

84.

85.

214

.716

.017

.519

.020

.722

.6

Bal

ance

of t

rade

in g

oods

and

ser

vice

s, %

of G

DP

[6]

-0.1

1.2

1.3

0.8

0.8

2.2

2.3

2.3

2.4

2.4

2.5

Cur

rent

acc

ount

bal

ance

, US

$bn

[6]

-17.

1-1

3.0

-13.

0-1

5.8

-16.

4-8

.6-1

0.0

-12.

0-1

4.4

-17.

2-2

0.3

Cur

rent

acc

ount

bal

ance

, % o

f GD

P [6

]-3

.4-2

.5-2

.5-2

.8-2

.7-1

.3-1

.4-1

.6-1

.8-2

.0-2

.3

Fore

ign

rese

rves

ex

gold

, US

$bn

[9]

102.

710

5.8

108.

911

2.2

115.

611

9.0

122.

612

6.3

130.

113

0.1

130.

1

Impo

rt co

ver,

mon

ths

[9]

6.4

6.1

5.8

5.5

5.3

5.0

4.7

4.5

4.2

3.9

3.6

Not

es: e

BM

I est

imat

es. f

BM

I for

ecas

ts. S

ourc

es: 1

EU

RO

STA

T/B

MI,

US

$; 2

EU

RO

STA

T/B

MI;

3 0.

0; 4

Cen

tral S

tatis

tical

Offi

ce/B

MI;

5 IM

F; 6

Nat

iona

l Ban

k of

Pol

and/

BM

I; 7

BM

I; 8

BM

I/Min

istry

of F

inan

ce; 9

IM

F/B

MI.

Executive Summary ................................................................................................................................. 5Core Views ......................................................................................................................................................................................5Key Risk To Outlook ......................................................................................................................................................................5

Chapter 1: Political Outlook .................................................................................................................... 7SWOT Analysis .......................................................................................................................................................... 7BMI Political Risk Ratings ........................................................................................................................................ 7Domestic politics ....................................................................................................................................................... 8Economic Slowdown Creates Challenges For Tusk ...................................................................................................................8

While popular support for the Civic Platform-led government has fallen to all time lows, and is now polling lower than opposition party Law and Justice, we maintain our expectation for the government to serve out its term. Improvements in the labour market and economic activity should help to bolster support for the government in the second half of the year, although the razor-thin parliamentary majority remains a challenge.

Long-Term Political Outlook .................................................................................................................................... 9A Maturing Regional Power ...........................................................................................................................................................9

We consider Poland's long-term political risk profile to be on an upward trajectory, reflecting the country's maturing political institutions and greater confidence in the conduct of external affairs. Solid macroeconomic fundamentals underpin our expectation for improvement over the long run. Nevertheless, Poland still faces significant challenges to political stability in its external relations and at home.

Chapter 2: Economic Outlook ............................................................................................................... 13SWOT Analysis ........................................................................................................................................................ 13BMI Economic Risk Ratings ................................................................................................................................... 13Economic Activity ................................................................................................................................................... 14Middle Income Trap Overshadows Recovery ............................................................................................................................14Balance Of Payments .............................................................................................................................................. 16Cyclical Factors Obscure Structural Trend ...............................................................................................................................16

Despite Poland's current account posting its second consecutive surplus, we maintain our forecast for a deficit this year. Although we have revised up our figures slightly to 2.5% of GDP, from a previous forecast of 3.1%, we regard the recent trends as being cyclically driven, and expect the surplus to prove transient once domestic demand recovers towards the end of the year.

Fiscal Policy ............................................................................................................................................................. 18Wider Budget Deficits, But Credibility Intact .............................................................................................................................18

In light of weaker-than-expected government revenues, we have adjusted down our forecast for Poland's fiscal deficit in 2013 and 2014, and now expect the deficit to arrive at 4.0% of GDP and 3.6% of GDP respectively. However, the causes of the wider deficit are primarily cyclical rather than structural, and the government continues to make progress on structural consolidation.

TABLE: MAIN BUDGETARY MEASURES ........................................................................................................................................................... 18

Monetary Policy ....................................................................................................................................................... 19Fiscal Stimulus To Usurp Monetary Easing...............................................................................................................................19

Despite consumer prices heading close to deflationary territory, we do not expect the National Bank of Poland to make any more rate cuts this year, as we believe doing so could further weaken bank profitability by lowering net interest margins, acting as a disincentive to lending and creating tighter lending conditions in practice. The recent round of monetary easing has yet to yield any tangible increases in aggregate demand, and the announcement that the government is planning to increase spending suggests that fiscal stimulus is about to overtake monetary easing as the authorities preferred tool.

Currency Forecast ................................................................................................................................................... 21PLN: Maintaining Medium-Term Bearish Bias ...........................................................................................................................21TABLE: CURRENCY FORECASTS ....................................................................................................................................................................... 21

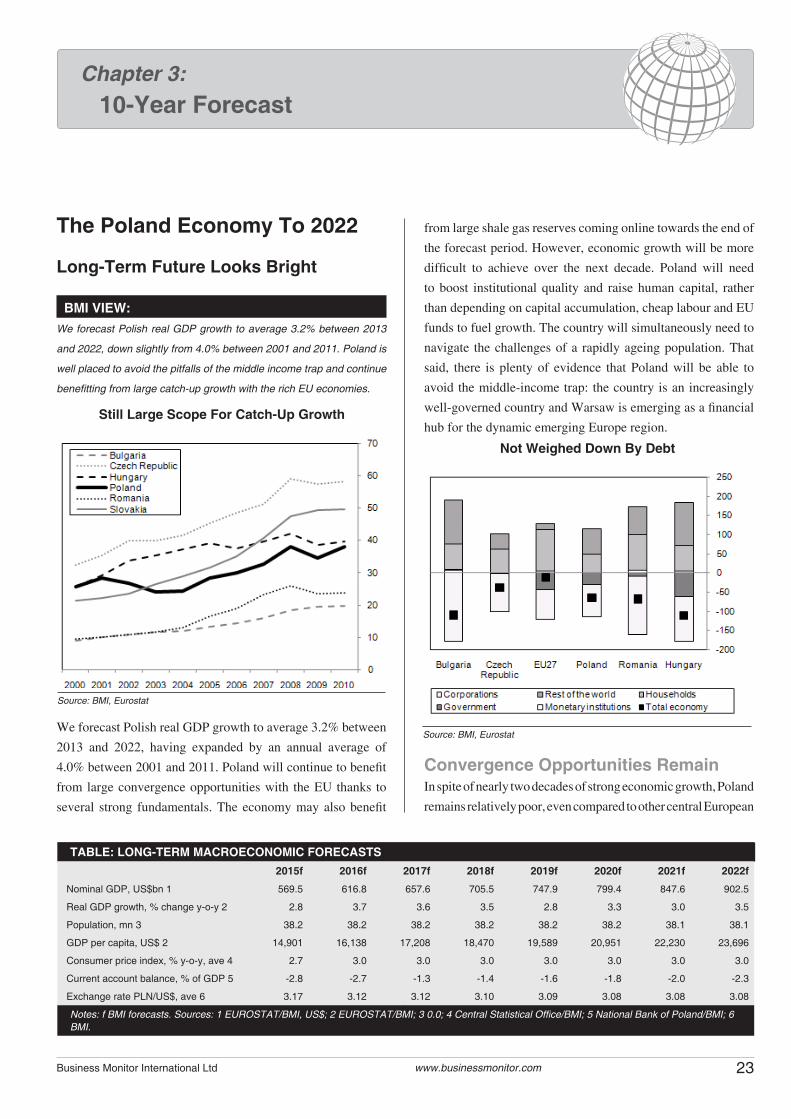

Chapter 3: 10-Year Forecast .................................................................................................................. 23The Poland Economy To 2022................................................................................................................................ 23

3Business Monitor International Ltd www.businessmonitor.com

Contents

Long-Term Future Looks Bright .................................................................................................................................................23We forecast Polish real GDP growth to average 3.2% between 2013 and 2022, down slightly from 4.0% between 2001 and 2011. Poland is well placed to avoid the pitfalls of the middle income trap and continue benefitting from large catch-up growth with the rich EU economies.

TABLE: LONG-TERM MACROECONOMIC FORECASTS ................................................................................................................................... 23

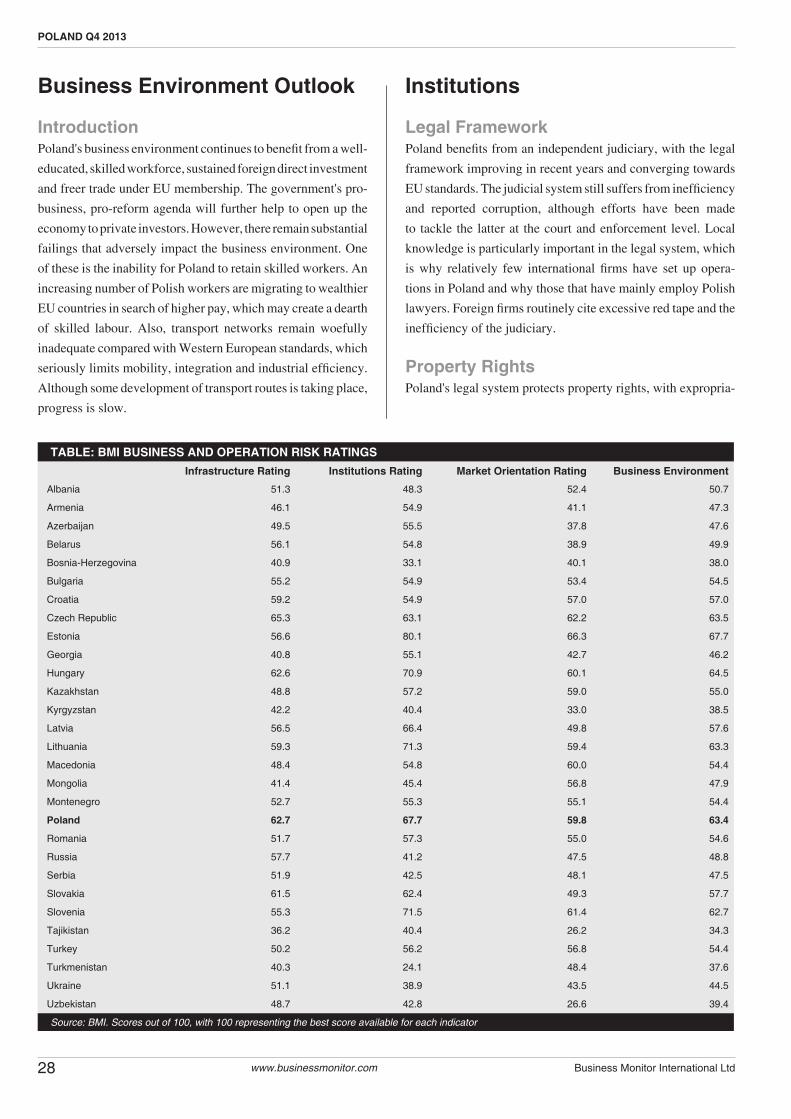

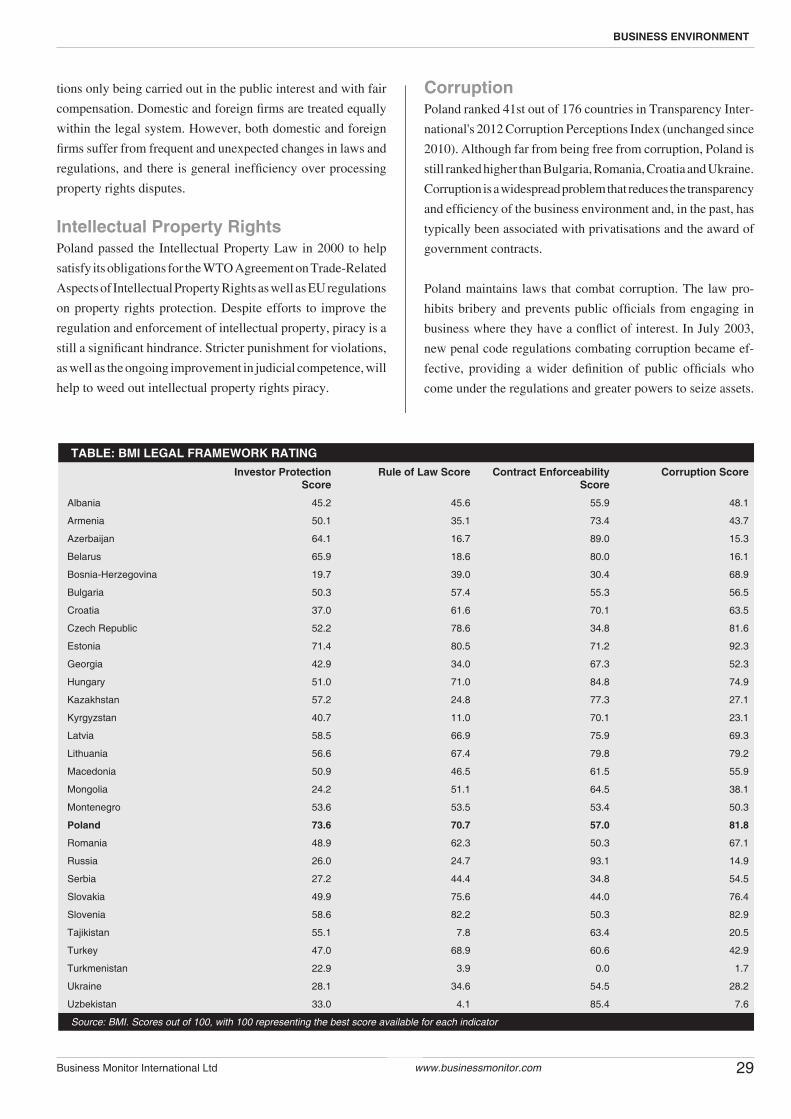

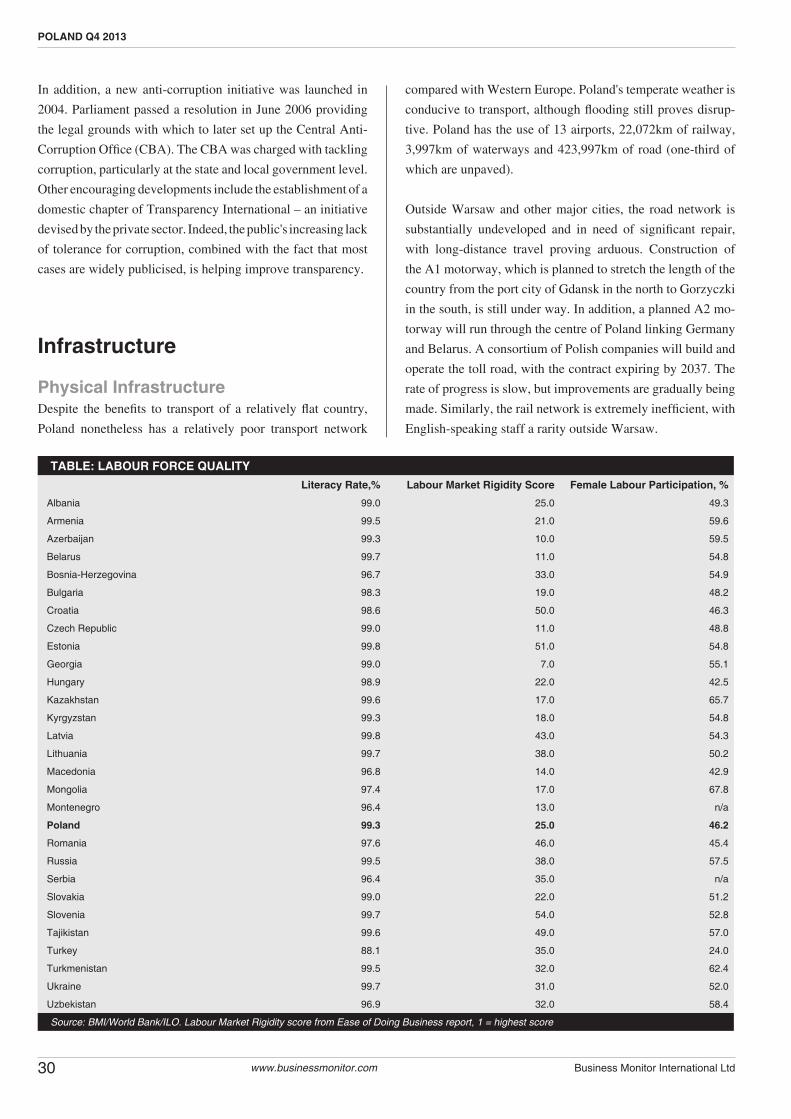

Chapter 4: Business Environment ........................................................................................................ 27SWOT Analysis ........................................................................................................................................................ 27BMI Business Environment Risk Ratings ............................................................................................................. 27Business Environment Outlook ............................................................................................................................. 28Institutions ............................................................................................................................................................... 28TABLE: BMI BUSINESS AND OPERATION RISK RATINGS .............................................................................................................................. 28TABLE: BMI LEGAL FRAMEWORK RATING ....................................................................................................................................................... 29

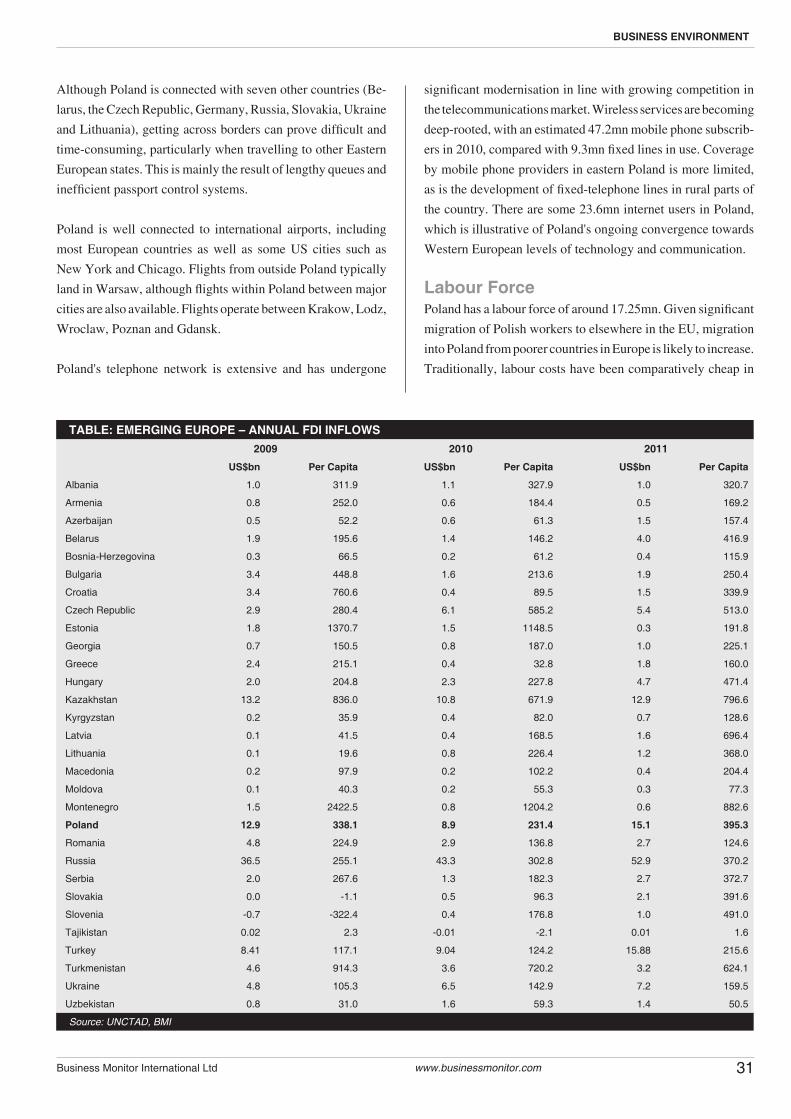

Infrastructure ........................................................................................................................................................... 30TABLE: LABOUR FORCE QUALITY ..................................................................................................................................................................... 30TABLE: EMERGING EUROPE – ANNUAL FDI INFLOWS ................................................................................................................................... 31TABLE: TRADE AND INVESTMENT RATINGS .................................................................................................................................................... 32

Market Orientation ................................................................................................................................................... 33TABLE: TOP EXPORT DESTINATIONS .............................................................................................................................................................. 33

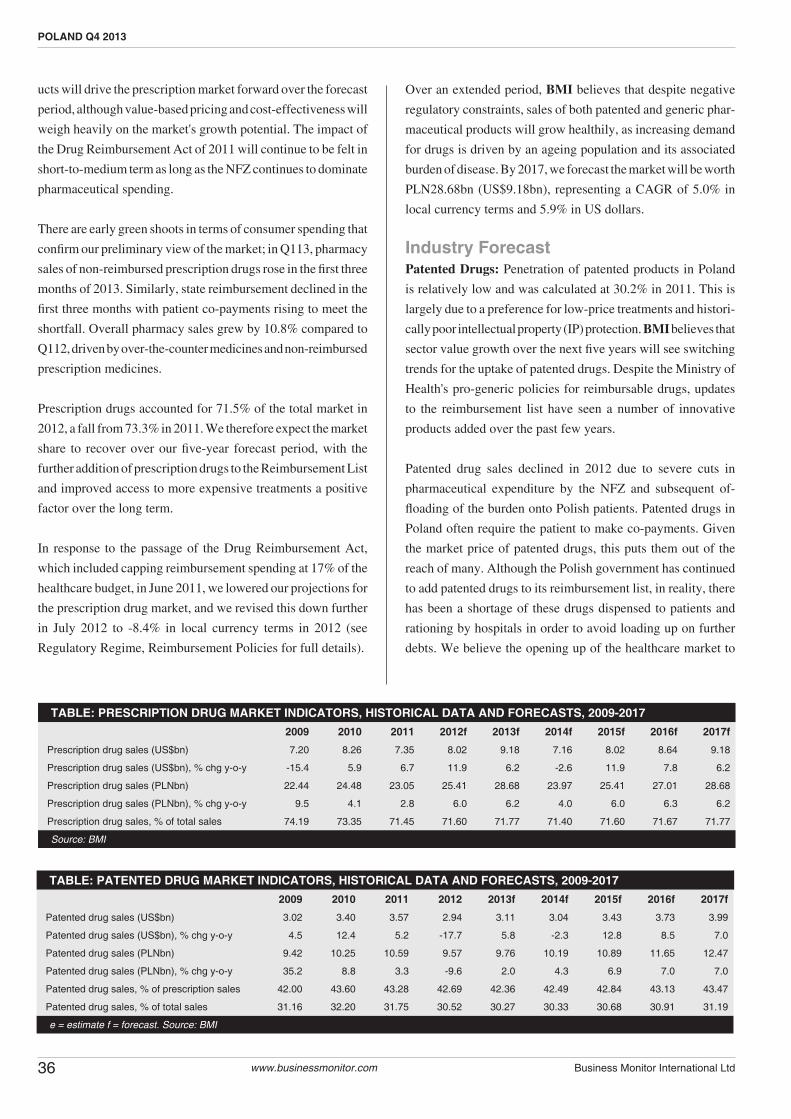

Operational Risk ..................................................................................................................................................... 34Pharmaceuticals ...................................................................................................................................................... 35Executive Summary ....................................................................................................................................................................35

Chapter 5: Key Sectors .......................................................................................................................... 35Pharmaceuticals ...................................................................................................................................................... 35TABLE: PRESCRIPTION DRUG MARKET INDICATORS, HISTORICAL DATA AND FORECASTS, 2009-2017 ............................................. 36TABLE: PATENTED DRUG MARKET INDICATORS, HISTORICAL DATA AND FORECASTS, 2009-2017 .................................................... 36TABLE: GENERICS DRUG MARKET INDICATORS, HISTORICAL DATA AND FORECASTS, 2009-2017 ...................................................... 37TABLE: OVER-THE-COUNTER MEDICINE MARKET INDICATORS, HISTORICAL DATA AND FORECASTS, 2009-2017 ............................ 38

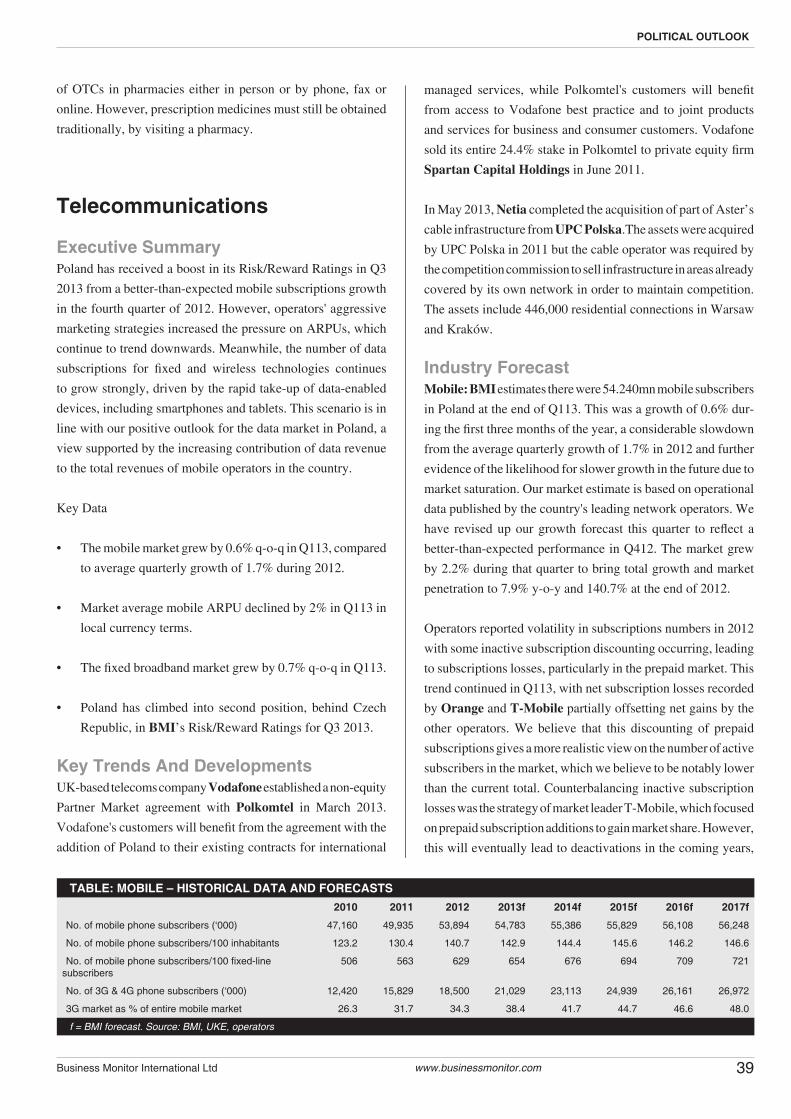

Telecommunications ............................................................................................................................................... 39TABLE: MOBILE – HISTORICAL DATA AND FORECASTS ............................................................................................................................... 39TABLE: ARPU – HISTORICAL DATA AND FORECASTS (PLN) ......................................................................................................................... 40TABLE: FIXED LINE – HISTORICAL DATA AND FORECASTS .......................................................................................................................... 41TABLE: INTERNET – HISTORICAL DATA AND FORECASTS ........................................................................................................................... 42

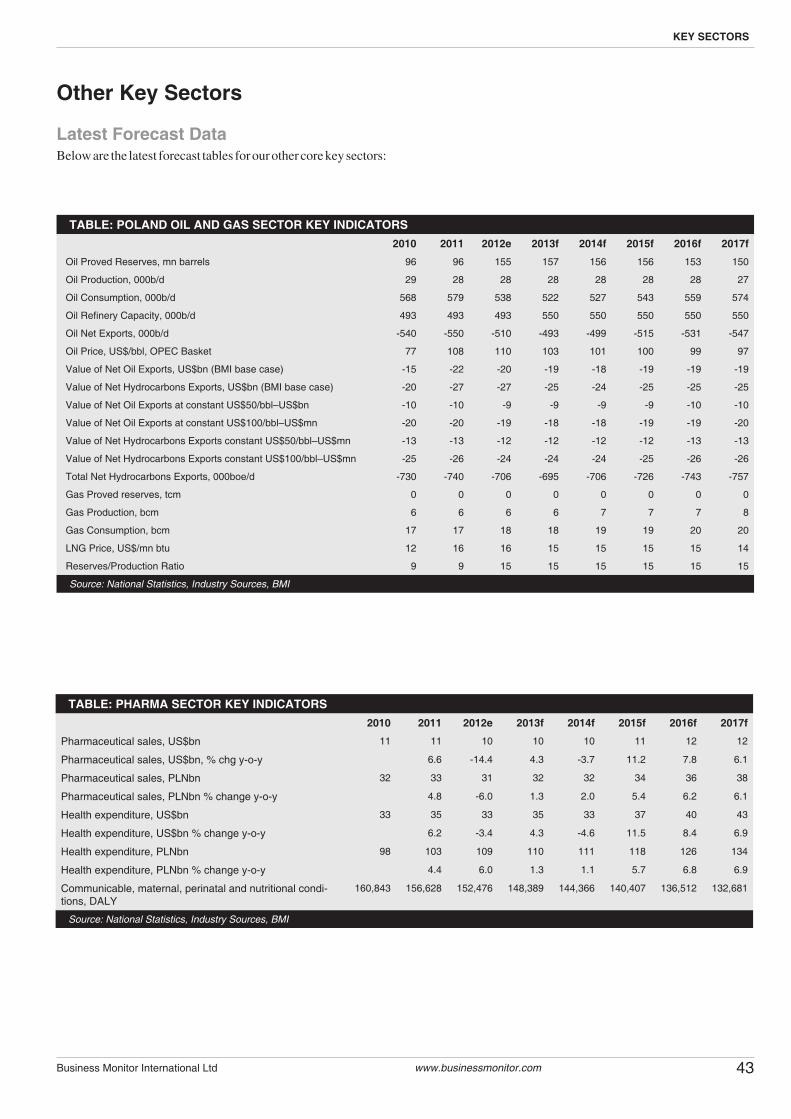

Other Key Sectors ................................................................................................................................................... 43TABLE: POLAND OIL AND GAS SECTOR KEY INDICATORS ........................................................................................................................... 43TABLE: PHARMA SECTOR KEY INDICATORS ................................................................................................................................................... 43TABLE: TELECOMS SECTOR KEY INDICATORS ............................................................................................................................................... 44TABLE: DEFENCE AND SECURITY SECTOR KEY INDICATORS ..................................................................................................................... 44TABLE: INFRASTRUCTURE SECTOR KEY INDICATORS ................................................................................................................................. 44TABLE: FOOD AND DRINK SECTOR KEY INDICATORS ................................................................................................................................... 45TABLE: AUTOS SECTOR KEY INDICATORS ...................................................................................................................................................... 45TABLE: FREIGHT KEY INDICATORS ................................................................................................................................................................... 45

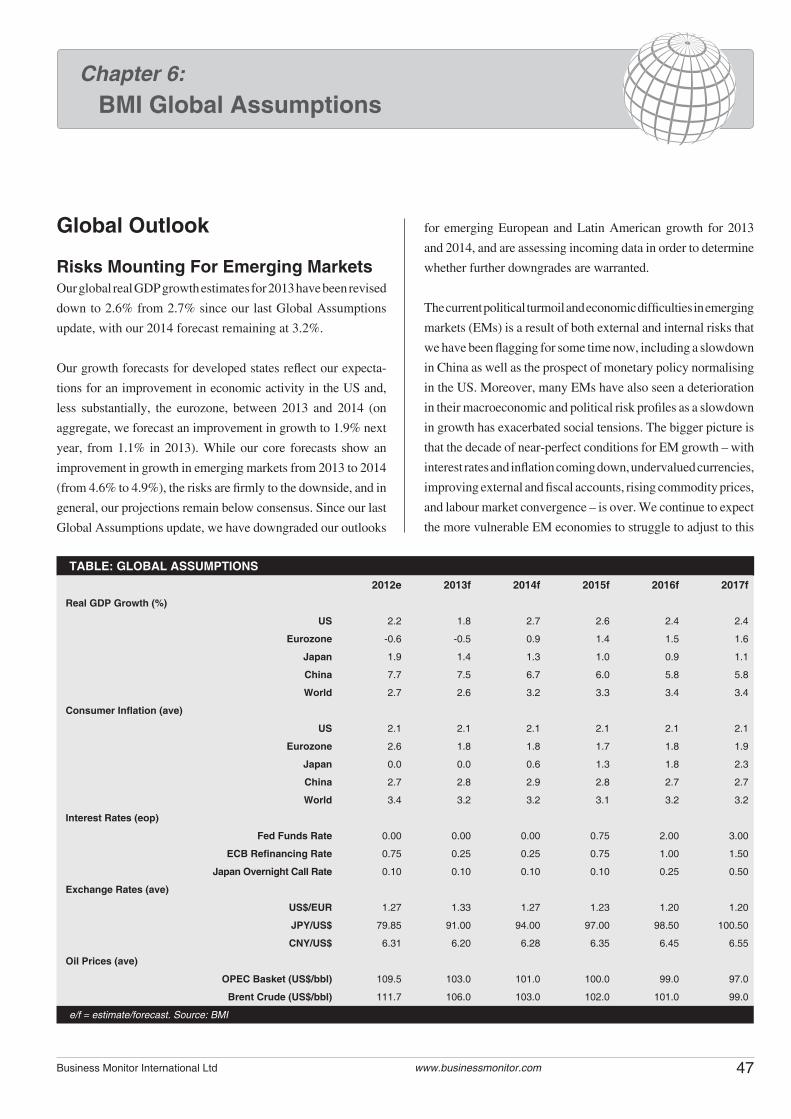

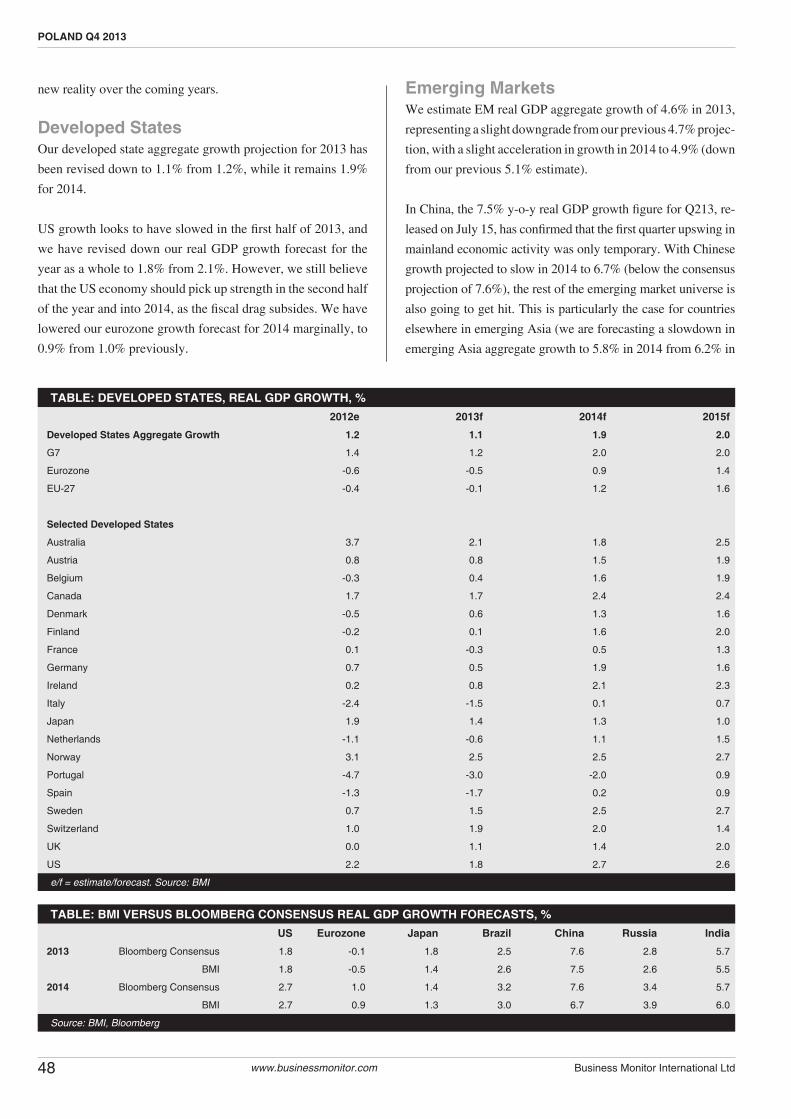

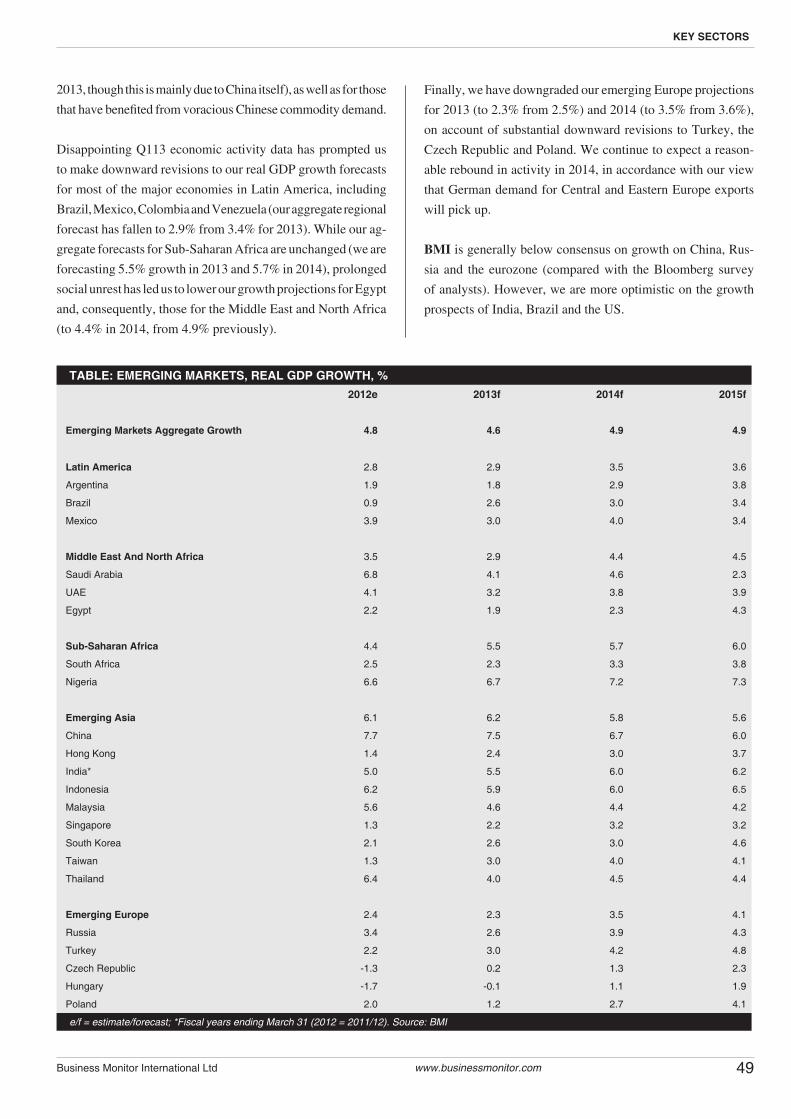

Chapter 6: BMI Global Assumptions .................................................................................................... 47Global Outlook ......................................................................................................................................................... 47Risks Mounting For Emerging Markets ......................................................................................................................................47TABLE: GLOBAL ASSUMPTIONS ........................................................................................................................................................................ 47TABLE: DEVELOPED STATES, REAL GDP GROWTH, % .................................................................................................................................. 48TABLE: BMI VERSUS BLOOMBERG CONSENSUS REAL GDP GROWTH FORECASTS, % .......................................................................... 48TABLE: EMERGING MARKETS, REAL GDP GROWTH, % ................................................................................................................................. 49

4 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

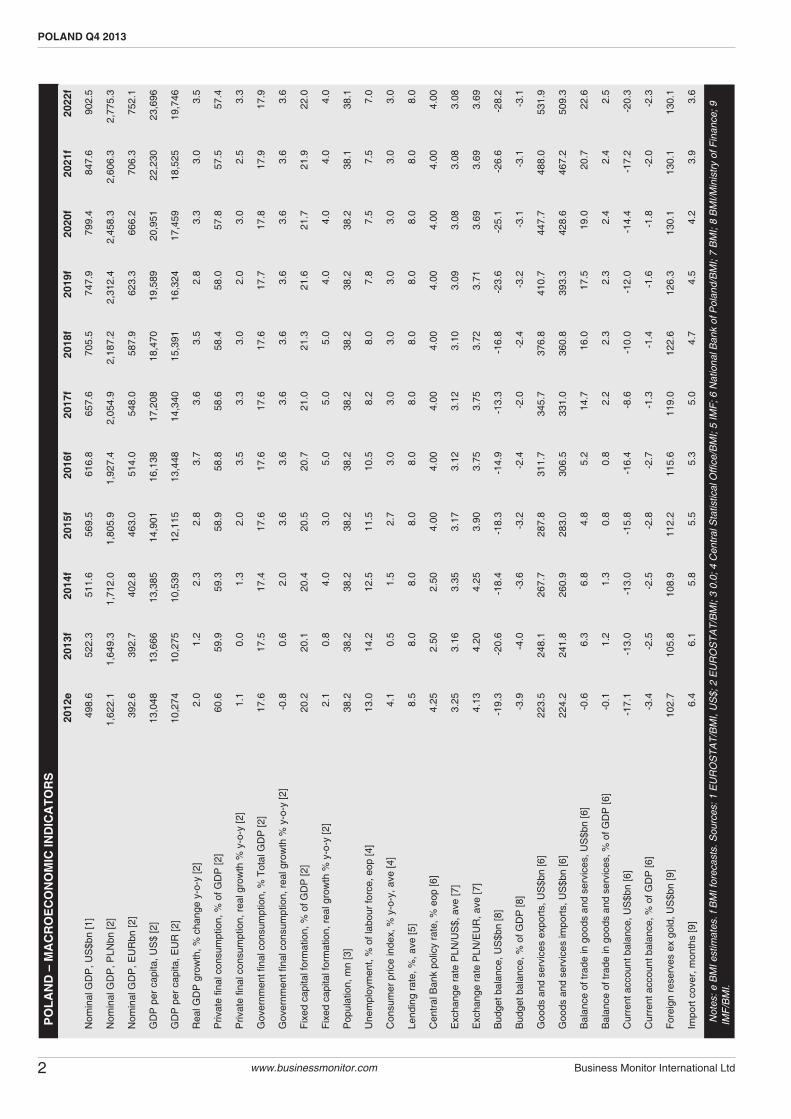

Core Views While we are forecasting relatively robust economic activity over

the medium-term, high unemployment and stagnant real wages will

continue to weigh on real GDP growth.

Poland’s external position remains relatively strong. We forecast

the current account deficit to narrow from 4.3% of GDP in 2011 to

2.5% in 2013 as the economic slowdown reduces import demand.

However, a large stock of foreign-owned government paper and

ongoing private sector deleveraging represent the two major risks

to our sanguine outlook.

We continue to expect the Civic Platform (PO)-led government

to serve out its term. The government won a recent parliamen-

tary vote of confidence, suggesting its parliamentary majority is

safe for the time being. We also believe that the opposition will

struggle to broaden its appeal despite the rising government

unpopularity, limiting its ability to challenge the ruling coalition.

Major Forecast Changes

In light of the disinflationary environment and a sharp deceleration

in domestic demand, we have revised down our fiscal deficit projec-

tions, which we now expect to arrive at 4.0% in 2013 and 3.6% in

2014. Despite our expectations for Poland to miss the EU’s 3.0%

of GDP budget target this year, Poland will likely avoid punishment

under the exceptional growth clause which permits some leeway

on targets due to very low annual growth

Due to weak domestic demand, we have revised our current account

forecasts for 2013, and now expect the current account deficit to

arrive at 2.5% of GDP from a previous forecast of 3.1%.

Low inflation and slowing growth have paved the way for further

monetary easing, and we now forecast 75 basis points of cuts to

the base rate in 2013, bringing it to 2.50% by year-end.

Key Risk To Outlook Although not our core scenario, we highlight the risk of Greece

leaving the euro, potentially leading to a disorderly breakup of the

whole common currency bloc. This would likely push Poland into

recession.

5Business Monitor International Ltd www.businessmonitor.com

Executive Summary

Brief Methodology

7Business Monitor International Ltd www.businessmonitor.com 7Business Monitor International Ltd www.businessmonitor.com

SWOT Analysis

Strengths EU membership and eventual eurozone accession should facilitate

medium-term political stability. The next scheduled general election

is in 2015, giving the Civic Platform (Platforma Obywatelska, PO)-led

coalition space to implement politically painful austerity measures.

Weaknesses The sudden rise in popularity of a radical reformist party such as

Palikot’s Movement shows a growing discontent with traditional

parties and the electorate’s desire for change. Threatened by this,

the governing coalition could be tempted to bow to populist reforms

in an effort to appease the electorate and halt the party’s rise.

Opportunities There is scope for further integration with key Euro-Atlantic institu-

tions, which will elevate Poland’s international profile.

The election of Bronislaw Komorowski (formerly of Civic Platform) as

president provides the coalition with a head of state sympathetic to

the government’s agenda, thereby removing the potential roadblock

of a presidential veto.

Threats The need to undertake deep fiscal consolidation in an effort to bring

the country’s fiscal accounts under control could see support for Civic

Platform start to wane. Indeed, several PO deputies have already

defected.

BMI Political Risk RatingsDonald Tusk’s re-election in late 2011 was the first time since the fall

of communism that a government won a second term, marking an

important achievement for Poland’s maturing democracy. The country

now enjoys broad political stability. Poland’s long-term political risk rat-

ing of 86.4 reflects our expectations that, as long-term economic and

political convergence with the West continues, political conditions will

remain favourable.

Chapter 1: Political Outlook

S-T Political Rank TrendTurkmenistan 82.7 1 =Estonia 80.4 2 =Czech Republic 78.3 3 =Poland 76.5 4 =Kazakhstan 71.5 5 -Russia 71.0 6 =Latvia 71.0 6 =Mongolia 70.4 8 +Lithuania 70.2 9 =Croatia 68.1 10 -Azerbaijan 67.5 11 =Ukraine 67.1 12 +Hungary 66.0 13 =Romania 65.4 14 =Slovakia 65.2 15 =Montenegro 64.8 16 =Georgia 61.5 17 =Uzbekistan 60.8 18 =Turkey 59.2 19 =Armenia 57.1 20 =Slovenia 56.5 21 =Macedonia 56.2 22 =Albania 54.2 23 +Tajikistan 51.9 24 =Belarus 51.7 25 =Serbia 49.8 26 =Bulgaria 49.4 27 -Moldova 44.4 28 =Kosovo 40.4 29 =Kyrgyzstan 36.0 30 -Bosnia-Herzegovina 33.8 31 =Regional ave 62.5 / Global ave 65.2 / Emerging Markets ave 62.6

L-T Political Rank TrendCzech Republic 87.0 1 =Poland 86.4 2 =Estonia 84.8 3 =Slovenia 83.2 4 =Lithuania 79.3 5 =Slovakia 79.2 6 =Latvia 77.1 7 =Hungary 73.9 8 =Croatia 73.2 9 -Bulgaria 73.1 10 =Romania 69.9 11 =Mongolia 67.7 12 +Turkey 65.6 13 =Albania 63.8 14 =Macedonia 63.4 15 =Montenegro 61.5 16 =Kazakhstan 60.3 17 =Armenia 59.6 18 =Russia 57.0 19 =Serbia 55.8 20 =Ukraine 53.0 21 =Turkmenistan 52.6 22 =Bosnia-Herzegovina 51.8 23 =Moldova 51.1 24 =Belarus 50.3 25 =Uzbekistan 50.2 26 =Azerbaijan 49.0 27 =Kosovo 48.3 28 =Georgia 46.8 29 =Tajikistan 42.2 30 =Kyrgyzstan 37.2 31 =Regional ave 64.5 / Global ave 63.1 / Emerging Markets ave 59.5

Domestic politics

Economic Slowdown Creates Challenges For Tusk

BMI VIEWWhile popular support for the Civic Platform-led government has fallen

to all time lows, and is now polling lower than opposition party Law

and Justice, we maintain our expectation for the government to serve

out its term. Improvements in the labour market and economic activity

should help to bolster support for the government in the second half

of the year, although the razor-thin parliamentary majority remains a

challenge.

Poland's Prime Minister Donald Tusk is facing growing chal-

lenges on the domestic front, with recent polling showing support

for his government falling to record lows since taking power

back in November 2007. Poll readings from June show that

support for the Tusk administration fell to just 18% (although

July's poll showed a slight improvement, rising to 25%), from

40% after its re-election in 2011, as the government struggles

to reignite Poland's slowing economy. The administration has

long struggled with a razor- thin majority, and has experienced

two major scandals during its recent terms. The deputy leader of

the Civic Platform (PO)'s coalition partner, the Polish People's

Party (PSL), resigned as agriculture minister after allegations

of corruption in an organisation affiliated to the ministry. The

Polish media have since regularly reported on PSL patronage

within the Ministry for Agriculture. As a result, the opposition

Law and Justice (PiS) party has pulled ahead in opinion polling,

with a recent survey putting support for PiS at 32% against the

ruling Civic Platform at 25%. However, despite its slim major-

ity, we believe that the PO-led government is likely to serve out

its term. The government has clearly lost some support since it

won 39.2% of the vote at the last general election in November

2011, but the PiS will struggle to wrestle the middle ground of

Polish politics from the PO. The PiS relies on a hard-line Catholic

message that fails to resonate with the young and urban, while

its nationalist undertones alienate many.

There are several causes underpinning the slide in the govern-

ment's popularity, including the painful fiscal austerity pro-

gramme implemented by Tusk, including a deeply unpopular

pension reform that raised the retirement age to 67 years (from

65 for men and 60 for women). However, the weak economy

has also played a major role, with the sharpest decline in the

support for the government coinciding with the deceleration

in economic activity and rising unemployment experienced

most strongly from Q112 onwards. The labour market remains

a particular source of discontent, with the unemployment rate

reaching 14.4% in February 2013. While headline unemploy-

ment fell to 13.2% in June, the drop was attributable to seasonal

hiring patterns (the data is not seasonally-adjusted) and the year-

on-year trend shows employment continuing to fall in Poland.

We expect the economy to rebound in the second half of the

year, which should help ameliorate Civic Platform's approval

ratings to some extent, although substantial improvements in

labour market conditions will probably be delayed until 2014.

Faced with falling revenues due to weak growth, the govern-

ment's decision to forgo further and instead opt for a wider

budget deficit over the next two years will also help to prop up

8 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

Economic Headwinds Have Weakened PO’s Dominance

Opinion Poll: Evaluation of government

Source: CBOS

Opposition Pulls Into LeadPopular support for: (%)

Source: CBOS

support over the medium-term. The main risk facing Tusk at

the moment is the dangerously slim majority, which stood at

just five seats in August after a series of defections since 2011.

Long-Term Political Outlook

A Maturing Regional Power

BMI VIEWWe consider Poland's long-term political risk profile to be on an upward

trajectory, reflecting the country's maturing political institutions and

greater confidence in the conduct of external affairs. Solid macroeco-

nomic fundamentals underpin our expectation for improvement over

the long run. Nevertheless, Poland still faces significant challenges to

political stability in its external relations and at home.

We broadly expect Poland's political risk profile to improve

over the course of our 10-year forecast horizon, as the country

assumes greater responsibility at the regional and international

level and the domestic political environment continues to mature.

Our core scenario envisages Poland emerging as a solid 'middle

power' of Europe. A strong macroeconomic outlook, coupled

with greater maturity on the part of domestic policymakers,

would facilitate this general progression over the years ahead.

A member of the EU and NATO since 2004 and 1999 respec-

tively, Poland is established within a Western policy trajectory

track. We expect the EU to remain a key policy anchor for

Warsaw as Poland's political and economic dynamics become

more intimately intertwined with those of its EU neighbours,

particularly Germany. The handling of the six-month rotating

EU presidency by Prime Minister Tusk's government amid the

escalation of eurozone's sovereign debt crisis also highlighted

the country's increasing political maturity and integration in

European affairs.

Key to Poland's political risk trajectory will be the way it conducts

foreign relationships with regard to the US, the EU and – last but

not least – Russia. The Polish government's heretofore close-knit

relationship with its US counterparts is likely to persist over the

long term. Polish designs for influence at the European level,

however, could strain relations with Poland's partners on both

sides of the Atlantic. What is more, the country's relationship

with Russia will remain key to regional tensions and may suffer

as Warsaw's confidence grows in the years ahead.

In addition to significant foreign policy questions, the country

will face challenges at home. While economic growth remains

far from negative territory and has imbued Poland with a sense

of optimism and confidence after the country was among the

few to avoid recession in 2009, the future will not be without

policy choices and challenges, not least of which is related to

the unwinding of massive fiscal stimulus initiated between

2008 and 2010.

Finally, we highlight that a possible clash between an older,

conservative generation and younger, more liberal voters could

be on the cards in the years ahead.

External Relations: A Distinctly Polish AffairForeign policy will likely be a cornerstone of Poland's long-term

political risk trajectory. Considering Poland's tumultuous his-

tory, which has been typified by a relatively precarious national

security position as well as its geostrategic importance in the

European theatre, any consideration of the country's political

risk outlook must consider the possible permutations of foreign

affairs. Below, we consider the trajectory of Warsaw's relations

with three major states whose power and influence could come

to intersect in Poland: the US, Russia and the EU.

US-Poland Relations: These countries are likely to maintain

close ties over the course of our forecast period. The US was

a major ally in Poland's aspirations for independence from

communist rule and later a key pillar of support as the country

underwent a dramatic economic transition from a command-

9Business Monitor International Ltd www.businessmonitor.com

POLITICAL OUTLOOK

Labour Market Conditions Should Improve In 2014Unemployment (%) and Average Employment (% chg y-o-y)

Source: BMI, Bloomberg

based to market-based economy in the 1990s. The US is likely

to remain key to Poland's historically conditioned aspirations

to secure some form of sovereign guarantee and as a way to

increase the country's influence abroad.

From the perspective of the US, Poland serves as a useful and

staunch ally in Central Europe. Warsaw supported the US's 'War

on Terror' at a much higher level that its Western European

peers, in particular Germany and France, sending troops not

only to Afghanistan but also to Iraq. The May 2011 decision to

base a US F-16 fighter wing in Poland for the first time reflects

the prospect that the US-Polish relationship is a key strategic

consideration for both parties. While Poland clearly represents

the junior partner in the relationship, the US's strategic interests

in a Central European presence, and Polish aspirations towards

an existential security guarantee as well as regional power and

influence, mean that the basic underpinnings of the relationship

are likely to remain in place through the next decade.

Russia-Poland Relations: In stark contrast to the warm rela-

tionship enjoyed with the US, Poland's relationship with Rus-

sia is likely to remain less than rosy over our forecast period.

Historical tensions between the two countries run deep, not least

because of the legacy of Soviet dominance. Nevertheless, our

core scenario envisages Russia-Poland relations becoming more

pragmatic as increased political maturity in Poland translates into

more consistent foreign policy procedures and pronouncements;

this should reduce the likelihood of major diplomatic ructions.

However, considering that we believe the Poland-US relation-

ship will remain well established over the long term, increased

political and military integration with the US could strain ten-

sions with Russia. Moreover, we cannot discount the risk that

Polish lawmakers will attempt to score political points at home

by raising the level of nationalist rhetoric, which would most

likely paint Russia in an antagonistic light.

EU-Poland Relations: Our core scenario for Poland's relation-

ship with Brussels and EU member states envisages continued

cooperation. Parallel to a relatively positive macroeconomic

growth picture and maturing political arena, Poland will likely

enjoy growing influence at the supranational level, eventually

establishing itself as an effective middle power. In particular,

we believe Poland could become one of the leaders of the

'younger' members of the European integration project. While

this may unsettle some of the more established member states

such as Germany and France, Poland's relations with the EU

will most likely remain constructive over our forecast period.

In particular, Poland could have a particularly profound influ-

ence on European-level defence policymaking, considering the

country's vested interest in securing its own borders.

The tone and trajectory of relations with the EU could conversely

present a challenge to Poland's long-term political risk profile. In

particular, the Warsaw-Brussels relationship could be strained

by Poland's attempts to foster closer ties with the US – some-

thing that may place it at odds with major European powers

and may undercut European foreign policy options. Moreover,

and as alluded to above, Poland will likely enjoy increasing

status and influence at the supranational level over the coming

decade – something that will undoubtedly challenge Europe's

traditional dominance by France and Germany. EU immigration

10 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

The Hinge Of Europe Regional Map

Source: BMI

Political Risk Outperformer Long-Term Political Risk Rating & Component Scores

(Out Of 100)

Source: BMI

may also come under the spotlight, as the significant flows of

Polish workers into other European nations could come under

increasing scrutiny by foreign politicians hoping to boost their

political popularity at home amid weak domestic economies.

Challenges And Threats To StabilityDomestic Political Maturity: A key question and challenge

for Poland's long-term political outlook will be the level of

maturity shown by both institutions and politicians. Prime Min-

ister Tusk's re-election on October 9, the first re-election of an

incumbent government since the end of communist rule, bodes

well for policy continuity and marks an increased maturity in

the country's political system. We highlight this as a positive

development, as Poland's political landscape remains heavily

fractured along ideological and social lines.

Social Challenges Ahead: Overall, we believe that Poland's

sound macroeconomic fundamentals will most likely keep

disputes over social and economic policy relatively muted.

Poland remains one of the most socially conservative countries

in Europe, with strong Roman Catholic roots as demonstrated

by the near-iconic status enjoyed by the late Pope John Paul II.

In turn, we cannot rule out more divisive social policy issues

coming to the fore, as a relatively benign macroeconomic back-

drop enables voters to increasingly shift their voting preference

formulation along social lines. In such an event, we highlight

that a younger, more liberal class of voters that harbours little

memory of life under communist rule and the movement for

independence could come into conflict with a older and gener-

ally more conservative class. Furthermore, we believe that, as

the country enters a period of fiscal austerity, greater questions

regarding the socially optimal allocation of wealth could come

to the forefront of domestic policy considerations.

Long-Term Political Risk RatingPoland's long-term political risk rating stands at 86.4 out of 100,

according to BMI’s proprietary risk rating system, which ranks

the country 13th out of the 177 countries assessed worldwide.

Moreover, the rating marks Poland as a clear outperformer in

the European space, outranking even the eurozone average of

82.4. The high rating reflects what we see as a well-established

domestic policy trajectory, with Poland scoring particularly well

in 'policy continuity'. Moreover, domestic public policy disputes

as well as issues regarding minority rights are relatively limited,

boding well for the 'characteristics of policy' and 'characteristics

of society' components.

Over the long term, we expect Poland's membership in the EU

to be secure, providing a key policy anchor. To us, the key risk

to Poland's political risk rating over our forecast horizon relates

to how the country adapts to increasing influence in regional

and international affairs. Below, we present a wide range of

scenarios towards 2022. We assign scores for likelihood out

of 10, with 10 being highly likely and 1 being highly unlikely.

Scenarios For Political ChangeScenario One–A European 'Middle Power' Within The EU: As alluded to above, our core scenario entails Poland

establishing itself as an effective 'middle power' of Europe and

achieving greater integration with the EU and its constituent

supranational institutions. Under such a sequence of events, this

would see Poland leveraging its clear economic outperformer

status in the Central and Eastern European space and should

see the country gain increasing influence among its European

peers. Moreover, we expect Poland's young democratic political

culture and institutions to grow more mature over the course of

our forecast period, which should bode well for policy continuity

and implementation. In turn, a more consistent and steady hand

at the wheel of both domestic and foreign policymaking bodes

well for increasing Poland's influence abroad. In terms of foreign

policy specifically, a strong relationship with the US will persist

and Poland will prove adept at handling affairs with Russia.

Likelihood: 8

Scenario Two–Greater Assertiveness At The EU's Expense: Our second possible trajectory entails the country undergoing a

similar increase in confidence regarding its domestic and external

affairs, underpinned by a strong macroeconomic story at home.

However, under this alternative chain of events, the country's

increased assertiveness comes at the expense of good relations

with the EU. Indeed, considering the fundamental way that

Poland's historical insecurity shapes the conduct of its external

affairs, the country may find itself frustrated in its attempts to

find a satisfying security guarantee within the European security

structure. At that point, Warsaw may be forced to adopt a more

assertive foreign policy stance than that of its EU peers in order

to satisfy a sense of self-security, much like it did in backing

the US-led 'War on Terror'. This may strain relations with the

EU, not least in the foreign policy sphere. Furthermore, we

see scope that Poland could forego joining the euro. Indeed,

Poland has already delayed the adoption of the single currency

indefinitely, having originally planned to enter the eurozone

some time in 2012.

Likelihood: 6

11Business Monitor International Ltd www.businessmonitor.com

POLITICAL OUTLOOK

Scenario Three–An Economic Faltering: While our core

scenario for Poland sees economic growth chugging along at an

average rate of 3.2% in real terms over 2013-2022, we cannot

rule out the possibility that macroeconomic expansion falters

and the current optimism surrounding the future of the country

concomitantly wanes. In such an event, we highlight the risk

that a more populist brand of politics takes hold in Poland,

derailing the maturing market-based, liberal policy consensus

that is currently on the ascendancy. This would pose the po-

tential for less consistent domestic policymaking. This could

also derail Poland's aspirations to take on a larger role at the

EU and international level.

Likelihood: 4

Scenario Four–Excessive Assertiveness: While much less

likely, we do see scope that Poland becomes much more asser-

tive in its foreign policy stance. Fiscal austerity and military

retrenchment on both sides of the Atlantic (against the backdrop

of a Russian military modernisation drive) pose the risk that

Warsaw begins to become more bellicose in its rhetoric towards

Russia, which could lead to a deterioration in relations – some-

thing that may make Poland's key allies in the EU and the US

more nervous. Efforts by the US to roll back its presence in

NATO and in Europe could lead to greater assertiveness and

seeking of existential guarantees by Polish politicians. Indeed,

Warsaw was in need of reassurance following the US's decision

in 2009 to scale back an anti-ballistic missile shield based in

Poland while also seeking rapprochement with the Russians.

As mentioned above, Poland's efforts to effect material security

guarantees under the EU framework would also likely fail to

assuage Polish concerns.

While we believe the direct threat of greater Russian assertiveness

over its former satellite states is remote, the fundamental’security

question'-driven nature of Polish foreign policy formation

means that a more bellicose and confrontational Warsaw can-

not be ruled out. While our likelihood rating for this outcome

is low, we caution that, combined with a faltering of Poland's

strong domestic growth story, a swing towards more populist

politics–which would most likely tap latent nationalism–would

raise the probability of this outcome materially.

Likelihood: 2

12 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

13Business Monitor International Ltd www.businessmonitor.com

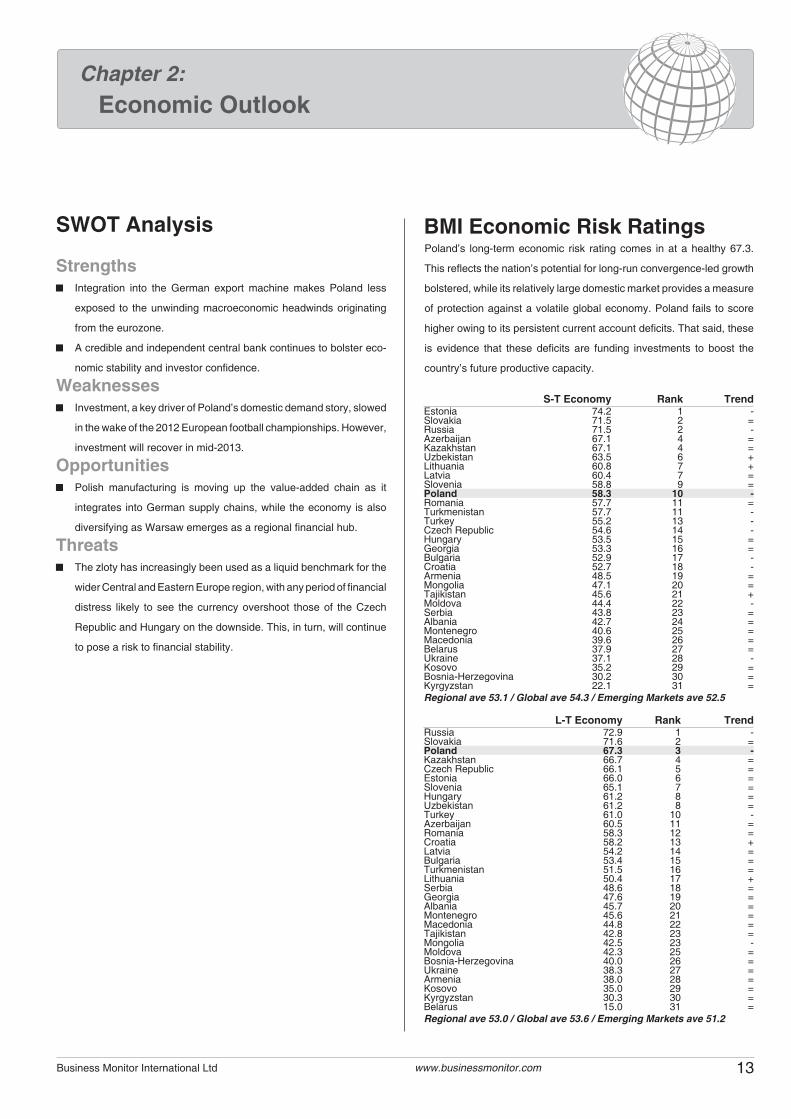

SWOT Analysis

Strengths Integration into the German export machine makes Poland less

exposed to the unwinding macroeconomic headwinds originating

from the eurozone.

A credible and independent central bank continues to bolster eco-

nomic stability and investor confidence.

Weaknesses Investment, a key driver of Poland’s domestic demand story, slowed

in the wake of the 2012 European football championships. However,

investment will recover in mid-2013.

Opportunities Polish manufacturing is moving up the value-added chain as it

integrates into German supply chains, while the economy is also

diversifying as Warsaw emerges as a regional financial hub.

Threats The zloty has increasingly been used as a liquid benchmark for the

wider Central and Eastern Europe region, with any period of financial

distress likely to see the currency overshoot those of the Czech

Republic and Hungary on the downside. This, in turn, will continue

to pose a risk to financial stability.

BMI Economic Risk RatingsPoland’s long-term economic risk rating comes in at a healthy 67.3.

This reflects the nation’s potential for long-run convergence-led growth

bolstered, while its relatively large domestic market provides a measure

of protection against a volatile global economy. Poland fails to score

higher owing to its persistent current account deficits. That said, these

is evidence that these deficits are funding investments to boost the

country’s future productive capacity.

Chapter 2: Economic Outlook

S-T Economy Rank TrendEstonia 74.2 1 -Slovakia 71.5 2 =Russia 71.5 2 -Azerbaijan 67.1 4 =Kazakhstan 67.1 4 =Uzbekistan 63.5 6 +Lithuania 60.8 7 +Latvia 60.4 7 =Slovenia 58.8 9 =Poland 58.3 10 -Romania 57.7 11 =Turkmenistan 57.7 11 -Turkey 55.2 13 -Czech Republic 54.6 14 -Hungary 53.5 15 =Georgia 53.3 16 =Bulgaria 52.9 17 -Croatia 52.7 18 -Armenia 48.5 19 =Mongolia 47.1 20 =Tajikistan 45.6 21 +Moldova 44.4 22 -Serbia 43.8 23 =Albania 42.7 24 =Montenegro 40.6 25 =Macedonia 39.6 26 =Belarus 37.9 27 =Ukraine 37.1 28 -Kosovo 35.2 29 =Bosnia-Herzegovina 30.2 30 =Kyrgyzstan 22.1 31 =Regional ave 53.1 / Global ave 54.3 / Emerging Markets ave 52.5

L-T Economy Rank TrendRussia 72.9 1 -Slovakia 71.6 2 =Poland 67.3 3 -Kazakhstan 66.7 4 =Czech Republic 66.1 5 =Estonia 66.0 6 =Slovenia 65.1 7 =Hungary 61.2 8 =Uzbekistan 61.2 8 =Turkey 61.0 10 -Azerbaijan 60.5 11 =Romania 58.3 12 =Croatia 58.2 13 +Latvia 54.2 14 =Bulgaria 53.4 15 =Turkmenistan 51.5 16 =Lithuania 50.4 17 +Serbia 48.6 18 =Georgia 47.6 19 =Albania 45.7 20 =Montenegro 45.6 21 =Macedonia 44.8 22 =Tajikistan 42.8 23 =Mongolia 42.5 23 -Moldova 42.3 25 =Bosnia-Herzegovina 40.0 26 =Ukraine 38.3 27 =Armenia 38.0 28 =Kosovo 35.0 29 =Kyrgyzstan 30.3 30 =Belarus 15.0 31 =Regional ave 53.0 / Global ave 53.6 / Emerging Markets ave 51.2

Economic Activity

Middle Income Trap Overshadows RecoveryMacro Outlook : Polish economic indicators are showing tenta-

tive signs of improvement, giving weight to our expectations

for a gradual economic rebound to take hold in the second half

of 2013. Nonetheless, we reiterate that the recovery will be

protracted, and primarily led by exports, with domestic demand

unlikely to start showing strong signs of an improvement until

2014. Accordingly, the recovery remains strongly contingent

upon sustained demand from Germany and other key trade

partners. While we are modestly optimistic towards Germany's

economic outlook, we see greater risks emerging from other

European partners such as France, Italy and the Czech Republic,

as well as slowing demand from China.

Nonetheless, our core view is that the economic slowdown has

bottomed, and real GDP growth should arrive around 1.2% in

2013. However, we have downgraded our forecasts for 2014,

forecasting real GDP to grow by 2.3%, from a previous forecast

of 2.7%, and 2.8% in 2015, from a previous forecast of 4.1%

respectively. We see medium-term growth prospects becoming

increasingly challenging in Poland, with growing risks of the

country falling victim to the middle-income trap unless greater

efforts are made to encourage innovation and R&D investment.

Investors should not assume the country will automatically

revert to 4.0%-plus higher real GDP growth rates, particularly

as the lower-end of the manufacturing sector will come under

greater competition from South-Eastern European countries

such as Romania and Turkey.

Real GDP By Expenditure BreakdownPrivate Consumption: While the retail sales index grew 1.8%

y-o-y in June, following average growth of just -0.1% in the

four preceding months, we think a robust recovery in household

consumption this year is still off the cards.

The labour market remains weak, with unemployment continuing

to trend higher over the first half of 2013, and the majority of

the fall in Q213 attributable to seasonal hiring patterns. Weak

household consumption is particularly negative for Poland’s

economic activity prospects relative to other CEE-4 econo-

mies, as Poland is much more heavily reliant upon household

consumption as an engine of growth.

Nonetheless, there are signals that point towards an improve-

ment in 2014. Consumer confidence has started to pick up, with

'consumer confidence towards personal finances over the next 12

months' rising to -11.5 in July, from -18.7 at the start of 2013.

Our expectations for a gradual recovery in exports should see

the labour market start to improve as hiring picks up, and this

should also feed through into improved household consumption.

Government Consumption: In our last quarterly growth up-

date, we suggested that a combination of weaker growth and

lower than expected inflation would drive weaker government

revenues, which without additional adjustments would limit

the room for a major expansion in government spending over

2013 and 2014. This has largely materialised, with revenue

undershoot forcing the government to suspend the legislative

50% public debt-to-GDP ratio limit in order to avoid making

14 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

Domestic Demand Still FlatliningReal GDP By Expenditure Selected Components, % chg y-o-y

Source: BMI, NBP

Polish Companies Suffer From Lack Of InnovationInnovation Among Small Companies (10-49 employees) –

Technology Innovation

Source: BMI, NBP, Eurostat

emergency cuts to the budget. While this arguably amounts to

de facto fiscal stimulus, it is unlikely to have any substantial

impact on growth this year as government spending in real

terms will not increase. Furthermore, both the remaining debt

caps at 55% of GDP and 60% of GDP (the latter of which is

constitutionally binding) remain in place, acting as a restraint on

expansionary fiscal policy. We forecast government consump-

tion to contribute just 0.1 percentage points (pp) to headline

real GDP growth in 2013.

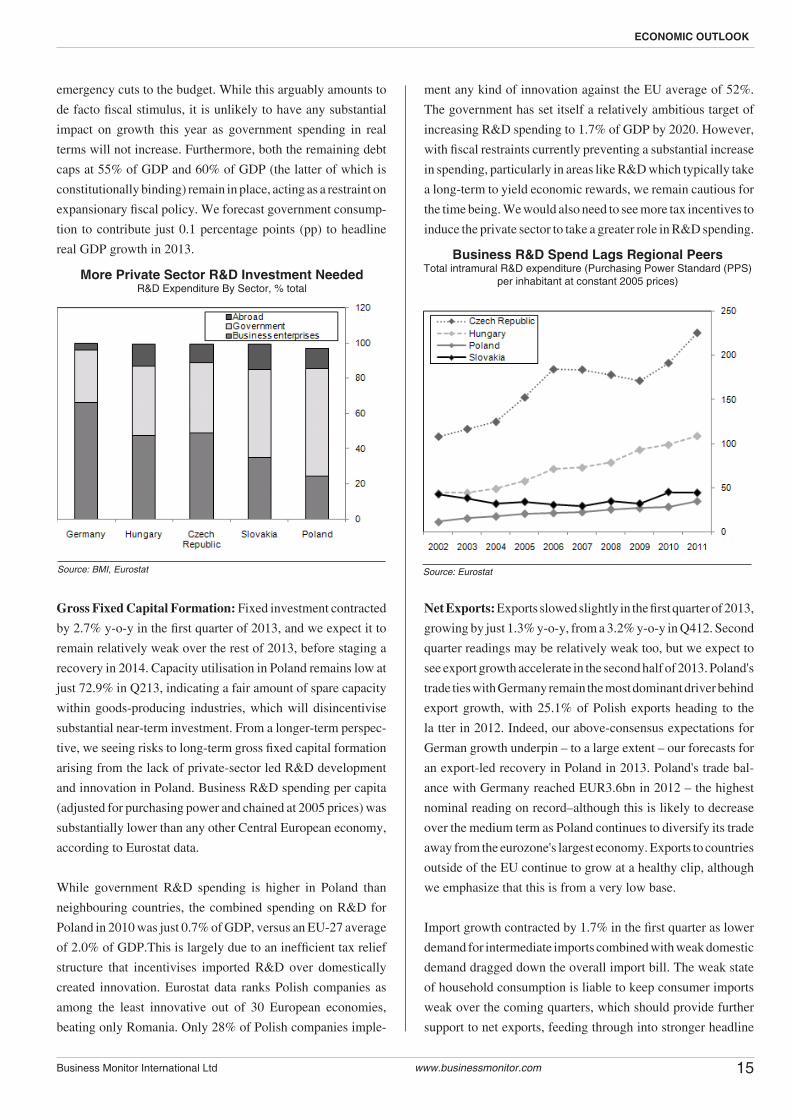

Gross Fixed Capital Formation: Fixed investment contracted

by 2.7% y-o-y in the first quarter of 2013, and we expect it to

remain relatively weak over the rest of 2013, before staging a

recovery in 2014. Capacity utilisation in Poland remains low at

just 72.9% in Q213, indicating a fair amount of spare capacity

within goods-producing industries, which will disincentivise

substantial near-term investment. From a longer-term perspec-

tive, we seeing risks to long-term gross fixed capital formation

arising from the lack of private-sector led R&D development

and innovation in Poland. Business R&D spending per capita

(adjusted for purchasing power and chained at 2005 prices) was

substantially lower than any other Central European economy,

according to Eurostat data.

While government R&D spending is higher in Poland than

neighbouring countries, the combined spending on R&D for

Poland in 2010 was just 0.7% of GDP, versus an EU-27 average

of 2.0% of GDP.This is largely due to an inefficient tax relief

structure that incentivises imported R&D over domestically

created innovation. Eurostat data ranks Polish companies as

among the least innovative out of 30 European economies,

beating only Romania. Only 28% of Polish companies imple-

ment any kind of innovation against the EU average of 52%.

The government has set itself a relatively ambitious target of

increasing R&D spending to 1.7% of GDP by 2020. However,

with fiscal restraints currently preventing a substantial increase

in spending, particularly in areas like R&D which typically take

a long-term to yield economic rewards, we remain cautious for

the time being. We would also need to see more tax incentives to

induce the private sector to take a greater role in R&D spending.

Net Exports: Exports slowed slightly in the first quarter of 2013,

growing by just 1.3% y-o-y, from a 3.2% y-o-y in Q412. Second

quarter readings may be relatively weak too, but we expect to

see export growth accelerate in the second half of 2013. Poland's

trade ties with Germany remain the most dominant driver behind

export growth, with 25.1% of Polish exports heading to the

la tter in 2012. Indeed, our above-consensus expectations for

German growth underpin – to a large extent – our forecasts for

an export-led recovery in Poland in 2013. Poland's trade bal-

ance with Germany reached EUR3.6bn in 2012 – the highest

nominal reading on record–although this is likely to decrease

over the medium term as Poland continues to diversify its trade

away from the eurozone's largest economy. Exports to countries

outside of the EU continue to grow at a healthy clip, although

we emphasize that this is from a very low base.

Import growth contracted by 1.7% in the first quarter as lower

demand for intermediate imports combined with weak domestic

demand dragged down the overall import bill. The weak state

of household consumption is liable to keep consumer imports

weak over the coming quarters, which should provide further

support to net exports, feeding through into stronger headline

15Business Monitor International Ltd www.businessmonitor.com

ECONOMIC OUTLOOK

More Private Sector R&D Investment NeededR&D Expenditure By Sector, % total

Source: BMI, Eurostat

Business R&D Spend Lags Regional PeersTotal intramural R&D expenditure (Purchasing Power Standard (PPS)

per inhabitant at constant 2005 prices)

Source: Eurostat

real GDP in 2013.

Risks To OutlookAs we are forecasting an export-driven recovery, our forecasts

our heavily contingent on a sustained recovery in Germany's

manufacturing sector. We are slightly above consensus for Ger-

man real GDP growth in 2013, expecting 0.5% growth against

Bloomberg consensus expectations of 0.4%, although the range

of the survey varies from zero to 1.0% growth indicate substantial

variance in growth expectations. Nonetheless, should German

manufacturing growth disappoint, this would probably shave

a few tenths of a percentage point off our headline real GDP

forecast for Poland.

Balance Of Payments

Cyclical Factors Obscure Structural Trend

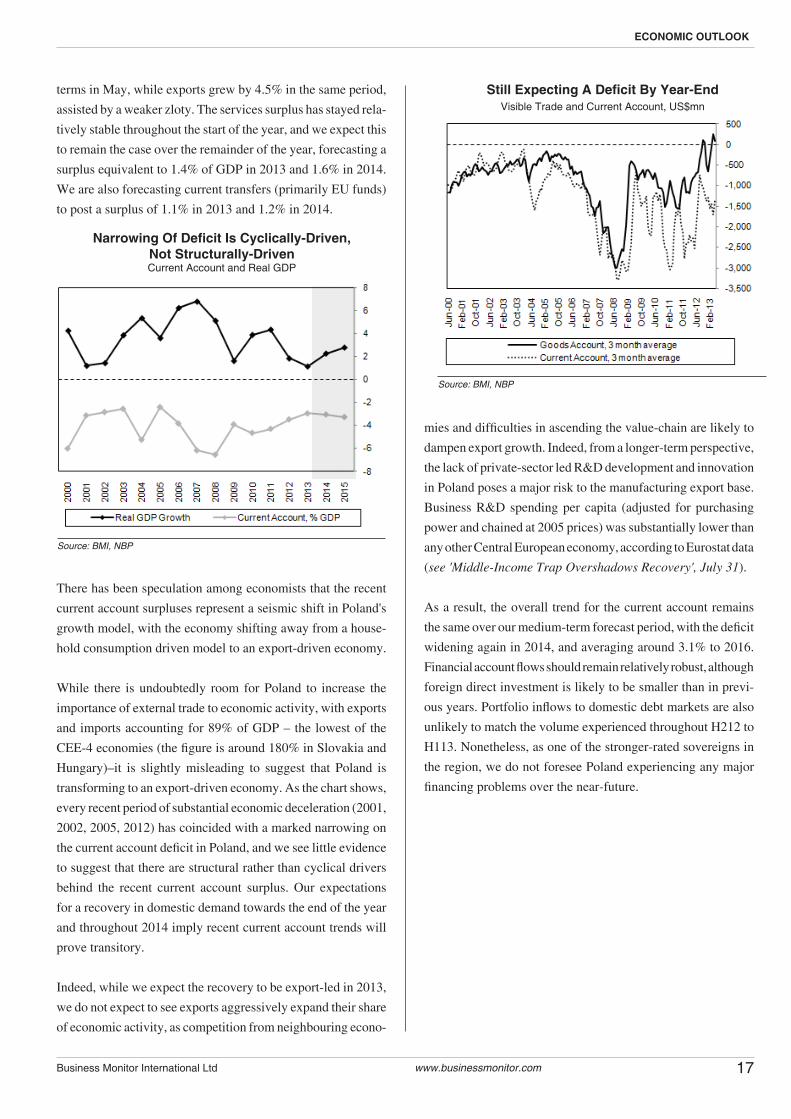

BMI VIEW : Despite Poland's current account posting its second consecutive sur-

plus, we maintain our forecast for a deficit this year. Although we have

revised up our figures slightly to 2.5% of GDP, from a previous forecast

of 3.1%, we regard the recent trends as being cyclically driven, and

expect the surplus to prove transient once domestic demand recovers

towards the end of the year.

Poland's current account has moved sharply into surplus for the

second consecutive month in May, driven by a major improve-

ment in the country's visible trade balance.

We have adjusted our forecasts for the current account, and

now expect a deficit equivalent to 2.5% of GDP in 2013, from a

previous forecast of 3.1%. Nonetheless, while central bank head

Marek Belka suggested some of the improvement in the current

account may be sustained, we regard the surplus as primarily

cyclical, and expect the trade surplus to disappear in the second

half of the year, pulling the current account back into deficit.

The narrowing trade surplus has be en driven by weak import

growth, as Poland struggles with the weakest household con-

sumption on record. Imports contracted by 3.2% in year-on- year

16 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

Household Consumption Should RecoverTowards Q413

Goods Imports & Exports, six month average (US$mn)

Source: BMI, NBP

Surplus Driven By Trade Account,As Imports Collapse

Current Account Components, US$mn

Source: BMI, NBP

Germany Still Dominates ExportsExports By Destination, % total

Source: BMI, Eurostat

terms in May, while exports grew by 4.5% in the same period,

assisted by a weaker zloty. The services surplus has stayed rela-

tively stable throughout the start of the year, and we expect this

to remain the case over the remainder of the year, forecasting a

surplus equivalent to 1.4% of GDP in 2013 and 1.6% in 2014.

We are also forecasting current transfers (primarily EU funds)

to post a surplus of 1.1% in 2013 and 1.2% in 2014.

There has been speculation among economists that the recent

current account surpluses represent a seismic shift in Poland's

growth model, with the economy shifting away from a house-

hold consumption driven model to an export-driven economy.

While there is undoubtedly room for Poland to increase the

importance of external trade to economic activity, with exports

and imports accounting for 89% of GDP – the lowest of the

CEE-4 economies (the figure is around 180% in Slovakia and

Hungary)–it is slightly misleading to suggest that Poland is

transforming to an export-driven economy. As the chart shows,

every recent period of substantial economic deceleration (2001,

2002, 2005, 2012) has coincided with a marked narrowing on

the current account deficit in Poland, and we see little evidence

to suggest that there are structural rather than cyclical drivers

behind the recent current account surplus. Our expectations

for a recovery in domestic demand towards the end of the year

and throughout 2014 imply recent current account trends will

prove transitory.

Indeed, while we expect the recovery to be export-led in 2013,

we do not expect to see exports aggressively expand their share

of economic activity, as competition from neighbouring econo-

mies and difficulties in ascending the value-chain are likely to

dampen export growth. Indeed, from a longer-term perspective,

the lack of private-sector led R&D development and innovation

in Poland poses a major risk to the manufacturing export base.

Business R&D spending per capita (adjusted for purchasing

power and chained at 2005 prices) was substantially lower than

any other Central European economy, according to Eurostat data

(see 'Middle-Income Trap Overshadows Recovery', July 31).

As a result, the overall trend for the current account remains

the same over our medium-term forecast period, with the deficit

widening again in 2014, and averaging around 3.1% to 2016.

Financial account flows should remain relatively robust, although

foreign direct investment is likely to be smaller than in previ-

ous years. Portfolio inflows to domestic debt markets are also

unlikely to match the volume experienced throughout H212 to

H113. Nonetheless, as one of the stronger-rated sovereigns in

the region, we do not foresee Poland experiencing any major

financing problems over the near-future.

17Business Monitor International Ltd www.businessmonitor.com

ECONOMIC OUTLOOK

Narrowing Of Deficit Is Cyclically-Driven, Not Structurally-DrivenCurrent Account and Real GDP

Source: BMI, NBP

Still Expecting A Deficit By Year-EndVisible Trade and Current Account, US$mn

Source: BMI, NBP

Fiscal Policy

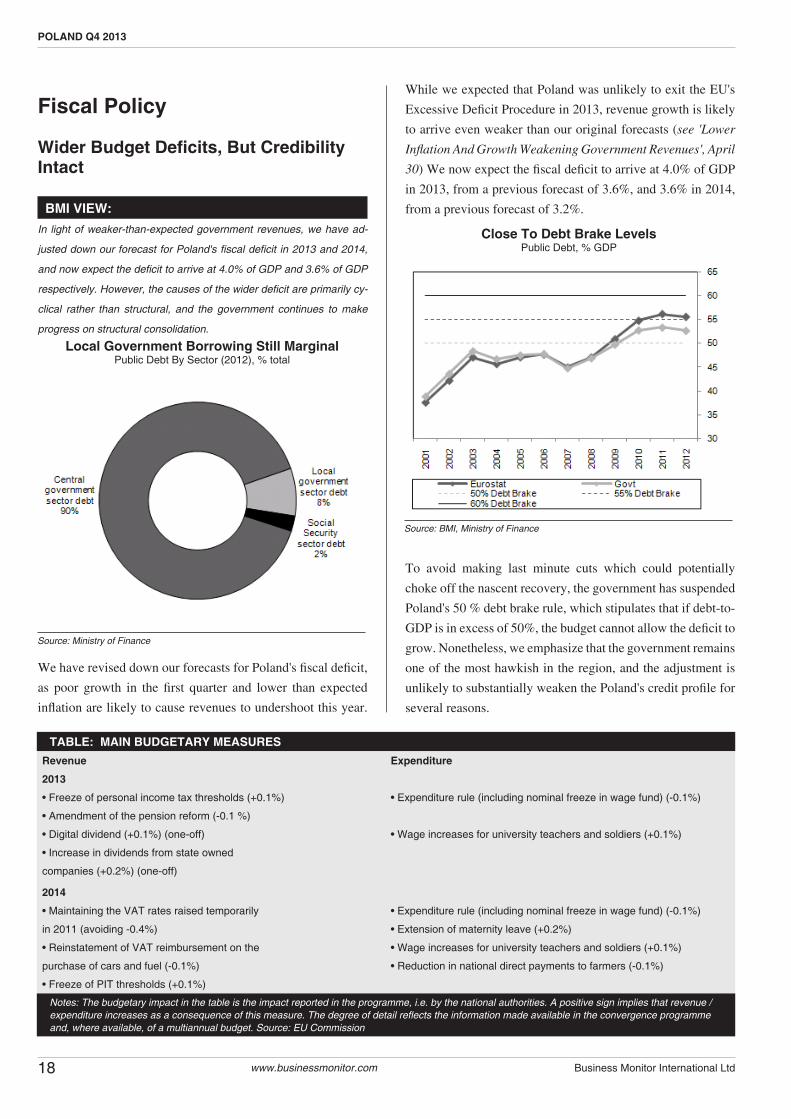

Wider Budget Deficits, But Credibility Intact

BMI VIEW: In light of weaker-than-expected government revenues, we have ad-

justed down our forecast for Poland's fiscal deficit in 2013 and 2014,

and now expect the deficit to arrive at 4.0% of GDP and 3.6% of GDP

respectively. However, the causes of the wider deficit are primarily cy-

clical rather than structural, and the government continues to make

progress on structural consolidation.

We have revised down our forecasts for Poland's fiscal deficit,

as poor growth in the first quarter and lower than expected

inflation are likely to cause revenues to undershoot this year.

While we expected that Poland was unlikely to exit the EU's

Excessive Deficit Procedure in 2013, revenue growth is likely

to arrive even weaker than our original forecasts (see 'Lower

Inflation And Growth Weakening Government Revenues', April

30) We now expect the fiscal deficit to arrive at 4.0% of GDP

in 2013, from a previous forecast of 3.6%, and 3.6% in 2014,

from a previous forecast of 3.2%.

To avoid making last minute cuts which could potentially

choke off the nascent recovery, the government has suspended

Poland's 50 % debt brake rule, which stipulates that if debt-to-

GDP is in excess of 50%, the budget cannot allow the deficit to

grow. Nonetheless, we emphasize that the government remains

one of the most hawkish in the region, and the adjustment is

unlikely to substantially weaken the Poland's credit profile for

several reasons.

18 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

Local Government Borrowing Still MarginalPublic Debt By Sector (2012), % total

Source: Ministry of Finance

Close To Debt Brake LevelsPublic Debt, % GDP

Source: BMI, Ministry of Finance

TABLE: MAIN BUDGETARY MEASURESRevenue Expenditure

2013

• Freeze of personal income tax thresholds (+0.1%) • Expenditure rule (including nominal freeze in wage fund) (-0.1%)

• Amendment of the pension reform (-0.1 %)

• Digital dividend (+0.1%) (one-off) • Wage increases for university teachers and soldiers (+0.1%)

• Increase in dividends from state owned

companies (+0.2%) (one-off)

2014

• Maintaining the VAT rates raised temporarily • Expenditure rule (including nominal freeze in wage fund) (-0.1%)

in 2011 (avoiding -0.4%) • Extension of maternity leave (+0.2%)

• Reinstatement of VAT reimbursement on the • Wage increases for university teachers and soldiers (+0.1%)

purchase of cars and fuel (-0.1%) • Reduction in national direct payments to farmers (-0.1%)

• Freeze of PIT thresholds (+0.1%)

Notes: The budgetary impact in the table is the impact reported in the programme, i.e. by the national authorities. A positive sign implies that revenue / expenditure increases as a consequence of this measure. The degree of detail reflects the information made available in the convergence programme and, where available, of a multiannual budget. Source: EU Commission

First, the causes of the wider deficit are primarily cyclical rather

than structural. Indeed, the government continues to make

progress on structural consolidation, which official forecasts

expect to arrive at 2.5% of GDP in 2014, from 5.5% in 2011.

While Poland's finance ministry described the move to suspend

the debt law as ‘strong stimulus’, the move is only ‘stimulus'

in so far as the government will not be pressing ahead with

further cuts to adapt to smaller budget revenues, rather than a

full-scale stimulus package. Second, Poland's fiscal conservatism

is enshrined in the 55% debt/GDP debt brake and 60% debt/

GDP debt brake rules, both of which currently remain in place.

While the government could theoretically lift the 55% debt

brake rule (although we think this outcome is highly unlikely),

the 60% rule is enshrined in Chapter X, Article 216 of Poland's

constitution. Altering the constitution would require at least a

two thirds majority in Poland's lower house.

Public debt levels will continue to rise in Poland, bringing them

close to the second 55% debt brake level which would bar the

next budget from increasing the ratio of central government debt-

to-GDP. Our current forecasts (which are based on public debt

levels calculated using the EU ESA-95 methodology), forecast

public debt to rise to 57.7% of GDP in 2013 – although this would

not contravene the 55% debt law as the Polish government uses

a different methodology which calculates public debt-to-GDP

around three percentage points lower than the EU methodology.

Risks To OutlookWhile we expect government borrowing costs to rise over the

coming quarters, this is primarily due to our expectations for

investors to reallocate capital out of emerging market debt as

US yields begin to rise, rather than an idiosyncratic repricing

of Poland's sovereign risk profile. Overall, government borrow-

ing costs will remain among the lowest in Emerging Europe,

restrained by the country's strong reputation for conservative

fiscal management, and a relatively liquid secondary market

for government bonds.

Monetary Policy

Fiscal Stimulus To Usurp Monetary Easing

BMI VIEW: Despite consumer prices heading close to deflationary territory, we do

not expect the National Bank of Poland to make any more rate cuts this

year, as we believe doing so could further weaken bank profitability

by lowering net interest margins, acting as a disincentive to lending

and creating tighter lending conditions in practice. The recent round of

monetary easing has yet to yield any tangible increases in aggregate

demand, and the announcement that the government is planning to

increase spending suggests that fiscal stimulus is about to overtake

monetary easing as the authorities preferred tool.

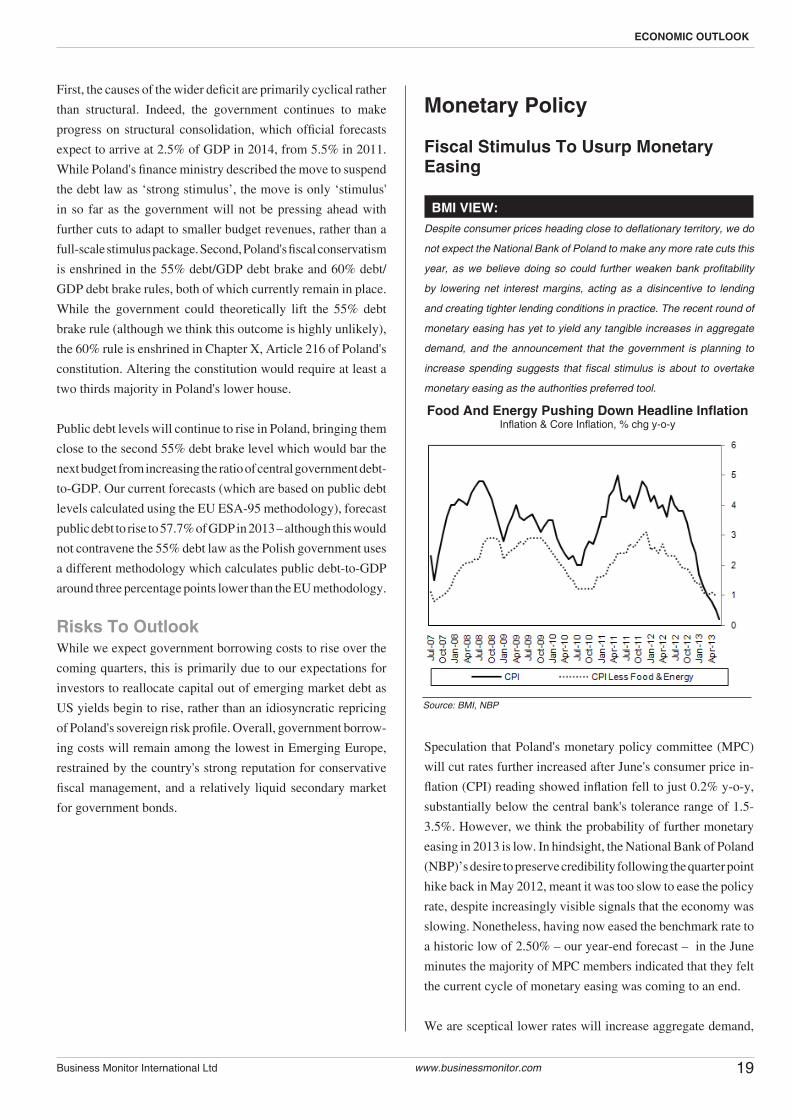

Speculation that Poland's monetary policy committee (MPC)

will cut rates further increased after June's consumer price in-

flation (CPI) reading showed inflation fell to just 0.2% y-o-y,

substantially below the central bank's tolerance range of 1.5-

3.5%. However, we think the probability of further monetary

easing in 2013 is low. In hindsight, the National Bank of Poland

(NBP)’s desire to preserve credibility following the quarter point

hike back in May 2012, meant it was too slow to ease the policy

rate, despite increasingly visible signals that the economy was

slowing. Nonetheless, having now eased the benchmark rate to

a historic low of 2.50% – our year-end forecast – in the June

minutes the majority of MPC members indicated that they felt

the current cycle of monetary easing was coming to an end.

We are sceptical lower rates will increase aggregate demand,

19Business Monitor International Ltd www.businessmonitor.com

ECONOMIC OUTLOOK

Food And Energy Pushing Down Headline InflationInflation & Core Inflation, % chg y-o-y

Source: BMI, NBP

and could actually weaken the banking sector by driving lower

net interest margins (see 'Regional Equity Strategy', July 16).

Furthermore, the recent announcement that the government

is planning to suspend the legal limits on public debt, paving

the way for fiscal stimulus, implies that the authorities have

acknowledged the limitations of monetary policy in boosting

growth. Polish forward rate agreements concur with our assess-

ment, with both the 3x6 and 6x9 contracts implying no further

rate cuts by year-end.

The NBP's senior loan officer survey shows that domestic banks

expect corporate lending standards to tighten over the next quar-

ter, due to both the unfavourable forecasts of macroeconomic

conditions and the cuts in NBP rates. The rate cutting cycle has

been creating pressure on bank net interest margins, acting as a

disincentive to lending, and reducing profitability in an already

challenging economic climate. Polish banks are primarily deposit

funded, indicating a reduced reliance on wholesale funding and

have thus not benefitted particularly from lower interbank rates.

The majority of deposits in the banking sector are fixed term,

meaning that banks are not able to immediately reduce interest

rates on most deposits to offset lower interest rates on loans.

As a result, net interest margins, particularly on floating-rate

loans benchmarked to WIBOR (Poland's interbank lending rate),

have been weakened, which has made banks more reluctant to

lend, thus actually driving a tightening in lending standards to

the corporate sector. As WIBOR is strongly correlated with

the NBP's benchmark rate, we think this will make the MPC

disinclined to cut the benchmark rate any further.

Senior Loan Officer Survey: "If your bank's lending policies

(credit standards or terms) applied to corporate loans and credit

lines have changed over the last three months, please indicate

how the following factors have influenced the changes: NBP's

monetary policy decisions"

Only two out of the ten MPC members voted for a 50 basis point

cut at the last meeting, with even Anna Zielinska-Glebocka,

one of the most dovish MPC members, suggesting that she saw

the optimum rate at somewhere between 2.25-2.50%.As we do

not believe that more rate cuts will stimulate lending, the main

argument for further monetary easing appears to be that doing

so will weaken the currency, providing a boost for domestic

exporters. However, the zloty has already fallen 6.0% against

the euro since December 2012, while the broad REER (BIS

calculation) has weakened by 3.0%. While further weakness

could provide a greater boost to exporters, it will also suppress

domestic demand – already at its weakest on record.

Finance Minister Jan Vincent-Rostowski recently suggested that

the central bank should keep cutting rates, which is logical given

that further cuts could help to minimise government borrowing

costs as it embarks on fiscal stimulus in September, by keeping

yields down on local debt. However, Poland's benchmark rate

is among the lowest in CEE, and we emphasise that further cuts

could trigger capital outflows from non-resident government

bond owners, which could in fact cause government borrow-

ing costs to rise. In summary, we think that potential economic

benefits from further rate cuts are limited, and expect that fiscal

stimulus will overtake monetary policy as a preferred policy

tool to support domestic demand over the remainder of the year.

20 Business Monitor International Ltdwww.businessmonitor.com

POLAND Q4 2013

Rate Cuts Weakening Corporate LendingSenior Loan Officer Survey

Notes: The difference between the percentage of responses “Contributed considerably to the easing of lending policies” and “Contributed somewhat to the easing of lending policies” and the percentage of responses “Contributed considerably to the tightening of lending policies” and “Contributed somewhat to the tightening of lending policies”. A negative index indicates a given factor’s greater contribution to the tightening than to the easing of lending policies. Source: BMI, NBP Senior Loan Officer Survey

Zloty Already WeakenedEURPLN Cross-rate & Broad REER (LHS, inverted scale)

Source: BMI, Bloomberg, BIS

Currency Forecast

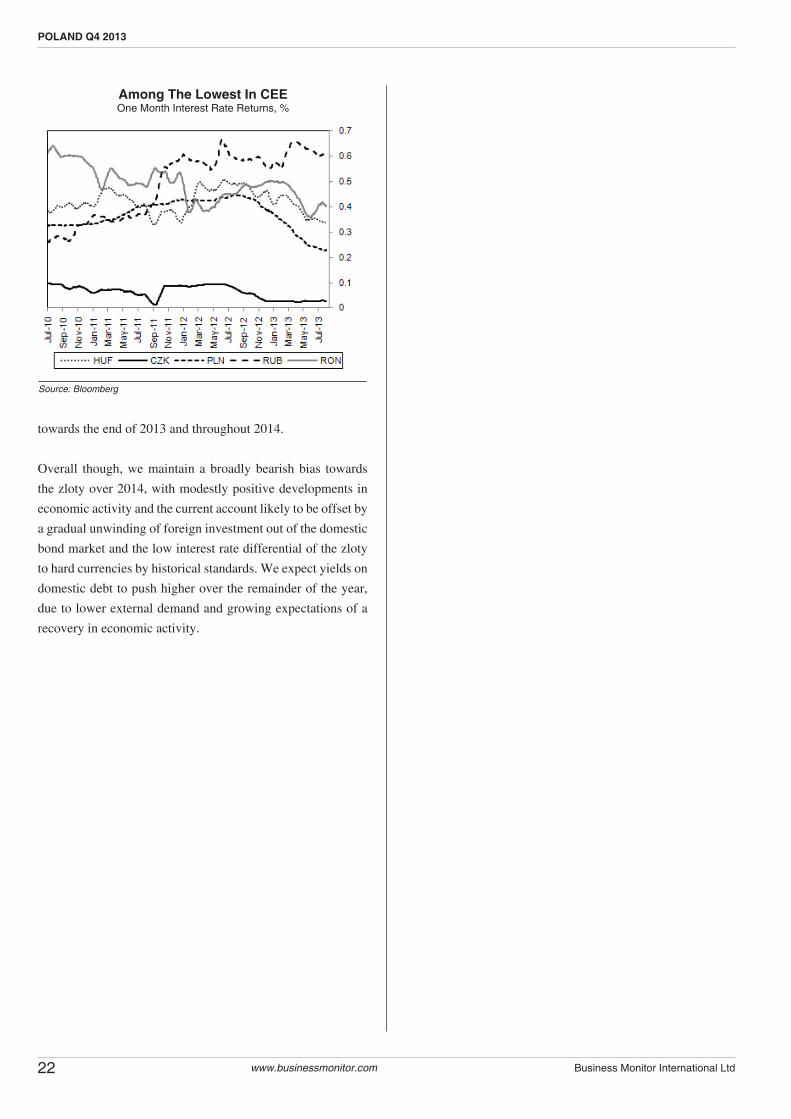

PLN: Maintaining Medium-Term Bearish BiasShort-Term Outlook: With no further rate cuts anticipated in

our view, we expect the zloty to range trade around the PLN4.2

0-4.3 0/EUR level over the coming months. Demand for zloty-

denominated debt is weak and is likely to remain so, as rising

US treasury yields keep investors wary of emerging market debt,

which has underperformed so far this year. Nonetheless, demand

for the zloty will remain robust enough to keep it anchored around

current levels. Economic data over the next few months should

point towards a steady, albeit somewhat protracted recovery,

primarily driven by net exports, implying buying pressure on

the zloty should stay relatively stable.