policies at the national and regional level – south asia: beverages and spices in sri lanka anura...

TRANSCRIPT

Policies at the National and Regional Level – South Asia: Beverages and Spices

in Sri Lanka

Anura Herath

Sri LankaIDRC/UNCTAD Workshop on Standards and

Trade 16-17 May 2002, Geneva

Status Summary: Spice & beverage Sector

Sector

National EconomyGDP - 0.57%

Tot. FE (5600 Rm):1.75%Agric. FE - 8.5%

ProductionLand - 53,000 ha (9% of total)

Farms: 250,000Av Size: 1/4 ha

About 20%-50% HH income

EnvironmentBiodiversity

Land degradation

Socio-Economy/TechnologyLabour intensive

High women participationAll local inputs

Traditional Areas of ProductionTraditional Areas of Production

Progress of the Sector Progress of the Sector [1980-2000][1980-2000]

Sector has progressedThere is a tremendous potential in the world

market

Local Scene

Area (ha): 30,240 - 53,600

Foreign Exchange (US $ mn): 6.4 - 69.7

Exports (mt):10,300 - 17,900

Global Scene

Imports (mt): 220,000 - 500,000

Growth Rate: 3-4%

Per capita spice consumption: 2.33 -

3.19

Markets for SL Spices & BeveragesMarkets for SL Spices & Beverages

• Cinnamon: USA – 10%; Mexico – 44%

• Cardamom: Singapore – 21%; UK - 5%, South Africa; Bangladesh

• Clove: India – 26%; Saudi Arabia – 15%; UK – 7%

• Pepper: UAS – 10%; UK – 11%; India – 25%

• Coffee : UK – 5%; Italy – 9%; Austria – 12%, Germany – 23%

• Cocoa: UK; Germany; Italy

Tax structure for EACTax structure for EAC

Country Coffee Cocoa Cinnamon Pepper Cardamom CloveJapan 0% 20% 0%; 20-35% 0% all 0%; 4.2% 0%; 4.2% 4.2%USA 0% all 0%; 1% 0% 0% 0% 0%EU 4%; 10-30% 6.7%; 12% 0%; 1.3% 0% 20% 10%Mexico 20% all 15% all 10% all 10% 20% 10%Russia 0%, 10% 0% all 0% all 0% all 0% all 0% allSouth Africa 0% all 0%; 20% 0% all 0% all 0% all 0% allBrazil 10% all 10%; 20% 10% all 10% all 10% all 10% allChina-MFN 40%; 60% 20%; 45% 35% all 45% all 6% 3%Australia 0% 0%; 5% 0% 0% 0% 0%Indonesia 30% all 10%; 20% 30% all 30% all 30% 5%Venezuela 10% all 10%; 20% 10%; 15% 10%; 15% 10% all 10% allSri Lanka 35% all 35% all 35% all 35% all 35% all 35% all

Increase in market accessIncrease in market access

Country% Export upto 80%

Pot.reduction rate

Weighted by % of export

Italy 2.3% 0.0% 0.0%Germany FR 2.6% 0.0% 0.0%Guatemala 2.6% 24.0% 0.6%Chile 2.7% 24.0% 0.6%Equador 2.9% 24.0% 0.7%Spain 3.9% 0.0% 0.0%Peru 6.4% 24.0% 1.5%Colombia 6.4% 24.0% 1.5%USA 10.7% 0.0% 0.0%Mexico 44.4% 24.0% 10.7%

Access Increase in % 16%

Cinnamon 1990 - 1999

Cardamom = 8% Clove = 22%

Pepper = 18% Coffee = 17%

Export Volume of Spices & BeveragesExport Volume of Spices & Beverages

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998

Exp

ort

Vol

um

e (m

t)

Total Spice Coffee & cocoa

Quality Requirements

CleanlinessSpecifications

Wholeinsects dead

Excretamammalian

Excretaother

Mold Insectinfested

Extraneousmatter

Bycount

Bymg./lb

Bymg./lb

% bywgt.

% bywgt.

% bywgt.

Cardamom 4 3 1.0 1.00 1.00 0.50

Cinnamon 2 1 2.0 1.00 1.00 0.50

Cloves 4 5 8.0 1.00 1.00 1.00

Mace 4 3 1.0 2.00 1.00 0.50

Nutmeg (broken) 4 5 1.0 SF(4) SF(4) 0.50

Nutmeg (whole) 4 0 0.0 SF(5) SF(5) 0.00

Black pepper 2 1 5.0 SF(6) SF(6) 1.00

White pepper 2 1 1.0 SF(7) SF(7) 0.50

Aflatoxin DDT etc. Radiation Solvent residues

For all 4 ppb 1- 0.5 ppm 10-6% 1 ppm

u

SF= 4,5,6,7: 1-5% insect or infected pieces

Percentage of Product Volume with High Moisture Percentage of Product Volume with High Moisture Level and Mould at the Exporter LevelLevel and Mould at the Exporter Level

0%

5%

10%

15%

20%

25%

30%

35%

40%

% o

f V

olum

e th

e E

xpor

ter

Lev

el

Wet 19% 12% 16% 9% 38% 15% 38%

Semi-dry 5% 6% 7% 5% 0% 1% 0%

with mould 1% 2% 1% 1% 2% 6% 2%

Cinnamon Pepper Coffee Nutmeg Clove Cocoa Cradamom

National level survey of 350 traders

Main reasons for low qualityMain reasons for low quality

• Improper harvesting

• Unfavourable drying systems. Nearly 70% of the producers use sun drying on home yard with no proper surface for drying. Roadside drying is common.

• Experience frequent rain during the harvesting period. About 69% of producers claimed the problem.

• Only 5% of the producers use a mechanical dryer.

• About 64% reported of poor storage.

Estimated Proportion of Products with Substandard Quality and the Reprocessing Cost to meet SPS

Requirements

Product >20% M >15% M % Mould Exp. Mt Reproce.mt

Cost $

Cinnam. 19% 5% 1% 9,130 2,313 433,676

Pepper 12% 6% 2% 3,611 717 134,414

Coffee 16% 7% 1% 1,550 378 70,784

Nutmeg 9% 5% 1% 752 108 20,162

Clove 38% 0% 2% 1,296 515 96,554

Cocoa 15% 1% 6% 127 28 5,256

Cardam. 38% 0% 2% 18 7 1,336

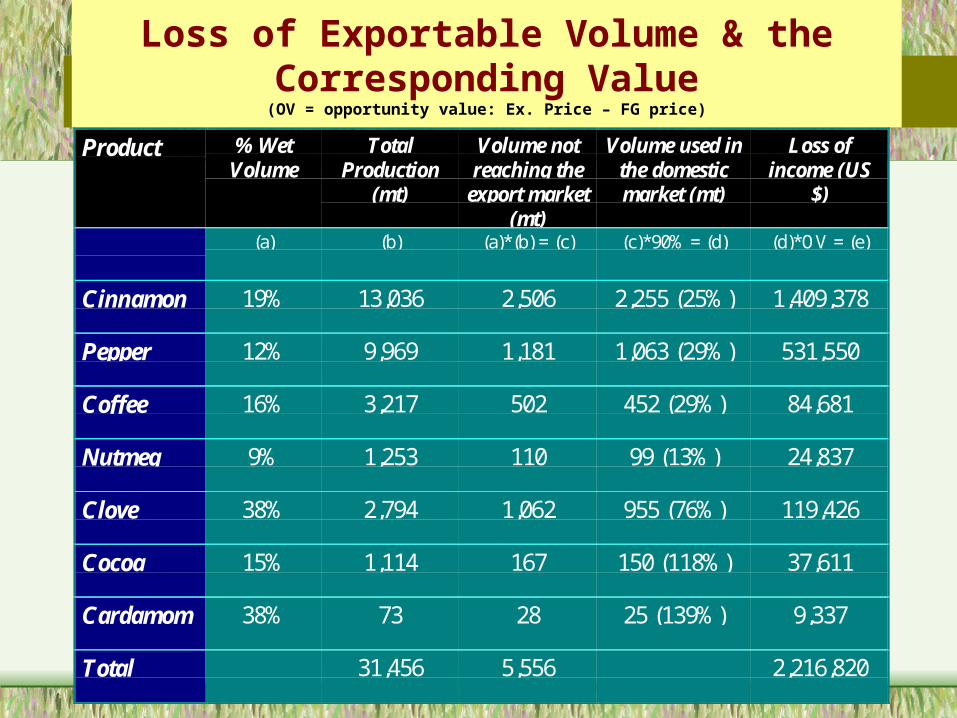

Loss of Exportable Volume & the Corresponding Value

(OV = opportunity value: Ex. Price – FG price)

Product % WetVolume

TotalProduction

(mt)

Volume notreaching the

export market(mt)

Volume used inthe domesticmarket (mt)

Loss ofincome (US

$)

(a) (b) (a)*(b) = (c) (c)*90% = (d) (d)*OV = (e)

Cinnamon 19% 13,036 2,506 2,255 (25%) 1,409,378

Pepper 12% 9,969 1,181 1,063 (29%) 531,550

Coffee 16% 3,217 502 452 (29%) 84,681

Nutmeg 9% 1,253 110 99 (13%) 24,837

Clove 38% 2,794 1,062 955 (76%) 119,426

Cocoa 15% 1,114 167 150 (118%) 37,611

Cardamom 38% 73 28 25 (139%) 9,337

Total 31,456 5,556 2,216,820

Loss of EmploymentProduct Estimated

reprocessedquantity

before export(mt)

Labour forreprocessing(# persons /

year)

Volume notreaching the

exportmarket (mt)

Total labourloss

(persons/year)

Net labourloss

(persons/year)

Cinnamon 2,313 368 2,506 1,917 1,549

Pepper 717 114 1,181 456 342

Coffee 378 60 502 262 202

Nutmeg 108 17 110 48 30

Clove 515 82 1,062 314 232

Cocoa 28 4 167 57 52

Carda. 7 1 28 7 6

Total 4,066 647 5,556 3,061 2,415

Loss of FE due to non Loss of FE due to non compliancecompliance• Loss of prices: Average FOB price is 41% less than the average world

market price for coffee, 34% for cocoa, 20% for pepper, 69% for nutmeg and 30% for cardamom. This difference, according to the exporters, is mainly due to non-compliance

• Volume loss at the retail trade level: If the quality is in line with SPS requirements, this volume could have been exported at about US $ 2.2 million per year

• Value loss at the exporter level due to lack of quality: There is a reprocessing cost of about 0.7 million US $ per year. This will reduce the competitiveness.

• In total the estimated value of foreign exchange loss due to non-compliance is US $ 2.9million / year: about 5% of the total FE earnings from spices & beverage crops

Overall Impact – What Policies?Overall Impact – What Policies?

• Overall impact on country’s GNP

• Negative impact on poverty alleviation

• Permanent loss of markets

Policy Interventions

Basis for Policy Directions Basis for Policy Directions (understanding the sector)(understanding the sector)

• Small Size of the cultivation– Heterogeneity– Low capital and low credit – low investment– Subsistence nature – poverty issue– Information gap – basically government

sources: GOSL cannot reach the base for lack of funds

Holding size of cardamom: Sri LankaHolding size of cardamom: Sri Lanka

Distribution of Holding Size and Cumulative Distribution: Cardamom

0

2

4

6

8

10

12

14

0.08 0.2 0.4 0.6 0.8 1 1.2 2 >2

Holding Size (ha)

Fre

qu

ency

0%

20%

40%

60%

80%

100%

120%

Cu

mu

lati

ve %

Frequency Cumulative %

yHolding size of Cinnamon: Sri LankayHolding size of Cinnamon: Sri Lanka

Distribution of Holding Size and Cumulative Distribution: Cinnamon

0

5

10

15

20

25

30

35

0.08 0.2 0.4 0.6 0.8 1 1.2 2 More

Holding Size (ha)

Fre

qu

en

cy

0%

20%

40%

60%

80%

100%

120%

Cu

mu

lati

ve

%

Frequency Cumulative %

Holding size of Pepper: Sri LankaHolding size of Pepper: Sri Lanka

Distribution of Holding Size and Cumulative Distribution: Pepper

0

10

20

30

40

50

60

70

80

0.08 0.2 0.4 0.6 0.8 1 1.2 2 More

Holding Size (ha)

Fre

qu

en

cy

0%

20%

40%

60%

80%

100%

120%

Cu

mu

lati

ve

%

Frequency Cumulative %

0

10

20

30

40

50

60

70

>.5 ac 0.5-1 ac 1-2 ac 2-4 ac >4 ac

Fre

qu

ency

0%

20%

40%

60%

80%

100%

120%

% c

um

ula

tive

Frequency %

Holding size of Coffee: Sri LankaHolding size of Coffee: Sri Lanka

Basis for Policy Directions Basis for Policy Directions (understanding the sector)(understanding the sector)

• Small Size of the cultivation • % marketed in the domestic market

– Considerable• hence total production meeting the cost of

compliance may not be cost effective for the small scale producers

– The price gab between Grade 1 & 2 is inadequate for high investment

• Pepper – 7-10%; Cinnamon – 10-15%; Coffee – 5-8%

Domestically Traded Volumes & Domestically Traded Volumes & share of that out of exportsshare of that out of exports

Product Total Production

(mt)

Volume not reaching the

export market (mt)

Volume used in the domestic market (mt)

Cinnamon 13,036 2,506 2,255 (25%)

Pepper 9,969 1,181 1,063 (29%)

Coffee 3,217 502 452 (29%)

Nutmeg 1,253 110 99 (13%)

Clove 2,794 1,062 955 (76%)

Cocoa 1,114 167 150 (118%)

Cardamom 73 28 25 (139%)

Basis for Policy Directions Basis for Policy Directions (understanding the sector)(understanding the sector)

• Small Size of the cultivation • % marketed in the domestic market • Awareness

– There is a considerable gap in time & precise information: • producer – exporter• Exporter – consumer

– Gap between the national inquiry points & producers– Government information sources are less efficient due to lack of

resources

Producers’ Knowledge on Producers’ Knowledge on processingprocessing

Producers' Knowledge on the Recomemded Processing Methods{data from a survey of 1075 producers of spices and beverage crops}

Lack of know ledge81%

Only partial know ledge8%

Know s the process11%

Percentage of Producers having Percentage of Producers having knowledge on Processingknowledge on Processing

0%

20%

40%

60%

80%

100%

Lack ofknowledge

Only partialknowledge

Knows theprocess

Cardamom

Cinnamon

Citronella

Cocoa

Coffee

Pepper

Percentage of Trading Partners at Different Points of the Trade Channel who have Reported the Inferior

Quality of Spices

0%

10%

20%

30%

40%

50%

60%

70%

% t

rade

rs in

the

sam

ple

Exporter Retail buyer Village Collector Wholesale buyer

Information Gap

Well planned training Well planned training programme is neededprogramme is needed

• There are about 70,000 traders involved in the industry

• The total cost then would be in the range of US $ 1.954 million

• The annual budget allocation is US $ 24,400, which is only 3% of the requirement

Basis for Policy Directions Basis for Policy Directions (understanding the sector)(understanding the sector)

• Small Size of the cultivation • % marketed in the domestic market • Awareness • Cost of Production

– Less competitive & thus cost increase is not attractive

Cost of production becomes high - Cost of production becomes high - 20022002

Product Cost of Production (US $/kg)

Cost of processing at

farm-gate (US $/kg)

Total cost of production (US $/kg)

Farm-gate price (US

$/kg)

Pepper 0.76 0.19 0.95 1.95

Coffee 0.34 0.23 0.56 0.54

Cocoa 0.33 0.25 0.58 0.70

Cinnamon 2.00 0.19 2.19 4.70

Cardamom 1.85 0.38 2.23 8.88

Basis for Policy Directions Basis for Policy Directions (understanding the sector)(understanding the sector)

• Small Size of the cultivation • % marketed in the domestic market • Awareness • Cost of Production • Technology

– Not in line with giving high quality

SummarySummary

• The sector is important for FE earning and poverty alleviation

• Improved market access is only marginal if SPS requirements are not met, so emphasis on quality is essential

• There is a notable cost in complying with standards

• Quality is affected by weather, technology and knowledge factors

• The policy interventions should take the basic features of the sector.

Policy Direction for Sri Policy Direction for Sri LankaLanka

• Increase awareness in lowering cost of production and increasing quality.

• Encourage central processing and out-grower systems

• Emphasise on the possibility of exchanging improved genetic material and plant varieties which help in increasing competitiveness

• Increase facilities for national inquiry points

• Improve the capacity to detect and eliminate contaminants, to process spices to acceptable standards, and proper packaging etc.

• Encourage capacity building on HRD

• Develop strategies, may be collectively with other DC, to take Technical Assistance under SPS measures through a close consultative process with all the stakeholders

• Provide state assistance to central collection and processing points to maintain the homogeneity of quality.

• Encourage regional co-operation through producers’ meetings