policies & procedures updated:...

TRANSCRIPT

POLICIES & PROCEDURES

UPDATED: 10/13/15

Geneva Financial, LLC Mission Statement:

Offering the greatest home financing options, at the highest compensation, and the lowest price, so we are always doing what is best for the client.

Building the Nation’s Best Mortgage Company with our employees, one mortgage at a time.

Our Vision: Geneva Financial, LLC is unlike our big banking platform competitors; nor do we

wish to ever become them. Our clients are our employees, and we are accommodating almost to a fault. We are growing the Company with our

employees; not on top of them. Not a fan of the corporate culture. When is the last time you spoke with the owner of your company? When is the last time anyone listened to your concerns or input. You can call me anytime. We have an open

door policy at Geneva Financial, LLC.

Together we can grow this Company as a community, or as a family; and forever avoid that Corporate Culture that brought many to Geneva Financial, LLC in the

first place. I look forward to doing this together, as a team.

Our employees are so important to us, that within the next 5 years we hope to be “Employee Owned.” Yes, we will be selling a portion of the Company stock back to

the employees that helped grow our Company and make it what it is. We never wish to sell out to an investor or competitor as I have never found one that cares more for the employees than it does profit. Profits are important, but not at the

expense of everyone else. We can all experience tremendous success together. That’s how we got here in the first place. Opportunities are coming…

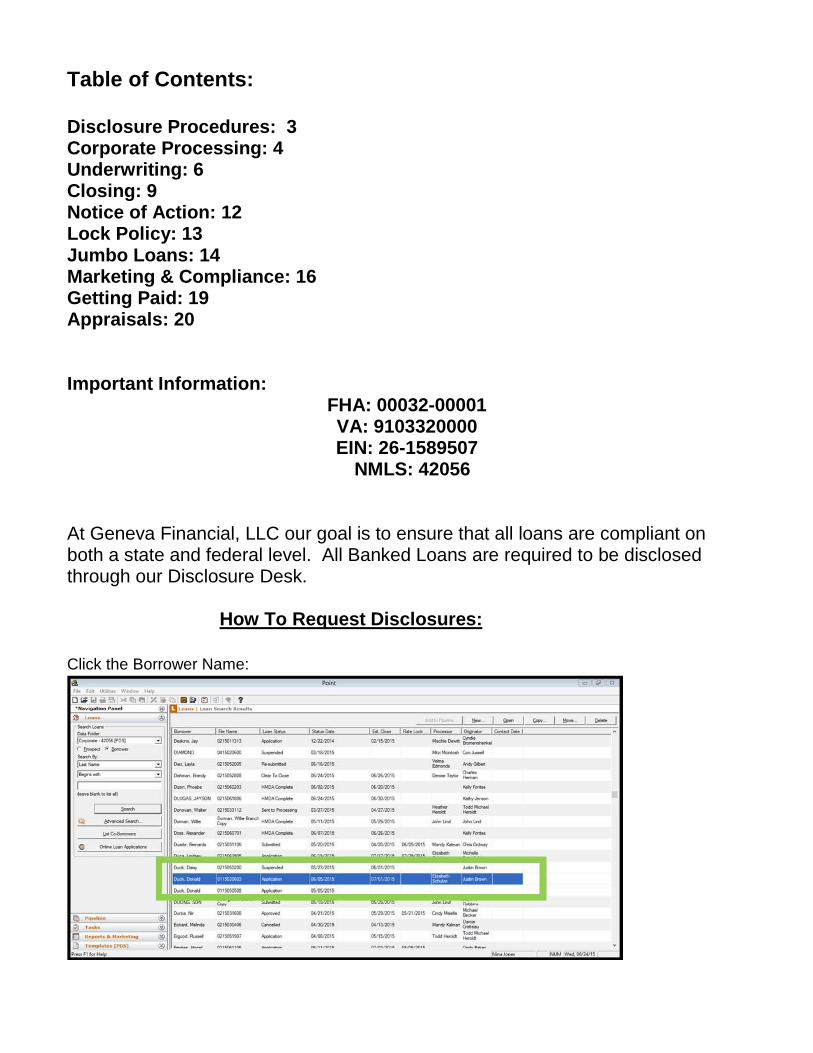

Table of Contents: Disclosure Procedures: 3 Corporate Processing: 4 Underwriting: 6 Closing: 9 Notice of Action: 12 Lock Policy: 13 Jumbo Loans: 14 Marketing & Compliance: 16 Getting Paid: 19 Appraisals: 20 Important Information:

FHA: 00032-00001 VA: 9103320000 EIN: 26-1589507

NMLS: 42056 At Geneva Financial, LLC our goal is to ensure that all loans are compliant on both a state and federal level. All Banked Loans are required to be disclosed through our Disclosure Desk.

How To Request Disclosures:

Click the Borrower Name:

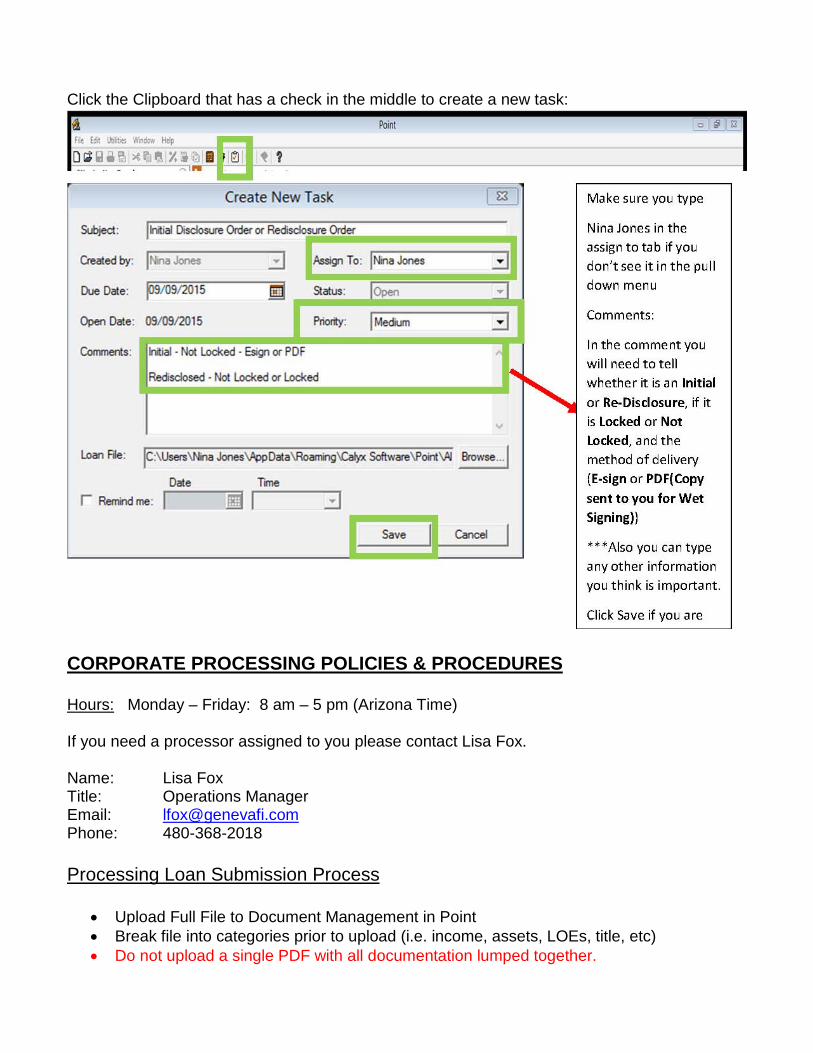

Click the Clipboard that has a check in the middle to create a new task:

CORPORATE PROCESSING POLICIES & PROCEDURES Hours: Monday – Friday: 8 am – 5 pm (Arizona Time) If you need a processor assigned to you please contact Lisa Fox. Name: Lisa Fox Title: Operations Manager Email: [email protected] Phone: 480-368-2018 Processing Loan Submission Process

• Upload Full File to Document Management in Point • Break file into categories prior to upload (i.e. income, assets, LOEs, title, etc) • Do not upload a single PDF with all documentation lumped together.

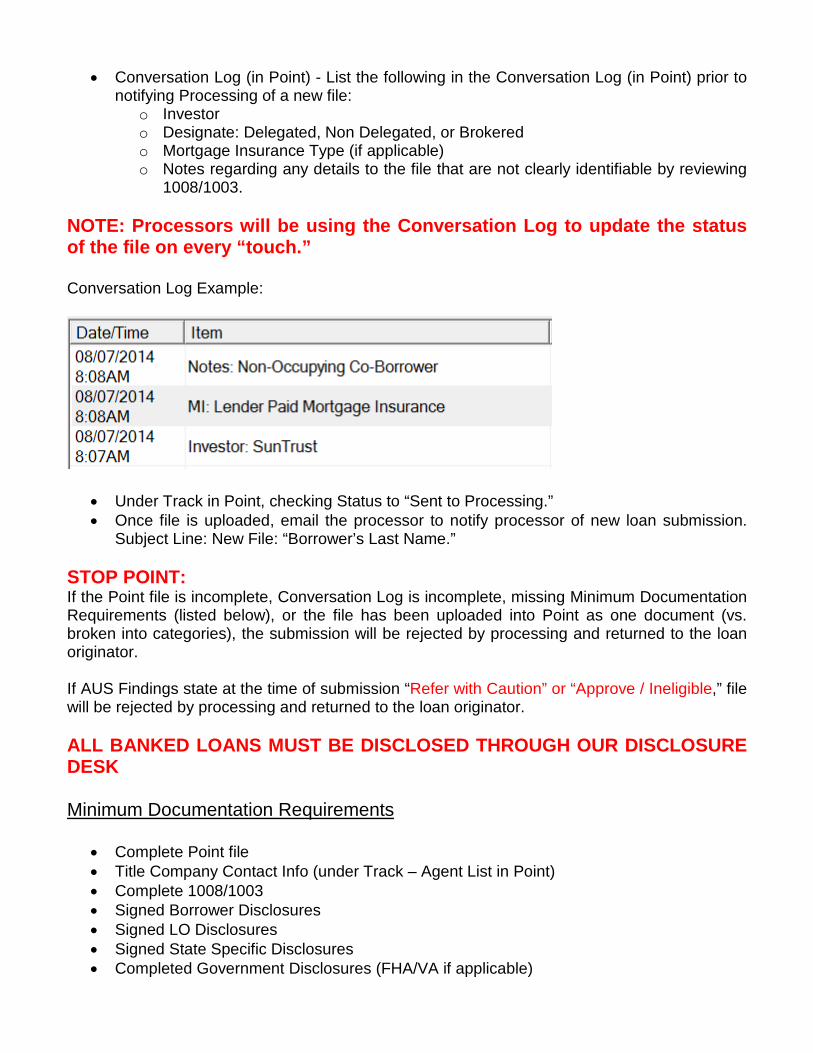

• Conversation Log (in Point) - List the following in the Conversation Log (in Point) prior to notifying Processing of a new file:

o Investor o Designate: Delegated, Non Delegated, or Brokered o Mortgage Insurance Type (if applicable) o Notes regarding any details to the file that are not clearly identifiable by reviewing

1008/1003. NOTE: Processors will be using the Conversation Log to update the status of the file on every “touch.” Conversation Log Example:

• Under Track in Point, checking Status to “Sent to Processing.” • Once file is uploaded, email the processor to notify processor of new loan submission.

Subject Line: New File: “Borrower’s Last Name.” STOP POINT: If the Point file is incomplete, Conversation Log is incomplete, missing Minimum Documentation Requirements (listed below), or the file has been uploaded into Point as one document (vs. broken into categories), the submission will be rejected by processing and returned to the loan originator. If AUS Findings state at the time of submission “Refer with Caution” or “Approve / Ineligible,” file will be rejected by processing and returned to the loan originator. ALL BANKED LOANS MUST BE DISCLOSED THROUGH OUR DISCLOSURE DESK Minimum Documentation Requirements

• Complete Point file • Title Company Contact Info (under Track – Agent List in Point) • Complete 1008/1003 • Signed Borrower Disclosures • Signed LO Disclosures • Signed State Specific Disclosures • Completed Government Disclosures (FHA/VA if applicable)

• AML / Disparate Impact / OFAC Disclosures • QM Findings • AUS Findings (must be Approved / Eligible) • Income Documentation • W2s • Pay Stubs • Tax Returns (if requested on findings, self-employed, or 2106 expenses) • Asset Documentation (if applicable) • Proof of Non Payroll Deposits • Detailed explanation for anything unusual regarding transaction. This information should

be listed in the Conversation Log in Point. • Billing Information (if processor is to order appraisal)

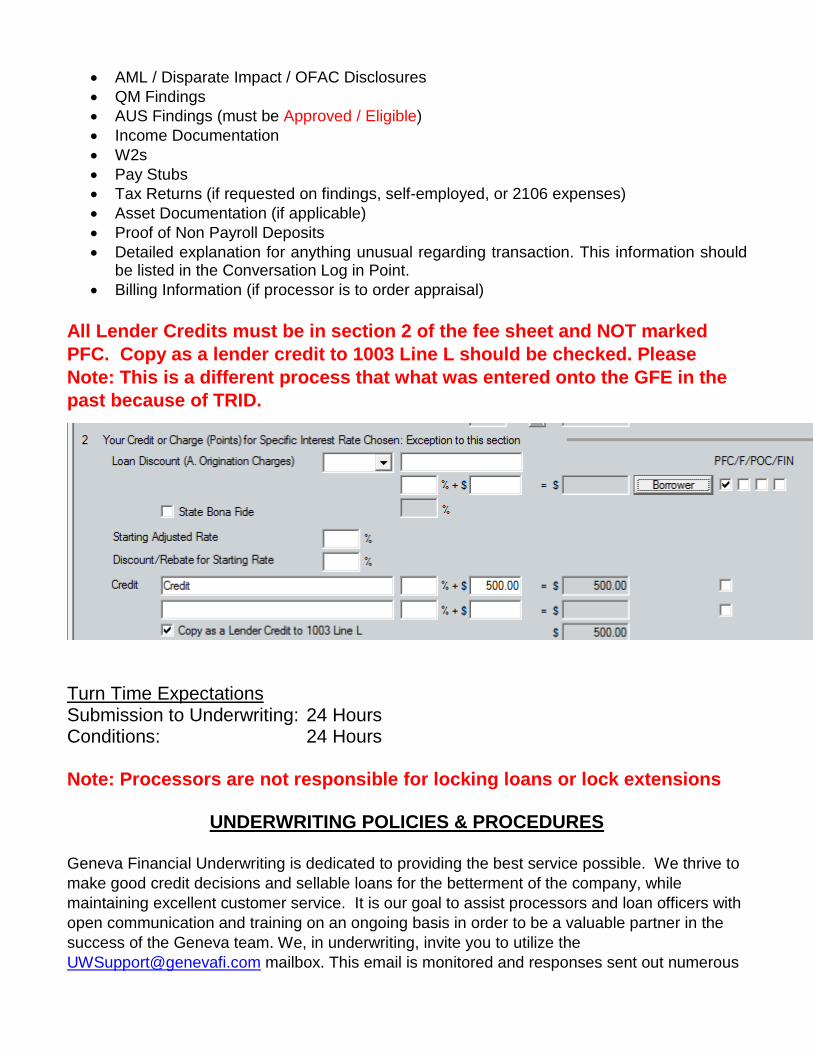

All Lender Credits must be in section 2 of the fee sheet and NOT marked PFC. Copy as a lender credit to 1003 Line L should be checked. Please Note: This is a different process that what was entered onto the GFE in the past because of TRID.

Turn Time Expectations Submission to Underwriting: 24 Hours Conditions: 24 Hours Note: Processors are not responsible for locking loans or lock extensions

UNDERWRITING POLICIES & PROCEDURES

Geneva Financial Underwriting is dedicated to providing the best service possible. We thrive to make good credit decisions and sellable loans for the betterment of the company, while maintaining excellent customer service. It is our goal to assist processors and loan officers with open communication and training on an ongoing basis in order to be a valuable partner in the success of the Geneva team. We, in underwriting, invite you to utilize the [email protected] mailbox. This email is monitored and responses sent out numerous

times during the day by the underwriting department. Please send all scenario or guideline questions to this address and not the submission email address or directly to underwriters.

Name: Whitni Baker Title: Underwriting Manager – DE/SAR Email: [email protected] Phone: 858-314-8431 Bio: I have been in the mortgage industry for 28 years in many different capacities. I

have been in underwriting for 20 years. I have a training background that has allowed me to assist many underwriters obtain their FHA and VA certifications. I am the mother of three women and I have four grandkids. I am an avid reader, football fan and a constant visitor to the zoos.

Name: Lorraine Giron Title: Underwriter Email: [email protected] Phone: 623-466-2220 Bio: I have been on the Mortgage Banking side of the business since 2007 working for

major banking institutions such as USAA FSB (San Antonio, TX and Phoenix, AZ), Chase and Wells Fargo. Prior to Mortgage Banking, I worked on the appraisal side of the Industry for 6 years as an account manager and office manager. The majority of my career has been specializing in VA loans and it's something that I enjoy. My father was a Vietnam Veteran; a proud Marine. We grew up with an understanding of the military culture and what it means to serve so veterans hold a special place.

Name: Cindy Hunter Title: Underwriter Email: [email protected] Phone: 702-462-8371 Bio: I have been in the business since 1996 and underwriting since 2002. I worked for

Chase, Wells Fargo and Ryland Homes. I specialize in all types of loans- VA, FHA, USDA, Conventional and DPA loan programs. I am looking forward to Geneva getting our USDA approval so that we can shine as a company on Rural Housing front. In my spare time I like to go Camping, Fishing and one day plan on traveling to Italy to find my roots.

Hours Monday – Friday: 8 am – 5 pm (Arizona Time) Underwriting Loan Submission Process

• Upload Full File to Document Management in Point

• Break file into appropriate Package Type, Categories and Type prior to upload (i.e. income, assets, LOEs, title, etc.):

o Package Type is “Submission” at initial submission and “Conditions” when submitting conditions (use the drop down menu).

o Category is based on the document type (use the drop down menu): Borrower = ID, social security verification, OFAC, Patriot Act Assets = Bank statements, large deposit documentation, explanation

letters, gift documentation, etc. Income = Paystubs, W-2’s tax returns, transcripts, VOE’s, explanation

letters, etc. Credit = Credit report, supporting documentation, explanation letters, etc. Disclosure = Signed 1003 and all disclosures Credit Underwriting Approval = DO findings, LP findings Property = Purchase contract, addendums, counter offer, flood cert,

insurance Title = Prelim, HUD, Plat, Taxes, CPL, wire instructions, etc. Appraisal Valuation = Appraisal, SSR’s, etc. Closing = All closing documents, invoices, etc. (This should be under

Package Type “Closing”, not Submission or Conditions) o Type = Description of the document (i.e., paystub for B1, Wells Fargo June and

July bank statements, etc.). You can type the description or use the drop down menu.

• Conversation Log (in Point): List the following in the Conversation Log (in Point) prior to

notifying Underwriting of a new file: o Mortgage Insurance Type (if applicable) o Notes regarding any details to the file that are not clearly identifiable by reviewing

1008/1003.

• Under Track in Point, checking Status to “Submitted.”

• Move the file to the Underwriting Folder

• Once file is uploaded, email [email protected] to notify underwriting of new loan submission. Subject Line: New File – “Borrower’s Last Name and Loan Number.”

• Once the loan is underwritten, you will receive an underwriting determination, the status of the loan will be changed to either Approved or Suspended and moved back into the Processing folder in Point.

• Once final conditions have been uploaded into Point, break file into appropriate Package

Type, Categories and Type prior to upload (i.e. income, assets, LOEs, title, etc) per instructions above (Reminder, conditions are to be in the Conditions package type). Only submit back to underwriting once ALL conditions have been received and uploaded.

• Under Track in Point, checking Status to “Re-Submitted.”

• Move the file to the Underwriting Folder

• Once file is uploaded, email [email protected] to notify underwriting of loan submission for final review. Subject Line: Re-Submitted File – “Borrower’s Last Name and Loan Number.”

• Once the loan is underwritten, you will receive an underwriting determination, the status of the loan will be changed to either Clear to Close or Approved (if not all conditions cleared) or Suspended and moved back into the Processing folder in Point.

STOP POINT: If the Point file is incomplete, Conversation Log is incomplete, missing Minimum Documentation Requirements (listed below), or the file has been uploaded into Point as one document (vs. broken into Package Type, Categories), the submission will be rejected by underwriting and returned to processing. If AUS Findings state at time of submission “Refer with Caution” or “Approve / Ineligible,” file will be rejected by underwriting and returned to processing. Minimum Documentation Requirements

• Complete Point file • Complete 1008/1003 • AUS Findings (must be Approved / Eligible) • Income Documentation

o Income Calculation Worksheet o W2s o Pay Stubs o Tax Returns (if requested on findings, self-employed, or 2106 expenses)

• Asset Documentation (if applicable) • Proof of Non Payroll Deposits • Detailed explanation for anything unusual regarding transaction. This information should

be listed in the Conversation Log in Point. Note: All Submissions, Conditions, and CTC Conditions must be uploaded into Point. Do not email submission or conditions. Required for CTC: Final Lock Confirmation Once the file has been CTC than the underwriter will move the file back to the Processing Folder so you are able to submit to Closing.

CLOSING DEPARTMENT POLICIES & PROCEDURES Closing Department Contact Name: Mischle DeWitt (Closing Manager) Email: [email protected]

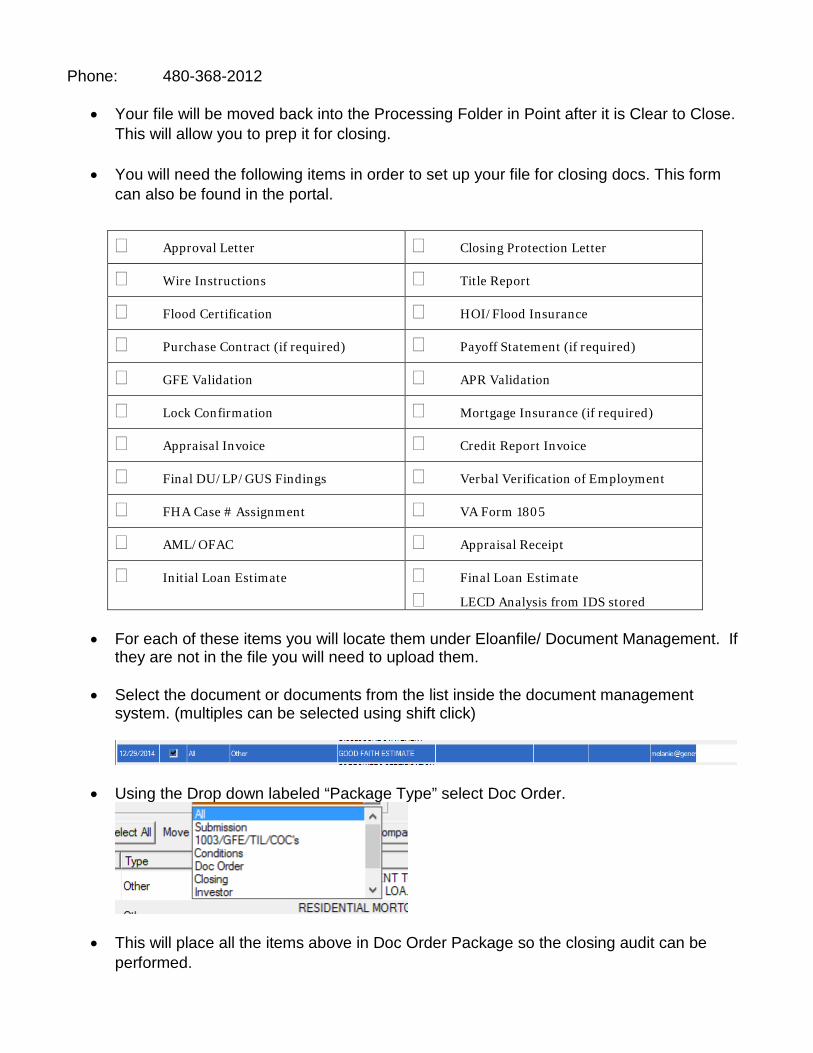

Phone: 480-368-2012

• Your file will be moved back into the Processing Folder in Point after it is Clear to Close. This will allow you to prep it for closing.

• You will need the following items in order to set up your file for closing docs. This form can also be found in the portal.

� Approval Letter � Closing Protection Letter

� Wire Instructions � Title Report

� Flood Certification � HOI/Flood Insurance

� Purchase Contract (if required) � Payoff Statement (if required)

� GFE Validation � APR Validation

� Lock Confirmation � Mortgage Insurance (if required)

� Appraisal Invoice � Credit Report Invoice

� Final DU/LP/GUS Findings � Verbal Verification of Employment

� FHA Case # Assignment � VA Form 1805

� AML/OFAC � Appraisal Receipt

� Initial Loan Estimate � Final Loan Estimate

� LECD Analysis from IDS stored

• For each of these items you will locate them under Eloanfile/ Document Management. If they are not in the file you will need to upload them.

• Select the document or documents from the list inside the document management

system. (multiples can be selected using shift click)

• Using the Drop down labeled “Package Type” select Doc Order.

• This will place all the items above in Doc Order Package so the closing audit can be performed.

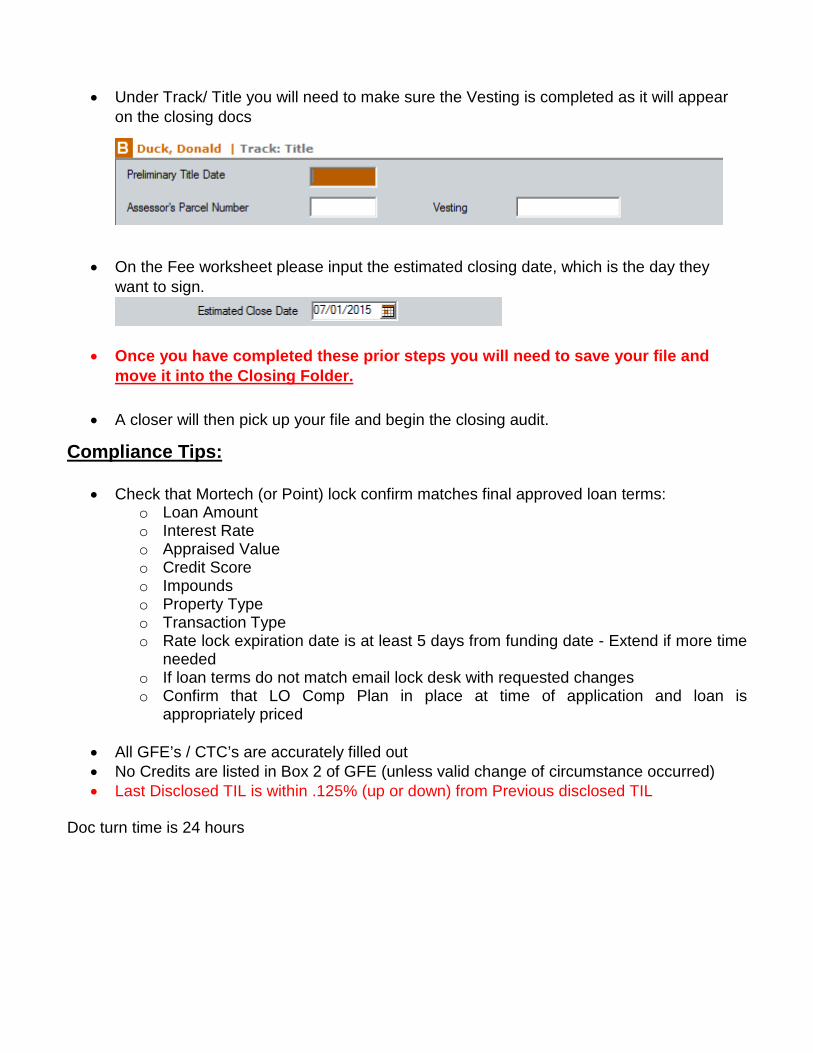

• Under Track/ Title you will need to make sure the Vesting is completed as it will appear

on the closing docs

• On the Fee worksheet please input the estimated closing date, which is the day they

want to sign.

• Once you have completed these prior steps you will need to save your file and move it into the Closing Folder.

• A closer will then pick up your file and begin the closing audit.

Compliance Tips: • Check that Mortech (or Point) lock confirm matches final approved loan terms:

o Loan Amount o Interest Rate o Appraised Value o Credit Score o Impounds o Property Type o Transaction Type o Rate lock expiration date is at least 5 days from funding date - Extend if more time

needed o If loan terms do not match email lock desk with requested changes o Confirm that LO Comp Plan in place at time of application and loan is

appropriately priced

• All GFE’s / CTC’s are accurately filled out • No Credits are listed in Box 2 of GFE (unless valid change of circumstance occurred) • Last Disclosed TIL is within .125% (up or down) from Previous disclosed TIL

Doc turn time is 24 hours

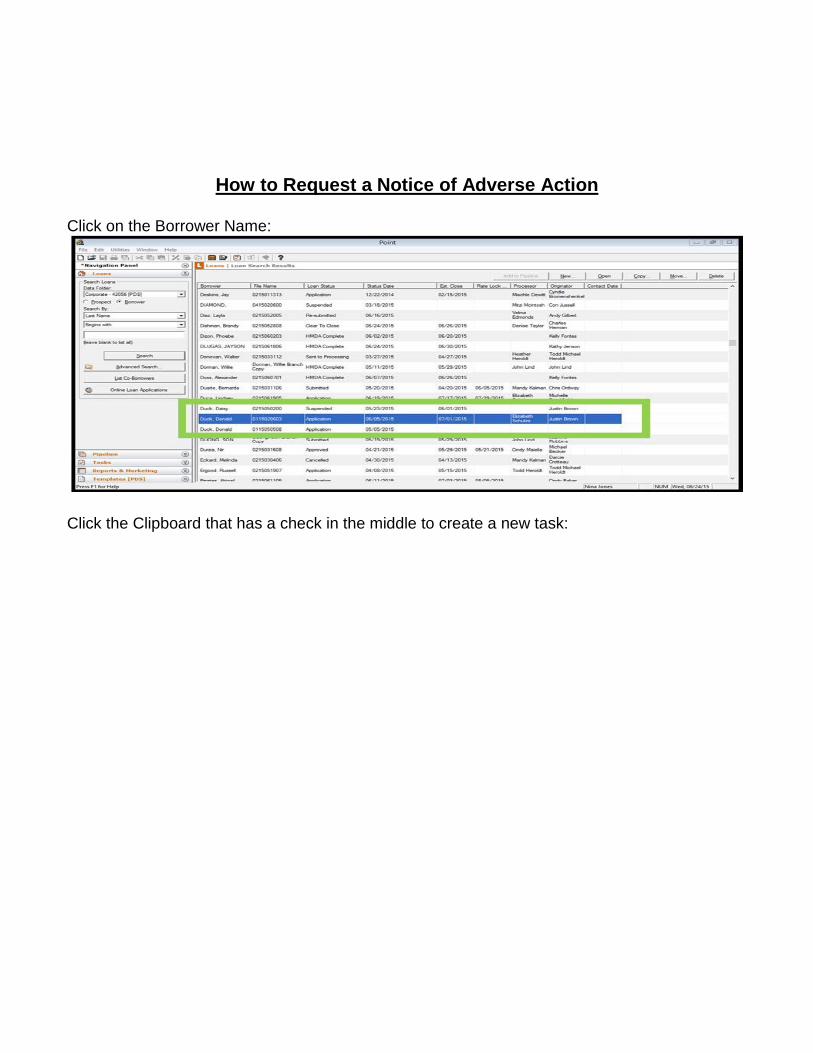

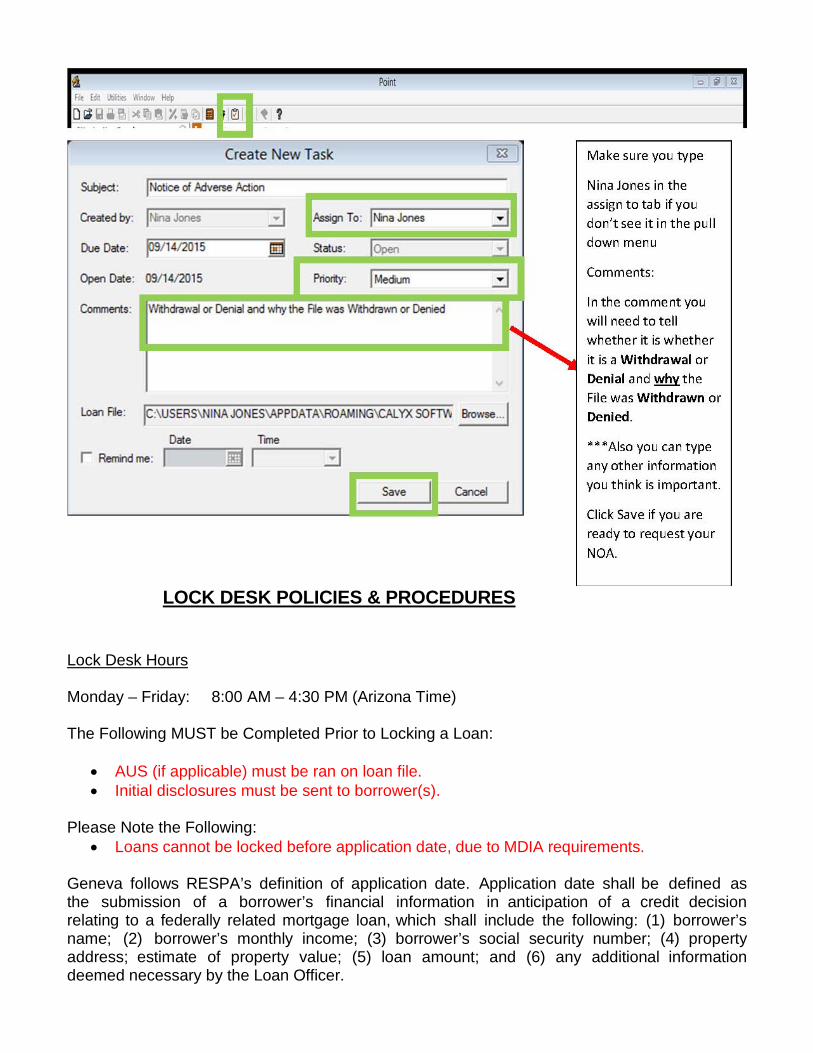

How to Request a Notice of Adverse Action

Click on the Borrower Name:

Click the Clipboard that has a check in the middle to create a new task:

LOCK DESK POLICIES & PROCEDURES

Lock Desk Hours Monday – Friday: 8:00 AM – 4:30 PM (Arizona Time) The Following MUST be Completed Prior to Locking a Loan:

• AUS (if applicable) must be ran on loan file. • Initial disclosures must be sent to borrower(s).

Please Note the Following:

• Loans cannot be locked before application date, due to MDIA requirements. Geneva follows RESPA’s definition of application date. Application date shall be defined as the submission of a borrower’s financial information in anticipation of a credit decision relating to a federally related mortgage loan, which shall include the following: (1) borrower’s name; (2) borrower’s monthly income; (3) borrower’s social security number; (4) property address; estimate of property value; (5) loan amount; and (6) any additional information deemed necessary by the Loan Officer.

Lock Duration Lock periods are available ranging from 25 to 55 days; no 10-day locks shall be granted, under any circumstances. Please make sure your lock term is sufficient to get you through the FUNDING of your loan. Lock Submission(s) All locks need to be submitted through Mortech’s portal at: www.mortech.com (No exceptions). The Geneva Financial Customer ID is 04gene01. Please refer to your welcome email for your credentials. If you are unable to locate them please contact [email protected] for a reset. LOCKING A LOAN IN MORTECH:

• Choose “Get Pricing” tab • Enter product and parameters of loan • Hit “Get Rates” • Your rate/pricing options will appear in the “rate results” screen at the top • If you would like to move forward with the lock, you can highlight your desired rate/price

and choose “Register lock” on the left hand menu • A new screen will pop up where you will have to enter specifics about the borrower and

property • Hit “submit” at the bottom and wait for the lock desk to confirm the lock (you will receive a

confirmation e-mail from Mortech once the lock has been confirmed with the investor) Loans that are banked are NOT to be registered/locked directly on the Investor web site. The Lock Desk will reviewed submitted lock requests to make sure all necessary information is included in the lock request and will register your loan with the appropriate Investor.

• Accurate lock request will be locked with the investor and then a lock confirmation will be sent to the Loan Officer via Mortech. Incorrect or incomplete lock request will be rejected and the Loan Officer will be notified via Mortech that the lock was not accepted and the reason why.

Please do not confirm the rate/price with the Borrower until the lock is confirmed by the Lock Desk. LOCK CONFIRMATIONS Once the loan has been confirmed by the lock desk, a confirmation e-mail will be sent to the Loan Officer via Mortech. You can access your lock confirmation on the Mortech site by taking the following steps:

1. Log into Mortech

2. Choose “Prospects” and “Search” 3. Change the first date on right hand side of page to on or before the lock request date 4. Hit “Search Prospects” 5. Click on the Borrower’s name 6. Choose “Lock” option on the grey menu that appears at the right 7. Choose “Lock Confirmation”

Final lock confirmation must match final underwriting approval for loan amount, LTV, etc. CHANGE REQUEST:

• Once you login to Mortech, go to “Prospects” and “Search” • Enter in your borrower’s name and change the first date on the right hand side of the

page to the date that you locked the loan or before • Hit “Search Prospects” • Clink on Borrower’s name • Choose “Lock” option on the grey menu that appears at the right • Choose “Change Request” • Add notes for the items that you need to change or the amount of time that you need to

extend and hit “Send” LOCKING JUMBO LOANS IN MORTECH: When you price Jumbo loans on Mortech, you will not be able to see the investor that the loan is priced with. As important, when you lock the loan on Mortech, you will also not be able to see the investor that the loan is locked with. It is imperative that the pricing and locks match the investor that the loan is submitted to for underwriting. These Jumbo products are not underwritten in-house (non-delegated).

It is imperative that you follow the procedures listed below. If you do not, your loan may not be priced, locked, or submitted as you intended.

• Loan officer creates prospect or imports prospect to Mortech. • Loan officer prices Jumbo loan. • Loan officer emails Lock Desk to provide Investor information. • Lock Desk Emails Best Investor Name and Pricing back to Loan Officer and notes the

Mortech file the quote in the notes. • Processor submits file to investor for non-delegated underwriting. • When Loan officer is ready to lock they submit their lock through Mortech and reference

the investor that will be UW the loan. • Lock Desk will confirm price and investor and either will lock if it matches the request or

will advise the loan officer of the change in price. • Loan officer will confirm price change in order to lock. • Lock Desk locks loan.

Lock Extensions Policy

A rate lock can be extended if the active lock is within 10 days of expiration and for a maximum of 30 days from the original rate lock expiration. If the original lock term expires before the lock is extended, the loan will subject to re-pricing. All extensions are handled in the Mortech pricing engine by accessing your loan and selecting the Extend button on the Lock Request Application. Extension Costs Lock extension are at .02 per day. If your Mortech lock has expired then you will be charged an additional .25 bases points in addition to the .02 per day. It should be noted that extension costs can be avoided by locking for longer periods at the time of initial lock. Additionally, the second lock extension is more costly, so it is generally advisable to extend for a longer period of time. Re-Lock Policy Re-locks are only available for loans that have lock commitments that have expired or program/product changes that are not eligible for re-pricing from the original rate sheet. Re-locks are subject to worse case pricing and under no circumstance will the re-lock price be better than the original locked price. Re-locks are handled in the Mortech pricing engine by accessing your loan and selecting the Send a Loan Comment button and requesting a re-lock terms you need. Market Re-Prices If, from the time the lock is submitted, the market re-prices for the worse, the lock in Mortech may not be honored. In that case a new rate lock may need to be submitted. If pricing improves, the price improvement will be passed on to the file. Lock Corrections Lock corrections are handled through Mortech using the Change Loan Terms form (button on bottom right of lock screen). Terms need to be updated and the request submitted to Lock Desk. Please be sure to advise the lock desk of corrections (i.e. Loan amount, value, and LTV changes, etc.) as soon as possible so that updated pricing can be confirmed and the changes can properly be disclosed to the Borrower(s). Lock Flip Policy If a loan is locked and no longer qualifies for the current program, it may be re- locked or “flipped” to another investor only if the current investor does not offer or does not have a comparable product. Please note this only applies to Best Effort locks. For instance, if a loan is locked at Investor A as a Conventional 30 year fixed and it changes to an FHA 5/1 ARM, you cannot flip it to Investor B if Investor A offers both products. If Investor A does not offer the FHA 5/1 ARM, the lock can be flipped to Investor B. Adding or dropping a borrower shall not be sufficient reason to flip a lock.

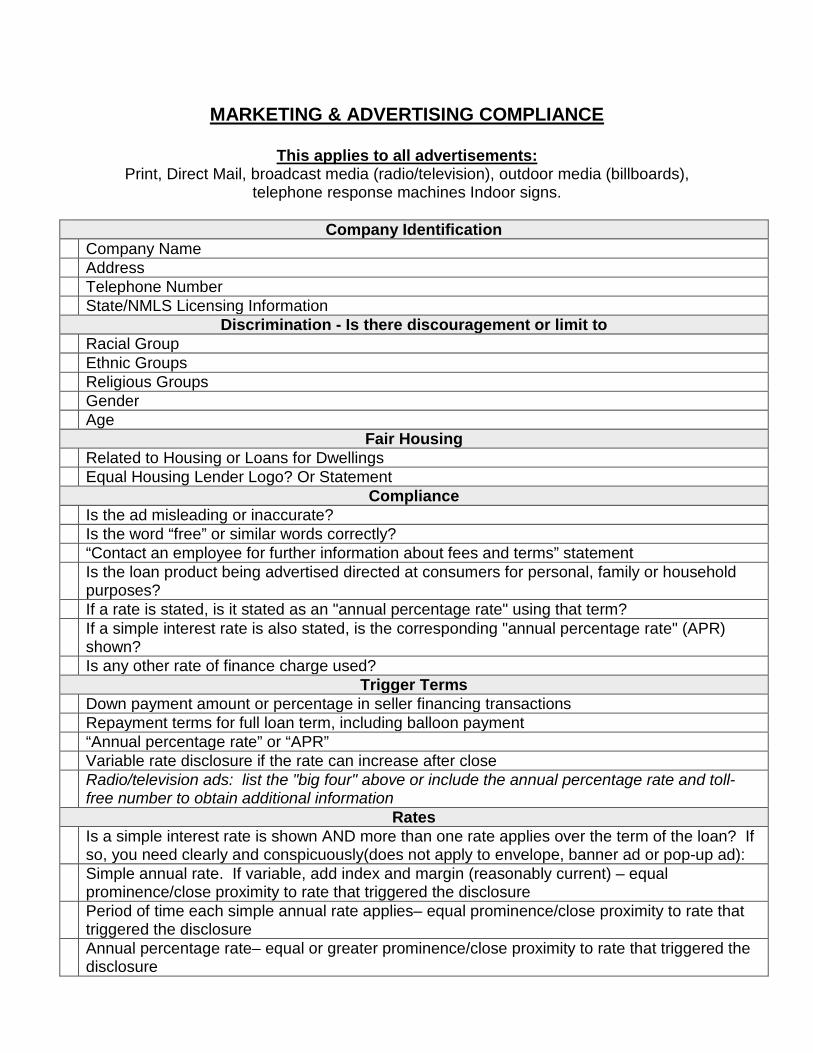

MARKETING & ADVERTISING COMPLIANCE

This applies to all advertisements: Print, Direct Mail, broadcast media (radio/television), outdoor media (billboards),

telephone response machines Indoor signs.

Company Identification Company Name Address Telephone Number State/NMLS Licensing Information

Discrimination - Is there discouragement or limit to Racial Group Ethnic Groups Religious Groups Gender Age

Fair Housing Related to Housing or Loans for Dwellings Equal Housing Lender Logo? Or Statement

Compliance Is the ad misleading or inaccurate? Is the word “free” or similar words correctly? “Contact an employee for further information about fees and terms” statement

Is the loan product being advertised directed at consumers for personal, family or household purposes?

If a rate is stated, is it stated as an "annual percentage rate" using that term?

If a simple interest rate is also stated, is the corresponding "annual percentage rate" (APR) shown?

Is any other rate of finance charge used? Trigger Terms

Down payment amount or percentage in seller financing transactions Repayment terms for full loan term, including balloon payment “Annual percentage rate” or “APR” Variable rate disclosure if the rate can increase after close

Radio/television ads: list the "big four" above or include the annual percentage rate and toll-free number to obtain additional information

Rates

Is a simple interest rate is shown AND more than one rate applies over the term of the loan? If so, you need clearly and conspicuously(does not apply to envelope, banner ad or pop-up ad):

Simple annual rate. If variable, add index and margin (reasonably current) – equal prominence/close proximity to rate that triggered the disclosure

Period of time each simple annual rate applies– equal prominence/close proximity to rate that triggered the disclosure

Annual percentage rate– equal or greater prominence/close proximity to rate that triggered the disclosure

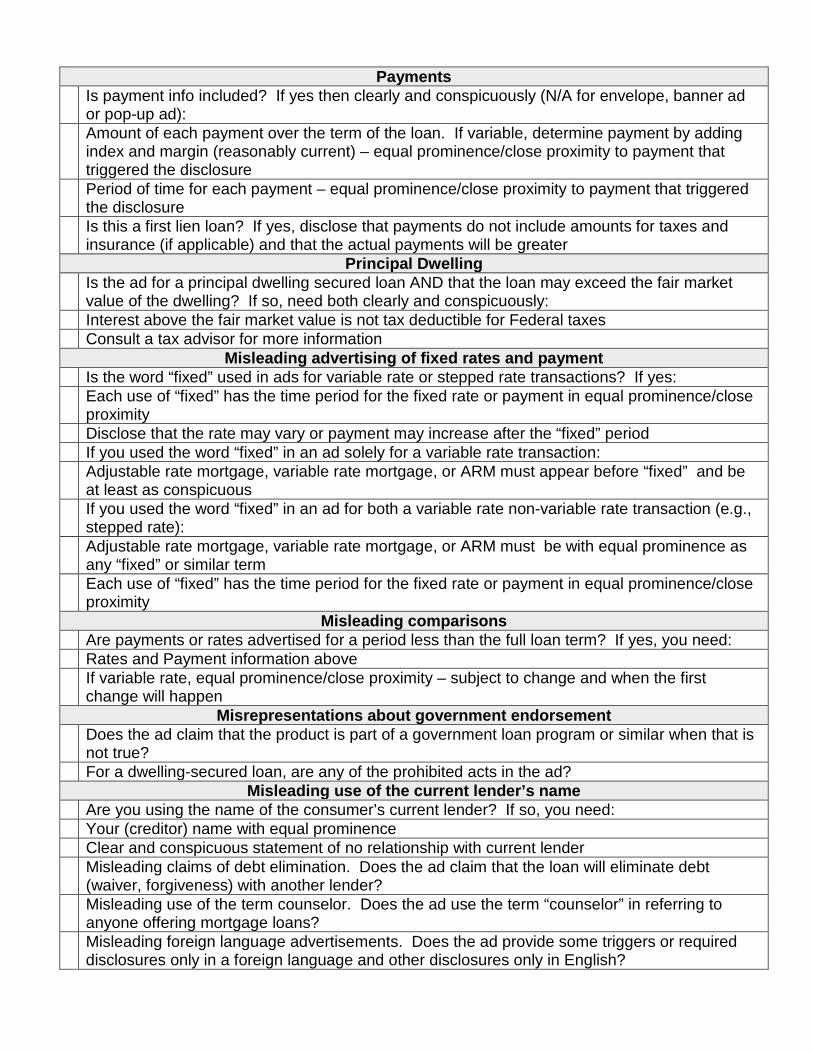

Payments

Is payment info included? If yes then clearly and conspicuously (N/A for envelope, banner ad or pop-up ad):

Amount of each payment over the term of the loan. If variable, determine payment by adding index and margin (reasonably current) – equal prominence/close proximity to payment that triggered the disclosure

Period of time for each payment – equal prominence/close proximity to payment that triggered the disclosure

Is this a first lien loan? If yes, disclose that payments do not include amounts for taxes and insurance (if applicable) and that the actual payments will be greater

Principal Dwelling

Is the ad for a principal dwelling secured loan AND that the loan may exceed the fair market value of the dwelling? If so, need both clearly and conspicuously:

Interest above the fair market value is not tax deductible for Federal taxes Consult a tax advisor for more information

Misleading advertising of fixed rates and payment Is the word “fixed” used in ads for variable rate or stepped rate transactions? If yes:

Each use of “fixed” has the time period for the fixed rate or payment in equal prominence/close proximity

Disclose that the rate may vary or payment may increase after the “fixed” period If you used the word “fixed” in an ad solely for a variable rate transaction:

Adjustable rate mortgage, variable rate mortgage, or ARM must appear before “fixed” and be at least as conspicuous

If you used the word “fixed” in an ad for both a variable rate non-variable rate transaction (e.g., stepped rate):

Adjustable rate mortgage, variable rate mortgage, or ARM must be with equal prominence as any “fixed” or similar term

Each use of “fixed” has the time period for the fixed rate or payment in equal prominence/close proximity

Misleading comparisons Are payments or rates advertised for a period less than the full loan term? If yes, you need: Rates and Payment information above

If variable rate, equal prominence/close proximity – subject to change and when the first change will happen

Misrepresentations about government endorsement

Does the ad claim that the product is part of a government loan program or similar when that is not true?

For a dwelling-secured loan, are any of the prohibited acts in the ad? Misleading use of the current lender’s name

Are you using the name of the consumer’s current lender? If so, you need: Your (creditor) name with equal prominence Clear and conspicuous statement of no relationship with current lender

Misleading claims of debt elimination. Does the ad claim that the loan will eliminate debt (waiver, forgiveness) with another lender?

Misleading use of the term counselor. Does the ad use the term “counselor” in referring to anyone offering mortgage loans?

Misleading foreign language advertisements. Does the ad provide some triggers or required disclosures only in a foreign language and other disclosures only in English?

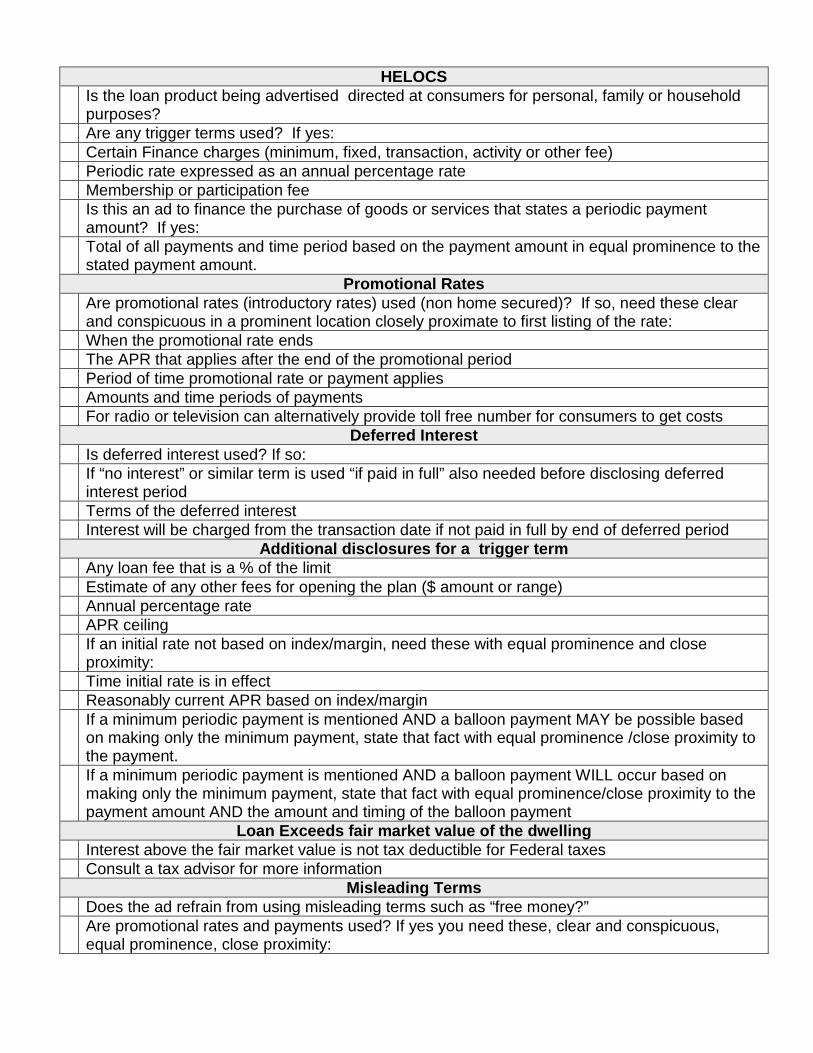

HELOCS

Is the loan product being advertised directed at consumers for personal, family or household purposes?

Are any trigger terms used? If yes: Certain Finance charges (minimum, fixed, transaction, activity or other fee) Periodic rate expressed as an annual percentage rate Membership or participation fee

Is this an ad to finance the purchase of goods or services that states a periodic payment amount? If yes:

Total of all payments and time period based on the payment amount in equal prominence to the stated payment amount.

Promotional Rates

Are promotional rates (introductory rates) used (non home secured)? If so, need these clear and conspicuous in a prominent location closely proximate to first listing of the rate:

When the promotional rate ends The APR that applies after the end of the promotional period Period of time promotional rate or payment applies Amounts and time periods of payments For radio or television can alternatively provide toll free number for consumers to get costs

Deferred Interest Is deferred interest used? If so:

If “no interest” or similar term is used “if paid in full” also needed before disclosing deferred interest period

Terms of the deferred interest Interest will be charged from the transaction date if not paid in full by end of deferred period

Additional disclosures for a trigger term Any loan fee that is a % of the limit Estimate of any other fees for opening the plan ($ amount or range) Annual percentage rate APR ceiling

If an initial rate not based on index/margin, need these with equal prominence and close proximity:

Time initial rate is in effect Reasonably current APR based on index/margin

If a minimum periodic payment is mentioned AND a balloon payment MAY be possible based on making only the minimum payment, state that fact with equal prominence /close proximity to the payment.

If a minimum periodic payment is mentioned AND a balloon payment WILL occur based on making only the minimum payment, state that fact with equal prominence/close proximity to the payment amount AND the amount and timing of the balloon payment

Loan Exceeds fair market value of the dwelling Interest above the fair market value is not tax deductible for Federal taxes Consult a tax advisor for more information

Misleading Terms Does the ad refrain from using misleading terms such as “free money?”

Are promotional rates and payments used? If yes you need these, clear and conspicuous, equal prominence, close proximity:

All Advertising pieces must be submitted to our compliance manager Bill Morwood for approval prior to print. Please email them to [email protected]. This document can also be found in the Portal.

AUDIT POLICIES & PROCEDURES

Our mission statement: To provide accurate and knowledgeable guidance to loan officers and associated staff. To ensure the integrity of each file under Federal and internal guidelines. We strive to deliver the highest standard of customer service to our loan officers and staff members.

Policy and Procedure – Time Frames

Commission payroll occurs every other week on Friday. Loans submitted for payroll will be accepted Monday-Friday covering a full 10 business day period. Loans submitted after 5pm AZ time will be considered “Submitted” but will not be considered until the next pay period (2 weeks later).

Policy and Procedure – Brokered Loan Submission

Brokered loans are due for audit within 7 days of funding. Files submitted for payroll more than 7 days after funding will be subject to a $500 fee.

Loans will be considered for payroll after the following steps have been completed:

• Ensure all required documentation (see Audit Checklist) is in the Point file – this includes the signed closing package and broker check

• Ensure the Point file is marked as “Funded” • Email: [email protected] – include the Point file number and borrower last name

in the subject line

Files will be audited for completion, data accuracy and compensation prior to submitting to accounting for payroll.

A list of any missing items from the file will be emailed to the loan officer and/or processor as necessary and will be due no later than 12 pm the Monday prior to the pay period. Files that miss the specified cutoff times will be eligible for a manual check at a $100 fee. Manual checks for this reason cannot be requested prior to 1 pm on the Wednesday prior to submission. All other manual checks can be requested at the time the payroll/commission worksheet is received by the loan officer or branch manager, as applicable.

Policy and Procedure – Banked Loan Submission

Banked loans are audited at the time the file is submitted to the closing department for signing. The closing department/doc drawer is responsible for verifying the compensation requirements are being met. Any discrepancies will be discussed with the loan officer/branch manager as necessary. The closer/doc drawer will document the file to relay any pertinent compensation issues for payroll completion.

As the loan is funding the funder will create the “Closing Worksheet” to display all pertinent closing/wire transfer information. This document will be made available to payroll for

completion. At the end of each business day the funding department will notify payroll via email which loans have funded. Payroll will then verify and complete the “Closing Worksheet” to deliver to accounting to be entered for the applicable pay period. The loan officer/branch manager will receive a PDF version of the payroll/commission worksheet as applicable.

APPRAISAL POLICIES & PROCEDURES AMC Appraisal Contacts Company: Tri-Serve Name: Mark Walser Email: [email protected] Phone: 925-698-2056 Website: www.triservllc.com Company: Streetlinks Name: Mary Hudson (Account Executive) Email: [email protected] Phone: 317-215-8243 Website: www.Streetlinks.com Company: USRes Name: Email: Phone: Website: Please email [email protected] for AMC credentials Appraisal can be order once you have the Disclosures signed by the borrower(s).