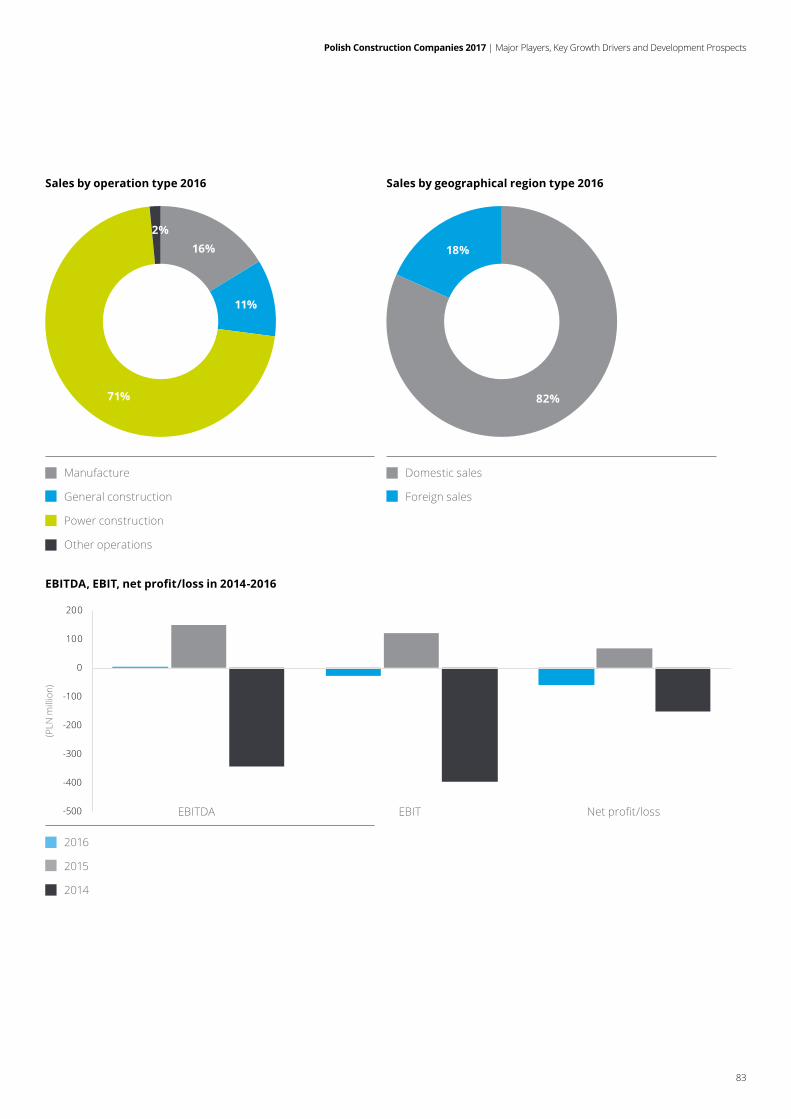

polish construction companies 2017 – major players, key ... · polish construction companies 2017...

TRANSCRIPT

Polish Construction Companies 2017 – Major Players, Key Growth Drivers and Development Prospects

Introduction 5

Section 1. Analysis of the largest construction companies 7

1.1. Ranking of the largest Polish construction companies by revenue earned in 2016 8

1.2. Ranking of the largest Polish construction companies by operating income achieved in 2016 10

1.3. RankingofthelargestPolishconstructioncompaniesbynetprofitachievedin2016 12

1.4. Debt analysis of the largest construction companies in 2016 15

1.5. Relation of capital expenditure to sales ratio of the largest construction companies in 2016 16

1.6. Geographical and generic structure of revenue earned by the largest construction companies in 2016 18

1.7. Market cap of the largest construction companies listed on the Warsaw Stock Exchange 26

Section 2. Prospects for development of construction companies in Poland 33

2.1. Introduction 34

2.2. Macroeconomic factors: economic growth, public debt 39

2.3. EU funds 41

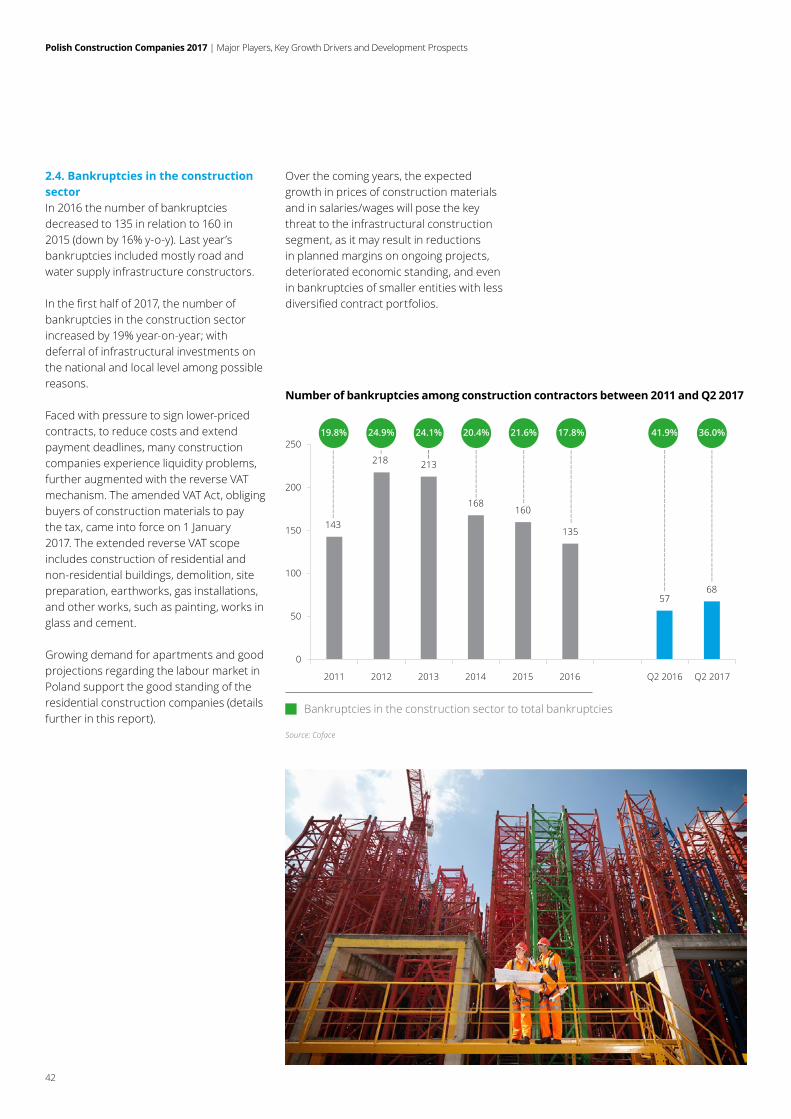

2.4. Bankruptcies in the construction sector 42

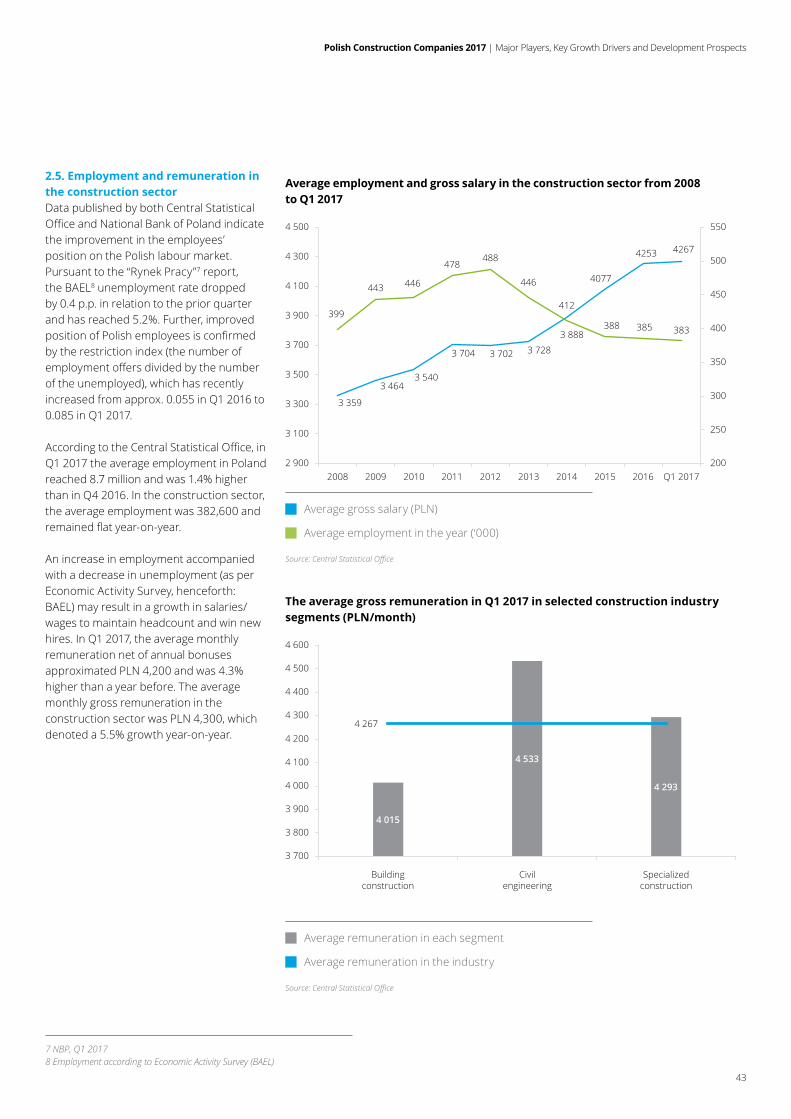

2.5. Employment and remuneration in the construction sector 43

2.6. Development prospects for construction market segments in Poland 45

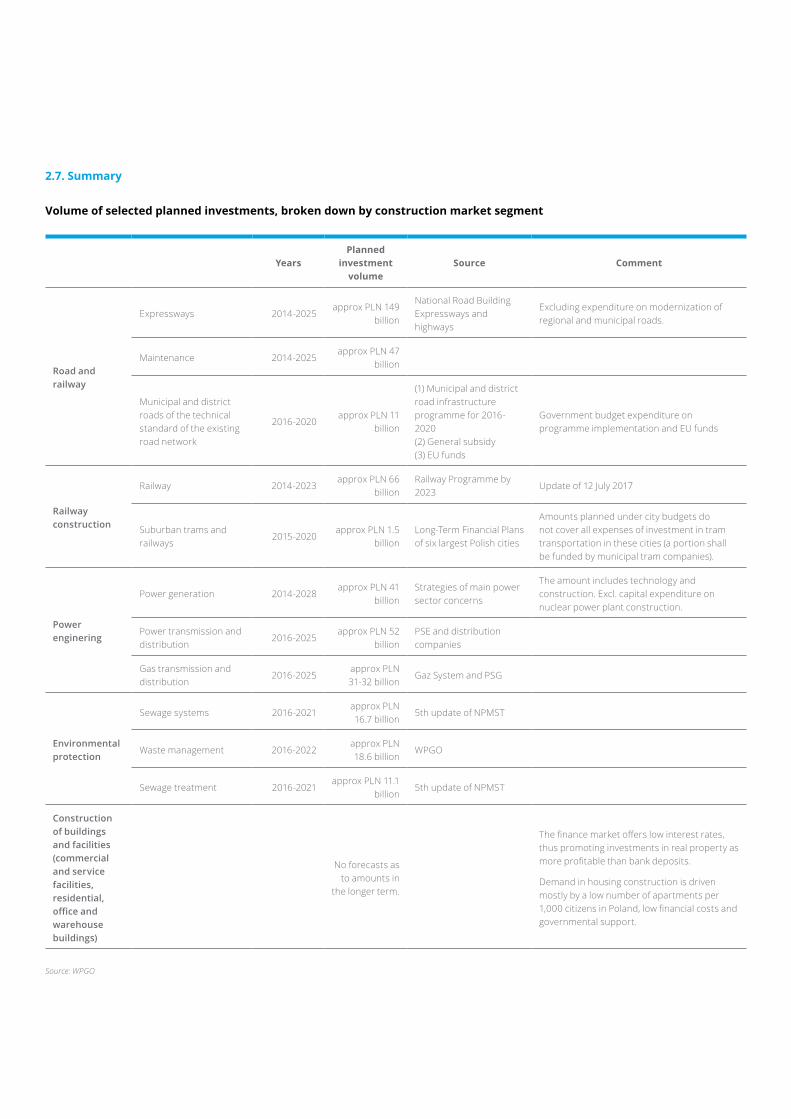

2.7. Summary 67

Section 3. Profiles of largest construction companies in Poland 69

Bibliography 115

Contact 117

Contents

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

5

Introduction

Ladies and Gentlemen,

We have the pleasure to present to you thefiftheditionofourannualreport:"Polish Construction Companies 2017 - Key Players, Key Growth Factors and Perspectives for Industry Growth", in which we present the analysis of the condition ofthefifteenlargestPolishconstructioncompanies in terms of revenues and describe the prospects of market development broken down into its key sectors.

As projected, after a period of growth over the years 2014-2015, 2016 saw a decrease in construction and assembly contracts, whichwasreflectedinourranking.Thetotalrevenueofthefifteenlargestconstruction companies exceeded PLN 28.6 billion, but was 3% lower than a year before, although still higher than in 2014 (PLN 27.9 billion).

The slowdown seen on the construction market resulted mostly from a deferral in new tender procedures regarding large infrastructural projects, co-funded under 2014-2020 EU perspective.

At the end of 2016, there was a revival and improvement in the construction industry. Growth rate and further development of the construction market will depend will dependmostlyoneffectiveuseofEUfundsunder2014-2020perspectivetofinancelarge projects, especially regarding roads and railways. Despite a material increase in the number of new projects announced at the end of 2016 and in 2017, sector representatives remain concerned that deferred public procurement procedures regarding large projects may result in accumulation of work, construction material price increases and problems with accesstoqualifiedstaff.

2017willnotseeintensifiedconstructionworks as most projects follow the “design and construct” approach. In the upcoming years, construction companies will on the one hand focus on taking most advantage of the increased volume of projects and look for opportunities ensuring long-term growth in value after 2020 on the other. At present, expansion on foreign markets can be observed, accompanied with business diversificationandinvestinginnewcompetencies, such as modernization of buildings or maintenance of infrastructure.

Asinpreviouseditions,thefirstpartofthereportincludesafinancialanalysisoffifteenentitiesthathaveachievedthestrongest market standing in 2016. It examinestheirrevenues,salesprofits,netprofits,debt,geographicalandrevenuestructure.

The second part of the report presents growth projections for the industry, both in short and medium term, including expenditure planned in each market segment and statistics regarding bankruptcies and employment trends in the construction sector. At the end of this section, a summary of the industry’s current condition and the key growth drivers are presented from the perspective of the largest Polish construction companies and key public investors, such as PKP Polskie Linie Kolejowe S.A.

Inthefinalpartofthereport,webrieflyexamine the characteristics of the business activityofthefifteenmostimportantmarket players in 2016. We include the most crucial information concerning the scope of their activities, ownership structuresanddetailedfinancialdataderivedfromtheirannualfinancialstatements.

The report has been based on publicly availablefinancialdataorinformationprovided to us directly by the entities presented herein.

WehopethatyouwillfindthereportPolish Construction Companies 2017 – Major Players, Key Growth Drivers and Development Prospects informative and that it will give you a better understanding of the current situation on the Polish construction market, including the opportunities and challenges that lie ahead of sector investors and construction companies.

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

6

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

7

Section 1. Analysis of largest

construction companies

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

8

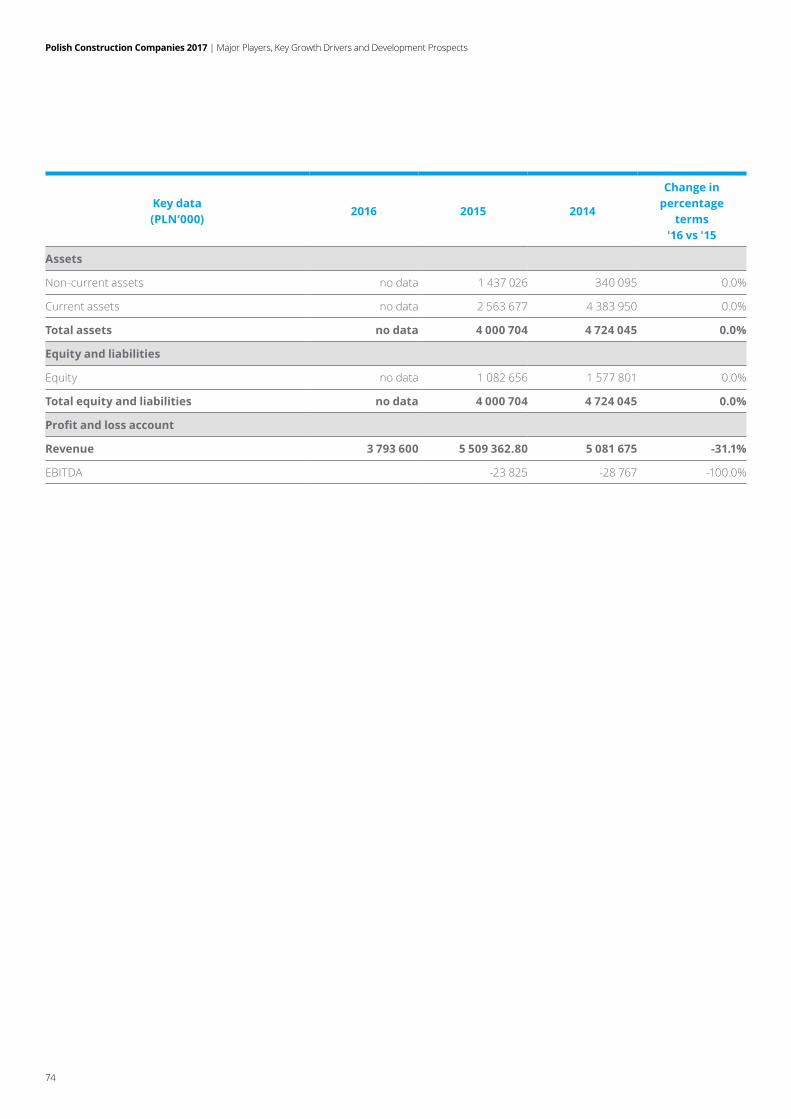

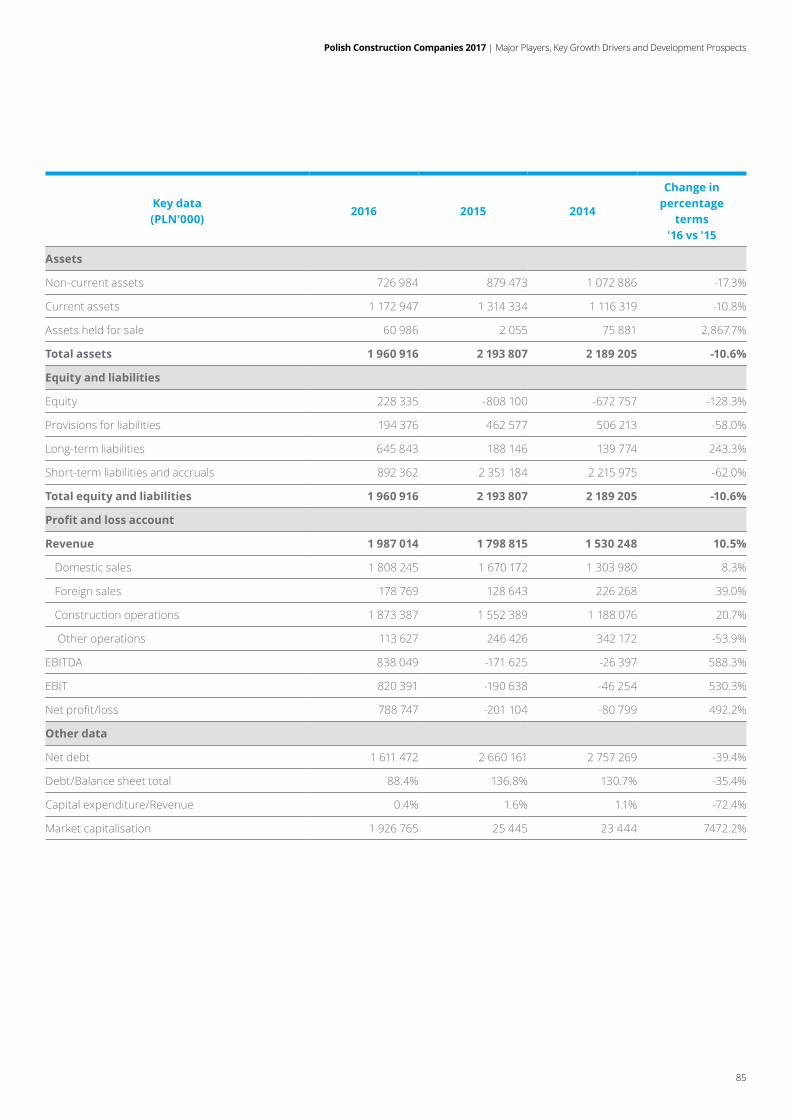

1.1. Ranking of the largest Polish construction companies by revenue earned in 2016In2016,revenueofthefifteenlargestconstruction companies reached PLN 28.6 billion, which denotes an almost 3% decrease in comparison to the prior year. Budimex Group, with revenue of PLN 5.6 billion (a 8.5% increase in comparison to 2015) has become the leader, followed by Skanska S.A. with revenue of PLN 3.8 billion. At this point it should be emphasized that in previous years, our ranking included aggregatefinancialdataofallSkanskaGroupcompanies operating in Poland, while this

year, the Group has provided us only with information regarding revenue generated by Skanska S.A. As in prior years, the last place has been taken by Strabag, an Austrian origin company, with a revenue decrease of 11% vs. prior year, equal to PLN 3.4 billion.

In 2016, the Budimex Group, the ranking leader, saw the highest revenue growth in terms of value (by PLN 438 million). The PBG Group also experienced a substantial revenue increase (PLN 188 million, i.e. 10.5%). The third best result was achieved by the Mostostal Warszawa Group, with revenue increase of PLN 128 million (10%

compared to the prior year) following two years of drop, which has moved it two places up in the ranking. Revenue increase seen by other entities included in the ranking did not exceed PLN 120 million.

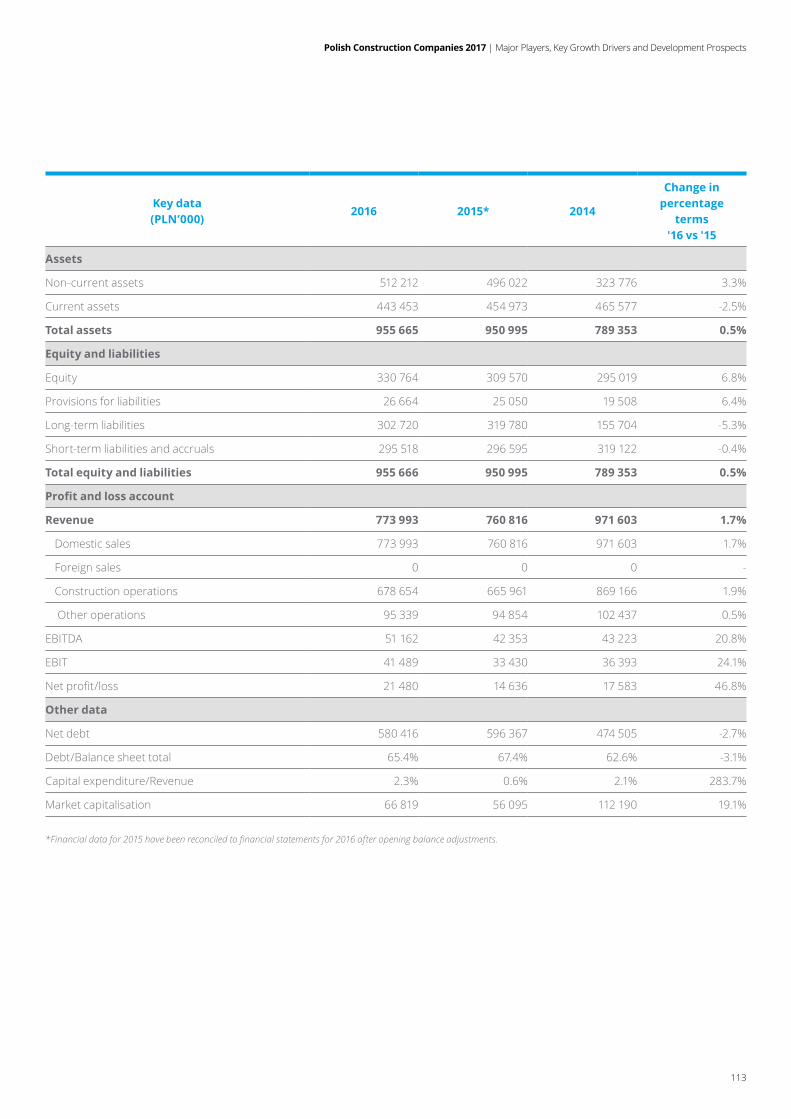

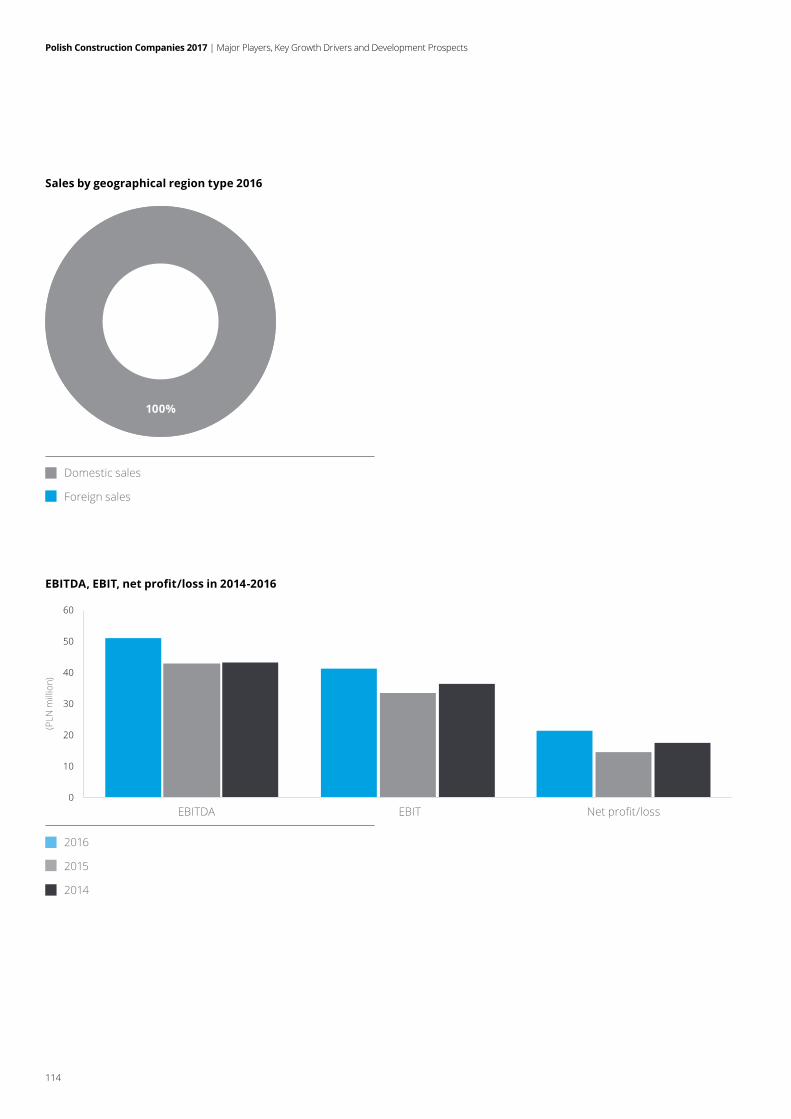

Table 1.1: The largest construction companies in Poland by revenue in 2016 (PLN ‘000)

No. Company nameRevenue

2016Revenue

2015Change in

nominal terms

Change in percentage

terms

1 Budimex Group 5 572 290 5 133 994 438 296 8.5%

2 Skanska S.A.1 3 793 600 4 430 900 -637 300 -14.4%

3 Strabag Group2 3 423 635 3 847 423 -423 788 -11.0%

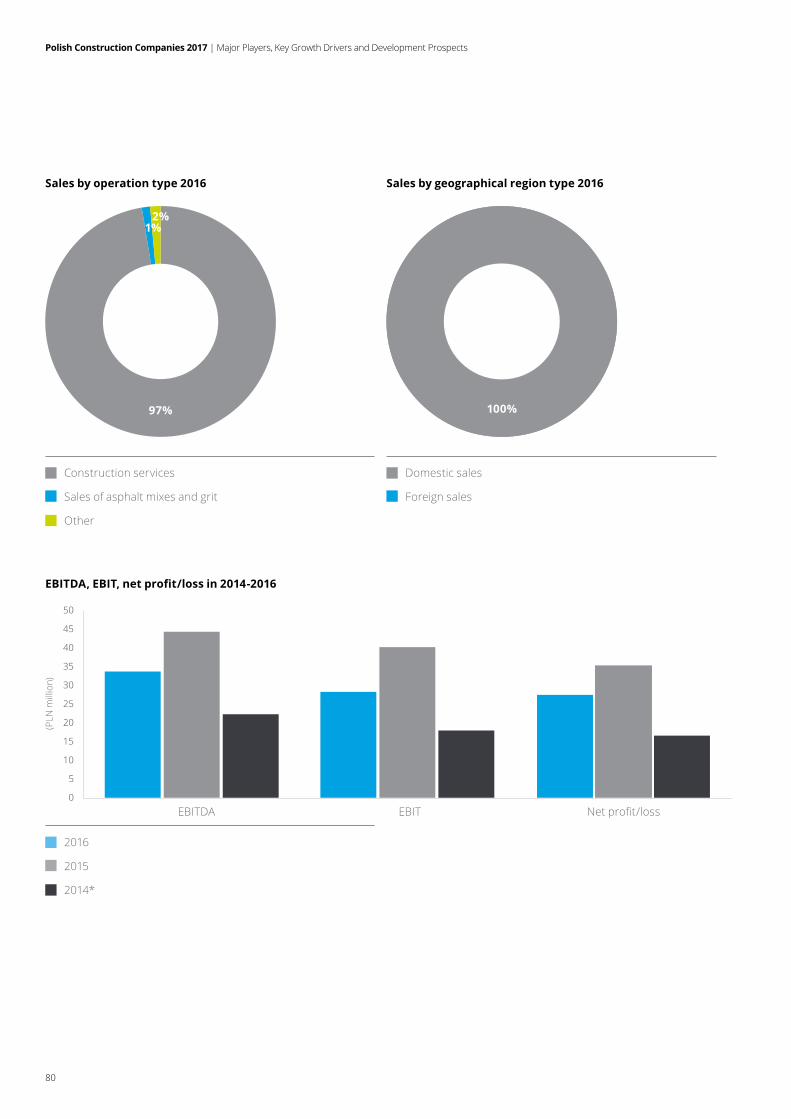

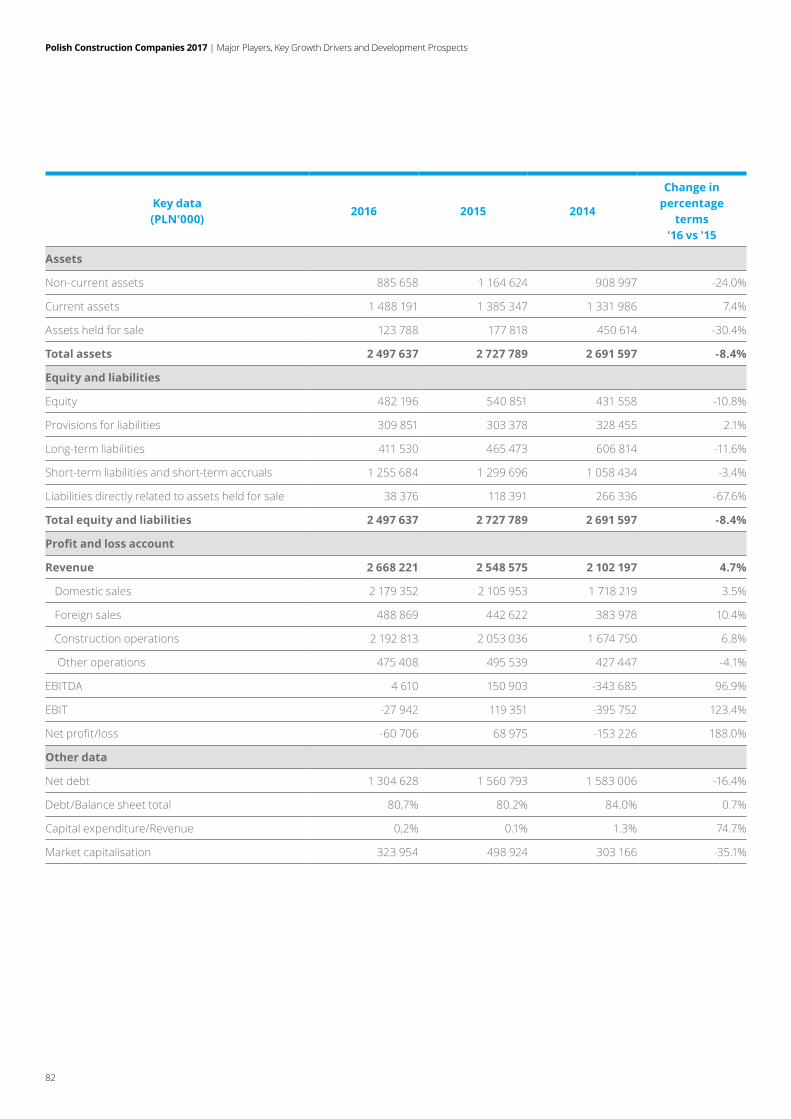

4 Polimex-Mostostal Group 2 668 221 2 548 575 119 646 4.7%

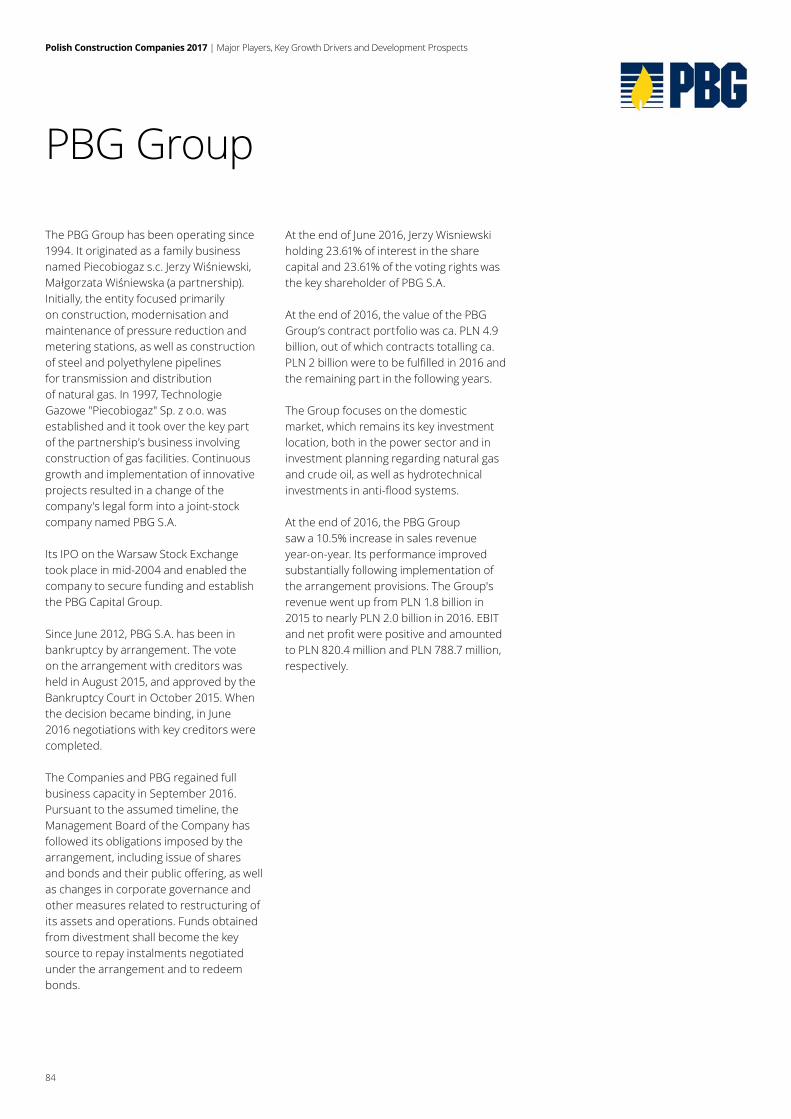

5 PBG Group 1 987 014 1 798 815 188 199 10.5%

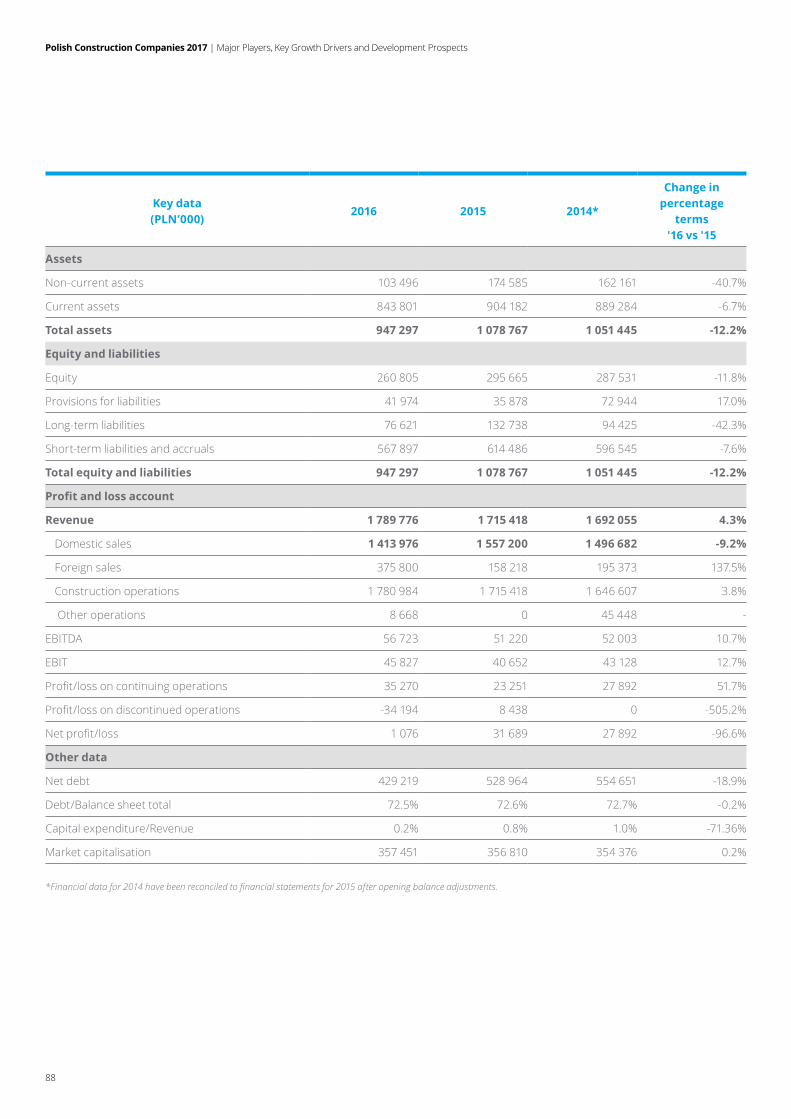

6 Erbud Group3 1 789 776 1 715 418 74 358 4.3%

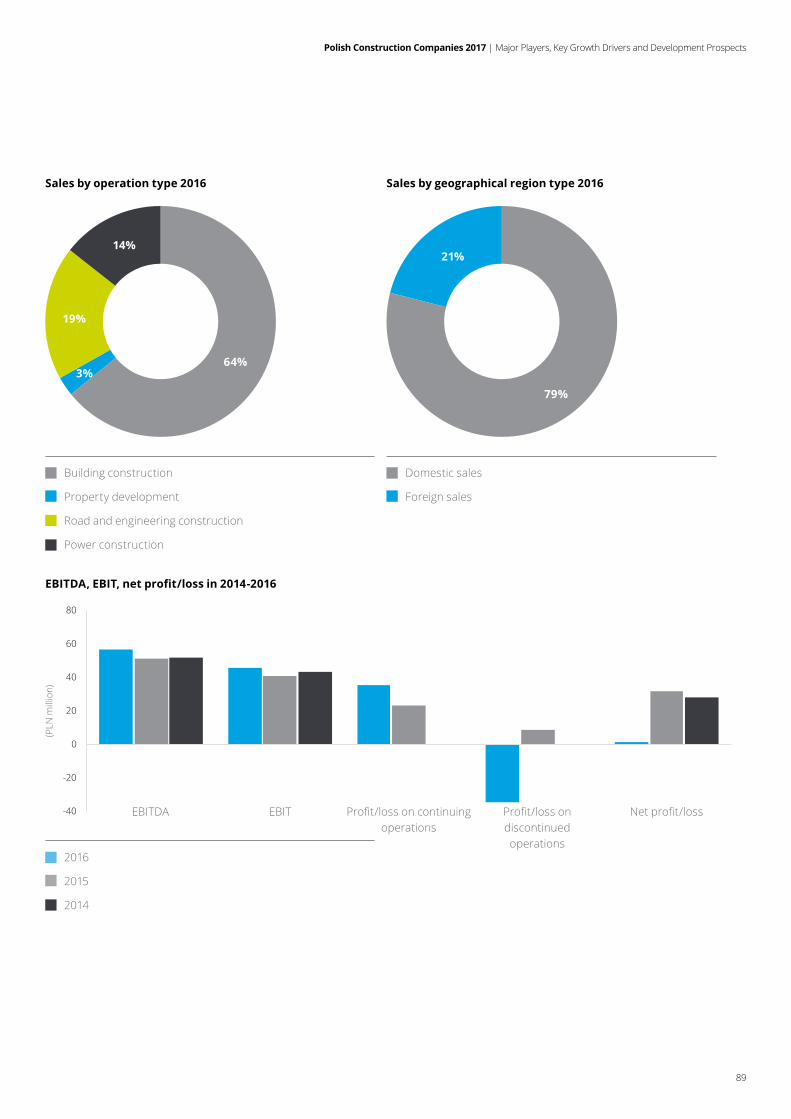

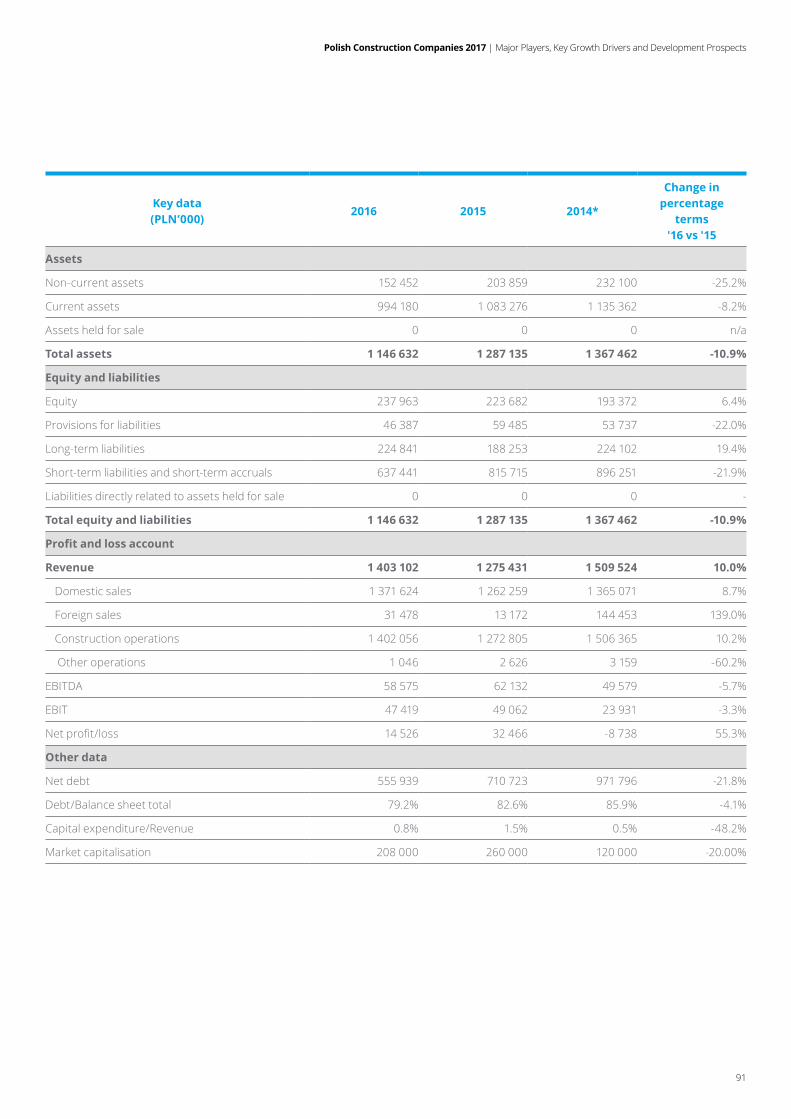

7 Mostostal Warszawa Group 1 403 102 1 275 431 127 671 10.0%

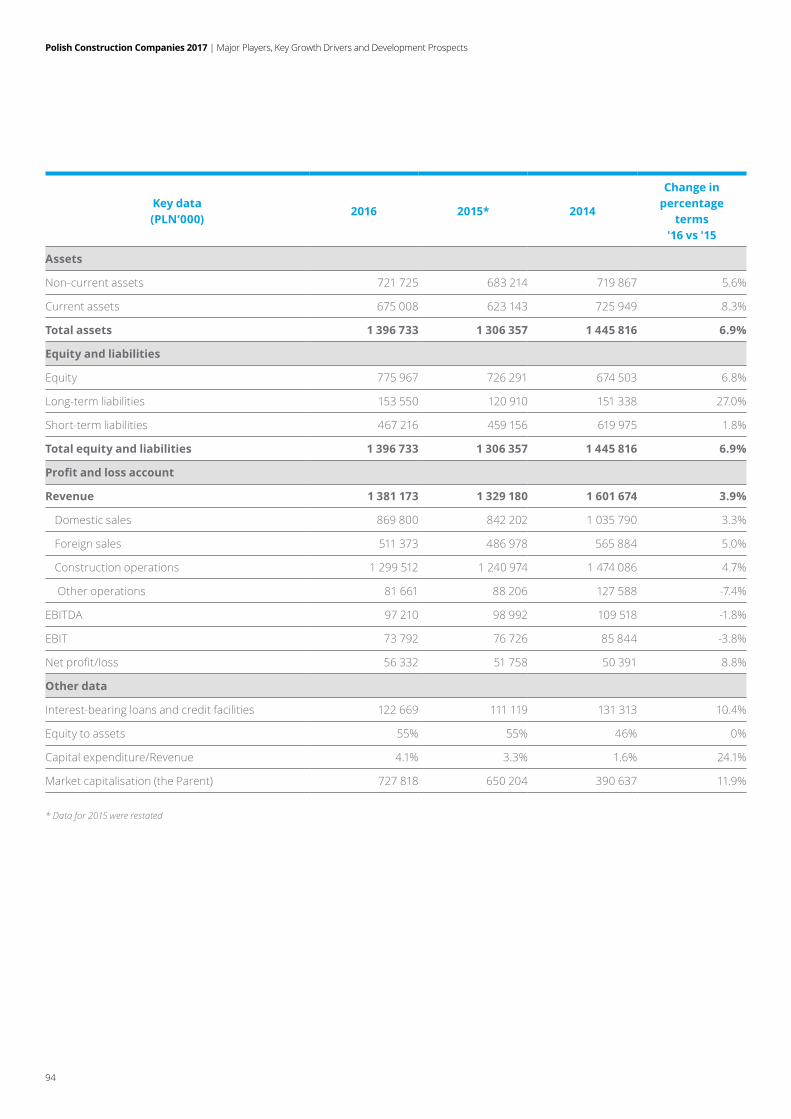

8 Trakcja Group 1 381 173 1 329 180 51 993 3.9%

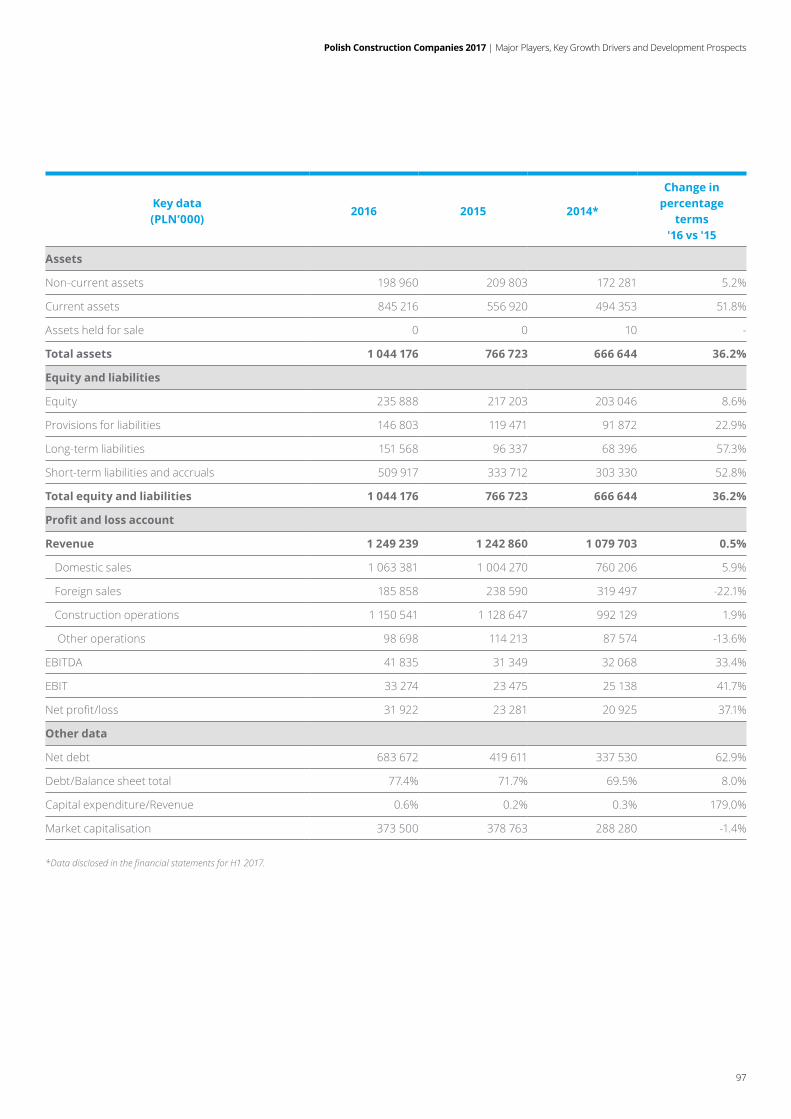

9 Unibep Group 1 249 239 1 242 860 6 379 0.5%

10 PORR Group4 1 109 738 1 294 204 -184 466 -14.3%

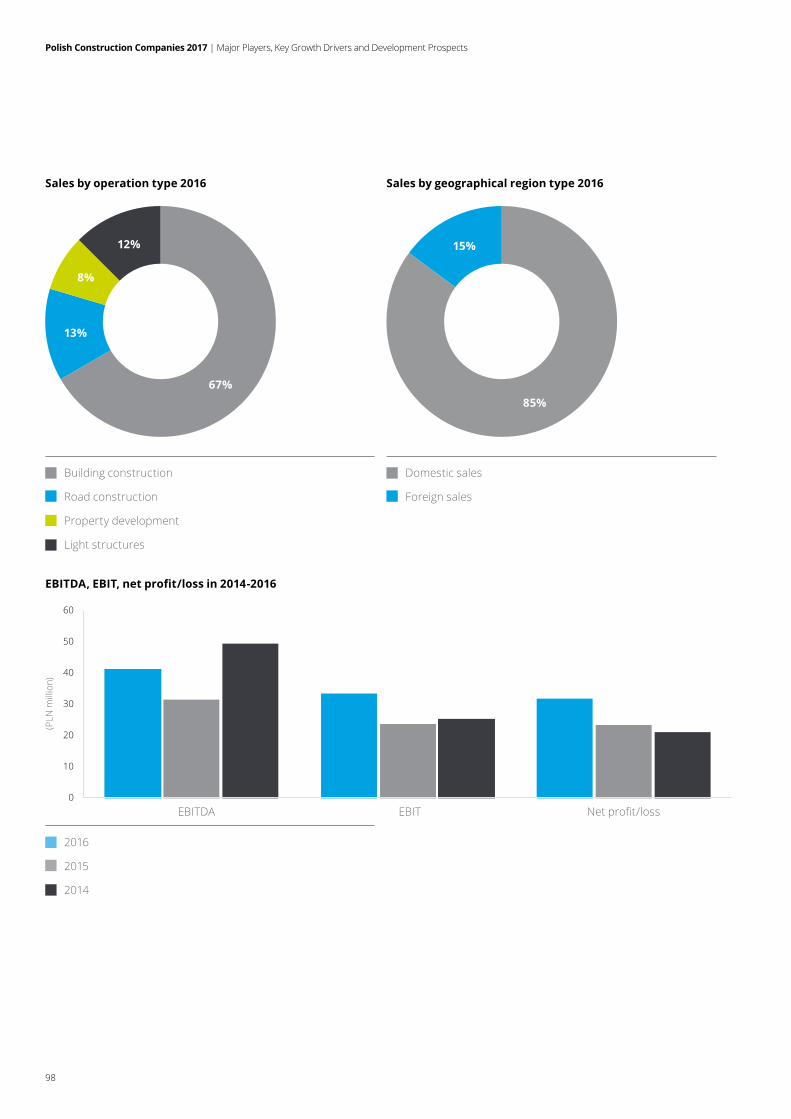

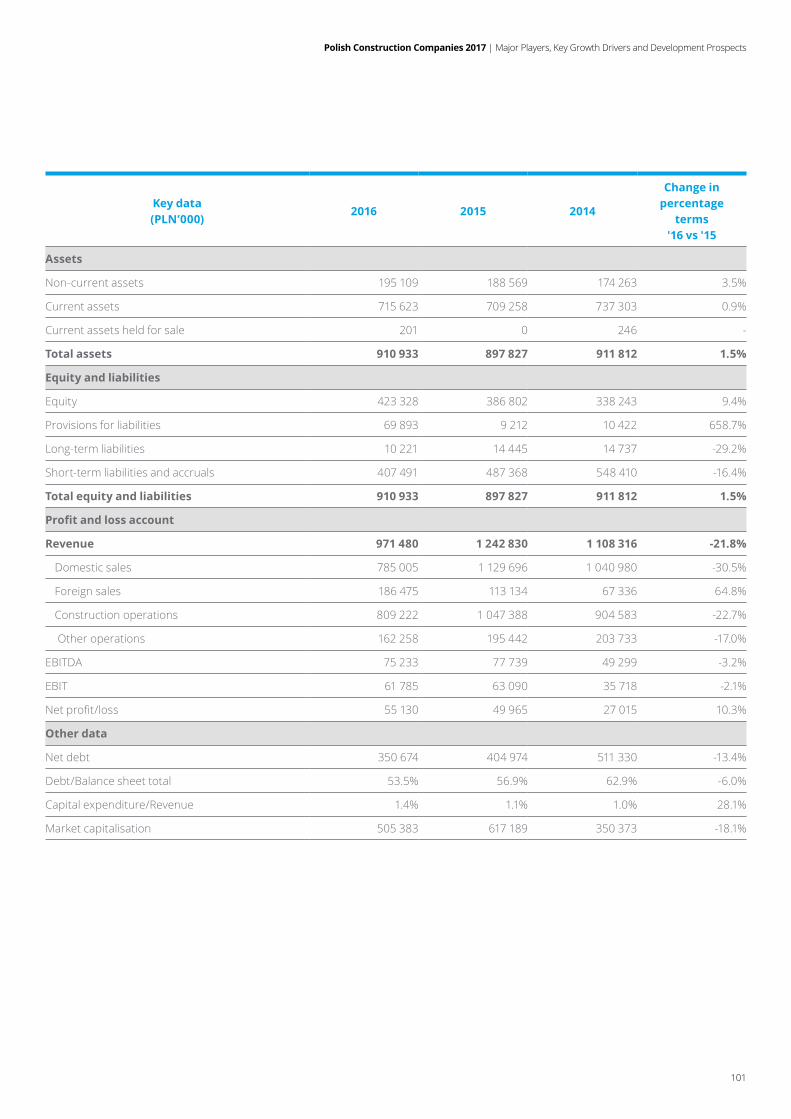

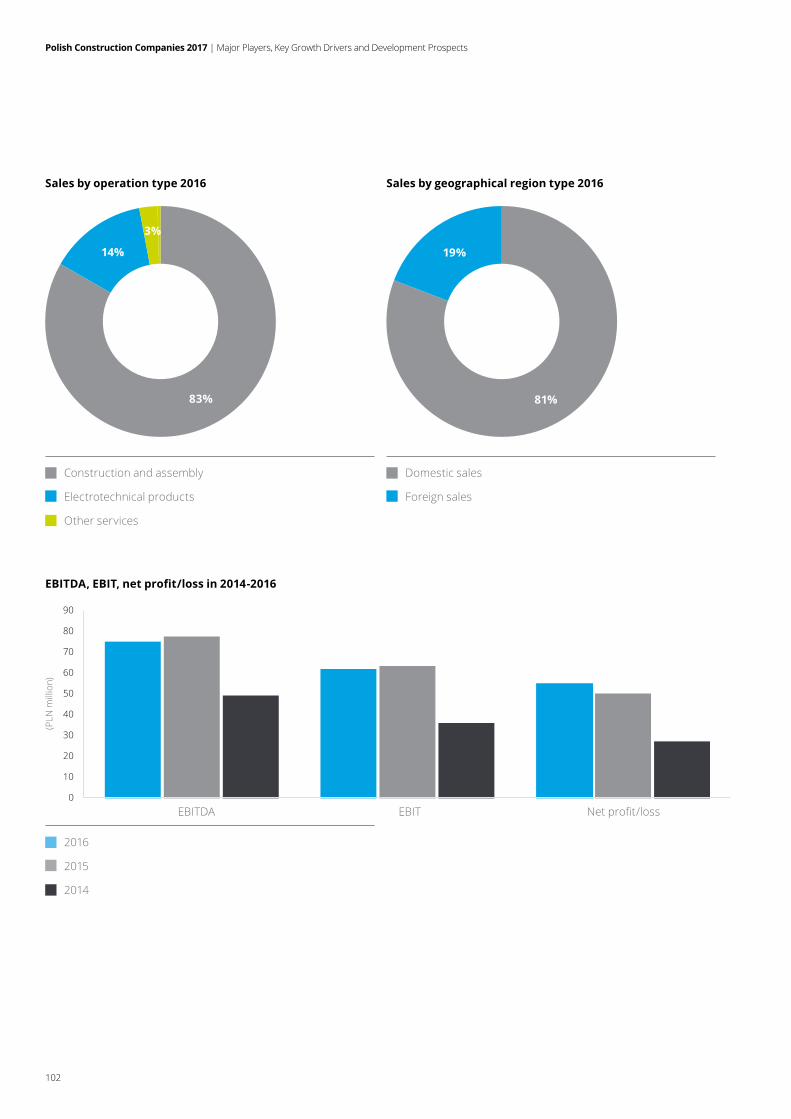

11 Elektrobudowa Group 971 480 1 242 830 -271 350 -21.8%

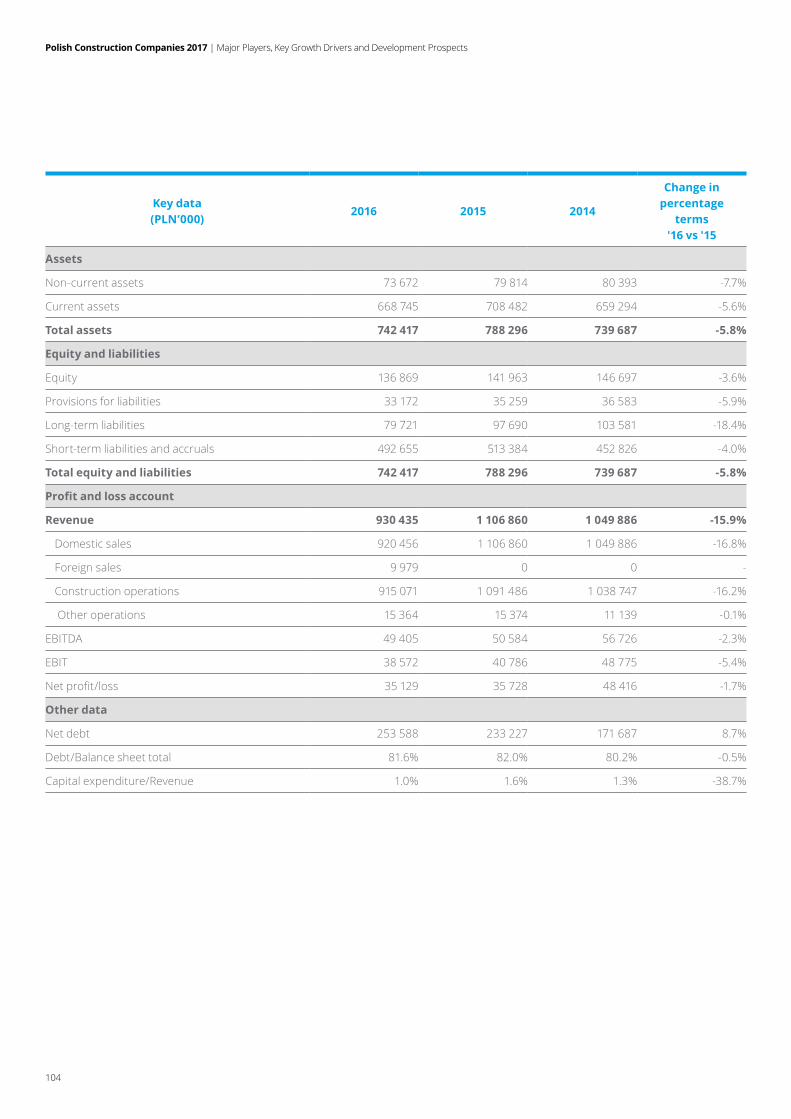

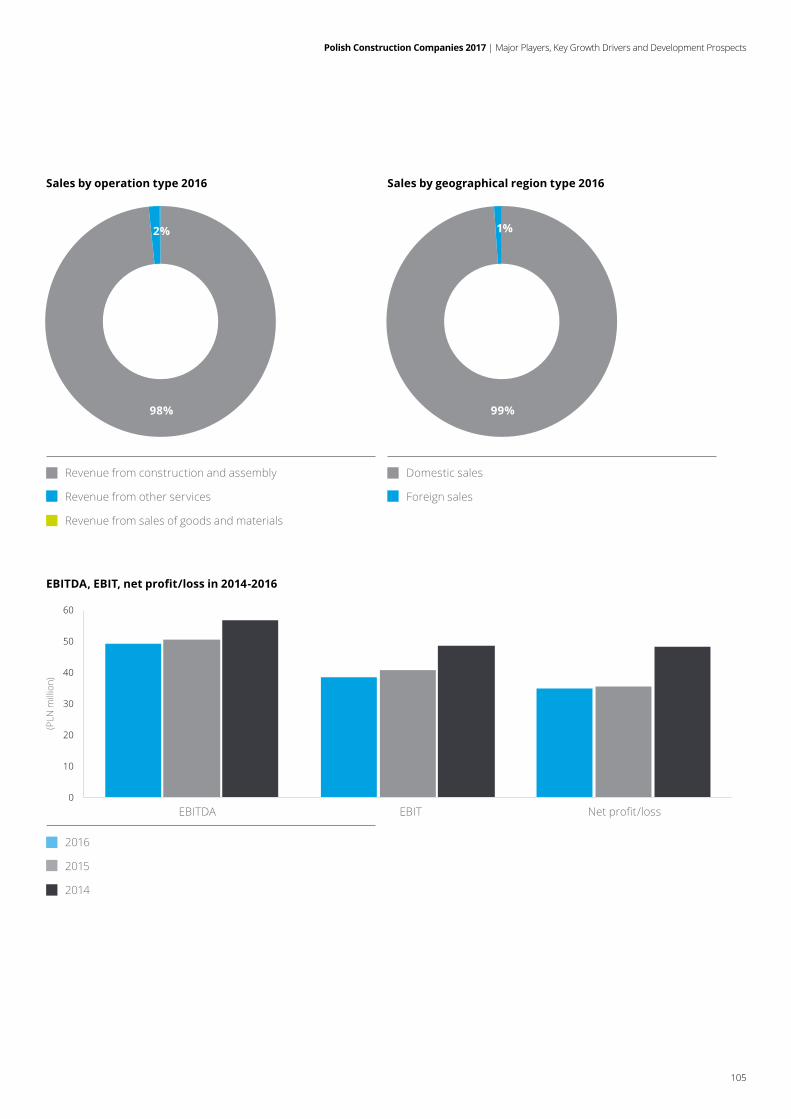

12 Warbud S.A. 930 435 1 106 860 -176 425 -15.9%

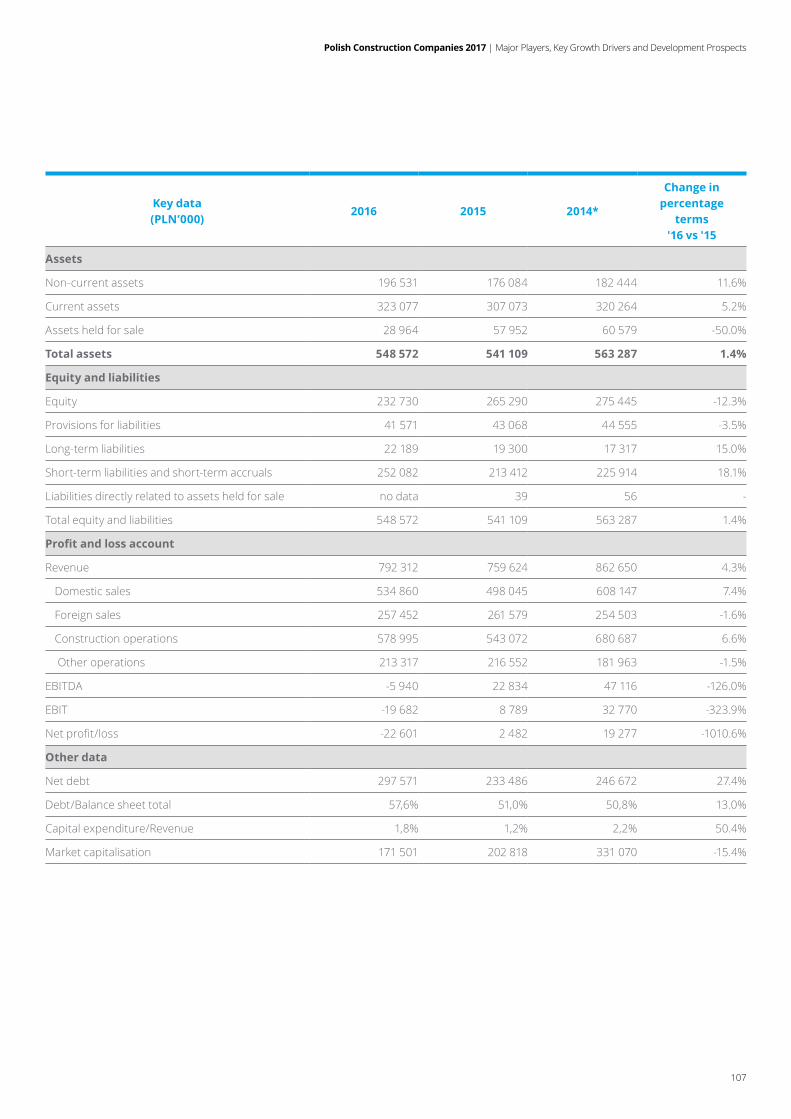

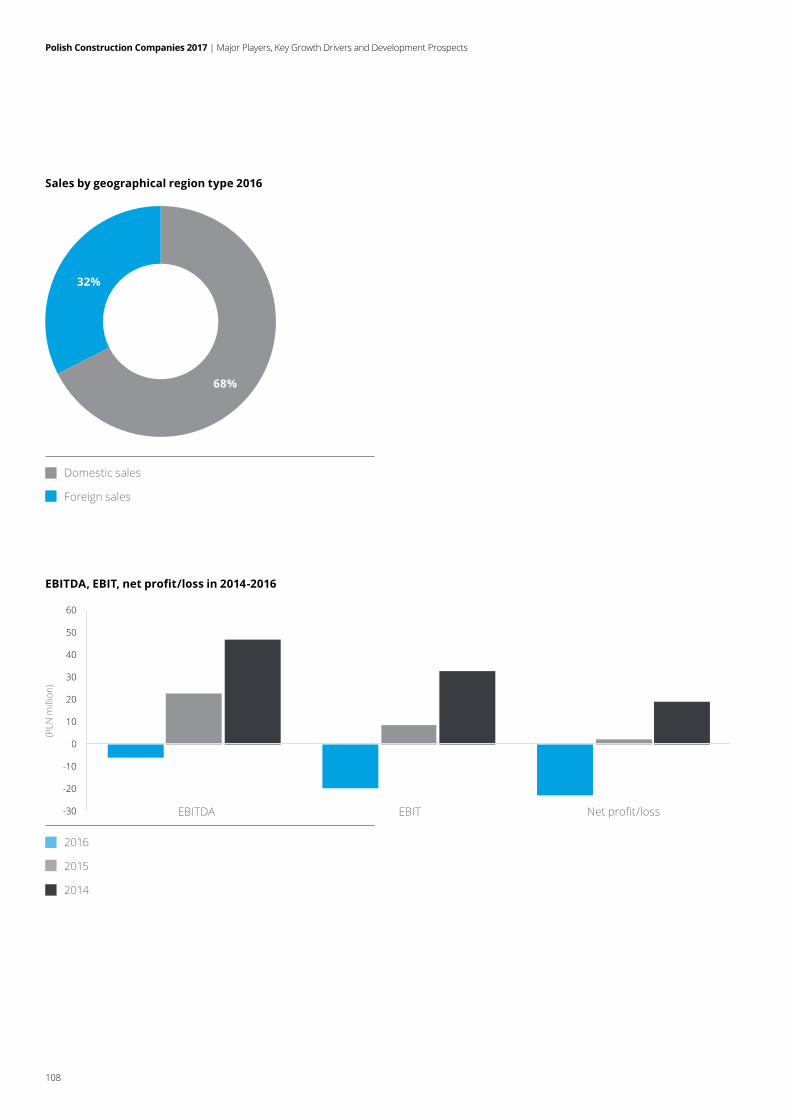

13 Mostostal Zabrze Group 792 312 759 624 32 688 4.3%

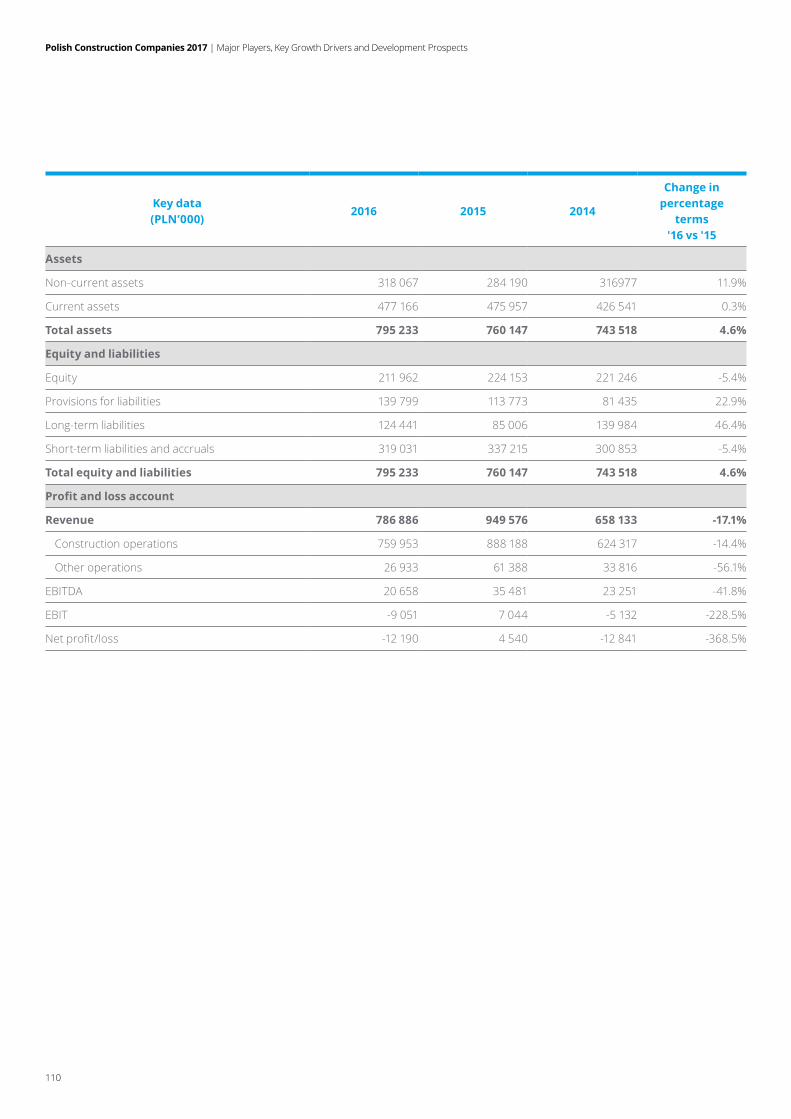

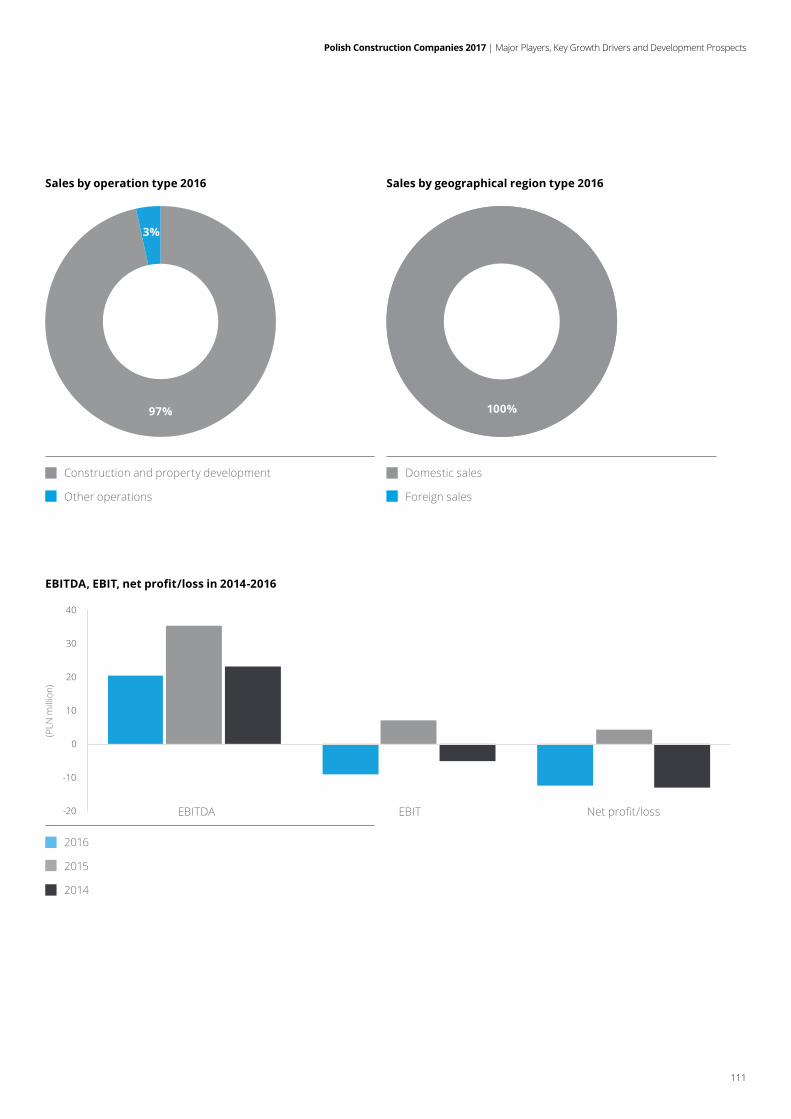

14 Mota - Engil Central Europe S.A. 786 886 949 576 -162 690 -17.1%

15 Mirbud Group 773 993 760 816 13 177 1.7%

Total 28 632 894 29 436 505 -803 611 -2.7%

Average 1 908 860 1 962 434 -53 574 -2.7%

Note: This analysis does not take account of the revenue generated by foreign branches of construction companies operating in Poland or that of special purpose vehicles established to carry out specific projects as part of consortia, as their revenue is included in the revenue of the consortium members.

Source: Financial statements of the reviewed companies for 2015 -2016

New in the ranking Increase Decrease No change

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

9

Strabag Group and Skanska S.A. have seen the most substantial revenue decrease, by PLN 637 million and PLN 424 million, respectively. Elektrobudowa Group has experienced a slightly smaller drop (by PLN 271 million), but the most substantial percentage one among those ranked (by 22%). Mota Engil Central Europe and Warbud also saw revenue drops in excess of 15% (by 17% and 16%, respectively).

The current year ranking includes two new entities,whichjoinedthegroupofthefifteenlargest construction businesses in 2016

following a substantial increase in the scale of their operations

in Poland: Mostostal Zabrze Group and Mirbud Group (with revenue for 2016 of PLN 792 million and PLN 774 million, respectively).

In 2014 and 2015 we observed a favourable turn on the construction market. Revenue of the sector companies increased as a result of large infrastructural projects being carriedoutunderthefirstEUperspective.The revenue stagnation observed in 2016 resulted mostly from delays in new

public procurement procedures regarding infrastructure to be performed under the new 2014-2020

EUfinancialperspective.Basedontheranking, it is clear that certain entities had problemswithfillingtheircontractportfolio.Additionally, it is important to note that new projects are often implemented under the “design and construct” approach, therefore even if a public procurement procedure is openedandfinalized,constructionwork(i.e.actual revenue generation) will commence nine to 18 months of the contract date.

Chart 1.1: Change in average revenue of the ranked companies between 2011 and 2016 (PLN ‘000)

Based on previous editions of reports presenting the largest construction companies in Poland (Deloitte reports: Polish Construction Companies 2011-2016)

-20%

-23%

7%5%

-3%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

2012 2013 2014 2015 2016

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

10

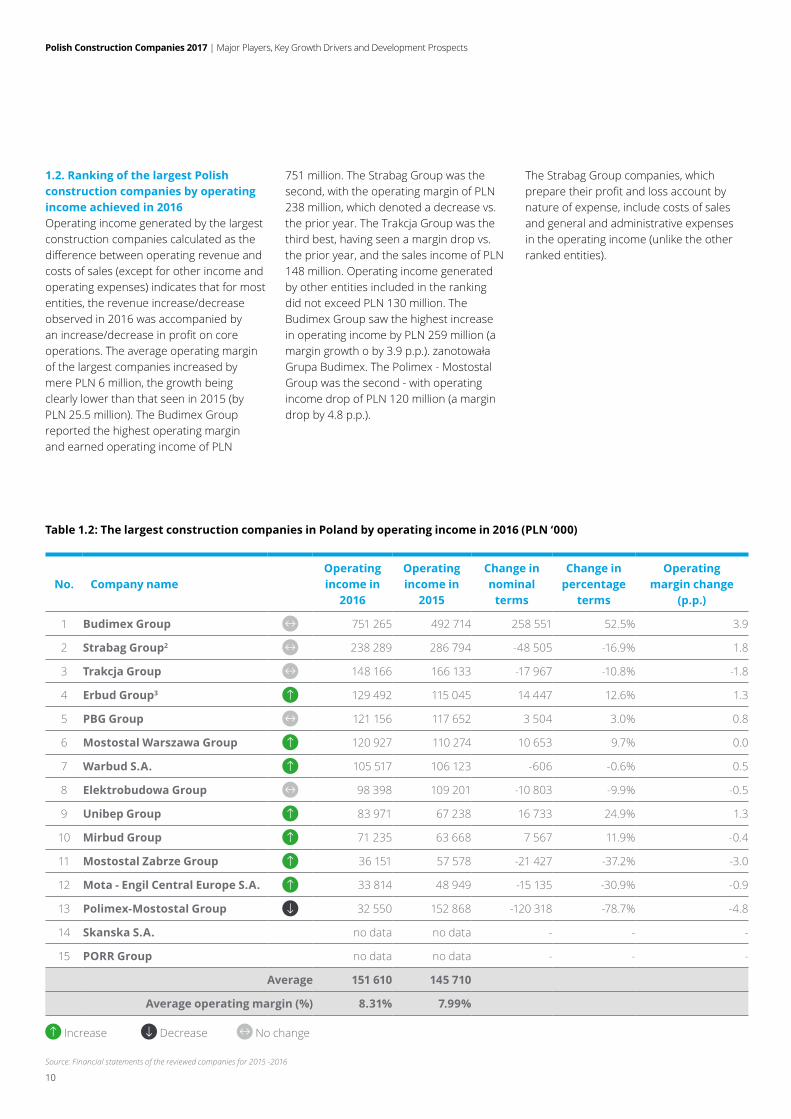

1.2. Ranking of the largest Polish construction companies by operating income achieved in 2016Operating income generated by the largest construction companies calculated as the differencebetweenoperatingrevenueandcosts of sales (except for other income and operating expenses) indicates that for most entities, the revenue increase/decrease observed in 2016 was accompanied by anincrease/decreaseinprofitoncoreoperations. The average operating margin of the largest companies increased by mere PLN 6 million, the growth being clearly lower than that seen in 2015 (by PLN 25.5 million). The Budimex Group reported the highest operating margin and earned operating income of PLN

751 million. The Strabag Group was the second, with the operating margin of PLN 238 million, which denoted a decrease vs. the prior year. The Trakcja Group was the third best, having seen a margin drop vs. the prior year, and the sales income of PLN 148 million. Operating income generated by other entities included in the ranking did not exceed PLN 130 million. The Budimex Group saw the highest increase in operating income by PLN 259 million (a margingrowthoby3.9p.p.).zanotowałaGrupa Budimex. The Polimex - Mostostal Group was the second - with operating income drop of PLN 120 million (a margin drop by 4.8 p.p.).

The Strabag Group companies, which preparetheirprofitandlossaccountbynature of expense, include costs of sales and general and administrative expenses in the operating income (unlike the other ranked entities).

Table 1.2: The largest construction companies in Poland by operating income in 2016 (PLN ‘000)

No. Company nameOperating income in

2016

Operating income in

2015

Change in nominal

terms

Change in percentage

terms

Operating margin change

(p.p.)

1 Budimex Group 751 265 492 714 258 551 52.5% 3.9

2 Strabag Group2 238 289 286 794 -48 505 -16.9% 1.8

3 Trakcja Group 148 166 166 133 -17 967 -10.8% -1.8

4 Erbud Group3 129 492 115 045 14 447 12.6% 1.3

5 PBG Group 121 156 117 652 3 504 3.0% 0.8

6 Mostostal Warszawa Group 120 927 110 274 10 653 9.7% 0.0

7 Warbud S.A. 105 517 106 123 -606 -0.6% 0.5

8 Elektrobudowa Group 98 398 109 201 -10 803 -9.9% -0.5

9 Unibep Group 83 971 67 238 16 733 24.9% 1.3

10 Mirbud Group 71 235 63 668 7 567 11.9% -0.4

11 Mostostal Zabrze Group 36 151 57 578 -21 427 -37.2% -3.0

12 Mota - Engil Central Europe S.A. 33 814 48 949 -15 135 -30.9% -0.9

13 Polimex-Mostostal Group 32 550 152 868 -120 318 -78.7% -4.8

14 Skanska S.A. no data no data - - -

15 PORR Group no data no data - - -

Average 151 610 145 710

Average operating margin (%) 8.31% 7.99%

Increase Decrease No change

Source: Financial statements of the reviewed companies for 2015 -2016

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

11

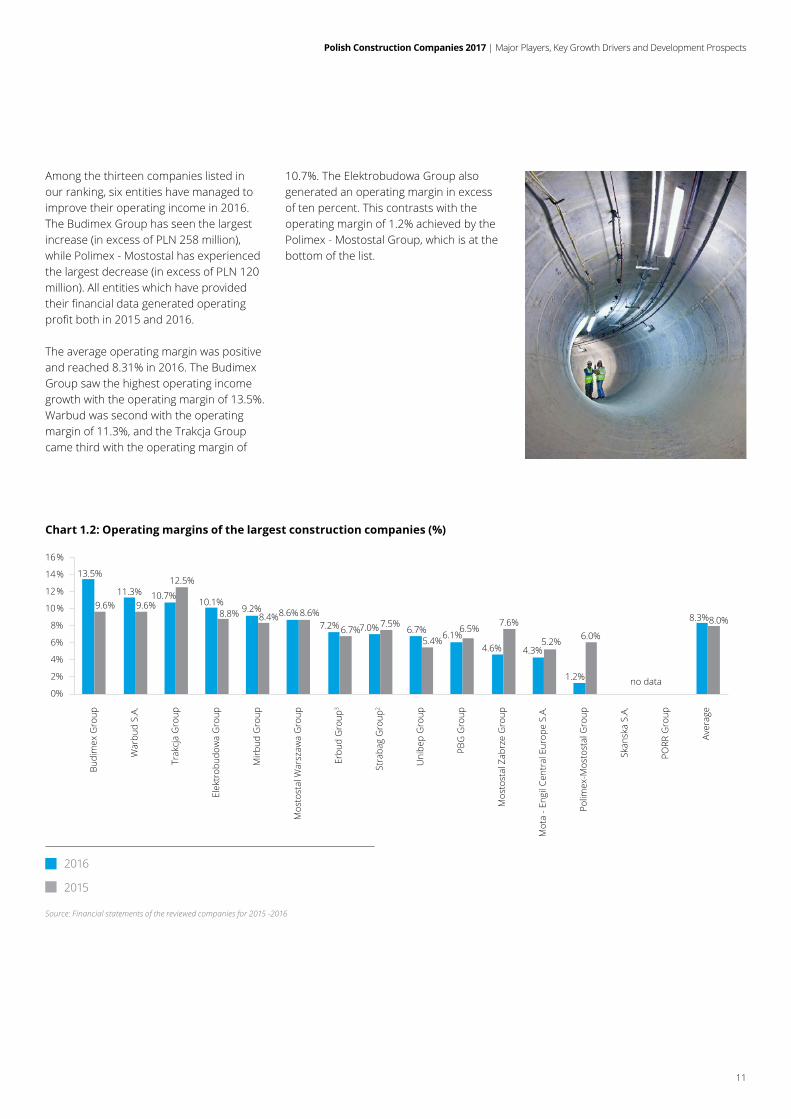

Among the thirteen companies listed in our ranking, six entities have managed to improve their operating income in 2016. The Budimex Group has seen the largest increase (in excess of PLN 258 million), while Polimex - Mostostal has experienced the largest decrease (in excess of PLN 120 million). All entities which have provided theirfinancialdatageneratedoperatingprofitbothin2015and2016.

The average operating margin was positive and reached 8.31% in 2016. The Budimex Group saw the highest operating income growth with the operating margin of 13.5%. Warbud was second with the operating margin of 11.3%, and the Trakcja Group came third with the operating margin of

10.7%. The Elektrobudowa Group also generated an operating margin in excess of ten percent. This contrasts with the operating margin of 1.2% achieved by the Polimex - Mostostal Group, which is at the bottom of the list.

Chart 1.2: Operating margins of the largest construction companies (%)

Source: Financial statements of the reviewed companies for 2015 -2016

2016

2015

13.5%

11.3% 10.7%10.1%

9.2% 8.6%7.2% 7.0% 6.7% 6.1%

4.6% 4.3%

1.2%

8.3%9.6% 9.6%

12.5%

8.8% 8.4% 8.6%

6.7%7.5%

5.4%6.5%

7.6%

5.2% 6.0%

8.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

Budi

mex

Gro

up

War

bud

S.A.

Trak

cja

Gro

up

Elek

trob

udow

a G

roup

Mirb

ud G

roup

Mos

tost

al W

arsz

awa

Gro

up

Erbu

d G

roup

3

Stra

bag

Gro

up2

Uni

bep

Gro

up

PBG

Gro

up

Mos

tost

al Z

abrz

e G

roup

Mot

a - E

ngil

Cent

ral E

urop

e S.

A.

Polim

ex-M

osto

stal

Gro

up

Skan

ska

S.A.

PORR

Gro

up

Aver

age

no data

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

12

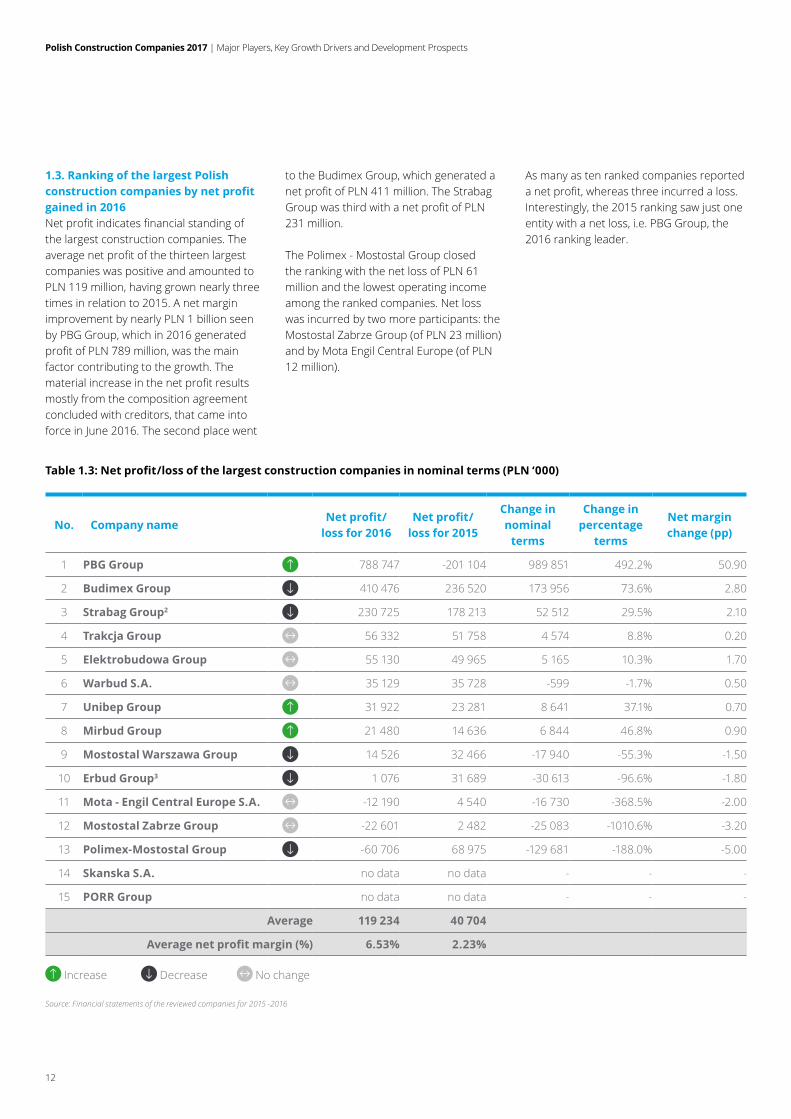

1.3. Ranking of the largest Polish construction companies by net profit gained in 2016 Netprofitindicatesfinancialstandingofthe largest construction companies. The averagenetprofitofthethirteenlargestcompanies was positive and amounted to PLN 119 million, having grown nearly three times in relation to 2015. A net margin improvement by nearly PLN 1 billion seen by PBG Group, which in 2016 generated profitofPLN789million,wasthemainfactor contributing to the growth. The materialincreaseinthenetprofitresultsmostly from the composition agreement concluded with creditors, that came into force in June 2016. The second place went

to the Budimex Group, which generated a netprofitofPLN411million.TheStrabagGroupwasthirdwithanetprofitofPLN231 million.

The Polimex - Mostostal Group closed the ranking with the net loss of PLN 61 million and the lowest operating income among the ranked companies. Net loss was incurred by two more participants: the Mostostal Zabrze Group (of PLN 23 million) and by Mota Engil Central Europe (of PLN 12 million).

As many as ten ranked companies reported anetprofit,whereasthreeincurredaloss.Interestingly, the 2015 ranking saw just one entity with a net loss, i.e. PBG Group, the 2016 ranking leader.

Table 1.3: Net profit/loss of the largest construction companies in nominal terms (PLN ‘000)

No. Company nameNet profit/

loss for 2016Net profit/

loss for 2015

Change in nominal

terms

Change in percentage

terms

Net margin change (pp)

1 PBG Group 788 747 -201 104 989 851 492.2% 50.90

2 Budimex Group 410 476 236 520 173 956 73.6% 2.80

3 Strabag Group2 230 725 178 213 52 512 29.5% 2.10

4 Trakcja Group 56 332 51 758 4 574 8.8% 0.20

5 Elektrobudowa Group 55 130 49 965 5 165 10.3% 1.70

6 Warbud S.A. 35 129 35 728 -599 -1.7% 0.50

7 Unibep Group 31 922 23 281 8 641 37.1% 0.70

8 Mirbud Group 21 480 14 636 6 844 46.8% 0.90

9 Mostostal Warszawa Group 14 526 32 466 -17 940 -55.3% -1.50

10 Erbud Group3 1 076 31 689 -30 613 -96.6% -1.80

11 Mota - Engil Central Europe S.A. -12 190 4 540 -16 730 -368.5% -2.00

12 Mostostal Zabrze Group -22 601 2 482 -25 083 -1010.6% -3.20

13 Polimex-Mostostal Group -60 706 68 975 -129 681 -188.0% -5.00

14 Skanska S.A. no data no data - - -

15 PORR Group no data no data - - -

Average 119 234 40 704

Average net profit margin (%) 6.53% 2.23%

Increase Decrease No change

Source: Financial statements of the reviewed companies for 2015 -2016

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

13

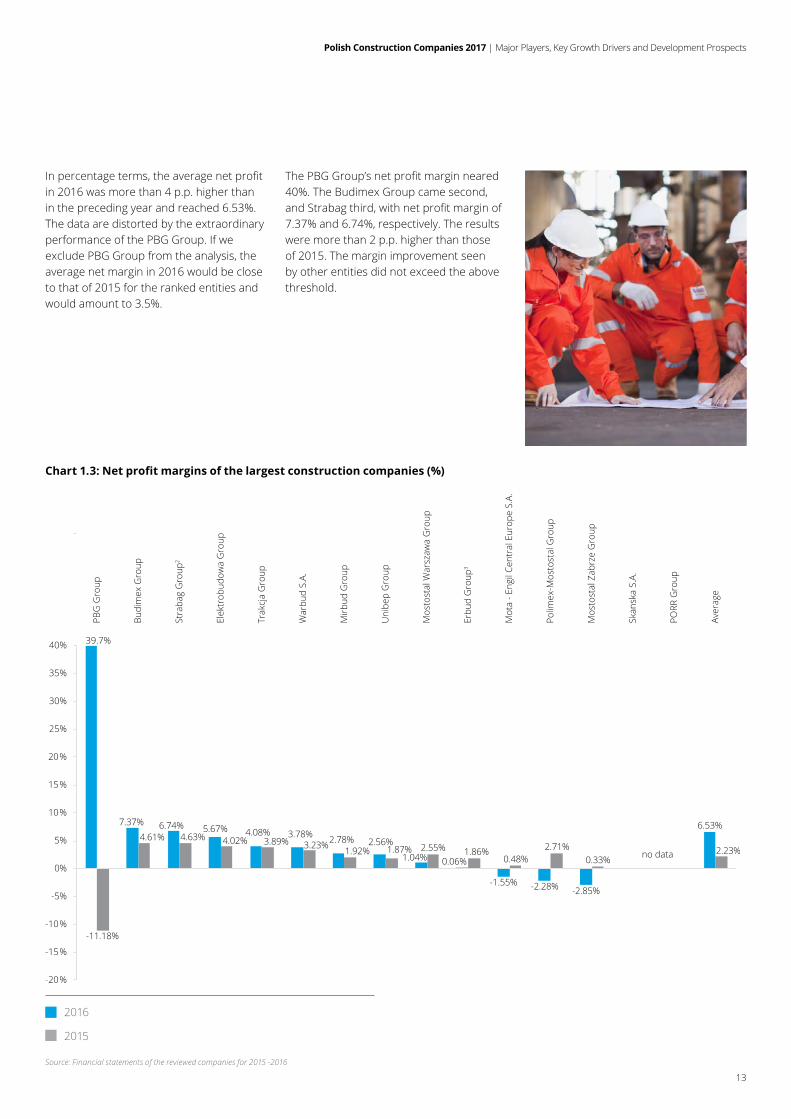

Inpercentageterms,theaveragenetprofitin 2016 was more than 4 p.p. higher than in the preceding year and reached 6.53%. The data are distorted by the extraordinary performance of the PBG Group. If we exclude PBG Group from the analysis, the average net margin in 2016 would be close to that of 2015 for the ranked entities and would amount to 3.5%.

ThePBGGroup’snetprofitmarginneared40%. The Budimex Group came second, andStrabagthird,withnetprofitmarginof7.37% and 6.74%, respectively. The results were more than 2 p.p. higher than those of 2015. The margin improvement seen by other entities did not exceed the above threshold.

Chart 1.3: Net profit margins of the largest construction companies (%)

2016

2015

Source: Financial statements of the reviewed companies for 2015 -2016

7.37% 6.74% 5.67% 4.08% 3.78% 2.78% 2.56%

1.04% 0.06%

-1.55% -2.28% -2.85%

6.53%

-11.18%

4.61% 4.63% 4.02% 3.89% 3.23% 1.92% 1.87% 2.55% 1.86%0.48%

2.71%0.33%

2.23%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

PBG

Gro

up

Budi

mex

Gro

up

Stra

bag

Gro

up2

Elek

trob

udow

a G

roup

Trak

cja

Gro

up

War

bud

S.A.

Mirb

ud G

roup

Uni

bep

Gro

up

Mos

tost

al W

arsz

awa

Gro

up

Erbu

d G

roup

3

Mot

a - E

ngil

Cent

ral E

urop

e S.

A.

Polim

ex-M

osto

stal

Gro

up

Mos

tost

al Z

abrz

e G

roup

Skan

ska

S.A.

PORR

Gro

up

Aver

age

no data

25%

30%

35%

40% 39.7%

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

14

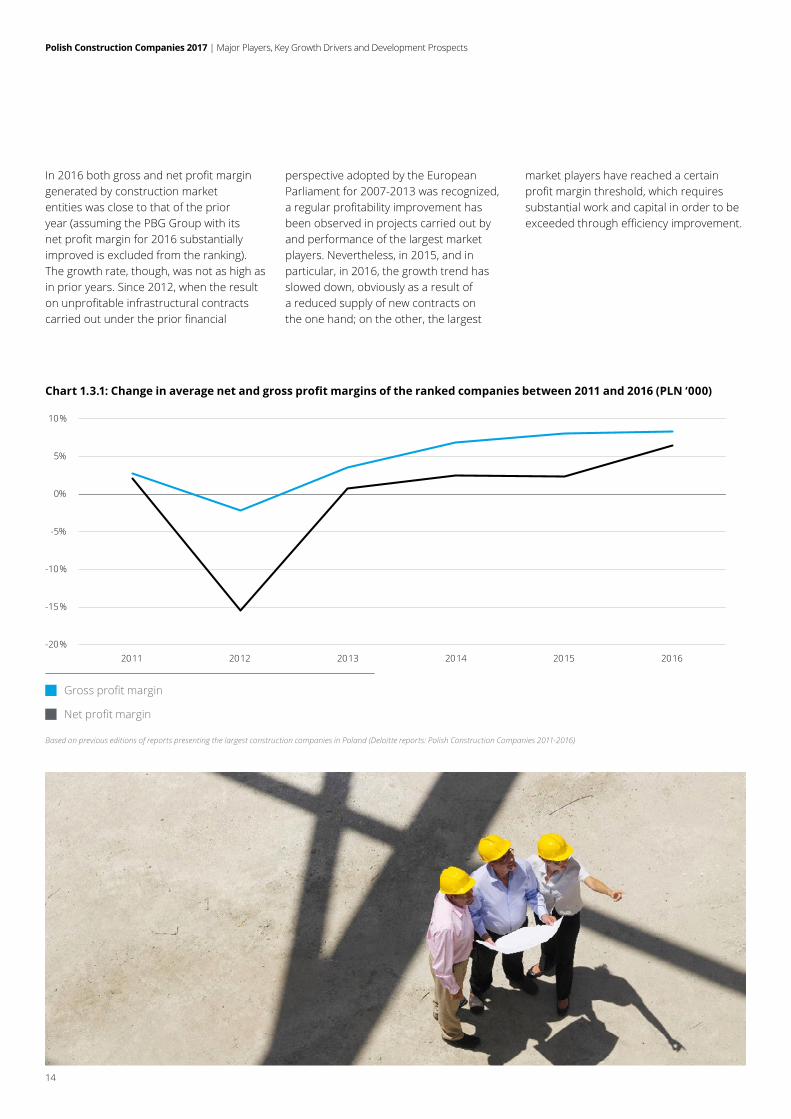

In2016bothgrossandnetprofitmargingenerated by construction market entities was close to that of the prior year (assuming the PBG Group with its netprofitmarginfor2016substantiallyimproved is excluded from the ranking). The growth rate, though, was not as high as in prior years. Since 2012, when the result onunprofitableinfrastructuralcontractscarriedoutunderthepriorfinancial

perspective adopted by the European Parliament for 2007-2013 was recognized, aregularprofitabilityimprovementhasbeen observed in projects carried out by and performance of the largest market players. Nevertheless, in 2015, and in particular, in 2016, the growth trend has slowed down, obviously as a result of a reduced supply of new contracts on the one hand; on the other, the largest

market players have reached a certain profitmarginthreshold,whichrequiressubstantial work and capital in order to be exceededthroughefficiencyimprovement.

Based on previous editions of reports presenting the largest construction companies in Poland (Deloitte reports: Polish Construction Companies 2011-2016)

Chart 1.3.1: Change in average net and gross profit margins of the ranked companies between 2011 and 2016 (PLN ‘000)

Grossprofitmargin

Netprofitmargin

-20%

-15%

-10%

-5%

0%

5%

10%

2011 2012 2013 2014 2015 2016

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

15

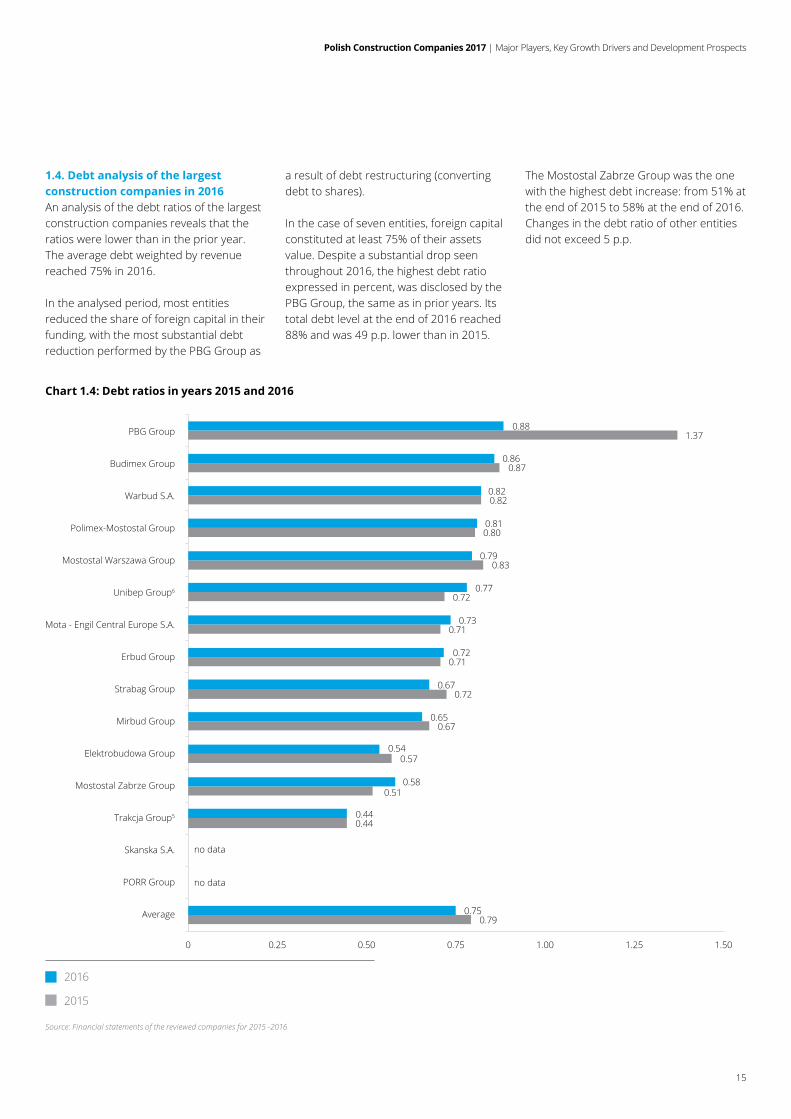

1.4. Debt analysis of the largest construction companies in 2016 An analysis of the debt ratios of the largest construction companies reveals that the ratios were lower than in the prior year. The average debt weighted by revenue reached 75% in 2016.

In the analysed period, most entities reduced the share of foreign capital in their funding, with the most substantial debt reduction performed by the PBG Group as

a result of debt restructuring (converting debt to shares).

In the case of seven entities, foreign capital constituted at least 75% of their assets value. Despite a substantial drop seen throughout 2016, the highest debt ratio expressed in percent, was disclosed by the PBG Group, the same as in prior years. Its total debt level at the end of 2016 reached 88% and was 49 p.p. lower than in 2015.

The Mostostal Zabrze Group was the one with the highest debt increase: from 51% at the end of 2015 to 58% at the end of 2016. Changes in the debt ratio of other entities did not exceed 5 p.p.

Chart 1.4: Debt ratios in years 2015 and 2016

2016

2015

Source: Financial statements of the reviewed companies for 2015 -2016

0.79

0.44

0.51

0.57

0.67

0.72

0.71

0.71

0.72

0.83

0.80

0.82

0.87

1.37

0.75

no data

0.44

0.58

0.54

0.65

0.67

0.72

0.73

0.77

0.79

0.81

0.82

0.86

0.88

0 0.25 0.50 0.75 1.00 1.25 1.50

PBG Group

Budimex Group

Warbud S.A.

Polimex-Mostostal Group

Mostostal Warszawa Group

Unibep Group6

Mota - Engil Central Europe S.A.

Erbud Group

Strabag Group

Mirbud Group

Elektrobudowa Group

Mostostal Zabrze Group

Trakcja Group5

Skanska S.A.

PORR Group

Average

no data

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

16

As in the prior year, the debt ratio of the Trakcja Group was the lowest among the ranked companies and reached the level of 44%. At the end of 2016, in the largest construction companies, the average debt ratio weighed with revenue dropped by 4 p.p. vs. the prior year.

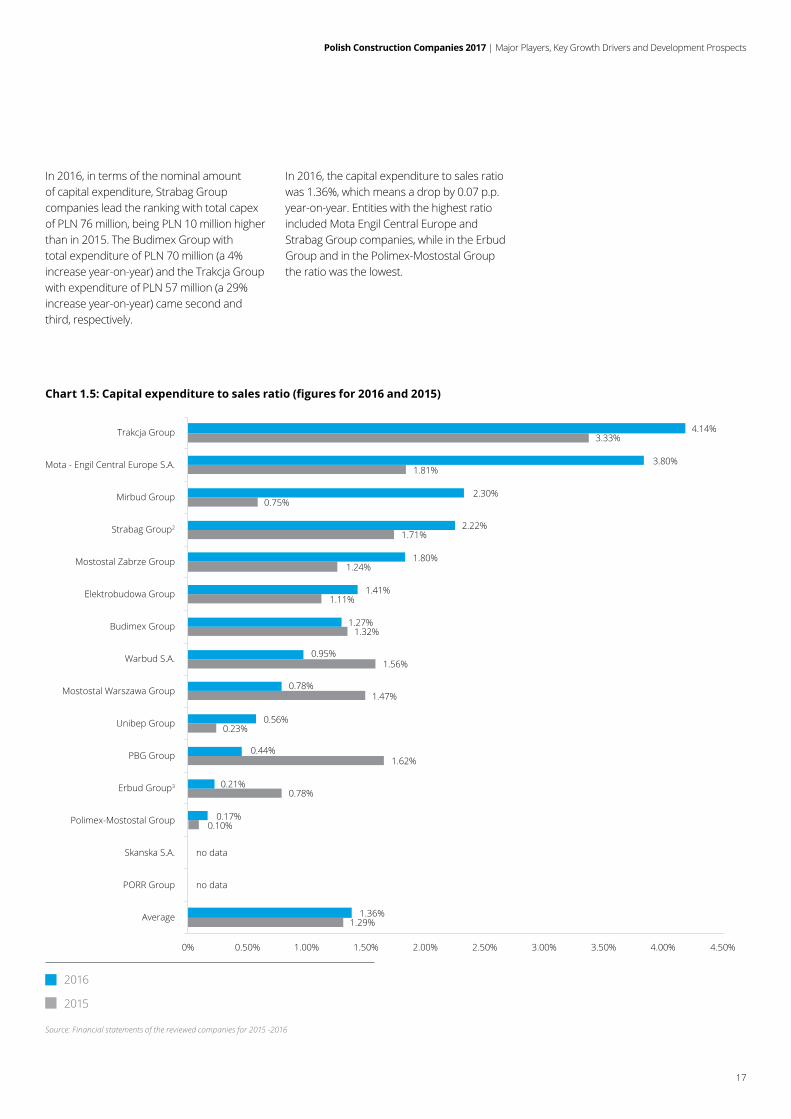

1.5. Relation of capital expenditure to sales ratio of the largest construction companies in 2016Companies operating in the construction sector usually demonstrate a low capital expenditure to sales ratio due to high sales volumes and relatively low capital expenditure necessary to provide construction services. In 2016 the total capital expenditure of the largest market players exceeded PLN 320 million and were 5% higher than in 2015.

Table 1.5: Capital expenditure of the fifteen largest construction companies in nominal terms (PLN ‘000)

No. Company nameCapital

expenditure in 2016

Capital expenditure in

2015

Change in nominal terms

Change in percentage

terms

1 Strabag Group 75 956 65 830 10 126 15%

2 Budimex Group 70 898 67 915 2 983 4%

3 Trakcja Group 57 153 44 309 12 844 29%

4 Mota - Engil Central Europe S.A. 29 829 17 182 12 647 74%

5 Mirbud Group 17 821 4 353 13 468 309%

6 Mostostal Zabrze Group 14 300 9 418 4 882 52%

7 Elektrobudowa Group 13 694 13 838 -144 -1%

8 Mostostal Warszawa Group 10 898 18 757 -7 859 -42%

9 Warbud S.A. 8 876 17 220 -8 344 -48%

10 PBG Group 8 834 29 214 -20 380 -70%

11 Unibep Group 6 971 2 825 4 146 147%

12 Polimex-Mostostal Group 4 484 2 480 2 004 81%

13 Erbud Group 3 800 13 318 -9 518 -71%

14 Skanska S.A. no data no data - -

15 PORR Group no data no data - -

Total 323 514 306 659 16 855 5%

Average 24 886 23 589 1 297 5%

Source: Financial statements of the reviewed companies for 2015 -2016

Increase Decrease No change

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

17

In 2016, in terms of the nominal amount of capital expenditure, Strabag Group companies lead the ranking with total capex of PLN 76 million, being PLN 10 million higherthan in 2015. The Budimex Group with total expenditure of PLN 70 million (a 4% increase year-on-year) and the Trakcja Group with expenditure of PLN 57 million (a 29% increase year-on-year) came second and third, respectively.

In 2016, the capital expenditure to sales ratio was 1.36%, which means a drop by 0.07 p.p. year-on-year. Entities with the highest ratio included Mota Engil Central Europe and Strabag Group companies, while in the Erbud Group and in the Polimex-Mostostal Group the ratio was the lowest.

Chart 1.5: Capital expenditure to sales ratio (figures for 2016 and 2015)

2016

2015

Source: Financial statements of the reviewed companies for 2015 -2016

0.23%

1.47%

1.56%

1.32%

1.11%

1.29%

no data

no data

0.10%

0.78%

1.62%

1.24%

1.71%

0.75%

1.81%

3.33%

1.36%

0.17%

0.21%

0.44%

0.56%

0.78%

0.95%

1.27%

1.41%

1.80%

2.22%

2.30%

3.80%

4.14%

0% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 4.00%

Trakcja Group

Mota - Engil Central Europe S.A.

Mirbud Group

Strabag Group2

Mostostal Zabrze Group

Elektrobudowa Group

Budimex Group

Warbud S.A.

Mostostal Warszawa Group

Unibep Group

PBG Group

Erbud Group3

Polimex-Mostostal Group

Skanska S.A.

PORR Group

Average

4.50%

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

18

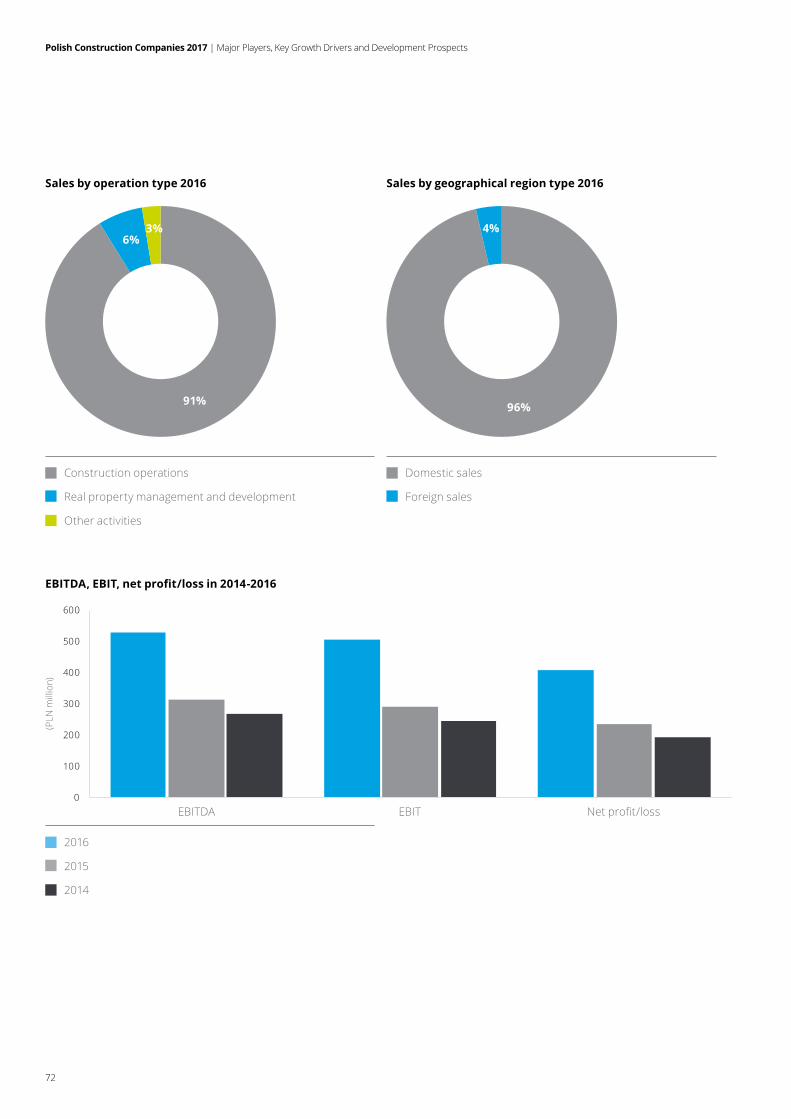

1.6. Geographical and generic structure of revenue earned by the largest construction companies

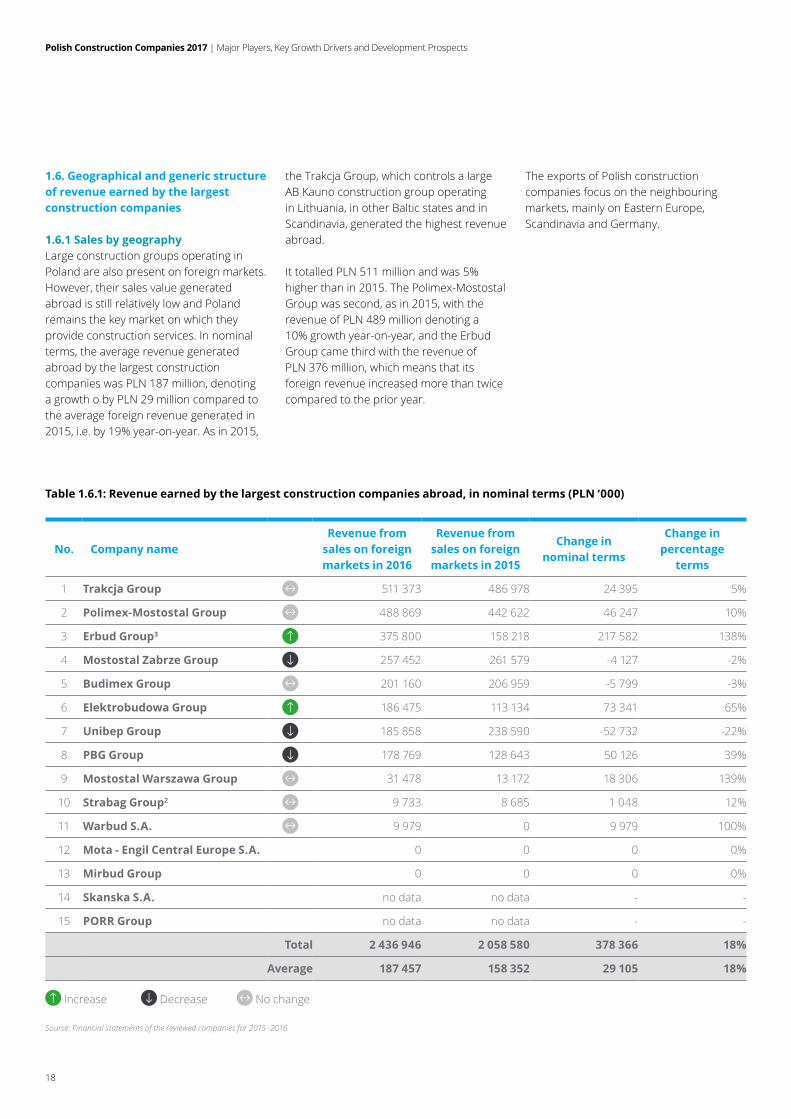

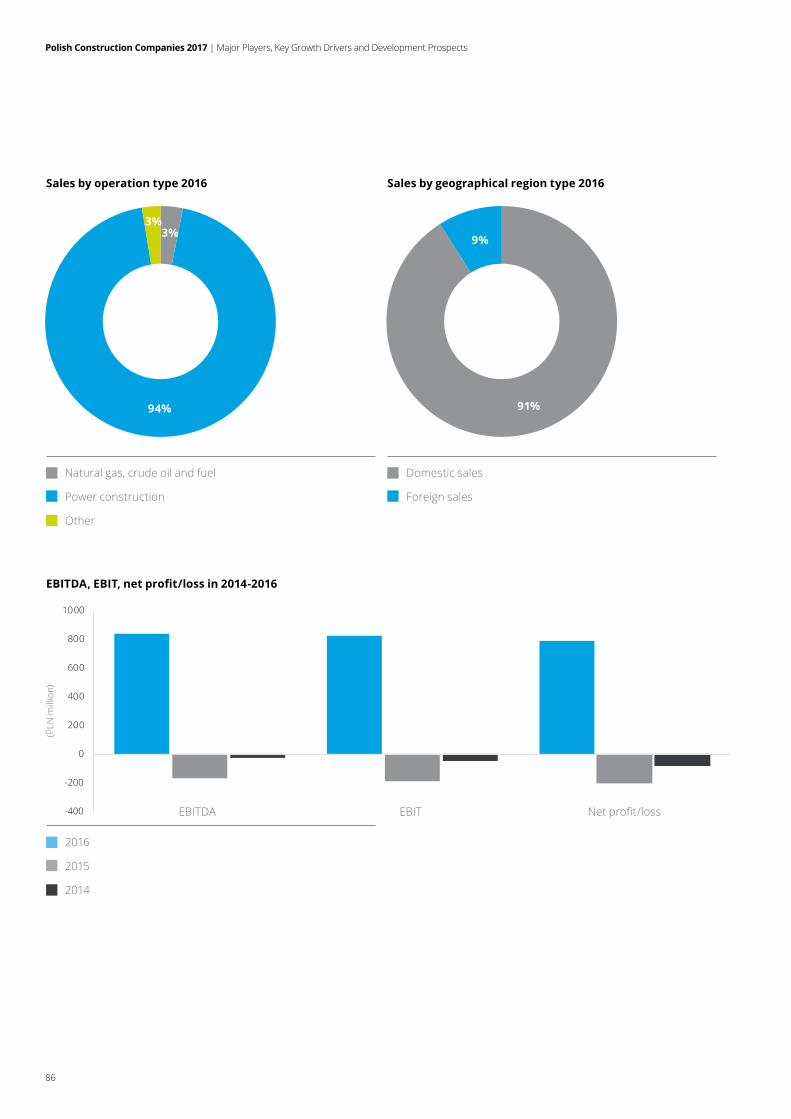

1.6.1 Sales by geography Large construction groups operating in Poland are also present on foreign markets. However, their sales value generated abroad is still relatively low and Poland remains the key market on which they provide construction services. In nominal terms, the average revenue generated abroad by the largest construction companies was PLN 187 million, denoting a growth o by PLN 29 million compared to the average foreign revenue generated in 2015, i.e. by 19% year-on-year. As in 2015,

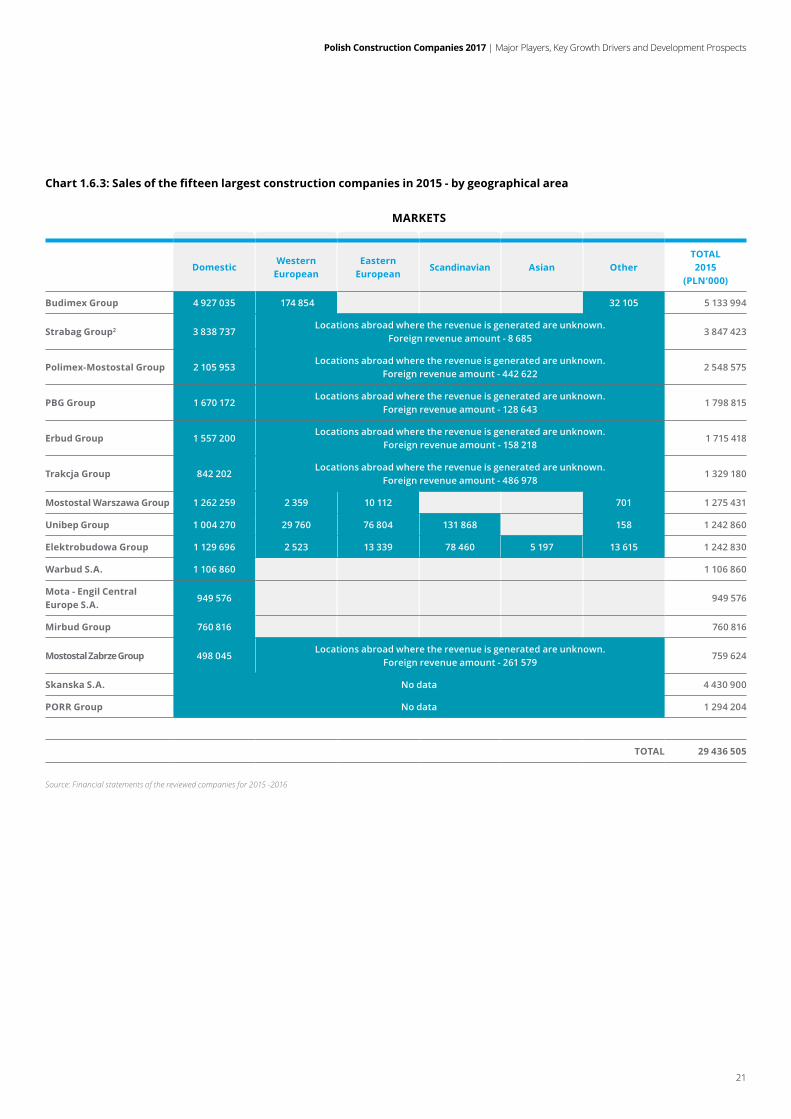

the Trakcja Group, which controls a large AB Kauno construction group operating in Lithuania, in other Baltic states and in Scandinavia, generated the highest revenue abroad.

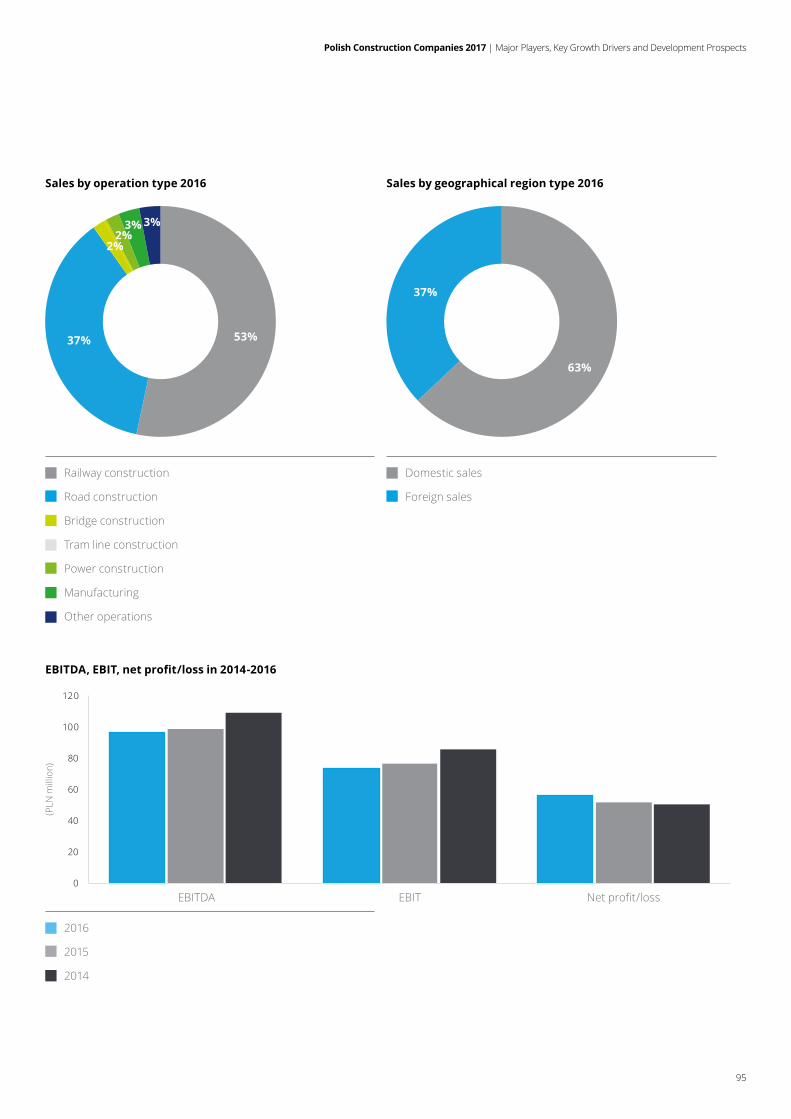

It totalled PLN 511 million and was 5% higher than in 2015. The Polimex-Mostostal Group was second, as in 2015, with the revenue of PLN 489 million denoting a 10% growth year-on-year, and the Erbud Group came third with the revenue of PLN 376 million, which means that its foreign revenue increased more than twice compared to the prior year.

The exports of Polish construction companies focus on the neighbouring markets, mainly on Eastern Europe, Scandinavia and Germany.

Table 1.6.1: Revenue earned by the largest construction companies abroad, in nominal terms (PLN ‘000)

No. Company nameRevenue from

sales on foreign markets in 2016

Revenue from sales on foreign markets in 2015

Change in nominal terms

Change in percentage

terms

1 Trakcja Group 511 373 486 978 24 395 5%

2 Polimex-Mostostal Group 488 869 442 622 46 247 10%

3 Erbud Group3 375 800 158 218 217 582 138%

4 Mostostal Zabrze Group 257 452 261 579 -4 127 -2%

5 Budimex Group 201 160 206 959 -5 799 -3%

6 Elektrobudowa Group 186 475 113 134 73 341 65%

7 Unibep Group 185 858 238 590 -52 732 -22%

8 PBG Group 178 769 128 643 50 126 39%

9 Mostostal Warszawa Group 31 478 13 172 18 306 139%

10 Strabag Group2 9 733 8 685 1 048 12%

11 Warbud S.A. 9 979 0 9 979 100%

12 Mota - Engil Central Europe S.A. 0 0 0 0%

13 Mirbud Group 0 0 0 0%

14 Skanska S.A. no data no data - -

15 PORR Group no data no data - -

Total 2 436 946 2 058 580 378 366 18%

Average 187 457 158 352 29 105 18%

Source: Financial statements of the reviewed companies for 2015 -2016

Increase Decrease No change

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

19

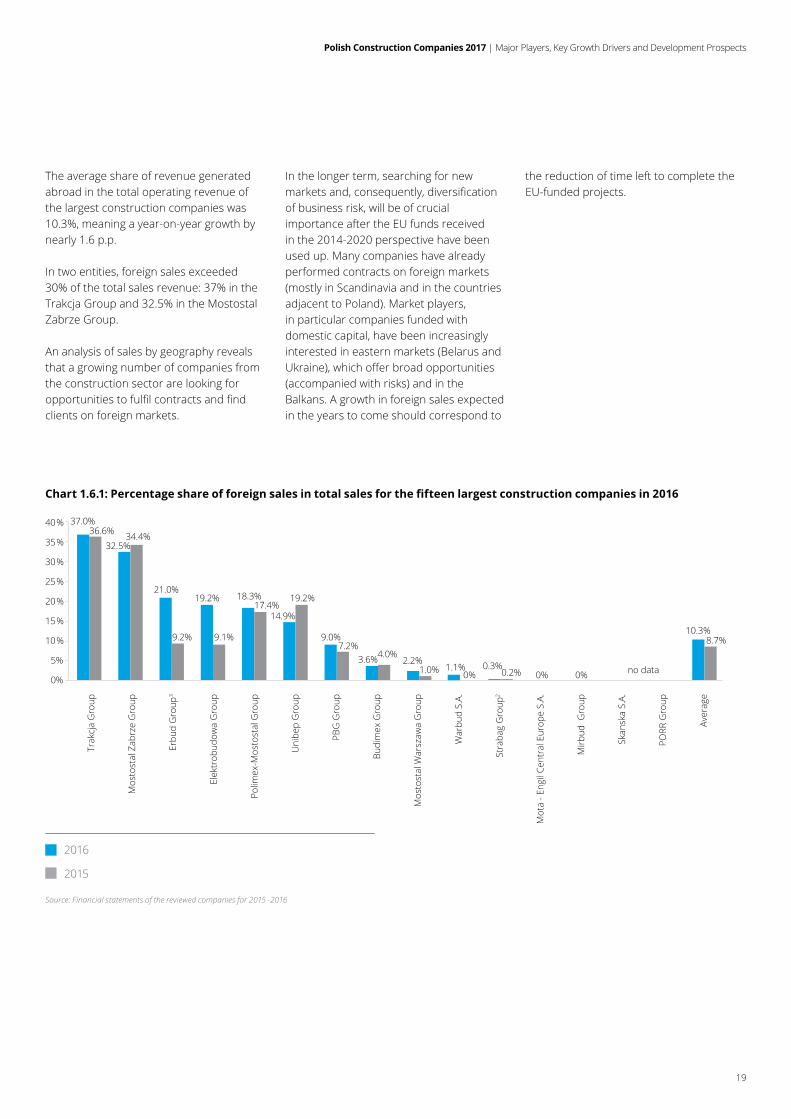

The average share of revenue generated abroad in the total operating revenue of the largest construction companies was 10.3%, meaning a year-on-year growth by nearly 1.6 p.p.

In two entities, foreign sales exceeded 30% of the total sales revenue: 37% in the Trakcja Group and 32.5% in the Mostostal Zabrze Group.

An analysis of sales by geography reveals that a growing number of companies from the construction sector are looking for opportunitiestofulfilcontractsandfindclients on foreign markets.

In the longer term, searching for new marketsand,consequently,diversificationof business risk, will be of crucial importance after the EU funds received in the 2014-2020 perspective have been used up. Many companies have already performed contracts on foreign markets (mostly in Scandinavia and in the countries adjacent to Poland). Market players, in particular companies funded with domestic capital, have been increasingly interested in eastern markets (Belarus and Ukraine),whichofferbroadopportunities(accompanied with risks) and in the Balkans. A growth in foreign sales expected in the years to come should correspond to

the reduction of time left to complete the EU-funded projects.

Chart 1.6.1: Percentage share of foreign sales in total sales for the fifteen largest construction companies in 2016

2016

2015

Source: Financial statements of the reviewed companies for 2015 -2016

37.0%

32.5%

21.0%19.2% 18.3%

14.9%

9.0%

3.6% 2.2% 0.3%0% 0%

10.3%

36.6% 34.4%

9.2% 9.1%

17.4%19.2%

7.2%4.0%

1.0% 1.1% 0.2% no data0%

5%

10%

15%

20%

25%

30%

35%

40%

Trak

cja

Gro

up

Mos

tost

al Z

abrz

e G

roup

Erbu

d G

roup

3

Elek

trob

udow

a G

roup

Polim

ex-M

osto

stal

Gro

up

Uni

bep

Gro

up

PBG

Gro

up

Budi

mex

Gro

up

Mos

tost

al W

arsz

awa

Gro

up

War

bud

S.A.

Stra

bag

Gro

up2

Mot

a - E

ngil

Cent

ral E

urop

e S.

A.

Mirb

ud G

roup

Skan

ska

S.A.

PORR

Gro

up

Aver

age

8.7%

0%

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

20

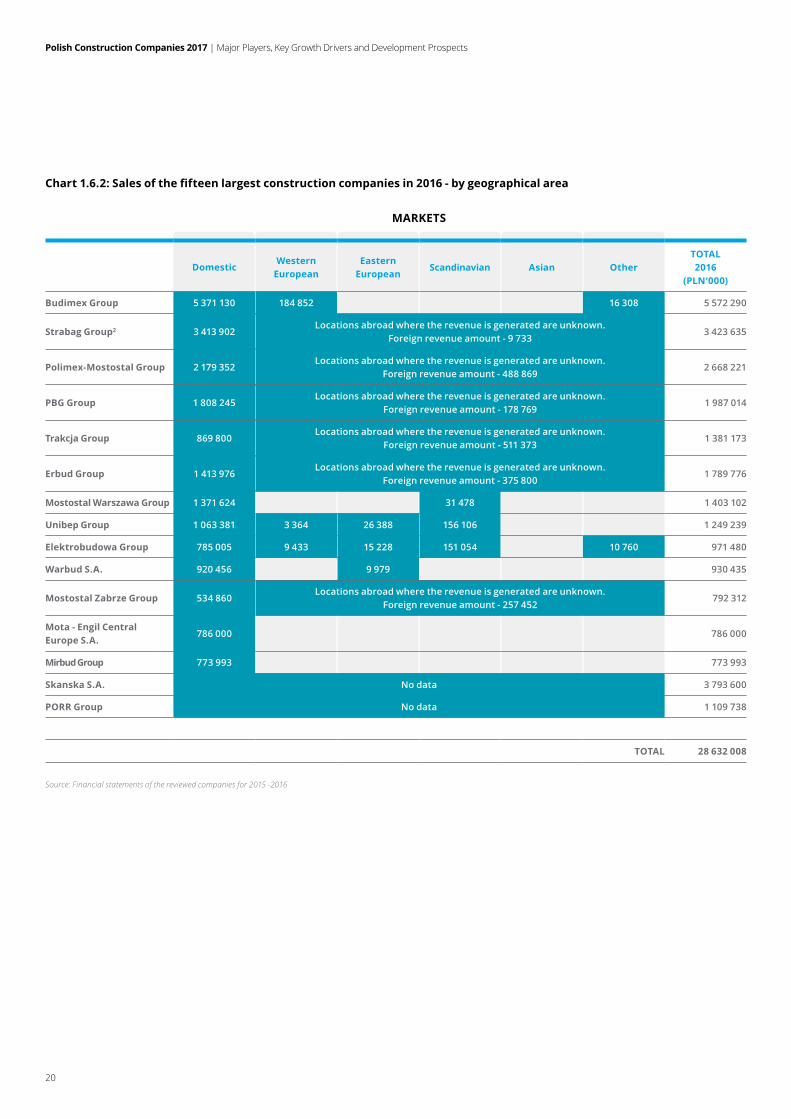

Chart 1.6.2: Sales of the fifteen largest construction companies in 2016 - by geographical area

Source: Financial statements of the reviewed companies for 2015 -2016

DomesticWestern

EuropeanEastern

EuropeanScandinavian Asian Other

TOTAL2016

(PLN‘000)

Budimex Group 5 371 130 184 852 16 308 5 572 290

Strabag Group2 3 413 902Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 9 7333 423 635

Polimex-Mostostal Group 2 179 352Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 488 8692 668 221

PBG Group 1 808 245Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 178 7691 987 014

Trakcja Group 869 800Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 511 3731 381 173

Erbud Group 1 413 976Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 375 8001 789 776

Mostostal Warszawa Group 1 371 624 31 478 1 403 102

Unibep Group 1 063 381 3 364 26 388 156 106 1 249 239

Elektrobudowa Group 785 005 9 433 15 228 151 054 10 760 971 480

Warbud S.A. 920 456 9 979 930 435

Mostostal Zabrze Group 534 860Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 257 452792 312

Mota - Engil Central Europe S.A.

786 000 786 000

Mirbud Group 773 993 773 993

Skanska S.A. No data 3 793 600

PORR Group No data 1 109 738

TOTAL 28 632 008

MARKETS

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

21

Chart 1.6.3: Sales of the fifteen largest construction companies in 2015 - by geographical area

Source: Financial statements of the reviewed companies for 2015 -2016

DomesticWestern

EuropeanEastern

EuropeanScandinavian Asian Other

TOTAL2015

(PLN‘000)

Budimex Group 4 927 035 174 854 32 105 5 133 994

Strabag Group2 3 838 737Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 8 6853 847 423

Polimex-Mostostal Group 2 105 953Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 442 6222 548 575

PBG Group 1 670 172Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 128 6431 798 815

Erbud Group 1 557 200Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 158 2181 715 418

Trakcja Group 842 202Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 486 9781 329 180

Mostostal Warszawa Group 1 262 259 2 359 10 112 701 1 275 431

Unibep Group 1 004 270 29 760 76 804 131 868 158 1 242 860

Elektrobudowa Group 1 129 696 2 523 13 339 78 460 5 197 13 615 1 242 830

Warbud S.A. 1 106 860 1 106 860

Mota - Engil Central Europe S.A.

949 576 949 576

Mirbud Group 760 816 760 816

Mostostal Zabrze Group 498 045Locations abroad where the revenue is generated are unknown.

Foreign revenue amount - 261 579759 624

Skanska S.A. No data 4 430 900

PORR Group No data 1 294 204

TOTAL 29 436 505

MARKETS

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

22

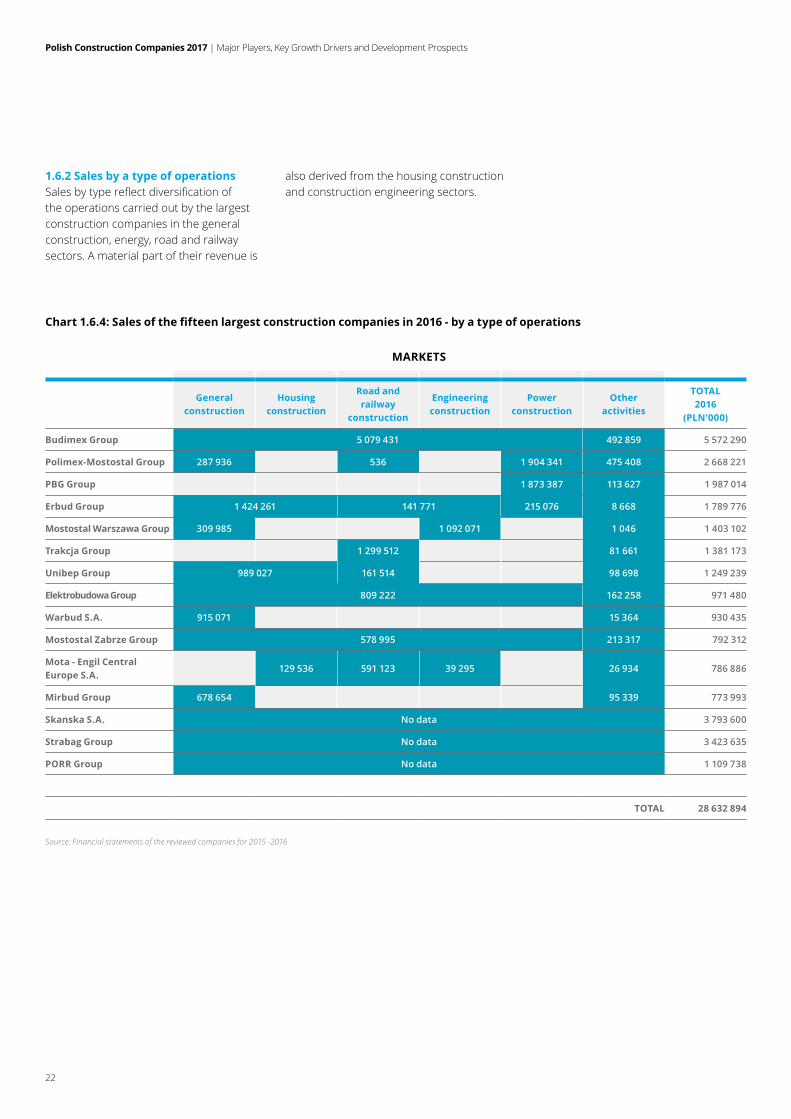

1.6.2 Sales by a type of operationsSalesbytypereflectdiversificationofthe operations carried out by the largest construction companies in the general construction, energy, road and railway sectors. A material part of their revenue is

also derived from the housing construction and construction engineering sectors.

Chart 1.6.4: Sales of the fifteen largest construction companies in 2016 - by a type of operations

Source: Financial statements of the reviewed companies for 2015 -2016

General construction

Housingconstruction

Road and railway

construction

Engineering construction

Power construction

Other activities

TOTAL2016

(PLN‘000)

Budimex Group 5 079 431 492 859 5 572 290

Polimex-Mostostal Group 287 936 536 1 904 341 475 408 2 668 221

PBG Group 1 873 387 113 627 1 987 014

Erbud Group 1 424 261 141 771 215 076 8 668 1 789 776

Mostostal Warszawa Group 309 985 1 092 071 1 046 1 403 102

Trakcja Group 1 299 512 81 661 1 381 173

Unibep Group 989 027 161 514 98 698 1 249 239

Elektrobudowa Group 809 222 162 258 971 480

Warbud S.A. 915 071 15 364 930 435

Mostostal Zabrze Group 578 995 213 317 792 312

Mota - Engil Central Europe S.A.

129 536 591 123 39 295 26 934 786 886

Mirbud Group 678 654 95 339 773 993

Skanska S.A. No data 3 793 600

Strabag Group No data 3 423 635

PORR Group No data 1 109 738

TOTAL 28 632 894

MARKETS

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

23

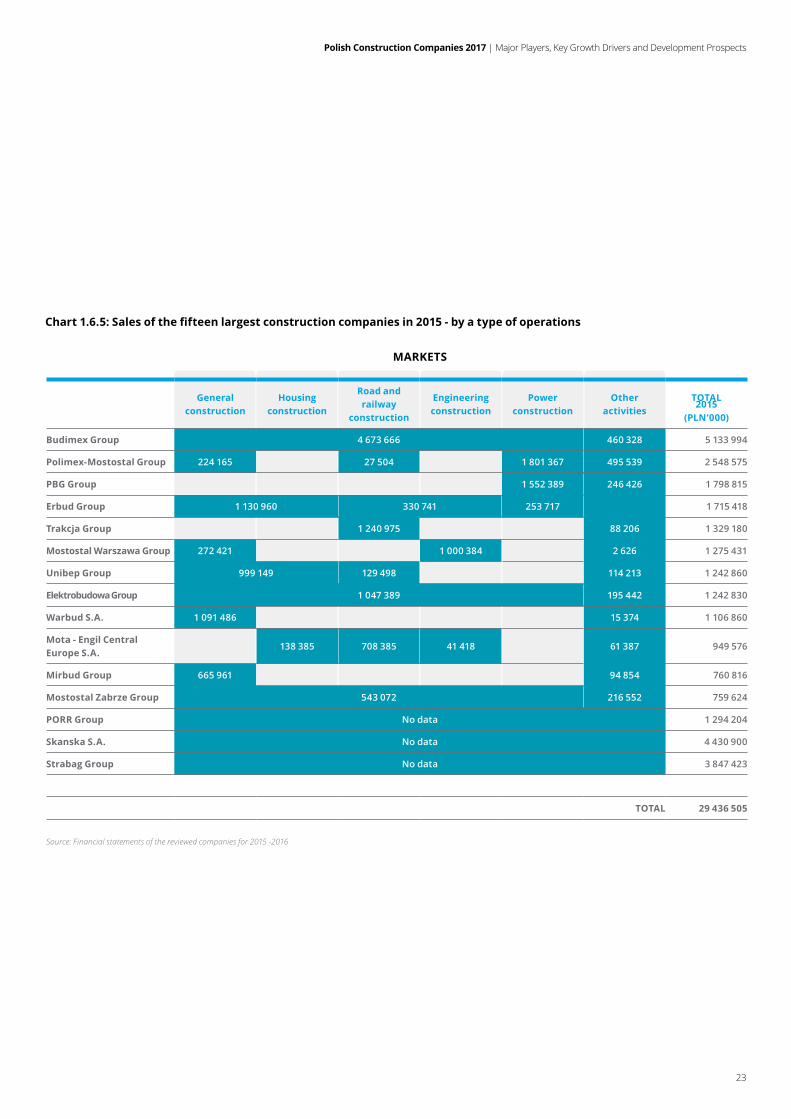

Chart 1.6.5: Sales of the fifteen largest construction companies in 2015 - by a type of operations

Source: Financial statements of the reviewed companies for 2015 -2016

General construction

Housingconstruction

Road and railway

construction

Engineering construction

Power construction

Other activities

TOTAL2015

(PLN‘000)

Budimex Group 4 673 666 460 328 5 133 994

Polimex-Mostostal Group 224 165 27 504 1 801 367 495 539 2 548 575

PBG Group 1 552 389 246 426 1 798 815

Erbud Group 1 130 960 330 741 253 717 1 715 418

Trakcja Group 1 240 975 88 206 1 329 180

Mostostal Warszawa Group 272 421 1 000 384 2 626 1 275 431

Unibep Group 999 149 129 498 114 213 1 242 860

Elektrobudowa Group 1 047 389 195 442 1 242 830

Warbud S.A. 1 091 486 15 374 1 106 860

Mota - Engil Central Europe S.A.

138 385 708 385 41 418 61 387 949 576

Mirbud Group 665 961 94 854 760 816

Mostostal Zabrze Group 543 072 216 552 759 624

PORR Group No data 1 294 204

Skanska S.A. No data 4 430 900

Strabag Group No data 3 847 423

TOTAL 29 436 505

MARKETS

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

24

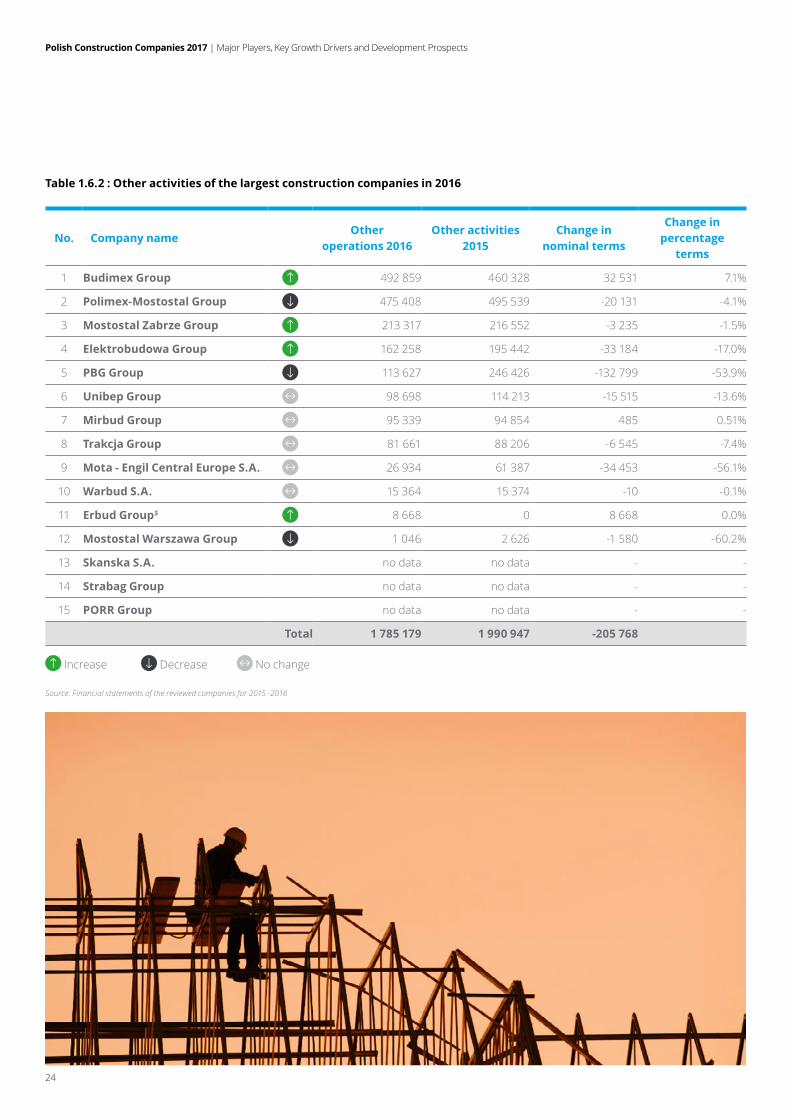

No. Company nameOther

operations 2016Other activities

2015Change in

nominal terms

Change in percentage

terms

1 Budimex Group 492 859 460 328 32 531 7.1%

2 Polimex-Mostostal Group 475 408 495 539 -20 131 -4.1%

3 Mostostal Zabrze Group 213 317 216 552 -3 235 -1.5%

4 Elektrobudowa Group 162 258 195 442 -33 184 -17.0%

5 PBG Group 113 627 246 426 -132 799 -53.9%

6 Unibep Group 98 698 114 213 -15 515 -13.6%

7 Mirbud Group 95 339 94 854 485 0.51%

8 Trakcja Group 81 661 88 206 -6 545 -7.4%

9 Mota - Engil Central Europe S.A. 26 934 61 387 -34 453 -56.1%

10 Warbud S.A. 15 364 15 374 -10 -0.1%

11 Erbud Group3 8 668 0 8 668 0.0%

12 Mostostal Warszawa Group 1 046 2 626 -1 580 -60.2%

13 Skanska S.A. no data no data - -

14 Strabag Group no data no data - -

15 PORR Group no data no data - -

Total 1 785 179 1 990 947 -205 768

Source: Financial statements of the reviewed companies for 2015 -2016

Table 1.6.2 : Other activities of the largest construction companies in 2016

Increase Decrease No change

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

25

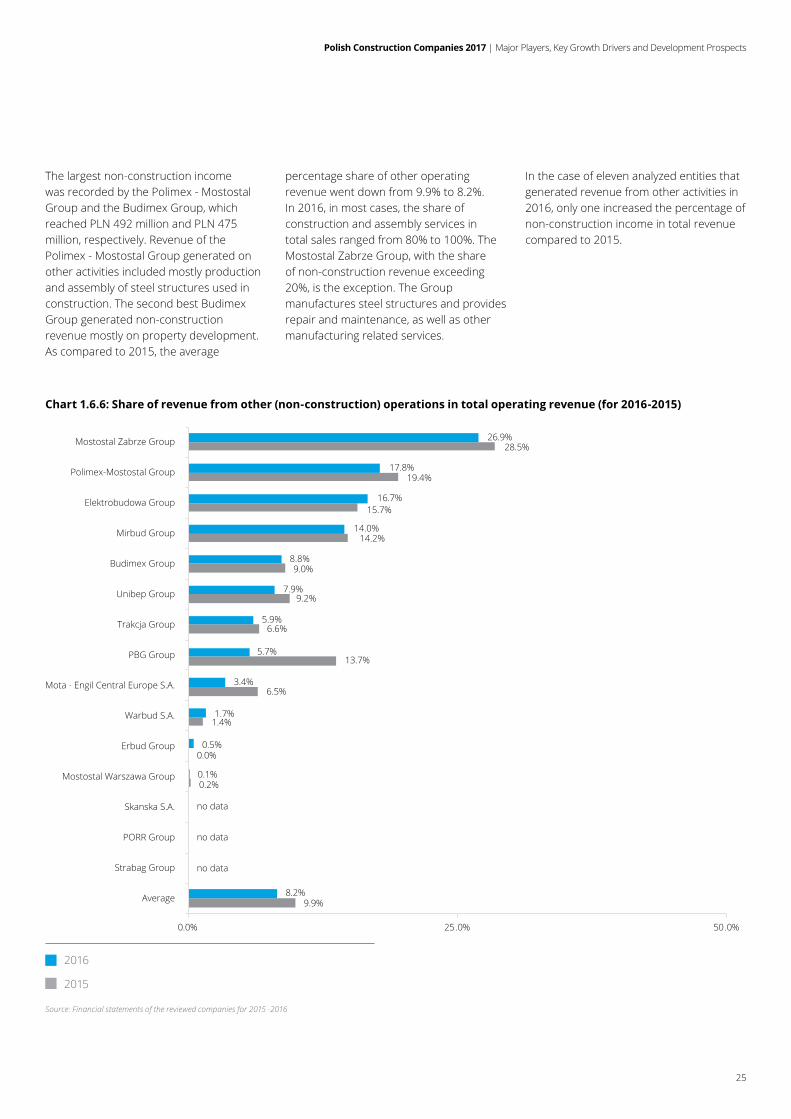

The largest non-construction income was recorded by the Polimex - Mostostal Group and the Budimex Group, which reached PLN 492 million and PLN 475 million, respectively. Revenue of the Polimex - Mostostal Group generated on other activities included mostly production and assembly of steel structures used in construction. The second best Budimex Group generated non-construction revenue mostly on property development. As compared to 2015, the average

percentage share of other operating revenue went down from 9.9% to 8.2%. In 2016, in most cases, the share of construction and assembly services in total sales ranged from 80% to 100%. The Mostostal Zabrze Group, with the share of non-construction revenue exceeding 20%, is the exception. The Group manufactures steel structures and provides repair and maintenance, as well as other manufacturing related services.

In the case of eleven analyzed entities that generated revenue from other activities in 2016, only one increased the percentage of non-construction income in total revenue compared to 2015.

Chart 1.6.6: Share of revenue from other (non-construction) operations in total operating revenue (for 2016-2015)

2016

2015

Source: Financial statements of the reviewed companies for 2015 -2016

9.9%

no data

0.2%

0.0%

1.4%

6.5%

13.7%

9.2%

9.0%

14.2%

15.7%

19.4%

28.5%

8.2%

no data

no data

0.1%

0.5%

1.7%

3.4%

5.7%

7.9%

8.8%

14.0%

16.7%

17.8%

26.9%

0.0% 25.0% 50.0%

Mostostal Zabrze Group

Polimex-Mostostal Group

Elektrobudowa Group

Mirbud Group

Budimex Group

Unibep Group

Trakcja Group

PBG Group

Mota - Engil Central Europe S.A.

Warbud S.A.

Erbud Group

Mostostal Warszawa Group

Skanska S.A.

PORR Group

Strabag Group

Average

6.6%5.9%

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

26

An analysis of the aforesaid data shows clearly that still a relatively low share of revenue is earned on operations other than those directly related to the implementation of construction projects. This trend should reverse once projects receiving EU support in the second financialperspectivehavebeenfinalized.Itshould be emphasised, though, that large construction groups have already begun to diversify their business and invest in areas which are not directly related to construction or property development operations, such as property management, supply and installation of specialist industrial equipment or construction advisory and consulting services.

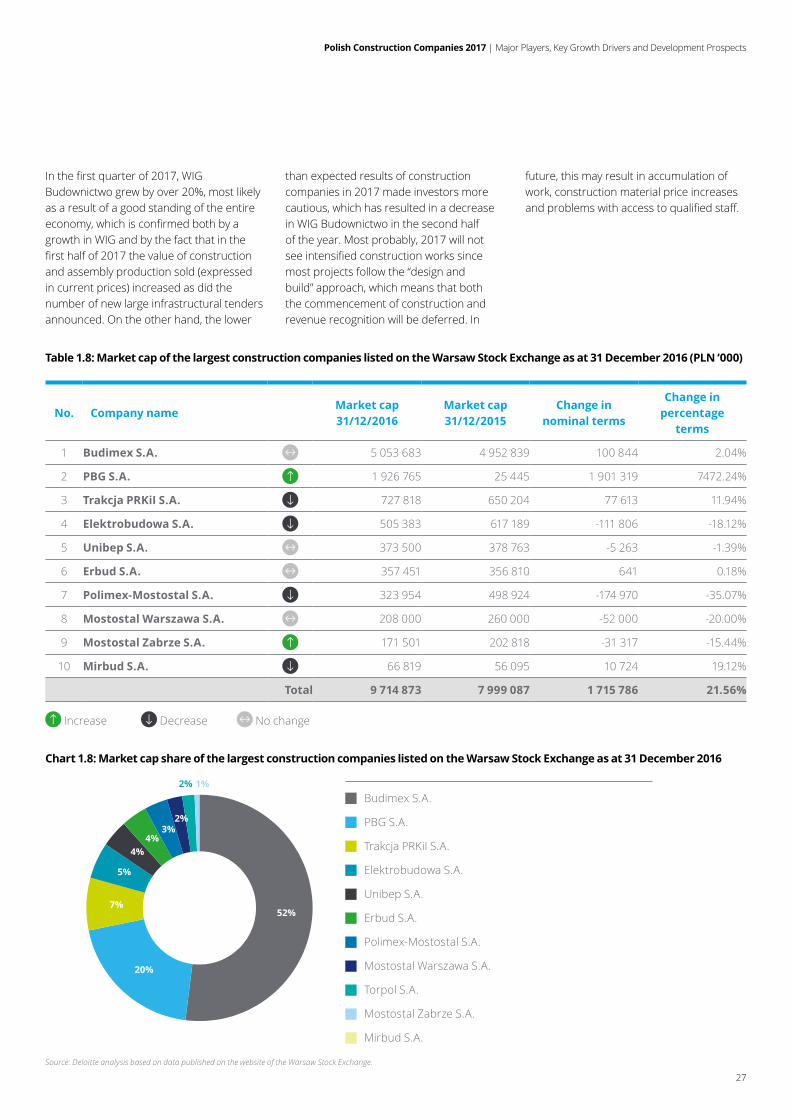

1.7. Market cap of the largest construction companies listed on the Warsaw Stock ExchangeFollowingasignificantincreaseinWIG Budownictwo is a subindex of Warsaw Stock Exchange Index (WIG) which submits only construction companies listed on WIG. index in 2015, the subsequent year saw a slowdown related to an overall decrease in construction and assembly related production, resulting mostly from delays in public procurement procedures regarding large infrastructural projects. In 2016, WIG BUD dropped by 1.5%. At the same time, WIG increased by more than 10%.

Tenoutofthefifteenlargestconstructioncompanies were listed on the Warsaw Stock Exchange. At the end of 2016, the combined market cap of the ten construction companies listed on the Warsaw Stock Exchange was PLN 9.7 billion and was PLN 1.7 billion higher than their combined market cap at the end of 2015. In percentage terms, the combined market cap rose by 21%. The substantial increase

resulted from an increase in the PBG Group market cap, which in turn had resulted from a composition agreement signed with creditors and completion of the bankruptcy procedure. With PBG excluded from the analysis, the total market cap of the listed companies included in the ranking would decreased by 2%.

Budimex, whose market cap was PLN 5,054 million (up by 2% as compared to 2015), whose share in the total cap of all companies presented in the table exceeds 50%, has been an unquestionable leader since 2011. The PBG Group has come second, and Trakcja PRKiL third, with market capitalisation of PLN 1,927 million and PLN 728 million, respectively.

Chart 1.7.1: Construction and assembly production ratio in 2016 YOY - cumulative year over year changes

Source: Deloitte analysis based on data available on the website of the Central Statistical Office ( January 2017 report).

-18%

-16%

-14%

-12%

-10%

-8%

-6%

-4%

-2%

0%

I II III IV V VI VII VIII IX X XI XII-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

I II III IV V VI VII VIII2016 2017

Chart 1.7.2: Construction and assembly production ratio in 2017 YOY - cumulative year over year changes

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

27

Inthefirstquarterof2017,WIGBudownictwo grew by over 20%, most likely as a result of a good standing of the entire economy,whichisconfirmedbothbyagrowth in WIG and by the fact that in the firsthalfof2017thevalueofconstructionand assembly production sold (expressed in current prices) increased as did the number of new large infrastructural tenders announced. On the other hand, the lower

than expected results of construction companies in 2017 made investors more cautious, which has resulted in a decrease in WIG Budownictwo in the second half of the year. Most probably, 2017 will not seeintensifiedconstructionworkssincemost projects follow the “design and build” approach, which means that both the commencement of construction and revenue recognition will be deferred. In

future, this may result in accumulation of work, construction material price increases andproblemswithaccesstoqualifiedstaff.

Table 1.8: Market cap of the largest construction companies listed on the Warsaw Stock Exchange as at 31 December 2016 (PLN ‘000)

No. Company nameMarket cap 31/12/2016

Market cap 31/12/2015

Change in nominal terms

Change in percentage

terms

1 Budimex S.A. 5 053 683 4 952 839 100 844 2.04%

2 PBG S.A. 1 926 765 25 445 1 901 319 7472.24%

3 Trakcja PRKiI S.A. 727 818 650 204 77 613 11.94%

4 Elektrobudowa S.A. 505 383 617 189 -111 806 -18.12%

5 Unibep S.A. 373 500 378 763 -5 263 -1.39%

6 Erbud S.A. 357 451 356 810 641 0.18%

7 Polimex-Mostostal S.A. 323 954 498 924 -174 970 -35.07%

8 Mostostal Warszawa S.A. 208 000 260 000 -52 000 -20.00%

9 Mostostal Zabrze S.A. 171 501 202 818 -31 317 -15.44%

10 Mirbud S.A. 66 819 56 095 10 724 19.12%

Total 9 714 873 7 999 087 1 715 786 21.56%

Increase Decrease No change

Chart 1.8: Market cap share of the largest construction companies listed on the Warsaw Stock Exchange as at 31 December 2016

Budimex S.A.

PBG S.A.

Trakcja PRKiI S.A.

Elektrobudowa S.A.

Unibep S.A.

Erbud S.A.

Polimex-Mostostal S.A.

Mostostal Warszawa S.A.

Torpol S.A.

Mostostal Zabrze S.A.

Mirbud S.A.

Source: Deloitte analysis based on data published on the website of the Warsaw Stock Exchange.

52%

20%

7%

5%

4%4%

3%2%

2% 1%

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

28

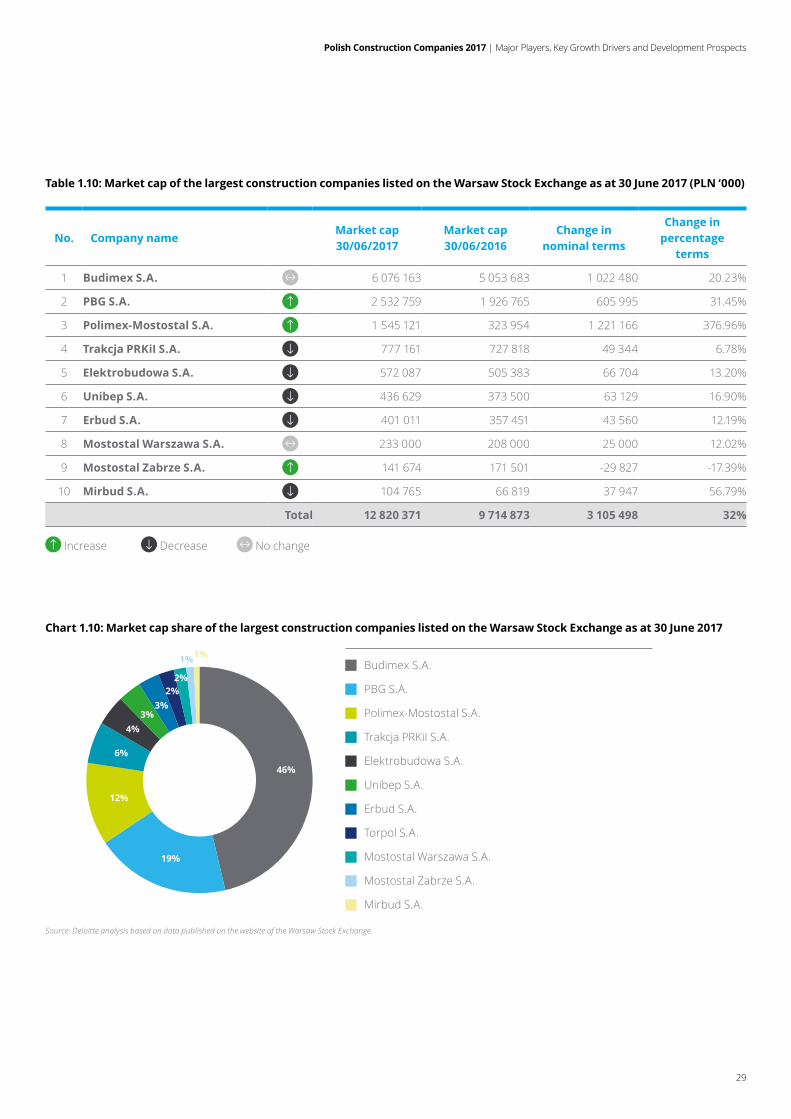

Basedonfinancialdataavailableasat30June 2017, the total cap of the presented companies increased by over 30% compared to the end of December 2016.

The substantial growth in the market cap of the listed construction companies has resulted mostly from a growth in the value of shares in Budimex (by nearly 20%), PBG S.A. (by over 31%) and Polimex Mostostal S.A. (by over 376%). The increase in capitalisation of the three entities accounts for over PLN 2.8 billion of the total change of PLN 3.1 billion observed in the period from

31 December 2016 to 30 June 2017. When analysing each company’s capitalisation over the last six months, Polimex Mostostal saw its highest growth expressed in percent, contributed to by the largest domestic power companies that have become its shareholders. The increase in the value of shares in PBG S.A. has resulted from implemented restructuring measures. It is worth noting that in the second half of the year the growth of WIG BUD index turned into a decrease, unlike the continuing increase of WIG. The turn of the trend results indirectly from a change in quoted

prices of the largest entities and market valuation of risks related to contracts they have been working on.

Chart 1.9: Changes in Warsaw Stock Exchange Index and WSE Construction Index in period 01/2016 - 09/2017

WIG

WIG BUDOW

Source: Deloitte analysis based on data published on the website of the Warsaw Stock Exchange.

80

90

100

110

120

130

140

150

01.2

016

02.2

016

03.2

016

04.2

016

05.2

016

06.2

016

07.2

016

08.2

016

09.2

016

10.2

016

11.2

016

12.2

016

01.2

017

02.2

017

03.2

017

04.2

017

05.2

017

06.2

017

07.2

017

08.2

017

09.2

017

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

29

Table 1.10: Market cap of the largest construction companies listed on the Warsaw Stock Exchange as at 30 June 2017 (PLN ‘000)

No. Company nameMarket cap 30/06/2017

Market cap 30/06/2016

Change in nominal terms

Change in percentage

terms

1 Budimex S.A. 6 076 163 5 053 683 1 022 480 20.23%

2 PBG S.A. 2 532 759 1 926 765 605 995 31.45%

3 Polimex-Mostostal S.A. 1 545 121 323 954 1 221 166 376.96%

4 Trakcja PRKiI S.A. 777 161 727 818 49 344 6.78%

5 Elektrobudowa S.A. 572 087 505 383 66 704 13.20%

6 Unibep S.A. 436 629 373 500 63 129 16.90%

7 Erbud S.A. 401 011 357 451 43 560 12.19%

8 Mostostal Warszawa S.A. 233 000 208 000 25 000 12.02%

9 Mostostal Zabrze S.A. 141 674 171 501 -29 827 -17.39%

10 Mirbud S.A. 104 765 66 819 37 947 56.79%

Total 12 820 371 9 714 873 3 105 498 32%

Increase Decrease No change

Chart 1.10: Market cap share of the largest construction companies listed on the Warsaw Stock Exchange as at 30 June 2017

Source: Deloitte analysis based on data published on the website of the Warsaw Stock Exchange.

Budimex S.A.

PBG S.A.

Polimex-Mostostal S.A.

Trakcja PRKiI S.A.

Elektrobudowa S.A.

Unibep S.A.

Erbud S.A.

Torpol S.A.

Mostostal Warszawa S.A.

Mostostal Zabrze S.A.

Mirbud S.A.

46%

19%

12%

6%

4%3%

3%2%

2%

1%1%

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

30

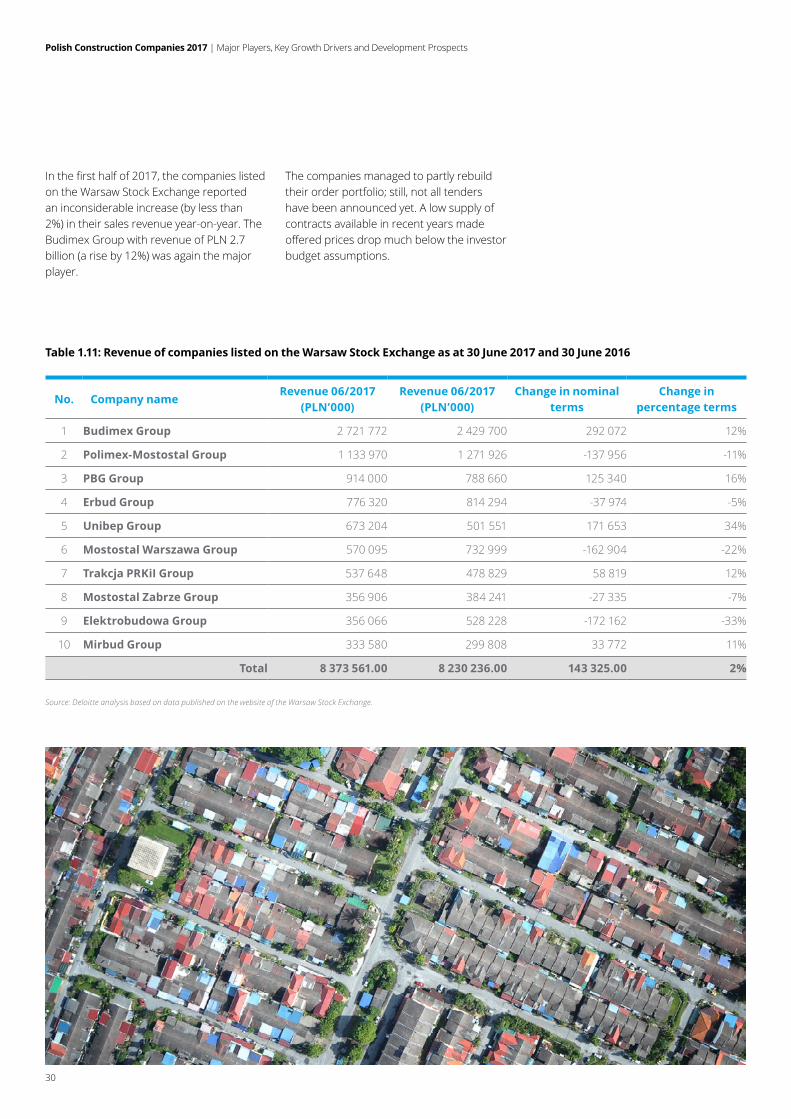

Inthefirsthalfof2017,thecompanieslistedon the Warsaw Stock Exchange reported an inconsiderable increase (by less than 2%) in their sales revenue year-on-year. The Budimex Group with revenue of PLN 2.7 billion (a rise by 12%) was again the major player.

The companies managed to partly rebuild their order portfolio; still, not all tenders have been announced yet. A low supply of contracts available in recent years made offeredpricesdropmuchbelowtheinvestorbudget assumptions.

Table 1.11: Revenue of companies listed on the Warsaw Stock Exchange as at 30 June 2017 and 30 June 2016

No. Company nameRevenue 06/2017

(PLN’000)Revenue 06/2017

(PLN’000)Change in nominal

terms Change in

percentage terms

1 Budimex Group 2 721 772 2 429 700 292 072 12%

2 Polimex-Mostostal Group 1 133 970 1 271 926 -137 956 -11%

3 PBG Group 914 000 788 660 125 340 16%

4 Erbud Group 776 320 814 294 -37 974 -5%

5 Unibep Group 673 204 501 551 171 653 34%

6 Mostostal Warszawa Group 570 095 732 999 -162 904 -22%

7 Trakcja PRKiI Group 537 648 478 829 58 819 12%

8 Mostostal Zabrze Group 356 906 384 241 -27 335 -7%

9 Elektrobudowa Group 356 066 528 228 -172 162 -33%

10 Mirbud Group 333 580 299 808 33 772 11%

Total 8 373 561.00 8 230 236.00 143 325.00 2%

Source: Deloitte analysis based on data published on the website of the Warsaw Stock Exchange.

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

31

Chart 1.11: Revenue of construction companies listed on the Warsaw Stock Exchange in the first half of 2017 and 2016 (PLN’000)

Source: Financial statements as at 30 June 2017

Revenue June 2017 (PLN million)

Revenue June 2016 (PLN million)

0

500�000

1�000�000

1�500�000

2�000�000

2�500�000

3�000�000

Budi

mex

Gro

up

Polim

ex-M

osto

stal

Gro

up

PBG

Gro

up

Erbu

d G

roup

Uni

bep

Gro

up

Mos

tost

al W

arsz

awa

Gro

up

Trak

cja

PRKi

I Gro

up

Mos

tost

al Z

abrz

e G

roup

Elek

trob

udow

a G

roup

Mirb

ud G

roup

Therefore, strong margin pressure shall affectinvestmentbudgets.Additionally,risksrelatedtosignificantaccumulationofworks in 2018-2020 may translate into a growth in construction material prices and reducedavailabilityofqualifiedstaff(whichcan be observed at present in all economy sectors).Thiswillaffectfutureperformanceof the companies and, despite apparently positive indications, may adversely impact theirfinancialstandingandquotedstockprices.

1 In the prior year, our ranking included aggregate data of all Skanska Group companies operating in Poland, while this year, the Group has provided us only with information regarding revenue generated by Skanska S.A.

2 Due to absence of consolidated financial statements, for simplification purposes, the financial data of the Strabag Group include the total of revenue generated by Strabag Sp. z o.o. and Strabag Infrastruktura Południe Sp. z o.o. Financial data for 2015 have been reconciled to financial statements for 2016 after opening balance adjustments.

3 Financial data for 2015 have been reconciled to financial statements for 2016 after opening balance adjustments.

4 Due to absence of consolidated financial statements, for simplification purposes, the financial data of the PORR Group include the total of the revenue generated by PORR Polska Construction S.A. and PORR Polska Infrastructure S.A. Financial data for 2015 have been reconciled to financial statements for 2016 after opening balance adjustments.

5 For the ratio calculation purposes, the balance sheet total has been reconciled to the financial statements for 2016 after adjustment of the balance sheet total as at 31 December 2015.

6 For the ratio calculation purposes, the balance sheet total has been reconciled to the financial statements for the six months of 2017 after adjustment of the balance sheet total as at 31 December 2016.

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

32

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

33

Section 2. Prospects

for development of construction

companies in Poland

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

34

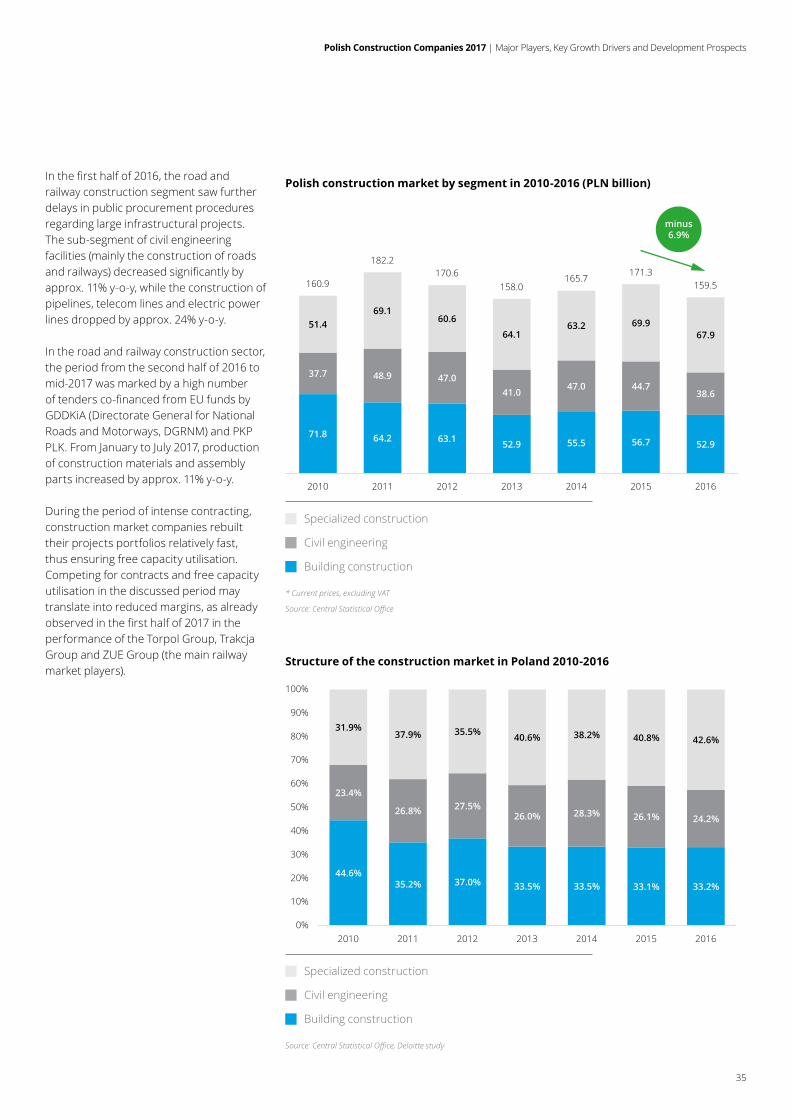

2.1. IntroductionIn 2016, the construction market value decreased by 6.9% to PLN 159.5 billion in relation to PLN 171.3 billion in 2015. Nevertheless, the market standing was differentindifferentmarketsegments.Thus, evaluation of the observed trends requires an individual approach to each segment. The building construction segment saw record-high apartment sales levels; at the same time, the railway and road construction segment rebounded only in the second half of 2016 due to deferred public procurement procedures co-financedwithEUfunds.

In 2016, a record-high number of apartmentswasofferedandsold.About62,000 apartments were sold in the six largest agglomerations (Warsaw, Kraków,Wrocław,Tricity,PoznańandŁódź)comparedtoapprox.52,000in20151. The demand was contributed to by continuing low interest rates, high availability of mortgage loans, growth in salaries and wages, as well as by decreasing unemployment. Apartment purchases for investment purposes contributed to the demand increase, in particular in districts of large cities with well-developed transportation systems. The percentage of apartments purchased for cash in large cities (mostly for investment purposes) has approximated 40%.

According to REAS projections, in 2017 the number of apartments sold in key agglomerations shall approximate 72,000, denoting a 16% increase year-on-year. An 18% increase in WIG Deweloperzy duringthefirstninemonthsof2017hasconfirmedthegoodstandingofthissector.The projected growth of the residential construction market

seems to be well-founded taking into account the following factors:

• prices per square meter being relatively stablewith a slight tendency to grow;

• land banks built by property developers to secure future investments;

• about 75% of apartments to be completed in 2017 being sold already;

• apartment sizes being better adjusted to financialcapabilityofclients;

• own contribution required by mortgage loan providers.

2016 was another year of record high supplyofofficespaceinPoland.Atpresent,officespaceavailableinPolandapproximates 9 million sq. m, out of which nearly 5 million sq. m located in Warsaw. In 2016,800,000sq.mofofficespacewerecommissioned, half of which in Warsaw. According to statistics, though, compared toWesternEurope,thePolishofficespacemarketisnotsaturatedyet(e.g.officespaceavailable in Munich equals 22 million sq. m). In the coming years, demand for new officespaceshouldbesupportedbysuchfactors as being the largest economy in the region, infrastructure development owing to access to EU funds, well educated labour, and universities in large cities supplying labourmarketwitheducatedstaff.

The standing of the retail and service space market was good. In 2016, it increased by o 470,000 sq. m. A supply growth projected for 2017 is 400,000 sq. m, out of which 360,000 sq. m being already in progress. A tax on retail sales or Sunday trade ban/limitation, if introduced, may adversely impact the market growth. On the other hand, growth in salaries and reduced unemployment may counteract the negative trend.

1 REAS, 2016

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

35

Inthefirsthalfof2016,theroadandrailway construction segment saw further delays in public procurement procedures regarding large infrastructural projects. The sub-segment of civil engineering facilities (mainly the construction of roads andrailways)decreasedsignificantlybyapprox. 11% y-o-y, while the construction of pipelines, telecom lines and electric power lines dropped by approx. 24% y-o-y.

In the road and railway construction sector, the period from the second half of 2016 to mid-2017 was marked by a high number oftendersco-financedfromEUfundsbyGDDKiA (Directorate General for National Roads and Motorways, DGRNM) and PKP PLK. From January to July 2017, production of construction materials and assembly parts increased by approx. 11% y-o-y.

During the period of intense contracting, construction market companies rebuilt their projects portfolios relatively fast, thus ensuring free capacity utilisation. Competing for contracts and free capacity utilisation in the discussed period may translate into reduced margins, as already observedinthefirsthalfof2017intheperformance of the Torpol Group, Trakcja Group and ZUE Group (the main railway market players).

71.8 64.2 63.1 52.9 55.5 56.7 52.9

37.7 48.9 47.041.0 47.0 44.7

38.6

51.469.1

60.6

64.163.2 69.9

67.9

160.9

182.2170.6

158.0165.7

171.3159.5

2010 2011 2012 2013 2014 2015 2016

minus6.9%

Specialized construction

Civil engineering

Building construction

* Current prices, excluding VAT

Source: Central Statistical Office

Polish construction market by segment in 2010-2016 (PLN billion)

44.6%35.2% 37.0% 33.5% 33.5% 33.1% 33.2%

23.4%

26.8% 27.5%26.0% 28.3% 26.1% 24.2%

31.9%37.9% 35.5% 40.6% 38.2% 40.8% 42.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2011 2012 2013 2014 2015 2016

Structure of the construction market in Poland 2010-2016

Specialized construction

Civil engineering

Building construction

Source: Central Statistical Office, Deloitte study

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

36

The construction market standing improvementseenin2017isreflectedingrowing prices of shares in construction companies quoted on Warsaw Stock Exchange. The broad WIG Budownictwo index, including 47 companies, grew by 13% from January 2016 to August 2017. Pursuant to our analysis, WIG-Budownictwo index has followed WIG from the beginning of 2016 to September 2017, albeit the growth has been slower.

The road transport market growth shall be triggered by the continuing motorway construction, including the completion of A2 motorway sections between Warsaw and Terespol, expressways and ring roads, among others those in Kraków and Warsaw, as well as the plan of building pan-European roads, such as Via Carpatia.

Further growth in the construction segment will be supported with investments in power generation, including the completion of the pending construction of power units, such as Opole, Kozienice, Żerań,StalowaWola,andcommencingthe construction of new ones, such as OstrołękaC(approx.100MW).Further,the value of power transmission and distribution investments planned until 2025 is estimated at PLN 52 billion.

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

01.2

014

04.2

014

07.2

014

10.2

014

01.2

015

04.2

015

07.2

015

10.2

015

01.2

016

04.2

016

07.2

016

10.2

016

01.2

017

04.2

017

07.2

017

01.01.2016=100%

WIG Budownictwo and WIG benchmarked to 1 January 2016

Source: Stooq

Additionally, international gas transmission and distribution pipelines are planned to connect Poland to Denmark and Lithuania, as well as the North-South one going through Poland. The total value of gas transmission and distribution investments planned until 2025 approximates PLN 26 billion.

WIG

WIG BUDOW

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

37

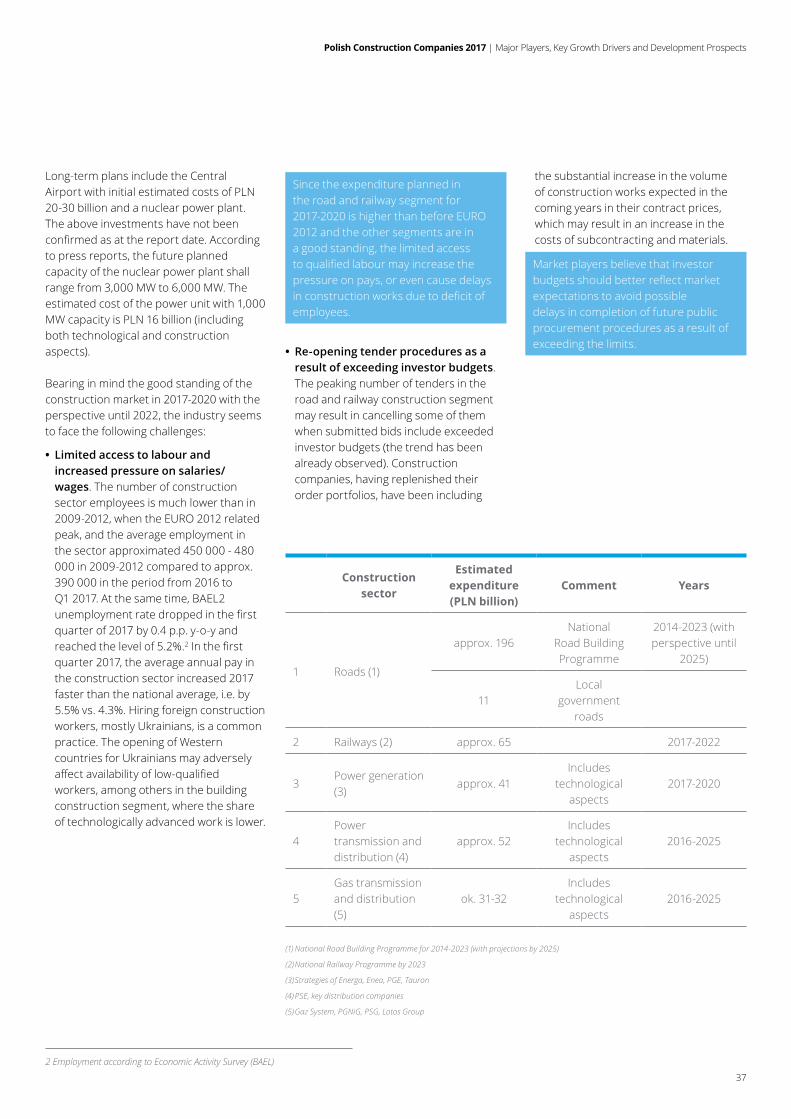

Long-term plans include the Central Airport with initial estimated costs of PLN 20-30 billion and a nuclear power plant. The above investments have not been confirmedasatthereportdate.Accordingto press reports, the future planned capacity of the nuclear power plant shall range from 3,000 MW to 6,000 MW. The estimated cost of the power unit with 1,000 MW capacity is PLN 16 billion (including both technological and construction aspects).

Bearing in mind the good standing of the construction market in 2017-2020 with the perspective until 2022, the industry seems to face the following challenges:

• Limited access to labour and increased pressure on salaries/wages. The number of construction sector employees is much lower than in 2009-2012, when the EURO 2012 related peak, and the average employment in the sector approximated 450 000 - 480 000 in 2009-2012 compared to approx. 390 000 in the period from 2016 to Q1 2017. At the same time, BAEL2 unemploymentratedroppedinthefirstquarter of 2017 by 0.4 p.p. y-o-y and reached the level of 5.2%.2Inthefirstquarter 2017, the average annual pay in the construction sector increased 2017 faster than the national average, i.e. by 5.5% vs. 4.3%. Hiring foreign construction workers, mostly Ukrainians, is a common practice. The opening of Western countries for Ukrainians may adversely affectavailabilityoflow-qualifiedworkers, among others in the building construction segment, where the share of technologically advanced work is lower.

Construction sector

Estimated expenditure (PLN billion)

Comment Years

1 Roads (1)

approx. 196National

Road Building Programme

2014-2023 (with perspective until

2025)

11Local

government roads

2 Railways (2) approx. 65 2017-2022

3Power generation (3)

approx. 41Includes

technological aspects

2017-2020

4Power transmission and distribution (4)

approx. 52Includes

technological aspects

2016-2025

5Gas transmission and distribution (5)

ok. 31-32Includes

technological aspects

2016-2025

(1) National Road Building Programme for 2014-2023 (with projections by 2025)

(2) National Railway Programme by 2023

(3) Strategies of Energa, Enea, PGE, Tauron

(4) PSE, key distribution companies

(5) Gaz System, PGNiG, PSG, Lotos Group

Since the expenditure planned in the road and railway segment for 2017-2020 is higher than before EURO 2012 and the other segments are in a good standing, the limited access toqualifiedlabourmayincreasethepressure on pays, or even cause delays inconstructionworksduetodeficitofemployees.

• Re-opening tender procedures as a result of exceeding investor budgets. The peaking number of tenders in the road and railway construction segment may result in cancelling some of them when submitted bids include exceeded investor budgets (the trend has been already observed). Construction companies, having replenished their order portfolios, have been including

the substantial increase in the volume of construction works expected in the coming years in their contract prices, which may result in an increase in the costs of subcontracting and materials. Market players believe that investor budgetsshouldbetterreflectmarketexpectations to avoid possible delays in completion of future public procurement procedures as a result of exceeding the limits.

2 Employment according to Economic Activity Survey (BAEL)

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

38

• Limiting bid evaluation criteria to price. In mid-2016 the 60/40 tender criterion was introduced, according to which the maximum price weight for a bid is 60%, while quality criteria account for the other 40%. The most frequent practice adopted by public bodies is to consider the guarantee terms and delivery date as the key quality criteria. Consequently, the lowest price remains the key condition, since all tender participants usually adopt the maximum permitted guarantee period and the shortest possible contract delivery deadline.

Making the price the only bid assessment criterion may result in difficultiesincontractdelivery,inparticular in light of growing prices of materials and labour. Black scenarios may include a replay of that preceding EURO 2012, i.e. bankruptcies of selected construction market players.

• Limited supply of construction materials, in particular in the railway construction segment. Construction market players are concerned about a potential bottleneck in the form of limited supply of special construction materials, such as ties. The time-consuming construction material attestation procedure and capacity increase processes may result in a shortage of certain construction materials, and delays in completion of planned infrastructural investments.

Limited supply of construction materials may result in delays in construction contract completion and price increases, which in turn will translate in reduced contractor margins.

• Adverse traffic changes.Intensifiedconstruction works necessitating railway trafficchangesmayresultinnegativepublicity, in particular if causing adverse effectsincargotransport(amongothersof aggregates), which may increase their transport costs.

Costs of railway transport of selected materials, including aggregates, may increaseasaresultofdifficultiescausedby ongoing modernisation works.

• Organising construction sites in accordance with “design and build” formula. The Designing Period may take from a few months to over a year and is usually long due to questions regarding the tender documentation, asked by potential contractors.

On the one hand, “design and build” approachallowcontractorsefficienciesowing to their participation in the designing procedure; on the other hand, though, they often involve an extended tender procedure.

Developing and accepting a template agreementthatreflectsbothclient’sandcontractor’s interests and guidelines regarding tender description and procedures is an important factor that may facilitate the completion of road and railway investments. In February 2017, the Ministry of Infrastructure and Construction adopted “New Road Construction Standards” that provide a general framework for road construction projects. The ongoing work includes a draft agreement with contractors to comprise:

• risk sharing;

• independence of third-party engineers;

• protection of sub-contractors;

• reduced number of disputes and faster settlement procedures;

• rationalised system of liquidated damages;

• obligation to conclude employment contracts.

An Expert Council has been established to facilitate the completion of railway investments, with the objective to optimise the investment process. The Council wants tointroduceaunifiedtemplateagreementfor all railway investments. Although certain ideas have been implemented, certain issues, such as the payment model fortheengineer,unifiedinterpretationofcurrentlegalregulations,certificationoftender participants or bid selection criteria applicable to railway accessibility, remain unsolved.

Positive projections for the period until 2020 regarding selected macroeconomic indicators, such as economic growth and national debt, support the good standing of the construction segment, which in medium term may translate into improved access to funding from the State budget, also for infrastructural investments.

In a long term, after 2020, with reduced EU funds, development of infrastructure maintenance services and use of alternative funding sources such as PPP, provide the opportunities to be looked for to sustain the road and railway investments in Poland. The Ministry of Infrastructure and Construction plans to update the transport strategy, extending its perspective, indicating strategic projects and aiming at stabilisation of the road construction market with the annual investment value approximating PLN 15 billion to PLN 17 billion over a long term, following the completion of projects included in the current EU perspective.

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

39

DGP growth decomposition, 2012-2017

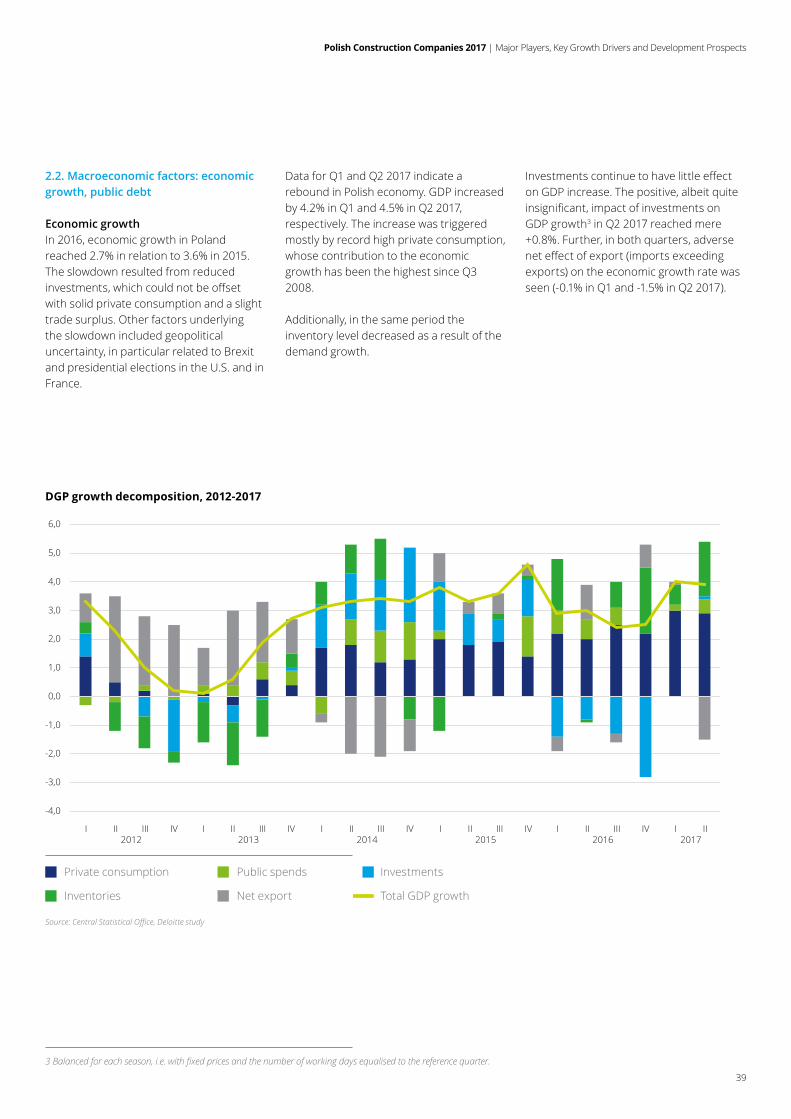

2.2. Macroeconomic factors: economic growth, public debt

Economic growthIn 2016, economic growth in Poland reached 2.7% in relation to 3.6% in 2015. The slowdown resulted from reduced investments,whichcouldnotbeoffsetwith solid private consumption and a slight trade surplus. Other factors underlying the slowdown included geopolitical uncertainty, in particular related to Brexit and presidential elections in the U.S. and in France.

Data for Q1 and Q2 2017 indicate a rebound in Polish economy. GDP increased by 4.2% in Q1 and 4.5% in Q2 2017, respectively. The increase was triggered mostly by record high private consumption, whose contribution to the economic growth has been the highest since Q3 2008.

Additionally, in the same period the inventory level decreased as a result of the demand growth.

Investmentscontinuetohavelittleeffecton GDP increase. The positive, albeit quite insignificant,impactofinvestmentsonGDP growth3 in Q2 2017 reached mere +0.8%. Further, in both quarters, adverse neteffectofexport(importsexceedingexports) on the economic growth rate was seen (-0.1% in Q1 and -1.5% in Q2 2017).

-4,0

-3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

6,0

I II III IV2012

I II III IV2013

I II III IV2014

I II III IV2015

I II III IV2016

I II2017

Private consumption Public spends Investments

Inventories Net export Total GDP growth

3 Balanced for each season, i.e. with fixed prices and the number of working days equalised to the reference quarter.

Source: Central Statistical Office, Deloitte study

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

40

Projected GDP growth in Poland, 2017-2021

Pursuant to the monetary policy assumptions for 2027 published by the National Bank of Poland, in subsequent quarters, high private consumption should besupportedbyagrowinginflation,triggered by increasing salaries and food prices, a growth in the Eurozone, which is Poland’s key partner and an increase in investmentlevelcausedbyagoodfinancialstanding and increased use of EU funds.

The optimistic outlook is supported bypositive adjustments to Polish economic growth projections for 2017, introduced in 2016 by international bodies:

• European Commission from +3.2% to +3.5% in 2017 (2 May 2017);

• OECD from +3.2% to +3.6% in 2017 (6 June 2017);

• Moody’s from +3.2% to +4.3% in 2017 (4 September 2017).

EIU4 anticipates a growth rate of approx. 3.2% to 3.5% in the years 2018-2021.

Government debtAt the end of 2016, government debt to GDP ratio increased to 51.4% compared to 49.0% at the end of 2015 o (a 2.4% increase y-o-y). Pursuant to the government debt management strategy for 2017-2020, published by the Minister of Finance on 16 September 2016, in 2017 further increase in government debt is assumed up to 52.3%. Since the national debt is related to local self-government debt, the increase in the former may translate into limited co-funding of infrastructural projects by local authorities.

Thefirsthalfof2017sawanimprovementin the state budget. In June 2017, the Ministry of Finance announced the total budget surplus of PLN 5.9 billion, while according to budget projections for 2017, in JunethedeficitwasnearPLN19billion.Thesubstantialdifference,approximatingPLN25 billion in nominal terms, resulted from high tax proceeds (a year-on-year growth by PLN 23.4 billion). year-on-year.

If the positive trends continue throughout 2017, the improved budget standing may translate into reduced national debt and, consequently, promote co-funding of infrastructural projects. This will depend, though, on durability of the increase in tax proceeds, which is of importance, among othersduetoanincreaseinfixedbudgetexpenses related to 500+ programme.

3.7%

5.0%

1.6%1.3%

3.3%3.6%

2.7%

3.2% 3.1% 2.8%

3.5%3.3%

0%

1%

2%

3%

4%

5%

6%

2010 2011 2012 2013 2014 2015 2016 2017P 2018P 2019P 2020P 2021P

53.4%52.6%

53.9%

47.8%

49.0%

51.4%

52.3%51.7%

51.1%

49.5%

45%

46%

47%

48%

49%

50%

51%

52%

53%

54%

55%

2011 2012 2013 2014 2015 2016 2017P 2018P 2019P 2020P

Source: EIU "Country Forecast Poland - August 2017"

Government debt as a GDP percentage

Source: Ministry of Finance – “Public Finance Sector Debt Management Strategy for 2017-2020”, September 2016

4 August 2017

Polish Construction Companies 2017 | Major Players, Key Growth Drivers and Development Prospects

41

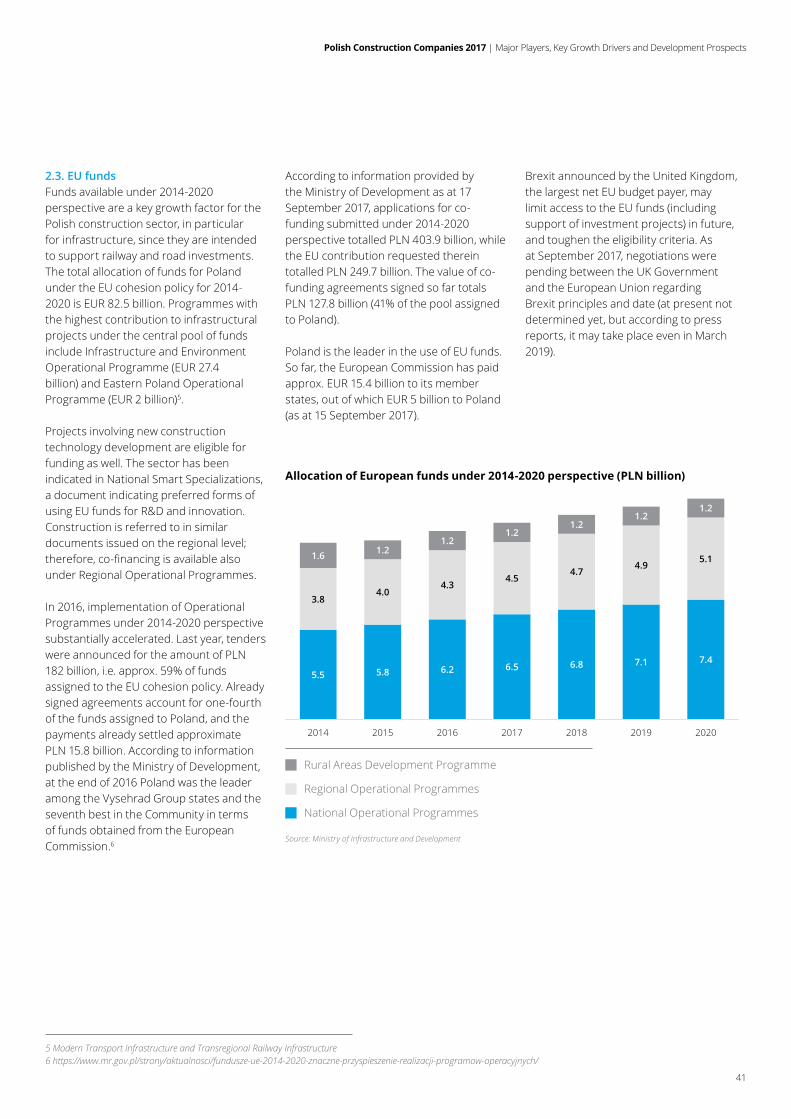

Allocation of European funds under 2014-2020 perspective (PLN billion)

Source: Ministry of Infrastructure and Development

2.3. EU fundsFunds available under 2014-2020 perspective are a key growth factor for the Polish construction sector, in particular for infrastructure, since they are intended to support railway and road investments. The total allocation of funds for Poland under the EU cohesion policy for 2014-2020 is EUR 82.5 billion. Programmes with the highest contribution to infrastructural projects under the central pool of funds include Infrastructure and Environment Operational Programme (EUR 27.4 billion) and Eastern Poland Operational Programme (EUR 2 billion)5.

Projects involving new construction technology development are eligible for funding as well. The sector has been indicated in National Smart Specializations, a document indicating preferred forms of using EU funds for R&D and innovation. Construction is referred to in similar documents issued on the regional level; therefore,co-financingisavailablealsounder Regional Operational Programmes.

In 2016, implementation of Operational Programmes under 2014-2020 perspective substantially accelerated. Last year, tenders were announced for the amount of PLN 182 billion, i.e. approx. 59% of funds assigned to the EU cohesion policy. Already signed agreements account for one-fourth of the funds assigned to Poland, and the payments already settled approximate PLN 15.8 billion. According to information published by the Ministry of Development, at the end of 2016 Poland was the leader among the Vysehrad Group states and the seventh best in the Community in terms of funds obtained from the European Commission.6

5.5 5.8 6.2 6.5 6.8 7.1 7.4

3.84.0

4.34.5