politics probe research geopolitics turkish...

TRANSCRIPT

Turkey: Strong growth, but sustainable?

JUNE 19 - JULY 03, 2017 - 14DOUBLE ISSUE

GUNDUZ FINDIKCIOGLUFrom our chief economist

ISSN

: 256

4-6

788

PROBE

Turkish assets The biggest threats to a

continuation in foreign interest in national assets 05

GEOPOLITICS

Russian experience Unsupported and limp foreign policies difficult to change once

full effect has been felt 12

POLITICS

Cabinet reshuffle Changes to Turkey’s cabinet now not expected to chime

until next year 06

RESEARCH

Not voting for Turkey Turkey ranks 6th last in HSBC’s

Expat Explorers’ survey of favored countries 15

2

at a glanceXGDP growth in 2017: Q1:5%

XGDP: $840 billion (2017, annualized)

XGDP per capita: $10,807 (2016)

XDomestic debt stock: 668.6 billion TRY (2016)

XExternal debt stock: $417 billion (2016)

XBudget balance: -11.5 billion TRY (January - May)

XUnemployment rate: 11.7% (March)

XInflation: CPI 11.72%, PPI 15.32% (annual - May)

XExports: $12.8 billion (April)

XImports: $17.7 billion (April)

XCurrent-account balance: $33.2 billion (April-annualized )

XEconomic confidence index: 100.5 (+1p) (April)

XICI Manufacturing PMI: 53.5 (+1.8p) (April)

XMusiad PMI: 53.6 (-3.2p) (Sameks, April)

TURKEY

USD/TRY

BIST-100

3.5130

98,192

%-0.61

%-0.62

%-0.76

Weekly change

Friday’s close / weekly change

EUR/TRY

3.9270Weekly change

Turkey’s unemployment rate climbs to 11.7%The number of unemployed people in Tur-key aged 15 years and older increased by 619,000 year-on-year to total 3.642 million in March 2017, according to Turkstat data released last Thursday. The unemployment rate has now reached 11.7%, reflecting a 1.6% increase. For the same period, the non-ag-ricultural unemployment rate was 13.7%, a 1.8% increase, youth unemployment, which includes people aged between 15-24, is now 21.4%, a rise of 4.4%, and the unemploy-ment rate for people aged 15-64 is 12%, an increase of 1.7%.

Turkish current account gap narrows to $ 3.6 billion in AprilTurkey’s current account deficit shrunk to $3.6 billion in April, a fall of $542 million year-on-year, the central bank said Monday. April’s deficit means the 12-month rolling deficit stands at $33.2 million, the bank said.

The improvement was mainly driven by a reduction in the import-export gap to $3.5 billion, down $563 million from a year ear-lier, and an increase in net income from ser-vices to $1.1 billion, up $346 million.

Turkish economic growth races to 5% in first quarter Turkish economic growth unexpected-ly accelerated at the start of the year to a near two-year peak. GDP growth in Turkey hit 5% in the first three months of the year compared to the same period last year, and was up from 3.5% in the last quarter of 2016, when the economy bounced back after re-cording its worst quarter since the financial crisis. The growth surprised economists polled by Bloomberg who had expected a reading of 3.5% for the year-on-year expan-sion. The actual performance was the best since the third quarter of 2015, with Turk-stat figures placing quarter-on-quarter growth up by 1.4%. Turkstat said govern-ment spending was up 9.4% for the peri-od, while consumer spending rose 5.1% and investment climbed by 2.2%. Exports leapt 10.6%, while imports inched up 0.8% in a pe-

MACRO

OVERVIEW

ALMOST 20 PERCENT OF TURKISH ADULT POPULATION OBESEFOCUS

Nearly one in five people in Turkey is obese, according to the results of a 2016 health survey released by the Turkish Statistical Institute on May 31. The survey showed that 19.6% of Turks aged 15 and older had a body mass index (BMI) of 30 or over, TurkStat said. The rate was slightly higher in 2014, at 19.9%.

A BMI of 18.5 to 25 is considered normal while a BMI of 25 to 29.9 is considered overweight, with 30 or over falling into the obese category. The rate of obesity in women aged 15 and older is 23.9%, according to the survey, while 15.2% of men are obese, and 38.6% falling into the pre-obese category,

3

A SYRIAN PERSPECTIVE

The number of Syrians living in Turkey is around 3 million, according to official records. This figure is more than the population of many countries in Europe. The number of immigrant and refugee students currently enrolled in primary education in Turkey is more than 500,000. In comparison, the number of students in primary education in Finland is around 370,000. A research study by Xsights on Syrian immigrants, which make up around 4% of Turkey’s population, reveals some remarkable data. The living conditions of the Syrians residing outside the camps in Turkey, the daily difficulties they face and their plans for their future were examined in the study. The results are as follows:

X20% of the Syrians who live outside the camps in Turkey had no family members in their country. However, 32% had a relative in countries outside of Turkey

X79% of the Syrians living outside the camps experienced language problems every day

X75% had difficulties in finding accommodation and/or housing

X82% faced difficulties in finding jobs

XOnly 14% said they are aware of their rights, and 26% felt integrated in Turkey, though Syrian beneficiaries of public services felt more integrated

XWhile 73% of the Syrians living outside the camps felt safe, 38% said they were satisfied with living in Turkey.

SOCIAL CHECK-UP

OVERVIEW

riod in which the lira fell by 2%.

Key interest rates on hold The Central Bank kept its main interest rates steady on June 15, in line with mar-ket expectations. The bank kept its closely watched late liquidity window at 12.25% and its benchmark repo rate on hold at 8%, saying it would stick to a tight policy stance until the inflation outlook signifi-cantly improved. All 16 economists polled by Reuters predicted the bank would leave the repo rate unchanged, as well as cor-rectly predicting that the overnight lend-ing rate, at 9.25%, and the overnight bor-rowing rate, at 7.25%, would remain un-changed. The bank said it would continue to use all available instruments in pursuit of its price stability objective. “The tight stance in monetary policy will be main-tained until the inflation outlook displays a significant improvement. Inflation ex-pectations, pricing behavior and other factors affecting inflation will be closely monitored and, if needed, further mone-tary tightening will be delivered,” it said in a bank press release.

Mavi Jeans IPO pricing bottoms out The initial public offering (IPO) of Turk-ish jeans fashion retailer Mavi Giyim was priced at 43 lira (€11) per share, an amount at the bottom end of the range which put the company’s value at around 2.14 billion lira ($606 million). The obtained price was announced on June 12 in a statement by Turkey’s Is Yatirim, the domestic coordi-nator and bookrunner for the offering in a brand favoured by Lady Gaga and Chelsea Clinton, among other A-list celebrity lumi-naries. In the IPO, Mavi Giyim sold a total of around 27.3 million shares, or roughly a 55% stake in the enterprise, raising around 1.17 billion lira. The Akarlilar family, the founding family behind Mavi Giyim, and Turkven Private Equity Fund II, held book-building over June 8-9 to offer a stake of up to 55 percent in an Istanbul stock exchange IPO with a price range of between 43 lira to 51.6 lira per share.

Vitol completes acquisition of Turkey’s Petrol Ofisi VIP Turkey Enerji AS, a subsidiary of Vi-tol Investment Partnership Ltd has com-pleted its acquisition of OMV Petrol Ofisi Holding A.S (“Petrol Ofisi”) from OMV AG., the company announced. The trans-action was first announced on 3 March 2017. “We will work closely with the Petrol Ofisi management team and employees to energise our brand, strengthen our deal-er relationships and serve our clients and customers in the best way possible. Vitol has a history of investing to grow business-es and this is a tremendous opportunity to refocus Petrol Ofisi for the future,” Javed Ahmed, head of investments, at Vitol and chairman of Petrol Ofisi, said in a state-ment. Petrol Ofisi is the market leader in fuel products and distribution in Turkey with a market share of circa 23%. Its busi-ness comprises the largest retail station network, with more than 1,700 service sta-tions, and the largest fuel storage and logis-tics business in Turkey, with a total storage capacity in excess of 1 million cubic me-ters, It is Turkey’s leading distributor of lubricants and the into-wing supply of jet

BUSINESS

ALMOST 20 PERCENT OF TURKISH ADULT POPULATION OBESEwhich means they have a BMI of 25 to 30. Alev Keser, associate professor of nutrition and diabetics at Ankara University’s Faculty of Health Sciences, told Anadolu Agency that the discrepancy between men and women had to do with the higher levels of estrogen hormone in women. “Compared to men, women have higher levels of estrogen, and more fat tissue. On the other hand, men have more muscular tissue which increases energy consumption as it boosts [the] basal metabolic rate,” Keser said. Keser said that since in general men work more than women, and women tend to be more at home, this may in turn cause women to move less and consume more food than men. Keser also noted the technological developments in agriculture and industry which led to an increase in the production of foods with high levels of saturated fat, sugar and salt. “Easy access to this kind of unhealthy food and reduced physical activity leads to an unhealthy lifestyle, which in turns leads to obesity,” she said. Keser underlined that obesity had become a critical health problem that could be prevented by embracing a healthy lifestyle based on a balanced diet and regular exercise.

4

PROMISING FIGURES CREATE HOPE FOR TOURISM

A boost in visitor numbers, which turned the negative indicators of the first quarter of 2017 positive in April, have increased hopes for a revived tourism sector for the rest of 2017. The number of tourists coming to Turkey in April increased by 18.1% compared to April 2016. As May figures have not yet been announced, the tourism industry expects an increase of around 20%. Israeli tourist bookings are also increasing while the aborted crisis with Russia has eased fears among coastal cities. The decline in the number of European tourists is expected to turn positive in July, August and September. This is especially due to high demand, while the increase in prices in Spain and Greece indicate that European tourists may prefer Turkey in last-minute sales. Recent terrorist attacks in the European capitals show that security issues are not specific to Turkey. Tourism professionals believe Turkey’s tourism will return to factory settings in 2018 barring extraordinary developments and predict 2019 to be a breakthrough year.

Russians and Israelis revive Antalyan tourism marketAccording to the daily newspaper DUNYA, there was a 30% year-on-year increase in visitors to Antalya in the first five months of 2017. A total of 1,911,994 tourists visited Antalya during the January-May period, with the number of Russian tourists to the whole of Turkey increasing by 5,135 in May. The number of Russian tourists who visited Antalya in January-May was 691,484. The number of Ukrainian tourists increased by 53% to 136,399, while there were also significant increases in the number of Israeli visitors. Israeli tourists reached 45,579, reflecting a 19% increase. However, there was a sharp decline in European visitors, where Turkey is the strongest in the tourism market. The number of German tourists coming to Antalya in the first five months of the year decreased by 35% year-on-year, falling to 376,212. The decline was not only from Germany, but also the Netherlands, England, Belgium, Denmark, Sweden, Switzerland, Norway, France and Austria.

Turkven behind acquisition of MNG KargoA Dubai-based company acquired one of Tur-

key’s leading logistics companies, MNG Kargo,

Turkish newspapers reported last week. Mirage

Cargo BV applied to the Turkish Competition

Authority to seek approval for the deal. The

Netherlands-based special purpose vehicle

(SPV) was reported as the buyside in the deal.

Indeed the buyer entity was based in Dubai.

However, another Dubai-based logistics com-

pany with the same name caused controversy

about the identity of the buyer. Mirage Cargo

Services LLC is the name of the Dubai compa-

ny. There is no information whether the original

Mirage Cargo Services is involved in the deal or

not. The only certainty is that Turkish private

equity firm Turkven holds the majority stake in

the SPV that applied to take over the Turkish

parcel delivery company.

MNG Kargo was rumoured to have attracted

interest from Turkven and Turkish investor

Haydar Sancak jointly, according to local press

reports that suggested a $248 million valuation

for the deal. Sources familiar with the industry

suggested the amount was too high for the

company. It would make sense if the price was

in Turkish lira, a banker said.

Established 15 years ago, the company had

recently undergone restructuring in its own-

ership to clear the hurdles of a potential sale.

Mehmet Nazif Gunal, MNG Holding’s chairman,

was holding the majority stake in the company.

The company, which has 9,000 employees, 815

branches and 2,600 vehicles, delivers parcels

to around 600,000 adresses daily, according

to press reports. Its competitors are Yurtici

Kargo and Aras Kargo.

The buyer, Turkven, has led or co-led invest-

ments of more than $5 billion in 19 deals since

2000. It is one of the leading private equity

firms in Turkey with a total of $2 billion assets

under management. The PE, in a consortium

with BC Partners and DeA Capital, has conduct-

ed the largest PE-led deal in Turkey with the

buyout of Migros for £3.2 billion. It has recently

invested in Mikro Yazilim, a software company,

alongside its other portfolio companies.

OFF THE RECORD

OVERVIEW

fuel at 20 airports. The total sales volume in 2016 was 10.68 million tonnes.

Otokar shares plunge after mass tank production not approvedStocks of Koç Holding’s Otokar plummet-ed almost 10% on June 12 after Turkey’s defense authority refused to accept the company’s offer to start mass production of the main domestic battle tank Altay. In a statement late on June 9, Otokar said its fi-nal offer to start the mass production of the Altay was found ineligible by the Undersec-retary of Defense Industry (SSM), due to disagreements over some contract terms, mainly over price, adding the authority would likely meet the need through a ten-der. The final offer included the mass pro-duction of 250 Altay tanks and their inte-grated logistic support operations, accord-ing to the statement. After Otokar stocks plummeted early June 12, its continuous trading was suspended and an order col-lection of the call auction period began, the company said June 12. After losing value by 16.9% in early trading, the company shares

slightly rebounded to a near-9.5% decrease at noon, Reuters reported.

More than 6,000 startups launched in Turkey in MayThe number of new companies launched in Turkey was 15.12% higher year-on-year in May, the Turkish Union of Cham-bers and Commodity Exchanges (TOBB) said in a report on Friday. Some 6,158 new companies started doing business in Tur-key in the month, which was also a 3.07% decrease compared with April 2017, ac-cording to the report. TOBB’s May figures showed an 8.20% month-on-month rise in the number of companies that went out of business, 792 in the month. The report also showed that 583 foreign-partnered or foreign-funded new companies were established in May. Some 174, or 28.8%, of foreign-partnered companies were found-ed directly by Syrian people or by Syrian nationals in partnerships.

TOURISM BUSINESS

5 PROBE

1 What is the current environment like in terms of Turkish assets?From last November until now, oil pric-es have fallen to their lowest level. The

US dollar is also at its lowest level since Pres-ident Trump’s election victory. The appe-tite for global risk has risen. One of the most concrete signs of this is the rise of worldwide stock exchanges. One of the most striking indi-cators of the increase in risk appetite is the fact that Turkey’s assets were relaunched and Bor-sa Istanbul (BIST), in which more than 60% of traded stocks are owned by foreign investors, reached a record-high of 100,000 points in one day.

2 How have global investors recently been approaching Turkish assets?Apart from the interest in tbe BIST,

global investors have in the last quarter bought Turkish assets exceeding $1.3 billion in block sales. Of this, $1.1 billion consists of Turkcell, Koç and Sabancı Holding shares. Elsewhere, Turkey’s leading jeans brand, Mavi, made an in-itial public offering worth $350 million, 70% of which was bought by global investors.

3 What is the level of interest in private funds within Turkey?Private funds have invested approxi-mately $1 billion in Turkish companies

in the last 12 months, despite the economic and political upheavals of 2016. For the first time since 2012, they have been partnering with Turkish companies at this level for the last 12 months. Over the same period, Turkish compa-nies have received the highest investment lev-els from private funds in Eastern Europe, cen-tral Asian countries and the Middle East.

4 Will the situation causing BIST records to be threatened persist? A weak dollar, low interest and strong

European growth are all generating a positive conjuncture. With no deterioration in this set of circumstances, it is expected that interest in the BIST and Turkish assets will continue in a fluctuating course. The profit capital ra-tio of Turkey’s 500 largest industrial corpora-tions exceeded 16% in a difficult year (2016) and banks’ profitability hit 13%. The 5% growth in the first quarter of 2017, which came after 3.5% growth in the last quarter of 2016, is lend-ing a positive air for the whole year ahead, even if this level of growth is not sustainable.

5 How will the Turkish market be influenced by developments in global markets?The external conjuncture is helping in

the appreciation of Turkey’s assets. According to the Institute of International Finance (IIF), $290 billion was invested in developing coun-try markets in the first four months of 2017. Another $4.3 billion from abroad entered into the stock and bond markets in the same peri-od. The process is expected to continue. Money entering developing countries this year will in-crease by 35% to $970 billion. Capital flows to emerging countries are expected to exceed $1 trillion in 2018.

6 How did the Fed’s interest rate hike affect Turkey?The Fed did not change its strong hawk-like stance at last week’s meet-

ing and retained its current strategy. The Fed pulled the policy rate down to 1.25, which in-creased the interest rates by 25 basis points

as expected. The Fed’s move did not negatively affect the Turkish market. The dollar against the lira, which had fallen below 3.50 just prior to the Fed’s decision, also maintained this lev-el after the interest rate increase. There was al-so no significant fluctuation on the BIST. The Turkish Central Bank’s monetary policy com-mittee, which gathered the day after the Fed’s announcement, kept all interest rates constant.

7 How will the Turkish economy be affected by the Qatar crisis?With less than a 0.5% share, it is not a particularly important country in

terms of exports, though Qatar does have more than a 5% stake in direct capital investments. This amount makes Qatar one of Turkey’s most important investors aside from the European Union. No negative development in the capital flow is expected, and there may be an increase in the short term. Exports are expected to in-crease, especially for food items.

8 Will the crisis affect Turkish contractors in Qatar?Until now, Turkish companies have done contracting business worth $17

billion in Qatar. The volume of active jobs, espe-cially those undertaken by Tekfen, is $5 billion. The new jobs Turkey has undertaken in Qatar and in countries disengaged with Qatar is also $5 billion, with $2.4 billion of it in Qatar. Expec-tations are that jobs within Turkish companies will not decline.

9 Will structural reforms be the new story in Turkey?An attempt to undertake comprehen-sive structural reforms under the cur-

rent conjuncture means giving up on growth in the upcoming period. It is hard to find a politi-cian who will take on the responsibility.

10 What is the likelihood of early elections in the com-ing period?There is little chance of there be-

ing an early general election this year because there is no preparation time. In addition, along-side revised expectations inside the Cabinet, which started with a predicted 12-strong minis-terial reshuffle, which was later pared back to five, it seems to have lost its priority on the agenda. In fact, expectations that the long-awaited Cabinet reshuffle will be not earlier than 2018 are increas-ing. The government insists the general election will be held, as planned, in November 2019.

Turkish assets

A host of evidence points towards strong foreign

interest in Turkish assets. What are the main threats

to a continuation?

Things aboutThings about

6POLITICS

Cabinet changes to chime in 2018

A new date – spring 2018 – for the keenly awai-ted cabinet reshuffle has been indicated wit-hin Parliament corridors. While the waiting period for a revised cabinet had been brou-

ght onto the agenda before the April 16 referendum it was again phased out after the referendum. The shift in expectations for cabinet changes to be delayed until 2018 is linked to the 180-day road map to be set out by congress and ministers. According to AK Party sources, the provincial and district conventions will be comple-ted by the end of this year. Following completion of pro-vincial congresses, the AK Party’s ordinary congress will be held in spring 2018, possibly in May. The main changes in the party and cabinet will take place after the ordinary congress following changes seen during the provincial and district congresses. This staff will carry the AK Party to the local, parliamentary and presiden-tial elections scheduled for 2019. The existing cabinet will continue for some time with the current ministeri-al team, who will complete their 180-day short-term ac-tion program by the end of this month so it can be imple-mented in July. The action program and its successful implementation will also determine whether ministers will receive posts all the way to 2019.

Parliament preparing for summer workPreparing to enter the summer holiday after having enacted the Manufacturing Reform Package and ad-justment laws for the High Council of Judges and Pros-ecutors, Parliament has returned to work on the in-ternal regulations of Parliament, with the president stating: “The current internal regulations are over and the AK Party and the MHP will join forces and hopefully hand it over.” The AK Party has prepared a proposal for amendments to the 30-point internal regulation that would accelerate the adoption of the new Constitution and the work of Parliament. Expectations are that this 30-item proposal, which has already been presented to the prime minister, is to be enacted in July with the sup-port of the MHP.

Steps towards adjustment legislationThe government has initiated legislative amendments to the Constitution, which was changed after the April 16 referendum. The negotiating process has begun for the first harmonization package, which includes the amendment of 132 articles within 16 laws including the Military Penal Code, the Judges Prosecutors’ Law, the Constitutional Court, the Council of State Law and the Supreme Court Law. Internal regulations and the judi-cial package will be enacted first, while the six-month period for adjustment laws is currently in progress. CANAN SAKARYA / ANKARA

C O M M E N T A R Y O N T H E N E W S

I was harshly criticized by one of my readers after I had argued that arrested journalists should be released pending trial. “Let’s ask the public about their articles and speeches, will the people think they are innocent?” said the critical fellow. Who should decide who is “guilty” or “innocent”, an independent judiciary or the nation? …No doubt, the idea that people are becoming political subjects is a positive development. Unfortunately, the rule of law and the checks and balances did not run parallel to this notion. So the “national will” was identified with the majority party. It should be called “majoritarian democracy” and it is authoritarian. Today, there are defeats on the basis of instability and tensions. Since the idea of “rule of law” is not established, we look at every subject politically, judicial independence is not institutionalized in any period, the judiciary has always been viewed as a political instrument. The Supreme Court has even approved the state of emergency to be a regime outside law’s control! ...In today’s stage of democratic development, our sore and urgent need is “the rule of law”. Law cannot be superior without “checks and balances” as the judiciary knuckles under politics. What should be asked of the public is who will be given legislatory and executive powers, and exceptional referendum issues.

A person from Ankara speaks at a fast-breaking dinner. “Anyone a little bit critical is excommunicated. When people mention their constructive criticism for the better, they say: ‘No, you have no right to criticize,’ or ‘You are Gulenist’. ...We are being isolated and marginalized. That’s why everyone is so afraid and silent. What is going on, for God’s sake? Who do lynch mobs take courage from? Why are they not stopped?” ...People lost confidence in each other. The best way is to stay silent, take no risks, never speak… This is the solution that many people prefer. But a friend who tells the truth is a blessing. ...The greatest danger for a society is loosing its faith in justice. Whatever happens, you have to give people the right to defend themselves. People who have been under arrest for months have not yet been taken to court. We need to speed up. They may be released if their case is looked at. …Being unfair is the first step on the path of corruption. It is so dangerous to pass that critical threshold. The right of the individual means the right of society. Being unfair regarding this corrupts society. It is the only sin that cannot be forgiven.

Husamettin Cindoruk, a veteran right-wing politican, expressed his important and pessimistic findings to a Cumhuriyet reporter. “The one-party period has begun. There is no light at the end of the tunnel,” he said. It is impossible not to agree with Cindoruk who says the possibility of a sustainable democracy in Turkey has been lost. The only possible objection is that the regimes that are in force and will begin to be implemented in two and a half years are not “semi-presidential” and “presidential”, either of which can be described as totalitarian one-man regimes. ...The multi-party system, which was brought to life through the sincere and persistent efforts of the leader of the then one party and founder of the Republic (Atatürk), has failed to repeat the success demonstrated by the previous one-party regime that led to it. The multi-party regime failed to transform from a multi-party state to pluralism, while the one-party system did succeed in transforming into a multi-party system with democratic methods. ...Today’s one-party regime lags far behind the one-party regime of Ismet Inonu because that particular one-party system was facing a multi-party system and democracy. Today’s religious one-party system has turned to a one-man system and a growing totalitarianism.

YENI SAFAKJune 13

KEMAL OZTURK

CUMHURIYETJune 12

ALI SIRMEN

HURRIYETJune 13

TAHA AKYOL

What should we ask the

public?

Right to criticism, right

to defend, rightful share

Even worse than

one-party state

7 BUSINESS BY LAW

Retail industry lease agreements: a two-dimensional view

The retail industry has led the Turkish economy in recent years and shop-ping malls are the most

essential part of the industry. Shop-ping malls have recently undergo-ne a challenging period by virtue of social and economic developments throughout the country. Tending to grow together, they have faced substantial declines as to decrea-ses in footfalls due to recent adverse events as well as a reduction of the consumption appetite due to eco-nomic constriction. In this trend, shopping malls have been adversely affected regarding leases, since re-tailer profitability has declined and foreign exchange rates have increa-sed significantly.

The fact that shopping mall rents are determined by foreign curren-cies creates an independent con-cern on account of the retail in-dustry. Thus, retailers have been demanding incentives from shop-ping mall managements such as a fixed exchange rate, rent reduc-tion or payment possibilities in the domestic currency. Alternatively, since retailers’ revenue feasibili-ties are figured out by an expecta-tion of foreign exchange income, shopping mall investors who most-ly paid back their loans in foreign currency for at least five to nine years were forced to be cautious regarding the aforementioned de-mands.

Today, 118 of 371 shopping malls in Turkey are collecting their rents in domestic currency, namely Turk-ish lira, meanwhile the remaining 253 are collecting in foreign cur-rencies. Six of these foreign curren-cy-collecting shopping malls have

converted their lease agreements and started to collect in Turkish li-ra, as a consequence of President Recep Tayyip Erdogan’s call that those who had drafted their lease agreements in foreign currencies should amend the payment clauses by means of determining Turkish li-ra as the new payment instrument.

This article evaluates the cases and possibilities of adaptation of rents in the retail industry in the light of essential adverse develop-ments from the two perspectives of shopping malls and retailers.

Conditions to allow demand of le-ase rate adaptation for deduction purposes In view of the aforementioned prec-edents, the existence of all four con-ditions is required for the adapta-tion of rent amounts. These are:

1) An unexpected development that cannot be foreseen by the par-ties should arise during a long con-tractual term

2) Such an extraordinary devel-opment should arise under a reason not originated from the lessee

3) Conditions determined at the commencement date of the rela-tionship should have essentially changed against the Lessee due to such an unexpected development

4) The lessee, at the time of ad-aptation request, should either not perform its obligations or should perform such obligations with the reservations of the adaptation re-quest.

Contractual status of retailersRegarding lease agreements be-tween the merchant parties, the Su-preme Court strictly interprets the

condition of predictability where courts expect a prudent merchant to envisage a crisis and locate the risk of fluctuation on foreign ex-change rates in advance. For in-stance, despite the fact that Tur-key’s inflation rate does not change regularly, an adaptation claim re-garding the contract concluded af-ter the February 2000 crisis, the period from when adaptation de-mands are accepted, has been re-jected on the ground that “a prudent merchant should have foreseen the economic changes during a crisis period.”

From the view of shopping mall investorsIn light of legislation and legal prac-tice, the position of the shopping mall investor seems crystal clear. However, even the legal protection shield protects lessors until the Su-preme Court change its approach; the reality is that a shopping mall may only protect its value with a strong and sustainable shopping mix and brands. Therefore, even if the shopping mall investor seems to be protected by the law against retailers’ adaptation requests, it is clear that they should not remain unresponsive to retailers’ expecta-tions. The big picture demonstrates the fact that industry players can only win together.

ConclusionWhen we review the current con-juncture of Turkey – aside from the uncertainty of the inflation rate, de-valuations of the past, or current ex-change rate fluctuations – the fact that Turkey has faced with difficult socio-economic developments, consecutive terror attacks, the coup attempt on July 15, 2016 sequent negative events, and after recent events affecting the economy such as the US presidential elections; it is foreseeable that industries will be negatively affected. However, in re-cent history, there is no court rul-ing that formulates the solution as the inflation increase as double or such will not be deemed as an un-foreseeable extraordinary occasion. When past court rulings and the Su-preme Court’s general attitude have been taken into consideration, it is a moral certainty that courts would evaluate and rule the Turkish mar-ket conditions as foreseeable.

Despite the aforementioned real-ity in Turkey, shopping mall inves-tors do evaluate, and also should, under a sustainable win-win prin-ciple that the parties need each oth-er for life for the creation of an envi-ronment that provides a long-term profitable market.

VEFA RESAT MORAL, MANAGING

PARTNER, MORAL LAW FIRM

The opinions expressed in this page are the author’s own and do not reflect the views of the firm and the publication or any other individual attorney.

8BUSINESS

Politico-economic landscape behind Turkish M&A decline

Turkey experienced a significant decline in mergers and acquisi-tions in 2016 after be-

ing negatively affected by the glob-al political and economic uncer-tainties of the past year, as the volume of M&As in the country decreased by 53 % to a value of $7.7 billion.

In addition, market conditions and internal unrest in the coun-try contributed to a considerable decrease in investor interest in the Turkish M&A market in 2016, with the country recording its lowest cross-border M&A figures since 2009. This reflected the lack of social, economic and political stability in Turkey.

Of course, 2016 was a difficult year across the whole world. With echoes of Brexit still reverberat-ing, concerns about the result of the US presidential election tra-versed the globe. The OPEC sum-mit, Italy’s referendum and pro-posals by the US Federal Reserve to raise interest rates followed. In the Middle East, the impact of political uncertainty, security is-sues and a mounting refugee crisis spread to Europe and the US.

Decreasing numbers In January, reputable indepen-dent auditing and consultan-cy firms such as Deloitte, Ernst & Young and PwC, published their annual reports which in-cluded analyses of the Turkish M&A market. Although the re-ports showed slight differences, the overview of the 2016 Turk-ish M&A market can be captured succinctly in numbers. The to-tal deal volume in 2016 in Turkey was around $7.7 billion via 248 transactions, 53 % less than in

2015, which totaled around $16.4 billion through 245 transactions.

In 2015, foreign investors were involved in 125 deals, while for-eign investors carried out only 93 transactions in 2016. The to-tal deal volume for these transac-tions was around $3.8 billion in 2016, set against around $11.5 bil-lion in 2015. Thus, the total annu-al volume of deals involving for-eign investors in 2016 decreased by 67 % year-on-year, plummet-ing to one of its lowest levels in history.

Despite a changing investment flow in the Turkish market due to various internal and external fac-tors, foreign investors have in the past typically maintained their investment activities with an un-derstanding of the risks involved. However, investor risks became “unforeseeable” over the course of 2016, surpassing the circumstanc-es to which they had become ac-customed. This was due to a com-bination of domestic and interna-tional political events, increasing geopolitical risks, security issues, the attempted coup d’état and the resultant national state of emer-gency declared soon after.

Political crises with Germany and the Netherlands followed, re-sulting in serious tensions with

countries that had once been among the country’s top foreign investors. The reduction of Tur-key’s credit rating by international rating agencies and fluctuations in exchange rates also had an impact on the local economy and M&A market. The devaluation of the Turkish lira caused foreign inves-tors to significantly reduce their interest in non-exporting Turkish companies that generated insuf-ficient income as a result of weak exchange rates.

Changing investor profile In 2016, investors from the US, the UK and Japan topped the list of deal numbers. But the foreign investor profile changed in 2016. Interest in Turkish M&A by Qa-tari, South Korean, Japanese and Chinese investors increased, while deal numbers for Western investors declined by 36 % (from 90 deals in 2015 to only 58 in 2016). That said, with respect to the transactions reported to the Turkish Competition Authority, investors from the Netherlands and Germany did top of the list. That is likely to be because for-eign private equity funds deter-mine bidder companies in those countries.

In 2016, Turkish investors at-

tained an annual deal volume of around $3.9 billion through 155 transactions – a 20 % decrease compared to 2015. Considering the Turkish M&A market also suf-fered in 2015, the current situation is not looking promising.

Technology and energy sectors at the forefront In 2016, most of the deals in the Turkish M&A market were real-ized in the information and mo-bile services, technology and en-ergy sectors. Energy was by far the leading sector in terms of deal value, while the information sec-tor was first in terms of number of deals. Furthermore, manufac-turing and financial services were among the more prominent mar-kets in 2016. These sectors are ex-pected to attract the most invest-ments in 2017.

2017 may be promising Current circumstances make it difficult to expect significant pos-itive developments in 2017. It is anticipated that political and eco-nomic uncertainties, currency fluctuations and security issues may continue to affect the Turkish M&A market negatively this year.

The constitutional referendum on 16 April 2017 marked a critical milestone in Turkey, which could lead to a better year. Moreover, al-though 2017 may still fall short of Turkey’s potential, privatization of the Privatization Administra-tion’s portfolio along with com-pletion of transactions suspend-ed to limit the negative effects of the currency could still paint a promising picture for Turkey’s future. UMUT KOLCUOĞLU

Turkish M&A market numbers in 2016The total volume of M&As in Turkey in 2016 decreased by 53 % to $7.7 billion through 248 transactions. The number of transactions carried out by foreign investors declined by 67 % to 93, totaling $3.8 billion in 2016.

Interest in Turkish M&As by Qatari, South Korean, Japanese and

Chinese investors increased, while deal numbers for Western investors declined dramatically by 36 %.

Turkish investors attained an annual deal volume of around $3.9 billion via 155 transactions with a 20 % reduction compared to 2015.

9 BUSINESS

Prysmian Group Turkey exports high-level executives from Bursa

Manufacturing in 82 facilities within 50 countries and with 30,000 employers

worldwide, Prysmian Group is the cable industry leader and its Bur-sa manufacturing facility one of the largest three factories within the group.

Besides cable manufacturing, the factory located in Mudanya de-termines the highest management of the group with the staff it trains within the group’s academy. “We don’t only produce cables. It’s a ca-ble school here,” says Prysmian Group Turkey CEO Erkan Aydog-du. “We also train the production managers and facility managers of a world leading enterprise.”

A total of 111 employers were trained last year, with 120 em-ployers being trained in 2017. There are mid- and high-level ex-ecutives among the trainees who are set to play a part in the compa-ny’s future. Many executives who now serve as high-level executives around the world within Prysmian Group started working at the Bur-

sa factory. Just like Aydogdu, who started working at the Prysmian Bursa factory in 1997 when it was Siemens, the most important re-gion for the group, Prysmian America, also has a Turkish CEO who is in charge of 13 facilities in the US. Besides him, many fac-tory managers in several coun-tries are former Bursa employers. The general director responsible for manufacturing in Asia is also Turkish. In addition, the Eastern Europe investment director is al-so Turkish. In fact, 13 Turks serve as high-level executives within Prysmian Group worldwide.

“We send many of our col-leagues to facilities abroad for giv-en periods. Actually it’s our mis-sion,” says Aydogdu. “We have a motivating role for other facto-ries. We may be good at one thing, but it’s not enough. We seek to be the best and force this.” All em-ployers within the group are as-sessed through a common system in terms of KPIs and behaviors. The system is called “Prysmian, People, Performance (P3) and

“Prysmian, People, Performance, Potential (P4)”

“We wrote a success story still resonating within the group”Asked why the group chose Tur-key and Bursa especially, Aydog-du notes: “Some characteristics of Turkish people turn into valuable raw materials when processed cor-rectly. For instance having a quick mind, being result-oriented or flex-ible, etc. Prysmian Group became a part of the standardization system of SAP in 2007 known as ‘One Cli-ent’. In the countries first adapting the system, deliveries couldn’t be made for two to three months. But we started our deliveries only two days after adapting the system. So we wrote a success story still reso-nating within the whole group…”

Aydogdu continues: “To meet the incremental demand in fiber optic cable and to ease off the cur-rent production line there had to be an investment made.” He noted that it was impossible to shut down the whole production during the 30-40 days of the investment pro-cess. They were told whether or not to make the investment or do it by shutting down the production. Aydogdu states that they founded a team of 22 employers and planned what needed to be done. “We start-ed in the afternoon on 30 Decem-ber. We put the system in use on the

night of 31 December. We were all here on New Year’s Eve and ate din-ner together. The next day we in-formed Italy that we had completed the investment. We became a mod-el with our pace. We have plenty of such examples,” boasts Aydogdu.

“As in the Draka example, there may be new acquisitions” Prysmian Group Turkey started to meet the demand from Turkey’s en-ergy and telecommunications sec-tors with the factory established in Mudanya by Siemens in 1964. The company became part of the Pirelli family along with many other Sie-mens Cable enterprises in 1999. As a result of a share transfer in 2005, the factory started operating un-der the name Prysmian. Then, af-ter merging with Draka in 2011, Prysmian was named Prysmian Group globally. Aydogdu signals that there may be new acquisitions such as the Draka example. Stating that there are differences between the strong sides of both Prysmian and Draka, Aydogdu says: “The merger of these two groups blended their fund of knowledge. Our com-pany doesn’t acquire companies simply to acquire them. As in the Draka example, it aims to build the right partnership at the right time. There may be new acquisitions.”

OMER FARUK CIFTCI

E S RA OZARFAT - BURSA

“Turkey factory functions as a bridge within the group”Prysmian Group Turkey manufactures on 180,000 square meters of land, 79,000 of which is closed. Publicly traded at Borsa İstanbul, Prysmian Group Turkey employs 450 people. With a capacity utilization rate of 89% in 2016, Prysmian Group Turkey is also the export hub of the group. A total of 29% of its turnover of 953.5 million TL last year was in exports to more than 40 countries among a broad geography such as Azerbaijan, Barbados, China, France, Iraq, the UK, North Africa, Middle Eastern countries, Papua New Guinea, Sri Lanka, Chile, Turkmenistan and Jordan. Some 86% of its sales are generated

from energy, 10% from telecommunications and 4% from fiber cables. Its capacity is almost threefold of an average cable factory. In terms of energy units, its annual capacity is 55,000 tones. Its copper capacity for telecommunication is 1.2 million double kilometers and 500k for fiber kilometers. Its Bursa factory is the only factory within the group that can manufacture all three items under one roof, with 22 types of cables manufactured. Despite manufacturing predominantly energy cables in Bursa, Prymsian is one of few enterprises that can produce its own fiber.

10ANALYSIS

Economy strengthens but is it sustainable?

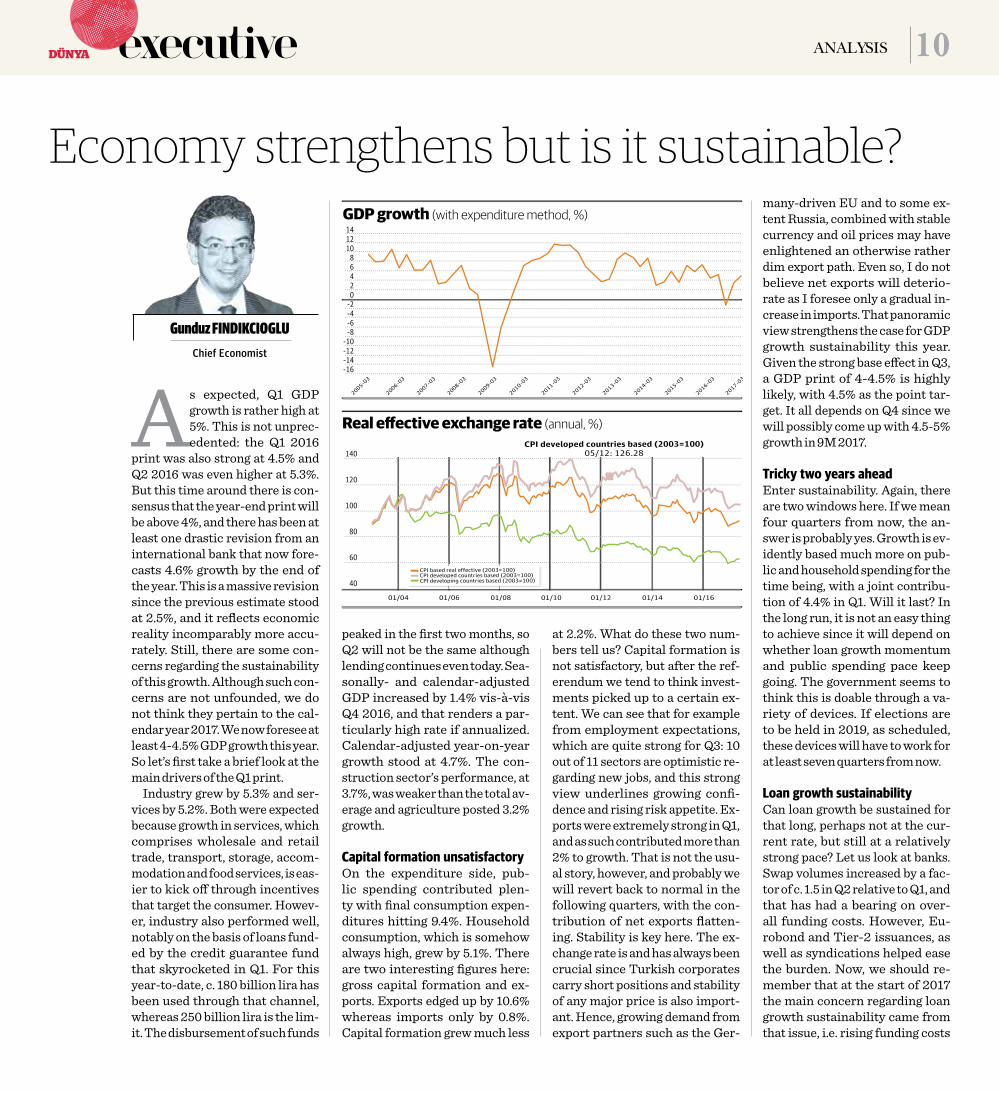

As expected, Q1 GDP growth is rather high at 5%. This is not unprec-edented: the Q1 2016

print was also strong at 4.5% and Q2 2016 was even higher at 5.3%. But this time around there is con-sensus that the year-end print will be above 4%, and there has been at least one drastic revision from an international bank that now fore-casts 4.6% growth by the end of the year. This is a massive revision since the previous estimate stood at 2.5%, and it reflects economic reality incomparably more accu-rately. Still, there are some con-cerns regarding the sustainability of this growth. Although such con-cerns are not unfounded, we do not think they pertain to the cal-endar year 2017. We now foresee at least 4-4.5% GDP growth this year. So let’s first take a brief look at the main drivers of the Q1 print.

Industry grew by 5.3% and ser-vices by 5.2%. Both were expected because growth in services, which comprises wholesale and retail trade, transport, storage, accom-modation and food services, is eas-ier to kick off through incentives that target the consumer. Howev-er, industry also performed well, notably on the basis of loans fund-ed by the credit guarantee fund that skyrocketed in Q1. For this year-to-date, c. 180 billion lira has been used through that channel, whereas 250 billion lira is the lim-it. The disbursement of such funds

peaked in the first two months, so Q2 will not be the same although lending continues even today. Sea-sonally- and calendar-adjusted GDP increased by 1.4% vis-à-vis Q4 2016, and that renders a par-ticularly high rate if annualized. Calendar-adjusted year-on-year growth stood at 4.7%. The con-struction sector’s performance, at 3.7%, was weaker than the total av-erage and agriculture posted 3.2% growth.

Capital formation unsatisfactoryOn the expenditure side, pub-lic spending contributed plen-ty with final consumption expen-ditures hitting 9.4%. Household consumption, which is somehow always high, grew by 5.1%. There are two interesting figures here: gross capital formation and ex-ports. Exports edged up by 10.6% whereas imports only by 0.8%. Capital formation grew much less

at 2.2%. What do these two num-bers tell us? Capital formation is not satisfactory, but after the ref-erendum we tend to think invest-ments picked up to a certain ex-tent. We can see that for example from employment expectations, which are quite strong for Q3: 10 out of 11 sectors are optimistic re-garding new jobs, and this strong view underlines growing confi-dence and rising risk appetite. Ex-ports were extremely strong in Q1, and as such contributed more than 2% to growth. That is not the usu-al story, however, and probably we will revert back to normal in the following quarters, with the con-tribution of net exports flatten-ing. Stability is key here. The ex-change rate is and has always been crucial since Turkish corporates carry short positions and stability of any major price is also import-ant. Hence, growing demand from export partners such as the Ger-

many-driven EU and to some ex-tent Russia, combined with stable currency and oil prices may have enlightened an otherwise rather dim export path. Even so, I do not believe net exports will deterio-rate as I foresee only a gradual in-crease in imports. That panoramic view strengthens the case for GDP growth sustainability this year. Given the strong base effect in Q3, a GDP print of 4-4.5% is highly likely, with 4.5% as the point tar-get. It all depends on Q4 since we will possibly come up with 4.5-5% growth in 9M 2017.

Tricky two years aheadEnter sustainability. Again, there are two windows here. If we mean four quarters from now, the an-swer is probably yes. Growth is ev-idently based much more on pub-lic and household spending for the time being, with a joint contribu-tion of 4.4% in Q1. Will it last? In the long run, it is not an easy thing to achieve since it will depend on whether loan growth momentum and public spending pace keep going. The government seems to think this is doable through a va-riety of devices. If elections are to be held in 2019, as scheduled, these devices will have to work for at least seven quarters from now.

Loan growth sustainabilityCan loan growth be sustained for that long, perhaps not at the cur-rent rate, but still at a relatively strong pace? Let us look at banks. Swap volumes increased by a fac-tor of c. 1.5 in Q2 relative to Q1, and that has had a bearing on over-all funding costs. However, Eu-robond and Tier-2 issuances, as well as syndications helped ease the burden. Now, we should re-member that at the start of 2017 the main concern regarding loan growth sustainability came from that issue, i.e. rising funding costs

Gunduz FINDIKCIOGLUChief Economist

11 ANALYSIS

Regarding asset quality, we have seen Non-performing Loan (NPL) sales albeit at a deeper discount – 5.5% rather than the previous 10% – but they can still be sold. For banks, the discount is not that important: what matters most is liquidity. So, a 3.2% NPL ratio is almost stable although it would have been above 4% without sales. Sales continue, and 3 billion lira NPLs have already been sold year-to-date. That is small compared to balance sheets, but they help at the margin. Loan reserve requirement ratios have been lowered, and that also rather helped. As for the guar-anteed loans that grew at break-neck speed in Q1, they are mostly 1-2 years maturity. The impact on asset quality will not be visible be-fore Q2 2018 at the earliest.

In short, if EM appetite endures a banking system with a 3.2% NPL ratio and reduced requirement ra-tios, 16.4% capital adequacy ratio, with a prospect for multiple ex-pansion in valuations, one could easily ink in 16% Return on Aver-age Equity (ROAE) and 22% as-set growth in 12 months’ time. If FX-loans are to be securitized with the state acting as leader and sold overseas, especially project fi-nance and large corporate loans, there will be plenty of room and liquidity ahead. That is, unless things turn upside down and EMs are screened with a fine-grained

lens as a result of both the Fed and ECB’s balance sheet contractions that lay ahead. This is my main concern since rate hikes are pre-dicted, but a combined balance sheet/interest rate sea-change might have a large impact on pric-ing for EM assets of all sorts. Oth-erwise, the banking system may keep going at high speed as it is for at least the next year. We should al-so keep in mind that 85% of loans disbursed through the credit guar-antee fund are covered by the state. This is important since the advent of IFRS-9 will reduce the leeway provided by the regulator in terms of loan reserve requirements.

Monetary policy not behind growthThe Treasury has borrowed at high ratios. Nevertheless, in the short run that could be good as it provides liquidity to the bond market. May 2017 budget figures showcase a positive development, but for the first five months the deficit is 11 trillion lira. That may go on for yet another while but not forever. We do not see that as a cru-cial concern though, as we consid-er a rather considerable slack on that front. Alternatively, the Cen-tral Bank’s recent no-change poli-cy looks admissible especially giv-en that growth is high and there is a net exports component in it. The exchange rate is clearly compet-

itive as shown by the graph that depicts historical data. In other words, at 3.50 to the dollar, the li-ra is still cheap in a sense. Mon-etary policy is rather flexible in a nice sort of way. What this means is the central bank doesn’t have to change the policy rate since the average funding rate – at c. 12% is tight – and the late liquidity rate – 12.25% – is high. The central bank can always change the weights of the funding mix and lower its av-erage funding rate without touch-ing any of the particular interest rates. It makes sense to assume that, if inflation trends down to be-low 10%, the bank will seize this opportunity to lower the late li-quidity rate, but even without do-ing so it has the flexibility to adjust the effective rate down. We should note that at lira deposit rates hit-ting 15%, loan rates at around 17-18%, and the average funding rate at 12%, there is still 5% GDP and 10.6% export growth. We might al-so remember that in the previous monetary policy committee meet-ing of the central bank, the aver-age funding rate was barely around 11.5%. Hence, since mid-April the monetary policy stance was clear-ly tight, and that tightness con-trolled the exchange and to some extent the inflation rates. Growth stimuli did not come from mon-etary policy, but from the cred-it guarantee fund, from the regu-lator’s bank-friendly stance and from public spending.

Decent outlookWith the end of the currency pass-through and lower food prices, as inflation recedes down to below 10%, which is more likely than not to happen this year although for most of the year low double-digit inflation will be persistent, the cen-tral bank may find an opportunity to fine-tune its stance and loosen a lit-tle. So, this is the view now: 4-4.5% GDP growth, 9-10% CPI, slightly lower funding/loan/deposit rates, 16-17% ROAE and CAR, 22-23% as-set growth. Not bad, huh?

in a world where the Fed would hike further – which it did and will continue to do so – and the expect-ed rating downgrade, which hap-pened by the way with an initial 40 bps cost impact. Both negative incidents took place, but with no visible consequences. The cred-it guarantee fund played a huge role there, which caused a 123% increase in commercial and SME credits channelled through that device. Still, the loan-to-depos-it ratio for lira credits reached 150%. Lira deposit rates went up to 15% as a result. Nevertheless, loan rates also went up and with the help of dividends, Q1 banking sector performance proved quite good. As expected, Borsa Istanbul (BIST) 100 recently hit 100.000. Even so, we cannot talk of a multi-ple expansion since Turkish banks trade at 0.9 PB and 6.1 PE, with 38% discount relative to emerg-ing market (EM) peers. Although multiples stayed flat, stock pric-es went up because balance sheet and P&L developments shored up such an increase. Now, it all de-pends on the consequences of the Fed’s likely further hikes and the Central Bank’s future stance. If EM appetite goes on, even as the Fed continues to hike, the late li-quidity window may be left to die off, and Turkish lira-denom-inated 10-year Treasuries could tend down towards 10%. This would cause a multiple expansion through the valuation discount rate. Oversold Turkish assets were in 2H 2016, and what we see is a partial recovery of that past move-ment, without multiple enhance-ment.

Stable lira plays its partLira stabilization within the 3.50-3.60 band in relation to the dollar has helped tremendously since banks do not carry short positions, but corporates do. It helped im-prove business sentiment, and al-so helped exports boom to some extent. Again, currency stabili-zation is key to everything here.

12GEOPOLITICS

The unwitting surren-der of U.S. hegemony has allowed Russia, on-ce thought to have been

sidelined for decades after the col-lapse of the Soviet Union, to incre-mentally expand its influence. Just as the Soviet collapse was not anti-cipated, the diagnosis for that col-lapse was weak, prompting specu-lation that it would not recover for some time. In fact, it has.

The death late last month of stra-tegic genius Zbigniew Brzezinski prompted me to revisit an inter-view he gave long after the end of the Soviet Union in which he dis-cussed the United States’ support of the mujahideen in Afghanistan against the Soviets. The aim was to draw Moscow into a quagmire, forcing it to deplete its already waning resources, resulting in the defeat of the main U.S. rival, Brzez-inski, a former U.S. national securi-ty adviser, said.

As the Soviets pursued their am-bition to prove they were a super-power, they failed to see that their resources were not of a scope to support this dream, wasted those resources and, in the end, were ex-hausted and splintered. The les-son that emerges for any leader that wants to dominate a region, or even the world, is that when a na-tion seeks to realize a foreign pol-

icy for which it lacks the adequate underpinning, it may herald its own undoing.

It is important to note that once a policy is implemented, it may be-come impossible to change it, even when it is clear that it will fail. In other words, you can fall hostage to your own policies.

In Afghanistan, when the Sovi-ets were met with setbacks at the outset, they felt compelled to devote more resources than they had antic-ipated to the intervention to prove their strength and protect their prestige. In insisting on this show of force, they were greatly weakened and, eventually, collapsed.

It would be an oversimplifica-tion to tie the fall of a nation to one event. Adam Przeworski, a polit-ical scientist of Polish origin, like Brzezinski, points to the loss of faith in the ideals that the Soviet Union projected, spurred by cor-ruption and poverty, so that even those served by the system could no longer defend it.

Therein lies a second lesson. No matter how much the rulers of a country speak of morality, hones-ty and other lofty ideals, if these are

apparent during the implementa-tion of policies, an indisputable par-adox emerges.

Russia todayLet’s fast forward three decades. While Russia’s recovery may not be terribly impressive at first glance, it is clear that there is no absence of a state, and no one ex-pects Russia to be thrust into cha-os and break apart.

True, it is grappling with eco-nomic challenges; its economy is fragile and far too dependent on natural and raw resources. Other than commodities, it has few ex-ports. The government spends its budget on defense and not on pro-ductive investments.

Yet Russia has again been elevat-ed to the status of a global arbiter. Little remains of the country in ru-ins that former president Boris Yelt-sin left behind in 1999, when he was succeeded by President Vladimir Putin. Though much of this success may be down to the high global oil prices of the 2000s, allowing Russia to rebuild its economy, another key factor cannot be overlooked.

The disintegration of the Soviet

Union came with the acceptance by the elite who ruled the country that they could no longer sustain its uni-ty. Beginning with the Baltic repub-lics, the other members of the feder-al union split off without a fight.

But the institutions of that federal system remained standing. The So-viet army, which was always domi-nated by the Russians, turned into the Russian armed forces. Today’s Russian Foreign Ministry bears lit-tle difference from its Soviet prede-cessor; most of the diplomatic corps is still educated at an academy dat-ing back to the Soviet period.

Institutional continuityThese examples of institution-al continuity were, without a doubt, key to Russia’s rapid recov-ery. Building the institutions of state from scratch is difficult and time-consuming. Had the cadres that came to power in Russia top-pled the organizations they were left, they would have struggled to build new ones and would have been beholden to the services these institutions provided.

This perspective offers a third lesson from the Russian experi-ence. The administrators of the state should protect the institu-tions that they inherit and not for-get that they can benefit from them. Sure, these institutions may not al-ways allow those in power to do as they please. Yet they also reduce the chances of mistakes and increase the odds that decisions and policies are successfully implemented.

The Soviet and Russian example offers a humbling message to rapid-ly rising countries and their polit-ical rulers, whose self-confidence knows no bounds and who often fail to see likenesses in historical realities.

Russian experience offers lessons for political leaders elsewhere

Ilter TURAN Columnist

13 COMMENTARY

Growth certainly rose, but to what extent?

The 5% growth surprise from nowhere

Allow me to issue a remin-der that growth was 4.5 percent in the first qu-arter of last year and wi-

de-ranging expectations were be-ing predicted. First-quarter growth was foreseen to be between 2 per-cent and 5 percent. Why was it so difficult to more accurately forecast growth?

Due to the new GDP series, mak-ing a forecast is complicated. In plain words, the old GDP amount was cal-culated based on TurkStat figures. But the new GDP calculation is

based on both administrative and Fi-nance Ministry records. All of which means it is difficult to make a GDP forecast based on short-term busi-ness statistics and we have certainly seen the result of this complication.

For instance, the industrial pro-duction increase for the first quar-ter in comparison with the same pe-riod last year was only 1.8 percent, according to TurkStat data, but the growth of industrial production as a share of GDP amounted to 5.3 per-cent. How can we explain the differ-ence between these two figures and

wouldn’t it be better if we had closed this gap? Dunya asked these ques-tions to TurkStat Deputy Chairman Mehmet Aktaş.

Aktaş noted that the statistical body is working intensively on cal-culating the short-term business statistics, which include the in-dustrial production figures based on administrative records. He said new short-term business statistics will be based on 2015 figures and that TurkStat is trying hard to com-plete the new calculations by the be-ginning of 2018.

Industry-led growthThe industry sector, with a one-fifth share of GDP, was largely re-sponsible for pulling growth up to 5 percent in the first quarter. As mentioned, there was an increase of 5.3 percent in industrial produc-tion. Elsewhere, there were respec-tive increases of 3.2 percent and 3.7 percent in the agriculture and construction sectors. Meanwhile, the service sector, including trade, transportation, accommodation and food services, generated an add-ed value increase of 5.2 percent.

The Turkish economy surpassed all expecta-tions to grow by 5 per-cent in the first quarter

of 2017. This figure is, in a sense, a consequence of all the measures taken to revive the economy in re-cent months. Some warnings ha-ve been made that such measures may well distress the economy in the future. That is indeed possible as Turkey is trying to drive a wind-will with a pair of bellows right now and is currently succeeding. Things may become complicated in the future and growth could cau-se distress elsewhere in areas such as increased inflation, though that is a matter for debate.

Let’s assume that this growth of 5 percent was achieved with only healthy measures that won’t trou-ble the economy. Let’s assume the annual growth will also be 5 per-cent for the whole of this year.

Even so, there are some other facts we have to consider. Facts, that is, and figures released last week by TurkStat, originating from Eurostat, the statistical office of the European Union…

Turkey has a long way to comeIndeed, Turkey has been among the fastest-growing countries in the world over the last couple of years. But even with such rates of growth, it’s been impossible to catch up with the fastest-growing economies in Europe.

Eurostat calculates income per capita based on purchasing pow-er parity (PPP), takes the EU aver-age as 100 and ranks all 28 member countries. So, the average of 100 for the EU is only 62 for Turkey. In oth-er words, Turkey is 38 percent be-hind the EU average on a PPP basis. To express the situation more gen-erally, whereas the average income

per capita for 28 EU countries is three, Turkey has an average of an inch below two.

Only eight countries in Europe – Romania, Croatia, Montene-gro, Macedonia, Serbia, Bosnia and Herzegovina, and Albania – have less income per capita based on PPP than Turkey. The richest country in Europe based on PPP is Luxembourg, followed by Ireland, Switzerland, Norway and Iceland.

Real personal consumption According to a statement made by TurkStat, developmental compar-ison was based on Gross Domes-tic Product (GDP) per capita, and real personal consumption index-es were more reasonable to use to compare consumers’ level of wel-fare. TurkStat underlined that re-al personal consumption does not only include goods and servic-es but also education and health services provided by the state or non-governmental organizations. So, what is Turkey’s real person-al consumption status? Unfortu-nately, as it stands in the PPP ba-sis income per capita, Turkey does

not rank well for real personal con-sumption.

The average for 28 EU countries is accepted as 100 and the real per-sonal consumption level of Turkey was calculated as 61 for 2016.

Luckily, we have low pricesTurkey has low GDP per capita based on PPP. It also has a low re-al personal consumption level. But luckily Turkish residents have an-other low figure in their favor: the price level in Turkey is far below the EU average. TurkStat’s state-ment noted: “If a country’s price level index is higher than 100, it means it is a relatively ‘expensive’ country compared with others. But if its price level index is lower than 100, it means it is a relatively ‘cheap’ country.”

Turkey remains far below the EU average in terms of price lev-els relating to real personal con-sumption. Turkey’s price level in-dex is around 55. So where goods and services can be bought for 55 euros here, it requires 100 euros to buy the same goods and services in EU-member countries.

Alaattin AKTASEconomist

14COMMENTARY

Transition to production-based growth required

In recent times, we have be-come accustomed to the fact that growth rates have con-sistently reached beyond

our expectations, especially since the calculation method was alte-red. As a matter of fact, this is the case we’ve been facing in the first quarter of 2017. The general expe-ctation among analysts had been for 3.8% growth ahead of the data. But the actualization was a whop-ping five.

When forecasting growth, the most considered parameters are ‘not adjusted’ figures and the man-ufacturing industry growth rate. It was expected that this figure and the manufacturing industry increase rate used in GDP calcu-lations would be close. The man-

ufacturing industry production increase rate was 1.5% in the first quarter, but the manufacturing in-dustry increase rate used in GDP calculations, which is based on economic territories, was 5.1% for the same period. The gap can’t be explained only by a difference in the methodology of calculations – and this has been going on for three years. According to the new series manufacturing industry in-dex, the average monthly increase rate since the first quarter of 2013 has been 3.0%. Despite this figure, the average manufacturing indus-try share of GDP amounts to 6.1%.

Similarly, the service sector – another big economic territory – has also achieved a respectable high growth rate of 5.2%. Howev-

er, the ‘retail sales volume index’ calculated by TurkStat declined by 2.3% year-on-year. It’s odd that the service sector showed such an increase while sales volume de-clined. Whereas the retail trade sector confidence index declined by 11.3% over the same period, the increase in the service sector con-fidence index was only 0.7%. With the new series we can’t now see the allocation of investment ex-penditure (gross fixed capital for-mation) between the public sec-tor, price sector, construction, ma-chine and equipment, and other assets. Total investment expend-iture rose by only 2.2%. But ma-chine and equipment investment over the same period declined by a high rate: 10.1%. (On the other

hand, building licenses in terms of square measurements, for in-stance, declined by 17.2%.)

Another odd discrepancy among economic indicators lies between growth and unemploy-ment. In an economy growing by 5%, unemployment would be ex-pected to decline or at least level out. Yet, despite overall growth of 5%, 12.1% unemployment record-ed for the fourth quarter of 2016 rose to 12.6% in the first quarter of 2017. If we accept the accuracy of the figures, they indicate a signifi-cant increase in labor productivity (GDP per worker) for the last two quarters. However, another expla-nation may be the increase in ref-ugee employment not reflected by official statistics.

Lo and behold, Turkey grew by 5%!TuğrulBELLI

Columnist

Turkey grew by 5% in the first three months of the year. Let’s be happy with that. But the public

should also recognize the source of this growth. The government took a large number of measures to revi-ve the stagnating and slowing eco-nomy and it blew money to mar-kets through credits. Consequent-ly, it pursued practices that would increase consumption expenditu-re. As a result of these measures household consumption increased by 5.1% and state expenditure rose by 9.4%.

Some 3.1% of the growth came from household consumption and 1.3% came from increases to state expenditure. In brief, 4.4% of the 5% growth was generated through consumption increases. The share of investment is 0.6%. Attention please: we spent on consumption,

not investment. The manufacturing industry is

the main dynamic powering this growth. TurkStat released the fig-ure for industrial production in-creases (based on manufacturing quantity-volume) as 1.4% for the first three months. But industry’s share (as added value) of the GDP is 5.3%. The manufacturing in-dustry’s added value increased by 1.5%. That indicates a significant structural change within the sec-tor for the first quarter of 2017. It indicates that the added value in-crease surpassed the manufactur-ing increase. It’s an important in-dicator regarding change that we should emphasize.

The government won’t have the ability to blow money to the mar-kets all the time to increase de-mand. The traditional source of consumption-based growth is in-

come. Unless household and state income increase continuously, consumption won’t increase ei-ther. Production is the source of in-come in an economy. Production creates income and employment. Therefore, the public should know how the Turkish economy grew by 5% in the first three months of the year. Don’t forget that consump-tion-based growth without produc-tion is not sustainable.

People are at the core of any econ-omy. Whether managing or man-aged, employer or employee, the morale of the people determines the direction of the economy. Mo-rale means feeling good today and having confidence in the future. We were depressed for a long time for different reasons, so 5% growth is like receiving money from our own homes. Investors and industry will observe that business is growing

and increase their investment and production accordingly.

Wholesalers and retailing Ana-tolian tradesmen will assume busi-ness is growing and renew their stocks. The ones with money or the opportunity to borrow will think “tomorrow will be better than to-day” and increase their expendi-tures. Interest rates won’t become cheaper unless inflation falls. But a “things are going well and will go well” attitude will encourage the debtors and the ones who want to become indebted. They will start not to worry about interest rates. Growth figures were released just at a time when the market and the people needed a boost in morale. The growth rate figures for the first quarter will promote buoyancy for a while. If this boom turns into a production increase, then we may yet enter a real growth period.

TevfikGUNGORColumnist

15 RESEARCH

Expats in Turkey earn less but live well

Turkey provides relati-vely good living oppor-tunities for foreigners but can not meet their

economic expectations, especially for a career, according to the 2016 edition of the HSBC Expat Explo-rer survey.

Turkey ranked 39th among the 45 countries in which all catego-ries were evaluated – below Qatar and China but ahead of Peru and Egypt; last year it ranked 36th out of 39 countries. In terms of politi-cal stability, expats ranked Turkey second last after Brazil.

The Expat Explorer survey, conducted by the HSBC Group through interviews with more than 26,000 foreign employees in 190 countries, examines areas in-cluding career opportunities, fi-nancial returns, living standards, security and family-friendly envi-ronment.

Failures in economic category According to the survey results, among the economy-related ques-tions, Turkey could only enter the top 30 in the savings and dis-posable income categories. Job security, career opportunities, work-life balance and salary in-creases were among the catego-ries in which Turkey found itself in last place. Though the country did shine in the living standards category, ranking 18th (among 45 countries) in this area. Secu-rity, health services and finance floored Turkey’s ranking while it attained high positions in subcat-egories such as culture, integra-tion, acquisition of property and healthy living.

The living standards of expats’ families were among the most im-portant issues for foreign work-ers. Turkey performed relatively moderately – ranking 31st – in this category. This was the area where Turkey showed the highest im-

provement compared to last year, when it came 38th among 39 coun-tries.

However, some subcategories highlighted serious problems. Foreign employees evaluated Tur-key as the worst among all coun-tries surveyed in terms of the qual-ity of schools. This result is in line with OECD research, which al-so reveals the poor quality of ed-ucation in Turkey. The sub-areas that saved Turkey from falling in-to last place in this category were child-raising costs in connection with social life, integration and ed-ucation quality.

Y-generation live abroad to build careers and financial returnsThe survey also reflects the ten-dencies of foreign workers as well as country rankings. According to

the survey, Y-generation foreign workers (born between 1980 and 1999) live abroad to progress their careers and improve in new areas. Almost half of the foreign work-ers in this group find the work they do abroad more satisfying than in their own country.

Almost a quarter (22%) of Y-generation foreign workers in-dicated that their desire to direct their own careers and acquire new goals was influential in moving abroad. This ratio is 14% for ex-pats aged between 34-54, while only 7% of expats over 55 cited this reason as to why they live abroad. Having said that, the survey shows that Y-generation expats are look-ing for new challenges. Two out of every five participants in this group (43%) said they went abroad for a different experience, while

this ratio falls to 38 percent for ex-pats aged between 34-54 and to 30 percent for those over 55 years old. Practically half (49%) of Y-genera-tion expats find their work abroad to be more satisfying than in their own country.

Working abroad speeds up long-term financial ambitionsThe majority of expats indicat-ed that working abroad more ef-ficiently enables them to reach long-term financial targets. Two out of every five expats who partic-ipated in the survey said that mov-ing abroad accelerated the pro-cesses for saving for retirement (40%) or buying real estate (41%). Around one third of respondents (29%) indicated that living abroad provides opportunities to save for the education of their children.

“I haven’t met an expat happy to leave Turkey” Evaluating the survey results, International Investors Association (YASED) President Ahmet Erdem said the reality on the ground is slightly different despite Turkey being declared among the least habitable countries for expats. “I have never met an expat who left Turkey happiliy after working here,”

he said. “I think this is true in terms of personal and professional lives. Turkey is a very good country to improve yourself both in terms of living and work. It has a lively and developing market structure. When you look at the business environment, it is a positive country for an expat for job satisfaction.”

16BUSINESS

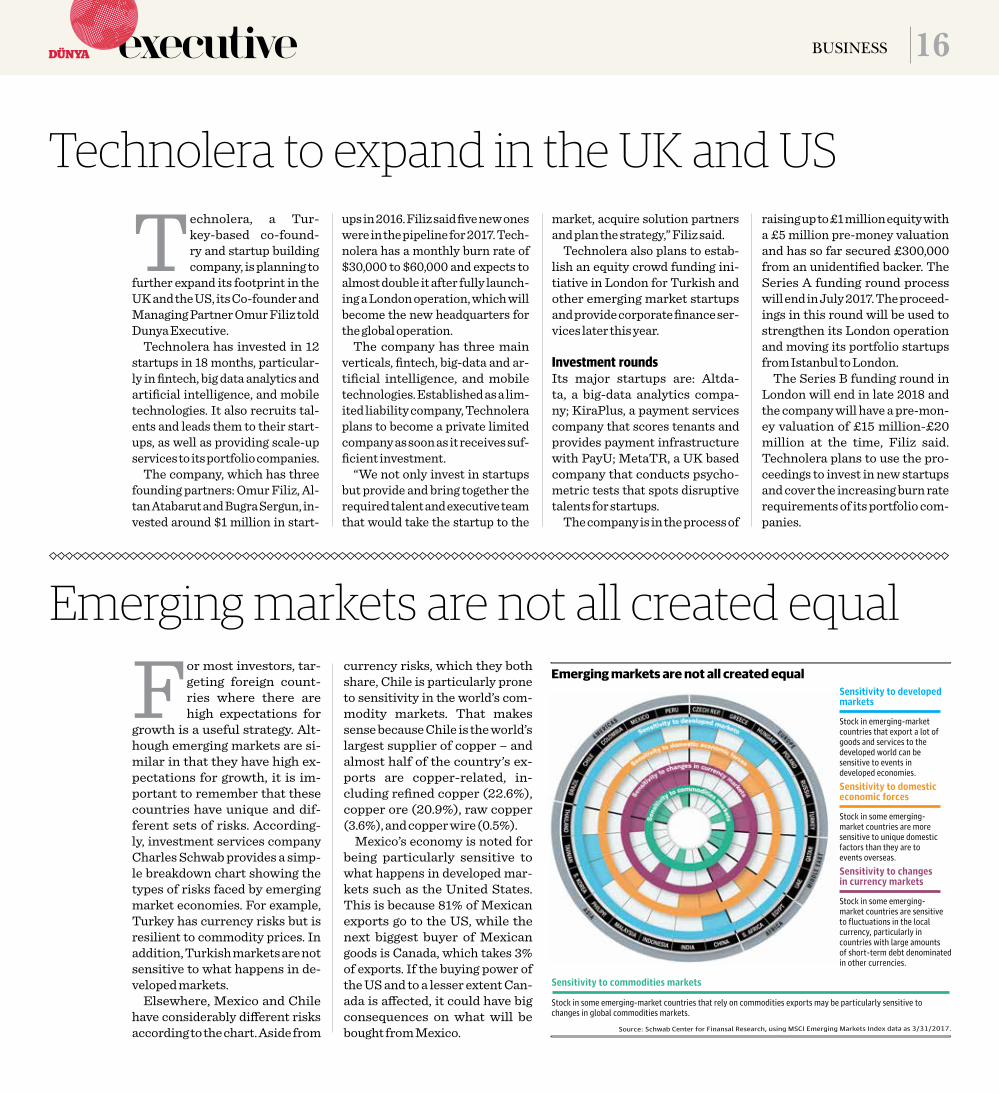

Technolera to expand in the UK and US

Technolera, a Tur-key-based co-found-ry and startup building company, is planning to

further expand its footprint in the UK and the US, its Co-founder and Managing Partner Omur Filiz told Dunya Executive.

Technolera has invested in 12 startups in 18 months, particular-ly in fintech, big data analytics and artificial intelligence, and mobile technologies. It also recruits tal-ents and leads them to their start-ups, as well as providing scale-up services to its portfolio companies.

The company, which has three founding partners: Omur Filiz, Al-tan Atabarut and Bugra Sergun, in-vested around $1 million in start-

ups in 2016. Filiz said five new ones were in the pipeline for 2017. Tech-nolera has a monthly burn rate of $30,000 to $60,000 and expects to almost double it after fully launch-ing a London operation, which will become the new headquarters for the global operation.

The company has three main verticals, fintech, big-data and ar-tificial intelligence, and mobile technologies. Established as a lim-ited liability company, Technolera plans to become a private limited company as soon as it receives suf-ficient investment.