portfolio construction:portfolio construction ......portfolio construction:portfolio construction:...

TRANSCRIPT

Portfolio Construction:Portfolio Construction: Considerations in Today’s Investment EnvironmentEnvironmentMarco Bravo CFAMarco Bravo, CFAPortfolio ManagerAAM Company

The 2014 Executive Education Roundtable Series

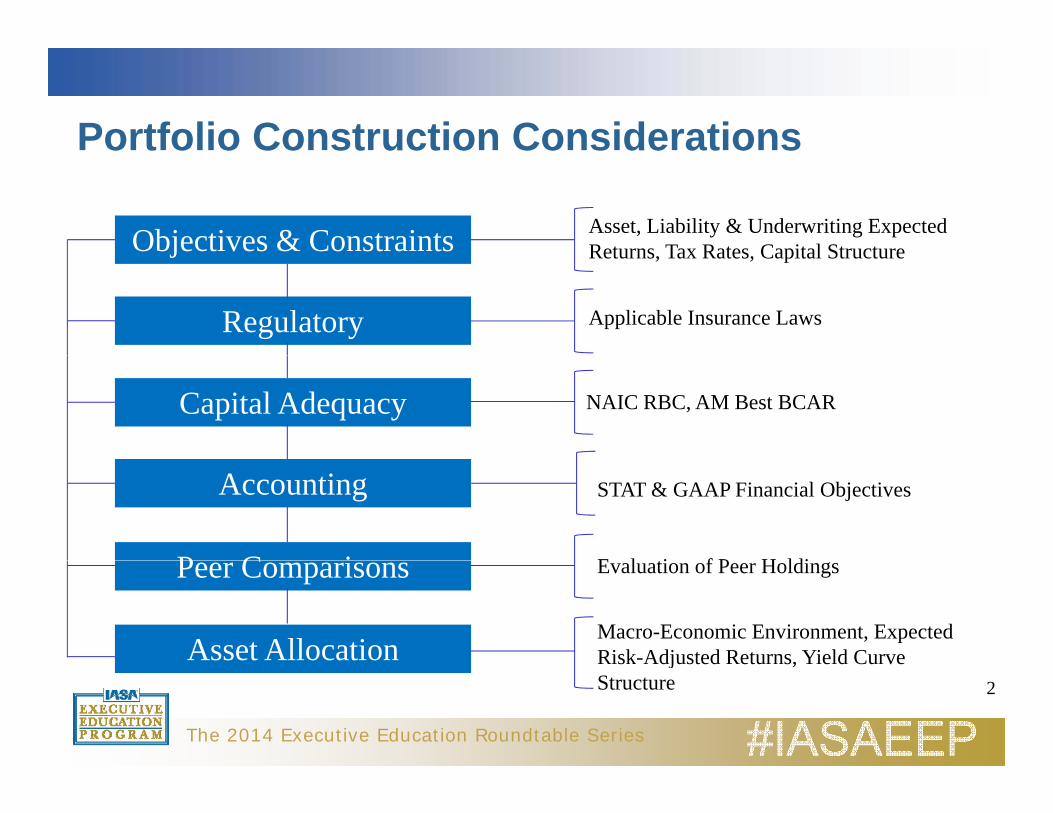

Portfolio Construction Considerationso t o o Co st uct o Co s de at o s

Objectives & Constraints Asset, Liability & Underwriting Expected Returns Tax Rates Capital Structurej

Regulatory

Returns, Tax Rates, Capital Structure

Applicable Insurance Laws

Capital Adequacy NAIC RBC, AM Best BCAR

Accounting

P C i

STAT & GAAP Financial Objectives

E l ti f P H ldiPeer Comparisons

Asset Allocation

Evaluation of Peer Holdings

Macro-Economic Environment, Expected Risk-Adjusted Returns, Yield Curve

The 2014 Executive Education Roundtable Series

Risk Adjusted Returns, Yield Curve Structure 2

Portfolio Construction ConsiderationsPortfolio Construction Considerations

Key considerations in today’s investment environment:

Investment Policy Objectives & Constraints

Key Risk Measures

Asset & Liability Management

Taxabilityy

Asset Allocation

Fed PolicyFed Policy

Relative Value Assessment

Risk Assets

The 2014 Executive Education Roundtable Series

Risk Assets3

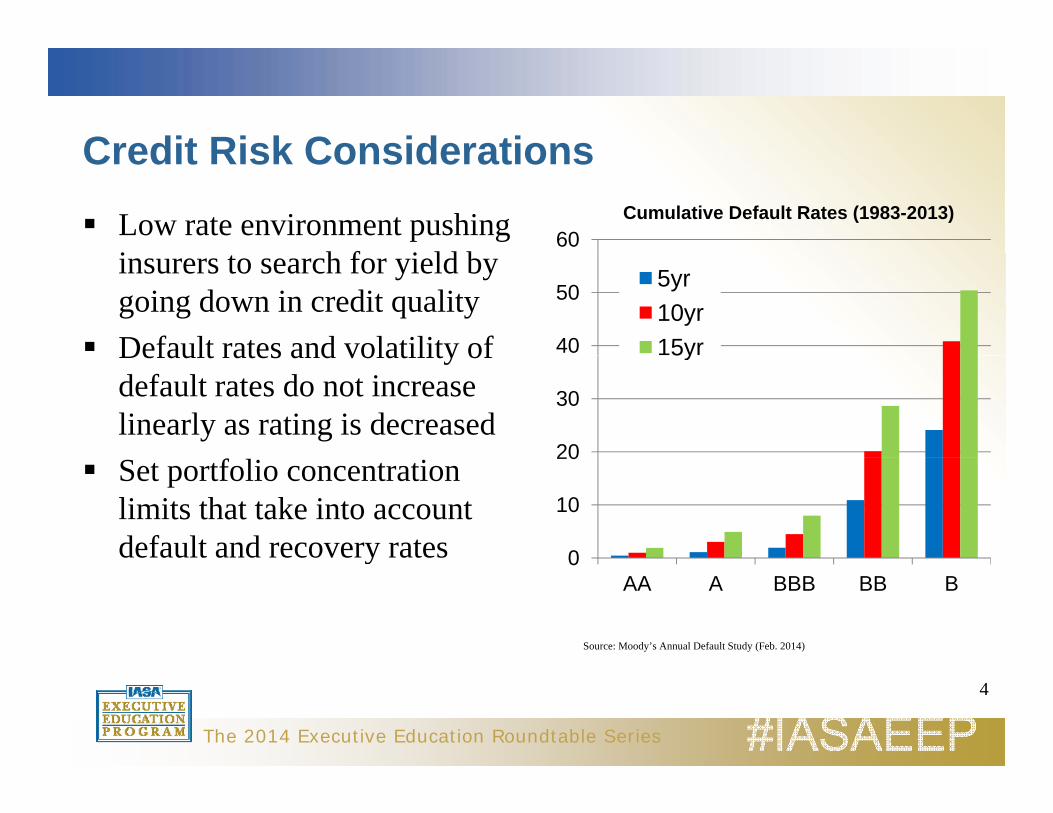

Credit Risk Considerations

60Cumulative Default Rates (1983-2013)

Credit Risk Considerations

Low rate environment pushing i h f i ld b

40

50 5yr10yr15yr

insurers to search for yield by going down in credit qualityDefault rates and volatility of

20

30

5yDefault rates and volatility of default rates do not increase linearly as rating is decreased

0

10

20Set portfolio concentration limits that take into account default and recovery rates 0

AA A BBB BB B

Source: Moody’s Annual Default Study (Feb. 2014)

y

4

The 2014 Executive Education Roundtable Series

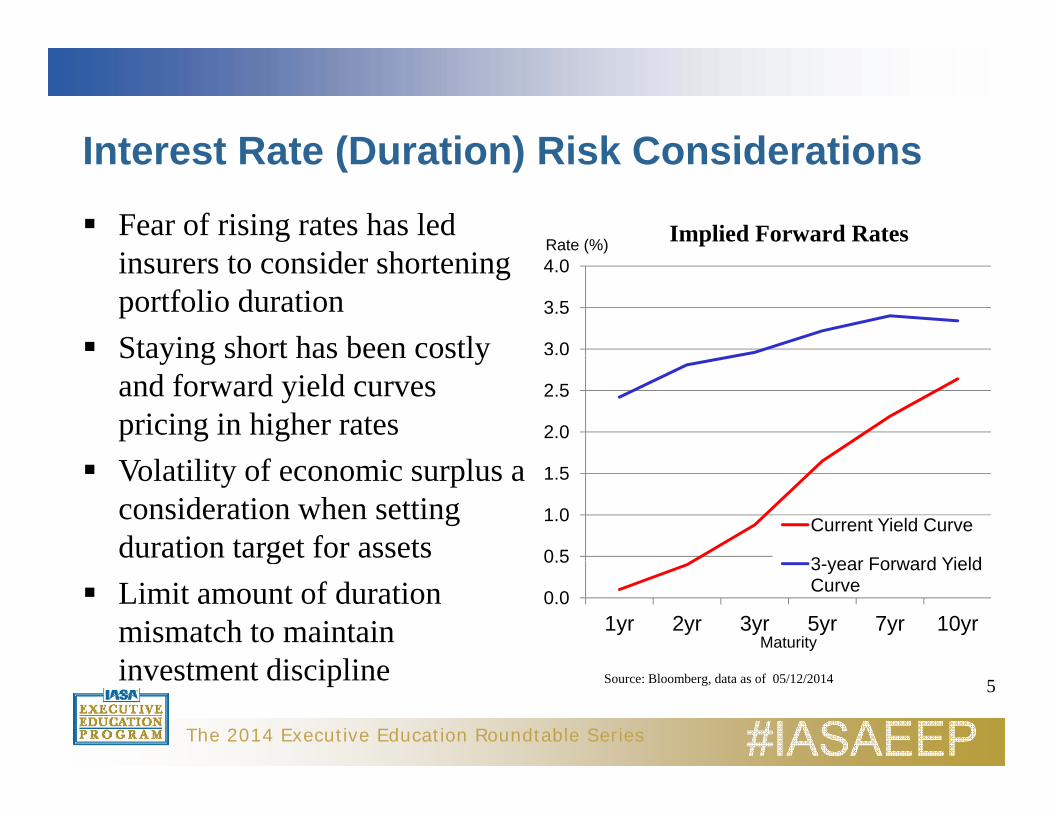

Interest Rate (Duration) Risk ConsiderationsInterest Rate (Duration) Risk Considerations

Rate (%)Fear of rising rates has led i id h i

Implied Forward Rates

3.0

3.5

4.0( )

insurers to consider shortening portfolio duration Staying short has been costly

2.0

2.5

Staying short has been costly and forward yield curves pricing in higher rates

0 5

1.0

1.5

Current Yield Curve

3 year Forward Yield

Volatility of economic surplus a consideration when setting duration target for assets

0.0

0.5

1yr 2yr 3yr 5yr 7yr 10yrMaturity

3-year Forward Yield Curve

gLimit amount of duration mismatch to maintain i t t di i li

The 2014 Executive Education Roundtable Series

investment discipline Source: Bloomberg, data as of 05/12/2014 5

Liquidity Risk ConsiderationsLiquidity Risk Considerations

Liquidity risk tends to be a bigger concern for P&C companies h if / l h C ithan Life/Health Companies

Increase in surrender activity for annuity writers is a concern if rates move above current crediting ratesrates move above current crediting rates

Manage liquidity risk through laddered maturity investment profile with ranking of liquid assetsprofile with ranking of liquid assets

Consider liquidity back-stop facility such as membership in Federal Loan Bank

The 2014 Executive Education Roundtable Series

6

Asset & Liability Management ConsiderationsAsset & Liability Management Considerations

Risk of asset duration extending in a rising rate environmentIncreasing investment leverage increases importance of asset/liability duration matchCompare assets and liability cash flows under various interestCompare assets and liability cash flows under various interest rate scenariosInterest sensitive assets and liabilities requires the use of effective duration versus modified durationSegregating liabilities by product line imposes pricing discipline so that long term yields do not get used for pricingdiscipline so that long-term yields do not get used for pricing short-term liabilities

The 2014 Executive Education Roundtable Series

7

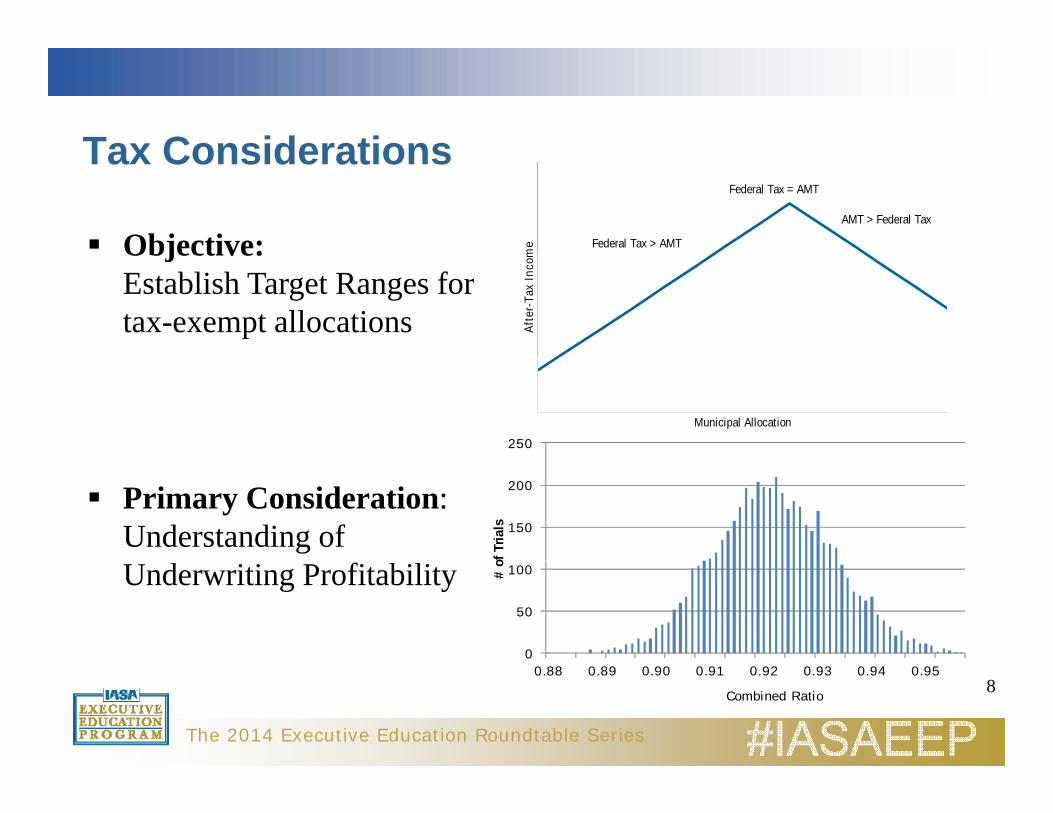

Tax ConsiderationsTax Considerations

me Federal Tax > AMT

Federal Tax = AMT

AMT > Federal Tax

Objective:

Afte

r-Ta

x In

comObjective:

Establish Target Ranges for tax-exempt allocations

Municipal Allocation

250

Primary Consideration: Understanding of 150

200of

Tria

ls

Underwriting Profitability

0

50

100# o

The 2014 Executive Education Roundtable Series

0.88 0.89 0.90 0.91 0.92 0.93 0.94 0.95

Combined Ratio 8

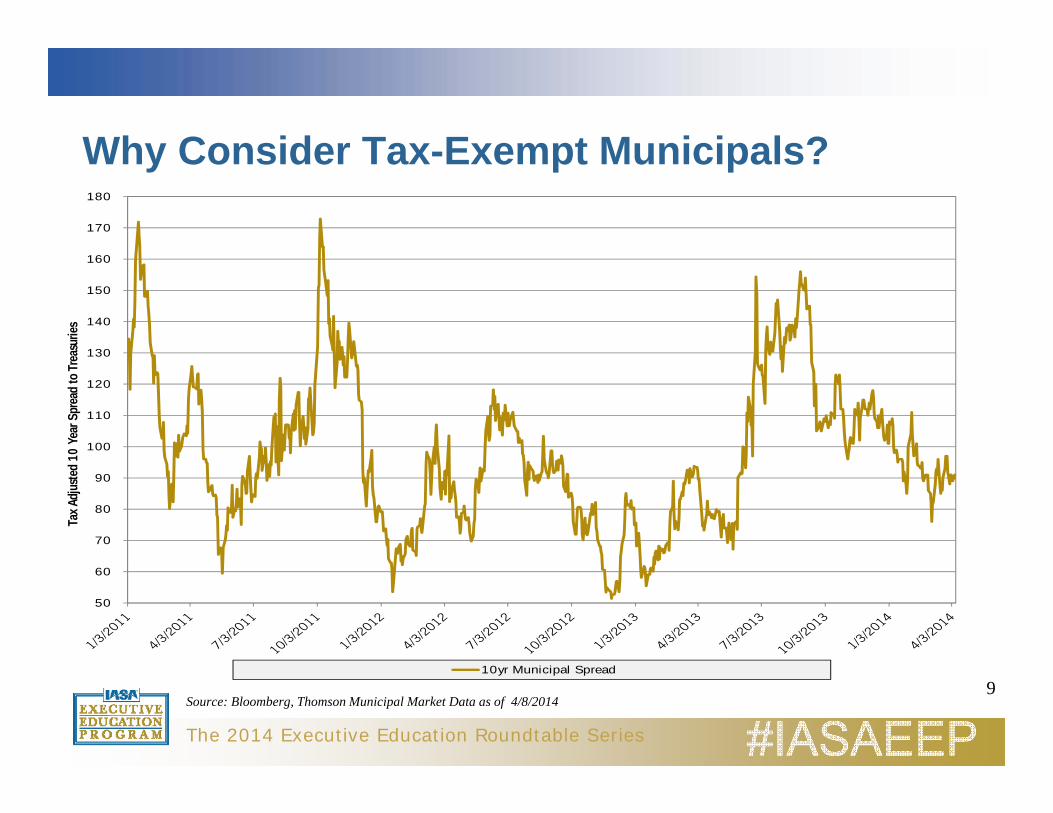

Why Consider Tax Exempt Municipals?Why Consider Tax-Exempt Municipals? 170

180

130

140

150

160

asur

ies

100

110

120

130

10 Y

ear S

prea

d to

Trea

70

80

90

Tax A

djuste

d 1

50

60

The 2014 Executive Education Roundtable Series

10yr Municipal Spread

Source: Bloomberg, Thomson Municipal Market Data as of 4/8/20149

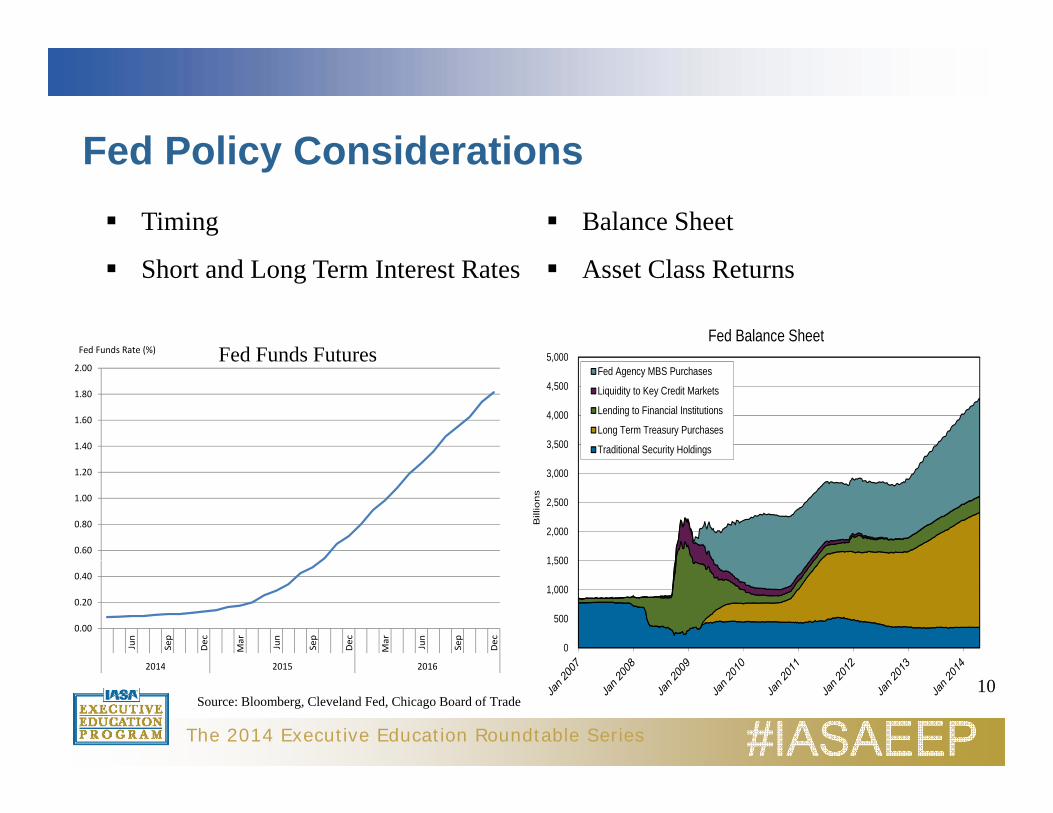

Fed Policy ConsiderationsFed Policy ConsiderationsTiming Balance Sheet

Short and Long Term Interest Rates

Fed Funds Rate (%)5 000

Fed Balance Sheet

Asset Class Returns

Fed Funds Futures

1.40

1.60

1.80

2.00

3,500

4,000

4,500

5,000Fed Agency MBS Purchases

Liquidity to Key Credit Markets

Lending to Financial Institutions

Long Term Treasury Purchases

Traditional Security Holdings

Fed Funds Futures

0.60

0.80

1.00

1.20

1 500

2,000

2,500

3,000

Bill

ion

s

0.00

0.20

0.40

Jun

Sep

Dec

Mar Jun

Sep

Dec

Mar Jun

Sep

Dec

2014 2015 2016

0

500

1,000

1,500

The 2014 Executive Education Roundtable Series

2014 2015 2016

Source: Bloomberg, Cleveland Fed, Chicago Board of Trade10

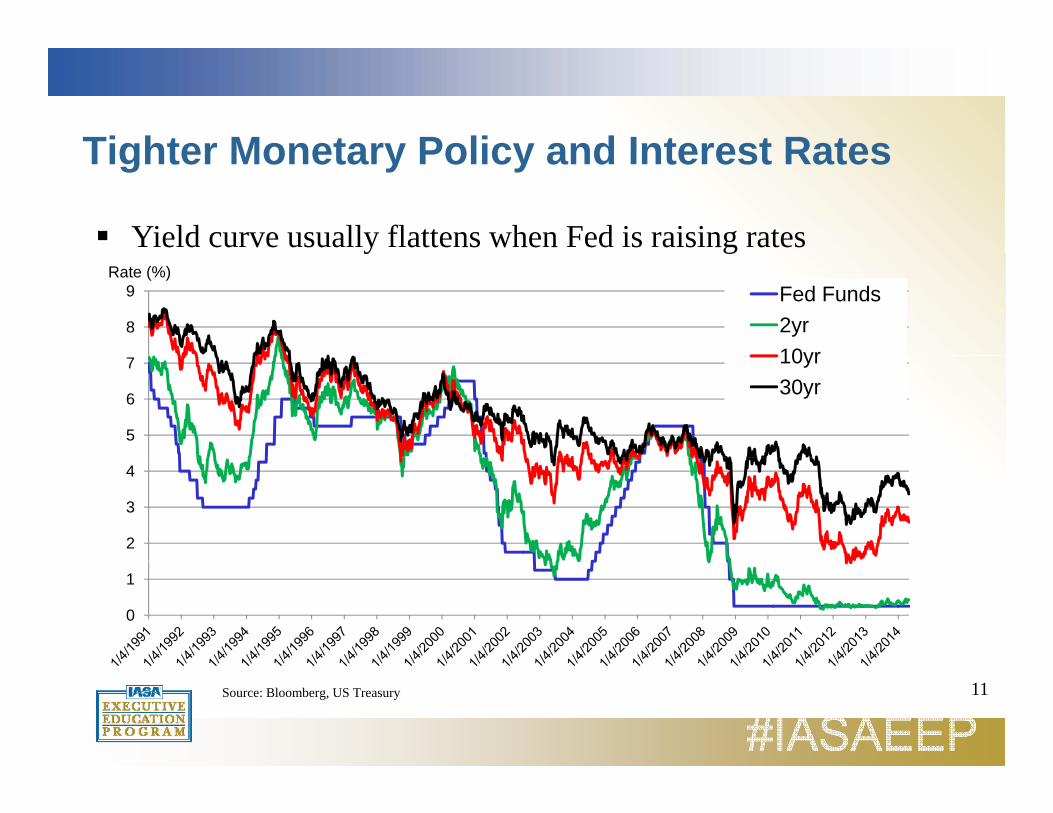

Tighter Monetary Policy and Interest RatesTighter Monetary Policy and Interest Rates

Yield curve usually flattens when Fed is raising rates

8

9Rate (%)

Fed Funds2yr10yr

y g

5

6

7 10yr30yr

2

3

4

0

1

Source: Bloomberg, US Treasury 11

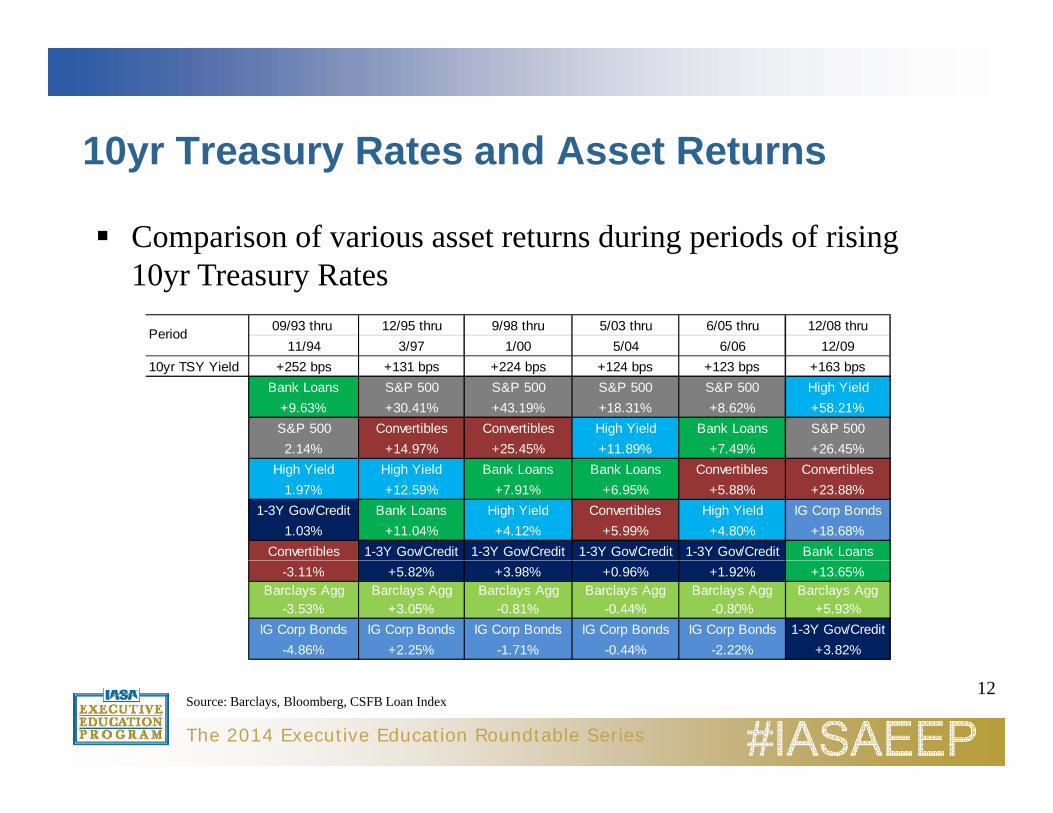

10yr Treasury Rates and Asset Returns10yr Treasury Rates and Asset Returns

Comparison of various asset returns during periods of rising p g p g10yr Treasury Rates

09/93 thru 12/95 thru 9/98 thru 5/03 thru 6/05 thru 12/08 thru11/94 3/97 1/00 5/04 6/06 12/09

Period

10yr TSY Yield +252 bps +131 bps +224 bps +124 bps +123 bps +163 bpsBank Loans S&P 500 S&P 500 S&P 500 S&P 500 High Yield

+9.63% +30.41% +43.19% +18.31% +8.62% +58.21%S&P 500 Convertibles Convertibles High Yield Bank Loans S&P 5002.14% +14.97% +25.45% +11.89% +7.49% +26.45%

High Yield High Yield Bank Loans Bank Loans Convertibles Convertibles1.97% +12.59% +7.91% +6.95% +5.88% +23.88%

1-3Y Gov/Credit Bank Loans High Yield Convertibles High Yield IG Corp Bonds1.03% +11.04% +4.12% +5.99% +4.80% +18.68%

Convertibles 1-3Y Gov/Credit 1-3Y Gov/Credit 1-3Y Gov/Credit 1-3Y Gov/Credit Bank Loans-3.11% +5.82% +3.98% +0.96% +1.92% +13.65%

Barclays Agg Barclays Agg Barclays Agg Barclays Agg Barclays Agg Barclays Agg-3.53% +3.05% -0.81% -0.44% -0.80% +5.93%

IG Corp Bonds IG Corp Bonds IG Corp Bonds IG Corp Bonds IG Corp Bonds 1-3Y Gov/Credit-4.86% +2.25% -1.71% -0.44% -2.22% +3.82%

The 2014 Executive Education Roundtable Series

Source: Barclays, Bloomberg, CSFB Loan Index12

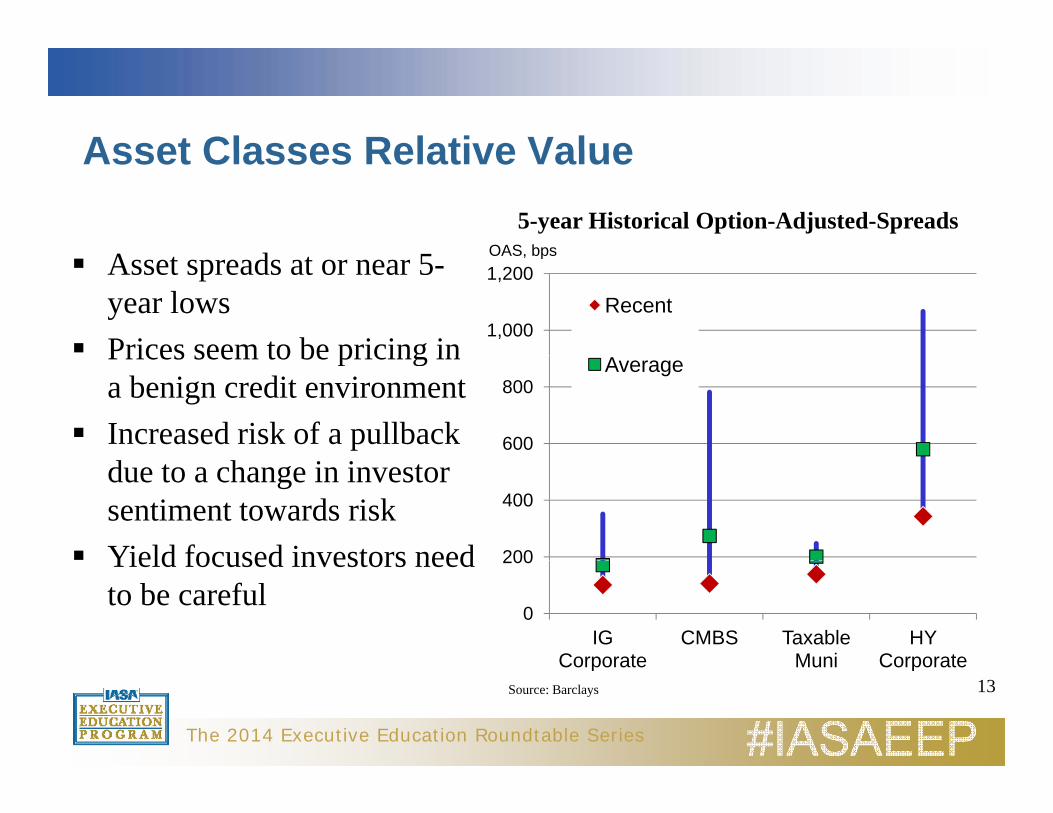

Asset Classes Relative ValueAsset Classes Relative Value

OAS bps

5-year Historical Option-Adjusted-Spreads

d

1,000

1,200OAS, bps

Recent

Asset spreads at or near 5-year lowsPrices seem to be pricing in

600

800AveragePrices seem to be pricing in

a benign credit environmentIncreased risk of a pullback

200

400due to a change in investor sentiment towards riskYield focused investors need

0

200

IG Corporate

CMBS Taxable Muni

HY Corporate

Yield focused investors need to be careful

The 2014 Executive Education Roundtable Series

Corporate Muni CorporateSource: Barclays 13

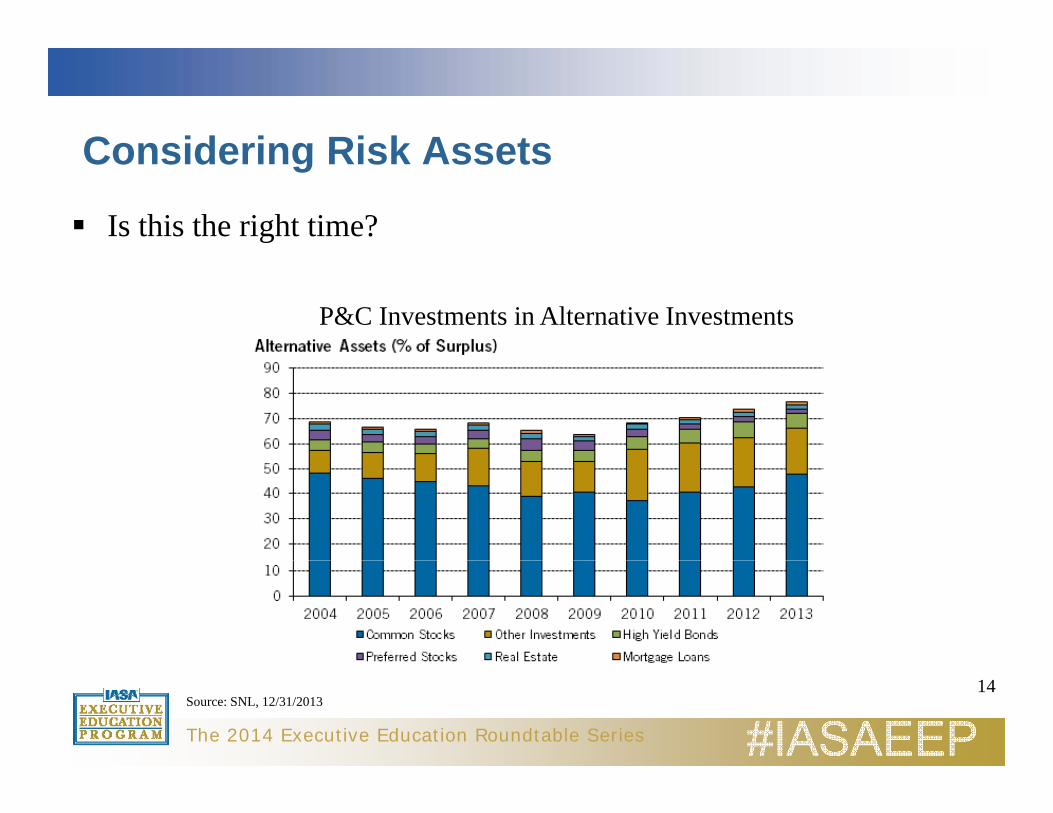

Considering Risk AssetsConsidering Risk Assets

Is this the right time?

P&C Investments in Alternative Investments

The 2014 Executive Education Roundtable Series

Source: SNL, 12/31/201314

Questions?

The 2014 Executive Education Roundtable Series

15