positioning ifrs & psab in the federal...

TRANSCRIPT

KPMG LLP

Public Sector Audit Practice

Positioning IFRS & PSAB in the Federal Government

November 24, 2010

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 2

Agenda

1. The Journey: Canadian Accounting Standard Changes2. Key IFRS differences3. Key PSAB differences4. Federal Government Impact

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3

The Journey: Canadian Accounting Standard Changes

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4

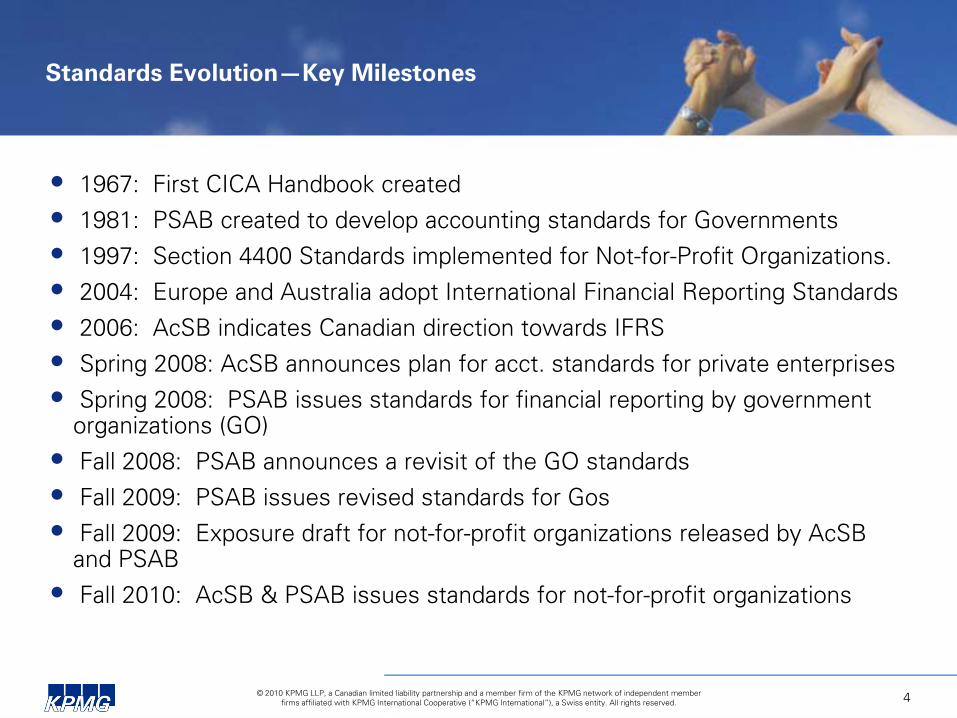

Standards Evolution—Key Milestones

• 1967: First CICA Handbook created • 1981: PSAB created to develop accounting standards for Governments • 1997: Section 4400 Standards implemented for Not-for-Profit Organizations. • 2004: Europe and Australia adopt International Financial Reporting Standards• 2006: AcSB indicates Canadian direction towards IFRS• Spring 2008: AcSB announces plan for acct. standards for private enterprises• Spring 2008: PSAB issues standards for financial reporting by government

organizations (GO)• Fall 2008: PSAB announces a revisit of the GO standards• Fall 2009: PSAB issues revised standards for Gos• Fall 2009: Exposure draft for not-for-profit organizations released by AcSB

and PSAB• Fall 2010: AcSB & PSAB issues standards for not-for-profit organizations

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 5

Accounting Standard Setting in Canada

Public SectorAccounting Board

(PSAB)

GovernmentsGovernment Organizations

Accounting Standards Board (AcSB)

Publicly-traded CompaniesPrivate Companies

Pension PlansNon-Govt. Not-for-Profits

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6

Public Accountable Entities

Public AccountableEntities

Part I of Accounting Handbook

IFRS

Definition: • Issued any class of instruments in a public market;• Hold assets in a fiduciary capacity for a broad group of outsiders

When?: Years beginning on or after January 1, 20111-year deferral for rate regulated, investment companies and segregated accounts of life insurance companies.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 7

Private Enterprises

Private Enterprises

Part IIFRS

Part IIAccounting

Standards for Private Enterprises

When?: Years beginning on or after January 1, 2011

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 8

Pension Plans

Pension PlansPart IV

Accounting Standards for Pension Plans

When?: Years beginning on or after January 1, 2011

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

Public Sector

GovernmentsPublic Sector Accounting Standards

Government Organizations

Depends on Type of Government Organization

Government organizations are organizations that are controlled by a government. Government organizations are included in the government reporting entity.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 10

GBEs/GBTOs—Original Direction

In 2008:

Government Business Enterprises

Government Business Type Organizations

Part IIFRS

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 11

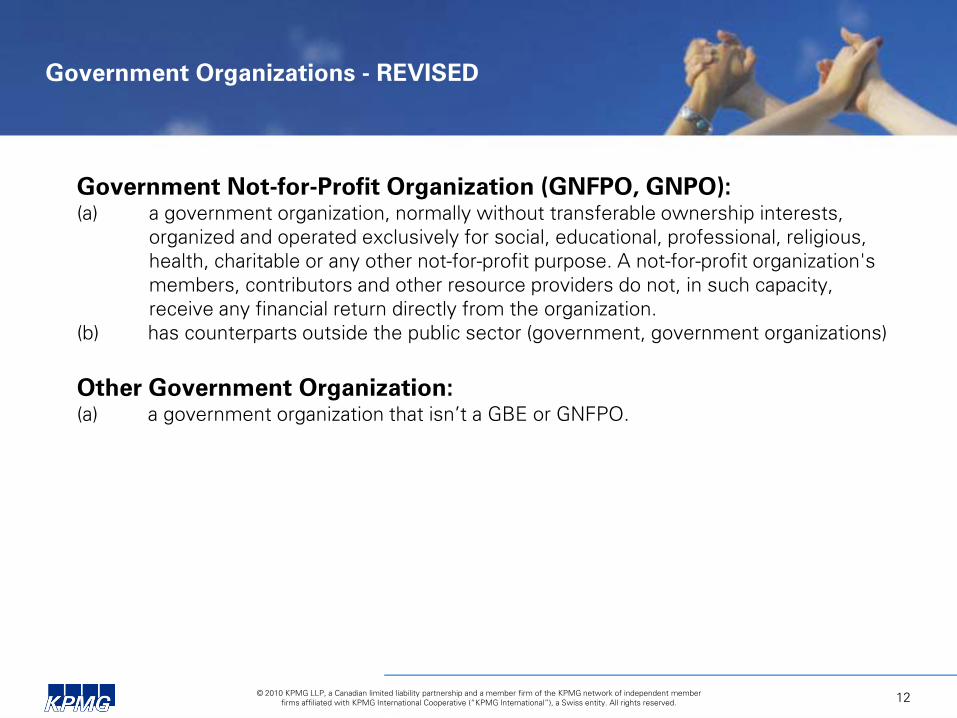

Government Organizations – REVISED

Government Business Enterprise (GBE):(a) it is a separate legal entity with the power to contract in its own name and that can

sue and be sued;(b) it has been delegated the financial and operational authority to carry on a business;(c) it sells goods and services to individuals and organizations outside of the government

reporting entity as its principal activity; and(d) it can, in the normal course of its operations, maintain its operations and meet its

liabilities from revenues received from sources outside of the government reporting entity.

Government Business-Type Organization (GBTO):(a) it is a separate legal entity with the power to contract in its own name and that can

sue and be sued;(b) it has been delegated the financial and operational authority to carry on a business;

and(c) it sells goods and services to individuals and as its principal activity

When?: Effective for years beginning on or after January 1, 2011

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 12

Government Organizations - REVISED

Government Not-for-Profit Organization (GNFPO, GNPO):(a) a government organization, normally without transferable ownership interests,

organized and operated exclusively for social, educational, professional, religious, health, charitable or any other not-for-profit purpose. A not-for-profit organization's members, contributors and other resource providers do not, in such capacity, receive any financial return directly from the organization.

(b) has counterparts outside the public sector (government, government organizations)

Other Government Organization:(a) a government organization that isn’t a GBE or GNFPO.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 13

Government Business Enterprises

Government Business Enterprises

Part IIFRS

When?: Years beginning on or after January 1, 2011• One year deferred for Rate Regulated entities

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 14

Other Government Organizations

Other Government Organizations

Public Sector Accounting Standards

Part IIFRS

OGO’s apply PSAS unless IFRS is considered to be the more appropriate basis of accounting for the OGO based on financial statement user needs based on criteria.

When?: Years beginning on or after January 1, 2011

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 15

Not-for-Profit Organizations

Concurrent Exposure Drafts:

AcSB Move S4400 series to Part B of HandbookPrivate Enterprise Part II is standards for items not covered by S4400

PSAB Move S4400 series into the PSAB Handbook, labeled as Section 4200.PSAS as the basis for standards for items not covered by S4200 series of standards for not-for-profit organizations

Both Boards to create a joint task force to look at improvements to accounting standards for not-for-profit organizations.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 16

Not-for-Profit Organizations

Non-GovernmentNFPOs

Part III – Accounting Standards for Not-for-Profit organizations

Part II – Private Enterprise

Part I - IFRS

When?: Years beginning on or after January 1, 2012 Early adoption is allowed

Option

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 17

Government Not-for-Profit Organizations

GovernmentNFPOs

S4200 of Public Sector Accounting Standards

Other Sections of PSAS Handbook

Public Sector Accounting Standards on a stand alone basis (without S4200)

Current GNFPOs: Years beginning on or after January 1, 2012. Early adoption is allowed

Current GBTOs reclassifying to GNFPO: GBTO classification is eliminated for years beginning on or after January 1, 2011.

Option

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 18

Summary

Public Accountable Enterprises

Private Enterprises

Non-Government NFPOs

Pension Plans

Accounting Handbook

Part 1: IFRS

Part 2: Private Enterprise

Part 3: NFPOs

Part 4: Pension Plans

Governments

Government Business Enterprise

Government NFPOs

Other Government Organizations

Public Sector Accounting HandbookPublic Sector Accounting Standards

(without S4200)S4200 – Public Sector Accounting

Standards for Not-For-Profit Organizations

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 19

Future Steps

Accounting Standards Board / International Acct. Standards Board• Clarity on IFRS for investment companies• Resolution of rate regulated accounting issues with IFRS • New/revised IFRS sections – (Over 20 projects currently underway)

PSAB/Not-for-Profit Organizations• Finalize financial instrument standard• Finalize government transfers standard• Joint taskforce with AcSB on NFPO accounting standards• Conceptual framework project

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 20

International Financial Reporting Standards:

Key differences

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 21

IFRS versus Canadian GAAP – Similarities

•Similar basic concepts

•Similar structure and content of financial statements

•Some standards in IFRS provide similar approach as Canadian GAAP

•More recent Canadian standards aligned with IFRS (e.g. Inventories, Financial Instruments)

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 22

IFRS versus Canadian GAAP – Differences

•Fewer bright lines and rules•Some IFRS standards differ considerably from Cdn GAAP •More accounting policy choices•Greater use of fair value and reversal of PY writedowns

Applying IFRS requires more professional judgement and results in greater volume of disclosures

•Many differences in application/interpretationBE CAREFUL – The devil is in the detail!

• IFRS 1: Transitional guidance upon first-time adoption of IFRS.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Statement Presentation

•Balance sheet:• Classifications are generally consistent with Cdn GAAP• Three years of balance sheets required if FS restated

• Income Statement:• Expenses strictly classified by nature or function• Nature: purchases, depreciation, salaries, advertising• Function: cost of sales, distribution, fundraising, administration

• If by function, all costs should be allocated•No “one-line” charges for restructurings, impairment etc.

•Significantly more note disclosure

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 24

Property, Plant & Equipment

•Components approach – more rigorously applied and broader than under Canadian GAAP•allocate cost to significant parts of the asset

•Subsequent measurement options for PPE are cost or revaluation model•Impairment tests required:• Based on fair value and discounted future cash flows from use• Reversal of prior impairment charges

•One-time transition election to record individual assets at deemed cost equaling fair value at transition date (January 1, 2010).

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 25

Provisions

•A liability of uncertain timing or amount•Recognize if probable a liability has been incurred•Recognize on basis of legal OR constructive obligation•Probable = “More likely than not” rather than “likely”•Measure at “best estimate” – may be one of•most likely outcome – single best estimate•expected value – probability weighted expected value•midpoint – where a range of probable estimates

•Discounting required when effect is material

More items to be recognized…measurement may differ

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 26

Public Sector Accounting Standards: Key Differences

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Agenda

• Presentation Impacts:• Financial Statements – PSAB Standalone• Financial Statements – Section 4200

• PSAB Measurement Impacts:• Liabilities• Government Transfers• Post Employment Benefits• Financial Instruments

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Statement Presentation - PSAB

• Statement of Financial Position:• Financial assets presented separately and apart from non-financial assets• Financial assets - Liabilities = net financial assets (net debt)•Non-financial assets are shown below net debt•Net debt + non-financial assets = Accumulated surplus/deficit

• Statement of Operations:• Expenses are reported by function or major program and disclosed by object•When the revenues and expenses displayed are not gross amounts, the gross

amounts are disclosed• A comparison with the original budget is provided

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Statement Presentation-PSAB (cont)

• Statement of Net Financial Assets/Net Debt:• Explains the difference between period surplus/deficit and the change in the net

financial assets/net debt amount on statement of financial position• Change in non-financial assets

• Statement of Cash Flows:• Cash flows are classified by operating, capital, investing and financing activities• Cash equivalents (typically < 90-day original maturity) are included in cash balance.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Statement Presentation--PSAB + S4200

• Statement of Financial Position• Statement of Operations• Statement of Changes in Net Assets• Statement of Cash Flows• Notes to the financial statements

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Fund Accounting--PSAB + S4200

Accounting Policy Choice: Deferral or Restricted Fund Method• Deferral Method of Accounting for Contributions:•restricted contributions related to expenses of future periods are

deferred and recognized as revenue in the period in which the related expenses are incurred. •Endowment contributions are reported as direct increases in net

assets•All other contributions are reported as revenue

• Restricted Fund of Accounting for Contributions:•Separates activities into a general fund, restricted funds and an

endowment fund•Contributions are reports as revenue in one of the funds depending

its restrictions (if any) and the nature of those restrictions

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Statement of Financial Position--PSAB + S4200

•Net Assets:•Unrestricted net assets•Restricted net assets—those set aside for specific purpose•Endowment net assets—those that must be maintained

permanently•Net assets invested in capital assets—optional presentation•Typically equals the entity’s capital assets less supporting long-term

debt and deferred capital contributions

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Liabilities

•Liabilities:

•present obligations of an entity to others arising from past transactions or events, the settlement of which is expected to result in the future sacrifice of economic benefits.

•Three characteristics:•embody a duty or responsibility to others, leaving an entity little or

no discretion to avoid settlement of the obligation;•the duty or responsibility to others entails settlement by future

transfer or use of assets, provision of goods or services, or other form of economic settlement at a specified or determinable date, on occurrence of a specified event, or on demand; and•the transactions or events obligating the entity have already

occurred.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Types of Liabilities

• Liabilities arise from many types of obligations. Obligations result in an entity being bound or committed to a particular course of action. • They can arise from:• agreements or contracts;• another government's legislation;• a government's own legislation;• constructive obligations (that is, those that can be inferred

from the facts in a particular situation); and• equitable obligations (that is, those that are based on ethical

or moral considerations).

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Constructive and Equitable Obligations

•Significant professional judgement required to determine if the entity has “little or no discretion”•Must consider whether the entity has created a valid expectation

among others and, as a result, has no realistic alternative but to settle its obligation.•Preponderance of Evidence:• the entity acknowledges and indicates it will act upon its decision to accept

responsibility for the obligation; and• the entity has sufficiently communicated its decision to the affected parties.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 36

Government Transfers – Re-Exposure Draft

Issue Re-exposure approachTransferor Recognize expense when authorized and eligibility criteria, if any,

have been met by the recipient.

Recipient:-Operating

Revenue in the period transfer is authorized and eligibility criteria, if any, have been met by the recipient, except when and to the extent that the transfer gives rise to a liability under PS3200: Liabilities.

Recipient:-Capital

Revenue in the period transfer is authorized and eligibility criteria, if any, have been met by the recipient, except when and to the extent that the transfer gives rise to a liability under PS3200: Liabilities.

Capital: Recognition in revenue

Recognize in revenue when, and in proportion to how, the liability is settled.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 37

Government Transfers – Re-Exposure Draft

A liability may arise in relation to:

• An operating transfer

• a capital transfer for the purpose of acquiring/developing a capital asset

• a capital transfer for the purpose of acquiring /developing a capital asset to be used to provide service for a number of years

• a transfer of capital assets to be used to provide service for a number of years

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 38

Employee Future Benefits

Topic Current Standards PSA Handbook

Actuarial gains and losses Can elect corridor method whereby gain and losses less than 10% of plans asset or obligations can be deferred and not amortized

All actuarial gains and losses must be amortized

Discount rate Market interest rates on high quality debt instruments with matching cash flows or interest rate at which obligation could be settled

Short-term forecast of rates of return on assets held or cost of borrowing

Plan amendments Deferred and recognized based on employee average remaining service life (EARSL)

Recognized immediately

Measurement of assets Market value with option to adjust to market over a period not to exceed five years

Market value with option to adjust to market over a period not to exceed five years

Compensated Absences Cost should be accrued when the event that obligates the entity occurs. Current Handbook indicates that, as a practical matter entities are not required to accrue liabilities that accumulate but do not vest, such as sick leave benefit

Cost should be accrued in period employee renders service.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Instruments

Financial Instruments Exposure Draft

•Two Measurement Categories:• Fair Value• Cost or amortized cost

•Fair value measurement applies to:• Derivatives• Portfolio investments in equity instruments that are quoted in an

active market

•Fair value option available•Remeasurement gains and losses reported in a separate

statement

39

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

Financial Instruments - Statement of Remeasurement Gains and Losses

•New Statement to the Financial Statements•Reports the following• Change in the fair value of a financial instrument • Foreign exchange gains/losses on items recorded in the cost or amortized cost

category•Other comprehensive income of government business enterprises

40

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 41

Other Impacts on Federal Government

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

GAAP Hierarchy

•Section PS 1150 provides guidance on the source of GAAP for all governments, and those organizations that consider the CICA Public Sector Accounting Handbook to be the most appropriate to their objectives and circumstances. (referred to as a "public sector reporting entity“).•For these entities:• the primary source of GAAP is defined to be standards contained in the PSA

Handbook, as well as Public Sector Guidelines and appendices and illustrative material of those pronouncements.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

GAAP Hierarchy

•Public sector reporting entities should apply every primary source of GAAP (PSAB) that deals with the accounting and reporting in their financial statements of transactions or events encountered by the entity.•When PSAB does not deal with accounting and reporting matters encountered

by the entity, or additional guidance is needed to apply PSAB to specific circumstances, the selection of an appropriate accounting policy requires the exercise of professional judgment. • In these circumstances, a public sector reporting entity should adopt

accounting policies and disclosures that are consistent with:(a) the primary sources of GAAP; and(b) the application of the concepts described in Section PS 1000

Financial Statement Concepts (i.e. the conceptual framework)

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

GAAP Hierarchy

Other sources of GAAP are to be evaluated by the public sector reporting entity based on the following criteria:

(a) The specificity of the source(b) The authority of the issuer or author(c) The continued relevance of the source(d) The development process for the source

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

GAAP Hierarchy

•Secondary Sources of GAAP could include: • PSAB 4200 Government Not-for-Profit Organizations• International Financial Reporting Standards• CICA Accounting Standards for Private Enterprises• International Public Sector Accounting Standards• Public Sector Standards set by other countries

But be careful—must conform with the PSAB conceptual framework

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 46

Consolidation of Government Organizations

Different consolidation methods

• Government Business Enterprises:• Modified equity method: “one-line consolidation”• No requirement to adjust to accounting policies of the Govt.• Therefore, IFRS results are consolidated into Govt. FS

• Other Government Organizations:• Full consolidation: “line-by-line consolidation”• Requires adjustments of accounting policies to match Govt. accounting

policies•OGOs reporting under IFRS must prepare a reconciliation to PSAB

standards for consolidation into Govt. FS

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 47

Consolidation of Government Organizations (cont.)

Different consolidation methods

• Government Not-for-Profit Organizations:• Full consolidation: “line-by-line consolidation”• Requires adjustments of accounting policies to match Govt. accounting

policies•GNFPOs using PSAB +S4200 must prepare a reconciliation to PSAB

standalone standards for consolidation into Govt. FS-- If deferral method of accounting for contributions is used then

likely not many differences -- If restricted method of accounting for contribution is used then

there will likely be differences related to revenue recognition

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 48

Quarterly Reporting

• Required beginning in the April-June 2011 quarter:-- for Crowns, prepared in accordance with their basis of accounting-- for March 31st year-end Crowns, April-June 2011 quarter is the first

quarter of IFRS or PSAB -- comparative figures are required

• Conversions must be completed sooner.

© 2010 KPMG LLP, a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 49

Questions

Questions?

Andrew C. NewmanAudit Partner

Public Sector Audit Practice613-212-2877