post baccalaureate diploma in accounting

TRANSCRIPT

Post Baccalaureate Diploma in Accounting

The School of University Studies and Career Access and Community and Continuing Education have

developed the Post Baccalaureate in Accounting Diploma program. It is a program designed for students

to take the necessary courses to enter into the Certified Professional Accountant’s (CPA) program. All

courses have been approved by the CPA.

Rationale:

This program has been designed so that anyone with an approved Bachelor’s degree (as approved by

CPA) can take the courses, referred to as pre-requisite learning according to the CPA. Students can then

enter into the CPA Professional Education Program.

It is known that there is a substantial need for CPAs in Canada. The program will attract both domestic

and international students.

Admission Requirements

Successful completion of a recognized Bachelor Degree in a field other than Business, Commerce or

Accounting. It is the responsibility of the student to confirm that their Bachelor Degree satisfies the

degree prerequisite of the CPA Professional Education Program.

(https://www.cpacanada.ca/en/become-a-cpa/pathways-to-becoming-a-cpa/cpa-pep-admission-

undergraduate-degree-holders/entering-cpa-pep-other-degrees)

International students from a non-English speaking country will be required to provide proof of a

minimum 6.0 Academic IELTS or 80 iBT TOEFL result or equivalent within two years.

Suggested Course Map:

Semester 1

COM 204 – Financial Accounting (3 credits)

MATH 157 - Business Statistics (3 credits)

ECON 201 – Principles of Economics: Microeconomics (3 credits)

CIS 165 – Business Information Systems (3 credits)

LAW 294 – Business Law (3 credits)

Semester 2

ACC 251 – Intermediate Accounting I (3 credits)

ACC 255 – Management Accounting I (3 credits)

ECON 202 – Principles of Economics: Macroeconomics (3 credits)

FIN 257 – Finance I (3 credits)

MATH 257 – Business Statistics II (3 credits)

Semester 3

ACC 252 – Intermediate Accounting II (3 credits)

ACC 256 - Management Accounting II (3 credits)

ACC 281 – Taxation I *** (3 credits)

FIN 258 – Finance II (3 credits)

BUS 415 – Business Ethics *** (3 credits)

Semester 4

ACC 450 Advanced Financial Accounting *** (3 credits)

ACC 455 Advanced Managerial Accounting *** (3 credits)

ACC 381 Taxation II *** (3 credits)

BUS 410 Strategic Management *** (3 credits)

ACC 340 Audit & Assurance *** (3 credits)

PROGRAM PROFILE

Post Baccalaureate Diploma in Accounting

Program Title: Post Baccalaureate Diploma in Accounting

Full-time or Part-time

Admission type: Open

Length of program: 2 years

Program description: The program is designed for students to take the necessary courses to enter into the Certified Professional Accountant’s (CPA) program. All courses have been approved by the CPA. Graduates of the Post Baccalaureate in Accounting Diploma program are able to enter into the Certified Professional Accountant’s (CPA) Professional Education Program (CPA PEP)

ADMISSION REQUIREMENTS

Successful completion of a recognized Bachelor Degree in a field other than Business, Commerce or

Accounting. It is the responsibility of the student to confirm that their Bachelor Degree satisfies the

degree prerequisite of the CPA Professional Education Program.

(https://www.cpacanada.ca/en/become-a-cpa/pathways-to-becoming-a-cpa/cpa-pep-admission-

undergraduate-degree-holders/entering-cpa-pep-other-degrees)

International students from a non-English speaking country will be required to provide proof of a

minimum 6.0 Academic IELTS or 80 iBT TOEFL result or equivalent within two years.

GRADUATION REQUIREMENTS

The student must have a grade of B- or higher in all courses. This grade is required by CPA.

PROGRAM OUTLINE

COM 204 - Financial Accounting (3 credits)

MATH 157 – Business Statistics (3 credits)

ECON 201 – Principles of Economics: Microeconomics (3 credits)

CIS 165 – Business Information Systems (3 credits)

LAW 294 – Business Law (3 credits)

ACC 251 – Intermediate Accounting I (3 credits)

ACC 255- Management Accounting I (3 credits)

ECON 202 - Principles of Economics: Microeconomics (3 credits)

FIN 257 – Finance I (3 credits)

MATH 257 – Business Statistics II (3 credits)

ACC 252- Intermediate Accounting II (3 credits)

ACC 256 - Management Accounting II (3 credits)

ACC 281 - Taxation I (3 credits)

FIN 258 – Finance II (3 credits)

BUS 415 – Business Ethics (3 credits)

ACC 450 – Advanced Financial Accounting (3 credits)

ACC 455 – Advanced Managerial Accounting (3 credits)

ACC 381 - Taxation II (3 credits)

BUS 410 – Strategic Management (3 credits)

ACC 340 – Audit and Assurance (3 credits)

School of University Studies and Career Access

Business Program

TAXATION I ACC 281

Approved by Education Council: TBA Credits: 3.0 Term: Total Course Hours: 60

Prerequisite: COM 204 or ACC 152 (minimum B- Grade) Co-requisite: NA

Lecture Hours: 60 Lab Hours: 0

Instructor: Office Hours:

Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: This course is an introduction to Canadian Tax Systems. Students will be introduced to the Income Tax Act with a focus on the structure of the Act. Course topics include taxable employment; business and property income; eligible deductions; capital cost allowance; capital gains; and taxes payable.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course the student will be able to demonstrate the following CPA competencies:

Determines taxes payable for a corporation in non-routine situations 6.1.3

Determines income taxes payable for an individual in routine situations 6.2.2

Advises on specific tax-planning opportunities for individuals 6.2.4

Analyzes estate-planning opportunities for individuals 6.2.5

(Meets a portion of the required CPA Competency in the following areas. The remaining portion is covered in ACC 381):

Assess a corporate entity’s general tax issues 6.1.1

Determines taxes payable for a corporation in routine situations 6.1.2

Analyzes the tax consequences or planning opportunities for complex corporate functions 6.1.5

Describes the tax consequences of other corporate and partnership restructuring transactions 6.1.6

Assess general tax issues for an individual 6.2.1

Analyzes tax consequences for non-residents 6.2.6

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s established standards of conduct. Penalties for misconduct, including plagiarism, cheating and personal misconduct are outlined in the Standards of Conduct: Student Responsibility and Accountability document found in the policies section of CNC’s website. All students should familiarize themselves with this document. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES: Text: Canadian Tax Principles, Volume 1, 2 and Study Guide 2017-18 Edition by Byrd and Chen. Required Materials: Calculator

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

Assignments 15% A+ 90 % - 100 %

Mid Term Exams (2 @ 25% each) 50% A 85 % - 89.9 %

Final Exam 35% A- 80 % - 84.9 % B+ 76 % - 79.9 % B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 % C+ 64 % - 67.9%

Note: In order to be considered a CPA Equivalent, a student must obtain a minimum of a B- in the course. Exams must represent 75% or more of the total student evaluation

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide.

COURSE TOPICS Module 1: Introduction to Federal Taxation in Canada Module 2: Procedures and Administration Module 3: Income or Loss from and Office or Employment Module 4: Taxable Income and Tax Payable for Individuals Module 5: Capital Cost Allowance and Cumulative Eligible Capital Module 6: Income or Loss from a Business Module 7: Income from Property Module 8: Capital Gains and Capital Losses Module 9: Other Income, Other Deductions and Other Issues Module 10: Retirement Savings and Other Special Income Arrangement Module 11: Taxable Income and Tax Payable for Individuals Revisited

School of University Studies and Career Access

Business Program

Business Ethics BUS 415

Credits: 3.0

Total Course Hours: 45

Approved by Education Council: TBA Term:

Prerequisite: 30 Credits in the Post Bacc. Diploma in Accounting Program (minimum B- Grade)

Co-requisite: NA

Lecture Hours: 45 Lab Hours: 0

Instructor: Office Hours: Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: Students will face ethical dilemmas throughout their career. This course will provide students with a

knowledge of ethical theories, and through the use of case studies students will have an

opportunity to apply theories and develop a methodology to help decision making in the complex

business environment where there are differing needs of various shareholders.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course students should be able to demonstrate the following

competencies:

Examine ethical issues they may face in their careers

Compare different ethical theories Differentiate between legal decisions and ethical decisions Illustrate Corporate Social Responsibility in ethical decision-making Combine critical thinking skills and business ethics to address ethical dilemmas

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s

established standards of conduct. Penalties for misconduct, including plagiarism, cheating and

personal misconduct are outlined in the Standards of Conduct: Student Responsibility and

Accountability Document found in the policies section of CNC’s website. All students should

familiarize themselves with this document.

http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES: Sexty, Robert W. (2014), “Canadian Business and Society: Ethics, Responsibilities & Sustainability,” McGraw Hill, 3rd ed. Case Pack from various sources such as Harvard and Ivey case studies.

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

Individual Research Paper 20% A+ 90 % - 100 %

Group Case Studies 2 x 15% 30% A 85 % - 89.9 %

Mid Term Exam 25% A- 80 % - 84.9 %

Final Exam 25% B+ 76 % - 79.9 % B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 % C+ 64 % - 67.9%

Note: In order to be considered a CPA Equivalent, a student must obtain a minimum of a B- in the course.

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide.

COURSE TOPICS

1. Introduction of Business Ethics

2. Ethics and Stakeholders

3. Ethical Theories

4. Corporate Social Responsibility, Concepts and Practice

5. Ethical Issues in Finance

6. Ethical Issues in Operations

7. Ethical Issues in Marketing

8. Ethical Issues in Human Resources

9. Ethical Issues in a Global Economy

10. Current issues in Business Ethics

School of University Studies and Career Access

Business Program

ADVANCED FINANCIAL ACCOUNTING ACC 450

Approved by Education Council: TBA Term:

Credits: 3.0

Prerequisite: ACC 252 (minimum B-grade) Co-requisite: NA

Lecture Hours: 60 Lab Hours: 0

Instructor: Office Hours: Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: In this course students will build on their learning from ACC 256. Topics that are covered more in depth than before include the accounting for: business combinations, reporting for both wholly and non- wholly owned subsidiaries; segment reporting; foreign currency transactions; reporting for non-for- profit entities and government entities.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course the student will meet the required CPA Competency in the following areas of Advanced Financial Reporting:

Explains implications of current trends and emerging issues in financial reporting 1.1.4

Identifies financial reporting needs for the public sector 1.1.5

Identifies specialized financial reporting requirements for specified regulatory and other filing requirements 1.1.6

Evaluates treatment for routine transactions 1.2.2

Evaluates treatment for non-routine transactions 1.2.3

Prepares routine financial statement note disclosure 1.3.2

Analyzes complex financial statement note disclosure 1.4.1

Evaluates financial statements including note disclosures 1.4.2

Analyzes and provides input in the preparation of the management communication 1.4.3

Interprets financial reporting results for stakeholders (external or internal) 1.4.4

Analyzes and predicts the impact of strategic and operational decisions of financial results 1.4.5

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s established standards of conduct. Penalties for misconduct, including plagiarism, cheating and personal misconduct are outlined in the Standards of Conduct: Student Responsibility and Accountability document found in the policies section of CNC’s website. All students should familiarize themselves with this document. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES: Text: Advanced Financial Accounting, Seventh Edition by Thomas Beech, V. Umashanker Trivedi and Kenneth E. MacAulay. Copyright 2014

Materials: Calculator

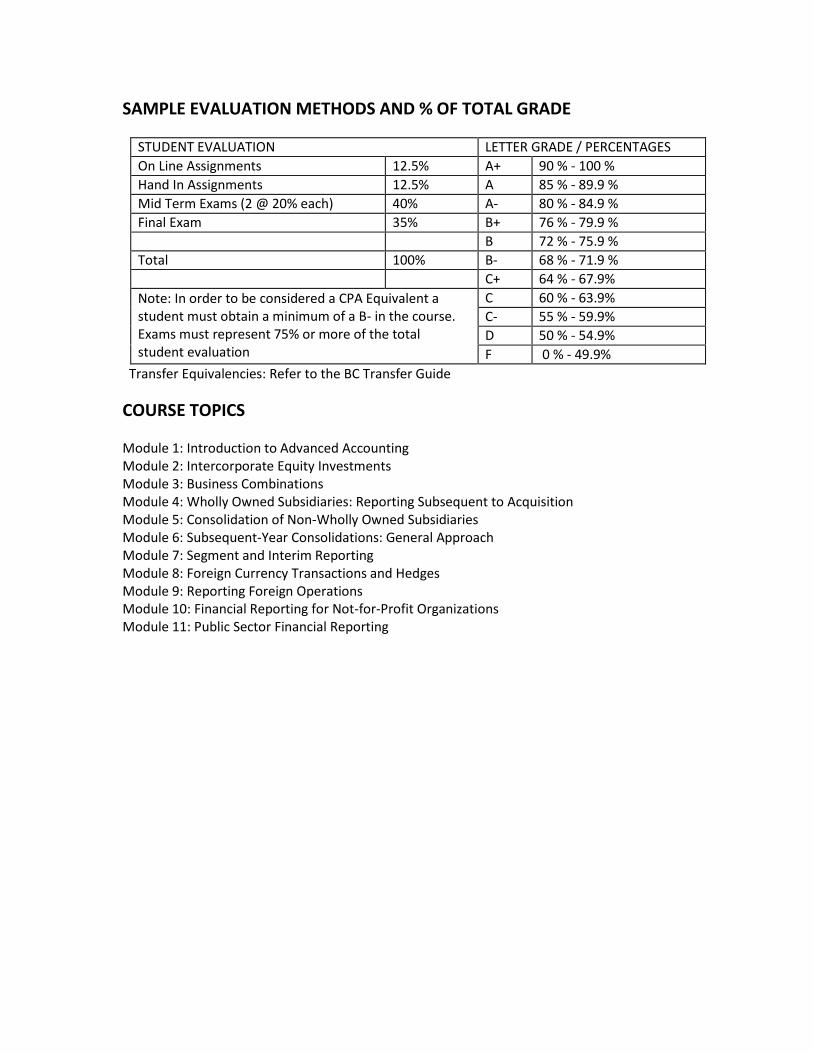

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

On Line Assignments 12.5% A+ 90 % - 100 %

Hand In Assignments 12.5% A 85 % - 89.9 %

Mid Term Exams (2 @ 20% each) 40% A- 80 % - 84.9 %

Final Exam 35% B+ 76 % - 79.9 % B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 % C+ 64 % - 67.9%

Note: In order to be considered a CPA Equivalent a student must obtain a minimum of a B- in the course. Exams must represent 75% or more of the total student evaluation

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide

COURSE TOPICS

Module 1: Introduction to Advanced Accounting Module 2: Intercorporate Equity Investments Module 3: Business Combinations Module 4: Wholly Owned Subsidiaries: Reporting Subsequent to Acquisition Module 5: Consolidation of Non-Wholly Owned Subsidiaries Module 6: Subsequent-Year Consolidations: General Approach Module 7: Segment and Interim Reporting Module 8: Foreign Currency Transactions and Hedges Module 9: Reporting Foreign Operations Module 10: Financial Reporting for Not-for-Profit Organizations Module 11: Public Sector Financial Reporting

School of University Studies and Career Access

Business Program

ADVANCED MANAGERIAL ACCOUNTING ACC 455

Approved by Education Council: TBA Term:

Credits: 3.0

Prerequisite: ACC 256 (minimum B- grade) Co-requisite: NA

Lecture Hours: 60 Lab Hours: 0

Instructor: Office Hours:

Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: Students will continuing learning about management accounting that they started in ACC 256. Topics will include: the nature of costs; opportunity cost of capital; capital budgeting; organizational architecture; responsibility accounting, budgeting; cost allocation theory and practices; absorption cost accounting, and the criticisms of it; standard costing and overhead.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course the student will be able to demonstrate the following

CPA competencies:

Evaluates mechanisms used for compliance purposes 2.1.3

Designs an effective risk management program and evaluates its impact on shareholder value 2.5.1

Recommends improvements to reporting systems to meet information needs 3.1.3

Recommends changes identified by applying process improvement methodologies 3.3.3

Recommends cost management improvements across the entity 3.3.4

Evaluates sustainable profit maximization and capacity management performance 3.5.2

Evaluates performance using accepted frameworks 3.6.1

Evaluates performance of responsibility centers 3.6.2

Evaluates root causes of performance issues 3.6.3

Analyzes the implications of management incentive schemes and employee compensation 3.7.1

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s established standards of conduct. Penalties for misconduct, including plagiarism, cheating and personal misconduct are outlined in the Standards of Conduct: Student Responsibility and Accountability document found in the policies section of CNC’s website. All students should familiarize themselves with this document. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES: Text: Accounting for Decision Making and Control Ninth Edition by Jerold Zimmerman. Copyright 2017 Required Materials: Calculator

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

Assignments 25% A+ 90 % - 100 %

Mid Term Exams (2 @ 20% each) 40% A 85 % - 89.9 %

Final Exam 35% A- 80 % - 84.9 %

B+ 76 % - 79.9 %

B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 %

C+ 64 % - 67.9%

Note: In order to be considered a CPA Equivalent a student must obtain a minimum of a B- in the course. Exams must represent 75% or more of the total student evaluation.

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide.

COURSE CONTENT or TOPICS

Module 1: Introduction Module 2: The Nature of Costs Module 3: Opportunity Cost of Capital and Capital Budgeting Module 4: Organizational Architecture Module 5: Responsibility Accounting and Transfer Pricing Module 6: Budgeting Module 7: Cost Allocation Theory Module 8: Cost Allocation Practices Module 9: Absorption Cost Systems Module 10: Criticism of Absorption Cost Systems: Incentive to Overproduce Module 11: Criticisms of Absorption Cost Systems: Inaccurate Product Costs Module 12: Standard Costs: Direct Labour and Materials Module 13: Overhead and Marketing Variances Module 14: Management Accounting in a Changing Environment

School of University Studies and Career Access

Business Program

TAXATION II ACC 381

Approved by Education Council: TBA Term:

Credits: 3.0

Prerequisite: ACC 281 (minimum B- grade) Co-requisite: NA

Lecture Hours: 60 Lab Hours: 0

Instructor: Office Hours:

Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: This course is a continuation of ACC 281 focusing Canadian Tax Systems. Students will continue to utilize the Income Tax Act with an emphasis on the structure of the Act. Course topics include taxable income and tax payable for corporations, taxation of corporate investment income; rollovers including those in section 85; taxation of sales of an incorporated business; partnerships; trust and estate planning, international taxes and other issues in taxation. In addition, students will be introduced to management decisions around corporate taxation.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course the student will be able to demonstrate the following CPA competencies:

Advises on tax consequences or specific tax planning opportunities for shareholders and closely and their closely held corporations 6.1.4

Determines income taxes payable for an individual in non-routine situations 6.2.3

(Meets a portion of the required CPA Competency that began in Taxation 281 in the following areas)

Assess a corporate entity’s general tax issues 6.1.1

Determines taxes payable for a corporation in routine situations 6.1.2

Analyzes the tax consequences or planning opportunities for complex corporate functions 6.1.5

Describes the tax consequences of other corporate and partnership restructuring transactions 6.1.6

Assess general tax issues for an individual 6.2.1

Analyzes tax consequences for non-residents 6.2.6

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s established standards of conduct. Penalties for misconduct, including plagiarism, cheating and personal misconduct are outlined in the Standards of Conduct: Student Responsibility and Accountability Document found in the policies section of CNC’s website. All students should familiarize themselves with this document. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES:

Text: Canadian Tax Principles, Volume 2 and Study Guide 2017-18 Edition by Byrd and

Chen. Required Materials: Calculator

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

Assignments 15% A+ 90 % - 100 %

Mid Term Exams (2 @ 25% each) 50% A 85 % - 89.9 %

Final Exam 35% A- 80 % - 84.9 %

B+ 76 % - 79.9 %

B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 %

C+ 64 % - 67.9%

Note: In order to be considered a CPA Equivalent a student must obtain a minimum of a B- in the course. Exams must represent 75% or more of the total student evaluation

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide.

COURSE TOPICS (As continued from ACC 281 – Taxation I)

Module 12: Taxable Income and Tax Payable for Corporations Module 13: Taxation of Corporate Investment Income Module 14: Other Issues in Corporate Taxation Module 15: Corporate Taxation and Management Decisions Module 16: Rollovers under Section 85 Module 17: Other Rollovers and Sale of an Incorporated Business Module 18: Partnerships Module 19: Trusts and Estate Planning Module 20: International Issues in Taxation Module 21: GST/HST/PST

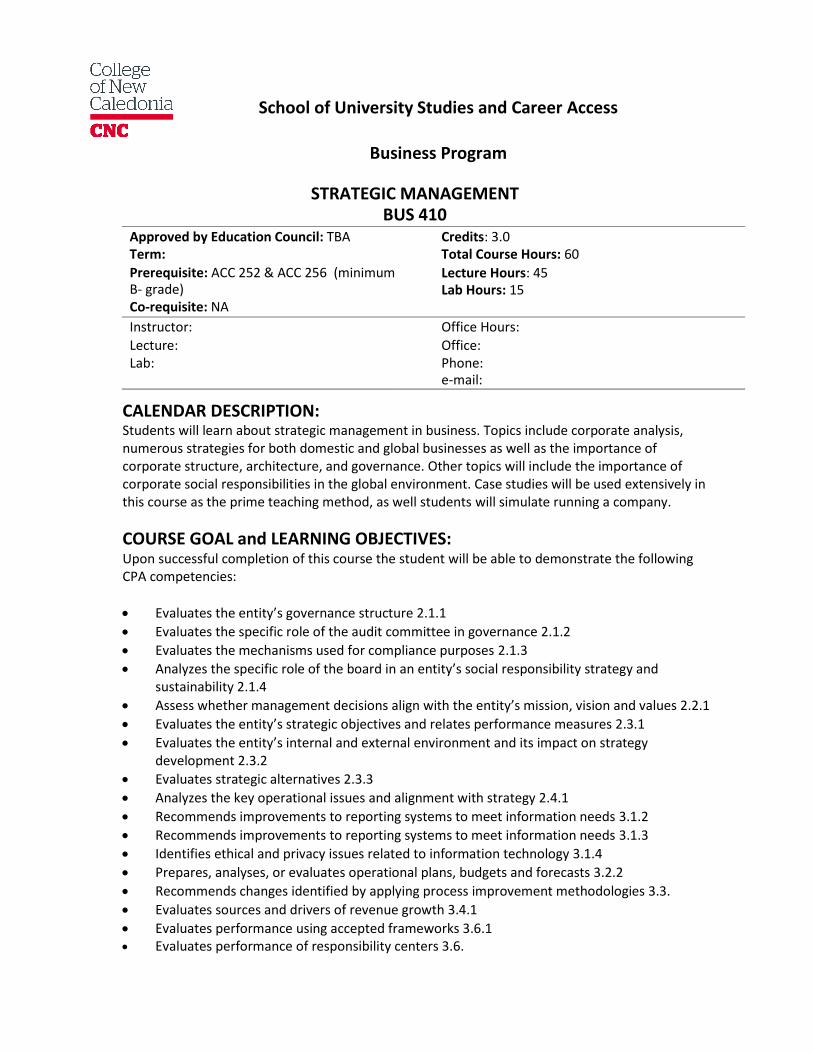

School of University Studies and Career Access

Business Program

STRATEGIC MANAGEMENT BUS 410

Approved by Education Council: TBA Term:

Credits: 3.0 Total Course Hours: 60

Prerequisite: ACC 252 & ACC 256 (minimum B- grade) Co-requisite: NA

Lecture Hours: 45 Lab Hours: 15

Instructor: Office Hours:

Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: Students will learn about strategic management in business. Topics include corporate analysis, numerous strategies for both domestic and global businesses as well as the importance of corporate structure, architecture, and governance. Other topics will include the importance of corporate social responsibilities in the global environment. Case studies will be used extensively in this course as the prime teaching method, as well students will simulate running a company.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course the student will be able to demonstrate the following CPA competencies:

Evaluates the entity’s governance structure 2.1.1

Evaluates the specific role of the audit committee in governance 2.1.2

Evaluates the mechanisms used for compliance purposes 2.1.3

Analyzes the specific role of the board in an entity’s social responsibility strategy and sustainability 2.1.4

Assess whether management decisions align with the entity’s mission, vision and values 2.2.1

Evaluates the entity’s strategic objectives and relates performance measures 2.3.1

Evaluates the entity’s internal and external environment and its impact on strategy development 2.3.2

Evaluates strategic alternatives 2.3.3

Analyzes the key operational issues and alignment with strategy 2.4.1

Recommends improvements to reporting systems to meet information needs 3.1.2

Recommends improvements to reporting systems to meet information needs 3.1.3

Identifies ethical and privacy issues related to information technology 3.1.4

Prepares, analyses, or evaluates operational plans, budgets and forecasts 3.2.2

Recommends changes identified by applying process improvement methodologies 3.3.

Evaluates sources and drivers of revenue growth 3.4.1

Evaluates performance using accepted frameworks 3.6.1 Evaluates performance of responsibility centers 3.6.

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s established standards of conduct. Penalties for misconduct, including plagiarism, cheating and personal misconduct are outlined in the Standards of Conduct: Student Responsibility and Accountability document found in the policies section of CNC’s website. All students should familiarize themselves with this document. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES:

Text: Strategic Management Theory by Hill, Schilling and Jones. Copyright 2017

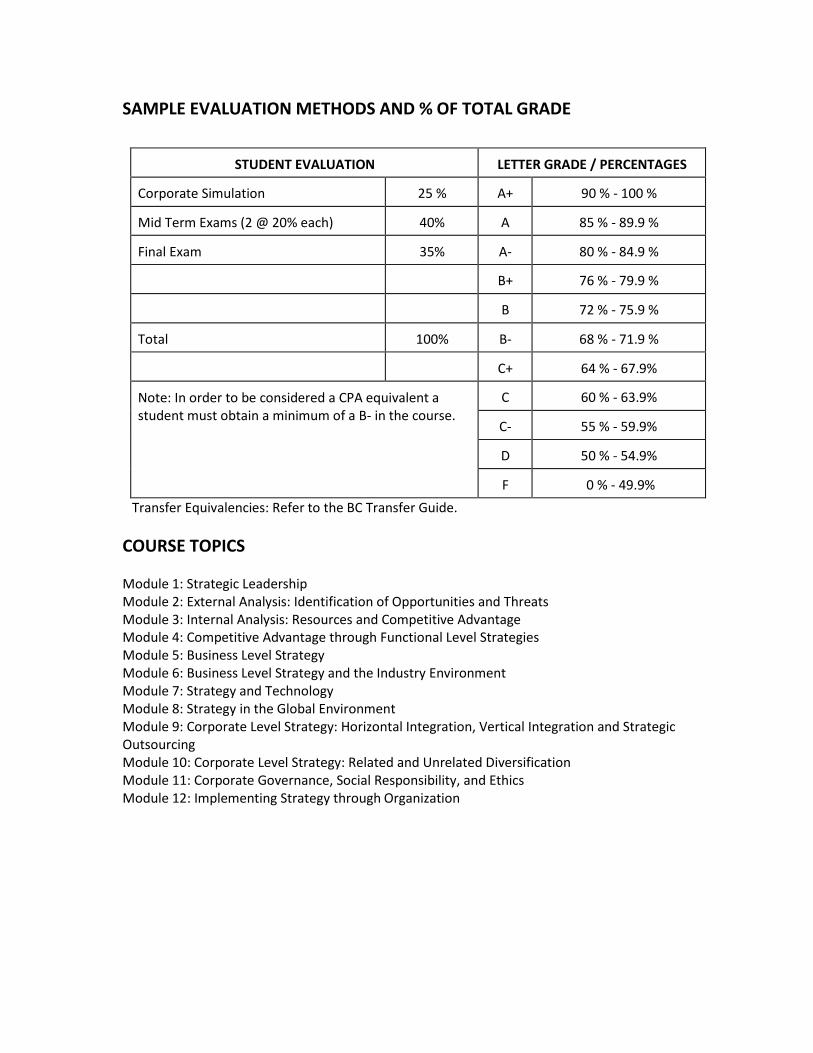

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

Corporate Simulation 25 % A+ 90 % - 100 %

Mid Term Exams (2 @ 20% each) 40% A 85 % - 89.9 %

Final Exam 35% A- 80 % - 84.9 %

B+ 76 % - 79.9 %

B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 %

C+ 64 % - 67.9%

Note: In order to be considered a CPA equivalent a student must obtain a minimum of a B- in the course.

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide.

COURSE TOPICS

Module 1: Strategic Leadership Module 2: External Analysis: Identification of Opportunities and Threats Module 3: Internal Analysis: Resources and Competitive Advantage Module 4: Competitive Advantage through Functional Level Strategies Module 5: Business Level Strategy Module 6: Business Level Strategy and the Industry Environment Module 7: Strategy and Technology Module 8: Strategy in the Global Environment Module 9: Corporate Level Strategy: Horizontal Integration, Vertical Integration and Strategic Outsourcing Module 10: Corporate Level Strategy: Related and Unrelated Diversification Module 11: Corporate Governance, Social Responsibility, and Ethics Module 12: Implementing Strategy through Organization

School of University Studies and Career Access

Business Program

AUDIT & ASSURANCE ACC 340

Approved by Education Council: TBA Term:

Credits: 3.0 Total Course Hours: 60

Prerequisite: COM 204 or ACC 152 (minimum B- Grade) Co-requisite: NA

Lecture Hours: 45 Lab Hours: 15

Instructor: Office Hours:

Lecture: Office: Lab: Phone:

e-mail:

CALENDAR DESCRIPTION: Students will learn about the audit profession, the audit process, application of the audit process, reporting and other assurance engagements. Major topics will include materiality, risk, internal control, control risk, independence and ethics in the profession. Students will apply the audit process in doing an audit practice set of a fictional company during their lab time.

COURSE GOAL and LEARNING OBJECTIVES: Upon successful completion of this course the student will be able to demonstrate the following CPA competencies:

Assesses the entity’s risk assessment processes 4.1.1

Evaluates the information system, including the related processes 4.1.2

Advises on an entity’s assurance needs 4.2.1

Explains the implications of pending changes in assurance standards 4.2.2

Assesses issues related to the undertaking of the engagement of project 4.3.1

Assesses which set of criteria to apply the subject matter being evaluated 4.3.2

Assess or develops which standards or guidelines to apply based on the nature and expectations of the assurance engagement or project 4.3.3

Assesses materiality for the assurance engagement or project 4.3.4

Assesses the risks of the project, or, for audit engagements, assesses the risks of material misstatement at the financial statement level and at the assertion level for classes of transactions, account balances, and disclosures 4.3.5

Develops appropriate procedures based on the identified risk of material misstatement 4.3.6

Performs the work plan 4.3.7

Evaluates the evidence and results of analysis 4.3.8

Documents the work performed and its results 4.3.9

Draws conclusions and communicates results 4.3.10

Prepares or interprets information and reports for stakeholders 4.3.11

Applies comprehensive auditing techniques 4.4.1

ACADEMIC HONESTY AND STUDENT CONDUCT Students are expected to conduct themselves with academic integrity and in accordance with CNC’s established standards of conduct. Penalties for misconduct, including plagiarism, cheating and personal misconduct are outlined in the Standards of Conduct: Student Responsibility and Accountability document found in the policies section of CNC’s website. All students should familiarize themselves with this document. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=83

ACCESSIBILITY SERVICES Students who require academic accommodations as a result of a disability should advise both the instructor and Accessibility Services. Students requiring support should familiarize themselves with the Accommodations for Students with Disabilities policy. http://tools.cnc.bc.ca/CNCPolicies/policyFiles.ashx?polId=137

CLASSROOM BASED RESEARCH If classroom based research is conducted, the class will be instructed on appropriate ways of conducting research with human subjects based on the CNC Policy and Procedure for Ethical Research. The ethical framework for this study will be articulated by the instructor in the classroom.

SAMPLE REFERENCES:

Text: Auditing: The Art and Science of Assurance Engagements, Canadian Thirteenth Edition by Arens, Elder, Beasley and Jones. Copyright 2016 Supplemental Text: Practice Audit Set TBD Materials: Calculator

SAMPLE EVALUATION METHODS AND % OF TOTAL GRADE

STUDENT EVALUATION LETTER GRADE / PERCENTAGES

Assignments (Lab) 25% A+ 90 % - 100 %

Mid Term Exams (2 @ 20% each) 40% A 85 % - 89.9 %

Final Exam 35% A- 80 % - 84.9 %

B+ 76 % - 79.9 %

B 72 % - 75.9 %

Total 100% B- 68 % - 71.9 %

C+ 64 % - 67.9%

Note: In order to be considered a CPA Equivalent a student must obtain a minimum of a B- in the course. Exams must represent 75% or more of the total student evaluation

C 60 % - 63.9%

C- 55 % - 59.9%

D 50 % - 54.9%

F 0 % - 49.9%

Transfer Equivalencies: Refer to the BC Transfer Guide.

COURSE TOPICS Module 1: The Demand for Audit and Other Assurance Services Module 2: The Public Accounting Profession and Audit Quality Module 3: Legal Liability Module 4: Professional Judgement and Ethics Module 5: Audit Responsibilities and Objectives Module 6: Client Acceptance and Planning the Audit Module 7: Materiality and Risk Module 8: Internal Control and Control Risk Module 9: Audit Evidence Module 10: Audit Strategy and Audit Program Module 11: Audit Sampling Concepts Module 12: Audit of the Revenue Cycle Module 13: Audit of the Acquisition and Payment Cycle Module 14: Audit of Inventory and Distribution Cycle Module 15: Audit of the Human Resources and Payroll Cycle Module 16: Audit of the Capital Acquisition and Repayment Cycle Module 17: Audit of Cash Balances Module 18: Completing the Audit Module 19: Audit Reports on Financial Statements Module 20: Other Assurance and Non Assurance Services Note: Modules 11 – 18 will be covered in the Labs as students will be doing an audit practice set.