power sector challenges, reforms and opportunities in...

TRANSCRIPT

www.gsb.uct.ac.za/mir @AntonEberhard

Prof Anton Eberhard Management Program in Infrastructure Reform and Regulation

University of Cape Town

Power Sector Challenges, Reforms

and Opportunities in East Africa

Presentation to DFID, London 23 June 2014

www.gsb.uct.ac.za/mir

@AntonEberhard

www.gsb.uct.ac.za/mir @AntonEberhard

Outline

1. Africa’s power challenges

2. The response: power sector reform

1. Ongoing need to improve performance of state-

owned electricity utilities

2. Need to accelerate investment in power

generation and networks

www.gsb.uct.ac.za/mir @AntonEberhard

Power infrastructure in Africa is underdeveloped

• Installed capacity in SSA is around 80,000 MW – Spain has more

– South Africa accounts for more than half

– Kenya 1500, Tanzania 1200, Uganda 680, Rwanda 85

• Installed capacity per capita 10% of LA

• Consumption per capita barely 1% of high-income

countries and declining

www.gsb.uct.ac.za/mir @AntonEberhard

A global outlier

Generation capacity (MW per million population)

Electrification rate (Percentage of households)

Electricity consumption (kWh per capita per year)

Power prices (US$ per kilowatt-hour)

Source: Africa Infrastructure Country Diagnostic

www.gsb.uct.ac.za/mir @AntonEberhard

Supply is often unreliable

• Insufficient investment in maintenance and refurbishment

• WB Enterprise surveys reveal average of 56 days per annum with power interruptions – losses in forgone sales and damaged equipment

• More than half of large

firms have back-up

generators

• Own-generation now a

significant proportion of

installed capacity

www.gsb.uct.ac.za/mir @AntonEberhard

Days in year with power interruptions

Source: World Bank Enterprise Surveys

www.gsb.uct.ac.za/mir @AntonEberhard

Very low access to power

Source: Earthlights, 2000

Overall Rural

% %

Tanzania 15 4

Kenya 19 7

Uganda 15 7

Rwanda 16 2

www.gsb.uct.ac.za/mir @AntonEberhard

Access to energy by income quintile unequal

0%

20%

40%

60%

80%

100%

Q1 Q2 Q3 Q4 Q5

Electricity for lighting

Wood/Charcoal for cooking

Gas/LPG for Cooking

Kerosene/Paraffin for Cooking

Source: Africa Infrastructure Country Diagnostic

www.gsb.uct.ac.za/mir @AntonEberhard

Hidden or quasi-fiscal costs of poor electricity service

Source: Africa Infrastructure Country Diagnostic

www.gsb.uct.ac.za/mir @AntonEberhard

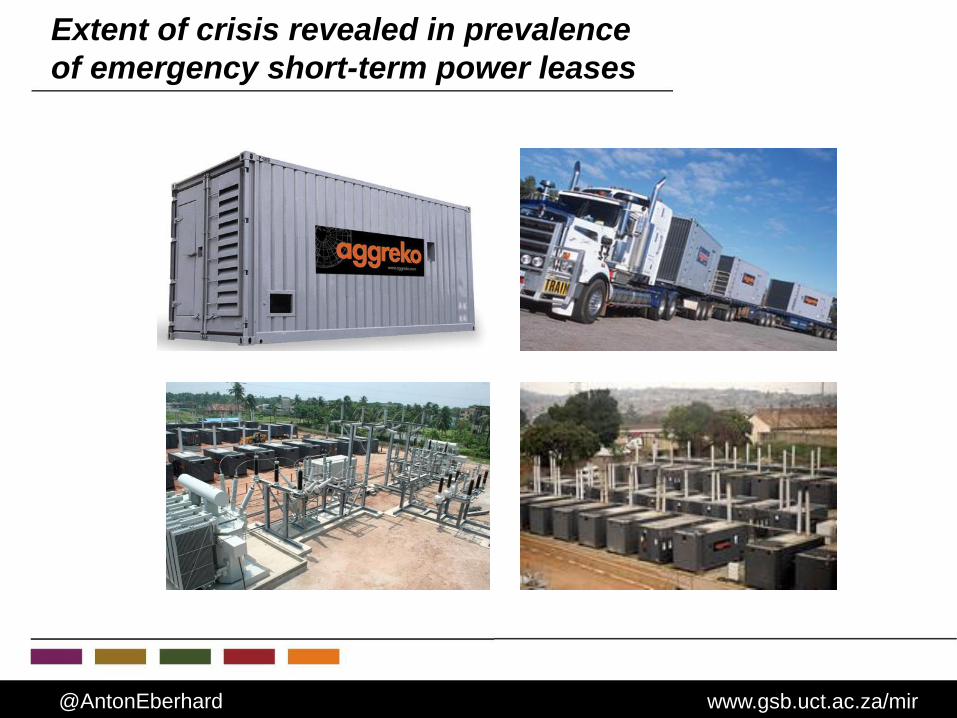

Extent of crisis revealed in prevalence

of emergency short-term power leases

www.gsb.uct.ac.za/mir @AntonEberhard

Emergence of the “standard model” of reform

Vertically-integrated, publicly-owned monopoly

Commercialisation and corporatisation

Independent regulation

Unbundling to separate potentially competitive elements from non-competitive elements

Private sector participation

Introduction of competition IPPs for the market

or wholesale competition in the market

eventually customer choice and retail competition

www.gsb.uct.ac.za/mir @AntonEberhard

MODEL 1:NATURAL MONOPOLY

MODEL 4:RETAIL COMPETITION

MODEL 3:WHOLESALE COMPETITION

MODEL 2:SINGLE BUYER

Utilities are vertically integrated

Generation, transmission and distribution are not subject to competition

No-one has choice of supplier

Single buyer chooses from various generators (IPPs)

Access to transmission xxx not permitted for sales to final customers

Single buyer has monopoly over transmission networks and over sales to final customer

Distribution companies buy direct from generator (IPPs)

Distribution companies have monopoly over final customers

Open access to transmission wires

Generators compete to supply power

Power pool established to

facilitate x

All customers have choice of supplier

Open access to T & D wires

Distribution is separate from retail activity

Retail industry is competitive

Generation (G)

Transmission (T)

Distribution (D)

Customer (C)

IPP IPP

Single buyer G & T

D D

C

G GG

TPower poolexchange

Franchisecustomers

(FC)

Largecustomers

(LC)

D

C

D

LC

D

C

G GG

TPower poolexchange

www.gsb.uct.ac.za/mir @AntonEberhard

Power market structures in E. Africa

Uganda

G IPPs

T

D

Kenya Tanzania / Rwanda

Private State-owned

KenGen

KPLC

G IPPs

T

D Tanesco

D

T

G IPPs

UEDCL

UETCL

UEGCL

Umeme

Eskom

www.gsb.uct.ac.za/mir @AntonEberhard

Nowhere in Africa has “standard reform model” been implemented in full

• Initial power sector reform plans often stalled or reversed – Nowhere do we have full wholesale or retail electricity competition

– Many countries have not unbundled • e.g. Tanzania, Rwanda

– Private sector participation is still often constrained

• Instead, hybrid power markets have developed – Incumbent state-owned utilities have retained dominant market

positions

– Independent Power Producers (IPPs) are being introduced on the margin

– i.e. both State Owned Enterprise (SOEs) and IPPs are involved in new generation investments

[Exceptions are private concessions in countries such as Uganda, West Africa and privatisation in Nigeria]

www.gsb.uct.ac.za/mir @AntonEberhard

Hybrid power markets are challenging

Performance of state-owned utilities

– Still responsible for electricity provision

– Often unable to finance new investment

– And poor financial and technical efficiencies

New investment Responsibilities for planning, procurement and

contracting “fall between the cracks” – unclear,

neglected, sub-optimal => inadequate investment

www.gsb.uct.ac.za/mir @AntonEberhard

State-owned utilities require ongoing reform

1. Clarification of roles and responsibilities • Public entity management legislation

• Corporatisation

• Codes of corporate governance

• Performance / management contracts

• Effective supervisory / monitoring agencies

• Transparent transfers for social programmes

2. Changing the political-economy of the uitlity • Improved transparency and information

• Structural reform and direct competition

• Mixed-capital enterprises

www.gsb.uct.ac.za/mir @AntonEberhard

Need to clarify and allocate responsibilities for

generation investments

• Allocate responsibility and build capacity for generation

expansion planning

• Develop clear criteria for allocating new build opportunities between the incumbent SOE and IPPs?

• Allocate responsibility & initiate timely competitive bids for IPPs

• Develop procedures for evaluating unsolicited bids

• Develop capacity for contract negotiations with new IPPs

• Avoid potential conflicts of interest when SOEs are the Single-Buyer

www.gsb.uct.ac.za/mir @AntonEberhard

IPP performance differs

• Kenya has better record in attracting IPPs

– Dynamic planning system

– Timely initiation of international competitive tenders

– Capacity to effectively procure and contract built in KPLC

• Tanzania has worst record

– Poor planning

– Unsolicited bids rater than ICBs

– Series of corruptions scandals in new power deals

Kenya’s IPPs much cheaper and more reliable than Tanzania

www.gsb.uct.ac.za/mir @AntonEberhard

Uganda is attracting many small IPP investments MW

• Bujagali 250

• Jacobsen, Namanve 50

• Electro-Maxx, Tororo 20

• Mpanga Hydro 18

• TronderPower, Bugoye 13

• Kasese Cobalt, Mubuku III 9.5

• Kilembe Mines 5

• EcoPower, Ishasha 6.5

• Kakira Sugar 12

• Kinyara Sugar (captive) 5

• Kabalega 9 etc

www.gsb.uct.ac.za/mir @AntonEberhard

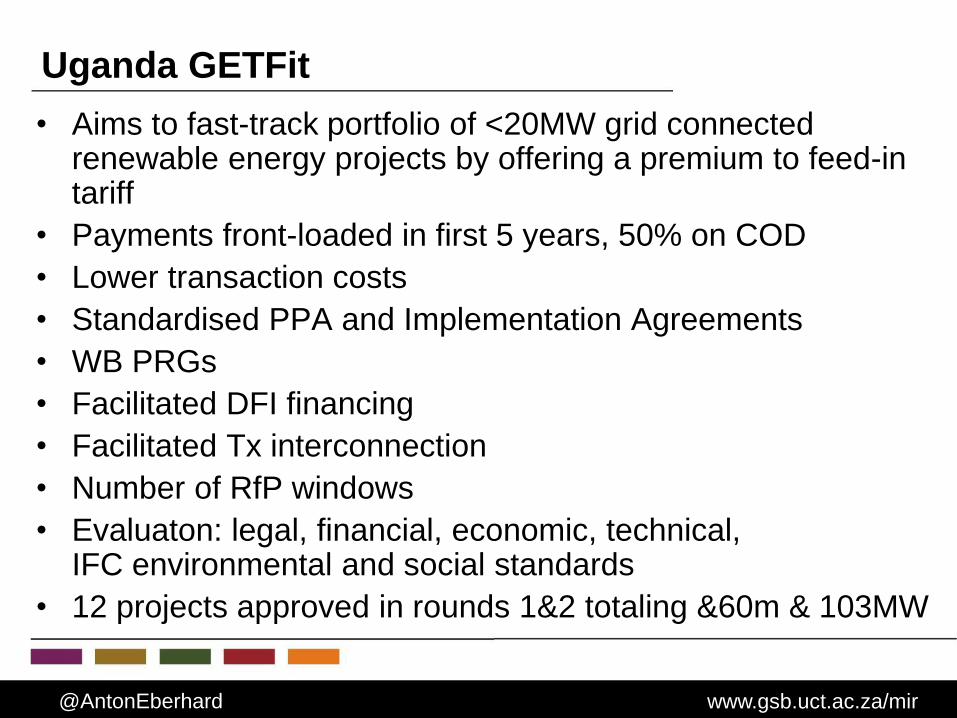

Uganda GETFit

• Aims to fast-track portfolio of <20MW grid connected renewable energy projects by offering a premium to feed-in tariff

• Payments front-loaded in first 5 years, 50% on COD

• Lower transaction costs

• Standardised PPA and Implementation Agreements

• WB PRGs

• Facilitated DFI financing

• Facilitated Tx interconnection

• Number of RfP windows

• Evaluaton: legal, financial, economic, technical, IFC environmental and social standards

• 12 projects approved in rounds 1&2 totaling &60m & 103MW

www.gsb.uct.ac.za/mir @AntonEberhard

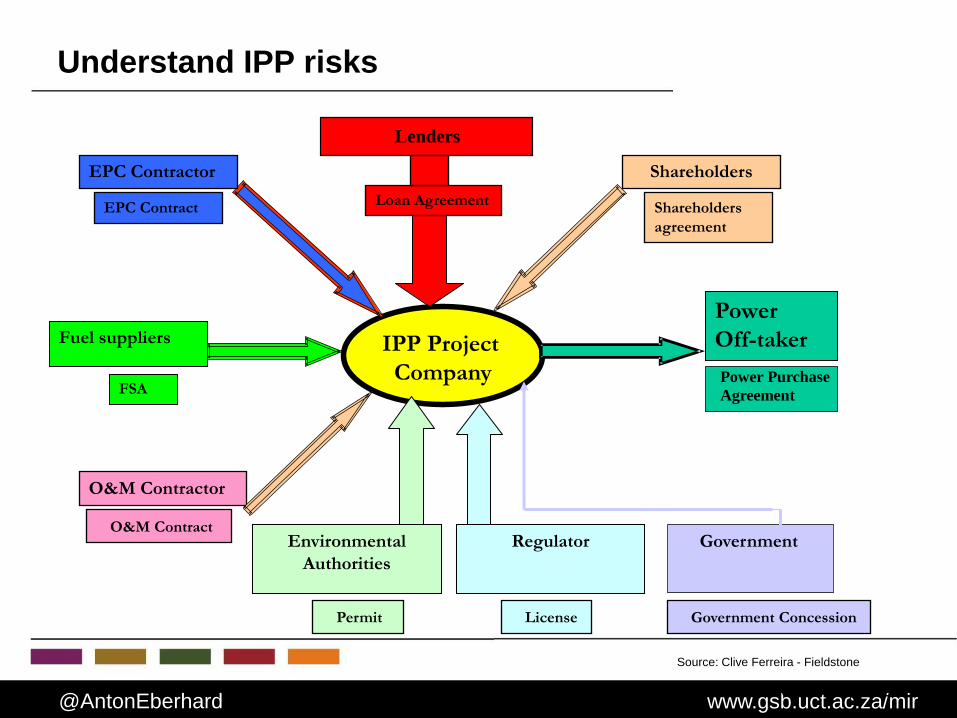

Power

Off-taker

Power Purchase

Agreement

IPP Project

Company

Fuel suppliers

FSA

Lenders

O&M Contractor

O&M Contract

EPC Contractor Shareholders

EPC Contract Loan Agreement

Environmental

Authorities

Permit

Shareholders

agreement

Regulator

License Government Concession

Modified from Clive Ferreira, Fieldstone

Source: Clive Ferreira - Fieldstone

Government

Understand IPP risks

www.gsb.uct.ac.za/mir @AntonEberhard

Contributing elements to IPP success

• Favourable investment climate

• Clear policy and legal framework

• Coherent power sector planning

• Transparent and credible regulatory oversight

• Competitive bidding practices

Country level

www.gsb.uct.ac.za/mir @AntonEberhard

Contributing elements to success

• Committed equity partners

• Favourable debt arrangements

• Secure and adequate revenue stream – Credit worthiness of off-taker

– PPA

– Appropriate security & credit enhancement measures

• Secure, competitive fuel contracts

• Positive technical performance

• Ongoing strategic and risk management

Project level

www.gsb.uct.ac.za/mir @AntonEberhard

In summary

• The scale of the challenge implies that ideological debates

around public versus private investment are irrelevant /

meaningless

• All sources of finance have to be mobilised

• Which means an integrated approach of

– fixing public utilities

– accelerating private sector participation

– welcoming also non-OECD sources of finance and

projects

www.gsb.uct.ac.za/mir @AntonEberhard

DfiD’s role in facilitating more investment in power

• Strengthen enabling environment for investment – Clear policy and legal framework

– Coherent power sector planning PPIAF

– Transparent and credible regulatory oversight TAF

– Competitive bidding practices

• Support to governments in structuring transactions (DevCo)

• Early stage project development (InfraCo Africa)

• Mobilisation of domestic capital markets (DevCo)

• Long-term debt & mezzanine finance (EAIF)

• Specific support for renewables (GETFiT, GAP)

• …………

• …………

www.gsb.uct.ac.za/mir @AntonEberhard

Prof Anton Eberhard Research, training courses, consultancy

University of Cape Town

The Management Programme in Infrastructure

Reform & Regulation (MIR) is an emerging centre

of excellence and expertise in Africa. It is

committed to enhancing knowledge and capacity to

manage the reform and regulation of the electricity,

gas, telecommunications, water and transport

industries in support of sustainable development.

www.gsb.uct.ac.za/mir