powerpoint presentation€¦ · ppt file · web view · 2017-09-0150 days of gst – practical...

TRANSCRIPT

50 Days of GST – Practical Issues Impacting Trade & Industry

Sectoral Impact – Logistics, Transportation & Related Services

www.amtoi.org

Presented by Vivek Kele, President, AMTOIDate 23rd August , 2017

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

GST Path breaking tax reform Harmonization of taxes Elimination of tax as a cost Possible elimination of unwanted business structures Long way to go Confusion in the market in many sectors Classification issues in goods Classification issues in services

2

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

GST in India CGST would be a levy by the Central Government through law made by

the Parliament.

SGST would be a levy by each State through law made by State Legislature.

IGST would be a levy by the Centre through law made by the Parliament

on the supply of any goods and / or services in the course of inter-State

trade or commerce.

IGST would also apply on a supply of goods and / or services in the course of import into the territory of India.

GST Compensation Cess would be a levy by the Central Government on inter / intra-State supplies of goods or services or both.

3

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

GST at a Glance The distinction between goods and services continue. Goods have 8 rates viz. Zero rated, Exempt, 0.25%, 3%, 5%, 12%,

18% and 28%. Some items also attract cess. Services have 5 rates viz. Exempt, 5%, 12%, 18% and 28%. Different place of supply provisions for goods and

services. Different place of supply provisions based on location of

persons. Location of supplier of services defined. Location of recipient of services defined. Export of services defined.

4

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Service Sector Earlier, service tax was paid to the Centre at the rate of 14% with

SBC of 0.5% and KKC of 0.5%.

Earlier, a Pan India Organization generally paid service tax at one location.

New law makes a distinction between supply of services within a State and supply of services in the course of inter-State trade or commerce.

Where a supply of services is within a State, the transaction would attract CGST and SGST.

Where a supply of services takes place in the course of Inter-State trade or commerce, it would attract IGST.

Cost of providing services would go up.

5

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

IGST VS.CGST+SGST Where the location of a supplier and the place of supply are in

different States, or in two different Union Territories or a State and a Union Territory, IGST is applicable.

Where the location of the supplier and the place of supply are in the same State, CGST and SGST would be applicable. Where services are imported into the territory of India, IGST is applicable.

Supply of Goods or Services or both to or by a SEZ developer or unit is treated as inter-State supply.

Place of supply would be determined as per the provisions of the IGST Act.

6

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

What is an Export of Service There must be a supply of service. Supplier of service is located in India. Recipient of service is located outside India. Place of supply of service is outside India. Payment for services is received in convertible foreign

exchange. Parties are not mere branches or offices of one another.

7

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Location of Supplier of Services

PARTICULARS LOCATION OF RECIPIENTWhere supply is received at a place of business for which registration has been obtained.

Location of such place of business.

Where supply is received at a place otherthan the place of business for whichregistration has been obtained (a fixed

establishment elsewhere)

Location of such fixed establishment

Where supply is received at more than oneestablishment, whether the place of businessor fixed establishment.

Location of the establishment most directly concerned with the provision of the supply

In the absence of such places Usual place of residence of the supplier

8

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Location of Recipient of Services

PARTICULARS LOCATION OF RECIPIENTWhere supply is received at a place of business for which registration has been obtained.

Location of such place of business.

Where supply is received at a place otherthan the place of business for whichregistration has been obtained (a fixed

establishment elsewhere)

Location of such fixed establishment

Where supply is received at more than oneestablishment, whether the place of businessor fixed establishment.

Location of the establishment most directly concerned with the receipt of the supply

In the absence of such places Usual place of residence of the recipient.

9

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Key TermsFixed Establishment means a place (other than the registered place of business) which is characterized by sufficient degree of permanence and suitable structure in terms of human and technical resources to supply services or to receive and use services for its own needs.

Place of business includes A place from where business is ordinarily carried on, and includes a

warehouse, a godown or any other place where a taxable person stores his goods, supplies or receives goods or services or both; or

A place where a taxable person maintains his books of account ;or A place where a taxable person is engaged in business through an

agent, by whatever name called. Usual place of residence means

In the case of an individual, the place where he ordinarily resides. In other cases, the place where the person is incorporated or

otherwise legally constituted. 10

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

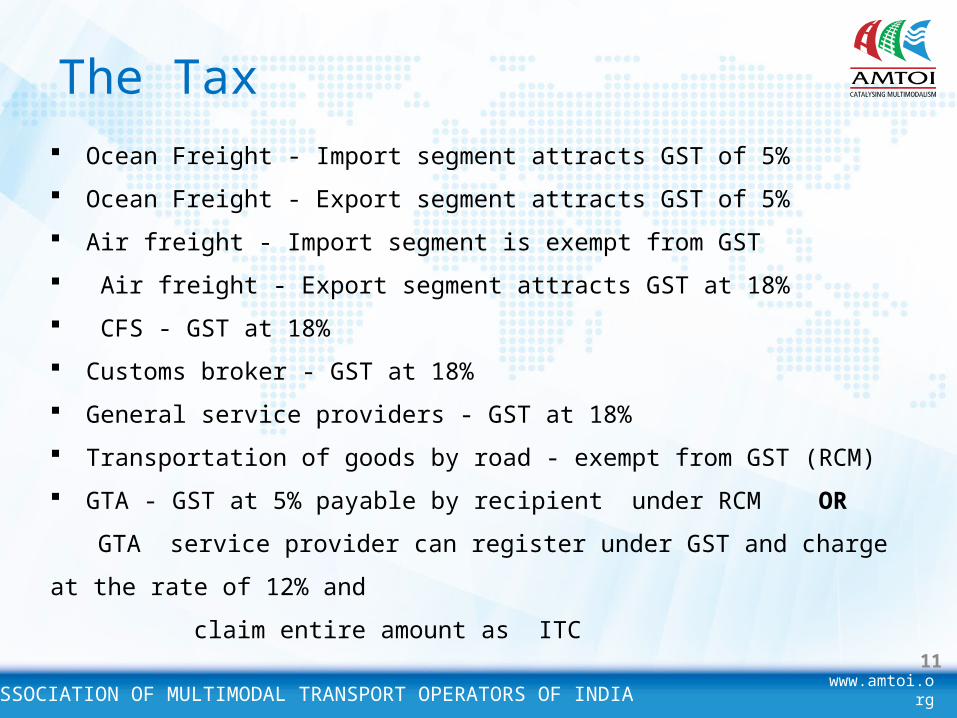

The Tax Ocean Freight - Import segment attracts GST of 5% Ocean Freight - Export segment attracts GST of 5% Air freight - Import segment is exempt from GST Air freight - Export segment attracts GST at 18% CFS - GST at 18% Customs broker - GST at 18% General service providers - GST at 18% Transportation of goods by road - exempt from GST (RCM) GTA - GST at 5% payable by recipient under RCM OR

GTA service provider can register under GST and charge at the rate of 12% and claim entire amount as ITC

11

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Returns – Changes in Due Dates

GSTR-1 for the month of July 2017 has to be filed between 1st and 5th September 2017

GSTR-2 for the month of July 2017 has to be filed between 6th and 10th September 2017.

GSTR-1 for the month of August 2017 has to be filed between 16th and 20th September 2017

GSTR-2 for the month of July 2017 has to be filed between 21st and 25th September 2017.

GSTR-3B which is supposed to be a summary of outward and inward supplies for the month of July 2017 should be submitted by 20th August 2017

GSTR-3B which is supposed to be a summary of outward and inward supplies for the month of August 2017 should be submitted by 20th September 2017. 12

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

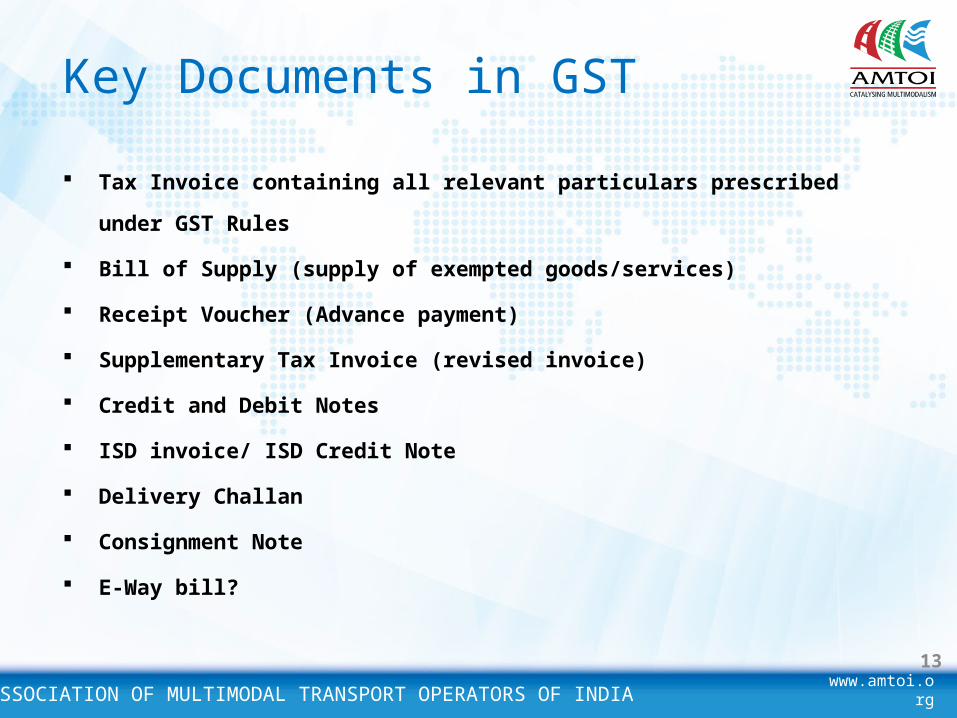

Key Documents in GST Tax Invoice containing all relevant particulars prescribed under

GST Rules Bill of Supply (supply of exempted goods/services) Receipt Voucher (Advance payment) Supplementary Tax Invoice (revised invoice) Credit and Debit Notes ISD invoice/ ISD Credit Note Delivery Challan Consignment Note E-Way bill?

13

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Other Issues – New ConceptsTax even on advances for supply of goods and input tax credit. Technology based environment. Reverse charge mechanism. Supply of goods or services by unregistered person to registered

person. Reimbursement Rate of tax IGST on imports Valuation in respect of related party transactions. GST on inter-unit billing and valuation. TDS if notified.

14

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

GST on Export FreightIn India logistics cost is much higher than developed countries as a ratio of GDP and GST will only further blunt our competitive edge globally. (In developed countries logistics cost is around 5% – 8% while in India it is about 13%). Internationally there is no levy of VAT or GST on international transportation of goods by air or sea or land or on freight forwarding or on related services.

Conclusion: International Transport of Goods should not be taxed at all

15

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Interplay of Section 12 &13 of IGST Act, 2017• When an Indian Company engages an Indian freight forwarder For

third Country transport (Eg Singapore to London) by virtue of Section 12, this transaction becomes liable to GST.

• When the same Indian Co engages a foreign freight forwarder Section 13(9) of the IGST Act comes in to the play and no GST is applicable. This tilts the advantage in favor of foreign freight forwarders

Conclusion: Such transactions involving international Transport of Goods should not be taxed at all.

16

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Interplay of Section 12 & 13 of the IGST Act, 2017 (Contd…)When an Overseas Company engages an Indian freight forwarder to move import goods (Eg. Singapore to India on CIF basis). Since the goods are shipped on CIF basis, by virtue of Section 13 (9), such transactions of international transport of goods into India becomes liable to GST. However the Overseas Company is not faced with any incidence of tax on the same transaction when he chooses to work with a foreign freight forwarder. The Indian freight forwarder loses his competitive edge when he is competing against foreign freight forwarders for transactions involving imports into IndiaFurther in the same transaction mentioned above, tax is charged on tax and repeatedly three times which unfortunately the Indian Importer has to pay Result;1. There is loss of business to Indian freight forwarders;2. There is no parity since a foreign freight forwarder is in a better position in

the GST regime.3. Loss of business in India would also mean loss of direct tax payments since

the income is no longer earned in India when contracts are given to foreign freight forwarders. Loss of employment opportunities since logistics is highly labour oriented 17

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Our Recommendations 1. In the service tax regime, freight forwarding was not taxed and

where a consolidated amount was charged for the entire transaction under a single contract, where the freight forwarder acts on his own account, the same was considered as bundled and not taxable.

2. International transportation of goods by road, rail, inland waterways, sea, air or any other mode including freight forwarding should be zero rated or the entire chain of activity must be exempted.

3. Ancillary services in relation to international transportation of goods like Customs clearances, warehousing, storage, cargo handling, packing, unitization, port, airport, terminal, etc. should be zero rated or exempted.

4. All services related to logistics carried out overseas, which are otherwise taxed in those countries must be zero rated, irrespective of the location of the customer.

Conclusion: Our request is to eliminate such anomalies and disparities and the International Transport of Goods should not be taxed.

18

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Specific Category for Multimodal Transport(Mixed Supply Vs Composite Supply)

Our recommendation is for tax exemption of international transport and allied services pertaining to international transport.

Multimodal Transport by nature of business in an inclusive business module and there by natural course of business it’s comprehensive. On page no 68 of service tax guidance book ‘Taxation of service : An Education Guide, June 20,2012’, which describes the same activities as bundled services and which were exempt or zero rated.

Conclusion: We should be Governed by INCO terms and all services covered for Delivery of the Goods as per INCO terms should be categorized as Composite services and should not be taxed at all.

19

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Invoices Raised by Service Providers

Principal to Principal Transition : At the same time, we have no of cases where, the service provider refuses to raise the invoices in the name of the actual receiver of the services. In all such cases, there is a loss of credit. This is resulting in an increase in the transition cost. For example, companies such as ONGC and IOCL ask the EPC Company to manage all their procurement, which includes delivering of goods to their site. Bill of ladings will always be in the name of the Importer. Shipping companies refuse to raise the invoice in the name of EPC Company or in the name of the forwarder or the customs broker. In all such cases, there is a loss of credit as companies like ONGC and IOCL is only concerned with the final invoice of the EPC Company

20

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

Invoices Raised by Service Providers (Contd…)

Pure Agent Transition: Though the government has issued clarification on the concept of pure agent transition, there are no of organization who do not issue the invoice in the name of the actual service receiver. They refuse to raise the GST invoice on the actual receiver of the services. In such a case, the logistics company is unable to act as a pure agent. Companies such as ports, airports and CFS to name a few refuse to raise invoices on the name of the importer and exporter.

Conclusion: Our recommendation is the person who is making the payment must have the option to decide on the actual receiver of the services

21

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

GTA Service ProviderGTA provides the service of road transport and also provide other services which are other than road transportation. In the course of business GTA may pay GST on the following cases;

1. Payment of GST towards purchase of transport vehicles.2. Payment of GST towards services taken in course of transport of

goods.3. GST paid as RCM towards services taken in course of transport of

goods.4. Payment of GST towards purchase of equipment used for services

other than transport.5. Payment of GST towards services taken in course handling

business of other verticals.6. GST paid as RCM towards services taken in course handling

business of other verticals.7. GST paid for indirect expenses such as Audit fees, Insurance

(building, staff), etc Which of the cases can the company rendering GTA services and other services consider for ITC ? As per latest circular we can charge 12% GST and claim ITC, but will the service receivers agree??

22

www.amtoi.orgASSOCIATION OF MULTIMODAL TRANSPORT OPERATORS OF INDIA

23

THANK YOU !!!