ppg update · fy2019 target / initiative sales growth 3-5% in constant currencies adjusted eps...

TRANSCRIPT

PPG UpdateMay 21, 2019

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements made by or on behalf of the Company. This presentation contains

forward-looking statements that reflect the Company’s current views with respect to future events and financial performance. You can identify forward-looking statements by

the fact that they do not relate strictly to current or historic facts. Forward-looking statements are identified by the use of the words “aim,” “believe,” “expect,” “anticipate,”

“intend,” “estimate,” “project,” “outlook,” “forecast” and other expressions that indicate future events and trends. Any forward-looking statement speaks only as of the date on

which such statement is made, and the Company undertakes no obligation to update any forward looking statement, whether as a result of new information, future events or

otherwise. You are advised, however, to consult any further disclosures we make on related subjects in our reports to the Securities and Exchange Commission. Also, note

the following cautionary statements:

Many factors could cause actual results to differ materially from the Company’s forward-looking statements. Such factors include global economic conditions, increasing price

and product competition by foreign and domestic competitors, fluctuations in cost and availability of raw materials, the ability to achieve selling price increases, the ability to

recover margins, the ability to maintain favorable supplier relationships and arrangements, the timing of and the realization of anticipated cost savings from restructuring

initiatives, difficulties in integrating acquired businesses and achieving expected synergies therefrom, economic and political conditions in international markets, the ability to

penetrate existing, developing and emerging foreign and domestic markets, foreign exchange rates and fluctuations in such rates, fluctuations in tax rates, the impact of

future legislation, the impact of environmental regulations, unexpected business disruptions, the effectiveness of our internal control over financial reporting, the

unpredictability of existing and possible future litigation, including asbestos litigation, and governmental investigations. However, it is not possible to predict or identify all such

factors. Consequently, while the list of factors presented here and under Item 1A of PPG’s 2018 Form 10-K is considered representative, no such list should be considered to

be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward-looking statements.

Consequences of material differences in the results compared with those anticipated in the forward-looking statements could include, among other things, lower sales or

earnings, business disruption, operational problems, financial loss, legal liability to third parties, other factors set forth in Item 1A of PPG’s 2018 Form 10-K and similar risks,

any of which could have a material adverse effect on the Company’s consolidated financial condition, results of operations or liquidity.

All of this information speaks only as of May 21, 2019, and any distribution of this presentation after that date is not intended and will not be construed as updating or

confirming such information. PPG undertakes no obligation to update any forward-looking statement, except as otherwise required by applicable law.

For purposes of the analyses described in this presentation, PPG’s architectural coatings businesses refers to PPG’s architectural coatings Americas and Asia Pacific and

architectural coatings EMEA strategic business units, which are included in PPG’s Performance Coatings reportable segment. PPG’s industrial coatings businesses refer to

all of PPG’s other (non-architectural) strategic business units, which make up the remainder of the Performance Coatings reportable segment and the Industrial Coatings

reportable segment.”

Forward-looking statements and other notes

2

FY2019 Target / Initiative

Sales Growth 3-5% in constant currencies

Adjusted EPS Growth 7-10% excluding currency translation impacts, including improvement toward pre-inflationary operating margins

Cost Savings $70 million from cost savings programs

Incentive

CompensationMaintain 10% EPS growth as the earnings-related metric for management variable long-term incentive compensation

Capital Return Increase annual dividend (on a per share basis)

Governance Engaged proxy solicitor and undertook extensive efforts to eliminate classified board and remove supermajority voting

Portfolio Review Strategic and operational review of the business and implications for shareholder value creation

Reiterating our 2019 targets and initiatives

In addition PPG enhanced its Board with the addition of two highly-qualified independent directors

3

PPG actions taken to optimize portfolio and improve operations

PPG continues to evolve its portfolio and strengthen operations to deliver shareholder value

2016 2017 201820152014 2019

Acquisitions:

Q3 2014: Homax, Masterwork

Q4 2014: Comex, Westmoreland Supply

Q2 2015: REVOCOAT

Q3 2015: Majority interest in LJF, Cuming Microwave and IVC

Q4 2015: Remaining interest in Chemfil Canada

Q3 2016: MetoKote

Q4 2016: Remaining interest in PPG Univer

Q1 2017: Deutek, Futian

Q3 2017: Crown

Q1 2018: ProCoatings

Q4 2018: SEM Products, Inc.

Q1 2019: Whitford Worldwide

Q2 2019: Hemmelrath

Q4 2016: Target of $125MM in annual savings

Q2 2018: Target of $85MM in annual savings

Q2 2019: Expected target ~$125MM in annual savings

Q2 2016: 40% stake in Pittsburgh Glass Works

Q4 2016: European fiber glass business, NA flat glass manufacturing and glass coatings operations; and 50% stake in PFG Fiber Glass JVs

Q2 2017: Mexican plasterboard & cement-board business

Q3 2017: US fiber glass business

Q1 2018: Packaging deco ink business

Global Cost

Savings Initiatives:

Divestitures:

4

1. Robust evaluation of portfolio and balance sheet opportunities conducted by independent financial

advisors

• Morgan Stanley and Goldman Sachs separately analyzed potential separation transactions and capital allocation

alternatives

2. Separate review of US / Canada architectural coatings conducted by globally-recognized independent

consulting firm

• Assessed opportunities to recover earnings related to 2018 customer assortment changes

3. Comprehensive internal operational and organizational analysis

• Deep dive review of competitiveness and profitability across regions, businesses and products

Comprehensive evaluation of PPG value creation opportunities

Focus on creating the most value for our shareholders – “nothing is sacred”

1

2

3

5

Independent third party reviews in parallel with comprehensive internal assessment – under direction of

PPG’s Board of Directors

Portfolio Evaluation: Scope and key considerations

Scope of Independent Reviews Key Considerations

• Alternatives to separate architectural and

industrial coatings businesses

• Other broad-ranging portfolio and strategic

options

• Balance sheet and related cash deployment

value creation opportunities

• Value maximization for PPG shareholders

• Equity market valuation estimates under

various scenarios

• Implications on business competitiveness,

customers and future growth potential

• Value of synergies or dis-synergies and other

financial impacts resulting from portfolio

adjustments

• Tax implications, if any, of various potential

transactions

• Balance sheet effects, liability assignment

and cash deployment considerations

In depth independent reviews of portfolio and value creation opportunities

1

6

1

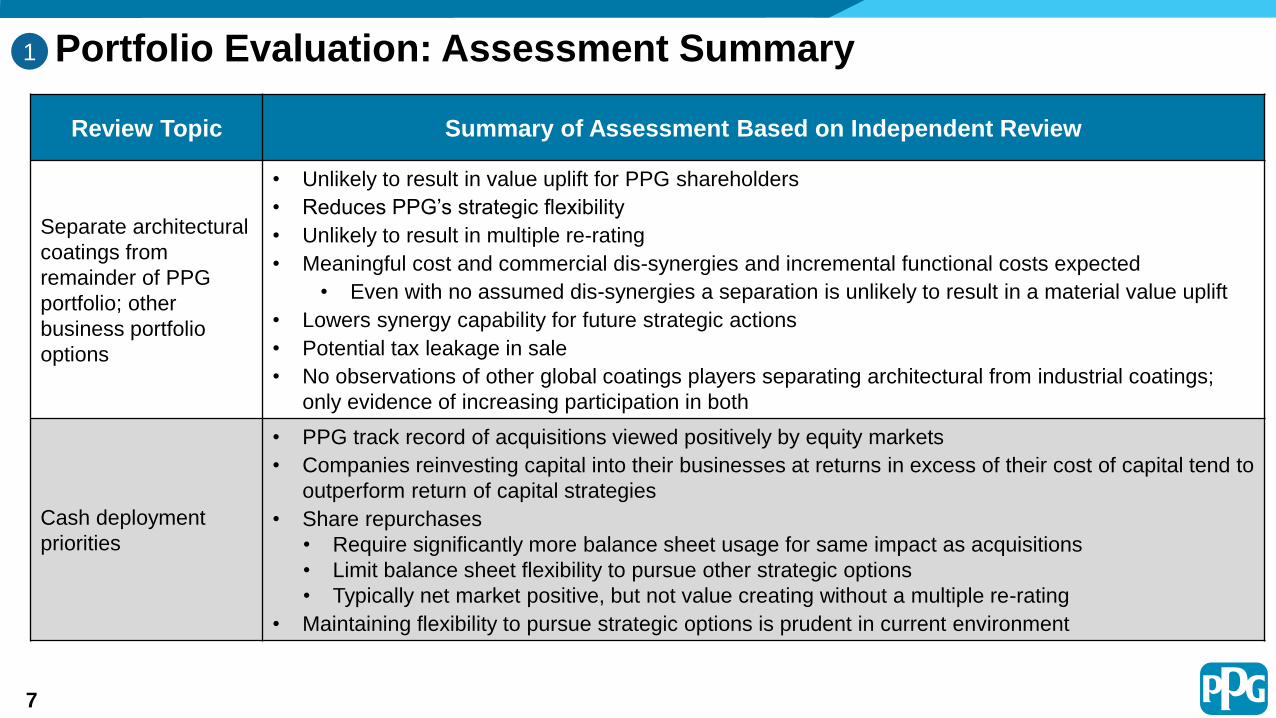

Review Topic Summary of Assessment Based on Independent Review

Separate architectural

coatings from

remainder of PPG

portfolio; other

business portfolio

options

• Unlikely to result in value uplift for PPG shareholders

• Reduces PPG’s strategic flexibility

• Unlikely to result in multiple re-rating

• Meaningful cost and commercial dis-synergies and incremental functional costs expected

• Even with no assumed dis-synergies a separation is unlikely to result in a material value uplift

• Lowers synergy capability for future strategic actions

• Potential tax leakage in sale

• No observations of other global coatings players separating architectural from industrial coatings;

only evidence of increasing participation in both

Cash deployment

priorities

• PPG track record of acquisitions viewed positively by equity markets

• Companies reinvesting capital into their businesses at returns in excess of their cost of capital tend to

outperform return of capital strategies

• Share repurchases

• Require significantly more balance sheet usage for same impact as acquisitions

• Limit balance sheet flexibility to pursue other strategic options

• Typically net market positive, but not value creating without a multiple re-rating

• Maintaining flexibility to pursue strategic options is prudent in current environment

Portfolio Evaluation: Assessment Summary

7

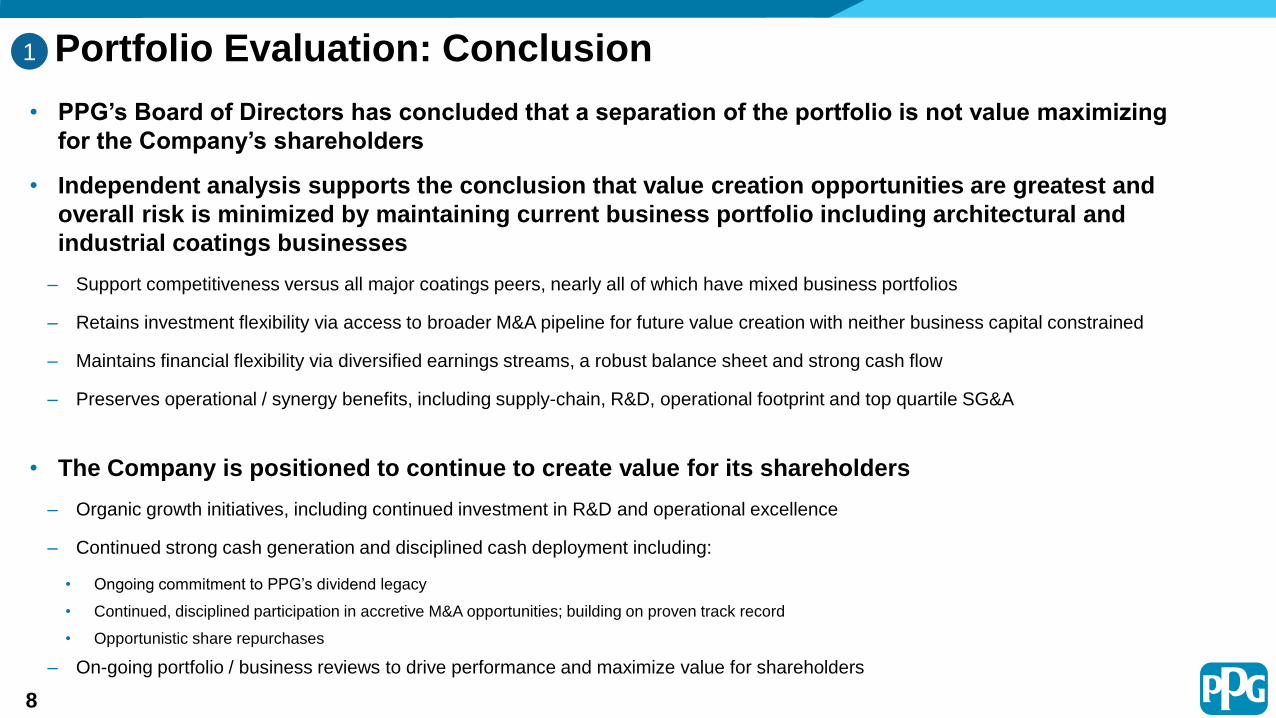

Portfolio Evaluation: Conclusion

• PPG’s Board of Directors has concluded that a separation of the portfolio is not value maximizing

for the Company’s shareholders

• Independent analysis supports the conclusion that value creation opportunities are greatest and

overall risk is minimized by maintaining current business portfolio including architectural and

industrial coatings businesses

‒ Support competitiveness versus all major coatings peers, nearly all of which have mixed business portfolios

‒ Retains investment flexibility via access to broader M&A pipeline for future value creation with neither business capital constrained

‒ Maintains financial flexibility via diversified earnings streams, a robust balance sheet and strong cash flow

‒ Preserves operational / synergy benefits, including supply-chain, R&D, operational footprint and top quartile SG&A

• The Company is positioned to continue to create value for its shareholders

‒ Organic growth initiatives, including continued investment in R&D and operational excellence

‒ Continued strong cash generation and disciplined cash deployment including:

• Ongoing commitment to PPG’s dividend legacy

• Continued, disciplined participation in accretive M&A opportunities; building on proven track record

• Opportunistic share repurchases

‒ On-going portfolio / business reviews to drive performance and maximize value for shareholders

1

8

Globally-recognized independent consulting firm’s assessment of operations and growth investments

for the U.S. and Canada architectural coatings business

Operational Review: Scope and outcomes2

Scope

• Thoroughly review overall operations,

commercial approaches and growth-focused

investments/spending

• Review commercial strategies by various

retail channels

• Assist in detailed action planning and

execution implementation to return business

to prior absolute earnings level (pre-customer

assortment changes)

Key Outcomes

• Established key milestones and project

management office to facilitate prioritization and

implementation of earnings improvement

initiatives

• Successful execution of previously announced

restructuring (4 plants and other support costs)

• Longer-term operational excellence guidance

and monitoring tools, including salesforce

effectiveness, retail network optimization and

growth investment return maximization

• Recommendation on specific commercial retail

strategies, including digital and e-commerce

Focus on delivering rapid earnings recovery, ongoing operational excellence and future channel strategies

9

Comprehensive internal operational and organizational assessment to identify opportunities to improve

profitability, cash flow, productivity and growth across PPG

Internal PPG Assessment: Scope and action plans

Targeting full year run rate savings of ~$125MM

3

Scope

• Detailed review of cash flow, profitability and

growth trends/trajectory by sub-region for all

PPG business units and product categories

• Benchmarking of operational, supply chain

and functional costs across PPG businesses

and regions to identify and leverage “best-in-

class” practices

• Analysis of near-term synergy opportunities

from recent acquisitions

• All of the above vetted against current and

future external end-use market macro-

economic expectations

Key Actions

• Exit certain low-profit or unprofitable product

lines or geographies with small market positions

• Further consolidate low growth regional

manufacturing / supply chain footprint

• Reorganize business cost structures to reflect

current economic climate

• Maximize synergy capture from recent

acquisitions, taking best in class practices from

both legacy PPG and acquired businesses

10

• Maintain current business portfolio

‒ Provides greatest opportunity for shareholder value creation

‒ Focused accretive cash deployment; prioritize acquisitions

‒ Continued management accountability for delivering results

• Rapidly return U.S. & Canada architectural coatings

business to prior earnings level

‒ Mid-2019 goal of absolute earnings neutrality

‒ Position business for future success

operationally and commercially

• Operational excellence across all of PPG

‒ Execute on cost savings and business optimization action plans

‒ Reinforce PPG’s historic operational focus and maintain

industry-leading cost structure

Conclusion

11

Appendix

~45% ~35%

~50% ~40%

~80%

~15%

~30%

~55% ~65%

~50% ~60%

~20%

~100%

~85%

~70%

Momentum towards combining architectural and industrial coatings

continues across the industry

~40% ~40% ~40%

~70%

~50%

~25%

~60% ~60% ~60%

~30%

~100%

~50%

~75%

Architectural Coatings Industrial Coatings

Industry

20172013

Industry

13

Major / Recent Acquisitions

Source: Morgan Stanley Global Chemicals Investor Guide, company investor presentations

1. Pro forma for acquisition of DuluxGroup and Betek

2

Legend:

Recent coatings transactions continue to highlight the value of a

combined business portfolio

Acquirer Target Date

June

2018

December

2016

October

2016

March

2016

Announced Rationale

"The strong sales and distribution capabilities of Fabryo will help us to further improve

our business in the region, leveraging our combined resources and expertise, and

strengthen our position as the leading paints and coatings company in Europe" – Ruud

Joosten (COO AkzoNobel)

"[Nippon Paint Holdings] wanted to expand our architectural paints in the U.S. and have

been searching for the right partner" – Tetsushi Tado (CEO Nippon Paint)

"The acquisition will increase Kansai Paint’s footprint in the mid-range decorative coatings

segment, and widen our dealer network particularly in the northern region" – Yoshikazu

Takahashi (Asia Pacific CEO Kansai Paint)

"The combination expands our brand portfolio and customer relationships in North

America, significantly strengthens our Global Finishes business, and extends our

capabilities into new geographies and applications, including a scale platform to grow in

Asia-Pacific and EMEA" – John Morikis (CEO Sherwin-Williams)

Target

Focus

Architectural

Architectural

Architectural

Industrial

+

Architectural

14

Architectural Pending

“The combination of DuluxGroup and Nippon will provide further avenues for growth for

DuluxGroup and create exciting opportunities for all of the DuluxGroup management and

employees. Nippon intends to maintain the legacy developed by DuluxGroup and facilitate

DuluxGroup’s existing vision.” – Tetsushi Tado (Nippon president / CEO)

Architectural Pending

“Nippon Paint, by acquiring Betek Boya, will achieve a No.1 market share in Turkey in

addition to Asia, where the company has long had a strong presence in, and the Pacific

region, where a separate acquisition was recently announced… expect generation of revenue

and cost synergies” – Nippon Press Release 4/26/2019

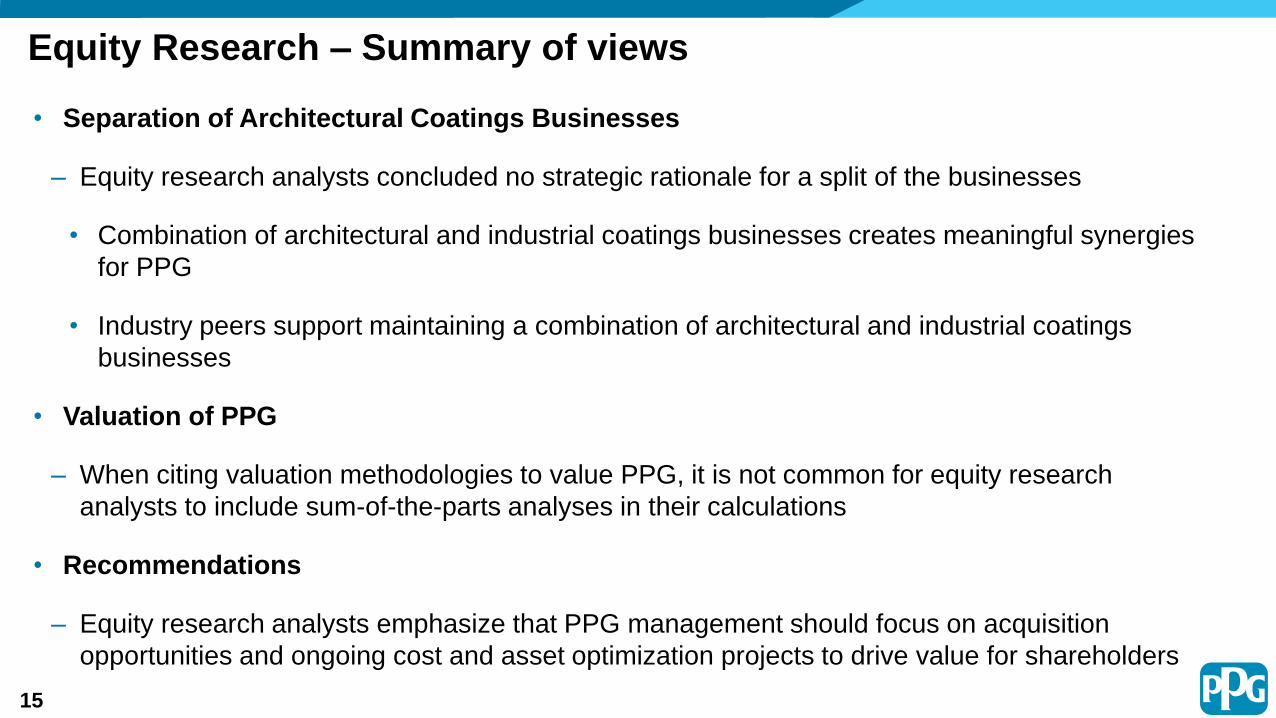

• Separation of Architectural Coatings Businesses

‒ Equity research analysts concluded no strategic rationale for a split of the businesses

• Combination of architectural and industrial coatings businesses creates meaningful synergies

for PPG

• Industry peers support maintaining a combination of architectural and industrial coatings

businesses

• Valuation of PPG

‒ When citing valuation methodologies to value PPG, it is not common for equity research

analysts to include sum-of-the-parts analyses in their calculations

• Recommendations

‒ Equity research analysts emphasize that PPG management should focus on acquisition

opportunities and ongoing cost and asset optimization projects to drive value for shareholders

Equity Research – Summary of views

15

Architectural and industrial coatings provide shareholder value

creation opportunities

Source: PPG estimates, Exane BNP Paribas Research (10/2/18), Sherwin/VAL investor presentation, Company transcripts

Distribution, Packaging, and

Manufacturing

Chemical Raw Materials

(Additives, Solvents & Pigments,

Resins and Latex, Titanium Dioxide)

Distribution, Packaging, and

Manufacturing

Chemical Raw Materials

(Additives, Solvents & Pigments,

Resins and Latex, Titanium Dioxide)

Average

Architectural Coatings

Average

Industrial Coatings

Industry estimates – figures vary greatly by end-use and application

16

Similar raw materials lead to synergy opportunitiesTypical coatings acquisition synergy and efficiencies

Category Value Creation

Raw material and other supply-chain Meaningful to Significant

Research & development Meaningful

Cost structure and back-office Modest to Meaningful

Manufacturing, logistics and other operations Modest

Incremental revenue None to Modest

Active and broad M&A strategy has enhanced PPG’s portfolio

17

Hemmelrath Industrial Addition of formulating and manufacturing solutions

SEM Products Industrial Expand auto refinish offerings

Whitford Industrial Expand into low-friction coatings

Crown Industrial Expand coatings service business

Cuming

MicrowaveIndustrial Expand aerospace technology capabilities

Futian China Industrial Gain scale in China refinish; mid-tier product line

IVC Industrial Expand powder technology / South China footprint

LJF Industrial Expand aerospace sealant adjacency

MetoKote Industrial Establish coatings service business

Revocoat Industrial Expand automotive adhesive adjacency

Spraylat Industrial Expanded liquid technologies; powder footprint

AkzoNobel NA Architectural Grow scale in U.S.

Comex Architectural Leading architectural position in Mexico

ProCoatings Architectural Additional architectural scale in Netherlands

Univar Italy Architectural Gain scale in architectural Italy

Target Details Technology Geography Scale AdjacencyType

PPG M&A has created significant shareholder value

1. ROCs post-completion unavailable due to recent timing of transaction2. ROCs are representative of the acquisition project; not overall company

Acq 10Acq 9Acq 8Acq 7Acq 6Acq 5Acq 4Acq 3Acq 2Acq 1

Estimated ROC Pre-Completion Increase in ROC Post-Completion

WACC

Average Post-Completion ROC

11

Acquisitions since 2014 have averaged ~2x PPG WACC

18

Industry leading 2018 adjusted return on capital*

19

~15%

~13% ~12%

~8%

~5%

Measurable proof of PPG’s successful, disciplined and value creating M&A

1. *Adjusted ROC excluding nonrecurring items (see reconciliation at end of presentation)

PPG has maintained balanced cash deployment

Source: Company filingsNote: €1bn Special Dividend from sale of Specialty Chemicals in 2017 removed from AkzoNobel Capital Deployment; USD/EUR = $1.24

Share Repurchases Dividends Capex Acquisitions

Cash Deployment: 2014 – 2018

$12.8bn $14.5bn $2.4bn $1.8bn $6.0bn Total Capital

Deployed

Acquisitions

Capex

Dividends

Share

Repurchases

20

PPG aggressively manages cost structure

SG&A as % of sales

21

Corporate cost as % of sales Recent PPG cost savings programs

Date Focus Target

Savings

Status

Q4,

2016

Reduce Europe operational footprint,

marine coatings business unit cost

structure, acquisition synergy capture

$125

million

Nearly

complete

Q2,

2018

Adjust cost structure following U.S.

architectural customer assortment changes

$85 million Underway

Q2,

2019

Continue to optimize global cost structure ~$125

million

Scope

Being

finalized

Adjusted EBITDA margin of sales (FY18)

19%

16% 16%

13%11%

Source: Annual company filings

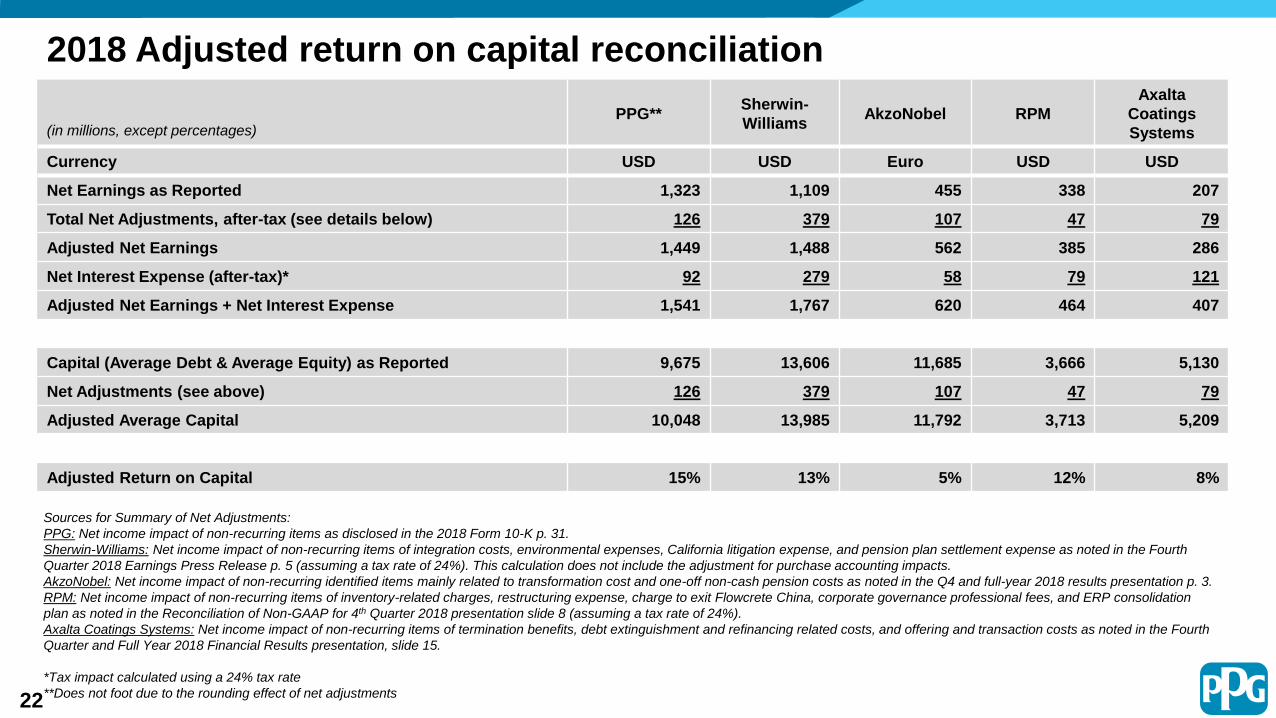

Source: Annual company filings See detailed reconciliation on following slides

(in millions, except percentages)PPG**

Sherwin-

WilliamsAkzoNobel RPM

Axalta

Coatings

Systems

Currency USD USD Euro USD USD

Net Earnings as Reported 1,323 1,109 455 338 207

Total Net Adjustments, after-tax (see details below) 126 379 107 47 79

Adjusted Net Earnings 1,449 1,488 562 385 286

Net Interest Expense (after-tax)* 92 279 58 79 121

Adjusted Net Earnings + Net Interest Expense 1,541 1,767 620 464 407

Capital (Average Debt & Average Equity) as Reported 9,675 13,606 11,685 3,666 5,130

Net Adjustments (see above) 126 379 107 47 79

Adjusted Average Capital 10,048 13,985 11,792 3,713 5,209

Adjusted Return on Capital 15% 13% 5% 12% 8%

2018 Adjusted return on capital reconciliation

22

Sources for Summary of Net Adjustments:

PPG: Net income impact of non-recurring items as disclosed in the 2018 Form 10-K p. 31.

Sherwin-Williams: Net income impact of non-recurring items of integration costs, environmental expenses, California litigation expense, and pension plan settlement expense as noted in the Fourth

Quarter 2018 Earnings Press Release p. 5 (assuming a tax rate of 24%). This calculation does not include the adjustment for purchase accounting impacts.

AkzoNobel: Net income impact of non-recurring identified items mainly related to transformation cost and one-off non-cash pension costs as noted in the Q4 and full-year 2018 results presentation p. 3.

RPM: Net income impact of non-recurring items of inventory-related charges, restructuring expense, charge to exit Flowcrete China, corporate governance professional fees, and ERP consolidation

plan as noted in the Reconciliation of Non-GAAP for 4th Quarter 2018 presentation slide 8 (assuming a tax rate of 24%).

Axalta Coatings Systems: Net income impact of non-recurring items of termination benefits, debt extinguishment and refinancing related costs, and offering and transaction costs as noted in the Fourth

Quarter and Full Year 2018 Financial Results presentation, slide 15.

*Tax impact calculated using a 24% tax rate

**Does not foot due to the rounding effect of net adjustments

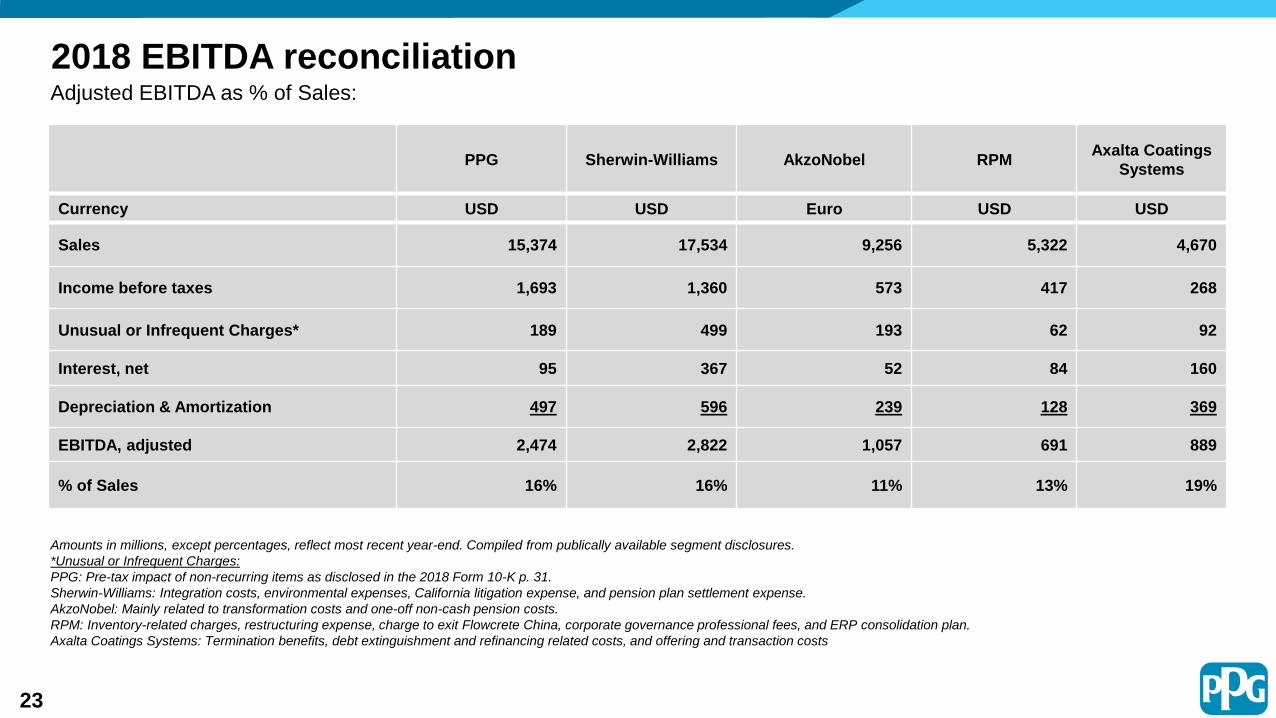

PPG Sherwin-Williams AkzoNobel RPMAxalta Coatings

Systems

Currency USD USD Euro USD USD

Sales 15,374 17,534 9,256 5,322 4,670

Income before taxes 1,693 1,360 573 417 268

Unusual or Infrequent Charges* 189 499 193 62 92

Interest, net 95 367 52 84 160

Depreciation & Amortization 497 596 239 128 369

EBITDA, adjusted 2,474 2,822 1,057 691 889

% of Sales 16% 16% 11% 13% 19%

Adjusted EBITDA as % of Sales:

2018 EBITDA reconciliation

23

Amounts in millions, except percentages, reflect most recent year-end. Compiled from publically available segment disclosures.

*Unusual or Infrequent Charges:

PPG: Pre-tax impact of non-recurring items as disclosed in the 2018 Form 10-K p. 31.

Sherwin-Williams: Integration costs, environmental expenses, California litigation expense, and pension plan settlement expense.

AkzoNobel: Mainly related to transformation costs and one-off non-cash pension costs.

RPM: Inventory-related charges, restructuring expense, charge to exit Flowcrete China, corporate governance professional fees, and ERP consolidation plan.

Axalta Coatings Systems: Termination benefits, debt extinguishment and refinancing related costs, and offering and transaction costs