practitioners’ judgment and deferred tax dis- closure: a...

TRANSCRIPT

WU International Taxation Research Paper Series

No. 2014 - 07

Practitioners’ Judgment and Deferred Tax Dis-closure: A Case for Materiality

Eva Eberhartinger Nadia Genest Soojin Lee

Editors:

Eva Eberhartinger, Michael Lang, Rupert Sausgruber and Martin Zagler (Vienna University of Economics and Business), and Erich Kirchler (University of Vienna)

Correspondence Address: Eva Eberhartinger and Nadia Genest, WU Vienna University of Economics and Business Department of Finance, Accounting and Statistics, Tax Management Group, Welthandelsplatz 1, A – 1020 Vienna, Austria; Soojin Lee, Rietlandpark 301, 1019 DW Amsterdam, The NetherlandsE-mail: [email protected]; [email protected]; [email protected]

Practitioners’ Judgment and Deferred Tax Disclosure: A Case for

Materiality

Eva Eberhartinger*, Nadia Genest*, Soojin Lee**

* WU Vienna University of Economics and Business, Department of Finance, Accounting and

Statistics, Austria, ** International Bureau of Fiscal Documentation (IBFD), The Netherlands

The authors would like to thank Matthias Petutschnig, Caren Sureth-Sloane, two anonymous

reviewers of VHB Jahrestagung 2014, and the participants and discussants of the WU Accounting

Research Seminar, and of the EAA, AAA and CAAA annual congresses. Financial support from the

Austrian Science Fund (FWF): W 1235-G16 is gratefully acknowledged.

Practitioners’ Judgment and Deferred Tax Disclosure: A Case for Materiality

Abstract

Against the background of increasing tension between the need for additional

disclosure and an information overload in financial statements, this study investigates

the relevance of specific tax accounting information in an experimental setting.

Participants make judgments on the financial performance, investment attractiveness

and tax position of the firm, in absence or in presence of detailed tax information in the

other comprehensive income statement. Our results do not support the notion that such

deferred tax information has an effect on the judgment of experts, as long as the

amounts of deferred tax are normal. However, when the detailed amounts of deferred

tax are abnormally high, judgment differs significantly. Our result is important for

standard setters, as they may consider further developing guidance in standards (such

as IAS 1 and IAS 12) and in the Practice Statement for how to judge materiality of

information, in accordance with the materiality principle set forth in IAS 1.31. By

doing so, the risk of information overload can be reduced. Our study thus contributes to

the current debate on the extent of disclosure. Our results are novel and the method

used allows for the isolation of effects and the identification of causal relationships.

Keywords: deferred taxes; other comprehensive income; income tax disclosure;

information processing

2

Practitioners’ Judgment and Deferred Tax Disclosure: A Case for

Materiality

1. Introduction

One of the main purposes of financial statements is to provide information and insight into the

financial and economic state of a firm. Indeed, enhancing transparency is one of the drivers of

financial reporting. According to the principal-agent theory, additional disclosure will reduce

information asymmetry, lower transaction costs and thus decrease the cost of capital and enhance the

firm’s market value. Hence, disclosure requirements have increased considerably in recent years. As a

reaction to ever increasing disclosure requirements, complaints of an information overload have arisen,

claiming that too much disclosure may obscure true transparency (EFRAG, 2011; PwC, 2011; KPMG,

2011; ESSEC, 2013; Raedy, Seidman & Shackelford, 2011; Groves, 1994). Such complaints relate to

cognitive biases: amongst a multitude of information, where the difference between material and

immaterial items of information is blurred, information processing – by financial statement users, in

our case – is flawed (Schroder, Driver & Streufert, 1967; Agnew & Szykman, 2005). The tension

between more detailed disclosure in order to reduce information asymmetry, and less but material

disclosure in order to avoid an information overload, is reflected in accounting rules which demands

detailed disclosure only when the information is material.1

To better understand the effect of cognitive biases in relation to financial statement disclosure,

1 In December 2014 IAS 1.31 was amended to provide as follows: “Some IFRSs specify information that is required to be included in the financial statements, which include the notes. An entity need not provide a specific disclosure required by an IFRS if the information resulting from that disclosure is not material. This is the case even if the IFRS contains a list of specific requirements or describes them as minimum requirements. An entity shall also consider whether to provide additional disclosures when compliance with the specific requirements in IFRS is insufficient to enable users of financial statements to understand the impact of particular transactions, other events and conditions on the entity’s financial position and financial performance”.

3

we test the effect of disclosure on the judgment of financial statement users on the firm in an

experimental setting. Based on cognitive theory, we attempt to answer the questions as to whether

disclosure per se (as compared to non-disclosure), and whether the amounts which are disclosed

(abnormally high as compared to normal), have an effect on users’ judgment of the economic state of

the firm. We find that users’ judgment is affected only in those cases where amounts are abnormally

high.

We use the example of tax information in other comprehensive income (OCI). To test the

effect of disclosure of tax information on separate OCI line items, we use an experimental setting

which allows us to ceteris paribus manipulate tax information only and identify causal relation

between such information and users’ judgment. We present the participants (172 accounting experts,

mostly practitioners) of the different treatment groups with anonymized financial statements of a

listed multinational corporation (MNC). The financial statements in each treatment group varies with

respect to the detailed tax information presented on the OCI. The tax information is either not

available (all figures are presented on a net-of-tax-basis, after deduction of the normal amount of

deferred tax: Group A receives Case A “Net-of-Tax”), or separately disclosed for each line item

(Group B receives Case B “Tax detail”), or abnormally high amounts of tax information is separately

disclosed for each line item (Group C receives Case C “Tax detail x3”2). In each of the treatment

groups, participants make judgments on the financial performance, investment attractiveness and tax

position of the firm based on the financial statement information they receive.

Our results show no significant difference in judgment between two treatments in a normal

setting (Case A “Net-of-Tax” versus Case B “Tax Detail”). However, we do observe a significant

difference in judgment for Case C (Case B “Tax Detail” versus Case C “Tax Detail x3”) where the

amounts of deferred tax information are abnormally high (tripled) while the OCI total remains

2 The pre-tax OCI line item is adapted accordingly, so that the net-of-tax OCI line item and the OCI total remain unchanged.

4

unchanged. Our results confirm that tax information in OCI has a significant impact on the judgment

of practitioners in the case of information which is perceived as abnormal, and which therefore

deviates from expectations.

The International Accounting Standard Board (IASB) is well aware of the importance of the

materiality principle. Its disclosure initiative (IASB, 2013d) results from a survey which points to the

concept of materiality as one major cause of the “disclosure problem”, i.e. too little relevant

information and too much irrelevant information (IASB, 2013a). Consequently, IAS 1 was amended

in 2014 to clarify that an entity is not required to disclose information which is immaterial to enabling

preparers’ use of judgment. The IASB is currently working on a Materiality Practice Statement

project, and on a Definition of Materiality project. Our research connects to the IASB’s focus on the

materiality principle and provides further insight on information processing by financial statement

users.

In this study, we specifically focus on the disclosure of deferred tax on items of OCI required

by IAS 12 Accounting for Income Taxes. The standard requires an entity to separately disclose

deferred taxes on OCI line items, either on the face of the OCI statement or in the notes. Deferred tax

in OCI is particularly well suited for our research question, as it reflects the tension between the need

for disclosure and the possible information overload. On the one hand, the recent public and political

debate has shown a particular concern for the tax position of multinationals. Calls for even more

disclosure on tax, for example public country-by-country reporting (OECD, 2015), indicate that tax

disclosure is considered highly relevant. On the other hand, the usefulness of OCI is in doubt, and

users seem to have little confidence in OCI statements (Black, 2016; Dhaliwal, Subramanyam and

Trezevant, 1999). The IASB takes the view that disclosing taxes on OCI line items would improve the

clarity and transparency of OCI: "Users of financial statements often requested further information on

tax amounts relating to components of other comprehensive income, because tax rates often differed

from those applied to profit or loss” (IAS 1, BC 68). However, there are opposing views asserting that

allocating taxes to each OCI component can be arbitrary and may involve a high degree of

5

subjectivity due to undefined tax rates (IAS 1, BC 67). Consequently, deferred tax information in OCI

is particularly useful for our analysis.

To our knowledge, this is the first paper that focuses on the cognitive limits of financial statement

disclosure in connection with the materiality principle. Existing studies rather explore the impact of

cognitive limits of financial statement disclosures in relation with the presentation format of

accounting information (e.g. Novak, 2016) or with decision quality (e.g. Iselin, 1988). Our paper

contributes to the stream of literature about information overload in accounting (Eppler & Mengis,

2004) by providing insights into how the concept of information overload interacts with the

materiality principle. Additionally, it contributes to the current debate on the extent of disclosure

(IASB, 2013d) and sheds light on the quantitative aspects of materiality.3 Thus, our result is important

for both preparers of financial statements and standards setters. Accordingly, our paper responds to a

call for research on the value relevance of tax information given in OCI (Black, 2016). Our results

further question the real impact from the IASB’s recent initiatives toward detailed tax disclosure, as

its effects can be unnoticeable in a real-life setting.

This paper proceeds as follows: section 2. studies the background in literature and presents

the hypothesis; section 3. presents the research design; section 4. analyses the results; section 5.

discusses the results and section 6. concludes.

2. Theory, Literature and Hypotheses

2.1. OCI and Tax Disclosure

According to the agency theory, additional disclosure will reduce information asymmetry, lower

transaction costs and thus decrease the cost of capital and enhance the firm’s market value (for

example Botosan & Plumlee, 2002). As such, most of the existing capital market studies show price

3 Thus, this study does not investigate the qualitative aspect of materiality.

6

relevance as well as return relevance of OCI and specific OCI items (Dhaliwal et al., 1999;

Goncharov & Hodgson, 2011; also Cahan, Courtenay, Gronewoller & Upton, 2000; Kanagaretnam,

Mathieu & Shehata, 2009; Biddle & Choi, 2006).

Literature on the relevance of tax disclosure assume that accounting information in general,

and tax disclosure specifically, is considered to be value relevant to equity investors (Barth, Beaver &

Landsman 2001). For instance, McAnally, McGuire and Weaver (2010) and Atwood, Cao, Drake and

Myers (2011) find future-oriented value relevance of tax information, which is highly utilized by

equity investors and reflects current earnings power. In this respect, Lev and Nissim (2004)

empirically test contemporary earnings impacts by showing a stronger association between the tax-to-

book income ratios with current earnings-price ratios. With a particular concern for deferred taxes,

empirical studies find a positive association of deferred tax accounts with firm value (Ayers, 1998)

and with the value of equity in terms of stock returns (Givoly & Hayn, 1992). Yet, a negative relation

between deferred taxes and common stock value is also documented (Chandra & Ro, 1997; Chaney &

Jeter, 1992). Although the directions of the correlations differ, past studies support the informative

attributes of deferred tax information, which is taken into account by investors through the market’s

perception of deferred tax assets and liabilities as real assets and liabilities (Chang, Herbohn &

Tutticci, 2009).

On the other hand, there is a stream of research severely doubting the value-relevance of tax

disclosure. For bond raters’ judgments, the studies of Huss and Zhao (1991) and Chattopadhyay,

Arcelus and Srinivasan (1997) investigate whether the existence of deferred taxes would influence the

corporate bond rating. Both studies show no difference in bond ratings resulting from different

treatment of deferred taxes. With respect to the detailed book-tax difference, Raedy et al. (2011) find

little evidence that equity market prices differ, and conclude that such detailed tax disclosures matter

less to the equity market. Such observations support the view that investors do not perceive deferred

taxes as decision-relevant information and are thus less likely to incorporate deferred taxes in

assessing the firm value (Chludek, 2011).

7

Equally significant, tax disclosure can also include misleading contents that undermine its

relevance. Overesch and Schreiber (2006) show that the relevance of tax information under IAS 12

depends on the respective type of tax planning a firm engages. Limits of effective tax rate disclosure

are also shown by Wilkie and Limberg (1993) and Dunbar and Sansing (2002), who suggest that

effective tax rate is not strongly related to a firm’s performance or tax preferences, and thus effective

tax rate is not able to explain a firm’s tax planning practices. Deficiency in financial reporting of

income taxes is also identified by Bauman, Bauman and Halsey (2001), who find that earnings

management effects of the deferred tax assets allowance cannot be determined solely from the

financial disclosure, and suggest that financial disclosures still need to improve.

In line with principal-agent theory and with the majority of the literature – which shows that

OCI, in itself, as well as disclosure on deferred tax is relevant to users, we propose the following

hypothesis.

H1: Information in OCI, which includes tax information, affects financial statement

users’ perception of the firm’s economic state.

2.2. Cognitive Biases

According to cognitive theory, limited attention stems from restricted capacity to process the

mass of information in the environment. Since cognitive capacity is limited, attention must be

selective and necessitates effort (Kahneman, 1973). Consequently, as generating conscious thoughts

such as judgments on a firm’s economic position requires a focus on particular ideas or memories at

the price of others, differential processing cost arises. Such process implies that some inputs are more

easily perceived than other. The prominence or the level of contrast with others in its context is what

makes a particular item of information more salient (Fiske & Taylor, 1991).

Some researchers suggest that the perception of such information depends on prior user’s

expectations (Hand, 1990; Schrand & Walther, 2000). For instance, large gap between expected

8

amounts and actual amounts in accounting makes information more prominent, which leads to easier

information processing for the user, and to more influence of such information on users’ judgment of

the economic state of the firm.

According to availability heuristic, the way in which attention is directed in conscious thought

is based on possibly recalling related examples (Tversky & Kahneman, 1973), which can lead to

biased thought or judgment. Therefore, when dealing with unfamiliar or complex information, users’

judgment is restricted by cognitive limitations (Hirst & Hopkins, 1998). The theory of bounded

rationality, as developed by Simon (1955; 1956), suggests that human cognition is also limited by

practical boundaries. Constraining factors such as time lead to a simplification of the human decision-

making process. Therefore, in a complex setting, human rationality is limited and does not necessarily

lead to optimal outcomes (Simon, 1991). As such, large amount of information can be viewed as a

complex setting. Accordingly, research from various disciplines show that the quality of decision of

an individual is positively correlated with the amount of information received only up to a certain

point (Agnew & Szykman, 2005; Schroder et al., 1967). Beyond this point, additional information

cannot be processed anymore, and information overload happens (O’Reilly, 1980), which blurs the

individual decision-making process (Schick et al., 1990).

In this regard, Chen, Danielson and Schoderbek (2003) find that the complexity and

unfamiliarity of the deferred tax adjustments disclosure leads to analysts’ misinterpretation of the one-

time items of deferred tax adjustments to tax rate changes. Similar findings are observed by Amir and

Sougiannis (1999), who document that analysts fail to fully capture the implications of tax carry-

forwards on future earnings, and analysts tend to be less precise and biased (i.e. more optimistic) in

forecasting earnings of firms with tax carry-forwards. Given the high complexity of book-tax

differences, Weber (2007) concludes that mispricing is the result of misinterpretation of predictable

future returns which are related to book-to-tax differences.

In summary, the findings from prior literature indicate that the relevance of tax information

9

and its usefulness are evaluated differently in different settings. Although the theoretical aim of

(value-) relevance of (deferred) taxes is set out by principle, its practical effects appear to be rather

mixed, as shown in the findings from prior empirical and behavioural studies. These findings indicate

that the contents of tax disclosure are not necessarily relevant to users. Some favourable views on tax-

relevance seem to be undermined by information overload that users have to deal with.

Based on theory and prior studies, we therefore propose the following hypotheses.

H2: Tax information in OCI affects financial statement users’ perception of the

firm’s economic state, if displayed on the face of the statement.

H3: Abnormal tax information in OCI affects financial statement users’ perception

of the firm’s economic state, if displayed on the face of the statement.

3. Research Design

3.1. Structure

We structure the experiment along the lines of Anandarajan, Belzile, Curatola and Viger (2008), who

use a similar approach to study whether the presentation format of stock-option reporting matters. Our

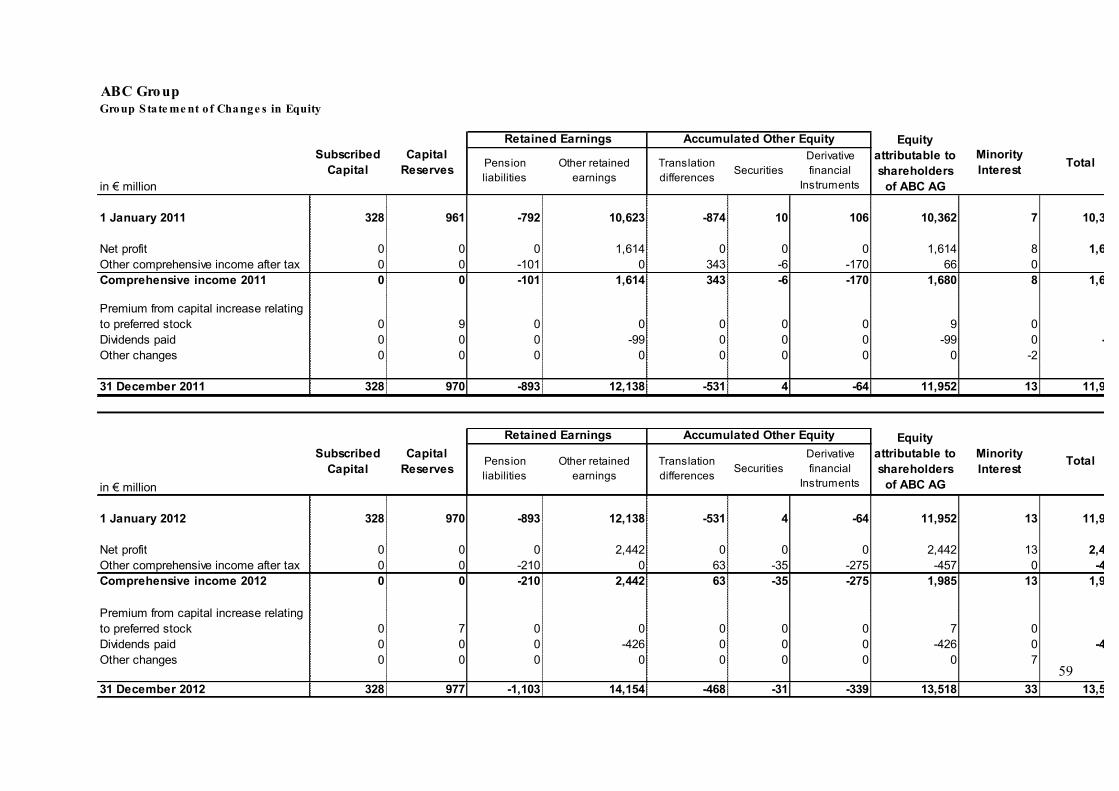

participants receive an identical set of financial statements, including balance sheet, comprehensive

income statement, cash flow statement and statement of changes in equity. The statement of other

comprehensive income is manipulated: three different groups receive different versions with regard to

the quality of the information on deferred tax. Through a questionnaire that includes a set of 7

questions in total, participants are asked to judge the economic state of the firm.

3.2. Participants

172 individuals participated in the experiment. The participants are a mix of practitioners and students.

10

Practitioners include experts in the field of accounting, auditing or tax. Approximately one third (36%)

of all participants are certified tax advisors4 and/or certified public accountants. Approximately two

thirds (63%) of all participants are employed by a tax consulting/audit firm at the time of the

experiment. Not all participants have International Financial Reporting Standards (IFRS) experience,

but all have a strong accounting background. Participants also include students in the Master Program

in Tax and Accounting at ### University. As previous education includes financial reporting and

international accounting, these participants have considerable knowledge and a good understanding of

the field. Almost half of the students (46 %) also work (at least) part-time in tax/accounting practice,

and usually seek a professional career in accounting, auditing or tax.

[Insert Table 1 about here]

Given the overlap between practitioners and students (some practitioners also study;

approximately half of the students also work in practice), and to further support the external validity

of the experiment, we form two categories of participants (see Table 2, discussed in section 3.4): 89

“practitioners” include participants with over one year of tax/accounting work experience (also

students with respective work experience); 83 “non-practitioners” include those with nil or up to one

year of experience (mostly students).

Participants were recruited during two tax and accounting conferences that were held at the

### University5. They were invited to stay after the end of the conference and contribute to a research

project. Further, student data were collected during a class in international taxation and another in

4 In ###country###, certified tax advisors possess a university degree, at least three years of practice and hey must have passed an extensive exam on tax and accounting (financial, managerial). They can be considered expert not only in tax but also in financial reporting. 5 Data collection was carried out in two steps; first in 2013 with Cases A and B to test whether there is a difference in users’ perception of the firm with normal amounts of tax information in OCI (in such a case, there would have been no need for the second step) and then in 2015 with Case C to include a comparison with overstated amounts of tax information in OCI.

11

international accounting.6 All 172 participants were told nothing other than that the project is related

to IFRS reporting.

3.3. Test instrument and questionnaire

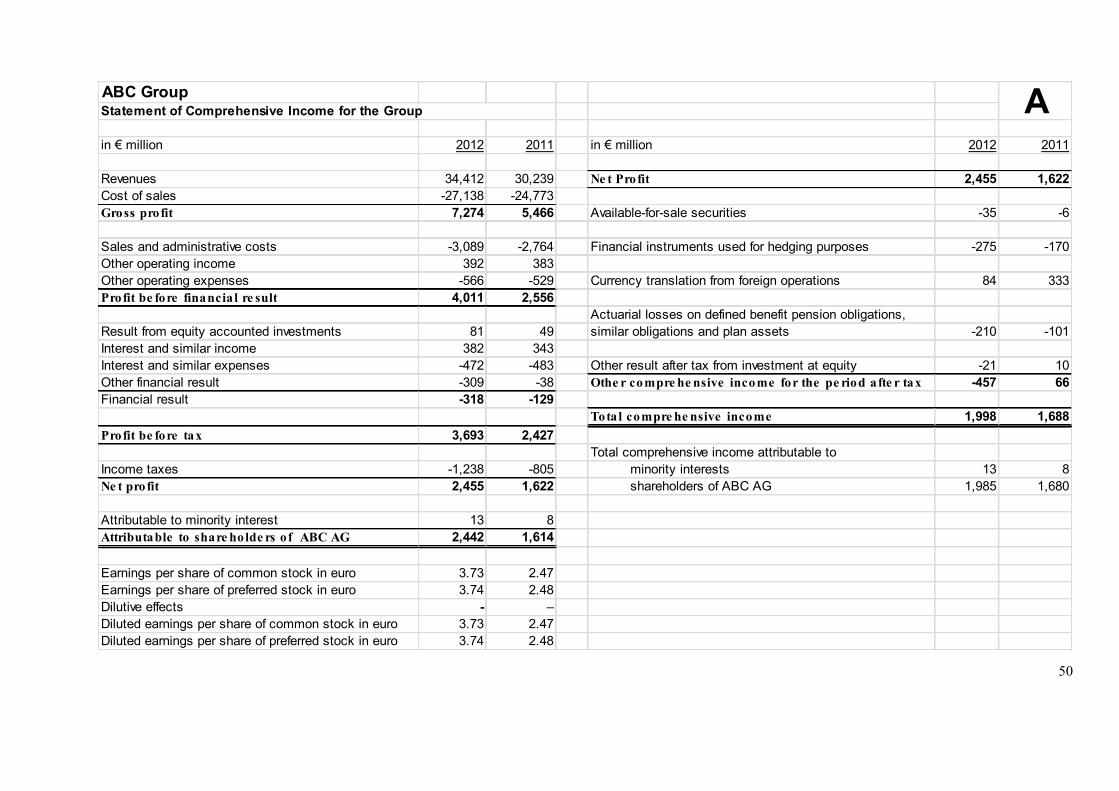

Our test instrument is the financial statements of a model corporation, including balance sheet;

comprehensive income statement; statement of changes in equity; and cash flow statement. We did

not include notes, statement on corporate governance, management report, etc.

The financial statements given to participants are based on the model financial statement of

an actual MNC after thorough screening. The criteria for choosing the respective MNC were: listing

on an active market (in our case, the German prime market DAX), IFRS reporting (non-industry

specific) and detailed disclosure of deferred tax on OCI on a per-item basis. Furthermore, we chose a

model statement where amounts of deferred tax per line item are average or above the DAX 30

companies, to ensure that amounts are representative but not negligible. To this end, we assume that

items of deferred tax were considered as being material from the firm’s perspective. A one-sample t-

test was run to compare our test instrument’s relative deferred tax figures per OCI line item to the

DAX 30 companies in 2013. The test instrument’s relative deferred tax is not significantly higher

(left-sided t-test, p > 0.05) for any of the line items.7

To eliminate the possibility that participants may be able to identify the model company and

thus might be biased in their judgment, we divided the amounts of the model financial statements by

two, thus maintaining the internal consistency of the statements, and we modified the reporting year.

The statements were distributed in a neutral format to participants. We did not provide any company-

specific information, except clarification that it is a multinational public corporation named “ABC

Group”.

6 Neither co-author was involved in teaching or grading the class. 7 The Mann-Whitney U test gives two line items with a significant (p < 0.05) difference.

12

3.4. Tax information

We manipulate tax in OCI in three ways. In Case A “Net-of-Tax” the line items of OCI were

presented net-of-tax, without any explicit information or mention of deferred tax. In Case B “Tax

Detail”, line items of OCI were presented in gross figure (before tax), followed immediately by the

line “deferred tax” and the net amount. Cases A and B therefore reflect a normal setting, as the

numbers are derived directly from our model statement, i.e. “real life”. Our third manipulation Case C

“Tax Detail x3” represents abnormally high amounts of deferred tax: the nominal deferred tax figures

from Case B were tripled, and the before-tax line items were adapted accordingly.8 In all three

manipulations, the figures of OCI line items after tax and of total OCI after tax are identical.

The manipulation allows us to test our hypotheses. Case A “Net-of-Tax” versus Case B “Tax

Detail” shows the effect of absence versus presence of tax information on judgment (H2) in a normal,

i.e. realistic setting. Case A “Net-of-Tax” versus Case C “Tax Detail x3” shows the effect of

providing versus not providing tax information on judgment in a setting where amounts are

abnormally high (H3).

Contrasting Case B “Tax Detail” versus Case C “Tax Detail x3” allows a more

comprehensive view: the cases not only vary with regard to tax detail, but also with regard to the pre-

tax line items. Any variation in judgment between the two treatments reflects users´ different

perception of both informations (pre-tax line item and tax) and therefore allows to reflect on the

question, whether OCI in itself is deemed relevant for judgment (H1).

Table 2 describes the allocation of participants among the three cases:

[Insert Table 2 about here]

8 A one-sided t-test shows significance (p < 0.05) for the relative deferred tax for three out of five line items compared to the DAX 30 in 2013. Means are largely driven by divergent reclassification to the profit and loss statement. The Mann Whitney U test gives three line items with a significant (p < 0.05) difference.

13

3.5. Judgment

For the questionnaire, we mainly refer to the list of questions used in the study of Anandarajan et al.

(2008), which we modified moderately according to our focus on tax. The questionnaire is composed

of three parts: judgment questions, demographic data and manipulation check. The judgment

questions enquire as to the participants’ perceptions of the firm’s overall financial performance (three

questions), investment appeal (three questions) and tax position (one question), generally using a

nine-point Likert scale, with 1 being “the most favourable and positive opinion” and 9 being “the

most unfavourable and negative opinion”.9 To determine financial performance, three questions on the

financial condition (Q1), on the ability of the group to meet its payments obligations in a timely

manner (Q3) and on its profitability (Q5) are used. Investment appeal is tested by asking about the

riskiness of investing in shares of the firm (Q2), on future growth perspective (Q4) and on the

attractiveness of an investment in shares of the firm (Q6). Finally, the perception of the tax burden of

the firm (very low to very high) is tested (Q7).

By requesting demographic data and professional background information, we collected,

among other information, each participant’s occupation, field of profession, education level and

experience with IFRS.

Finally, one last question tests the participants’ acknowledgement of the (non-)disclosure of

deferred tax information in the comprehensive income statement. This manipulation check allows us

to determine whether the participants recognize the presence or absence of deferred tax information

correctly, in other words, whether they even noticed our specific item of interest.

9 Only regarding profitability (Question 5) are respondents asked to rate the future profitability of the company by using a three-point scale, where 1 is “decrease”, 2 is ”remain” and 3 is “increase”, in order to avoid arbitrary answers.

14

Given that the first language of all participants is ###, all questions and financial statements

are prepared in that language to eliminate any possibility of misinterpretation or misunderstanding.

Before running the experiment, the questionnaires and financial statements were cross-checked by

two other independent ### native speakers. The experiment underwent a pilot test with participants

who are knowledgeable of IFRS reporting.

3.6. Test procedure

In the experiment, we carried out test procedures in three steps. First, we randomly and anonymously

allocated participants to Group A or B (respectively related to Case A “Net-of-Tax” and Case B “Tax

Detail”) for the first round, and Group A or C (respectively related to Case A “Net-of-Tax” and Case

C “Tax Detail x3”) for the second round of data collection. Second, we distributed instructions and

explained that there is no right or wrong answer for this experiment, while not revealing our intentions.

After verifying participants’ understanding of the instructions, we distributed the two sets of

questionnaires for demographic data and judgment questions, and provided the respective financial

statements. Participants were allowed to use as much time as they deemed necessary to complete the

questionnaires, which generally took around 15 minutes. Third, after having collected questionnaires

and financial statements from the participants, we distributed the final manipulation check.

Given that there is no “better” or “more successful” way to answer the questionnaire, and

given that, in particular for fully employed practitioners, any kind of compensation could be only

symbolic, compensation was not offered to participants.10

In brief, Figure 1 below presents the framework and process of our experiment.

10 The question arises as to whether the lack of compensation to subjects reduces external validity, as subjects may not put the same effort into the task when not being rewarded. At least for the professionals group, this assumption is weak, given that the selection procedure ensured the intrinsic motivation of subjects. Furthermore, adequate compensation for professionals (opportunity cost) is precluded by budgetary constraints. We do not believe that for the student group validity is limited. Irrespective, tests of practitioners only suffice to confirm the results and provide external validity.

15

[Insert Figure 1 about here]

4. Results

4.1. Analysis

Participants, as described above, were allocated randomly to the three groups. Randomization among

all participants was in general successful. Only in Group C, significantly (p < 0.05) higher experience

and age, but lower levels of education11 can be observed. The main analysis includes all participants,

while a subsequent analysis focuses exclusively on the subset of practitioners providing better

randomization and higher external validity. The majority of participants (82%) passed the

manipulation check, i.e. correctly identified whether or not detailed information on deferred taxes in

OCI was available (practitioners only: 81%).

Due to the non-normal distribution of data, we use the Kruskal-Wallis Rank-Sum test to

compare results from Cases A “Net-of-Tax”, B “Tax Detail” and C “Tax Detail x3” altogether,

followed by a Mann-Whitney U test for more detailed bilateral results. The Kruskal-Wallis result for

all participants, presented in Table 3, shows that judgment of investment risk (Q2, p = 0.002) and

timeliness of payments (Q3, p = 0.076) significantly differs among the three groups.

[Insert Table 3 about here]

For a more detailed view, and to test our first hypothesis, which states that information in OCI

affects users’ perception, we use the Mann-Whitney U test for Case B “Tax Detail” versus Case C

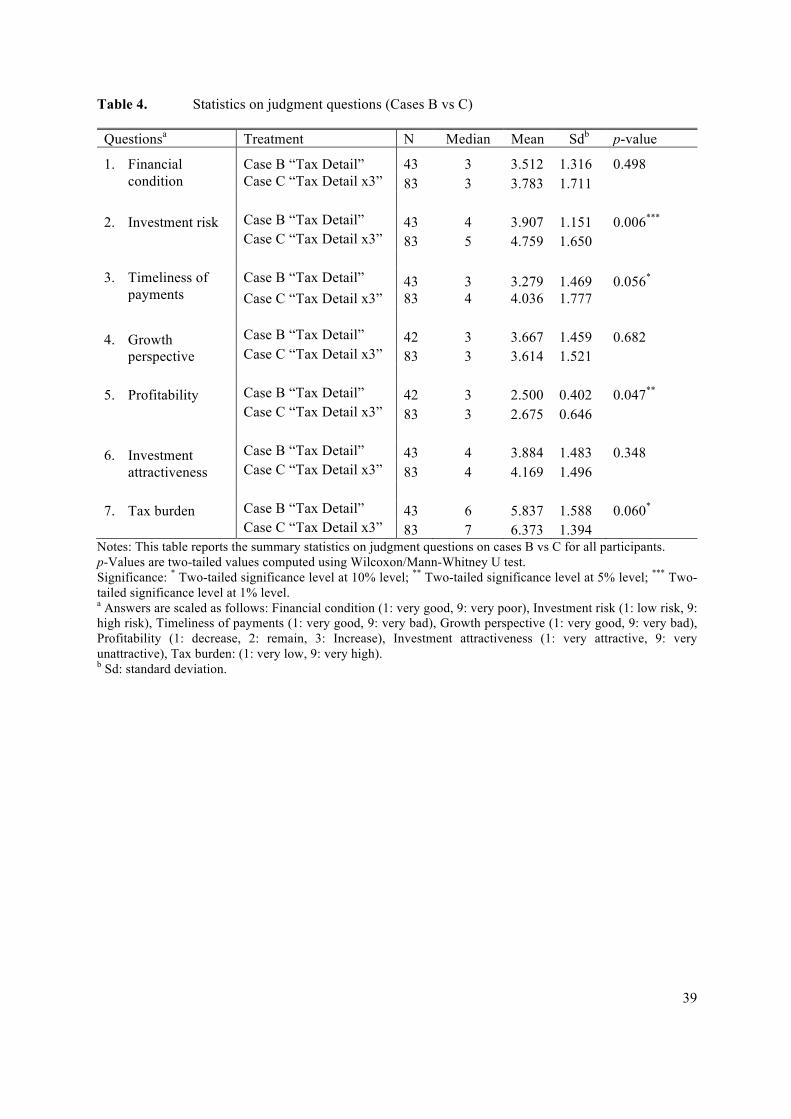

“Tax Detail x3” (Table 4). The results show that judgments on investment risk (Q2, p = 0.006),

timeliness of payments (Q3, p = 0.056), profitability (Q5, p = 0.047) and tax burden (Q7, p = 0.06)

11 Levels of education are, from highest to lowest: doctoral degree, master’s degree, bachelor’s degree and high school.

16

differ significantly, depending on whether normal amounts, or abnormally high amounts of pre-tax

OCI line items and deferred taxes were disclosed. Therefore, when there is a change in both the

amounts of tax information and OCI items, differences in users’ judgment are significant.

[Insert Table 4 about here]

Testing the subsample of practitioners only (not tabulated), Case B “Tax Detail” versus Case

C “Tax Detail x3” reveals significant difference in judgments on investment risk (Q2, p = 0.054) and

on timeliness of payments (Q3, p = 0.075). This result confirms the assumption that users value OCI

information in general, especially when they are less experienced. We therefore find support for our

first hypothesis (H1). In other words, OCI matters.

Our second hypothesis is specifically directed to normal tax information. For Case A “Net-of-

Tax” versus Case B “Tax Detail”, judgment does not differ significantly. More precisely, the results

from the Mann-Whitney U test reveal that the null hypothesis cannot be rejected for any of our seven

questions (Table 5, p > 0.1 for Q1 – Q7). Therefore, as long as the tax information in OCI is normal

and matches the user’s expectations in so far as it does not deviate significantly from average amounts,

such information does not affect users’ judgment of the firm, H2 is not supported.

To test our third hypothesis, which posits that abnormal tax information (in our case:

abnormally high amounts) matter, we contrast Case A “Net-of-Tax” versus Case C “Tax Detail x3”.

Table 5 confirms that judgments on investment risk (Q2, p = 0.002) and timeliness of payments (Q3,

p = 0.06) differ significantly. In other words, only when tax amounts are abnormally high the

participants’ judgment differ. Our results confirm that tax information in OCI significantly affects

users’ judgment of a firm’s economic state in case of abnormal information, which (possibly) deviates

from expectations (H3).

[Insert Table 5 about here]

Our results hold when testing practitioners only. Again, Case A “Net-of-Tax” versus Case B

17

“Tax Detail” does not show any significant difference in judgment, whereas abnormally high amounts

lead to significantly different judgment of investment risk and timeliness of payments (not tabulated;

Q2 and Q3: p < 0.05).

However, the answers to Q7 regarding the firm’s level of the tax burden do not differ

significantly (p = 0.12). Thus, while we do find that abnormal tax information matters for judging the

firm from a general perspective, we find no confirmation that the judgment of specifically the firm’s

tax burden is based on OCI – in spite of the information being recognized and used for other judgment

questions. It seems that rather, the tax burden is judged without referring to OCI, judgment instead is

based upon information from the income statement and balance sheet, which we do not manipulate

and which therefore does not vary among the three cases. This result is in line with the view that tax

information in OCI may be arbitrary and subjective (IAS1, BC 67) and therefore not appropriate to

specifically be included in tax burden analyses.

In addition to the non-parametric analyses, confirmation and further information can be given

by ordered Logit and Tobit regressions (not tabulated),12 which include demographic variables. Most

importantly, the treatment (with or without normal detailed tax information; Cases A “Net-of-Tax”

and B “Tax Detail”) does not lead to significant results, whereas including the abnormally high

amounts of detailed tax information (Case C “Tax Detail x3”) in the regressions leads to more

significant results.13

12 Further supported by ordered Probit; tables available upon request. 13 For questions Q1 on the 10 %, for Q3 and Q6 on the 5% level and for Q2 on the 1% level; regressions on Cases A “Net-of-Tax”, B “Tax Detail” and C “Tax Detail x3”. For questions Q1 on the 10 % level and for Q2 on the 5% level; regressions on Cases A “Net-of-Tax” and C “Tax Detail x3”. For questions Q6 and Q7 on the 10% level, for Q1 and Q3on the 5% level and for Q2 on the 1% level; regression on Cases B “Tax Detail” and C “Tax Detail x3”. The control variables used are: passing of the manipulation check (yes/no); years of experience; education; IFRS experience; number of consolidated annual statements of listed corporations reviewed during the past three years; age; and gender. Of these, one specific aspect of prior professional experience shows some significance in the normal scenario (Cases A “Net-of-Tax” and B “Tax Detail”), namely the number of consolidated annual statements of listed corporations reviewed during the past three years. For questions Q1 and Q3 on the 10% level, and for Q6 on the 5% level; further, age is significant for Q2 on the 1%

18

To summarize, our results support our first and third hypothesis, i.e. different (tax and non-tax)

information in OCI affects users’ judgment of the firm, and abnormal tax information in OCI affects

users’ judgment on the economic state of the firm. In contrast, our second hypothesis is not supported:

We do not find that revealing normal tax information in OCI affects judgment. These results are in

line with the theory of processing information and support the reasoning according to which

information that is beyond expectations is more salient and is consequently more likely to influence

users’ judgment.

4.2. Robustness

To further strengthen our results for all participants and for practitioners only, as described in the

previous section, we perform several additional analyses of subsamples. One very straightforward

confirmation is that in any of the subsamples (manipulation check passed / not passed; practitioners /

non-practitioners; level of IFRS-experience; accounting profession; and any combination of these)

Case A “Net-of-Tax” versus Case B “Tax Detail” shows no significantly different judgment (not

tabulated). We can thus rule out that our results originate from insufficient IFRS knowledge or

experience, or other lack of insight. In cases where the deferred tax information meets expectations,

our participants judge the firm not differently. We cannot reject the assumption that detailed

disclosure of tax in OCI makes no difference when participants are exposed to the normal setting.

Also the results of Case A “Net-of-Tax” versus Case C “Tax Detail x3” can be confirmed in

our sample splits. Q2 on investment risk yields significantly different judgment for participants who

passed the manipulation check, for practitioners only, and for practitioners who passed the

manipulation check.14 Q3 on timeliness of meeting payments obligations shows significantly lower

judgment for Case C “Tax Detail x3”, when the sample is reduced to practitioners and further to

level. Judgment does not differ significantly depending on the passing of the manipulation check. 14 In addition, the results on Q2 hold for participants who failed the manipulation check, for non-practitioners, and for non-practitioners who failed the manipulation check.

19

practitioners who passed the manipulation check.

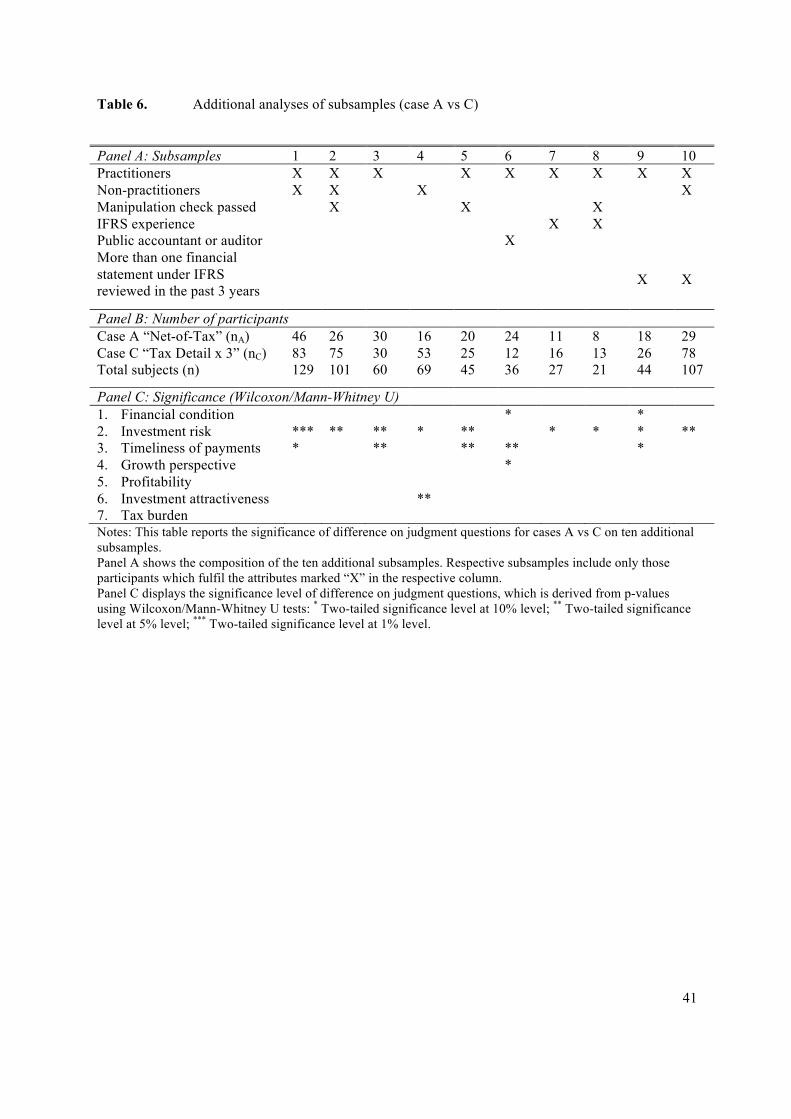

Table 6 illustrates our subsamples and the respective levels of significance, which we found

for all seven judgment questions.15

[Insert Table 6 about here]

5. Discussion

Our experiment and the statistical analyses provide three main results: First, they show that disclosure

of normal tax information (Cases A “Net-of-Tax” versus B “Tax Detail”) does not affects users’

judgment of the firm in any way. Indeed, it appears that average tax information meets users’

expectations, which draws no attention. This result is in line with cognitive theory on limited attention

and differential processing cost, as well as availability heuristic. As the disclosed tax information does

not deviate from expectations, no particular focus is needed to process it and users rather pay attention

to other pieces of information to build their judgment. Thus, results from testing Cases A “Net-of-Tax”

versus B “Tax Detail” do not enable us to reject the null hypothesis (H20) according to which

disclosing tax information on the face of financial statement does not lead to different users’ judgment

about a firm’s economic state.

Second, our results show that disclosing of abnormally high amounts of deferred taxes (Case

A “Net-of-Tax” versus Case C “Tax Detail x3”) attract users’ attention, as their judgment

significantly differs for some of the questions regarding the firms’ economic position. Judgment,

differs in particular regarding the investment risk (Q2) and the timeliness of payments (Q3).

Participants judge the risk of investing in the shares of the company significantly higher, when

15 A group size of less than 10 participants reduces reliability of results; nevertheless, results also of small groups give an indication and are therefore tabulated.

20

deferred tax in OCI is abnormally high. Equally, they judge the ability of the firm to meet its payment

obligations in a timely manner significantly worse. It is surprising that judgment of the tax burden of

the firm (Q7) does not differ significantly. It seems that when judging the tax burden of the firm, users

rather rely on information found in the income statement and balance sheet, instead of considering

OCI information. Nonetheless, results from testing Cases A “Net-of-Tax” versus C “Tax Detail x3”

permit the rejection of the null hypothesis (H30), and supports the notion that disclosing abnormally

high tax amounts leads to different users’ judgments about the firms’ economic position, in particular

with regard to investment risk and timeliness of payments.

Third, we find that comparing judgments from disclosures of normal tax information and

abnormally high amounts of tax information (Case B “Tax Detail” versus Case C “Tax Detail x3”)

also leads to significant differences in users’ judgment. However, in this particular case, not only tax

information changed, but also OCI information in general – OCI pre-tax line items had to be adjusted

to take into account tripled tax information in such way that net amounts of OCI line items and OCI

total remained unchanged. Thus, we can infer that OCI information (tax and non-tax) is relevant for

users of financial statements. It is noteworthy that users’ judgments on investment risk (Q2),

timeliness of payments (Q3), profitability (Q5) and tax burden (Q7) differ when all participants (i.e.

practitioners and non-practitioners) are included in the sample, while it is only significant for

judgment of investment risk (Q2) and timeliness of payments (Q3) when testing exclusively

practitioners. Consequently, this result shows that more experienced users (practitioners) perceive less

relevance in OCI information than less experienced ones. Nonetheless, testing Cases B “Tax detail”

versus C “Tax Detail x3” supports the first hypothesis H1, meaning that information included in OCI

seems to be relevant to users of financial statements.

6. Conclusions

Disclosure in financial reporting in general, and in tax accounting in particular, has become

21

more comprehensive, which is justified by the need for transparency and for relevant information.

These are also the main reasons for recent amendments of IAS 12 and IAS 1, which increase the

requirements for disaggregated disclosure on tax in the financial statements. This study attempts to

evaluate whether doubts regarding the benefits of additional disclosure are well founded. We

investigate whether one specific issue of tax disclosure, deferred taxes in OCI, is relevant to users. To

the best of our knowledge, this is the first paper that focuses on tax in OCI. Other studies, in particular

on the decision usefulness of OCI or on the decision usefulness of (deferred) tax accounting, do not

focus on information processing of the actual users and perceptions of income tax disclosures.

Our results demonstrate that there is no significant difference between two treatments of tax

information in OCI in a normal, i.e. realistic, setting; we therefore cannot confirm that detailed

information on deferred tax on a per-item basis is relevant to the judgment of financial statement users

regarding the financial performance, investment appeal and tax position of the model firm.

Given that empirical evidence supports the informative role of OCI (Fernández & Arana,

2010) and highlights the benefits by disclosing more disaggregated contents in OCI (Pinto, 2005;

Mitra & Hossain, 2009; Kubota, Suda and Takehara 2011), our results indicate that tax information in

OCI has significant impact on the judgment of financial statement users in the case of abnormal, i.e.

overstated, figures. In other words, while we cannot find any support for relevance of normal tax

information in OCI, we do find such support when facing abnormally (unexpected) high amounts of

tax information.

Our study informs the current debate on the materiality principle. Given our results, two

approaches are conceivable. Either “material” is understood as “abnormal”, in which case, firms

should be asked to disclose detailed information only if beyond expectations; or “material” is

understood as “important to know whether abnormal or not”. In the latter case, any normal or

abnormal (tax) information should be disclosed that would potentially affects users’ judgment, if it

were abnormal. Such interpretation of “materiality” supports information overload. The IASB has

22

placed some emphasis on the disclosure of tax information in OCI, and has given only little weight to

doubts that were brought forward during the due process, such as possible arbitrary tax allocation and

lack of availability of data. The trust that the IASB has placed in the relevance of such information in

a “normal” setting, however, cannot be supported.

23

References

Aboody, D. (1996). Recognition versus Disclosure in Oil and Gas Industry. Journal of Accounting

Research, 34 (Supplement), 21-32. https://doi.org/10.2307/2491423

Agnew, J. R., & Szykman, L. R. (2005). Asset Allocation and Information Overload: The Influence of

Information Display, Asset Choice, and Investor Experience. Journal of Behavioral Finance,

6(2), 57–70. https://doi.org/10.1207/s15427579jpfm0602_2

Ahmed, A. S., Kilic, E., & Lobo, G. J. (2006). Does Recognition versus Disclosure Matter? Evidence

from Value-Relevance of Banks’ Recognized and Disclosed Derivative Financial Instruments.

The Accounting Review, 81(3), 567-588. https://doi.org/10.2308/accr.2006.81.3.567

Al Jifri, K., & Citron, D. (2009). The Value Relevance of Financial Statement Recognition versus

Note Disclosure: Evidence from Goodwill Accounting. European Accounting Review, 18(4),

123-140. https://doi.org/10.1080/09638180802324351

Amir, E., & Sougiannis, T. (1999). Analysts’ Interpretation and Investors’ Valuation of Tax

Carryforwards*. Contemporary Accounting Research, 16(1), 1–33.

https://doi.org/10.1111/j.1911-3846.1999.tb00572.x

Anandarajan, A., Belzile, R., Curatola, A. P. & Viger, C. (2008). Disclosure versus Recognition in

Stock-Option Reporting: Are Sophisticated Users’ Perceptions and Judgments Influenced by the

Reporting Format? In Advances in Accounting Behavioral Research (Vol. 11, pp. 31–57).

Emerald Group Publishing Limited. https://doi.org/10.1016/S1475-1488(08)11002-X

Atwood, T. J., Drake, M. S., Myers, J. N., & Myers, L. A. (2011). Do earnings reported under IFRS

tell us more about future earnings and cash flows? Journal of Accounting and Public Policy,

30(2), 103–121. https://doi.org/10.1016/j.jaccpubpol.2010.10.001

24

Ayers, B. C. (1998). Deferred Tax Accounting under SFAS No. 109: An Empirical Investigation of

Its Incremental Value-Relevance Relative to APB No. 11. The Accounting Review, 73(2), 195–

212.

Barth, M. E., Beaver, W. H., & Landsman, W. R. (2001). The relevance of the value relevance

literature for financial accounting standard setting: another view. Journal of Accounting and

Economics, 31(1–3), 77–104. https://doi.org/10.1016/S0165-4101(01)00019-2

Bauman, C. C., Bauman, M. P., & Halsey, R. F. (2001). Do Firms Use the Deferred Tax Asset

Valuation Allowance to Manage Earnings? The Journal of the American Taxation Association,

23(s-1), 27–48. https://doi.org/10.2308/jata.2001.23.s-1.27

Bernard, V., & Schipper, K. (1994). Recognition and Disclosure in Financial Reporting (Unpublished

dissertation). University of Michigan, Ann Arbor, MI.

Biddle, G. C., & Choi, J.-H. (2006). Is Comprehensive Income Useful? Journal of Contemporary

Accounting & Economics, 2(1), 1–32. https://doi.org/10.1016/S1815-5669(10)70015-1

Black, D. E. (2016). Other comprehensive income: a review and directions for future research.

Accounting & Finance, 56(1), 9–45. https://doi.org/10.1111/acfi.12186

Blouin, J. and Robinson, L. (2012). Academic Research on FIN 48: What Have We Learned?

Prepared for the Financial Accounting Foundations’ Post-Implementation Review of

Financial Accounting Standards Board Interpretation No. 48.

http://ssrn.com/abstract=2191137 (accessed 6 October 2013).

Botosan, C. A., & Plumlee, M. A. (2002). A Re-examination of Disclosure Level and the Expected

Cost of Equity Capital. Journal of Accounting Research, 40(1), 21–40. https://doi.org/10.1111/

1475-679X.00037

Bratten, B., Choudhary, P., & Schipper, K. (2013). Evidence that Market Participants Assess

25

Recognized and Disclosed Items Similarly When Reliability Is Not an Issue. Accounting

Review, 88(4), pp. 1179-1210. https://doi.org/10.2308/accr-50421

Cahan, S. F., Courtenay, S. M., Gronnewoller, P. L., & Upton, D. R. (2000). Value Relevance of

Mandated Comprehensive Income Disclosures. Journal of Business Finance & Accounting,

27(9–10), 1233–1265. https://doi.org/10.1111/1468-5957.00356

Chambers, D., Linsmeier, T. J., Shakespeare, C., & Sougiannis, T. (2007). An evaluation of SFAS

No. 130 comprehensive income disclosures. Review of Accounting Studies, 12(4), 557–593.

https://doi.org/10.1007/s11142-007-9043-2

Chandra, U., & Ro, B. T. (1997). The association between deferred taxes and common stock risk.

Journal of Accounting and Public Policy, 16(3), 311–333. https://doi.org/10.1016/S0278-

4254(97)00021-5

Chaney, P. K., & Jeter, D. C. (1994). The Effect of Deferred Taxes on Security Prices. Journal of

Accounting, Auditing & Finance, 9(1), 91–116. https://doi.org/10.1177/0148558X9400900106

Chang, C., Herbohn, K., & Tutticci, I. (2009). Market’s perception of deferred tax accruals.

Accounting & Finance, 49(4), 645–673. https://doi.org/10.1111/j.1467-629X.2009.00307.x

Chattopadhyay, S., Arcelus, F. j., & Srinivasan, G. (1997). Deferred Taxes and Bond Ratings: A

Canadian Case. Journal of Business Finance & Accounting, 24(3), 541–557.

https://doi.org/10.1111/1468-5957.00120

Chen, K. C. W., Danielson, M. G., & Schoderbek, M. P. (2003). Analysts’ Interpretation of Transitory

Earnings Components: Evidence from Forecast Revisions after Disclosure of the 1993 Deferred

Tax Adjustment. Journal of Accounting, Auditing & Finance, 18(3), 333–353.

https://doi.org/10.1177/0148558X0301800303

26

Cheng, C. S. A., Cheung, J. K., & Gopalakrishnan, V. (1993). On the Usefulness of Operating

Income, Net Income and Comprehensive Income in Explaining Security Returns. Accounting

and Business Research, 23(91), 195–203. https://doi.org/10.1080/00014788.1993.9729879

Chludek, A. K. (2011). Perceived versus Actual Cash Flow Implications of Deferred Taxes: An

Analysis of Value Relevance and Reversal under IFRS. Journal of International Accounting

Research, 10(1), pp. 1-25.

Christensen, T. E., Paik, G. H. and Stice, E. K. (2008). Creating a Bigger Bath Using the Deferred

Tax Valuation Allowance. Journal of Business Finance and Accounting, 35(5-6), pp. 601-625.

Davis-Friday, P. Y., Folani, L. B., Liu, C. S., & Mittelstaedt, H. F. (1999). The Value Relevance of

Financial Statement Recognition vs. Disclosure: Evidence from SFAS no. 106. The

Accounting Review, 74(4), 403-423. https://doi.org/10.2308/accr.1999.74.4.403.

Davis-Friday, P. Y., Liu, C. S., & Mittelstaedt, H. F. (2004). Recognition and Disclosure Reliability:

Evidence from SFAS no. 106. Contemporary Accounting Research, 21(2), 399-429.

https://doi.org/10.1506/T0VC-Q15Y-W5QV-4UKQ

Dhaliwal, D., Subramanyam, K. R., & Trezevant, R. (1999). Is comprehensive income superior to net

income as a measure of firm performance?1. Journal of Accounting and Economics, 26(1–3),

43–67. https://doi.org/10.1016/S0165-4101(98)00033-0

Dunbar, A. E., & Sansing, R. C. (2002). Measuring Corporate Tax Preferences. The Journal of the

American Taxation Association, 24(2), 1–17. https://doi.org/10.2308/jata.2002.24.2.1

Emrick, C., Wasden, M. and Young, R. (2006). Moody’s Approach to Other Comprehensive Income

Items When Calculating Effective Leverage for Finance Companies,

http://ssrn.com/abstract=959014 (accessed 5 March 2013).

ESSEC Knowledge (2013). Cracking Down on Tax Avoidance: Are Financial Reporting Disclosures

27

Out of Control? ESSEC Business School, http://www.essec.edu/news-faculty/faculty-news-

detail/article/sevir-contre-levasion-fiscale-les-publications-dinformation-financiere-sont-elles-

hors-de-c.html (accessed 20 June 2014).

EY (2014). Improving Disclosure Effectiveness, http://www.ey.com/Publication/vwLUAssets/

Applying IFRS: Improving disclosure effectiveness/$FILE/Applying-DisclEffectiveness-

July%202014.pdf (accessed 20 March 2017).

Eppler, Martin J. & Mengis, Jeanne (2004). The Concept of Information Overload: A Review of

Literature from Organization Science, Accounting, Marketing, MIS, and Related Disciplines.

The Information Society, 20:5, 325-344, DOI: 10.1080/01972240490507974

The European Financial Reporting Advisory Group (2011). Improving the Financial Reporting of

Income Tax. (Discussion Paper) Retrieved from the Financial Reporting Council website:

https://www.frc.org.uk/Our-Work/Publications/ASB/Improving-the-Financial-Reporting-of-

Income-Tax.pdf

Fernández, F. S. & Arana, M. M. C. (2010). Effects of Comprehensive Income on ROE in a Context

of Crisis: Empirical Evidence for IBEX-35 Listed Companies (2004-2008). International

Business & Economics Research Journal, 9(1), pp. 117-128. Retrieved from https://www.

cluteinstitute.com/ojs/index.php/IBER/article/view/513

Financial Times (2011). Lex column: Fairyland Value Accounting, 24 Oct. 2011.

Fiske, S.T. (1995). Social Cognition, in Tesser, A. (Ed.), Advanced Social Psychology (pp. 149-194).

New York: McGraw-Hill.

Fiske, S., Taylor, S. (1991). Social Cognition, (2nd Ed.). New York: McGraw-Hill.

Givoly, D., & Hayn, C. (1992). The Valuation of the Deferred Tax Liability: Evidence from the Stock

Market. The Accounting Review, 67(2), 394–410.

28

Goncharov, I., & Hodgson, A. (2011). Measuring and Reporting Income in Europe. Journal of

International Accounting Research, 10(1), 27–59. https://doi.org/10.2308/jiar.2011.10.1.27

Gopalakrishnan, V. (1994). The Effect of Recognition vs. Disclosure on Investor Valuation: The Case

of Pension Accounting. Review of Quantitative Finance and Accounting, 4, pp. 83-396.

https://doi.org/10.1007/BF01078805.

Gordon, E. A. & Joos, P. R. (2004). Unrecognized Deferred Taxes: Evidence from the UK. The

Accounting Review, 79(1) pp. 97-124.

Groves, R. J. (1994). Financial Disclosure: When More Is Not Better. Financial Executive, 10(3),

pp.11-14.

Guthrie, J. (2011). Barclays’ Lucas is a Counter-Intuitive Credit Crusader. Financial Times, 15

November 2011.

Hand, J.R.M. (1990). A Test of the Extended Functional Fixation Hypothesis. Accounting Review

65(4), pp. 740-763.

Hirshleifer, D., & Teoh, S. H. (2003). Limited attention, information disclosure, and financial

reporting. Journal of Accounting and Economics, 36(1-3), pp. 337-386.

https://doi.org/10.1016/j.jacceco.2003.10.002

Hirst, D. E., & Hopkins, P. E. (1998). Comprehensive Income Reporting and Analysts’ Valuation

Judgments. Journal of Accounting Research, 36, 47–75. https://doi.org/10.2307/2491306

Huss, H. F., & Zhao, J. (1991). An Investigation of Alternative Treatments of Deferred Taxes in Bond

Raters’ Judgments. Journal of Accounting, Auditing & Finance, 6(1), 53–68.

https://doi.org/10.1177/0148558X9100600105

International Accounting Standard Board (IASB) (2012). Hans Hoogervorst speech, Korea, April

29

2012, http://www.ifrs.org/Alerts/Conference/Documents/HansHoogervorstApril2012Korea.

pdf (accessed 12 August 2013).

International Accounting Standard Board (IASB) (2010). The Conceptual Framework for Financial

Reporting, London: International Accounting Standards Board.

International Accounting Standard Board (IASB) (2013a). Discussion forum: Financial Reporting

Disclosure Feedback Statement, London: International Accounting Standards Board.

International Accounting Standard Board (IASB) (2013b). A Review of the Conceptual Framework

for Financial Reporting, London: International Accounting Standards Board.

International Accounting Standard Board (IASB) (2013c). Joint Effort Needed to Tackle Disclosure

Problem, London: International Accounting Standards Board.

International Accounting Standard Board (IASB) (2013d). Disclosure Initiative, London:

International Accounting Standards Board, http://www.ifrs.org/Current-Projects/IASB-

Projects/Disclosure-Initiative/Pages/Disclosure-Initiative.aspx (accessed 2 March 2017).

Iselin, E. R. (1988). The effects of information load and information diversity on decision quality in a

structured decision task. Accounting, Organizations and Society, 13(2), 147–164.

https://doi.org/10.1016/0361-3682(88)90041-4

Israeli, D. (2015). Recognition versus Disclosure: Evidence from Fair Value of Investment Property.

Review of Accounting Studies, 20(4), pp. 1457-1503. https://doi.org/10.1007/s11142-015-

9335-x.

Kahneman, D., (1973). Attention and Effort. Englewood Cliffs, NJ: Prentice-Hall.

30

Kanagaretnam, K., Mathieu, R., & Shehata, M. (2009). Usefulness of comprehensive income

reporting in Canada. Journal of Accounting and Public Policy, 28(4), 349–365.

https://doi.org/10.1016/j.jaccpubpol.2009.06.004

KPMG. (2011). Disclosure Overload and Complexity: Hidden in Plain Sight

http://www.kpmg.com/US/en/IssuesAndInsights/ArticlesPublications/Documents/disclosure-

overload-complexity.pdf (Accessed 20 June 2013)

Kubota, K., Suda, K., & Takehara, H. (2011). Information Content of Other Comprehensive Income

and Net Income: Evidence for Japanese Firms. Asia-Pacific Journal of Accounting &

Economics, 18(2), 145–168. https://doi.org/10.1080/16081625.2011.9720879

Kubota, K., Suda, K., & Takehara, H. (2011). Information Content of Other Comprehensive Income

and Net Income: Evidence for Japanese Firms. Asia-Pacific Journal of Accounting &

Economics, 18(2), 145–168. https://doi.org/10.1080/16081625.2011.9720879

Landsman, W. R., Miller, B. L., Peasnell, K., & Yeh, S. (2011). Do Investors Understand Really Dirty

Surplus? The Accounting Review, 86(1), 237–258. https://doi.org/10.2308/accr.00000014

Lev, B., & Nissim, D. (2004). Taxable Income, Future Earnings, and Equity Values. The Accounting

Review, 79(4), 1039–1074. https://doi.org/10.2308/accr.2004.79.4.1039

Lisowsky, P., Robinson, L., & Schmidt, A. (2013). Do Publicly Disclosed Tax Reserves Tell Us

About Privately Disclosed Tax Shelter Activity? Journal of Accounting Research, 51(3), 583–

629. https://doi.org/10.1111/joar.12003

Maines, L. A., & McDaniel, L. S. (2000). Effects of Comprehensive-Income Characteristics on

Nonprofessional Investors’ Judgments: The Role of Financial-Statement Presentation Format.

The Accounting Review, 75(2), 179–207.

31

McAnally, M. L., McGuire, S. T., & Weaver, C. D. (2010). Assessing the Financial Reporting

Consequences of Conversion to IFRS: The Case of Equity-Based Compensation. Accounting

Horizons, 24(4), 589–621. https://doi.org/10.2308/acch.2010.24.4.589

Mitra, S., & Hossain, M. (2009). Value-relevance of pension transition adjustments and other

comprehensive income components in the adoption year of SFAS No. 158. Review of

Quantitative Finance and Accounting, 33(3), 279–301. https://doi.org/10.1007/s11156-009-

0112-4

Nisbett, R. E., Zukier, H., & Lemley, R. E. (1981). The Dilution Effect: Nondiagnostic Information

Weakens the Implications of Diagnostic Information. Cognitive Psychology, 13(2), pp. 248-

277. https://doi.org/10.1016/0010-0285(81)90010-4.

Novak, A. (2016). Issues in the Recognition versus Disclosure of Financial Information Debate. Naše

Gospodarstvo/Our Economy, 62(4), 52–61. https://doi.org/10.1515/ngoe-2016-0024

OECD (2015). Transfer Pricing Documentation and Country-by-Country Reporting, Action 13 - 2015

Final Report. Paris: OECD Publishing. http://dx.doi.org/10.1787/9789264241480-en.

O’Hanlon, J. F., & Pope, P. F. (1999). The Value-Relevance of UK Dirty Surplus Accounting Flows.

The British Accounting Review, 31(4), 459–482. https://doi.org/10.1006/bare.1999.0116

O’Reilly, C. A. (1980). Individuals and Information Overload in Organizations: Is More Necessarily

Better? The Academy of Management Journal, 23(4), 684–696. https://doi.org/10.2307/255556

Overesch, M. and Schreiber, U. (2006). Does Accounting for Taxes on Income Provide Information

About Tax Planning Performance?: Evidence from German Multinationals (Discussion Paper

No. 06-072). Retrieved from ZEW – Centre for European Economic Research website:

ftp://ftp.zew.de/pub/zew-docs/dp/dp06072.pdf.

32

Phillips, J. D., Pincus, M., Rego, S. O., & Wan, H. (2004). Decomposing Changes in Deferred Tax

Assets and Liabilities to Isolate Earnings Management Activities. The Journal of the American

Taxation Association, 26(s-1), 43–66. https://doi.org/10.2308/jata.2004.26.s-1.43

Phillips, J., Pincus, M., & Rego, S. O. (2003). Earnings Management: New Evidence Based on

Deferred Tax Expense. The Accounting Review, 78(2), 491–521.

Pinto, J. A. (2005). How Comprehensive is Comprehensive Income? The Value Relevance of Foreign

Currency Translation Adjustments. Journal of International Financial Management &

Accounting, 16(2), 97–122. https://doi.org/10.1111/j.1467-646X.2005.00113.x

Plumlee, M. A. (2003). The Effect of Information Complexity on Analysts’ Use of That Information.

The Accounting Review, 78(1), 275–296.

Poterba, J., Rao, N., & Seidman, J. (2007). Deferred Tax Positions and Incentives for Corporate

Behavior Around Corporate Tax Changes (Working Paper No. 12923). National Bureau of

Economic Research. https://doi.org/10.3386/w12923

PricewaterhouseCoopers (PwC) (2011). Investor View: Improving Income Tax Disclosures,

http://www.pwc.com/en_GX/gx/audit-services/corporate-reporting/publications/investor-

view/pdf/pwc-improving-income-tax-disclosures.pdf (accessed 8 September 2014).

Raedy, J. S., Seidman, J. K., & Shackelford, D. A. (2011). Is There Information Content in the Tax

Footnote? (SSRN Scholarly Paper No. ID 1759266). Rochester, NY: Social Science Research

Network. Retrieved from https://papers.ssrn.com/abstract=1759266

Rapoport, M. (2011, February 7). “Toxic” Assets Still Lurking at Banks. Wall Street Journal.

Retrieved from http://www.wsj.com/articles/SB1000142405274870457010457612470114

4189910

33

Schick, A. G., Gordon, L. A., & Haka, S. (1990). Information overload: A temporal approach.

Accounting, Organizations and Society, 15(3), 199–220. https://doi.org/10.1016/0361-

3682(90)90005-F

Schrand, C. M., & Walther, B. R. (2000). Strategic Benchmarks in Earnings Announcements: The

Selective Disclosure of Prior-Period Earnings Components. The Accounting Review, 75(2),

151–177.

Schrand, C. M., & Wong, M. H. F. (2003). Earnings Management Using the Valuation Allowance for

Deferred Tax Assets under SFAS No. 109*. Contemporary Accounting Research, 20(3), 579–

611. https://doi.org/10.1506/480D-098U-607R-5D9W

Schroder, H. M., M. J. Driver, & S. Streufert (1967). Human Information Processing. New York, NY:

Holt, Rinehart, & Winston.

Simon, H. A. (1955). A Behavioral Model of Rational Choice. The Quarterly Journal of Economics,

69(1), 99–118. https://doi.org/10.2307/1884852

Simon, H. A. (1956). Rational Choice and the Structure of the Environment. Psychological Review,

63(2), p. 129. https://doi.org/10.1037/h0042769

Simon, H. A. (1991). Bounded Rationality and Organizational Learning. Organization Science, 2(1),

125–134.

Tversky, A., & Kahneman, D. (1973). Availability: A heuristic for judging frequency and probability.

Cognitive Psychology, 5(2), 207–232. https://doi.org/10.1016/0010-0285(73)90033-9

Weber, D. P. (2009). Do Analysts and Investors Fully Appreciate the Implications of Book-Tax

Differences for Future Earnings?. Contemporary Accounting Research, 26(4), 1175–1206.

https://doi.org/10.1506/car.26.4.7

34

Wilkie, P. & Limberg, S. (1993) Measuring Explicit Tax (Dis) Advantage for Corporate Taxpayers:

An Alternative to Average Effective Tax Rates. The Journal of the American Taxation

Association, 15, 46-71.

35

Figures

Fig. 1. Framework for the effects of the presence of deferred tax details in OCI

Financial statements including: Balance sheet

Comprehensive income statement Cash flow statement

Statement of changes in equity

TREATMENT

Case A “Net-of-Tax” Case B “Tax Detail” Case C “Tax Detail x3” Deferred taxes on OCI are netted against each OCI item and thus not shown in the comprehensive income statement (nor elsewhere in the statements)

Deferred taxes are allocated to each OCI item, details of deferred tax effects are shown in the comprehensive income statement.

Deferred taxes are allocated to each OCI item, details of deferred tax effects are shown in the comprehensive income statement and multiplied by three.

INFORMATION PROCESSING

Limited attention + differential processing cost: Does information meet expectation?

Manipulation Check:

Does ABC Group report deferred taxes in its comprehensive income statement? (Yes/No)

JUDGMENT

Financial performance • Financial condition • Payment obligation • Profitability

Investment appeal

• Growth perspective • Investment risk • Investment attractiveness

Tax position

• Tax burden

36

Tables

Table 1. Descriptive statistics on demographic variables

All participants = 172 N Mean SD Min P25 Median P75 Max

No. of years of experience 167 6.056 9.244 0.000 0.000 1.500 8.000 43.000

Education level 171 2.632 0.583 1.000 2.000 3.000 3.000 4.000

Age 170 31.006 11.045 22.000 24.000 25.000 37.000 72.000

Experience with IFRS 172 0.645 0.480 0.000 0.000 1.000 1.000 1.000

No. of financial statements under IFRS reviewed in the past 3 years

170 8.982 22.339 0.000 1.000 3.000 10.000 220.000

Gender 172 97 male

75 female Notes: This table reports descriptive statistics for the demographic variables used in our study for all participants. Definition of variables: No. of years of experience, number of years of relevant professional experience according to participants; Education level, the highest level of education reached, measured as: Doctoral degree (=1), Master’s degree (=2), Bachelor’s degree (=3) and High school (=4); Experience with IFRS, experience in reviewing the annual or consolidated financial statements according to IFRS, measured as: Yes (=0) or No (=1); No. of financial statements under IFRS reviewed in the past 3 years, number of consolidated financial statements of publicly traded corporations reviewed during the past 3 years.

37

Table 2. Composition of participants

Practitionera Non-Practitionerb Total Case A “Net-of-Tax”c 30 16 46 Case B “Tax Detail”d 29 14 43 Case C “Tax Detail x3”e 30 53 84 Total 89 83 172 Notes: This table describes the composition of our experiment’s participants. a Practitioner refers to participants with over one year of tax/accounting work experience. b Non-Practitioner refers to participants with no or up to one year of experience. c Case A “Net-of-Tax” refers to the case in which line items of OCI were presented net-of-tax, without any explicit information or mention of deferred tax. d Case B “Tax detail” refers to the case in which line items of OCI were given before tax, followed immediately by the line “deferred tax” and the net amount. e Case C “Tax detail x3” refers to the case presenting abnormally high amounts of deferred tax: the nominal deferred tax figures from Case B were tripled, and the before-tax line items were adapted accordingly.

38

Table 3. Statistics on judgment questions (Cases A, B and C)

Questionsa Treatment N Median Mean Sdb p-values 1. Financial

condition Case A “Net-of-Tax” 46 3 3.652 1.418 0.799 Case B “Tax Detail” 43 3 3.512 1.316 Case C “Tax Detail x3” 83 3 3.783 1.711

2. Investment risk Case A “Net-of-Tax” 46 3 3.804 1.327 0.002*** Case B “Tax Detail” 43 4 3.907 1.151 Case C “Tax Detail x3” 83 5 4.759 1.650 3. Timeliness of

payments Case A “Net-of-Tax” 46 3 3.400 1.606 0.076* Case B “Tax Detail” 43 3 3.279 1.469

Case C “Tax Detail x3” 83 4 4.036 1.777 4. Growth

perspective Case A “Net-of-Tax” 44 3 3.477 1.210 0.883 Case B “Tax Detail” 42 3 3.667 1.459

Case C “Tax Detail x3” 83 3 3.614 1.521 5. Profitability Case A “Net-of-Tax” 44 3 2.614 0.689 0.283 Case B “Tax Detail” 42 3 2.500 0.402 Case C “Tax Detail x3” 83 3 2.675 0.646 6. Investment

attractiveness Case A “Net-of-Tax” 45 3 3.778 1.278 0.357 Case B “Tax Detail” 43 4 3.884 1.483

Case C “Tax Detail x3” 83 4 4.169 1.496 7. Tax burden Case A “Net-of-Tax” 46 6 5.935 1.421 0.122 Case B “Tax Detail” 43 6 5.837 1.588 Case C “Tax Detail x3” 83 7 6.373 1.394

Notes: This table reports the summary statistics on judgment questions on cases A, B and C for all participants. p-Values are two-tailed values computed using Kruskal-Wallis Rank-Sum test. Significance: * Two-tailed significance level at 10% level; *** Two-tailed significance level at 1% level. a Answers are scaled as follows: Financial condition (1: very good, 9: very poor), Investment risk (1: low risk, 9: high risk), Timeliness of payments (1: very good, 9: very bad), Growth perspective (1: very good, 9: very bad), Profitability (1: decrease, 2: remain, 3: Increase), Investment attractiveness (1: very attractive, 9: very unattractive), Tax burden: (1: very low, 9: very high). b Sd: standard deviation.

39

Table 4. Statistics on judgment questions (Cases B vs C)

Questionsa Treatment N Median Mean Sdb p-value

1. Financial condition

Case B “Tax Detail” 43 3 3.512 1.316 0.498 Case C “Tax Detail x3” 83 3 3.783 1.711

2. Investment risk Case B “Tax Detail” 43 4 3.907 1.151 0.006*** Case C “Tax Detail x3” 83 5 4.759 1.650 3. Timeliness of

payments

Case B “Tax Detail” 43 3 3.279 1.469 0.056* Case C “Tax Detail x3” 83 4 4.036 1.777

4. Growth perspective

Case B “Tax Detail” 42 3 3.667 1.459 0.682 Case C “Tax Detail x3” 83 3 3.614 1.521

5. Profitability Case B “Tax Detail” 42 3 2.500 0.402 0.047** Case C “Tax Detail x3” 83 3 2.675 0.646 6. Investment

attractiveness Case B “Tax Detail” 43 4 3.884 1.483 0.348 Case C “Tax Detail x3” 83 4 4.169 1.496

7. Tax burden Case B “Tax Detail” 43 6 5.837 1.588 0.060* Case C “Tax Detail x3” 83 7 6.373 1.394

Notes: This table reports the summary statistics on judgment questions on cases B vs C for all participants. p-Values are two-tailed values computed using Wilcoxon/Mann-Whitney U test. Significance: * Two-tailed significance level at 10% level; ** Two-tailed significance level at 5% level; *** Two-tailed significance level at 1% level. a Answers are scaled as follows: Financial condition (1: very good, 9: very poor), Investment risk (1: low risk, 9: high risk), Timeliness of payments (1: very good, 9: very bad), Growth perspective (1: very good, 9: very bad), Profitability (1: decrease, 2: remain, 3: Increase), Investment attractiveness (1: very attractive, 9: very unattractive), Tax burden: (1: very low, 9: very high). b Sd: standard deviation.

40

Table 5. Statistics on judgment questions (cases A vs B and A vs C)

Notes: This table reports the summary statistics on judgment questions on cases A vs B and A vs C for all participants. p-Values are two-tailed values computed using Wilcoxon/Mann-Whitney U tests. Significance: * Two-tailed significance level at 10% level; *** Two-tailed significance level at 1% level. a Answers are scaled as follows: Financial condition (1: very good, 9: very poor), Investment risk (1: low risk, 9: high risk), Timeliness of payments (1: very good, 9: very bad), Growth perspective (1: very good, 9: very bad), Profitability (1: decrease, 2: remain, 3: Increase), Investment attractiveness (1: very attractive, 9: very unattractive), Tax burden: (1: very low, 9: very high). b Sd: standard deviation.

Questionsa Treatment N Median Mean Sdb p-values

1. Financial condition

Case A “Net-of-Tax” 46 3 3.652 1.418 0.611 Case B “Tax Detail” 43 3 3.512 1.316

Case A “Net-of-Tax” 46 3 3.652 1.418 0.917 Case C “Tax Detail x3” 83 3 3.783 1.711

2. Investment risk

Case A “Net-of-Tax” 46 3 3.804 1.327 0.487 Case B “Tax Detail” 43 4 3.907 1.151

Case A “Net-of-Tax” 46 3 3.804 1.327 0.002*** Case C “Tax Detail x3” 83 5 4.759 1.650

3. Timeliness of payments

Case A “Net-of-Tax” 46 3 3.400 1.606 0.953 Case B “Tax Detail” 43 3 3.279 1.469

Case A “Net-of-Tax” 46 3 3.400 1.606 0.060* Case C “Tax Detail x3” 83 4 4.036 1.777

4. Growth perspective

Case A “Net-of-Tax” 44 3 3.477 1.210 0.609 Case B “Tax Detail” 42 3 3.667 1.459

Case A “Net-of-Tax” 44 3 3.477 1.210 0.910 Case C “Tax Detail x3” 83 3 3.667 1.521

5. Profitability

Case A “Net-of-Tax” 44 3 2.614 0.689 0.229 Case B “Tax Detail” 42 3 2.500 0.402

Case A “Net-of-Tax” 44 3 2.614 0.689 0.592 Case C “Tax Detail x3” 83 3 2.675 0.646

6. Investment attractiveness

Case A “Net-of-Tax” 45 3 3.778 1.278 0.752 Case B “Tax Detail” 43 4 3.884 1.483

Case A “Net-of-Tax” 45 3 3.778 1.278 0.156 Case C “Tax Detail x3” 83 4 4.169 1.496

7. Tax burden

Case A “Net-of-Tax” 46 6 5.935 1.421 0.797 Case B “Tax Detail” 43 6 5.837 1.588

Case A “Net-of-Tax” 46 6 5.935 1.421 0.120 Case C “Tax Detail x3” 83 7 6.373 1.394

41

Table 6. Additional analyses of subsamples (case A vs C)

Panel A: Subsamples 1 2 3 4 5 6 7 8 9 10 Practitioners X X X X X X X X X Non-practitioners X X X X Manipulation check passed X X X IFRS experience X X Public accountant or auditor X More than one financial statement under IFRS reviewed in the past 3 years

X X