pre-budget memorandum 2013-2014 - ficcificci.in/.../ficci_pre-budget-memorandum-2013-14.pdf · when...

TRANSCRIPT

PRE-BUDGET MEMORANDUM

2013-2014

PRE-BUDGET MEMORANDUM

2013-2014

I. PREAMBLE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1-4

Implementation of Reports of key Committees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Debate on Inheritance Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Dispute resolution measures . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2

Refunds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Taxation of dividends from overseas. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Import duties . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Service Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Goods and Services Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

Expanding the tax base and dealing with unaccounted monies . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

II. ECONOMIC OVERVIEW AND KEY ISSUES . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5-9

Output and Prices . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Money & Banking. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Public Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Industry . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

External Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

Key Issues and Reforms Needed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

III. SECTORAL ISSUES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10-75

CEMENT . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

TEXTILE AND APPAREL. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

AGRICULTURE AND ALLIED SECTORS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

PAPER INDUSTRY. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

HEALTHCARE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

STEEL AND OTHER FERROUS METALS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

NON-FERROUS METALS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

SOLAR ENERGY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

OIL AND GAS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

C O N T E N T S

(i)

ENVIRONMENT SECTOR . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

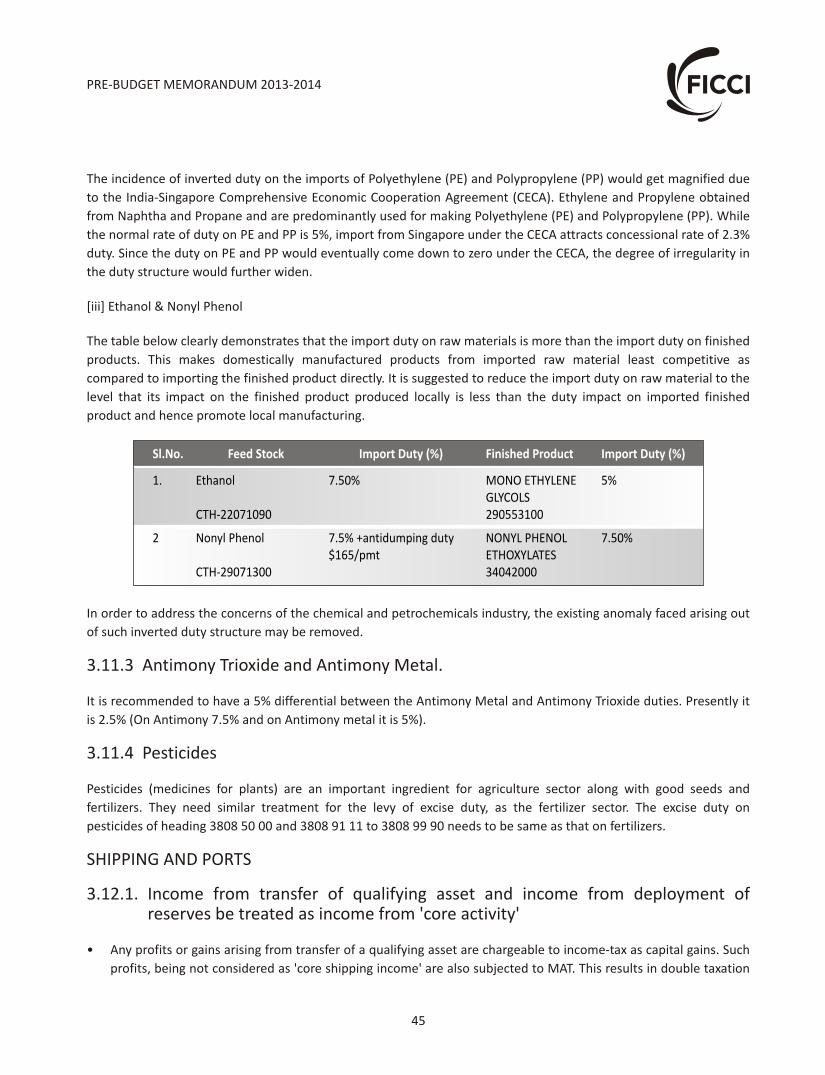

CHEMICALS AND PETROCHEMICALS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

SHIPPING AND PORTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

POWER . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 47

EDUCATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

CIVIL AVIATION . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

VEGETABLE OIL & OIL SEEDS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

INFRASTRUCTURE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

ENTERTAINMENT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

CIGARETTE/TOBACCO INDUSTRY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 59

HOUSING AND REAL ESTATE . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 61

LIFE SCIENCES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

MEDICAL EQUIPMENTS AND DEVICES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

ELECTRONICS HARDWARE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 69

TOURISM. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

RETAIL . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 72

CONSUMER ELECTRONICS. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

CHLOR ALKALI INDUSTRY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 74

IV. DIRECT TAXES. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76-181

Tax Rates - Companies/Firms/Limited Liability Partnership . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

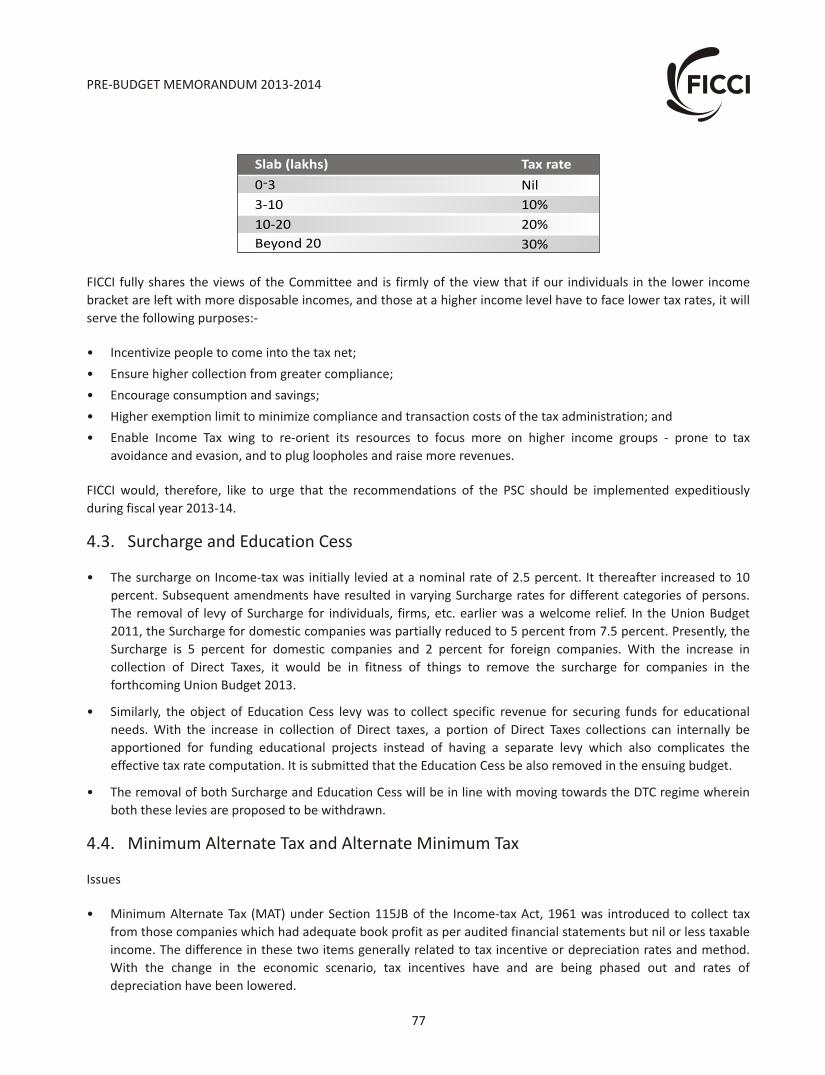

Tax Rates - Individual Taxpayers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

Surcharge and Education Cess . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

Minimum Alternate Tax and Alternate Minimum Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 77

MAT on infrastructure companies. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Dividend Distribution Tax under Section 115-O . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 79

Rationalization of provisions of Section 14A and Rule 8D. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 81

Introduction of Technological Upgradation Allowance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 82

Depreciation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

Disallowance under Section 40(a)(i) and 40(a)(ia) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

Disallowance of cash payments under Section 40A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 84

(ii)

Taking/Repayment of Loans and Deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

Deemed Dividend [Section 2(22)(e)]. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 85

Carry Backward of Business Losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 87

Section 35D - Amortization of certain preliminary expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Non-Resident related issues . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 88

Advance Ruling . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 102

Tax Incentives and benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 106

- Profit Linked Incentives . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 107

- Investment Linked Incentives. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 109

Restoration of exemption of income from investment in infrastructure . . . . . . . . . . . . . . . . . . . . . 112and other projects

Tax Incentives - Weighted deduction under section 35(2AB) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 113

Deduction under section 80JJAA . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 115

Deduction under section 42 for Infructuous or Abortive Exploration Expenses. . . . . . . . . . . . . . . . 116

Deduction for Expenditure on prospecting for certain minerals. . . . . . . . . . . . . . . . . . . . . . . . . . . . 116

Deductibility in respect of subscription to long-term infrastructure bonds . . . . . . . . . . . . . . . . . . . 116

Income tax exemption in case of Sale of Carbon Credits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

Mergers and Acquisitions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 117

Amendment to Section 9(1) - Retrospective insertion of Explanations . . . . . . . . . . . . . . . . . . . . . . 127

Amendment to Section 2(14) and Section 2(47) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 128

Insertion of Section 50D . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Amendment to Section 68 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

Amendment to Section 115JB . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

Capital Gains . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 130

Transfer Pricing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 133

Financial Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 141

Assessment and Procedural Aspects. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 143

Electronic Filing of income-tax returns . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 145

Compulsory filing of income tax return in relation to assets located outside India . . . . . . . . . . . . . 147

Assessment Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 148

Reassessment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 151

(iii)

Time limit for completing income-tax proceedings, where matters are . . . . . . . . . . . . . . . . . . . . . . 151partially set-aside by higher Appellate Authorities

Stay of Demand by the Tribunal . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 152

Refunds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 153

Maintenance of Books of Account in Digital Form . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 154

Personal Tax related aspects . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 155

Calculation of interest for delay in deposit of taxes withheld - meaning of 'month' . . . . . . . . . . . . 163

Interest payable in case of default in furnishing return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 163

Interest for deferment of advance tax under Section 234C of the Act . . . . . . . . . . . . . . . . . . . . . . 164

Deduction in respect of interest on time deposits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 164

Receipt of amount under Life Insurance Policy - Section 10(10D)(d) . . . . . . . . . . . . . . . . . . . . . . . . 165

Monetary Limit for Accounts Audit . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

Relaxation on mandatory requirement of PAN (Section 206AA). . . . . . . . . . . . . . . . . . . . . . . . . . . . 165

Tax Deducted at Source (TDS) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 168

Retrospective Amendments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 171

Amendment in the definition of 'Charitable Purpose' . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 172

Credit in respect of foreign taxes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 175

Modification of Definition of Association of Persons (AOP) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 176

Corporate Social Responsibility costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 178

Deduction for Road Safety Development Programmes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 178

Inclusive Method of accounting - Section 145A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

Enhancement of Limits for TDS under Section 194C for Payment to Contractors . . . . . . . . . . . . . . 179

Wealth Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 179

V. INDIRECT TAXES . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182-247

Service Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

- Exemptions. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 182

- Valuation of Services . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 187

- Place of Provision of Services Rules . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 190

- Reverse Charge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 195

- Miscellaneous . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 197

Central Excise . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 205

(iv)

Customs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 211

Cenvat Credit Scheme . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 220

Structural and Procedural Issues. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230

- Structural Changes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230

- Independence of Adjudication Wing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230

- Improvement in Dispute Resolution Mechanism . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 230

- Expanding the Scope of Authority for Advance Rulings . . . . . . . . . . . . . . . . . . . . . . . . . . 232

- Introduction of Advance Pricing Mechanism in Customs Law in line with . . . . . . . . . . . . 234 Transfer Pricing regulations of Direct Taxes

- Extension of Large Taxpayer Unit (LTU) Scheme . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 234

- Annual Audit of Service Providers by Chartered Accountants. . . . . . . . . . . . . . . . . . . . . . 234

- Common Procedural Issues. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

- Rate of Interest for delayed payment of excise duty or service tax . . . . . . . . . . . . . . . . . 235

- Time limit for disposal of appeals by CESTAT. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 235

- New Benches of CESTAT at Hyderabad, Lucknow, Ranchi etc. . . . . . . . . . . . . . . . . . . . . . . 235

- Expiry of Stay order if appeal is not disposed of within the period of 180 days . . . . . . . . 236

- Issue of multiple notices on same issue for different periods . . . . . . . . . . . . . . . . . . . . . . 236

- Maintenance of scanned copies of documents in lieu of originals . . . . . . . . . . . . . . . . . . 236

- Merger of duties and cesses etc. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 236

- Streamlining of Instructions / Circulars by issue of Annual Master Circulars . . . . . . . . . . 237

- Customs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237

- Period of interest free warehousing of goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 237

- Refund of Extra Duty Deposit in case of provisional assessment . . . . . . . . . . . . . . . . . . . 237

- Finalization of provisional assessments within prescribed time lines . . . . . . . . . . . . . . . . 238

- Bank Guarantees to be returned if the assessee wins first appeal . . . . . . . . . . . . . . . . . . 238

- Refund of excess Customs duty paid in case of amendment to Bill of . . . . . . . . . . . . . . . 238 Entry to rectify clerical mistakes

- Import of Commercial Samples / Prototypes / Critical Spare Parts as Baggage . . . . . . . . 239

- Confirmation of Proof of Export . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 239

- Implementation of the Report of Indian Institute of . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 239 Foreign Trade on Trade Facilitation

(v)

(vi)

- Central Excise . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240

- Demand of interest for differential Excise Duty paid due to price increase . . . . . . . . . . . . . . 240 subsequent to removal of goods

- Availability of Credit on Bill of Entry. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240

- Clearance of goods for captive consumption . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 240

- Valuation of Goods manufactured by job worker for captive . . . . . . . . . . . . . . . . . . . . . . . . . 241 consumption by the manufacturer

- Export of Excisable Goods . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 241

- End Use Certificate for import of waste paper . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 242

- Clarificatory amendment to Rule 8 (3A) of the Central Excise Rules . . . . . . . . . . . . . . . . . . . . 242

- Central Excise valuation - impact of the judgment of the Supreme Court in Fiat case . . . . . . 242

Goods and Services Tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 243

Central Sales Tax . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 244

I. PREAMBLE

1

PRE-BUDGET MEMORANDUM -20142013

The Union Budget to be presented to the Parliament would be in the midst of one of the most challenging times the

world is facing. The USA is dealing with the fiscal cliff, Europe with an all pervasive crisis and the rest of world bracing

for a slowdown. We in India need to come out of the 'perceived policy paralysis' and need to present a Budget which

will continue to inspire investor confidence and help us get back to the 8-9 per cent growth trajectory.

The tax policies that we implement and follow go a long way in impacting foreign investment in the country and are

an integral part thereof. As it happens, some of the recent policy developments have not gone down well with the

investors and have shaken their faith in the efficacy of the judicial system. We at FICCI do believe that the ensuing

Budget offers a platform to communicate to the investing community that we are willing to offer a stable and

consistent tax environment conducive for investment and in conformity with our priorities.

Our detailed memorandum on the various recommendations follows. What we would like to set out in this Preamble

are the key issues which we believe need to be addressed in the forthcoming Budget:

1.1. Implementation of Reports of key Committees

One of the key positive developments in the recent past has been the setting up of the Shome and Rangachary

Committees to address the various concerns that the taxpaying community has. The Draft Reports of the Shome

Committee on GAAR and on retrospective amendment to Section 9 of the Income Tax Act have been received very

positively by the taxpaying community. It is imperative that the final reports of the Shome Committee are placed in

the public domain and, more important, the recommendations acted upon. Similarly, it is imperative that the

recommendations of the Rangachary Committee are placed in the public domain and acted upon. If this is not done

urgently, there is a danger that the deliberations of these Committees will be perceived as one more symbolic

exercise with little result to show.

FICCI would like to endorse several of the recommendations contained in the Draft Reports of the Shome

Committee. In particular, FICCI supports the view of the Committee that GAAR needs to be implemented after

adequate 3 year notice, the existing investments and structures need to be grand fathered and the subjectivity be

taken out of the implementation process. FICCI also endorses the view of the Committee that Retrospective

amendments to tax laws should be a rare phenomenon only to prevent abuse and not to overcome judicial

pronouncements, that where retrospective amendments are made they should not result in withholding tax

obligations, interest and penalty and the need to curtail the implications of amendment to Section 9 of the Income-

tax Act by prescribing threshold limits.

The Rangachary Committee has heard at length the IT/ITES industry and has come up with recommendations on

resolution of several disputes. It has also prescribed Safe Harbour Rules. Apart from implementing these

recommendations, it is necessary to ensure that other industries too find a mechanism of dispute resolution.

1.2. Debate on Inheritance Tax

The recent invitation by the Hon'ble FM to views on the revival of Inheritance Tax has sparked of a major debate.

Coming at a time when there is a need to generate capital resources to invest in developmental needs, any proposal

to introduce Inheritance Tax would be counterproductive.

A substantial portion of the resources generated in the post liberalization era is in listed entities which have helped

the progress of the country. To impose a tax which could potentially require a promoter to dilute his shareholding in

a Company merely to pay incidence of Inheritance Tax is preposterous. Moreover such a tax could be very onerous

for illiquid assets e. g. self occupied housing where the value of the property may have steeply escalated.

When the Estate Duty was in existence, the fact was that the cost of administering the tax was more that the taxes

garnered. In a country where there are few social security measures, imposition of such a tax would indeed be

counterproductive. It will lead to misuse of the provisions and there would be attempts to find loopholes to avoid

payment of such a tax.

Over a period of time, the Government has cast the net of taxes wide and there are several other avenues to

increase the tax base. FICCI strongly opposes any imposition of Inheritance Tax; in any case, even in an extreme case

if such a tax was to be imposed, there is a need for a wider debate including the need to work out the ambit of the

tax, the exemptions, the rates, etc. Such a tax should not, if at all, be imposed in a hurry and without extensive

debate which must necessarily encompass the societal ramifications as these are likely to be significant.

1.3. Dispute resolution measures

One of the key concerns of the taxpaying community is the prolonged litigation, the length of time it takes to resolve

a dispute, the need to make on account payments in the interregnum, etc. The Dispute Resolution Panel (DRP) and

the Mutual Agreement Procedure (MAP) in the context of Direct Taxes have not proved effective mechanisms in this

regard. The fact that multiple benches of ITAT/High Courts give differing decisions has not helped the cause of the

taxpaying community.

FICCI strongly recommends that there be a 'conciliation bench' which can be approached by a tax payer to help

'settle' tax disputes. This will ensure that where a tax payer has already got a favourable resolution of a dispute on a

matter, the dispute is not continued in the later years as a matter of routine. Similarly, non-resident tax payers can

focus on quantum of profits attributable to a Permanent Establishment or the adjustment on a Transfer Pricing issue.

Industry has observed that the assessing officers tend to display a revenue bias in adjudicating tax disputes. This

tendency is pronounced in disputes relating to indirect taxes. There is always pressure of maximizing revenue since

yearly targets for collection of duties are assigned to each such officer. This results in show cause notice/demands

getting confirmed even when the same are legally untenable as is evident from the statistics of appeals decided in

favour of the Department or against it. It is suggested that the adjudicating officers should be disengaged from the

duties of revenue collection. Moreover, revenue realizations dependent as they are on the economic activities should

not be a parameter to assess the efficiency or competence of a revenue officer.

2

PRE-BUDGET MEMORANDUM 2013-2014

1.4. Refunds

Tax payers are indeed concerned about the substantial refunds pending at the tax office on account of both Direct

and Indirect taxes. There is a spiral here because there is a higher withholding tax and most often tax payers are

unable to get lower tax withholding certificates because the Departments within the Tax Office who deal with

withholding tax and those dealing with assessments are different and each have their own separate Budgets. The tax

payer is stuck in between.

Once higher taxes are withheld, there is a need for a refund and one finds, in practice, that tax offices make high

pitched assessments to avoid refunds. We thus get into prolonged litigation and a tax payer has major problems

trying to get back funds which are legitimately his. A new internal instruction that refunds will not be issued if a case

is chosen for scrutiny makes a mockery of the whole system and is outrageous. This spiral needs to be broken. There

is a need to issue instructions or guidance for issue of lower or nil withholding certificates. All pending refunds need

to be granted forthwith, even when a case is chosen for scrutiny assessment.

1.5. Taxation of dividends from overseas

Over the last few years, corporate India has emerged as a fairly active global player and Indian business houses have

made investments and acquisitions which do India proud. The returns from these investments, when brought to

India, suffer tax unlike domestic dividends which are tax free in the hands of the recipients. In the last Budget, the

rate of tax was reduced to 15 per cent. FICCI believes that such dividends received out of tax paid profits overseas

and subjected to withholding taxes in those jurisdictions, should not be subjected to further tax in India on

remittance. Indeed, the US example has shown that when corporates are permitted to repatriate dividends tax free,

there is a significant inflow of funds; inward remittance of forex at this point of time would be a very welcome step

for our economy. FICCI recommends that tax on dividends from overseas be done away with; in the alternative, tax

on such dividends should be treated akin to minimum alternate tax, creditable against the normal tax liability and

payable only if the tax on normal income is less than the tax on such dividends.

1.6. Import duties

Domestic Industry continues to suffer from cost disadvantages on account of higher local taxes such as VAT, octroi,

entry tax as also due to higher cost of financing and inadequate infrastructure. It deserves a minimal level of

protection to compete with imported goods. FICCI would suggest that generally the basic customs duties should

continue at existing levels till such time a comprehensive Goods and Services Tax is introduced and the cost of

financing is reduced to competitive levels.

1.7. Service Tax

A comprehensive service tax based on the concept of a negative list of services has been introduced with effect from

1st July, 2012. It is an important step towards introduction of GST. However, it is noticed that while the levy is

universal in its application (barring the negative list and exemptions); there are restrictions on the availment of

Cenvat credit. This dichotomy needs to be resolved urgently.

Further, several doubts have been expressed about the scope of the new levy. Some of the issues requiring

clarification have been listed in the memorandum. The Ministry of Finance should issue clarifications on these issues

at the earliest to avoid litigation.

3

PRE-BUDGET MEMORANDUM 2013-2014

1.8. Goods and Services Tax

The recent move by the Hon'ble Finance Minister in reviving the move to introduce the GST, sooner rather than later,

is indeed welcome. FICCI indeed has strongly supported introduction of GST and believes that this will go a long way

in streamlining the economy and provide impetus to the growth of our GDP. FICCI believes that it is imperative that

this economic reform which is critical to the growth of the country be not a subject of party politics and should be

pushed forward at the soonest possible.

Also, it is important that the framework of GST should encompass the multiple taxes currently levied at the state and

local levels and should subsume all of them.

1.9. Expanding the tax base and dealing with unaccounted monies

Any system that taxes those who are in the tax net on a progressively higher basis leaving out those who manage to

outside the tax net is regressive and will not achieve the objectives of economic and inclusive growth.

On the subject of funds lying overseas, while being fully sensitive on the Government's rights to appropriately deal

with defaulters, FICCI has strongly recommended that India enters into an agreement with countries like Switzerland

on the lines of similar treaties entered into it by the UK as this will ensure that taxes are collected on such monies,

including future earnings. FICCI would be happy to contribute to this thought process and feels that this move should

not be delayed further.

Finally, on this subject, it is observed that despite persistent efforts in the last few years there is hardly any widening

of the tax base; efforts so far made have yielded dismal results. FICCI sees the need to tax all the sectors which are

presently outside the scope of the tax net albeit at much higher levels of income/wealth. There is no economic

justification to not tax persons who have income above the threshold of maximum marginal rates payable by other

tax payers. Changes needed to the Constitution of India in this regard should be initiated and a debate on this subject

needs to take place.

4

PRE-BUDGET MEMORANDUM 2013-2014

II. ECONOMIC OVERVIEW AND KEY ISSUES

5

PRE-BUDGET MEMORANDUM -20142013

Economic Overview

2.1. Output and Prices

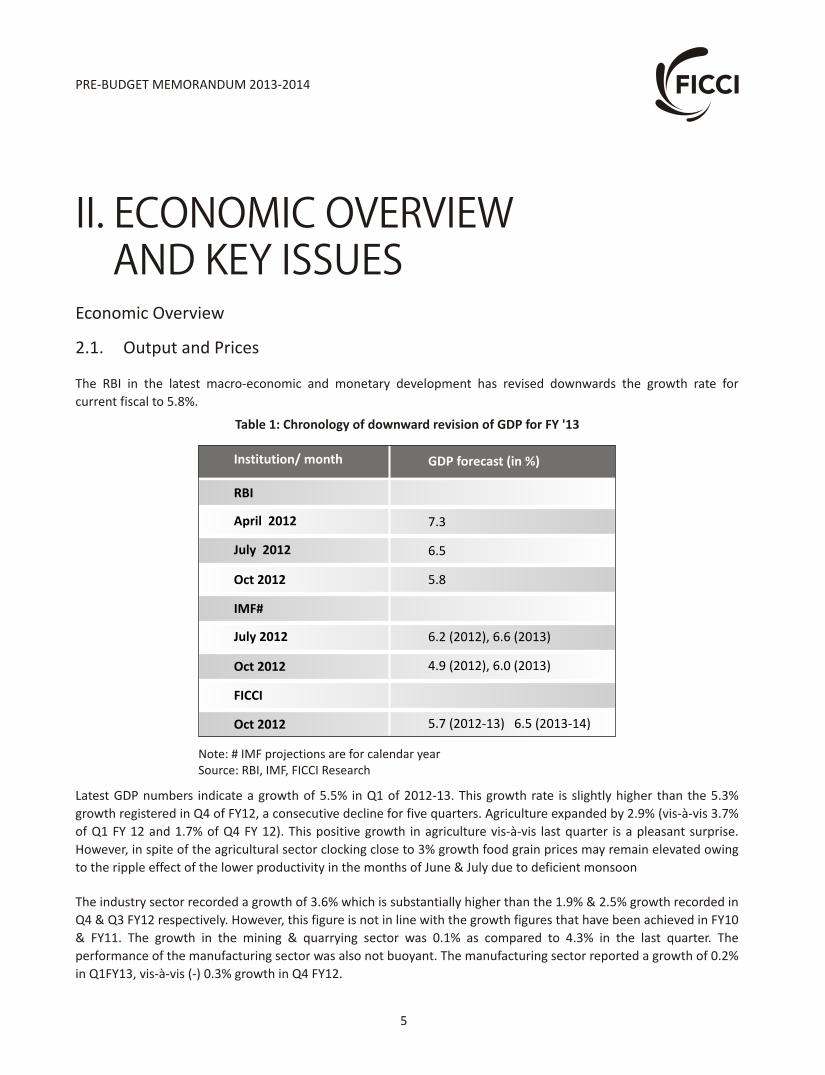

The RBI in the latest macro-economic and monetary development has revised downwards the growth rate for

current fiscal to 5.8%.

Table 1: Chronology of downward revision of GDP for FY '13

Latest GDP numbers indicate a growth of 5.5% in Q1 of 2012-13. This growth rate is slightly higher than the 5.3%

growth registered in Q4 of FY12, a consecutive decline for five quarters. Agriculture expanded by 2.9% (vis-à-vis 3.7%

of Q1 FY 12 and 1.7% of Q4 FY 12). This positive growth in agriculture vis-à-vis last quarter is a pleasant surprise.

However, in spite of the agricultural sector clocking close to 3% growth food grain prices may remain elevated owing

to the ripple effect of the lower productivity in the months of June & July due to deficient monsoon

The industry sector recorded a growth of 3.6% which is substantially higher than the 1.9% & 2.5% growth recorded in

Q4 & Q3 FY12 respectively. However, this figure is not in line with the growth figures that have been achieved in FY10

& FY11. The growth in the mining & quarrying sector was 0.1% as compared to 4.3% in the last quarter. The

performance of the manufacturing sector was also not buoyant. The manufacturing sector reported a growth of 0.2%

in Q1FY13, vis-à-vis (-) 0.3% growth in Q4 FY12.

Institution/ month GDP forecast (in %)

RBI

April 2012

July 2012

Oct 2012

IMF#

July 2012

Oct 2012

FICCI

Oct 2012

7.3

6.5

5.8

6.2 (2012), 6.6 (2013)

4.9 (2012), 6.0 (2013)

5.7 (2012-13) 6.5 (2013-14)

Note: # IMF projections are for calendar yearSource: RBI, IMF, FICCI Research

The construction sector recorded a growth of 10.9% in the first quarter as compared to 4.8% in Q4 FY 12. The sector

has not recorded such a high growth ever since Q2 FY08. This year's good performance could be due to delayed

monsoon which otherwise affects construction activity. Cement dispatch numbers for the quarter have been fairly

decent and may be the delay in the monsoons this year has lent some support to the cement companies.

However, the worrying point was the growth rate in service sector at a low of 6.9% as compared to 10.2% in Q1 FY

12. At a disaggregated level, it was the trade, hotels & restaurants sector which dragged the services growth down.

The trade, hotels & restaurants sector recorded an all-time low growth of 4% in Q1FY13 as compared to 7% in the

last quarter and close to 14% in Q1 FY 12.

Headline inflation came in at 7.81% year on year (YoY) in Sep'12, sharply higher than previous month's print of 7.55%

YoY. The inflation print for the month of September came in at a 10-month high. The July number was revised

upward to 7.52% YoY from provisional estimate of 6.87% YoY.

Primary inflation eased to 8.77% YoY in Sep'12 from 10.4% YoY in July with food price inflation at 7.9% YoY. Within

food, the structural components of inflation in protein rich items witnessed a sharp spike compared to the previous

month. Prices for cereals jumped 14.2% YoY in Sep'12 from 10.7% YoY respectively in August. This can be mainly

owed to the spike in wheat inflation to18.6% YoY from a prior of 12.9% YoY. Meanwhile, the decline in fruits and

vegetables prices by 3.37% month on month (MoM) helped limit the monthly rise in food inflation levels.

Fuel inflation rose sharply to 11.9% YoY from 8.3% YoY, owing to a partial impact of the 13.6% hike in high speed

diesel prices in the month. The fuel inflation is likely to rise higher in October, as the rest of direct impact coupled

with the indirect impact of hike in diesel prices will be witnessed.

Inflation pressures in the manufacturing sector surged to 6.26% YoY in Sep'12 and core printed 5.57% YoY. Both

indices continue to exhibit an upward momentum.

The Central Bank is facing a sharp growth-inflation conundrum with growth continuing to remain weak, while

inflation is likely to increase in the coming months.

Table 2: Inflation rates as on Sep 2012

FY13

September

All Commodities

Primary Articles

Food Articles

Fuel & Power

Manufactured

1.1

0.5

0.6

0.5

FY12

Month YTD* Year Year

4.6 7.8

6.2 8.8

7.9 7.9

4 5.9 11.9

3.6 6.3

Source: Office of Economic Advisor* Note: YTD Implies year till date (as of Sept'12)

PRE-BUDGET MEMORANDUM -20142013

10.0

12.2

9.6

14

8

6

2.2. Money & Banking

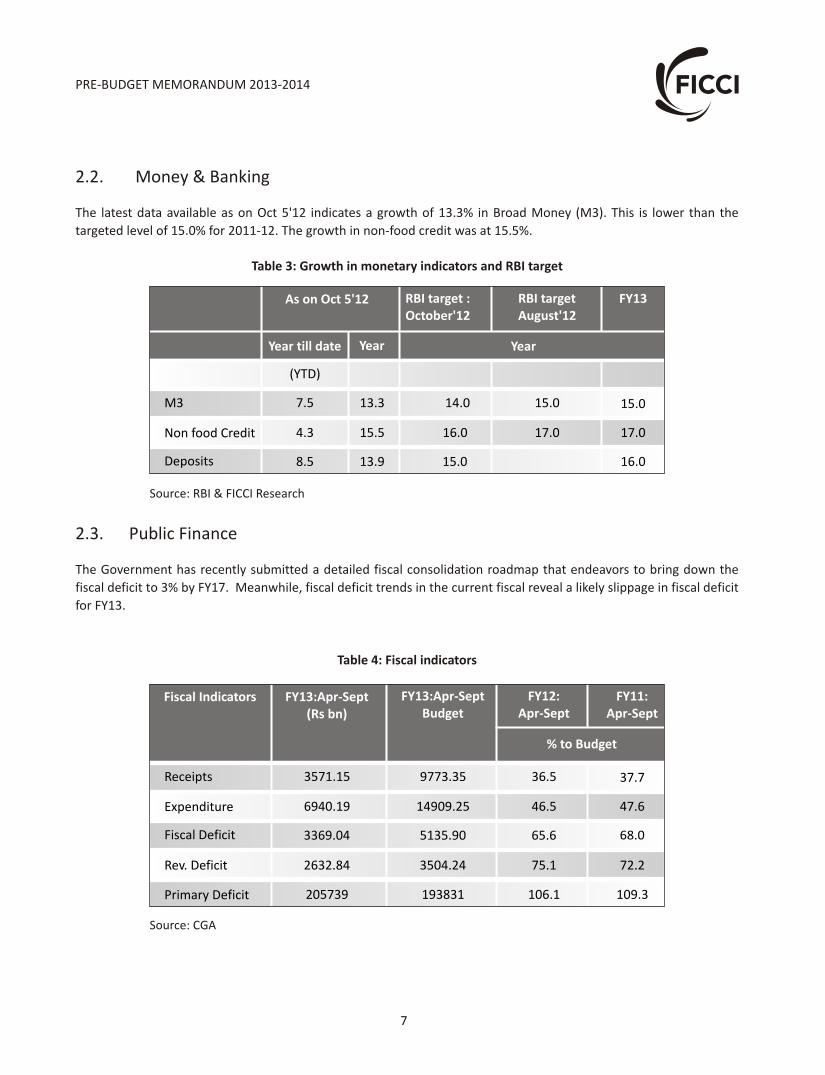

The latest data available as on Oct 5'12 indicates a growth of 13.3% in Broad Money (M3). This is lower than the

targeted level of 15.0% for 2011-12. The growth in non-food credit was at 15.5%.

2.3. Public Finance

The Government has recently submitted a detailed fiscal consolidation roadmap that endeavors to bring down the

fiscal deficit to 3% by FY17. Meanwhile, fiscal deficit trends in the current fiscal reveal a likely slippage in fiscal deficit

for FY13.

Table 3: Growth in monetary indicators and RBI target

As on Oct 5'12

(YTD)

7.5

4.3

8.5

13.3

15.5

RBI target : October'12

14.0 15.0

16.0 17.0

13.9 15.0 16.0

Source: RBI & FICCI Research

RBI target August'12

FY13

Year till date Year Year

15.0

17.0

M3

Non food Credit

Deposits

Table 4: Fiscal indicators

FY13:Apr-Sept(Rs bn)

3571.15

3369.04

6940.19

FY13:Apr-SeptBudget

9773.35 37.7

14909.25 47.6

5135.90 68.0

Source: CGA

FY12:Apr-Sept

FY11:Apr-Sept

36.5

46.5

Receipts

Expenditure

Fiscal Deficit

Fiscal Indicators

% to Budget

Rev. Deficit

Primary Deficit

2632.84

205739

3504.24

193831

65.6

75.1

106.1

72.2

109.3

PRE-BUDGET MEMORANDUM -20142013

7

2.4. Industry

The IIP print for the month of August was a positive surprise and came in at 2.7% YoY. On the manufacturing PMI

front, the performance has been stable at 52.8 for August as well as September.

The performance on a segmental basis was more encouraging for manufacturing and mining. Mining growth

improved to 2% YoY in August as against -1.6% YoY earlier. However, for the April-August period it continues to

remain in the negative territory at -0.6% YoY. Manufacturing clocked 2.9% YoY in August whereas during Apr-Aug it

has been 0% YoY.

As per the two-industry classification, 13 out of the 22 industry groups displayed positive growth among which were

publishing, printing and radio, TV and communication equipment.

Industries such as office, accounting and computing machinery and motor vehicles and other transport equipment

demonstrated negative growth.

Further, components such as capital goods have started to show reduced volatility and declined by 1.7% YoY as

against the lows of -28.1% YoY seen in June. For April-August capital goods continues to show contraction of -13.8%

YoY. The positive surprise however, ensued from the consumer goods front, which grew by 5% YoY as against 0.5%

YoY earlier. April-August, consumer goods clocked 3.5% YoY.

Table 5: IIP Growth Trend: Apr- Aug'12

Basic

7.6

2.8

Capital

7.3 4.4

-13.8 3.5

Source: MoSPI

Intermediate Consumer

0.8

0.6

Apr- Aug '11

Apr- Aug '12

Period General

5.6

0.4

2.5. External Sector

Cumulative trade deficit for FY2013 (April-August) now stands at $71.3 bn as against $76 bn in the same period last

year. Cumulative exports for FY2013 (April-August) now stand at $119 bn - a decline of 6.6% over the corresponding

period last year. Cumulative imports for FY2013 (April-August) now stand at $190 bn - a decline of 6.6% over the

corresponding period last year.

Nevertheless, exports trajectory is expected to improve slightly going ahead owing to the lagged impact of the sharp

Rupee depreciation against the major trading partners in early part of FY2013.

However on the downside, on the imports side, the rise in international crude oil prices in the August-September

period is expected to be reflected in incoming trade data and thereby poses upside risks to quantum of India's trade

deficit.

PRE-BUDGET MEMORANDUM -20142013

8

PRE-BUDGET MEMORANDUM -20142013

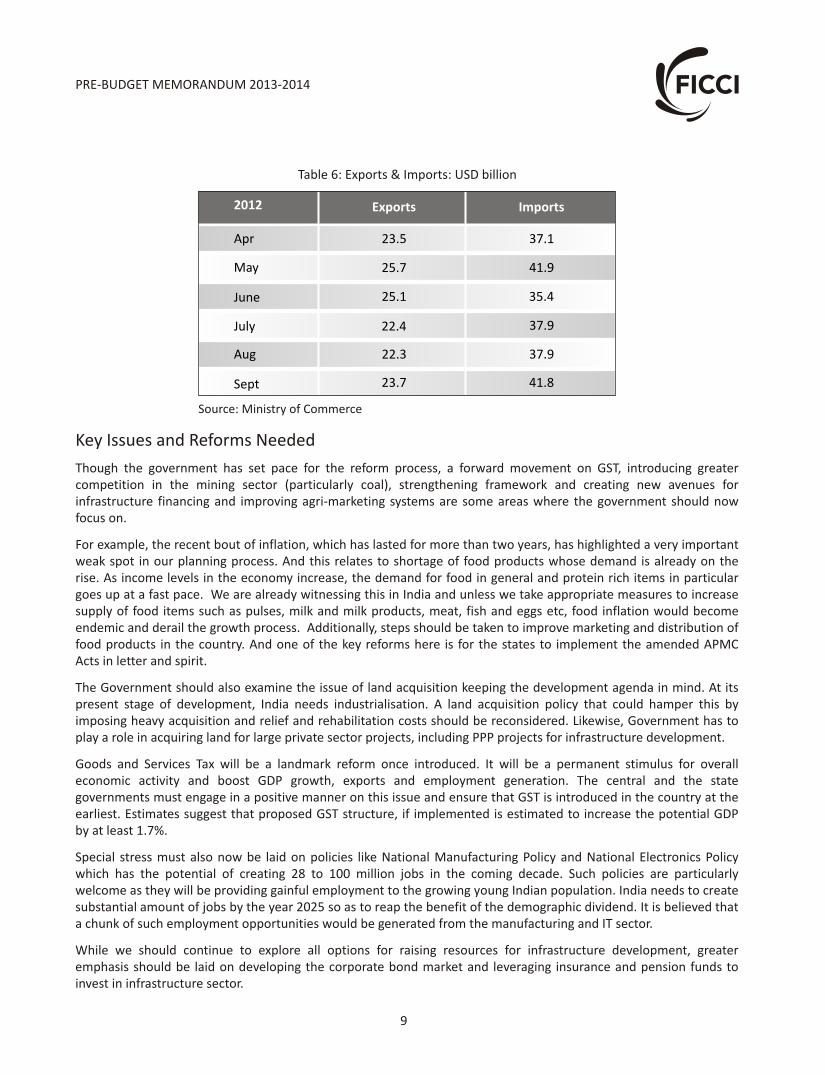

Table 6: Exports & Imports: USD billion

2012 Exports

Apr

May

June

July

Aug

Sept

23.5

25.7

25.1

23.7

Source: Ministry of Commerce

Imports

41.9

35.4

37.9

41.8

22.4

22.3

37.1

37.9

Key Issues and Reforms Needed

Though the government has set pace for the reform process, a forward movement on GST, introducing greater competition in the mining sector (particularly coal), strengthening framework and creating new avenues for infrastructure financing and improving agri-marketing systems are some areas where the government should now focus on.

For example, the recent bout of inflation, which has lasted for more than two years, has highlighted a very important weak spot in our planning process. And this relates to shortage of food products whose demand is already on the rise. As income levels in the economy increase, the demand for food in general and protein rich items in particular goes up at a fast pace. We are already witnessing this in India and unless we take appropriate measures to increase supply of food items such as pulses, milk and milk products, meat, fish and eggs etc, food inflation would become endemic and derail the growth process. Additionally, steps should be taken to improve marketing and distribution of food products in the country. And one of the key reforms here is for the states to implement the amended APMC Acts in letter and spirit.

The Government should also examine the issue of land acquisition keeping the development agenda in mind. At its present stage of development, India needs industrialisation. A land acquisition policy that could hamper this by imposing heavy acquisition and relief and rehabilitation costs should be reconsidered. Likewise, Government has to play a role in acquiring land for large private sector projects, including PPP projects for infrastructure development.

Goods and Services Tax will be a landmark reform once introduced. It will be a permanent stimulus for overall economic activity and boost GDP growth, exports and employment generation. The central and the state governments must engage in a positive manner on this issue and ensure that GST is introduced in the country at the earliest. Estimates suggest that proposed GST structure, if implemented is estimated to increase the potential GDP by at least 1.7%.

Special stress must also now be laid on policies like National Manufacturing Policy and National Electronics Policy which has the potential of creating 28 to 100 million jobs in the coming decade. Such policies are particularly welcome as they will be providing gainful employment to the growing young Indian population. India needs to create substantial amount of jobs by the year 2025 so as to reap the benefit of the demographic dividend. It is believed that a chunk of such employment opportunities would be generated from the manufacturing and IT sector.

While we should continue to explore all options for raising resources for infrastructure development, greater emphasis should be laid on developing the corporate bond market and leveraging insurance and pension funds to invest in infrastructure sector.

9

10

CEMENT

3.1.1. Reduction in the rate of excise duty on Cement

Excise duty is levied on Cement @12% + Rs.120 per MT. These duty rates are one of the highest and other core

industries such as coal and steel attract duty at around 5%. Cement is one of the core infrastructure industries and it

requires large scale investments and capacity additions in view of the expected GDP growth and projected demand

for cement over the medium to long term.

Further, the excise duty structure for both cement as well as cement clinker has become quite complicated in the last

few years. Earlier it was at a specific rate per MT. Now, it has become ad-valorem cum specific duty and is further

also related to the declared MRP of the product.

There is surplus capacity of cement in the country and cement market is on a bearish trend. Therefore excise duty

rate on cement should be significantly reduced for growth of the industry at par with other core and infrastructure

industries.

3.1.2. Levy of Clean Energy Cess on Coal

A clean energy cess has been levied on coal, peat and lignite with effect from 1.7.2010. Energy is one of the major

cost drivers for cement. Though levied as a duty of excise, no cenvat credit is being allowed against this levy. This

cess, along with state VAT etc. is putting further pressure on an industry faced with surplus capacity, falling

realizations and increasing costs.

It is requested that Cenvat credit be allowed on Clean Energy Cess so as to mitigate the impact on costs.

3.1.3. Classifying Cement as “Declared Goods”

Cement is one of the basic and core infrastructure industries. However, unlike other similar industries/goods, cement

is subject to higher rates of taxation. It is requested that Cement be stipulated as “Declared Goods” under Section 14

of Central Sales Tax Act so that it is put on an equal footing with other core sector goods like coal and steel.

3.1.4. Levy of Customs Duty on Cement Imports

Presently, import of cement into India is freely allowed without paying basic customs duty. However, all the major

inputs for manufacturing cement such as limestone, gypsum, pet coke, packing bags etc. attract customs duty. In this

situation, duty free import causes further hardships to the Indian cement industry.

Hence, it is requested that to provide a level playing field, basic customs duty be levied on cement imports into India.

III. SECTORAL ISSUES

PRE-BUDGET MEMORANDUM -20142013

Alternatively, import duties on goods required for manufacture of cement be abolished and freely allowed without

levy of duty.

3.1.5. Reduction of Customs Duty on Imports under EPCG scheme

The EPCG is meant to encourage exports. Hence, the scheme allows import of capital goods at concessional duty rate

of 3% and export obligation is also attached along with it. Now the normal customs duty is in the range of 5-7.5%

unlike 15-20% earlier. Recognizing this, the Government has already reduced duty to 0% for certain sectors. It is

suggested that this concession should be extended to cement industry as well.

3.1.6. Abolition of import duty on tyre chips

Cement industry is an energy intensive industry and requires huge amounts of energy resources. However, it does

not get adequate supplies of domestic coal and hence has to resort to expensive imported coal. To meet its

requirements, the industry is developing alternative energy sources like tyre chips etc.

It is suggested that tyre chips be allowed to be imported by removing it from the Negative list. Further, the import

duty on the same be reduced to zero.

3.1.7. Customs Duty on Pet Coke

Pet coke is one of the important fuels used by Cement Industry. This is expensive and mostly imported and the

situation is further compounded by the fact that the import duty on pet coke is 5%, whereas on final product

'Cement' there is no basic customs duty.

The Cement Industry, therefore, requests that Customs Duty on pet coke be abolished. This would remove the

aberration in the structure of duties existing in cement imports vis-à-vis its inputs.

3.1.8. Treatment of Waste Heat Recovery as Renewable Energy Source

Energy cost is a very substantial part of the cost of producing cement. The prices of conventional energy resources

are rising higher and higher and further, greater use of these is adversely affecting the environment. Also, various

Governments are imposing renewable energy obligations on the industry.

Cement industry is putting up Waste Heat Recovery plants so as to derive more energy from the same energy

resource. In a way, this is akin to green energy. All of this requires further capital investments.

To help the industry in its endeavor to produce more such environment friendly energy, it is requested that such

energy generation be treated as Renewable Energy Source.

3.1.9. Incentives for Limestone availability for future growth

As per IBM data the total cement grade limestone reserve available to meet the industry requirements is 89.86

billion tonnes. Based on the expected growth and consumption pattern, the current reserves are expected to last

only for another 35 - 41 years. There is a need to streamline and simplify the procedures related to limestone mining

leases approval / renewal.

11

PRE-BUDGET MEMORANDUM 2013-2014

There is a need to provide incentives like lower royalty rate, excise rebate for usage of marginal and low grade

limestone.

In order to ensure systematic mining operation for better recovery, there is need to integrate small mining leases in a

limestone belt.

In order to encourage utilization of limestone deposits located in remote areas, there is a need to offer incentives like

road freight subsidy, lower royalty/excise rates etc. It is to be ensured that the systematic mining is carried out as per

approved mining plan.

3.1.10. Stimulus to the sectors which are major users of Cement

Using cement concrete technology for roads - All new expansions in the national and state highways may be made of

cement concrete as a policy. To begin with, this % could be 30% of total allocations. All existing city roads having

bitumen surface be converted gradually to cement concrete and new ones should preferably be constructed with

cement concrete technology. All connecting roads in villages must be done with cement concrete technology.

TEXTILE AND APPAREL

3.2.1. Indian Textile Industry

The Indian Textiles & Clothing industry has an overwhelming presence in the economic life of the country. It

contributes about 14% to industrial production, 4% to the GDP, and 17% to the country's export earnings. It also

provides direct employment to over 35 million persons which is second only after agriculture. India's total textile and

apparel industry size (domestic + exports) is estimated to be $ 89 billion in 2011 and is projected to grow at a CAGR

of 9.5% to reach $ 223 billion by 2021. The domestic textile and apparel market in India is worth $ 58 billion and has

the potential to grow at a CAGR of 9%, to reach $ 141 billion by 2021.

3.2.2. Challenges to the Textile Industry and National Fibre Policy

• The present demand of the industry is collectively met by 8 million tons of different fibres in India. It is envisaged

that fibre demand will reach 11.5 million tons by 2015, thereby necessitating an incremental production of 3.5

million tons.

• The two major category or fibres are cotton and man-made. The current ratio of consumption being 60:40.

• As per the draft National Fibre Policy (NFP) 2010-11, we need to harness the potential of Man Made Fibres to

catalyse the growth of the textile industry, as globally the fibre ratio is 60% man-made to the total fibre

consumption.

• Also, the evolving trends in the textile industry have created huge potential for technical textile, used primarily

for specialty applications. Due to wide functional diversity, the growth in this segment would be met by man-

made fibres.

12

PRE-BUDGET MEMORANDUM 2013-2014

•

dismantling of textile quotas (2005), whereas the cotton textile industry has witnessed substantial growth.

Indian cotton apparel exports to the world have grown at about 10.7% CAGR, while MMF apparel exports have

witnessed a decline.

• One major impediment in India is disparity of excise duty that the man-made fibre chain is subjected to.

• There have been genuine and forceful attempts by the Government towards realizing fibre neutrality when the

excise duty in 2008-09 was reduced to 4% to spur growth of the T&C industry, when the global industry faced

the economic downturn.

• But in subsequent years, there were gradual increases in excise duty from 4% to present rate of 12%.

Following suggestions may be considered by the Government for the balanced growth of the Indian Textile industry:-

3.2.3. Excise Duty on Man-made Fibres

The excise duty on polyester fibers and yarns has been raised from time to time for the last about 4 years from a

level of 4% in December 2008 to 12% in March 2012. Higher duty on synthetics results in costlier fabrics and

consequently suppresses the demand for garments using polyester fiber and yarns. A higher duty on synthetics not

only acts against the fiber neutral policy of the Government but also impacts the export of value added garments.

In order to reduce the price of synthetic fabrics and to improve the capacity utilization of the fiber/yarn

manufacturers it is requested that the duty structure on fiber and yarns be revisited and duties on polyester fibers /

filament yarn should be brought down to 4%. Such a reduction in duty would help not only the polyester yarn / fiber

manufacturers but also the texturizers, weavers, knitting industry, processors and apparel manufacturers.

A reduction in excise duty as suggested is not likely to affect the revenue collections because of increased volumes of

man-made fibres and yarns

3.2.4. Accumulation of Cenvat Credit

The draw texturized yarn was exempted from the levy of NCCD with effect from 17-05-2003, however, the duty on

the inputs namely POY, for such yarn was continued which has resulted in accumulation of NCCD credit with the DTY

manufacturers. The accumulated credit of manufacturing units needs to be reimbursed back to the units who have

paid this, alternatively same to be credited to Basic Excise duty account of assesses under excise rules.

Indian man-made fibres textile industry has not been able to create a mark in the global textiles market post

13

PRE-BUDGET MEMORANDUM 2013-2014

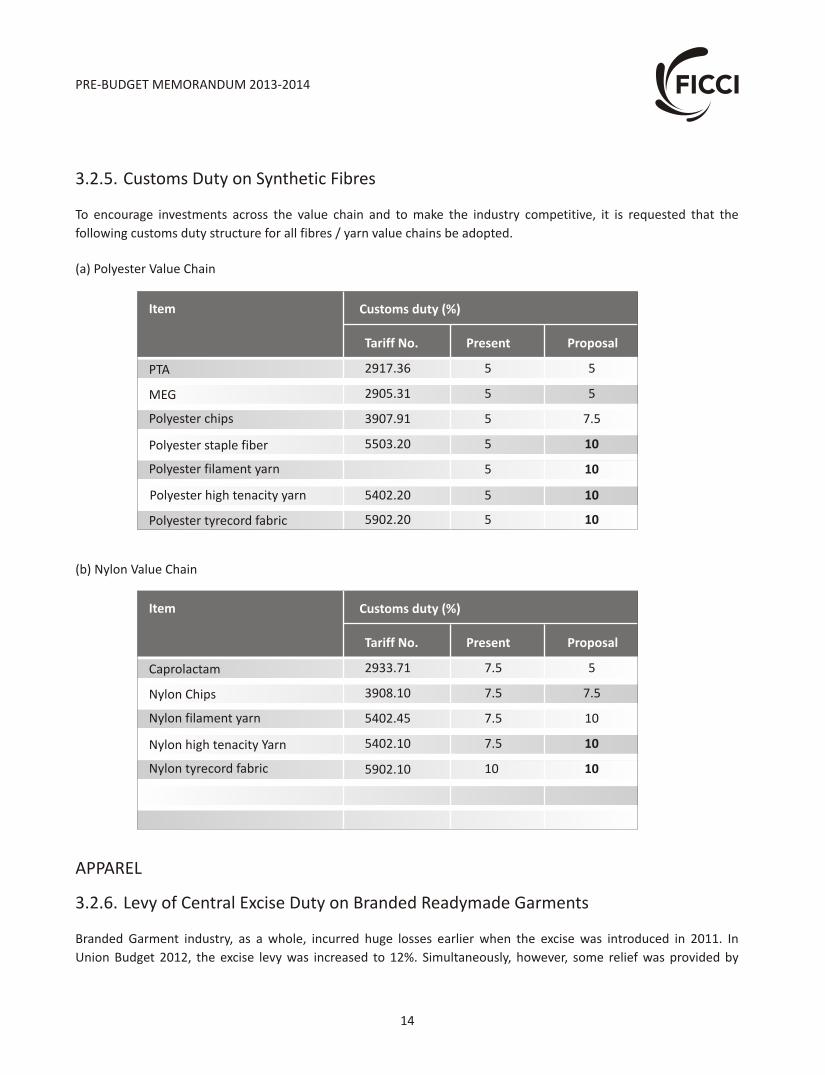

3.2.5. Customs Duty on Synthetic Fibres

To encourage investments across the value chain and to make the industry competitive, it is requested that the

following customs duty structure for all fibres / yarn value chains be adopted.

APPAREL

3.2.6. Levy of Central Excise Duty on Branded Readymade Garments

Branded Garment industry, as a whole, incurred huge losses earlier when the excise was introduced in 2011. In

Union Budget 2012, the excise levy was increased to 12%. Simultaneously, however, some relief was provided by

14

PRE-BUDGET MEMORANDUM 2013-2014

Item Customs duty (%)

Tariff No. Present

PTA 2917.36 5

MEG 2905.31 5

Polyester chips 3907.91 5

Polyester staple fiber 5503.20 5

Polyester filament yarn 5

Polyester tyrecord fabric 5902.20 5

Polyester high tenacity yarn 5402.20 5

Proposal

5

5

7.5

10

10

10

10

(b) Nylon Value Chain

Item Customs duty (%)

Tariff No. Present

Caprolactam 2933.71 7.5

Nylon Chips 3908.10 7.5

Nylon filament yarn 5402.45 7.5

Nylon high tenacity Yarn 5402.10 7.5

Nylon tyrecord fabric 10

Proposal

5

7.5

10

10

105902.10

(a) Polyester Value Chain

increasing the abatement from 55% to 70%. The increase in abatement, while being a very welcome step, is not,

unfortunately, enough to mitigate the severe cost pressure under which the industry is operating. The slowdown in

the economy with consequential impact on consumer sentiment has resulted in sluggish demand. Most of the

branded garment businesses are incurring losses or earn marginal profits due to high incidence of retail costs,

marketing expenses, VAT, freight and octroi. The Branded Garment Industry provides employment to lakhs of semi-

skilled women in manufacturing garments in the country. The fall in demand will have an adverse impact on the

employment of these workers from economically backward class who have very limited scope of employability

otherwise. In view of the issues stated above, it is strongly urged that the abatement provided for branded garments

be increased from 70% to 85%. Alternately, excise duty at 1% may be levied without any entitlement for abatement,

in line with similar levy imposed on about 130 items, which were exempt from central excise duty till then, in the

Union Budget of 2011. This will provide much needed relief to industry and go a long way in rebuilding the growth

sentiment.

3.2.7. Sample Movement

In garment industry, development, display and approval of samples is an iterative and fundamental activity involving

manufacture and movement of samples across supply chain - from Brand Owner to Vendor/Job worker, washing

units, value add in form of embellishments etc. and then finally from manufacturer/Brand Owner to the Buyers. To

maintain records for these multiple movements is a cumbersome process and there is no commercial transaction

involving consideration.

To facilitate the business process, it is submitted that necessary clarification be issued to consider regular delivery

challan of concerned parties with an endorsement 'For Sample Purpose. No Commercial Value' as proof and samples

be exempt from Excise Duty. Further to prevent misuse of the facility, such garments may be mutilated in the front.

3.2.8. Import of goods falling under Chapters 51, 52, 54, 55, 58 - Testing of Samples

Goods covered by the above stated chapters attract different specific duties at 8 digit HS code level. The difference in

the product description under various sub -classifications cannot be determined or identified by physical inspection

and requires submission of samples for tests by Textile Committee. This results in inordinate delays in clearance of

goods.

It is recommended that the structure of specific duties applicable to the goods covered by the said chapters be

rationalized to reduce the testing requirements. Further, clarifications/instructions may be issued to field formations

to accept test reports of any accredited testing laboratory after matching the sample fabric affixed on the test report

with the import consignment.

3.2.9. Presence of Azo dyes - Certification by international agencies

Textile goods of Chapters 51 to 62 are required to be accompanied by a certificate from a laboratory accredited by

the government of the exporting country confirming that the goods are free from Azo dyes and other harmful

chemicals. If the goods are not accompanied by such certificate, they are subjected to mandatory testing - as

prescribed vide DGFT's Public Notice No. 12 (RE-2001)/1997-2002 - to ensure that the products imported are free

from Azo dyes and other harmful chemicals. This process leads to delay in clearances and resultant additional costs.

15

PRE-BUDGET MEMORANDUM 2013-2014

Internationally, the Institute of the International Association for Research and Testing in the Field of Textile Ecology

accredits mills after carrying out rigorous controls to ensure that they do not use prohibited dyes/chemicals. Once

accredited, the certification remains valid for a specific period and a specific group of products. It is an internationally

accepted practice to accept the accreditations and not insist for consignment wise testing.

It is recommended that the international practice of accepting the accreditation certificate issued by Institute of the

International Association for Research and Testing in the Field of Textile Ecology be adopted in India also.

AGRICULTURE AND ALLIED SECTORS

3.3.1. Background

It is essential that an integrated holistic view of the agriculture value chain is taken towards providing the necessary

fillip to the stagnating agricultural growth. This requires a joint participatory approach from all concerned

stakeholders including the farmers, input vendors, traders, processors and the Government. The Union Budget can

be a very effective catalyst by laying down a comprehensive policy framework and providing a tremendous thrust

through appropriate fiscal benefits and closely monitor action plans.

We believe that an enabling policy framework with attractive fiscal incentives can be provided to attract private

investments in the rural economy. Private investment in agriculture and allied activities can provide the necessary

boost to the already committed Government spends and can have a multiplier effect in the rural economy. The under

noted suggestions and recommendations are being made in the aforesaid context.

3.3.2. Increase Investment in Agriculture and Allied Sectors

In the last budget there was no increase in funding for agriculture research. It is requested that funding to research

institutes like ICAR, state agriculture universities may be increased and a special fund created for fast track

development of high yielding varieties, hybrids and plantlets multiplied through tissue culture and other advanced

technologies under PPP mode. Similarly, a special fund may be created for research and development of high yielding

dairy cattle.

China has come up with a unique scheme where they have given a rebate to companies per unit of

Hybrid/plantlet/min tuber sold domestically for the particular crop that they want to promote. This has encouraged

companies to up production of this type of planting material.

3.3.3. Support Diversification in Captive Fishery through Innovative Financing

In order to realize the unexploited potential in fresh water fish farming, long line shark and tuna fishing, financial

assistance / incentives should be provided under special fund. This financial assistance could be provided through

soft loans, equity, risk covers and insurance, as well as through establishment of integrative farm to fork chains,

information and market intelligence, quality and safety measure.

3.3.4. Weather Stations

Government should announce a separate fund for investing in automatic weather stations in India as the expanded

network would help farmers in mitigating their risk through weather insurance products. Investments in automatic

16

PRE-BUDGET MEMORANDUM 2013-2014

weather stations should be eligible for direct tax incentive in the form of 100% tax holiday in respect of the profits

earned from this segment for a period of 10 years.

3.3.5. Model Farms

Companies be encouraged to set up model farms for farmer training and demonstration. New technologies,

equipment etc should get a 25 % subsidy subject to a maximum of Rs 5 Lakhs per farm and this should be disbursed

after at least 1000 farmers have been trained at the farm

3.3.6. Horticulture

Horticulture today accounts for about 28% of value added in the Agriculture sector and 52% of India's agri-exports

but takes up barely 9% of arable land. The Government has rightly identified the National Horticulture Mission as a

key driver of growth and value addition. This sector is also characterized by high wastages - up to 35% in the case of

certain fruits and vegetables. Large scale investments are required in cold chain infrastructure to minimize waste and

improve farmer realizations.

Cold chain infrastructure is not confined to cold storages only, but extends to temperature handling across the value

chain from farms to consumers. The cold chain thus includes farm level pre-coolers, small capacity chill cold storage,

refrigerated trucks, cold storages, food processing plants, refrigerated display cabinets for retail shops and deep

freezers.

In order to encourage rapid investment and attract foreign direct investment towards minimizing horticultural

wastage and enhancing shelf-life, it is recommended that customs duty rates on cold chain equipment and their

parts be pegged at 5% or below. Similarly, excise duty rates on cold chain equipment and parts need to be lowered to

5% or below to expand domestic manufacture, which is presently in its infancy.

3.3.7. Income Tax for Dairy Cooperatives

Under the prevailing taxation system, while primary dairy cooperatives at the village level are exempt from paying

income tax, the district and state level cooperatives are taxed at the rate of 35 percent. In 2006-07, the Government

reduced the income tax rate for private dairy companies by 10 percent but did not reduce it for cooperatives. In

order to strengthen the co-operative dairy sector, which occupies 18% of the sector the income tax rate for co-

operative sector needs to be brought at par with private dairy companies.

3.3.8. Other fiscal incentives for Cooperatives

Provide fiscal incentives to corporates aiming at increasing crop productivity and developing the entire supply chain

i.e. sorting and grading centres, warehouses, temperature and humidity controlled warehouses, cold storages,

temperature controlled transport up to consumer location. Grant fiscal incentives by way of 100 per cent

depreciation on all investments in physical assets like infrastructure development by the private sector in agriculture

and the entire agri-value chain. They should be given 100% tax holiday in respect of the profits of the undertaking for

a period of at least 10 years and further giving the assessee an option to claim this tax holiday for any 10 consecutive

years out of 15 years.

17

PRE-BUDGET MEMORANDUM 2013-2014

3.3.9. Tax exemption to Electronic Spot Exchanges

Electronic spot exchanges are directly connecting farmers to markets through purchase/sale of agricultural

commodities in the country, thereby, helping in evolving National Common Market by providing a Pan-India

alternative market across the country, for enhancement of farmers' price realization by reducing cost of

intermediation. Such an institutional framework merits Government support for full growth, therefore, the

Government may provide tax exemption to these spot exchanges for a period of 5 years.

3.3.10. Weighted Deduction for Water Harvesting, Conversation etc.

Investments made by companies in water harvesting, water conservation, repair and renovation of water bodies,

interlinking of small canals/river lets should be eligible for 150 per cent weighted deduction on expenditure. The

operation and maintenance of the above activities should also be eligible for similar benefits.

3.3.11. Excise duty exemption for Agricultural Machines

Excise duty and VAT exemption for agricultural machinery and equipments.

3.3.12. Service Tax Exemptions for Agriculture sector

Service tax exemption may be granted to the following services:-

• In terms of Notification No. 25/2012, S.T. dated 20/06/2012 exemption from service tax has been provided, inter-

alia, to services provided by a goods transport agency by way of transportation of fruits, vegetables, eggs, milk,

food grains or pulses in a goods carriage. It is recommended that the scope of exemption be enhanced to include

all agricultural produce including oil seeds, coffee, tea, spices and staples as well as marine products.

• As per extant Service Tax laws the agro-sector has been supported by keeping a bulk of services relating to

agriculture or agricultural produce in the Negative List or in the list of exempted services. However, there are

some services like Security Services, Laboratory Testing Services and so on - which are essential to secure storage

of agricultural produce and to determine quality of the produce - are subjected to Service Tax. It is

recommended that all services provided for agricultural produce be kept outside the ambit of taxable services.

3.3.13. Import Duty Exemption

Import duty exemption may be granted to the following items:-

• Laser Land Leveler and its components such as transmitter

• Machines for cleaning, sorting or grading seed, grain or dried leguminous vegetables

• Harvesting machinery; threshing machinery, root or tuber harvesting machines such as potato diggers and

potato harvesters

• Machines for cleaning, sorting or grading eggs, fruit or other agricultural produce

18

PRE-BUDGET MEMORANDUM 2013-2014

3.3.14. Tea Industry

• FICCI recommends that Indian Tea Industry be given interest subsidy @ 5% on the applicable rate of interest on

the funds specifically borrowed by the Tea Companies earmarked for the activities under the Special Purpose Tea

Fund i.e. replanting and/or rejuvenation etc ('SPTF').

• Tea producers are discouraged to take up developmental activities in their estates whether in field or in factories

due to inadequate subsidy component under the various Schemes of Tea Board. It is, therefore, prayed that the

rate of subsidy should be increased to 40% across the board on all the schemes under the aegis of Tea Board,

Ministry of Commerce (from the existing 25%).

• It is recommended to continue the benefit available under section 33AB of the Act even under the Direct Tax

Code.

• Orthodox Production Subsidy Scheme be included under the ambit of Section 10(30) of the Income Tax Act,

1961.

• FICCI recommends to provide financial incentive to encourage organic tea cultivation.

• Tea Estates are located in the remotest corners of the country and no alternate accommodation is available

locally, the managerial personnel, under force of circumstances, are to be provided with fully furnished

residential accommodation to enable them to attend their routine duties round the clock. It is therefore

suggested that for calculation of perquisites in respect of residential accommodation and for the value of

furniture provided to the employees working in the tea estate, such tea estate should be treated as 'remote

area', like those working at a mining site or an onshore oil exploration site, or a project executive site or an

accommodation provided in an offshore site.

• FICCI suggests that only 40% of the book profit of tea companies should be subjected to MAT. A suitable

modification in section 115JB of Act be made accordingly.

PAPER INDUSTRY

3.4.1. Customs Duty on Paper/Paperboards

The Indian Paper/Paperboard industry has made significant capital investments to ramp up capacities for meeting

domestic requirements. The Industry has strong backward linkages with the farming community, from whom wood,

which is a raw material, is sourced. A large part of this wood is grown in backward marginal/sub-marginal land, which

is potentially unfit for other use. In India an estimated 5 lakh farmers are engaged in growing plantations of

Eucalyptus/Subabul etc, over an estimated 10 lakh hectares. This has generated significant employment

opportunities for the local community and benefits have been reaped from this source, which are higher than other

commercial crops. It is therefore strategically important and also necessary to keep Paper/Paperboard industry

outside the ambit of FTA's (ASEAN etc) and recognize this Industry as “sensitive” deserving special treatment.

Increased imports from foreign countries are severely impacting the cost competitiveness of many paper mills in

India.

In order to provide a level playing field to the domestic industry it is recommended that:

19

PRE-BUDGET MEMORANDUM 2013-2014

(i) the Customs duty for import of Paper and Paperboards should be increased and brought in line with agricultural

products as currently industry is sourcing majority of its raw materials from Agro-forestry - supporting millions of

farmers in creating value on their marginal lands.

(ii) this category to be kept in the Negative List (i.e., no preferential treatment) in bi-lateral and multi-lateral trade

treaties and agreements.

3.4.2. Customs Duty on Import of Pulp

In May 2012 the Government reduced the import duty on pulp from 5% to “Nil”. More than 1,250 thousand MT of

pulp, valued at approximately USD 820 million (about Rs. 4,600 crores) is imported in to the country every year. The

customs duty for these imports is estimated to be about Rs. 230 crores per annum. The break-up of the pulp imports

is as under:

20

Type of Pulp Quantity ('000 MT)

Hard Wood Pulp

900 3,200

Soft Wood Pulp

200 840

Bleached Chemi Thermo Mechanical Pulp (BCTM Pulp) 5402.45 7.5

Total

1,260 4,580

Value (Rs. Crores)

PRE-BUDGET MEMORANDUM 2013-2014

In view of the fact that Soft Wood cannot be grown in the country and in the absence of BCTM technology in India,

requirements of Soft Wood Pulp and BCTM Pulp will have to be met through the import route only. However, in so

far as Hard Wood Pulp is concerned, it would be pertinent to note that the domestic industry is working closely with

the farming community for creating sustainable supply of wood - a key raw material for hard wood pulp - through re-

development of waste-lands.

Cheaper imports of duty free hardwood pulp would not be in the interest of Indian farmers as the benefit will flow to

farmers in exporting countries like Indonesia and Brazil.

Accordingly, for creation of sustainable sources of fibre required by the pulp and paper industry it is recommended

that:

(i) 5% customs duty on pulp be reinstated only for Hard Wood Pulp; and,

(ii) policy measures put in place to facilitate private sector participation in plantation development programmes.

3.4.3. Reduction of Excise Duty on Poly-coated Paper products - Central Excise Tariff No. 4811 59 00

Paper and paperboard that is coated / impregnated / covered with plastic is classified under Central Excise Tariff

4811 59 00 with an excise levy of 10% ad valorem - even as a large number of paper / paperboard items covered by

21

Central Excise Tariff 4802, 4804, 4805, 4807, 4808 and 4810 are exigible to excise duty only at 6% ad valorem.

Plastic coated paper and paperboard are essentially bio-degradable paperboard and are eco-friendly substitutes for

plastics which do not conform to requisite hygiene and environmental standards. The global trend is to actively

discourage the use of plastics and to replace it with plastic coated paper / paperboard.

In India the major consumers of this type of paper / paperboards are SSI / SME units engaged in manufacture of

paper cups that are increasingly being supplied to institutional customers like the Railways, the FMCG sector and the

household sector.