presentación de powerpoint · 20,0 40,0 60,0 80,0 100,0 120,0 2005 2006 2007 2008 2009 2010 2011...

TRANSCRIPT

Asociación Latinoamericana de Exportadores de Servicios

Semana de Smart TalentPrograma Servicios Globales – UruguayXXI

Facultad de Ciencias Económicas de UdelaR

Montevideo – Abril 2016

JAVIER PEÑA CAPOBIANCOSecretario General ALES,Uruguay.@JavierPenaCapob

COFCO Jiangxi Rice Processing Limited (CHINA)

Whenzhen, Jiangxi, China

-

20,0

40,0

60,0

80,0

100,0

120,0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Fixed-telephone subscriptions Mobile-cellular subscriptions

Active mobile-broadband subscriptions Fixed (wired)-broadband subscriptions

Revolución de TIC

Economía del Conocimiento

Source: World Economic Forum, “The Shifting Geography of Global Value Chains: Implications for Developing Countries and Trade Policy”, 2012.

75 - 80% of developed countries

GDP and employment

65% of Latin American countries

GDP

63% of FDI in the OECD

48% of FDI in LAC

60% of Services FDI goes to mid-

high technoogy segments

Service participation in the economy

Services account for the largest share of GDP, FDI and Employment

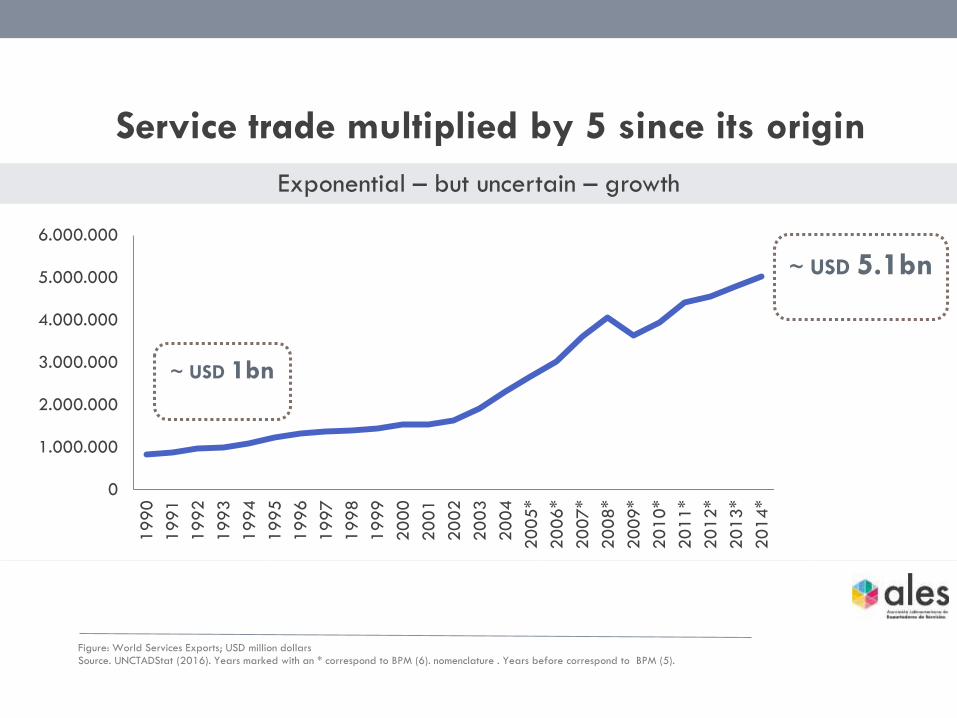

Figure: World Services Exports; USD million dollars

Source. UNCTADStat (2016). Years marked with an * correspond to BPM (6). nomenclature . Years before correspond to BPM (5).

0

1.000.000

2.000.000

3.000.000

4.000.000

5.000.000

6.000.000

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

*

20

06

*

20

07

*

20

08

*

20

09

*

20

10

*

20

11

*

20

12

*

20

13

*

20

14

*

Service trade multiplied by 5 since its origin

Exponential – but uncertain – growth

~ USD 5.1bn

~ USD 1bn

19,50%

-10,70%

4,81%

16,12%

-22,26%

0,77%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Services seem tougher than goods

Higher growth rates, dynamism and more resilient to crisis

Figure: Interannual growth rate of goods and services1990 – 2014; (%)

Source: UNCTADStat (2015).

Goods Services

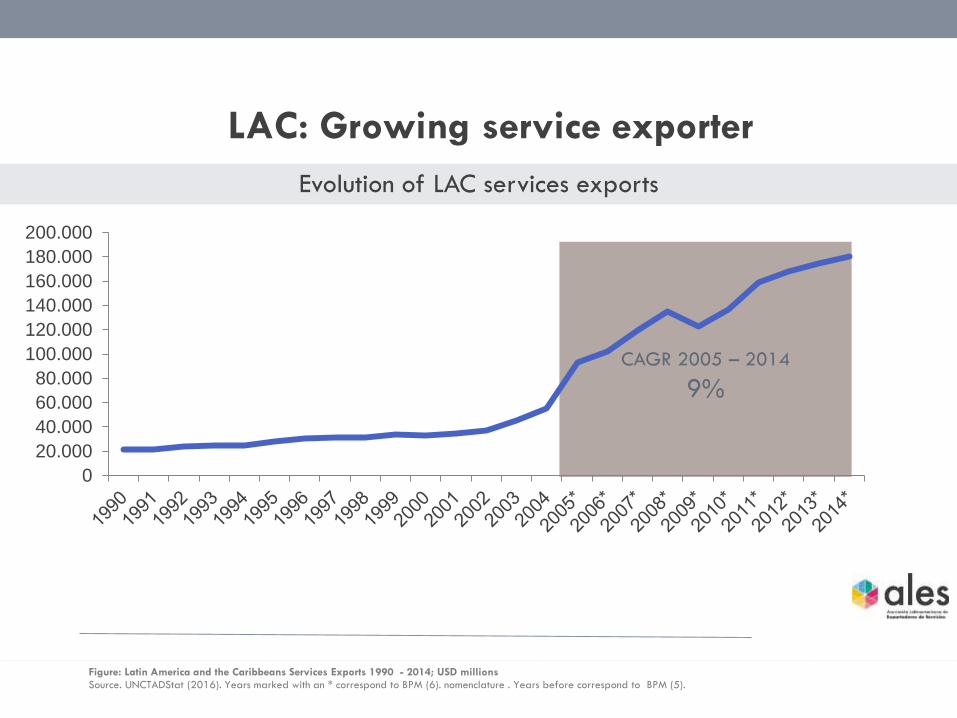

LAC: Growing service exporter

Evolution of LAC services exports

CAGR 2005 – 2014

9%

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

180.000

200.000

Figure: Latin America and the Caribbeans Services Exports 1990 - 2014; USD millions

Source. UNCTADStat (2016). Years marked with an * correspond to BPM (6). nomenclature . Years before correspond to BPM (5).

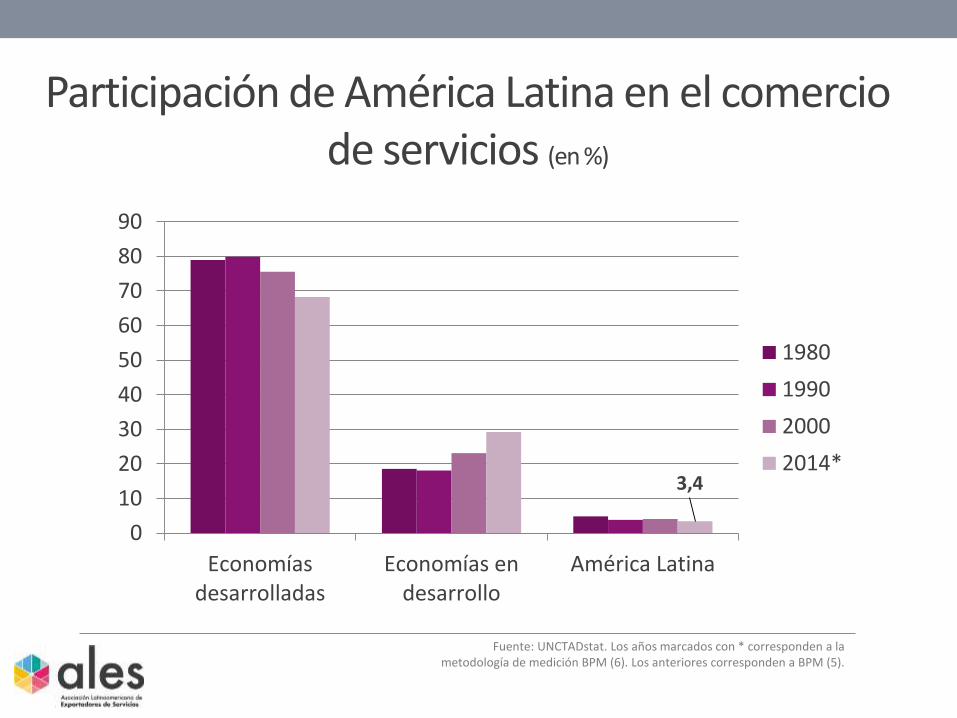

Participación de América Latina en el comercio de servicios (en %)

Fuente: UNCTADstat. Los años marcados con * corresponden a la metodología de medición BPM (6). Los anteriores corresponden a BPM (5).

3,4

0

10

20

30

40

50

60

70

80

90

Economíasdesarrolladas

Economías endesarrollo

América Latina

1980

1990

2000

2014*

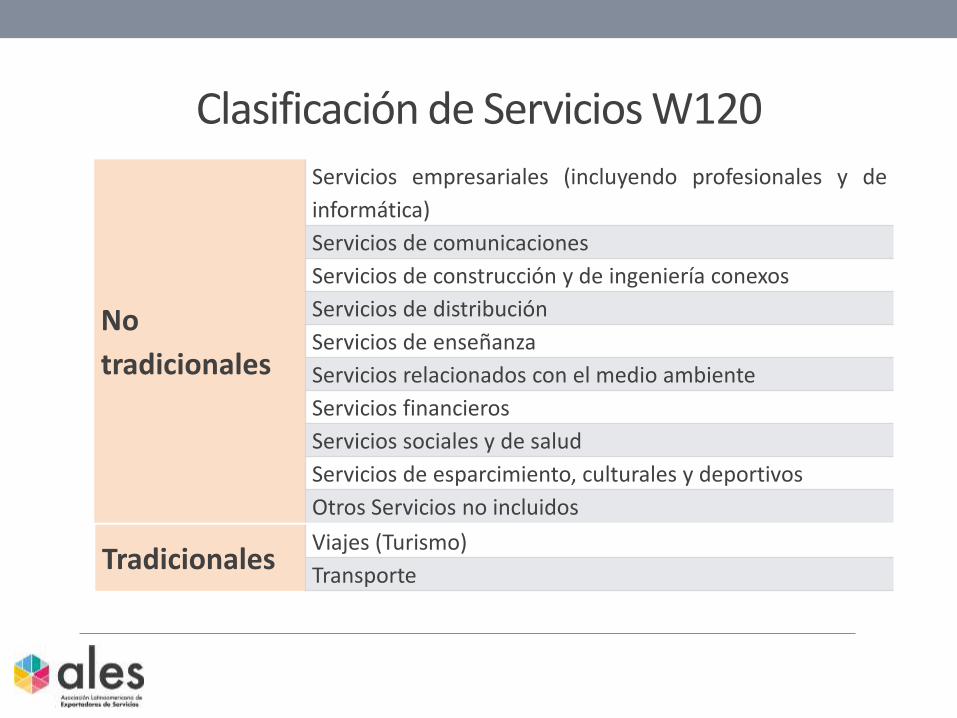

Clasificación de Servicios W120

No

tradicionales

Servicios empresariales (incluyendo profesionales y de

informática)

Servicios de comunicaciones

Servicios de construcción y de ingeniería conexos

Servicios de distribución

Servicios de enseñanza

Servicios relacionados con el medio ambiente

Servicios financieros

Servicios sociales y de salud

Servicios de esparcimiento, culturales y deportivos

Otros Servicios no incluidos

TradicionalesViajes (Turismo)

Transporte

Crecimiento de Servicios No tradicionales Participación en total de exportaciones de servicios por categoría (%)

Fuente: UNCTADstat. Los años seleccionados corresponden a la metodología de medición BPM (6).

21,8 21,9 21,4 21,6 22,5 19,7 20,9 20,4 20,2 19,5 19,0

28,2 25,8 24,8 24,0 23,824,2 24,3 24,3 24,4 24,8 24,7

49,9 48,8 50,2 50,8 50,3 52,7 51,6 52,2 52,0 52,5 53,1

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005* 2006* 2007* 2008* 2009* 2010* 2011* 2012* 2013* 2014*

Transporte Viajes No tradicionales

Tasa de Crecimiento Anual: 10,03%

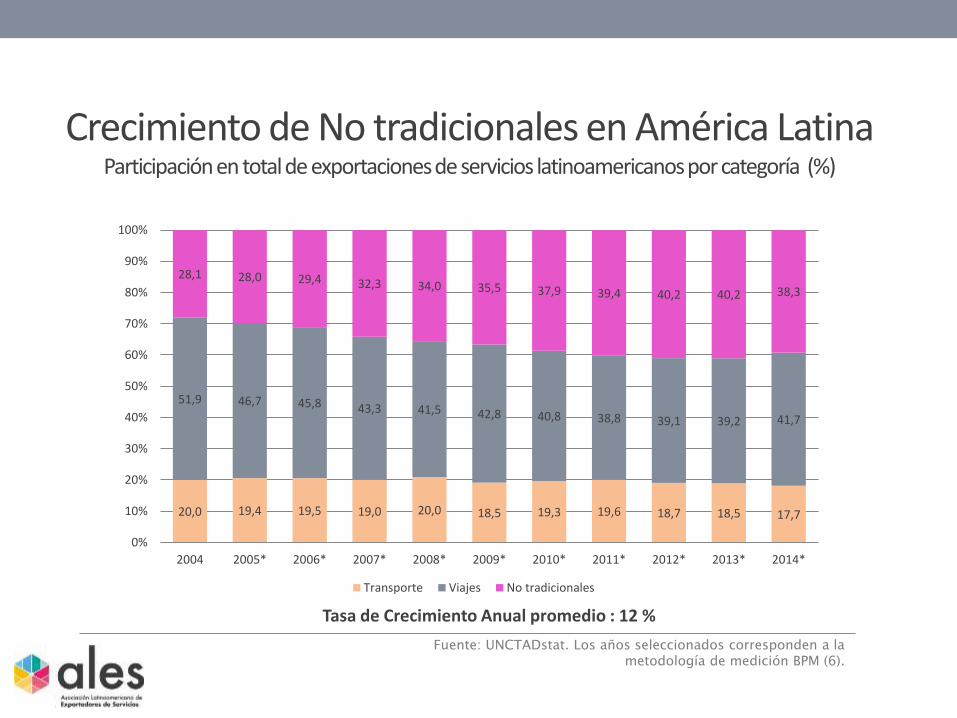

Crecimiento de No tradicionales en América Latina Participación en total de exportaciones de servicios latinoamericanos por categoría (%)

Fuente: UNCTADstat. Los años seleccionados corresponden a la metodología de medición BPM (6).

20,0 19,4 19,5 19,0 20,0 18,5 19,3 19,6 18,7 18,5 17,7

51,9 46,7 45,8 43,3 41,5 42,8 40,8 38,8 39,1 39,2 41,7

28,1 28,0 29,4 32,3 34,0 35,5 37,9 39,4 40,2 40,2 38,3

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2005* 2006* 2007* 2008* 2009* 2010* 2011* 2012* 2013* 2014*

Transporte Viajes No tradicionales

Tasa de Crecimiento Anual promedio : 12 %

Sillicom ValeyCosta Rica

UruguayIndia

En cualquier parte

La decisión de deslocalizar

Tip

o d

e a

ctiv

idad

Cualquier tarea en cualquier momentoKPOITOBPO

Captive Center

Proveedor

Razones para deslocalizar

57%

55%

45%

45%

43%

42%

35%

49%

50%

45%

46%

51%

45%

39%

0% 10% 20% 30% 40% 50% 60%

Mejorar eficiencias

Reducir costos

Asegurar la continuidad del negocio

Acceder a conocimientosespecializados

Concentrarse en el core business

Mitigar riesgos utilizandoespecialistas

Reducir la cantidad de empleados

Global

BRIC

Fuente: Grant Thornton IBR (2014), p.5. Los valores asignados a cada elemento corresponden al porcentaje de empresas que respondió: “Qué tan importantes son los siguientes

elementos en la decision de tercerizar operaciones de back-office?”.

Why considering Latin America?

Nearshore | ‘follow-the-sun’ strategy

The new state of the art

Skills | young, creative and effective

Language capabilities | english, spanish and portuguese

Cultural similarity | us and spain

Cost-effective pricing structure | 40% savings + decline of currency

Complementarity| scalability & specialization

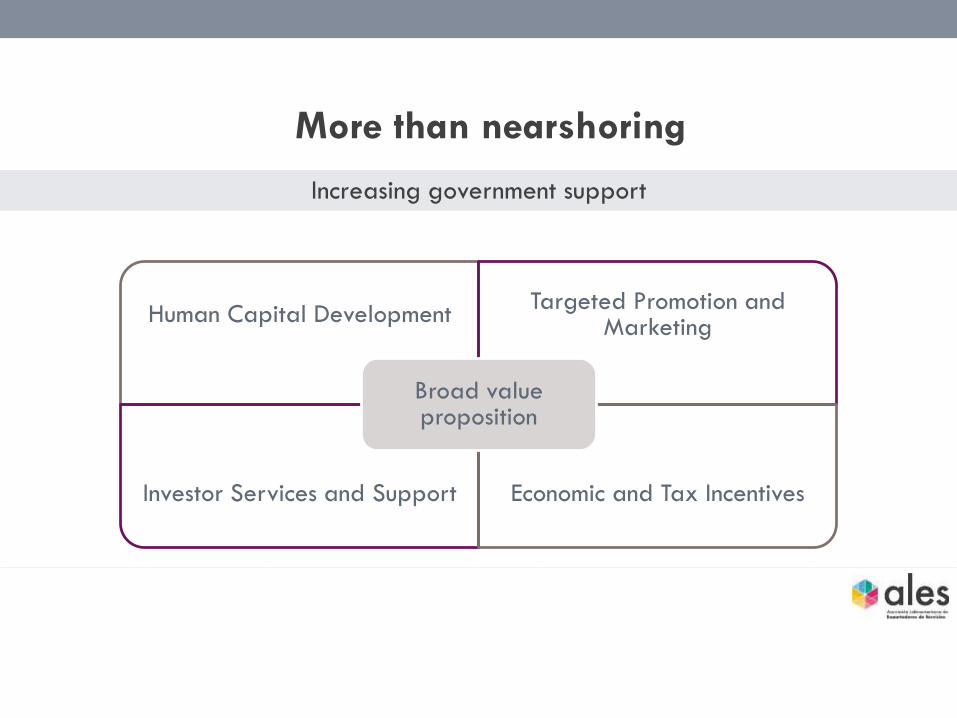

More than nearshoring

Increasing government support

Human Capital DevelopmentTargeted Promotion and

Marketing

Investor Services and Support Economic and Tax Incentives

Broad value proposition

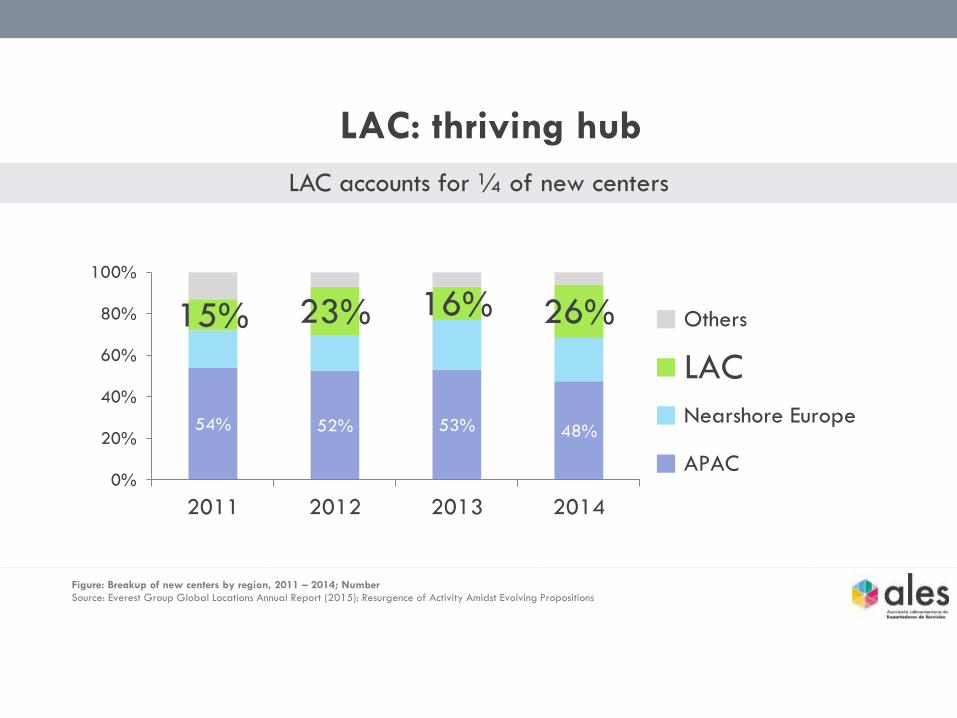

LAC accounts for ¼ of new centers

54% 52% 53% 48%

15% 23% 16% 26%

0%

20%

40%

60%

80%

100%

2011 2012 2013 2014

Others

LAC

Nearshore Europe

APAC

Figure: Breakup of new centers by region, 2011 – 2014; Number

Source: Everest Group Global Locations Annual Report (2015): Resurgence of Activity Amidst Evolving Propositions

LAC: thriving hub

Several competitive players

Growing number of hot locations

9 Nascent locations

3 Emerging locations

2 Mature locations

14 Hot locations

out of 20

Figure: Location Heatmap

Source: Everest Group Global Locations Annual Report (2015)

International recognition

LAC countries are present in all Global Services rankings

1. Brazil

2. Mexico

3. Chile

4. Costa rica

5. Colombia

6. Panama

7. Argentina

8. Trinidad and Tobago

9. Jamaica

10. Uruguay

A.T. Kearney Global Services Locations 2016 Tholons TOP 100 Outsourcing Destinations

2016

1. Costa Rica (San José)

2. Chile (Santiago)

3. Argentina (Buenos Aires)

4. Uruguay (Montevideo)

5. Mexico (Mexico City)

+ 16 others

Total: 10 / 55 Total: 21 / 100

Global in-house & SSC in LAC

Let them tell the story

HP

IBM

INTEL SS

P&G GBS

WALMART GSS

MC DONALDS

YAHOO!

ORACLE

JPMORGAN CHASE

SYKES

TECH DATA

TELETECH

BAYER

DHL

BASF

MERCK

BOSCH

HELLMANS LOGISTIC

FUJITSU

AMAZON

CONCENTRIX

CONVERGYS

EXXON MOBIL

JOHNSON & JOHNSON

WESTERN UNION

WORLD VISION

THOMSON REUTERS

PFIZER

MICROSOFT

WALT DISNEY

ERNST & YOUNG

CITI BUSINES SERVICES

SHELL

PHILIPS

HSBC

BRITISH AMERICAN TOBACCO

ASTRA ZENECA SS

NESTLE

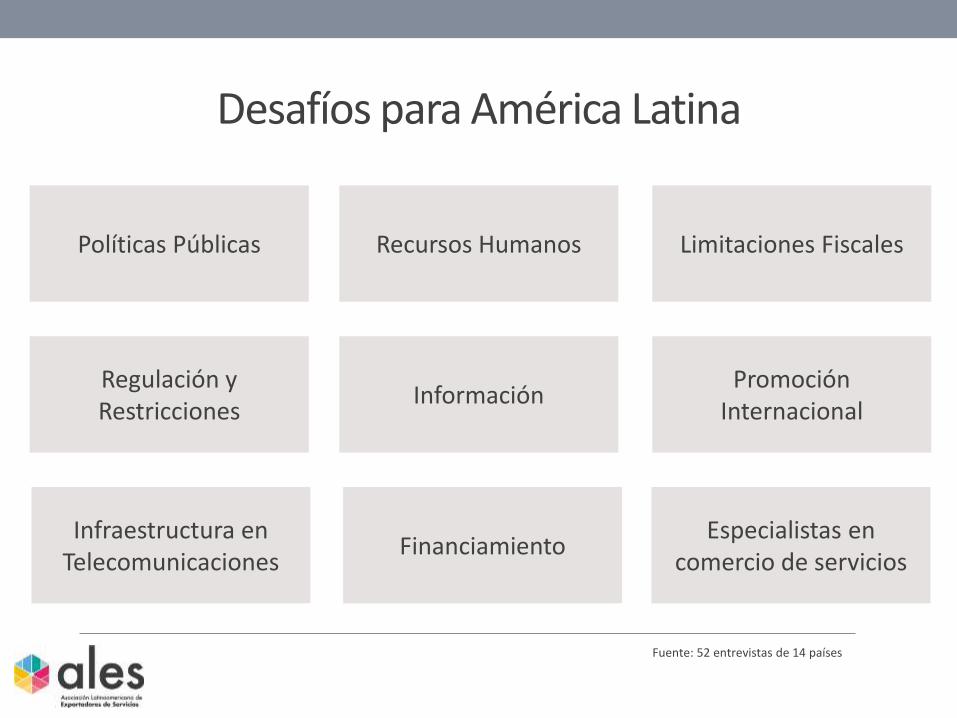

Desafíos para América Latina

Políticas Públicas Recursos Humanos Limitaciones Fiscales

Regulación y Restricciones

Información Promoción

Internacional

Infraestructura en Telecomunicaciones

Especialistas en comercio de servicios

Fuente: 52 entrevistas de 14 países

Financiamiento

About us

16 Countries

35 Members

In our 10 year anniversary

EVENTO

Pulse para añadir un título

16 países, 35 instituciones